Embed Size (px)

Citation preview

Credit Rating is an estimate of the credit worthiness of an individual, corporation, or a country. It is an opinion made by credit evaluators of a borrower’s potential to repay debt. Every rating grade comes with its probability of default, which in turn assists investor/lender to take informed investment decision. Rating is arrived after considering various financial, non-financial parameters, past credit history and future outlook. There are various types of ratings viz. Issuer Rating/ Obligor Rating, Bank loan Rating, Issue based Ratings, Project Rating etc. Based on type of borrower/issuer, Ratings can be classified as Individual Rating, Corporate Rating, Bank/Financial Institutions Rating, SME Rating, MFI Rating etc. SMERA offering:

1. SMERA Credit Ratings provides a comprehensive and independent third-party evaluation of the overall condition of the applicant. Currently, SMERA offers Obligor Ratings which takes into account the financial and non-financial factors that have bearing on the credit worthiness of the applicant.

2. At present, SMERA offers following products:

o MSME Rating o Greenfield & Brownfield Grading o Microfinance Institutions (MFI) Rating o Green Rating o Risk Management Solutions

3. SMERA Rating endeavors to enhance the market standing of the applicant amongst lenders, trading partners and prospective customers.

1) Wide Recognition and Acceptance Considering that different banks deploy customized rating processes and disclosure requirements while disbursing credit, applicants find themselves investing significant time, effort and money while approaching lenders for credit. At SMERA, we have adopted a standardized, comprehensive, transparent and reliable rating process to arrive at a representative risk of a unit. Further, SMERA is supported by SIDBI and a large number of public and private sector banks in the country & such wide acceptance by the lender fraternity has made SMERA Ratings an integral part of the loan sanctioning process. The Rating process is standardized across the industry and sectors and this has enabled simplification of application process to the lenders, thus making it cost-effective for the units while applying for credit either for the first time or while enhancing their credit limit

2) Memorandum of Understanding (MOU) with Banks SMERA has entered into MOUs with 29 Banks/Financial Institutions. Banks such as:, State Bank of India, Punjab National Bank, Syndicate Bank, Canara Bank, State Bank of Bikaner & Jaipur, Dena Bank, Corporation Bank, Union Bank of India, UCO Bank, CitiGroup, Bank of India, Vijaya Bank, Allahabad Bank and Bank of Baroda and many others are working closely with SMERA to popularize third party ratings amongst their existing as well as potential MSME units in the country. Some of these banks are also extending interest rate benefits to better rated SMERA units.

3) Favourable borrowing terms Better Ratings from SMERA has started benefiting MSME units by way of favorable borrowing terms, such as:

Lower collateral requirements

Reduced Interest Rates

Simplified lending norm

4) Faster Access to Credit SMERA Ratings have enabled banks/ lending institutions in reducing their turnaround time in processing credit applications from the MSME units, thus providing applicants access to timely and adequate credit.

5) Lower Rating Fees SMERA Rating fees are economical and affordable for MSME units, with eligible SSI units enjoying rating fee subsidy up to 75% under the "Performance & Credit Rating Scheme of NSIC". In order to avail the 75% subsidy, the eligible SSI units should possess an valid SSI Registration Certificate / Entrepreneur Memorandum Number (Permanent / Provisional)& should not have availed any rating subsidy in the past from NSIC)..

6) D&B D-U-N-S® Number Units availing SMERA Ratings are assigned a unique 9 digit D&B D-U-N-S® Number. This number is an international identification number, which provides unique identity to single business entity. D&B D-U-N-S® Number is used by the world's most influential standards-setting organizations and is recognized, recommended and/or required by more than 500 global, industry and trade associations for their internal requirements.

7) SMERA : An initiative of leaders SME Rating Agency of India Limited (SMERA) is a joint initiative by Small Industries Development Bank of India (SIDBI), Dun & Bradstreet Information Services India Private Limited (D&B), and several leading banks in the country. SMERA is the country's first & only dedicated rating agency that focuses primarily on the MSME segment. SMERA's primary objective is to provide Ratings that are comprehensive, transparent and reliable. The objective of this Rating is to facilitate greater and easier flow of credit from the banking sector to MSMEs and also as a tool to facilitate self improvement.

8) Fair evaluation amongst peers SMERA Ratings categorize MSMEs on the basis of their size, thus enabling ease of comparison of the rated unit with its peer within the industry. The size categorization enables rational comparison of companies of the same size, thus ensuring that the smaller units are not compared with larger units or companies and are put at a disadvantage while applying for credit.

