Embed Size (px)

Citation preview

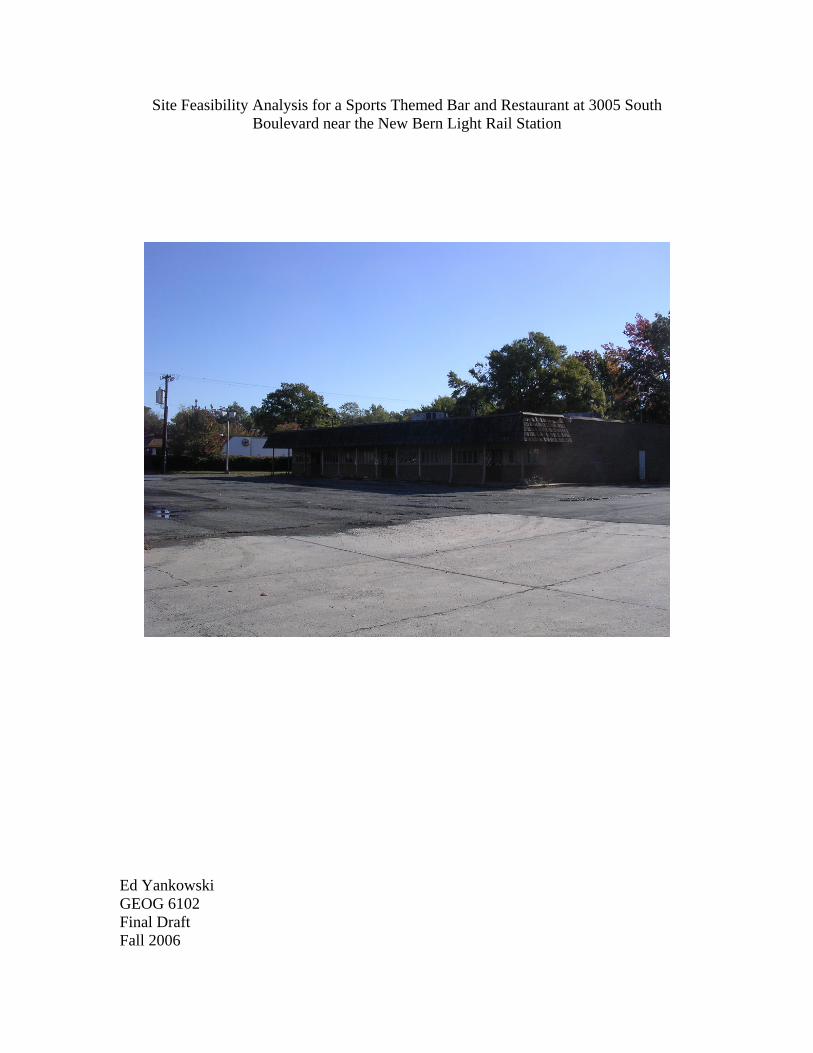

Site Feasibility Analysis for a Sports Themed Bar and Restaurant at 3005 South Boulevard near the New Bern Light Rail Station

Ed Yankowski GEOG 6102 Final Draft Fall 2006

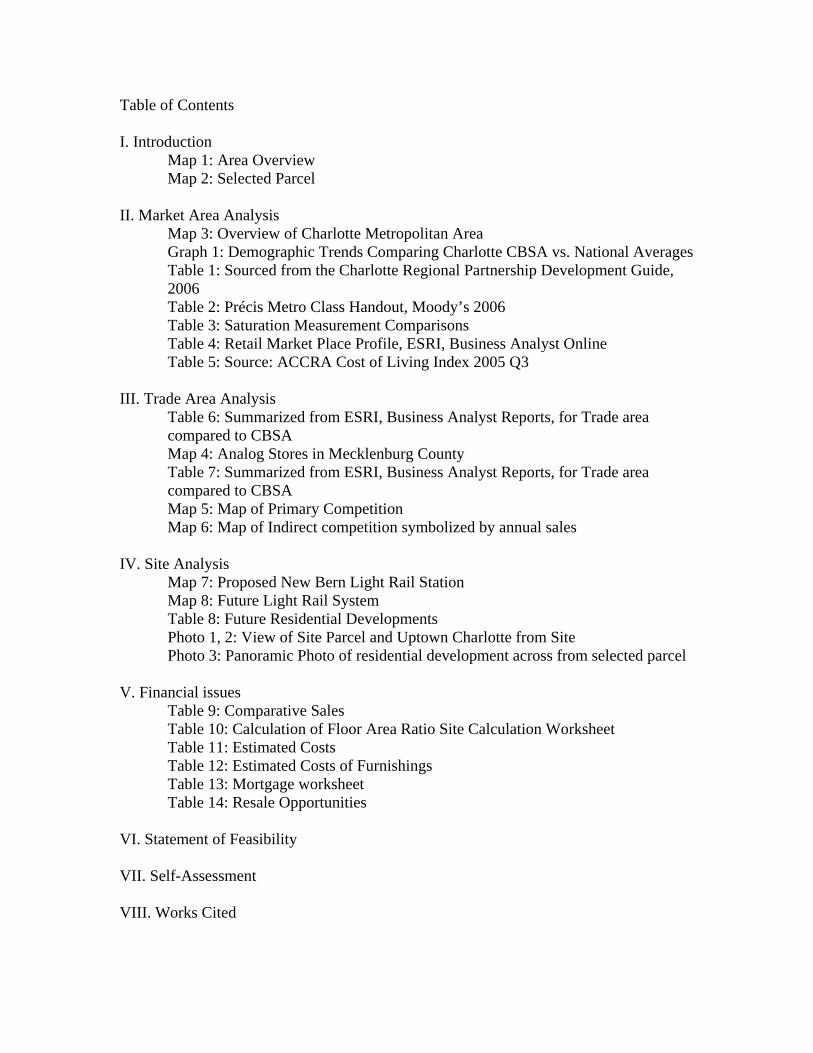

Table of Contents I. Introduction

Map 1: Area Overview Map 2: Selected Parcel

II. Market Area Analysis

Map 3: Overview of Charlotte Metropolitan Area Graph 1: Demographic Trends Comparing Charlotte CBSA vs. National Averages Table 1: Sourced from the Charlotte Regional Partnership Development Guide, 2006 Table 2: Précis Metro Class Handout, Moody’s 2006 Table 3: Saturation Measurement Comparisons Table 4: Retail Market Place Profile, ESRI, Business Analyst Online Table 5: Source: ACCRA Cost of Living Index 2005 Q3

III. Trade Area Analysis

Table 6: Summarized from ESRI, Business Analyst Reports, for Trade area compared to CBSA Map 4: Analog Stores in Mecklenburg County Table 7: Summarized from ESRI, Business Analyst Reports, for Trade area compared to CBSA Map 5: Map of Primary Competition Map 6: Map of Indirect competition symbolized by annual sales

IV. Site Analysis

Map 7: Proposed New Bern Light Rail Station Map 8: Future Light Rail System Table 8: Future Residential Developments Photo 1, 2: View of Site Parcel and Uptown Charlotte from Site Photo 3: Panoramic Photo of residential development across from selected parcel

V. Financial issues

Table 9: Comparative Sales Table 10: Calculation of Floor Area Ratio Site Calculation Worksheet Table 11: Estimated Costs Table 12: Estimated Costs of Furnishings Table 13: Mortgage worksheet Table 14: Resale Opportunities

VI. Statement of Feasibility VII. Self-Assessment VIII. Works Cited

Introduction:

The purpose of this feasibility study is to determine the likelihood of the financial success

of a sports themed restaurant at 3005 South Boulevard, in Charlotte, North Carolina

which is located in Mecklenburg County, the most populated county in both North and

South Carolina. This study will contain four major areas, followed by a conclusion to

determine if this project will receive any funding. After a brief description of the subject

parcel, we will discuss the strength of the entire Charlotte market, an analysis of the trade

area that we are proposing, an in depth analysis of the subject site, and finally a financial

analysis to determine the viability of this project moving forward. Our direct competition

will be casual dining restaurants that serve alcohol and have a variety of sporting events

on the televisions, and our indirect competition will be any other full service or quick

service restaurant that fall in our trade area,

Parcel Description:

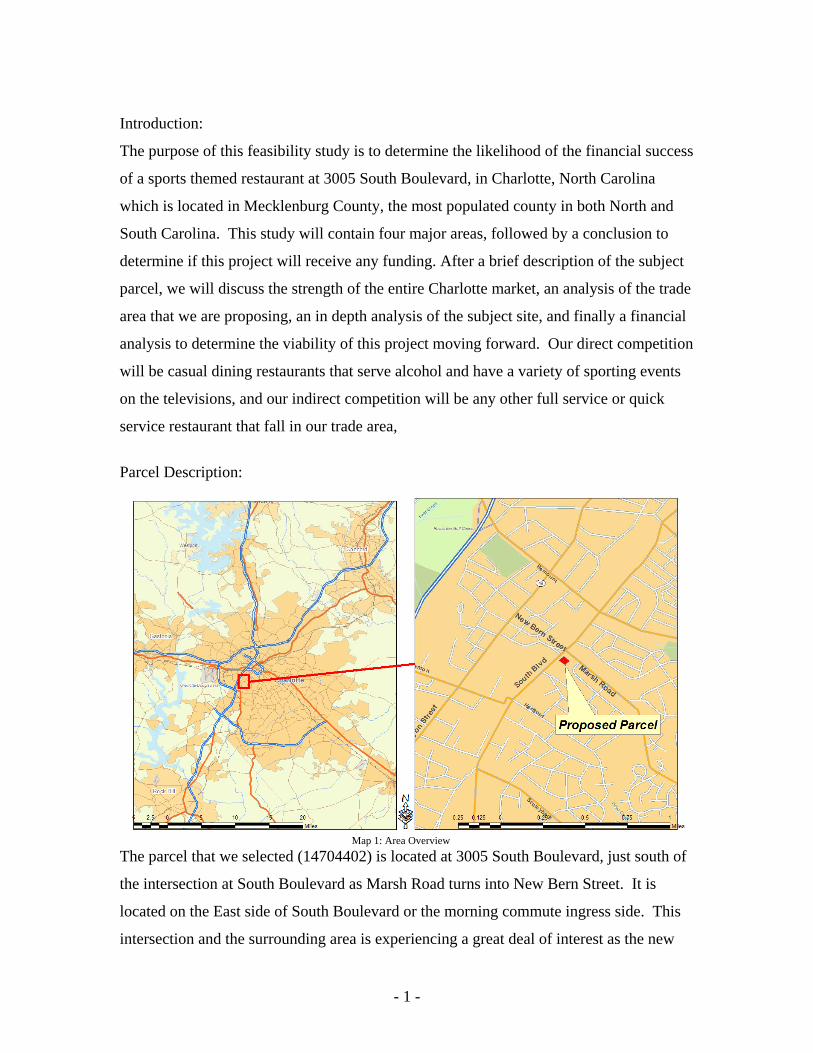

The parcel that we selected (14704402) is located at 3005 South Boulevard, just south of

the intersection at South Boulevard as Marsh Road turns into New Bern Street. It is

located on the East side of South Boulevard or the morning commute ingress side. This

intersection and the surrounding area is experiencing a great deal of interest as the new

