Embed Size (px)

Citation preview

Steppe Capitalist Equity Research:

APU JSC (MSE: APU)

8 January 2018, www.steppecapitalist.com

HOLD Rating with Target Price of MNT 866

We are initiating coverage of APU JSC (APU or the Company) a

Mongolian Stock Exchange listed alcohol and beverage producer with a

HOLD rating and 12 month target price of MNT 866.

Merger with Heineken (the Merger): APU is closing a merger

transaction with Heineken’s business in Mongolia (Evergreen Investment

LLC or Evergreen) publically announced in July 2017 and effectively

becoming a near monopoly player with more than 80% share of the

local alcoholic beverage market. The transaction will mark as the largest

merger in the country.

Immediate value drivers: (i) the Merger expected to create over MNT

13bn cost synergies in 2018-2021; (ii) a vertical integration with the

trading business (APU Trading LLC), taking place as part of the Merger is

an important value driver for APU public shareholders. It results in

immediate 10 percentage point increase in gross margins previously only

captured by the shareholders of APU Trading (Shunkhlai Group).

Longer term value driver: Having secured a dominant position in the

local market APU is strategically focusing on growth through

exports, as the market for alcoholic beverages in Mongolia (the largest

EBITDA generator) has limited growth potential.

Having Heineken as a strategic shareholder will help APU to achieve the

immediate and long-term strategic targets through the use of Heineken’s

international supply chain network and marketing expertise.

As a result of the consolidation in 2017, APU expects to see 65% jump in

revenue to MNT 492bn, 10 percentage point increase in gross margins to

39% and an EPS of MNT 68.

We conclude that the market has largely priced in the value gain from the

Merger as the share price surged 99% since the announcement.

MSE:APU 5-Jan-18

Rating HOLD

Target price (MNT) 866

52-week range (MNT) 271-906

Closing price (MNT) 692

Upside 25%

Market cap. (MNT bn) 736.7

Shares O/S (m) 1064

Free float 6%

Daily volume (MNT m) 34

Industry Beverage,

dairy

Authors

Khangai Tserenraash [email protected]

Enkhbold Baasanjav [email protected]

Bat-Uul Baldandorj [email protected]

Uuganbayar Bayaraa [email protected]

Share price performance

0.0

0.2

0.4

0.6

0.8

1.0

-

250

500

750

1,000

Dec-1

6

Ap

r-1

7

Au

g-1

7

Dec-1

7

Volume (m) Price

TABLE OF CONTENTS

HOLD Rating with Target Price of MNT 866 ................................................... 0

TABLE OF CONTENTS ..................................................................................... 0

COMPANY OVERVIEW ..................................................................................... 1

Market leader with well-established operations .............................................. 1

Vertically integrated operations ....................................................................... 1

Corporate Governance .................................................................................... 2

INDUSTRY OVERVIEW ..................................................................................... 3

Vodka market – sluggish growth ..................................................................... 3

Beer market – moderate growth ...................................................................... 4

Dairy market – high growth.............................................................................. 4

Soft drink – high growth outlook ...................................................................... 5

Export markets: Chinese market analysis ....................................................... 5

GROWTH STRATEGY AND MERGER ............................................................. 6

APU strategy: growth through international markets ....................................... 6

Transaction details .......................................................................................... 6

Key regulatory approvals received .................................................................. 7

FINANCIAL OUTLOOK ...................................................................................... 8

Earnings outlook .............................................................................................. 8

Cashflow outlook ............................................................................................. 9

Financial Summary ........................................................................................ 10

VALUATION ..................................................................................................... 11

Discounted cashflow valuation ...................................................................... 11

Comparable valuation .................................................................................... 11

Valuation summary – Target price ................................................................ 11

INVESTMENT RISKS ....................................................................................... 12

Meaningful sensitivity to margins and discount rate ...................................... 12

Risks to our target price ................................................................................. 12

IMPORTANT INFORMATION AND DISCLOSURES ...................................... 13

Shareholding in the subject company ........................................................... 13

Our ratings classifications .............................................................................. 13

