Embed Size (px)

Citation preview

REGULATION AND SUPERVISIONOF

MICROFINANCE INSTITUTIONS

Case Studies

Edited by

Craig Churchill

The MicroFinance NetworkOccasional Paper No. 2

Regulation and Supervision Case Studies

i

TABLE OF CONTENTS

TABLE OF CONTENTS ........................................................................................................................ i

TABLE OF TABLES ............................................................................................................................ iii

CONTRIBUTORS................................................................................................................................. iv

ACKNOWLEDGMENTS ..................................................................................................................... vi

LIST OF ACRONYMS ........................................................................................................................ vii

INTRODUCTION .................................................................................................................................. 1

PROJECT PURPOSE ................................................................................................................................. 1BACKGROUND....................................................................................................................................... 2

INDONESIA........................................................................................................................................... 5

Shari Berenbach

BACKGROUND....................................................................................................................................... 5BANK RAKYAT INDONESIA UNIT DESA ................................................................................................... 8SUPERVISION OF MFIS IN INDONESIA.................................................................................................... 10

BANGLADESH.................................................................................................................................... 15

Janney Carpenter

CONTEXT: THE FORMAL AND SEMI-FORMAL FINANCIAL SECTORS ........................................................ 16EXISTING REGULATION: THE GRAMEEN BANK CHARTER ...................................................................... 21THE REGULATION DILEMMA: HOW MUCH AND HOW TO DO IT WELL? .................................................. 25OBSERVATIONS AND CONCLUSIONS...................................................................................................... 31

PHILIPPINES ...................................................................................................................................... 35

Eduardo C. Luang and Malena Vasquez

MAJOR LEGISLATIVE INITIATIVES FOR FINANCIAL SECTOR REFORM....................................................... 35ROLES AND RESPONSIBILITIES OF REGULATORS .................................................................................... 38MICROFINANCE STANDARDS INITIATIVE............................................................................................... 39

BOLIVIA.............................................................................................................................................. 43

Rachel Rock

BOLIVIAN REGULATORY FRAMEWORK.................................................................................................. 43CREATION OF BANCOSOL .................................................................................................................... 49LOS ANDES: THE FIRST BOLIVIAN PRIVATE FINANCIAL FUND ............................................................... 55

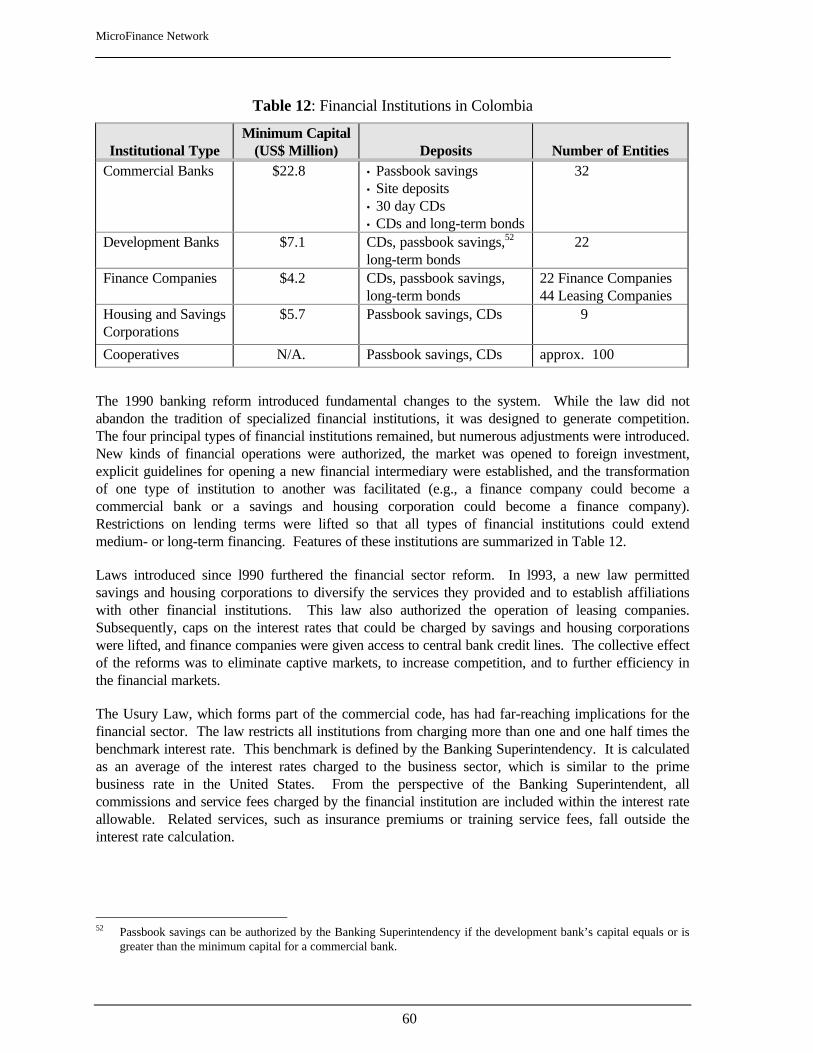

COLOMBIA......................................................................................................................................... 59

Shari Berenbach

FINANCIAL SECTOR IN COLOMBIA ........................................................................................................ 59FINANSOL ........................................................................................................................................... 61

MicroFinance Network

ii

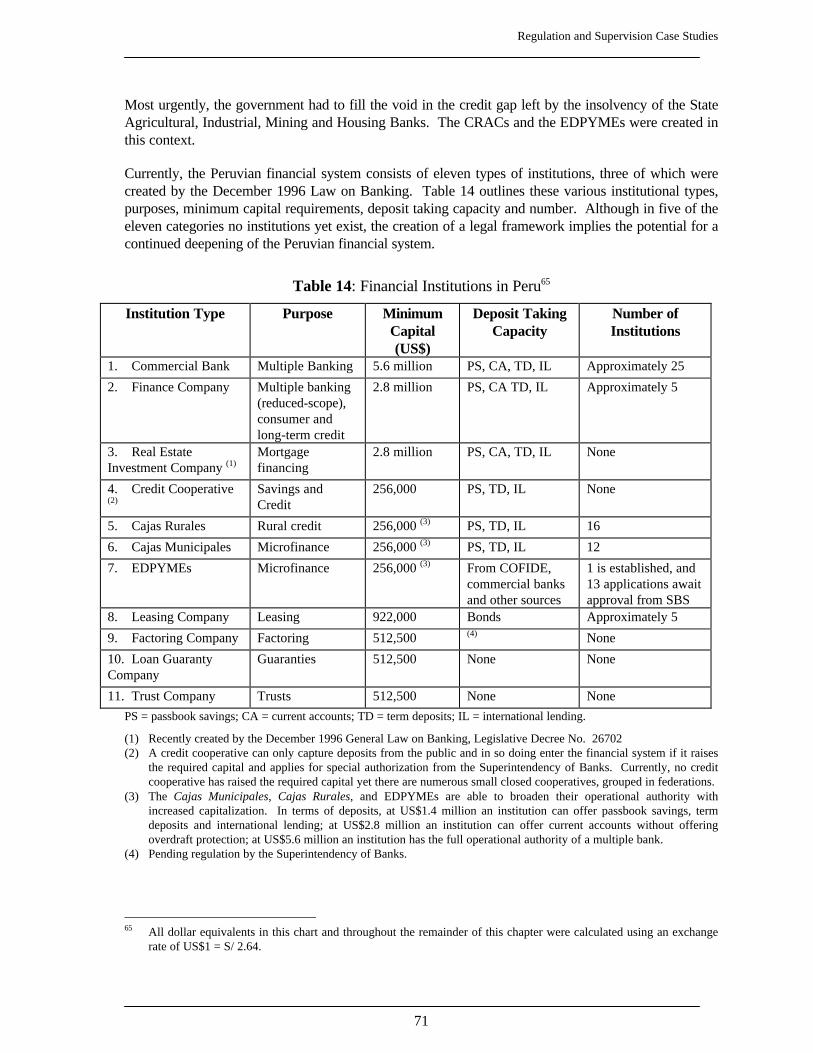

PERU.....................................................................................................................................................69

Rachel Rock

ECONOMIC CONTEXT ...........................................................................................................................69PERUVIAN FINANCIAL SYSTEM: STRUCTURE AND ACTORS .....................................................................70CAJAS MUNICIPALES ............................................................................................................................75CAJAS RURALES...................................................................................................................................82EDPYMES..........................................................................................................................................82CONCLUSION .......................................................................................................................................85

KENYA .................................................................................................................................................87

Janney Carpenter, Kimanthi Mutua, and Henry Oloo Oketch

CONTEXT: THE FORMAL AND SEMI-FORMAL FINANCIAL SECTORS IN KENYA .........................................87K-REP BANK LIMITED ..........................................................................................................................89CONCLUSIONS AND LESSONS ................................................................................................................97

WEST AFRICA ....................................................................................................................................99

Anne-Marie Chidzero and Gilles Galludec

HISTORY OF THE LAW ..........................................................................................................................99STATUS OF IMPLEMENTATION OF THE LAW..........................................................................................100FEATURES OF THE LAW AND THE DECREES OF APPLICATION.................................................................101DEVELOPMENTAL IMPACT ..................................................................................................................104ISSUES...............................................................................................................................................104

SOUTH AFRICA ................................................................................................................................107

Rudolph Wilhemse and Steven Goldblatt

MICROENTREPRENEURS AND ACCESS TO FINANCE...............................................................................107FINANCIAL SYSTEM INSTITUTIONS......................................................................................................108BANKING LAWS AND REGULATIONS ....................................................................................................110SELF-REGULATION FOR MICROFINANCE INSTITUTIONS ........................................................................114

BIBLIOGRAPHY...............................................................................................................................117

Regulation and Supervision Case Studies

iii

TABLE OF TABLES

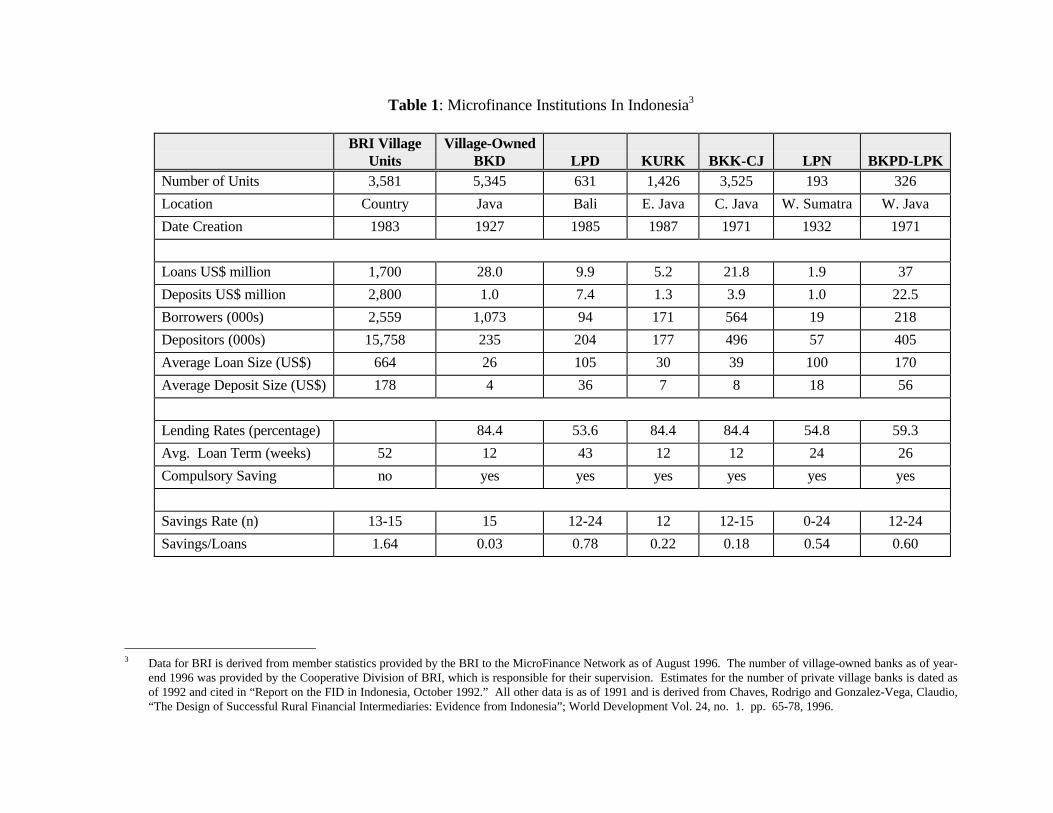

Table 1: Microfinance Institutions In Indonesia............................................................................6

Table 2: Summary Overview MFIs in Indonesia ..........................................................................7

Table 3: Supervisory Arrangements in Indonesia........................................................................ 10

Table 4: Banking Supervision Reports....................................................................................... 11

Table 5: BRI Village Unit Loan Classification and Reserves ...................................................... 11

Table 6: Loan and Deposit Size Comparison of BRI Unit Desa and Village-owned Banks .......... 12