Map 1: Area Overview

- 1 -

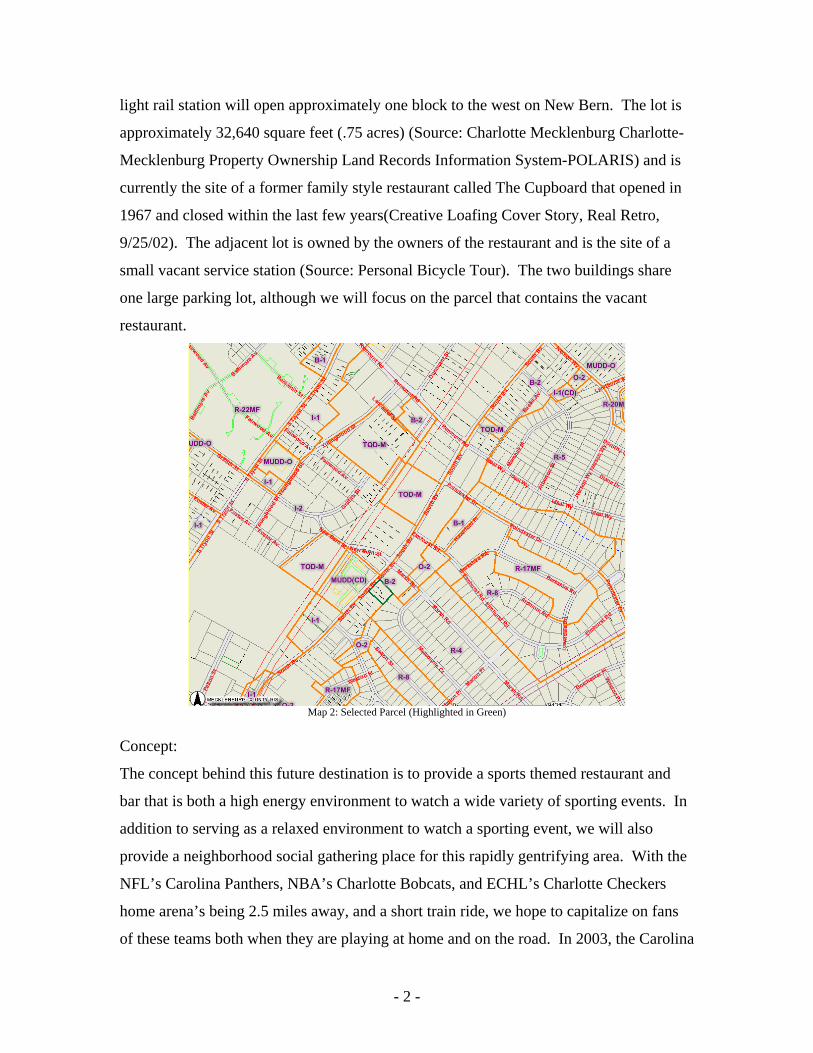

light rail station will open approximately one block to the west on New Bern. The lot is

approximately 32,640 square feet (.75 acres) (Source: Charlotte Mecklenburg Charlotte-

Mecklenburg Property Ownership Land Records Information System-POLARIS) and is

currently the site of a former family style restaurant called The Cupboard that opened in

1967 and closed within the last few years(Creative Loafing Cover Story, Real Retro,

9/25/02). The adjacent lot is owned by the owners of the restaurant and is the site of a

small vacant service station (Source: Personal Bicycle Tour). The two buildings share

one large parking lot, although we will focus on the parcel that contains the vacant

restaurant.

Map 2: Selected Parcel (Highlighted in Green)

Concept:

The concept behind this future destination is to provide a sports themed restaurant and

bar that is both a high energy environment to watch a wide variety of sporting events. In

addition to serving as a relaxed environment to watch a sporting event, we will also

provide a neighborhood social gathering place for this rapidly gentrifying area. With the

NFL’s Carolina Panthers, NBA’s Charlotte Bobcats, and ECHL’s Charlotte Checkers

home arena’s being 2.5 miles away, and a short train ride, we hope to capitalize on fans

of these teams both when they are playing at home and on the road. In 2003, the Carolina

- 2 -

Panthers averaged 72,820 fans per game for a total of over 582,500 fans for their season

(Source: Infoplease Daily Almanac). The first year the Charlotte Bobcats played at the

new uptown arena, they averaged over 14,000 fans a game for a total attendance of

545,178 over their 38 home games (Source: Slam Sports, Charlotte Bobcats Attendance

Comparison ). Finally, the ECHL Charlotte Checkers averaged 5,800 fans per game,

which ranks fourth highest in the league (Source: Slapshot for Success, Greater Charlotte

Biz, November, 2006). With these arena’s being so close, our location is an ideal

restaurant to visit prior to or after any of these home games. While our local fans can

enjoy many of these events live, we also plan to televise their road contests, as well as

offer satellite cable packages to watch out of market games across the country. We will

differentiate ourselves from other restaurants by offering an upscale yet friendly

environment that appeals to both men and women by providing a wide selection of high

quality food and drink. We will also have state of the art televisions with satellite

coverage local, regional and national sporting events in order to appeal to customers on

off peak times. Included in the technology will be an audio control at each table so each

party can decide which sporting event to listen to without trying to hear over other games

or the atmosphere of the bar.

Target Market:

After observing numerous local sports-themed bars in the Charlotte area, it appears that

the typical consumer is a younger male (ages 25-44) that appears to be middle to upper

middle income with above average disposable income. Some of the sports themed bars

in town are also restaurants which would allow children to visit, but for this preliminary

analysis we will focus on a target market of professional males ages 25-44 with income

between $35,000 and $74,999. During the year, there are a range of sports that young

men would view at a sports bar, from local and distant professional and college football,

basketball, baseball, and hockey, as well as NASCAR. Because we are also attempting to

cater to the neighborhood residents who would desire a local neighborhood bar, we will

add the professional women of the same ages with the same income $35,000 and

$74,999. In our trade area, there are several restaurants that our potential customers can

choose to visit that currently have similar formats, and these locations would be our

- 3 -

direct competition. These include Mac’s Speed Shop, Southend Brewery, Picasso’s

Sports Bar and Grill, Fox & The Hound, Stool Pigeons, Angry Ale’s, and the Graduate

Pub. Each of these establishments has been open for a lengthy time, and we would

certainly be viewed as newcomer to this format in Charlotte. We believe that our

restaurant will differentiate by our high quality food and our quality service added with

our great atmosphere. Our indirect competition in the area would be any quick service or

other restaurant that serves food in a casual dining atmosphere. We will not classify fast

food restaurants as indirect competition because of the major difference in our full

service nature and alcohol sales.

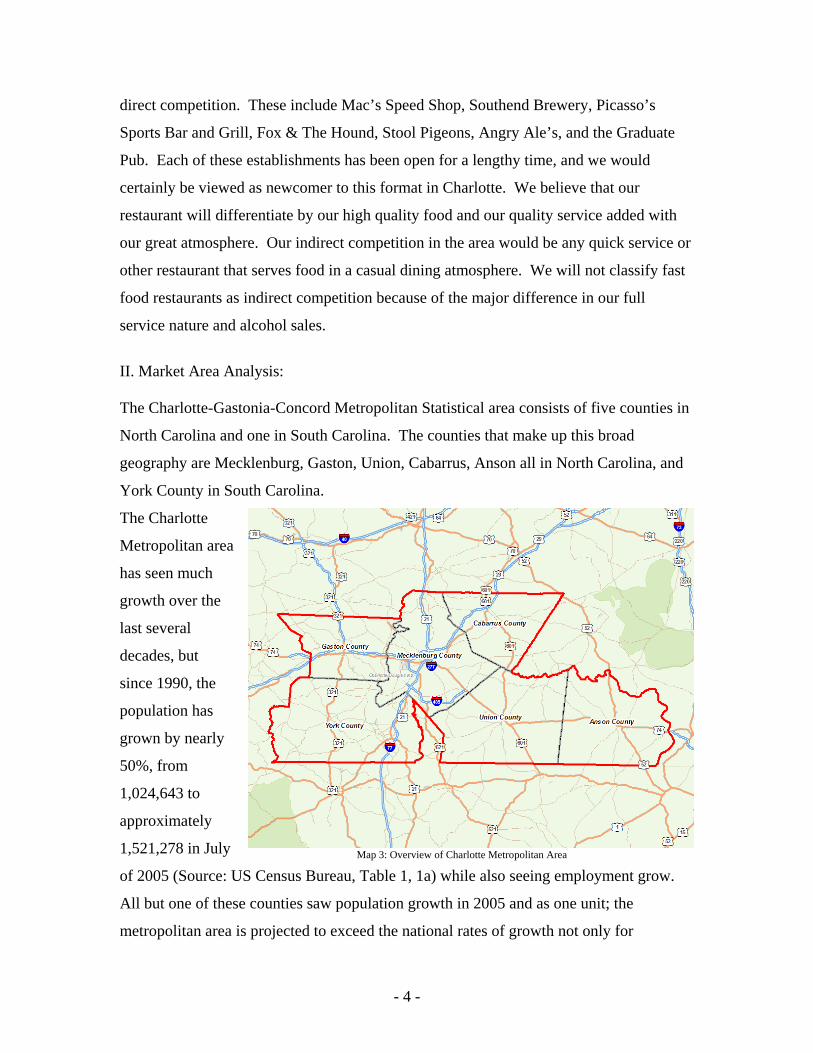

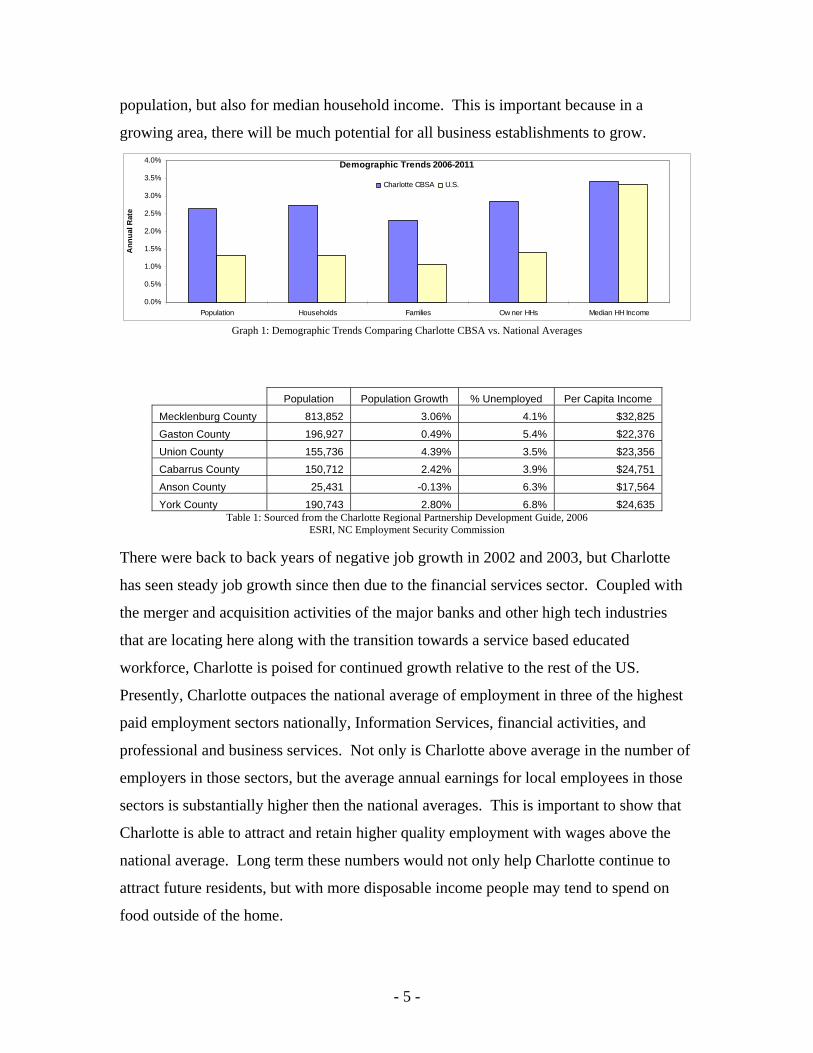

II. Market Area Analysis: The Charlotte-Gastonia-Concord Metropolitan Statistical area consists of five counties in

North Carolina and one in South Carolina. The counties that make up this broad

geography are Mecklenburg, Gaston, Union, Cabarrus, Anson all in North Carolina, and

York County in South Carolina.

The Charlotte

Metropolitan area

has seen much

growth over the

last several

decades, but

since 1990, the

population has

grown by nearly

50%, from

1,024,643 to

approximately

1,521,278 in July

of 2005 (Source: US Census Bureau, Table 1, 1a) while also seeing employment grow.

All but one of these counties saw population growth in 2005 and as one unit; the

metropolitan area is projected to exceed the national rates of growth not only for

Map 3: Overview of Charlotte Metropolitan Area

- 4 -

population, but also for median household income. This is important because in a

growing area, there will be much potential for all business establishments to grow.

