Embed Size (px)

Citation preview

The Dbriefs Financial Reporting series presents:

SEC hot topics

Bob Uhl, Partner, national office – Accounting ServicesMark Bolton, Director, national office- Accounting ServicesKathleen Malone, Director, national office- SEC ServicesHero Alimchandani, Senior Manager, national office- SEC Services

November 13, 2015

2 Copyright © 2015 Deloitte Development LLC. All rights reserved.

SEC updateAgenda

• SEC overview, current landscape and rulemaking

• Disclosure effectiveness

• SEC review process

• SEC comment trends

• Question and answer

3 Copyright © 2015 Deloitte Development LLC. All rights reserved.

This webcast does not provide official Deloitte & Touche LLP interpretive accounting guidance.

Check with a qualified advisor before taking any action.

See later slides for information on obtaining written summaries of issues discussed today.

Keep in mind

4 Copyright © 2015 Deloitte Development LLC. All rights reserved.

To enhance participants’ understanding of important accounting issues and developments pertaining to recent actions of the SEC and others.

Learning objective

5 Copyright © 2015 Deloitte Development LLC. All rights reserved.

How often in the last three years have you had interactions with the SEC staff?

• None• Once or twice• Annually• More than once a year• N/A

Poll question #1

SEC overview, current landscape,rulemaking

7 Copyright © 2015 Deloitte Development LLC. All rights reserved.

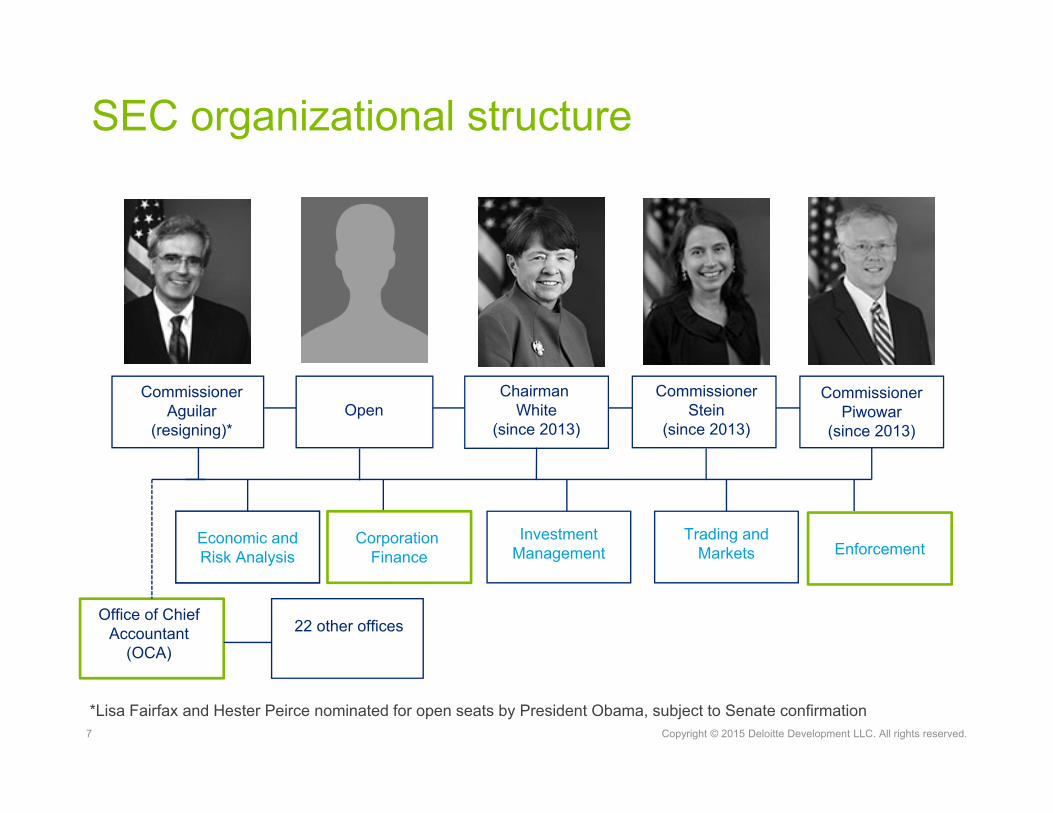

SEC organizational structure

Chairman White

(since 2013)

CommissionerPiwowar

(since 2013)Open

CorporationFinance

InvestmentManagement

Office of Chief Accountant

(OCA)

Trading and Markets

CommissionerStein

(since 2013)

22 other offices

Corporation Finance

Economic and Risk Analysis Enforcement

Commissioner Aguilar

(resigning)*

*Lisa Fairfax and Hester Peirce nominated for open seats by President Obama, subject to Senate confirmation

