Embed Size (px)

Citation preview

Risk and regulation in a digitalised worldA survey for UK asset managers

March 2017

Contents

Introduction and executive summary

1

Top motivators for the risk and compliance functions

3

Legal risk, strategy risk and technology risk trended strongly compared with 2015

5

Survey findings 7

1 Risk and regulation in a digitalised world A survey for UK asset managers

Introduction and executive summary

EY Risk and Regulation in a Digitalised World survey offers a revealing insight into the unique set of challenges confronting our industry’s risk and other control function professionals. In comparing the views of 42 chief risk officers, heads of operational risk and chief compliance officers from some of the most recognised asset managers servicing the needs of European investors, we can draw valuable conclusions from how asset managers of different styles and sizes are coping with the prospect of managing risks and complying with multiple regulations across the financial industry.

This year’s survey – the eighth in the series – took place in an environment of greater political uncertainty, lower yields and a tectonic drive towards digitalisation. Boards and C-suite functions (chief executive officers (CEOs), chief financial officers (CFOs), chief operating officers (COOs), chief technology officers (CTOs), chief risk officers (CROs) and chief compliance officers CCOs)) were factoring in the ramifications of managing increasing complexity from cross-regulatory measures, the financial impacts on the balance sheet and (given several high-profile process failures during 2015) the need for business resilience.

The need to manage both strategy and, particularly, legal risk was back on the agenda for CROs and CCOs to a degree not witnessed since the financial crisis. Private debt, alternative solutions investing and private markets (featuring private equity (PE), real estate and infrastructure funds) proved popular with investors looking for returns in a low-yield environment. The focus on fees and charges by regulators, liquidity risks from redemptions and capital retractions by the banks, plus the entrance of new models in the FinTech space (the cloud, robo-advice or selection and blockchain) were all significant departure points from last year’s survey. There was also a new theme in 2016 – how to design the ‘front office of the future’.

Perhaps strangely, firms were adapting to the pace and complexity of regulations this year, as a greater proportion of non-discretionary spend was dedicated to that sector. A mid-tier asset manager could expect to spend anything from £5 to £15 million over the course of 2016 to 2018 in order to prepare for, and comply with, the revised Markets in Financial Instruments Directive (MiFID II) alone, for example. Factoring in the simultaneous regulatory measures from the Market Abuse Regulation (MAR), the Securities Financing Transaction Regulation (SFTR), the Packaged Retail and Insurance-based Investment Products (PRIIPs) regulation and the fourth Anti-Money Laundering Directive (AMLD IV) could easily see the total exceed £20 million over a four-year horizon.

2Introduction and executive summary

This does not include the considerable dislocation expected under the General Data Protection Regulation (GDPR) and the arrival of new technical regulations in the FinTech space. Meanwhile, any firms hoping for respite following the UK’s referendum vote on 23 June 2016 were disappointed – there was still going to be a recalibration to cater for UK market needs while the industry awaited greater clarity on whether Brexit would be ‘hard’ (ie, potentially triggering major changes) or ‘soft’.

Some key themes from 2015 still remain. Asset managers continued to undergo transformational change from the perspectives of regulation, tax changes, customer interaction, distribution economics, attention to governance, stewardship and shareholders, technology provision, competition for talent and societal expectations. Fifty-four percent of respondents were taking initial steps to link the management of (mis)conduct risk with the UK’s individual accountability regime (the Senior Managers Regime), even though the latter is likely to take effect during H1 2018.

Regulators were also placing a greater burden of proof – investor protection, conduct, best execution, disclosure and reporting – squarely on the asset manager, irrespective of whether firms chose to outsource or not. It was also partly down to a focus on the personal – whether control function, material risk taker, portfolio manager or trader. The accumulation of personal data was beginning to cause some firms to wonder at the amount of work to be done when complying with the GDPR to come.

The survey also recorded several new developments compared with last year:

1) Regulatory capital and operational resilience – several asset managers posted off-the-scale Internal Capital Adequacy Assessment Process – Individual Capital Guidance (ICAAP ICG) scores during 2015. This trend continued into 2016 and was accompanied by a focus on balance sheet capital to cover liquidity risk, particularly for bank-owned asset managers. ICG scores in excess of 200% were no longer uncommon. Nor were moves to link regulatory capital allocations to misconduct risk. Firms were generally more prepared to deal with the sorts of system outages witnessed during March, April and August 2015 to avoid being awarded higher-than-average ICG scores. Attention moved to ‘cyber resilience’ as a critical hygiene factor, with focus on examples of malware installations, ransomware demands or computer network attacks (CNAs) and espionage. Given the need for extensive reporting requirements (eg, client, trade, transaction and best execution reporting needed under MiFID II), attention to market, reference and metadata was a consistent theme.

2) Liquidity in the market – this was a prevalent theme all year, partly due to the extension of quantitative easing (QE) and a move into a negative interest rate environment in some countries, but also as a result of redemptions and gates in non-equities (particularly real estate markets) plus extensive liquidity retraction due to fewer banks being able or willing to hold inventory. The root causes may be associated with Capital Requirements Directive (CRD) IV’s liquidity coverage ratio (LCR) and net stable funding ratio (NSFR), as well as capital retraction anticipated in complying with the fundamental review of the trading book (FRTB). The net result for many asset managers using derivatives (eg, liability-driven investing firms) or hedging as part of an investment strategy was fewer sell-side firms prepared to quote in size, or maintain large ranges or tenors in bonds or over-the-counter (OTC) traded derivatives respectively.

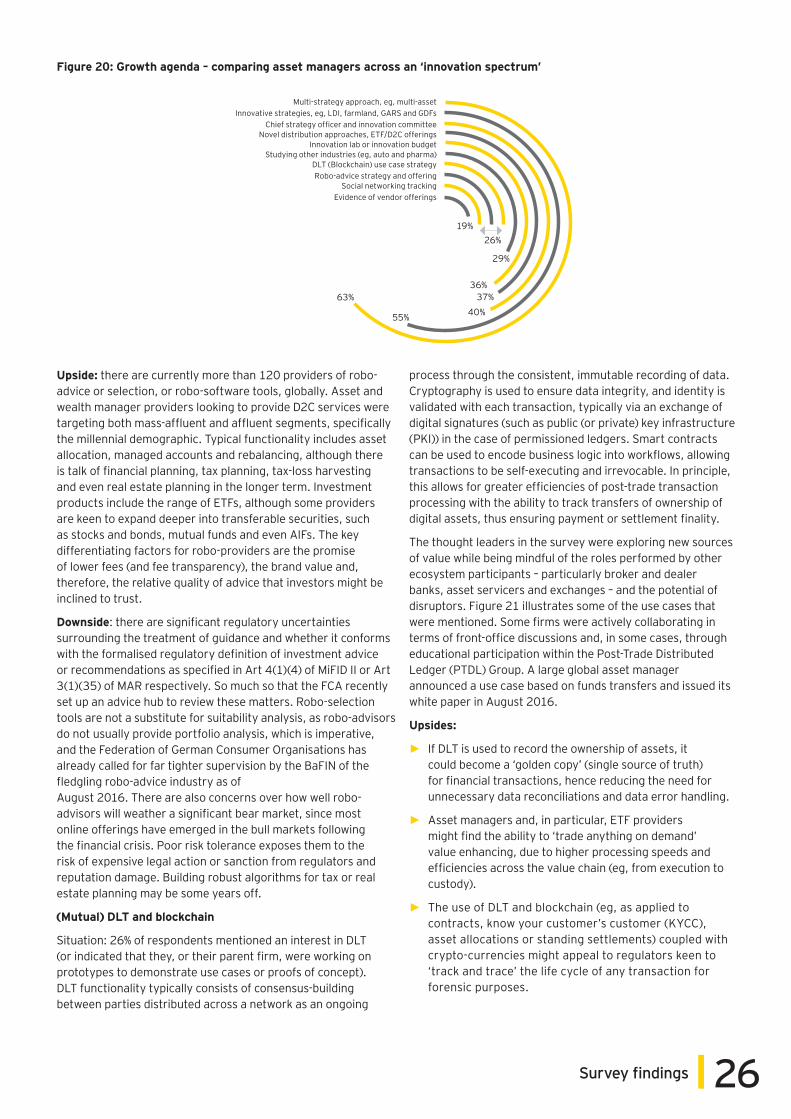

3) FinTech and the ‘growth’ agenda – the need to manage complexity and simplify was a continuing trend, particularly for bank- and insurance-owned asset managers looking to manage their cost or income ratios downwards in the face of several change features. Several firms were continuing their innovation strategies. The prevalence of new approaches in the digital, robotics, robo-advice and selection, and distributed ledger technology (DLT) or blockchain spaces indicated a ready and vibrant desire to develop simpler digitalised models able to improve client coupling and lower the future cost of regulatory compliance.

It is clear that the role of the risk and compliance professionals has never been more in demand, yet some businesses were challenged to maintain headcount in order to cope with the complexities facing the function. In this fluid environment, we believe that traditional and alternative asset managers derive enormous value from tracking peer progress and giving careful thought to what lies on their early warning ‘risk radars’ over the coming year.

This year’s survey featured one-on-one interviews with CROs, heads of operational risk and heads of compliance or CCOs, conducted between January and September 2016, giving respondents the scope to anonymously share candid opinions. Critical conclusions are featured in the comparison template at the end of this section for reference by CROs, CCOs and seniors from the board or the business. The composition of interviewees represented the customary selection of large (top 20), medium-sized and several alternative investment management firms (by assets under management (AuM)). As ever, we are grateful to them for their patience and considerable support in this endeavour.

3 Risk and regulation in a digitalised world A survey for UK asset managers

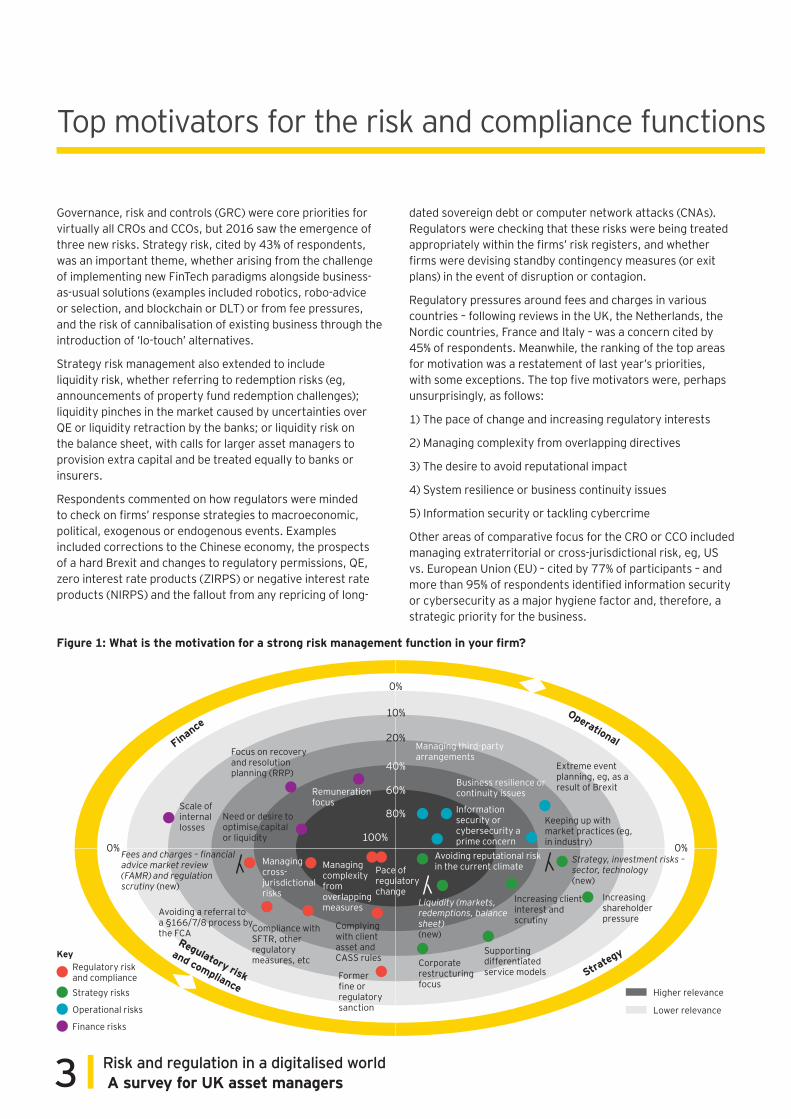

Top motivators for the risk and compliance functions

Governance, risk and controls (GRC) were core priorities for virtually all CROs and CCOs, but 2016 saw the emergence of three new risks. Strategy risk, cited by 43% of respondents, was an important theme, whether arising from the challenge of implementing new FinTech paradigms alongside business-as-usual solutions (examples included robotics, robo-advice or selection, and blockchain or DLT) or from fee pressures, and the risk of cannibalisation of existing business through the introduction of ‘lo-touch’ alternatives.

