Embed Size (px)

Citation preview

Investment Symposium March 2010

F3– Replicating Portfolios in the Insurance Industry

Curt Burmeister Mike Dorsel

Patricia Matson

Moderator

Hueyfang Chen

1

Replicating Portfolios in the Insurance Industry

AgendaBasics of Replicating Portfoliosby Tricia Matson, FSA, MAAA

Replicating Portfolios: Advanced Approachesby Mike Dorsel, CFA, ASA

Using Trade Restrictions to Improve Your Replicating Portfoliosby Curt Burmeister

2

Basics ofR li ti P tf liReplicating Portfolios

Tricia Matson, Principal Deloitte Consulting LLP

March 22, 2010

Overview

• Basics of replicating portfolios

• Uses of replios

• Industry statusy

• Approaches

• Considerations

• Candidate Assets

• Testing of Fit

• Summary

©2010. Private and confidential.4

3

Basics of Replicating Portfolios

• Portfolio of assets which can be used to replicate the behaviour of life insurance liabilities under different economic scenarios

• Once a replicating portfolio of assets has been found, then under a wide range of economic conditions, the value of the replicating portfolio equals the value of the liabilities

• The RP can then be used as to estimate the MVL when market conditions change without time consuming model re-runs

• This enables companies to quickly recalculate liabilities, balance sheets, capital requirements and embedded values:– As economic conditions change– Under “what ifs” and specific scenarios– To project market consistent balance sheets

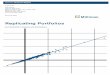

Value of replicating portfolio againstprojected liability value

©2010. Private and confidential.

o p oject a et co s ste t ba a ce s eets

Target ValueR

eplic

atin

g P

ortfo

lio

Uses of Replios

Likely initial uses: Possible future benefits:

Accelerated liability valuation can be used to make complex actuarial calculations more accessible, allowing them to be run more frequently and allowing management to monitor capital positions more closely

• Regular risk reporting/economic capital analysis

• Calculation of market consistent balance sheet

• Benchmark liability replicating portfolio to compare against actual asset portfolio (egmeasurement of basis risk, etc)

• Projecting realistic balance sheets (for

• Business planning

• Testing impact of management actions

• Articulation of risk appetite

• Solvency II

• IFRS

• Investment performance measurement

©2010. Private and confidential.6

• Projecting realistic balance sheets (for sensitivity testing, risk analysis, cost of capital analysis)

• Investment performance measurement

• Hedging strategy analysis

4

Industry Status: Drivers for Change

RegulatoryPressure

Solvency II

Drivers for ChangeOpportunities• Competitive advantage• Standardized reporting • More efficient use of

resources

Rating

ERMTurbulentMarkets

Best Practices

Risky andComplex

IFRS

Real-time reportingof risk exposure and capital position

• Improved risk management and controls

• Better capital management• Improved view of economics

Challenges• Changing the cultural mindset• Ensuring global consistency • Updating policies & systems• Training personnel

©2010. Private and confidential.

Rating Agencies &ERM

Peer Pressure

pExposures

a g pe so e• Improving internal risk

management• Understanding judgments• Avoiding over-reliance on

models• Upfront costs to adopt

7

Industry Status: Global Landscape

• Significant use of replios by global insurers:– Led by large multinationals with UK and EU headquarters– Gradually expanding to other countries as their subsidiaries pave the way– Implementation underway at several domestic US insurers– Implementation underway at several domestic US insurers

• For these insurers the drivers tend to be:– The need for timely market-consistent economic capital calculations– Allocating capital appropriately across the group– Solvency II and the use test– Quick and simple representation of the liabilities for use in financial analysis, risk limit

setting and risk reporting– Identification and measurement of ALM risks

©2010. Private and confidential.8

5

Approaches: Three Methods for Replicating Portfolios

Balance Sheet Method Aggregate Cashflow Method Annual Cashflow Method

• Find a portfolio of assets whose total future discounted (or rolled-up) cash flows match the total discounted (or rolled-up) liability cash flows closely in a

• Find a portfolio of assets whose future cash flows by time match the liability cash flows closely in a range of scenarios for all years

• Find a portfolio of assets whose current market value matches the fair value of liabilities under a range of sensitivities

y yrange of scenarios

• One set of sufficiently varied economic scenarios (say 1000 projections)

• Can be used to update market consistent balance sheets

• Cannot project RBS

• One set of sufficiently varied economic scenarios (say 1000 projections)

• Can be used to update and project market consistent balance sheets

• Care need with some policyholder behaviour in choice of candidate assets

• Market consistent balance sheets for range of sensitivities (say 50 x 1000 projections)

• Can be used to update market consistent balance sheets

• Does not use individual cash flow information

• Many projections required

• Doesn’t capture all behaviour unless very complex sensitivities

©2010. Private and confidential.9

Base Equities up 10%

Equities down 10%

Equity volatility up 5%

Equity vol down

5%

Interest rates up

1%

… Interest rate vol down 1%

Asset shares 1,000 1,050 950 1,000 1,000 970 … 1,000Cost of guarantees 50 45 57 53 45 47 … 48Guarantee charge -25 -27 -24 -25 -25 -23 … -25Cost of smoothing 5 5 10 7 4 4 … 5Other liabilities 8 8 8 8 8 8 … 8Total liability 1,038 1,081 1,001 1,043 1,032 1,006 … 1,036