8 Copyright © 2015 Deloitte Development LLC. All rights reserved.

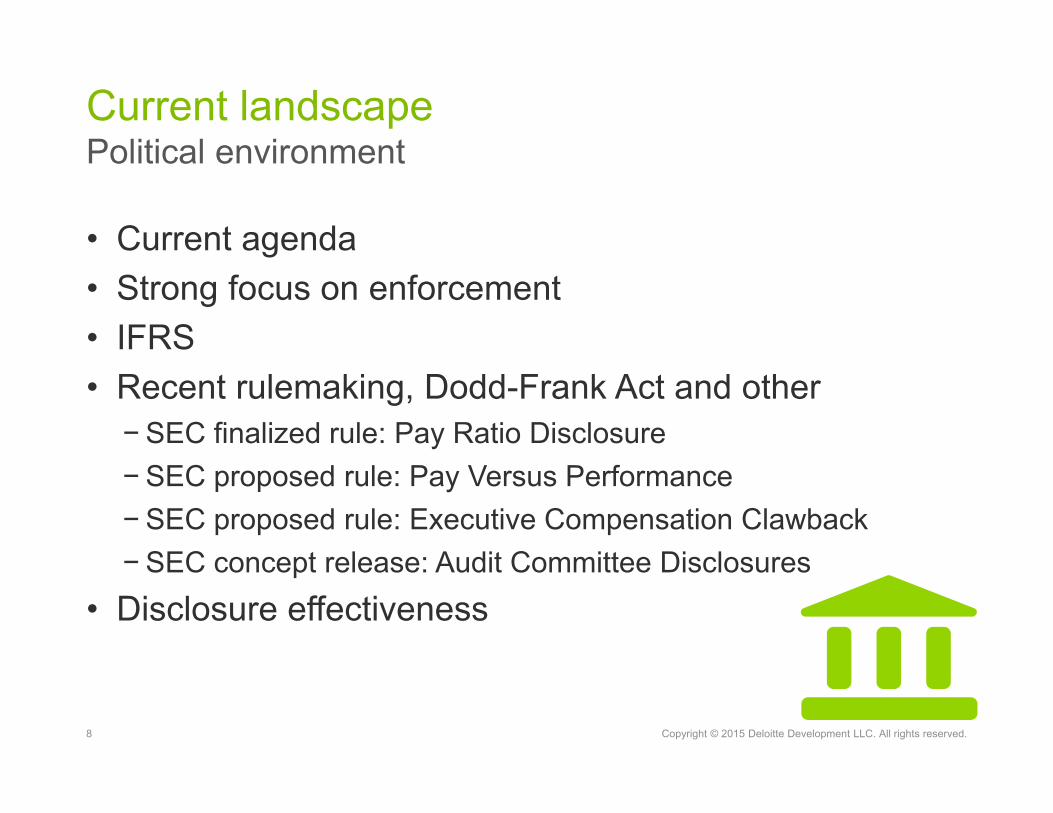

Political environmentCurrent landscape

• Current agenda• Strong focus on enforcement• IFRS• Recent rulemaking, Dodd-Frank Act and other

− SEC finalized rule: Pay Ratio Disclosure− SEC proposed rule: Pay Versus Performance− SEC proposed rule: Executive Compensation Clawback− SEC concept release: Audit Committee Disclosures

• Disclosure effectiveness

9 Copyright © 2015 Deloitte Development LLC. All rights reserved.

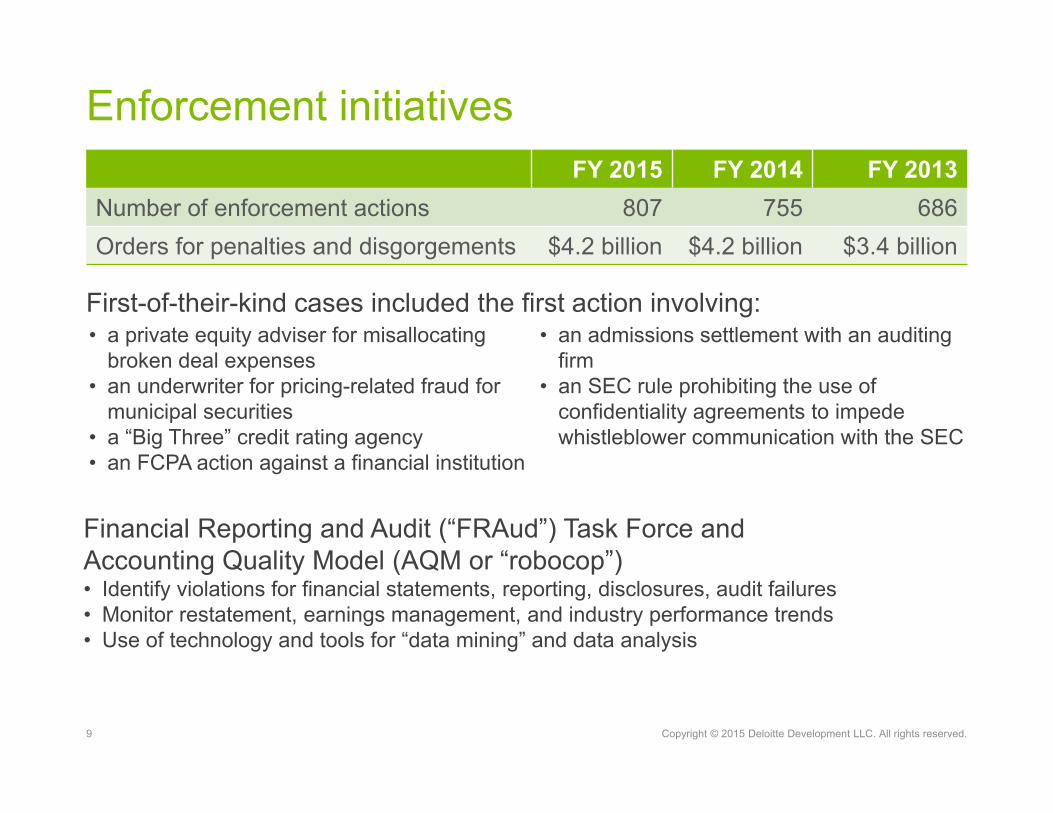

Financial Reporting and Audit (“FRAud”) Task Force and Accounting Quality Model (AQM or “robocop”)• Identify violations for financial statements, reporting, disclosures, audit failures• Monitor restatement, earnings management, and industry performance trends• Use of technology and tools for “data mining” and data analysis

Enforcement initiativesFY 2015 FY 2014 FY 2013

Number of enforcement actions 807 755 686Orders for penalties and disgorgements $4.2 billion $4.2 billion $3.4 billion

First-of-their-kind cases included the first action involving: • a private equity adviser for misallocating

broken deal expenses • an underwriter for pricing-related fraud for

municipal securities • a “Big Three” credit rating agency • an FCPA action against a financial institution

• an admissions settlement with an auditing firm

• an SEC rule prohibiting the use of confidentiality agreements to impede whistleblower communication with the SEC