Strategy risk management also extended to include liquidity risk, whether referring to redemption risks (eg, announcements of property fund redemption challenges); liquidity pinches in the market caused by uncertainties over QE or liquidity retraction by the banks; or liquidity risk on the balance sheet, with calls for larger asset managers to provision extra capital and be treated equally to banks or insurers.

Respondents commented on how regulators were minded to check on firms’ response strategies to macroeconomic, political, exogenous or endogenous events. Examples included corrections to the Chinese economy, the prospects of a hard Brexit and changes to regulatory permissions, QE, zero interest rate products (ZIRPS) or negative interest rate products (NIRPS) and the fallout from any repricing of long-

dated sovereign debt or computer network attacks (CNAs). Regulators were checking that these risks were being treated appropriately within the firms’ risk registers, and whether firms were devising standby contingency measures (or exit plans) in the event of disruption or contagion.

Regulatory pressures around fees and charges in various countries – following reviews in the UK, the Netherlands, the Nordic countries, France and Italy – was a concern cited by 45% of respondents. Meanwhile, the ranking of the top areas for motivation was a restatement of last year’s priorities, with some exceptions. The top five motivators were, perhaps unsurprisingly, as follows:

1) The pace of change and increasing regulatory interests

2) Managing complexity from overlapping directives

3) The desire to avoid reputational impact

4) System resilience or business continuity issues

5) Information security or tackling cybercrime

Other areas of comparative focus for the CRO or CCO included managing extraterritorial or cross-jurisdictional risk, eg, US vs. European Union (EU) – cited by 77% of participants – and more than 95% of respondents identified information security or cybersecurity as a major hygiene factor and, therefore, a strategic priority for the business.

Figure 1: What is the motivation for a strong risk management function in your firm?

0%100%

80%

0%

10%

20%

40%

60%

0%

FinanceOperational

Regulatory risk

and complianceStra

tegy

Scale of internal losses

Focus on recovery and resolution planning (RRP)

Remuneration focus

Fees and charges – financial advice market review (FAMR) and regulation scrutiny (new)

Avoiding a referral to a §166/7/8 process by the FCA Compliance with

SFTR, other regulatory measures, etc

Former fine or regulatory sanction

Complying with client asset and CASS rules

Managing cross- jurisdictional risks

Managing complexity from overlapping measures

Pace of regulatory change

Need or desire to optimise capital or liquidity

Managing third-party arrangements

Business resilience or continuity issues

Information security or cybersecurity a prime concern

Keeping up with market practices (eg, in industry)

Extreme event planning, eg, as a result of Brexit

Avoiding reputational risk in the current climate

Liquidity (markets, redemptions, balance sheet) (new)

Corporate restructuring focus

Supporting differentiated service models

Increasing client interest and scrutiny

Strategy, investment risks – sector, technology (new)

Increasing shareholder pressure

KeyRegulatory risk and complianceStrategy risks

Operational risks

Finance risks

Higher relevance

Lower relevance

4Top motivators for the risk and compliance functions

5 Risk and regulation in a digitalised world A survey for UK asset managers

Legal risk, strategy risk and technology risk trended strongly compared with 2015

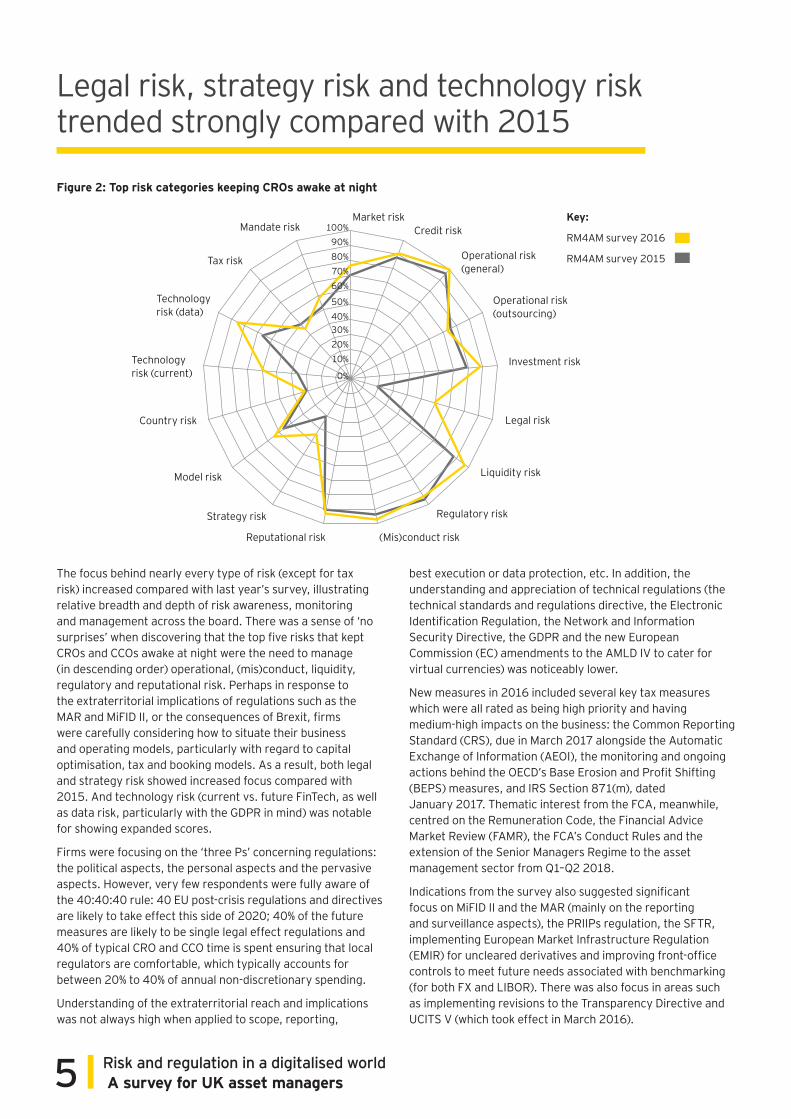

The focus behind nearly every type of risk (except for tax risk) increased compared with last year’s survey, illustrating relative breadth and depth of risk awareness, monitoring and management across the board. There was a sense of ‘no surprises’ when discovering that the top five risks that kept CROs and CCOs awake at night were the need to manage (in descending order) operational, (mis)conduct, liquidity, regulatory and reputational risk. Perhaps in response to the extraterritorial implications of regulations such as the MAR and MiFID II, or the consequences of Brexit, firms were carefully considering how to situate their business and operating models, particularly with regard to capital optimisation, tax and booking models. As a result, both legal and strategy risk showed increased focus compared with 2015. And technology risk (current vs. future FinTech, as well as data risk, particularly with the GDPR in mind) was notable for showing expanded scores.

Firms were focusing on the ‘three Ps’ concerning regulations: the political aspects, the personal aspects and the pervasive aspects. However, very few respondents were fully aware of the 40:40:40 rule: 40 EU post-crisis regulations and directives are likely to take effect this side of 2020; 40% of the future measures are likely to be single legal effect regulations and 40% of typical CRO and CCO time is spent ensuring that local regulators are comfortable, which typically accounts for between 20% to 40% of annual non-discretionary spending.

Understanding of the extraterritorial reach and implications was not always high when applied to scope, reporting,

best execution or data protection, etc. In addition, the understanding and appreciation of technical regulations (the technical standards and regulations directive, the Electronic Identification Regulation, the Network and Information Security Directive, the GDPR and the new European Commission (EC) amendments to the AMLD IV to cater for virtual currencies) was noticeably lower.

New measures in 2016 included several key tax measures which were all rated as being high priority and having medium-high impacts on the business: the Common Reporting Standard (CRS), due in March 2017 alongside the Automatic Exchange of Information (AEOI), the monitoring and ongoing actions behind the OECD’s Base Erosion and Profit Shifting (BEPS) measures, and IRS Section 871(m), dated January 2017. Thematic interest from the FCA, meanwhile, centred on the Remuneration Code, the Financial Advice Market Review (FAMR), the FCA’s Conduct Rules and the extension of the Senior Managers Regime to the asset management sector from Q1–Q2 2018.

Indications from the survey also suggested significant focus on MiFID II and the MAR (mainly on the reporting and surveillance aspects), the PRIIPs regulation, the SFTR, implementing European Market Infrastructure Regulation (EMIR) for uncleared derivatives and improving front-office controls to meet future needs associated with benchmarking (for both FX and LIBOR). There was also focus in areas such as implementing revisions to the Transparency Directive and UCITS V (which took effect in March 2016).