S i m u l a t i o n R o l l - u p c a s h f l o w

1 1 1 52 1 1 03 1 4 54 1 2 05 1 3 3

… …1 , 0 0 0 1 2 1

Simulation 2006 2007 2008 2009 … 2026

1 6 5 10 13 … 32 6 7 11 12 … 23 7 5 6 7 … 54 5 4 15 5 … 15 4 2 3 7 … 2… … … … … … …

1,000 6 2 8 9 … 4

Data Inputs:

unless very complex sensitivities performed

Approaches: Sample Replicating Portfolio Process

Insurance Contract

Insurance Contract

Capital Market Equivalent

Capital Market Equivalent

Guaranteed Liabilities

Guaranteed Liabilities

Zero Coupon Cashflows

Zero Coupon Cashflows

Maturity guarantees

Maturity guarantees Put OptionPut Option

O ti t O ti t I t t R t I t t R t

4. Choose suitable candidate assets

Max95%75%50%25%5%Min

5. Output – updated liabilities, sensitivities or projections

3. Generate cash flows under defined scenarios

Optimisation Engine

Option to annuitiseOption to annuitise

Interest Rate Swaption

Interest Rate Swaption

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Dec

-14

Jun-

15

Dec

-15

Jun-

16

Dec

-16

Jun-

17

Dec

-17

Jun-

18

Dec

-18

Jun-

19

Dec

-19

Jun-

20

Dec

-20

Jun-

21

Dec

-21

Jun-

22

Dec

-22

Jun-

23

Dec

-23

Jun-

24

Dec

-24

Jun-

25

Dec

-25

Jun-

26

Dec

-26

Replicating Portfolio

©2010. Private and confidential.10

Time points

1d 10d

1

234

2000

x xx xx x

x x

x x

1

23

2000

1000

Time point

Price or %

3M USD LIBOR

1

23

2000

1000

30Y USD RATE

1

23

2000

1000

RISK FACTOR N

1d 10d

Risk factor scenariosPrice

Inflation

Salary Inflation

UK Equities

Overseas Equities

UK Bonds

Cash

Index Linked

Target Value

Rep

licat

ing P

ort

folio

Value of replicating portfolio againstprojected liability value

1. Choose economic scenarios

2. Actuarial cash flow projection system

6. Validate through detailed testing program

Liability Model

6

Considerations: Implementation ApproachDeloitte’s recommended implementation approach is split into a Discovery Phase and an Implementation Phase. We recommend that a pilot exercise be used to test out the methodology and technology.

Implementation Considerations:

D i i

Implementation Methodology:

Project Management and Benefits Realisation

Change Management and Transition into BAU

Discovery Phase Implementation Phase

PIL

OT

Require-ments

Definition

ProgramDesign Planning

Design Build

Deploy Technology

InfrastructureAlgorithmics Configuration

Technology Infrastructure

Algorithmics Components

Rollout

Design issues:• Governing objective• Choice of software• Dashboard – required outputs• Reporting granularity required by product• Frequency of recalibration• Required reporting frequency• Approach by product type• Allowance for non-market risk• Acceptance testing process• Allowance for new business

©2010. Private and confidential.11

Project Management and Benefits Realisation

Change Management and Transition into BAU

Discovery Phase Implementation Phase

BU

1

Require-ments

Definition

ProgramDesign Planning

Design Build

Deploy Technology

InfrastructureAlgorithmics Configuration

Technology Infrastructure

Algorithmics Components

BU

2

BU

3

Wider considerations• Design of implementation program• Information to be provided by cash flow

models• Training and communication are critical• Useful management information needed for

business buy in

As used in this presentation, “Deloitte” means Deloitte Consulting LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Considerations: Top 5 implementation challenges

Implementation challenges:

1. Buy-in from the business

• Involve in the development project• Visible senior management support required to drive the process• Link to management of the business must be demonstrated – not just an academic exercise• Implementation should produce benefits as quickly as possible• A process that produces “rough” numbers that can be refined later helps build momentum

2. Design of acceptance testing

3. Knowledge transfer and training of implementation teams

©2010. Private and confidential.12

4. Speed and efficiency of end-to-end process which is key to embedding

5. Data transfer processes• The link between live market data and both the replicating portfolio and the actual assets held is important - this

must be streamlined and accurate to allow quick revaluation• We have seen three methods used - actual assets, roll forward using indices, roll forward allowing for cashflows.

The choice varies based on systems and timescales involved and can be refined a a later date

7

Considerations: Top 5 technical challenges

Technical issues:

1. Choosing and modelling appropriate candidate assets2. Policyholder behaviour and dynamic management actions3. Non-market risk4. Selecting scenarios that bring out the full nature of the liabilities5. Using a suitable optimisation routine

• Allowance for non-market risk is important when using for economic capital analysis

©2010. Private and confidential.13

• Particularly important where there is non-linearity between market and non-market risk factors

Candidate Assets

• Suitable candidate assets must be defined. The types of assets allowed would depend on the purpose of the replicating portfolio:– If the intention is to produce a replicating portfolio that can be invested in, the assets must be

tradeable.– If the replicating portfolio is to be used to provide a benchmark for asset performance, synthetic

assets such as zero coupon bonds can be used. These assets must be easily priceable given actual financial market conditions, but it is not necessary to be able to invest in them.

– More complex synthetic assets can be used, such as an asset representing the asset share mix of the liabilities, if the only purpose is to produce a portfolio that mirrors the behaviour of the liabilities.

• Care should be taken with management actions - suitable assets that capture the same effects as the actions should be used.

