Embed Size (px)

Citation preview

Mar-Apr 2013 33

We live in a world of relentless changes. In the current climate, a change that the banking

community must face and prepare for is tightened regulations. After the global economic downturn in 2008 resulted in the collapse of a venerable investment bank, Lehman Brothers Holdings Inc., there has been an upswing in regulatory actions taken by regulators in a number of jurisdictions.

Lehman Brothers fi led for bankruptcy in the United States on 15 September 2008. In Hong Kong, both the Securities and Futures Commission (SFC) and the

Hong Kong Monetary Authority (HKMA) received numerous complaints from investors concerning the conduct and selling practices of licensed corporations, banks and other fi nancial institutions and their staff.

To address the issues, the SFC and the HKMA issued consultation papers and reports in late 2008 and provided recommendations to strengthen the fi nancial industry’s regulations, product approval regime, disclosure requirements processes and dispute resolution mechanisms.

Regulationsfor Combating the“Mis-selling” of Investment Products

Financial REGULATIONS

34 Financial REGULATIONS

From time to time, the regulators have imposed new measures and requirements on authorized institutions and licensed corporations in relation to the conduct and selling practices on investment products, with a view to combating and controlling the risks of “mis-selling” within the financial industry.

Code of Conduct under the SFCThe Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission (hereafter called the “Code of Conduct”) has been revised over the years to introduce new measures and regulatory requirements. Some of the key obligations relating to the selling and distributing of investment products set out in the Code of Conduct in June 2012 are as follows:-

• Investor characterizationUnder paragraph 5.1A of the Code of Conduct, except where a client is a professional investor, intermediaries should – as part of the know-your-client procedures – assess the client’s knowledge of derivatives and characterize the client based on their knowledge of derivatives. It is important for intermediaries to explain the relevant risks associated with investment products to a client who is without knowledge of derivatives. In addition, records of the warning and other communications with the client should be properly kept.

• Pre-sale disclosure of monetary benefitsNew disclosure requirements will ensure intermediaries must deliver sales-related information, including monetary and non-monetary benefits received from the sale of an investment product, to their clients prior to or at the point of sale.

• Professional investorsIf an investor who meets the definition under Schedule 1, Part 1 of the Securities and Futures Ordinance (Cap 571) and is assessed to be a professional investor under the Securities and Futures (Professional Investor) Rules and the Code of Conduct, certain Code of Conduct requirements can be waived, including the need to ensure the suitability of a recommendation or solicitation. However, before intermediaries consider whether a

particular client is a professional investor, they have to assess and be reasonably satisfied that such a person is knowledgeable and has sufficient expertise in relevant products and markets, having regard to the following factors:

(a) the types of products traded; (b) frequency and size of trades (to be

regarded as a professional investor, that person would be expected to have traded not less than 40 transactions per annum);

(c) dealing experience (a professional investor would be expected to have been active in the relevant market for at least two years);

(d) knowledge and expertise in the relevant products; and

(e) awareness of the risks involved in trading in the relevant products and/or markets.

The assessment has to be in writing and documented.

Selling Practices Requirements for IntermediariesAs one of the major developments in controlling “mis-selling” practices, the SFC requires intermediaries making investment recommendations or solicitations be subjected to suitability obligations. Intermediaries should take into consideration information about their clients through the exercise of due diligence to ensure the recommendation or solution for that client is reasonable in all circumstances. Some of the key suitability obligations include:

• Knowing your clientsIntermediaries need to know and understand their clients, including their financial situation, investment experience and investment objectives. The client’s information needs to be fully documented and updated on an ongoing basis, where appropriate.