9) Benefit of SMERA Ratings to Units

Enhances credibility of the unit

Open doors to corporate sector having large vendor base

A tool to instill good governance practices within the unit proving beneficial in the long run

Aids in building trust in the international trade partners

A tool for self correction and improvement

Better SMERA Ratings encourage lenders to offer credit on better terms

Enables getting shortlisted by customers/lenders/vendors/private equity and other financiers

Approach newly incorporate SME Exchange for broad basing share holding and funding

10) Benefits of SMERA Ratings to Banks/Lenders

Provides banks/lenders a neutral, third party and an un-biased opinion on the borrower

Provides comfort to lenders

Facilitates pricing of loan products on attractive terms

Provides an early warning signals to banks during periodic review of accounts

Rating Methodology (Manufacturing)

SMERA rating framework considers a number of financial and non financial parameters of the enterprise and the impact of the macro economic factors like government policies, trade policies and regulations and the industry specific dynamics. SMERA believes that the industry in which a SME operates has a direct bearing on the overall performance of the SME and therefore rates SMEs based on industry benchmarks. SMERA Rating is a comprehensive assessment of the enterprise taking into considerations the overall financial and non financial performance of the subject company vis-à-vis the other peers in the industry in the same line of business and size criteria.

Based on its assessment and understanding, SMERA has developed rating methodology framework which mainly addresses the following areas

A) Industry Risk The industry in which an enterprise operates plays a crucial role in the credit risk assessment. It is a key determinant of the level and volatility in earnings of any business

B) Business Risk Business risk is the possibility of a credit customers failing to pay because of circumstances connected with the customer’s business activities and management.

I) Market Risk :

Market risk is the exposure of the unit to the forward and backward linkage in the course of conducting its business, and the risk of facing sustained periods of unfavorable trends in such factors as product prices, raw material prices, single product dependence, pricing inflexibility, etc.

II) Operating Efficiency

In markets where competitiveness is largely determined by costs, the market position is determined by the unit’s operational efficiency. The result of these factors is reflected in the ability of the unit to maintain /improve its market share and command differential in pricing. In a competitive market, it is critical for any business unit to control its costs at all levels. This assumes greater importance in commodity or "me too " businesses, where low cost producers almost always have an edge. Cost of production to a large extent is influenced by location of the production unit(s), access to raw materials, access to human resources, scale of operations, technology, level of integration , experience and the ability of the unit to efficiently use its resources.

C) Management Risk Management risk refers to the instance of risk of non payment arising out of a business failure due to the perceived inefficacies of the management. The elements in management risk are assessing the management quality judged on the basis of the basic educational qualification, professional experience of the entrepreneur; and business attitude that is related to the motivation of carrying out the business and pursuing business strategies.

Majority of the Indian SMEs are essentially managed by one or two key persons. In this scenario, the quality of management personnel becomes critical. In assessing management quality three factors are critical:

Character - relate to the willingness to pay. Apart from the characteristic disposition of honesty and integrity, several aspects are judge in terms of

a. Track record of previous borrowing and payment is an indicator. b. Whether the owners/ directors have a financial interest in the business. c. Business premises given the impression of a well-run unit.

Ability - relates basically to the ability to pay. Credit worthiness of the buttoner/borrowing company is assessed, including financial strength, and

Capacity - refers to the borrower having technical, managerial and financial abilities in order to operate profitably and succeed in business.

Quality of management would determine level of control, overall organizational capability, willingness to service loan, etc. Absence or inadequate of presence of these factors would lead towards greater risks. Type of organizational also adds to the management risk.

Past experience of the management in handling similar business, performance of group companies and their track record, vision and mission of the management, organisation structure, succession issues, networth and corporate governance also plays an important role in assessing the management.

D) Financial Risk Financial risk analysis involves thorough evaluation of the financials of the SMEs. Careful analysis of the audited financials, observations of auditors in the auditors report and notes to accounts, consistent treatment of financials play an important role. Key ratio analysis, trend ratios, financial disclosures and off Balance sheet items and their impact on the profitability is studied and analysed in depth. Further the source of financial funding and their impact on the capital employed structure needs to be analysed. Availability of liquid investments, unutilized lines of credit, financial strength of group companies, market reputation, relationship with financial institutions and banks, enterprise perceptions and experience of tapping funds from different sources also play an important role in financial analysis. Past performance of the company, level of financial transparency i.e. quality of documents and future plans plays an important role in the determination of rating.

While the focus of rating exercise is to evaluate the future cash flow adequacy for servicing debt obligations, a detailed review of the past financial statements is critical for better understanding of the influence of all the business and financial risk factors. Evaluation of the existing financial position is also important for determining the sources of secondary cash flows and claims that may have to be serviced in future

E) New Project risks: The scale and nature of new projects can significantly influence the risk profile of any . Unrelated diversifications into new products are invariably assessed in greater detail.

