Embed Size (px)

Citation preview

RTD8: Taking Responsibility – Achieving Change

Monitoring & Reporting Tourism Carbon Emissions

Rachel Dunk ([email protected]) Steven Gillespie, Jacob Pryor, Josh Thomas

ICARB (www.icarb.org)

“If you want me to do things only for ROI

reasons, you should get out of this stock.”Tim Cook, Feb 2014

4

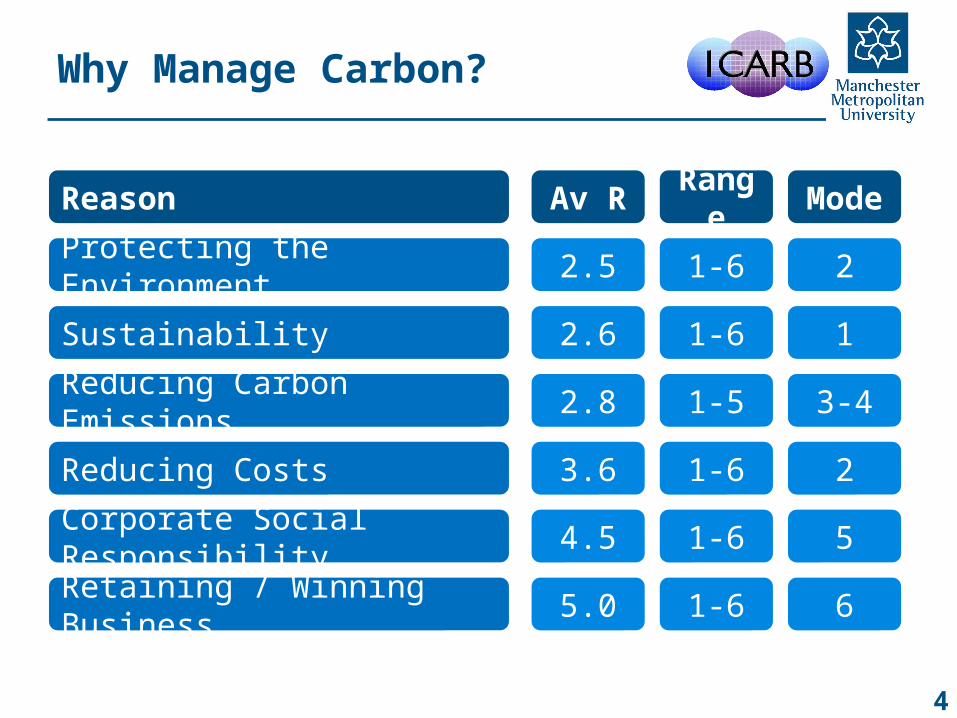

Why Manage Carbon?