Mar-Apr 2013 35

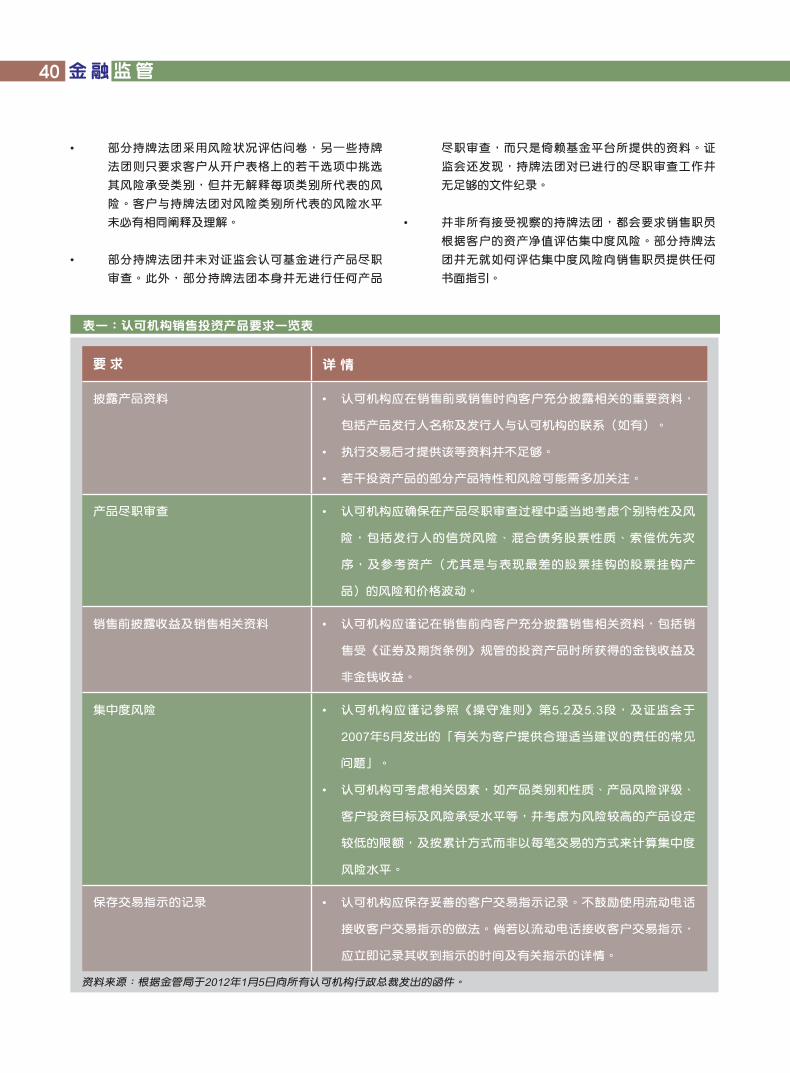

Table One: Highlights of Requirements for Authorized Institutions (AIs) on Selling

Investment Products

Requirements Particulars

Disclosure of product information • AIs should make adequate disclosure of relevant material

information, including the name of the product issuer and the

issuer’s affiliation with the AIs (if any), to customers prior to or

at the point of sales.

• It is not sufficient to provide such information after a transaction

has been executed.

• Some special product features and risks of certain investment

products may warrant particular attention.

Product due diligence • AIs should ensure that, among other factors, the special

features and risks including the issuer’s credit risk, the hybrid

debt-equity nature, priority of claim, and the risks and price

volatility of the reference asset (especially for equity-linked

product linked to the worst performing stock) are properly taken

into account in their product due diligence process.

Pre-sale disclosure of benefits and sales related information

• AIs are reminded to give adequate pre-sale disclosure to

customers of sales related information, including monetary and

non-monetary benefits received in selling investment products

regulated under the Securities and Futures Ordinance.

Concentration risks • AIs are reminded to make reference to paragraphs 5.2 and 5.3

of the Code of Conduct and the frequently asked questions

(FAQ) on Suitability Obligations issued by the SFC in May

2007.

• AIs may take into account relevant factors like product type

and nature, product risk ratings, customer’s investment

objectives and risk tolerance level, and so on, and consider

setting a lower threshold for higher-risk products, and using a

cumulative basis instead of per transaction basis in calculating

the concentration risk level.

Maintenance of order records • AIs are reminded to maintain proper records of client orders.

Use of mobile phones for receiving client order instructions

is discouraged. Where client order instructions are accepted

through mobile phones, the ti me of receipt and the order

details should be recorded immediately.

Source: Based on a Letter to The Chief Executives of all Authorized Institutions, Issued byThe HKMA on 5 January 2012.

36 Financial REGULATIONS

• Product due diligence Intermediaries need to understand the investment products they recommend to clients. Product due diligence should be conducted on a continuous basis at appropriate intervals having regard to the nature, features and risks of the investment products being offered.

In addition, intermediaries should make their own enquiries and obtain full explanations from product issuers about the risks inherent in the investment products. They should document verification work and enquiries they have made about the investment products, the criteria for selecting the products and in what aspects they are considered suitable for different risk categories of investors, and the approval they obtain from senior management for promoting the products.

• Risk profilingIntermediaries must match the risk return profile of each investment product sold to a client to the personal circumstances of that client. They are required to exercise professional judgment to assess whether the characteristics and risk exposures of an investment product are suitable for and in the best interests of the client.

• Providing all relevant material information to clients to help clients make informed decisionsIntermediaries are required to help their clients make decisions by providing them with all the relevant information about the recommended investment products (such as prospectuses, offering circulars, product key facts statements, and so on) and proper explanations as to why they are suitable for the clients. It is not enough for the intermediaries to provide these documents and ask the clients to read them themselves, or merely read the documents to the clients without explanations.