10 Copyright © 2015 Deloitte Development LLC. All rights reserved.

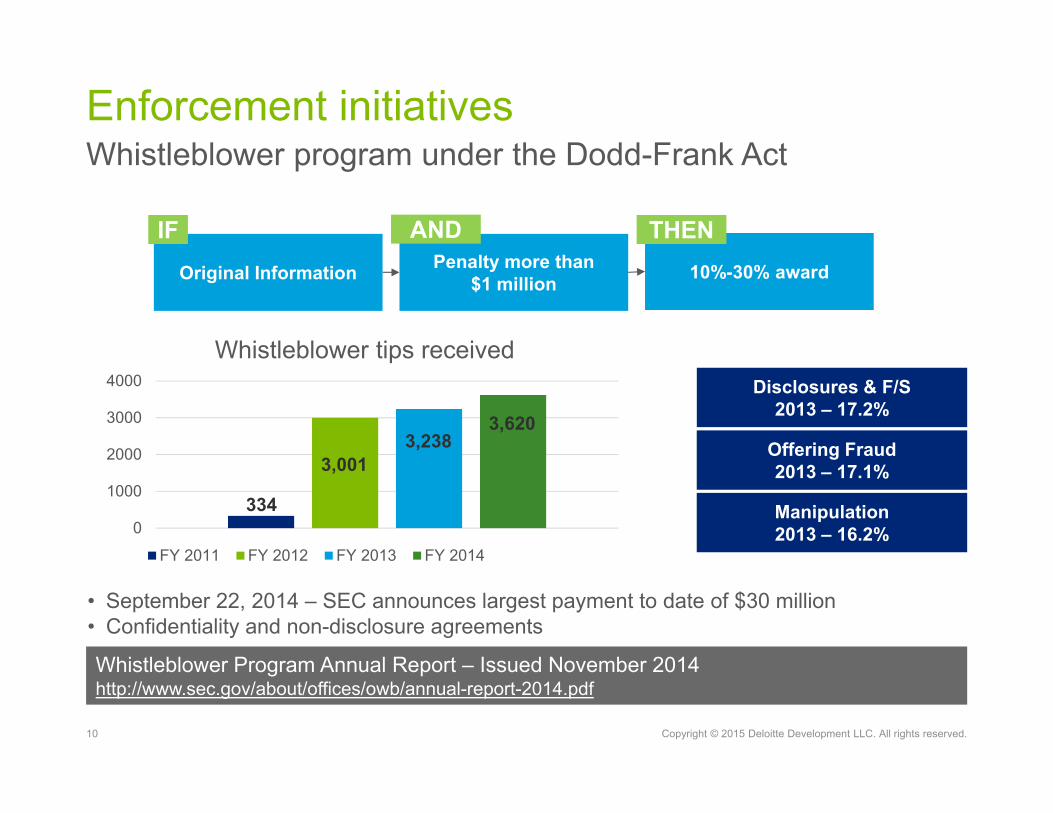

Whistleblower program under the Dodd-Frank ActEnforcement initiatives

• September 22, 2014 – SEC announces largest payment to date of $30 million• Confidentiality and non-disclosure agreements

Whistleblower Program Annual Report – Issued November 2014 http://www.sec.gov/about/offices/owb/annual-report-2014.pdf

Disclosures & F/S2013 – 17.2%

Offering Fraud2013 – 17.1%

Manipulation2013 – 16.2%0

1000

2000

3000

4000

Whistleblower tips received

FY 2011 FY 2012 FY 2013 FY 2014

Penalty more than$1 million 10%-30% awardOriginal Information

IF AND THEN

334

3,0013,238

3,620

11 Copyright © 2015 Deloitte Development LLC. All rights reserved.

If you have a question on a form and content matter in a Form S-1 registration statement during the initial offering process, which part of the SEC would you be dealing with?

• Division of Corporation Finance• Division of Enforcement• Office of Chief Accountant (OCA)• Division of Investment Management • None of the above

Poll question #2

12 Copyright © 2015 Deloitte Development LLC. All rights reserved.

CAQ SEC Regulations Committee meetings• CF-OCA associate chief accountants now assigned by topics• Merger of Financial Services industry review (AD) groups• Financial reporting for spin-offs• Requests to review incomplete filings

Recent rulemaking - Dodd-Frank Act• Continued effort on required rulemaking• Recent rulemaking

• SEC final rule: Pay ratio disclosure• SEC proposed rule: Pay versus performance• SEC proposed rule: Executive compensation “clawback”• SEC concept release: Audit committee disclosures• SEC final rule: Crowdfunding

SEC reporting update & rulemaking initiatives

13 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• Finalized • Ratio of the median of the annual total compensation of all employees to

the annual total CEO compensation• In any filing that requires Item 402 executive compensation disclosures• Definition of employee• The three-month rule• Identify median employee once every three years• Disclose ratio no later than 120 days after fiscal year end• Effective fiscal year beginning on or after January 2017

Pay ratio disclosure

14 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• When is a “clawback” required? − In the event of a restatement− Culpability not required

• “Excess” IBC (incentive-based compensation)• Applies to current and former executive officers• Three-year look-back period for recovery• Comments were due by September 14• Challenges when using stock price or total shareholder return as a basis• Accounting implications

− Diverse views

Refer to our Heads Up issued on August 5

“Clawback” proposal

15 Copyright © 2015 Deloitte Development LLC. All rights reserved.

• SEC’s concept release: audit committee disclosures

• Requests comments on 74 questions• Audit committee’s oversight of the auditor• Audit committee’s process for appointing/retaining the auditor• Qualifications of the audit firm• Comments were due September 8• SEC speech- “…commenters questioned whether a potential lack of

Commission action to improve disclosures would result in a shift back to the previous practice of generally only disclosing the minimum information required.”

Audit committee matters

16 Copyright © 2015 Deloitte Development LLC. All rights reserved.

In the next section, we are going to cover the SEC’s recent focus on disclosure effectiveness. Based on the SEC’s request for comments on Regulation S-X as it relates to entities other than the registrant (acquirees, investees, guarantors, etc.), with which of the following does your company most struggle (choose only one):

• Applying the significant subsidiary tests • Ability to obtain or provide the required other entity financial statements

or information• Ability to get financial statements of other entities audited in accordance

with the appropriate auditing requirements • Preparing condensed consolidating financial information for guarantors