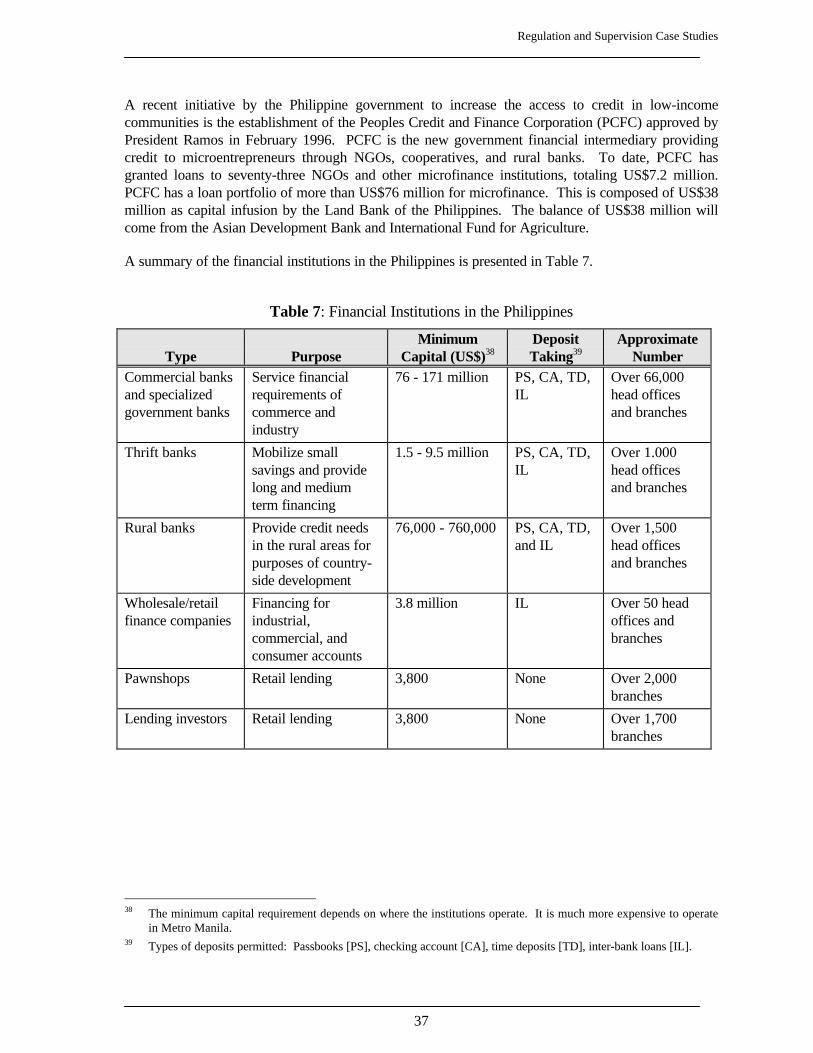

Table 7: Financial Institutions in the Philippines ........................................................................ 37

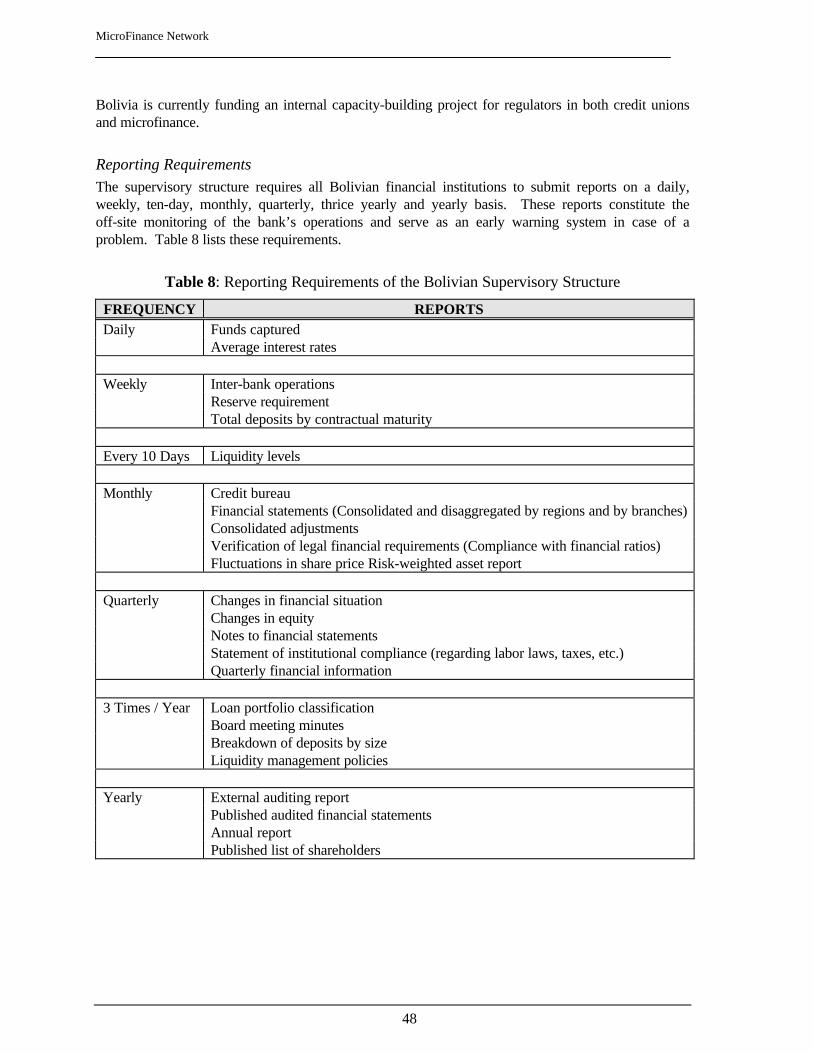

Table 8: Reporting Requirements of the Bolivian Supervisory Structure..................................... 48

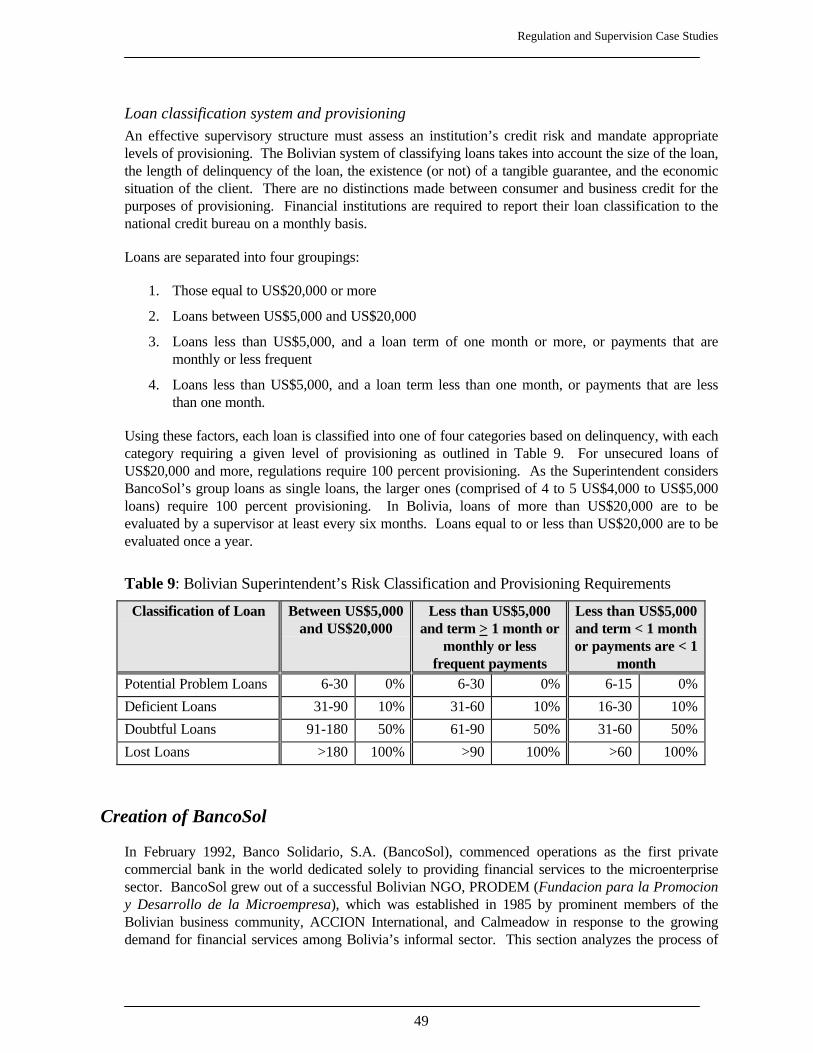

Table 9: Bolivian Superintendent’s Risk Classification and Provisioning Requirements .............. 49

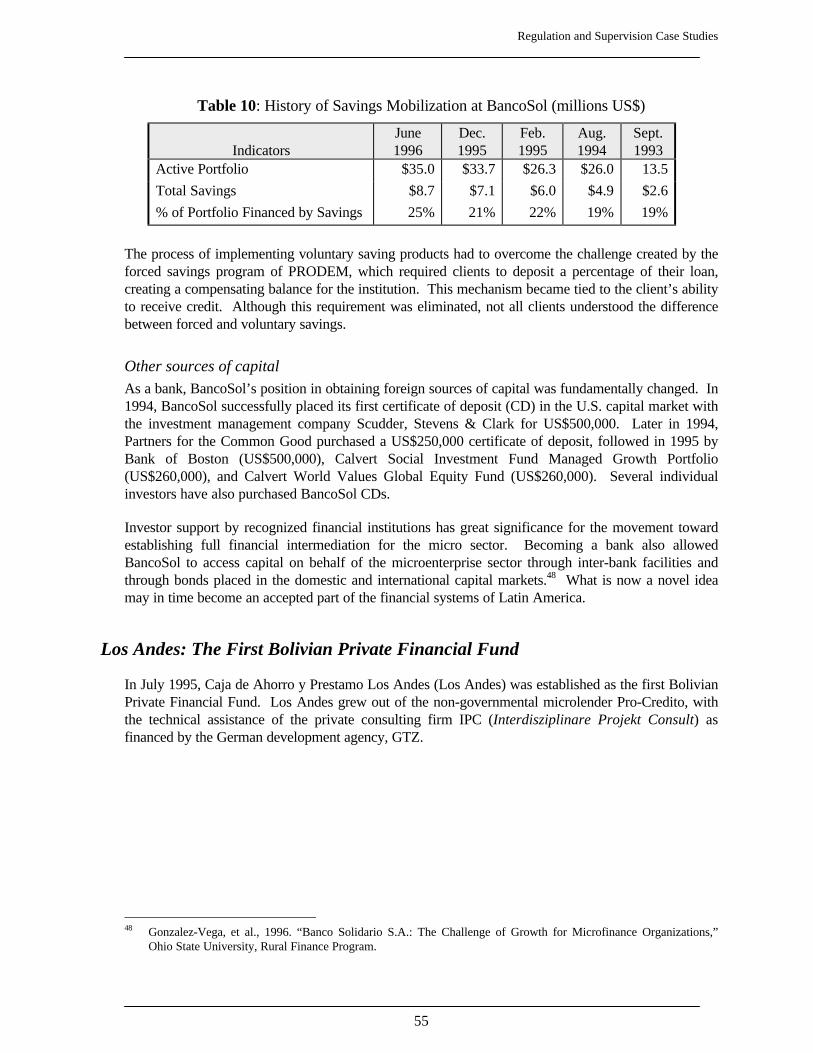

Table 10: History of Savings Mobilization at BancoSol (millions US$)...................................... 55

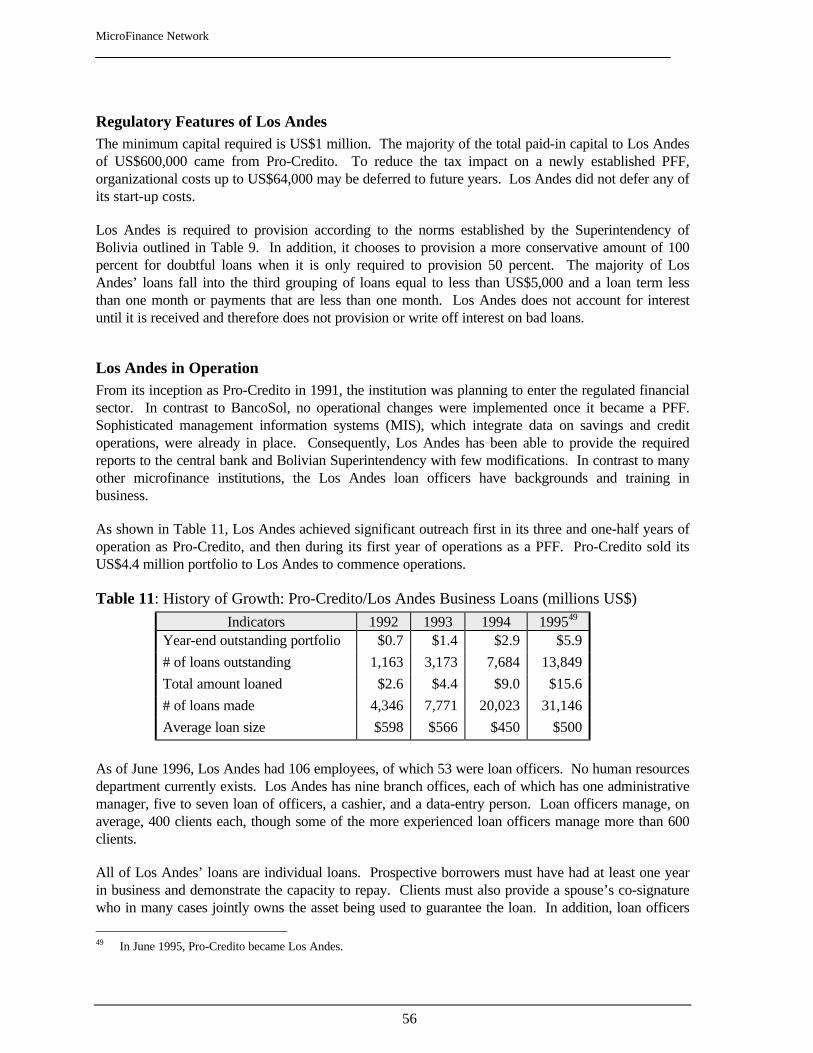

Table 11: History of Growth: Pro-Credito/Los Andes Business Loans (millions US$)................. 56