Demographic Trends 2006-2011

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Population Households Families Ow ner HHs Median HH Income

Ann

ual R

ate

Charlotte CBSA U.S.

Graph 1: Demographic Trends Comparing Charlotte CBSA vs. National Averages

Population Population Growth % Unemployed Per Capita Income Mecklenburg County 813,852 3.06% 4.1% $32,825 Gaston County 196,927 0.49% 5.4% $22,376 Union County 155,736 4.39% 3.5% $23,356 Cabarrus County 150,712 2.42% 3.9% $24,751 Anson County 25,431 -0.13% 6.3% $17,564 York County

Table 1: Sourced from the Charlotte Regional Partnership Development Guide, 2006 190,743 2.80% 6.8% $24,635

ESRI, NC Employment Security Commission There were back to back years of negative job growth in 2002 and 2003, but Charlotte

has seen steady job growth since then due to the financial services sector. Coupled with

the merger and acquisition activities of the major banks and other high tech industries

that are locating here along with the transition towards a service based educated

workforce, Charlotte is poised for continued growth relative to the rest of the US.

Presently, Charlotte outpaces the national average of employment in three of the highest

paid employment sectors nationally, Information Services, financial activities, and

professional and business services. Not only is Charlotte above average in the number of

employers in those sectors, but the average annual earnings for local employees in those

sectors is substantially higher then the national averages. This is important to show that

Charlotte is able to attract and retain higher quality employment with wages above the

national average. Long term these numbers would not only help Charlotte continue to

attract future residents, but with more disposable income people may tend to spend on

food outside of the home.

- 5 -

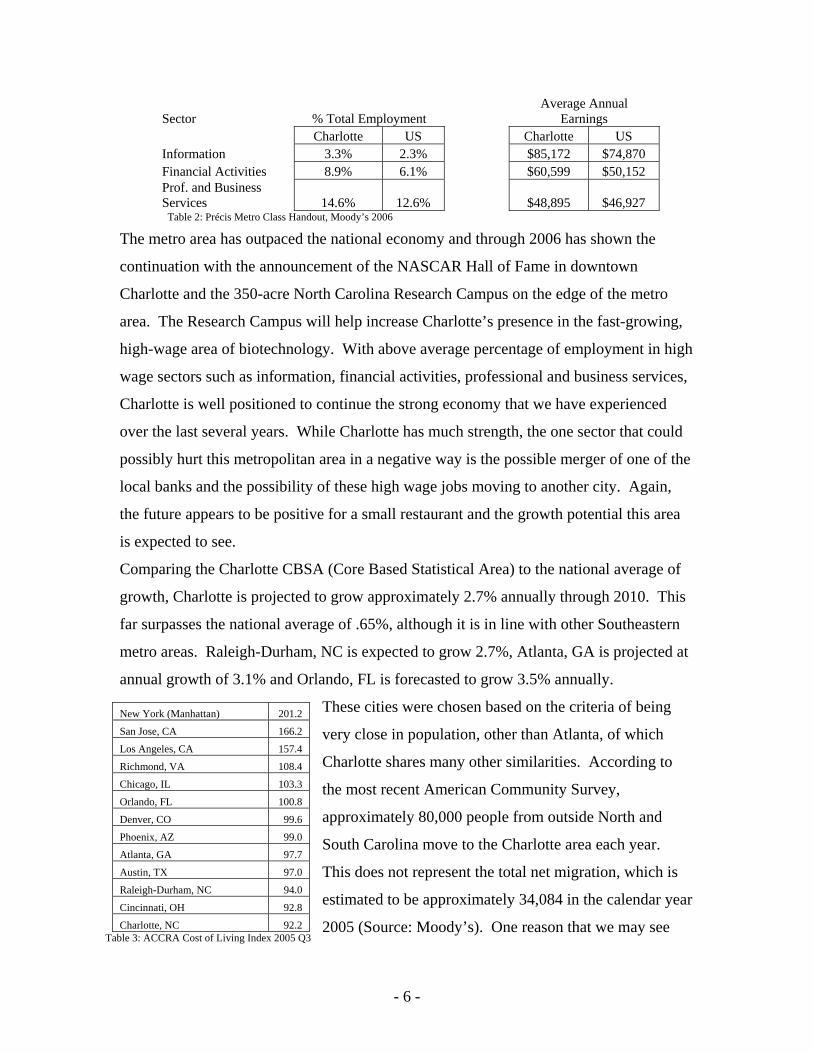

Average Annual Earnings Sector % Total Employment

Charlotte US Charlotte US Information 3.3% 2.3% $85,172 $74,870 Financial Activities 8.9% 6.1% $60,599 $50,152 Prof. and Business Services 14.6% 12.6% $48,895 $46,927

Table 2: Précis Metro Class Handout, Moody’s 2006

The metro area has outpaced the national economy and through 2006 has shown the

continuation with the announcement of the NASCAR Hall of Fame in downtown

Charlotte and the 350-acre North Carolina Research Campus on the edge of the metro

area. The Research Campus will help increase Charlotte’s presence in the fast-growing,

high-wage area of biotechnology. With above average percentage of employment in high

wage sectors such as information, financial activities, professional and business services,

Charlotte is well positioned to continue the strong economy that we have experienced

over the last several years. While Charlotte has much strength, the one sector that could

possibly hurt this metropolitan area in a negative way is the possible merger of one of the

local banks and the possibility of these high wage jobs moving to another city. Again,

the future appears to be positive for a small restaurant and the growth potential this area

is expected to see.

Comparing the Charlotte CBSA (Core Based Statistical Area) to the national average of

growth, Charlotte is projected to grow approximately 2.7% annually through 2010. This

far surpasses the national average of .65%, although it is in line with other Southeastern

metro areas. Raleigh-Durham, NC is expected to grow 2.7%, Atlanta, GA is projected at

annual growth of 3.1% and Orlando, FL is forecasted to grow 3.5% annually.

These cities were chosen based on the criteria of being

very close in population, other than Atlanta, of which

Charlotte shares many other similarities. According to

the most recent American Community Survey,

approximately 80,000 people from outside North and

South Carolina move to the Charlotte area each year.

This does not represent the total net migration, which is

estimated to be approximately 34,084 in the calendar year

2005 (Source: Moody’s). One reason that we may see

New York (Manhattan) 201.2

San Jose, CA 166.2

Los Angeles, CA 157.4

Richmond, VA 108.4

Chicago, IL 103.3

Orlando, FL 100.8

Denver, CO 99.6

Phoenix, AZ 99.0

Atlanta, GA 97.7

Austin, TX 97.0

Raleigh-Durham, NC 94.0

Cincinnati, OH 92.8

Charlotte, NC 92.2 Table 3: ACCRA Cost of Living Index 2005 Q3

- 6 -

continued growth is the cost of living index compared to other major metropolitan areas.

We see that Charlotte enjoys a comparative advantage to Orlando, Atlanta, and Raleigh

when discussing cost of living expenses, and this can only help Charlotte attract more

residents. The future is projected to bring much growth to Charlotte, and with that

growth there is an expectation that a wide variety of restaurants and drinking places

would be needed. With North American Industry Classification System (NAICS) data

provided to ESRI from InfoUSA, they are able to prepare a Retail Market Place report by

classifying each retail establishment according to their primary function. This is then

used to estimates sales, or supply to consumers by the establishments in the specific area.

They also project what the expected amount of money spent, or demand potential by

consumers in the retail establishments. From these numbers, you can infer the surplus or

leakage in an area by taking the difference between the two numbers. A leakage would

signify that an area may be ripe for expansion and a surplus could indicate that an area is

currently oversaturated. Retail Market Place reports obtained from ESRI indicate that the

expected demand for food and drink in our metropolitan area is approximately $2.7

billion worth of sales, while on the supply side there is only $1.9 billion of supply

(Source: ESRI, Business Analyst Online, and Retail Market Place Report). This measure

is an indication that the Charlotte metropolitan area can support approximately $800

million of additional supply in the six county area, thus indicating a possible potential for

expansion. Reviewing the other similar sized cities indicate that they are all at a

MSA Charlotte Hartford Raleigh Orlando Atlanta $1.8 $1.7 $1.2 $3.6 $7.4 Supply $2.7 $2.3 $1.7 $3.0 $9.4 Demand

Surplus/Leakage -$0.8 -$0.6 -$0.5 $0.6 -$2.0

Table 4: Retail Market Place Profile, ESRI, Business Analyst Online

shortage of supply, with the exception of Orlando, which is heavily dependent on the out

of metro area tourist for their economy. The restaurant business is an extremely

competitive business, although using a simple measure to determine the market saturation

for similar sized cities; we see that Charlotte possibly has some room for expansion in the

full service restaurant and bar business. When looking at the number of full service

restaurants (SIC 722110) per person and drinking establishments (SIC Codes 581301-8)

Charlotte is just below the average of our comparison cities. Full service restaurants

were chosen because of our food component and drinking establishments were selected

- 7 -

because that will be our primary business. So many SIC codes were used because of the

different classifications of bars, but we feel that this number is an adequate measure of

the Charlotte metropolitan area.

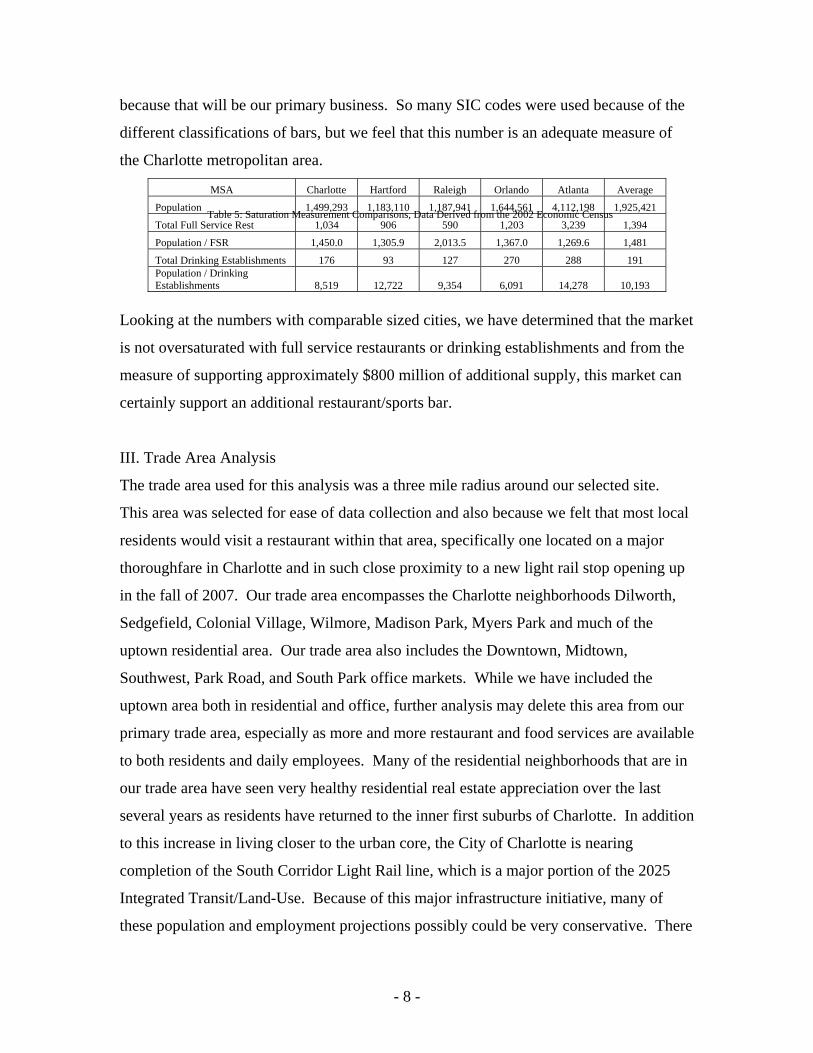

MSA Charlotte Hartford Raleigh Orlando Atlanta Average

Population 1,499,293 1,183,110 1,187,941 1,644,561 4,112,198 1,925,421

Total Full Service Rest 1,034 906 590 1,203 3,239

Looking at the numbers with comparable sized cities, we have determined that the market

is not oversaturated with full service restaurants or drinking establishments and from the

measure of supporting approximately $800 million of additional supply, this market can

certainly support an additional restaurant/sports bar.