and issuers• Don’t know or N/A

Poll question #3

Disclosure effectiveness

18 Copyright © 2015 Deloitte Development LLC. All rights reserved.

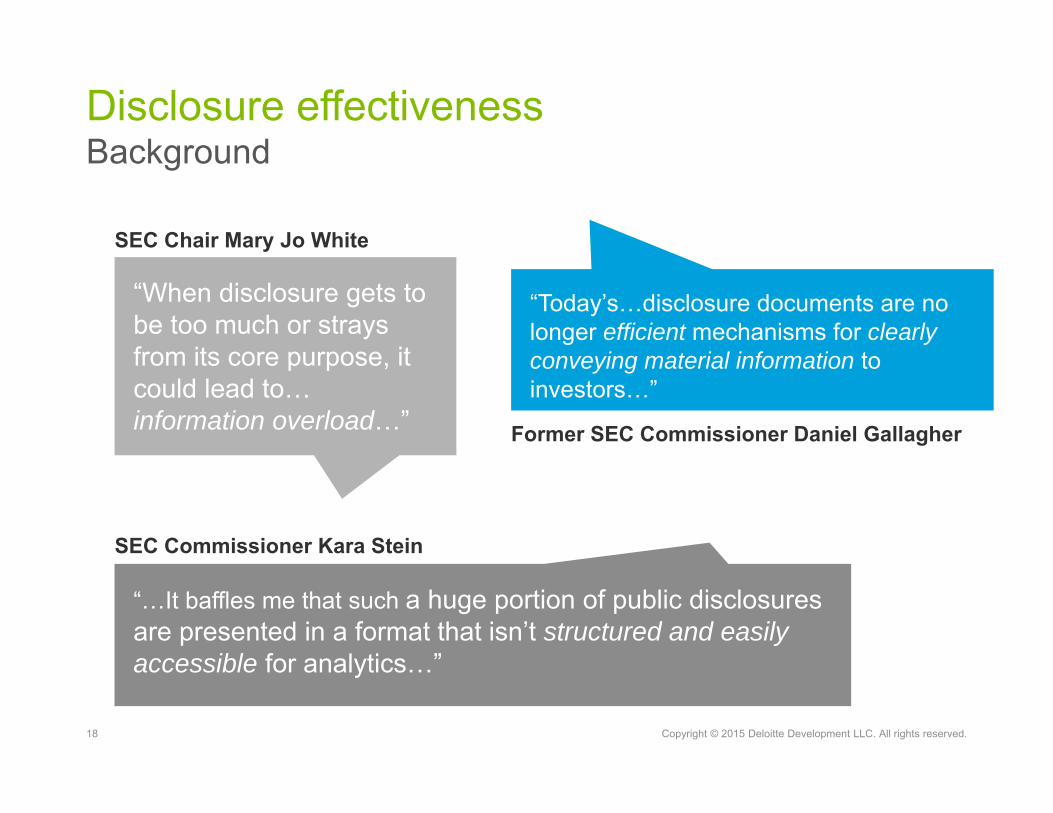

BackgroundDisclosure effectiveness

“When disclosure gets to be too much or strays from its core purpose, it could lead to… information overload…”

“…It baffles me that such a huge portion of public disclosures are presented in a format that isn’t structured and easily accessible for analytics…”

“Today’s…disclosure documents are no longer efficient mechanisms for clearly conveying material information to investors…”

SEC Chair Mary Jo White

Former SEC Commissioner Daniel Gallagher

SEC Commissioner Kara Stein

19 Copyright © 2015 Deloitte Development LLC. All rights reserved.

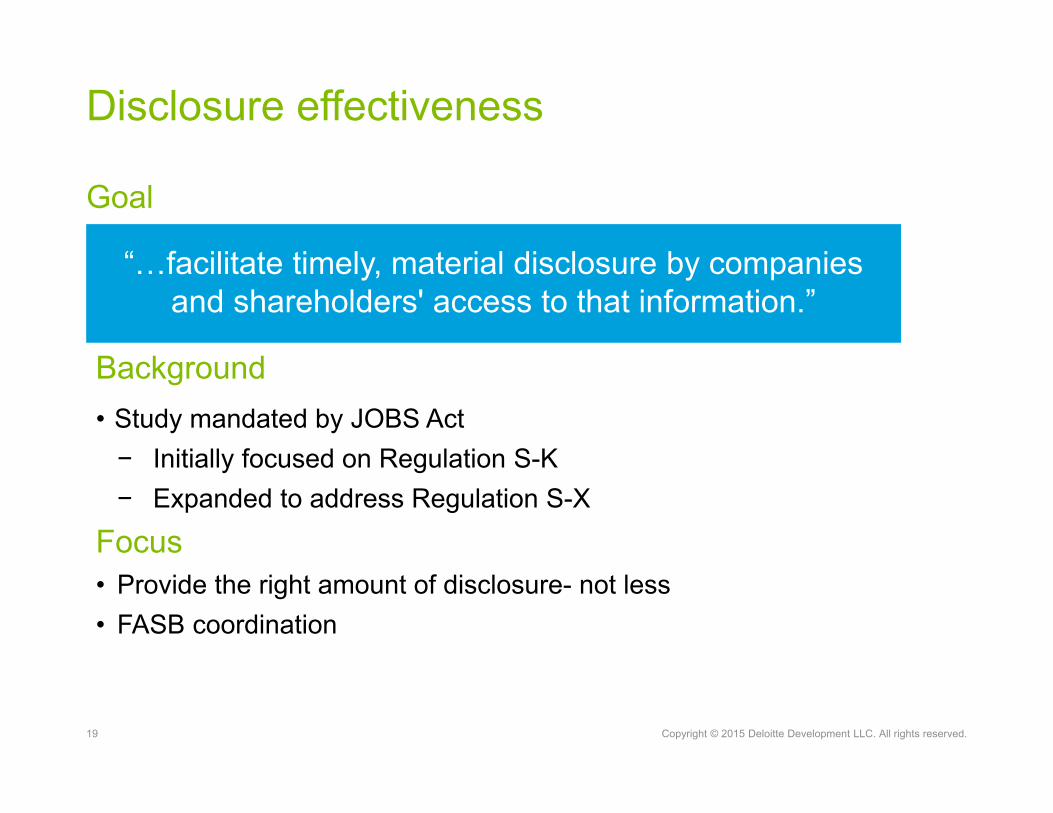

Disclosure effectiveness

Background• Study mandated by JOBS Act

− Initially focused on Regulation S-K− Expanded to address Regulation S-X

Focus • Provide the right amount of disclosure- not less• FASB coordination

“…facilitate timely, material disclosure by companies and shareholders' access to that information.”

Goal

Copyright © 2015 Deloitte Development LLC. All rights reserved.