©2010. Private and confidential.14

• The optimisation method used affects the constraints that can be put on the replicating portfolio. Such constraints could include:– Requiring all asset weights to be positive– Trading constraints - useful if the intention is to invest in the portfolio created– Requiring certain results to hold - such as the overall value of the portfolio at the start being equal to

the value of the liabilities, or the intrinsic value of guarantees to be valued correctly

8

Features and Behaviors

Fixed cash flows

Candidate Assets

Zero coupon bonds

Candidate Assets

Sample liability features and behaviors and candidate assets

BasicCash Flows

Fixed cash flowsInvestment index-linked cash flowsCredited rate based on bond yieldsLongevity related

EmbeddedGuarantees

Zero coupon bondsEquity / property total return indexBond total return indexLife table amortizing bonds, mortality swaps

Equity put options Equity call options Bond put option, American style or Bermudian swaptionVanilla swaptions, quanto swaptionsForward start optionsCliquet / lookback options

Guaranteed accumulation valuesParticipation in investment profit upside (ex EIA)Guaranteed minimum credited ratesGuaranteed annuity rates, GMIBGuaranteed reinvestment terms on future premiumsRatchets / non-negative reversionary bonus

©2010. Private and confidential.

DynamicPolicyholderbehaviour

Option take-up rates depend on moneynessLapse rates increase in high marketsLapse rates increase in low marketsEquity fund lapse rate depends on interest ratesPremium persistency dependent on option value

Power law optionsUp and out optionsDown and out optionsOutside barrier optionsCompound options (options on options)

UniversalLifewith

SecondaryGuarantee

Product Features

Flexibility of premiums and death benefitsPositive performance, in particular investment, returned to policyholderMinimum credited ratesMinimum guaranteed death benefit if performance is poor

Policyholder Behavior

Lapse/disintermediationReduced lapse if in the money (ITM) guarantee (may increase with age)Premium persistencyLoans/withdrawals

Management Actions

Increase cost of insurance (COI) Reduce credited ratesIncrease expense loadsAll subject to caps/floors

Market Risk Factors

Interest ratesUp increases lapse riskDown may hit guaranteesHigher volatility raises guarantee costs

Credit riskUp may hit guarantees

Candidate Assets: Particular Replication Challenges by Product

VariableUniversal

LifeWith

Secondary Guarantee

VariableAnnuity

Fixed

Flexibility of premiums and death benefitsInvestment performance in SA fully passed to policyholderMinimum guarantees if equity performance is poorRetains some UL risks in GA

Reduced lapse if ITM guarantee (may increase with age)Premium persistencyLoans/withdrawalsFund allocation changes

Equity dropHits guaranteesReduces charge income

• Interest rates• Equity volatility increase raises

guarantee costs• Credit risk on GA

Typically single depositInvestment performance of SA fully passed to policyholderMinimum guarantees (AB/IB/DB/WB) if equity performance is poorSome $ in GA, usually small

Possibly ability to increase GMLB rider chargesReduce credited rates on GA

Single or multi depositMinimum guaranteed interest rate Reduce credited rates subject

Increase COIs Reduce credited rates on GAIncrease expense loadsAll subject to caps/floors

Reduced lapse if ITM guarantee (may increase with age) and vice versaAnnuitization ratePartial withdrawal rateReset rateFund allocation changes

Equity dropHit guaranteesReduces M&E income

• Interest rates• Equity volatility increase raises

guarantee costs• Credit risk on GA

Interest rates/creditSimilar to UL

©2010. Private and confidential.

Fixed Annuity /

Equity IndexedAnnuity

Minimum guaranteed interest rate (lower for EIA)Annuitization option (not rich)EIA includes single or multiple index optionsLegacy product a hybrid

Reduce credited rates subject to floorChange option budgeting for EIAs subject to floor

Lapse/disintermediationReduced lapse if ITM guarantee and vice versaAnnuitization

Similar to ULEquity levels for EIA

Up increases payoutsDown increases lapses

• Equity volatility increases cost of options

9

Testing of Fit

• Experience is developing as more work is done in this area– “Art” as well as science– Some subjectivity in the development and acceptance of replicating portfolios

• Calculate R2 for aggregate cash flows or cash flows by term across simulations

• For cash flow method, calculate R2 for projected future balance sheets (subject to runtime constraints)

• Check the average and the standard deviations of the errors• Check whether errors are normally distributed – if not, this

might imply need for options• Graphing results can be a powerful way of providing comfort:

–Scatter graphs of cashflows or future balance sheets by simulation are effective–Graphing the errors in the replication can also be informative

Statistics

•Compare market consistent value of liabilities against market value of replicating portfolio•Check modelling of intrinsic value of guarantees only – turn volatility off•Where projecting the balance sheet forwards, these tests should be done at future time periods as well as at the projection start date

–This would require a simulation fan approach to the testing•Check how well the replicating portfolio works for out of sample stress tests / scenarios

–This is an effective way of testing the robustness of the portfolio fit

Testing approaches

©2010. Private and confidential.17

• How close should you get? It depends:– For a life business without policyholder behaviour and with only simple management actions, we have

seen as much as R2 = 99.5% obtained– Restrictions to assets that you can invest in can affect how close a match you can get

portfolio fit

Summary

• Insurance companies are increasingly using replicating portfolio techniques in the management of their business

• The key benefit opportunities are:

– Making complex actuarial investigations more practical

– Speeding up liability valuation to provide real time management information

• We expect to see much activity in this area in the next few years

©2010. Private and confidential.18

We expect to see much activity in this area in the next few years

10

This presentation contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this presentation, rendering business, financial, investment, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this presentation.

