Embed Size (px)

Citation preview

INTERIM RESULTS PRESENTATION FOR THE 26 WEEKS ENDED 1 JULY 2018

InterimResults

for the period ended 1 July 2018

AGENDA

FINANCIAL REVIEWOPERATIONAL REVIEW

FINANCIAL REVIEW

Hans van Lierop

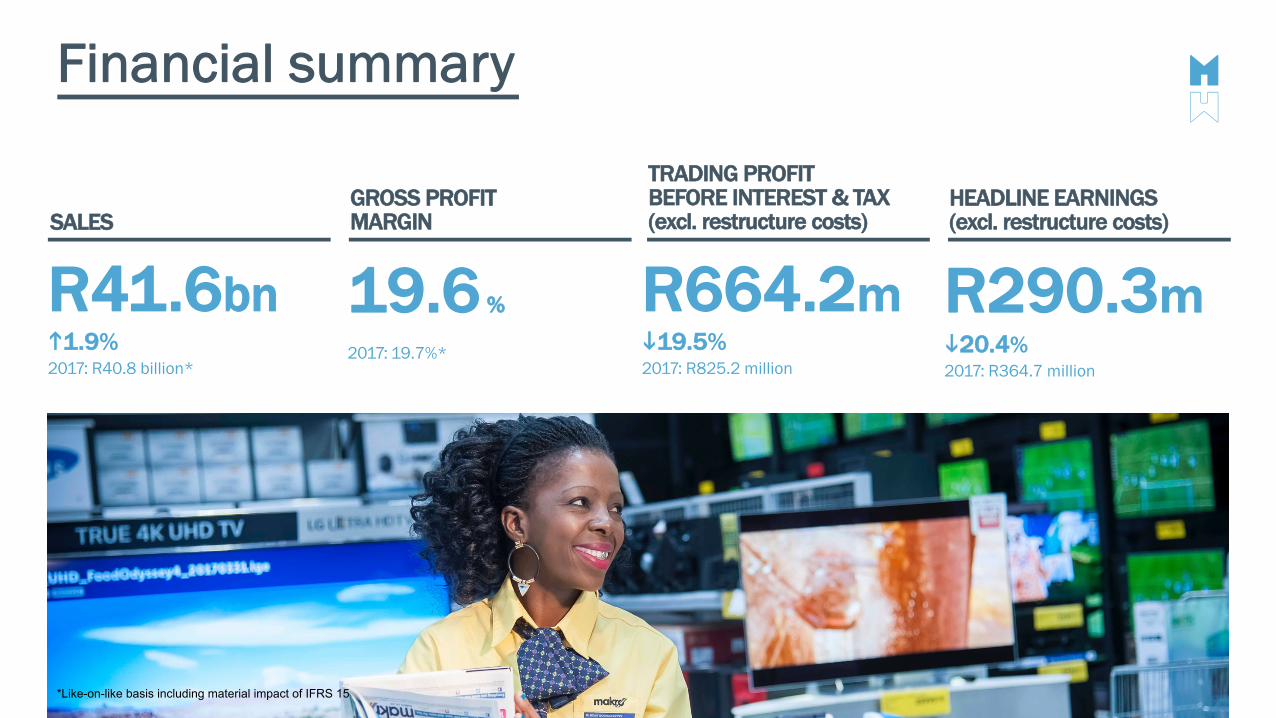

Financial summary

SALES

R290.3m 2

i20.4%2017: R364.7 million

GROSS PROFITMARGIN

TRADING PROFIT BEFORE INTEREST & TAX (excl. restructure costs)

HEADLINE EARNINGS (excl. restructure costs)

2017: 19.7%*

R41.6bnh1.9%2017: R40.8 billion*

19.6 % R664.2mi19.5%2017: R825.2 million

*Like-on-like basis including material impact of IFRS 15

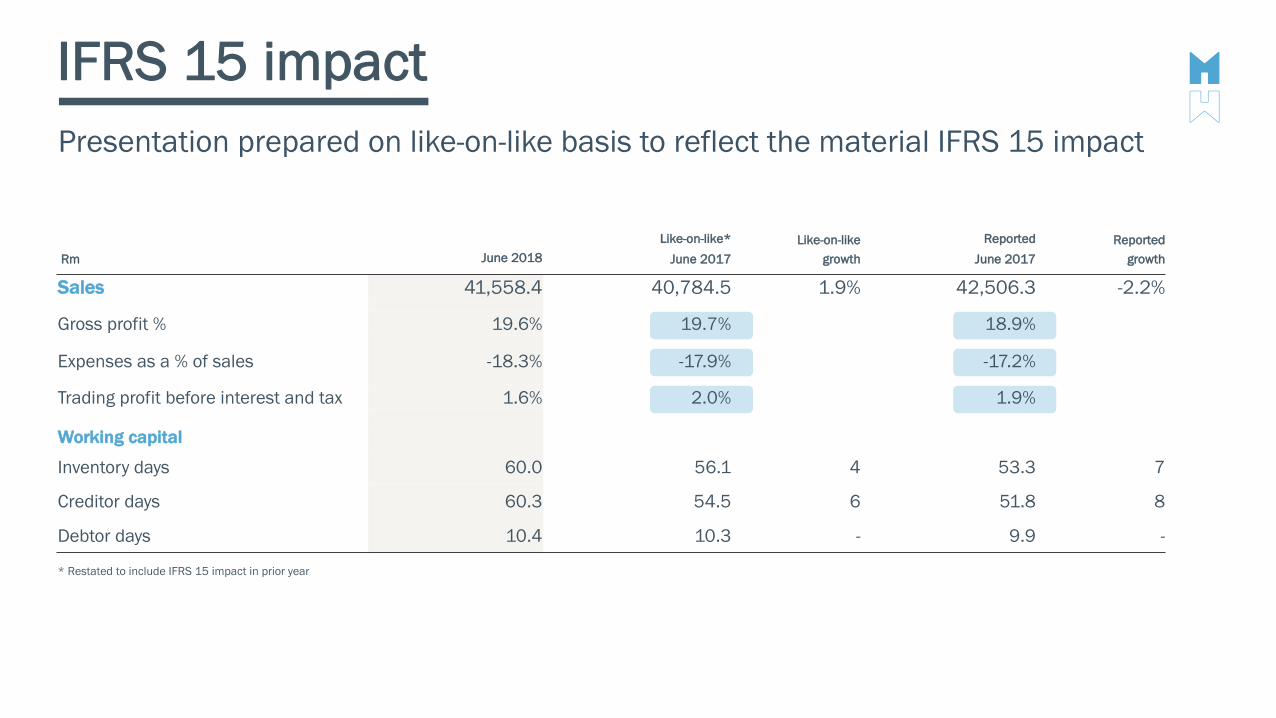

IFRS 15 impactPresentation prepared on like-on-like basis to reflect the material IFRS 15 impact

Like-on-like* Like-on-like Reported ReportedRm June 2018 June 2017 growth June 2017 growth

Sales 41,558.4 40,784.5 1.9% 42,506.3 -2.2%

Gross profit % 19.6% 19.7% 18.9%

Expenses as a % of sales -18.3% -17.9% -17.2%

Trading profit before interest and tax 1.6% 2.0% 1.9%

Working capital

Inventory days 60.0 56.1 4 53.3 7

Creditor days 60.3 54.5 6 51.8 8

Debtor days 10.4 10.3 - 9.9 -

* Restated to include IFRS 15 impact in prior year

Financial highlights

SALES GROWTH* EXPENSE MANAGEMENT

TRADING PROFIT BEFORE INTEREST & TAX(excl. restructure costs)

HEADLINE EARNINGS (excl. restructure costs)

