Embed Size (px)

Citation preview

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANA

A COMPONENT UNIT OF THE

STATE OF LOUISIANA

FINANCIAL STATEMENT AUDIT FOR THE YEAR ENDING JUNE 30, 2015

ISSUED MAY 18, 2016

LOUISIANA LEGISLATIVE AUDITOR 1600 NORTH THIRD STREET

POST OFFICE BOX 94397 BATON ROUGE, LOUISIANA 70804-9397

LEGISLATIVE AUDITOR DARYL G. PURPERA, CPA, CFE

ASSISTANT LEGISLATIVE AUDITOR FOR STATE AUDIT SERVICES

NICOLE B. EDMONSON, CIA, CGAP, MPA

DIRECTOR OF FINANCIAL AUDIT ERNEST F. SUMMERVILLE, JR., CPA

Under the provisions of state law, this report is a public document. A copy of this report has been submitted to the Governor, to the Attorney General, and to other public officials as required by state law. A copy of this report is available for public inspection at the Baton Rouge office of the Louisiana Legislative Auditor. This document is produced by the Louisiana Legislative Auditor, State of Louisiana, Post Office Box 94397, Baton Rouge, Louisiana 70804-9397 in accordance with Louisiana Revised Statute 24:513. One copy of this public document was produced at an approximate cost of $2.30. This material was produced in accordance with the standards for state agencies established pursuant to R.S. 43:31. This report is available on the Legislative Auditor’s website at www.lla.la.gov. When contacting the office, you may refer to Agency ID No. 3430 or Report ID No. 80150159 for additional information. In compliance with the Americans With Disabilities Act, if you need special assistance relative to this document, or any documents of the Legislative Auditor, please contact Elizabeth Coxe, Chief Administrative Officer, at 225-339-3800.

1

TABLE OF CONTENTS

Page Independent Auditor’s Report ......................................................................................................... 2

Management’s Discussion and Analysis ........................................................................................ 5

Statement Basic Financial Statements:

Statement of Net Position ..................................................................................... A ..................12

Statement of Revenues, Expenses, and Changes in Net Position..................................................................................................... B ..................13

Statement of Cash Flows ...................................................................................... C ..................14

Notes to the Financial Statements ...............................................................................................15

Schedule Required Supplementary Information:

Schedule of the Board’s Proportionate Share of the Net Pension Liability ...............................................................................1...................31

Schedule of Board Contributions ........................................................................2...................31

Schedule of Funding Progress for the Other Postemployment Benefits Plan ................................................................3...................32

Supplementary Information:

Schedule of Per Diem Paid Board Members ..........................................................4...................34

Exhibit Independent Auditor’s Report on Internal Control over

Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards .............................................. A

Appendix Management’s Corrective Action Plans and Responses

to the Findings and Recommendations .................................................................. A

LOUISIANA LEGISLATIVE AUDITOR

DARYL G. PURPERA, CPA, CFE

1600 NORTH THIRD STREET • POST OFFICE BOX 94397 • BATON ROUGE, LOUISIANA 70804-9397

WWW.LLA.LA.GOV • PHONE: 225-339-3800 • FAX: 225-339-3870

May 12, 2016

Independent Auditor’s Report

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANA STATE OF LOUISIANA New Orleans, Louisiana Report on the Financial Statements We have audited the accompanying financial statements of the business-type activities of the State Board of Certified Public Accountants of Louisiana (Board), a component unit of the state of Louisiana, as of and for the year ended June 30, 2015, and the related notes to the financial statements, which collectively comprise the Board’s basic financial statements as listed in the Table of Contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the

State Board of Certified Public Accountants of Louisiana Independent Auditor’s Report

3

effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the business-type activities of the Board as of June 30, 2015, and the respective changes in financial position and cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matters As disclosed in note 4 to the financial statements, the net pension liability for the Board was $1,212,498 at June 30, 2015, as determined by the Louisiana State Employees’ Retirement System (LASERS) and Teachers’ Retirement System of Louisiana (TRSL). The related actuarial valuations were performed by LASERS’s and TRSL’s actuaries using various assumptions. Because actual experience may differ from the assumptions used, there is a risk that this amount at June 30, 2015, could be under or overstated. As discussed in notes 1-K and 10 to the financial statements, the Board implemented Governmental Accounting Standards Board (GASB) Statement 68, Accounting and Financial Reporting for Pensions − an amendment of GASB Statement No. 27, and GASB Statement No. 71, Pension Transition for Contributions Made Subsequent to the Measurement Date − an amendment of GASB Statement No. 68, for the year ended June 30, 2015. The adoption of these standards required the Board to record its proportionate share of pension amounts related to its participation in cost-sharing, multiple-employer defined benefit pension plans, restating the previous year. As a result of the implementation, the Board’s net position decreased by $1,066,340; net pension liability was recorded in the amount of $1,178,353; and deferred outflow of resources was recorded in the amount of $112,013 as of July 1, 2014. Our opinion is not modified with respect to the matters emphasized above. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the Management’s Discussion and Analysis on pages 5 through 11, the Schedule of the Board’s Proportionate Share of the Net Pension Liability on page 31, the Schedule of Board Contributions on page 31, and the Schedule of Funding Progress for the Other Postemployment Benefits Plan on page 32 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by GASB, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary

State Board of Certified Public Accountants of Louisiana Independent Auditor’s Report

4

information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquires of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Supplementary Information Our audit was conducted for the purpose of forming an opinion on the financial statements that collectively comprise the Board’s basic financial statements. The Schedule of Per Diem Paid Board Members on page 34 is presented for purposes of additional analysis and is not a required part of the basic financial statements. The Schedule of Per Diem Paid Board Members is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the Schedule of Per Diem Paid Board Members is fairly stated, in all material respects, in relation to the basic financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated May 12, 2016, on our consideration of the Board’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. The report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Board’s internal control over financial reporting and compliance.

Respectfully submitted, Daryl G. Purpera, CPA, CFE Legislative Auditor

MET:DG:BDC:EFS:aa CPA2015

5

MANAGEMENT’S DISCUSSION AND ANALYSIS

Management’s Discussion and Analysis of the State Board of Certified Public Accountants of Louisiana’s (Board) financial performance presents a narrative overview and analysis of the Board’s financial activities for the year ended June 30, 2015. This document focuses on the current year’s activities, resulting changes, and currently known facts in comparison with the prior year’s information. Please read this document in conjunction with the additional information contained in the Board’s financial statements, which begin on page 12. FINANCIAL HIGHLIGHTS

The Board’s operating revenue is generated by fees for license and firm permit applications, annual license and permit renewals, and by fines, settlements, and cost recoveries from enforcement related activities.

Total operating revenue decreased by $35,065 (or 3.26%) from 2015 to 2014. More than 100% of that decrease occurred because revenue from enforcement actions were lower in this fiscal year than the prior year.

Revenue related to enforcement activity is subject to wide fluctuation from year to year. Fines and settlements, which include recoveries of enforcement costs, represent $78,208 (or 7.51%) of total operating revenues for the fiscal year 2015. Last fiscal year, revenue from enforcement activity was $116,937 (or 10.86%) of total operating revenue.

Nonoperating revenue consists of interest on a money market checking account. Interest earnings represent less than 0.35% of total revenues for both this fiscal year and last fiscal year.

Operating expenses increased by $113,172 (or 12.05%) from a total of $939,279 last fiscal year to $1,052,451 this fiscal year. More than 95% of the increase can be attributed to a 50% increase in the state retirement expense over the prior year; bad debt expense of almost $26,000; software acquisitions of nearly $12,000 more than last year’s acquisitions; and compensation increases including being more fully staffed throughout the year.

OVERVIEW OF THE FINANCIAL STATEMENTS The following graphic illustrates the minimum requirements for Special Purpose Governments Engaged in Business-Type Activities established by Governmental Accounting Standards Board (GASB) Statement 34, Basic Financial Statements—and Management’s Discussion and Analysis—for State and Local Governments.

State Board of Certified Public Accountants of Louisiana Management’s Discussion and Analysis

6

These financial statements consist of three sections - Management’s Discussion and Analysis (this section), the basic financial statements, and required supplementary information, as may be applicable. The Board includes a supplemental schedule of Board Member compensation. Basic Financial Statements The basic financial statements present information for the Board as a whole, in a format designed to make the statements easier for the reader to understand. The statements in this section include the Statement of Net Position; the Statement of Revenues, Expenses, and Changes in Net Position; and the Statement of Cash Flows. The Statement of Net Position (page 12) presents assets, deferred outflows of resources, liabilities, and deferred inflows of resources separately. The difference between assets plus deferred outflows and liabilities plus deferred inflows is net position, which may provide a useful indicator of whether the financial position of the Board is improving or deteriorating. The Statement of Revenues, Expenses, and Changes in Net Position (page 13) presents information showing how the Board’s assets changed as a result of current-year operations. Regardless of when cash is affected, all changes in net position are reported when the underlying transactions occur. As a result, there are transactions included that will not affect cash until future fiscal periods. The Statement of Cash Flows (page 14) presents information showing how the Board’s cash changed as a result of current-year operations. The cash flow statement is prepared using the direct method and includes the reconciliation of operating income (loss) to net cash provided (used) by operating activities (indirect method) as required by GASB Statement 34. Required Supplementary Information and Supplementary Information The required supplementary information presents additional information for the Board as required by the state’s Division of Administration. The Schedule of Per Diem Paid to Board Members (page 34) presents the compensation received by the Board Members in accordance with Louisiana Act No. 473 of 1999.

Management’s Discussion and Analysis

Basic Financial Statements

Required Supplementary Information (other than MD&A)

State Board of Certified Public Accountants of Louisiana Management’s Discussion and Analysis

7

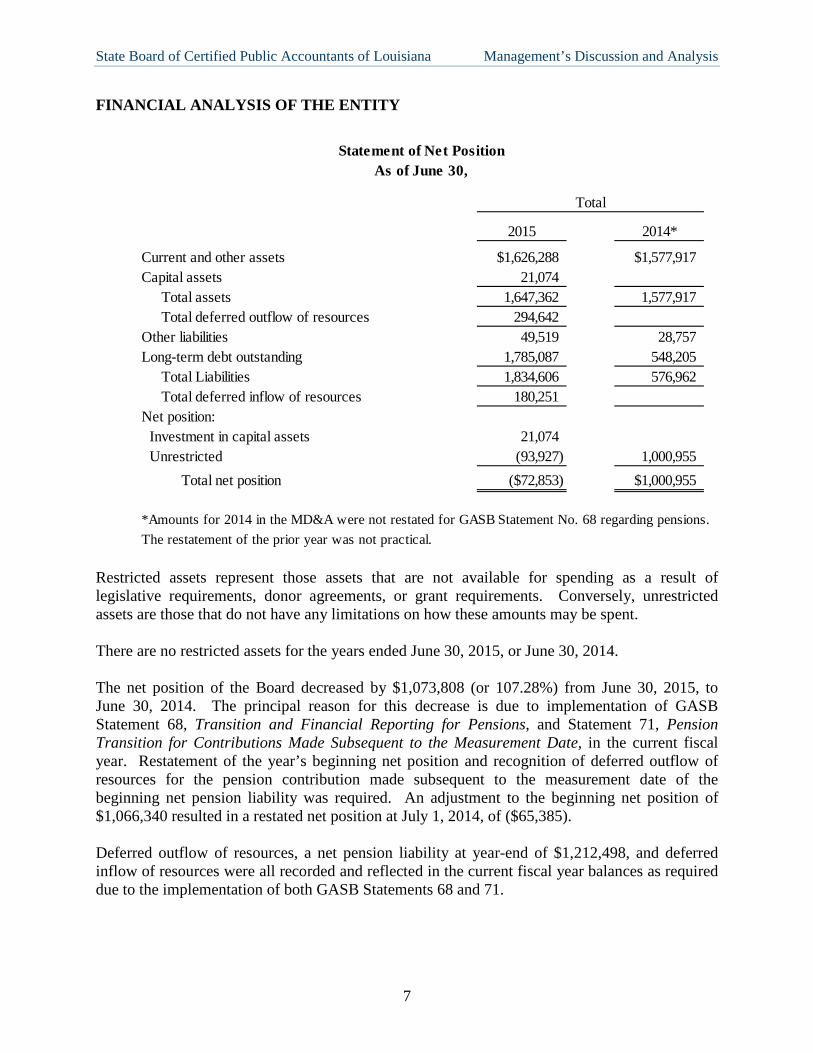

FINANCIAL ANALYSIS OF THE ENTITY

Restricted assets represent those assets that are not available for spending as a result of legislative requirements, donor agreements, or grant requirements. Conversely, unrestricted assets are those that do not have any limitations on how these amounts may be spent. There are no restricted assets for the years ended June 30, 2015, or June 30, 2014. The net position of the Board decreased by $1,073,808 (or 107.28%) from June 30, 2015, to June 30, 2014. The principal reason for this decrease is due to implementation of GASB Statement 68, Transition and Financial Reporting for Pensions, and Statement 71, Pension Transition for Contributions Made Subsequent to the Measurement Date, in the current fiscal year. Restatement of the year’s beginning net position and recognition of deferred outflow of resources for the pension contribution made subsequent to the measurement date of the beginning net pension liability was required. An adjustment to the beginning net position of $1,066,340 resulted in a restated net position at July 1, 2014, of ($65,385). Deferred outflow of resources, a net pension liability at year-end of $1,212,498, and deferred inflow of resources were all recorded and reflected in the current fiscal year balances as required due to the implementation of both GASB Statements 68 and 71.