III. Trade Area Analysis

The trade area used for this analysis was a three mile radius around our selected site.

This area was selected for ease of data collection and also because we felt that most local

residents would visit a restaurant within that area, specifically one located on a major

thoroughfare in Charlotte and in such close proximity to a new light rail stop opening up

in the fall of 2007. Our trade area encompasses the Charlotte neighborhoods Dilworth,

Sedgefield, Colonial Village, Wilmore, Madison Park, Myers Park and much of the

uptown residential area. Our trade area also includes the Downtown, Midtown,

Southwest, Park Road, and South Park office markets. While we have included the

uptown area both in residential and office, further analysis may delete this area from our

primary trade area, especially as more and more restaurant and food services are available

to both residents and daily employees. Many of the residential neighborhoods that are in

our trade area have seen very healthy residential real estate appreciation over the last

several years as residents have returned to the inner first suburbs of Charlotte. In addition

to this increase in living closer to the urban core, the City of Charlotte is nearing

completion of the South Corridor Light Rail line, which is a major portion of the 2025

Integrated Transit/Land-Use. Because of this major infrastructure initiative, many of

these population and employment projections possibly could be very conservative. There

1,394 Table 5: Saturation Measurement Comparisons, Data Derived from the 2002 Economic Census

Population / FSR 1,450.0 1,305.9 2,013.5 1,367.0 1,269.6 1,481

Total Drinking Establishments 176 93 127 270 288 191 Population / Drinking Establishments 8,519 12,722 9,354 6,091 14,278 10,193

- 8 -

are major developers that are proposing developments all along this corridor and also in

close proximity to our proposed restaurant. Historically this has not been a very

residential area, and because of that there are very few restaurants that cater to the

residential population. By entering this market before much of the expected population

would position us to gain many first mover advantages. By initially capturing the market

in the trade are, we can build up our faithful clientele, so in the future once this area

continues to grow, we will have our solid customer base to grow with. We will position

the restaurant to have certain loyalty programs and also a revolving menu to continue

attracting our core market all the while solidifying our relationship with them. We would

expect a large number of our customers to either live in our immediate trade area, or

possibly all along the light rail corridor if they were to be using the train for

transportation to our establishment.

Again our target markets are those customers between the ages of 25-44 that would like

to enjoy a full service restaurant with a sports theme. In the immediate trade area the

total resident population is 75,125, of which 25,625 of the population (34.1%) is our

target market. Looking at the entire metropolitan area shows that only 31.5% of the total

population would be our target market, so our target market is above average compared

to the entire area. These numbers however do not include the estimated residential units

that are under construction in this area. Our anticipation is that the future residents of this

area would visit and spend money at a local establishment within walking distance or a

short car or train ride. Since our trade area dips into the uptown office market, we see

that of the 8,308 business in the trade area, we see that we have approximately 117,899

employees that work here in this. The ration of daytime to nighttime population is also

very high because of the major employment center that falls in our trade area. While we

enjoy more favorable demographics from our immediate trade area, there is also a great

deal of competition that comes with this initially promising area. Of each variable

summarized in the following table, the only two that our site is less favorable than the

Charlotte Core Based Statistical Area (CBSA) as a region are persons per establishment

and the Leakage/Surplus figures. These leakage/surplus figures are the estimated demand

of a trade area minus the estimated supply of the area based on the NAICS codes and

ESRI’s proprietary equations for these estimates. The CBSA is an Office of Management

- 9 -

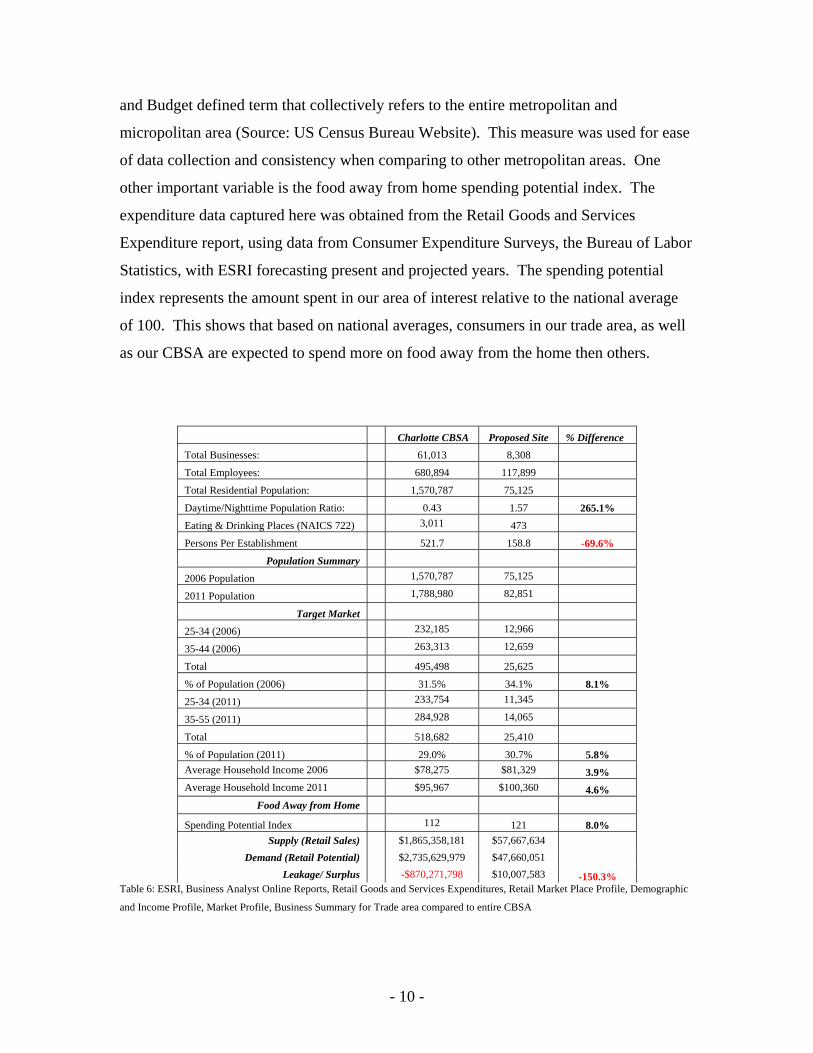

and Budget defined term that collectively refers to the entire metropolitan and

micropolitan area (Source: US Census Bureau Website). This measure was used for ease

of data collection and consistency when comparing to other metropolitan areas. One

other important variable is the food away from home spending potential index. The

expenditure data captured here was obtained from the Retail Goods and Services

Expenditure report, using data from Consumer Expenditure Surveys, the Bureau of Labor

Statistics, with ESRI forecasting present and projected years. The spending potential

index represents the amount spent in our area of interest relative to the national average

of 100. This shows that based on national averages, consumers in our trade area, as well

as our CBSA are expected to spend more on food away from the home then others.

Charlotte CBSA Proposed Site % Difference

Total Businesses: 61,013 8,308

Total Employees: 680,894 117,899

Total Residential Population: 1,570,787 75,125

Daytime/Nighttime Population Ratio: 0.43 1.57 265.1% 3,011 Eating & Drinking Places (NAICS 722) 473

Persons Per Establishment 521.7 158.8 -69.6%

Population Summary 1,570,787 75,125 2006 Population 1,788,980 82,851 2011 Population

Target Market 232,185 12,966 25-34 (2006) 263,313 12,659 35-44 (2006)

Total 495,498 25,625

% of Population (2006) 31.5% 34.1% 8.1% 233,754 11,345 25-34 (2011) 284,928 14,065 35-55 (2011)

Total 518,682 25,410

% of Population (2011) 29.0% 30.7% 5.8% Average Household Income 2006 $78,275 $81,329 3.9% Average Household Income 2011 $95,967 $100,360 4.6%

Food Away from Home 112 Spending Potential Index 121 8.0%

Supply (Retail Sales) $1,865,358,181 $57,667,634 Demand (Retail Potential) $2,735,629,979 $47,660,051

Leakage/ Surplus -$870,271,798 $10,007,583 -150.3% Table 6: ESRI, Business Analyst Online Reports, Retail Goods and Services Expenditures, Retail Market Place Profile, Demographic

and Income Profile, Market Profile, Business Summary for Trade area compared to entire CBSA

- 10 -

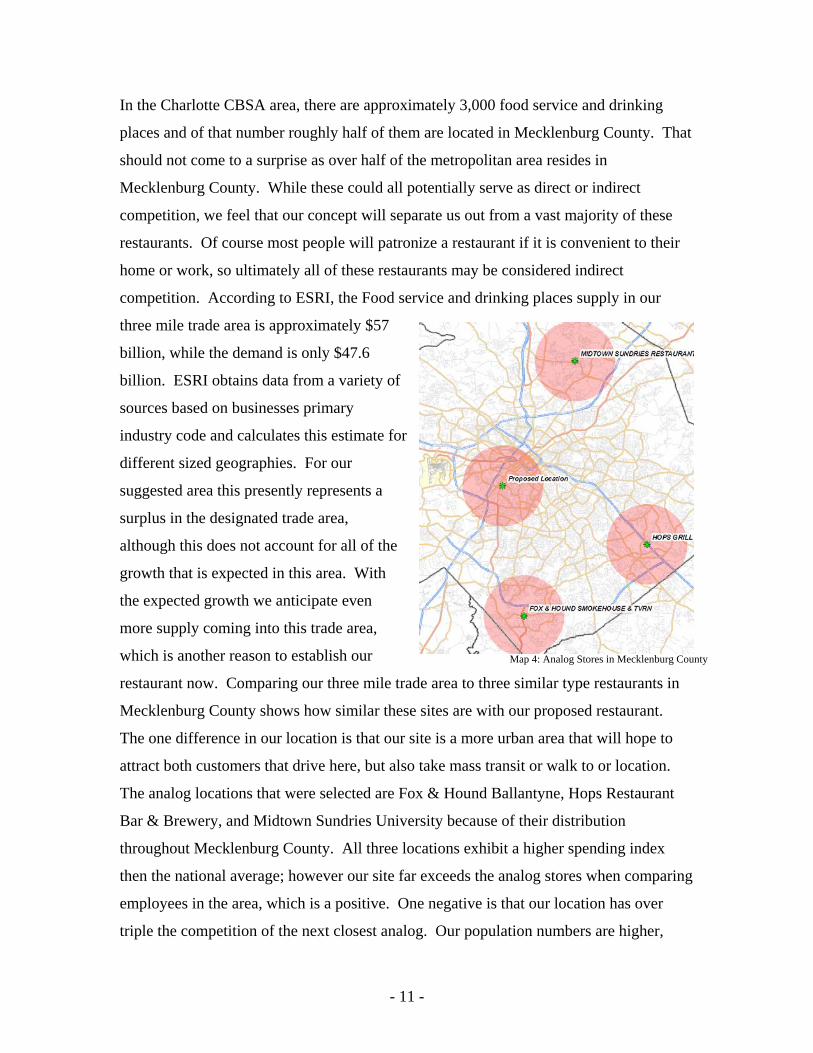

In the Charlotte CBSA area, there are approximately 3,000 food service and drinking

places and of that number roughly half of them are located in Mecklenburg County. That

should not come to a surprise as over half of the metropolitan area resides in

Mecklenburg County. While these could all potentially serve as direct or indirect

competition, we feel that our concept will separate us out from a vast majority of these

restaurants. Of course most people will patronize a restaurant if it is convenient to their

home or work, so ultimately all of these restaurants may be considered indirect

competition. According to ESRI, the Food service and drinking places supply in our