h1.9 % h3.9 % i19.5 % i20.4 %

h0.2% COMPARABLE h2.1% COMPARABLE

June 2018

COMP

* Like-on-like basis including material impact of IFRS 15 in both periods

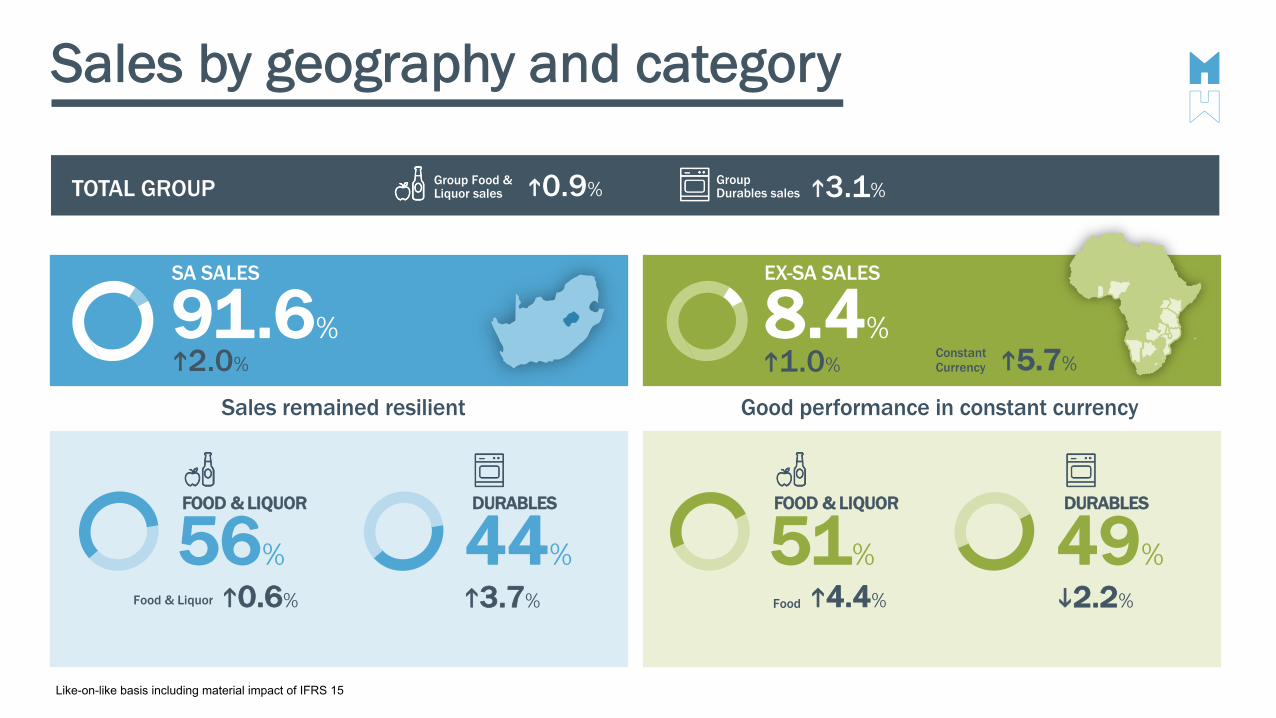

SA SALES

91.6%

EX-SA SALES

8.4%h2.0%

Sales by geography and category

h1.0%

Good performance in constant currency

FOOD & LIQUOR

51%i2.2%

DURABLES

Food h4.4%

49%

FOOD & LIQUOR

56%h3.7%

DURABLES

Food & Liquor h0.6%

44%

ConstantCurrency h5.7%

Group Durables sales h3.1%Group Food &

Liquor sales h0.9%TOTAL GROUP

Sales remained resilient

Like-on-like basis including material impact of IFRS 15

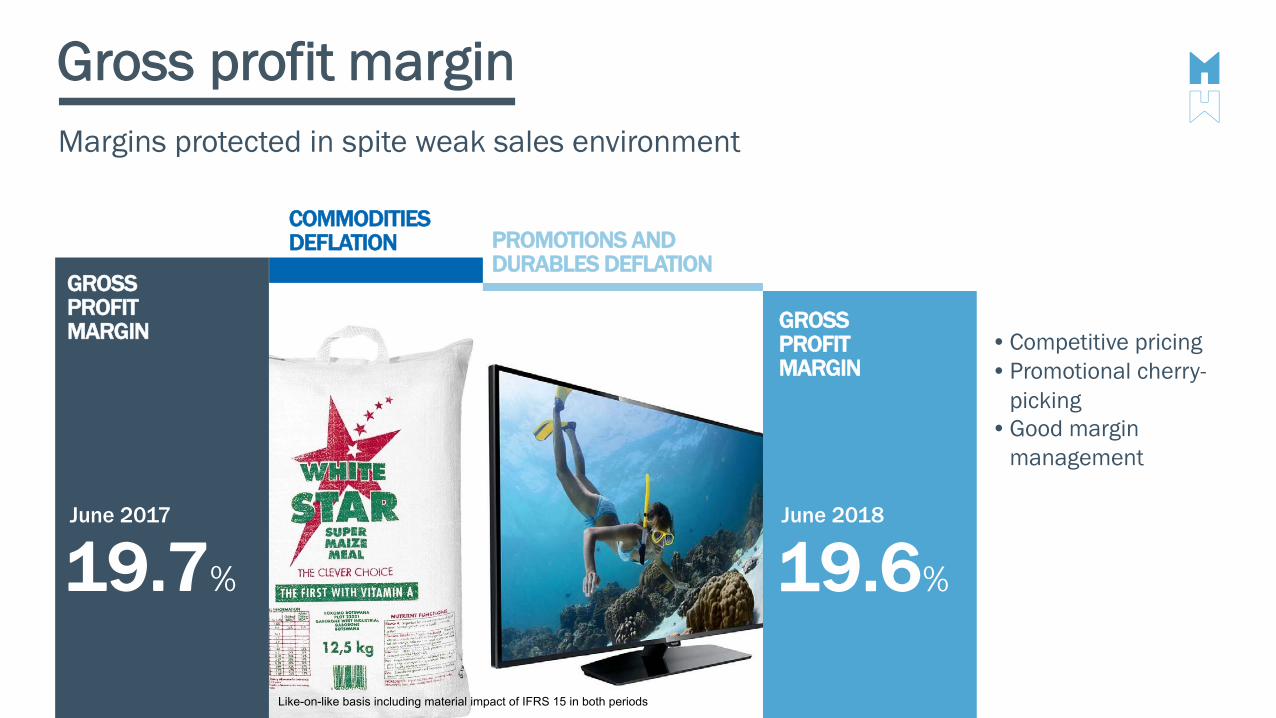

Gross profit margin

June 2017

19.7%

COMMODITIES DEFLATION PROMOTIONS AND

DURABLES DEFLATION

Margins protected in spite weak sales environment

GROSS PROFIT MARGIN

June 2018

19.6%

GROSS PROFIT MARGIN

•Competitive pricing•Promotional cherry-

picking •Good margin

management

Like-on-like basis including material impact of IFRS 15 in both periods

Sustained cost discipline

EMPLOYMENT COSTSDEPRECIATION OCCUPANCY COSTSOTHER OPERATING EXPENSES

h0.5%i2.0%• IT equipment and software• Re-assessment of useful lives(IFRS)

• FTEs remained stable• Improved staff scheduling• Selective replacement

• Net 0.8% trading space increase• Management of municipal and

energy costs• Favourable lease renewals

• 22% of total expenses• Continued focus on cost

containment

h5.8%h4.6%

h5.1 %h3.7%

n0.0 %i3.1%COMPARABLE COMPARABLE COMPARABLE COMPARABLE

Comparable expense growth limited to 2.1%

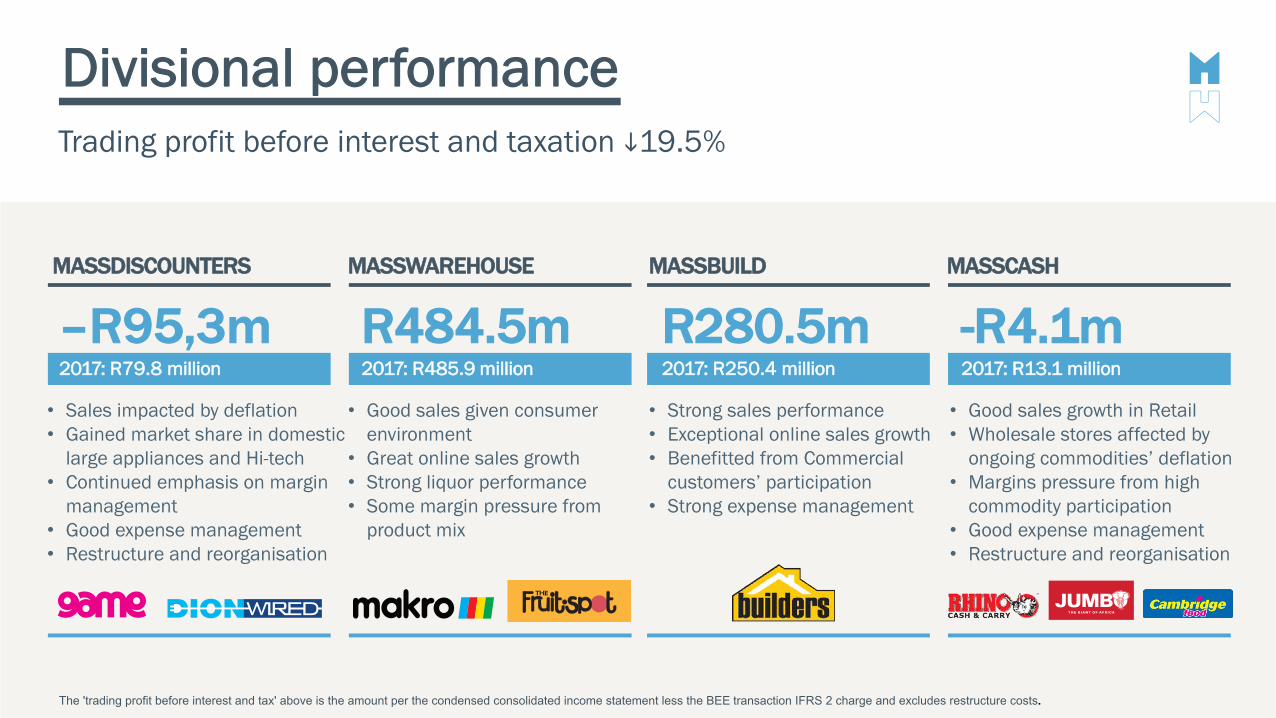

Divisional performance

–R95,3m2017: R79.8 million

R484.5m2017: R485.9 million

R280.5m2017: R250.4 million

-R4.1m2017: R13.1 million

MASSDISCOUNTERS MASSWAREHOUSE MASSBUILD MASSCASH

• Sales impacted by deflation• Gained market share in domestic

large appliances and Hi-tech• Continued emphasis on margin

management• Good expense management• Restructure and reorganisation

• Good sales given consumer environment

• Great online sales growth• Strong liquor performance• Some margin pressure from

product mix

• Strong sales performance• Exceptional online sales growth• Benefitted from Commercial

customers’ participation• Strong expense management

• Good sales growth in Retail• Wholesale stores affected by

ongoing commodities’ deflation• Margins pressure from high

commodity participation• Good expense management• Restructure and reorganisation

The 'trading profit before interest and tax' above is the amount per the condensed consolidated income statement less the BEE transaction IFRS 2 charge and excludes restructure costs.