Table 12: Financial Institutions in Colombia.............................................................................. 60

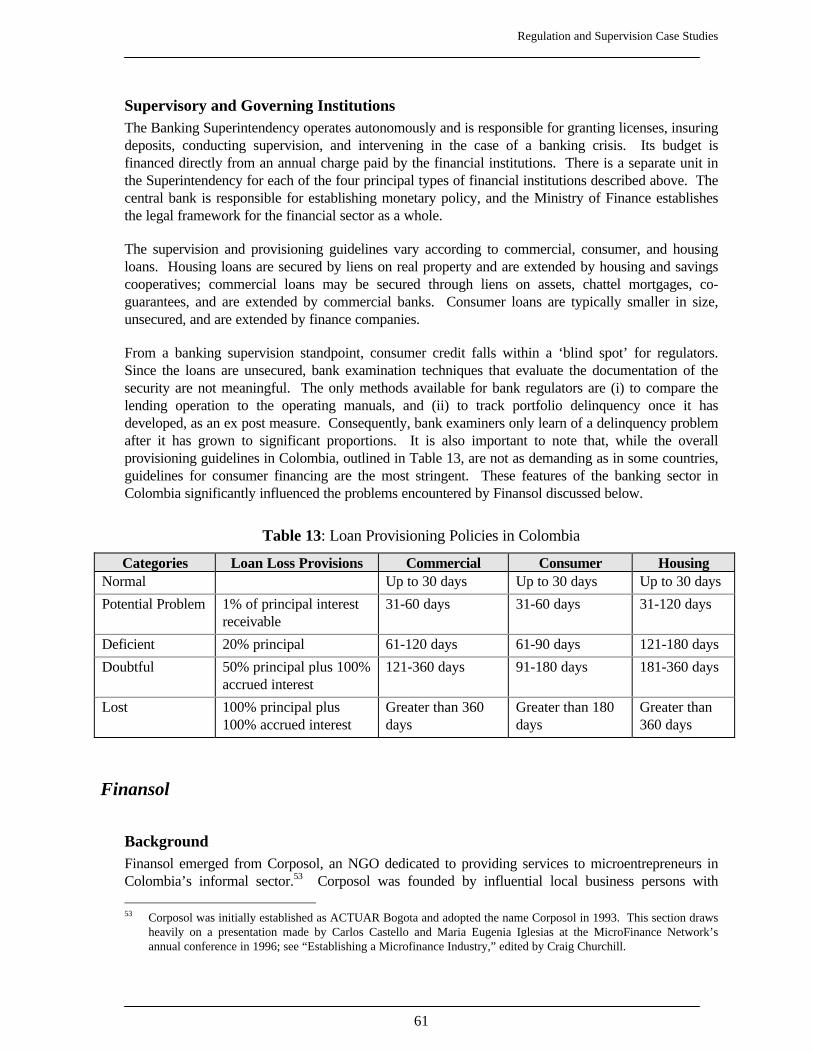

Table 13: Loan Provisioning Policies in Colombia ..................................................................... 61

Table 14: Financial Institutions in Peru...................................................................................... 71

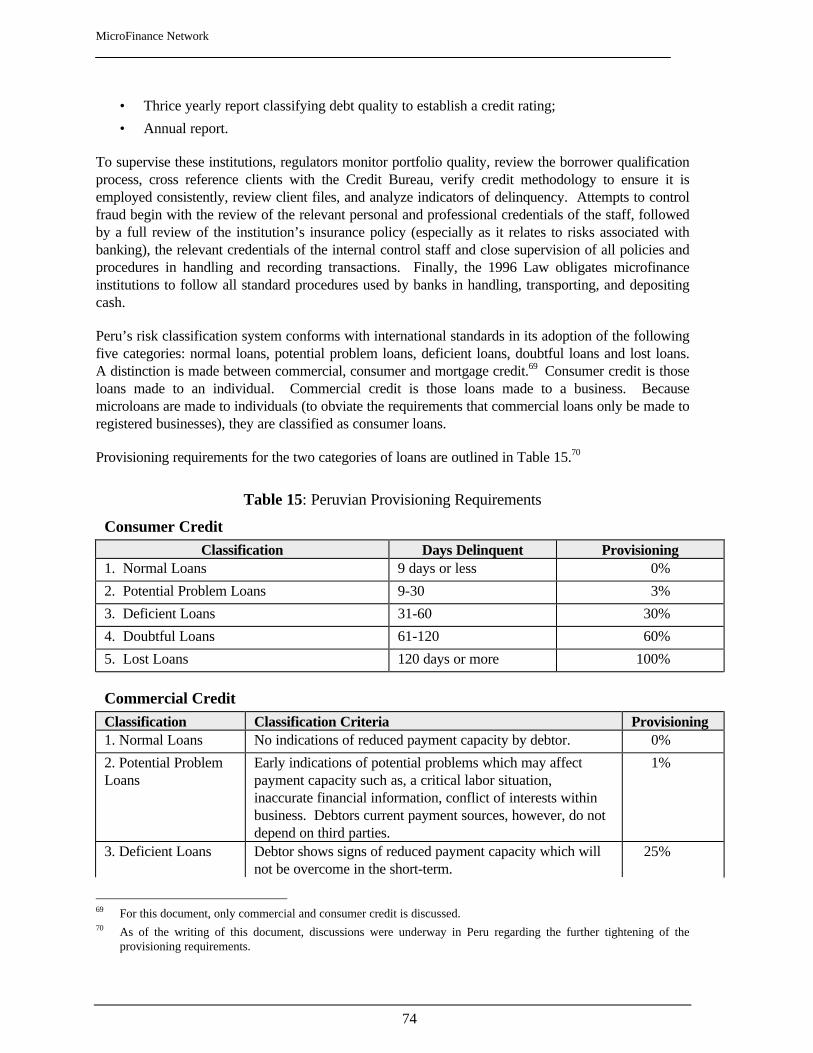

Table 15: Peruvian Provisioning Requirements .......................................................................... 74

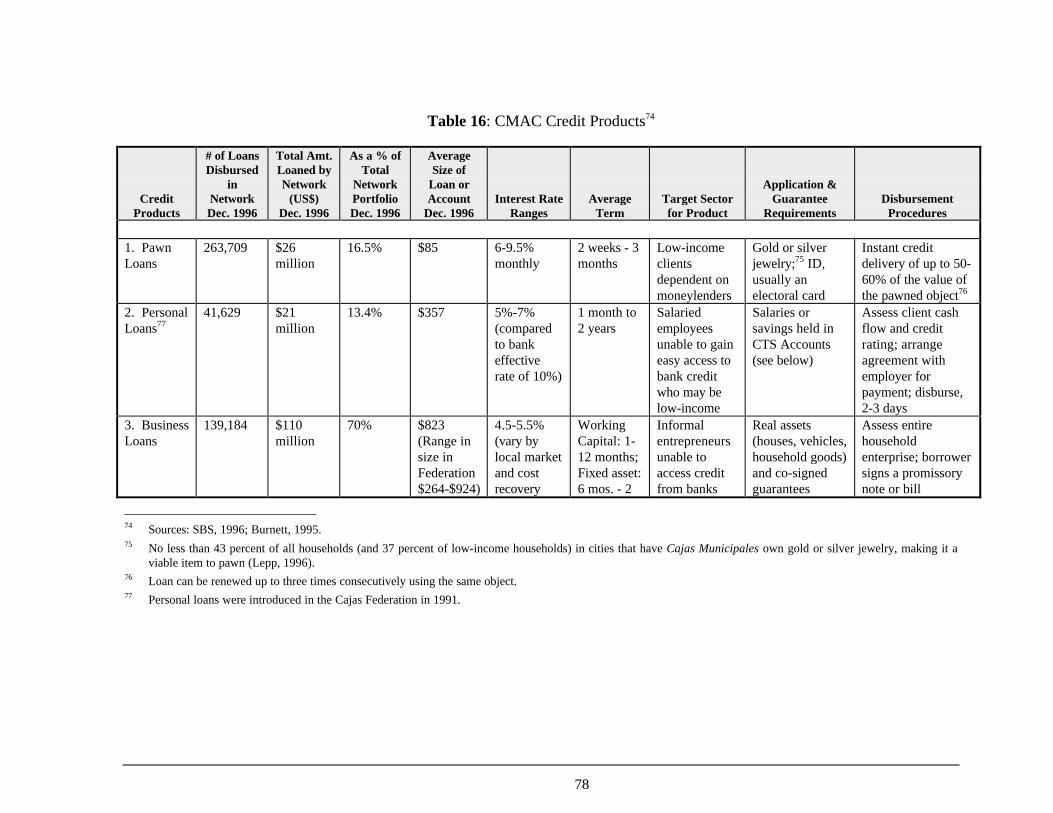

Table 16: CMAC Credit Products ............................................................................................. 78

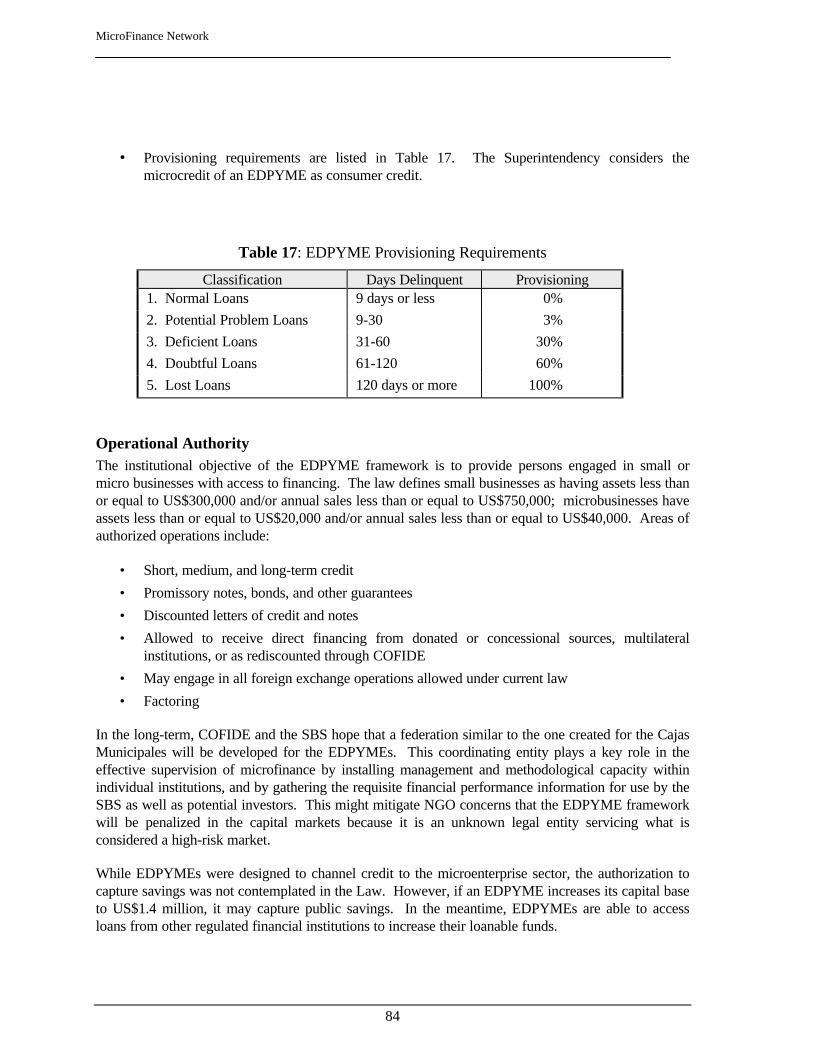

Table 17: EDPYME Provisioning Requirements ........................................................................ 84

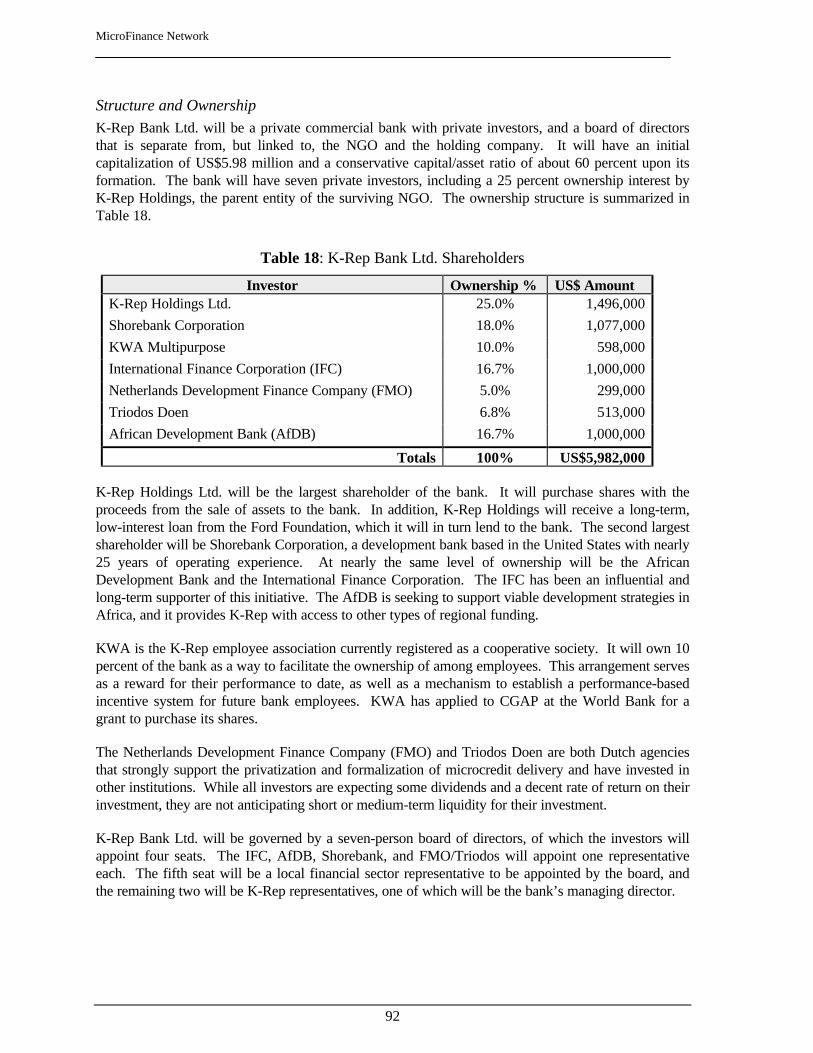

Table 18: K-Rep Bank Ltd. Shareholders .................................................................................. 92