three mile trade area is approximately $57

billion, while the demand is only $47.6

billion. ESRI obtains data from a variety of

sources based on businesses primary

industry code and calculates this estimate f

different sized geographies. For our

suggested area this presently represents a

surplus in the designated trade area,

although this does not account for all of the

growth that is expected in this area. With

the expected growth we anticipate even

more supply coming into this trade area,

which is another reason to establish our

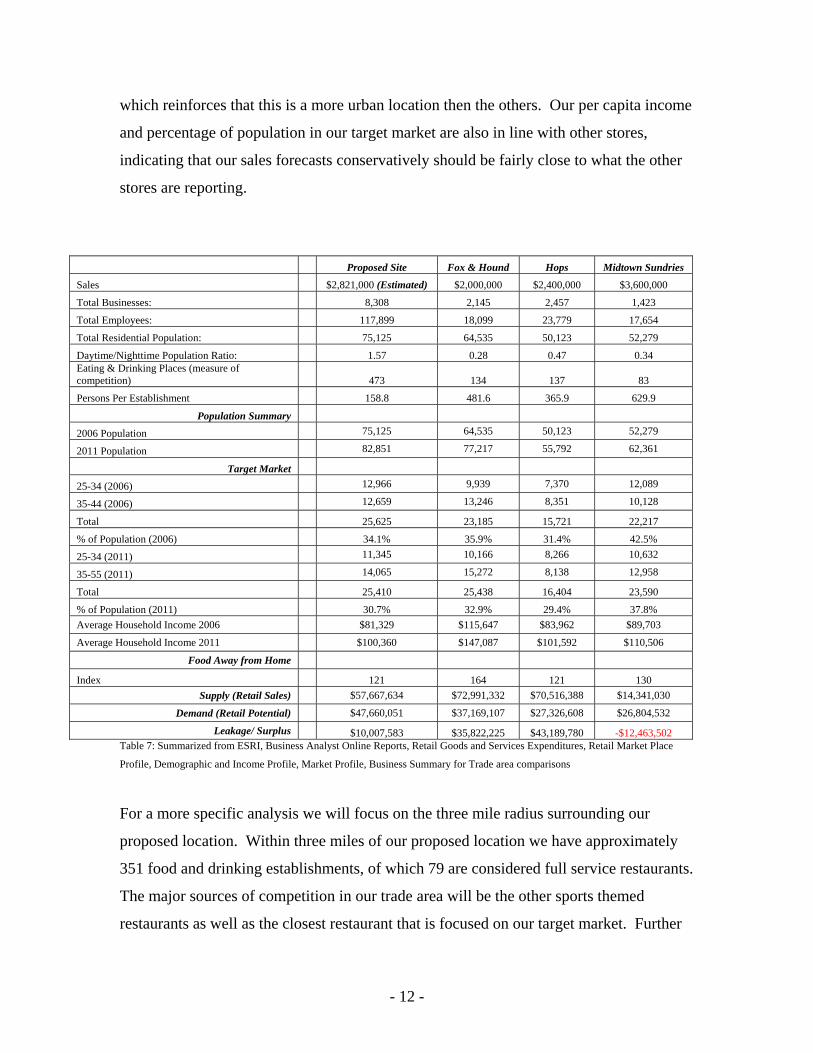

restaurant now. Comparing our three mile trade area to three similar type restaurants in

Mecklenburg County shows how similar these sites are with our proposed restaurant.

The one difference in our location is that our site is a more urban area that will hope to

attract both customers that drive here, but also take mass transit or walk to or location.

The analog locations that were selected are Fox & Hound Ballantyne, Hops Restaurant

Bar & Brewery, and Midtown Sundries University because of their distribution

throughout Mecklenburg County. All three locations exhibit a higher spending index

then the national average; however our site far exceeds the analog stores when comparing

employees in the area, which is a positive. One negative is that our location has over

triple the competition of the next closest analog. Our population numbers are higher,

or

Map 4: Analog Stores in Mecklenburg County

- 11 -

which reinforces that this is a more urban location then the others. Our per capita income

and percentage of population in our target market are also in line with other stores,

indicating that our sales forecasts conservatively should be fairly close to what the other

stores are reporting.

Proposed Site Fox & Hound Hops Midtown Sundries

Table 7: Summarized from ESRI, Business Analyst Online Reports, Retail Goods and Services Expenditures, Retail Market Place

Profile, Demographic and Income Profile, Market Profile, Business Summary for Trade area comparisons

For a more specific analysis we will focus on the three mile radius surrounding our

proposed location. Within three miles of our proposed location we have approximately

351 food and drinking establishments, of which 79 are considered full service restaurants.

The major sources of competition in our trade area will be the other sports themed

restaurants as well as the closest restaurant that is focused on our target market. Further

Sales $2,821,000 (Estimated) $2,000,000 $2,400,000 $3,600,000

Total Businesses: 8,308 2,145 2,457 1,423

Total Employees: 117,899 18,099 23,779 17,654

Total Residential Population: 75,125 64,535 50,123 52,279

Daytime/Nighttime Population Ratio: 1.57 0.28 0.47 0.34 Eating & Drinking Places (measure of competition) 473 134 137 83

Persons Per Establishment 158.8 481.6 365.9 629.9

Population Summary 75,125 64,535 50,123 52,279 2006 Population 82,851 77,217 55,792 62,361 2011 Population

Target Market 12,966 9,939 7,370 12,089 25-34 (2006) 12,659 13,246 8,351 10,128 35-44 (2006)

Total 25,625 23,185 15,721 22,217

% of Population (2006) 34.1% 35.9% 31.4% 42.5% 11,345 10,166 8,266 10,632 25-34 (2011) 14,065 15,272 8,138 12,958 35-55 (2011)

Total 25,410 25,438 16,404 23,590

% of Population (2011) 30.7% 32.9% 29.4% 37.8% Average Household Income 2006 $81,329 $115,647 $83,962 $89,703 Average Household Income 2011 $100,360 $147,087 $101,592 $110,506

Food Away from Home

Index 121 164 121 130 Supply (Retail Sales) $57,667,634 $72,991,332 $70,516,388 $14,341,030

Demand (Retail Potential) $47,660,051 $37,169,107 $27,326,608 $26,804,532 Leakage/ Surplus $10,007,583 $35,822,225 $43,189,780 -$12,463,502

- 12 -

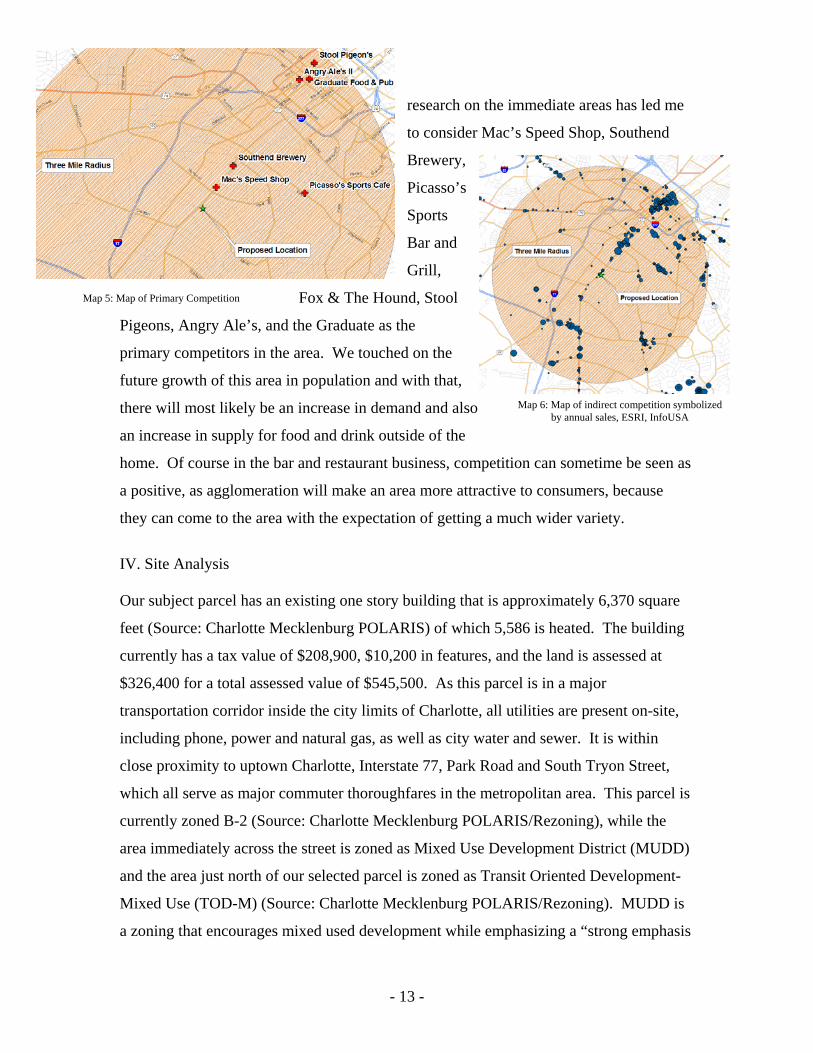

research on the immediate areas has led me

to consider Mac’s Speed Shop, Southend

Brewery,

Picasso’s

Sports

Bar and

Grill,

Fox & The Hound, Stool

Pigeons, Angry Ale’s, and the Graduate as the

primary competitors in the area. We touched on the

future growth of this area in population and with tha

there will most likely be an increase in demand and also

an increase in supply for food and drink outsid

t,

e of the

ome. Of course in the bar and restaurant business, com

meration will make an area more attractive to consumers, because

ng a much wider variety.

ng that is approximately 6,370 square

) of which 5,586 is heated. The building

his parcel is

D)

ment-

asis

Map 5: Map of Primary Competition

Map 6: Map of indirect competition symbolized by annual sales, ESRI, InfoUSA

h petition can sometime be seen as

a positive, as agglo

they can come to the area with the expectation of getti

IV. Site Analysis Our subject parcel has an existing one story buildi

feet (Source: Charlotte Mecklenburg POLARIS

currently has a tax value of $208,900, $10,200 in features, and the land is assessed at

$326,400 for a total assessed value of $545,500. As this parcel is in a major

transportation corridor inside the city limits of Charlotte, all utilities are present on-site,

including phone, power and natural gas, as well as city water and sewer. It is within

close proximity to uptown Charlotte, Interstate 77, Park Road and South Tryon Street,

which all serve as major commuter thoroughfares in the metropolitan area. T

currently zoned B-2 (Source: Charlotte Mecklenburg POLARIS/Rezoning), while the

area immediately across the street is zoned as Mixed Use Development District (MUD

and the area just north of our selected parcel is zoned as Transit Oriented Develop

Mixed Use (TOD-M) (Source: Charlotte Mecklenburg POLARIS/Rezoning). MUDD is

a zoning that encourages mixed used development while emphasizing a “strong emph

- 13 -

on pedestrian scale, urban development and amenities” (Source: Charlotte Zoning Code,

Chapter 9). TOD-M is a special zoning that is very similar to mixed use, however it o

occurs within ½ half mile or a 10-minute walk of a transit station.. While the proposed

business is approved for B-2 zoning, we may receive less stringent parking requirement

if the location was zoned either MU

nly

s

DD or TOD-M.

he

osing

s

s

el

.