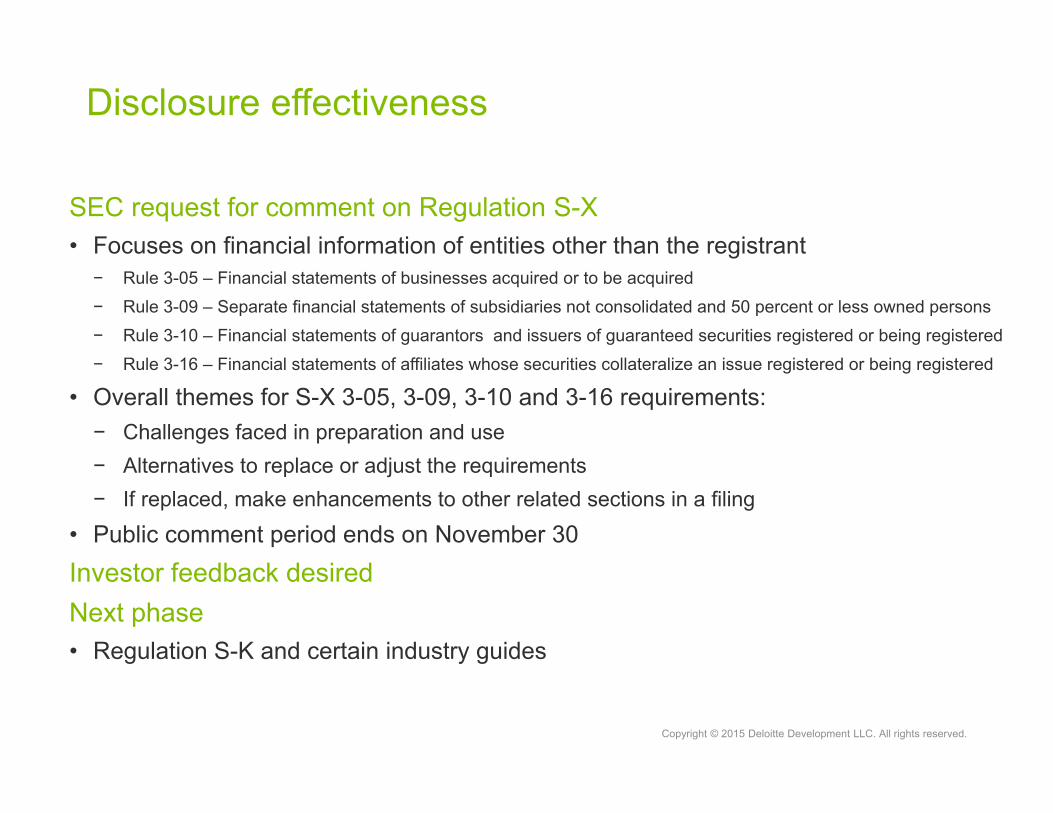

SEC request for comment on Regulation S-X• Focuses on financial information of entities other than the registrant

− Rule 3-05 – Financial statements of businesses acquired or to be acquired− Rule 3-09 – Separate financial statements of subsidiaries not consolidated and 50 percent or less owned persons− Rule 3-10 – Financial statements of guarantors and issuers of guaranteed securities registered or being registered− Rule 3-16 – Financial statements of affiliates whose securities collateralize an issue registered or being registered

• Overall themes for S-X 3-05, 3-09, 3-10 and 3-16 requirements:− Challenges faced in preparation and use− Alternatives to replace or adjust the requirements− If replaced, make enhancements to other related sections in a filing

• Public comment period ends on November 30Investor feedback desiredNext phase • Regulation S-K and certain industry guides

Disclosure effectiveness

21 Copyright © 2015 Deloitte Development LLC. All rights reserved.

SEC call to actionWhat can companies do now

22 Copyright © 2015 Deloitte Development LLC. All rights reserved.

What are companies doing?Disclosure effectiveness

• Eliminating immaterial or old information

• Supplementing narrative information with graphs, charts, etc.

• Broader changes throughout the filing

• Adding cross-references and reducing repetition

• Involving multiple groups within the company and the audit committee

23 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Why are companies making changes?Disclosure effectiveness

Improve clarity and usefulness of communications to investors

Reduce risk of inconsistencies within filings

Increase efficiency of preparation and review process

Improve investor confidence / reduce cost of capital

24 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Does your company plan to respond to the SEC’s request for comment for its disclosure effectiveness initiative?