2015 2014*

Current and other assets $1,626,288 $1,577,917Capital assets 21,074 Total assets 1,647,362 1,577,917 Total deferred outflow of resources 294,642Other liabilities 49,519 28,757Long-term debt outstanding 1,785,087 548,205 Total Liabilities 1,834,606 576,962 Total deferred inflow of resources 180,251Net position: Investment in capital assets 21,074 Unrestricted (93,927) 1,000,955 Total net position ($72,853) $1,000,955

*Amounts for 2014 in the MD&A were not restated for GASB Statement No. 68 regarding pensions. The restatement of the prior year was not practical.

Total

Statement of Net PositionAs of June 30,

State Board of Certified Public Accountants of Louisiana Management’s Discussion and Analysis

8

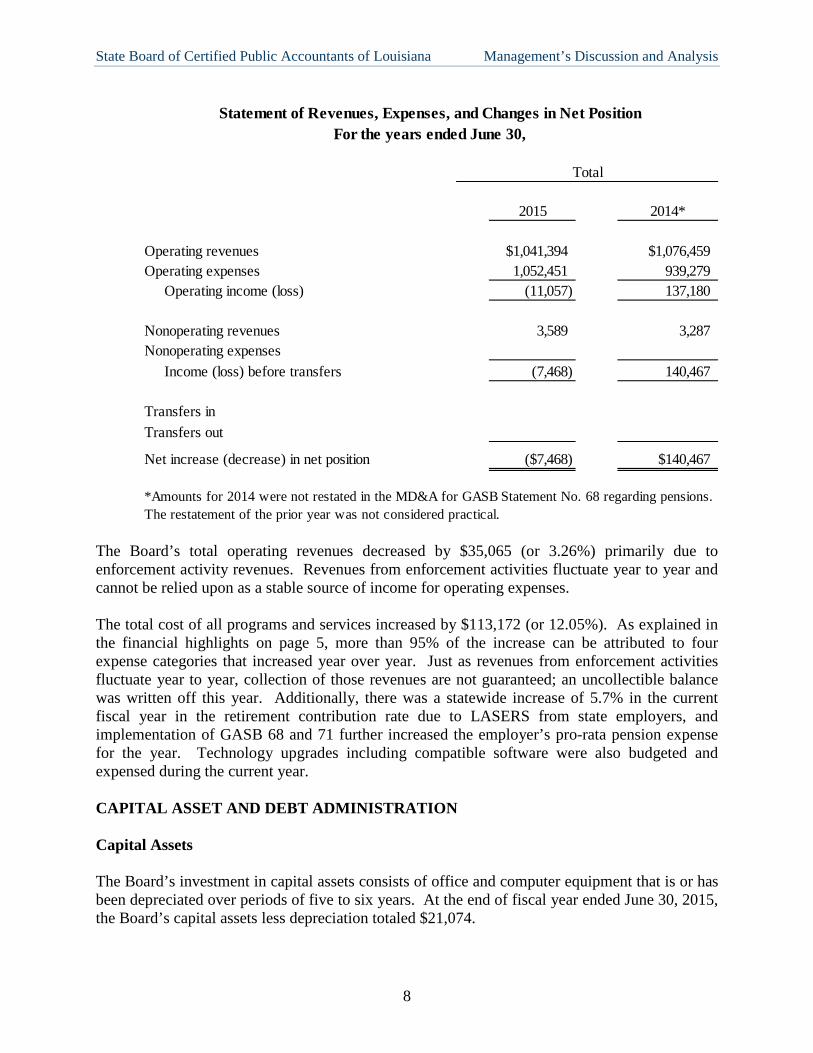

The Board’s total operating revenues decreased by $35,065 (or 3.26%) primarily due to enforcement activity revenues. Revenues from enforcement activities fluctuate year to year and cannot be relied upon as a stable source of income for operating expenses. The total cost of all programs and services increased by $113,172 (or 12.05%). As explained in the financial highlights on page 5, more than 95% of the increase can be attributed to four expense categories that increased year over year. Just as revenues from enforcement activities fluctuate year to year, collection of those revenues are not guaranteed; an uncollectible balance was written off this year. Additionally, there was a statewide increase of 5.7% in the current fiscal year in the retirement contribution rate due to LASERS from state employers, and implementation of GASB 68 and 71 further increased the employer’s pro-rata pension expense for the year. Technology upgrades including compatible software were also budgeted and expensed during the current year. CAPITAL ASSET AND DEBT ADMINISTRATION Capital Assets The Board’s investment in capital assets consists of office and computer equipment that is or has been depreciated over periods of five to six years. At the end of fiscal year ended June 30, 2015, the Board’s capital assets less depreciation totaled $21,074.

2015 2014*

Operating revenues $1,041,394 $1,076,459Operating expenses 1,052,451 939,279 Operating income (loss) (11,057) 137,180

Nonoperating revenues 3,589 3,287Nonoperating expenses Income (loss) before transfers (7,468) 140,467

Transfers inTransfers out

Net increase (decrease) in net position ($7,468) $140,467

*Amounts for 2014 were not restated in the MD&A for GASB Statement No. 68 regarding pensions. The restatement of the prior year was not considered practical.

Total

Statement of Revenues, Expenses, and Changes in Net PositionFor the years ended June 30,

State Board of Certified Public Accountants of Louisiana Management’s Discussion and Analysis

9

This year’s major addition to capital assets included the purchase and installation of a new computer server to replace obsolete servers that were more than six years old. Debt The Board has not financed through external borrowing or incurring debt and thus does not have any outstanding bonds or notes for this or the previous fiscal year. Other obligations include compensated absences (accrued vacation and compensatory leave) earned and accumulated by employees, retirement (pension) liabilities, and other postemployment benefits as described in the notes to the financial statements. The Board has claims and judgments of $0 outstanding at year-end compared with $0 last year. VARIATIONS BETWEEN ORIGINAL AND FINAL BUDGETS The Board’s annual budget is on a modified accrual basis of accounting excluding certain non-exchange revenues and noncash items such as accrued earnings of compensated absences, other postemployment benefits, and depreciation. The original budget approved for the year ended June 30, 2015, was amended once during the fiscal year. Similarly, the original budget for the year ended June 30, 2014, was also amended once during the prior fiscal year. For the year ended June 30, 2015, actual revenues were over the amended budget amount by $36,783 (or 3.65%). For the year ended June 30, 2014, actual revenues were over the final budget by $65,045 (or 6.41%). For the year ended June 30, 2015, actual expenses were under the final budget by $45,990 (or 4.19%). For the year ended June 30, 2014, actual expenses were under the final budget by $114,128 (or 10.83%). ECONOMIC FACTORS AND NEXT YEAR’S BUDGETS AND RATES License and firm permit fees, the Board’s primary sources of revenue, are reviewed annually and set at appropriate levels based on the Board’s financial position and anticipated needs. The Board’s appointed officials considered the following factors and indicators when setting next year’s budget:

The total number of licensees and registrants has been relatively stable over recent years, gradually increasing year to year. National forecasts of the volume of new licensee applications not keeping up with “baby boomer” retirements has not materialized in our state, and population outflows due to Hurricane Katrina and the 2008 recession appear to have stabilized. It is anticipated that the total number of licensees and registrants will continue to trend slightly upwards.

State Board of Certified Public Accountants of Louisiana Management’s Discussion and Analysis

10

License and annual renewal fees are monitored closely by the Board in order to balance its responsibilities as a regulator with its interest in keeping fees at reasonable levels in relation to operating costs.

Enforcement of statutes and rules is a significant function of the Board, and having the necessary resources available to investigate cases as they arise as well as having the technology and personnel to monitor those cases effectively is crucial.

The cost of other postemployment benefits (OPEB) are reported in annual actuarial reports, covering all state agencies, which is prepared and issued by an actuary retained by the state of Louisiana to estimate these costs under the applicable actuarial methods. The expense and accrued liability relates to the obligation to pay the employer share of post-retirement premiums of employees enrolled in the state health plan (OGB) at the time of retirement from state service. The Board annually monitors the OPEB costs when budgeting for fee considerations.

The cost of pension benefits was and will be reported in annual actuarial reports, covering all state agencies, which is prepared and issued by an actuary retained by the state of Louisiana to estimate these costs under the applicable actuarial methods. The expense and accrued liability related to the obligation, in excess of the actual cash payments expensed monthly, of the employer’s share of vested retirement benefits of employees retiring from state service will be recorded annually. The Board will monitor these costs when budgeting for fee considerations also.

The Board expects that next year’s revenues will be lower than this fiscal year’s actual revenues while expenses will be higher based on the following:

Licensee and firm permit revenues are expected to decrease by less than 3% in the upcoming year as compared to this fiscal year’s actual. The new fiscal year is a Continuing Professional Education (CPE) Reporting year in which it is expected that there will be an increase in active licensees changing their status to inactive (CPE exempt), which would result in less revenue.

Enforcement activities vary from year to year; therefore, both revenues and costs from those activities fluctuate. Conservative estimates expect that enforcement revenue will be about 30% lower in the coming year, while expenses are predicted to be higher. The Board will monitor this activity for changes throughout the year.

Retirement and insurance costs continue to rise as the employer contribution rates for both LASERS and health insurance premiums increase annually.

Upgrades in hardware were made this year, and continued investments in software and better technology are needed to meet the demands of recordkeeping, online

State Board of Certified Public Accountants of Louisiana Management’s Discussion and Analysis

11

renewals, enforcement, and information dissemination. Significant expenditures could be required to make these technology changes to provide better accountability, transparency, and greater efficiency.

CONTACTING THE BOARD’S MANAGEMENT This financial report is designed to provide our citizens, taxpayers, licensees, registrants, examination candidates, individuals and organizations served by CPAs, and other users with a general overview of the Board’s finances and to show the Board’s accountability for the money it receives. If you have questions about this report or need additional financial information, contact the Board’s executive director at 601 Poydras Street, Suite 1770, New Orleans, Louisiana, 70130.

12

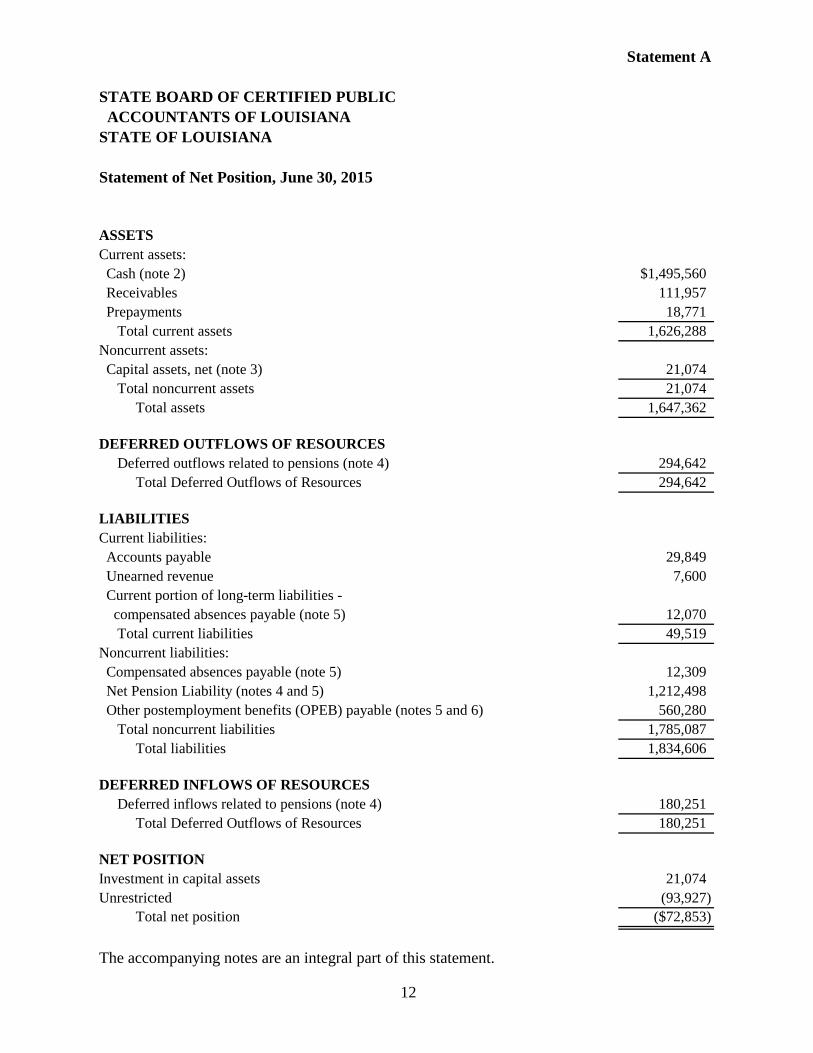

Statement A

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANASTATE OF LOUISIANA

Statement of Net Position, June 30, 2015

ASSETSCurrent assets: Cash (note 2) $1,495,560 Receivables 111,957 Prepayments 18,771 Total current assets 1,626,288Noncurrent assets: Capital assets, net (note 3) 21,074 Total noncurrent assets 21,074 Total assets 1,647,362

DEFERRED OUTFLOWS OF RESOURCES Deferred outflows related to pensions (note 4) 294,642 Total Deferred Outflows of Resources 294,642

LIABILITIESCurrent liabilities: Accounts payable 29,849 Unearned revenue 7,600 Current portion of long-term liabilities - compensated absences payable (note 5) 12,070 Total current liabilities 49,519Noncurrent liabilities: Compensated absences payable (note 5) 12,309 Net Pension Liability (notes 4 and 5) 1,212,498 Other postemployment benefits (OPEB) payable (notes 5 and 6) 560,280 Total noncurrent liabilities 1,785,087 Total liabilities 1,834,606

DEFERRED INFLOWS OF RESOURCES Deferred inflows related to pensions (note 4) 180,251 Total Deferred Outflows of Resources 180,251

NET POSITIONInvestment in capital assets 21,074Unrestricted (93,927) Total net position ($72,853)

The accompanying notes are an integral part of this statement.

