Embed Size (px)

Citation preview

Chapter 12-1

Chapter 12

Intangible Assets

Acct 3311, Ch 12, Slide 2, © Richard S. Mark

Characteristics No physical substance; Not financial instruments.

Generally long-term assets.

Intangible Assets

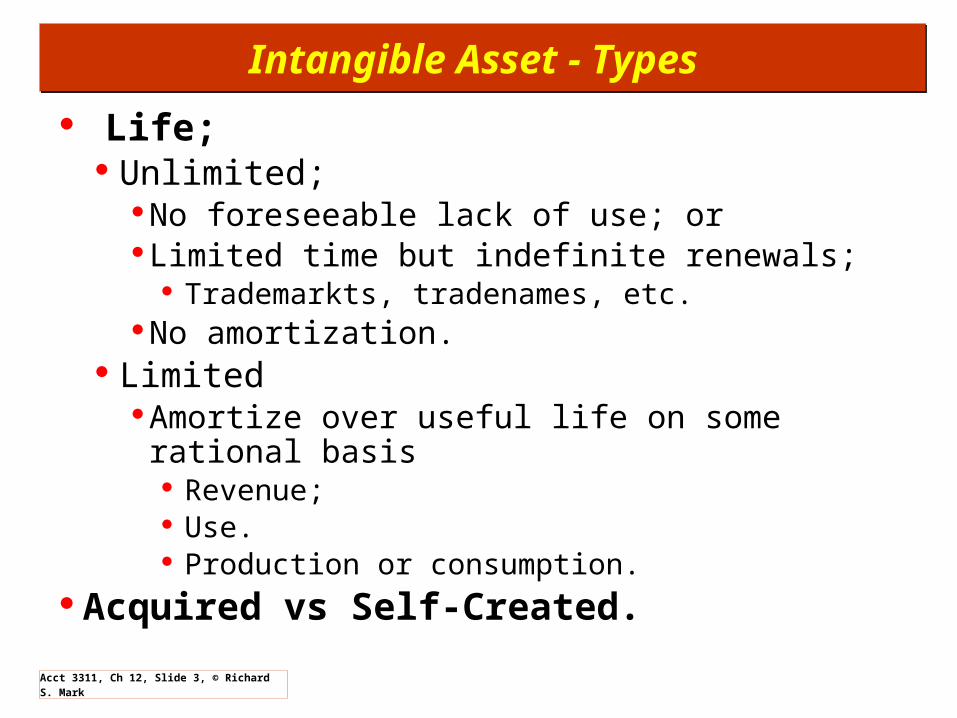

Acct 3311, Ch 12, Slide 3, © Richard S. Mark

Intangible Asset - Types Life;

Unlimited;No foreseeable lack of use; orLimited time but indefinite renewals;

Trademarkts, tradenames, etc.No amortization.

LimitedAmortize over useful life on some rational basis

Revenue; Use. Production or consumption.

Acquired vs Self-Created.

Acct 3311, Ch 12, Slide 4, © Richard S. Mark

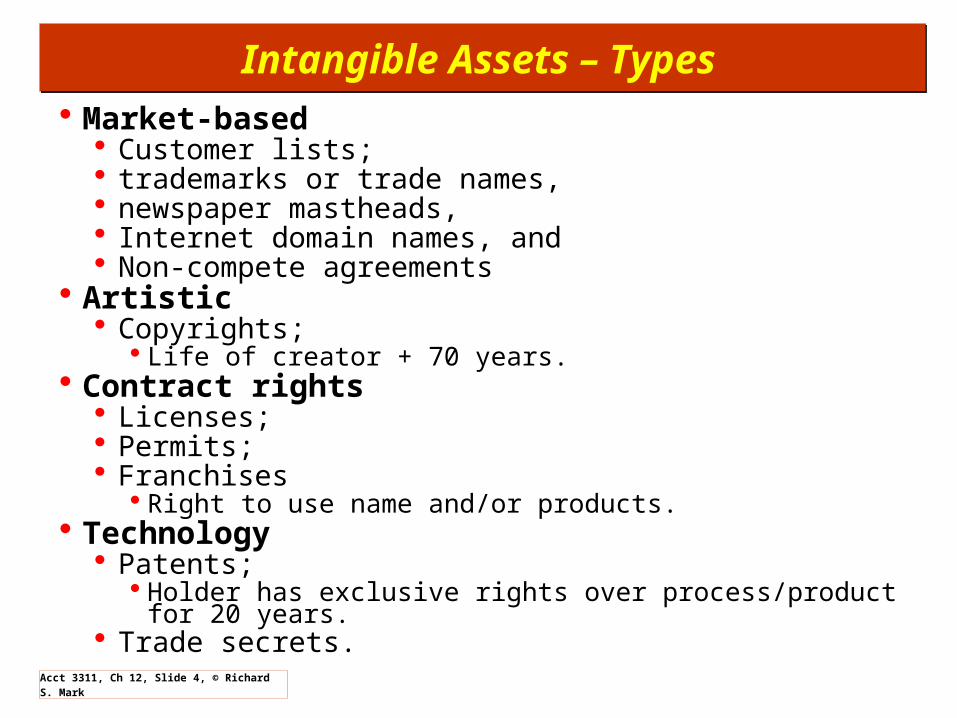

Intangible Assets – Types Market-based

Customer lists; trademarks or trade names, newspaper mastheads, Internet domain names, and Non-compete agreements

Artistic Copyrights;

Life of creator + 70 years. Contract rights

Licenses; Permits; Franchises

Right to use name and/or products. Technology

Patents;Holder has exclusive rights over process/product for 20 years.

Trade secrets.

