Embed Size (px)

Citation preview

Slide 1

Capital Budgeting Decision-making Criteria Capital Budgeting Payback Period Discounted Payback Net Present Value (NPV) Internal Rate of Return (IRR) Modified Internal Rate of Return (MIRR)

Slide 2

Capital Budgeting: the process of planning for purchases of long-term assets

Example: Suppose our firm must decide whether to

purchase a new plastic molding machine for $125,000. How do we decide?

Will the machine be profitable? Will our firm earn a high rate of return on the

investment?

Slide 3

Decision-making Criteria in Capital Budgeting The Ideal Evaluation Method should:

Include all cash flows that occur during the life of the project

Consider the time value of money Incorporate the required rate of return on the project

Slide 4

Payback Period How long will it take for the project to generate

enough cash to pay for itself?

0 1 2 3 4 5 86 7

(500) 150 150 150 150 150 150 150 150

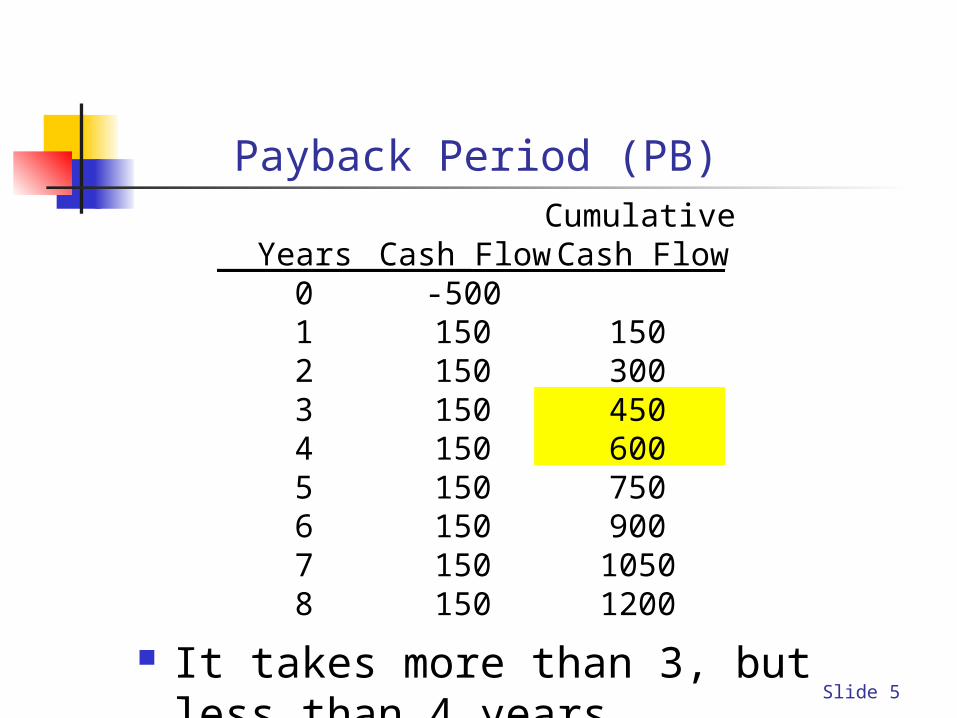

Slide 5

Payback Period (PB)Cumulative

Years Cash Flow Cash Flow0 -5001 150 1502 150 3003 150 4504 150 6005 150 7506 150 9007 150 10508 150 1200

