Embed Size (px)

Citation preview

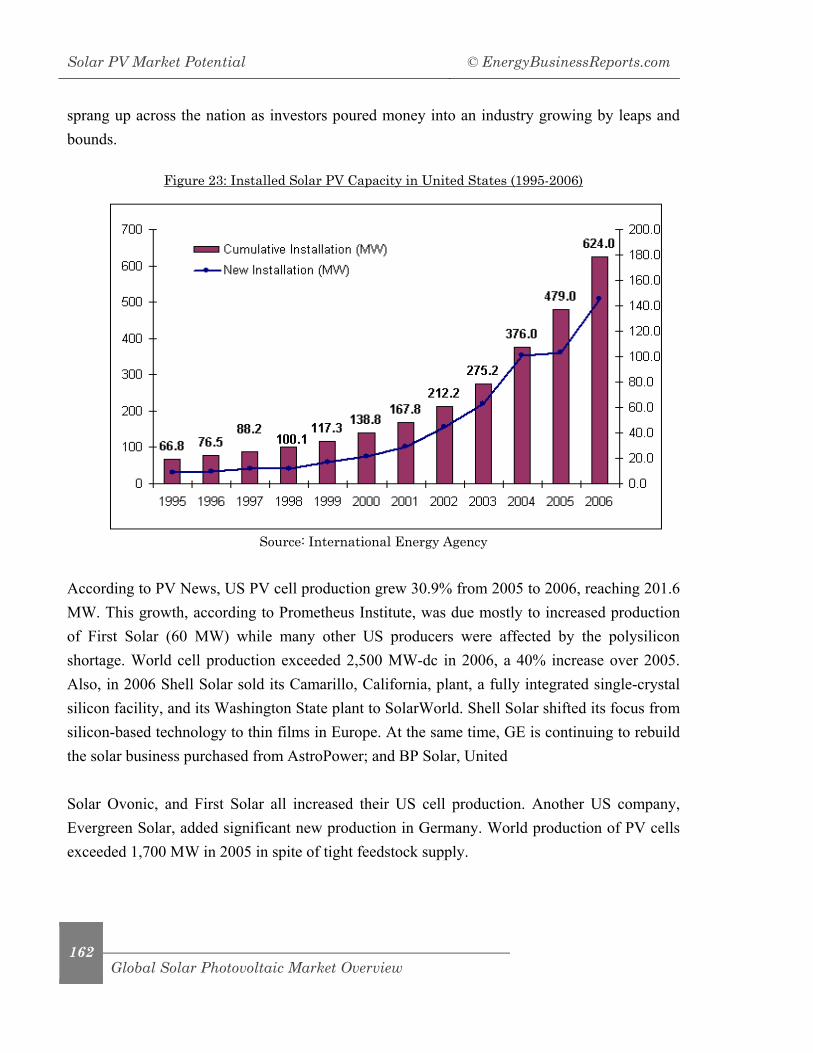

© EnergyBusinessReports.com Solar PV Market Potential

No material contained in this report may be reproduced in whole or in part without the express written permission of Energy Business Reports. This report is intended for the sole and exclusive use of the original purchaser and may not be distributed or transferred in any form to any other person or entity. The information in this report was prepared by Energy Business Reports and Energy Business Reports has used reasonable efforts in collecting, preparing and providing quality information and material, but does not warrant or guarantee the accuracy or completeness, adequacy or currency of the information contained in this report. Users of the information do so at their own risk and should independently corroborate said information prior to any use of it. The information contained in this report is not to be construed as advice. Energy Business Reports does not undertake to advise the recipient or any other reader of this report of changes in its opinions or information. This information is provided “as is” and Energy Business Reports assumes no liability for and User(s) acknowledges that Energy Business Reports shall have no liability for any uses, lawful or otherwise, made by User(s) of the information contained in this report.

Executive Summary ....................... 7 Introduction ..................................... 8 Energy from the Sun ....................... 8 Advantages & Disadvantages of Solar Power ............................................... 10 Availability of Solar Power ............. 11 Applications of Solar Technology ... 12 Solar Thermal Energy .................... 34 Solar Updraft Tower ....................... 34 Storing Solar Energy ...................... 38 Solar Thermal Technologies ........... 39

Introduction to Solar Photovoltaics ............................................................. 40

Overview .......................................... 40 History of Solar Cells ...................... 42 Three Generations of PV Cells ....... 44 Applications ..................................... 47 Sunlight Conditions for Using Solar PV Cells ................................................. 47 Impact of Weather Conditions on PV Cells ................................................. 50 PV Technology in Isolated Generation.......................................................... 50 Impact of Photovoltaic Cells on the Environment ................................... 51

Applications of Solar PV .............. 54 Stand Alone PV Systems ............... 54 Photovoltaic Power Station ............ 55 PV in Buildings .............................. 56 Photovoltaics with Battery Storage ......................................................... 57 The Concept of PV Storage ............ 57 Rural Electrification ...................... 58 Connecting Generators with PV .... 58 Utilities with a Grid-Connected PV System ............................................ 59 Hybrid Power Systems ................... 60 Distributed Generation & PV ........ 60 Small Scale DIY Solar Systems ..... 63

Solar PV System Performance.... 65

Photovoltaic Industry Value Chain Analysis ............................................ 67

Feedstock Component .................... 67 Profiling Solar Cells and Module Manufacturing ................................ 70 Balance of System .......................... 71

Silicon Feedstock Market Analysis ............................................................ 74

Shortage of Silicon ......................... 74

Table of Contents

Solar PV Market Potential © EnergyBusinessReports.com

2

Polysilicon Market Statistics ......... 75 Cost Analysis .................................. 77 Manufacturers of Electronic Grade Silicon .............................................. 79 Manufacturers of PV Grade Silicon ......................................................... 80 Dealing with Silicon Recycling ...... 81 Major Silicon Recyclers .................. 83 Outlook: Silicon Recycling .............. 89

Film Photovoltaics Analysis ........ 90 Major Players .................................. 92

Global Solar Photovoltaic Market Overview .......................................... 111

