Embed Size (px)

DESCRIPTION

yo

Citation preview

Regulations on FDI,ADR,GDR,IDR,FII, ECBs

Dr. Monika Chopra

FDI-Foreign Direct Investment

• What is FDI? It is an investment made to acquire a lasting

management interest (usually 10 percent of voting stock) in an enterprise operating in a country other than that of the investor.

Varieties of FDI

• FDI is permitted via:• Financial Collaborations• Joint Ventures & Technical Collaborations.• Capital markets via euro issues.• Private placements or preferential issues.

FORMS

1) By Direction*Inward*Outward2) By Target*Mergers and Acquisitions*Horizontal FDI*Forward Vertical FDI/Backward VerticalFDI

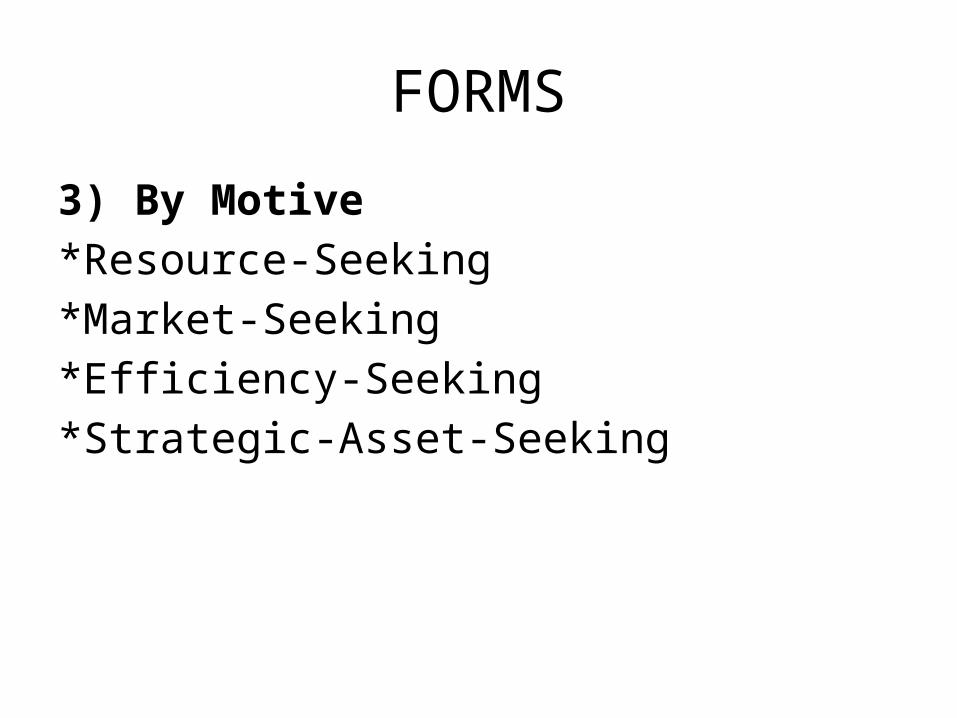

FORMS

3) By Motive*Resource-Seeking*Market-Seeking*Efficiency-Seeking*Strategic-Asset-Seeking

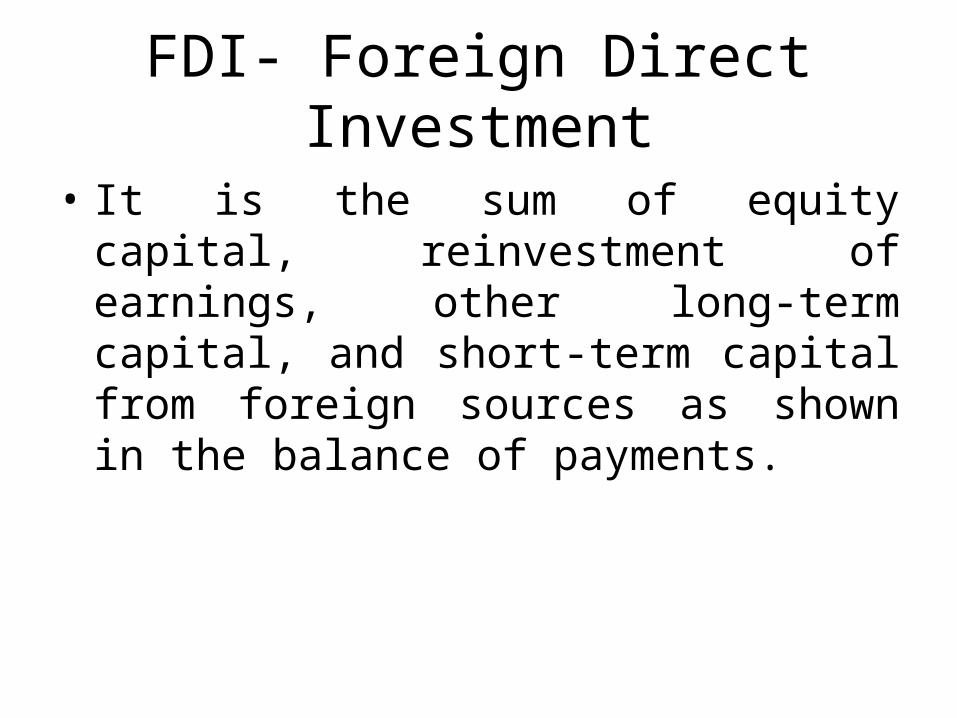

FDI- Foreign Direct Investment

• It is the sum of equity capital, reinvestment of earnings, other long-term capital, and short-term capital from foreign sources as shown in the balance of payments.

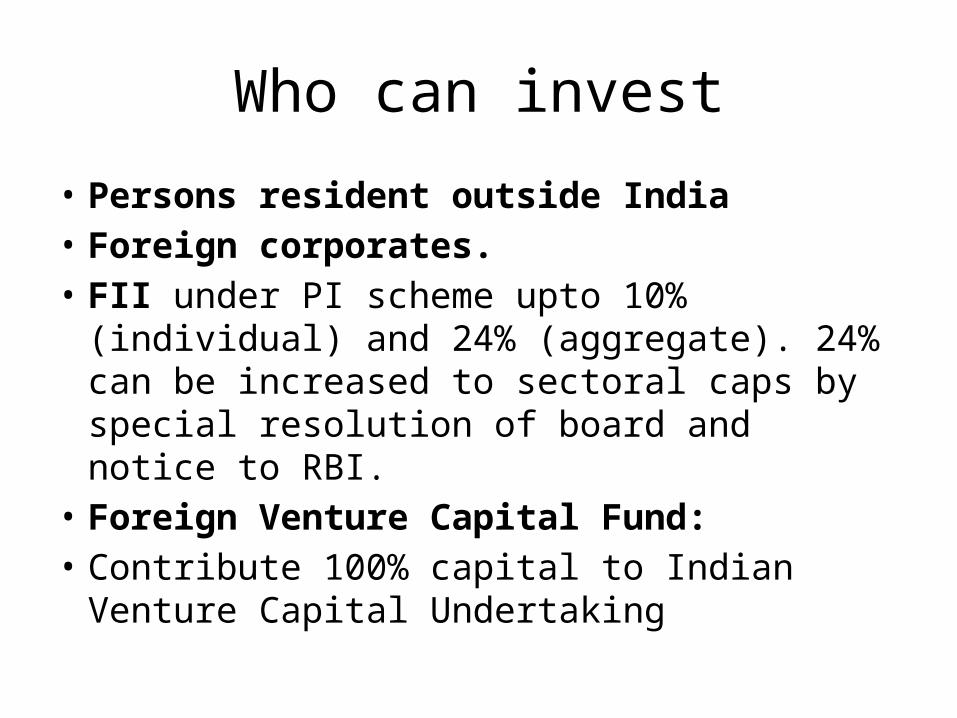

Who can invest

• Persons resident outside India • Foreign corporates.• FII under PI scheme upto 10%(individual) and

24% (aggregate). 24% can be increased to sectoral caps by special resolution of board and notice to RBI.