It takes more than 3, but less than 4 years

Slide 6

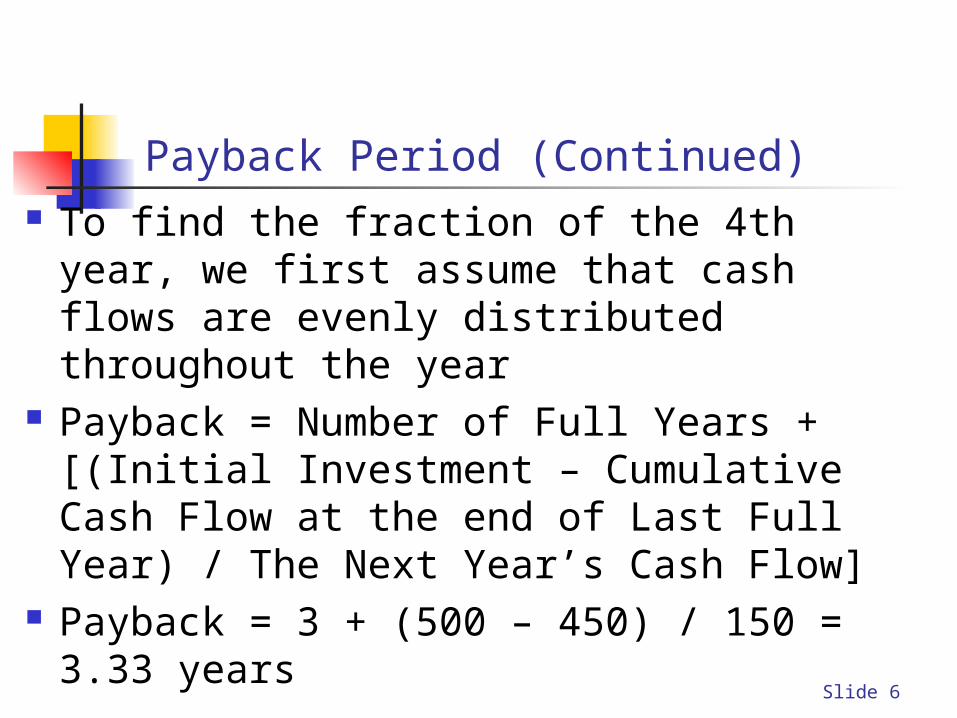

Payback Period (Continued) To find the fraction of the 4th year, we first

assume that cash flows are evenly distributed throughout the year

Payback = Number of Full Years + [(Initial Investment – Cumulative Cash Flow at the end of Last Full Year) / The Next Year’s Cash Flow]

Payback = 3 + (500 – 450) / 150 = 3.33 years

Slide 7

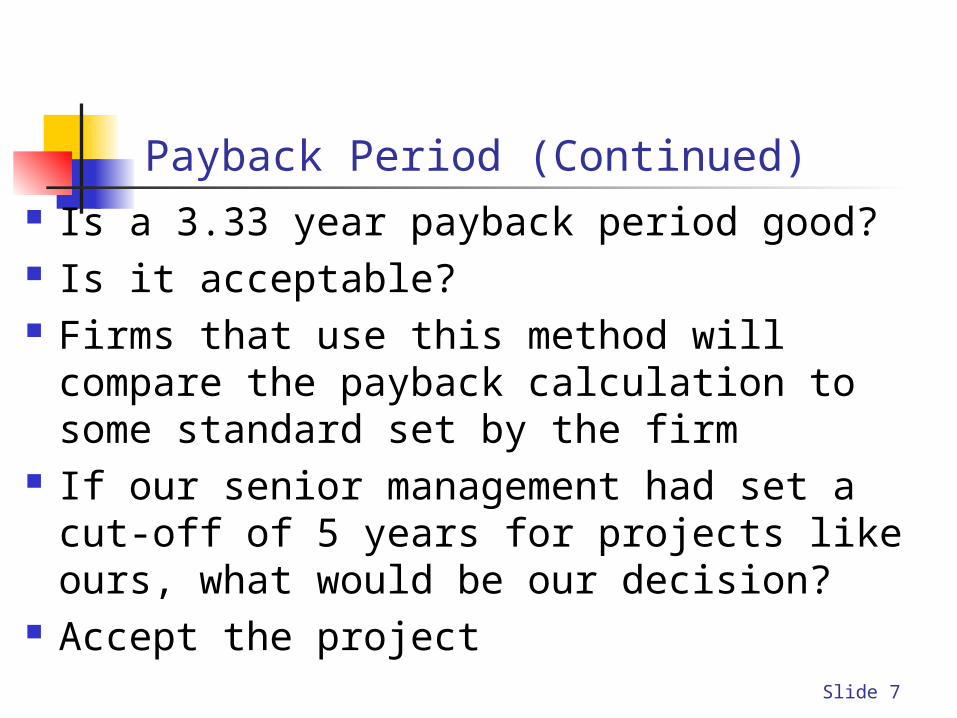

Payback Period (Continued) Is a 3.33 year payback period good? Is it acceptable? Firms that use this method will compare the

payback calculation to some standard set by the firm

If our senior management had set a cut-off of 5 years for projects like ours, what would be our decision?