• Yes• No• We participate in a trade group that will respond• Don’t know or N/A

Poll question #4

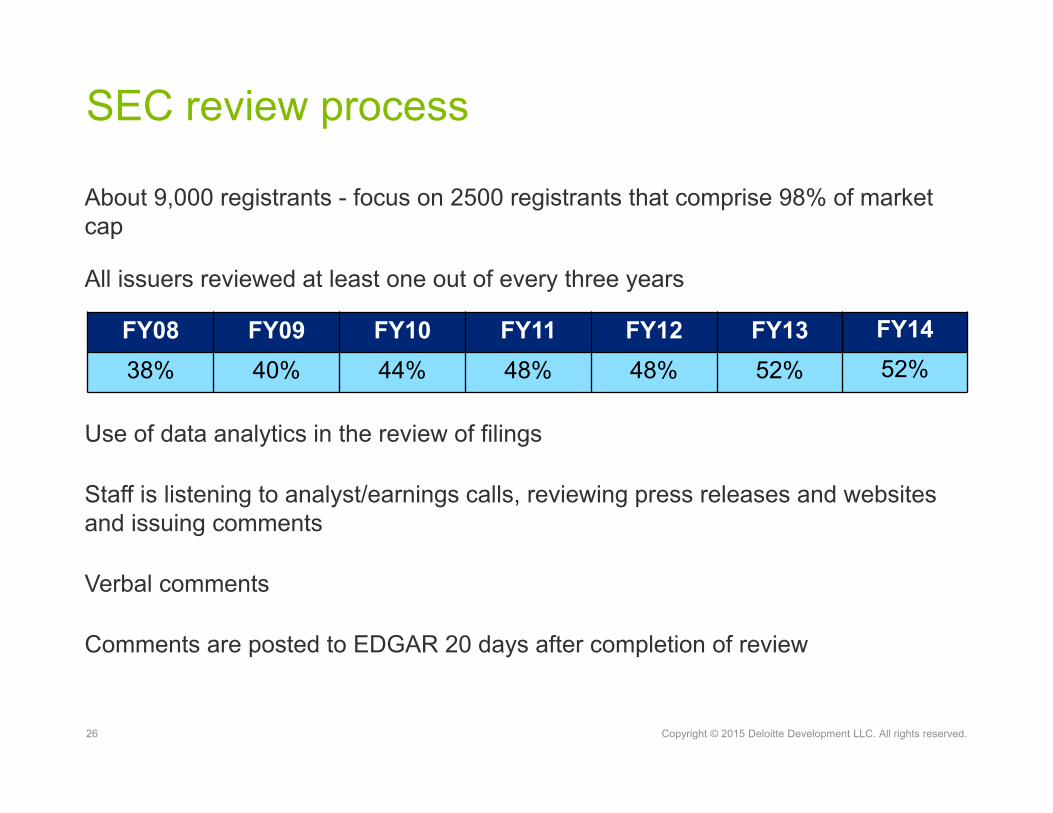

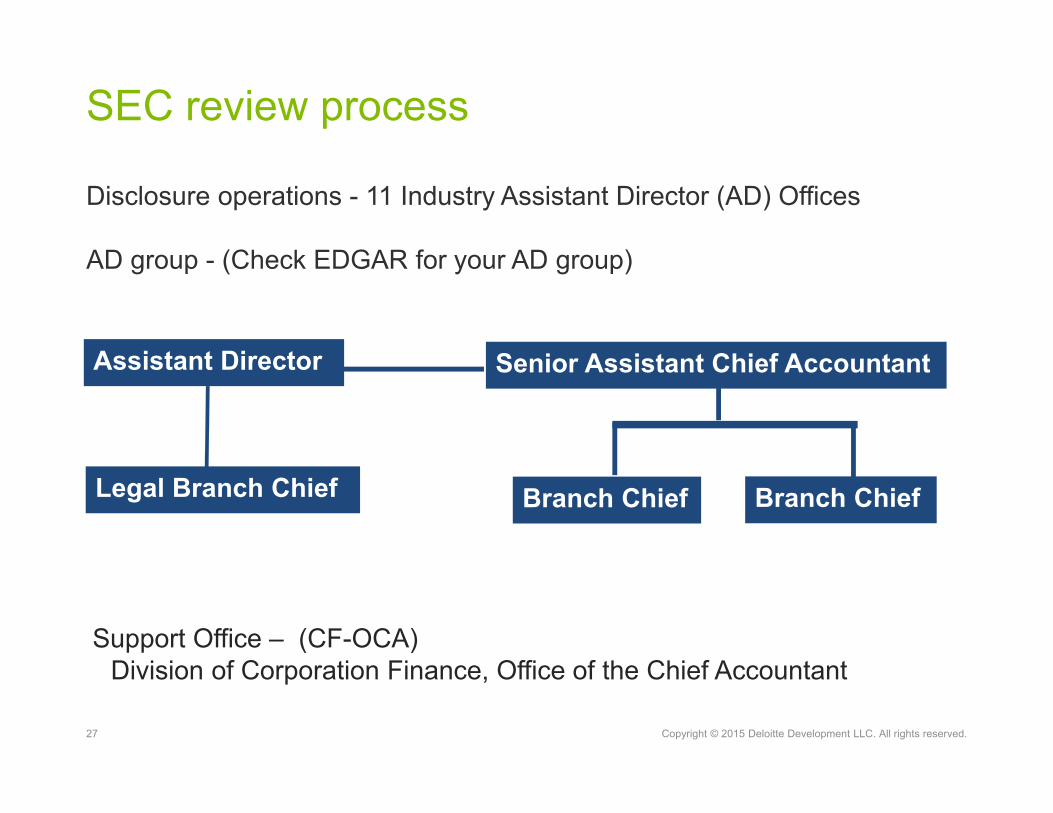

SEC review process

26 Copyright © 2015 Deloitte Development LLC. All rights reserved.

About 9,000 registrants - focus on 2500 registrants that comprise 98% of market cap

All issuers reviewed at least one out of every three years

Use of data analytics in the review of filings

Staff is listening to analyst/earnings calls, reviewing press releases and websites and issuing comments

Verbal comments

Comments are posted to EDGAR 20 days after completion of review

SEC review process

FY08 FY09 FY10 FY11 FY12 FY13 FY1438% 40% 44% 48% 48% 52% 52%

27 Copyright © 2015 Deloitte Development LLC. All rights reserved.

SEC review process

Disclosure operations - 11 Industry Assistant Director (AD) Offices

AD group - (Check EDGAR for your AD group)

Support Office – (CF-OCA) Division of Corporation Finance, Office of the Chief Accountant

Assistant Director

Branch Chief

Senior Assistant Chief Accountant

Branch ChiefLegal Branch Chief

28 Copyright © 2015 Deloitte Development LLC. All rights reserved.

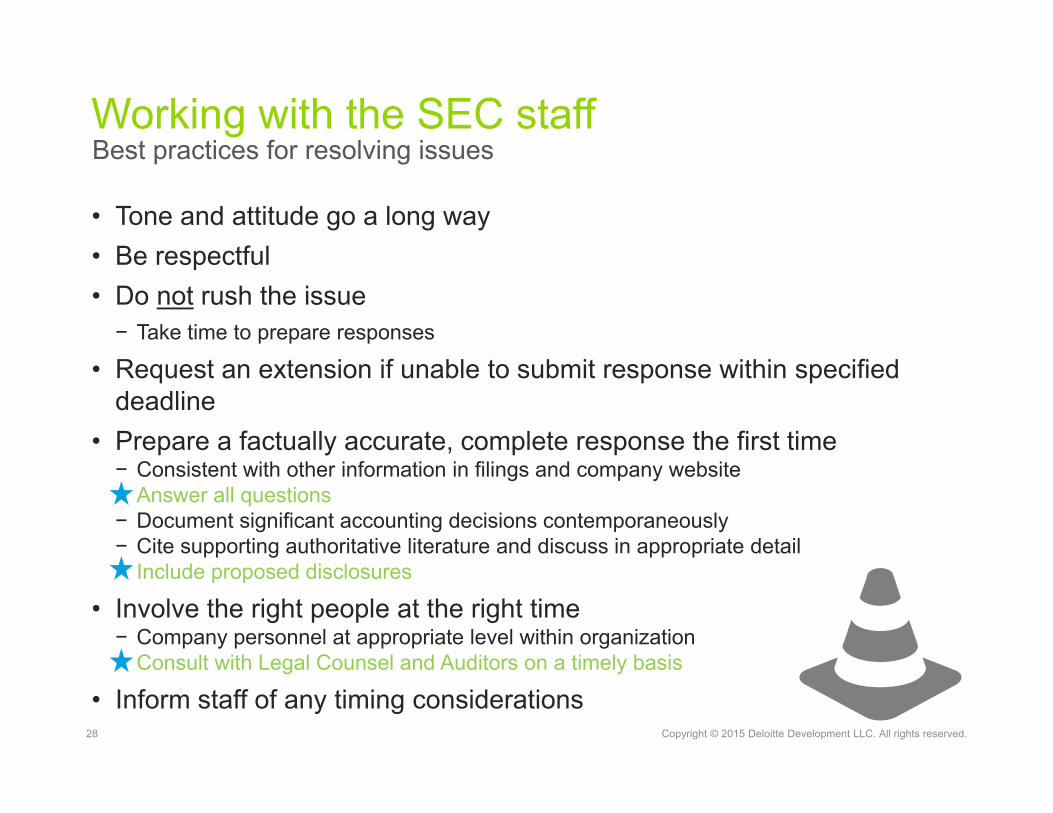

• Tone and attitude go a long way• Be respectful• Do not rush the issue

− Take time to prepare responses

• Request an extension if unable to submit response within specified deadline

• Prepare a factually accurate, complete response the first time− Consistent with other information in filings and company website− Answer all questions− Document significant accounting decisions contemporaneously− Cite supporting authoritative literature and discuss in appropriate detail− Include proposed disclosures

• Involve the right people at the right time− Company personnel at appropriate level within organization− Consult with Legal Counsel and Auditors on a timely basis

• Inform staff of any timing considerations

Working with the SEC staffBest practices for resolving issues

29 Copyright © 2015 Deloitte Development LLC. All rights reserved.

A company’s filing on Form 10-K is exempt from SEC staff review if the staff performed a full review on the company’s previous form 10-K filing.