Protecting the Environment 2.5

Sustainability 2.6

Reducing Carbon Emissions 2.8

Reducing Costs 3.6

Corporate Social Responsibility 4.5

Retaining / Winning Business 5.0

1-6

1-6

1-5

1-6

1-6

1-6

2

1

3-4

2

5

6

Av R Range ModeReason

5

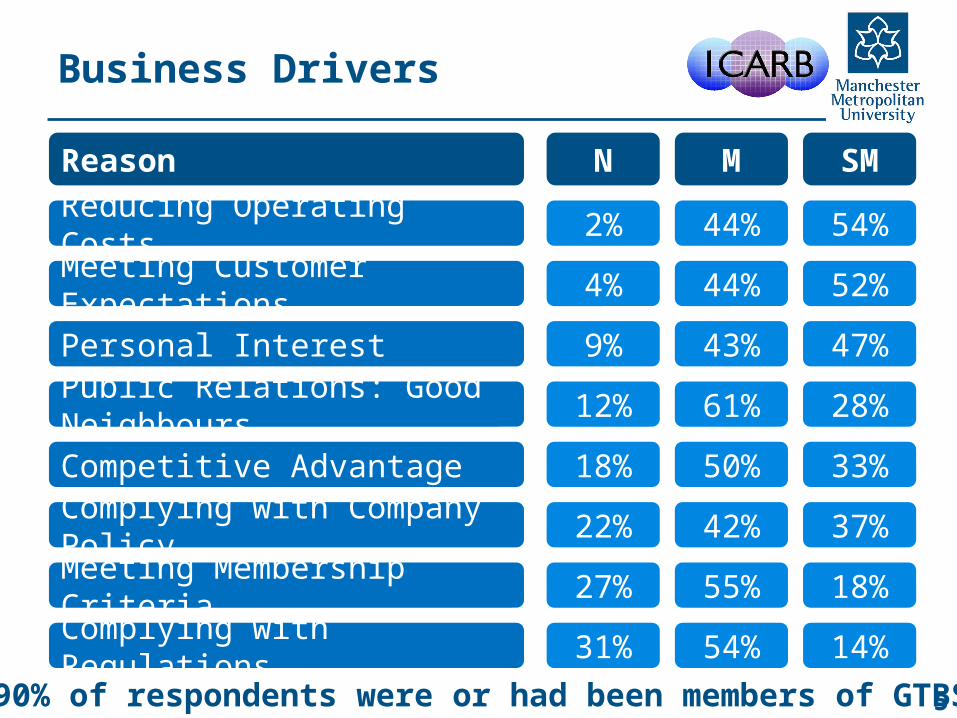

Business Drivers

Reducing Operating Costs 2%

Meeting Customer Expectations 4%

Personal Interest 9%

Public Relations: Good Neighbours 12%

Competitive Advantage 18%

Meeting Membership Criteria 27%

44%

44%

43%

61%

50%

55%

54%

52%

47%

28%

33%

18%

N M SMReason

Complying with Company Policy 22% 42% 37%

Complying with Regulations 31% 54% 14%90% of respondents were or had been members of GTBS

6

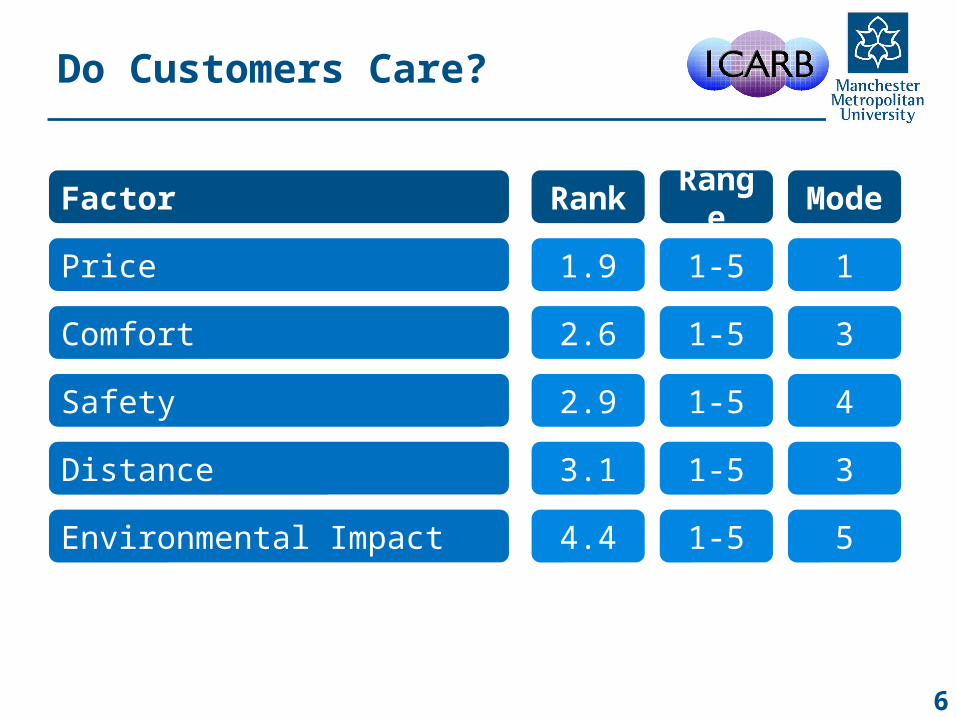

Do Customers Care?