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 1

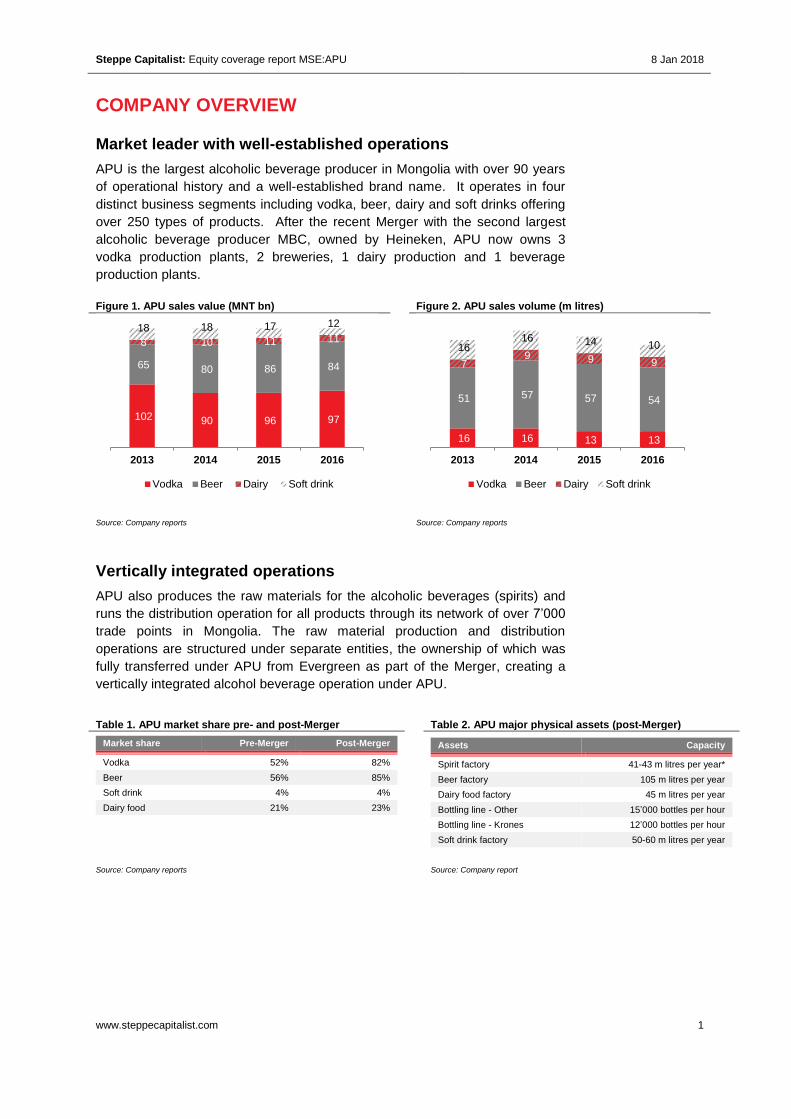

COMPANY OVERVIEW

Market leader with well-established operations

APU is the largest alcoholic beverage producer in Mongolia with over 90 years

of operational history and a well-established brand name. It operates in four

distinct business segments including vodka, beer, dairy and soft drinks offering

over 250 types of products. After the recent Merger with the second largest

alcoholic beverage producer MBC, owned by Heineken, APU now owns 3

vodka production plants, 2 breweries, 1 dairy production and 1 beverage

production plants.

Figure 1. APU sales value (MNT bn) Figure 2. APU sales volume (m litres)

Source: Company reports Source: Company reports

Vertically integrated operations

APU also produces the raw materials for the alcoholic beverages (spirits) and

runs the distribution operation for all products through its network of over 7’000

trade points in Mongolia. The raw material production and distribution

operations are structured under separate entities, the ownership of which was

fully transferred under APU from Evergreen as part of the Merger, creating a

vertically integrated alcohol beverage operation under APU.