T H E G I A N T O F A F R I C A

Trading profit before interest and taxation i19.5%

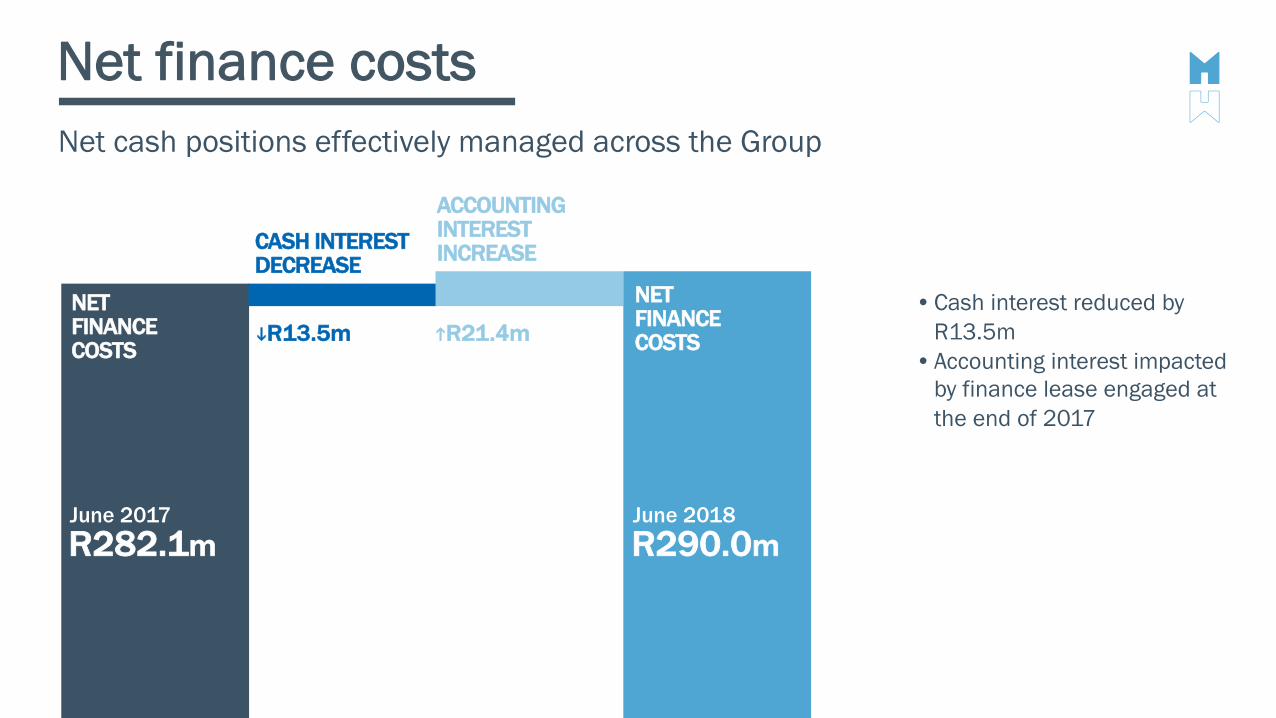

Net finance costs

June 2017R282.1m

CASH INTERESTDECREASE

ACCOUNTINGINTEREST INCREASE

Net cash positions effectively managed across the Group

NETFINANCECOSTS

•Cash interest reduced by R13.5m

•Accounting interest impacted by finance lease engaged at the end of 2017

June 2018R290.0m

hR21.4miR13.5m

NETFINANCECOSTS

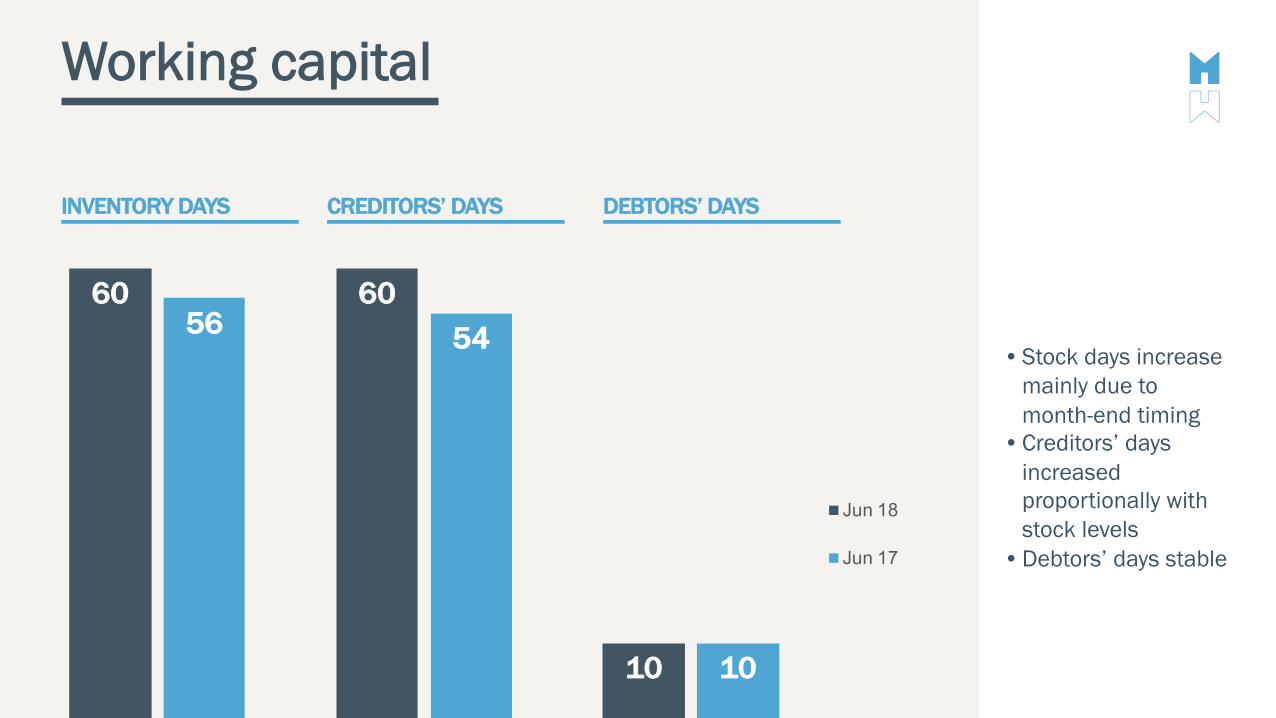

Working capital

DEBTORS’ DAYSCREDITORS’ DAYSINVENTORY DAYS

•Stock days increase mainly due to month-end timing

•Creditors’ days increased proportionally with stock levels

•Debtors’ days stable

60 60

10

56 54

10

Jun 18

Jun 17

OPERATIONAL REVIEW

Guy Hayward

The perfect storm

1st Qtr SA GDP declined CPI increase

Sources: Investec CPI update (July 2018). Statistics SA: Gross Domestic Product (GDP), 1st Quarter 2018. Econometrix Rand & Commodity Price Snapshot (June 2018)

PersonalTax

h5.1% y/yi2.2%hElectricity tarriff

h5.2%

Currency volatility

R/$ exchange rateh10.6%

VAT

h1%

Unemployment high

27.2%

Retail sales growth slowedConsumer confidenceFuel

i0.7% y/yh11.1% 22points

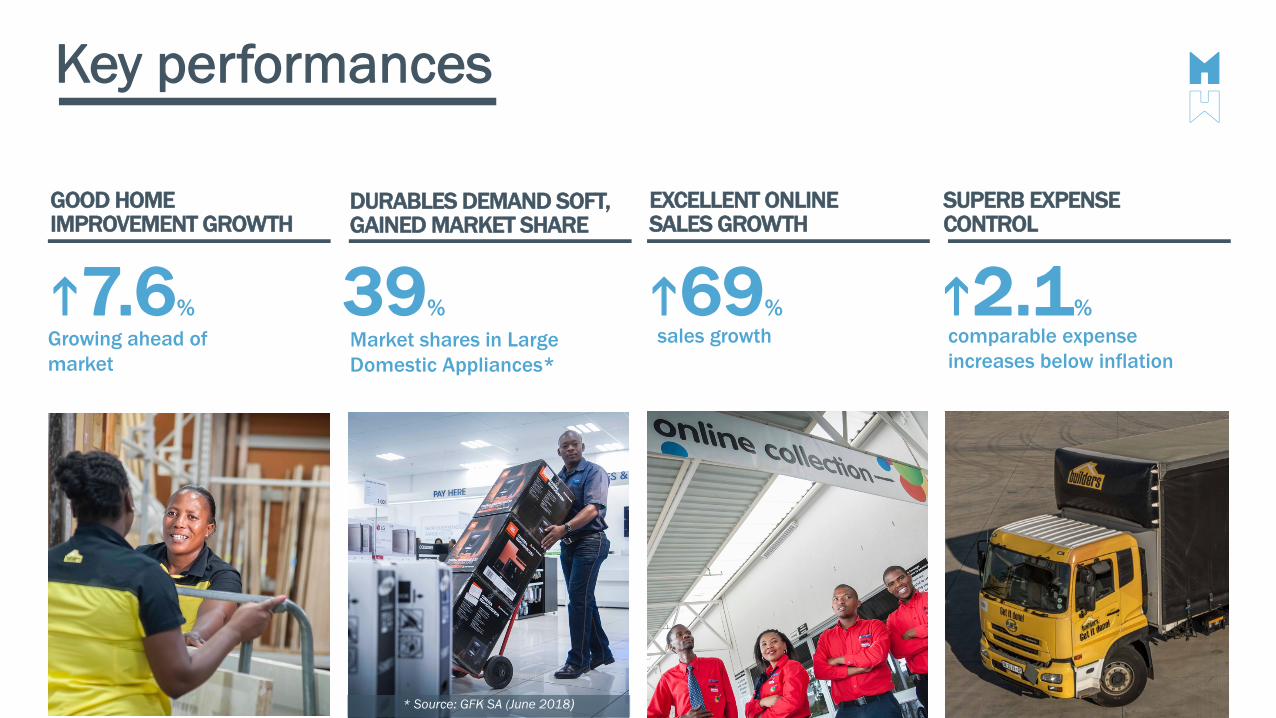

Key performances

Growing ahead of market

comparable expense increases below inflation

sales growthMarket shares in Large Domestic Appliances*

h2.1%39%h7.6% h69%

* Source: GFK SA (June 2018)