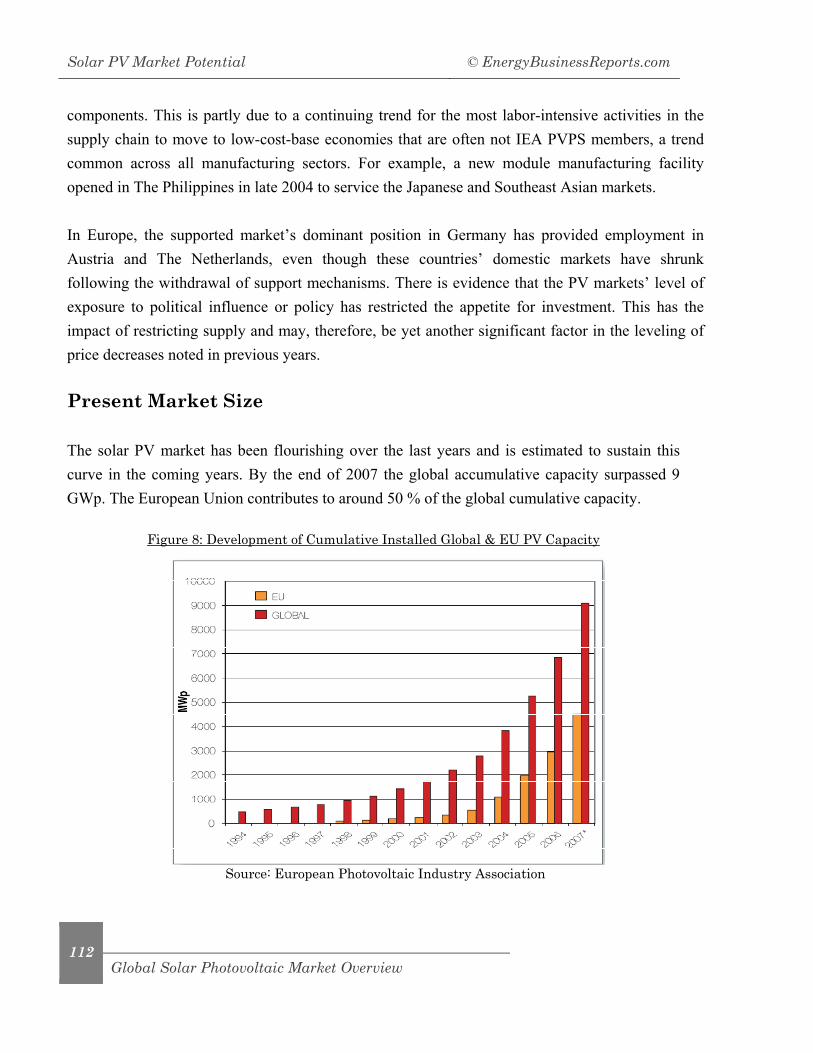

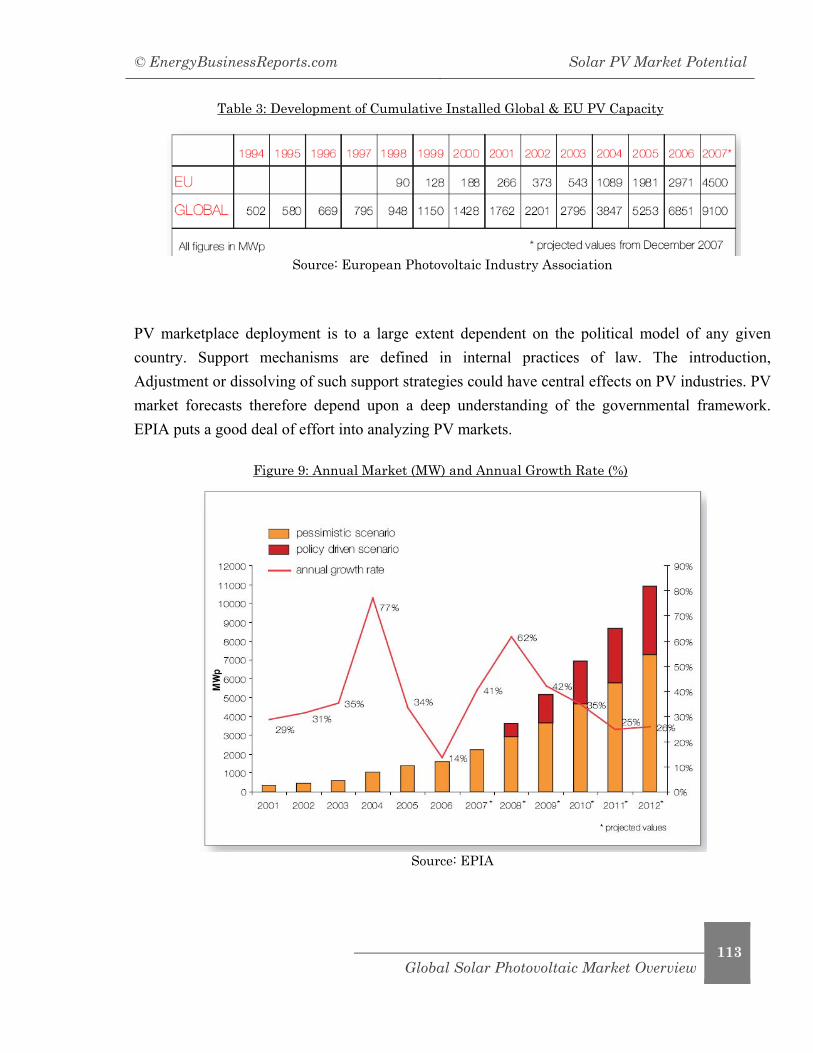

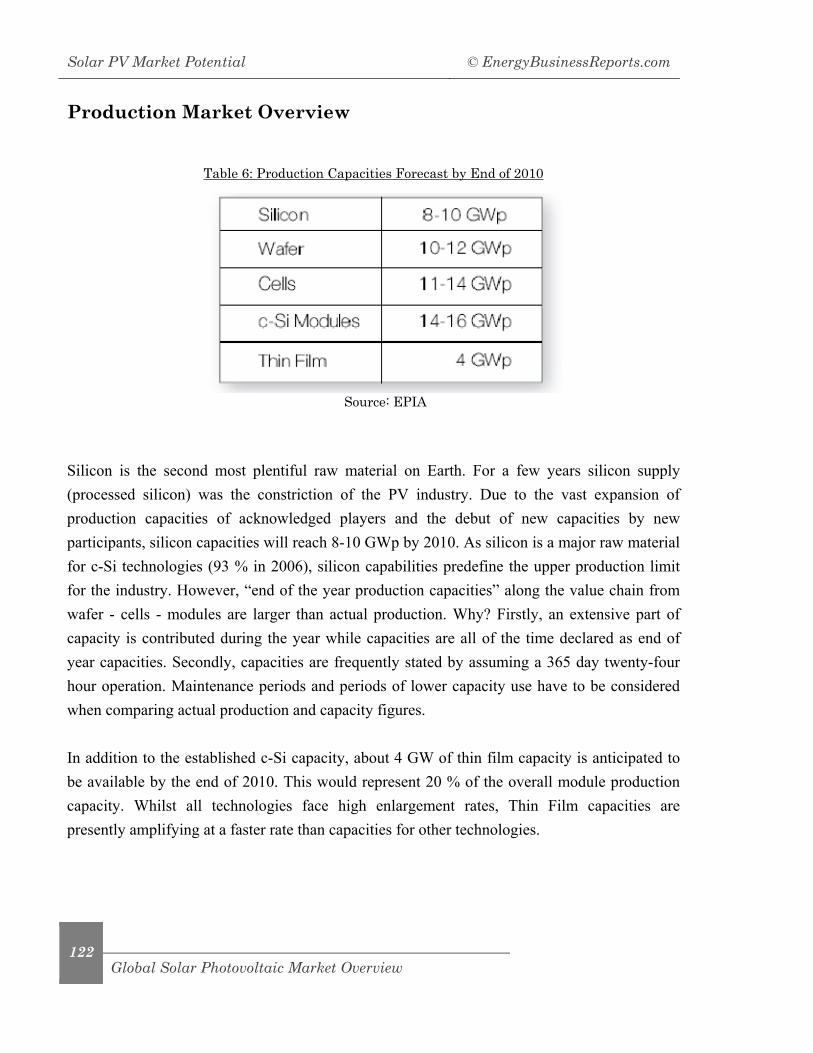

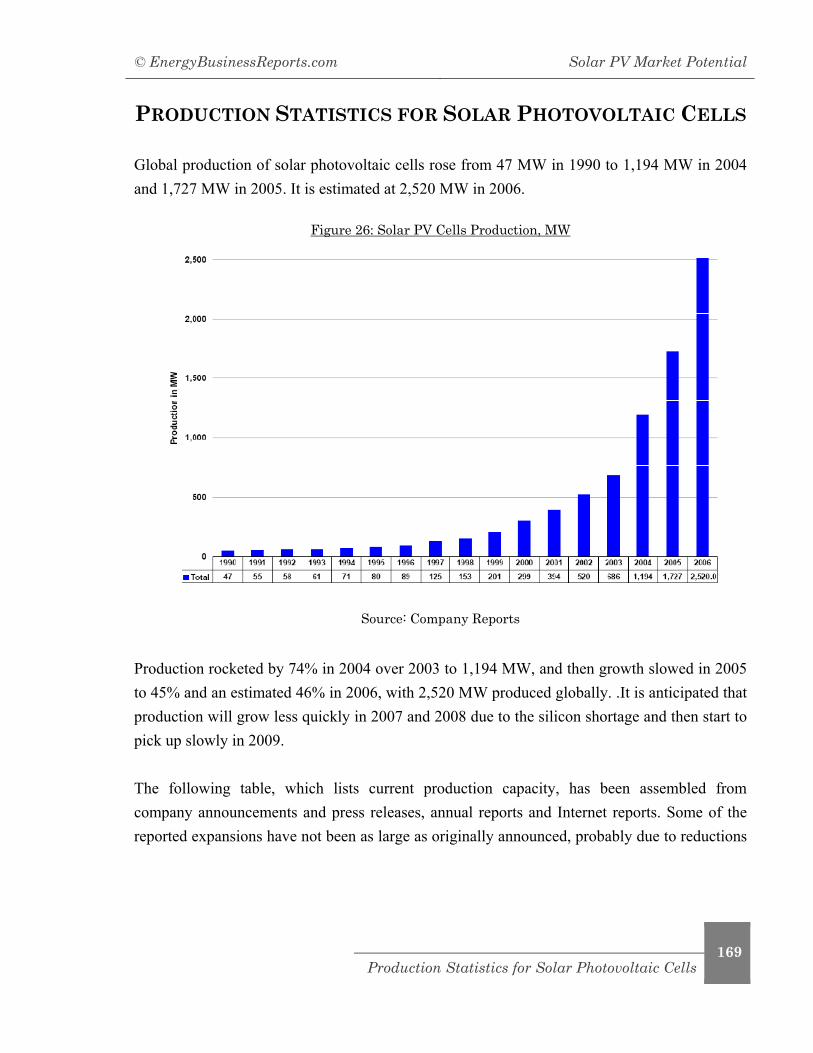

Present Market Size ....................... 112 Solar PV Manufacturers ................ 114 Market Growth ............................... 118 Production Market Overview ......... 122 Country-wise Analysis ................... 123 Outlook – Global Solar PV Capacity ......................................................... 165

Production Statistics for Solar Photovoltaic Cells .......................... 169

Regulatory Framework ................ 172 Renewable Energy Targets ............ 172 US Federal & State Incentives ...... 182 International Policies ..................... 187

Economics of Solar PV .................. 217

Major Players in the Global Solar PV Industry ............................................ 220

Aixin Silicon Sci-Tech Industrial Park ......................................................... 220 Akeena Solar, Inc ........................... 221 Amonix Incorporated ...................... 222

ArcticSolar AB ................................ 224 Asia Silicon Co., Qinghai ................ 225 ASE Americas Inc ........................... 226 AstroPower Inc ............................... 227 Atlantis Energy Inc ........................ 228 Baodiang Tianwei Yingli Green Energy Solar Company ................................ 229 Big Sun Energy ............................... 230 BP Solar International ................... 231 Canadian Solar Inc. ........................ 233 Canon .............................................. 234 Central Electronics Ltd. ................. 235 China Solar Power (Holdings) Ltd. 236 China Sunergy ................................ 237 China Xianjiang SunOasis Ltd. ..... 238 CSG Holding ................................... 239 Deutsche Solar AG .......................... 240 Ebara Solar ..................................... 241 Elkem .............................................. 242 Entech Inc ....................................... 243 EPV Energy Photovoltaics Inc ....... 244 ErSol ................................................ 245 Ertex Solar ...................................... 246 Evergreen Solar .............................. 247 Ever-Q ............................................. 249 First Solar ....................................... 250 Free Energy Europe S.A. ................ 251 GT Solar .......................................... 252 Kyocera ............................................ 255 Mitsubishi Electric Corporation .... 257 Photowatt International ................. 258 PowerLight Corporation ................. 259 Sanyo Electric ................................. 261 Sharp Electronics ............................ 262 Shell Solar ....................................... 263 Siemens Solar ................................. 265

© EnergyBusinessReports.com Solar PV Market Potential

3

Spire Corporation ............................ 266 SunPower Corporation.................... 268 TerraSolar, Inc. ............................... 270 United Solar Ovonic ........................ 272

Appendix ........................................... 273

Glossary ............................................ 281

About the Publisher ....................... 305

Solar PV Market Potential © EnergyBusinessReports.com

4

List of Figures and Tables

Figures

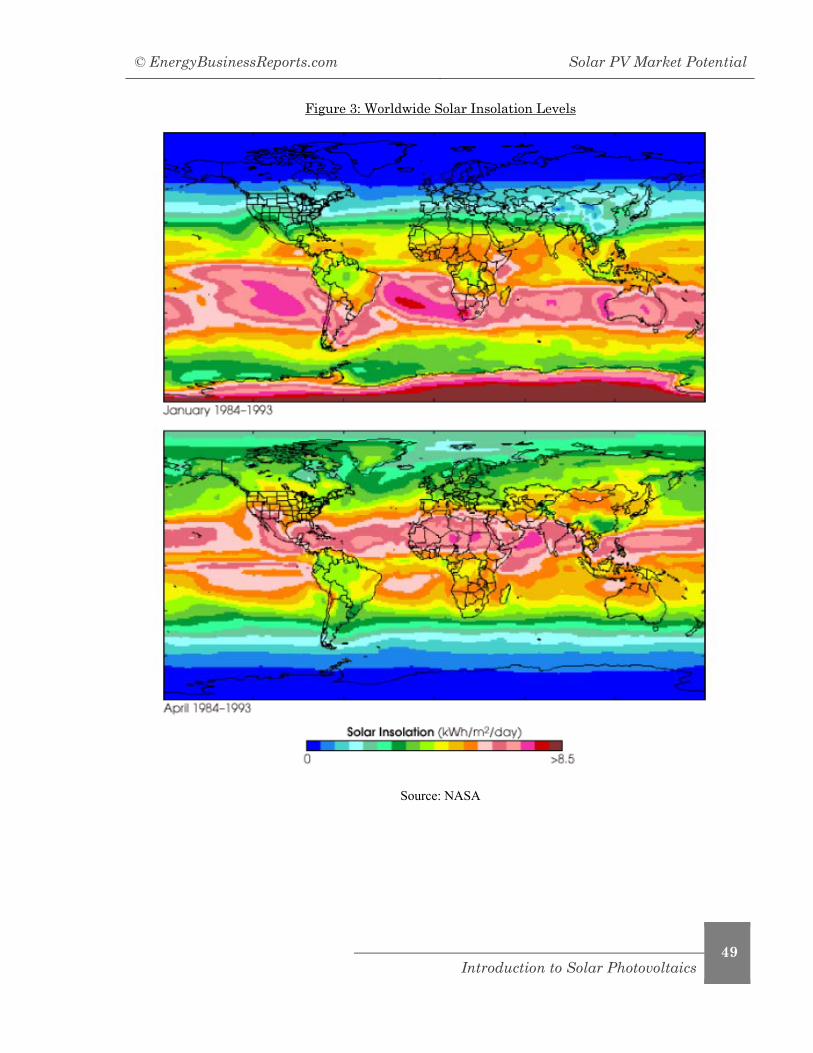

Figure 1: Breakdown of Incoming Solar Energy .......................................... 9 Figure 2: A Solar Cell Made from a Monocrystalline Silicon Wafer .............. 42 Figure 3: Worldwide Solar Insolation Levels ..................................................... 49 Figure 4: Hybrid Power Systems .......... 60 Figure 5: Conventional Distribution Network .................................................. 62 Figure 6: A Distribution Network with Distributed Generation ......................... 63 Figure 7: Production of Electronic Polysilicon in MT ................................... 76 Figure 8: Development of Cumulative Installed Global & EU PV Capacity ..... 112 Figure 9: Annual Market (MW) and Annual Growth Rate (%) ....................... 113 Figure 10: Production of Solar Cells by Country, MW ......................................... 116 Figure 11: Growth of Capacity by Manufacturers, 2005 to 2007 ................ 117 Figure 12: Global PV Capacity Growth & Forecast .............................................. 118 Figure 13: Regional Breakdown of Global PV Markets ................................ 119 Figure 14: Installed Global Solar PV Generating Capacity 1990 to 2006 by Application ............................................. 120 Figure 15: Global Installed Solar PV Capacity ................................................. 121

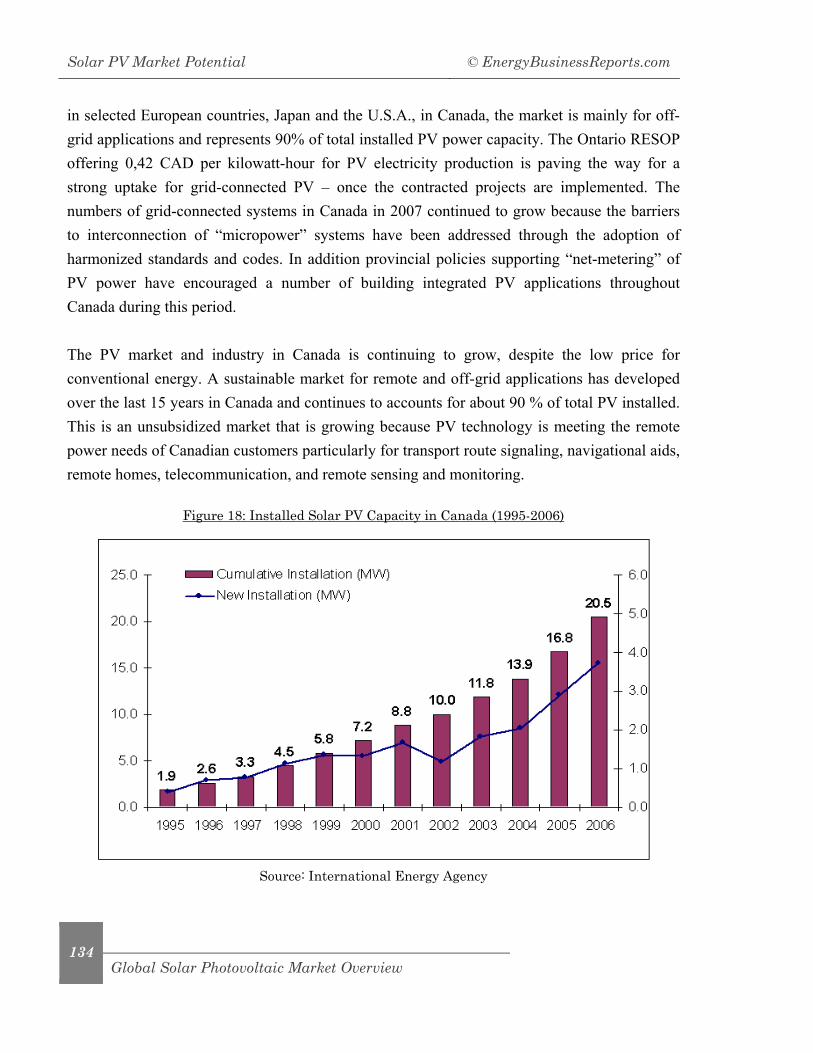

Figure 16: Installed Solar PV Generating Capacity of Austria 1990-2006 by Application ............................... 123 Figure 17: Installed Solar PV Capacity in Australia (1995-2006) ....................... 126 Figure 18: Installed Solar PV Capacity in Canada (1995-2006) .......................... 134 Figure 19: Installed Solar PV Capacity in France (1995-2006) ........................... 141 Figure 20: Installed Solar PV Capacity in Germany (1995-2006) ....................... 145 Figure 21: Development of Grid Connected PV Capacity in Germany .... 149 Figure 22: Installed Solar PV Capacity in Japan (1995-2006) ............................. 153 Figure 23: Installed Solar PV Capacity in United States (1995-2006) ................ 162 Figure 24: Installed Solar PV Capacity, MW, 1990-2010 ..................... 167 Figure 25: Installed Capacity in the Low Forecast by Region, MW, 1990 to 2010 ........................................................ 168 Figure 26: Solar PV Cells Production, MW ......................................................... 169 Figure 27: Prices Compared with Shipments 1975-2006 $/Watt ............... 218 Figure 28: Parabolic Trough ................. 273 Figure 29: Central Receiver or Solar Tower ..................................................... 273 Figure 30: Parabolic Dish ..................... 274 Figure 31: Photovoltaic Roof System .... 274 Figure 32: Cost of PV to Consumers & Manufacturing Shipments .................... 275