• Foreign Venture Capital Fund:• Contribute 100% capital to Indian Venture

Capital Undertaking

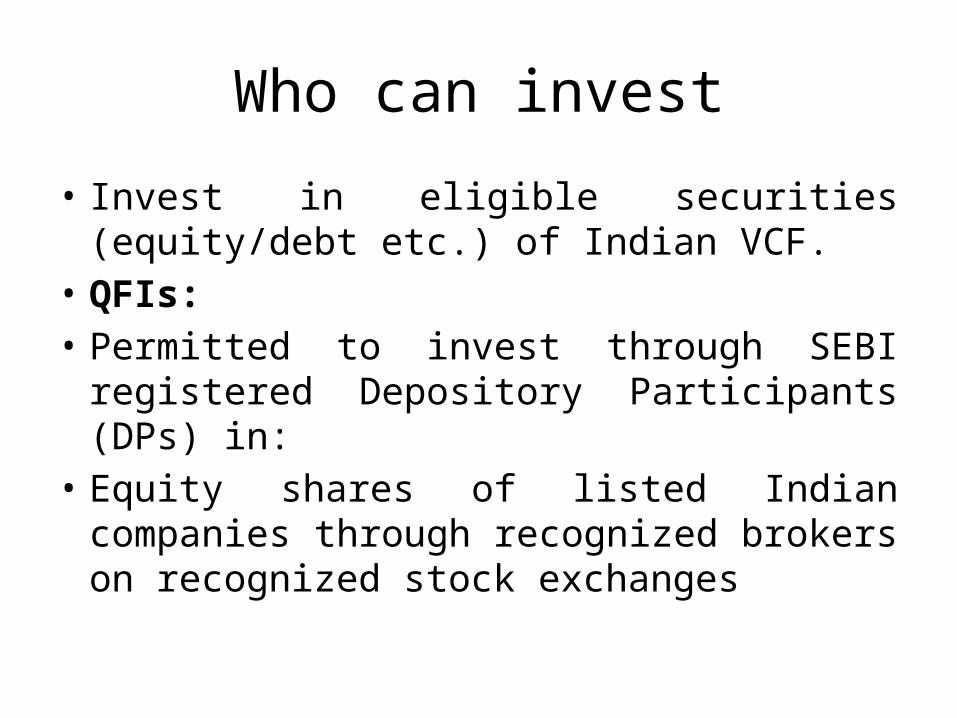

Who can invest

• Invest in eligible securities (equity/debt etc.) of Indian VCF.

• QFIs:• Permitted to invest through SEBI registered

Depository Participants (DPs) in:• Equity shares of listed Indian companies

through recognized brokers on recognized stock exchanges

Who can invest

• Equity shares offered to public.• Acquire equity shares by way of right shares,

bonus shares or equity shares on account of stock split / consolidation.

• Equity shares on account of amalgamation, demerger or such corporate actions subject to the prescribed investment limits.

• Dividend may be directly remitted or transferred to a pool a/c with no interest payment.

Entities in which FDI can be done

• Partnership/Proprietary concern• Indian Companies (Public)• FDI in Indian Venture Capital Fund(If in Trust,

Approval, If in Company: Automatic)• FDI in Limited liability partnerships

Types of Instruments used for FDI

• Equity shares, fully, compulsorily and mandatorily convertible debentures and fully, compulsorily and mandatorily convertible preference shares.

• The price/ conversion formula of convertible capital instruments should be determined at the time of issue of the instruments and should not in any case be lower than the fair value worked out, at the time of issuance of such instruments

Types of Instruments used for FDI

• Other types of Preference shares/Debentures i.e. non-convertible, optionally convertible or partially convertible for issue of which funds have been received on or after May 1, 2007 are considered as debt.

• All norms applicable for ECBs relating to eligible borrowers, recognized lenders, amount and maturity, end-use stipulations, etc. shall apply

Types of Instruments used for FDI

• These instruments would be denominated in rupees, the rupee interest rate will be based on London Interbank Offered Rate (LIBOR) plus the spread as permissible for ECBs of corresponding maturity.

• FDI via DRs and FCCBs

FDI via ADR/GDR

• The inward remittance received by the Indian company vide issuance of are treated as FDI and counted towards FDI.

• Listed companies restricted from raising funds from Indian Capital Market cannot raise via ADR/GDR.

• Unlisted company require prior approval or simultaneous listing.

• Unlisted companies have to list in domestic market on profit making or within three years of such issue.

FDI via ADR/GDR

• No end use restrictions on proceeds except investment in real estate and stock markets

• Two-way Fungibility Scheme:• A stock broker in India, registered with SEBI,

can purchase shares of an Indian company from the market for conversion into ADRs/GDRs based on instructions received from overseas investors; can also redeem them into shares

FDI via ADR/GDR

• Redemption and Reconversion should be equal.• Sponsored ADR/GDR issue:• The company offers its resident shareholders a

choice to submit their shares back to the company so that on the basis of such shares, ADRs / GDRs can be issued abroad.

• The proceeds of the ADR / GDR issue are remitted back to India and distributed among the resident investors who had offered their Rupee denominated shares for conversion.

FDI via ADR/GDR

• These proceeds can be kept in Resident Foreign Currency (Domestic) accounts in India by the resident shareholders who have tendered such shares for conversion into ADRs / GDRs.

FDI Routes

Automatic Route • FDI up to 100 per cent is allowed under the

automatic route in all activities/sectors except where the provisions of the consolidated FDI Policy, issued by the Government of India from time to time, are attracted.

• FDI in sectors /activities to the extent permitted under the automatic route does not require any prior approval either of the Government or the Reserve Bank of India.

FDI Routes

Government Route• FDI in activities not covered under the

automatic route requires prior approval of the Government which are considered by the Foreign Investment Promotion Board (FIPB).

Prohibited sectors

• FDI is prohibited under the Government Route as well as the Automatic Route in the following sectors:

i) Retail Trading (except single brand product retailing)