EXCELLENT ONLINE SALES GROWTH

SUPERB EXPENSE CONTROL

DURABLES DEMAND SOFT, GAINED MARKET SHARE

GOOD HOME IMPROVEMENT GROWTH

Household consumptionConsumer spending on Durables decreasing

Source: South African Reserve Bank

h1.6%

NON-DURABLES

h1.7%

SERVICES

i9.5%

DURABLES

i6.1%

SEMI-DURABLES

Consumer prioritising Food over Durables

Consumer delaying spend for promotions and prioritising value

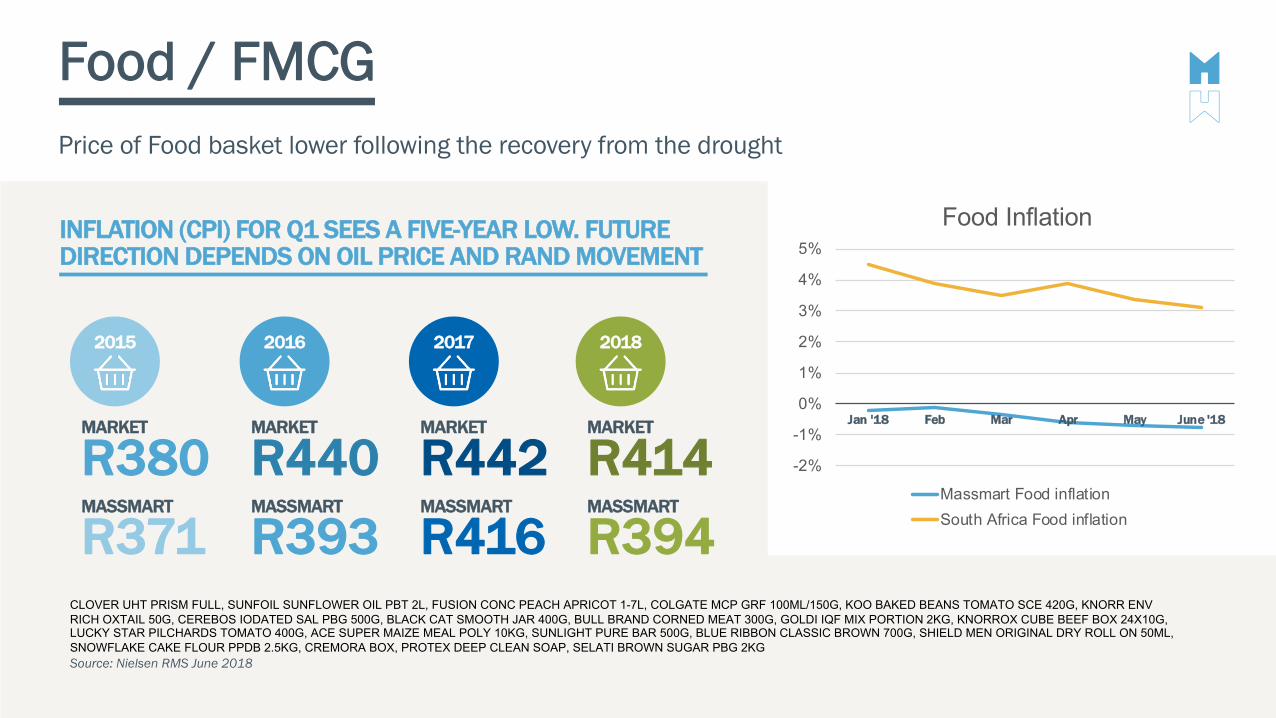

Food / FMCGPrice of Food basket lower following the recovery from the drought

CLOVER UHT PRISM FULL, SUNFOIL SUNFLOWER OIL PBT 2L, FUSION CONC PEACH APRICOT 1-7L, COLGATE MCP GRF 100ML/150G, KOO BAKED BEANS TOMATO SCE 420G, KNORR ENV RICH OXTAIL 50G, CEREBOS IODATED SAL PBG 500G, BLACK CAT SMOOTH JAR 400G, BULL BRAND CORNED MEAT 300G, GOLDI IQF MIX PORTION 2KG, KNORROX CUBE BEEF BOX 24X10G, LUCKY STAR PILCHARDS TOMATO 400G, ACE SUPER MAIZE MEAL POLY 10KG, SUNLIGHT PURE BAR 500G, BLUE RIBBON CLASSIC BROWN 700G, SHIELD MEN ORIGINAL DRY ROLL ON 50ML, SNOWFLAKE CAKE FLOUR PPDB 2.5KG, CREMORA BOX, PROTEX DEEP CLEAN SOAP, SELATI BROWN SUGAR PBG 2KGSource: Nielsen RMS June 2018

INFLATION (CPI) FOR Q1 SEES A FIVE-YEAR LOW. FUTURE DIRECTION DEPENDS ON OIL PRICE AND RAND MOVEMENT

R380MARKET

R371MASSMART

2015

R440MARKET

R393MASSMART

2016

R442MARKET

R416MASSMART

2017

R414MARKET

R394MASSMART

2018

-2%

-1%

0%

1%

2%

3%

4%

5%

Jan '18 Feb Mar Apr May June '18

Food Inflation

Massmart Food inflation

South Africa Food inflation

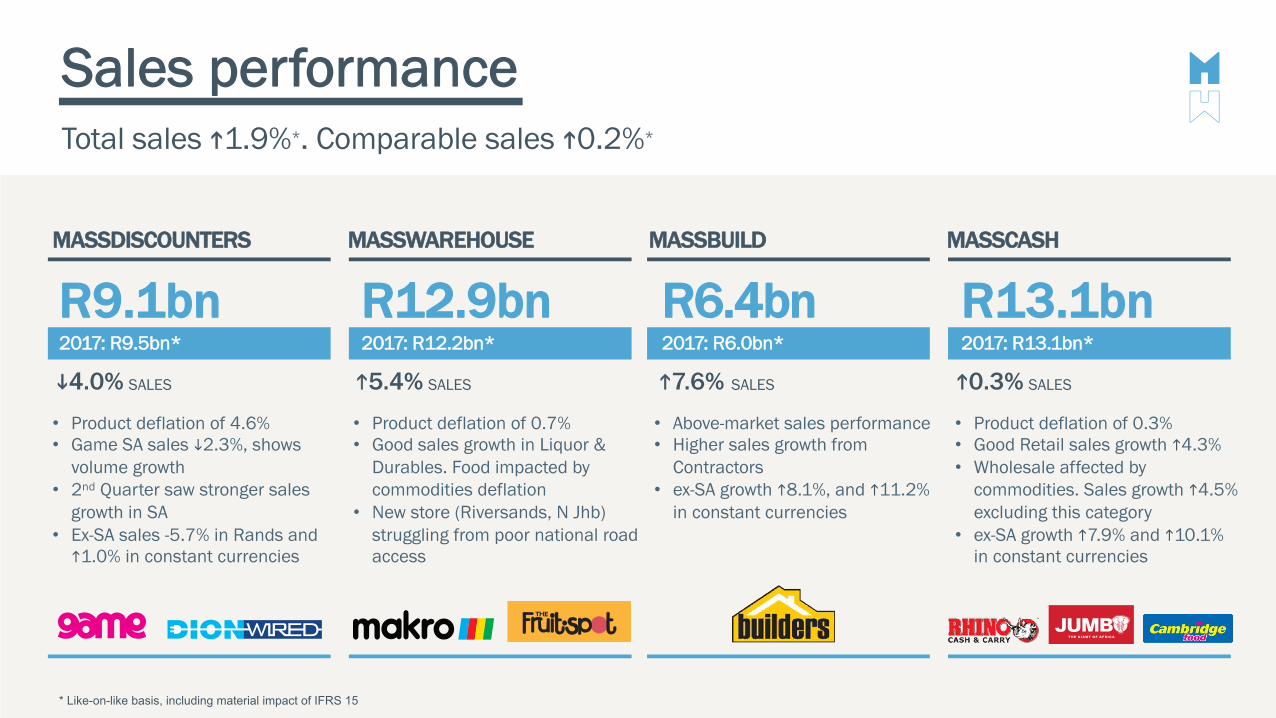

Sales performance

R9.1bn2017: R9.5bn*

R12.9bn2017: R12.2bn*

R6.4bn2017: R6.0bn*

R13.1bn2017: R13.1bn*

Total sales h1.9%*. Comparable sales h0.2%*

MASSDISCOUNTERS MASSWAREHOUSE MASSBUILD MASSCASH

• Product deflation of 4.6%• Game SA sales i2.3%, shows

volume growth • 2nd Quarter saw stronger sales

growth in SA • Ex-SA sales -5.7% in Rands and

h1.0% in constant currencies

• Product deflation of 0.7%• Good sales growth in Liquor &

Durables. Food impacted by commodities deflation

• New store (Riversands, N Jhb) struggling from poor national roadaccess

• Above-market sales performance• Higher sales growth from

Contractors • ex-SA growth h8.1%, and h11.2%

in constant currencies

• Product deflation of 0.3%• Good Retail sales growth h4.3%• Wholesale affected by

commodities. Sales growth h4.5% excluding this category

• ex-SA growth h7.9% and h10.1% in constant currencies

* Like-on-like basis, including material impact of IFRS 15

i4.0% SALES h5.4% SALES h7.6% SALES h0.3% SALES

T H E G I A N T O F A F R I C A

h71%

VAS and online sales growth

growth in gross income underpinned by RCS and bill payments

h29%Improvement in Lotto sales

h31%Instant money transfers

h25%Improvement in extended warranties gross written premiums

Successfully implemented suite of VAS: airtime, electricity, bill payments, lotto and gift cards

h69%Online sales growth

h23%Average basket size

h159%Online traffic growth

h91%Online marketplace growth

195Unique customer collection points

37%Commercial sales contribution to Makro online sales

Click & Collect and delivery available from all Builders stores in SA

Online sales now represent 1.6% sales participation

ONLINE SALESVALUE-ADDED SERVICES (VAS)

Private LabelNew product development and innovation driving sales growth and category leadership

• Focusing on KVI lines• Collaborative seasonal deals

to secure reduced cost prices and increased volumes

• Seeing good margin improvement across all GM brands

• Lusso tap range launched in February - contributes 63% to total tap sales in Massbuild

GEN MERCH

53BRANDS IN PORTFOLIO

14.7%SALES PENETRATION

2017: 14.4%

FOOD

21BRANDS IN PORTFOLIO

7.5%SALES PENETRATION

2017: 6.8%

Leveraging Group scale for efficiencyGroup –wide transport, logistics, planning & storage

Making good progress in providing reliable and cost effective availability of any product in any format or channel, by leveraging group scale

Savings achieved – reduced operating costs, improve margin & working capital

Supplier onboarding through Massmart Distribution Network continues to grow, with further growth planned for H2Objective to reduce cost to serve by 1%