13

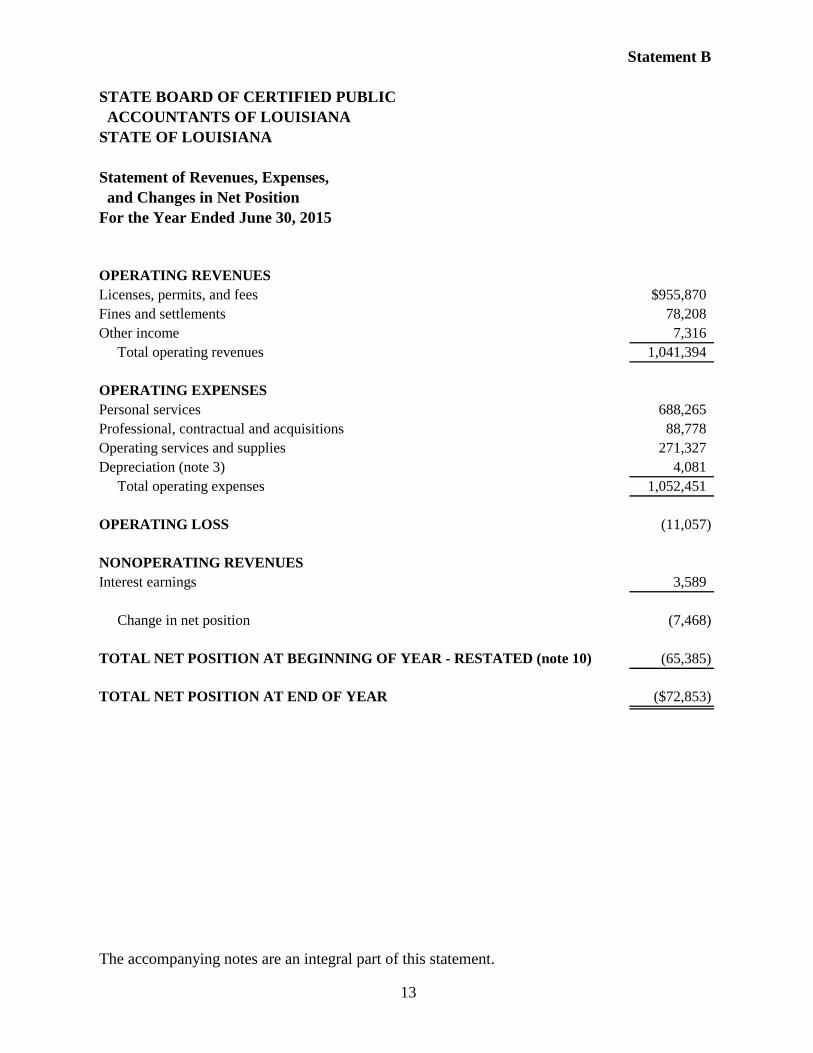

Statement B

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANASTATE OF LOUISIANA

Statement of Revenues, Expenses, and Changes in Net PositionFor the Year Ended June 30, 2015

OPERATING REVENUESLicenses, permits, and fees $955,870Fines and settlements 78,208Other income 7,316 Total operating revenues 1,041,394

OPERATING EXPENSESPersonal services 688,265Professional, contractual and acquisitions 88,778Operating services and supplies 271,327Depreciation (note 3) 4,081 Total operating expenses 1,052,451

OPERATING LOSS (11,057)

NONOPERATING REVENUESInterest earnings 3,589

Change in net position (7,468)

TOTAL NET POSITION AT BEGINNING OF YEAR - RESTATED (note 10) (65,385)

TOTAL NET POSITION AT END OF YEAR ($72,853)

The accompanying notes are an integral part of this statement.

14

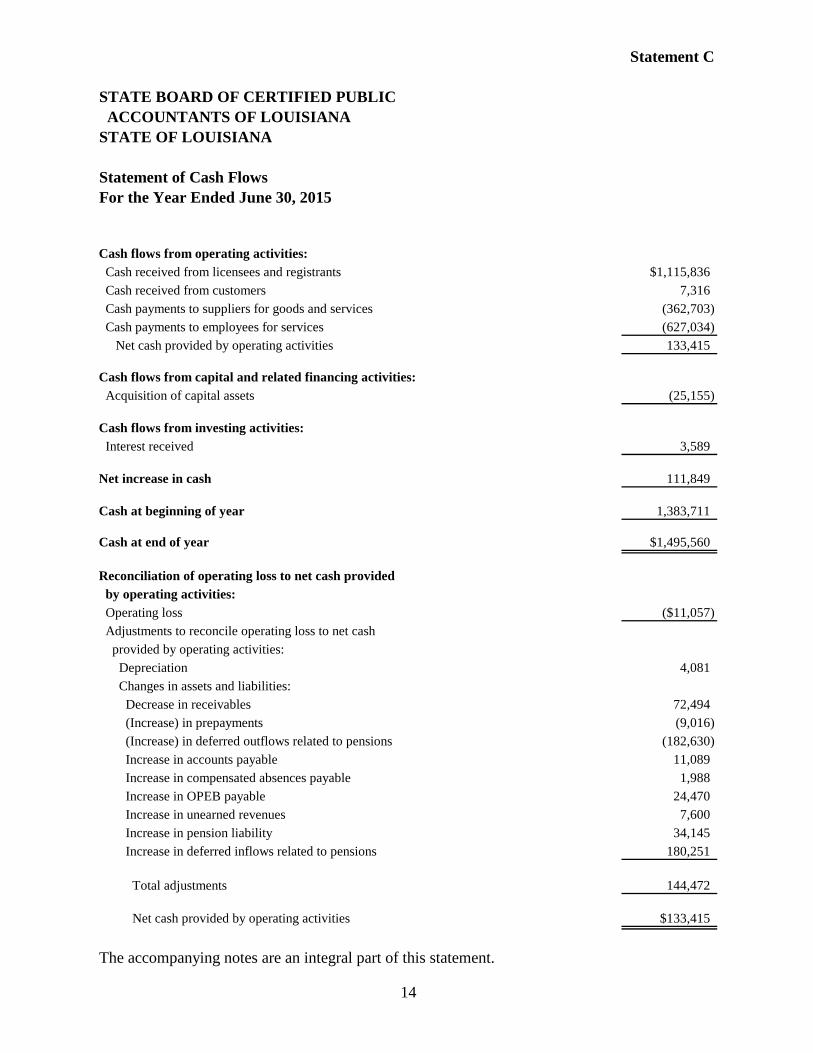

Statement C

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANASTATE OF LOUISIANA

Statement of Cash FlowsFor the Year Ended June 30, 2015

Cash flows from operating activities: Cash received from licensees and registrants $1,115,836 Cash received from customers 7,316 Cash payments to suppliers for goods and services (362,703) Cash payments to employees for services (627,034) Net cash provided by operating activities 133,415

Cash flows from capital and related financing activities: Acquisition of capital assets (25,155)

Cash flows from investing activities: Interest received 3,589

Net increase in cash 111,849

Cash at beginning of year 1,383,711

Cash at end of year $1,495,560

Reconciliation of operating loss to net cash provided by operating activities: Operating loss ($11,057) Adjustments to reconcile operating loss to net cash provided by operating activities: Depreciation 4,081 Changes in assets and liabilities: Decrease in receivables 72,494 (Increase) in prepayments (9,016) (Increase) in deferred outflows related to pensions (182,630) Increase in accounts payable 11,089 Increase in compensated absences payable 1,988 Increase in OPEB payable 24,470 Increase in unearned revenues 7,600 Increase in pension liability 34,145 Increase in deferred inflows related to pensions 180,251

Total adjustments 144,472

Net cash provided by operating activities $133,415

The accompanying notes are an integral part of this statement.

15

NOTES TO THE FINANCIAL STATEMENTS

INTRODUCTION The State Board of Certified Public Accountants of Louisiana (Board), a component unit of the state of Louisiana, was created by the Louisiana Legislature in 1908 and is established under the provisions of Louisiana Revised Statute (R.S.) 37:74. The Board is a licensing agency of the state of Louisiana. Effective July 1, 2001, the Board was among those transferred from the Department of Economic Development to the Office of the Governor by the legislature. The Board’s enabling legislation, the Louisiana Accountancy Act, is comprised by R.S. 37:71 et seq. The Board is composed of seven members who are appointed by the governor — five from designated geographic areas and two at-large. The Board acts in Louisiana’s public interest to promote the reliability of public accounting and financial reporting. The Board is charged with the responsibility of regulating the practice of certified public accountants (CPA) and firms in the state by enforcing the Accountancy Act, promulgating and enforcing rules of conduct, administering examinations of CPA candidates, and issuing and renewing licenses to practice as a CPA or CPA firm. Operations of the Board are funded through self-generated revenues primarily derived from fees for the issuance, application, and annual renewal of CPA certificates and licenses. The Board has nine full-time authorized employee positions. As of June 30, 2015, there were 7,419 active (licensed) and 3,018 inactive (unlicensed) certified public accountants and 2,192 CPA firms with licenses in Louisiana. 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A. BASIS OF PRESENTATION The Governmental Accounting Standards Board (GASB) is the accepted standard-setting body for establishing governmental accounting principles and reporting standards. These principles are found in the Codification of Governmental Accounting and Financial Reporting Standards, published by GASB. The accompanying financial statements have been prepared on the full accrual basis in accordance with such principles. B. REPORTING ENTITY GASB Codification Section 2100 has defined the governmental reporting entity to be the state of Louisiana. The Board is considered a component unit (enterprise fund) of the state of Louisiana because the state has financial accountability over the Board in that the governor appoints the board members. The accompanying financial statements present information only as to the transactions and activities of the Board. Annually, the state of Louisiana issues a comprehensive financial report, which includes the activity contained in the accompanying financial statements. The Louisiana Legislative Auditor audits the basic financial statements of the state of Louisiana.

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

16

C. BASIS OF ACCOUNTING For financial reporting purposes, the Board is considered a special-purpose government engaged only in business-type activities. All activities of the Board are accounted for within a single proprietary (enterprise) fund. Basis of accounting refers to when revenues and expenses are recognized in the accounts and reported in the financial statements. Basis of accounting relates to the timing of the measurements made, regardless of the measurement focus applied. The transactions of the Board are accounted for on a flow of economic resources measurement focus. With this measurement focus, all assets and all liabilities associated with the operations are included on the Statement of Net Position. Under the full accrual basis, revenues are recognized in the accounting period when they are earned, and expenses are recognized when the related liability is incurred. Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and/or producing and delivering goods in connection with a proprietary fund’s principal ongoing operations. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses.

D. BUDGET PRACTICES The Board prepares its budget in accordance with the Louisiana Licensing Agency Budget Act, R.S. 39:1331-1342. The budget is prepared on a modified accrual basis of accounting. Although budget amounts lapse at year-end, the Board retains its unexpended net position to fund expenses of the succeeding year.