ii) Atomic Energy

iii) Lottery Business

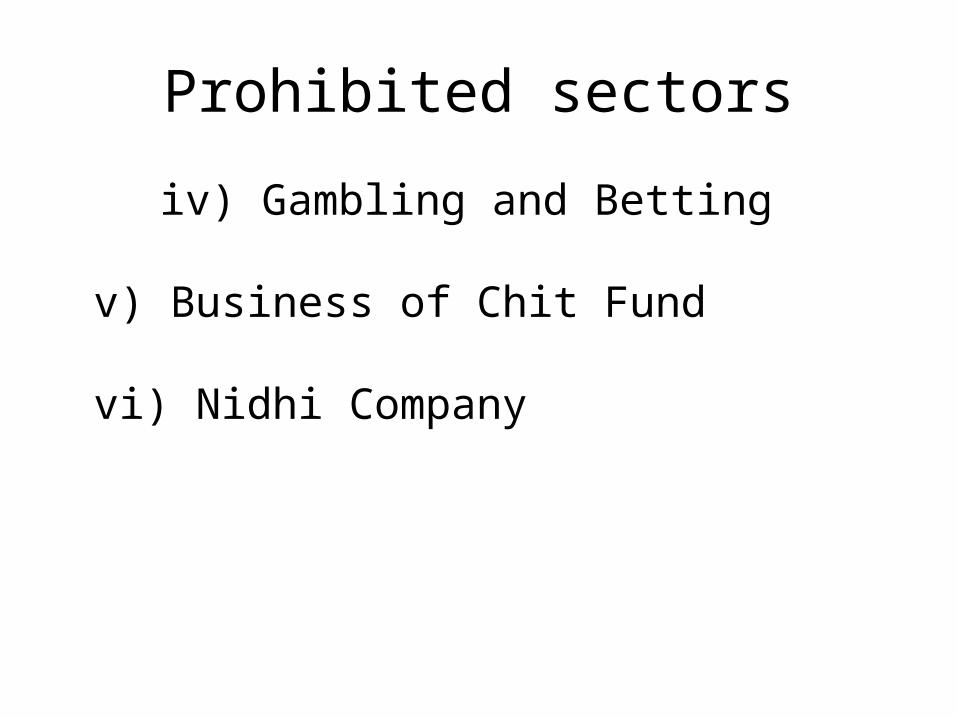

Prohibited sectors

iv) Gambling and Betting

v) Business of Chit Fund

vi) Nidhi Company

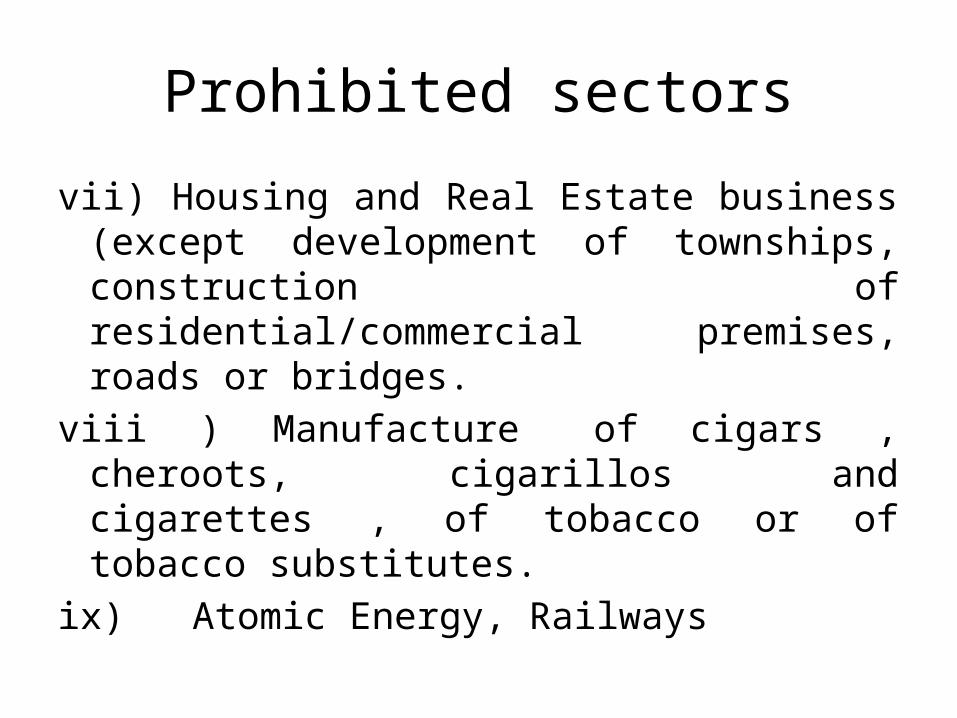

Prohibited sectors

vii) Housing and Real Estate business (except development of townships, construction of residen tial/commercial premises, roads or bridges.

viii ) Manufacture of cigars , cheroots, cigarillos and cigarettes , of tobacco or of tobacco substitutes.

ix) Atomic Energy, Railways

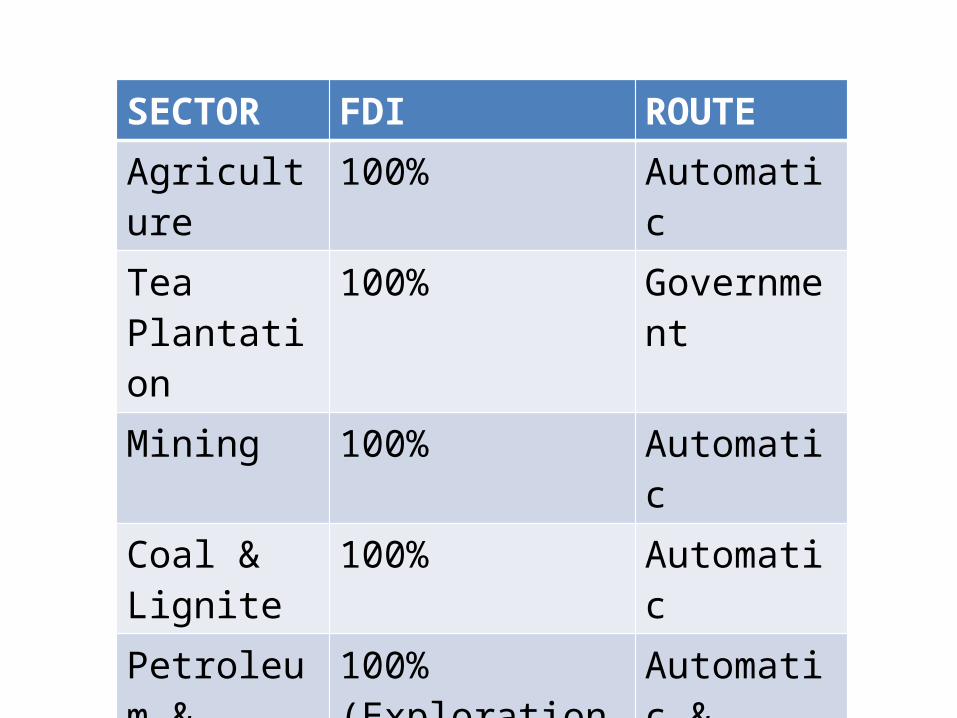

SECTOR FDI ROUTEAgriculture 100% AutomaticTea Plantation

100% Government

Mining 100% AutomaticCoal & Lignite

100% Automatic

Petroleum & Natural gas

100%(Exploration)49%(Refinery)

Automatic & Govt.

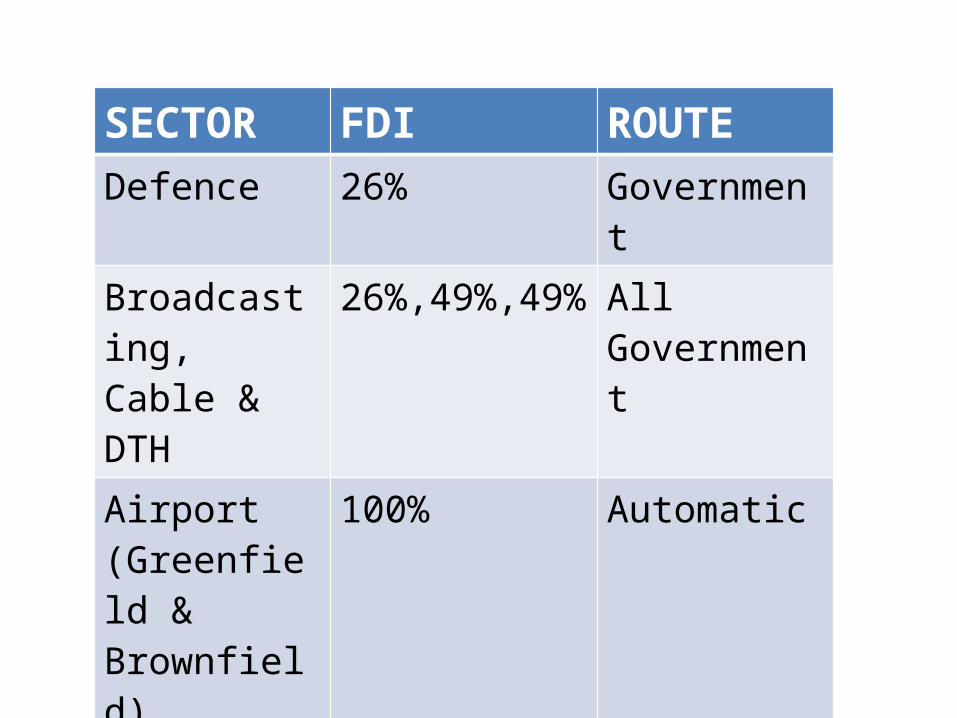

SECTOR FDI ROUTEDefence 26% GovernmentBroadcasting, Cable & DTH

26%,49%,49% All Government

Airport (Greenfield & Brownfield)