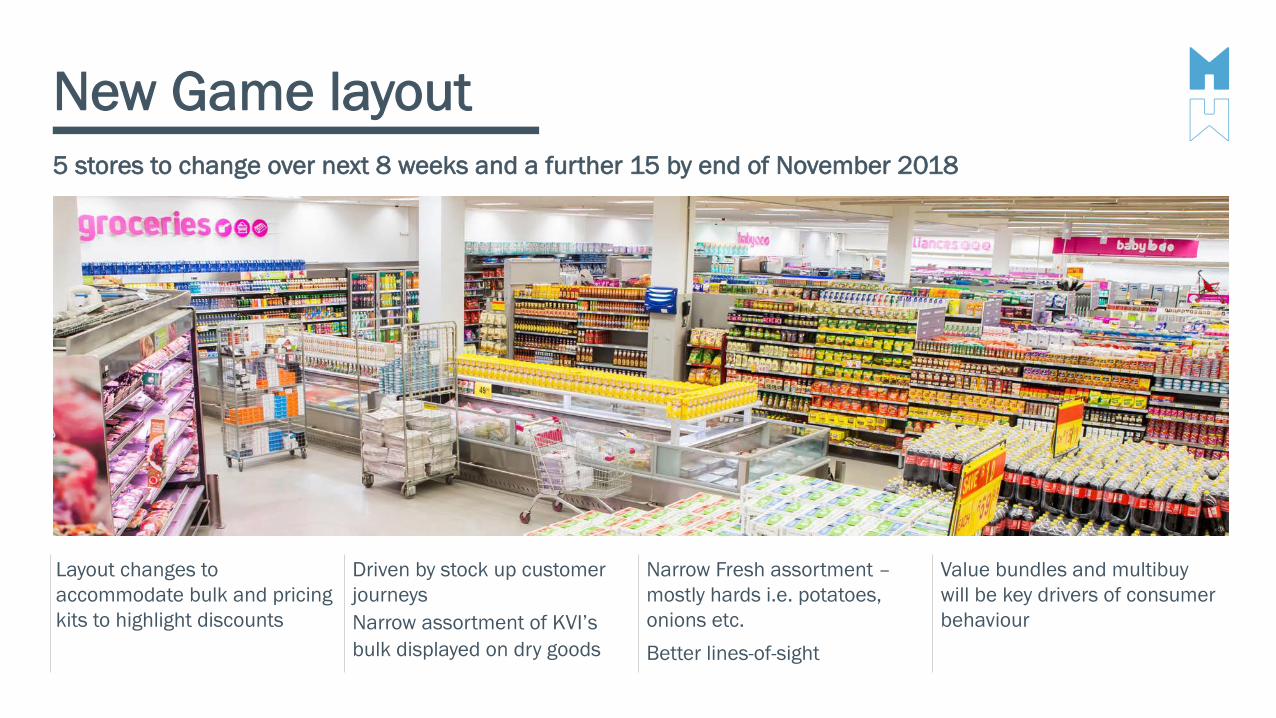

Layout changes to accommodate bulk and pricing kits to highlight discounts

Driven by stock up customer journeysNarrow assortment of KVI’s bulk displayed on dry goods

Narrow Fresh assortment –mostly hards i.e. potatoes, onions etc.Better lines-of-sight

Value bundles and multibuy will be key drivers of consumer behaviour

New Game layout5 stores to change over next 8 weeks and a further 15 by end of November 2018

Builders

Game

Jumbo

BotswanaNamibia

Zambia

Mozambique

Uganda

Nigeria

Tanzania

Malawi

Ghana

Lesotho

Kenya

NEW

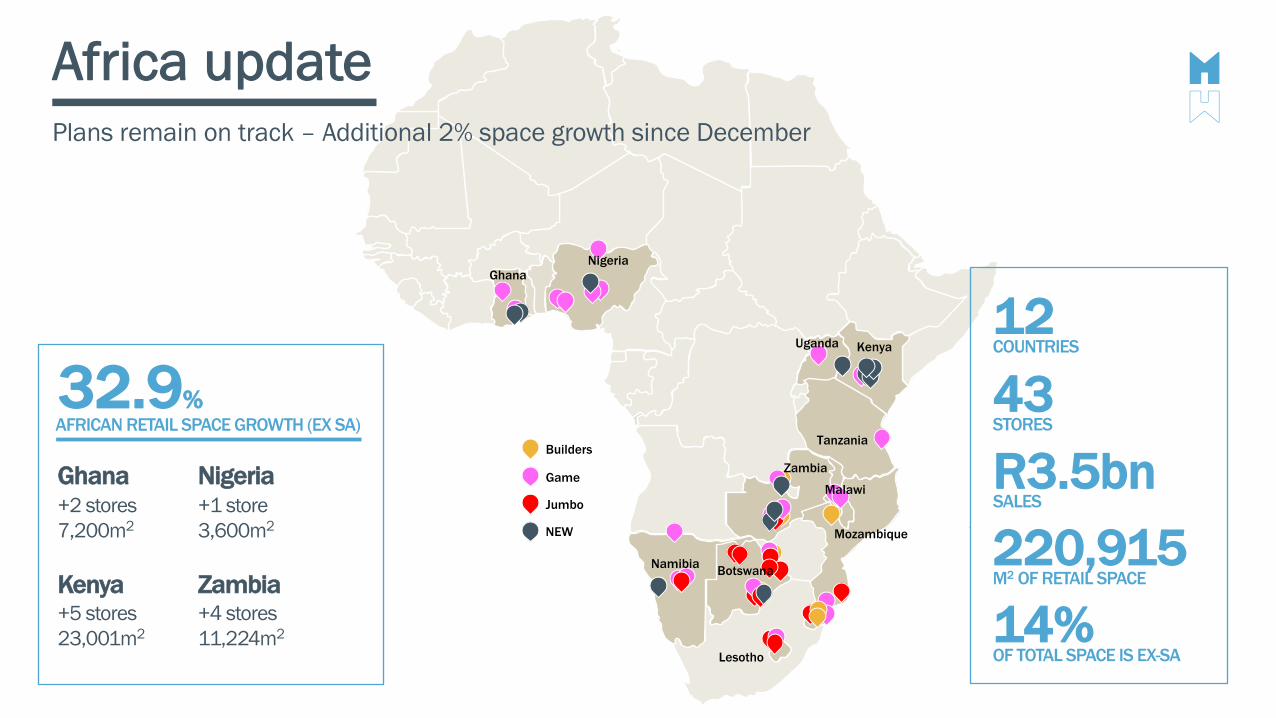

Africa update

AFRICAN RETAIL SPACE GROWTH (EX SA)32.9%

Ghana+2 stores 7,200m2

Kenya+5 stores 23,001m2

Nigeria+1 store 3,600m2

Zambia+4 stores 11,224m2

Plans remain on track – Additional 2% space growth since December

220,915M2 OF RETAIL SPACE

R3.5bnSALES

43STORES

12COUNTRIES

14%OF TOTAL SPACE IS EX-SA

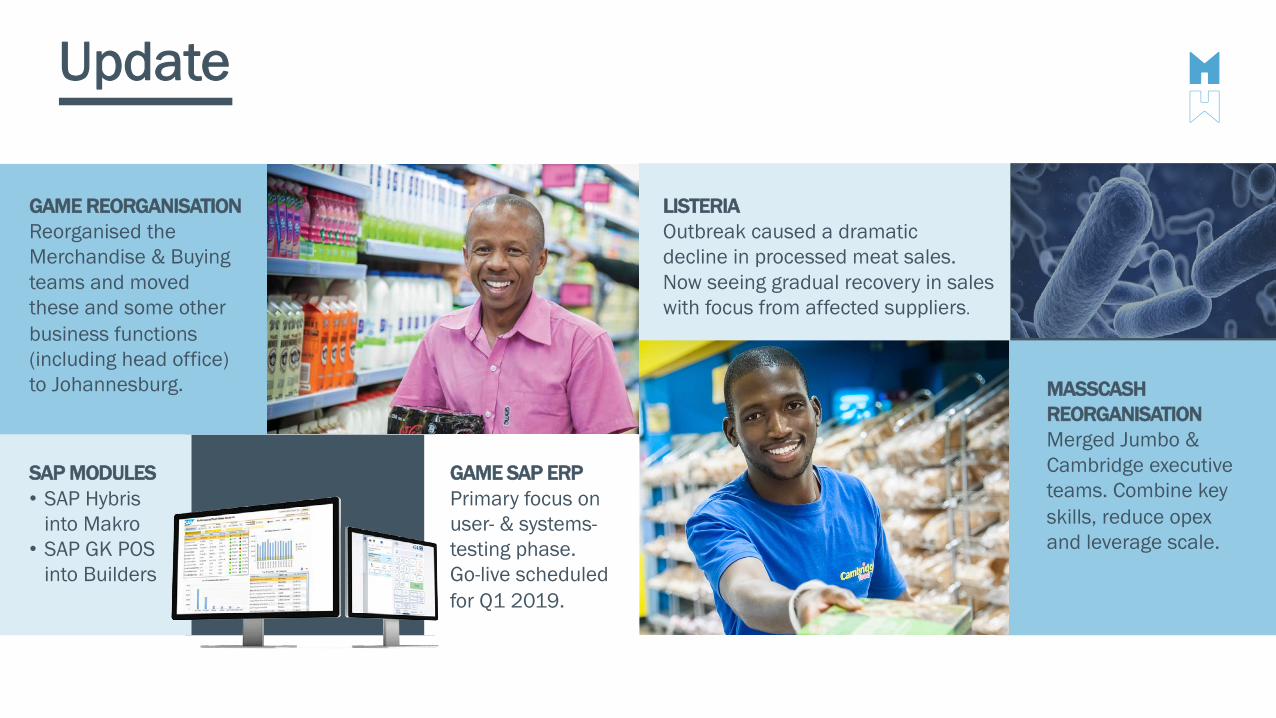

Update

GAME SAP ERPPrimary focus on user- & systems-testing phase.Go-live scheduled for Q1 2019.

MASSCASH REORGANISATIONMerged Jumbo & Cambridge executive teams. Combine key skills, reduce opexand leverage scale.

LISTERIAOutbreak caused a dramatic decline in processed meat sales. Now seeing gradual recovery in sales with focus from affected suppliers.

GAME REORGANISATIONReorganised the Merchandise & Buying teams and moved these and some other business functions (including head office) to Johannesburg.