Figure 2: Top risk categories keeping CROs awake at night

100%90%80%70%60%

50%40%30%20%10%

0%

Market riskCredit risk

Operational risk (general)

Operational risk (outsourcing)

Investment risk

Legal risk

Liquidity risk

Regulatory risk

(Mis)conduct riskReputational risk

Strategy risk

Model risk

Country risk

Technology risk (current)

Technology risk (data)

Tax risk

Mandate risk Key:

RM4AM survey 2016

RM4AM survey 2015

6Legal risk, strategy risk and technology risk trended strongly compared with 2015

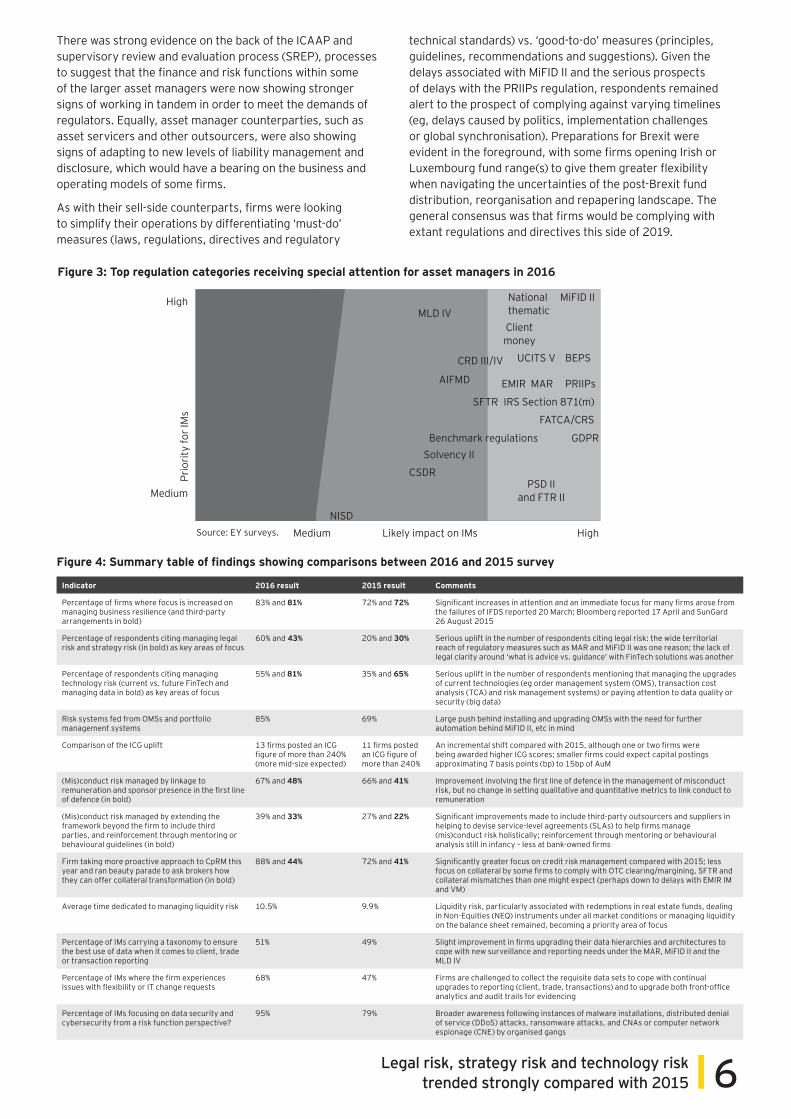

There was strong evidence on the back of the ICAAP and supervisory review and evaluation process (SREP), processes to suggest that the finance and risk functions within some of the larger asset managers were now showing stronger signs of working in tandem in order to meet the demands of regulators. Equally, asset manager counterparties, such as asset servicers and other outsourcers, were also showing signs of adapting to new levels of liability management and disclosure, which would have a bearing on the business and operating models of some firms.

As with their sell-side counterparts, firms were looking to simplify their operations by differentiating ‘must-do’ measures (laws, regulations, directives and regulatory

technical standards) vs. ‘good-to-do’ measures (principles, guidelines, recommendations and suggestions). Given the delays associated with MiFID II and the serious prospects of delays with the PRIIPs regulation, respondents remained alert to the prospect of complying against varying timelines (eg, delays caused by politics, implementation challenges or global synchronisation). Preparations for Brexit were evident in the foreground, with some firms opening Irish or Luxembourg fund range(s) to give them greater flexibility when navigating the uncertainties of the post-Brexit fund distribution, reorganisation and repapering landscape. The general consensus was that firms would be complying with extant regulations and directives this side of 2019.

Figure 3: Top regulation categories receiving special attention for asset managers in 2016

Figure 4: Summary table of findings showing comparisons between 2016 and 2015 survey

High

Medium

Prio

rity

for I

Ms

Source: EY surveys. Medium Likely impact on IMs HighNISD

CSDR

Solvency II

PSD II and FTR II

GDPR

MLD IV

AIFMD

CRD III/IV UCITS V

National thematicClient money

EMIR MAR

SFTR IRS Section 871(m)

PRIIPs

BEPS

MiFID II

FATCA/CRS

Benchmark regulations

Indicator 2016 result 2015 result Comments

Percentage of firms where focus is increased on managing business resilience (and third-party arrangements in bold)

83% and 81% 72% and 72% Significant increases in attention and an immediate focus for many firms arose from the failures of IFDS reported 20 March; Bloomberg reported 17 April and SunGard 26 August 2015

Percentage of respondents citing managing legal risk and strategy risk (in bold) as key areas of focus

60% and 43% 20% and 30% Serious uplift in the number of respondents citing legal risk: the wide territorial reach of regulatory measures such as MAR and MiFID II was one reason; the lack of legal clarity around ‘what is advice vs. guidance’ with FinTech solutions was another

Percentage of respondents citing managing technology risk (current vs. future FinTech and managing data in bold) as key areas of focus

55% and 81% 35% and 65% Serious uplift in the number of respondents mentioning that managing the upgrades of current technologies (eg order management system (OMS), transaction cost analysis (TCA) and risk management systems) or paying attention to data quality or security (big data)

Risk systems fed from OMSs and portfolio management systems

85% 69% Large push behind installing and upgrading OMSs with the need for further automation behind MiFID II, etc in mind

Comparison of the ICG uplift 13 firms posted an ICG figure of more than 240% (more mid-size expected)

11 firms posted an ICG figure of more than 240%

An incremental shift compared with 2015, although one or two firms were being awarded higher ICG scores; smaller firms could expect capital postings approximating 7 basis points (bp) to 15bp of AuM

(Mis)conduct risk managed by linkage to remuneration and sponsor presence in the first line of defence (in bold)

67% and 48% 66% and 41% Improvement involving the first line of defence in the management of misconduct risk, but no change in setting qualitative and quantitative metrics to link conduct to remuneration

(Mis)conduct risk managed by extending the framework beyond the firm to include third parties, and reinforcement through mentoring or behavioural guidelines (in bold)

39% and 33% 27% and 22% Significant improvements made to include third-party outsourcers and suppliers in helping to devise service-level agreements (SLAs) to help firms manage (mis)conduct risk holistically; reinforcement through mentoring or behavioural analysis still in infancy – less at bank-owned firms

Firm taking more proactive approach to CpRM this year and ran beauty parade to ask brokers how they can offer collateral transformation (in bold)

88% and 44% 72% and 41% Significantly greater focus on credit risk management compared with 2015; less focus on collateral by some firms to comply with OTC clearing/margining, SFTR and collateral mismatches than one might expect (perhaps down to delays with EMIR IM and VM)

Average time dedicated to managing liquidity risk 10.5% 9.9% Liquidity risk, particularly associated with redemptions in real estate funds, dealing in Non-Equities (NEQ) instruments under all market conditions or managing liquidity on the balance sheet remained, becoming a priority area of focus

Percentage of IMs carrying a taxonomy to ensure the best use of data when it comes to client, trade or transaction reporting

51% 49% Slight improvement in firms upgrading their data hierarchies and architectures to cope with new surveillance and reporting needs under the MAR, MiFID II and the MLD IV

Percentage of IMs where the firm experiences issues with flexibility or IT change requests

68% 47% Firms are challenged to collect the requisite data sets to cope with continual upgrades to reporting (client, trade, transactions) and to upgrade both front-office analytics and audit trails for evidencing

Percentage of IMs focusing on data security and cybersecurity from a risk function perspective?

95% 79% Broader awareness following instances of malware installations, distributed denial of service (DDoS) attacks, ransomware attacks, and CNAs or computer network espionage (CNE) by organised gangs

7 Risk and regulation in a digitalised world A survey for UK asset managers

Regulatory capital and operational resilienceCapital provision remained a focus in this year’s survey, against a backdrop of the financial stability board (FSB) and regulators paying greater attention to asset managers’ balance sheets in an attempt to reduce systemic risks (by ensuring that fund houses carry enough capital to weather stressed markets or operational conditions). Bank-owned asset managers were also spooked by a proposal from the Basel Committee on Banking Supervision (BCBS) issued in April 2016, suggesting that their parent entities hold extra capital in case their fund management operations are hit in a crisis. The BCBS proposed that these banks post additional Pillar I capital worth 1% of their fund arms’ entire AuM (not merely the money market fund component) against ‘step-in’ risk. Some respondents expressed concerns that the additional capital requirements and operational costs for banks could eventually make some forms of asset management less attractive, and might even force large banks out of running asset management divisions.

Comments from respondents were divided on whether their firm was due to receive a visit from the regulator as part of their ICAAP and SREP. Firms that were not due to be visited were understandably more relaxed and were contemplating target figures for ICG uplift (vs. Pillar I or Pillar II capital, depending on the span of the risks they wished to cover). Coverage for liquidity risk was a consistent and critical theme, whether arising to cover redemptions (in sectors such as real estate or money market funds) or to respond to regulators querying whether firms had sufficient capital provisioned on the balance sheet for larger firms.

A handful of asset managers saw their ICG scores rise by more than 30% in relative terms to join those who had posted off-the-scale ICAAP ICG scores during the 2013 to 2015 assessment window (see Figure 5). Thirteen firms posted comparative ICG scores in excess of 200, commenting on the varied and occasionally intrusive regulatory processes by teams from the FCA. The regulator remained keen on firms showing clearer and cleaner workings and demonstrating their awareness of culture elements – carrying out conduct risk refreshes or reinforcements biannually, for example.

There was a clear expectation that boards and CEOs would be expected to provide more concrete sponsorship in the form of a ‘tone from the top’ and play a greater role in overseeing the maintenance of the three lines of defence 3LoD approach in practice. A minority of firms complained that the 3LoD approach was no longer suitable to support GRC at their firm, and refinements (such as creating 1.5LoD or 2.5LoD sub-functions) were needed in practice.

The challenge by the FCA covered various areas of perennial interest: the proper articulation of the firm’s risk appetite, the applicability and effectiveness of ‘use’ tests and, finally, more quantitative questioning surrounding the assessments of market, credit and operational risk (OR) as line items. Respondents expected that the FCA would focus not only on the robustness of the OR framework but also on core competencies of the CRO and risk teams, as well as the CFO and finance teams. The sense was that smaller firms were being reviewed thematically on longer cycles, with a handful applying a capital calculation based on 7bp to 15bp of UK-administered AuM in order to arrive at an upper limit for capital provision.

Survey findings

Business and operational resilienceThe business resilience and business continuity procedures around systemically important providers were all important in view of 2015’s reported outages of critical suppliers in March, April and August respectively. The emphasis in 2016 shifted to order management system (OMS) and execution management system (EMS) providers, and other business-critical applications. The resilience of business systems and the operating model dependencies – for outsourcing providers, vendors or clearing houses – remained top of mind among CROs.

This year’s survey showed that 83% of asset managers (compared with 76% in 2015) felt that business continuity or system resilience was an issue for the 2LoD. The common concern centred on what might happen if a service provider (such as a fund administrator or material outsource provider with a large share of the market) faced severe operational disruption, financial distress or default. Would asset managers be able to perform critical and important regulated activities and, if not, would this result in creating detriment for end investors?