• True• False• Don’t know or N/A

Poll question #5

SEC comment trends

SEC comment letter trends

Copyright © 2015 Deloitte Development LLC. All rights reserved. 31

• Insights into areas the SEC staff has focused on in recent comment letters including:− Financial statement accounting and disclosure topics− SEC disclosure topics− Disclosure topics in initial public offerings− Industry-specific topics

◦ Consumer & Industrial Products◦ Energy & Resources◦ Financial Services◦ Health Sciences◦ Technology & Telecommunications

32 Copyright © 2015 Deloitte Development LLC. All rights reserved.

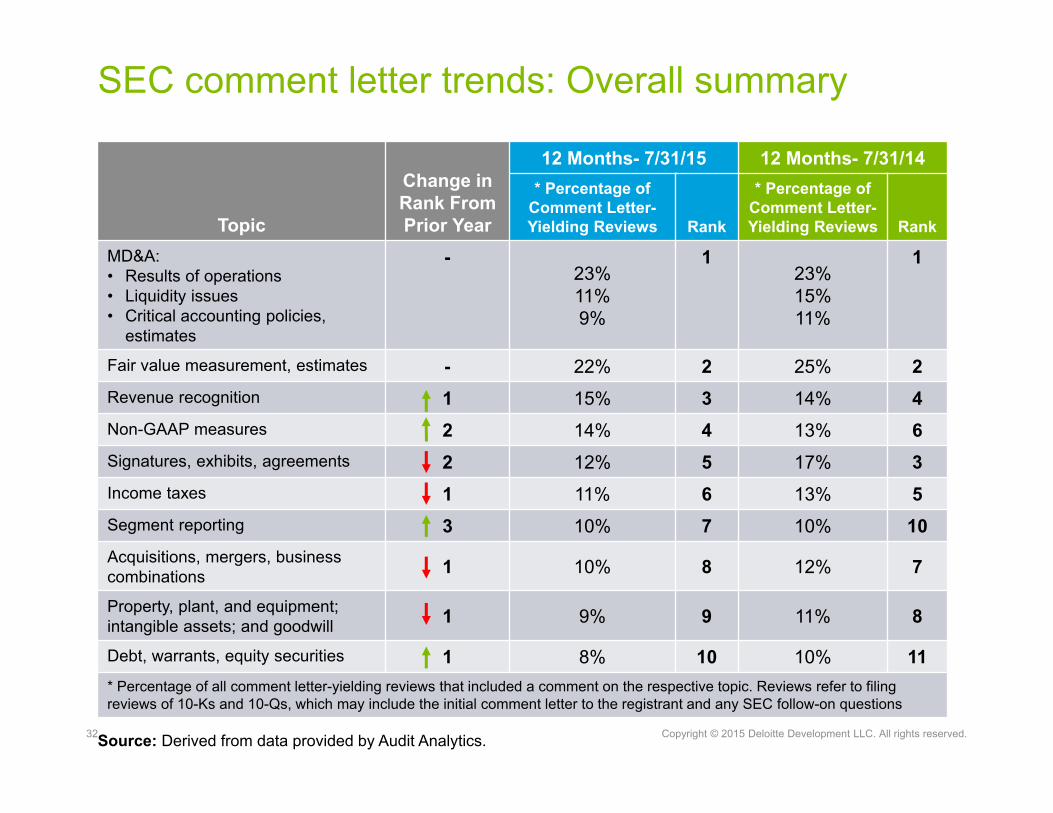

SEC comment letter trends: Overall summary

Topic

Change in Rank From Prior Year

12 Months- 7/31/15 12 Months- 7/31/14* Percentage of

Comment Letter-Yielding Reviews Rank

* Percentage of Comment Letter-Yielding Reviews Rank

MD&A:• Results of operations• Liquidity issues• Critical accounting policies,

estimates

-23%11%9%

123%15%11%

1

Fair value measurement, estimates - 22% 2 25% 2Revenue recognition 1 15% 3 14% 4Non-GAAP measures 2 14% 4 13% 6Signatures, exhibits, agreements 2 12% 5 17% 3Income taxes 1 11% 6 13% 5Segment reporting 3 10% 7 10% 10Acquisitions, mergers, businesscombinations 1 10% 8 12% 7

Property, plant, and equipment; intangible assets; and goodwill 1 9% 9 11% 8

Debt, warrants, equity securities 1 8% 10 10% 11* Percentage of all comment letter-yielding reviews that included a comment on the respective topic. Reviews refer to filing reviews of 10-Ks and 10-Qs, which may include the initial comment letter to the registrant and any SEC follow-on questions

Source: Derived from data provided by Audit Analytics.

33 Copyright © 2015 Deloitte Development LLC. All rights reserved.

SegmentsSEC comment letter trends

• Continued focus, including the SEC and PCAOB• Consider whether CODM is someone other than CEO• Chief Operating Decision Maker (CODM) package• SEC staff’s focus is evolving due to new technology:

− Historically SEC placed emphasis on CODM package- no longer determinative (still significant) factor

− Staff will consider total mix of information • Aggregation of operating segments still a focus -

consider both quantitative and qualitative factors

34 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Areas of focusSEC comment letter trends

Management’s Discussion and Analysis (MD&A)

• Disclose material trends and uncertainties — two-pronged approach• Enhanced liquidity and capital resources, critical accounting policy disclosures• Consistency with other communications (e.g., non-GAAP measures)• Focus on clarity (e.g., use of tables and charts)

Metrics

• “Tell a registrant’s story,” but include sufficient information and context to not mislead investors - balanced discussion

• Clearly define metrics and explain how calculated Explain how used by management and why important to investors

• Describe how a metric is related to current or future results of operations• Example industry metrics:

− Technology & Internet: Online users− Real estate: Occupancy and average rental rates− Retail: Same-store sales, number of visitors to website, catalogs mailed

35 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Non-GAAP financial measuresSEC comment trends

• Support why the non-GAAP measure is useful to investors− Clearly labeled and described− Appropriate conventional accounting terminology− Provided context for their presentation

• Reconcile to appropriate GAAP measure• Avoid “undue prominence” of a non-GAAP financial measure• Consistency • Compliance and disclosure interpretations (C&DIs)

36 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Metrics and Non-GAAP measures are one and the same and can be used interchangeably.