Copyright © 2010 Deloitte Development LLC, All rights reserved.

©2010. Private and confidential.19

Unlocking the global potential

R li ti P tf li Ad d A h ?

Local knowledge. Global power. 20INTERNAL

Replicating Portfolios: Advanced Approaches?

Algo User GroupMarch 2010

11

Replicating Portfolios: High-level Overview

Local knowledge. Global power. 21INTERNAL

What is a replicating portfolio?

• Replicating portfolio = a portfolio of hypothetical market securities whose economic sensitivities and/or cash flowsmatch well those of a portfolio of actual assets or liabilities

• Replicating portfolios provide:– a proxy for (re-)valuing the actual asset or liability portfolio under

different market conditions– the ability to recalculate asset/liability values, balance sheets,

capital requirements and attribution analyses very quickly and efficiently

– the ability to make complex actuarial calculations more accessible

Local knowledge. Global power. 22INTERNAL

y p(through accelerated liability valuation)

– a way to avoid the need to go back to the underlying liability projection models for determining many market risk sensitivities

– a means to complete many key calculations prior to the reporting period

12

Replication: initial setup process

1. Choose Economic Scenarios

2. Actuarial Projection

System

4. Choose

Optimisation Engine 3. Liability Cash Flows Under

Defined Scenarios

Replicating Portfolio

5. Perform Validation

Local knowledge. Global power. 23INTERNAL

4. Choose Suitable

Candidate Assets

6. Risk Dashboard, Economic Capital,

MVIS attribution, etc.

Re-valuing a liability portfolio using the replicating portfolio

• New market information can be processed quickly by re-valuing the replicating portfolio

• No need to go back to the

Valuation of the replicating portfolio is quick as all replicating assets can typically be valued by closed form solution using market data directly • No need to go back to the

actuarial projection system– No new scenarios– No new liability cash flows

• Cycle for re-valuation is now measured in minutes rather than weeks!

New Market Data

Replicating Portfolio

New Value of Replicating

Portfolio

Available in minutes

Local knowledge. Global power. 24INTERNAL

Available in minutes

13

Comparison of market consistent valuation approaches

Current Process• Risk-neutral scenarios

C h fl j d f i l

Replicating Portfolio Process• Smaller set of risk-neutral scenarios plus

a wide range of other scenarios• Cash flows projected from actuarial models

• Present value obtained by discounting cash flows

• Cycle time takes many weeks or months

• Re-valuation for market changes also takes weeks!

a wide range of other scenarios• Cash flows projected from actuarial

models

• Optimization of replicating portfolio weights based on fitting cash flows and/or market sensitivities across scenarios

• Re-valuation for a wide range of small and/or large market changes obtained in minutes!

Local knowledge. Global power. 25INTERNAL

Uses of Replicating Portfolios

Local knowledge. Global power. 26INTERNAL

14

Applications of replicating portfolios

Becoming more widely used at insurance companies around the world ☺

Current uses: Economic Framework & MCEV

Risk• Risk dashboards showing realistic economic sensitivities, stress tests, solvency

positions, VaR and/or CTE levelsRisk management

purposes • Real-time ALM analytics and risk position reporting

• Ad hoc and “what-if” analyses

• Liability benchmarks for investment management

Calculation of Economic

Capital

• Results for timely capital reporting and capital management

• Proxy for MV of liabilities and assets

• Simulate joint distributions quickly to calculate capital

Attribution

• Used to develop expectation of liability asset or movement as a result of changes in market conditions

• Isolate changes in the asset or liabilities in a given reporting period

Local knowledge. Global power. 27INTERNAL

Attribution analysis of assets and liabilities

• A tool to identify changes for equity levels, interest rates, volatilities, etc. and aid in determining the changes as they relate to other items

• More efficient MVBS and MVIS reporting

• Splitting risk and return into non-hedgeable, asset management and ALM/Treasury components

Future uses include: Solvency II & IFRS

Applying different calculation/estimation techniques

Liabilities & building blocks of MVL

Estimation approach

Relative size and effort to calculate

Assets

Other Liabs

Frictional Cost

Market value of taxes

Market Value Margins

Own Credit or Liquidity

Alternative estimation techniques in addition to RPs

Non‐HLV

HLV

~90% of M

VL (si

Assets Largely IFRS fair values

Local knowledge. Global power. 28INTERNAL

HLVRPs very valuable

HLV ize and effort)

15

ERC components

EUR MM FY 2008 FY 2007

AEGON Americas

AEGON NL

AEGON UK

AEGON CEE

AEGON Spain

AEGON Asia

Holdings and Other Countries

Offset AEGON NV AEGON NV AEGON NV

Investment and counterparty riskIR1 Fixed income

HY 2009

RPs can help calculate:• interest rate mismatch risk ERC• interest rate volatility risk ERC• currency mismatch risk ERC

• equity level risk ERCIR1a Spead mismatchIR2 Equity shockIR3 Alternative investmentsIR4 Counterparty riskIR5 Equity volatility

Mismatch riskMR1 Interest rateMR2 Interest rate volatilityMR3 Currency

Underwriting riskUR1C Mortality contagionUR1P Mortality and longevity level and trend

Mortality level and trendLongevity level and trend

UR2C Morbidity contagionUR2P Morbidity level and trendUR3C Persistency contagionUR3P Persistency parameterUR4C Property and casualty contagionUR4P Property and casualty parameter