E. CASH Cash consists of the amounts in interest-bearing demand deposit accounts, cash on hand, and petty cash. Under state law, the Board may deposit funds within a fiscal agent bank organized under the laws of the state of Louisiana, the laws of any other state in the Union, or the laws of the United States. F. CAPITAL ASSETS Capital assets consist of office and computer equipment and are capitalized at historical cost. The Board follows the Louisiana Property Assistance Agency and Office of Statewide Reporting and Accounting Policy guidance for capitalizing and reporting equipment. Only equipment valued at or more than $5,000 and computer software valued at or more than $1,000,000 are capitalized and depreciated for financial statement purposes. Depreciation for financial reporting is computed by the straight-line method over an asset’s useful life, which is five years for computer equipment and six years for

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

17

office equipment. Equipment, furniture, and software acquisitions with costs less than the above thresholds are charged as an administrative expense. G. NONCURRENT LIABILITIES

Noncurrent liabilities at June 30, 2015, include compensated absences, other postemployment benefits (OPEB), and net pension liability. A summary of changes in long-term obligations is presented in note 5. For purposes of measuring the net pension liability, deferred outflows of resources and deferred inflows of resources related to pensions, and pension expense, information about the fiduciary net position of the Louisiana State Employees’ Retirement System (LASERS) and the Teachers’ Retirement System of Louisiana (TRSL), and additions to/deductions from each systems’ fiduciary net position have been determined on the same basis as they are reported by the system. For this purpose, benefit payments (including refunds of employee contributions) are recognized when due and payable in accordance with the benefit terms. Investments are reported at fair value.

H. EMPLOYEE COMPENSATED ABSENCES Employees of the Board earn and accumulate annual and sick leave at varying rates depending on their years of service. The amount of annual and sick leave that may be accumulated by each employee is unlimited. Upon termination, employees or their heirs are compensated for up to 300 hours of unused annual leave at the employee’s hourly rate of pay at the time of termination. Upon retirement, unused annual leave in excess of 300 hours plus unused sick leave is used to compute retirement benefits. Employees who are considered having nonexempt status according to the guidelines contained in the Fair Labor Standards Act may be paid for compensatory leave (K-time) earned. Upon termination or transfer, an employee will be paid for any time and one-half compensatory leave earned and may or may not be paid for any straight hour-for-hour compensatory leave earned. Compensation paid will be based on the employee’s hourly rate of pay at termination or transfer. The cost of leave privileges, computed in accordance with GASB Codification Section C60, is recognized as an expense and a liability in the financial statements in the period in which the leave is earned. I. NET POSITION Net position comprises the various net earnings from operations, nonoperating revenues, and expenses. The Board’s net position is classified in the following components: Investment in capital assets consists of all capital assets, net of accumulated

depreciation.

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

18

Unrestricted net position consists of all assets not included in the other category previously mentioned. Unrestricted net position represents resources derived from the Board’s licenses, permits, and fees and is used for transactions related to the Board’s general operations. Unrestricted net position may be used at the discretion of the Board.

J. USE OF ESTIMATES The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

K. ADOPTION OF NEW ACCOUNTING PRINCIPLE

For the year ended June 30, 2015, the following statements were implemented: GASB Statement no. 68, Accounting and Financial Reporting for Pensions – an amendment of GASB Statement No. 27, and GASB Statement No. 71, Pension Transition for Contributions Made Subsequent to the Measurement Date – an amendment of GASB Statement No. 68. These statements changed the accounting and financial reporting for pensions that are provided to the employees of state and local governmental employers through pension plans that are administered through trusts. The cumulative effect of applying these statements is reported as a restatement of beginning net position for fiscal year 2015 (see note 10). The restatement of all prior-year deferred outflows and inflows was not practical, so only deferred outflows related to fiscal year 2014 contributions were recorded at implementation.

2. CASH The Board has cash (book balance) totaling $1,495,560 at June 30, 2015, which consists of the following:

Demand deposits $1,487,860Cash on hand 7,600Petty cash 100 Total $1,495,560

Custodial credit risk is the risk that in the event of a bank failure the Board’s deposits may not be recovered. Under state law, the Board’s deposits must be secured by federal deposit insurance or similar federal security or the pledge of securities owned by the fiscal agent bank. The fair market value of the pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent. These securities are held in the name of the Board or the pledging bank by a holding or custodial bank that is mutually acceptable to both parties. As of June 30, 2015, the Board’s total deposits (collected bank balances) was $1,583,054, which

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

19

was secured from risk by federal deposit insurance plus pledged securities held in the Board’s name. 3. CAPITAL ASSETS A summary of changes in capital assets follows:

Beginning EndingBalance Balance

July 1, 2014 Additions Deletions June 30, 2015

Equipment $33,332 $25,155 $58,487Less accumulated depreciation (33,332) (4,081) (37,413)

Capital assets, net NONE $21,074 NONE $21,074

4. PENSION PLAN The Board is a participating employer in two statewide, public employee retirement systems, LASERS and TRSL. Both systems have separate boards of trustees and administer cost-sharing, multiple-employer defined benefit pension plans, including classes of employees with different benefits and contribution rates (sub-plans). Article X, Section 29(F) of the Louisiana Constitution of 1974 assigns the authority to establish and amend benefit provisions of all sub-plans administered by these systems to the state legislature. Each system issues a public report that includes financial statements and required supplementary information. Copies of these reports for LASERS and TRSL may be obtained at www.lasersonline.org and www.trsl.org, respectively. TRSL also administers an optional retirement plan (ORP), which was created by R.S. 11:921-931 for academic and administrative employees of public institutions of higher education and is considered a defined contribution plan. A portion of the employer contributions for ORP plan members is dedicated to the unfunded accrued liability of the TRSL defined benefit plan. General Information about the Pension Plans Plan Descriptions/Benefits Provided All full-time Board employees are eligible to participate in LASERS unless an election is made to continue as a member of another retirement system, such as TRSL, for which they remain eligible for membership. LASERS - LASERS administers a plan to provide retirement, disability, and survivor’s benefits to eligible state employees and their beneficiaries as defined in R.S. 11:411-414. The age and years of creditable service (service) required in order for a member to receive retirement benefits are established by R.S. 11:441 and vary depending on the member’s hire date, employer, and job classification. Act 992 of the 2010 Regular Legislative Session closed existing sub-plans for

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

20

members hired before January 1, 2011, and created new sub-plans for regular members, hazardous duty members, and judges. The substantial majority of members may retire with full benefits at any age upon completing 30 years of service and at age 60 upon completing 5-10 years of service. Additionally, members may choose to retire with 20 years of service at any age, with an actuarially reduced benefit. Eligibility for retirement benefits and the computation of retirement benefits are provided for in R.S. 11:444. The basic annual retirement benefit for members is equal to a percentage (between 2.5% and 3.5%) of average compensation multiplied by the number of years of service, generally not to exceed 100% of average compensation. Average compensation is defined as the member’s average annual earned compensation for the highest 36 consecutive months of employment for members employed prior to July 1, 2006, or highest 60 consecutive months of employment for members employed after that date. A member leaving service before attaining minimum retirement but after completing certain minimum service requirements, generally 10 years, becomes eligible for a benefit provided the member lives to the minimum service retirement age and does not withdraw the accumulated contributions. Eligibility requirements and benefit computations for disability benefits are provided for in R.S. 11:461. All members with 10 or more years of service or members aged 60 or older regardless of date of hire who become disabled may receive a maximum disability benefit equivalent to the regular retirement formula without reduction by reason of age. Hazardous duty personnel who become disabled in the line of duty will receive a disability benefit equal to 75% of final average compensation. Provisions for survivor’s benefits are provided for in R.S. 11:471-478. Under these statutes, the deceased member who was in state service at the time of death must have a minimum of five years of service, at least two of which were earned immediately prior to death, or who had a minimum of 20 years of service regardless of when earned in order for a benefit to be paid to a minor or handicapped child. Benefits are payable to an unmarried child until age 18 or age 23 if the child remains a full-time student. The minimum service requirement is 10 years for a surviving spouse with no minor children, and benefits are to be paid for life to the spouse or qualified handicapped child. LASERS has established a Deferred Retirement Option Plan (DROP). When members enter DROP, their status changes from active member to retiree even though they continue to work and draw their salary for a period up to three years. The election is irrevocable once participation begins. During participation, benefits otherwise payable are fixed and deposited in an individual DROP account. Upon leaving DROP, members must choose among available alternatives for the distribution of benefits that have accumulated in their DROP accounts. TRSL - TRSL administers a plan to provide retirement, disability, and survivor benefits to employees who meet the legal definition of a “teacher” as provided for in R.S 11:701. Eligibility for retirement benefits and the calculation of retirement benefits are provided for in R.S. 11:761. Statutory changes closed existing, and created new, sub-plans for members hired on or after January 1, 2011.

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

21

Most members are eligible to receive retirement benefits (1) at the age of 60 with five years of service, (2) at the age of 55 with at least 25 years of service, or (3) at any age with at least 30 years of service. Retirement benefits are calculated by applying a percentage ranging from 2% to 3% of final average salary multiplied by years of service. Average compensation is defined as the member’s average annual earned compensation for the highest 36 consecutive months of employment for members employed prior to July 1, 2011, or highest 60 consecutive months of employment for members employed after that date. Under R.S. 11:778 and 11:779, members who have suffered a qualified disability are eligible for disability benefits if employed prior to January 1, 2011, and attained at least five years of service or if employed on or after January 1, 2011, and attained at least 10 years of service. Members employed prior to January 1, 2011, receive disability benefits equal to 2.5% of average compensation multiplied by the years of service, but not more than 50% of average compensation subject to statutory minimums. Members employed on or after January 1, 2011, receive disability benefits equivalent to the regular retirement formula without reduction by reason of age. Survivor benefits are provided for in R.S. 11:762. In order for survivor benefits to be paid, the deceased member must have been in state service at the time of death and must have a minimum of five years of service, at least two of which were earned immediately prior to death, or must have had a minimum of 20 years of service regardless of when earned in order for a benefit to be paid to a minor or handicapped child. Survivor benefits are equal to 50% of the benefit to which the member would have been entitled if retired on the date of death using a factor of 2.5% regardless of years of service or age or $600 per month, whichever is greater. Benefits are payable to an unmarried child until age 18, or age 23 if the child remains a full-time student. The minimum service credit requirement is 10 years for a surviving spouse with no minor children, and benefits are to be paid for life to the spouse or a qualified handicapped child. TRSL has established a DROP plan. When members enter DROP, their status changes from active member to retiree even though they continue to work and draw their salary for a period up to three years. The election is irrevocable once participation begins. During participation, benefits otherwise payable are fixed and deposited in an individual DROP account. Upon leaving DROP, new members must choose among available alternatives for the distribution of benefits that have accumulated in their DROP accounts. Cost of Living Adjustments As fully described in Title 11 of the Louisiana Revised Statutes, LASERS and TRSL allow for the payment of cost of living adjustments, or COLAs, that are funded through investment earnings when recommended by the board of trustees and approved by the legislature. These ad hoc COLAs are not considered to be substantively automatic. Contributions Article X, Section 29(E)(2)(a) of the Louisiana Constitution of 1974 assigns the legislature the authority to determine employee contributions. Employer contributions are actuarially