• True• False• Don’t know or N/A

Poll question #6

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Revenue recognitionSEC comment letter trends

• Gross vs. net • Multiple element arrangements• Sales returns• SAB Topic 11M disclosures

−What impact will the new standard have on a registrant’s financial position and results of operations when it is adopted in the future

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Fair value disclosures Comment letter trends

Common Comments:• Weighted average or range for Level 3 unobservable inputs• Sensitivity analysis should be sufficiently granular• Use of third-party pricing services

Copyright © 2015 Deloitte Development LLC. All rights reserved.

Internal Controls over Financial Reporting (ICFR)Comment letter trends

• Significant focus of SEC staff (reviews & enforcement)

• The “could” factor−Not limited to the size of the error identified−Immaterial misstatements “could” indicate a material

weakness

40 Copyright © 2015 Deloitte Development LLC. All rights reserved.

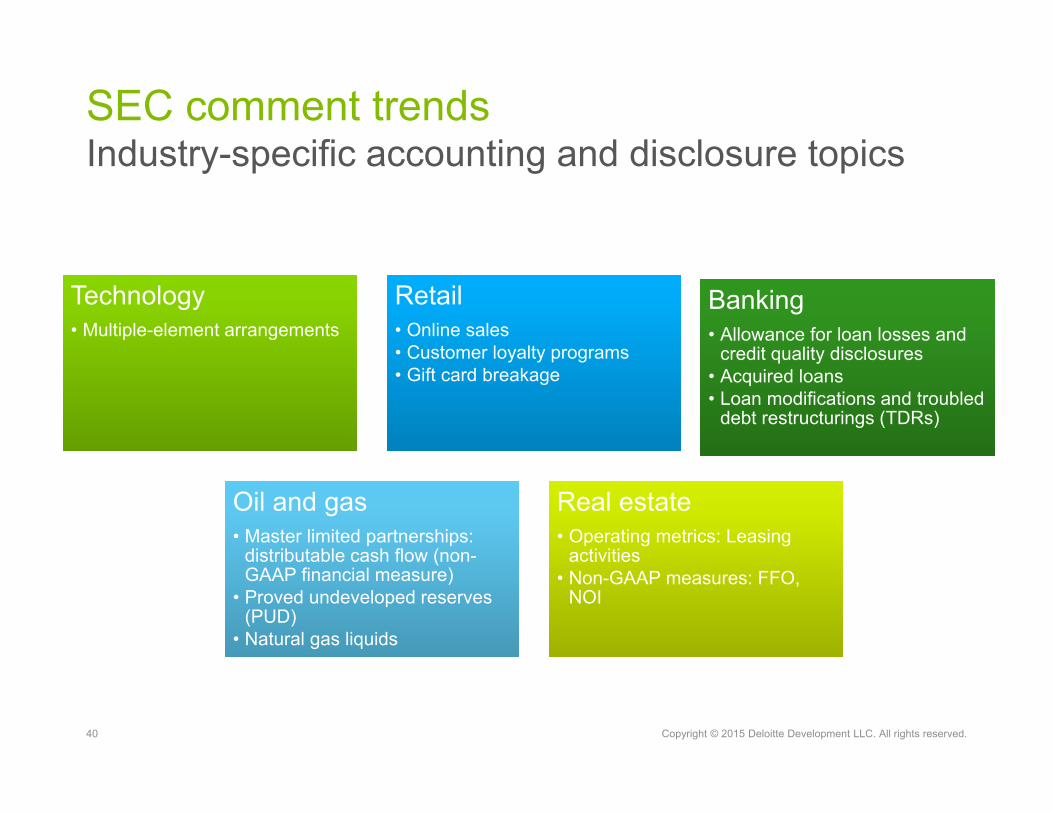

Industry-specific accounting and disclosure topicsSEC comment trends

Technology• Multiple-element arrangementsTechnology• Multiple-element arrangements

Retail• Online sales• Customer loyalty programs• Gift card breakage

Retail• Online sales• Customer loyalty programs• Gift card breakage

Banking• Allowance for loan losses and

credit quality disclosures• Acquired loans• Loan modifications and troubled

debt restructurings (TDRs)

Banking• Allowance for loan losses and

credit quality disclosures• Acquired loans• Loan modifications and troubled

debt restructurings (TDRs)

Oil and gas• Master limited partnerships:

distributable cash flow (non-GAAP financial measure)

• Proved undeveloped reserves (PUD)

• Natural gas liquids

Oil and gas• Master limited partnerships:

distributable cash flow (non-GAAP financial measure)

• Proved undeveloped reserves (PUD)

• Natural gas liquids

Real estate• Operating metrics: Leasing

activities• Non-GAAP measures: FFO,

NOI

Real estate• Operating metrics: Leasing

activities• Non-GAAP measures: FFO,

NOI

41 Copyright © 2015 Deloitte Development LLC. All rights reserved.

The assigned SEC reviewer only focuses on one specific industry and only provides comments that are very industry-specific. So, for example, a company in the real estate industry should not expect to receive comments in areas such as segments or non-GAAP measures.

• True• False• Don’t know or N/A

Poll question #7

Question and answer

43 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Contact info

Mark BoltonDirectorDeloitte & Touche [email protected]

Kathleen MaloneDirectorDeloitte & Touche [email protected]

Robert UhlPartnerDeloitte & Touche [email protected]

Hero AlimchandaniSenior ManagerDeloitte & Touche [email protected]

44 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Acronyms used in presentationAD: Assistant DirectorDCP: Disclosure Controls and ProceduresEDGAR: Electronic, Data Gathering, Analysis and RetrievalFASB: Financial Accounting Standards BoardFCPA: Foreign Corrupt Practices ActGAAP: Generally Accepted Accounting Principles

SEC: Securities and Exchange Commission

45 Copyright © 2015 Deloitte Development LLC. All rights reserved.

Eligible viewers may now download CPE certificates.

Click the CPE icon in the dock at the bottom of your screen.

46 Copyright © 2015 Deloitte Development LLC. All rights reserved.

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2015 Deloitte Development LLC. All rights reserved.36 USC 220506Member of Deloitte Touche Tohmatsu Limited