100% Automatic

Insurance 26% AutomaticTelecom Upto 49%

(Automatic)49-74% (Government)

Methods of FDI

A foreign company planning to set up business operations in India may:

• Incorporate a company as a Joint Venture or a Wholly Owned Subsidiary.

• Set up a Liaison Office / Representative Office or a Project Office or a Branch Office of the foreign company

Procedure after investment

• On receipt of share application money Report details of foreign investors within 30

days of receipt.• On issue of Shares Certificate regarding meeting of norms

regarding procedure for issue and meeting of sectoral caps

State the type of share issue viz. new, bonus, rights, ESOPs, merger/amalgamation

Calculation of FDI

• Investment in Indian companies can be made both by non-resident as well as resident Indian entities.

• Any non-resident investment in an Indian company is direct foreign investment.

• An Indian company would have indirect foreign investment if the Indian investing company has foreign investment in it.

Calculation of FDI

• The indirect investment can also be a cascading investment i.e. through multi-layered structure.

• It is also called Downstream Investment• Total FDI = Direct + Indirect FDI• Example

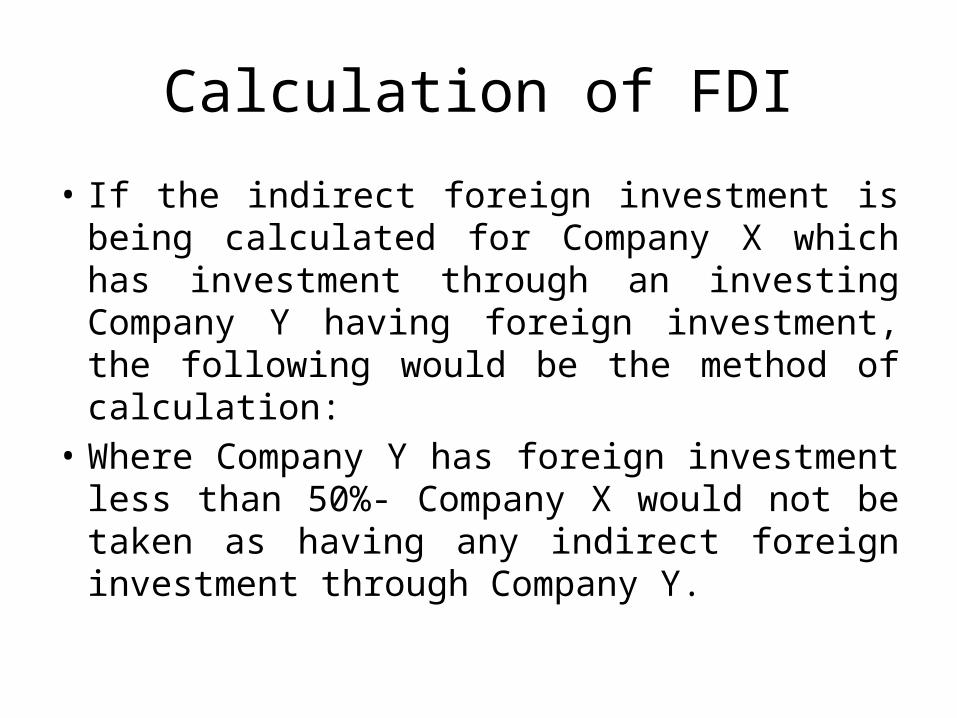

Calculation of FDI

• If the indirect foreign investment is being calculated for Company X which has investment through an investing Company Y having foreign investment, the following would be the method of calculation:

• Where Company Y has foreign investment less than 50%- Company X would not be taken as having any indirect foreign investment through Company Y.

Calculation of FDI

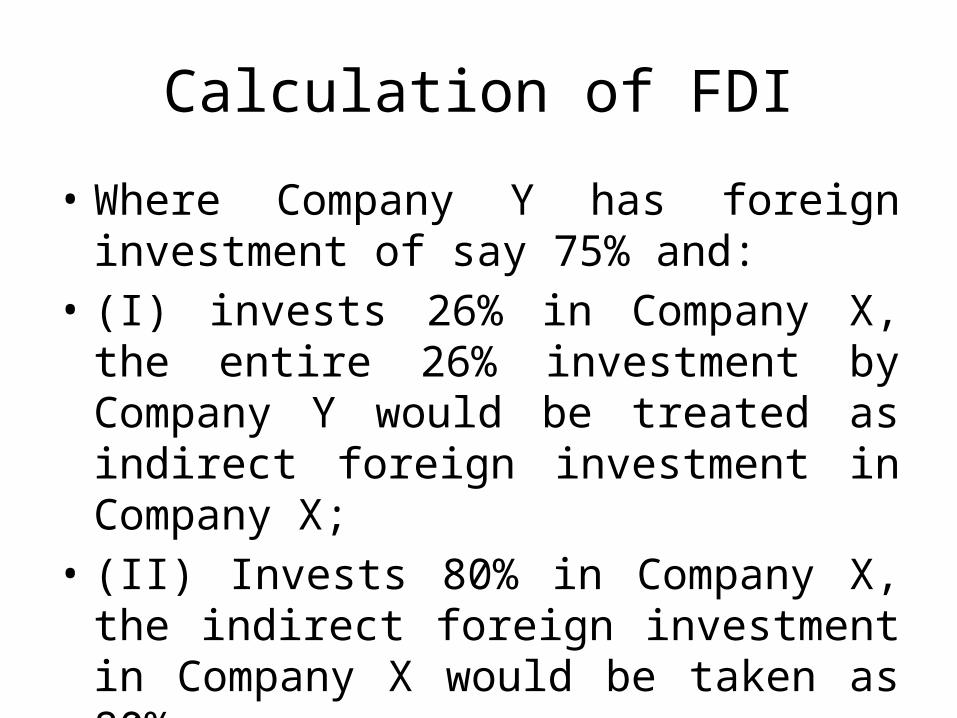

• Where Company Y has foreign investment of say 75% and:

• (I) invests 26% in Company X, the entire 26% investment by Company Y would be treated as indirect foreign investment in Company X;

• (II) Invests 80% in Company X, the indirect foreign investment in Company X would be taken as 80%