Accept the project

Slide 8

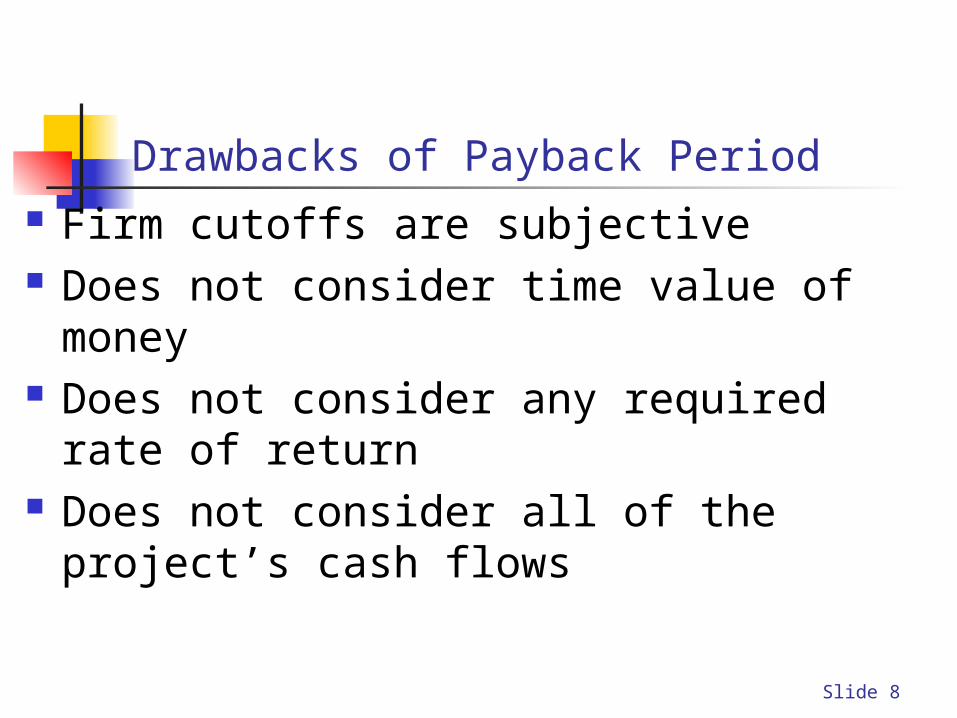

Drawbacks of Payback Period Firm cutoffs are subjective Does not consider time value of money Does not consider any required rate of return Does not consider all of the project’s cash flows