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

22

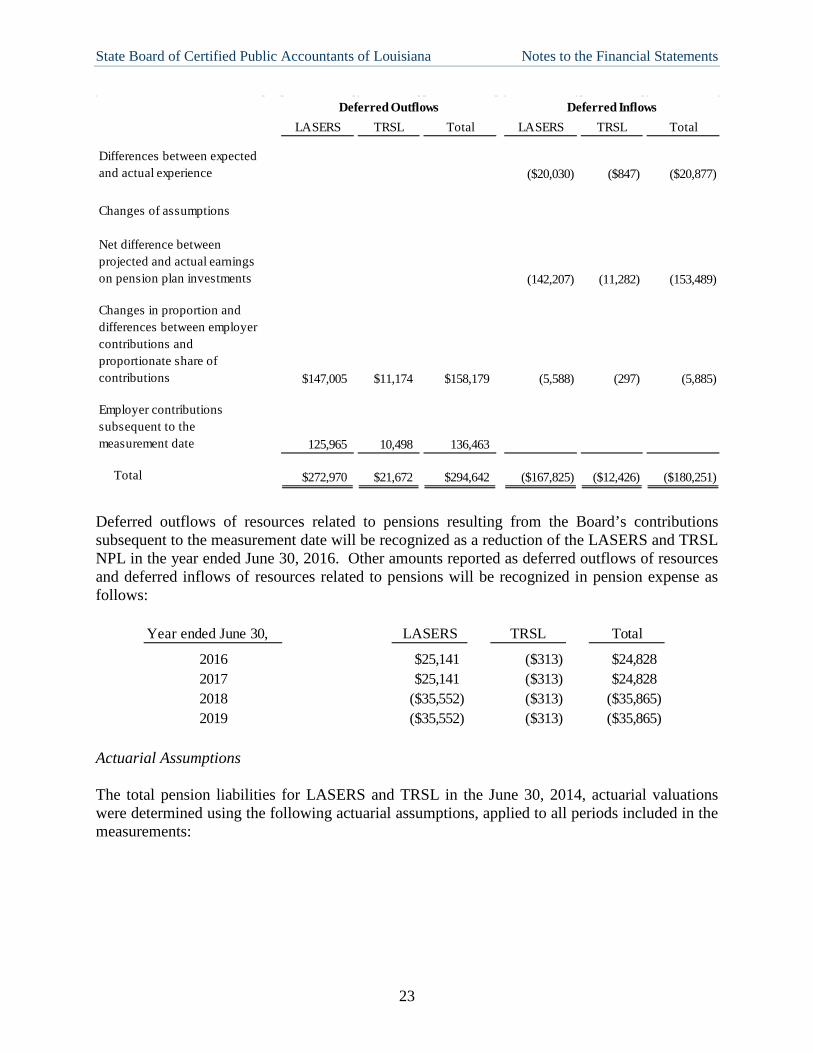

determined using statutorily-established methods on an annual basis and are constitutionally-required to cover the employer’s portion of the normal cost and provide for the amortization of the unfunded accrued liability. Employer contributions are adopted by the legislature annually upon recommendation of the Public Retirement Systems’ Actuarial Committee. For those members participating in the TRSL defined contribution ORP, a portion of the employer contributions are used to fund the TRSL defined benefit plans’ unfunded accrual liability. Employer contributions to LASERS for fiscal year 2015 were $125,965, with active member contributions ranging from 7.5% to 8%, and employer contributions of 37%. Employer defined benefit plan contributions to TRSL for fiscal year 2015 were $10,498, with active member contributions of 8% and employer contributions of 28%. Pension Liabilities, Pension Expense, and Deferred Outflows of Resources and Deferred Inflows of Resources Related to Pensions At June 30, 2015, the Board reported liabilities of $1,124,083 and $88,415 under LASERS and TRSL, respectively, for its proportionate share of the Net Pension Liability (NPL). The NPL for LASERS and TRSL was measured as of June 30, 2014, and the total pension liabilities used to calculate the NPL were determined by actuarial valuations as of that date. The Board’s proportions of the NPL were based on projections of the Board’s long-term share of contributions to the pension plans relative to the projected contribution of all participating employers, actuarially determined. As of June 30, 2014, the most recent measurement date, the Board’s proportions and the changes in proportion from the prior measurement date were 0.01798%, or an increase of 0.00303% for LASERS and 0.00087%, or an increase of 0.00012% for TRSL. For the year ended June 30, 2015, the Board recognized a total pension expense of $168,477, or $158,058 and $10,419 for LASERS and TRSL, respectively. The Board reported deferred outflows of resources and deferred inflows of resources related to pensions from the following sources:

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

23

Deferred Outflows Deferred InflowsLASERS TRSL Total LASERS TRSL Total

Differences between expected and actual experience ($20,030) ($847) ($20,877)

Changes of assumptions

Net difference between projected and actual earnings on pension plan investments (142,207) (11,282) (153,489)

Changes in proportion and differences between employer contributions and proportionate share of contributions $147,005 $11,174 $158,179 (5,588) (297) (5,885)

Employer contributions subsequent to the measurement date 125,965 10,498 136,463

Total $272,970 $21,672 $294,642 ($167,825) ($12,426) ($180,251)

Deferred outflows of resources related to pensions resulting from the Board’s contributions subsequent to the measurement date will be recognized as a reduction of the LASERS and TRSL NPL in the year ended June 30, 2016. Other amounts reported as deferred outflows of resources and deferred inflows of resources related to pensions will be recognized in pension expense as follows:

Year ended June 30, LASERS TRSL Total

2016 $25,141 ($313) $24,8282017 $25,141 ($313) $24,8282018 ($35,552) ($313) ($35,865)2019 ($35,552) ($313) ($35,865)

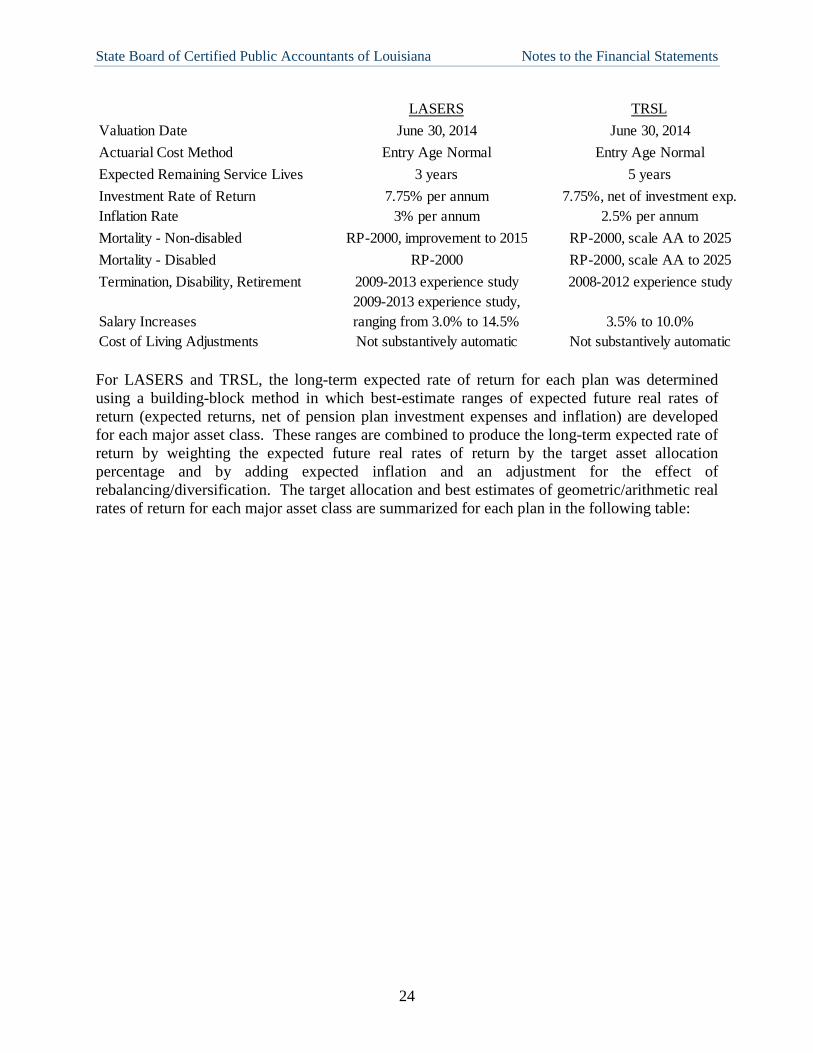

Actuarial Assumptions The total pension liabilities for LASERS and TRSL in the June 30, 2014, actuarial valuations were determined using the following actuarial assumptions, applied to all periods included in the measurements:

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

24

LASERS TRSLValuation Date June 30, 2014 June 30, 2014Actuarial Cost Method Entry Age Normal Entry Age NormalExpected Remaining Service Lives 3 years 5 yearsInvestment Rate of Return 7.75% per annum 7.75%, net of investment exp.Inflation Rate 3% per annum 2.5% per annumMortality - Non-disabled RP-2000, improvement to 2015 RP-2000, scale AA to 2025Mortality - Disabled RP-2000 RP-2000, scale AA to 2025Termination, Disability, Retirement 2009-2013 experience study 2008-2012 experience study

Salary Increases2009-2013 experience study, ranging from 3.0% to 14.5% 3.5% to 10.0%

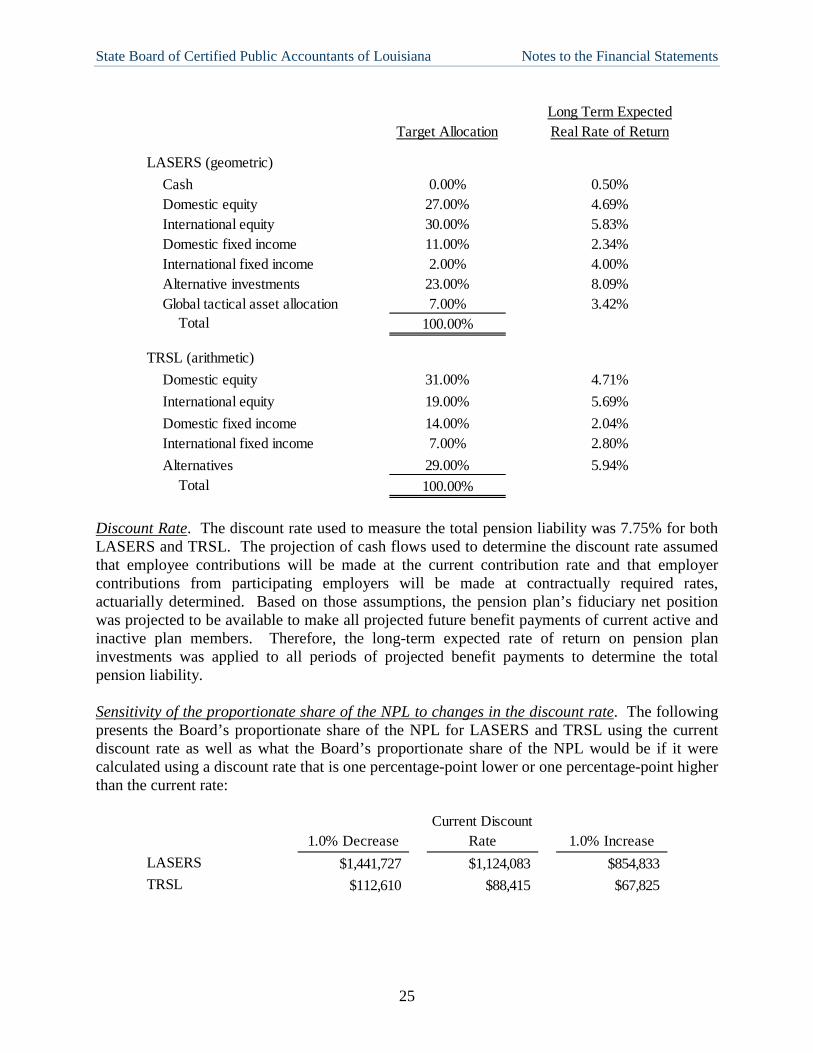

Cost of Living Adjustments Not substantively automatic Not substantively automatic For LASERS and TRSL, the long-term expected rate of return for each plan was determined using a building-block method in which best-estimate ranges of expected future real rates of return (expected returns, net of pension plan investment expenses and inflation) are developed for each major asset class. These ranges are combined to produce the long-term expected rate of return by weighting the expected future real rates of return by the target asset allocation percentage and by adding expected inflation and an adjustment for the effect of rebalancing/diversification. The target allocation and best estimates of geometric/arithmetic real rates of return for each major asset class are summarized for each plan in the following table:

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

25

Target AllocationLong Term ExpectedReal Rate of Return

LASERS (geometric) Cash 0.00% 0.50% Domestic equity 27.00% 4.69% International equity 30.00% 5.83% Domestic fixed income 11.00% 2.34% International fixed income 2.00% 4.00% Alternative investments 23.00% 8.09% Global tactical asset allocation 7.00% 3.42% Total 100.00%

TRSL (arithmetic) Domestic equity 31.00% 4.71% International equity 19.00% 5.69% Domestic fixed income 14.00% 2.04% International fixed income 7.00% 2.80% Alternatives 29.00% 5.94% Total 100.00%

Discount Rate. The discount rate used to measure the total pension liability was 7.75% for both LASERS and TRSL. The projection of cash flows used to determine the discount rate assumed that employee contributions will be made at the current contribution rate and that employer contributions from participating employers will be made at contractually required rates, actuarially determined. Based on those assumptions, the pension plan’s fiduciary net position was projected to be available to make all projected future benefit payments of current active and inactive plan members. Therefore, the long-term expected rate of return on pension plan investments was applied to all periods of projected benefit payments to determine the total pension liability. Sensitivity of the proportionate share of the NPL to changes in the discount rate. The following presents the Board’s proportionate share of the NPL for LASERS and TRSL using the current discount rate as well as what the Board’s proportionate share of the NPL would be if it were calculated using a discount rate that is one percentage-point lower or one percentage-point higher than the current rate:

1.0% DecreaseCurrent Discount

Rate 1.0% IncreaseLASERS $1,441,727 $1,124,083 $854,833TRSL $112,610 $88,415 $67,825