Firms could agree on the questions to ask, but not the concrete answers, because they had yet to:

i) Model the implications fully when operating under protracted stressed market conditions

ii) Reach full consensus over contingency planning (such as ‘switching arrangements’, ‘step-in rights’, ‘standby’, ‘warm second provider’ or ‘exit’ arrangements) in the event of an agent hitting financial problems

iii) Evaluate and price the liability arrangements to cover cases of fraud or insolvency of any end agents, such as sub-custodians or depositories (see (c) on the next page)

8Survey findings

Figure 6: Qualitative factors corresponding with higher-than-expected ICG scores

Figure 5: Comparison of known relative ICG uplifts (data drawn from 2013–16)

Unexpected score

Expected score

100 110 120 130 140 150 160 170 180 190 200 210 220 230 240 250 300 400 500

Relative % ICG upliftKey:

Small and medium-sized entities

Complex or illiquid products

Large entities

Strong distribution dependency

Strong brand

M&A candidate

Retail footprint

Black box methodology or valuations

The new ‘normal’

Bifurcation

Failing to complete the appropriate paperwork in a consistent manner or file it on time

Failing to educate CFO colleagues and finance teams on how to communicate risk scoring and mitigation plans to the regulator when called to do so

Mentioned most frequently by respondents

Key to ICG influencing factors:

Mentioned least frequently by respondents

Failing to model emerging risks driven by events accelerating or deteriorating trends, or changes driven by projects or processes

Failing to consider or communicate any limitations with the OR modelling to ensure that they were fully understood by the management team

Failing to provide evidence of risk assessments or key risk scenarios (KRSs) devised by the business, demonstrate involvement of the 1LoD with the risk and control self assessment (RCSA) and future scenario workshops or effective use of the ICAAP in business decision-making

Failing to model ‘combined scenario’ events (eg, dealing or corporate action error coupled with market downturn) to link loss events to risks effectively or to pinpoint other casualties

Failing to demonstrate sufficiently robust risk governance (eg, failure to minute management or board meetings, to field a level of independent challenge or to identify possible conflicts of interest)

Failing to provide evidence and failing to demonstrate a strong risk culture through effective risk appetite statements (supported by sufficient KRSs) or ‘stress tests’

Firms failing to demonstrate robust resilience and business continuity procedures – eg, management oversight, back-up, standby or step-in arrangements or exit planning procedures – around systematically important providers such as data vendors, system providers or asset servicing agents

Failing to demonstrate robustness around managing liquidity risk for the investment funds (eg, individual line items quantifying risks) and firms unable to demonstrate proper segregation procedures for client assets and client monies (eg, with CASS rules, EMIR or UCITS V in mind)

Failure to model the effect of reputational scandals, eg, miss-selling of products, miss-pricing of products, loss of founder or portfolio manager desk heads or star fund managers, major fraud scenario or cyber intrusions across the attack surface

9 Risk and regulation in a digitalised world A survey for UK asset managers

Board and senior management sponsorship

Importance of the OR appetite

In-house challenge and validationUse tests fully applied

Dynamic modelling approach (sensitivity analysis for all assets)

Strategic objectives

Business initiatives

OR foundations Guiding principles, strategy, governance, appetite, GRC structure and glossary

Risk identification and assessment

Risk monitoring Risk measurement

Risk reportingRegulatory and economic capital

Third-party substantiation

RCSA Scenario analysis

KRIsLoss data

Key | Demonstrated by most firms: Some firms: Few firms:

Technology

Number of operational incidents in 2015

Ann

ualis

ed im

plie

d lo

ss v

alue

(inc

ludi

ng in

cide

nts

reso

lved

in

the

clie

nts’

favo

ur) i

n U

S$ ‘0

00

Losses against the firm only

Includes corrections and breaks

Includes near misses

Includes gains in clients’ favour

500 1,000 1,500

1,000

0

2,000

3,000

4,000

5,000

6,000

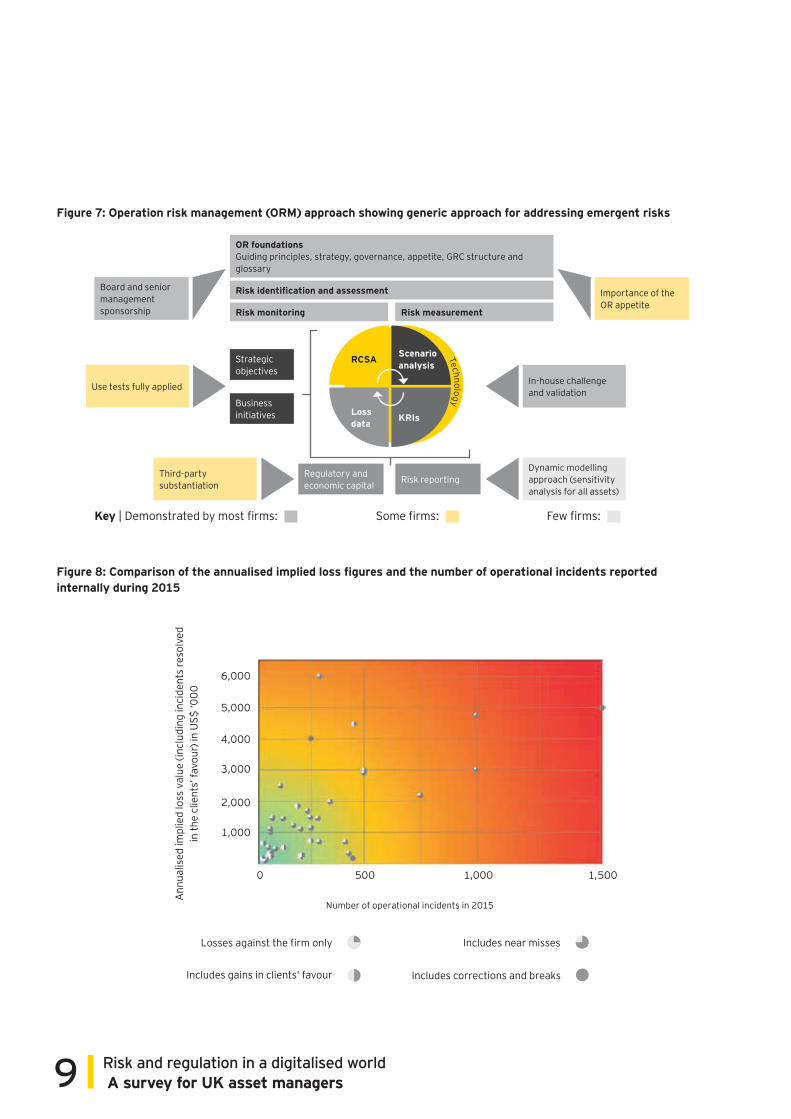

Figure 7: Operation risk management (ORM) approach showing generic approach for addressing emergent risks

Figure 8: Comparison of the annualised implied loss figures and the number of operational incidents reported internally during 2015

10Survey findings

Better news was that more firms are aware of key product and solution dependencies on third-party vendors such as OMS providers, or third-party service providers such as fund administrators or financial market infrastructures (eg, exchanges and central counterparty clearers). There was even more progress, with respondents:

a) Generally agreeing the definitions and materiality of critical operational functions and investment services and activities

b) Revalidating that they were able to monitor and manage the effectiveness of functions carried out against granular SLAs

c) Ensuring that settlement agents were in a position to offer upstream clients the choice between omnibus and individual client segregation, with information as to the costs and risks associated with each option (eg as per CSDR Art. 38(5) and (6) in EU/European economic area (EEA) countries) relating to insolvency law and procedures, recoverability of assets and indemnification in each jurisdiction

d) Cataloguing the KRIs for external and internal SLAs effectively, particularly in the case of service provision or outsourcing from third countries

e) Ensuring that catalogues and KRSs feature procedures for engaging with competent authorities in third countries

Eighty-one percent of respondents had already raised expectations and devised granular contingency plans based upon SLAs which they felt to be proactive, robust and realistic in the event of a termination of third-party activity under any circumstances, particularly under stressed market conditions or cyber attacks (see Figure 7). Developing a separate OR appetite remained a challenge for smaller entities, such as hedge funds. Many firms had made good progress in embedding their OR frameworks into the business, with a range of metrics being used to express the appetite (including expanding the range of anything from 40 to 120 KRIs and modelling loss values or capital provisions). The leading firms validated their OR frameworks using techniques including internal audit reviews, commissioning external reviews or remediating following regulatory reviews. Often, central risk units at the smaller firms were not able to rely entirely on independent verification, such as internal audit or review by external auditors, to meet this constant requirement, so looked to develop more continuous validation processes.

Other characteristics evident in this year’s survey were as follows:

► ►Improved coupling of loss events with root cause analysis, particularly for cyber or digital risks – the improvement in 2016 was noted in modelling the consequences of cyber attacks or the reputational consequences of mismanagement of digital risk. Not all firms linked loss events to root cause analysis to determine, for example, whether an impact represented an expected, a severe or a worst-case instance of the risk (and, for firms operating under comfort zone thresholds, whether any of the graphs on the previous page could be causally linked to the firm’s stated risk appetite), linking indicators such as deteriorating KRIs (or combinations thereof) to specific KRSs.

► ►OR system configurability – the focus on controls and their design or operating effectiveness was evident, particularly concerning front-office controls. However, a newer trend was firms choosing vendor solutions whose parameters and workflows could be self-configured by the 2LoD. The focus was on simplification and keeping costs down (reduced licence and maintenance fees, better optionality, exploring hosted solutions or relying on local processing). This was particularly notable in the case of firms selecting trade surveillance tools.

At least four different categories were recorded in terms of risk impact (eg, the direct cost impacts of client compensation or regulatory risk, or of the loss of revenue or redemptions impacting the AuM arising from reputational risk):

► ►Operational incidents or errors resulting in loss events against the firm

► ►Unintended gains or incidents resulting in the proceeds being awarded in the clients’ favour

► ►Qualified near-misses arising from errors and omissions

► ►False positives or situations arising from mistranscribing dealing tickets or operational breaks, failures or overdrafts which were corrected or remediated before they qualified as incidents such as the graph on the previous page

The survey noted even greater precision and granularity when benchmarking the financial impacts of operational incidents reported internally compared with last year’s survey. Some firms posted relatively constrained loss figures of less than US$250,000 during 2015 (see Figure 8) and adopted sophisticated techniques to time-average large loss events arising from incorrect client order processing, dealing errors, or the processing of corporate actions or rights issues. Firms that studiously retained data on unintended gains and

11 Risk and regulation in a digitalised world A survey for UK asset managers

qualified near misses were particularly interested in studying how other firms annualised their loss values – whether over a three- or five-year cycle – and whether peers were formalising a total loss value figure as a target ceiling.

Data sets that could be treated as loss events affecting the business vs. ‘inadvertent’ (consequences of force majeure or market movements). Leading firms provided overlays to differentiate positive impacts for clients vs. neutral or negative impacts. Annualised loss figures for smaller entities were comparable with last year’s data: more firms were counting near misses this year, and the annualised loss figures showed increases for several mid- to large-sized firms when comparing 2015 data with 2014 data.

Market liquidity risk and front-office controlsThe prime area of risk and regulatory focus for asset managers this year was the front office. More asset managers than ever before were focusing on how MiFID II would affect their dealing arrangements (eg, use of telephone trading, lo-touch channels to market such as direct electronic access (DEA), automated order routing (AOR) or smart order routing (SOR), use of specific broker algorithms, use of particular lit or dark venues, and timestamping or providing audit trails). All firms were looking to upgrade their front-office control procedures following the FCA’s Thematic Review TR14/13, especially for non-EQ-type instruments, manage conflicts upfront and upgrade transaction cost analysis (TCA) routines, particularly for telephone trading in non-equities. Although the latter were not strictly mandated by MiFID II, their use was key to demonstrating preventative controls and ‘fitness for purpose’ to regulators and discriminating end investors.