Acct 3311, Ch 12, Slide 5, © Richard S. Mark

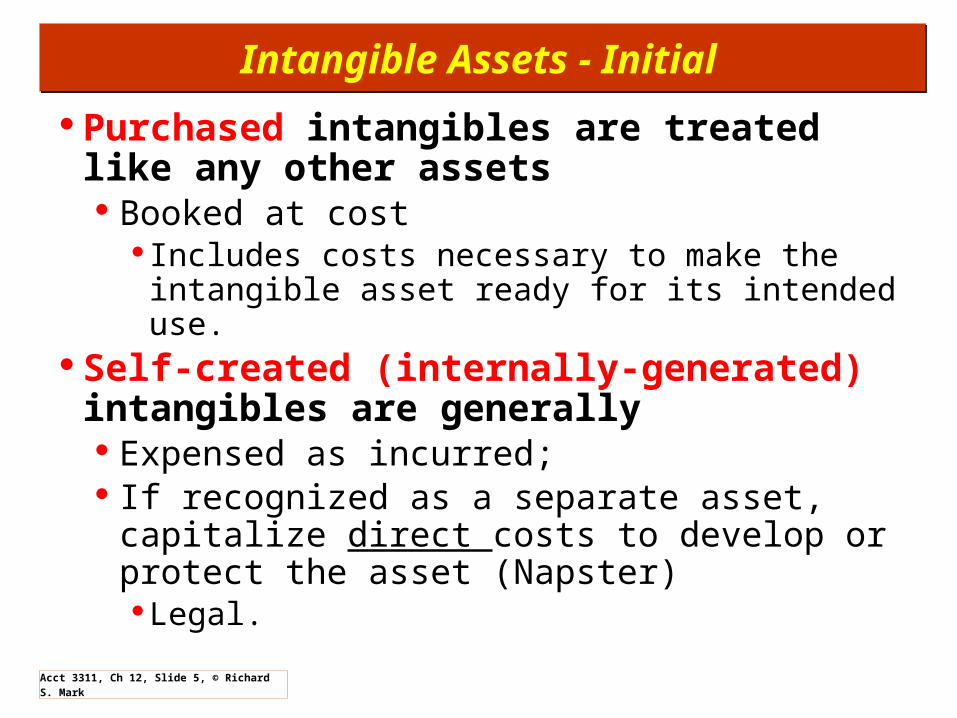

Intangible Assets - InitialPurchased intangibles are treated like any

other assets Booked at cost

Includes costs necessary to make the intangible asset ready for its intended use.

Self-created (internally-generated) intangibles are generally Expensed as incurred; If recognized as a separate asset, capitalize direct

costs to develop or protect the asset (Napster)Legal.

Acct 3311, Ch 12, Slide 6, © Richard S. Mark

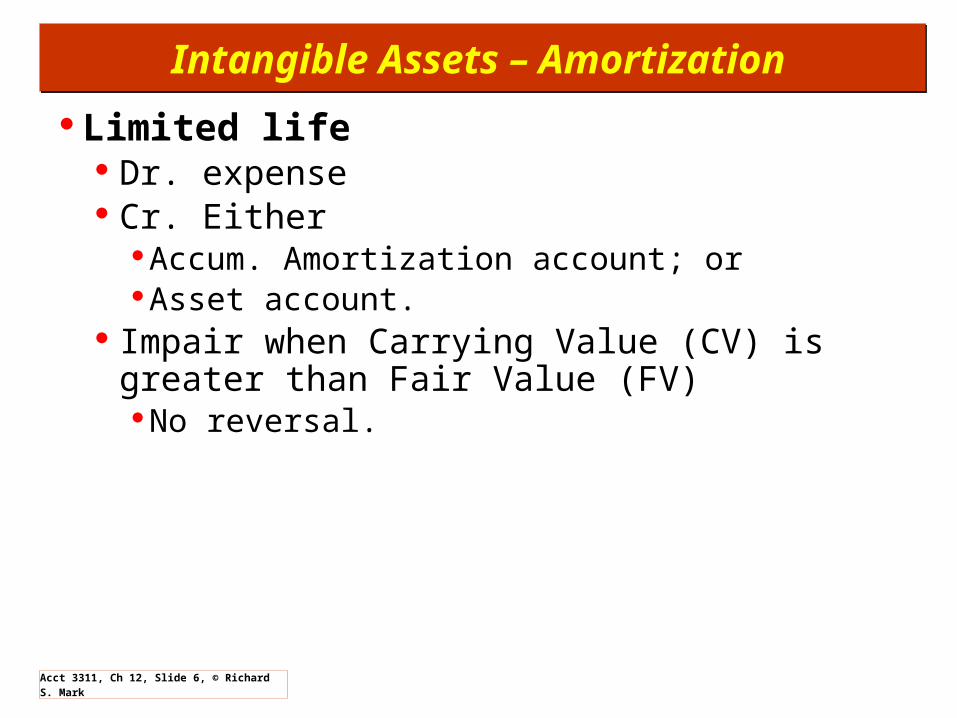

Intangible Assets – AmortizationLimited life

Dr. expense Cr. Either

Accum. Amortization account; orAsset account.

Impair when Carrying Value (CV) is greater than Fair Value (FV)No reversal.

Acct 3311, Ch 12, Slide 7, © Richard S. Mark

Green Market Inc. acquires the customer list of a large newspaper for $6,000,000 on January 1, 2010. Green Market expects to benefit from the information evenly over a three-year period.

Customer List ________Jan. 1

Cash _________

Customer list expense ________Dec. 31

201020112012

Customer list_________

Limited Life Intangibles - Amortization

Acct 3311, Ch 12, Slide 8, © Richard S. Mark

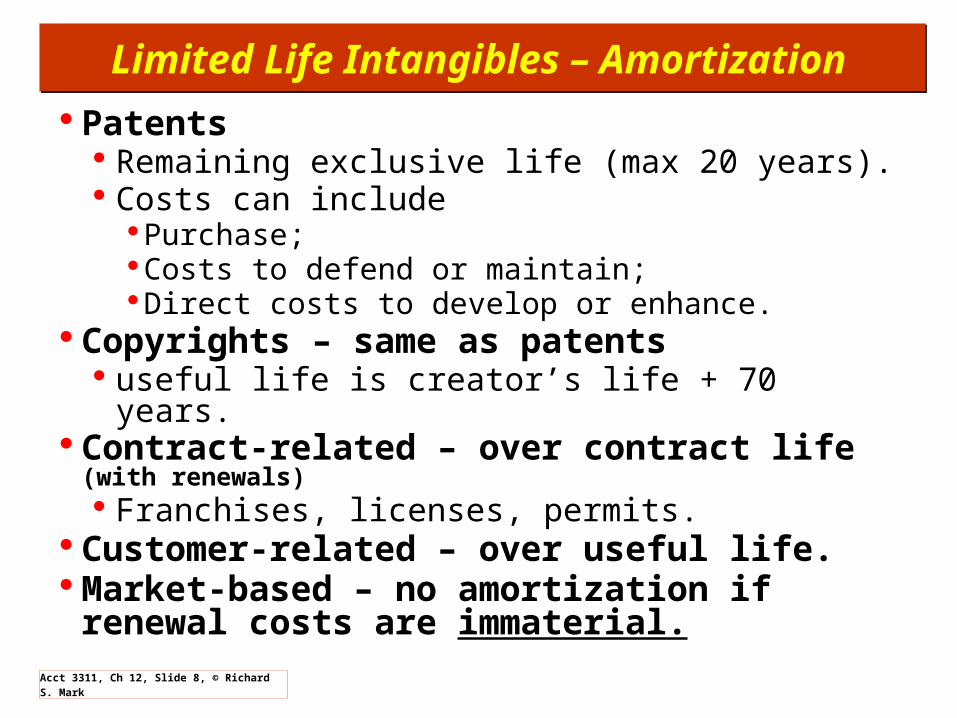

Limited Life Intangibles – AmortizationPatents

Remaining exclusive life (max 20 years). Costs can include

Purchase;Costs to defend or maintain;Direct costs to develop or enhance.