Slide 9

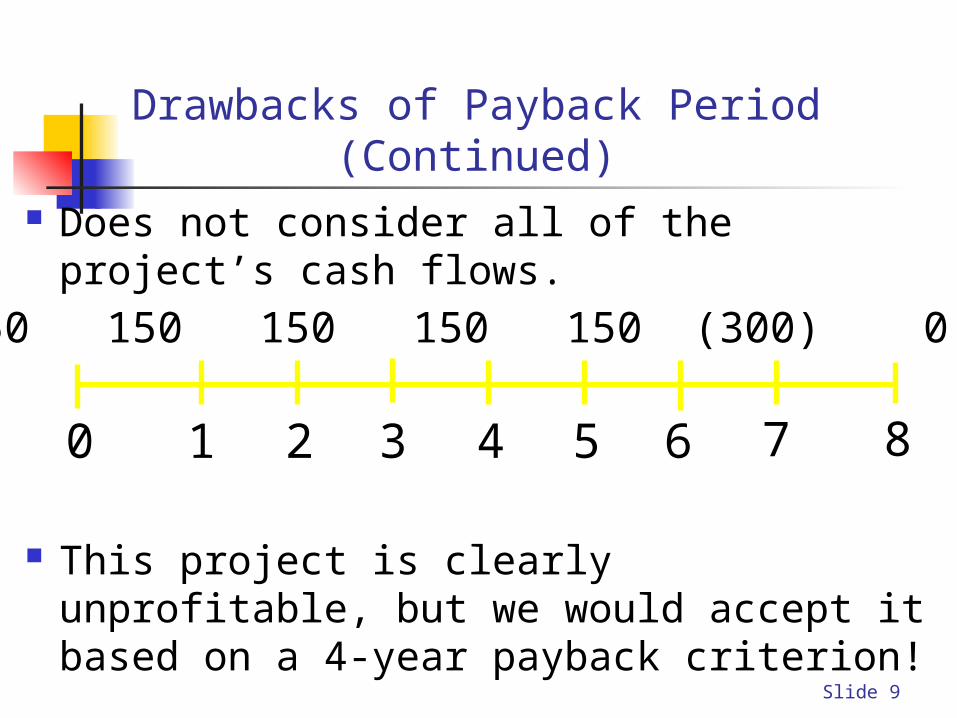

Drawbacks of Payback Period (Continued) Does not consider all of the project’s cash flows.

This project is clearly unprofitable, but we would accept it based on a 4-year payback criterion!

0 1 2 3 4 5 86 7

(500) 150 150 150 150 150 (300) 0 0

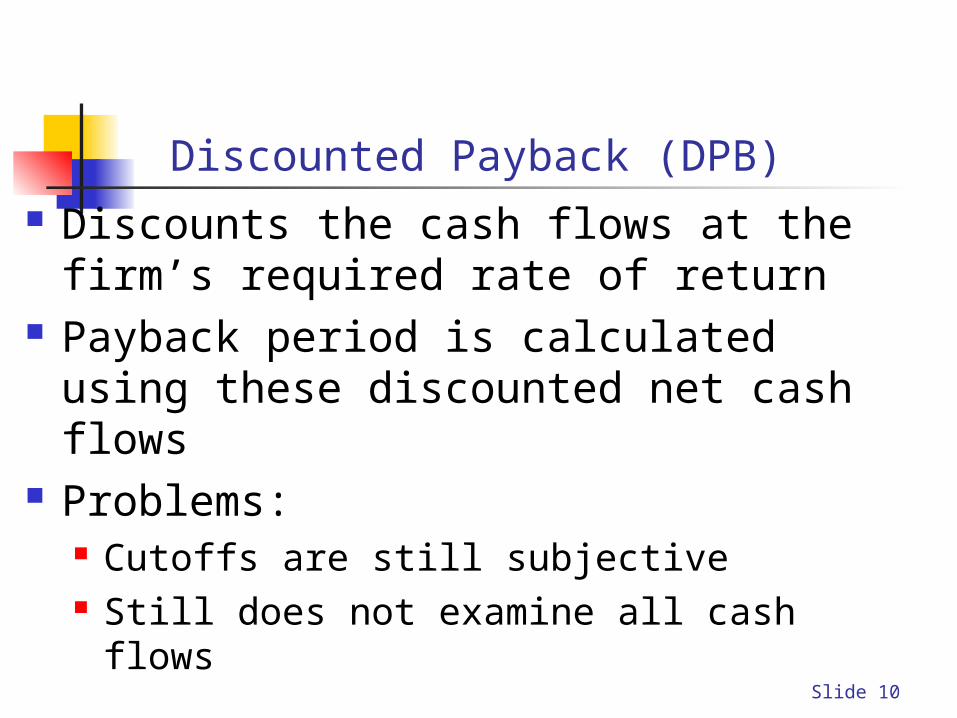

Slide 10

Discounted Payback (DPB) Discounts the cash flows at the firm’s required

rate of return Payback period is calculated using these

discounted net cash flows Problems:

Cutoffs are still subjective Still does not examine all cash flows

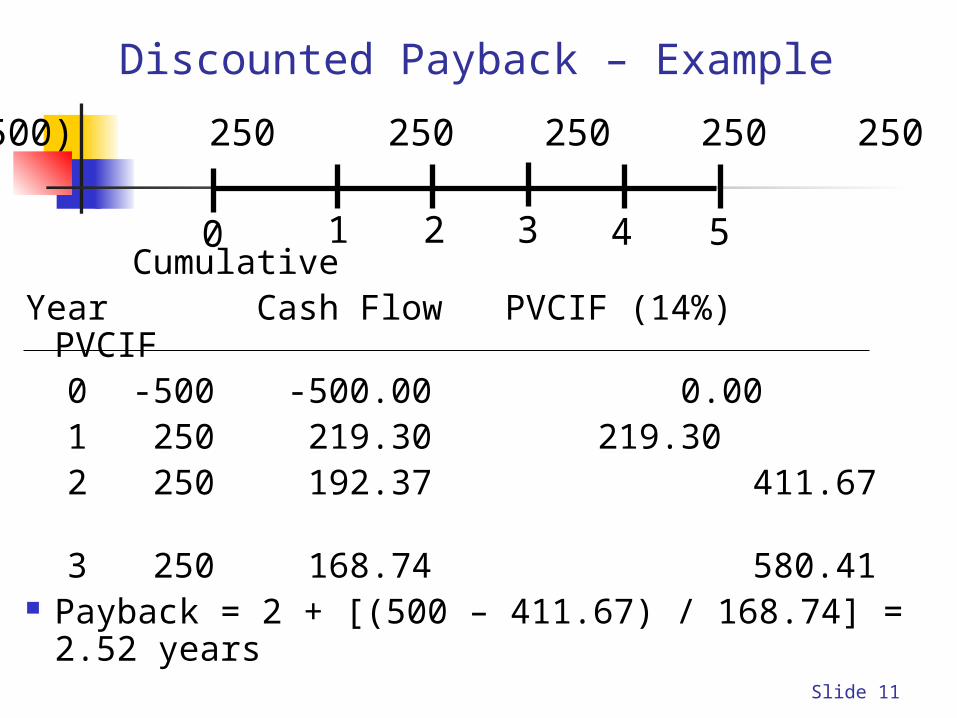

Slide 11

Discounted Payback – Example

CumulativeYear Cash Flow PVCIF (14%) PVCIF 0 -500 -500.00 0.00 1 250 219.30 219.30 2 250 192.37 411.67 3 250 168.74 580.41 Payback = 2 + [(500 – 411.67) / 168.74] = 2.52

years

0 1 2 3 4 5

(500) 250 250 250 250 250

Slide 12

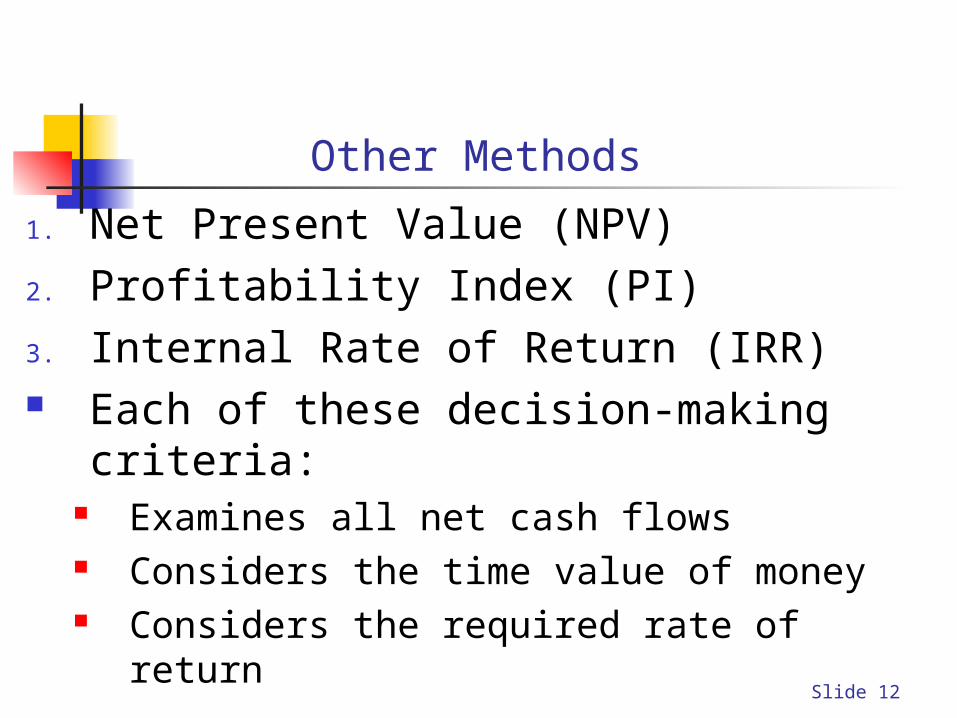

Other Methods

1. Net Present Value (NPV)

2. Profitability Index (PI)

3. Internal Rate of Return (IRR) Each of these decision-making criteria:

Examines all net cash flows Considers the time value of money Considers the required rate of return