The main risks from the new projects are time and cost overruns, even non-completion in an extreme case, during construction phase; financing tie-up; operational risks; and market risk. Besides clearly establishing the rationale of new projects, the protective factors that are assessed include track record of the management in project implementation, experience and quality of the project implementation team, experience and track record of technology supplier, implementation schedule, status of the project, project cost comparisons, financing arrangements, tie-up of raw material sources, composition of operations team and market outlook and plans.

Other parameters

Besides these 5 broad heads other parameters like applicability of pollution control certificate, impact of subsidies and sales tax deferral loans, impact of changes in accounting policies, unabsorbed depreciation and business loss, impact of non insurance or inadequate insurance of assets, extraordinary or windfall gains and losses, analysis of bank statements, violations of accounting standards if any, change in management, impact of the new monetary or fiscal policies or significant development in the industry are thoroughly assessed on case to case basis. Legal risks, foreign exchange fluctuation risk and hedging mechanism followed by the enterprise if any, is studied in detail.

SMERA rating framework considers a number of financial and non financial parameters of the enterprise and the impact of the macro economic factors like government policies, trade policies and regulations and the industry specific dynamics. SMERA also believes that the industry in which a SME operates has a direct bearing on the overall performance of the SME and therefore rates SMEs based on industry benchmarks SMERA Rating is a comprehensive assessment of the enterprise taking into considerations the overall financial and non financial performance of the subject company vis-à-vis the other peers in the industry in the same line of business and size criteria.

Based on its assessment and understanding, SMERA has developed rating methodology framework which mainly addresses the following areas

A) Industry Risk

B) Business Risk

C) Management Risk

D) Financial Risk

E) New Project Risks

Brownfield / Greenfield Grading Rationale SMERA Project/Startup Enterprise Grading is a comprehensive assessment of all the risk factors affecting the project completion and its continued operations thereafter. It is an independent, third party assessment of a unit providing a clear indication of the likelihood of viable operations post project completion.

The risk parameters proposed to be captured inter alia include following:

A) Construction and Project Specific Risks

Completion risk refers to the inability of a project to commence commercial operations on time and within the budgeted cost. The construction risk is high at the project commencement stage and requires efficient monitoring. According to SMERA, the risk associated at construction stage is high and the risk perception is influenced by credit worthiness, past project expertise and track record of the key stakeholders.

B) Management Risk The factors in this category provide an indication about the quality of management and the clarity of the promoters about the project, the project management expertise and the promoters’ integrity. Parameters like educational qualification, professional experience, previous track record in implementing projects of similar size and nature, networking ability, ability to raise funds, tie up with customer and suppliers etc are considered under this risk. C) Operational Risk / Business Risks The factors in this category provide an indication about operational risks and business risks associated with the project. This category analyze factors such as: location risk, access to raw materials, access to customers, logistic risks, product complexity, product obsolescence risks, competition risks, backward and forward synergies enjoyed by the unit, the fiscal and the tax advantages etc are analysed.

D) Market Risk / Industry Risk While assessing the application of a startup/new project, SMERA evaluates the industry/market risks associated with the project. Factors such as entry/exit barriers within the industry, level of competition, demand and supply dynamics, logistic factors etc. are considered while evaluating Industry Risk. Also, macro risks such as: risks arising from economic instability, recessionary economic conditions, impact of global factors etc. are also considered while assigning risk grades. Similarly, industry characteristics are also factored while assessing the project, hence growth vs. maturity phase or organized vs. un-organized type, distributed vs. consolidated phase are explored while assessing the risk of the project. Government policies also play an important part while assessing the project, hence changes in taxation policy, framework pertaining to taxation, reservation of products, patenting rules, duties and levies on products, withdrawals/introduction of special fiscal incentives, subsidies etc has direct bearing on the viability of the project.

E) Financial Risk While undertaking the financial analysis of the project, a comparison is carried out of the submitted projects’ financial ratios with the relevant industry financial ratio benchmarks. Financial factors of the project such as: breakeven point analysis, discounted cash payback, the sensitivity analysis vis-à-vis the assumptions of the project, debt service coverage ratio, future cash flows etc are analyzed in detail to assess the financial risk associated with the project

F) Sustainability Risk Under this category, the applicants’ understanding & preparedness in seeking the essential clearances from respective authorities is understood and compared with the requirements of the industry for starting the operations. In absence of proper understanding and clarity on the matters related to mandatory clearances to start operations, it is observed that projects have suffered cost overrun & losses and, on some occasions, resulted in closure of the unit by the regulatory or statutory authorities. Clearances such as: pollution clearance, power clearance, water clearance etc are considered before assigning a risk grade to the project. Similarly, location of the project near the industrial area, or place of historical importance, or wildlife area, or forests or wetland regions etc are also considered from the future sustainability of the project.