Copyrights – same as patents useful life is creator’s life + 70 years.

Contract-related – over contract life (with renewals) Franchises, licenses, permits.

Customer-related – over useful life. Market-based – no amortization if renewal

costs are immaterial.

Acct 3311, Ch 12, Slide 9, © Richard S. Mark

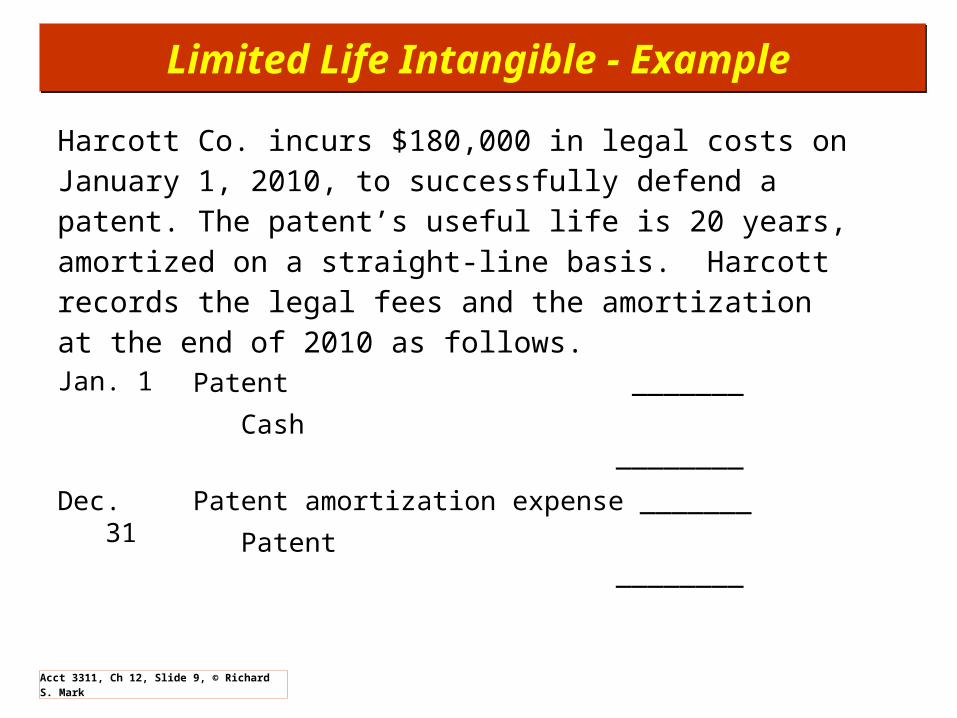

Harcott Co. incurs $180,000 in legal costs on January 1, 2010, to successfully defend a patent. The patent’s useful life is 20 years, amortized on a straight-line basis. Harcott records the legal fees and the amortization at the end of 2010 as follows.

Patent _______Jan. 1

Cash ________

Patent amortization expense _______Dec. 31

Patent________

Limited Life Intangible - Example

Acct 3311, Ch 12, Slide 10, © Richard S. Mark

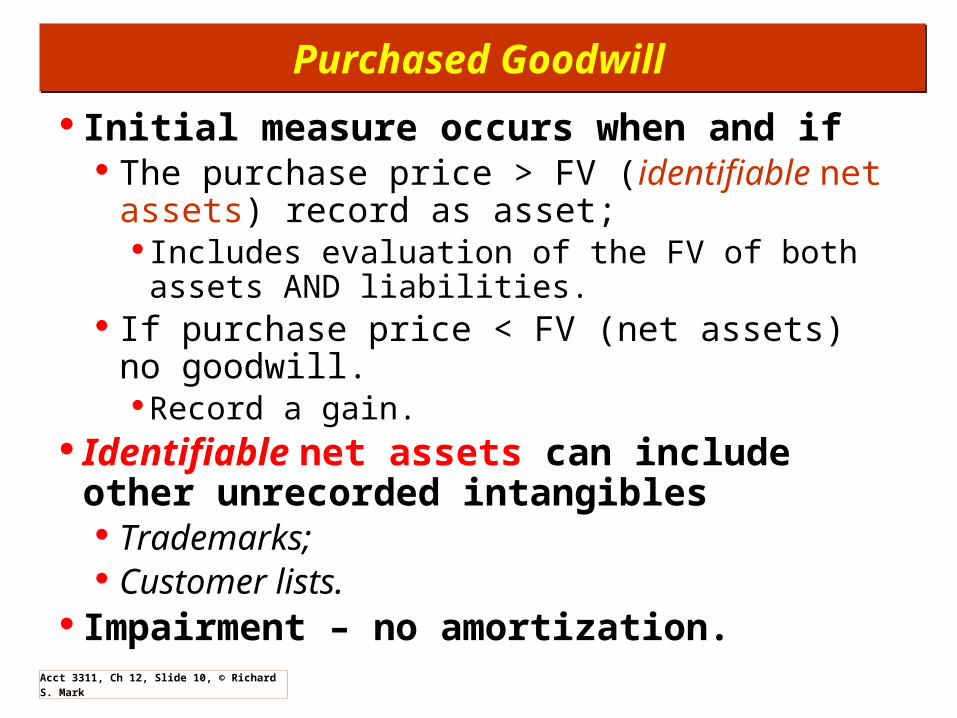

Purchased Goodwill Initial measure occurs when and if

The purchase price > FV (identifiable net assets) record as asset;Includes evaluation of the FV of both assets AND

liabilities. If purchase price < FV (net assets) no goodwill.

Record a gain. Identifiable net assets can include other

unrecorded intangibles Trademarks; Customer lists.

Impairment – no amortization.