O ti l i k

• equity volatility risk ERC• large and small economic sensitivities

RPs are not expected to help calculate:

RPs may also help calculate:• credit spread risk ERC

• aggregation of ERCs across risks, BUs and economies/geographies

Local knowledge. Global power. 29INTERNAL

Operational riskAfter tax gross ERCDiversification benefitsERC from shareholders' perspective

ERC from shareholders' perspectiveHoldings ERCOffset eliminationERC from policyholders' perspective

RPs are not expected to help calculate:• default and migration risk ERC

• counterparty risk ERC• mortality risk ERC• morbidity risk ERC

• policyholder behavior risk ERC• operational risk ERC

MVIS attribution

EUR MM

AEGONAmericas

AEGONNL

AEGONUK

AEGONCEE

AEGONSpain

AEGONAsia

Holdingsand OtherCountries

AEGON NVRPs can help calculate/estimate:

• economic variancesOpening Value (January 1, 2009)Value of New Business (MC VNB)Expected Existing Business Contribution(at reference rate)Experience VariancesAssumption ChangesCorrections and Model ChangesTotal Operating EarningsUnderlying Economic Variances

Interest Rate VariancesCredit VariancesChange in VOCR

• economic variances(i.e. changes in interest rates, equities, implied volatilities,

credit spreads and currencies)

RPs may also help calculate/estimate:• expected existing business contribution

• value of new business• change in liquidity premium

Local knowledge. Global power. 30INTERNAL

gEquity VariancesOther Variances

Currency Exposure VariancesTotal EarningsNon-Operational ChangesClosing Value (June 30, 2009)

RPs are not expected to help calculate/estimate:• experience variances

• assumption changes impact• non-operational changes

16

MVBS projections

ASSETSFuture profits on OBS contractsInvestments for general account

Derivatives for general account

AEGON NL

AEGON UK

AEGON NV consolidated MVN HY 2009

Investments and other assets held for account of policyholder

AEGON NV consolidated MVN FY 2008

AEGON CEE

AEGON Spain

AEGON Asia

Holdings and Other

Countries + Eliminations

(amounts in EUR millions)

AEGON Americas

RPs can help calculate/estimate: H d d Li bilit V lReinsurance assets

Defined benefit assetsDeferred tax assetsOther assets and receivables for general accountCash and cash equivalents for general accountTotal assets

Non-modeled business

Total assets

EQUITY AND LIABILITIESShareholder's equityHoldings activitiesEconomic available capital

LiabilitiesInsurance contracts for account of policyholderInsurance contracts general account

• Hedged Liability Value

RPs may help calculate/estimate:• tax items

• market value margins• frictional cost

• liquidity premium

Local knowledge. Global power. 31INTERNAL

Investment contracts for account of policyholderInvestment contracts for general accountBorrowings not related to capital fundingDerivativesProvisionsDefined benefit liabilitiesDeferred tax liabilitiesOther liabilitiesAccrualsValue of own credit riskTotal liabilities

Total equity and liabilities

Other estimation techniques should be used to adjust RP values for:

• actual vs expected inforce experience• changes in assumptions

• new business volume/mix variations

The Replication/Fitting Process

Local knowledge. Global power. 32INTERNAL

17

The Familiar Elements (1)

• Actuarial Projection Models– Same models used for AeMcS

• Business Hierarchy– How are model points currently split?

• by product, issue year, …– May want to split a bit differently

• fixed vs. flexible premiums?• vary by benefit types?

– BU submits in Excel format• Group reviews & enters into system

Local knowledge. Global power. 33INTERNAL

• Group reviews & enters into system

• Product Descriptions– Product features & their relationship to risk factors– Helps guide choice of candidate instruments

Business Hierarchy Example

US

Individual Annuities

Retirement Services

FA

SPDA Newer

SPDA Older

VA

Base Contract

GMDB

Terminal Funding

Deterministic Liabs

GA Assets

401k

Local knowledge. Global power. 34INTERNAL

SPIA

GA Assets

GMAB

GMIB

GMWB

18

The Familiar Elements (2)

• Market Data– To generate economic scenarios– To value candidate instruments/assets– To generate market risk distributionsg

• Economic Scenarios– Training

• vary market risk factors (rates, index levels, vols)• both large & more representative shocks

– Out-of Sample• to test predictive value of RP• checks values between/around training scenario sprays

Local knowledge. Global power. 35INTERNAL

g p y

• Cash flows– Projected for economic scenarios outlined above– Convert to CSV format and upload into system

Training Scenarios

Stress overview DescriptionBase risk-neutral sprayInterest rate stresses up interest rate shocks (large)

up interest rate sensitivities (smaller)down interest rate shocks (large)down interest rate shocks (large)down interest rate sensitivities (smaller)

Interest rate volatility interest rate volatility shocks (large)interest rate volatility sensitivities (smaller)

Equity stresses equity shocks (large)equity sensitivities (smaller)

Equity volatility equity vol shocks (large)equity vol sensitivities (smaller)

Combined stresses combined interest rate and equity sensitivities

Local knowledge. Global power. 36INTERNAL

• Total # of interest rate training scenarios = 1500• Total # of interest rate & equity training scenarios = 2500• Separate smaller set for pure (non-optional) fee business