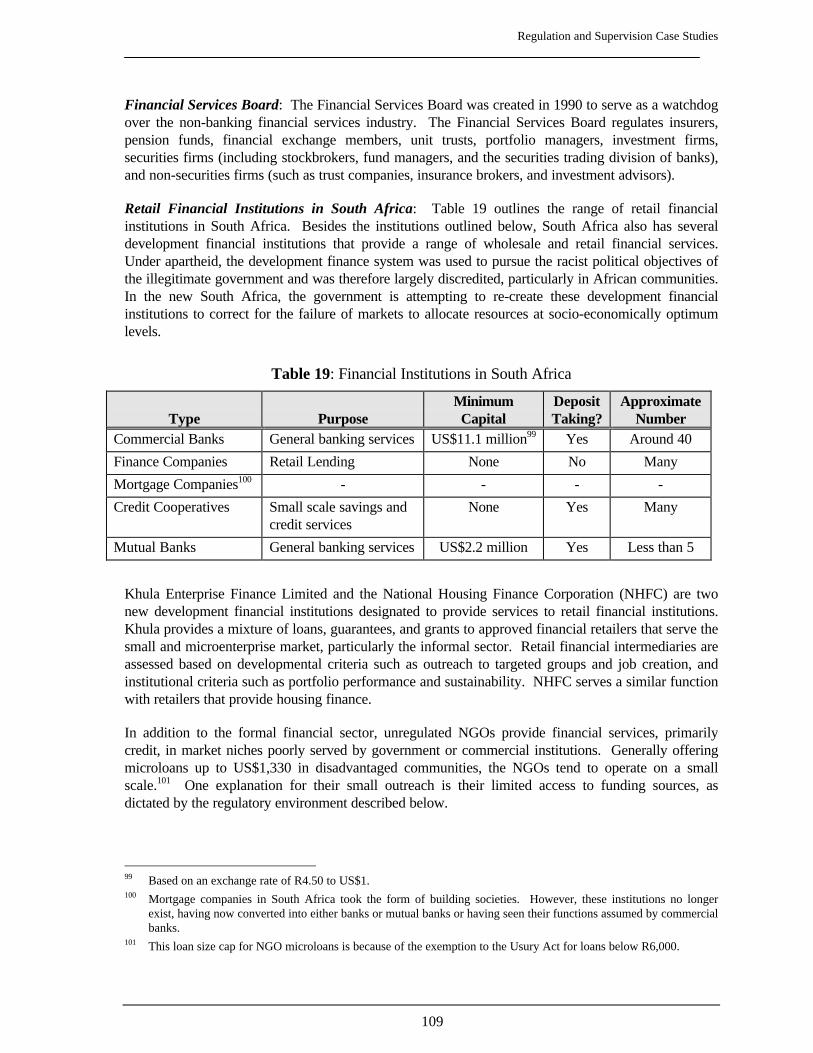

Table 19: Financial Institutions in South Africa ....................................................................... 109

MicroFinance Network

iv

CONTRIBUTORS

Shari Berenbach has over fifteen years of experience in the microfinance industry, having workedin nearly two dozen countries in Latin America, Asia, and Africa. She served as the Director ofPrograms for Partnership for Productivity and worked as a microfinance consultant for USAID,the World Bank, and the International Finance Corporation. In 1997, Ms Berenbach became theExecutive Director of the Calvert Social Investment Foundation, a corporate foundation that servesas a bridge between the capital markets and community economic development.

Janney Carpenter is a Managing Director of Shorebank Advisory Services (SAS), the consultingsubsidiary of Shorebank Corporation, a development bank based in Chicago, Illinois. Ms.Carpenter’s expertise is in development finance and microenterprise credit, both in the UnitedStates and internationally. In microenterprise, she has assessed best practices, provided strategicand business planning help, and conducted assessments and evaluations. In development finance,she has designed and helped establish several development finance institutions, includingcommunity development banks and loan funds.

Anne-Marie Chidzero is a Private Sector Development Specialist with emphasis on micro, small,and medium enterprise development. She shares her time between CGAP (the Consultative Groupto Assist the Poorest), where she works as an Operations Analyst, and the Private SectorDevelopment Department of the World Bank. Most of her microfinance work has been in Africa,where she has conducted financial appraisals of microfinance institutions, organized and conductedtraining programs for practitioners, donors, and governments, and led the World Bank’sdiscussions with the Central Bank of West Africa on a regulatory framework for microfinanceinstitutions.

Craig Churchill is the Coordinator of the MicroFinance Network and the Director ofCalmeadow’s Washington, DC, office. Over the past five years, he has been Director of theResearch and Program Evaluation at ACCION International, has done research for the WorldBank, and worked as an advisor to Get Ahead Financial Services in South Africa.

Gilles Galludec joined CGAP in December 1996 as a Financial Management Specialist. He hasaccumulated eight years of experience as a practitioner in the financial sector in Africa. Heworked as a banking expert for Postal Savings in Gabon, where he designed and managed thefinance and treasury department for four years. He also spent four years in Benin as a FinancialController of FECECAM (a major credit union network) to reorganize the accounting, internalcontrol, and management information systems.

Steven Goldblatt is an advocate at the Johannesburg Bar, retained as a legal advisor by the Landand Agricultural Policy Centre and the Minister of Agriculture and Land Affairs. He was amember of the Strauss Commission on Rural Financial Services.

Eduardo C. Luang is the Bank Project Director of TSPI Development Corporation and isprimarily responsible for setting up the proposed TSPI Bank. His tasks include preparing theoperating manuals and conceptualizing the organizational and operational details required toestablish and operate a thrift bank. He has 28 years of experience in banking and was VicePresident and Chief Operating Officer of Comsavings Bank. He has also served as a consultant

Regulation and Supervision Case Studies

v

for two foreign banks, State Mortgage and Investment Bank in Colombo, Sri Lanka, and People’sBank of Zanzibar, Ltd., Tanzania.

Kimanthi Mutua, currently the Managing Director of K-Rep, has over 20 years experience infinance in general, and small and micro enterprise development in Africa in particular. His specialskills lie in the design and management of microenterprise finance operations, the design andinstallation of management information systems, and financial analysis. He has played a principalrole in designing and implementing all of K-Rep’s microenterprise development programs. Overthe past 15 years, Mr. Mutua has authored numerous publications on various issues in the fields ofenterprise development and microfinance.

Henry Oloo Oketch is currently K-Rep’s Manager of the Research and Innovations Department.He has been involved in NGO development work since 1987. Mr. Oketch has extensive skills andexperience in the design of management information and monitoring systems, as well as appraisaland evaluation of micro enterprise development projects. He has provided consulting services tothe ILO, USAID, Ford Foundation, SNV/NOVIB (Uganda), World Vision International, ChristianChildren’s Fund, University of Edinburgh, and the Kenya Industrial Estates on micro and smallenterprise evaluation and system design.

Rachel Rock is the Director, Program Evaluation and Policy Development for ACCIONInternational. She is responsible for researching and documenting issues in the microfinance fieldfor ACCION’s publication series and is a member of the research team for the USAIDMicroenterprise Best Practices project. Before joining ACCION, Ms. Rock worked in communitydevelopment in the Dominican Republic and in strategic political consulting in several LatinAmerican countries. She also developed training materials for Working Capital, a domesticmicrocredit program in New England.

Malena Vasquez is a Corporate Planning Specialist of TSPI Development Corporation. Her workinvolves corporate planning, monitoring, and research. She has worked with TSPI for over fiveyears.

Rudolph Wilhemse is the chairman of EFK Tucker, Inc., a Johannesburg firm of attorneys. Hehas been involved in a number of initiatives relating to the provision of development finance to low-income communities.

MicroFinance Network

vi

ACKNOWLEDGMENTS

The MicroFinance Network, with the financial support of the British Department for InternationalDevelopment (DFID), the World Bank’s CGAP, and a private foundation, has undertaken thisresearch project to promote a greater awareness of appropriate regulatory and supervisoryapproaches for microfinance. The authors thank the funders of this project for their support.

An expert panel of bank supervisors served as advisors to this research. Their contributions helpedto ensure that this study considered the concerns and limitations of supervisory bodies. Mostimportantly, they repeatedly emphasized that, for the most part, bank superintendents are notparticularly interested in small financial institutions that do not pose a significant threat to thestability of the financial system. This panel includes:

• Hennie van Greuning, the former Chairman of the South African Reserve Bank, currentlyemployed at The World Bank

• Jorge Castellanos, the Colombian Banking Superintendent from 1994 to 1995, nowworking for JP Morgan in New York

• Luis Cortavaria, the former Banking Superintendent of Peru, currently working with theInternational Finance Corporation (IFC)

• Christopher Beshouri, a Financial Economist at the United States Department of Treasury

The authors are indebted to a long list of other readers and advisors to this project including:Elisabeth Rhyne (USAID); Richard Rosenberg and Joyita Mukherjee (CGAP); David Wright(DFID); Maria Otero and Carlos Castello (ACCION International); Barbara Calvin and StefanHarpe (Calmeadow); Robert P. Christen; Jacques Trigo LoubiPre (Bolivian Superintendent ofBanks and Financial Institutions); Maria Eugenia Iglesias (Finansol); Cliff Kellogg (Shorebank);Stuart Rutherford; Harald Huttenrauch and Mark Wenner (Inter-American Development Bank);Robert Vogel (IMCC); Mengistu Alemayehu (International Finance Corporation); Todd Farington;Jacinta Hamann (COFIDE); Don Johnston (HIID); Edgar Lasso (Finance Company Delegate tothe Colombian Banking Superintendent); and the staff of BCEAO.

The editor thanks the members of the MicroFinance Network for supporting this research, inparticular those members that have contributed their time and resources directly to this project:ACCION International, Accion Comunitaria del Peru, BancoSol, Bank Rakyat Indonesia, BRAC,Calmeadow, Finansol, K-Rep, and TSPI Development Corporation. The perseverance andcooperation of all the authors during this two year project is also greatly appreciated.

Regulation and Supervision Case Studies

vii

LIST OF ACRONYMS

ADB Asian Development Bank

AfDB African Development Bank

AMEDP Alliance of Micro Enterprise Development Practitioners

ASA Association for Social Advancement

BAP Bankers Association of the Philippines

BCEAO Banque Central des Etats de l’Afrique de L’Ouest

BKD Baden Kredit Desa

BKK Badan Kredit Kecamatan

BRAC Bangladesh Rural Advancement Committee

BRI Bank Rakyat Indonesia

BSP Bangko Sentral ng Pilipinas

CAF Corporacion Andina de Fomento

CAMEL Capital Adequacy Asset Quality Management Earnings Liquidity

CAS/SMEC Cellule d’Appui et de Suivi des Structures Mutualistes ou Coopérativesd’Epargne et de Crédit

CBK Central Bank of Kenya

CD Certificate of Deposit

CDF Credit and Development Forum

CGAP Consultative Group to Assist the Poorest

CIDA Canadian International Development Agency

CMAC Cajas Municipales de Ahorro y Crédito

COFIDE Corporacion Financiera de Desarrollo

CRAC Caja Rurale de Ahorro y Credito

EDPYME Entidades de Desarrollo para la Pequena y Microempresa

FEPCMAC Federation Peruana de Cajas Municipales de Ahorro y Credito

FONCODES Fondo Nacional de Compensacion y Desarrollo Social

FONDEM Fondo para el de la Desarrollo Microempresa

FMO Nederlandse Financierings-Mautschappij Voor Ontwikkelingslanded

FRASA Fondo Revolvente del Sector Agrario

GDP Gross Domestic Product

GTZ Gesellschaft fur Technische Zusammenarbeit

IDB Inter-American Development Bank

IFAD International Fund for Agriculture

IFC International Finance Corporation

IFI Instituto de Fomento Industrial

IIC Inter-American Investment Corporation

IPC Interdisziplinare Projekt Consult

MicroFinance Network

viii

K-Rep Kenya Rural Enterprise Program

KUK Kredit Usaha Kecil

KURK Kredit Usaha Rakyat Kecil

LPD Lembaga Perkreditan Desa

LPN Lumbung Pitih Nagari

MFI Microfinance Institution

MIS Management Information Systems

NBFI Non-Bank Financial Institution

NCC National Credit Council

NGO Non-Governmental Organization

NHFC National Housing Finance Corporation

PARMEC Prôjet d’Appui à la Réglementation des Mutuelles d’Epargne et de Credit

PCFC Peoples Credit and Finance Corporation

PDIC Philippine Deposit Insurance Corporation

PFF Private Financial Fund

PKSF Palli Karma Sahayak Foundation

PRODEM Fundacion para la Promocion y Desarrollo de la Micro empresa

ROSCA Rotating Savings and Credit Associations

ROA Return on Assets

SACCO Savings and Credit Cooperative

SBS Superintendencia de Banca y Seguros

SCC Savings and Credit Cooperatives

SDID Société de Développment International Desjardin

SDR Special Drawing Rights

SDS Social Development Society

UEMOA Union Economique et Monetaire d’Ouest Afrique

USAID United States Agency for International Development

Regulation and Supervision Case Studies

1

ÐÐ

INTRODUCTION

ÓÓ

Project Purpose

The MicroFinance Network is a global association of microfinance institutions (MFIs)commited toimproving the quality of life of low-income communities through the provision of credit,and other financial services.1 Network members believe these services should be provided bysustainable and profitable financial institutions that reach large numbers of clients not currently servedby the traditional banking sector.