© EnergyBusinessReports.com Solar PV Market Potential

5

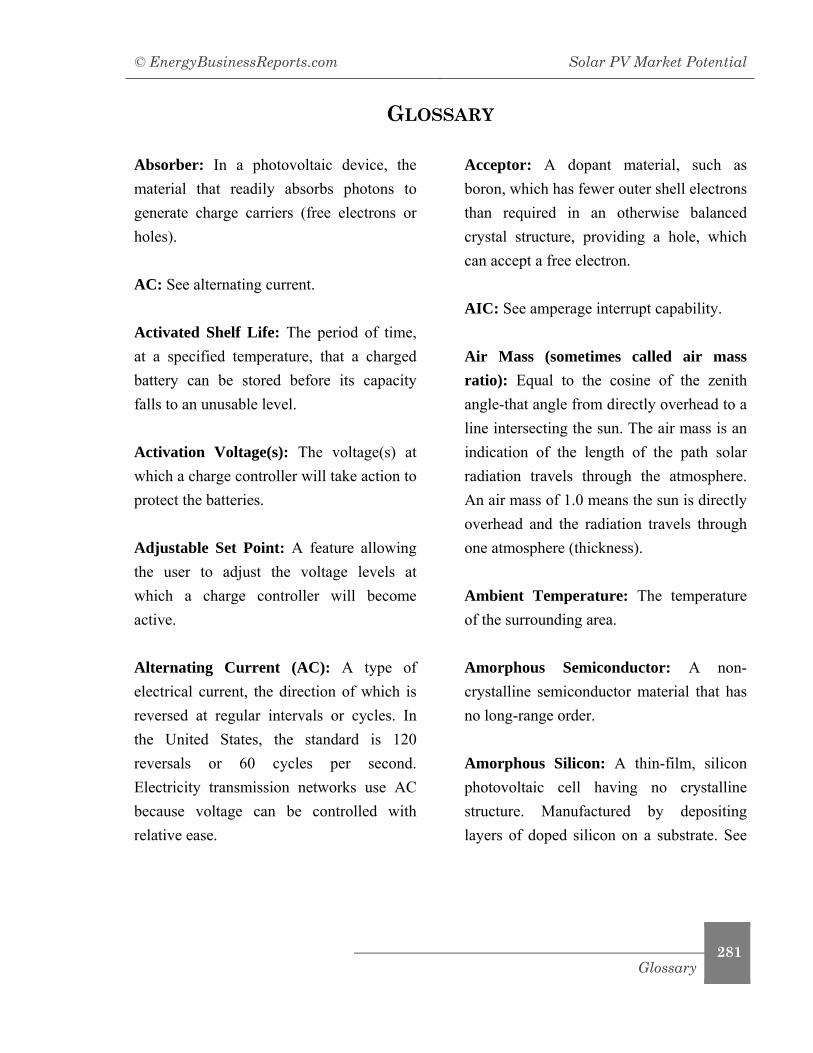

Figure 33: A Schematic Arrangement of a PV Cell ............................................ 275 Figure 34: Solar Parabolic Trough System Combined with Fossil Fuel Firing to Generate Electrical Power .... 276 Figure 35: Arrangement of a Central Receiver Solar Thermal System ........... 277 Figure 36: A Solar Pond Arrangement 277 Figure 37: Integrated Solar/Combined Cycle System (ISCC) ............................. 280

Tables

Table 1: Companies Producing Electronic Polysilicon in MT ................. 77 Table 2: Grades of Recycled Silicon ...... 82 Table 3: Development of Cumulative Installed Global & EU PV Capacity…113 Table 4: Annual Market (MW) and Annual Growth Rate (%)……………...114 Table 5: Comprehensive Industry Forecast for Major Worldwide Yearly