19

Out-of-sample Scenarios

Stress overview DescriptionChecking base value small variations in interest rates

small variations in equitiescombined interest rate and equity sensitivities

Checking interest rate variations in interest rates (e g parallel shocks)Checking interest rate movements

variations in interest rates (e.g. parallel shocks)combined interest rate and equity sensitivities

Checking equity variations in equitiescombined interest rate and equity sensitivities

Checking volatilities variations in interest rate volsvariations in equity volscombined interest rate vol & equity vol sensitivities

Local knowledge. Global power. 37INTERNAL

• Should be different from training scenarios• Total # of interest rate out-of-sample scenarios = 900• Total # of interest rate & equity out-of-sample scenarios = 2200

The New Elements – Optimization Requests

• Download Excel template with multiple tabs

• Choose candidate instruments by category– ZCBs swaptions index forwards index options– ZCBs, swaptions, index forwards, index options– Exotic derivatives (e.g. path-dependent options)

• Choose optimization settings– Deterministic, Multi-deterministic, IR stochastic, IR & Equity– Optimization function

• minimize abs error vs. squared error– Cash flow bucketing

h i h fl fit i i iti l t

Local knowledge. Global power. 38INTERNAL

• emphasize cash flow fit in initial quarters– Hard/soft value constraints– Trade penalties

• minimizes large offsetting positions & resulting RPs more intuitive

• Upload filled-out Excel template into system

20

Proof of Concept: Lessons Learned

PV of Liab Cash Flows versus PV of Rep Portfolio Cash Flows by Scenario

Importance of Replicating Universe

Liabilities often contain rich, complex embedded optionsVanilla replicating instruments alone y

(all 000s)

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

PV o

f Lia

b C

FsR^2=0.97

Vanilla replicating instruments alone may not be sufficient to capture sensitivities with a high degree of accuracy

Define a replicating universe that is:• Generic enough to be manageable • Rich enough to capture sensitivities

sufficiently

Determine bucketing scheme

• Using single buckets will usually not

Local knowledge. Global power. 39INTERNAL

00 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000

PV of Rep Portfolio CFs

• Using single buckets will usually not result in a good cash flow match for the first year

• In production, bucketing will at least break out first few quarters’ cash flows to ensure good cash flow match

Importance of replicating asset universe: finding a tradeoff

Vanilla Universe• Swaps• Swaptions• Zero Coupon Bonds

Caps and FloorsStructured (Complex)

• Caps and Floors• Forwards• Puts and Calls• etc

Universe

• Structures more reflective ofliability features

• plus vanilla instruments

Vanilla Universe Structured Universe

Local knowledge. Global power. 40INTERNAL

Vanilla Universe Structured Universe

Maintenance Easy Harder

Availability of instruments Typically available Often not available, require calibration

Speed of valuation Fast Slow

Stability of replicating portfolio Potentially less stable Tends to be more stable

Hedging Basis for hedge strategy Custom structures harder to apply for hedging purposes

Number of instruments Tend to use more Tend to use fewer

21

Replicating Instrument Set

Instrument Group Instrument TypeCore Cash Flow ZCB s(at key rates)Vanilla InterestDerivatives

IR SwapsCaps / FloorsEuropean Swaption (Cash Settled)European Swaption (Phys. Settled)

Exotic Interest Derivatives CMS Caps / FloorsStructured Yield Curve Instruments

Vanilla Market Index Derivatives

Market Index ForwardsEuropean Calls and Puts

Exotic Market Index Derivatives

American Calls and PutsForward Starting EuropeansSi l B i O ti

Local knowledge. Global power. 41INTERNAL

Single Barrier OptionsAsian/Lookback Calls and PutsCompound Index ForwardsEuropeans on Compound Indexes

The New Elements – Replication Results

• RP Results & Goodness-of-fit– Weights x Instruments– R-squared (necessary but not sufficient) – Scatter plots (pretty, intuitive & persuasive)p (p y, p )– Max & mean absolute regret (how meaningful?)– Interest rate & equity Greeks (e.g. KRDs, Delta/Gamma)– Other specified sensitivities (e.g. parallel shifts)– PV RP cash flow vs. PV benchmark cash flow

• absolute difference & % difference• relative % change vs. base• for all training & out-of-sample scenario sprays run by BU

Local knowledge. Global power. 42INTERNAL

• Compare and choose best fitting RP– More complex business will take more time & effort– Multiple iterations (and possibly new instruments) may be needed to get

comfortable

22

Sample scatter plot

Local knowledge. Global power. 43INTERNAL

GOF Approach (1 of 5)

Risk-neutralreplio value

Risk-neutralliability value

1

2 4

3

Risk-neutralreplio value

Risk-neutralliability value

1

2 4

3

True liability valueTheoreticalreplio valueTrue liability valueTheoreticalreplio value

1. “true” value of the liabilities – Consistent with observed asset market prices. Not directly observable. Other measures are alternative approaches to estimating this value.

2. risk-neutral liability value – Discounted value of the liability cashflows produced by the liability model under a risk-neutral scenario set.

3 theoretical RP value – Theoretical market value of the assets in the replicating

Local knowledge. Global power. 44INTERNAL

3. theoretical RP value Theoretical market value of the assets in the replicating portfolio, as calculated in Algo, usually using a closed form approach. Much easier and quicker to calculate than the risk-neutral liability value (2), and so can be used more flexibly.

4. risk-neutral RP value – Discounted value of the replicating portfolio asset cashflows under the risk-neutral scenario set used to calculate the risk-neutral liability measure (2).