Calculation of FDI

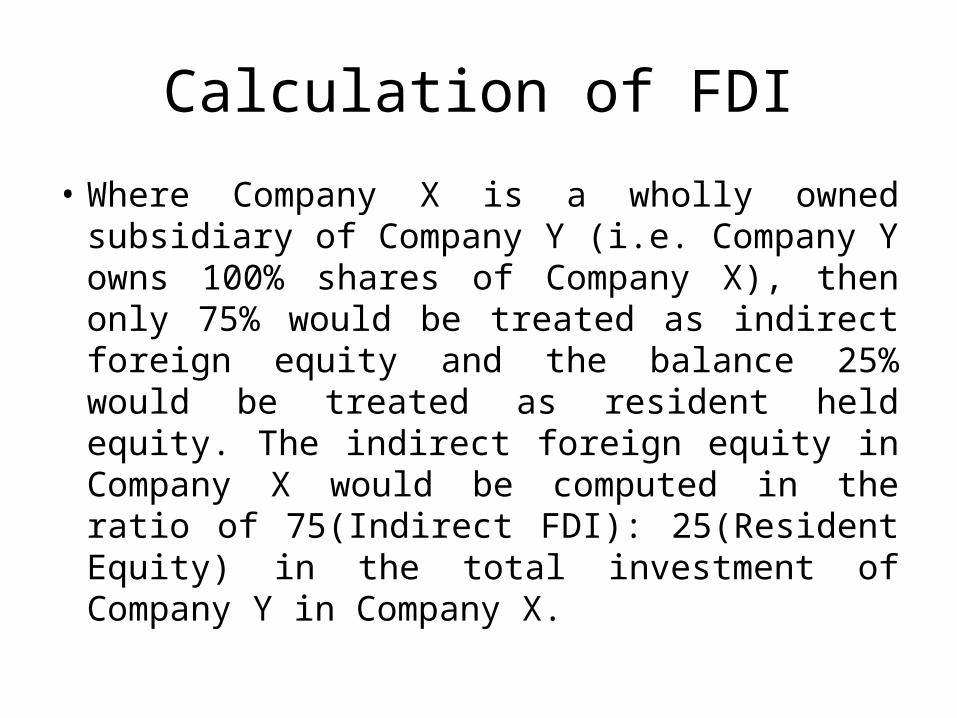

• Where Company X is a wholly owned subsidiary of Company Y (i.e. Company Y owns 100% shares of Company X), then only 75% would be treated as indirect foreign equity and the balance 25% would be treated as resident held equity. The indirect foreign equity in Company X would be computed in the ratio of 75(Indirect FDI): 25(Resident Equity) in the total investment of Company Y in Company X.

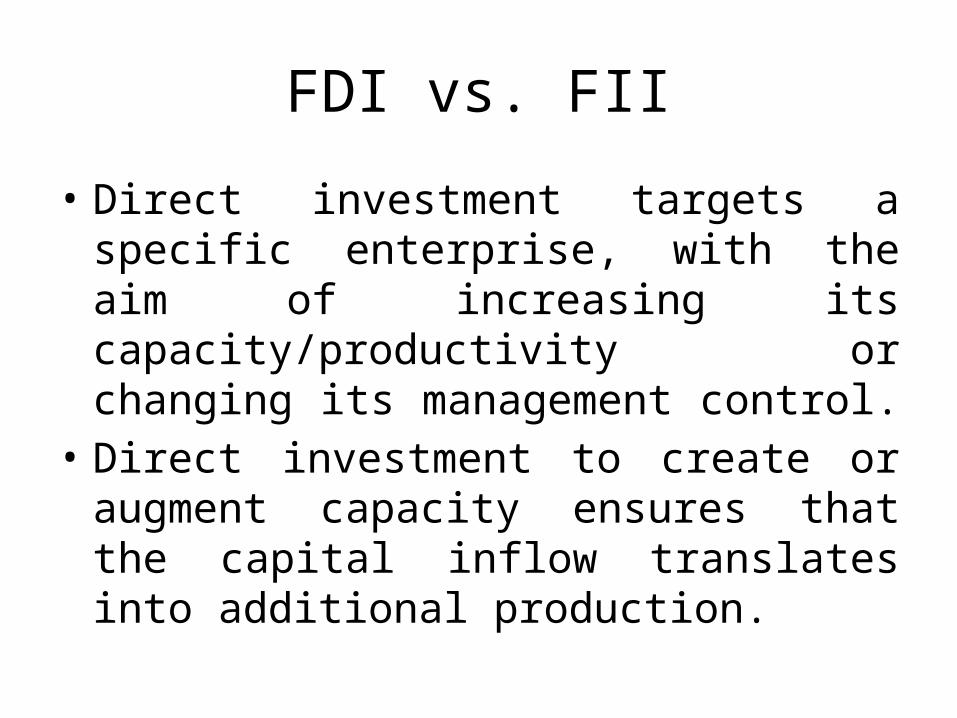

FDI vs. FII

• Direct investment targets a specific enterprise, with the aim of increasing its capacity/productivity or changing its management control.

• Direct investment to create or augment capacity ensures that the capital inflow translates into additional production.

FDI vs. FII

• FII investment that flows into the secondary market, the effect is to increase capital availability in general, rather than availability of capital to a particular enterprise.

• FDI tends to be much more stable than FII inflows. • FDI brings not just capital but also better

management and governance practices as well as technology transfer.

FDI vs. FII

• Know-how thus transferred along with FDI is often more crucial than the capital.

• No such benefit accrues in the case of FII inflows.

• The search by FIIs for credible investment options has tended to improve accounting and governance practices among listed Indian companies.

Who is an FII?

• An institution established or incorporated outside India as a pension fund, mutual fund, investment trust, insurance company, or reinsurance company.

• A foreign government agency or foreign central bank.

• AMC/ trustee of a broad based fund outside India.

Who is an FII?

• University Funds, Endowment Foundations, Charitable Trusts and Charitable Societies

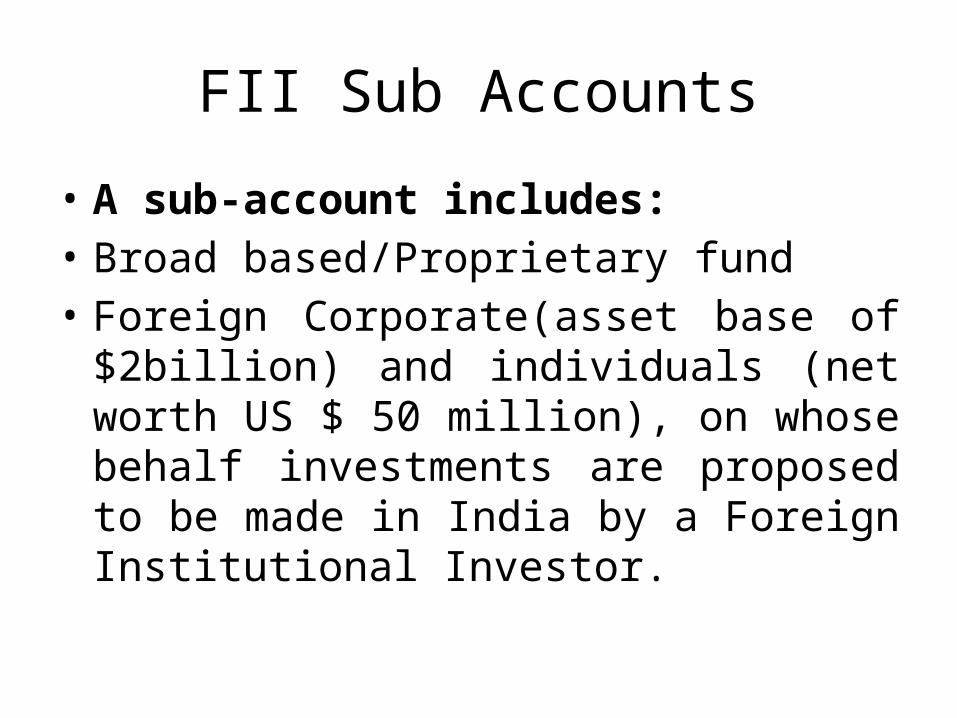

FII Sub Accounts

• A sub-account includes:• Broad based/Proprietary fund• Foreign Corporate(asset base of $2billion) and

individuals (net worth US $ 50 million), on whose behalf investments are proposed to be made in India by a Foreign Institutional Investor.