MFI Rating Methodology SMERA MFI Rating is an independent, third party comprehensive assessment of risks involved of underlying portfolio of MFI and its resultant impact. Besides evaluating creditworthiness of MFIs, SMERA ratings also assess trustworthiness, operational excellence, quality of loans etc of a Micro Finance Institution, amongst other subjective parameters. The assessment of MFIs also covers financial risk, operational risk, management risk,

political risk and matters related to its internal governance, strategic positioning, social responsiveness, liability of lenders and social profile.

Based on its assessment and understanding, SMERA has developed rating methodology framework which primarily addresses the following areas:

A) Business Orientation & Outreach

Business Orientation and Outreach of a MFI is an important parameter to assess the growth strategies employed by the MFI and its impact on MFIs’ development. Amongst other things, following factors are considered while assessing the business orientation and outreach of a MFI, factors such as: number of active borrowers covered, self help groups covered , their reach in number of villages & districts, number of branches opened since inception, size of the loan cycle, variety of loan products, increase in Gross Loan Portfolio etc. Similarly, parameters such as direction & clarity of the management, its vision and commitment, dependence on Government grants & subsidies, ability to raise variety of funds from the investors and lenders, degree of association with promoter institutions, audit reviews etc are also part of the analysis while assessing the MFIs’ business orientation.

B) Management Quality Management risk pertains to the risk of non-payment arising out of business failure due to the perceived management weakness. The primary parameter assessed under the management risk is the quality of management, & this is judged on the basis of the educational qualification, professional experience and business attitude of the entrepreneur towards the business.

Under quality of management other parameters such as: level of control, overall organizational capability, willingness to service loan, etc is also assessed under the management evaluation process.

C) Operational Efficiency and Risk Management Under this category analysis of MFIs internal manual is undertaken where in following factors are assessed: target market definition & its characteristics, loan origination, appraisal, approval, disbursement, monitoring and recovery processes and procedures; loan classification & provisioning; policies for interest accrual / non-accrual etc. Further, MFIs internal controls are also assessed by evaluating information systems for loan tracking; their capacity, reliability, and effectiveness for generating portfolio related information and report.

The capacity assessment refers to the ability of MFI’s internal system to cope with the transaction volumes, generation of variety of reports-including client payment history, loan delinquencies and their ageing, branch/geographic area/sector/credit officer wise break-ups, details and trends; details of rescheduled loans etc. Group cohesiveness is a key determinant in evaluation of MFI. MFIs criterion for selection of group, consistent Group Training and Group Recognition tests, loan utilization checks, recovery mechanisms etc are also analyzed under the capacity assessment of a MFI.

Assessment of asset liability mismatch is undertaken in detail while assessing a MFI. On initiation of MFIs activity, liquidity and asset-liability management of the institution starts becoming complex & hence, under the study, MFIs ability to deal with this complexity is assessed. Similarly, MFIs ability to deal with the fluctuating demand, prepayments by borrowers, varying interest rates and tenor of loans, their re-payment track record etc is assessed.

D) Portfolio Quality Loan portfolio is the most important asset of any MFI, as it is the primary income generating source for MFIs. Most failures amongst financial institutions stem from deterioration in the quality of loan portfolio. Thus it is imperative to track the year on year growth of the loan portfolio and its quality. SMERA analyses the portfolio quality of the MFIs by doing ageing analysis, sectoral analysis, product wise analysis etc. SMERA compares the portfolio

management system with organizational guidelines and generally accepted industry best practices to identify systemic inadequacies, depth of controls and resultant risks.

E) Financial Performance Ratios like Operational Self Sufficiency, Financial Self Sufficiency, Capital adequacy Ratios, Adjusted Return on Assets, Adjusted Return on Equity, Productivity ratios etc are analyzed. Yield on Portfolio, Loan loss reserve to Gross o/s portfolio, cost of funds ratio etc also require analysis.

F) Social and Lenders Responsibility MFIs outlook towards the social objectives while starting the enterprise is assessed. Hence following parameters are assessed: developmental and livelihood programmes run by the MFI, training provided, transparency and approach of the MFI towards client grievances, interest rate transparency, multiple lending’s etc are assessed. Thus an evaluation of MFI would be comprehensive assessment based on the financial and non financial parameters of any MFI.