SAP MODULES• SAP Hybris

into Makro• SAP GK POS

into Builders

4,4 million kWh renewable energy generating capacity –best in SA retail

Sustainable business

Highest BBBEE score in the retail sector with a score of 80.81

Overall winner of the ABSA and Business Day Supplier Development Awards

44 million Department of Basic Education-supplied meals prepared in Massmart mobile kitchens

Rated by FTSE in the top five companies globally for ESG performance in the Broadline Retail Sub-Sector

21 million litres of waterconserved through onsite water harvesting

In summary

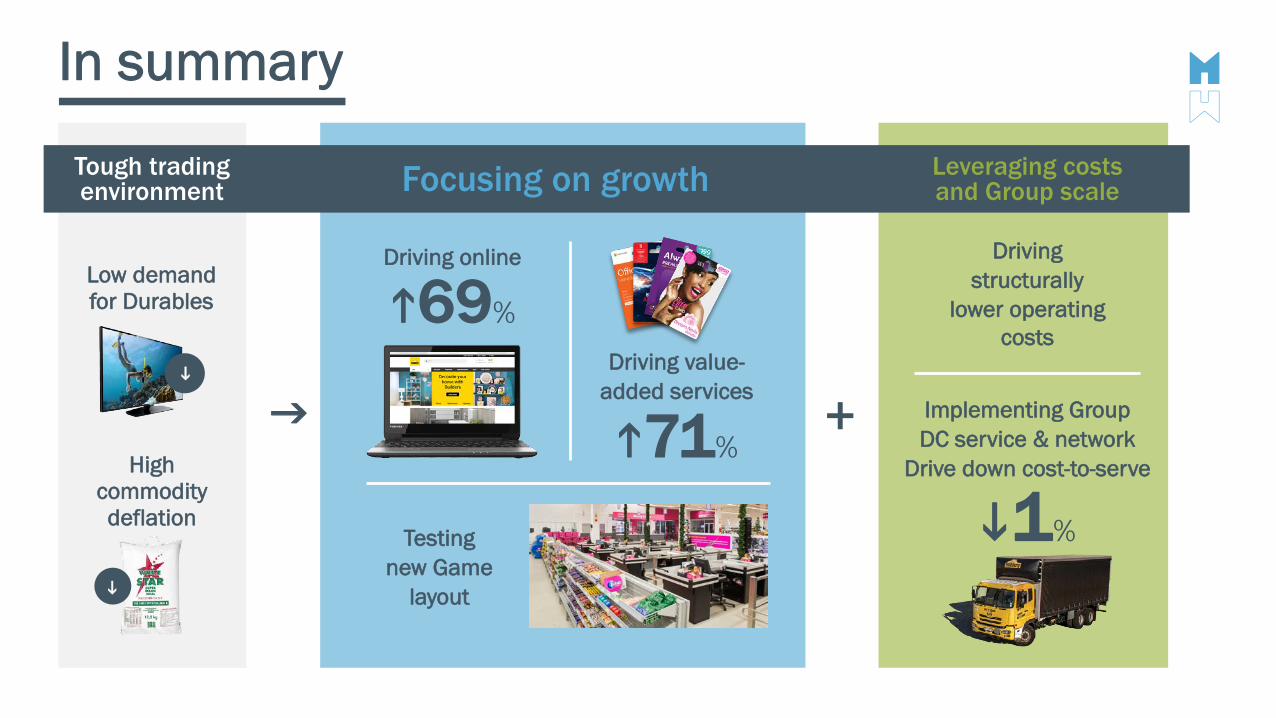

Low demand for Durables

High commodity deflation

i

iDriving value-

added services

h71%

Driving online

h69%

Testing new Game

layout

Focusing on growth

g

Tough trading environment

Leveraging costsand Group scale

+

i1%

Implementing Group DC service & network

Drive down cost-to-serve

Driving structurally

lower operating costs

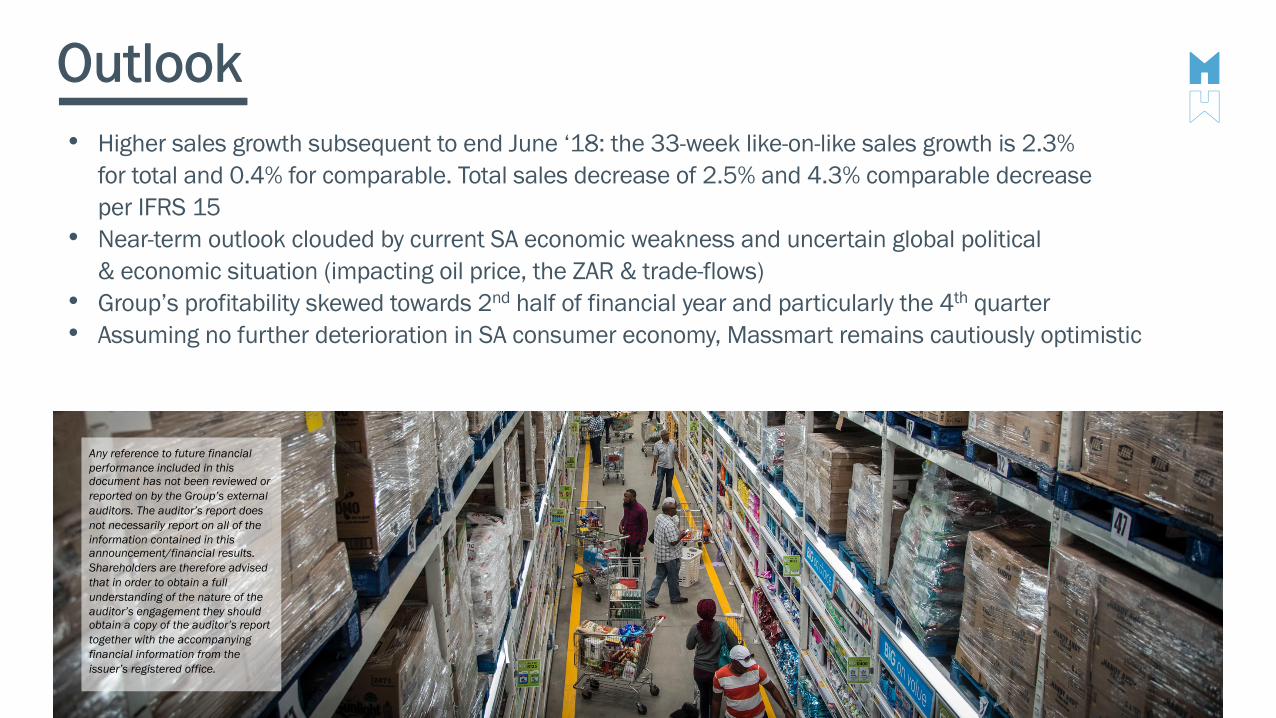

Outlook• Higher sales growth subsequent to end June ‘18: the 33-week like-on-like sales growth is 2.3%

for total and 0.4% for comparable. Total sales decrease of 2.5% and 4.3% comparable decrease per IFRS 15

• Near-term outlook clouded by current SA economic weakness and uncertain global political & economic situation (impacting oil price, the ZAR & trade-flows)

• Group’s profitability skewed towards 2nd half of financial year and particularly the 4th quarter • Assuming no further deterioration in SA consumer economy, Massmart remains cautiously optimistic

Any reference to future financial performance included in this document has not been reviewed or reported on by the Group’s external auditors. The auditor’s report does not necessarily report on all of the information contained in this announcement/financial results. Shareholders are therefore advised that in order to obtain a full understanding of the nature of the auditor’s engagement they should obtain a copy of the auditor’s report together with the accompanying financial information from the issuer’s registered office.

FOR FURTHER DETAILSWWW.MASSMART.CO.ZA/INTERIMRESULTS2018

ADDITIONAL INFORMATIONCondensed consolidated income statementTax rate reconciliationCash flow statementCapital expenditureCapex per categoryStore portfolioForecast stores: Jul 2018 – Jun 2020Number of shares

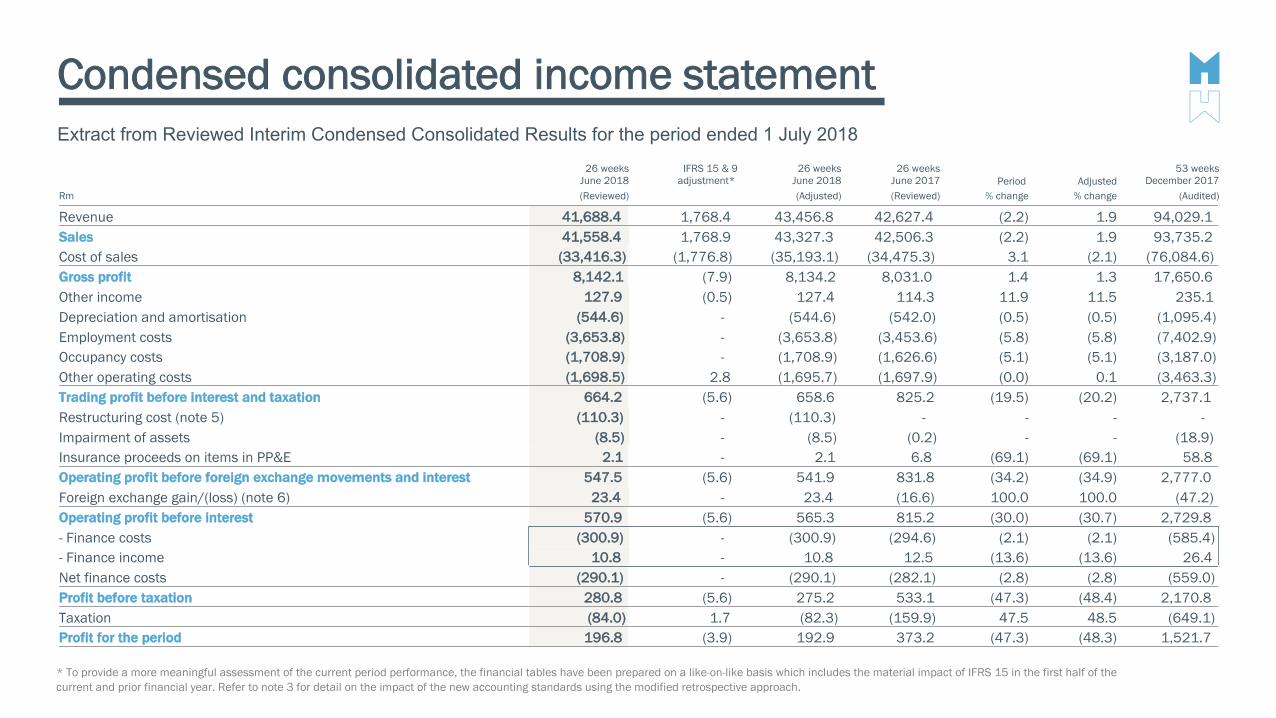

Condensed consolidated income statementExtract from Reviewed Interim Condensed Consolidated Results for the period ended 1 July 2018

* To provide a more meaningful assessment of the current period performance, the financial tables have been prepared on a like-on-like basis which includes the material impact of IFRS 15 in the first half of the current and prior financial year. Refer to note 3 for detail on the impact of the new accounting standards using the modified retrospective approach.