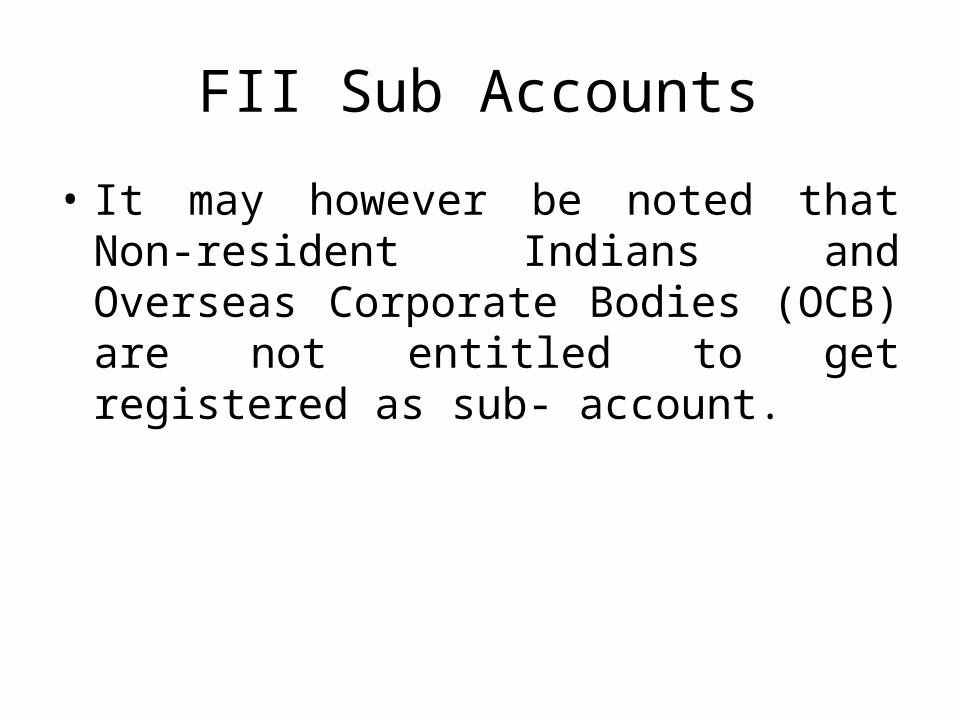

FII Sub Accounts

• It may however be noted that Non-resident Indians and Overseas Corporate Bodies (OCB) are not entitled to get registered as sub- account.

Investment allowed

• Securities in the primary and secondary markets including shares, debentures, and warrants of companies, unlisted, listed, or to be listed on a recognized stock exchange in India.

• Mutual funds schemes.• Dated government securities• Derivatives traded on a recognized stock

exchange

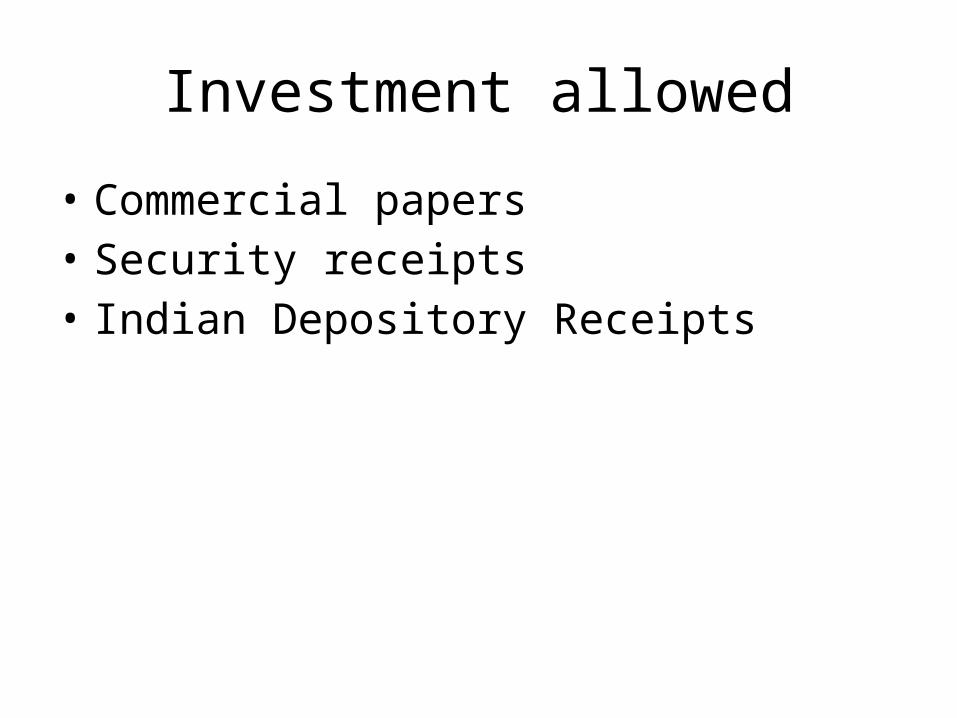

Investment allowed

• Commercial papers• Security receipts• Indian Depository Receipts

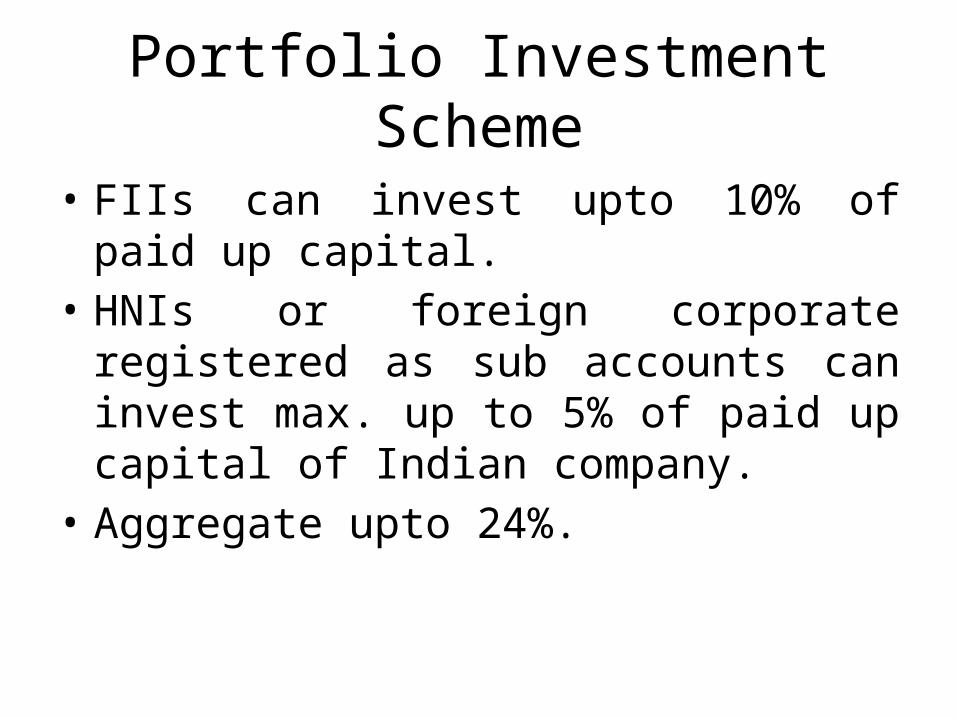

Portfolio Investment Scheme

• FIIs can invest upto 10% of paid up capital.• HNIs or foreign corporate registered as sub

accounts can invest max. up to 5% of paid up capital of Indian company.