Slide 13

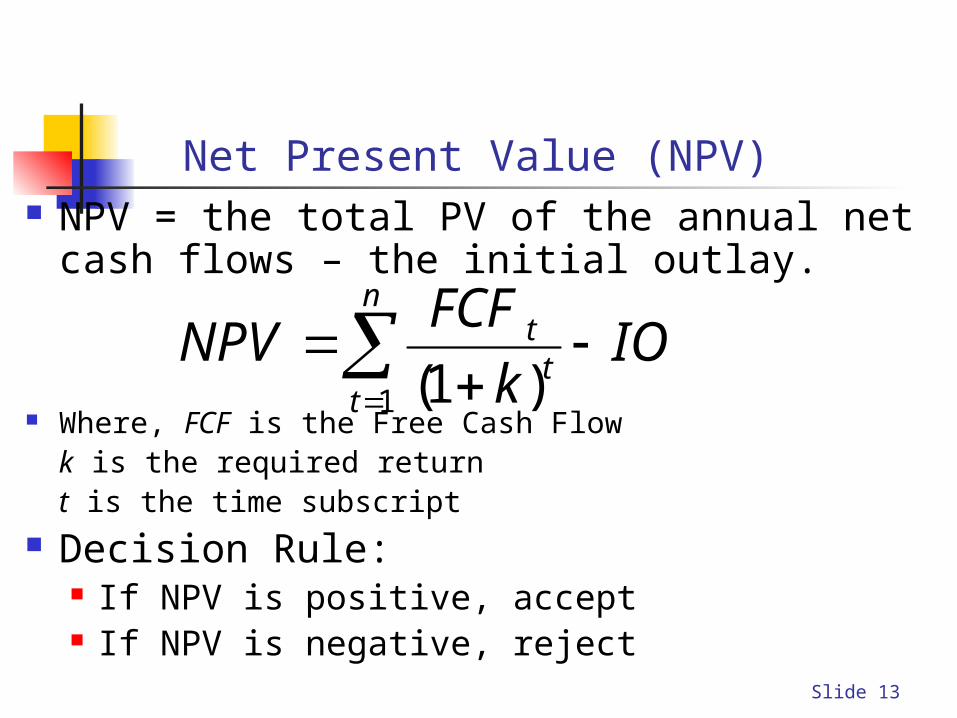

Net Present Value (NPV) NPV = the total PV of the annual net cash flows –

the initial outlay.

Where, FCF is the Free Cash Flowk is the required returnt is the time subscript

Decision Rule: If NPV is positive, accept If NPV is negative, reject

IOk

FCFNPV

n

tt

t

1 )1(

Slide 14

Profitability Index (PI)

Decision Rule: If PI is greater than or equal to 1, accept If PI is less than 1, reject

IO)k(

FCF

PI

IO)k(

FCFNPV

n

tt

t

n

tt

t

1

1

1

1

Slide 15

Internal Rate of Return (IRR) IRR: the return on the firm’s invested capital.

IRR is simply the rate of return that the firm earns on its capital budgeting projects

IRR is the rate of return that makes the PV of the cash flows equal to the initial outlay or NPV = 0

This looks very similar to our Yield to Maturity formula for bonds. In fact, YTM is the IRR of a bond