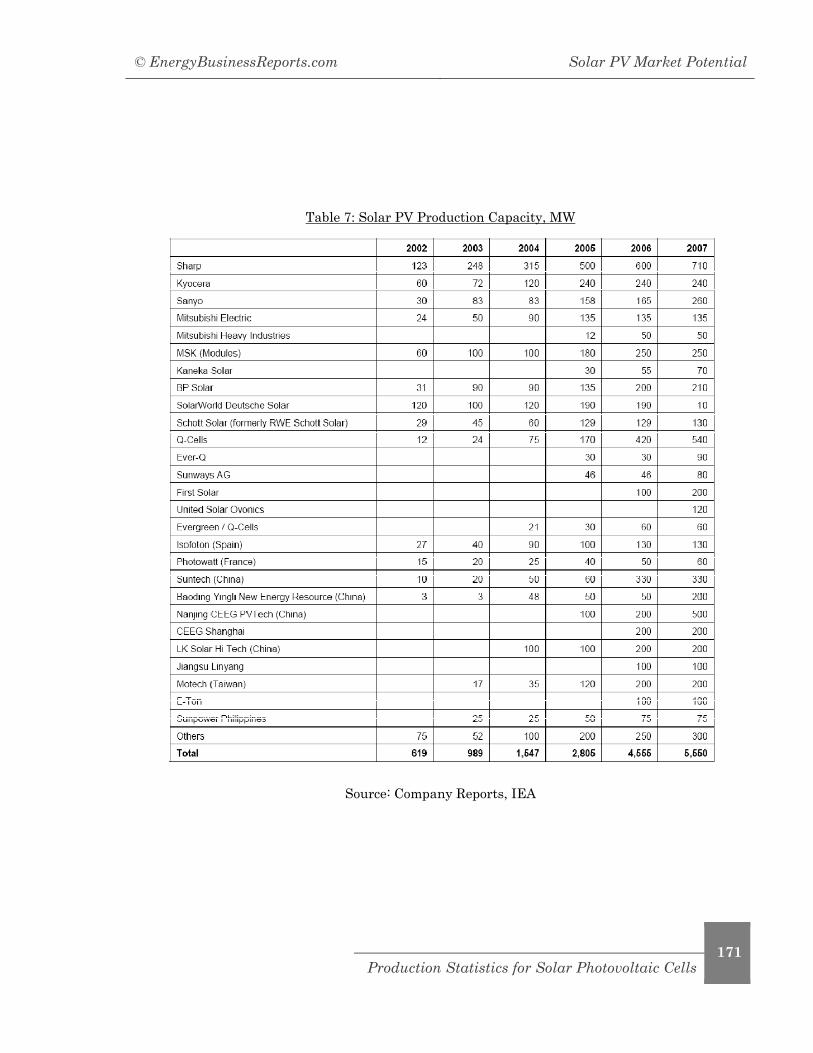

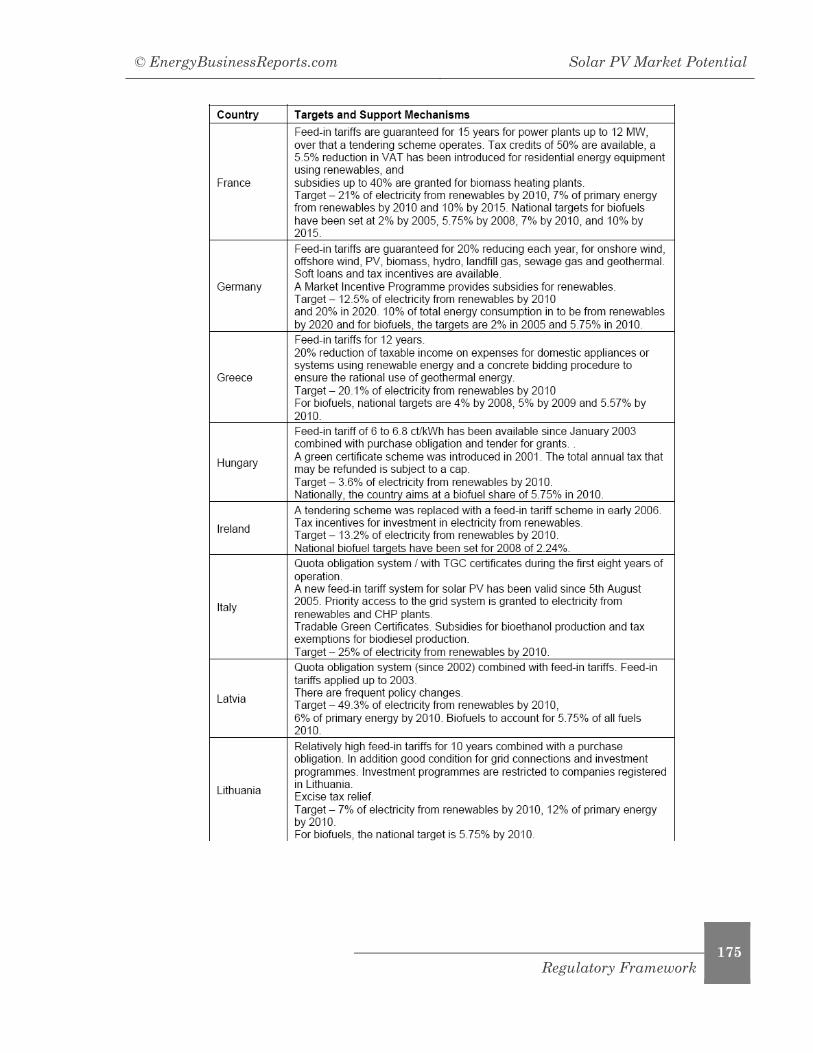

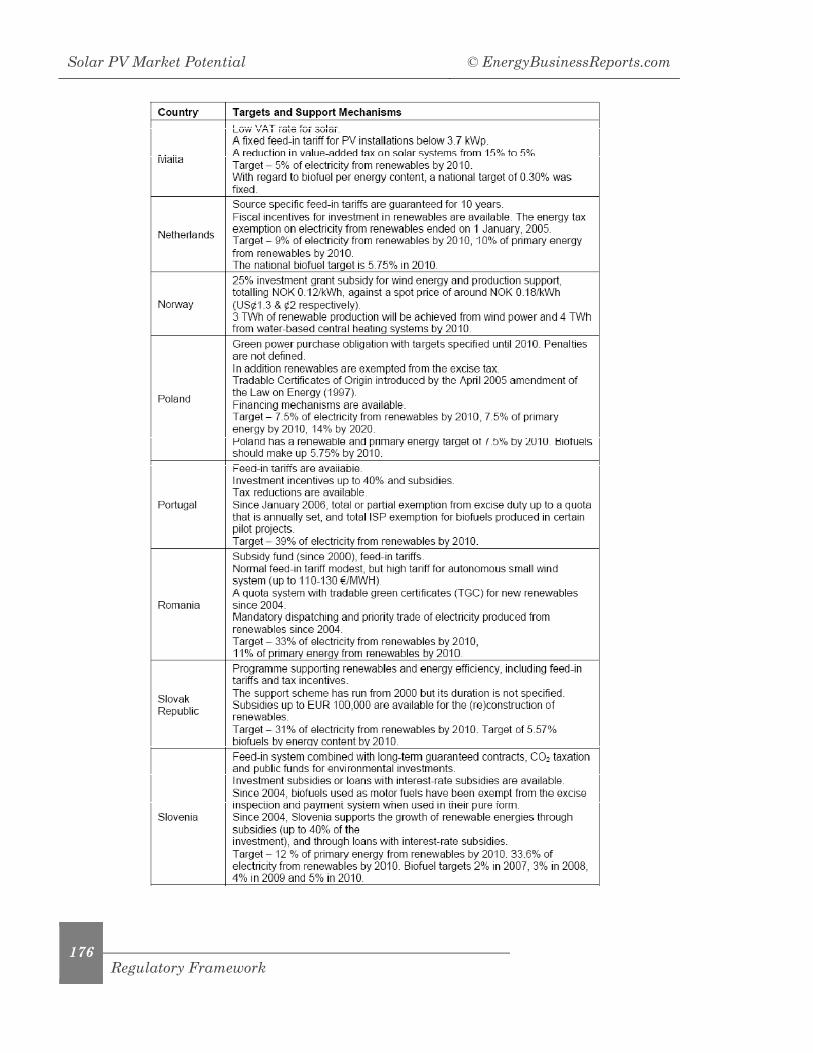

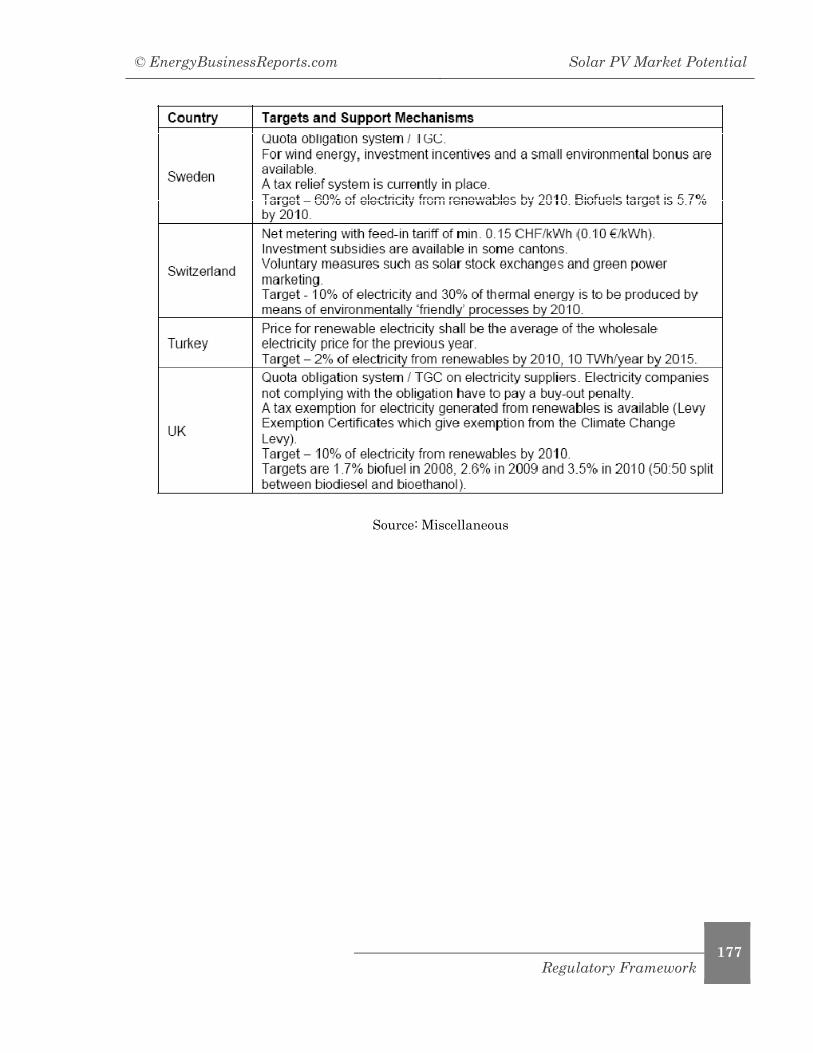

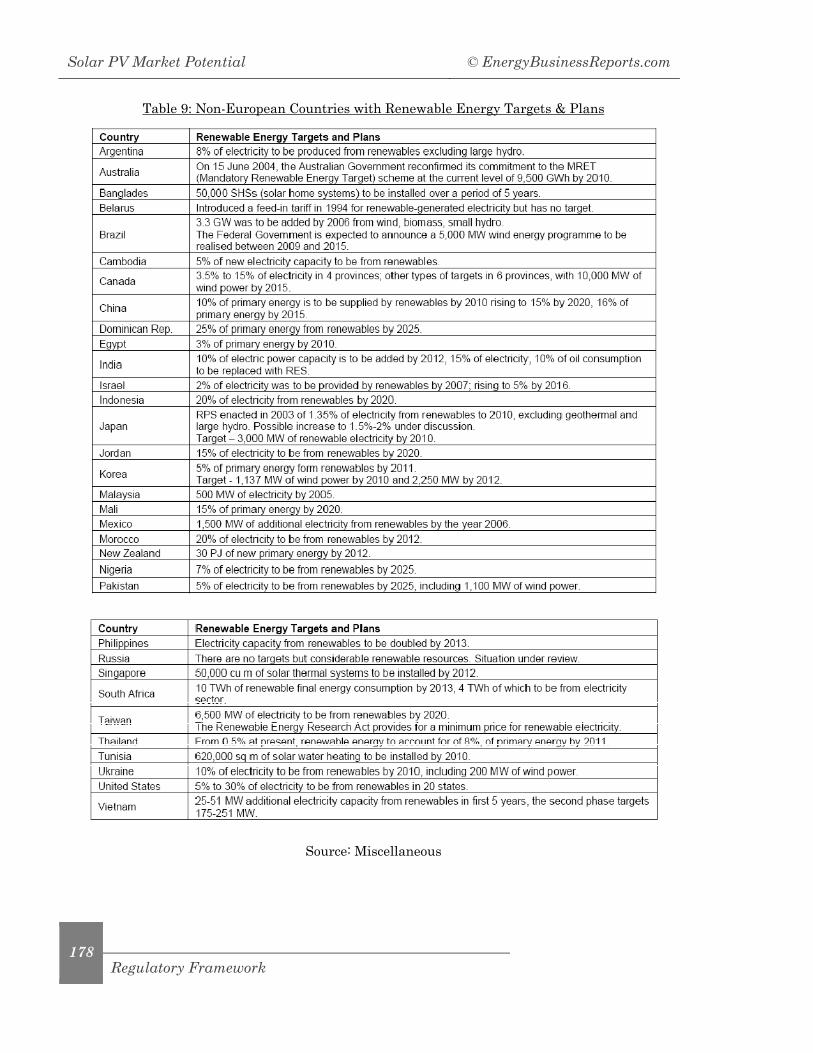

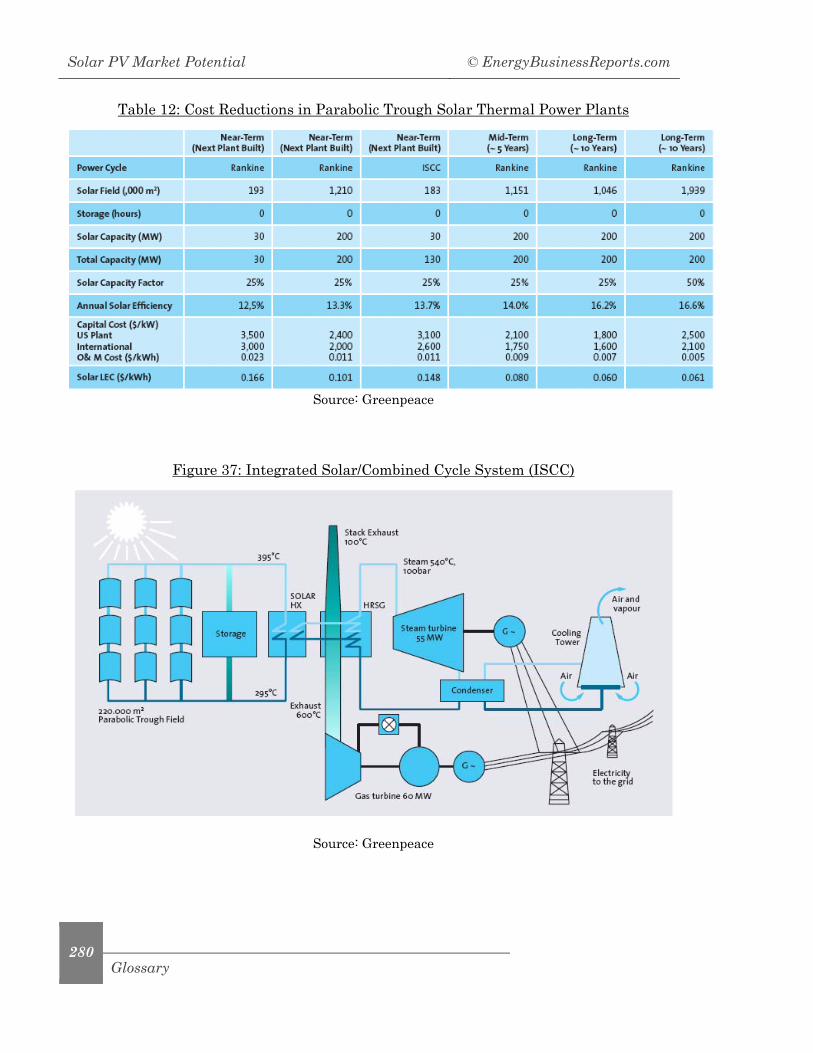

PV Markets in MW…………………………119 Table 6: Production Capacities Forecast by End of 2010…………………………..122 Table 7: Solar PV Production Capacity, MW………………………………………..171 Table 8: Renewables Targets and Support Mechanisms of European Countries………………………………...173 Table 9: Non-European Countries with Renewable Energy Targets & Plans....178 Table 10: Early Solar Thermal Power Plants……………………………………..278 Table 11: Comparison of Solar Thermal Power Technologies…………………....279 Table 12: Cost Reductions in Parabolic Trough Solar Thermal Power Plants..280

Solar PV Market Potential © EnergyBusinessReports.com

6

© EnergyBusinessReports.com Solar PV Market Potential

7

Executive Summary

EXECUTIVE SUMMARY

This report provides a comprehensive understanding of solar photovoltaic technologies, applications, regulatory framework, and economics. It examines the potential of the photovoltaic market and includes an analysis of the major players as well as regional and country analyses of the global PV market.

There is no shortage of solar-derived energy on Earth. Indeed the storages and flows of energy on the planet are very large relative to human needs. Since ancient times, solar energy has been harnessed for human use through a range of technologies. Solar radiation along with secondary solar resources such as wind and wave power, hydroelectricity and biomass, accounts for most of the available flow of renewable energy on Earth.

Photovoltaics (PV) is the field of technology and research related to the application of solar cells for energy by converting sunlight directly into electricity. Due to the growing demand for clean sources of energy, the manufacture of solar cells and photovoltaic arrays has expanded dramatically in recent years.

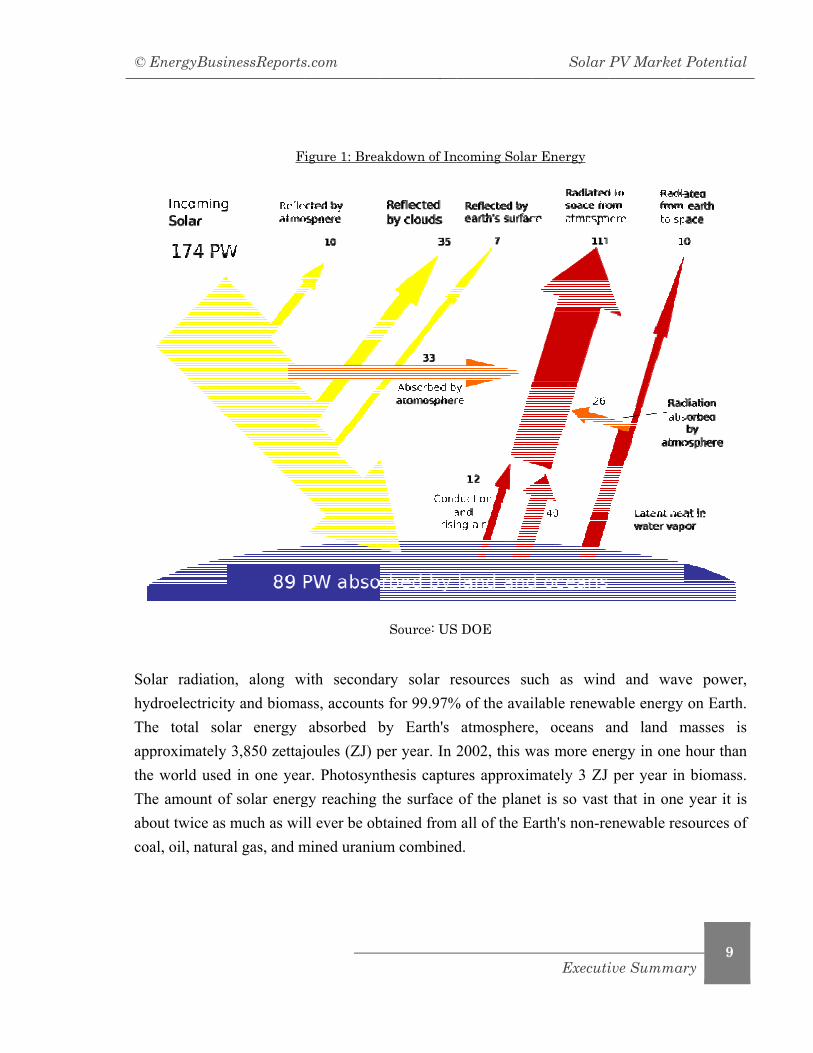

The Earth receives 174 petawatts (PW) of incoming solar radiation (insolation) at the upper atmosphere. Approximately 30% is reflected back to space while the rest is absorbed by clouds, oceans and land masses. The spectrum of solar light at the Earth's surface is mostly spread across the visible and near-infrared ranges with a small part in the near-ultraviolet.