• Aggregate upto 24%.

FII-Secondary Market

• FIIs are required to allocate their investment between equity and debt instruments in the ratio of 70:30. However, it is also possible for an FII to declare itself a 100% debt FII.

• FIIs can buy/sell securities on Stock Exchanges

FII-Secondary Market

• Trade on basis of taking and giving delivery of securities purchased or sold (except derivatives).

• Cannot buy more than 10% of issued capital.• No carry forward is allowed.• Keep margins prescribed by clearing house.• Allowed in interest rate futures and infra

bonds

FII-Secondary Market

• SEBI registered FIIs/sub-accounts of FIIs can now invest in primary issues of Non-convertible Debentures (NCDs)/ bonds to be listed only if listing of such bonds / NCDs is committed to be done within 15 days of such investment.

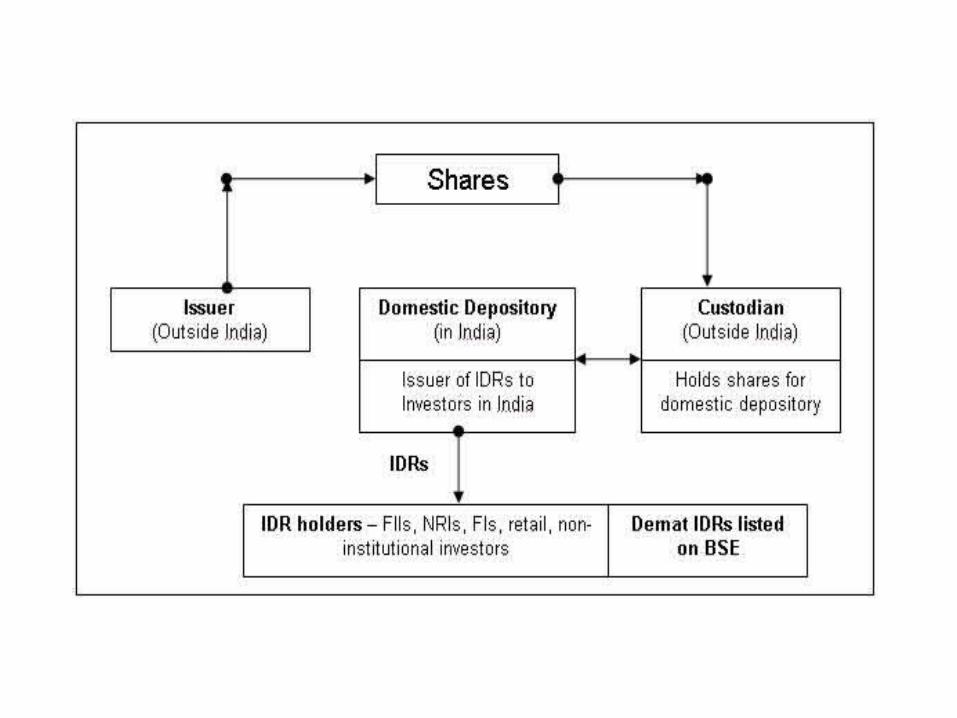

IDR- Indian Depository Receipts

• Eligilbility:• Pre issue paid up capital and free reserves of ‐ ‐

at least US$ 50 million • Minimum average market capitalization during

the last 3 years) in its parent country of at least US$ 100 million

• A continuous trading record or history on a stock exchange in its parent country for at least three immediately preceding years

IDR- Indian Depository Receipts

• A track record of distributable profits for at least three out of immediately preceding five years.

• Not prohibited to raise capital in home country, good compliance record.

Participants

• Custodian Bank• Domestic Depository• IDR holders.

ECB

External Commercial Borrowings (ECB) refer to commercial loans in the form of

• Bank loans, • Buyers’ credit,• Suppliers’ credit • Securitized instruments (e.g. floating rate notes

and fixed rate bonds, non-convertible, optionally convertible or partially convertible preference shares)

ECB

• Availed of from non-resident lenders with a minimum average maturity of 3 years.

• ECB can be accessed under two routes, viz., (i) Automatic Route and (ii) Approval Route.

Automatic route

Eligible Borrowers• Corporate • Infrastructure Finance Companies (IFCs)

except financial intermediaries, such as banks, financial institutions (FIs)

• Housing Finance Companies (HFCs) and Non-Banking Financial Companies (NBFCs)

Automatic route

• Units in SEZ.• NGOs

Lenders:• International capital market• Financial institutions • Government owned development financial

institutions• Export credit agencies

Automatic route

• Suppliers of equipments. • Foreign collaborators.• Foreign equity holders.

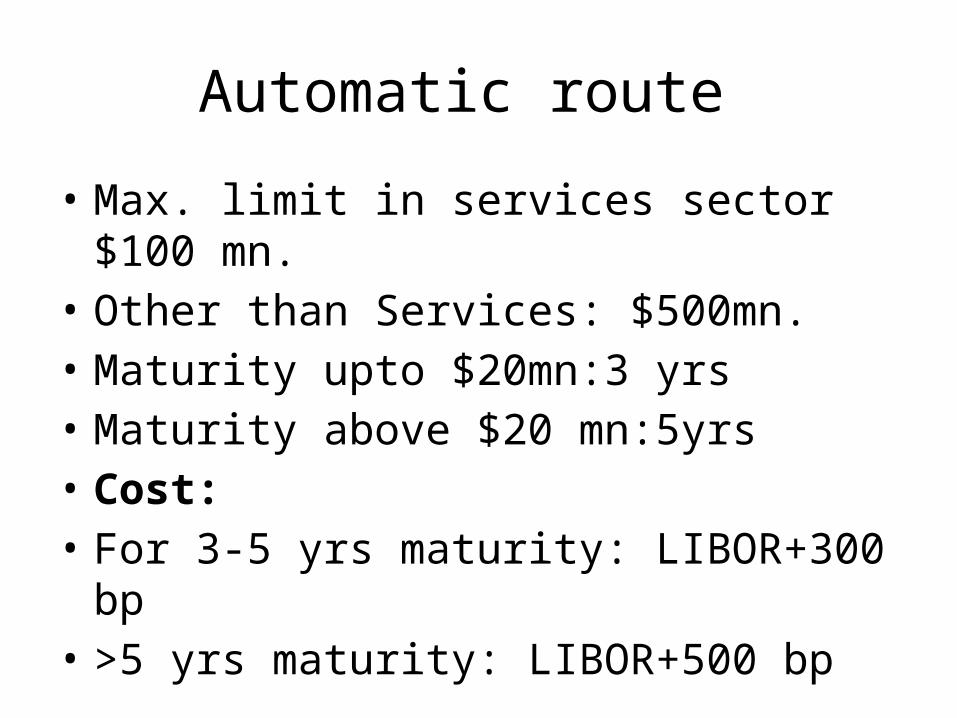

Automatic route

• Max. limit in services sector $100 mn.• Other than Services: $500mn.• Maturity upto $20mn:3 yrs• Maturity above $20 mn:5yrs• Cost:• For 3-5 yrs maturity: LIBOR+300 bp• >5 yrs maturity: LIBOR+500 bp