Slide 16

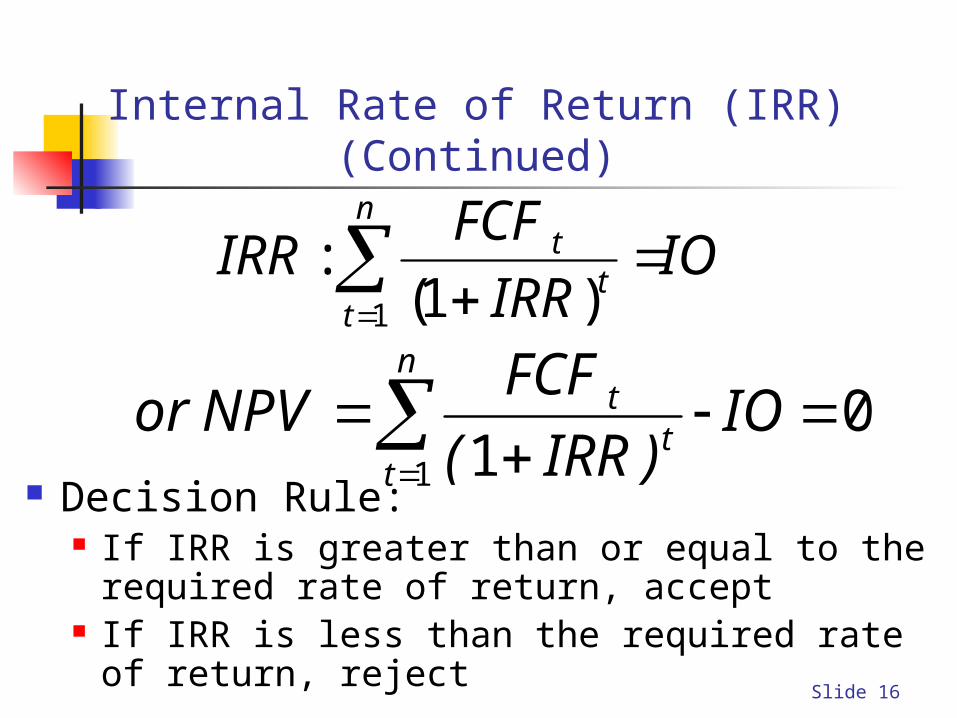

Internal Rate of Return (IRR) (Continued)

Decision Rule: If IRR is greater than or equal to the required rate of

return, accept If IRR is less than the required rate of return, reject

IOIRR

FCFIRR

n

tt

t

1 )1(

:

011

IO)IRR(

FCFNPV or

n

tt

t

Slide 17

Internal Rate of Return (IRR) (Continued)

IRR is a good decision-making tool as long as cash flows are conventional. (- + + + + +)

Problem: If there are multiple sign changes in the cash flow stream, we could get multiple IRRs. (- + + - + +)

0 1 2 3 4 5

(500) 200 100 (200) 400 300

1 2 3

Slide 18

Internal Rate of Return (IRR) (Continued)

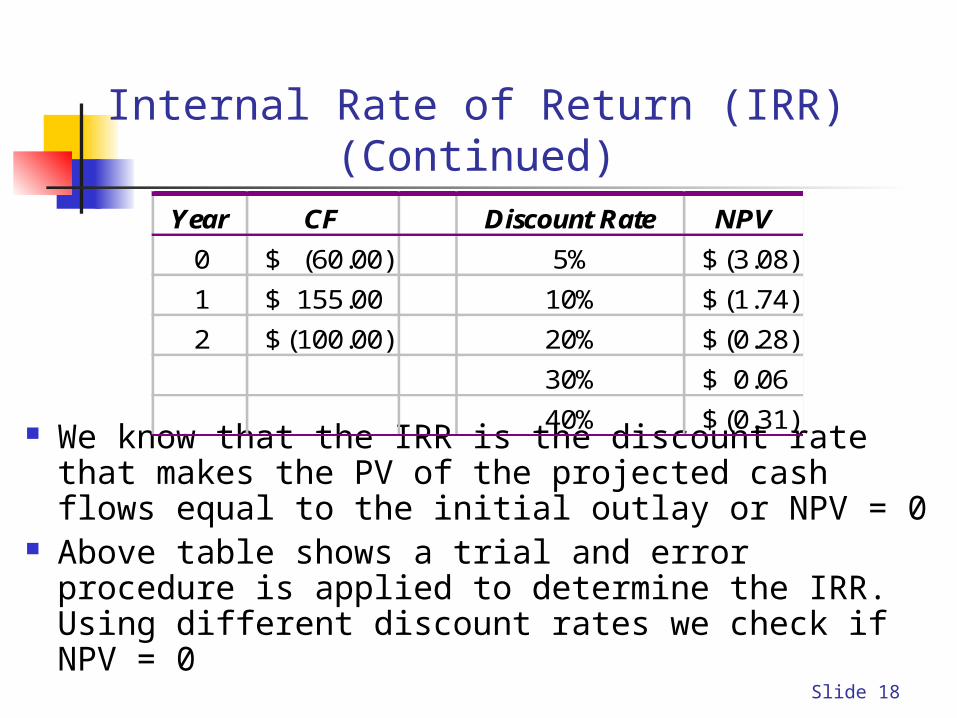

We know that the IRR is the discount rate that makes the PV of the projected cash flows equal to the initial outlay or NPV = 0