s

th

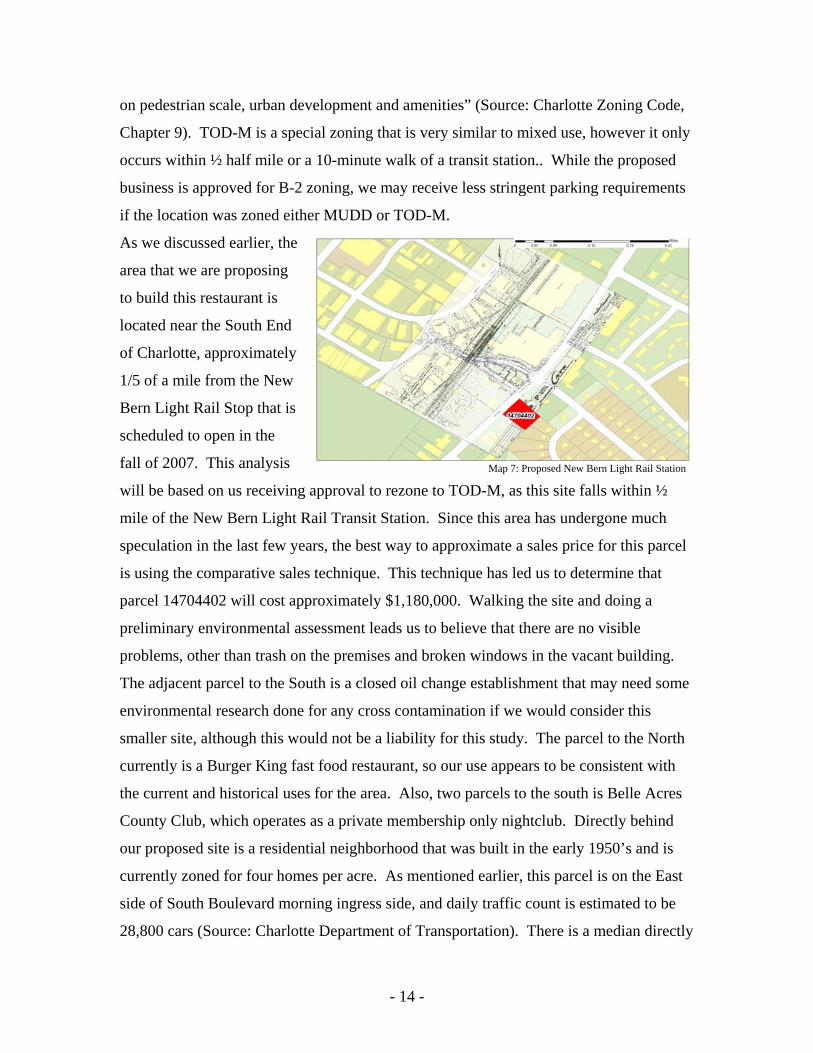

As we discussed earlier, t

area that we are prop

to build this restaurant i

located near the South End

of Charlotte, approximately

1/5 of a mile from the New

Bern Light Rail Stop that i

scheduled to open in the

fall of 2007. This analysis

will be based on us receiving approval to rezone to TOD-M, as this site falls within ½

mile of the New Bern Light Rail Transit Station. Since this area has undergone much

speculation in the last few years, the best way to approximate a sales price for this parc

is using the comparative sales technique. This technique has led us to determine that

parcel 14704402 will cost approximately $1,180,000. Walking the site and doing a

preliminary environmental assessment leads us to believe that there are no visible

problems, other than trash on the premises and broken windows in the vacant building

The adjacent parcel to the South is a closed oil change establishment that may need some

environmental research done for any cross contamination if we would consider thi

smaller site, although this would not be a liability for this study. The parcel to the North

currently is a Burger King fast food restaurant, so our use appears to be consistent wi

the current and historical uses for the area. Also, two parcels to the south is Belle Acres

County Club, which operates as a private membership only nightclub. Directly behind

our proposed site is a residential neighborhood that was built in the early 1950’s and is

currently zoned for four homes per acre. As mentioned earlier, this parcel is on the East

side of South Boulevard morning ingress side, and daily traffic count is estimated to be

28,800 cars (Source: Charlotte Department of Transportation). There is a median directly

Map 7: Proposed New Bern Light Rail Station

- 14 -

in front of the parcel that would prohibit cars turning directly into our parking lot drivin

southbound, but currently access coming from the North is done through the adjacen

shared parking lot. Since this was parcel was a restaurant for many years, there are no

expectations that there will be any adverse reaction from the surrounding residen

Attempts to interview residents in the neighborhood immediately bordering the rear of

the restaurant proved to be unproductive, however we can expect a positive reaction as

the site will no longer be a vacant building. One criticism of a recently opened full

service restaurant which also serves alcohol in the immediate trade area is complaints of

loud motorcycles and other noise pollution from the building and parking lot. Further

analysis should be done to determine if a noise barrier is to be built on the back of our

property to separate and buffer the neighborhood.

g

t

ts.

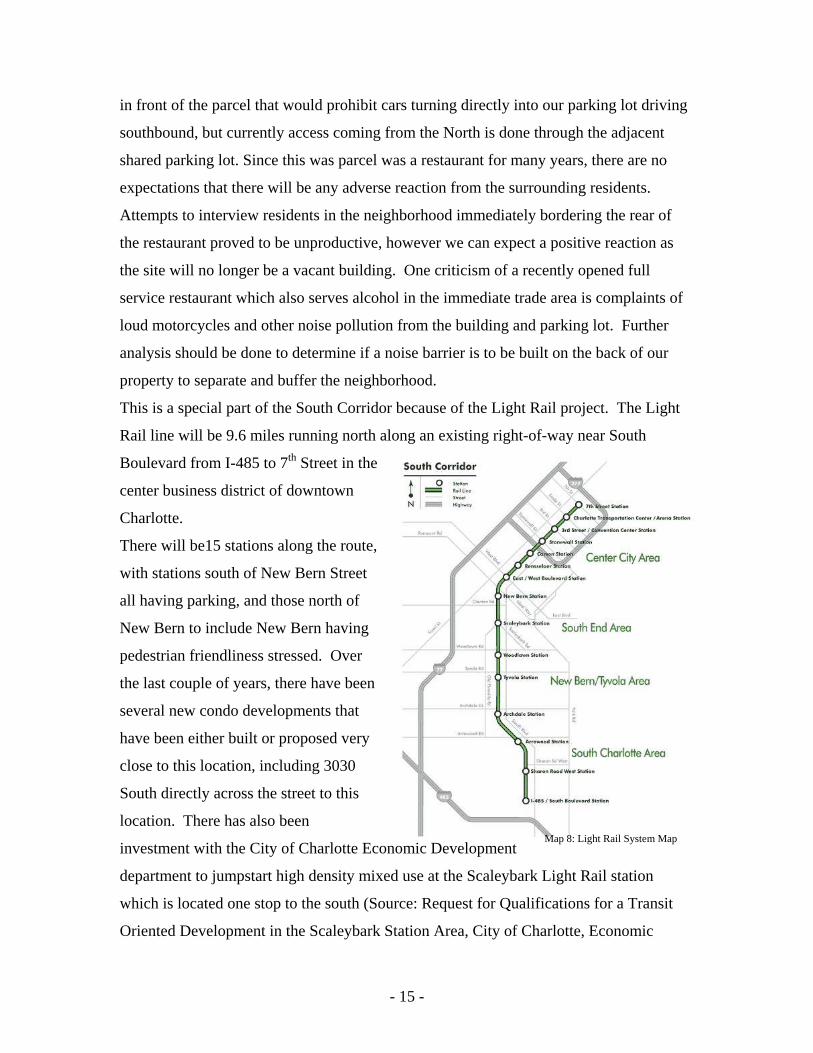

This is a special part of the South Corridor because of the Light Rail project. The Light

Rail line will be 9.6 miles running north along an existing right-of-way near South

Boulevard from I-485 to 7th Street in the

center business district of downtown

Charlotte.

There will be15 stations along the route,

with stations south of New Bern Street

all having parking, and those north of

New Bern to include New Bern having

pedestrian friendliness stressed. Over

the last couple of years, there have been

several new condo developments that

have been either built or proposed very

close to this location, including 3030

South directly across the street to this

location. There has also been

investment with the City of Charlotte Economic Development

department to jumpstart high density mixed use at the Scaleybark Light Rail station

which is located one stop to the south (Source: Request for Qualifications for a Transit

Oriented Development in the Scaleybark Station Area, City of Charlotte, Economic

Map 8: Light Rail System Map

- 15 -

Development Office). After a cursory search of the Charlotte Mecklenburg Rezoning

website, there are approximately 2800 residential condominium units proposed or

currently built within ½ mile of our proposed site (Source: Charlotte Rezoning Petitions

2006-128, 129; 2005-091,117). As these developments are all under development,

with the exception of 3030 South, we do not

know the future sales prices of these units. A

cursory search of real estate listings shows that

units in 3030 South range from $175,000 for a

692 square foot unit to 296,900 for a 1,112 square

foot unit (Source: MyTownhome Available Listings). Future residents in a development

such as this or the proposed similar developments in the future are expected to be

younger, and in the higher income categories; both characteristics that our business

requires. While the area demographics could lean towards the site not working, with the

upcoming light rail, the investment that the city is making towards high-density growth in

the South Corridor and the rapid higher income residential growth of this area may push

this over the edge. After consideration of costs based on the size of the parcel and size of

our proposed building, we may want to consider parcels within the area that are much

smaller to save on land acquisition costs as well as obtain a site that can be accessed from

both north and south on South Boulevard. The site adjacent may be a qualified site,

although we discussed the potential for environmental contamination.

Proposed Units

3030 South 110

Blue Sky Partners 200

Poindexter Village Up to 1000

Scaleybark Station Up to 1180

HH Hunt Corp 320

Total 2800 Table 8: Future Residential Developments

Photo 1, 2: View of Site Parcel and Uptown Charlotte from Site

- 16 -

Photo 3: Photo of Residential Complex across street from Parcel

V. Financial Analysis: This analysis is based on us purchasing the selected site (Parcel ID 14704402), although

it is not currently on the market. Since this area is about to experience a massive change

with the introduction of the light rail, there has been much speculative purchasing to

position for the major changes. In order to get a better approximation for the cost of the

property, I used the comparative sales technique by selecting seven parcels in the

immediate area that have sold from August of 2005 until now. These parcels were both

vacant and had abandoned buildings on them, so for this analysis we calculated the

average price per square foot of the parcel, as most buildings if they exist would need to

be torn down or completely remodeled, as is the case with our parcel. Because of the

heightened interest that this area has shown, the prices have escalated substantially in this

time, so if the purchase is delayed substantially, we may need to recalculate this at a

different, higher cost.

Parcel # Date purchased Acres Square Feet Sales Price $/Sq Ft 14701710 8/23/2005 4.92 214,271.64 $5,143,000 $24.00 12104112 11/3/2005 0.74 32,234.40 $1,750,000 $54.29 12104412 3/1/2006 1.90 82,764.00 $4,225,000 $51.05 12104116 1/31/2006 1.78 77,536.80 $2,226,000 $28.71 12104115 8/30/2005 2.13 92,957.04 $3,800,000 $40.88 12104120 3/3/2006 1.27 55,103.40 $1,600,000 $29.04 14701713 6/14/2006 0.84 36,590.40 $950,000 $25.96

Average 1.94 84,493.95 $2,813,429 $36.28 14704402 Subject Parcel 0.75 32,640.00 $1,184,031 $36.28 14704403 Parcel next door 0.50 21,570.00 $782,462 $36.28

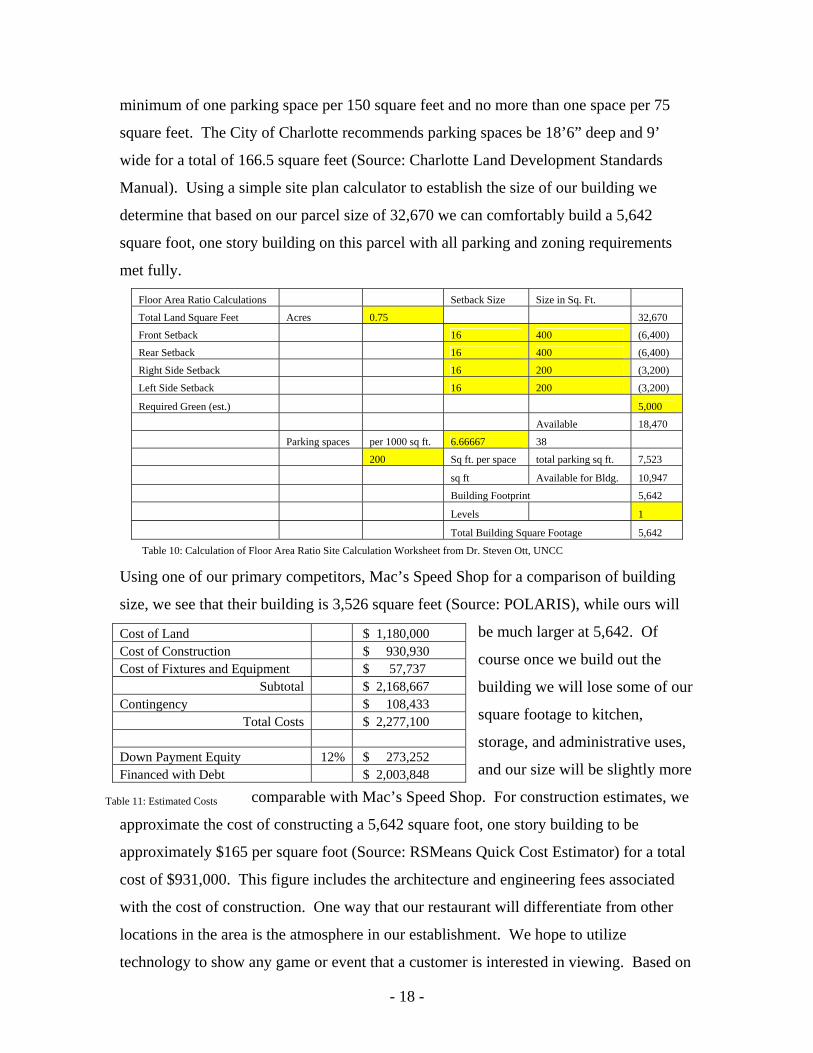

Table 9: Comparative Sales sourced from Charlotte-Mecklenburg Property Ownership Land Records Information System (POLARIS) In order to determine the size of the building that would be permitted on this site that is

zoned TOD-M we have accounted for several variables. As defined by the Charlotte City