Acct 3311, Ch 12, Slide 11, © Richard S. Mark

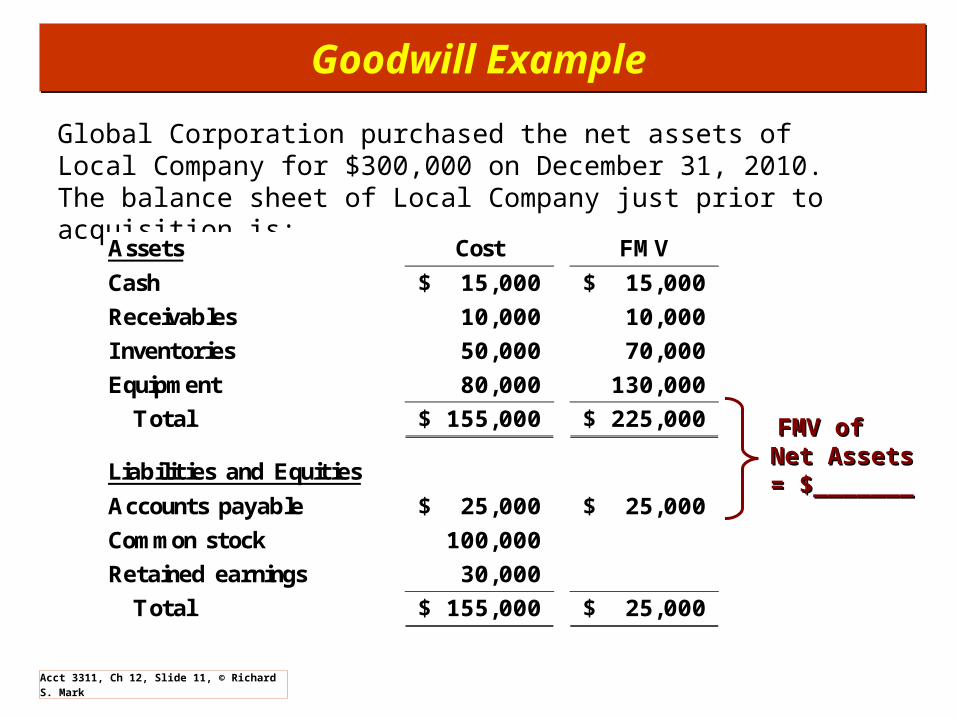

Global Corporation purchased the net assets of Local Company for $300,000 on December 31, 2010. The balance sheet of Local Company just prior to acquisition is:

Assets Cost FMV

Cash 15,000$ 15,000$

Receivables 10,000 10,000

I nventories 50,000 70,000

Equipment 80,000 130,000

Total 155,000$ 225,000$

Liabilities and Equities

Accounts payable 25,000$ 25,000$

Common stock 100,000

Retained earnings 30,000

Total 155,000$ 25,000$

FMV of FMV of Net Assets Net Assets = $_______= $_______

Goodwill Example

Acct 3311, Ch 12, Slide 12, © Richard S. Mark

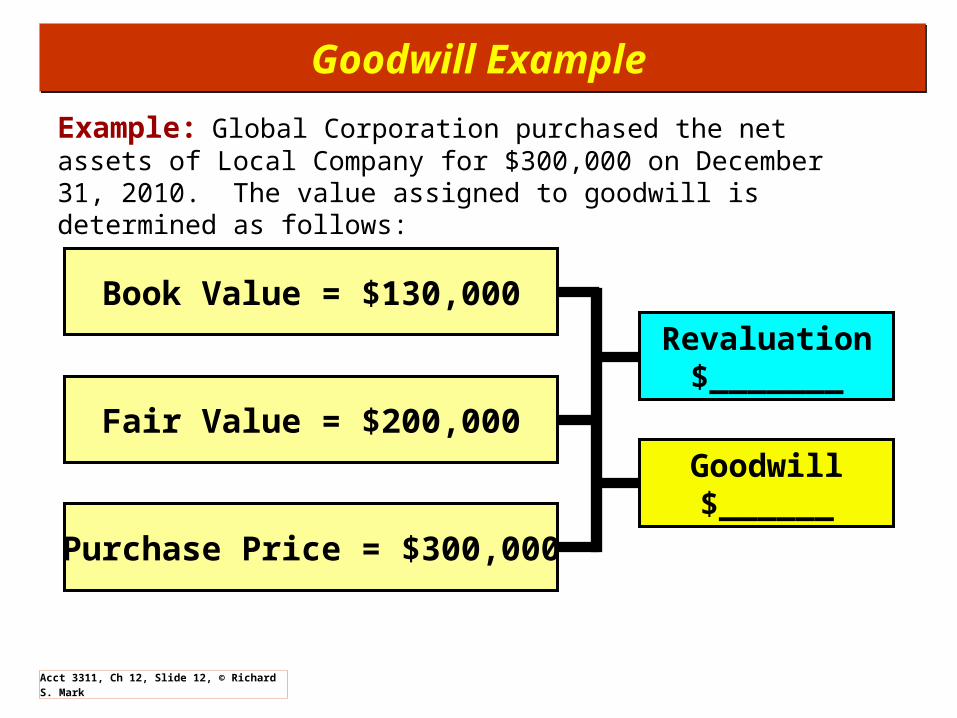

Book Value = $130,000

Fair Value = $200,000

Purchase Price = $300,000

Revaluation$_______

Goodwill$______

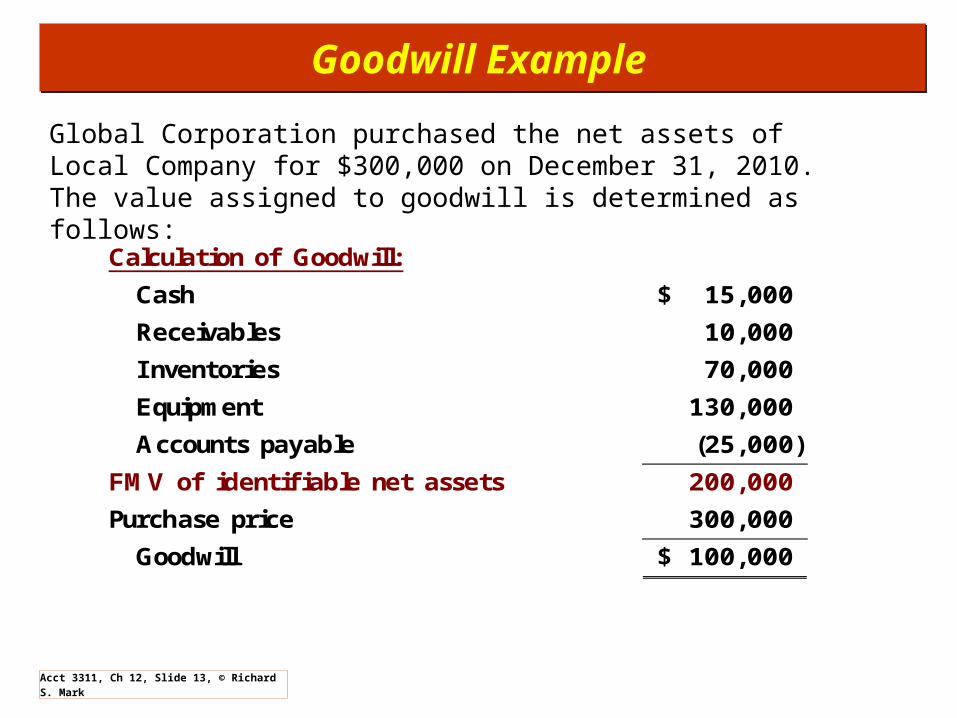

Example: Global Corporation purchased the net assets of Local Company for $300,000 on December 31, 2010. The value assigned to goodwill is determined as follows:

Goodwill Example

Acct 3311, Ch 12, Slide 13, © Richard S. Mark

Global Corporation purchased the net assets of Local Company for $300,000 on December 31, 2010. The value assigned to goodwill is determined as follows:

Calculation of Goodwill:

Cash 15,000$

Receivables 10,000

I nventories 70,000

Equipment 130,000

Accounts payable (25,000)

FMV of identifiable net assets 200,000

Purchase price 300,000

Goodwill 100,000$

Goodwill Example

Acct 3311, Ch 12, Slide 14, © Richard S. Mark

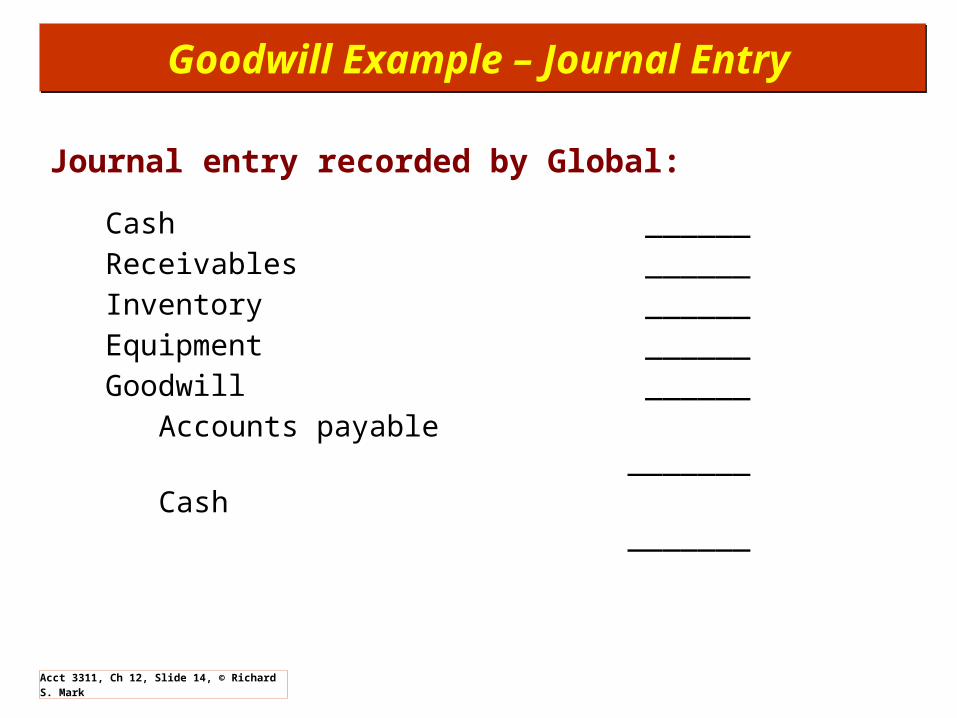

Journal entry recorded by Global:

Cash ______Receivables ______Inventory ______Equipment ______Goodwill ______

Accounts payable_______

Cash_______

Goodwill Example – Journal Entry

Acct 3311, Ch 12, Slide 15, © Richard S. Mark

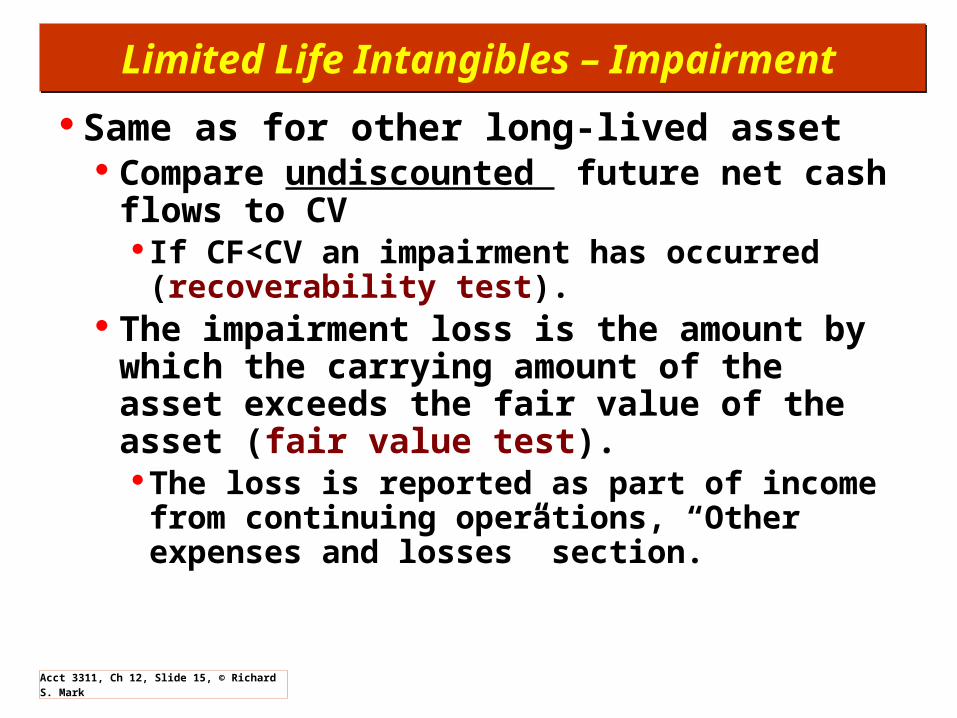

Limited Life Intangibles – ImpairmentSame as for other long-lived asset

Compare undiscounted future net cash flows to CV If CF<CV an impairment has occurred

(recoverability test). The impairment loss is the amount by which

the carrying amount of the asset exceeds the fair value of the asset (fair value test).The loss is reported as part of income from

continuing operations, “Other expenses and losses” section.