Above table shows a trial and error procedure is applied to determine the IRR. Using different discount rates we check if NPV = 0

Year CF Discount Rate NPV

0 (60.00)$ 5% (3.08)$

1 155.00$ 10% (1.74)$

2 (100.00)$ 20% (0.28)$

30% 0.06$

40% (0.31)$

Slide 19

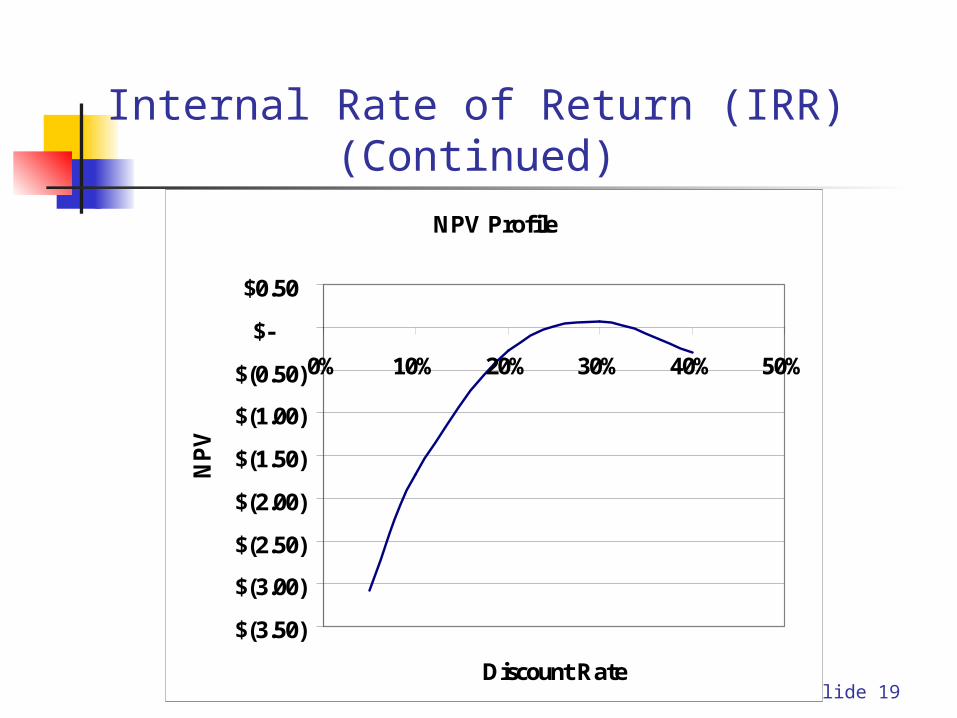

Internal Rate of Return (IRR) (Continued)NPV Profile

$(3.50)

$(3.00)

$(2.50)

$(2.00)

$(1.50)

$(1.00)

$(0.50)

$-

$0.50

0% 10% 20% 30% 40% 50%

Discount Rate

NP

V

Slide 20

Modified Internal Rate of Return (MIRR) IRR assumes that all cash flows are reinvested at

the IRR MIRR provides a rate of return measure that

assumes cash flows are reinvested at the required rate of return

Slide 21

Modified Internal Rate of Return (MIRR) Calculate the PV of the cash outflows (PVCOF) using the required

rate of return – this is usually the investment amount Calculate the FV of the cash inflows (FVCIF) at the last year of the

project’s time line. This is also called the terminal value (TV) Using the required rate of return MIRR is the growth rate of money from initial investment to

terminal value over the life of the investmentN I/Y P/Y PV PMT FV MODE

Project Life

MIRR 1 -Investment (PVCOF)

0 Terminal Value

(FVCIF)

Slide 22

Modified Internal Rate of Return (MIRR) (Continued)

Finding FV of Uneven Cash Flows: Cumulate CF one year at a time taking FV into account Find FV of each CF at the end of project life and then

sum FVs Use of NPV function (faster): First, find the PVCIF

(NPV) (exclude initial investment) using required return. Second, change the sign of NPV and store it in PV (now a single cash flow as PV of all cash inflows) to find FV at the end of project life