Zoning Ordinance, if a station area plan does not specify a setback, one of sixteen feet

shall be used (Source: Charlotte Zoning Code, Chapter 9): The base height for all

structures shall be 40 feet, although based on us constructing a one story building; this

should not affect our location. Lastly, when the land use is a restaurant, there is a

- 17 -

minimum of one parking space per 150 square feet and no more than one space per 75

square feet. The City of Charlotte recommends parking spaces be 18’6” deep and 9’

wide for a total of 166.5 square feet (Source: Charlotte Land Development Standards

Manual). Using a simple site plan calculator to establish the size of our building we

determine that based on our parcel size of 32,670 we can comfortably build a 5,642

square foot, one story building on this parcel with all parking and zoning requirements

met fully.

Floor Area Ratio Calculations Setback Size Size in Sq. Ft.

Total Land Square Feet Acres 0.75 32,670

Front Setback 16 400 (6,400)

Rear Setback 16 400 (6,400)

Right Side Setback 16 200 (3,200)

Left Side Setback 16 200 (3,200)

Required Green (est.) 5,000

Available 18,470

Parking spaces per 1000 sq ft. 6.66667 38

200 Sq ft. per space total parking sq ft. 7,523

sq ft Available for Bldg. 10,947

Building Footprint 5,642

Levels 1 Total Building Square Footage 5,642

Table 10: Calculation of Floor Area Ratio Site Calculation Worksheet from Dr. Steven Ott, UNCC

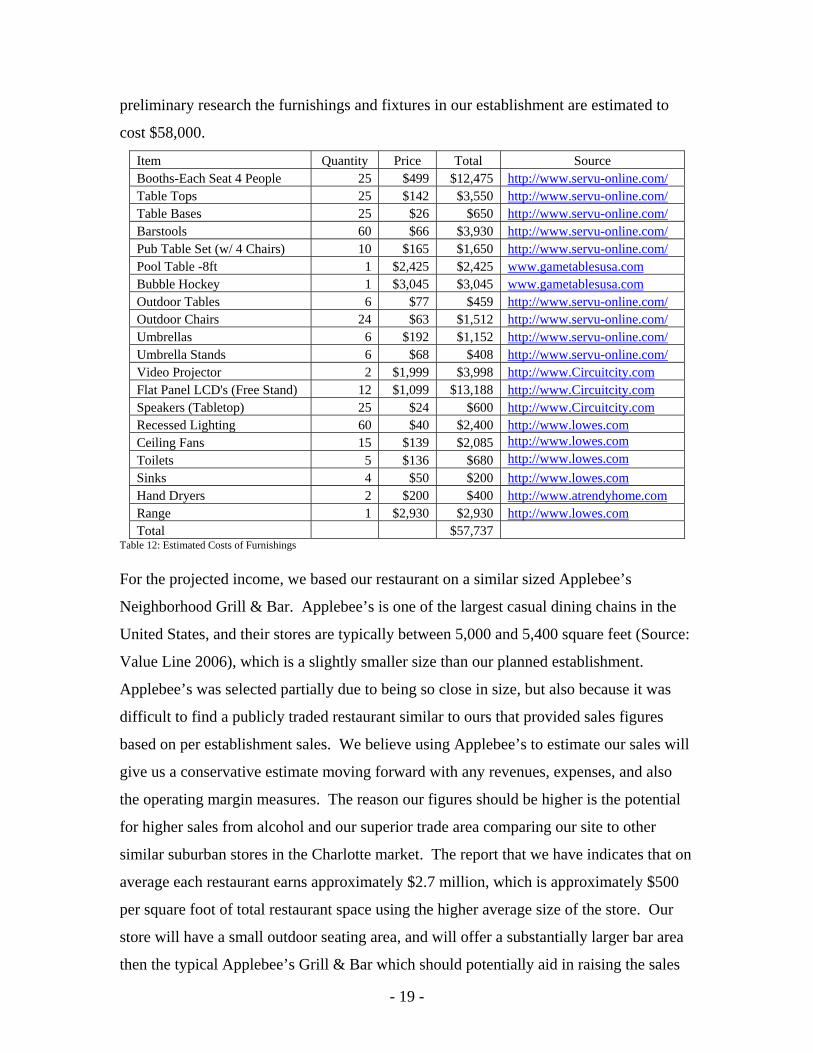

Using one of our primary competitors, Mac’s Speed Shop for a comparison of building

size, we see that their building is 3,526 square feet (Source: POLARIS), while ours will

be much larger at 5,642. Of

course once we build out the

building we will lose some of our

square footage to kitchen,

storage, and administrative uses,

and our size will be slightly more

comparable with Mac’s Speed Shop. For construction estimates, we

approximate the cost of constructing a 5,642 square foot, one story building to be

approximately $165 per square foot (Source: RSMeans Quick Cost Estimator) for a total

cost of $931,000. This figure includes the architecture and engineering fees associated

with the cost of construction. One way that our restaurant will differentiate from other

locations in the area is the atmosphere in our establishment. We hope to utilize

technology to show any game or event that a customer is interested in viewing. Based on

Cost of Land $ 1,180,000 Cost of Construction $ 930,930 Cost of Fixtures and Equipment $ 57,737

Subtotal $ 2,168,667 Contingency $ 108,433

Total Costs $ 2,277,100

Down Payment Equity 12% $ 273,252 Financed with Debt $ 2,003,848

Table 11: Estimated Costs

- 18 -

preliminary research the furnishings and fixtures in our establishment are estimated to

cost $58,000.

Item Quantity Price Total Source Booths-Each Seat 4 People 25 $499 $12,475 http://www.servu-online.com/Table Tops 25 $142 $3,550 http://www.servu-online.com/Table Bases 25 $26 $650 http://www.servu-online.com/Barstools 60 $66 $3,930 http://www.servu-online.com/Pub Table Set (w/ 4 Chairs) 10 $165 $1,650 http://www.servu-online.com/Pool Table -8ft 1 $2,425 $2,425 www.gametablesusa.com Bubble Hockey 1 $3,045 $3,045 www.gametablesusa.com Outdoor Tables 6 $77 $459 http://www.servu-online.com/Outdoor Chairs 24 $63 $1,512 http://www.servu-online.com/Umbrellas 6 $192 $1,152 http://www.servu-online.com/Umbrella Stands 6 $68 $408 http://www.servu-online.com/Video Projector 2 $1,999 $3,998 http://www.Circuitcity.com Flat Panel LCD's (Free Stand) 12 $1,099 $13,188 http://www.Circuitcity.com Speakers (Tabletop) 25 $24 $600 http://www.Circuitcity.com Recessed Lighting 60 $40 $2,400 http://www.lowes.com

http://www.lowes.comCeiling Fans 15 $139 $2,085 Toilets 5 $136 $680 http://www.lowes.com Sinks 4 $50 $200 http://www.lowes.comHand Dryers 2 $200 $400 http://www.atrendyhome.com Range 1 $2,930 $2,930 http://www.lowes.comTotal $57,737

Table 12: Estimated Costs of Furnishings For the projected income, we based our restaurant on a similar sized Applebee’s

Neighborhood Grill & Bar. Applebee’s is one of the largest casual dining chains in the

United States, and their stores are typically between 5,000 and 5,400 square feet (Source:

Value Line 2006), which is a slightly smaller size than our planned establishment.

Applebee’s was selected partially due to being so close in size, but also because it was

difficult to find a publicly traded restaurant similar to ours that provided sales figures

based on per establishment sales. We believe using Applebee’s to estimate our sales will

give us a conservative estimate moving forward with any revenues, expenses, and also

the operating margin measures. The reason our figures should be higher is the potential

for higher sales from alcohol and our superior trade area comparing our site to other

similar suburban stores in the Charlotte market. The report that we have indicates that on

average each restaurant earns approximately $2.7 million, which is approximately $500

per square foot of total restaurant space using the higher average size of the store. Our

store will have a small outdoor seating area, and will offer a substantially larger bar area

then the typical Applebee’s Grill & Bar which should potentially aid in raising the sales

- 19 -

per square foot. Based on our 5,642 square foot restaurant, we can expect annual sales to

be approximately $2.8 million. Basing our forward looking numbers on these sales

revenues, Value Line estimates that in 2006 the operating margin will be 15%, rising to

15.5% in 2007. We will assume the same growth year over year growth in our restaurant

as well. We are also estimating property taxes due to Charlotte-Mecklenburg County to

be approximately $23,000 based on our combined property being assessed at $1.8

million. The 2006 Charlotte and Mecklenburg combined Tax rate is currently 1.2775 per

$100 of valuation (Source: 2006 Property Tax Rates, Charlotte Mecklenburg Tax

Department).