Price 1.9

Comfort 2.6

Safety 2.9

Distance 3.1

Environmental Impact 4.4

1-5

1-5

1-5

1-5

1-5

1

3

4

3

5

Rank Range ModeFactor

77

How do we fill the bucket of

care?

8

9

Rules & Tools for Carbon Accounting

What does this animal look like?

10

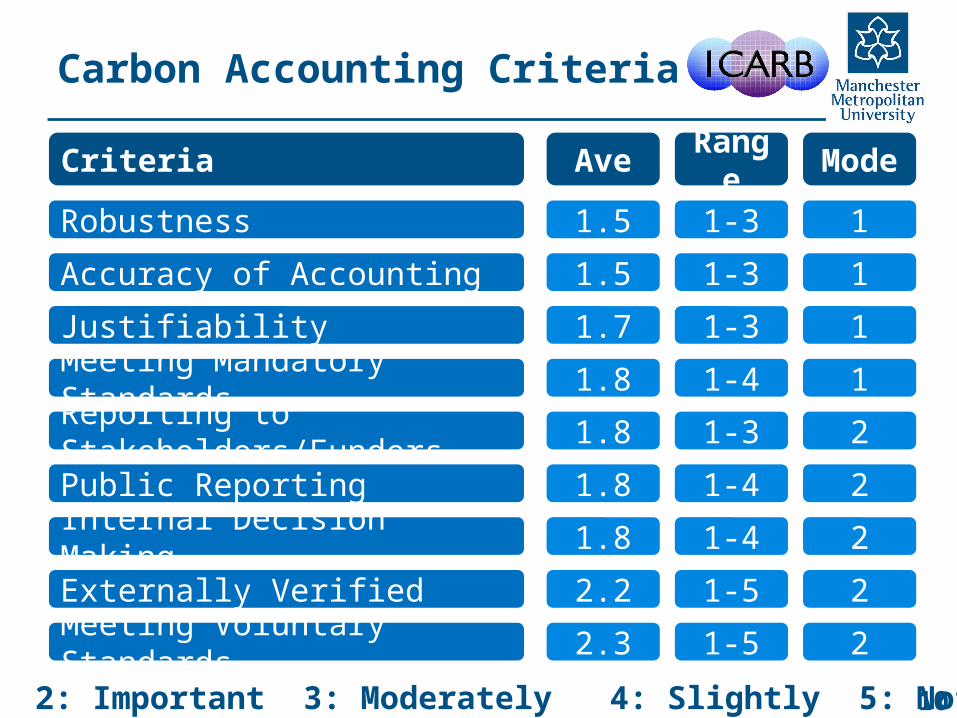

Carbon Accounting Criteria

Robustness 1.5

Accuracy of Accounting 1.5

Justifiability 1.7

Meeting Mandatory Standards 1.8

Reporting to Stakeholders/Funders 1.8

Public Reporting 1.8

1-3

1-3

1-3

1-4

1-3

1-4

1

1

1

1

2

2

Ave Range ModeCriteria

Internal Decision Making 1.8 1-4 2

Externally Verified 2.2 1-5 2

1: Very 2: Important 3: Moderately 4: Slightly 5: Not at all

Meeting Voluntary Standards 2.3 1-5 2

11

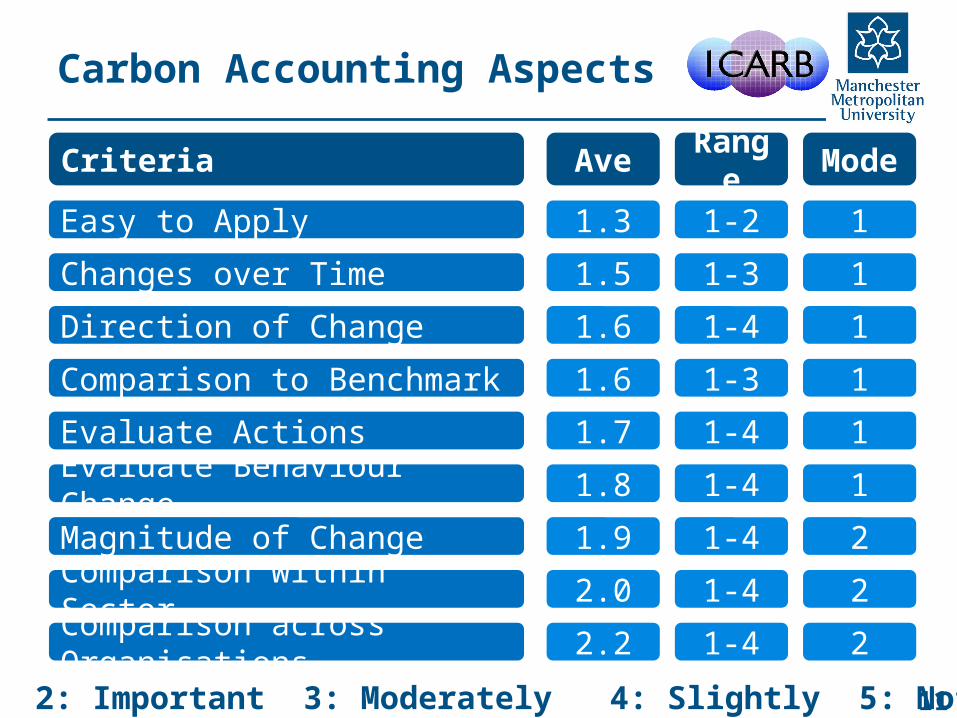