This research is designed to serve as a resource for bank supervisors, regulators, and policy makers.The Regulation and Supervision Project of the MicroFinance Network reviews case experiences innine countries that have some experience with MFIs and draws conclusions regarding approaches toregulation and supervision that are suited to the unique characteristics of those institutions. Countrieswere selected for review because of the presence of a MicroFinance Network member and because thissample presents a range of regulatory responses in diverse settings. The principal findings from thisproject are summarized in the first volume. The country case studies, presented in this second volume,offer a detailed analysis of the field experience.

Experiences in Bangladesh, Indonesia, and Bolivia provide evidence of the potential of microfinanceinstitutions to provide financial services on a large scale. While these are exceptional cases, themicrofinance community is emulating these models of success. Under proper conditions, including anappropriate regulatory environment, there will be an increasing number of successful MFIs in thecoming years. It is hoped that regulators will be proactive in their preparations for the microfinancewave. It is not necessary, desirable, or realistic to regulate all microfinance institutions. However, ifthese services include mobilizing voluntary savings from the general public beyond closedcommunities where common bonds exist, it is critical that some form of supervision be involved.

The cases examined highlight two general approaches to regulating microfinance institutions. Thesituations in Bolivia, Kenya, and Colombia show the experiences of regulating MFIs within theexisting regulatory framework, either as a commercial bank or as a finance company. Theseexperiences also highlight mismatches between the standard regulatory framework and the provisionof microfinance services. The cases from Peru, West Africa, and Bolivia again provide insight intoinitial attempts to create special categories of laws designed specifically for microfinance institutions.

A third set of experiences, from South Africa and the Philippines, demonstrates a learning process –for MFIs and policy makers – designed to create standards for the local microfinance industry. Whileit is too early in the development of these efforts to have a significant bearing on the discussion, they

1 Microfinance institutions (MFIs) assume a variety of institutional forms. While these cases speak most frequently

about non-profit microcredit programs that create regulated MFIs, other institutional types include government-owned banks that operate microfinance units, commercial banks that create microfinance subsidiaries, and creditunions. Successful MFIs typically provide a range of financial services to low-income communities, such as savings,personal or consumption loans, housing and enterprise loans.

MicroFinance Network

2

do suggest possible first steps towards identifying an appropriate regulatory approach formicrofinance.

Background

The emergence of the microfinance industry presents an unprecedented opportunity to extend financialservices to the vast majority of the economically active population. In developing countries,traditional banks typically serve no more than twenty percent of the population. The remainingcommunities historically have not had access to formal financial services, yet this non-traditionalmarket is immense. The World Bank estimates that the potential global market for microenterprisecredit currently stands at about 100 million clients.

In the last twenty years, leading MFIs have devised appropriate financial service technologies tobecome profitable financial intermediaries. These developments have established the means to extendfinancial services to excluded sectors, thereby laying the groundwork for the microfinance industry.Through the provision of these services, MFIs deepen the financial system and expand the economiccontribution of low-income communities. Just as new agricultural technologies spawned the greenrevolution in the l970s and 1980s, new financial technologies are producing the microfinancerevolution in the 1990s.

As they mature, many MFIs are realizing that they need to enter the formal financial system to fundtheir growth and to provide the diversity of financial services demanded by their target market.However, just as traditional lending techniques are inappropriate for the characteristics ofmicroenterprises, traditional banking regulation and supervisory practices are ill-suited to the uniquerisk profile of a microfinance institution.

In many countries, bank regulators now face the challenge of determining whether to regulate theemerging microfinance sector at all. If so, they need to consider an appropriate regulatory approach.As unregulated financial entities, MFIs have had considerable freedom to adapt operating methods toserve their target markets effectively. This has led to the development of a small but growing numberof robust, specialized financial institutions, innovative delivery methods, and an extension of thefinancial services market. As more MFIs grow in scale and complexity, regulators may seek tosupport their growth while safeguarding the financial system and protecting the interests of MFIclients. This is particularly important since these clients typically come from the most vulnerablesectors of the population.

When regulation is warranted, it requires coherent prudential guidelines that will allow the growth ofthe microfinance sector while protecting the interests of small savers and supporting the integrity ofthe financial sector as a whole. While appropriate regulatory approaches must be consistent with theregulatory framework of a given country, the case studies point to field lessons that illuminateappropriate regulation of this segment of the financial market. The essence of these lessons is toconsider the risk profile of microfinance institutions and rigorously apply prudential guidelines whereMFIs are vulnerable, but to offer flexibility in risk-control measures that do not apply to themicrofinance sector. Such effective regulation may be accomplished through exemptions andmodifications to existing financial-sector guidelines or through the establishment of specializedregulatory regimes.

Whichever means regulators adopt, they should be cautious not to move too hastily to establish anyregulations, nor to create regulations based only on one institutional model. There is a danger that

Regulation and Supervision Case Studies

3

regulations designed for the risk profile of commercial banks will box MFIs into practices that requirereplicating traditional banking practices, thereby losing their ability to reach their target market.

There is also a danger that the proliferation of MFIs, in response to a seemingly limitless market formicrofinance services, may exceed the regulators’ capacities of supervision. Yet, once MFIs areregulated entities, depositors may not adequately evaluate their risk. It is necessary to find a balance.Regulators should consider a line below which the financial markets are better left unregulated andfocus their attention on those institutions with the potential to obtain significant scale. In addition,until regulators develop an expertise with microfinance, it is probably preferable not to license toomany institutions.

While it is neither possible nor desirable to regulate all microfinance institutions, an increasing numberof MFIs are reaching significant scale, intend to mobilize savings, and merit further consideration bybank regulators. The case studies review some of the experiences to date of jurisdictions that haveattempted to shape regulation and supervision to the specific characteristics of microfinance.

While the cases in this publication are organized geographically, the issues and approaches transcendregions. K-Rep is encountering many of the same regulatory obstacles in Kenya that BancoSolcontinues to experience in Bolivia five years after creating the world’s first commercial bank dedicatedsolely to microfinance. South Africa and the Philippines are involved in similar processes to identifyan appropriate regulatory framework for microfinance in their countries. The crisis that occurredwith Finansol in Colombia could occur in Bangladesh or elsewhere unless similar ownership andgovernance issues are resolved. More than half of the countries in this small sample are struggling todetermine the appropriate role for government sponsored apex institutions. All countries are dealingwith the challenges that result from a lack of industry standards and common definitions for financialand performance indicators.

The new world of microfinance is not large. The MicroFinance Network, as a global association,seeks to make it even smaller so that important lessons can quickly cross national and regionalboundaries, and advance the field. This publication is an important step in striving for that objective.

MicroFinance Network

4

Regulation and Supervision Case Studies

5

ÐÐ

INDONESIA

ÓÓ

Shari Berenbach

In terms of scale, variety, and volume of MFIs, market penetration, and profitability, themicrofinancial services market in Indonesia is the most developed in the world. Indonesia is one offew countries where the microfinance market extends to the village level. There are more than fifteenthousand village banking units providing savings and credit to nearly seventeen million clients. Thiscase study focuses on a description of the microfinance institutions in Indonesia and a brief overviewof the legal and regulatory framework for the microfinancial services market as a whole. This chapteralso reviews the Bank Rakyat Indonesia’s (BRI) Unit Desa System, the largest microfinanceinstitution in the world, and gives special attention to the MFI supervision methods applied inIndonesia.

Background

The experience with village-based microfinance institutions in Indonesia dates back more than onehundred years and is part of the Dutch colonial legacy. Particularly in Central Java, the Dutchintroduced village-owned banks known as BKD (Badan Kredit Desa). In the late 1960s, during aperiod of monetary instability and high inflation rates, many of the village-owned banks faltered. Inthe 1970s and 1980s, building on its village banking tradition, national and provincial developmentbanks successfully promoted the effective delivery of rural financial services through village-levelbanking units. Today, a web of small banking institutions has evolved, providing financial services atsub-district market towns and in villages. This includes the traditional village-owned banks mentionedabove, the BRI village units, at least six provincial village banking networks, and private village bankssuch as Bank Dagang Bali.

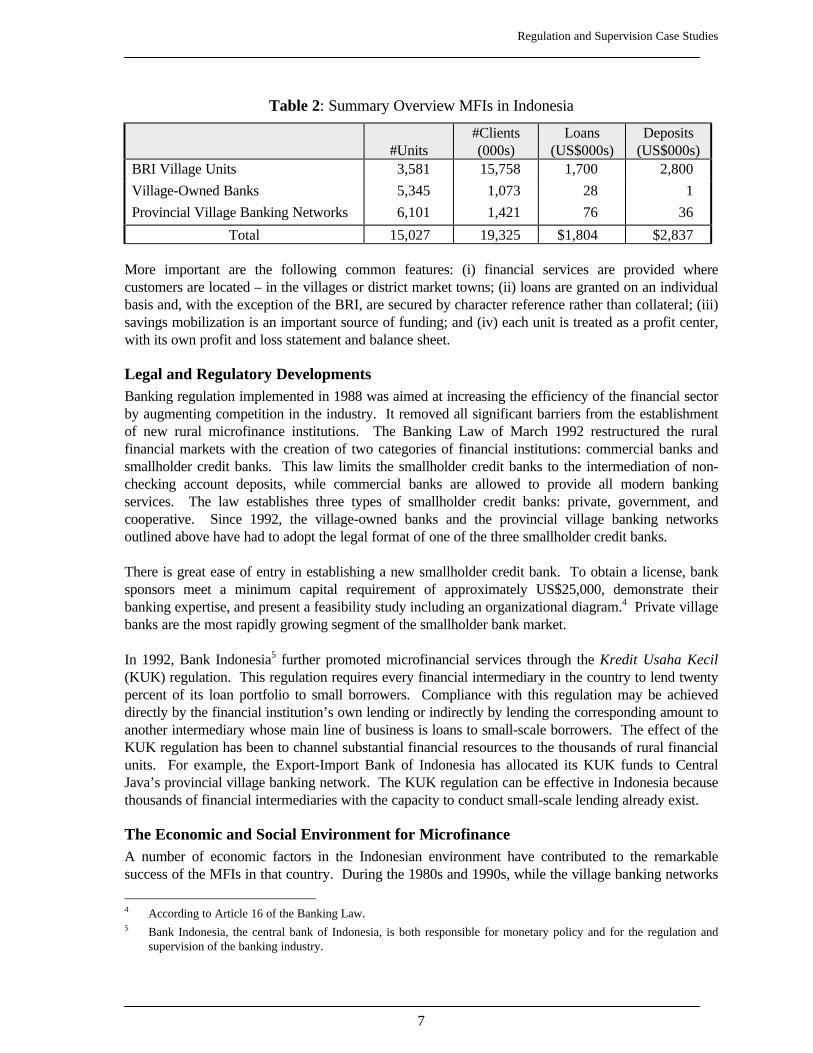

While the data presented in Table 1 on the following page provide an overview of the microfinancialservices market in Indonesia, Table 2 illustrates the variation among these financial institutions. Forexample, the village-owned banks and several of the provincial village banking networks2 average loansizes below US$50 and savings deposits below US$10. The average loan size and deposit of the BRIvillage units, the largest of this set, are US$664 and US$178 respectively.

2 For the purpose of this case study, the provincial village banking networks are those that were promoted by

provincial governments. These may be owned by the provincial government (Badan Kredit Kecamatan-BKK, KreditUsaha Rakyat Kecil-KURK), owned by the village (Lembaga Perkreditan Desa-LPD), or owned by their clients(Lumbung Pitih Nagari-LPN).

Table 1: Microfinance Institutions In Indonesia3

BRI VillageUnits

Village-OwnedBKD LPD KURK BKK-CJ LPN BKPD-LPK

Number of Units 3,581 5,345 631 1,426 3,525 193 326

Location Country Java Bali E. Java C. Java W. Sumatra W. Java

Date Creation 1983 1927 1985 1987 1971 1932 1971

Loans US$ million 1,700 28.0 9.9 5.2 21.8 1.9 37

Deposits US$ million 2,800 1.0 7.4 1.3 3.9 1.0 22.5

Borrowers (000s) 2,559 1,073 94 171 564 19 218

Depositors (000s) 15,758 235 204 177 496 57 405

Average Loan Size (US$) 664 26 105 30 39 100 170

Average Deposit Size (US$) 178 4 36 7 8 18 56

Lending Rates (percentage) 84.4 53.6 84.4 84.4 54.8 59.3

Avg. Loan Term (weeks) 52 12 43 12 12 24 26

Compulsory Saving no yes yes yes yes yes yes

Savings Rate (n) 13-15 15 12-24 12 12-15 0-24 12-24

Savings/Loans 1.64 0.03 0.78 0.22 0.18 0.54 0.60

3 Data for BRI is derived from member statistics provided by the BRI to the MicroFinance Network as of August 1996. The number of village-owned banks as of year-

end 1996 was provided by the Cooperative Division of BRI, which is responsible for their supervision. Estimates for the number of private village banks is dated asof 1992 and cited in “Report on the FID in Indonesia, October 1992.” All other data is as of 1991 and is derived from Chaves, Rodrigo and Gonzalez-Vega, Claudio,“The Design of Successful Rural Financial Intermediaries: Evidence from Indonesia”; World Development Vol. 24, no. 1. pp. 65-78, 1996.