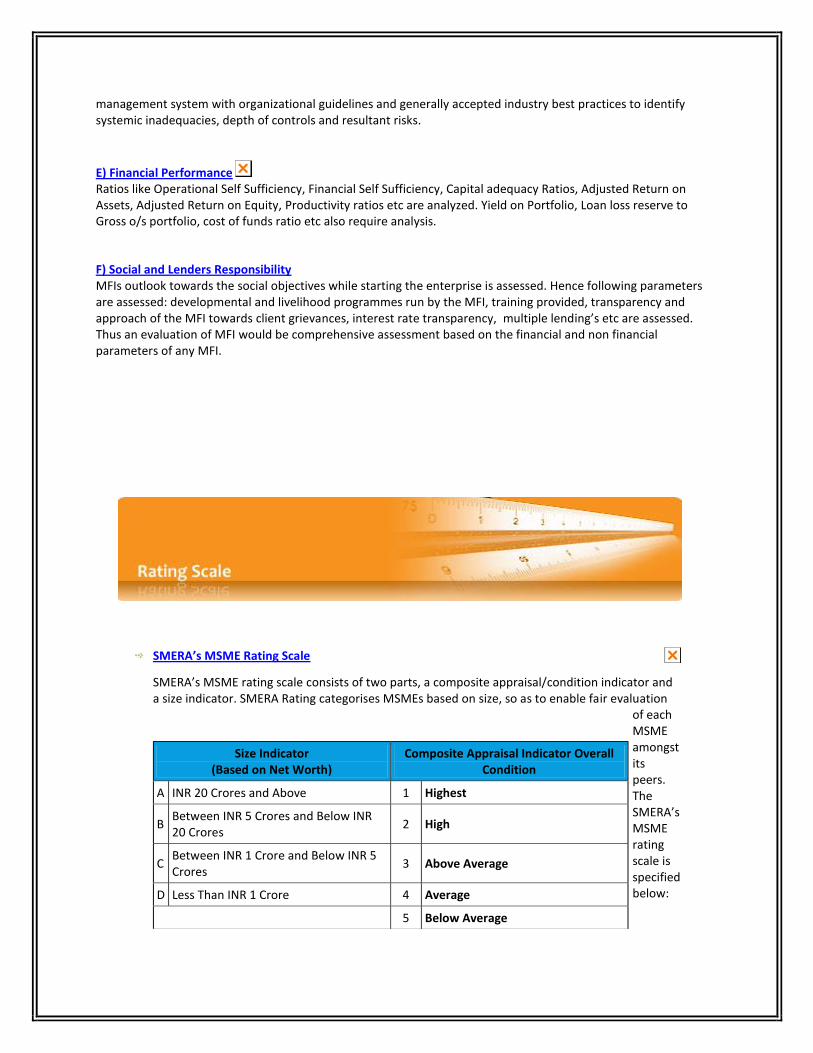

SMERA’s MSME Rating Scale

SMERA’s MSME rating scale consists of two parts, a composite appraisal/condition indicator and a size indicator. SMERA Rating categorises MSMEs based on size, so as to enable fair evaluation

of each MSME amongst its peers. The SMERA’s MSME rating scale is specified below:

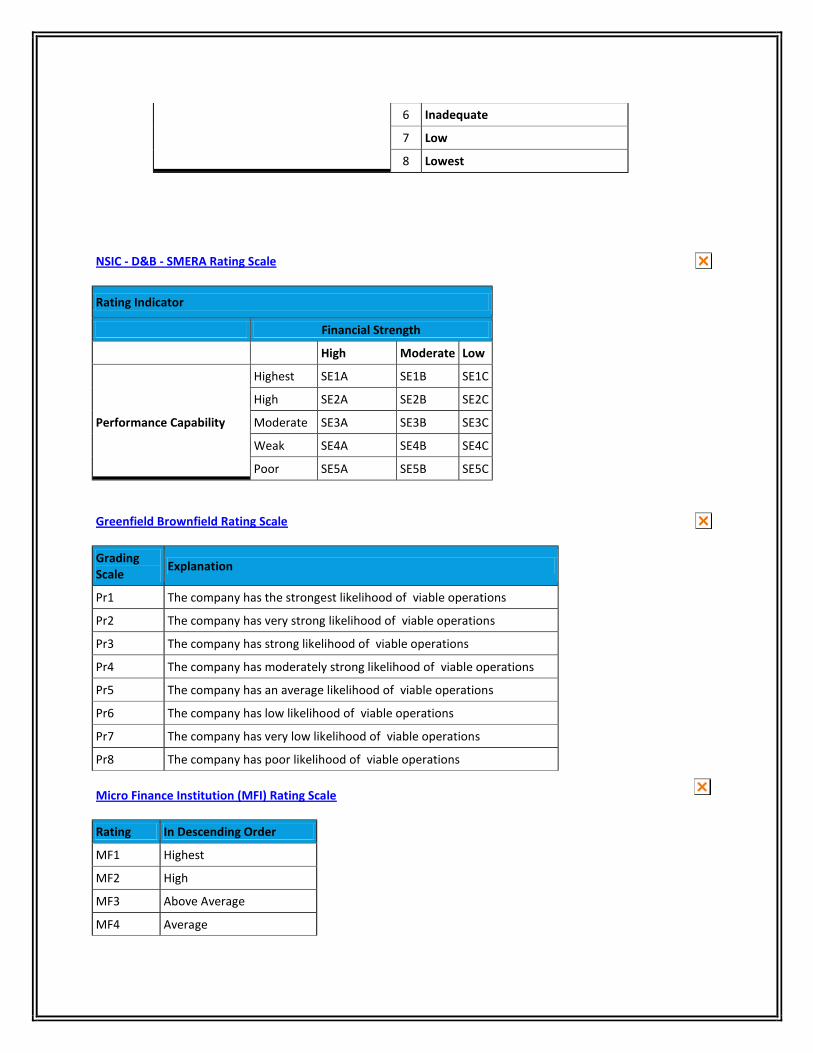

Size Indicator (Based on Net Worth)

Composite Appraisal Indicator Overall Condition

A INR 20 Crores and Above 1 Highest

B Between INR 5 Crores and Below INR 20 Crores

2 High

C Between INR 1 Crore and Below INR 5 Crores

3 Above Average

D Less Than INR 1 Crore 4 Average

5 Below Average

6 Inadequate

7 Low

8 Lowest

NSIC - D&B - SMERA Rating Scale

Rating Indicator

Financial Strength

High Moderate Low

Performance Capability

Highest SE1A SE1B SE1C

High SE2A SE2B SE2C

Moderate SE3A SE3B SE3C

Weak SE4A SE4B SE4C

Poor SE5A SE5B SE5C

Greenfield Brownfield Rating Scale

Grading Scale

Explanation

Pr1 The company has the strongest likelihood of viable operations

Pr2 The company has very strong likelihood of viable operations

Pr3 The company has strong likelihood of viable operations

Pr4 The company has moderately strong likelihood of viable operations

Pr5 The company has an average likelihood of viable operations

Pr6 The company has low likelihood of viable operations

Pr7 The company has very low likelihood of viable operations

Pr8 The company has poor likelihood of viable operations

Micro Finance Institution (MFI) Rating Scale

Rating In Descending Order

MF1 Highest

MF2 High

MF3 Above Average

MF4 Average

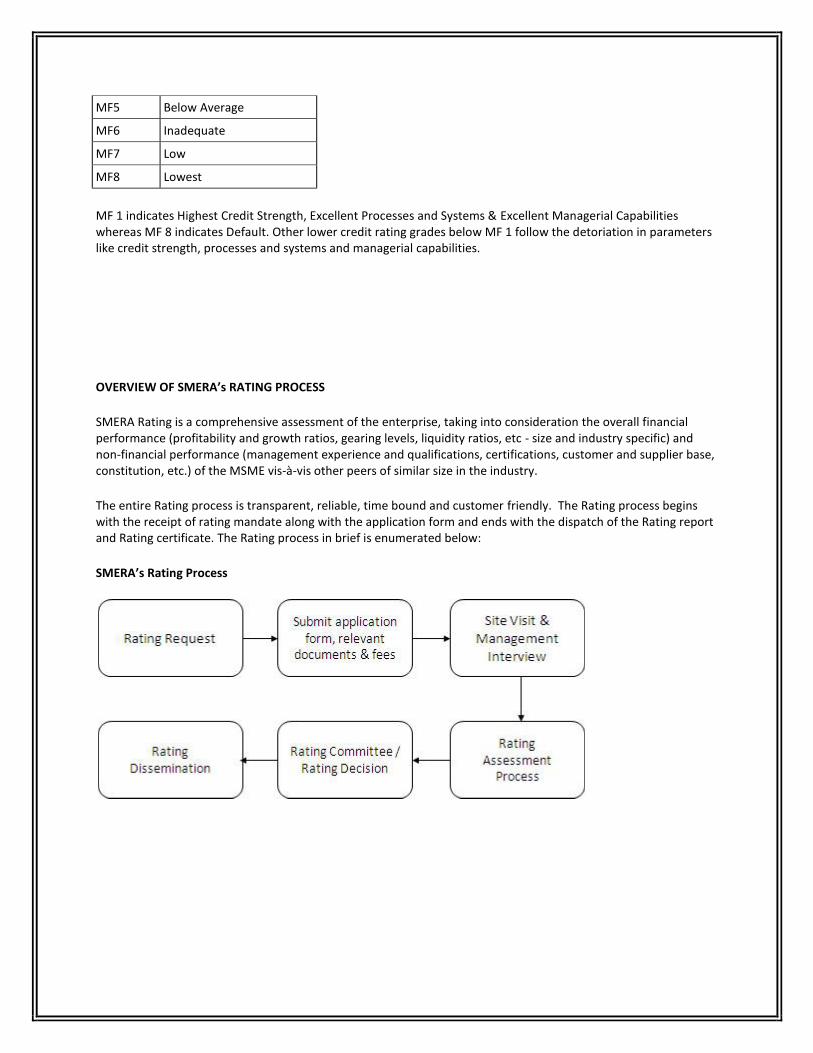

MF5 Below Average

MF6 Inadequate

MF7 Low

MF8 Lowest

MF 1 indicates Highest Credit Strength, Excellent Processes and Systems & Excellent Managerial Capabilities whereas MF 8 indicates Default. Other lower credit rating grades below MF 1 follow the detoriation in parameters like credit strength, processes and systems and managerial capabilities.