23

GOF Approach (2 of 5)

Risk-neutralreplio value

Risk-neutralliability value

1

2 4

3

Sampling error

Parameterization error

Risk-neutralreplio value

Risk-neutralliability value

1

2 4

3

Sampling error

Parameterization error

Risk-neutralreplio value

Risk-neutralliability value

1

2 4

3

Risk-neutralreplio value

Risk-neutralliability value

1

2 4

3

Sampling error

Parameterization error

True liability valueTheoreticalreplio value

Replication error

True liability valueTheoreticalreplio valueTrue liability valueTheoreticalreplio valueTrue liability valueTheoreticalreplio value

Replication error

• replication error – Caused by a replication being imperfect, with the RP not producing exactly the same cashflows as the liability model.

• sampling error – Due to the use of random scenarios in a risk-neutral valuation. D th b f i i

Local knowledge. Global power. 45INTERNAL

Decreases as the number of scenarios increases.• parameterization error – Limitation of the Economic Scenario Generator

(“ESG”), caused by the impracticality of creating a set of economic scenarios capable of accurately pricing all market instruments. The scenarios cannot be calibrated to the full set of economic parameters observable in the market. In particular, there are practical limits to the portion of full implied volatility surfaces for equity and interest options to which one can calibrate.

GOF Approach (3 of 5)

Risk-neutralreplio value

Risk-neutralliability value

2 4

Sampling error

Revised comparison

Risk-neutralreplio value

Risk-neutralliability value

2 4

Sampling error

Revised comparison

Replication error

True liability value Theoreticalreplio value

1 3

Parameterization error

Original comparison

Replication error

True liability value Theoreticalreplio value

1 3

Parameterization error

Original comparison

Local knowledge. Global power. 46INTERNAL

• The most intuitive comparison is between risk-neutral liability value (which many actuaries think is equal to the true liability value) and the theoretical RP value, since this is analogous to comparing ones “old” results to the “new” results.

• However, a preferable comparison is available, between the risk-neutral liability value and the risk-neutral RP value.

24

GOF Approach (4 of 5)

Risk-neutralreplio value

Risk-neutralliability value

2 4

Sampling error

Control variate dj f

Risk-neutralreplio value

Risk-neutralliability value

2 4

Sampling error

Control variate dj f

Replication error

True liability value Theoreticalreplio value

1 3

Parameterization error

adjustment factor

Replication error

True liability value Theoreticalreplio value

1 3

Parameterization error

adjustment factor

Local knowledge. Global power. 47INTERNAL

• New estimated liability value = RN liab value + (Theo RP value - RN RP value)

• New estimated liability value = (RN liab value - RN RP value) + Theo RP value

• New estimated liability value ≈ Theo RP value

GOF Approach (5 of 5)

Risk-neutralreplio value

Risk-neutralliability value

2 4

Sampling error

Parameterization

Revised comparison

Risk-neutralreplio value

Risk-neutralliability value

2 4

Sampling error

Parameterization

Revised comparison

Replication error

True liability value

Theoreticalreplio value

1

3

Parameterization error

Instrument valuation error

Original comparison

Replication error

True liability value

Theoreticalreplio value

1

3

Parameterization error

Instrument valuation error

Original comparison

Local knowledge. Global power. 48INTERNAL

• instrument valuation error – Caused by errors in the market data and/or valuation formulas for the assets in the replicating portfolio. Minimized through appropriate pre-optimization validation procedures.

25

The New Elements – Scaling Factors

• Should also adjust RP for non-market risk elements– Inforce

• Actual vs. expected actuarial experience• Actuarial assumption changes

– New business• Volume sold• Demographic mix sold

• Suggested approaches– Replicate business in materially distinct pieces

• inforce vs. new business• different sub-products?

Local knowledge. Global power. 49INTERNAL

• components of MVL (e.g. HLV, taxes, margins, LP)?– Scale each RP, using ratio of

• Current level of a volume driver (specific to product and risk type)• Projected value of same driver (to current date, using models at replication date)

– Calculated all projected RP values on an “aged” basis

The New Elements – Market Risk Reporting

• Market risk reports available – At any level of the business hierarchy– For assets, liabs or the difference

• VaR reports & market risk ERCs– Market risk ERCs ≈ 99.5% VaR for each risk factor

• CTE measures also readily available– Aggregate by applying copula (VCV matrix) to results

• consistent with current process

Local knowledge. Global power. 50INTERNAL

• Stress/Sensitivity Scenarios & MVIS attribution– Can help isolate MVIS economic variance sub-lines– Could also be used to populate risk disclosures– Predefined set for capturing risk dashboard

26

Using Trade Restrictions to ImproveUsing Trade Restrictions to Improve Your Replicating Portfolios

Curt BurmeisterVice President, Risk Solutions

Finding a Good Replicating Portfolio

Common Choices• Candidate Instrument Universe• Scenario Set• Objective Function • Constraints

Common Problems• Too many candidate instruments• Poor out-of-sample performance• Large offsetting trades

© 2010 Algorithmics Incorporated. All rights reserved. 52

• Hard to interpret results

27

Variable Annuity Portfolio – # Policies by GMDB type

~15000 Total Policies

Policy Date ROP Roll-up Ratchet Combo Total

< 2002 2428 1057 1960 664 6109

2002-2005 2165 444 879 1583 5071

2005-2007 1389 0 682 2147 4218

Total 5982 1501 3521 4394 15398

© 2010 Algorithmics Incorporated. All rights reserved. 53

Variable Annuity Portfolio – # Policies by ITM Band

1: MGDB Guarantee / Account Value < 0.92: 0.9 ≤ MGDB Guarantee / Account Value ≤ 1.13: 1.1 ≤ MGDB Guarantee / Account Value