Regulation and Supervision Case Studies

7

Table 2: Summary Overview MFIs in Indonesia

#Units#Clients(000s)

Loans(US$000s)

Deposits(US$000s)

BRI Village Units 3,581 15,758 1,700 2,800

Village-Owned Banks 5,345 1,073 28 1

Provincial Village Banking Networks 6,101 1,421 76 36

Total 15,027 19,325 $1,804 $2,837

More important are the following common features: (i) financial services are provided wherecustomers are located – in the villages or district market towns; (ii) loans are granted on an individualbasis and, with the exception of the BRI, are secured by character reference rather than collateral; (iii)savings mobilization is an important source of funding; and (iv) each unit is treated as a profit center,with its own profit and loss statement and balance sheet.

Legal and Regulatory DevelopmentsBanking regulation implemented in 1988 was aimed at increasing the efficiency of the financial sectorby augmenting competition in the industry. It removed all significant barriers from the establishmentof new rural microfinance institutions. The Banking Law of March 1992 restructured the ruralfinancial markets with the creation of two categories of financial institutions: commercial banks andsmallholder credit banks. This law limits the smallholder credit banks to the intermediation of non-checking account deposits, while commercial banks are allowed to provide all modern bankingservices. The law establishes three types of smallholder credit banks: private, government, andcooperative. Since 1992, the village-owned banks and the provincial village banking networksoutlined above have had to adopt the legal format of one of the three smallholder credit banks.

There is great ease of entry in establishing a new smallholder credit bank. To obtain a license, banksponsors meet a minimum capital requirement of approximately US$25,000, demonstrate theirbanking expertise, and present a feasibility study including an organizational diagram.4 Private villagebanks are the most rapidly growing segment of the smallholder bank market.

In 1992, Bank Indonesia5 further promoted microfinancial services through the Kredit Usaha Kecil(KUK) regulation. This regulation requires every financial intermediary in the country to lend twentypercent of its loan portfolio to small borrowers. Compliance with this regulation may be achieveddirectly by the financial institution’s own lending or indirectly by lending the corresponding amount toanother intermediary whose main line of business is loans to small-scale borrowers. The effect of theKUK regulation has been to channel substantial financial resources to the thousands of rural financialunits. For example, the Export-Import Bank of Indonesia has allocated its KUK funds to CentralJava’s provincial village banking network. The KUK regulation can be effective in Indonesia becausethousands of financial intermediaries with the capacity to conduct small-scale lending already exist.

The Economic and Social Environment for MicrofinanceA number of economic factors in the Indonesian environment have contributed to the remarkablesuccess of the MFIs in that country. During the 1980s and 1990s, while the village banking networks

4 According to Article 16 of the Banking Law.5 Bank Indonesia, the central bank of Indonesia, is both responsible for monetary policy and for the regulation and

supervision of the banking industry.

MicroFinance Network

8

were being developed, Indonesia enjoyed comparatively high rates of growth of output accompaniedby rapid growth of rural incomes and a reduction of poverty. Profitable investment opportunitiesemerged for the microentrepreneur as domestic markets became more integrated and internationalbarriers to trade were reversed. The rapid economic growth was coupled with the liberalization of thefinancial markets and a stable macroeconomic environment. Indonesia has not experienced significantdomestic inflation in recent years.

Since microfinance combines both economic and social agendas, it is not surprising that the socialenvironment in Indonesia also contributed to the creation of the world’s most sophisticatedmicrofinance market. Political stability and a strong presence of government at all administrativelevels contribute an effective institutional framework for the development of the MFIs. Indonesiabenefits from a high degree of social cohesion. This traditional social structure is particularlyimportant to the success of microfinance as it contributes to financial contract enforcement.Furthermore, high population density in a number of provinces greatly enhances the efficiency ofdecentralized banking systems and allows individual banking units to attain profitability quickly.

The most important factor in Indonesia’s microfinance success, however, is that the authoritiesrecognize the developmental benefit obtained by promoting organizations that permanently providefinancial services at market prices. While not all the economic and social elements mentionedpreviously must be present to create a successful microfinance industry, the emphasis on properpricing to allow the creation of sustainable institutions is critical.6

Bank Rakyat Indonesia Unit Desa

Bank Rakyat Indonesia is one of the largest commercial banks in Indonesia with US$13 billion in totalassets as of August 1996. It is also the most prominent institution in Indonesia’s microfinance sector.Originally one of five state-owned development banks, BRI today operates as a commercial bankowned by the government. Besides its standard commercial banking services and extensive branchnetwork throughout the country, it also operates the BRI Unit Desa division with total assets of US$3billion. Of the 44,000 BRI employees, 23,000 are employed in the Unit Desa’s activities. Althoughthe Unit Desa system represents only 23 percent of the Bank’s total assets, it generates 40 percent ofits total revenues, achieving a 4.7 percent return on assets.

The Unit Desa division had its origins in 1970 when the government charged BRI with serving thefinancial requirements of the Indonesian rice-intensification program. BRI established more than3,600 village units between 1970 and 1983, primarily in sub-district market towns. Bank Indonesiaprovided capital for these rural credits in the form of three percent liquidity credits, and the Ministryof Finance provided administrative operating subsidies.

By the early 1980s subsidies were discontinued, requiring BRI to adopt a new approach to ruralbanking. At this point, the Ministry of Finance, and particularly its Center for Policy andImplementation Studies, pressed for a significant liberalization of bank regulations. In July 1983, theMinister of Finance granted BRI authority to charge ‘break-even’ interest rates on commercial loansand savings. BRI responded to the new regulatory environment by adopting three significant policychanges to revitalize the Unit Desas:

6 This discussion draws heavily from Chaves and Gonzalez-Vega (1996).

Regulation and Supervision Case Studies

9

1. Transformation of the village units from subsidized credit conduits to full-service rural banks.

2. Internal treatment of the Unit Desas as semi-autonomous profit centers rather than simply aspostings in BRI’s overall accounts.

3. Evaluation of the village units based on their profitability rather than on hectares covered ormoney lent.

In January 1984, the operations of the Unit division began its new program financed by borrowings atinterest rates that reflected the cost of funds. In combination with lending rates that allowed a positivemargin, BRI established a built-in incentive to mobilize resources from savers, thus laying thegroundwork for the creation of a viable rural banking system.7

BRI’s success can be traced to a number of factors:

1. The use of scarce high-level management resources for microfinance development;

2. The development of financial instruments designed and priced specifically to meet localdemand and return profits;

3. Simple, transparent accounting and reporting procedures;

4. Treatment of each village unit as a profit center, with its own profit and loss statement andbalance sheet;

5. Attention to the appropriate timing and sequencing in building the village unit system;

6. The creation of specialized staff training and incentive systems that emphasize responsibilityat the unit level;

7. A decentralized management structure;

8. Knowledge of local markets;

9. Respect for and close relations with the units’ predominantly rural, lower-income clients;

10. A well-designed and implemented supervision process.8

7 This section draws heavily from Boomgard, James and Angell, Kenneth, “BRI’s Unit Desa System: Achievements

and Replicability” in Otero and Rhyne (eds.) The New World of Microenterprise Finance. West Hartford, CT:Kumarian.

8 These points are drawn from Sugianto and Robinson, Marguerite, “Commercial Banks as Microfinance Providers,”November 1996, prepared for the USAID Commercial Banks and Microenterprise Finance workshop, Washington,DC.

MicroFinance Network

10

Supervision of MFIs in Indonesia

With over 15,000 microfinance units in Indonesia and decades of experience, there are importantlessons learned about the supervision of microfinance institutions. The most important is that whileBank Indonesia has the legal responsibility to supervise all MFIs, it only directly supervises about onethousand units, which mostly include private village banks. As shown in Table 3, Bank Indonesia hasentered into a third-party arrangement with various agencies to provide MFIs with direct supervision,including on-site audits. For indirect supervision (e.g., monitoring field reports), MFIs provide somereports directly to Bank Indonesia. Bank Indonesia’s reliance on third parties to conduct directsupervision is reasonable given that the various village units account for ninety-eight percent of thebanking institutions but less than one percent of the total assets of the financial system.

Table 3: Supervisory Arrangements in Indonesia

# Units Supervisory BodyBRI Village Units 3,581 BRI-Village Unit Division

Village-Owned Banks 5,435 BRI-Small & Cooperative Division

Provincial Village Banking Networks 6,131 Provincial Development Banks

Private Village Banks 1,000 Bank Indonesia

BRI Supervision of the Unit DesasThe Unit Division oversees its own village network. This division’s operations are independent ofBRI’s commercial branch network, which offers a range of commercial banking services to a higher-end market. Separate from the BRI’s commercial banking branch network, the Unit Desas form theirown branch network. Pricing policies are set for the system as a whole and consistent administrativesystems are used across all units. Different from most branch arrangements, however, there isconsiderable local financial intermediation (e.g., collecting savings and on-lending from the samevillage unit), and each unit is evaluated for profitability.

In most BRI branches, there are two managers of the Unit division reporting directly to the bank’sbranch manager. The Unit Desa manager is responsible for visiting each unit weekly, to review thereports submitted, and to ensure their veracity. This responsibility may include supervising up to nineunits. If there are more than nine units in a given branch area, a Unit Officer is assigned to providesupport to the Unit Manager.

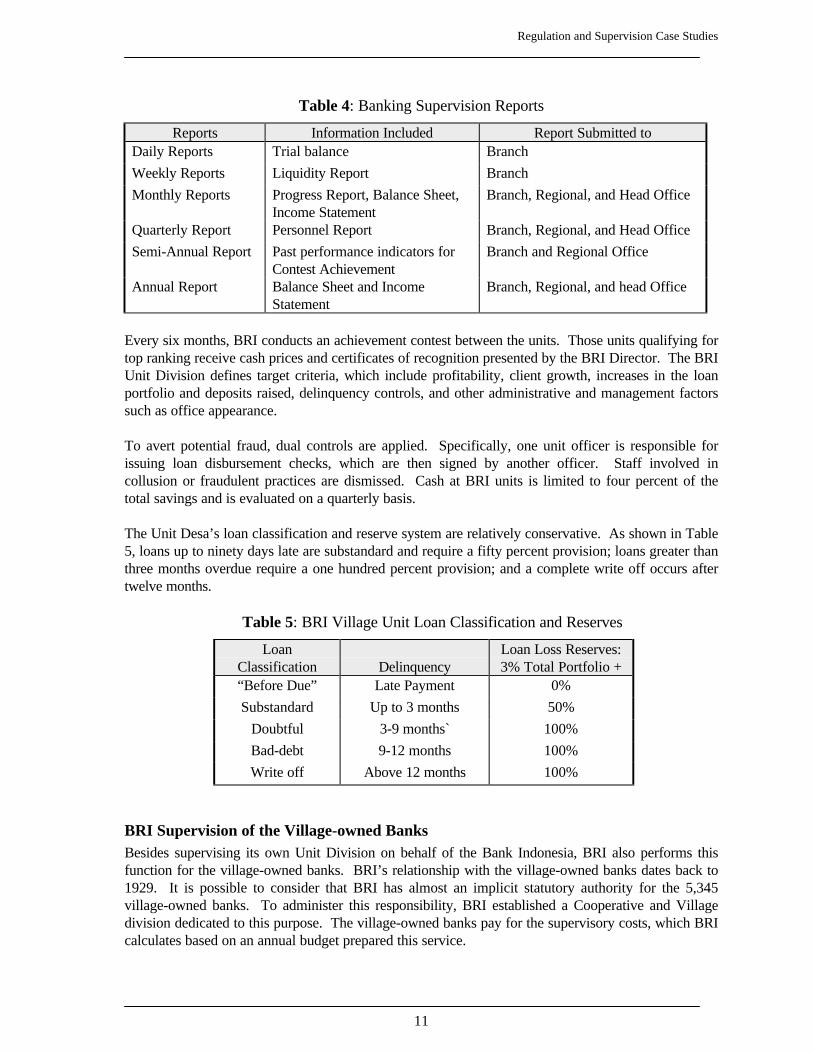

The BRI Unit Desa’s supervision of its own system includes elements of prudential control, standardmanagement, and financial controls. Regular reports comprise the documentation provided to the BRIUnits. These are outlined in Table 4. The monthly Progress Report includes twenty-seven keyindicators, which are tracked on a monthly basis to observe positive or negative performance trends.Performance indicators are ranked by color-coding: on-time repayment is ranked positive (green) ifless than two percent of the portfolio is in arrears; poor (red) status is assigned for those withdelinquency of greater than 4.5 percent; satisfactory (yellow) rating is provided for portfoliodelinquency above 2 percent and less than 4.5 percent. If a branch’s performance is poor, the UnitManager will visit borrowers directly, and new loans may be withheld until the Unit’s performanceimproves.