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

26

Pension plan fiduciary net position. Detailed information about LASERS and TRSL fiduciary net position is available in the separately-issued financial reports at www.lasersonline.org and www.trsl.org, respectively. Payables to the Pension Plan. At June 30, 2015, the Board had $12,300 and $0 in payables to LASERS and TRSL, respectively, for the June 2015 employee and employer legally-required contributions. 5. CHANGES IN LONG-TERM LIABILITIES (CURRENT AND NONCURRENT PORTION) The following is a summary of long-term liability transactions of the Board for the year ended June 30, 2015:

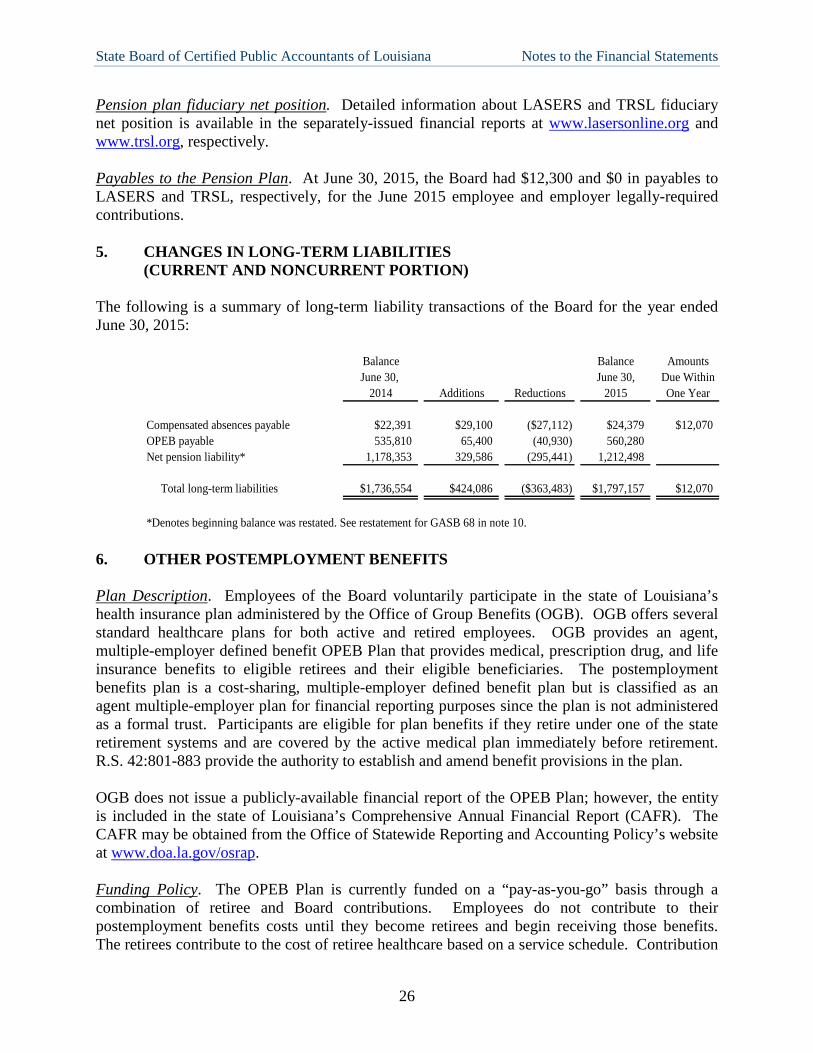

Balance Balance AmountsJune 30, June 30, Due Within

2014 Additions Reductions 2015 One Year

Compensated absences payable $22,391 $29,100 ($27,112) $24,379 $12,070OPEB payable 535,810 65,400 (40,930) 560,280Net pension liability* 1,178,353 329,586 (295,441) 1,212,498

Total long-term liabilities $1,736,554 $424,086 ($363,483) $1,797,157 $12,070

*Denotes beginning balance was restated. See restatement for GASB 68 in note 10.

6. OTHER POSTEMPLOYMENT BENEFITS Plan Description. Employees of the Board voluntarily participate in the state of Louisiana’s health insurance plan administered by the Office of Group Benefits (OGB). OGB offers several standard healthcare plans for both active and retired employees. OGB provides an agent, multiple-employer defined benefit OPEB Plan that provides medical, prescription drug, and life insurance benefits to eligible retirees and their eligible beneficiaries. The postemployment benefits plan is a cost-sharing, multiple-employer defined benefit plan but is classified as an agent multiple-employer plan for financial reporting purposes since the plan is not administered as a formal trust. Participants are eligible for plan benefits if they retire under one of the state retirement systems and are covered by the active medical plan immediately before retirement. R.S. 42:801-883 provide the authority to establish and amend benefit provisions in the plan. OGB does not issue a publicly-available financial report of the OPEB Plan; however, the entity is included in the state of Louisiana’s Comprehensive Annual Financial Report (CAFR). The CAFR may be obtained from the Office of Statewide Reporting and Accounting Policy’s website at www.doa.la.gov/osrap. Funding Policy. The OPEB Plan is currently funded on a “pay-as-you-go” basis through a combination of retiree and Board contributions. Employees do not contribute to their postemployment benefits costs until they become retirees and begin receiving those benefits. The retirees contribute to the cost of retiree healthcare based on a service schedule. Contribution

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

27

amounts vary depending on what healthcare provider is selected from the OPEB Plan and if the member has Medicare coverage. The contribution requirements of plan members and the Board are established and may be amended by R.S. 42:801-883. Employer contributions are based on plan premiums and the employer contribution percentage. This percentage is based on the date of participation in an OGB plan (before or after January 1, 2002) and employee years of service at retirement. Employees who begin participation or rejoin the plan before January 1, 2002, pay approximately 25% of the cost of coverage (except single retirees under age 65, who pay approximately 25% of the active employee cost). For those beginning participation or rejoining on or after January 1, 2002, the percentage of premiums contributed by the employer and employee is based on the following schedule:

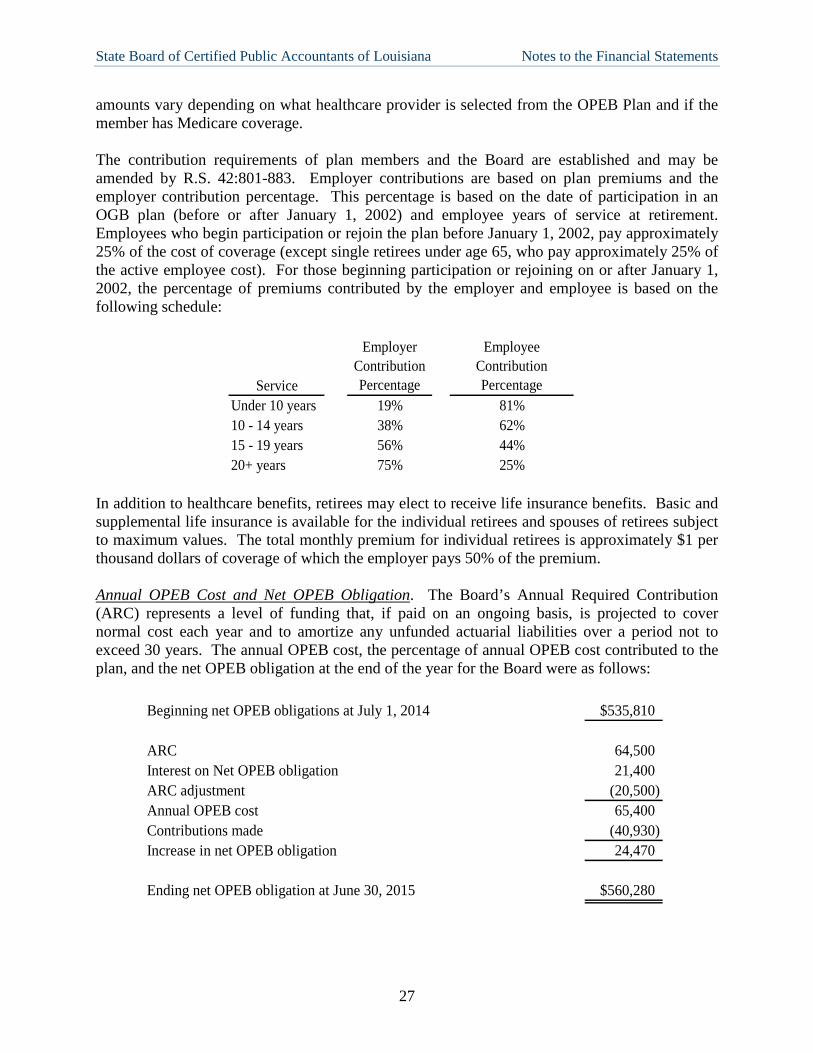

Service

Employer Contribution Percentage

Employee Contribution Percentage

Under 10 years 19% 81%10 - 14 years 38% 62%15 - 19 years 56% 44%20+ years 75% 25%

In addition to healthcare benefits, retirees may elect to receive life insurance benefits. Basic and supplemental life insurance is available for the individual retirees and spouses of retirees subject to maximum values. The total monthly premium for individual retirees is approximately $1 per thousand dollars of coverage of which the employer pays 50% of the premium. Annual OPEB Cost and Net OPEB Obligation. The Board’s Annual Required Contribution (ARC) represents a level of funding that, if paid on an ongoing basis, is projected to cover normal cost each year and to amortize any unfunded actuarial liabilities over a period not to exceed 30 years. The annual OPEB cost, the percentage of annual OPEB cost contributed to the plan, and the net OPEB obligation at the end of the year for the Board were as follows:

Beginning net OPEB obligations at July 1, 2014 $535,810

ARC 64,500Interest on Net OPEB obligation 21,400ARC adjustment (20,500)Annual OPEB cost 65,400Contributions made (40,930)Increase in net OPEB obligation 24,470

Ending net OPEB obligation at June 30, 2015 $560,280

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

28

The following table provides the Board’s annual OPEB cost, the percentage of annual OPEB cost contributed to the plan, and the net OPEB obligation for the last three fiscal years:

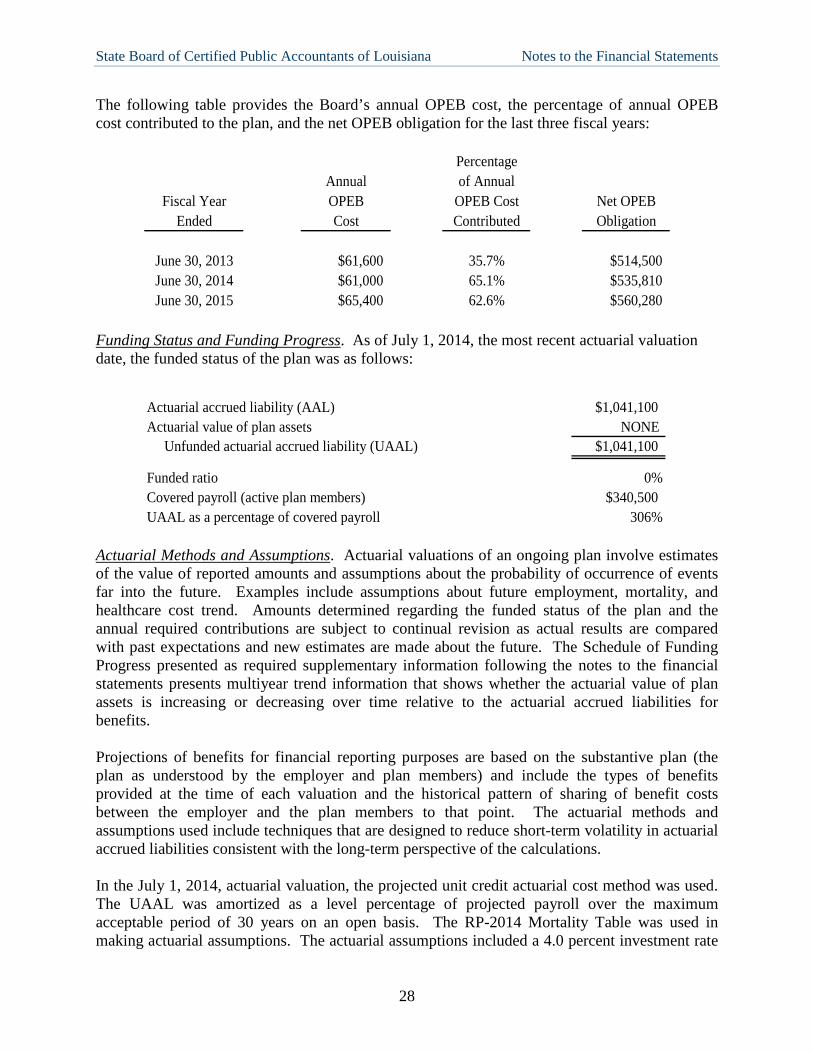

PercentageAnnual of Annual

Fiscal Year OPEB OPEB Cost Net OPEBEnded Cost Contributed Obligation

June 30, 2013 $61,600 35.7% $514,500June 30, 2014 $61,000 65.1% $535,810June 30, 2015 $65,400 62.6% $560,280