Solar energy is the light and radiant heat from the Sun that influences Earth's climate and weather and sustains life. Solar power is sometimes used as a synonym for solar energy or to refer to electricity generated from solar radiation.

Solar PV Market Potential © EnergyBusinessReports.com

8

Executive Summary

What is Solar Energy?

Introduction

Solar energy is the light and radiant heat from the Sun that influences Earth's climate and weather and sustains life. Solar power is sometimes used as a synonym for solar energy or more specifically to refer to electricity generated from solar radiation. Since ancient times, solar energy has been harnessed for human use through a range of technologies. Solar radiation, along with secondary solar resources such as wind and wave power, hydroelectricity and biomass, accounts for most of the available flow of renewable energy on Earth.

Solar energy technologies can provide electrical generation by heat engine or photovoltaic means, space heating and cooling in active and passive solar buildings; potable water via distillation and disinfection, daylighting, hot water, thermal energy for cooking, and high temperature process heat for industrial purposes.

Energy from the Sun

The Earth receives 174 petawatts (PW) of incoming solar radiation (insolation) at the upper atmosphere. Approximately 30% is reflected back to space while the rest is absorbed by clouds, oceans and land masses. The spectrum of solar light at the Earth's surface is mostly spread across the visible and near-infrared ranges with a small part in the near-ultraviolet.

The absorbed solar light heats the land surface, oceans and atmosphere. The warm air containing evaporated water from the oceans rises, driving atmospheric circulation or convection. When this air reaches a high altitude, where the temperature is low, water vapor condenses into clouds, which rain onto the earth's surface, completing the water cycle. The latent heat of water condensation amplifies convection, producing atmospheric phenomena such as cyclones and anti-cyclones. Wind is a manifestation of the atmospheric circulation driven by solar energy. Sunlight absorbed by the oceans and land masses keeps the surface at an average temperature of 14 °C. The conversion of solar energy into chemical energy via photosynthesis produces food, wood and the biomass from which fossil fuels are derived.

© E

SolhydThapptheThabocoa

EnergyBusi

lar radiationdroelectricitye total solproximately e world usede amount ofout twice as al, oil, natura

nessReports

F

n, along wy and biomalar energy 3,850 zettaj

d in one yeaf solar energmuch as wilal gas, and m

s.com

igure 1: Brea

with secondaass, accounts

absorbed bjoules (ZJ) par. Photosyntgy reaching ll ever be ob

mined uraniu

akdown of In

Source: US

ary solar res for 99.97%by Earth's per year. In thesis captuthe surface

btained fromum combined

ncoming Solar

S DOE

esources su% of the avai

atmosphere2002, this w

ures approximof the plane

m all of the Ed.

Solar

Executi

r Energy

uch as windilable renewe, oceans awas more enemately 3 ZJ et is so vast arth's non-re

PV Market

ive Summar

d and wavwable energy

and land mergy in one per year inthat in one

enewable res

Potential

9

ry

ve power, on Earth.

masses is hour than

n biomass. year it is

sources of

Solar PV Market Potential © EnergyBusinessReports.com

10

Executive Summary

From the table of resources it would appear that solar, wind or biomass would be sufficient to supply all of our energy needs, however, the increased use of biomass has had a negative effect on global warming and dramatically increased food prices by diverting forests and crops into biofuel production. As intermittent resources, solar and wind raise other issues.

Advantages & Disadvantages of Solar Power

Advantages

• The 122 petawatts of sunlight reaching the earth's surface is plentiful compared to the 13 terawatts of average power consumed by humans. Additionally, solar electric generation has the highest power density (global mean of 170 W/m2) among renewable energies.

• Solar power is pollution-free during use. Production end wastes and emissions are manageable using existing pollution controls. End-of-use recycling technologies are under development.

• Facilities can operate with little maintenance or intervention after initial setup.

• Solar electric generation is economically competitive where grid connection or fuel transport is difficult, costly or impossible. Examples include satellites, island communities, remote locations and ocean vessels.

• When grid-connected, solar electric generation can displace the highest cost electricity during times of peak demand (in most climatic regions), can reduce grid loading, and can eliminate the need for local battery power for use in times of darkness and high local demand; such application is encouraged by net metering. Time-of-use net metering can be highly favorable to small photovoltaic systems.

• Grid-connected solar electricity can be used locally thus minimizing transmission/distribution losses (approximately 7.2%).

© EnergyBusinessReports.com Solar PV Market Potential

11

Executive Summary

• Once the initial capital cost of building a solar power plant has been spent, operating costs are low when compared to existing power technologies.

Disadvantages

• Solar cells are costly, requiring a large initial capital investment.

• Limited power density: Average daily insolation in the contiguous U.S. is 3-9 kWh/m2 usable by 7-17.7% efficient solar panels.

• To get enough energy for larger applications, a large number of photovoltaic cells is needed. This increases the cost of the technology and requires a large plot of land.

• Like electricity from nuclear or fossil fuel plants, it can only realistically be used to power transport vehicles by converting light energy into another form of stored energy (e.g. battery stored electricity or by electrolyzing water to produce hydrogen) suitable for transport.

• Solar cells produce DC which must be converted to AC when used in currently existing distribution grids. This incurs an energy loss of 4-12%.

Availability of Solar Power

There is no shortage of solar-derived energy on Earth. Indeed the storages and flows of energy on the planet are very large relative to human needs. Consider the following:

• The amount of solar energy intercepted by the Earth every minute is greater than the amount of energy the world uses in fossil fuels each year.

• Tropical oceans absorb 560 trillion gigajoules (GJ) of solar energy each year, equivalent to 1,600 times the world’s annual energy use.

Solar PV Market Potential © EnergyBusinessReports.com

12

Executive Summary

• The energy in the winds that blow across the United States each year could produce more than 16 billion GJ of electricity - more than one and one-half times the electricity consumed in the United States in 2000.

• Annual photosynthesis by the vegetation in the United States is 50 billion GJ, equivalent to nearly 60% of the nation’s annual fossil fuel use.

Plants, on average, capture 0.1% of the solar energy reaching the Earth. The land area of the lower 48 United States intercepts 50 trillion GJ per year, equivalent to 500 times of the nation’s annual energy use. This energy is spread over 8 million square kilometers of land area, so that the energy absorbed per unit area is 6.1 million GJ per square kilometer per year. This results in potential biomass production of 6,100 GJ per square kilometer per year. Compared to the 0.1% efficiency of vegetation, roof installable amorphous silicon solar panels capture 8%-14% of the solar energy, while more expensive crystalline panels capture 14%-20%, and large scale desert mirror-concentrator heat engine based setups may capture up to 30-50%.

Applications of Solar Technology

Daylighting

Solar lighting or daylighting is the use of natural light to provide illumination. Daylighting offsets energy use in electric lighting systems and reduces the cooling load on HVAC systems (this assumes that daylighting is replacing incandescent lighting, which produces more heat than light). The use of natural light also offers physiological and psychological benefits, although this is difficult to quantify.

Daylighting features include building orientation, window orientation, exterior shading, sawtooth roofs, clerestory windows, light shelves, skylights and light tubes. These features may be incorporated in existing structures but are most effective when integrated in a solar design package which accounts for factors such as glare, heat gain, heat loss and time-of-use. Architectural trends increasingly recognize daylighting as a cornerstone of sustainable design.

© EnergyBusinessReports.com Solar PV Market Potential

13

Executive Summary

Daylight saving time (DST) can be seen as a method of utilizing solar energy by matching available sunlight to the hours of the day in which it is most useful. DST energy savings have been estimated to reduce total electricity use in California by 0.5% (3400 MWh) and peak electricity use by three percent (1000 MW).

Heliostat Power Plans

The solar power tower (also known as 'Central Tower' power plants or 'Heliostat' power plants or power towers) is a type of solar furnace using a tower to receive the focused sunlight. It uses an array of flat, moveable mirrors (called heliostats) to focus the sun's rays upon a collector tower (the target). The high energy at this point of concentrated sunlight is transferred to a substance that can store the heat for later use. The most recent heat transfer material that has been successfully demonstrated is liquid sodium. Sodium is a metal with a high heat capacity, allowing that energy to be stored and drawn off throughout the evening. That energy can, in turn, be used to boil water for use in steam turbines. Water had originally been used as a heat transfer medium in earlier power tower versions (where the resultant steam was used to power a turbine). This system did not allow for power generation during the evening. Examples of heliostat based power plants are the 10 MWe Solar One, Solar Two, and the 15 MW Solar Tres plants. Neither of these are currently used for active energy generation. In South Africa, a solar power plant is planned with 4000 to 5000 heliostat mirrors, each having an area of 140 m².

Passive Solar Building Design

Passive solar building design involves the modeling, selection and use of appropriate passive solar technologies to maintain the building environment at a comfortable temperature through the sun's daily and annual cycles. As a result it also minimizes the use of active solar, renewable energy and especially fossil fuel technologies.

Passive solar building design is only one part of thermally efficient building design, which in turn is only one part of sustainable design, although the terms are often used erroneously as synonyms (passive solar design does not relate to factors such as ventilation, evaporative cooling, or life cycle analysis unless these operate solely by the sun).

Solar PV Market Potential © EnergyBusinessReports.com

14

Executive Summary

The available technologies can be categorized into various categories from which design choices can be made. These include three basic ways for harnessing the sun's energy, and several other techniques:

Direct solar gain: Direct gain involves using the positioning of windows, skylights and shutters to control the amount of direct solar radiation reaching the interior spaces themselves, and to warm the air and surfaces within the building. The use of sun-facing windows and a high-mass floor is a short-cycle example of this. Direct solar gain systems suffer because historically there were no reasonably priced transparent thermally insulating materials with R-values comparable to standard wall insulation. This is now changing in Europe, where super insulated windows have been developed and are widely used to help meet the German Passive House standard.

Indirect solar gain: Indirect gain, in which solar radiation is captured by a part of the building envelope designed with an appropriate thermal mass (such as a water tank or a solid concrete or masonry wall behind glass). The heat is then transmitted indirectly to the building through conduction and convection. Examples of this are Trombe walls, water walls and roof ponds. The Australian deep-cover earthed-roof, innovated by the Baggs family of architects, is an annualized example of this path. In practice indirect solar gain systems have suffered from being difficult to control, and from the lack of reasonably priced transparent thermally insulating materials.

Isolated solar gain: Isolated gain, involves passively capturing solar heat and then moving it passively into or out of the building using a liquid (for example using a thermosiphon solar space heating system) or air (perhaps using a solar chimney), either directly or using a thermal store. Sun-spaces, greenhouses, and "solar closets" are alternative ways of capturing isolated heat gain from which warmed air can be taken. In practice it has been found that some owners use these structures as living spaces, heating them with conventional fuels and therefore significantly increasing, rather than reducing, the environmental impact of the building.

© EnergyBusinessReports.com Solar PV Market Potential

15

Executive Summary

Other passive solar design techniques:

• Building position - Based on the local climate and the sun's positioning (determined using a heliodon), the entire building can be positioned and angled to be oriented towards or away from the sun (according whether heating or cooling is the primary concern), overshadowing from other structures or natural features can be avoided or used, and the building can be set into the ground using earth sheltering techniques.

• Building properties - The shape (and consequently the surface area) of the building can be controlled to reduce the heating or cooling requirement, and the use of materials properties to reflect, absorb, or transmit energy (for example using visible color) is also a consideration.

• External environment - Energy-efficient landscaping materials, including the use of trees and plants can be selected to reflect or absorb heat, create summer shading (particularly in the case of deciduous plants), and create shelter from the wind.

Although not classified as a passive solar technology, the use of thermal insulation or super insulation is invariably employed to reduce heat loss or unwanted heat gain.