Acct 3311, Ch 12, Slide 16, © Richard S. Mark

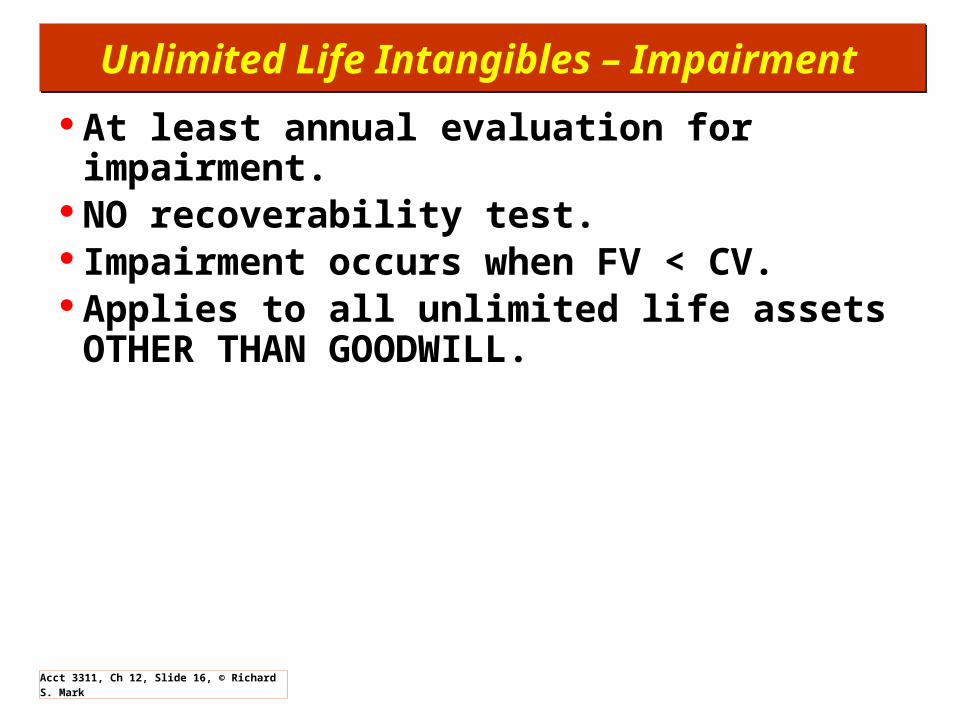

Unlimited Life Intangibles – ImpairmentAt least annual evaluation for impairment.

NO recoverability test. Impairment occurs when FV < CV.Applies to all unlimited life assets OTHER

THAN GOODWILL.

Acct 3311, Ch 12, Slide 17, © Richard S. Mark

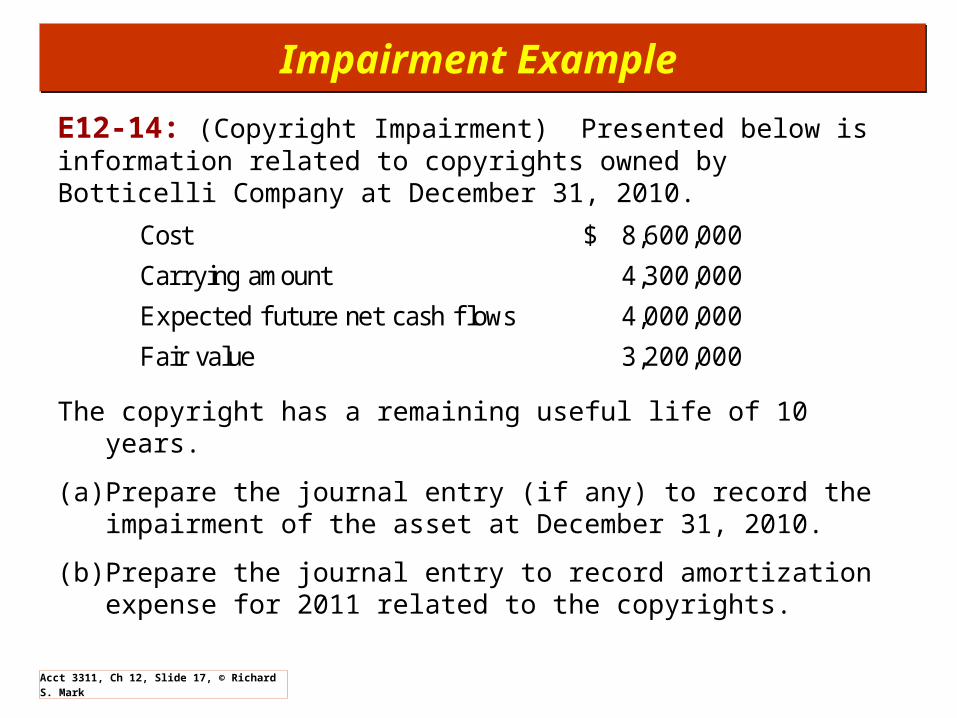

E12-14: (Copyright Impairment) Presented below is information related to copyrights owned by Botticelli Company at December 31, 2010.

Cost 8,600,000$

Carrying amount 4,300,000

Expected f uture net cash flows 4,000,000

Fair value 3,200,000

The copyright has a remaining useful life of 10 years.

(a) Prepare the journal entry (if any) to record the impairment of the asset at December 31, 2010.

(b) Prepare the journal entry to record amortization expense for 2011 related to the copyrights.

Impairment Example

Acct 3311, Ch 12, Slide 18, © Richard S. Mark

Compare expected future net cash flows to the carrying amount of the asset.