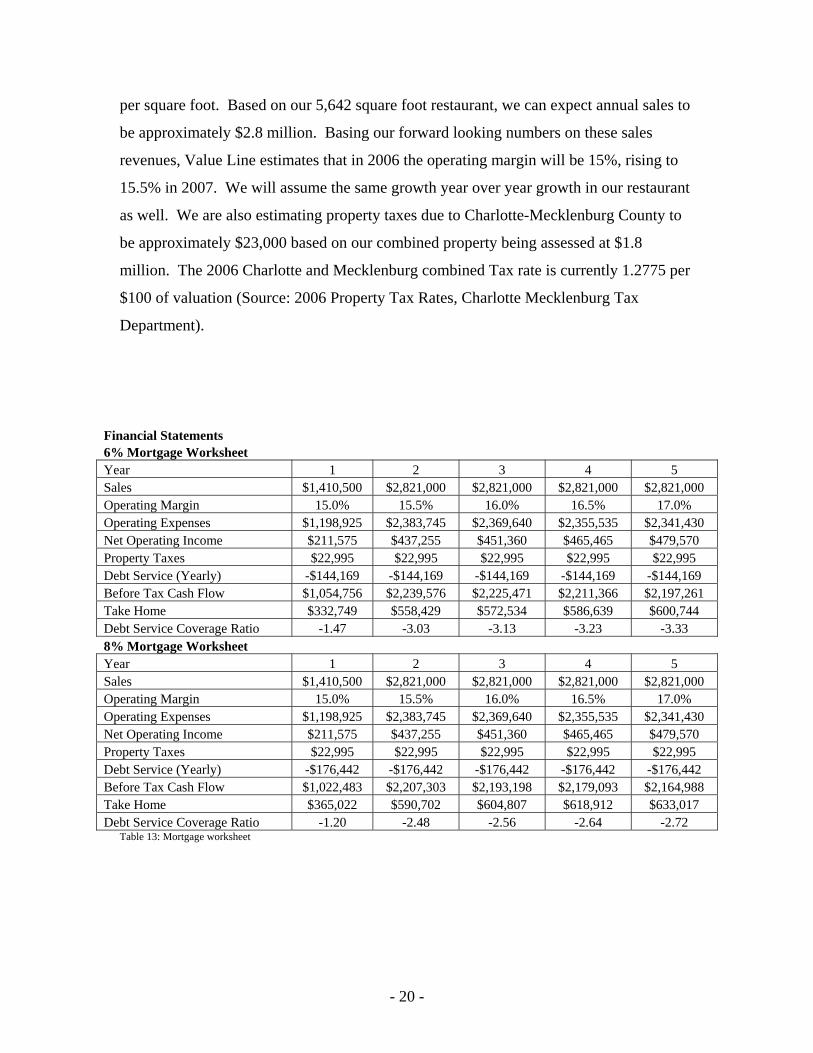

Financial Statements 6% Mortgage Worksheet Year 1 2 3 4 5 Sales $1,410,500 $2,821,000 $2,821,000 $2,821,000 $2,821,000 Operating Margin 15.0% 15.5% 16.0% 16.5% 17.0% Operating Expenses $1,198,925 $2,383,745 $2,369,640 $2,355,535 $2,341,430 Net Operating Income $211,575 $437,255 $451,360 $465,465 $479,570 Property Taxes $22,995 $22,995 $22,995 $22,995 $22,995 Debt Service (Yearly) -$144,169 -$144,169 -$144,169 -$144,169 -$144,169 Before Tax Cash Flow $1,054,756 $2,239,576 $2,225,471 $2,211,366 $2,197,261 Take Home $332,749 $558,429 $572,534 $586,639 $600,744 Debt Service Coverage Ratio -1.47 -3.03 -3.13 -3.23 -3.33 8% Mortgage Worksheet Year 1 2 3 4 5 Sales $1,410,500 $2,821,000 $2,821,000 $2,821,000 $2,821,000 Operating Margin 15.0% 15.5% 16.0% 16.5% 17.0% Operating Expenses $1,198,925 $2,383,745 $2,369,640 $2,355,535 $2,341,430 Net Operating Income $211,575 $437,255 $451,360 $465,465 $479,570 Property Taxes $22,995 $22,995 $22,995 $22,995 $22,995 Debt Service (Yearly) -$176,442 -$176,442 -$176,442 -$176,442 -$176,442 Before Tax Cash Flow $1,022,483 $2,207,303 $2,193,198 $2,179,093 $2,164,988 Take Home $365,022 $590,702 $604,807 $618,912 $633,017 Debt Service Coverage Ratio -1.20 -2.48 -2.56 -2.64 -2.72

Table 13: Mortgage worksheet

- 20 -

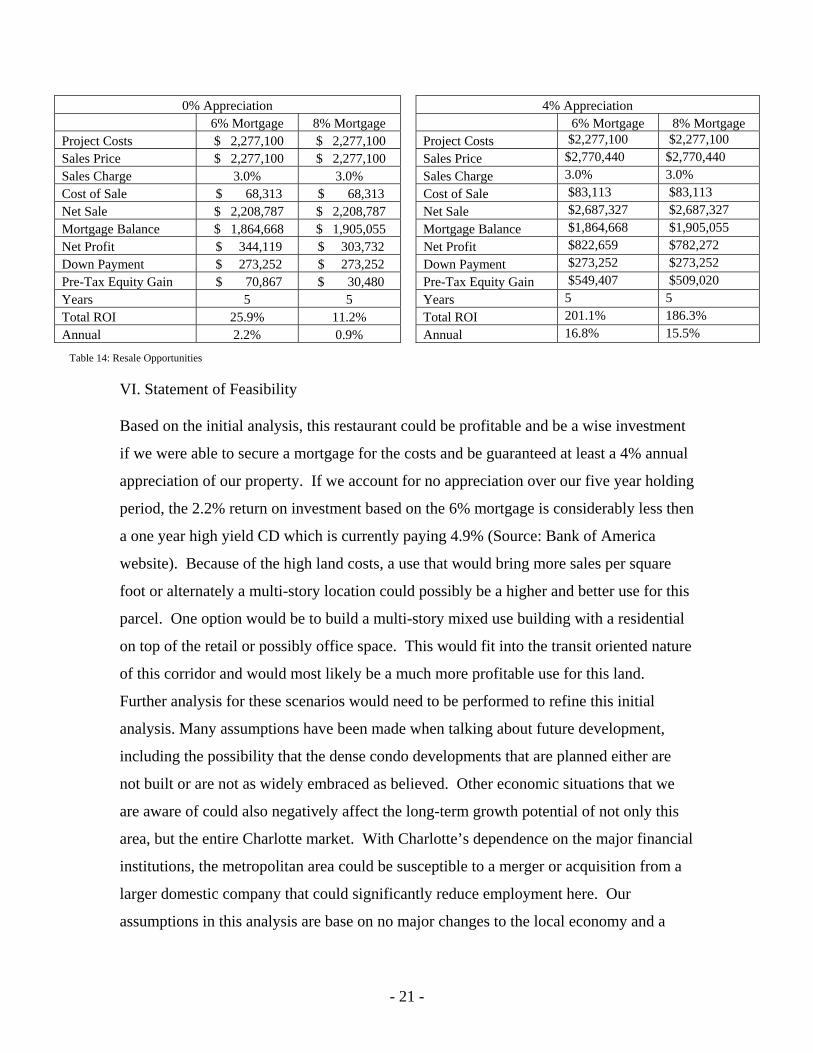

0% Appreciation 4% Appreciation 6% Mortgage 8% Mortgage 6% Mortgage 8% Mortgage

$2,277,100 $2,277,100 Project Costs $ 2,277,100 $ 2,277,100 Project Costs $2,770,440 $2,770,440 Sales Price $ 2,277,100 $ 2,277,100 Sales Price 3.0% 3.0% Sales Charge 3.0% 3.0% Sales Charge $83,113 $83,113 Cost of Sale $ 68,313 $ 68,313 Cost of Sale $2,687,327 $2,687,327 Net Sale $ 2,208,787 $ 2,208,787 Net Sale $1,864,668 $1,905,055 Mortgage Balance $ 1,864,668 $ 1,905,055 Mortgage Balance $822,659 $782,272 Net Profit $ 344,119 $ 303,732 Net Profit $273,252 $273,252 Down Payment $ 273,252 $ 273,252 Down Payment $549,407 $509,020 Pre-Tax Equity Gain $ 70,867 $ 30,480 Pre-Tax Equity Gain

Years 5 5 Years 5 5 201.1% 186.3% Total ROI 25.9% 11.2% Total ROI 16.8% 15.5% Annual 2.2% 0.9% Annual

Table 14: Resale Opportunities

VI. Statement of Feasibility Based on the initial analysis, this restaurant could be profitable and be a wise investment

if we were able to secure a mortgage for the costs and be guaranteed at least a 4% annual

appreciation of our property. If we account for no appreciation over our five year holding

period, the 2.2% return on investment based on the 6% mortgage is considerably less then

a one year high yield CD which is currently paying 4.9% (Source: Bank of America

website). Because of the high land costs, a use that would bring more sales per square

foot or alternately a multi-story location could possibly be a higher and better use for this

parcel. One option would be to build a multi-story mixed use building with a residential

on top of the retail or possibly office space. This would fit into the transit oriented nature

of this corridor and would most likely be a much more profitable use for this land.

Further analysis for these scenarios would need to be performed to refine this initial

analysis. Many assumptions have been made when talking about future development,

including the possibility that the dense condo developments that are planned either are

not built or are not as widely embraced as believed. Other economic situations that we

are aware of could also negatively affect the long-term growth potential of not only this

area, but the entire Charlotte market. With Charlotte’s dependence on the major financial

institutions, the metropolitan area could be susceptible to a merger or acquisition from a

larger domestic company that could significantly reduce employment here. Our

assumptions in this analysis are base on no major changes to the local economy and a

- 21 -

continuation of the population growth that Charlotte has historically had and is projected

to gain in the next several years.

VII. Self-Assessment From the beginning I felt that this would not be a financial success because I struggled to

find an accurate projection to the future population and demographics of this corridor.

The trade area that I drew accounted for a large portion West of I-77, even though that is

not part of our target market. In addition to capturing non-targeted areas, we also

captured the center business district of Charlotte, which skewed many of numbers,

mainly in competition and the number of employees. I would need to do further research

to determine if someone that works uptown and did not commute home via South

Boulevard would patronize our proposed location. For the next phase of analysis I could

add some metric for commuters or visitors to Charlotte that actually ride the light rail,

and possibly add some consumer studies to see what types of people would ride a train to

a restaurant in Charlotte.

- 22 -

VIII. Works Cited US Census Bureau, (www.census.gov) Table 1. Annual Estimates of the Population of Metropolitan and Micropolitan Statistical Areas: April 1, 2000 to July 1, 2005; Table 1a Population in Metropolitan and Micropolitan Statistical Areas in Alphabetical Order and Numerical and Percent Change for the United States and Puerto Rico: 1990 and 2000, Regional Economic Profiles https://bea.gov/bea/regional/reis/action.cfm comparison of 1969 -2004 accessed 9/24/06. Fast Facts about CATS http://216.1.6.76/cgi-bin/MsmGo.exe?grab_id=103499000&EXTRA_ARG=B1%3DGo&CFGNAME=MssFind%2Ecfg&host_id=1&page_id=768&query=1998+transit+tax&hiword=1998+TRANSIT+TAX+TRANSITION+TRANSITIONS+TRANSITO+TRANSITE+TRANSITS+ accessed 9/24/06 ESRI Business Analyst Reports for Metropolitan areas, analog trade areas, and proposed trade areas. http://www.esri.com/software/bao/index.html Reports include Retail Goods and Services Expenditures, Retail Market Place Profile, Demographic and Income Profile, Market Profile, Business Summary. All reports can be provided at request. South Corridor Light Rail Project History http://www.charmeck.org/Departments/CATS/Rapid+Transit+Planning/South+Corridor/South+History.htm Charlotte Future for Transportation and Light Rail information http://www.charmeck.org/Departments/Charlotte+Future/ County Business Patterns (http://censtats.census.gov) for number of establishments in area. Core Based Statistical Area Definition, US Census Bureau Website http://www.census.gov/hhes/www/housing/resseg/cbsa.html Charlotte Chamber of Commerce Website, Economic Profile http://www.charlottechamber.com/content.cfm?category_level_id=133&content_id=190 Charlotte Rezoning Petitions 2006-129 2006-128 2005-117 2005-091 National Restaurant Association, Restaurant Industry at a Glance, North Carolina http://www.restaurant.org/research/state/index.cfm 2006 Property Tax Rates, Charlotte Mecklenburg Tax Department http://charmeck.org/Departments/Tax+Collections/Tax+Rates/2006TaxRates.htm

- 23 -

Bizstats.com RSMeans Quick Cost Estimator http://www.realestatejournal.com/toolkit/constructioncosts/ Request for Qualifications for a Transit Oriented Development in the Scaleybark Station Area, City of Charlotte Economic Development Office Charlotte Department of Transportation, Data collected 2003, 2004 and through June 2005 by CDOT Data Collection Section http://www.charmeck.org/Departments/Transportation/Roads/Traffic+Counts.htm Charlotte Zoning Code, Chapter 9 http://www.charmeck.org/NR/rdonlyres/epjh4qq5b6l7hwu7wkl7gsqyb72ecnqzl452trgowmgnjjherel6gmoflzp3pflm2low2ox56oqht7xz4uylc5sfbhf/ZoningOrdCityChapter09.pdf Charlotte Land Development Standards Manual (Effective December 1, 2006) Parking Standards, 50.09A Bank of America Website, www.bankofamerica.com to obtain prevailing interest rates. Infoplease 2003 NFL Attendance (http://www.infoplease.com/ipsa/A0905961.html, accessed December 1, 2006) Slam Sports, Charlotte Bobcats Attendance Comparison (http://slam.canoe.ca/StatsBKP/BC-BKP-STAT-CHARLOTTEATTCOMP-R.html accessed December 1, 2006) Slapshot for Success, Greater Charlotte Biz, November 2006, Checkers Attendance Figure. MyTownhome Website: Available Listings for 3030 South Community. http://www.mytownhome.com/cgi-bin/searchbrs2.pl accessed December 2, 2006

- 24 -