Levels of Usage

1. Pragmatic: A house can easily achieve 30% or better cost reductions in heating expense without obvious changes to its appearance, comfort or usability. This is done using good siting and window positioning, small amounts of thermal mass, with good but conventional insulation and occasional supplementary heat from a central radiator connected to a water heater. Sunrays may fall onto a wall during the daytime, which will radiate heat in the evening.

2. Annualized: Historically, most "passive solar" approaches have depended on near-daily solar capture and storage, only expected to maintain temperatures through a few days and nights. These are now termed "short-cycle passive solar". More recent research has developed techniques to capture warm-season solar heat, convey it to a seasonal thermal store for use months later during the cool or cold season. This is referred to as "annualized passive solar."

Solar PV Market Potential © EnergyBusinessReports.com

16

Executive Summary

This requires large amounts of thermal mass. One technique buries water-proof insulation in seven-meter skirts around the foundation, and buries loops of plastic pipe or ducts under the foundations and slab. The "skirts" of insulation prevent heat leaks from weather or water.

3. Minimum machinery: A "purely passive" solar-heated house would have no mechanical furnace unit, relying instead on energy captured from sunshine, only supplemented by "incidental" heat energy given off by lights, candles, other task-specific appliances (such as those for cooking, entertainment, etc.), showering, people and pets. The use of natural air currents (rather than mechanical devices such as fans) to circulate air is related, though not strictly solar design.

4. Systems sometimes use limited electrical and mechanical controls to operate dampers, insulating shutters, shades or reflectors. Some systems enlist small fans or solar-heated chimneys to start or improve convective air-flow. A reasonable way to analyze these systems is by measuring their coefficient of performance. A heat pump might use 1 J for every 4 J it delivers giving a COP of 4, a system that only uses a 30W ceiling fan to heat an entire house with 10 kW of solar heat would have a COP of 300.

Solar Cookers

A solar box cooker traps the sun's energy in an insulated box; such boxes have been successfully used for cooking, pasteurization and fruit canning. Solar cooking is helping many developing countries, both reducing the demands for local firewood and maintaining a cleaner breathing environment for the cooks.

The first known western solar oven is attributed to Horace de Saussure in 1767, which impressed Sir John Herschel enough to build one for cooking meals on his astronomical expedition to the Cape of Good Hope in Africa in 1830. Today, there are many different designs in use around the world.

Solar ovens are just one part of the alternative energy picture, but one that is accessible to a great majority of people. A reliable solar oven can be built from everyday materials in just a few hours or purchased readymade.

© EnergyBusinessReports.com Solar PV Market Potential

17

Executive Summary

Solar ovens can be used to prepare anything that can be made in a conventional oven or stove - from baked bread to steamed vegetables to roasted meat. Solar ovens allow you to do it all, without contributing to global warming or heating up the kitchen and placing additional demands on cooling systems. Nearly 75% of U.S. households prepare at least one hot meal per day; one-third prepare two or more. Some of those meals could be made in an environmentally responsible way, using a solar oven.

The World Health Organization reports that cooking with fuel wood is the equivalent of smoking two packs of cigarettes a day. Inhalation of smoke from cooking fires causes respiratory diseases and death. One of the solutions advocated to address this problem is solar cooking which makes no smoke at all. It just uses free and abundant solar energy.

Solar Electric Vehicles

A solar car is an electric vehicle powered by solar energy obtained from solar panels on the surface of the car. Photovoltaic (PV) cells convert the sun's energy directly into electrical energy. However, solar cars are not currently a practical form of transportation. Although they can operate for limited distances without the sun, the solar cells are generally very fragile. Also, development teams have focused their efforts toward optimizing the efficiency of the vehicle, with little concern for passenger comfort. Most solar cars have only enough room for one or two people.

Solar cars compete in races (often called rayces) such as the World Solar Challenge and the American Solar Challenge. These events are often sponsored by government agencies, such as the United States Department of Energy, who are keen to promote the development of alternative energy technology (such as solar cells). Such challenges are often entered by universities to develop their students' engineering and technological skills, but many professional teams have entered competitions as well, including teams from GM and Honda.

Design of Solar Cars

Solar cars combine technology typically used in the aerospace, bicycle, alternative energy and automotive industries. Unlike typical race cars, solar cars are designed with severe energy

Solar PV Market Potential © EnergyBusinessReports.com

18

Executive Summary

constraints imposed by the race regulations. These rules limit the energy to only that collected from solar radiation and as a result optimizing the design to account for aerodynamic drag, vehicle weight, rolling resistance and electrical efficiency are paramount. Conventional thinking has to be challenged, for example, rather than a conventional automobile seat which would weigh tens of pounds, one solar car designed by the University of Michigan employed a nylon mesh seat combined with a five-point harness that weighed less than three pounds.

The design of a solar car is governed by the power equation:

Briefly, the left hand side represents the energy input into the car (batteries and power from the sun) and the right hand side is the energy needed to drive the car along the race route (overcoming rolling resistance, aerodynamic drag, going uphill and accelerating). Everything in this equation can be estimated except v. The parameters include:

η = Motor, controller and drive train efficiency (decimal)

ηb = Watt-hour battery efficiency (decimal)

E = Energy available in the batteries (joules)

P = Estimated average power from the array (watts)

x = Daily race route distance (meters)

W = Weight of the vehicle (newtons)

= First coefficient of rolling resistance (non-dimensional)

= Second coefficient of rolling resistance (newton-seconds per meter)

© EnergyBusinessReports.com Solar PV Market Potential

19

Executive Summary

N = Number of wheels on the vehicle (integer)

ρ = Air density (kilograms per cubic meter)

Cd = Coefficient of drag (non-dimensional)

A = Frontal area (meters squared)

h = Total height that the vehicle will climb (meters)

Na = Number of times the vehicle will accelerate in a race day (integer)

g = Gravity constant (meters per second squared)

v = Average velocity over the route

Solving the equation for velocity results in a large equation (approximately 100 terms). Using the power equation as the arbiter, vehicle designers can compare various car designs and evaluate the comparative performance over a given route. Combined with CAD and systems modeling, the power equation is a useful tool in solar car design.

The driver's cockpit usually only contains a single seat, although a few cars do contain room for a second passenger. They contain some of the features available to drivers of traditional vehicles such as brakes, accelerator, turn signals, rear view mirrors (or camera), ventilation, and sometimes cruise control. A radio for communication with their support crews is almost always included.

Solar cars are fitted with some gauges seen in conventional cars. Aside from keeping the car on the road, the driver's main priority is to keep an eye on these gauges to spot possible problems. Drivers also have a safety harness, and optionally (depending on the race) a helmet similar to racing car drivers.

Solar PV Market Potential © EnergyBusinessReports.com

20

Executive Summary

Electrical System of the Car

The electrical system is the most important part of the car's systems as it controls all of the power that comes into and leaves the system. The battery pack plays the same role in a solar car that a petrol tank plays in a normal car in storing power for future use. Solar cars use a range of batteries including lead-acid batteries, nickel-metal hydride batteries (NiMH), Nickel-Cadmium batteries (NiCd), Lithium ion batteries and Lithium polymer batteries. Lead-acid batteries are less expensive and easier to work with but have less power to weight ratio. Typically, solar cars use voltages between 84 and 170 volts.

Power electronics monitor and regulate the car's electricity. Components of the power electronics include the peak power trackers, the motor controller and the data acquisition system.

The peak power trackers manage the power coming from the solar array to maximize the power and deliver it to be stored in the motor. They also protect the batteries from overcharging. The motor controller manages the electricity flowing to the motor according to signals flowing from the accelerator.

Many solar cars have complex data acquisition systems that monitor the whole electrical system while even the most basic cars have systems that provide information on battery voltage and current to the driver. One such system utilizes Controller Area Network (CAN).

Drive Train

The setup of the motor and transmission is unique in solar cars. The electric motor normally drives only one wheel (usually at the back of the car) due to the low amount of power it generates. Solar car motors are normally rated at between 2 and 5 hp (1 and 3 kW); the most common type of motor is a dual-winding DC brushless. The dual-winding motor is sometimes also used as a transmission because multi-geared transmissions are rarely used.

© EnergyBusinessReports.com Solar PV Market Potential

21

Executive Summary

There are three basic types of transmissions used in solar cars:

• A single reduction direct drive;

• A variable ratio drive belt;

• A direct drive transmission (hub motor).

There are several varieties of each type. The most common is the direct drive transmission.

Mechanical Systems of the Car

The mechanical systems are designed to keep friction and weight to a minimum while maintaining strength. Designers normally use titanium and composites to ensure a good strength-to-weight ratio.

Solar cars usually have three wheels, but some have four. Three wheelers usually have two front wheels and one rear wheel: the front wheels steer and the rear wheel follows. Four wheel vehicles are set up like normal cars or similarly to three wheeled vehicles with the two rear wheels close together.

Solar cars have a wide range of suspensions because of varying bodies and chassis. The most common front suspension is the double-A-arm suspension found in traditional cars. The rear suspension is often a trailer-arm suspension found in motor cycles.

Solar cars are required to meet rigorous standards for brakes. Disc brakes are the most commonly used due to their good braking ability and ability to adjust. Mechanical and hydraulic brakes are both widely used with the brakes designed to move freely by minimize brake drag.

Steering systems for solar cars also vary. The major design factors for steering systems are efficiency, reliability and precision alignment to minimize tire wear and power loss. The

Solar PV Market Potential © EnergyBusinessReports.com

22

Executive Summary

popularity of solar car racing has led to some tire manufacturers designing tires for solar vehicles. This has increased overall safety and performance.

Solar Array of the Car

The solar array consists of hundreds of photovoltaic solar cells converting sunlight into electricity. Cars can use a variety of solar cell technologies; most often polycrystalline silicon, monocrystalline silicon, or gallium arsenide. The cells are wired together into strings while strings are often wired together to form a panel. Panels normally have voltages close to the nominal battery voltage. The main aim is to get as many cells in as small a space as possible. Designers encapsulate the cells to protect them from the weather and breakage.

Designing a solar array isn't as easy as just stringing bunch of cells together. A solar array acts like a lot of very small batteries all hooked together in series. The total voltage produced is the sum of all cell voltages. The problem is that if a single cell is in shadow it acts like a diode, blocking the flow of current for the entire string of cells. To correct against this, array designers use by-pass diodes in parallel with smaller segments of the string of cells, allowing current to flow around the non-functioning cell(s). Another consideration is that the battery itself can force current backwards through the array unless there are blocking diodes put at the end of each panel.

The power produced by the solar array depends on the weather conditions, the position of the sun and the capacity of the array. At noon on a bright day, a good array can produce over two kilowatts (2.6 hp).

Some cars have employed free standing or integrated sails to harness wind energy, which is allowed by the race regulations.

Chassis & Bodies

Solar cars have very distinctive shapes as there are no established standards for design. Designers aim to minimize drag, maximize exposure to the sun, minimize weight and make vehicles as safe as possible.

© EnergyBusinessReports.com Solar PV Market Potential

23

Executive Summary

In chassis design the aim is to maximize strength and safety while keeping the weight as low as possible. There are three main types of chassis:

• Space frame;

• Semi-monocoque or carbon stream;

• Monocoque.

The space frame uses a welded tubed structure to support the body which is a lightweight composite shell attached to the body. The semi-monocoque chassis uses composite beams and bulkheads to support the weight and is integrated into the belly with the top sections often being attached to the body. A monocoque structure uses the body of the car as an integrated load bearing structure.

Composite materials are widely used in solar cars. Carbon fiber, Kevlar and fiberglass are common composite structural materials while foam and honeycomb are commonly used filler materials. Epoxy resins are used to bond these materials together. Carbon fiber and Kevlar structures can be as strong as steel but with a much lighter weight.

Race Strategy & Solar Cars

Optimizing energy consumption is of prime importance in a solar car race. Therefore it is very important to be able to closely monitor the speed, energy consumption, energy intake from solar panel, among other things in real time. Some teams employ sophisticated telemetry that relays vehicle performance data to a computer in a following support vehicle.

The strategy employed depends upon the race rules and conditions. Most solar car races have set starting and stopping points where the objective is to reach the final point in the least amount of total time. Since aerodynamic drag rises exponentially with speed, the energy the car consumes also rises exponentially. This simple fact means that the optimum strategy is to travel at a single steady speed during all phases of the race. Given the varied conditions in all races and the limited (and continuously changing) supply of energy, most teams have race speed

Solar PV Market Potential © EnergyBusinessReports.com

24

Executive Summary

optimization programs that continuously update the team on how fast the vehicle should be traveling.

Solar Hot Water Systems

Solar hot water systems use sunlight to heat water. They may be used to heat domestic hot water or for space heating. These systems are basically composed of solar thermal collectors and a storage tank. The three basic classifications of solar water heaters are:

• Active systems which use pumps to circulate water or a heat transfer fluid;

• Passive systems which circulate water or a heat transfer fluid by natural circulation. These are also called thermosiphon systems;

• Batch systems using a tank directly heated by sunlight.