Carbon Accounting Aspects

Easy to Apply 1.3

Changes over Time 1.5

Direction of Change 1.6

Comparison to Benchmark 1.6

Evaluate Actions 1.7

Evaluate Behaviour Change 1.8

1-2

1-3

1-4

1-3

1-4

1-4

1

1

1

1

1

1

Ave Range ModeCriteria

Magnitude of Change 1.9 1-4 2

Comparison within Sector 2.0 1-4 2

Comparison across Organisations 2.2 1-4 2

1: Very 2: Important 3: Moderately 4: Slightly 5: Not at all

12

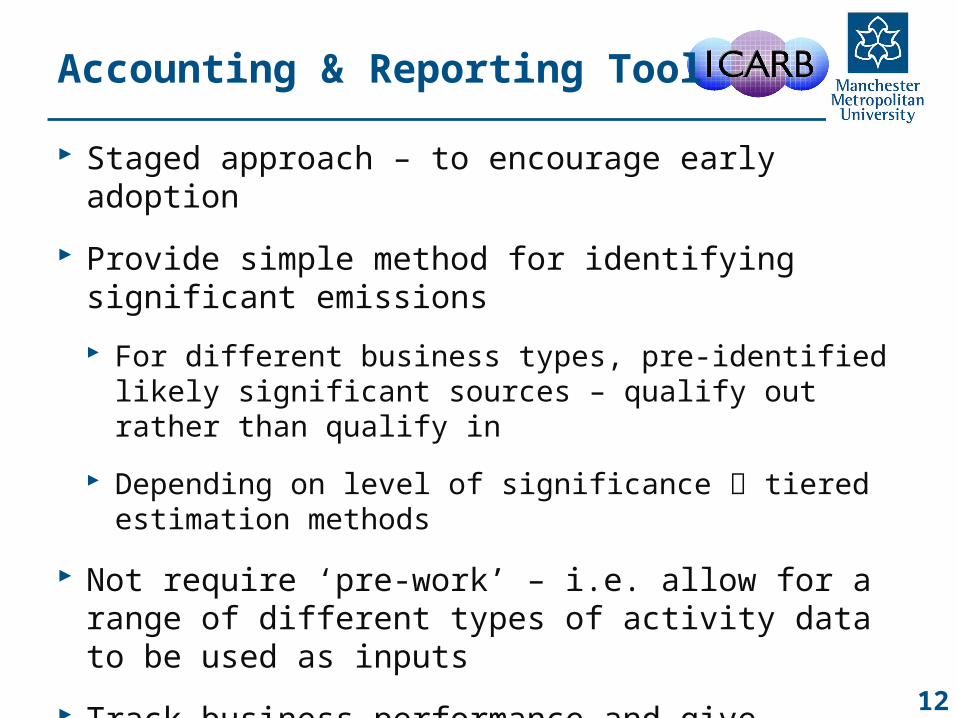

Accounting & Reporting Tool

Staged approach – to encourage early adoption

Provide simple method for identifying significant emissions

For different business types, pre-identified likely significant sources – qualify out rather than qualify in

Depending on level of significance tiered estimation methods