Front-office control awareness and improvements were most noticeable in terms of post-trade reviews and late trade allocation (LTA) fairness, with only 10% and 8% of respondents reporting challenges in these areas respectively (see Figure 9). Areas such as pre-trade warnings (eg, mandate restrictions), checks on cancelled, amended or delayed placements, or compliance with short-selling or ID checks for third-country booking restrictions all showed relatively healthy scores. The only areas where attention clearly needs to be paid included managing portfolio manager notifications and communications, reviews of short-selling arrangements, reviews of spot FX execution, segregation of portfolio manager duties and unusual settlement cycles (which are more sensitive to abuse).

There were slight improvements with greater centralisation of dealing desks, but challenges with non-EQ products and adapting to new platforms for NEQs under MiFID II (eg,

organised trading facilities (OTFs) vs. systematic internalisers), and also applying the new FIX tagging for OMSs and EMSs. Most firms were expecting to revise best execution policies and desk procedures, and the underlying data support behind them, for both hi- and lo-touch trading models in order- and quote-driven markets; the more advanced firms were taking account of both time-sensitive trades in liquid and illiquid markets for more asset classes (including spot FX).

All respondents commented that they would be profiling their dealers in order to produce supportive evidence of broker selection, including understanding which broker execution venues would likely fall under the systematic internaliser definition (thus relieving the asset manager seller of the obligation to trade report), the top five execution venues, use of single venues and use of algorithm or dark venue procedures. Attention to TCA procedures for NEQs (particularly FX), consolidating market data for prints (not just indications) and audit trail storage and retrievals were areas of focus – so was MiFID II RTS 25 (regarding clock synchronisation) for the larger participants using multilateral trading facilities (MTFs) as of Q3 2016.

The increased banking regulatory capital provision under Basel III associated with the introduction of the NSFR and the FRTB inevitably correlated with a lesser appetite to commit capital in the RFQ fixed income, currencies and commodities (FICC) inventory businesses. Given the impact of bond market volatility since October 2014 - and investment banks retracting quotes in corporate and high-yield fixed income instruments, and long-tenor IRS and inflation swap instruments or fixed income exchanged traded funds (ETFs), it was not surprising that many asset managers (including all liability-driven investing (LDI) and ETF firms) were paying close, if not more, attention to their trading patterns and their liquidity risk controls this year.

2016 was also when best execution for NEQs came of age. With MiFID II due to take effect on 3 January 2018, all firms indicated the need to revisit their order execution policy documents, their desk procedures (for each relevant asset class) and their supporting data (from timestamping the processing of orders, and selecting particular broker execution venues or trading venues such as MTFs or OTFs), and supporting data from TCA tools. The focus was on best execution factors, policies and procedures, and some areas of thematic interest also extended to querying whether a ‘best execution price’ was a clear price level which could be applied to certain types of trading (eg, switch, curve or ‘fly’ trades). Respondents also questioned the MiFID II demarcation between RTS 28 Art 2(5)-defined ‘passive’ (providing liquidity) vs. ‘aggressive’ (taking liquidity) trades, given the

12Survey findings

requirement that systems demarcate the two categories.

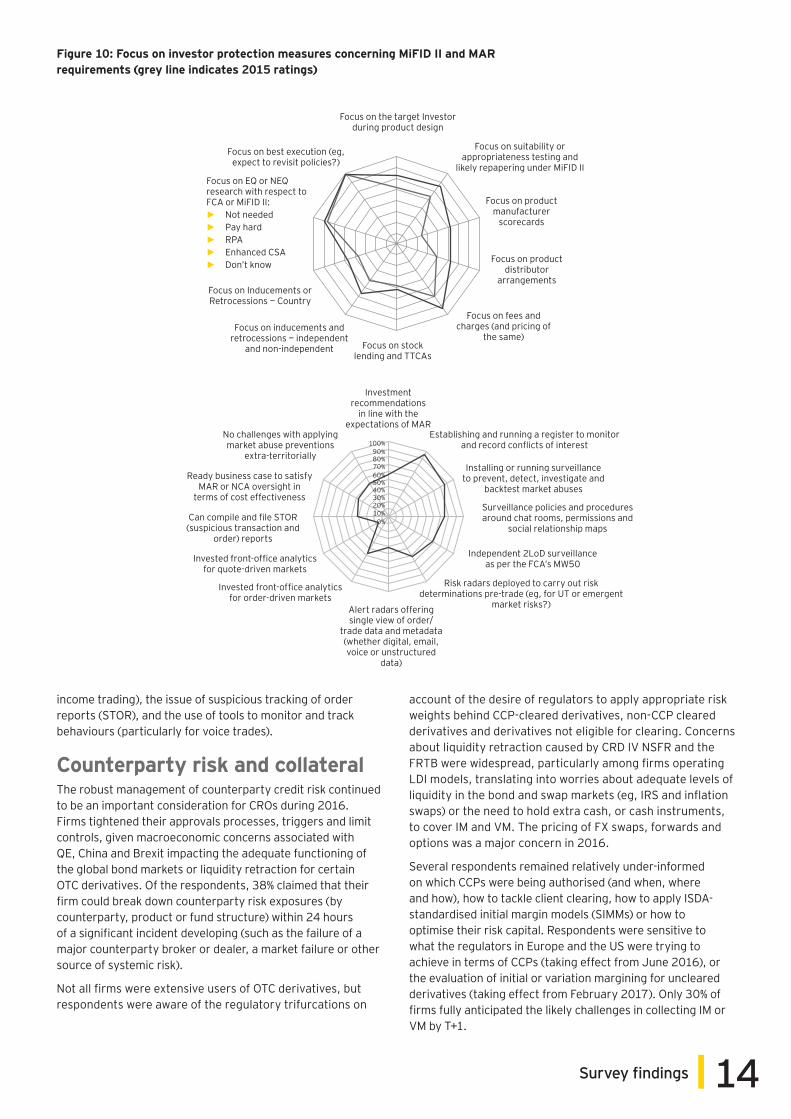

Preparations behind the other aspects of MiFID II investor protection requirements, plus the MAR, remained a prime focus for respondents (see Figure 10). The need to repaper and manage the suitability statements or appropriateness modifications, changes to manufacture or distribution processes, and the accompanying fees and changes (featuring ex-ante and ex-post disclosures) was a consistent theme, with more firms paying attention to these areas than recorded in last year’s survey.

One of the most controversial areas of focus for respondents in the survey was how to treat the subject of research provision under MiFID II, with 83% of asset managers focused on the issue. MiFID II requires asset managers to understand the pricing of research in all its components (including services such as access, polling, any use of expert networks or detailed analytics – not just sector-specific or desk research into stock selection). Respondents, however, baulked at proposals to link provision of fixed income sub-sector research with evidence of best execution, querying how the MiFID II measures could be applied to primary market issuance, discussions of market colour or the issue of sales notes.

MiFID II also requires firms to justify why research costs are value adding to the client (eg, original thought, intellectual rigour and meaningful conclusions). They are required to upgrade administration systems to allocate budgets by funds or by client, because they also need to provide pre- and post-spend research information to clients at the year-end. Concerns were raised by respondents at the prospect of a drop in quality as a result of falling waterfront coverage by the sell-side – recent surveys suggest that analyst research budgets could fall by as much as 20% to 30%. Others were worried about higher costs, greater fragmentation or detriment to the trading of small-cap equities.

13 Risk and regulation in a digitalised world A survey for UK asset managers

Respondents indicated a variety of responses, with 24% of firms yet to make a final decision at the time of writing (half the 2015 figure) and some yet to commit fully:

► Zero option – the firm generates its own research or the investment style does not depend on research (firm operates as hedge fund, LDI-only firm, etc) – 10% of firms

► Pay hard – establishing the appropriate account and administration arrangements, and paying from the firm’s bottom line accordingly (suits firms with a highly focused investment strategy or those concerned about the direction of travel of holding client money) – 23% of firms

► Establish research payment accounts (RPAs) for each client – setting up the appropriate account and administration arrangements to focus on drawing research from a smaller universe of brokers/providers from firms mindful of the opportunity costs to the balance sheet of ‘paying hard’ – 17% of firms

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Non-centralised dealing desk

SYSC for NEQ-like products

Pre-trade warnings to restrict trading

Non-standard settlement cycles

Changes to order routing and RFQ

Systems and Controls (SYSC) for EQ-like products

Post-trade reviews

Cancelled and amended trades

LTA fairness

Changes in platforms, eg, OTFs and SIs

Applying new actionable indication of interest (AIOI) and RFQ tagging

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Revising desk procedures

Handling client-specific instructions

Broker classification and selection factors

Revising procedures regarding algorithms

Monitoring and conducting TCA

Revising factors and factor weights

Supplying top five execution venues

Specifying circumstances and single venue

Revising procedures regarding dark pools

Consolidating market data (comparability)

Audit trails and record keeping

► Outsourced RPAs – firms exploring whether other institutions, such as asset servicers or agency brokers, will follow the path of Instinet, which announced its application in March 2015 as a payment institution with the FCA – see RPAs above

► ►Retain/expand commission sharing accounts (CSAs) – asset managers preferring to ‘wait and see’ whether NCAs such as the FCA would allow ‘enhanced CSA’ arrangements once the measures are transposed – 26% of firms

Firms’ preparations to boost market surveillance and prevent unauthorised trading (UT) were growing themes in 2016, as was the need to make optimum use of dealing screen real estate. Given that the MAR took effect on 3 July 2016, there was an unsurprisingly strong focus on market abuse prevention (defined in MAR 596/2014 Annex 1). Areas of relative weakness concerned the specification of MAR Art 3(1)(35) recommendations, the tracking of unstructured data, provision of front-office analytics (particularly for fixed

Figure 9: Expectations on challenges with front-office procedures and best execution procedures in terms of preparing for MiFID II

14Survey findings

income trading), the issue of suspicious tracking of order reports (STOR), and the use of tools to monitor and track behaviours (particularly for voice trades).

Counterparty risk and collateralThe robust management of counterparty credit risk continued to be an important consideration for CROs during 2016. Firms tightened their approvals processes, triggers and limit controls, given macroeconomic concerns associated with QE, China and Brexit impacting the adequate functioning of the global bond markets or liquidity retraction for certain OTC derivatives. Of the respondents, 38% claimed that their firm could break down counterparty risk exposures (by counterparty, product or fund structure) within 24 hours of a significant incident developing (such as the failure of a major counterparty broker or dealer, a market failure or other source of systemic risk).

Not all firms were extensive users of OTC derivatives, but respondents were aware of the regulatory trifurcations on

account of the desire of regulators to apply appropriate risk weights behind CCP-cleared derivatives, non-CCP cleared derivatives and derivatives not eligible for clearing. Concerns about liquidity retraction caused by CRD IV NSFR and the FRTB were widespread, particularly among firms operating LDI models, translating into worries about adequate levels of liquidity in the bond and swap markets (eg, IRS and inflation swaps) or the need to hold extra cash, or cash instruments, to cover IM and VM. The pricing of FX swaps, forwards and options was a major concern in 2016.