Intermediates should always present balanced views, including any disadvantages and downside risks of the recommended investment products to their clients, and give them sufficient time to consider and evaluate the information and recommendations provided.

• Employing competent staff and providing appropriate trainingIntermediates should ensure products are sold by staff members who have a sufficient understanding of both the products and their obligations to clients. It is also important to ensure that all staff members are properly trained in carrying out their roles.

• Documenting and retaining the rationale for each recommendationIntermediaries should document and provide a copy to each client of the rationale underlying their investment recommendations made to the clients, including any queries raised by their clients and the responses given to them. Additionally, intermediaries should keep sufficient documentation on all client transactions and the related advice provided to clients.

Did the Market Players Follow the Regulatory Requirements?The SFC conducted a thematic inspection of selling practices for 10 licensed corporations (LCs) and summarized its findings in a report in October 2012 (hereafter called the “Thematic Report”). The inspected LCs were mainly independent financial advisers, wealth management affiliates of global financial institutions and stock brokers.

The Thematic Report set out deficiencies and weaknesses in the LCs’ conduct and selling practices relating to the sale of investment products. Some of the key findings are:

• Inadequate resources and procedures for the LCs to supervise their staff diligently. In addition, there is inadequate training for staff and insufficient self-examination of controls and procedures to ensure the LCs comply with all applicable legal and regulatory requirements.

• Some LCs adopted risk-profiling questionnaires while others asked clients to simply pick a risk tolerance category from a number of options in the account opening form but without explanations. There was no certainty that the client and the LC had the same interpretation and understanding of the risk categories being represented.

Mar-Apr 2013 37

prevent mis-selling in the past few years, and the focus is more on investor protection.

He said the prevention of mis-selling is a priority for regulators around the world. The SFC has been actively working with the International Organization of Securities Commissions (IOSCO) on this initiative. The focus will be first to look into the creators of the financial products aimed at individual investors; and secondly, to look into the distribution channels to determine how to control the behavior of sales people who coerce customers to buy unsuitable products. Over the next 12 months, it is expected that more proposals will be issued on the prevention of misrepresentation of financial products to retail investors.

On 14 December 2012, the Asia Financial Consumer Protection Roundtable, jointly organised by the SFC, the HKMA and the Organisation for Economic Co-operation and Development (OECD), was held in Hong Kong as the first high-level international conference on financial consumer protection. Professor K.C. Chan, the Secretary for Financial Services and the Treasury, highlighted during the event that it is a policy objective of the Hong Kong Government to strike a balance between generating market development and enhancing financial stability and protection.

Closing the GapBoth the SFC and the HKMA have achieved much in terms of putting into place preventive measures and new requirements to control “mis-selling” practices in the financial industry in Hong Kong. The SFC has also pointed out in its Thematic Report last year that it will take appropriate regulatory action against LCs found to have breached the Code of Conduct and other applicable requirements.

To close the gap between regulatory requirements and sales practices, senior managers of intermediaries should take immediate steps to review their existing systems and practices in order to identify areas that may be unfair or not in the interests of their clients. In this way, they will ensure they are complying with the new regulatory requirements.

ANNIE CHANManaging DirectorForensic and Investigation ServicesMazars Hong Kong

Some LCs did not conduct product due diligence on SFC-authorized funds. In addition, some LCs did not conduct any product due diligence themselves but merely relied on the information available on a fund platform. The SFC also found that there was inadequate documentation on the due diligence work performed.

• Not all the inspected LCs require sales staff to assess concentration risk by taking into account their clients’ net worth. Some LCs do not provide written guidelines to sales staff on how a concentration risk assessment should be performed.

• Some LCs only kept little documentation, which was not sufficient to explain how the recommendations were considered suitable having regard to the clients’ personal circumstances. Even if the sales staff kept their own notes regarding the client’s circumstances and/or subsequent changes, copies of the notes were not kept in the LCs’ records.

• Some LCs relied solely on a client’s declaration of their derivative knowledge instead of carrying out a proper assessment by making appropriate enquiries or gathering relevant information from the clients.

However, the SFC’s Thematic Report also provided some examples of good practice concerning staff training, the establishment of elaborate compliance monitoring procedures, and additional controls set up for elderly customers that have been adopted by certain LCs.

The HKMA also set out similar guidelines and requirements for authorized institutions that are selling investment products. Please refer to Table One below for more details.

Helping Investors Make Informed DecisionsThe Investor Education Center, a subsidiary of the SFC was established on 20 November 2012 to help investors become better equipped to make informed financial decisions and manage their money wisely.

Ashley Alder, the chief executive of the SFC, said in the third annual Pan-Asian Regulatory Summit held on 27 November 2012 that Hong Kong has achieved much to

38

Mar-Apr 2013 39

40

Mar-Apr 2013 41