Funding Status and Funding Progress. As of July 1, 2014, the most recent actuarial valuation date, the funded status of the plan was as follows:

Actuarial accrued liability (AAL) $1,041,100Actuarial value of plan assets NONE Unfunded actuarial accrued liability (UAAL) $1,041,100

Funded ratio 0%Covered payroll (active plan members) $340,500UAAL as a percentage of covered payroll 306%

Actuarial Methods and Assumptions. Actuarial valuations of an ongoing plan involve estimates of the value of reported amounts and assumptions about the probability of occurrence of events far into the future. Examples include assumptions about future employment, mortality, and healthcare cost trend. Amounts determined regarding the funded status of the plan and the annual required contributions are subject to continual revision as actual results are compared with past expectations and new estimates are made about the future. The Schedule of Funding Progress presented as required supplementary information following the notes to the financial statements presents multiyear trend information that shows whether the actuarial value of plan assets is increasing or decreasing over time relative to the actuarial accrued liabilities for benefits. Projections of benefits for financial reporting purposes are based on the substantive plan (the plan as understood by the employer and plan members) and include the types of benefits provided at the time of each valuation and the historical pattern of sharing of benefit costs between the employer and the plan members to that point. The actuarial methods and assumptions used include techniques that are designed to reduce short-term volatility in actuarial accrued liabilities consistent with the long-term perspective of the calculations. In the July 1, 2014, actuarial valuation, the projected unit credit actuarial cost method was used. The UAAL was amortized as a level percentage of projected payroll over the maximum acceptable period of 30 years on an open basis. The RP-2014 Mortality Table was used in making actuarial assumptions. The actuarial assumptions included a 4.0 percent investment rate

State Board of Certified Public Accountants of Louisiana Notes to the Financial Statements

29

of return (discount rate). Retirement rate assumptions differ by employment group and date of plan participation. The health care cost trend rate assumption is used to project the cost of health care to future years. The valuation uses a health care cost trend rate of 8.0% and 7.0% for pre-Medicare and Medicare eligible employees, respectively, scaling down to ultimate rates of 4.5% per year. Assumptions also include payroll growth of 3%. 7. OPERATING LEASE The Board’s total rental and lease expense for June 30, 2015, was $90,757, which includes an operating lease for office space with a monthly rental of $5,342, currently in a five-year term extension of the amended lease that ends as of August 31, 2016. The Board has no capital leases. Future minimum operating lease payments under this operating lease for the years ending June 30 are as follows:

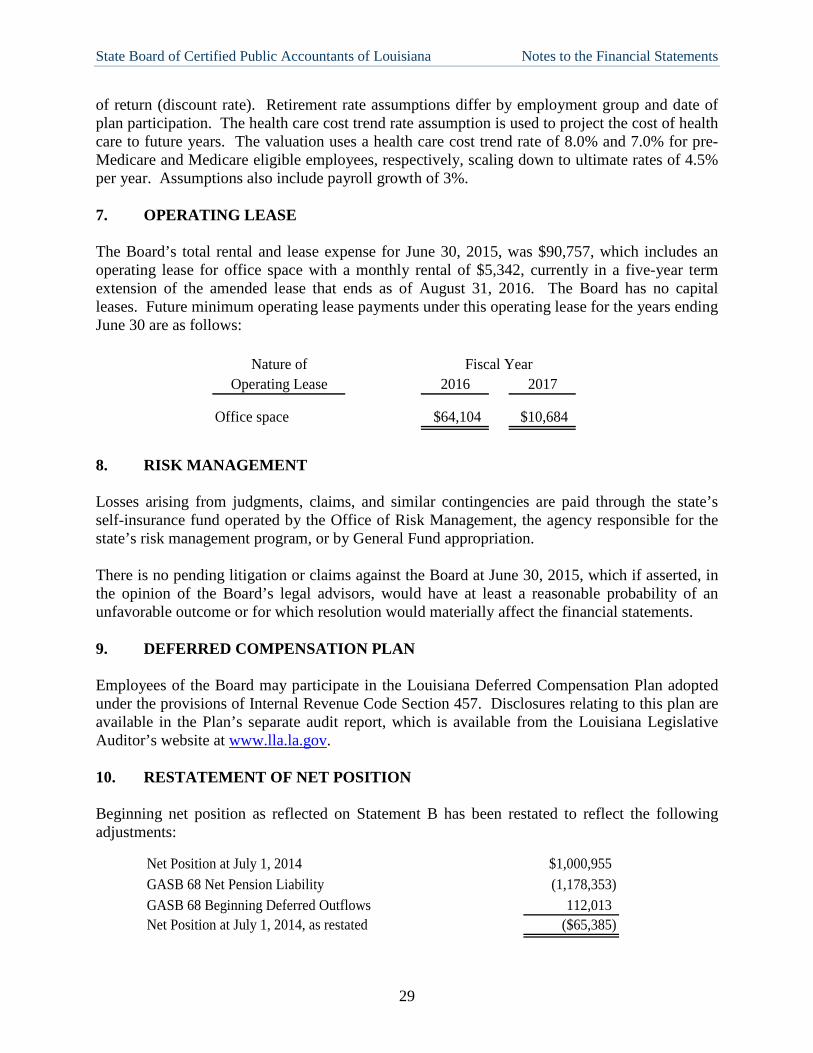

Nature of

Operating Lease 2016 2017

Office space $64,104 $10,684

Fiscal Year

8. RISK MANAGEMENT Losses arising from judgments, claims, and similar contingencies are paid through the state’s self-insurance fund operated by the Office of Risk Management, the agency responsible for the state’s risk management program, or by General Fund appropriation. There is no pending litigation or claims against the Board at June 30, 2015, which if asserted, in the opinion of the Board’s legal advisors, would have at least a reasonable probability of an unfavorable outcome or for which resolution would materially affect the financial statements. 9. DEFERRED COMPENSATION PLAN Employees of the Board may participate in the Louisiana Deferred Compensation Plan adopted under the provisions of Internal Revenue Code Section 457. Disclosures relating to this plan are available in the Plan’s separate audit report, which is available from the Louisiana Legislative Auditor’s website at www.lla.la.gov. 10. RESTATEMENT OF NET POSITION Beginning net position as reflected on Statement B has been restated to reflect the following adjustments:

Net Position at July 1, 2014 $1,000,955GASB 68 Net Pension Liability (1,178,353)GASB 68 Beginning Deferred Outflows 112,013Net Position at July 1, 2014, as restated ($65,385)

30

REQUIRED SUPPLEMENTARY INFORMATION

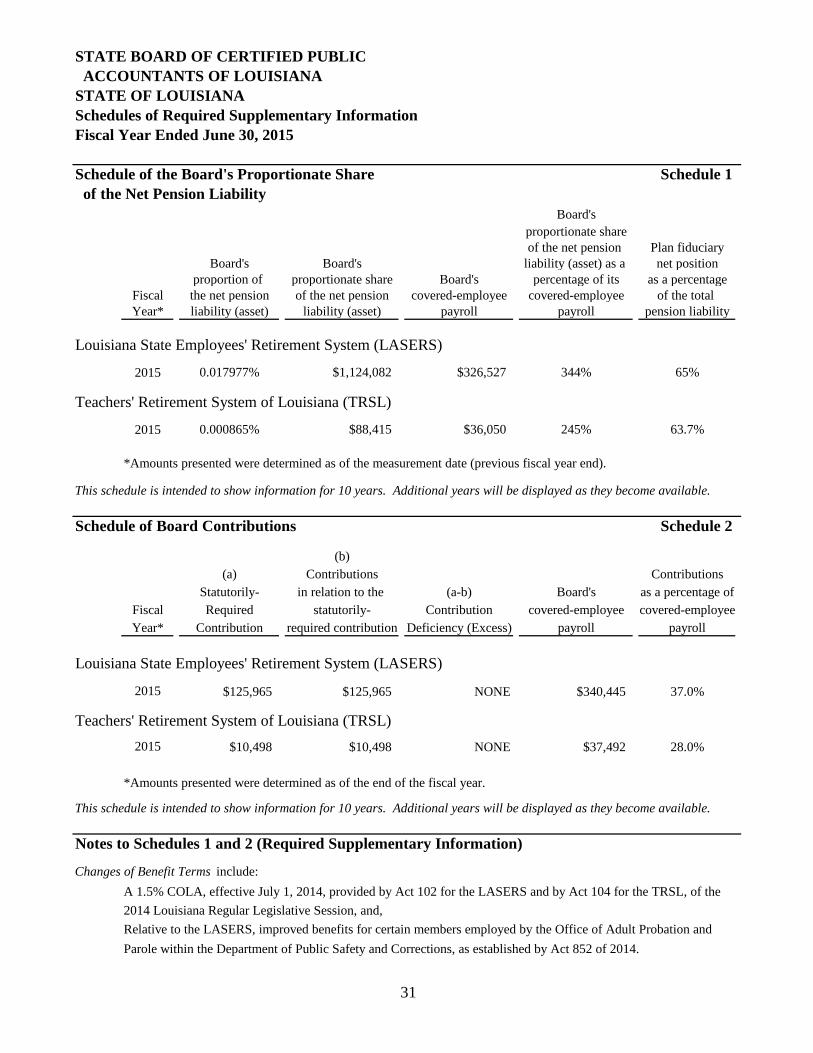

Schedule of the Board’s Proportionate Share of the Net Pension Liability

Schedule 1 presents the Board’s Net Pension Liability.

Schedule of Board Contributions

Schedule 2 presents the amount of contributions the Board made to the pension system.

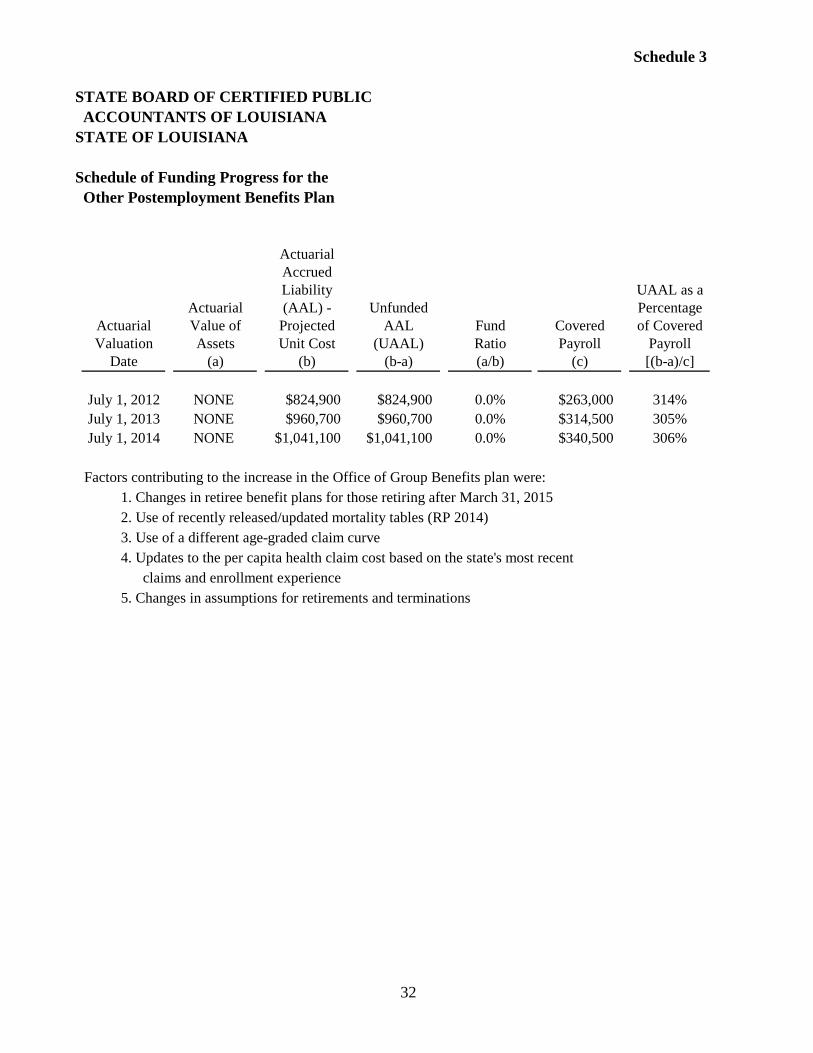

Schedule of Funding Progress for the Other Postemployment Benefits Plan

Schedule 3 presents certain specific data regarding the funding progress for the Other Postemployment Benefits Plan, including the unfunded actuarial accrued liability.