Regulation and Supervision Case Studies

11

Table 4: Banking Supervision Reports

Reports Information Included Report Submitted toDaily Reports Trial balance Branch

Weekly Reports Liquidity Report Branch

Monthly Reports Progress Report, Balance Sheet,Income Statement

Branch, Regional, and Head Office

Quarterly Report Personnel Report Branch, Regional, and Head Office

Semi-Annual Report Past performance indicators forContest Achievement

Branch and Regional Office

Annual Report Balance Sheet and IncomeStatement

Branch, Regional, and head Office

Every six months, BRI conducts an achievement contest between the units. Those units qualifying fortop ranking receive cash prices and certificates of recognition presented by the BRI Director. The BRIUnit Division defines target criteria, which include profitability, client growth, increases in the loanportfolio and deposits raised, delinquency controls, and other administrative and management factorssuch as office appearance.

To avert potential fraud, dual controls are applied. Specifically, one unit officer is responsible forissuing loan disbursement checks, which are then signed by another officer. Staff involved incollusion or fraudulent practices are dismissed. Cash at BRI units is limited to four percent of thetotal savings and is evaluated on a quarterly basis.

The Unit Desa’s loan classification and reserve system are relatively conservative. As shown in Table5, loans up to ninety days late are substandard and require a fifty percent provision; loans greater thanthree months overdue require a one hundred percent provision; and a complete write off occurs aftertwelve months.

Table 5: BRI Village Unit Loan Classification and Reserves

LoanClassification Delinquency

Loan Loss Reserves:3% Total Portfolio +

“Before Due” Late Payment 0%

Substandard Up to 3 months 50%

Doubtful 3-9 months` 100%

Bad-debt 9-12 months 100%

Write off Above 12 months 100%

BRI Supervision of the Village-owned BanksBesides supervising its own Unit Division on behalf of the Bank Indonesia, BRI also performs thisfunction for the village-owned banks. BRI’s relationship with the village-owned banks dates back to1929. It is possible to consider that BRI has almost an implicit statutory authority for the 5,345village-owned banks. To administer this responsibility, BRI established a Cooperative and Villagedivision dedicated to this purpose. The village-owned banks pay for the supervisory costs, which BRIcalculates based on an annual budget prepared this service.

MicroFinance Network

12

As part of its regulatory oversight function, BRI establishes the interest rates charged on loans,interest rates paid on savings, and the maximum loan size. BRI is responsible for ensuring effectiveinternal control of the village-owned banks. Supervisors oversee about twenty village-owned banksand are required to make monthly visits. This is relatively close supervision considering that somevillage-owned banks are only open one day a week. In addition to the supervisors, there is also atraveling bookkeeper who works with about five village-owned banks.

The reporting requirement for village-owned banks is not as extensive as that provided by the UnitDesas. Under the supervision of BRI, village-owned banks produce a monthly balance sheet, incomestatement, and a portfolio report, which they submit to Bank Indonesia for review.

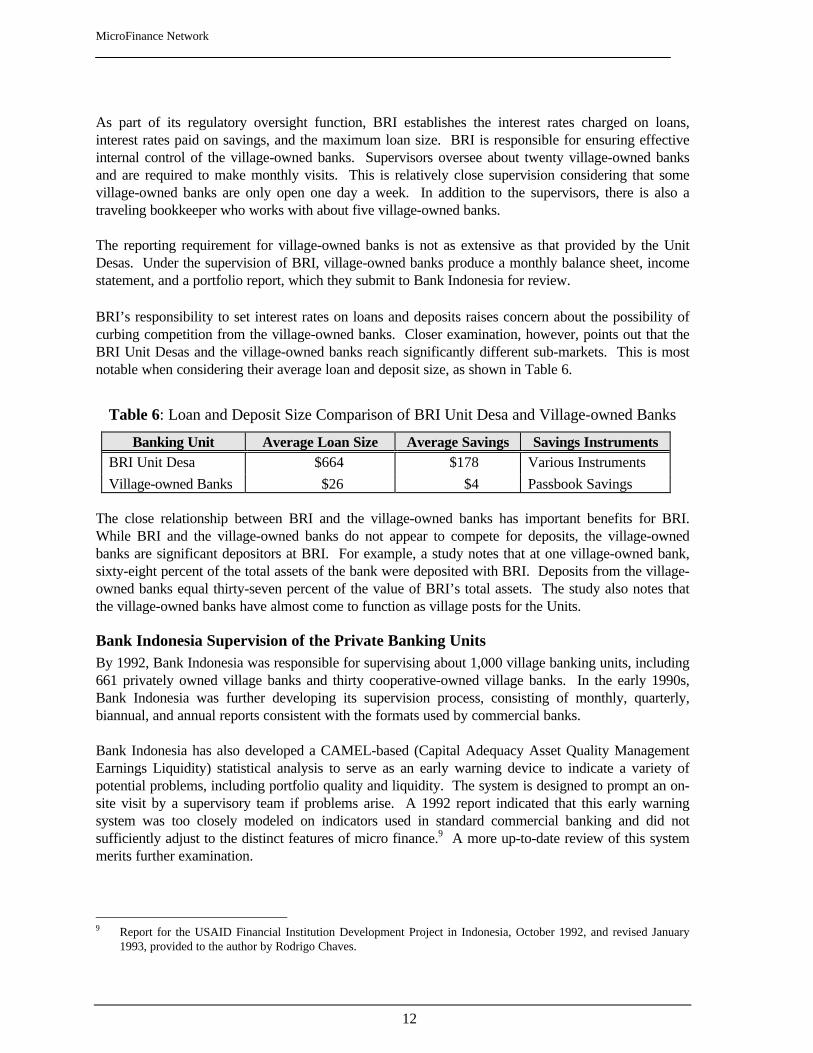

BRI’s responsibility to set interest rates on loans and deposits raises concern about the possibility ofcurbing competition from the village-owned banks. Closer examination, however, points out that theBRI Unit Desas and the village-owned banks reach significantly different sub-markets. This is mostnotable when considering their average loan and deposit size, as shown in Table 6.

Table 6: Loan and Deposit Size Comparison of BRI Unit Desa and Village-owned Banks

Banking Unit Average Loan Size Average Savings Savings InstrumentsBRI Unit Desa $664 $178 Various Instruments

Village-owned Banks $26 $4 Passbook Savings

The close relationship between BRI and the village-owned banks has important benefits for BRI.While BRI and the village-owned banks do not appear to compete for deposits, the village-ownedbanks are significant depositors at BRI. For example, a study notes that at one village-owned bank,sixty-eight percent of the total assets of the bank were deposited with BRI. Deposits from the village-owned banks equal thirty-seven percent of the value of BRI’s total assets. The study also notes thatthe village-owned banks have almost come to function as village posts for the Units.

Bank Indonesia Supervision of the Private Banking UnitsBy 1992, Bank Indonesia was responsible for supervising about 1,000 village banking units, including661 privately owned village banks and thirty cooperative-owned village banks. In the early 1990s,Bank Indonesia was further developing its supervision process, consisting of monthly, quarterly,biannual, and annual reports consistent with the formats used by commercial banks.

Bank Indonesia has also developed a CAMEL-based (Capital Adequacy Asset Quality ManagementEarnings Liquidity) statistical analysis to serve as an early warning device to indicate a variety ofpotential problems, including portfolio quality and liquidity. The system is designed to prompt an on-site visit by a supervisory team if problems arise. A 1992 report indicated that this early warningsystem was too closely modeled on indicators used in standard commercial banking and did notsufficiently adjust to the distinct features of micro finance.9 A more up-to-date review of this systemmerits further examination.

9 Report for the USAID Financial Institution Development Project in Indonesia, October 1992, and revised January

1993, provided to the author by Rodrigo Chaves.

Regulation and Supervision Case Studies

13

Supervision IssuesThe experience from Indonesia points to a number of important lessons regarding the supervision ofmicrofinance institutions.

Third Party Supervision is a Viable Alternative. Because of the volume of institutions to supervise,it has proven effective to contract-out prudential supervision to a third party. Bank Indonesia isfortunate to have appropriately qualified institutions, such as BRI and municipal development banks,to perform these functions. The supervision of effective regulation, however, should not be confusedwith abdicating responsibility to form appropriate regulatory guidelines. This should remain with thestatutory body responsible for regulation, regardless of whether the direct supervision is conducted bya third party or by an in-house division. The objective of the supervision should be to verify theaccuracy of data, monitor financial controls, and ensure adherence to bank regulations.

Simplification of the Supervision Methods. The greater number of institutions engaged in third-party supervisory arrangements and the higher volume of MFIs that require supervision, lead to theimportance of simplifying and standardizing the supervision process. For example, because of itssimplicity – and the fact that most village banks are not computerized – BRI firmly recommends theuse of cash accounting in place of accrual accounting. Loan classification should be definedaccording to standard, measurable indicators (e.g., days late as opposed to a qualitative analysis).Reports should be standardized, incorporating the same information for each period. The supervisionprocess should be designed towards increasing efficiency and reducing individual discretion.

Still a Challenge to Adjust to the Unique Features of MFIs. Even in Indonesia, after more thantwenty years’ experience with large scale microfinance, concern remains regarding the imposition ofcommercial banking methods and norms on MFIs. Sugianto and Robinson (1996) commented thatregulators required the same level of planning and documentation to open a four-person village-ownedunit as they would require of any commercial bank branch. They also found the requirements tonotarize the proof of collateral excessive for the needs of MFIs. Portfolio reporting formats used byBank Indonesia required MFIs to report on individual loans instead of analyzing the performance ofthe portfolio as a whole. There is also concern that some sections of the banking industry still favorsubsidized lending, leading to overall pricing distortions in the microfinancial services market.

Importance of Prudential Supervision of the Savings of the Low-income. The most importantlesson to come from the Indonesia experience is that it is possible to exert prudential supervision overinstitutions that provide savings services to the low-income market. Previous conventional wisdomcontended that, given their small size and great number, it is simply not economically viable orphysically possible to exert prudential supervision over thousands of small MFIs. Experience fromIndonesia shows that this is not the case. Even with average deposit sizes of less than US$5, if anappropriate and efficient system is adopted, it is possible for savings facilities to meet their cost ofsupervision. Financial services for low-income communities can be just as reliable as those offered allsectors of the society.

MicroFinance Network

14

Regulation and Supervision Case Studies

15

ÐÐ

BANGLADESH

ÓÓ

Janney Carpenter

Bangladesh has one of the oldest and most diverse microfinance sectors in the world, including someof the largest and most sophisticated microfinance institutions.10 The three largest MFIs, for example– Grameen Bank, BRAC, and ASA – served a combined membership of more than four million peopleas of December 1996.11 In Bangladesh, the unique circumstances of no regulatory oversight and alarge, well-funded non-governmental organization (NGO) community have resulted in the ad hocevolution of sophisticated and innovative MFIs seeking to alleviate poverty. Most MFIs inBangladesh combine microcredit with a strong education and social-change agenda to address thestructural poverty of rural landless individuals, so credit (and financial services) may be only part oftheir development activities.

Most MFIs in Bangladesh are NGOs, which are exempt from oversight by the central bank despitetheir ability to lend and collect deposits from members. According to the local trade association, 351NGOs provide microfinance services, credit and savings, though the four largest NGOs representabout 80 percent of the total loans outstanding.12 This chapter focuses on those organizations forwhich microfinance is the sole or primary activity and that are striving for financial self-sufficiency.

At present, the only MFI in Bangladesh regulated by the central bank is the Grameen Bank, thecountry’s largest microlender. Grameen was organized under a special, one-time bank charter issuedby the Ministry of Finance in 1983. Grameen has lent more than US$1.17 billion to about two millionmembers.13 Its innovation in peer group lending has become a local and global model for lending tothe asset-less persons.14 The Bangladesh Bank (the central bank) has traditionally viewed NGOs asdistinct from other financial institutions because of their social and development missions. However,as MFIs continue to expand and solicit member savings to finance loans, the Bangladesh Bank mustreconsider whether it needs some regulatory oversight to protect individual depositors and savers fromfraud and mismanagement.

10 This case study was written with assistance from: Cliff Kellogg of Shorebank Corporation, who conducted field

research in Dhaka; David Wright, Senior Advisor at the Department for International Development, UK; and StuartRutherford of Dhaka, Bangladesh; all of whom reviewed drafts and shared their valuable insights.

11 Credit and Development Forum, “CDF Statistics: Microfinance Statistics of NGOs,” Published in Dhaka,Bangladesh, April 1997 based on December 1996 data.

12 Ibid.13 As of December 1996, the exchange rate for the Bangladesh Taka was Tk. 42: US$1. Over the past few years, the

90-day Government Treasury Bill Rate has been maintained at 3-5%, and annual inflation has run 6-10%.14 The Grameen Bank pioneered a lending model that extends loans to members of five-person peer groups, thereby

replacing traditional collateral with peer pressure and incentives to maintain access to additional loans. ManyBangladesh microcredit organizations use the same model, or variations on it, because of its effectiveness with low-income, rural populations.

MicroFinance Network

16

This chapter highlights the current formal and semi-formal financial sectors in Bangladesh, how theGrameen Bank fits within the banking regulatory and supervisory framework, and the challenges ofdesigning an appropriate regulatory framework for MFIs in a country with limited experience inregulation and supervision. The case study is organized into the following sections:

• Context: The Formal and Semi-formal Financial Sectors;

• The Grameen Bank;

• The Regulation Dilemma: How Much and How To Do It Well?

• Observations and Conclusions from Bangladesh.

The Bangladesh Bank is currently reviewing the need to monitor and oversee MFIs as part of a WorldBank study.15 This presents Bangladesh with an opportunity to revisit these questions and create anappropriate oversight framework to protect depositors in these specialized financial intermediaries. Asless sophisticated consumers with little political representation, the most compelling argument forregulation of MFIs is to protect member savings. However, the Bangladesh Bank must exerciseregulation and supervision carefully to avoid quashing specialized financial intermediaries that havedeveloped innovative and effective ways of serving low-income persons.