OVERVIEW OF SMERA’s RATING PROCESS

SMERA Rating is a comprehensive assessment of the enterprise, taking into consideration the overall financial performance (profitability and growth ratios, gearing levels, liquidity ratios, etc - size and industry specific) and non-financial performance (management experience and qualifications, certifications, customer and supplier base, constitution, etc.) of the MSME vis-à-vis other peers of similar size in the industry.

The entire Rating process is transparent, reliable, time bound and customer friendly. The Rating process begins with the receipt of rating mandate along with the application form and ends with the dispatch of the Rating report and Rating certificate. The Rating process in brief is enumerated below:

SMERA’s Rating Process

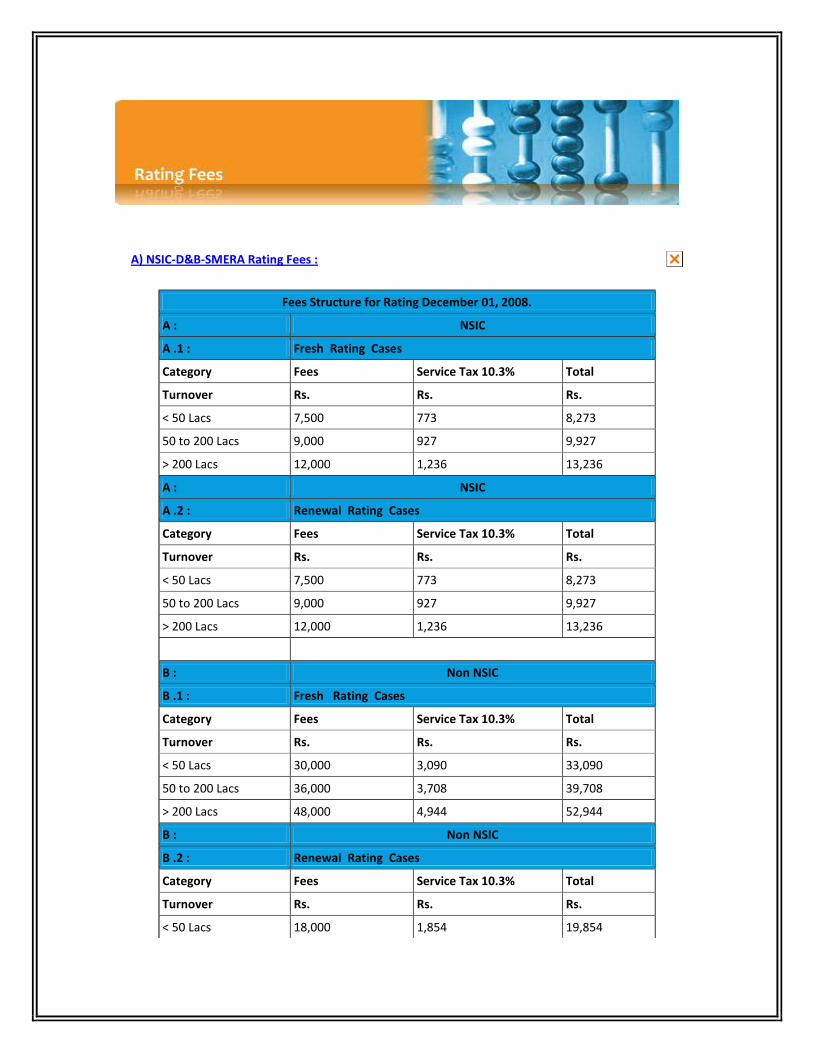

A) NSIC-D&B-SMERA Rating Fees :

Fees Structure for Rating December 01, 2008.

A : NSIC

A .1 : Fresh Rating Cases

Category Fees Service Tax 10.3% Total

Turnover Rs. Rs. Rs.

< 50 Lacs 7,500 773 8,273

50 to 200 Lacs 9,000 927 9,927

> 200 Lacs 12,000 1,236 13,236

A : NSIC

A .2 : Renewal Rating Cases

Category Fees Service Tax 10.3% Total

Turnover Rs. Rs. Rs.