31

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANASTATE OF LOUISIANASchedules of Required Supplementary InformationFiscal Year Ended June 30, 2015

Schedule of the Board's Proportionate Share Schedule 1 of the Net Pension Liability

Board'sproportionate shareof the net pension Plan fiduciary

Board's Board's liability (asset) as a net positionproportion of proportionate share Board's percentage of its as a percentage

Fiscal the net pension of the net pension covered-employee covered-employee of the total Year* liability (asset) liability (asset) payroll payroll pension liability

Louisiana State Employees' Retirement System (LASERS)

2015 0.017977% $1,124,082 $326,527 344% 65%

Teachers' Retirement System of Louisiana (TRSL)

2015 0.000865% $88,415 $36,050 245% 63.7%

*Amounts presented were determined as of the measurement date (previous fiscal year end).

This schedule is intended to show information for 10 years. Additional years will be displayed as they become available.

Schedule of Board Contributions Schedule 2

(b)(a) Contributions Contributions

Statutorily- in relation to the (a-b) Board's as a percentage ofFiscal Required statutorily- Contribution covered-employee covered-employeeYear* Contribution required contribution Deficiency (Excess) payroll payroll

Louisiana State Employees' Retirement System (LASERS)

2015 $125,965 $125,965 NONE $340,445 37.0%

Teachers' Retirement System of Louisiana (TRSL)2015 $10,498 $10,498 NONE $37,492 28.0%

*Amounts presented were determined as of the end of the fiscal year.

This schedule is intended to show information for 10 years. Additional years will be displayed as they become available.

Notes to Schedules 1 and 2 (Required Supplementary Information)

Changes of Benefit Terms include: A 1.5% COLA, effective July 1, 2014, provided by Act 102 for the LASERS and by Act 104 for the TRSL, of the

2014 Louisiana Regular Legislative Session, and, Relative to the LASERS, improved benefits for certain members employed by the Office of Adult Probation andParole within the Department of Public Safety and Corrections, as established by Act 852 of 2014.

32

Schedule 3

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANASTATE OF LOUISIANA

Schedule of Funding Progress for the Other Postemployment Benefits Plan

ActuarialAccruedLiability UAAL as a

Actuarial (AAL) - Unfunded PercentageActuarial Value of Projected AAL Fund Covered of CoveredValuation Assets Unit Cost (UAAL) Ratio Payroll Payroll

Date (a) (b) (b-a) (a/b) (c) [(b-a)/c]

July 1, 2012 NONE $824,900 $824,900 0.0% $263,000 314%July 1, 2013 NONE $960,700 $960,700 0.0% $314,500 305%July 1, 2014 NONE $1,041,100 $1,041,100 0.0% $340,500 306%

Factors contributing to the increase in the Office of Group Benefits plan were: 1. Changes in retiree benefit plans for those retiring after March 31, 2015 2. Use of recently released/updated mortality tables (RP 2014) 3. Use of a different age-graded claim curve

5. Changes in assumptions for retirements and terminations

4. Updates to the per capita health claim cost based on the state's most recent claims and enrollment experience

33

SUPPLEMENTARY INFORMATION

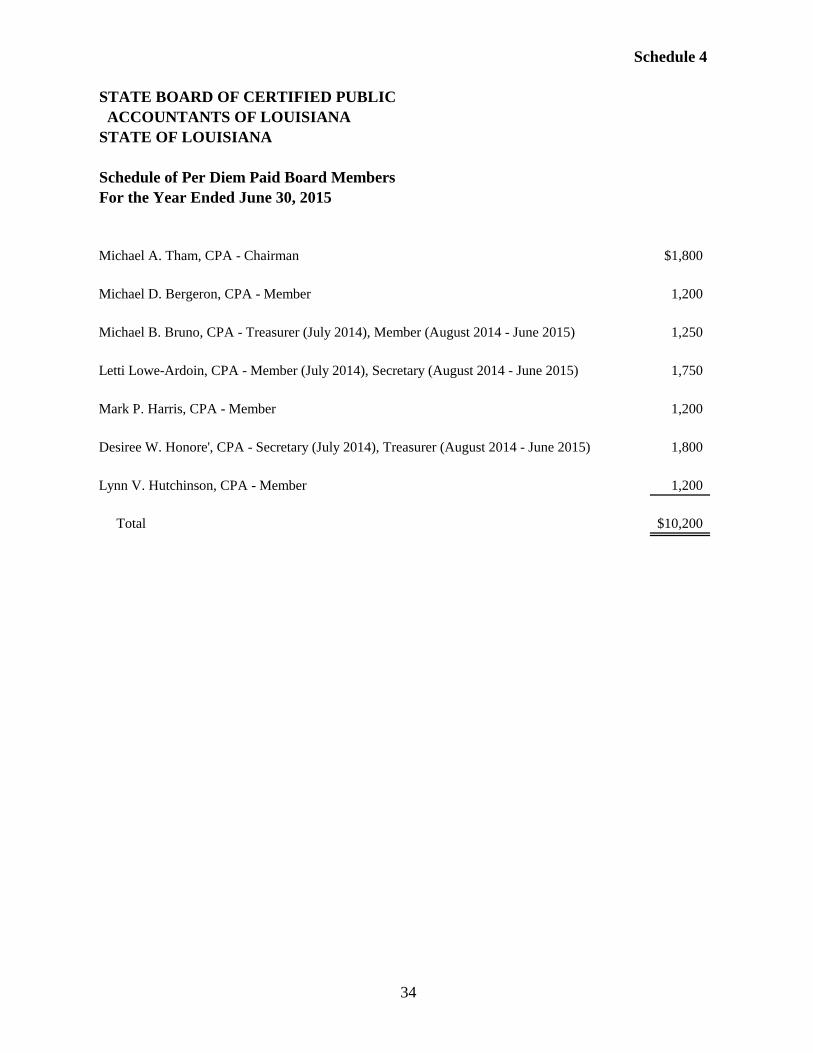

Schedule of Per Diem Paid Board Members For the Year Ending June 30, 2015

The Schedule of Per Diem Paid Board Members (Schedule 4) is presented in compliance with House Concurrent Resolution No. 54 of the 1979 Session of the Louisiana Legislature. Officers of the board receive compensation of $150 per month, and other members receive $100 per month in accordance with Act 473 of 1999.

34

Schedule 4

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANASTATE OF LOUISIANA

Schedule of Per Diem Paid Board MembersFor the Year Ended June 30, 2015

Michael A. Tham, CPA - Chairman $1,800

Michael D. Bergeron, CPA - Member 1,200

Michael B. Bruno, CPA - Treasurer (July 2014), Member (August 2014 - June 2015) 1,250

Letti Lowe-Ardoin, CPA - Member (July 2014), Secretary (August 2014 - June 2015) 1,750

Mark P. Harris, CPA - Member 1,200

Desiree W. Honore', CPA - Secretary (July 2014), Treasurer (August 2014 - June 2015) 1,800

Lynn V. Hutchinson, CPA - Member 1,200

Total $10,200

OTHER REPORT REQUIRED BY GOVERNMENT AUDITING STANDARDS

Exhibit A The following pages contain a report on internal control and on compliance with laws and regulations and other matters as required by Government Auditing Standards issued by the Comptroller General of the United States. This report is based solely on the audit of the financial statements and includes, where appropriate, any significant deficiencies and/or material weaknesses in internal control or compliance and other matters that would be material to the presented financial statements.

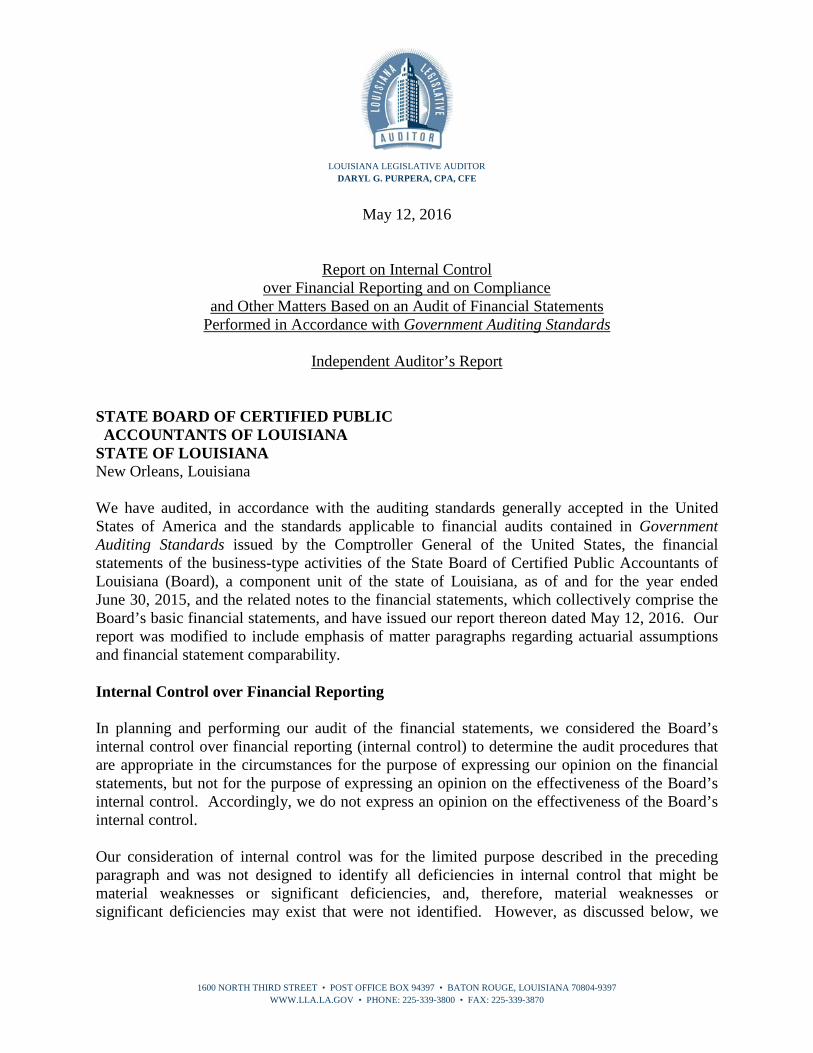

LOUISIANA LEGISLATIVE AUDITOR

DARYL G. PURPERA, CPA, CFE

1600 NORTH THIRD STREET • POST OFFICE BOX 94397 • BATON ROUGE, LOUISIANA 70804-9397

WWW.LLA.LA.GOV • PHONE: 225-339-3800 • FAX: 225-339-3870

May 12, 2016

Report on Internal Control over Financial Reporting and on Compliance

and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

Independent Auditor’s Report

STATE BOARD OF CERTIFIED PUBLIC ACCOUNTANTS OF LOUISIANA STATE OF LOUISIANA New Orleans, Louisiana We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the business-type activities of the State Board of Certified Public Accountants of Louisiana (Board), a component unit of the state of Louisiana, as of and for the year ended June 30, 2015, and the related notes to the financial statements, which collectively comprise the Board’s basic financial statements, and have issued our report thereon dated May 12, 2016. Our report was modified to include emphasis of matter paragraphs regarding actuarial assumptions and financial statement comparability. Internal Control over Financial Reporting In planning and performing our audit of the financial statements, we considered the Board’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Board’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Board’s internal control. Our consideration of internal control was for the limited purpose described in the preceding paragraph and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies, and, therefore, material weaknesses or significant deficiencies may exist that were not identified. However, as discussed below, we

State Board of Certified Public Accountants of Louisiana Report on Internal Control

Exhibit A.2

identified certain deficiencies in internal control that we consider to be material weaknesses and significant deficiencies. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis. We consider the following deficiencies in the Board’s internal control to be material weaknesses:

Inadequate Controls over Payroll and Leave The Board did not adequately review time sheets before processing payroll and did not properly post or track employee leave balances. During our review of the Board’s records, we noted the following:

Employee payroll is processed before time sheets are due, which does not allow adequate time for management to review time entry and leave balances prior to payment.

Employee records reflected negative leave balances. In three instances, employees had negative leave balances but the time sheets reflected additional leave approved and taken during the period.

Employee leave records did not match time sheet postings for two employees over multiple pay periods.

By advancing leave and paying an employee for time not worked, the Board may have violated Article 7, Section 14 of the Louisiana Constitution. These exceptions occurred because the Board’s payroll practices did not incorporate good internal control over payroll. Further, the Board’s practices were not documented in its written policies. Good internal control should include current written policies that address time sheet review and approval prior to payment and proper tracking of leave balances. Management should update its written policies to require that (1) employee time sheets are reviewed and approved before payroll is processed; (2) the sufficiency of employee leave balances are verified before leave requests are granted, and (3) employee leave balances are timely updated to reflect leave earned and taken each time period. The Board should further reconcile its employee leave records to time sheets and leave accruals for the entire fiscal year ending June 30, 2015, to ensure that leave balances on that date are accurate. Management concurred with the finding and outlined a plan of corrective action (see Appendix A, pages 1-2).

State Board of Certified Public Accountants of Louisiana Report on Internal Control

Exhibit A.3