Several respondents remained relatively under-informed on which CCPs were being authorised (and when, where and how), how to tackle client clearing, how to apply ISDA-standardised initial margin models (SIMMs) or how to optimise their risk capital. Respondents were sensitive to what the regulators in Europe and the US were trying to achieve in terms of CCPs (taking effect from June 2016), or the evaluation of initial or variation margining for uncleared derivatives (taking effect from February 2017). Only 30% of firms fully anticipated the likely challenges in collecting IM or VM by T+1.

Focus on the target Investor during product design

Focus on suitability or appropriateness testing and

likely repapering under MiFID II

Focus on product manufacturer

scorecards

Focus on product distributor

arrangements

Focus on fees and charges (and pricing of

the same)Focus on stock

lending and TTCAs

Focus on inducements and retrocessions — independent

and non-independent

Focus on Inducements or Retrocessions — Country

Focus on EQ or NEQ research with respect to FCA or MiFID II:

► Not needed ► Pay hard ► RPA ► Enhanced CSA ► Don’t know

Focus on best execution (eg, expect to revisit policies?)

Investment recommendations

in line with the expectations of MAR

Establishing and running a register to monitor and record conflicts of interest

Installing or running surveillance to prevent, detect, investigate and

backtest market abuses

Surveillance policies and procedures around chat rooms, permissions and

social relationship maps

Independent 2LoD surveillance as per the FCA’s MW50

Risk radars deployed to carry out risk determinations pre-trade (eg, for UT or emergent

market risks?)

Invested front-office analytics for order-driven markets

Invested front-office analytics for quote-driven markets

Can compile and file STOR (suspicious transaction and

order) reports

Ready business case to satisfy MAR or NCA oversight in

terms of cost effectiveness

No challenges with applying market abuse preventions

extra-territorially100%

90%80%70%60%50%40%30%20%10%

0%

Figure 10: Focus on investor protection measures concerning MiFID II and MAR requirements (grey line indicates 2015 ratings)

Alert radars offering single view of order/

trade data and metadata (whether digital, email, voice or unstructured

data)

15 Risk and regulation in a digitalised world A survey for UK asset managers

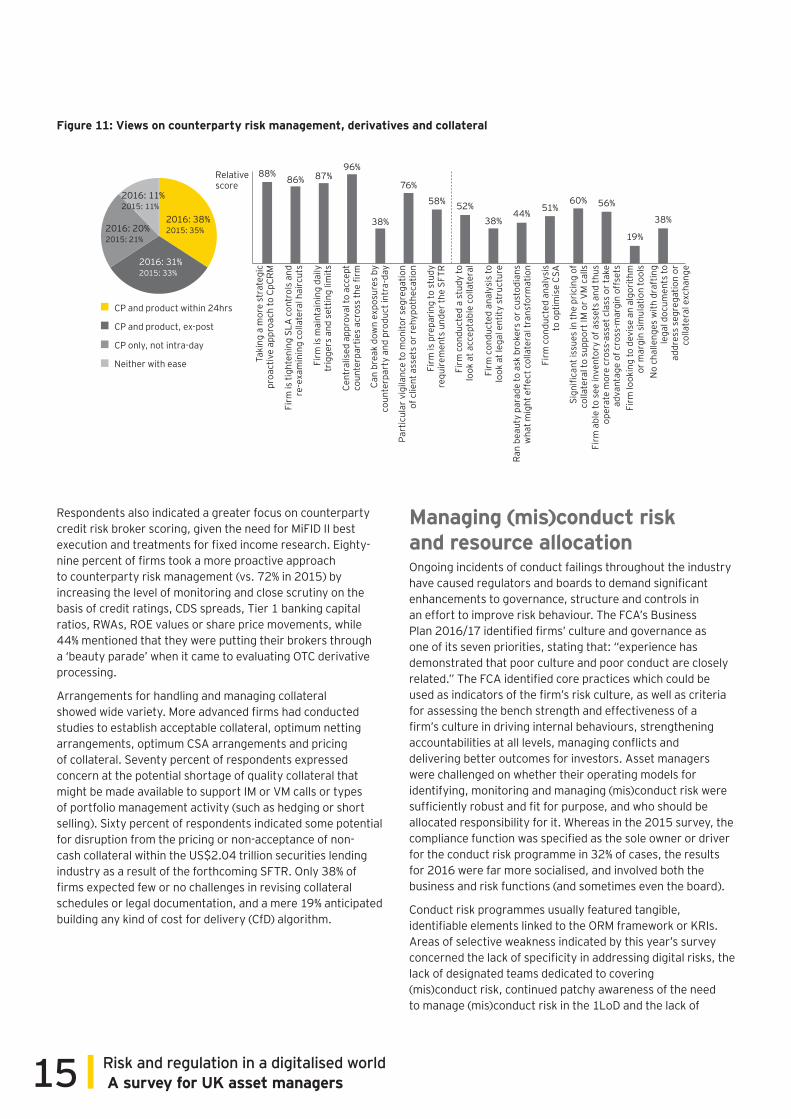

Respondents also indicated a greater focus on counterparty credit risk broker scoring, given the need for MiFID II best execution and treatments for fixed income research. Eighty-nine percent of firms took a more proactive approach to counterparty risk management (vs. 72% in 2015) by increasing the level of monitoring and close scrutiny on the basis of credit ratings, CDS spreads, Tier 1 banking capital ratios, RWAs, ROE values or share price movements, while 44% mentioned that they were putting their brokers through a ‘beauty parade’ when it came to evaluating OTC derivative processing.

Arrangements for handling and managing collateral showed wide variety. More advanced firms had conducted studies to establish acceptable collateral, optimum netting arrangements, optimum CSA arrangements and pricing of collateral. Seventy percent of respondents expressed concern at the potential shortage of quality collateral that might be made available to support IM or VM calls or types of portfolio management activity (such as hedging or short selling). Sixty percent of respondents indicated some potential for disruption from the pricing or non-acceptance of non-cash collateral within the US$2.04 trillion securities lending industry as a result of the forthcoming SFTR. Only 38% of firms expected few or no challenges in revising collateral schedules or legal documentation, and a mere 19% anticipated building any kind of cost for delivery (CfD) algorithm.

2016: 38% 2015: 35%2016: 20%

2015: 21%

2016: 11% 2015: 11%

2016: 31% 2015: 33%

CP and product within 24hrs

CP and product, ex-post

CP only, not intra-day

Neither with ease

Relative score

Taki

ng a

mor

e st

rate

gic

proa

ctiv

e ap

proa

ch to

CpC

RM

Firm

is ti

ghte

ning

SLA

con

trol

s an

d re

-exa

min

ing

colla

tera

l hai

rcut

s

Firm

is m

aint

aini

ng d

aily

tr

igge

rs a

nd s

ettin

g lim

its

Cent

ralis

ed a

ppro

val t

o ac

cept

co

unte

rpar

ties

acro

ss th

e fir

m

Can

brea

k do

wn

expo

sure

s by

co

unte

rpar

ty a

nd p

rodu

ct in

tra-

day

Part

icul

ar v

igila

nce

to m

onito

r seg

rega

tion

of c

lient

ass

ets

or re

hypo

thec

atio

n

Firm

is p

repa

ring

to s

tudy

re

quire

men

ts u

nder

the

SFTR

Firm

con

duct

ed a

stu

dy to

lo

ok a

t acc

epta

ble

colla

tera

l

Firm

con

duct

ed a

naly

sis

to

look

at l

egal

ent

ity s

truc

ture

Ran

beau

ty p

arad

e to

ask

bro

kers

or c

usto

dian

s w

hat m

ight

eff

ect c

olla

tera

l tra

nsfo

rmat

ion

Firm

con

duct

ed a

naly

sis

to o

ptim

ise

CSA

Sign

ifica

nt is

sues

in th

e pr

icin

g of

co

llate

ral t

o su

ppor

t IM

or V

M c

alls

Firm

abl

e to

see

inve

ntor

y of

ass

ets

and

thus

op

erat

e m

ore

cros

s-as

set c

lass

or t

ake

adva

ntag

e of

cro

ss-m

argi

n of

fset

sFi

rm lo

okin

g to

dev

ise

an a

lgor

ithm

or

mar

gin

sim

ulat

ion

tool

sN

o ch

alle

nges

with

dra

ftin

g le

gal d

ocum

ents

to

addr

ess

segr

egat

ion

or

colla

tera

l exc

hang

e

88%86% 87%

96%

38%

76%

58% 52%38%

44% 51%60% 56%

19%

38%

Figure 11: Views on counterparty risk management, derivatives and collateral

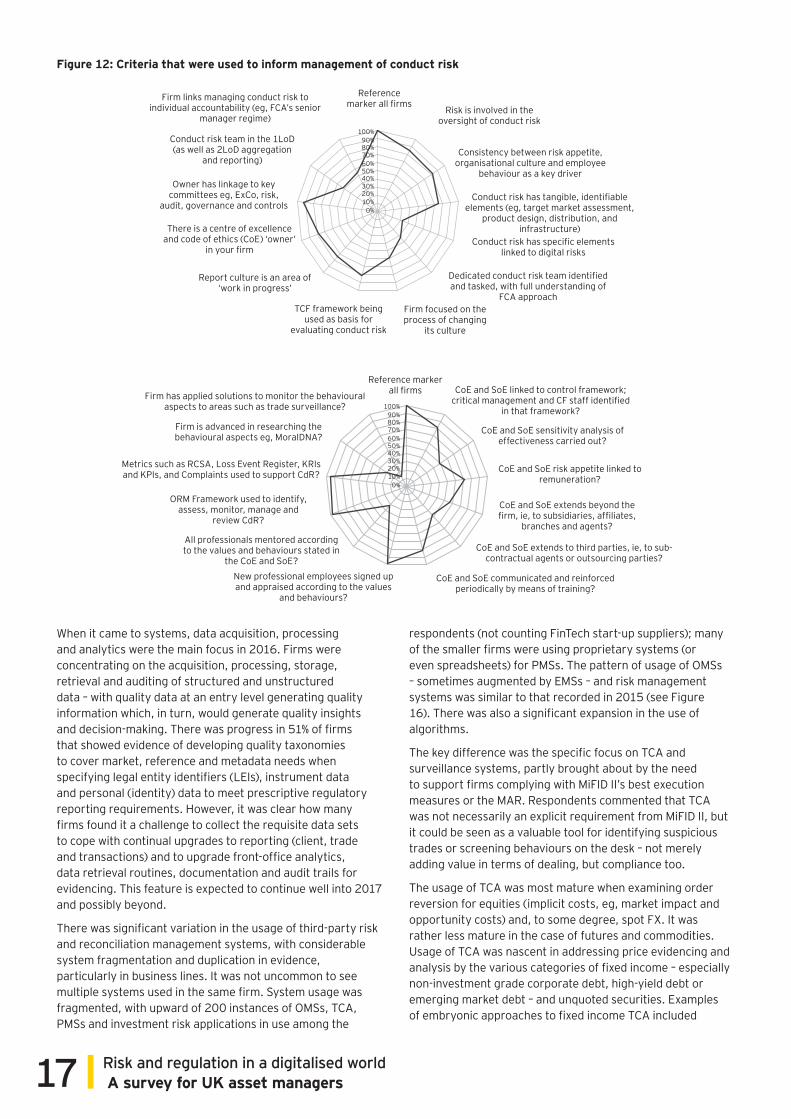

Managing (mis)conduct risk and resource allocationOngoing incidents of conduct failings throughout the industry have caused regulators and boards to demand significant enhancements to governance, structure and controls in an effort to improve risk behaviour. The FCA’s Business Plan 2016/17 identified firms’ culture and governance as one of its seven priorities, stating that: “experience has demonstrated that poor culture and poor conduct are closely related.” The FCA identified core practices which could be used as indicators of the firm’s risk culture, as well as criteria for assessing the bench strength and effectiveness of a firm’s culture in driving internal behaviours, strengthening accountabilities at all levels, managing conflicts and delivering better outcomes for investors. Asset managers were challenged on whether their operating models for identifying, monitoring and managing (mis)conduct risk were sufficiently robust and fit for purpose, and who should be allocated responsibility for it. Whereas in the 2015 survey, the compliance function was specified as the sole owner or driver for the conduct risk programme in 32% of cases, the results for 2016 were far more socialised, and involved both the business and risk functions (and sometimes even the board).