Not require ‘pre-work’ – i.e. allow for a range of different types of activity data to be used as inputs

Track business performance and give intensity measures

Allow automatic benchmarking & reporting

13

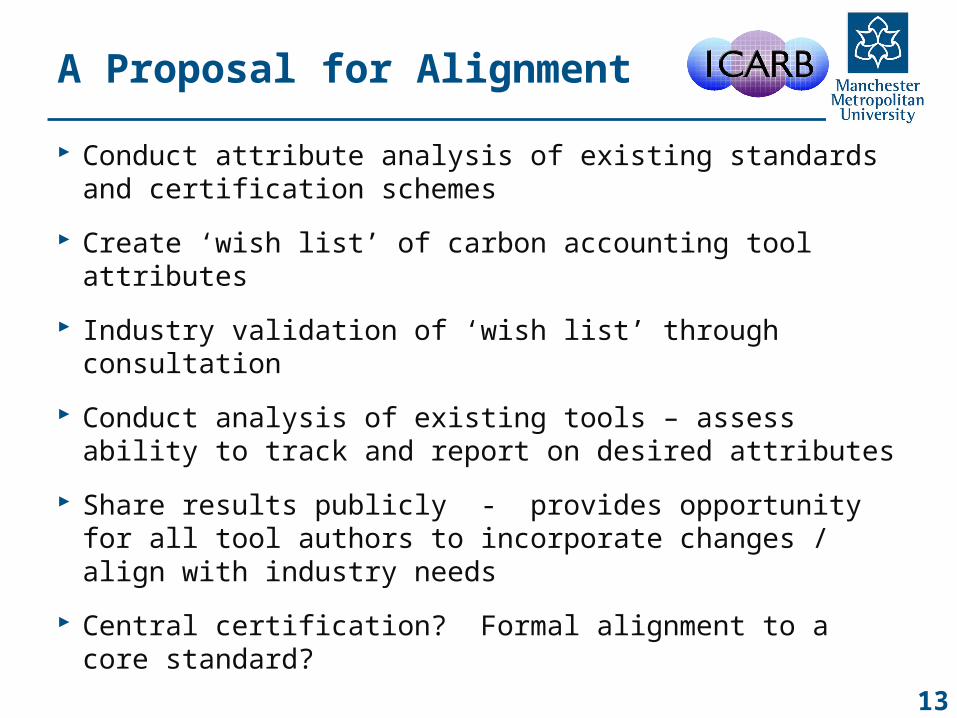

A Proposal for Alignment

Conduct attribute analysis of existing standards and certification schemes

Create ‘wish list’ of carbon accounting tool attributes

Industry validation of ‘wish list’ through consultation

Conduct analysis of existing tools – assess ability to track and report on desired attributes

Share results publicly - provides opportunity for all tool authors to incorporate changes / align with industry needs

Central certification? Formal alignment to a core standard?

14