Expected f uture cash flow 4,000,000$

Carrying value 4,300,000

(300,000)$

Asset _______________Asset _______________

Impairment Example(2) - Recoverability

Acct 3311, Ch 12, Slide 19, © Richard S. Mark

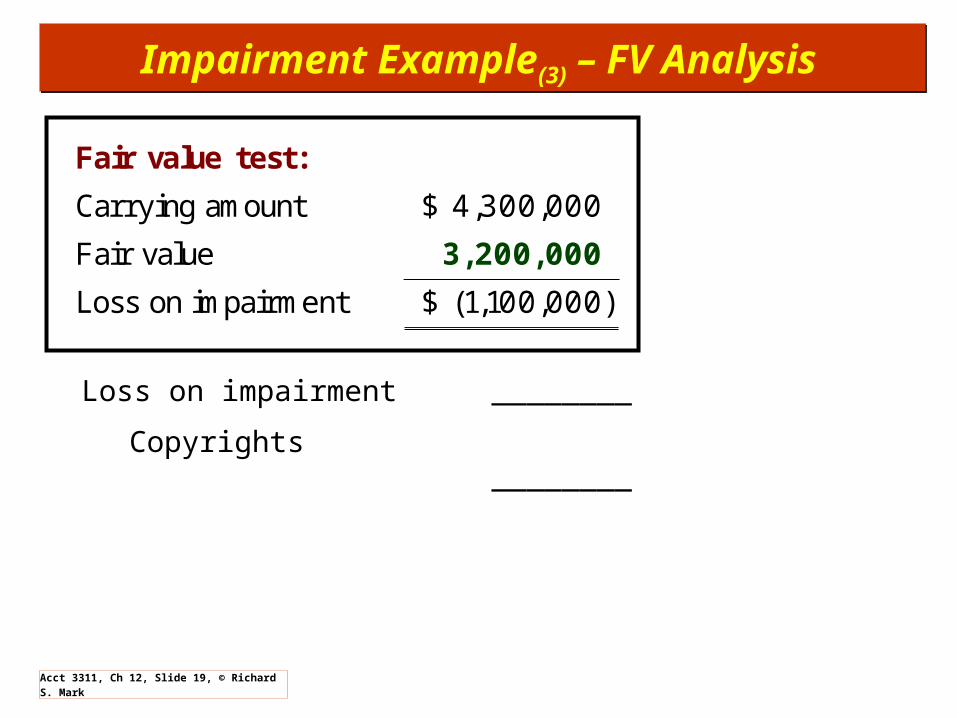

Fair value test:

Carrying amount 4,300,000$

Fair value 3,200,000

Loss on impairment (1,100,000)$

Loss on impairment ________

Copyrights ________

Impairment Example(3) – FV Analysis

Acct 3311, Ch 12, Slide 20, © Richard S. Mark

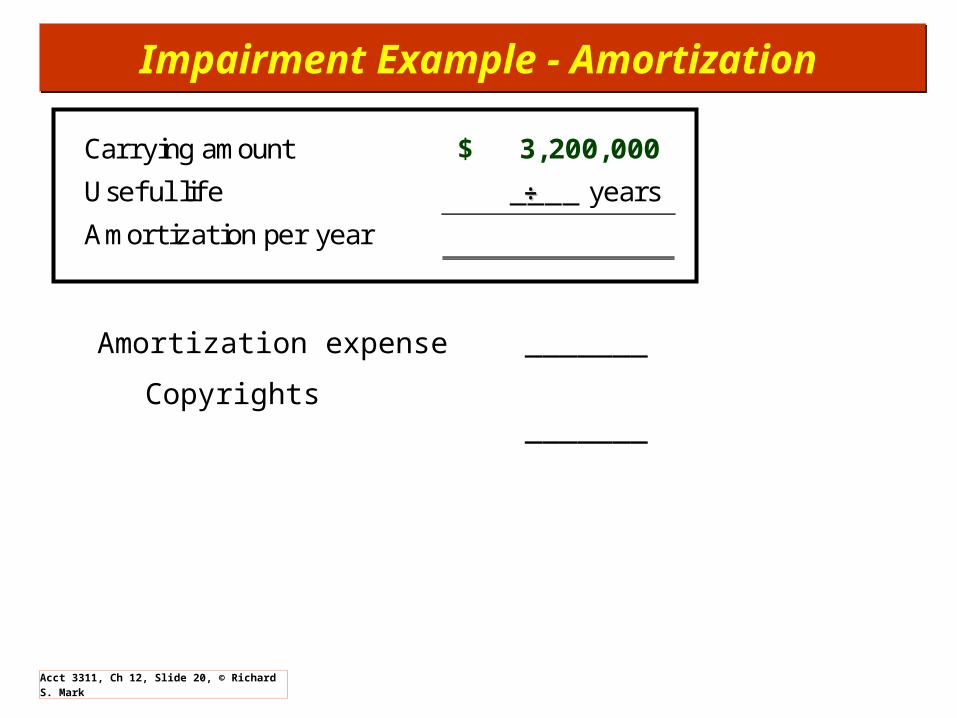

Carrying amount 3,200,000$

Usef ul lif e ____ years

Amortization per year

÷÷

Amortization expense _______

Copyrights _______

Impairment Example - Amortization

Acct 3311, Ch 12, Slide 21, © Richard S. Mark

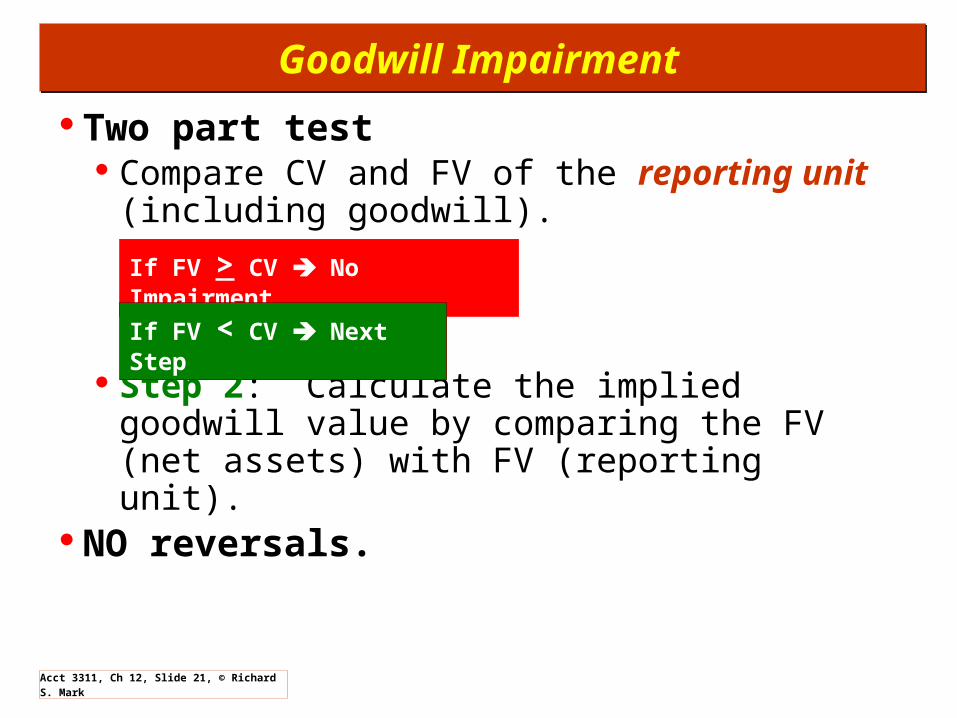

Goodwill ImpairmentTwo part test

Compare CV and FV of the reporting unit (including goodwill).

Step 2: Calculate the implied goodwill value by

comparing the FV (net assets) with FV (reporting unit).

NO reversals.