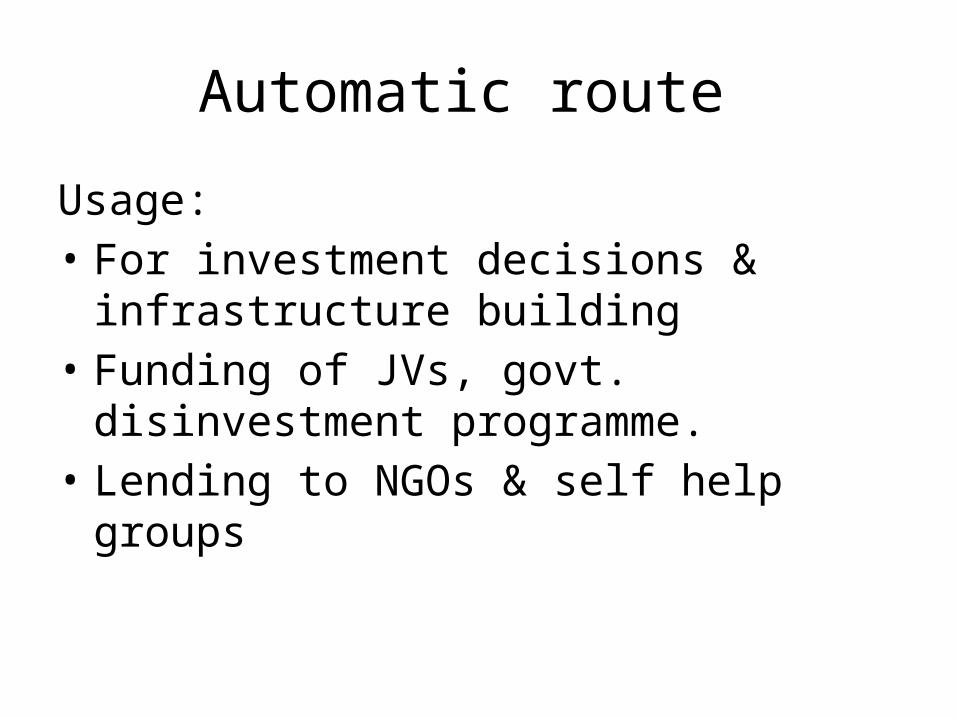

Automatic route

Usage:• For investment decisions & infrastructure

building• Funding of JVs, govt. disinvestment

programme.• Lending to NGOs & self help groups

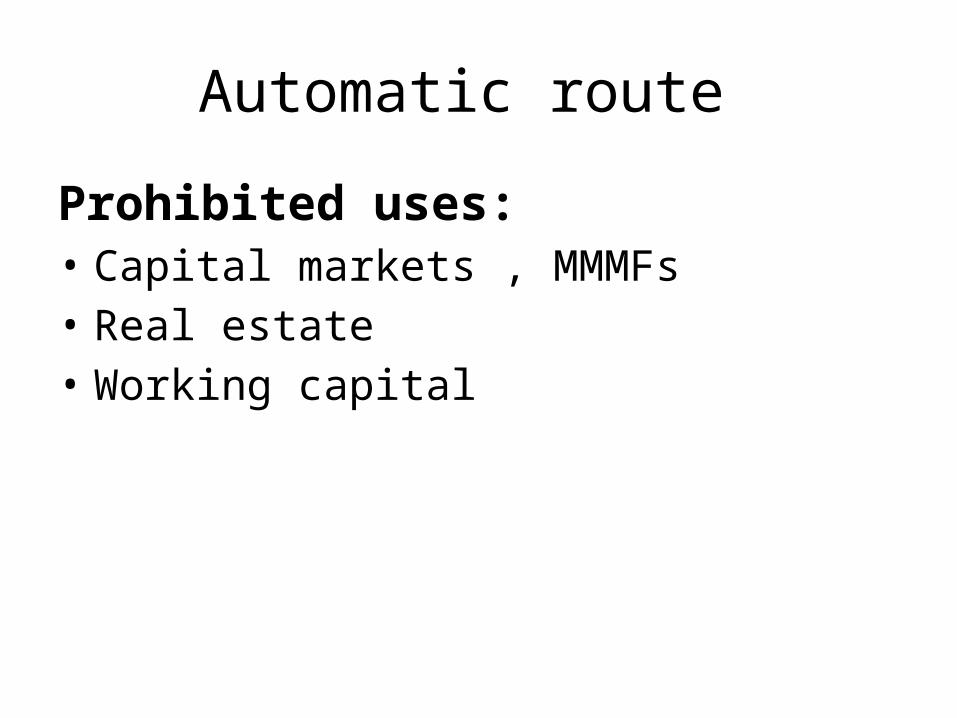

Automatic route

Prohibited uses:• Capital markets , MMMFs• Real estate • Working capital

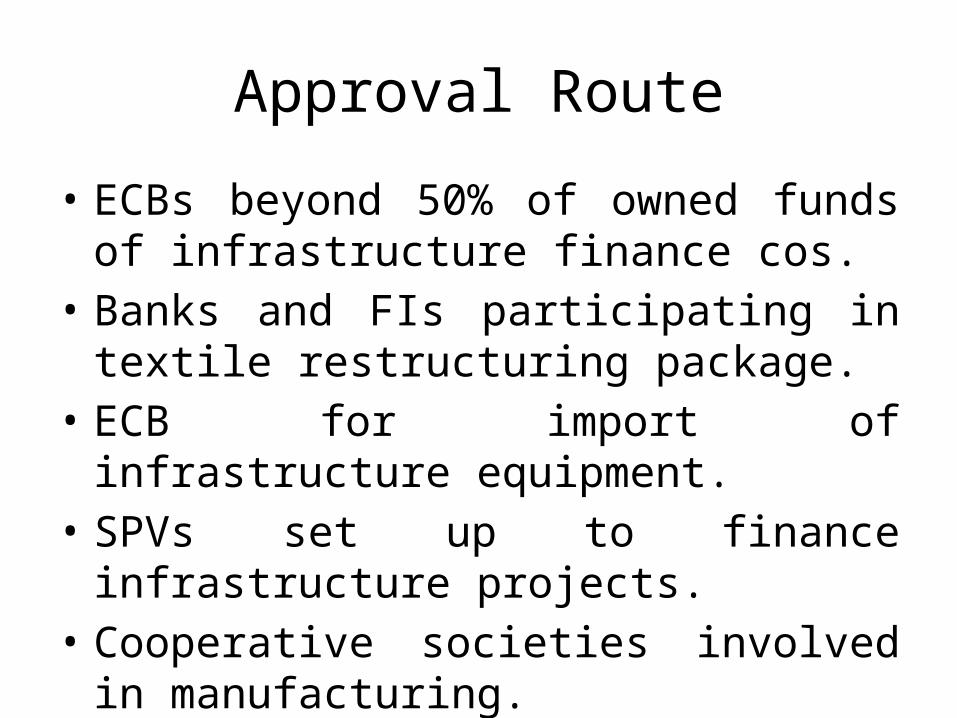

Approval Route

• ECBs beyond 50% of owned funds of infrastructure finance cos.

• Banks and FIs participating in textile restructuring package.

• ECB for import of infrastructure equipment.• SPVs set up to finance infrastructure projects.• Cooperative societies involved in

manufacturing.

Approval route

• Corporates violating ECB policy and are under investigation.

Amount: Additional ECB for ten yrs upto $250 mn above

500 mn level under automatic route.• Cost:• For 3-5 yrs maturity: LIBOR+300 bp• >5 yrs maturity: LIBOR+500 bp

Approval route

End Uses & Prohibited uses: same as earlier