Conduct risk programmes usually featured tangible, identifiable elements linked to the ORM framework or KRIs. Areas of selective weakness indicated by this year’s survey concerned the lack of specificity in addressing digital risks, the lack of designated teams dedicated to covering (mis)conduct risk, continued patchy awareness of the need to manage (mis)conduct risk in the 1LoD and the lack of

16Survey findings

linkage to the UK’s individual accountability Senior Managers and Certification Regime (SMCR), which is due to enter force after Q1 2018. Firms that were more advanced in their preparation had pinpointed the right senior individuals and were looking to establish their SMCR statements of prescribed responsibilities, grandfathering arrangements and responsibility maps, where the individuals belonged to a broader group in order to improve clarity of governance and reduced risk of overlap or conflict.

Codes (or statements) of ethics were used in different forms, with some firms needing to reinforce them periodically through training, mentoring using case examples or linkages to sensitivity analyses. Relative areas of weakness arose from extending the measures beyond the firm (ie, to subsidiaries or affiliates, or to third parties such as outsourcing agents). Only a minority of firms were actively researching behavioural aspects (in contrast to many banks), and even they had yet to identify or integrate solutions to generate meaningful metrics (again, in contrast with the sell side).

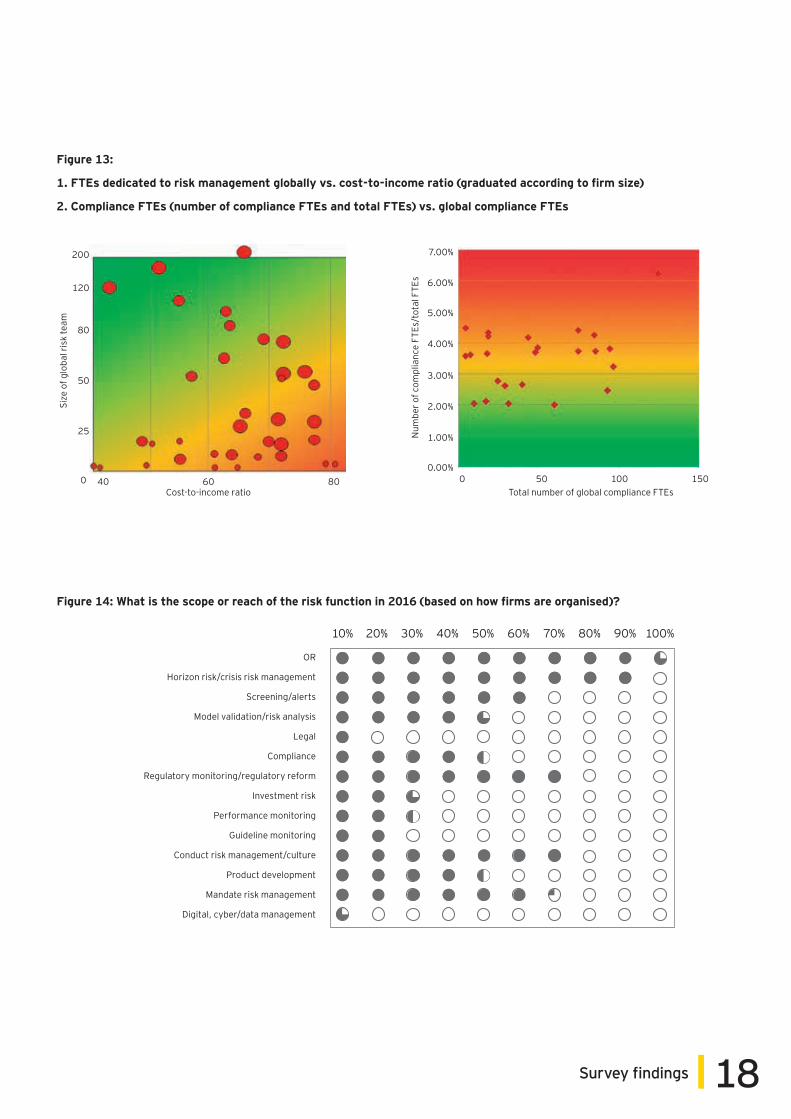

This year’s survey also focused more deeply on the quality and quantity of risk and compliance resources across firms, and how FTEs were being counted (see Figure 13). This was partly in response to asset managers benchmarking their capabilities against peers, partly down to increasing interest, even activism, and partly in response to regulators asking more penetrating questions about the bench strength and appropriateness of resources to challenge the business.

Not all respondents measured the risk or compliance functions the same way; some houses included regulatory reform and managing misconduct risk, or event horizon risk, in their totals for compliance. Some firms boosted their numbers using shared resources or hiring temporary staff (contractors). Size of team did not always correspond to cost-to-income ratio, and percentages were somewhat larger for the smaller houses or those carrying single investment styles. Team sizes did tend to correlate broadly with a wider range of investment styles and more global coverage. The mean percentage fraction for compliance teams (the number of compliance FTEs divided by the total number of FTEs) was 3.73% for a mean cost-to-income ratio of 66%; the ratio did not differ appreciably from that recorded in EY’s 2013 survey. Finally, the corresponding mean percentage fraction for risk teams (the number of risk FTEs divided by the total number of FTEs) was 3.31% of total FTE staffing.

The general trend was for risk and compliance headcount to be up by 5% to 6%, but this trend was far from universal – around 40% of firms posted level headcount FTEs with 2015, and four actually shrank their team sizes. Firms were definitely looking to upskill the quality of the risk resources to cover facets of business risk (see Figure 14), not just expanding team sizes. There was a new ‘controls consciousness’, given that regulators are increasingly expecting C-suite functions within asset managers to attest

personally, and skilled persons reviews (Section 166 notices in the UK) were being used to gather information and insight into the robustness of OpR frameworks. This was particularly relevant for front-office controls during 2016.

FinTechSeveral new concepts came of age during 2016: digitalised interfaces, robotics and robo-selection, information networks, peer-to-peer (P2P) platforms, virtual currencies and blockchain solutions. Respondents were challenged when trying to expand their GRC frameworks and KRIs in order to cope with increasing digitalised environments, such as that associated with lo-touch algorithmic trading. Managing the risk of parallel processing, disruptive new entrants and the potential for cyber attacks were significant considerations that prompted a minority of CROs to enquire whether they needed IT support skills located in risk teams, not merely shared at group level.

FinTech – covering crowdfunding, virtual payments, software, infrastructure or data and analytics – is at a critical point in its evolution. Many respondents commented on the challenge of managing upgrades to traditional incumbent solution vendors running order or risk management systems, operating on a cost per transaction, percentage of assets basis, or licence fee, maintenance charge or integration consulting model.

A minority of respondents were curious about the countdown to emergent FinTech disruptors in general production – typically, start-up innovative firms disintermediating incumbent financial services firms using breakout technologies to circumvent or replace existing infrastructure, operating to generate multiple revenue streams, including store-front advertising, viral marketing and monetisation of data.

A clear majority of respondents indicated that their firm was experiencing issues with flexibility or IT change requests (see Figure 15), explaining that it was challenging for the IT function to demonstrate the necessary flexibility to keep up with the volume of change requests, often the result of regulatory-driven change or transformation. In contrast, many of the top-quartile asset managers were already able to link their portfolio management systems (PMSs), OMSs, EMSs and general ledger (GL) systems into a seamless architecture.

While the appetite for surveillance solutions was high, comparatively few firms were integrating it with their order or RFQ and trade processing environments. Given the interest in adopting transversal solutions for reporting, it was little surprise that several respondents welcomed the prospect of more standard regulatory reporting templates (for client reporting, trade and transaction reporting for MiFID II, surveillance and STOR reporting for the MAR, and data documentation).

17 Risk and regulation in a digitalised world A survey for UK asset managers

When it came to systems, data acquisition, processing and analytics were the main focus in 2016. Firms were concentrating on the acquisition, processing, storage, retrieval and auditing of structured and unstructured data – with quality data at an entry level generating quality information which, in turn, would generate quality insights and decision-making. There was progress in 51% of firms that showed evidence of developing quality taxonomies to cover market, reference and metadata needs when specifying legal entity identifiers (LEIs), instrument data and personal (identity) data to meet prescriptive regulatory reporting requirements. However, it was clear how many firms found it a challenge to collect the requisite data sets to cope with continual upgrades to reporting (client, trade and transactions) and to upgrade front-office analytics, data retrieval routines, documentation and audit trails for evidencing. This feature is expected to continue well into 2017 and possibly beyond.

There was significant variation in the usage of third-party risk and reconciliation management systems, with considerable system fragmentation and duplication in evidence, particularly in business lines. It was not uncommon to see multiple systems used in the same firm. System usage was fragmented, with upward of 200 instances of OMSs, TCA, PMSs and investment risk applications in use among the

respondents (not counting FinTech start-up suppliers); many of the smaller firms were using proprietary systems (or even spreadsheets) for PMSs. The pattern of usage of OMSs – sometimes augmented by EMSs – and risk management systems was similar to that recorded in 2015 (see Figure 16). There was also a significant expansion in the use of algorithms.

The key difference was the specific focus on TCA and surveillance systems, partly brought about by the need to support firms complying with MiFID II’s best execution measures or the MAR. Respondents commented that TCA was not necessarily an explicit requirement from MiFID II, but it could be seen as a valuable tool for identifying suspicious trades or screening behaviours on the desk – not merely adding value in terms of dealing, but compliance too.

The usage of TCA was most mature when examining order reversion for equities (implicit costs, eg, market impact and opportunity costs) and, to some degree, spot FX. It was rather less mature in the case of futures and commodities. Usage of TCA was nascent in addressing price evidencing and analysis by the various categories of fixed income – especially non-investment grade corporate debt, high-yield debt or emerging market debt – and unquoted securities. Examples of embryonic approaches to fixed income TCA included

Reference marker all firms

Risk is involved in the oversight of conduct risk

Consistency between risk appetite, organisational culture and employee

behaviour as a key driver

Conduct risk has tangible, identifiable elements (eg, target market assessment,

product design, distribution, and infrastructure)

Conduct risk has specific elements linked to digital risks

Dedicated conduct risk team identified and tasked, with full understanding of

FCA approachFirm focused on the process of changing

its culture

TCF framework being used as basis for

evaluating conduct risk

Report culture is an area of ‘work in progress’

There is a centre of excellence and code of ethics (CoE) ‘owner’

in your firm

Owner has linkage to key committees eg, ExCo, risk,

audit, governance and controls

Conduct risk team in the 1LoD (as well as 2LoD aggregation

and reporting)

Firm links managing conduct risk to individual accountability (eg, FCA’s senior

manager regime)100%

90%80%70%60%50%40%30%20%10%

0%

100%90%80%70%60%50%40%30%20%10%

0%

Reference marker all firms CoE and SoE linked to control framework;

critical management and CF staff identified in that framework?