A Trombe wall is a passive solar heating and ventilation system consisting of an air channel sandwiched between a window and a sun-facing wall. Sunlight heats the air space during the day causing natural circulation through vents at the top and bottom of the wall and storing heat in the thermal mass. During the evening the Trombe wall radiates stored heat.

A transpired collector is an active solar heating and ventilation system consisting of a perforated sun-facing wall which acts as a solar thermal collector. The collector pre-heats air as it is drawn into the building's ventilation system through the perforations. These systems are inexpensive and commercial models have achieved efficiencies above 70%. Most systems pay for themselves within four to eight years.

Solar Photovoltaic Technology

Photovoltaics, PV, is a solar power technology that uses solar cells or solar photovoltaic arrays to convert energy from the sun into electricity. Photovoltaics is also the field of study relating to this technology.

© EnergyBusinessReports.com Solar PV Market Potential

25

Executive Summary

Solar cells produce direct current electricity from the sun’s rays, which can be used to power equipment or to recharge a battery. Many pocket calculators incorporate a solar cell.

When more power is required than a single cell can deliver, cells are generally grouped together to form “PV modules” that may in turn be arranged in “solar arrays” which are sometimes ambiguously referred to as solar panels. Such solar arrays have been used to power orbiting satellites and other spacecraft and in remote areas as a source of power for applications such as roadside emergency telephones, remote sensing, and cathodic protection of pipelines. The continual decline of manufacturing costs (dropping at three to five percent a year in recent years) is expanding the range of cost-effective uses including road signs, home power generation and even grid-connected electricity generation.

Large-scale incentive programs, offering financial incentives like the ability to sell excess electricity back to the public grid ("feed-in"), have greatly accelerated the pace of solar PV installations in Spain, Germany, Japan, the United States, Australia, South Korea, Italy, Greece, France, China and other countries.

Many corporations and institutions are currently developing ways to increase the practicality of solar power. While private companies conduct much of the research and development on solar energy, colleges and universities also work on solar-powered devices.

The most important issue with solar panels is cost. Because of much increased demand, the price of silicon used for most panels is now experiencing upward pressure. This has caused developers to start using other materials and thinner silicon to keep cost down. Due to economies of scale solar panels get less costly as people use and buy more - as manufacturers increase production, the cost is expected to continue to drop in the years to come. As of early 2006, the average cost per installed watt was about $6.50 to $7.50, including panels, inverters, mounts, and electrical items.

Grid-tied systems represented the largest growth area. In the U.S., with incentives from state governments, power companies and (in 2006 and 2007) from the federal government, growth is expected to climb. Net metering programs are one type of incentive driving growth in solar panel use. Net metering allows electricity customers to get credit for any extra power they send

Solar PV Market Potential © EnergyBusinessReports.com

26

Executive Summary

back into the grid. This would cause role reversal, as the utility company would be the buyer, and the solar panel owner would be the seller of electricity. To spur growth of their renewable energy market, Germany has adopted an extreme form of net metering, whereby customers get paid eight times what the power company charges them for any surplus they supply back to the grid. That large premium has made a huge demand in solar panels for that area.

Solar Power Satellites

A solar power satellite, or SPS, is a proposed satellite built in high Earth orbit that uses microwave power transmission to beam solar power to a very large antenna on Earth where it can be used in place of conventional power sources. The advantage of placing the solar collectors in space is the unobstructed view of the Sun, unaffected by the day/night cycle, weather, or seasons. However, the costs of construction are very high, and SPS will not be able to compete with conventional sources unless low launch costs can be achieved, or unless a space-based manufacturing industry develops and they can be built in orbit from off-Earth materials.

History of Solar Power Satellite

The SPS concept has been around since late 1968, but was considered impractical due to the lack of an efficient method of sending the power down to the Earth for use. Things changed in 1974 when Peter Glaser was granted patent number 3,781,647 for his method of transmitting the power to Earth using microwaves from a small antenna on the satellite to a much larger one on the ground, known as a rectenna.

Glaser's work took place at Arthur D. Little, Inc., who employed Glaser as a vice-president. NASA then became interested and granted them a contract to lead four other companies in a broader study in 1972. They found that while the concept had several major problems, chiefly the expense of putting the required materials in orbit and the lack of experience on projects of this scale in space, it showed enough promise to merit further investigation and research.

Most major aerospace companies then became briefly involved in some way, either under NASA grants or on their own money, to preserve a chance at the large contracts that would

© EnergyBusinessReports.com Solar PV Market Potential

27

Executive Summary

have been let out had the decision been made to go ahead with this concept. At the time the needs for electricity were booming, and there seemed to be no end in demand. When power use leveled off in the 1970s, the concept was shelved.

More recently the concept has again become interesting, generally due to increased energy demands and costs. At some price point the high construction costs of the SPS become favorable due to their low-cost delivery of power, and the varying costs of electricity sometimes approach (or even exceed) this point. In addition, continued advances in material science and space transport continue to whittle away at the startup cost of the SPS.

Components

The SPS essentially consists of three parts:

1. A huge solar collector, typically made up of solar cells;

2. A microwave antenna on the satellite, aimed at Earth;

3. An antenna occupying a large area on Earth to collect the power.

The SPS concept arose because space has several major advantages over earth for the collection of solar power. There is no air in space, so the satellites would receive somewhat more intense sunlight, unaffected by weather. In a geosynchronous orbit an SPS would be illuminated over 99% of the time. The SPS would be in Earth's shadow on only a few days at the spring and fall equinoxes; and even then for a maximum of an hour and a half late at night when power demands are at their lowest. This allows expensive storage facilities necessary to earth-based system to be avoided.

In many ways, the SPS as a concept is simpler than most power systems here on Earth. This includes the structure needed to hold it together, which in orbit can be considerably lighter due to the lack of weight. Some early studies looked at solar furnaces to drive conventional turbines, but as the efficiency of the solar cell improved, this concept eventually became

Solar PV Market Potential © EnergyBusinessReports.com

28

Executive Summary

impractical. In either case, another advantage of the design is that waste heat is re-radiated back into space, instead of warming the biosphere as with conventional sources.

The Earth-based receiver antenna (or rectenna) is also key to the SPS concept. It consists of a series of short dipole antennas, connected with a diode. Microwaves broadcast from the SPS are received in the dipoles with about 85% efficiency. With a conventional microwave antenna the reception is even better, but the cost and complexity is considerably greater. Rectennas would be multiple kilometers across. Crops and farm animals may be raised underneath the rectenna, as the thin wires used only slightly reduce sunlight, so the rectennas are not as expensive in terms of land as might be supposed.

For best efficiency the satellite antenna must be between one and 1.5 kilometers in diameter and the ground rectenna around 14 kilometers by 10 kilometers. For the desired microwave intensity this allows transfer of between 5 and 10 gigawatts of power. To be cost effective it needs to operate at maximum capacity. To collect and convert that much power, the satellite needs between 50 and 100 square kilometers of collector area using standard ~14% efficient monocrystalline silicon solar cells. State of the art and expensive triple junction gallium arsenide solar cells with a maximum efficiency of 28% could reduce the collector area by half. In both cases the solar station's structure would be several kilometers wide, making it much larger than most man-made structures here on Earth. While certainly not beyond current engineering capabilities, building structures of this size in orbit has never been attempted before.

Challenges

Launch Costs

Without a doubt, the most obvious problem for the SPS concept is the currently immense cost of space launches. Current rates on the Space Shuttle run between $3,000 and $5,000 per pound ($6,600/kg and $11,000/kg), depending on whose numbers are used. Calculations show that launch costs of less than about $400-500/kg to LEO seem to be necessary.

© EnergyBusinessReports.com Solar PV Market Potential

29

Executive Summary

However, economies of scale on expendable vehicles could give rather large reductions in launch cost for this kind of launched mass. Thousands of rocket launches could very well reduce the costs by ten to twenty times using standard costing models. This puts the economics into the range where this system could be conceivably attempted. Reusable vehicles could quite conceivably attack the launch problem as well; but are not a well developed technology.

To give an idea of the scale of the problem, assuming a typical solar panel mass of 20 kg per kilowatt, and without considering the mass of the support structure, antenna or significant mass reduction of focusing mirrors, a 4 GW power station would weigh about 80,000 metric tons. This is excessive though, as a space solar-panel would not need to support its own weight, and would not be subject to earth's corrosive atmosphere. Very lightweight designs could achieve one kg/kW, or 4000 metric tons for a four GW station. This would be the equivalent of between 40 and 800 HLLV launches to send the material to low earth orbit, where it would be turned into subassembly solar arrays, which then use ion-engine style rockets to move to GEO orbit. With an estimated serial launch cost for shuttle-based HLLVs of $500 million to $800 million, total launch costs would range between $20 billion (low cost HLLV, low weight panel) and $320 billion ('expensive' HLLV, unnecessarily heavy panel). On top of this, the cost of a large assembly area in LEO and GEO (which would be spread over several power satellites) and the costs of the materials and manufacture are added.

So how much money could a SSPS be expected to make? For every one gigawatt rating, a SSPS system will generate 8.75 terawatt-hours of electricity per year, or 175 TW•h over a twenty year lifetime. With current market prices of $0.22 per kW•h (UK, Jan06) and an SSPS's ability to send its energy to places of greatest demand, this would equate to $1.93 billion per year or $38.6 billion over its lifetime. The example four GW 'economy' SSPS above could therefore generate in excess of $154 billion over its lifetime. Assuming that facilities are available, it may turn out to be substantially cheaper to recast on-site steel in GEO, than launch it from Earth. If true then the initial launch cost could be spread over multiple lifespans.

Noting the problem of high launch costs in the early 1970s, organizations came up with the idea of building the SPS's in orbit with materials from the Moon. Launch costs from the Moon are about 100 times lower than from Earth, due to the lower gravity. This 1970s was predicated on the then advertised future launch costs of NASA's space shuttle and only works if the

Solar PV Market Potential © EnergyBusinessReports.com

30

Executive Summary

number of satellites to be built is on the order of several hundred; otherwise, the cost of setting up the production lines in space and mining facilities on the Moon are just as huge as launching from Earth in the first place. In 1980, when it became obvious NASA's launch cost estimates for the space shuttle were grossly optimistic, O'Neill et al published another route to manufacturing using lunar materials with much lower startup costs. This 1980s SPS concept relied less on human presence in space and more on partially self-replicating systems on the lunar surface under telepresence control of workers stationed on Earth.

Asteroid mining has also been seriously considered. A NASA design study produced a 10,000 ton mining vehicle to be assembled in orbit that would return a 500,000 ton asteroid 'fragment' to geostationary orbit. Only about 3000 tons of the mining ship would constitute traditional aerospace-grade payload. The rest would be reaction mass for the mass-driver engine; which could easily consist of the spent rocket stages used to launch the payload. Assuming that 100% of the returned asteroid was useful, and that the asteroid miner couldn't be reused, that represents nearly a 95% reduction in launch costs. The true merits of such a method would depend on a thorough mineral survey of the candidate asteroids. Once built, NASA's CEV should be capable of beginning such a survey, Congressional money and imagination permitting.

More recently the SPS concept has been suggested as a use for a space elevator. The elevator would make construction of an SPS considerably less expensive, possibly making them competitive with conventional sources. However it appears unlikely that even recent advances in materials science, namely carbon nanotubes, can reduce the price of construction of the elevator enough in the short term.

Currently, the costs of solar panels are too high to use them to produce bulk domestic electricity. However, the mass production of solar panels necessary to build a SPS system would be likely to reduce the costs sufficiently. As well, any panel design suited to SPS use is likely to be quite different than earth suitable panels. This may benefit as costs may be lower (see cost analysis above), but will not be able to take advantage of maximum economies of scale, and so piggyback on production of Earth based panels.

© EnergyBusinessReports.com Solar PV Market Potential

31

Executive Summary

It should be noted, however, that there are also certain developments in the production of solar panels. The production of thin film solar panels (so-called "nanosolar") could reduce production costs as well as weight and therefore reduce the total cost of the project. In addition, private space corporations could gain interest in transporting goods (such as satellites, supplies and parts of commercial space hotels) to LEO, since they already are developing spacecraft to transport space tourists.

Safety

The use of microwave transmission of power has been the most controversial item concerning SPS development, but the incineration of anything which strays into the beam's path is an extreme misconception. The beam's most intense section (the center) is far below the lethal levels of concentration even for an exposure which has been prolonged indefinitely. Furthermore, the possibility of exposure to the intense center of the beam can easily be controlled on the ground and an airplane flying through the beam surrounds its passengers with a protective layer of metal, which will intercept the microwaves. Over 95% of the beam will fall on the rectenna. The remaining microwaves will be dispersed to low concentrations well within standards currently imposed upon microwave emissions around the world.