If FV > CV No ImpairmentIf FV < CV Next Step

Acct 3311, Ch 12, Slide 22, © Richard S. Mark

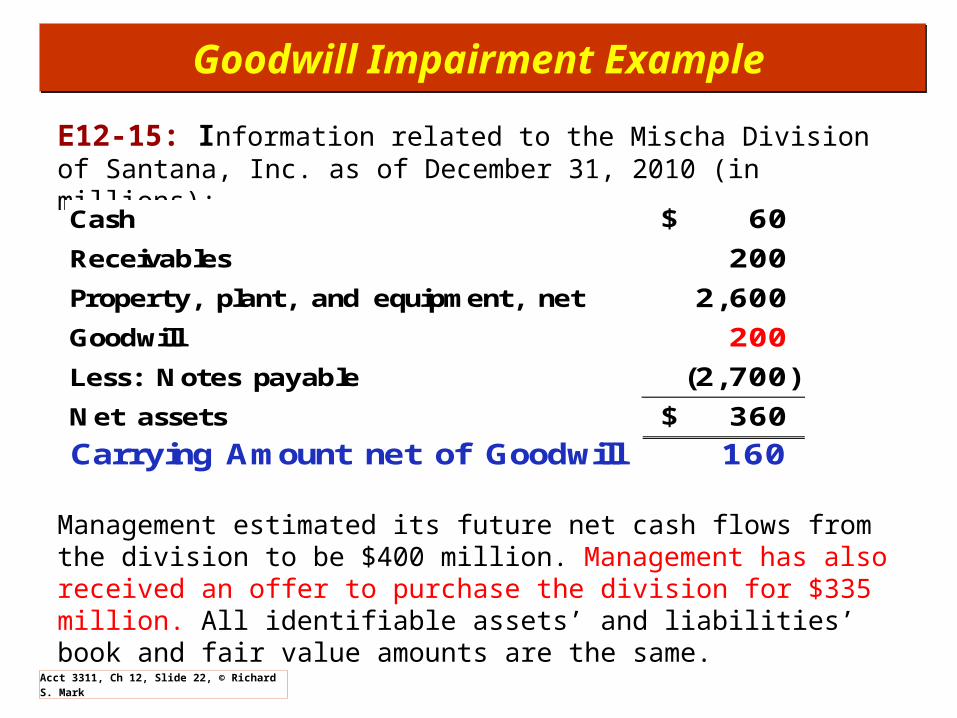

E12-15: Information related to the Mischa Division of Santana, Inc. as of December 31, 2010 (in millions):

Cash 60$

Receivables 200

Property, plant, and equipment, net 2,600

Goodwill 200

Less: Notes payable (2,700)

Net assets 360$

160 Carrying Amount net of Goodwill

Management estimated its future net cash flows from the division to be $400 million. Management has also received an offer to purchase the division for $335 million. All identifiable assets’ and liabilities’ book and fair value amounts are the same.

Goodwill Impairment Example

Acct 3311, Ch 12, Slide 23, © Richard S. Mark

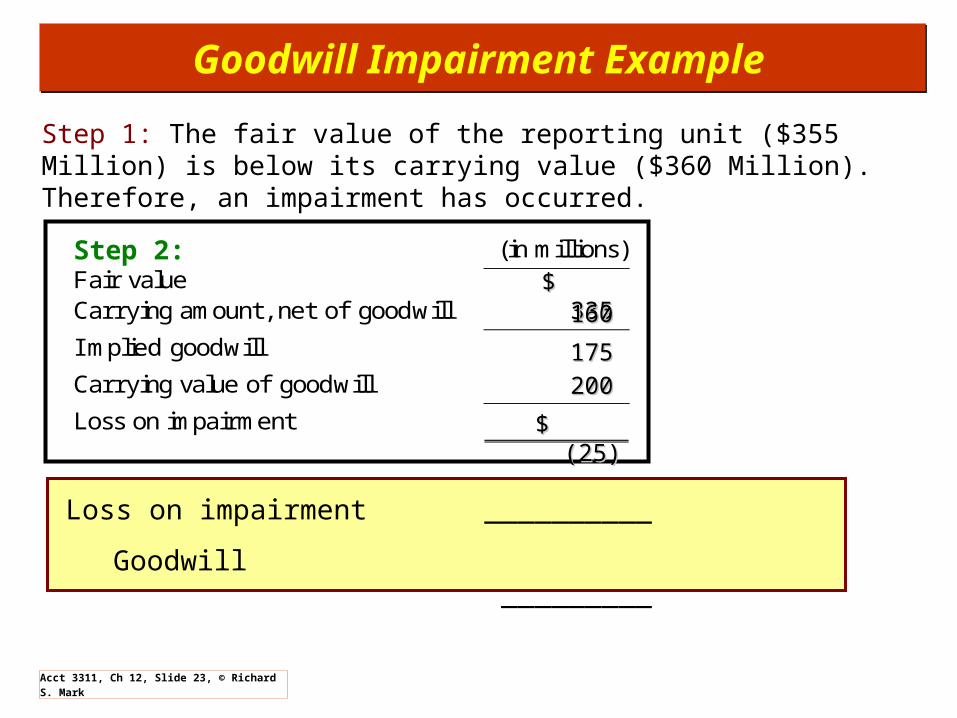

(in millions)Fair valueCarrying amount, net of goodwill

I mplied goodwill

Carrying value of goodwill

Loss on impairment

Step 1: The fair value of the reporting unit ($355 Million) is below its carrying value ($360 Million). Therefore, an impairment has occurred.

Step 2:

Loss on impairment __________

Goodwill _________

$ 335$ 335160160

175175200200

$ (25)$ (25)

Goodwill Impairment Example

Acct 3311, Ch 12, Slide 24, © Richard S. Mark

Research and Development Distinguish between

Research – activities associated with acquiring new knowledge; and

Development – converting the research to practical and profitable results for the business through Improved

processes; Products.

New products;Improved efficiencies in production process.

All are expensed as incurred.

Acct 3311, Ch 12, Slide 25, © Richard S. Mark

R&D CostsMaterials, Equipment, and Facilities

unless the R&D equipment or facility has future alternative uses- if so capitalize and apply depreciation to R&D.

Personnel;Purchased Intangibles used only for R&D;Contract Services for specific R&D activity;Reasonable allocation of indirect costs.

Acct 3311, Ch 12, Slide 26, © Richard S. Mark

Other Intangible CostsStart-up costs for a new operation.

Expense in period incurred Include organization costs

Legal & filing fees to incorporateAdvertising costs.

Expense in period incurredComputer software costs.

Expense before technological feasibility established