CoE and SoE sensitivity analysis of effectiveness carried out?

CoE and SoE risk appetite linked to remuneration?

CoE and SoE extends beyond the firm, ie, to subsidiaries, affiliates,

branches and agents?

CoE and SoE extends to third parties, ie, to sub-contractual agents or outsourcing parties?

CoE and SoE communicated and reinforced periodically by means of training?

New professional employees signed up and appraised according to the values

and behaviours?

All professionals mentored according to the values and behaviours stated in

the CoE and SoE?

ORM Framework used to identify, assess, monitor, manage and

review CdR?

Metrics such as RCSA, Loss Event Register, KRIs and KPIs, and Complaints used to support CdR?

Firm is advanced in researching the behavioural aspects eg, MoralDNA?

Firm has applied solutions to monitor the behavioural aspects to areas such as trade surveillance?

Figure 12: Criteria that were used to inform management of conduct risk

18Survey findings

0

25

50

80

120

200

60 Cost-to-income ratio

Size

of g

loba

l ris

k te

am

80 00.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

50 100 150Total number of global compliance FTEs

Num

ber o

f com

plia

nce

FTEs

/tot

al F

TEs

OR

Horizon risk/crisis risk management

Screening/alerts

Model validation/risk analysis

Legal

Compliance

Regulatory monitoring/regulatory reform

Investment risk

Performance monitoring

Guideline monitoring

Conduct risk management/culture

Product development

Mandate risk management

Digital, cyber/data management

10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Figure 13:

1. FTEs dedicated to risk management globally vs. cost-to-income ratio (graduated according to firm size)

2. Compliance FTEs (number of compliance FTEs and total FTEs) vs. global compliance FTEs

Figure 14: What is the scope or reach of the risk function in 2016 (based on how firms are organised)?

40

19 Risk and regulation in a digitalised world A survey for UK asset managers

determination of expected price, depictions of liquidity scores, ‘last-look’ pricing or large deals, or examining volatility in the bond futures markets at the point of execution.

A suite of newer TCA entrants appeared in the FX and FX forward (FXF) space, such as (in alphabetical order) BestX and QSI, FX Transparency, Global Trading Analytics, Klarity FX, LiquidMetrix and New Change FX. The use of surveillance systems was judged to be in its relative infancy – systems such as (in alphabetical order) Actimize, Bloomberg, ClusterSeven, Commcise, Cybernetix, GLASS, MetricStream, PTA, Rapptr, Risk Control, SMARSH, SMARTS, StarCompliance and Thomson Reuters were mentioned in addition to the system vendors above.

There was also an overwhelming awareness among CROs that monitoring, managing and maintaining data security (including ‘golden copy’ records for audit trail purposes) remained critical (see Figure 14). Only 73% of respondents indicated that data quality was managed satisfactorily within their organisation, and the same percentage indicated that their firm experienced challenges in recording or retrieving audit trails satisfactorily – a decline compared with 2015. Challenge areas for respondents in 2016 were insufficiently attributable data governance (including critical requirements such as the right to consent, the right to erasure, the obligations for data controllers and the need for ‘pseudonymisation’ to satisfy the requirements under the GDPR, which takes effect in May 2018.

MiFID II, meanwhile, will greatly expand the need to record and store audio phone calls, emails and face-to-face investor interactions, as well as data concerning order processing and high-frequency algorithmic trading (HFAT), best execution evidencing, broker profiling, transaction details and retention of client reports for up to five years. At the more sophisticated firms, respondents commented on how compliance departments had already begun to examine the MiFID II rules for client, trade and transaction reporting, and realised the full extent of the record-keeping requirements, particularly with respect to best execution and potential trade reporting obligations when executing via a non-systematic internaliser (SI) or when executing any component part of the transaction value chain in a third country.

MiFID II’s wide-ranging requirements mean that firms must ensure that much more than 100 fields are identified, recorded and stored in a secure, machine-readable, durable format which can be retrieved at will. Respondents at the larger mid-sized firms and larger asset managers by AuM were alluding to the fact that data storage capacity and computing power requirements would need to be reimagined, and big data strategies considered, in order to deliver the

49%

51%

5%

95%

68%

32%

Key:

Yes Partly or no

Figure 15: Summary of system and data issues recorded in this year’s survey

1. Issues with IT flexibility

2. Taxonomy used

3. Data security specific concern

20Survey findings

necessary scalability and future flexibility. Larger firms indicated that they might even be forced to look at cloud storage and computing for the first time – effectively entering the ‘data business’ themselves – and consider archive backup and multimedia recovery as solutions for other entities.

The big data challenges associated with current data processing requirements to comply with regulations adjacent to MiFID II (eg, the EMIR, the MAR and the SFTR) were a further consideration, given the extensive transaction reporting data load from each measure (the EMIR requires 85 data fields to be recorded; SFTR 71–77 (covering counterparty, transaction and collateral reporting) and MAR Annex XI STOR reporting requires more than 60 data components to be captured). Forty-five percent of respondents could point to the use of big data facilities, such as warehouses maintained by the parent or third parties – a significant improvement compared with 2015 (see Figure 17).

Future requirements under digital and CRM, robotics, robo-advice and future technologies such as DLT and blockchain were extended to cover the requirement of digitalisation, including store-front advertising, viral marketing and monetisation of data. The results from the respondents were recorded on the next page for easy comparison.

An appreciation of cyber risks and cyber threats, data leakage and data loss prevention (DLP), and advanced persistent threats (APT) is already prevalent among high-profile banks, financial market infrastructures and insurers. Given high-profile breaches and DDoS attacks (and the continued media interest in them), financial firms leveraging big data analytics to extract new and more valuable information from trade and transaction records were particularly concerned about the prospect of public awareness that controls had been breached.

Several asset managers were understandably concerned about the potential for intrusion or disruption of services. Respondents remained alert to a broader threat landscape, including interference with third-party communications (eg, instructions to brokers, venues, custodians, outsourcing agents, prime brokers or fund administrators) and points of entry, such as cluster or cloud computing. The survey noted a

distinct reluctance to ‘own up’ to incidents such as attempted attacks, cases of ransomware or financial losses, for fear of investor or client flight, or of putting regulators on notice that there was a concern.

Data security – concerning hacking, impersonations or cybercrime and cybersecurity against the firm as target (or the data warehouse or outsourcer as an entry point) – was seen as a concern by 95% of respondents (up from 79% in 2015). The threat landscape is very different today, with organised criminals (sometimes fronting hostile governments), the growth of hacktivism, state-sponsored cyber espionage and cyber terrorism resulting in more attacks on market infrastructure firms, banks and asset managers.

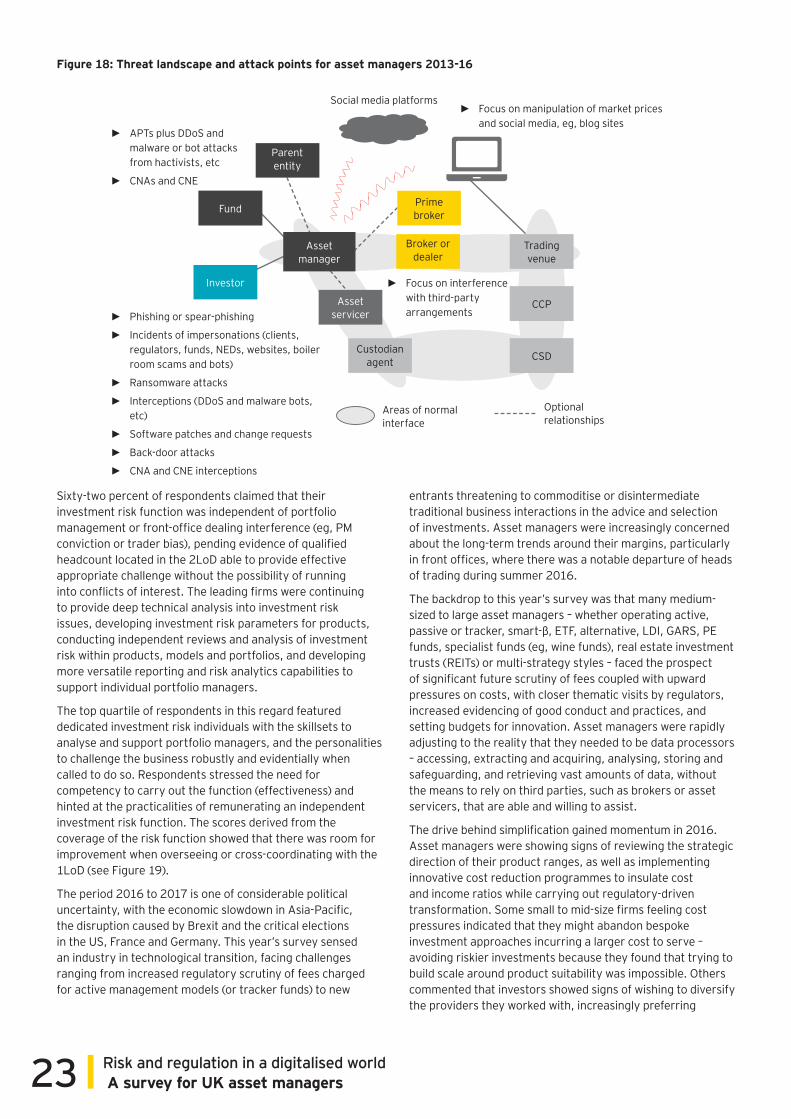

Some firms had taken preventative measures with regard to cybersecurity (see Figure 18). Examples included:

► Appointing an emergency committee involving senior members of staff, focusing on ‘protect, detect and respond’ (although not all risk departments have FTEs that are competent in this field)

► Remaining vigilant to the potential for ID security fraud, phishing, spear-phishing, whale-phishing, impersonation (of senior officers or directors, end clients, funds and non-executive directors (NEDs)) and, sometimes, more ambitious scams, including interception, website fabrication, boiler room scams, theft of client assets or fraudulent redemptions

► Logging all attempted DDoS or back-door attacks, particularly if the asset manager is being targeted as an entry point into a banking or insurance entity, or attacks by malware or mule entities – the latter could employ codes or bots that distinctly target users and online services, stealing data, installing ransomware (demanding payment of one bitcoin for release) or carrying out fraudulent activity without being detected

► ►Spending more effort on reinforcing firewalls and spending ‘soft’ time educating board members and NEDs on the importance of maintaining security (eg, not loading BYOD memory sticks or activating .exe files)

26%

14% 14% 13%11%

Num

ber o

f firm

s

Char

les

Rive

r

BRS

(Ala

ddin

)

Mar

kit t

hink

Folio

Bloo

mbe

rg T

OM

S

Prop

riet

ary

Fide

ssa