The intensity of microwaves at ground level that would be used in the center of the beam can be designed into the system, but is likely to be comparable to that used by mobile phones. The microwaves must not be too intense in order to avoid injury to wildlife, particularly birds. Experiments with deliberate irradiation with microwaves at reasonable levels have failed to show any negative effects even over multiple generations.

Some have suggested locating rectennas offshore, but this presents problems of its own.

A commonly proposed approach to ensuring fail-safe beam targeting is to use a retrodirective phased array antenna/rectenna. A "pilot" microwave beam is emitted from the center of the rectenna on the ground to establish a phase front at the transmitting antenna, where circuits in each of the antenna's subarrays compare the pilot beam's phase front with an internal clock phase to use as a reference to control the phase of the outgoing signal. This allows the transmitted beam to be centered precisely on the rectenna and to have a high degree of phase

Solar PV Market Potential © EnergyBusinessReports.com

32

Executive Summary

uniformity, but if the pilot beam is lost for any reason (if the transmitting antenna is turned away from the rectenna, for example) the phase control system fails and the microwave power beam is automatically defocused. Such a system would be physically incapable of focusing its power beam anywhere that did not have a pilot beam transmitter.

It is important for the system that as much of the microwave radiation as possible is focused on the rectenna as that increases the transmission efficiency. Outside of the rectenna the microwave levels rapidly decrease, nearby towns or cities should be completely unaffected.

The long-term effects of beaming power through the ionosphere in the form of microwaves has yet to be studied.

Economic Feasibility

Current prices for electricity on the grid fluctuate depending on time of day, but typical household delivery costs about 5 cents per kilowatt hour in North America. If the lifetime of an SPS is 20 years and it delivers 5 gigawatts to the grid, the commercial value of that power is 5,000,000,000 / 1000 = 5,000,000 kilowatt hours, which multiplied by $.05 per kW•h gives $250,000 revenue per hour. $250,000 × 24 hours × 365 days × 20 years = $43,800,000,000. By contrast, in England (Oct 2005) electricity can cost 9–22 cents per kilowatt hour. This would translate to a lifetime output of $77–$193 billion. In addition, in the case of England, the country is further north than even most inhabited parts of Canada, and hence receives little insolation over much of the year, so conventional solar power is not terribly competitive at 2006 per-kilowatt-hour delivered costs. (However, per-kilowatt-hour photovoltaic costs have been in exponential decline [10] for decades, with a 20-fold decrease from 1975 to 2001.)

In order to be competitive, an SPS must cost no more than existing suppliers; this may be difficult, especially if it is deployed to North America. Either it must cost less to deploy, or it must operate for a very long period of time. Many proponents have suggested that the lifetime is effectively infinite, but normal maintenance and replacement of less durable components makes this unlikely. Satellites do not, in our now-extensive experience, last forever.

© EnergyBusinessReports.com Solar PV Market Potential

33

Executive Summary

A potentially useful concept to contrast SPS with is the constructing a ground-based solar power system that generates an equivalent amount of power. Such a system would require a large solar array built in a well-sunlit area, the Sahara Desert for instance. However, an SPS also requires a large ground structure; the rectenna on the ground is much larger than the area of the solar panels in space. The ground-only solar array would have the advantages of costing considerably less to construct and requiring no significant technological advances.

However, such a system has disadvantages as well. A terrestrial solar station intercepts only one third of the solar energy that an array of equal size could intercept in space, since no power is generated at night and less light strikes the panels when the Sun is low in the sky. Further, if it is assumed that the array must supply baseline power (not a given), some form of energy storage would be required to provide power at night, such as hydrogen, compressed air, or pumped storage hydroelectricity. With present technology, energy storage on this scale is prohibitively expensive. Weather conditions would also interfere with power collection, and can cause greater wear and tear on the solar collectors than the environment of Earth orbit; a sandstorm could cause devastating damage, for example. Beamed microwave power allows one to send the power near to where it is needed, while a solar generating station in the Sahara would provide power most economically to the surrounding area, where current demand is relatively low. Alternatively, the ground-based power could be used on-site to produce chemical fuels for transportation and storage, as in the proposed hydrogen economy. Moreover, remote tropical location of a vast, centralized photovoltaic generator is a somewhat artificial scenario, and makes less sense every year as photovoltaic costs decline. The assumption that ground-based photovoltaics are most economically deployed in large, centralized arrays rather than distributed to end-use points (e.g., rooftops) should be questioned.

Many advances in construction techniques that make the SPS concept more economical could make a ground-based system more economical as well. For instance, many SPS plans are based on building the framework with automated machinery supplied with raw materials, typically aluminum. Such a system could just as easily be used on Earth, no shipping required. However, Earth-based construction already has access to extremely cheap human labor that would not be available in space, so such construction techniques would have to be extremely competitive.

Solar PV Market Potential © EnergyBusinessReports.com

34

Executive Summary

Advantages of SPS

The use of microwave beams to heat the oceans has been studied. Some research has speculated that microwave beams appropriately applied would be capable of deflecting the course of hurricanes.

Solar Thermal Energy

Solar thermal energy refers to the idea of harnessing solar power for practical applications from solar heating to electrical power generation. Solar thermal collectors, such as solar hot water panels, are commonly used to generate solar hot water for domestic and light industrial applications. Solar thermal energy is used in architecture and building design to control heating and ventilation in both active solar and passive solar designs.

Solar Updraft Tower

The solar updraft tower is a proposed type of renewable-energy power plant. Air is heated in a very large circular greenhouse-like structure, and the resulting convection causes the air to rise and escape through a tall tower. The moving air drives turbines, which produce electricity.

There are no solar updraft towers in operation at present. A research prototype operated in Spain in the 1980s, and EnviroMission proposes to construct a full scale power station using this technology in Australia.

Overview

The generating ability of a solar updraft power plant depends primarily on two factors: the size of the collector area and chimney height. With a larger collector area, more volume of air is warmed up to flow up the chimney; collector areas as large as 7 km in diameter have been considered. With a larger chimney height, the pressure difference increases the stack effect; chimneys as tall as 1000 m have been considered. Further, a combined increase of the collector area and the chimney height leads to massively larger productivity of the power plant.

© EnergyBusinessReports.com Solar PV Market Potential

35

Executive Summary

Heat can be stored inside the collector area greenhouse, to be used to warm the air later on. Water, with its relatively high specific heat capacity, can be filled in tubes placed under the collector increasing the energy storage as needed.

Turbines can be installed in a ring around the base of the tower, with a horizontal axis, as planned for the Australian project described below and seen in the diagram above; or - as in the prototype in Spain - a single vertical axis turbine can be installed inside the chimney.

Solar towers do not produce carbon dioxide emissions during their operation, but are associated with the manufacture of its construction materials, particularly cement. Net energy payback is estimated to be two to three years. The relatively low-tech approach could allow local resources and labor to be used for its construction and maintenance.

History

In 1903, Spanish Colonel Isidoro Cabanyes first proposed a solar chimney power plant in the magazine "La energía eléctrica". One of the earliest descriptions of a solar chimney power plant was written in 1931 by a German author, Hanns Günther. Beginning in 1975, Robert E. Lucier applied for patents on a solar chimney electric power generator; between 1978 and 1981 these patents, since expired, were granted in Australia, Canada, Israel and the U.S.

In 1982, a medium-scale working model of a solar chimney power plant was built under the direction of German engineer Jörg Schlaich in Manzanares, Ciudad Real, 150 km south of Madrid, Spain; the project was funded by the German government. The chimney had a height of 195 meters and a diameter of 10 meters, with a collection area (greenhouse) of 46,000 m² (about 11 acres, or 244 m diameter) obtaining a maximum power output of about 50 kW. During operation, optimization data was collected on a second-by-second basis. This pilot power plant operated successfully for approximately eight years and was decommissioned in 1989.

Solar PV Market Potential © EnergyBusinessReports.com

36

Executive Summary

Economical Feasibility of Solar Updraft Tower

With a very large initial capital outlay, no costs for consumables (i.e. fuel) and relatively constant income (from electricity sales) over the life of the project, a solar updraft tower would be placed in the same asset class as dams, bridges, tunnels, motorways and other similar large infrastructure projects. Financial viability would be assessed on a similar basis.

For example, the solar updraft tower being planned by Enviromission is expected to cost AUD$250 million ($189 million) to construct and will service 50,000 homes.

Unlike a wind farm, a Solar Tower is not expected to create a reliance on standby capacity from traditional energy sources.

Various types of thermal storage mechanisms (such as a heat-absorbing surface material or salt water ponds) could be incorporated to smooth out power yields over the day/night cycle and potentially allow a solar updraft tower to provide something similar to base load power. This is highly desirable, as most renewable power systems (wind, solar-electrical) are variable, and a typical national electrical grid requires a combination of base, variable and on-demand power sources for stability.

There is still a great amount of uncertainty and debate on what the cost of production for electricity would be for a solar updraft tower and thus whether a tower (large or small) can be made profitable.

It was claimed, in 2002, that a Solar Tower in Australia would be an expensive way of generating electricity as compared to a conventional wind farm.

However, a 2006 study claims that a large tower in the southwestern United States could not only outperform wind farms on a cost basis but also compete directly with current conventional gas-fired, and some coal-fired, plants.

No reliable electricity cost figures are expected until such time as engineering models are available for finalized tower designs and construction has begun on a production tower.

© EnergyBusinessReports.com Solar PV Market Potential

37

Executive Summary

Given the novelty and enormous scale of any commercial solar updraft tower project, tourism income may become a factor, particular for the first towers to be created. Some promotion videos for the Enviromission tower have even shown a glass observation area at the top of the tower.

Given that towers would likely be built in poorer areas with very low-value land, this may be more of interest to the local government than to the operator itself.

Converting Solar Energy to Electrical Energy

The solar updraft tower does not convert all the incoming solar energy into electrical energy. Many designs in the solar thermal group of collectors have higher conversion rates. The low conversion rate of the Solar Tower is balanced by the low investment cost per square meter of solar collection.

According to model calculations, a simple updraft power plant with an output of 200 MW would need a collector seven kilometers in diameter (total area of about 38 km²) and a 1000-metre-high chimney. The 38 km² collecting area is expected to extract about 0.5%, or 5 W/m² of 1 kW/m², of the solar power that falls upon it. Note that in comparison, biomass photosynthesis is about 0.1% efficient. Because no data is available to test these models on a large-scale updraft tower there remains uncertainty about the reliability of these calculations.

The performance of an updraft tower may be degraded by factors such as atmospheric winds, or by drag induced by bracings used for supporting the chimney. Another inefficiency is that reflection of light off the top of the canopy implies a loss of 7.7% of incoming solar energy, as calculated by the fresnel equations, if the canopy is made of common glass.

Location is also a factor. A Solar updraft power plant located at high latitudes such as in Canada may produce no more than 85% of a similar plant located closer to the equator.

Related Concepts

• The Vortex engine proposal replaces the physical chimney by a vortex of twisting air;

Solar PV Market Potential © EnergyBusinessReports.com

38

Executive Summary

• Floating Solar Chimney Technology proposes to keep a lightweight chimney aloft using rings of lifting balloons filled with a lighter-than-air gas;

• The chimney could be constructed up a mountainside, using the terrain for support;

• The inverse of the solar updraft tower is the downdraft-driven energy tower. Evaporation of sprayed water at the top of the tower would cause a downdraft by cooling the air and driving wind turbines at the bottom of the tower. This design does not require a large solar collector but does consume up to 50% of the generated energy operating the water pumps.

Storing Solar Energy

Storage is an important issue in the development of solar energy because modern energy systems usually assume continuous availability of energy. Solar energy is not available at night, and the performance of solar power systems is affected by unpredictable weather patterns; therefore, storage media or back-up power systems must be used.

Thermal mass systems can store solar energy in the form of heat at domestically useful temperatures for daily or seasonal durations. Thermal storage systems generally use readily available materials with high specific heat capacities such as water, earth and stone. Well-designed systems can lower peak demand, shift time-of-use to off-peak hours and reduce overall heating and cooling requirements.

Phase change materials such as paraffin wax and Glauber's salt are another thermal storage media. These materials are inexpensive, readily available, and can deliver domestically useful temperatures (approximately 64 °C). The "Dover House" (in Dover, Massachusetts) was the first to use a Glauber's salt heating system, in 1948.

Solar energy can be stored at high temperatures using molten salts. Salts are an effective storage medium because they are low-cost, have a high specific heat capacity and can deliver heat at temperatures compatible with conventional power systems. The Solar Two used this

© EnergyBusinessReports.com Solar PV Market Potential

39

Executive Summary

method of energy storage, allowing it to store 1.44 TJ in its 68 m³ storage tank with an annual storage efficiency of about 99%.

Off-grid PV systems have traditionally used rechargeable batteries to store excess electricity. With grid-tied systems, excess electricity can be sent to the transmission grid. Net metering programs give these systems a credit for the electricity they deliver to the grid. This credit offsets electricity provided from the grid when the system cannot meet demand, effectively using the grid as a storage mechanism.