ITM Band ROP Roll-up Ratchet Combo Total

1 4391 455 984 361 6192

2 1396 419 2241 3587 7645

3 195 627 296 446 1567

Total 5982 1501 3521 4394 15398

© 2010 Algorithmics Incorporated. All rights reserved. 54

28

Variable Annuity Cash Flows

Scenario dependent cash flows include Market Indices

1. guaranteed minimum death benefit 2. general account release3. commissions4. expenses5. mortality/expense charge6. revenue sharing7. surrender charges8. per policy fees

1. US Interest Rate Curve2. Russell 1000 3. S&P 5004. Nasdaq 1005. MSCI EAFE Index 6. MSCI Emerging Market Free7. MSCI REIT Index8. Lehman US Aggregate

© 2010 Algorithmics Incorporated. All rights reserved. 55

gg g

Replicating Universe and Optimization Setup

366 Replicating Instruments• Zero Coupon Bonds• Swaptions (physical settlement),

E it F d ( h i d )• Equity Forwards (on each index)• European Equity Options (on each index)

500 ScenariosSet A = 250 (used for optimization)Set B = 250 scenarios (used for out-of-sample testing)

© 2010 Algorithmics Incorporated. All rights reserved. 56

20 years of Annual Cash Flows

29

Annual Variable Annuity Cash Flows

© 2010 Algorithmics Incorporated. All rights reserved. 57

Try #1 - Unconstrained Problem

Match Linear (PV cash flows)

Solve optimization using scenario set A

Evaluate the results under scenario sets A & B

© 2010 Algorithmics Incorporated. All rights reserved. 58

30

Match Linear (PV Cash flow)

© 2010 Algorithmics Incorporated. All rights reserved. 59

R2 = 1.000 R2 = .299

Trading Budget Efficient Frontier

Construct an efficient frontier by adding a trading budget constraint and then solving the same problem with varying budget levels

© 2010 Algorithmics Incorporated. All rights reserved. 60

31

Another “Perfect” Solution – Min Units

© 2010 Algorithmics Incorporated. All rights reserved. 61

R2 = 1.000 R2 = .647

Out-of-Sample Evaluation

Evaluate the efficient frontier of replicating portfolios under scenario set B

© 2010 Algorithmics Incorporated. All rights reserved. 62

32

Best Out-of-Sample Solution (1.9K Units)

© 2010 Algorithmics Incorporated. All rights reserved. 63

R2 = .984 R2 = .953

Match Linear - R2 versus Units Traded

© 2010 Algorithmics Incorporated. All rights reserved. 64

33

Trade Penalties Also …

Reduce the number of instruments in the replicating portfolio

Make the replicating portfolio easier to interpret

Eliminate large offsetting positions

© 2010 Algorithmics Incorporated. All rights reserved. 65

Perfect Replication – Min Units

© 2010 Algorithmics Incorporated. All rights reserved. 66

34

Total Instruments Traded

© 2010 Algorithmics Incorporated. All rights reserved. 67

Best Out-of-Sample Solution (1.9K Units)

© 2010 Algorithmics Incorporated. All rights reserved. 68

35

Trade Restrictions

Can also be use to evaluate and compare different objective functions

© 2010 Algorithmics Incorporated. All rights reserved. 69

Match Quadratic - R2 versus Units Traded

© 2010 Algorithmics Incorporated. All rights reserved. 70

36

Match Linear versus Match Quadratic

© 2010 Algorithmics Incorporated. All rights reserved. 71

Match Linear (PV Cashflow) Set A

© 2010 Algorithmics Incorporated. All rights reserved. 72

37

Decisions for Constructing Trade Restrictions

Units or Value

Budget or Penalty

Size of weight, budget, or penalty

© 2010 Algorithmics Incorporated. All rights reserved. 73

References

Brodie, J., Daubechies,I., De Mol, C., Giannone, D. and I. Loris (2008), “Sparse and stable Markowitz portfolios,” European Central Bank Working Paper Series No. 936 (available at www.ecb.europa.eu)

DeMiguel V Garlappi L Nogales F J and R Uppal (2008) “A Generalized Approach toDeMiguel, V., Garlappi, L., Nogales, F.J. and R. Uppal (2008), A Generalized Approach to Portfolio Optimization: Improving Performance By Constraining Portfolio Norms.” London Business School.

Gotoh, J.-Y. and A. Takeda (2009), “On the Role of the Norm Constraint in Portfolio Selection,” Department of Industrial and Systems Engineering Discussion Paper Series ISE 09-03, Chuo University.

Hesterberg, T., Choi, N.H., Meier, L. and C. Fraley (2008), “Least angle and l1 penalized regression: A review,” Statistics Surveys 2, 61-93.

© 2010 Algorithmics Incorporated. All rights reserved. 74

Tibshirani, R. (1996), “Regression shrinkage and selection via the lasso,” Journal of the Royal Statistical Society Series B, 58, 267-288.

Wang, H., Li, G. and G. Jiang (2007), “Robust regression shrinkage and consistent variable selection through the LAD-lasso,” Journal of Business & Economic Statistics, 25:3, 347-355.

38

Q & AQuestions?

© 2010 Algorithmics Incorporated. All rights reserved. 75

Q & AQuest o s