< 50 Lacs 7,500 773 8,273

50 to 200 Lacs 9,000 927 9,927

> 200 Lacs 12,000 1,236 13,236

B : Non NSIC

B .1 : Fresh Rating Cases

Category Fees Service Tax 10.3% Total

Turnover Rs. Rs. Rs.

< 50 Lacs 30,000 3,090 33,090

50 to 200 Lacs 36,000 3,708 39,708

> 200 Lacs 48,000 4,944 52,944

B : Non NSIC

B .2 : Renewal Rating Cases

Category Fees Service Tax 10.3% Total

Turnover Rs. Rs. Rs.

< 50 Lacs 18,000 1,854 19,854

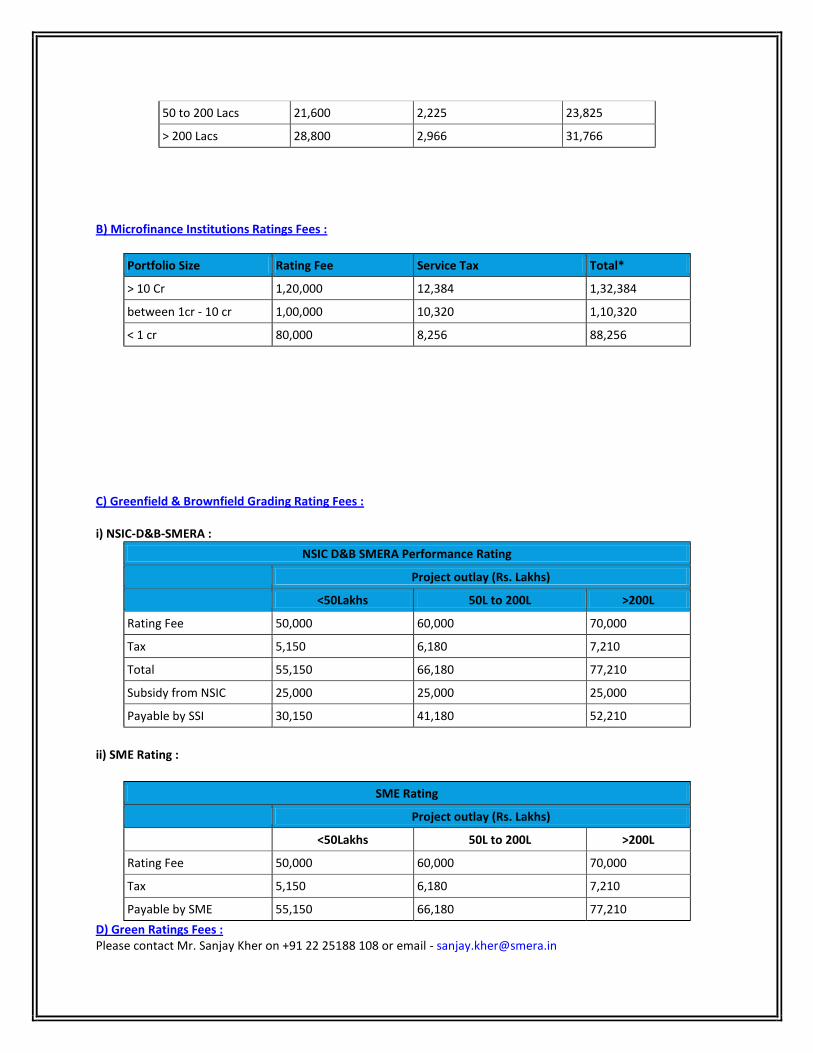

50 to 200 Lacs 21,600 2,225 23,825

> 200 Lacs 28,800 2,966 31,766

B) Microfinance Institutions Ratings Fees :

Portfolio Size Rating Fee Service Tax Total*

> 10 Cr 1,20,000 12,384 1,32,384

between 1cr - 10 cr 1,00,000 10,320 1,10,320

< 1 cr 80,000 8,256 88,256

C) Greenfield & Brownfield Grading Rating Fees : i) NSIC-D&B-SMERA :

NSIC D&B SMERA Performance Rating

Project outlay (Rs. Lakhs)

<50Lakhs 50L to 200L >200L

Rating Fee 50,000 60,000 70,000

Tax 5,150 6,180 7,210

Total 55,150 66,180 77,210

Subsidy from NSIC 25,000 25,000 25,000

Payable by SSI 30,150 41,180 52,210

ii) SME Rating :

SME Rating

Project outlay (Rs. Lakhs)

<50Lakhs 50L to 200L >200L

Rating Fee 50,000 60,000 70,000

Tax 5,150 6,180 7,210

Payable by SME 55,150 66,180 77,210

D) Green Ratings Fees : Please contact Mr. Sanjay Kher on +91 22 25188 108 or email - [email protected]