Context: The Formal And Semi-Formal Financial Sectors

Financial services in Bangladesh come from three areas: informal sources (family, friends, ROSCAsand savings clubs,16 and moneylenders); the semi-formal sector of NGO microlending; and the formalsector of agricultural and nationalized commercial banks, along with ten privately owned banks. Likemany countries, only the formal sector is regulated, with no regulation or supervision specificallyfocused on MFIs. The public policy reasons for regulating the financial sector are: (i) individualdepositors need protection from fraud and mismanagement by financial institutions because the publicdoes not have the information or expertise to evaluate those risks; and (ii) if the government providesdeposit insurance or financial support to the financial sector, it imposes some risk parameters on thoseinstitutions. As MFIs push further into financial intermediation and use member savings as a majorfunding source, some degree of oversight under the first rationale may be appropriate. At present,depositors and funders of NGO microfinance institutions rely primarily on the integrity ofmanagement to protect their funds.

The Formal SectorAs of December 1996, the formal financial sector in Bangladesh consisted of thirty-two bankinginstitutions: fifteen national commercial banks (state-owned commercial banks), two agricultural banknetworks (also state-owned), ten privately owned banks, and a few recently established non-bankfinance and leasing companies. The Bangladesh Bank is the primary regulatory authority. Though

15 In 1997, The World Bank lent US$100 million to the Bangladesh Bank to finance PKSF, a quasi-governmental

foundation that on-lends funds to NGOs that extend microcredit. This included US$5 million in technical assistancegrants, in part to review these issues.

16 Rotating Savings and Credit Associations (ROSCAs) and savings clubs are actively used in Bangladesh, according toStuart Rutherford’s essay “Informal Financial Services in the Dhaka Slums.” In Wood and Shariff (editors), WhoNeeds Credit. Zed Books, London and UP Dhaka. 1997.

Regulation and Supervision Case Studies

17

much smaller than the central bank, the Ministry of Finance is a political cabinet position andtherefore also wields significant influence.

Structure of the Formal SectorThe fifteen national, state-owned commercial banks are the largest institutions. While their primaryfocus is urban-based lending to the formal sector, they may also provide agricultural credit andmicrocredit through special rural-based programs. For the banks, collection rates on microloanprograms are generally below twenty percent.17 Agricultural banks generally focus on crop-basedlending to larger enterprises. Private banks tend to operate in urban areas, avoiding the rural creditsector because of the high transaction costs and perceived risk. In addition, a small number of creditunions and financial co-operatives also exist, few of which focus on the low-income market (seediscussion under semi-formal sector).

The Bangladesh Bank has encouraged bank lending to rural low-income communities by offeringfunds at a below-market interest rate to banks that undertake direct microlending. The nationalcommercial banks have also provided financing to MFIs on occasion, although there are no formalincentives for banks to lend to or invest in MFIs. A recent loan to the Association for SocialAdvancement (ASA), a NGO microfinance institution, by Agrani Bank, one of the nationalcommercial banks, was fully secured by ASA’s headquarters building and received no specialtreatment. The Bangladesh Bank, however, confirms that it “encourages” national commercial banksto lend to Grameen Bank. In 1995, the national commercial banks bought the full issue ofgovernment-guaranteed bonds floated by the Grameen Bank.

The RegulatorsBank regulation is conducted by the Bangladesh Bank and the Ministry of Finance. The Bank has theresponsibility to establish regulations and supervise the banking sector. It has the power to license andexamine all banks in the country and exerts great influence over the state-owned banks and theirdirectors, in part due to its accountability to the Ministry of Finance. It has a staff of approximatelysix thousand and is headed by a governor appointed by the Ministry of Finance.

The Ministry of Finance is a cabinet-level position within the government, and the Minister is a directpolitical appointee. Where the jurisdictions of the two agencies meet or overlap is unclear, but theMinistry of Finance is influential over the Bangladesh Bank.

Bank Regulatory Framework and SupervisionLike most central banks, the Bangladesh Bank has the authority for both prudential (or preventive)regulation that aims to limit the risks undertaken by banks in their quest for profits and growth, andprotective regulation that gives it the power to grant and revoke banking licenses and to assumecontrol of a mismanaged financial institution. Bank regulatory reform has been underway since 1989to strengthen the effectiveness of the Bangladesh Bank’s oversight of the formal financial sector and tobring supervision practices closer to international banking standards. In 1989, the Bangladesh Bankliberalized interest rates, ended government mandates on the allocation of credit to industrial sectors(although some interest rate subsidies remain for priority sectors such as agriculture), and introduced

17 “Staff Appraisal Report on Bangladesh Poverty Alleviation Microfinance Project.” August 14, 1996. Private Sector

Development and Finance Division, South Asia Region. The World Bank.

MicroFinance Network

18

risk-classification systems for reporting delinquency and portfolio quality.18 In late 1994, regulatoryreform continued as the Bank updated the risk-classification systems and permitted the licensing ofprivate and foreign banks, and non-bank financial institutions.19

Since 1994, there have been no usury laws for banks or MFIs, and fewer restrictions on banks’permitted business activities and pricing.20 Banks are required to submit an interest rate “band” fortheir lending in the current period, but this can be adjusted monthly. Banks are not required to lendonly to formally registered companies or to those which administer value-added taxes.

While the Bangladesh Bank’s regulations require banks to report financial condition, portfolio quality,and earnings to the central bank on a regular basis, the reporting standards remain less stringent thaninternational banking standards. For example, banks are only required to report as delinquent thoseloans unpaid after one year, and loans unpaid after two years are reported as bad debts. One thousandof the six thousand staff positions at the Bangladesh Bank are dedicated to examining the thirty-twonational commercial banks. While the central bank has strengthened considerably, it continues toaddress many challenges in the formal financial sector.

The Semi-Formal Sector: Microfinance InstitutionsAs noted above, most MFIs in Bangladesh are NGOs registered under the Societies Act of 1860,exempting them from central bank oversight. Most have a donor-funded loan pool and hold memberdeposits in a low-risk investment portfolio to pay interest on their savings. Several large MFIs,however – including ASA, Buro Tangail, and BRAC – use member savings to fund their lendingactivity as loan demand has outstripped the supply of donor capital.

The permissiveness of the current regulatory environment allows NGOs to undertake nearly all theactivities they need to meet their development objectives. They can accept deposits, extend credit, andraise capital from donors and private sources. While many organizations have used this flexibility toachieve impressive development impact through creative design, efficient branch networks, andvisionary leadership, their members and funders rely solely upon management to avert fraud,mismanagement, and/or unforeseen circumstances.

The few MFIs that have adopted a legal form with some regulation face minimal oversight andmonitoring. Although a legally chartered bank, Grameen faces minimal supervision. Financial co-operatives are chartered under the Co-operative Societies Ordinance of 1984, permitting them tomobilize deposits from the general public in addition to their members.21 While the government’sRegistrar of Co-operatives regulates these institutions, the registrar has little preventive or protectiveregulation and conducts minimal to no supervision. The largest financial co-operative is FederalSavings, with 26,000 members in urban Dhaka; SelfSave started just recently, and the SocialDevelopment Society (SDS), an existing NGO, is considering use of the ordinance. Now that MFIshave discovered this legal form, there is the potential for rapid expansion of financial co-operativeswith minimal supervision or oversight to protect depositors.

18 Circulars #33 and #34.19 Circular #20.20 Prior to 1994, agricultural lending was capped at 15% annual interest.21 Chapter IV, Article 32 of the Law was revised under Ex-President Ershad to allow more competition for the

country’s poorly performing banks by allowing co-operatives to take on more banking functions with fewerrestrictions than allowed under the British legislation.

Regulation and Supervision Case Studies

19

For those MFIs that are expanding to serve large numbers of low-income persons, and using membersavings to invest in loans and other higher risk instruments, the risks to members’ savings haveincreased significantly. Examples of the heightened risks include:

• Buro Tangail and ASA have funded loan growth from member savings for several years, andASA now raises deposits from the general public, calling them “associate members”;

• SDS mobilizes large amounts of savings by selling contractual savings products in ruralvillages, a vehicle that is often overlooked by those focusing on credit-giving NGOs;

• Federal Savings, a financial co-operative, collects weekly savings from 26,000 members andis growing rapidly, with minimal oversight from the Registrar of Co-operatives;

• Grameen Bank offers 11 different loan products to boost average loan volume per borrower,and has funded the jump in loan demand by issuing debt capital (1995 bond issuance) andincreasing savings per member.

Most of these institutions have strong and charismatic leaders, relatively weak boards of directors, andminimal outside financial review or audit. They will most likely continue to pursue savingsaggressively to fund their lending because the demand for credit exceeds the sources of donor capital.As they assume more of the risks associated with financial intermediaries, these MFI face twochallenges: (i) the need to strengthen their self-regulation and internal controls; and (ii) the possibilityof government regulation through the central bank or some other supervisory body.

So far, the regulatory framework has not caught up with the evolution of microfinance in Bangladesh.The few NGOs that have considered applying for a standard commercial banking license have eitherbeen denied approval or have found the process too time-consuming and uncertain to warrant thepursuit.

Finally, MFIs have faced little pressure or incentive to change the status quo. International donorshave been willing to finance their activities with minimal internal or external oversight requirements,and senior managers see no benefits and many problems with any regulation by the government.While there have been serious cases of fraud and/or mismanagement by NGOs resulting in the loss ofmember savings, they occurred in the 1980s and appear to have faded from memory.22

Structure of The Semi-Formal SectorA few large institutions dominate the microfinance industry in Bangladesh. In June 1996, GrameenBank and three NGOs served eighty-five percent of the active micro-borrowers.23 Grameen, BRAC,and Proshika have traditionally been the largest microlending organizations; Grameen has more than1,000 branches across Bangladesh, BRAC has 375, and Proshika lends to village organizations inmost districts. Each of these was started in the 1970s or early 1980s with a strong politicalempowerment and social change mission to help low-income persons. Some younger NGOs, such asASA and Buro Tangail, emphasize providing streamlined financial services and achieving financial 22 According to Stuart Rutherford, two notable cases include SEDO (Socio-Economic Development Organization),

which collected savings from many villages and failed to return them; and BURO (predecessor to Buro Tangail),which used members’ savings to pay salaries and administrative costs when donor funding failed to materialize,leaving thousands with lost savings.

23 The total number of micro borrowers in Bangladesh in June 1996 was approximately five million. They were beingserved by Grameen (2 million) BRAC (1.4 million), ASA (440,000) and SWANIRVAR Bangladesh (350,000).From Credit and Development Forum (CDF), Vol. 2, No. 1.

MicroFinance Network

20

self-sufficiency in a shorter time frame. ASA is now the third largest MFI in Bangladesh, and BuroTangail is growing rapidly.24

In general, most MFIs are increasing loan volumes and improving cost-effectiveness to achievefinancial self-sufficiency (or to reduce their dependence on subsidies significantly). While most MFIsin Bangladesh are striving for financial self-sufficiency, many provide non-financial services for theirmembers, which require annual donor support. Some of these complex NGOs are separating theirdevelopment and financial services activities to allow the latter to break even or achieve profitability.In addition, there has been a strong shift to the provision of financial services, rather than just credit.While most microlenders still require weekly savings as a screening device for members, ASA, BuroTangail, and BRAC have all launched voluntary savings products to meet their members’ liquidityneeds.

Regulators and IntermediariesThe Grameen Bank is regulated and supervised by the Ministry of Finance because of the bank’sunique charter. The 1983 Ordinance exempts Grameen from regulation by the Bangladesh Bank,although the Ministry of Finance delegates some of its monitoring responsibilities for Grameen to thecentral bank (this is described in greater detail below).

Those NGOs large enough to receive foreign funding are overseen by the NGO Bureau, which mustapprove all foreign aid inflows. To receive foreign funds, the NGO must submit a work plan and abudget for the proposed project. However, the Bureau does not conduct any assessment, examination,or evaluation of the financial condition of the NGO or the financial viability of the project. Fundersare responsible for completing their own risk assessment before funding an NGO, with no third partysupervision or monitoring other than annual financial audits and periodic evaluations and assessments.

One entity that will exert increasing influence over NGO microfinance institutions is the Palli KarmaSahayak Foundation (PKSF), a government-funded foundation created in 1990 to provide loans toNGOs engaged in microcredit. PKSF is becoming a more significant presence through its receipt of aUS$100 million World Bank loan in 1997 for lending to NGOs. While PKSF does not regulate MFIs,it can influence the semi-formal sector by setting performance and reporting standards for itsborrowers. One of its goals is to encourage professionalism and better management practices amongmicrocredit organizations. PKSF lends money at 4 to 5 percent for three and four year terms, andcurrently funds more than 200 NGOs. The government appoints the board, and the board elects amanaging director.25

Finally, the Credit and Development Forum was established in 1996 as a trade association formicrocredit NGOs, but has primarily served as an information clearing house thus far.

In summary, given the trends in the semi-formal financial sector in Bangladesh, regulators andfunders/investors should reassess whether NGOs that accept deposits should be exempt from centralbank oversight. Some regulation and supervision are necessary if NGOs are mobilizing savings andserving as financial intermediaries. However, it must be carefully designed and well executed to avoid

24 Buro Tangail had more than 30,000 members as of December 1996, according to an interview with Buro Tangail

Head Office. ASA had 544,000 active borrowers according to their March 1997 newsletter.25 The Managing Director of Grameen Bank is the current chairman of PKSF’s Board.

Regulation and Supervision Case Studies

21

opening a bureaucratic noose for the effective financial services sector for Bangladesh’s low-incomecommunities.

Existing Regulation: The Grameen Bank Charter