26 weeksJune 2018

IFRS 15 & 9 adjustment*

26 weeksJune 2018

26 weeksJune 2017 Period Adjusted

53 weeksDecember 2017

Rm (Reviewed) (Adjusted) (Reviewed) % change % change (Audited)

Revenue 41,688.4 1,768.4 43,456.8 42,627.4 (2.2) 1.9 94,029.1 Sales 41,558.4 1,768.9 43,327.3 42,506.3 (2.2) 1.9 93,735.2 Cost of sales (33,416.3) (1,776.8) (35,193.1) (34,475.3) 3.1 (2.1) (76,084.6)Gross profit 8,142.1 (7.9) 8,134.2 8,031.0 1.4 1.3 17,650.6 Other income 127.9 (0.5) 127.4 114.3 11.9 11.5 235.1 Depreciation and amortisation (544.6) - (544.6) (542.0) (0.5) (0.5) (1,095.4)Employment costs (3,653.8) - (3,653.8) (3,453.6) (5.8) (5.8) (7,402.9)Occupancy costs (1,708.9) - (1,708.9) (1,626.6) (5.1) (5.1) (3,187.0)Other operating costs (1,698.5) 2.8 (1,695.7) (1,697.9) (0.0) 0.1 (3,463.3)Trading profit before interest and taxation 664.2 (5.6) 658.6 825.2 (19.5) (20.2) 2,737.1 Restructuring cost (note 5) (110.3) - (110.3) - - - -Impairment of assets (8.5) - (8.5) (0.2) - - (18.9)Insurance proceeds on items in PP&E 2.1 - 2.1 6.8 (69.1) (69.1) 58.8 Operating profit before foreign exchange movements and interest 547.5 (5.6) 541.9 831.8 (34.2) (34.9) 2,777.0 Foreign exchange gain/(loss) (note 6) 23.4 - 23.4 (16.6) 100.0 100.0 (47.2)Operating profit before interest 570.9 (5.6) 565.3 815.2 (30.0) (30.7) 2,729.8 - Finance costs (300.9) - (300.9) (294.6) (2.1) (2.1) (585.4)- Finance income 10.8 - 10.8 12.5 (13.6) (13.6) 26.4 Net finance costs (290.1) - (290.1) (282.1) (2.8) (2.8) (559.0)Profit before taxation 280.8 (5.6) 275.2 533.1 (47.3) (48.4) 2,170.8 Taxation (84.0) 1.7 (82.3) (159.9) 47.5 48.5 (649.1)Profit for the period 196.8 (3.9) 192.9 373.2 (47.3) (48.3) 1,521.7

Tax rate reconciliation

%Jun 2018

(Reviewed)Jun 2017

(Reviewed))

Standard tax rate 28.0 28.0

Non-taxable income and disallowable expenses (0.5) 0.2

Assessed loss not utilised 1.9 2.8

Other - including foreign tax adjustments 0.5 (1,0)

Group tax rate 29.9 30.0

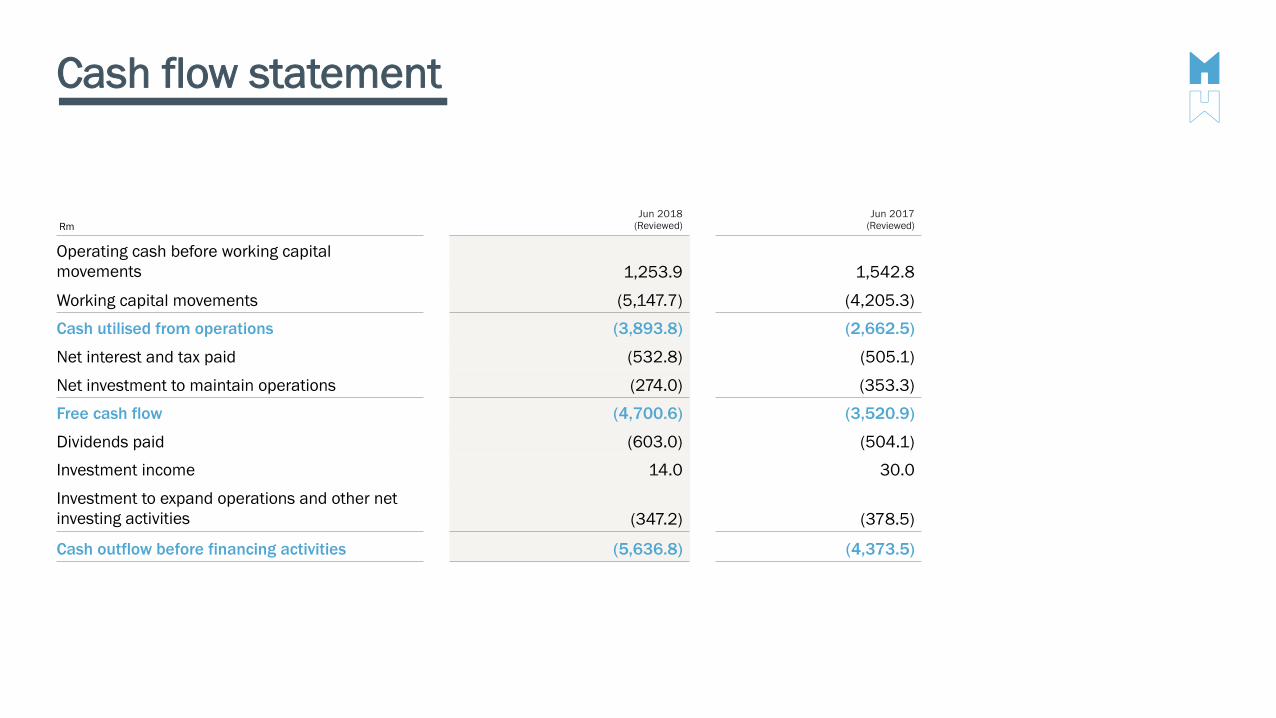

Cash flow statement

RmJun 2018

(Reviewed)Jun 2017

(Reviewed)

Operating cash before working capital movements 1,253.9 1,542.8

Working capital movements (5,147.7) (4,205.3)

Cash utilised from operations (3,893.8) (2,662.5)

Net interest and tax paid (532.8) (505.1)

Net investment to maintain operations (274.0) (353.3)

Free cash flow (4,700.6) (3,520.9)

Dividends paid (603.0) (504.1)

Investment income 14.0 30.0

Investment to expand operations and other net investing activities (347.2) (378.5)

Cash outflow before financing activities (5,636.8) (4,373.5)

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Property expansion

Businesses acquired

Investment to expandoperations

Investment to maintainoperations

Total capex as a % of sales

Total capex as a % of salesexcluding business andproperty acquisitions

Cape

x as

a %

of s

ales

JUN 2013

JUN 2015

JUN2014

JUN 2016

JUN 2017

JUN 2018

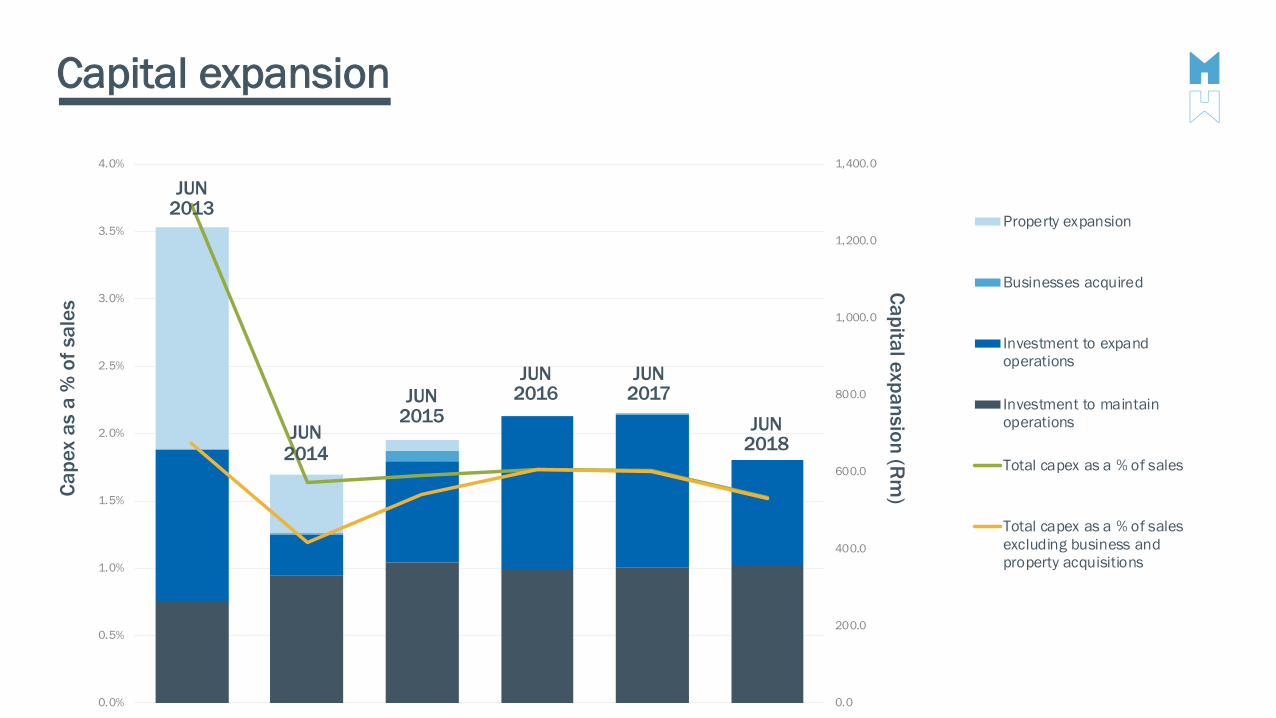

Capital expansion

Capital expansion (Rm

)

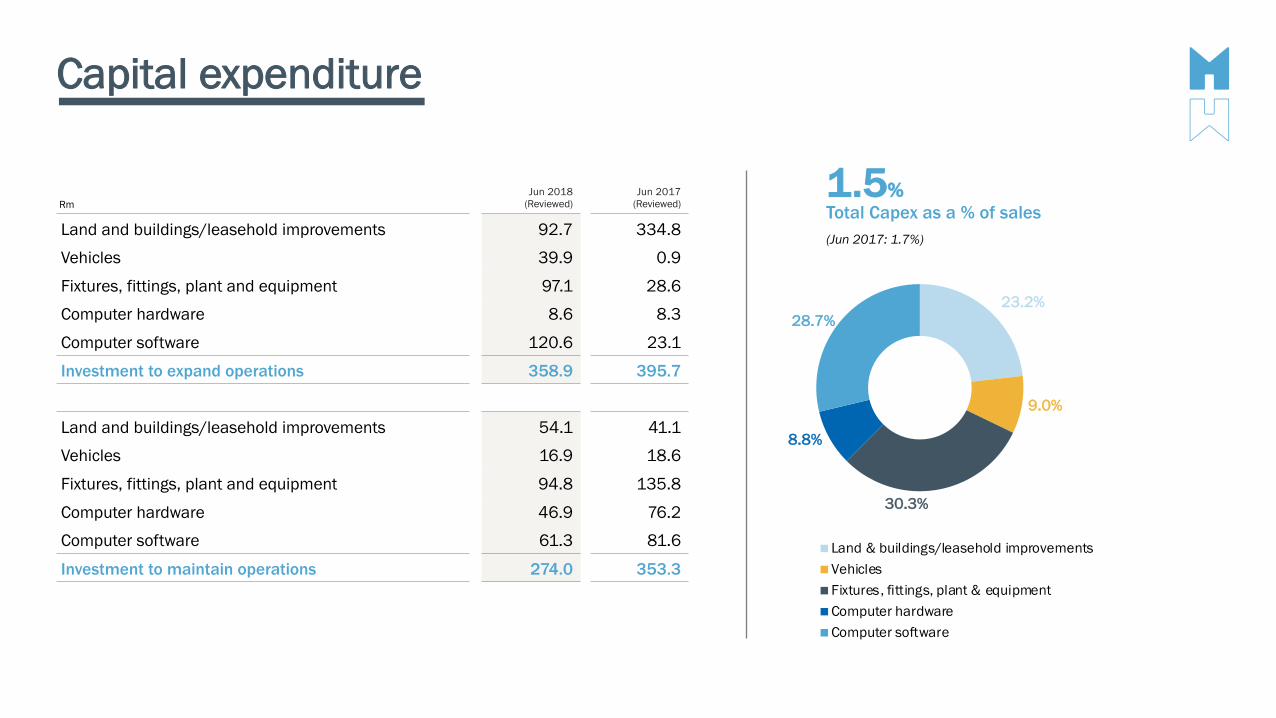

Capital expenditure

RmJun 2018

(Reviewed)Jun 2017

(Reviewed)

Land and buildings/leasehold improvements 92.7 334.8

Vehicles 39.9 0.9

Fixtures, fittings, plant and equipment 97.1 28.6

Computer hardware 8.6 8.3

Computer software 120.6 23.1

Investment to expand operations 358.9 395.7

Land and buildings/leasehold improvements 54.1 41.1

Vehicles 16.9 18.6

Fixtures, fittings, plant and equipment 94.8 135.8

Computer hardware 46.9 76.2

Computer software 61.3 81.6

Investment to maintain operations 274.0 353.3

23.2%

9.0%

30.3%

8.8%

28.7%

Land & buildings/leasehold improvementsVehiclesFixtures, fittings, plant & equipmentComputer hardwareComputer software

Total Capex as a % of sales(Jun 2017: 1.7%)

1.5%

Store portfolio

Total Massdiscounters Masswarehouse Massbuild Masscash

425 164 21 110 130Up from 423 in Dec 2017

Down from 166 in Dec 2017

21 in Dec 2017 Up from 108 In Dec 2017

Up from 128 in Dec 2017

+5-3

OpenedClosed

-2 DionWired-2 in South Africa

+3 Builders Express+2 in South Africa+1 in Mozambique

+2 Retail+2 in South Africa

-1 Builders Trade Depot-1 South Africa

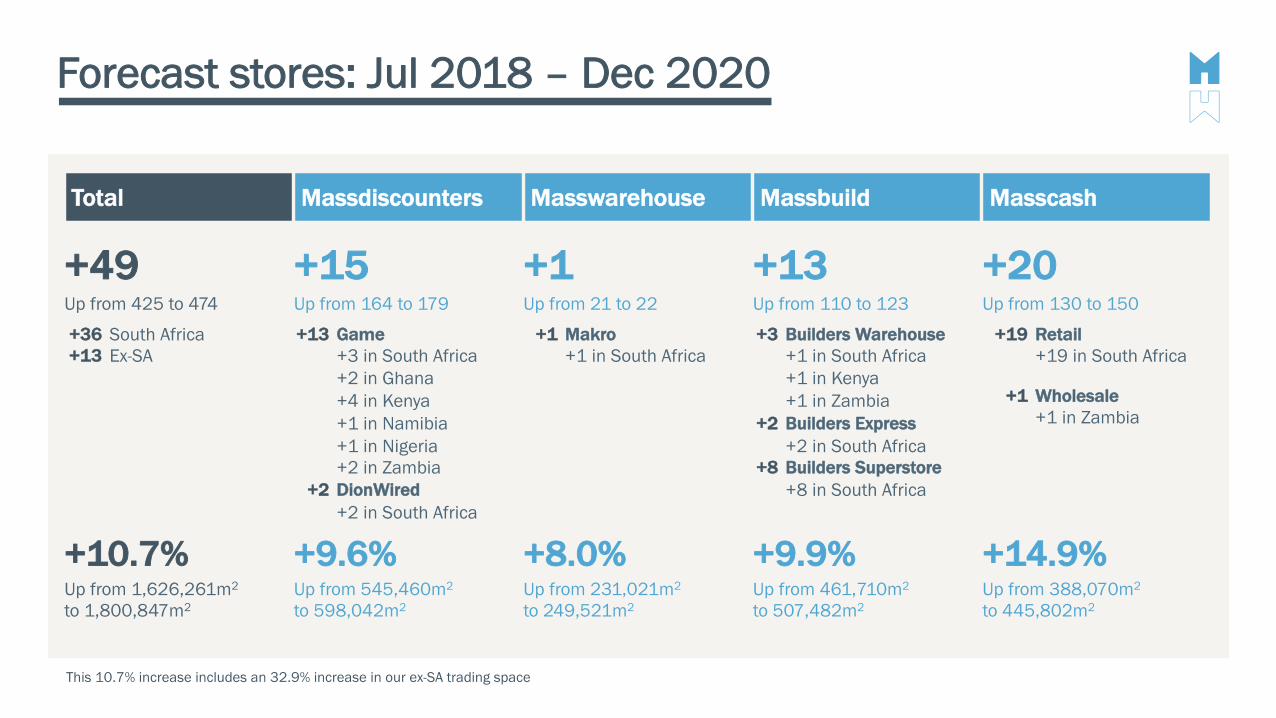

Forecast stores: Jul 2018 – Dec 2020

This 10.7% increase includes an 32.9% increase in our ex-SA trading space

Total Massdiscounters Masswarehouse Massbuild Masscash

+49 +15 +1 +13 +20Up from 425 to 474 Up from 164 to 179 Up from 21 to 22 Up from 110 to 123 Up from 130 to 150

+36 +13

South AfricaEx-SA

+13

+2

Game+3 in South Africa+2 in Ghana+4 in Kenya+1 in Namibia+1 in Nigeria+2 in ZambiaDionWired+2 in South Africa

+1 Makro+1 in South Africa

+3

+2

+8

Builders Warehouse+1 in South Africa+1 in Kenya+1 in ZambiaBuilders Express+2 in South AfricaBuilders Superstore+8 in South Africa

+19 Retail+19 in South Africa

+10.7% +9.6% +8.0% +9.9% +14.9%Up from 1,626,261m2

to 1,800,847m2Up from 545,460m2

to 598,042m2Up from 231,021m2

to 249,521m2Up from 461,710m2

to 507,482m2Up from 388,070m2

to 445,802m2

+1 Wholesale+1 in Zambia

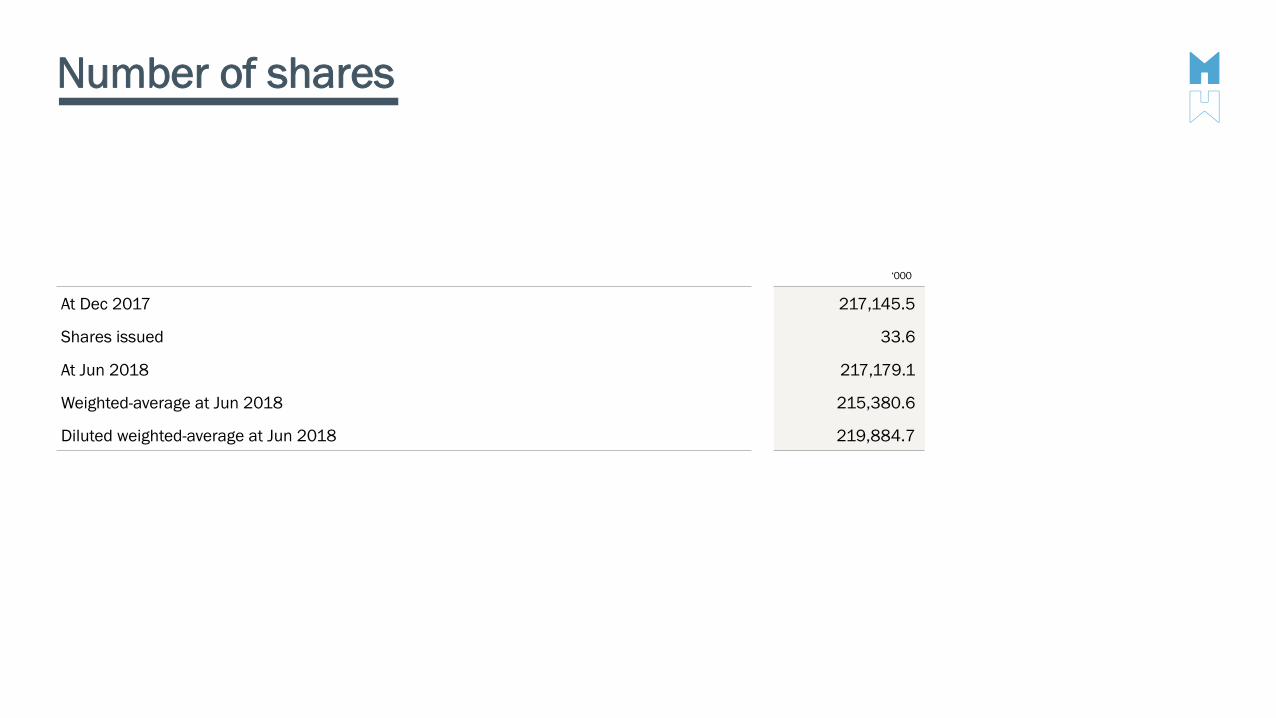

Number of shares

‘000

At Dec 2017 217,145.5

Shares issued 33.6

At Jun 2018 217,179.1

Weighted-average at Jun 2018 215,380.6

Diluted weighted-average at Jun 2018 219,884.7