Table 1. APU market share pre- and post-Merger Table 2. APU major physical assets (post-Merger)

Market share Pre-Merger Post-Merger

Vodka 52% 82%

Beer 56% 85%

Soft drink 4% 4%

Dairy food 21% 23%

Assets Capacity

Spirit factory 41-43 m litres per year*

Beer factory 105 m litres per year

Dairy food factory 45 m litres per year

Bottling line - Other 15’000 bottles per hour

Bottling line - Krones 12’000 bottles per hour

Soft drink factory 50-60 m litres per year

Source: Company reports Source: Company report

102 90 96 97

65 80 86 84

8 10 11 11 18 18 17 12

2013 2014 2015 2016

Vodka Beer Dairy Soft drink

16 16 13 13

51 57 57 54

7 9 9 9

16 16 14 10

2013 2014 2015 2016

Vodka Beer Dairy Soft drink

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 2

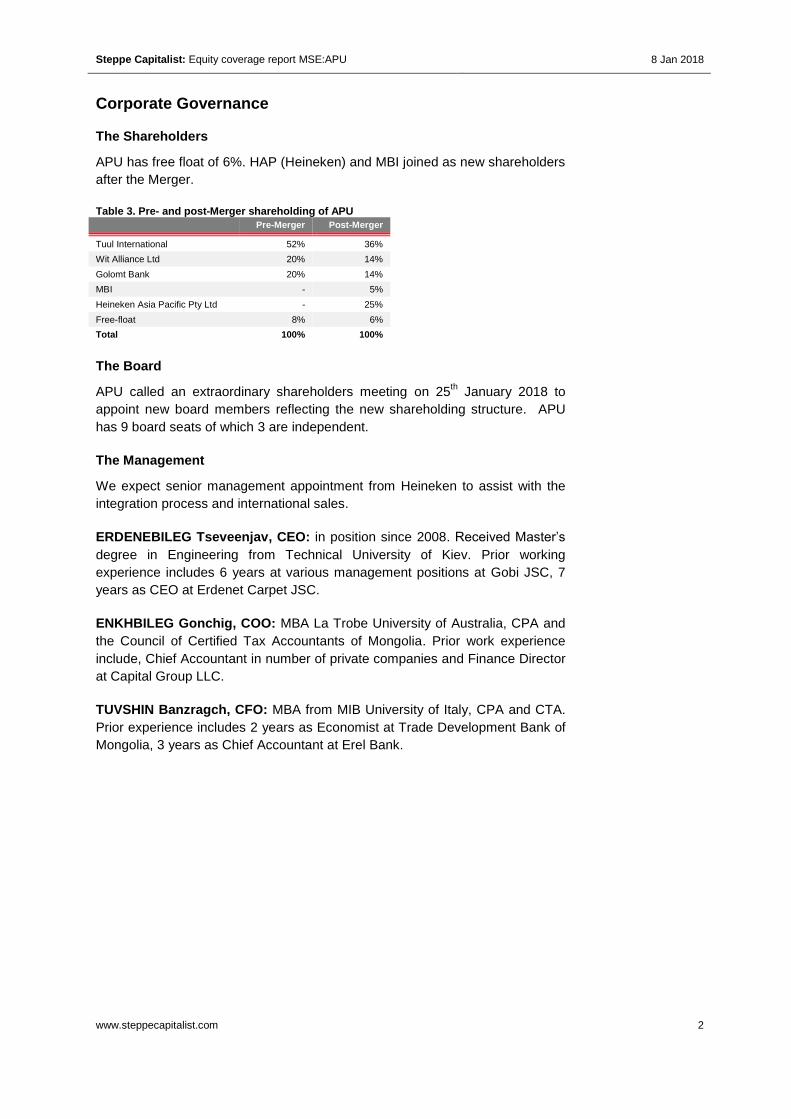

Corporate Governance

The Shareholders

APU has free float of 6%. HAP (Heineken) and MBI joined as new shareholders

after the Merger.

Table 3. Pre- and post-Merger shareholding of APU

Pre-Merger Post-Merger

Tuul International 52% 36%

Wit Alliance Ltd 20% 14%

Golomt Bank 20% 14%

MBI - 5%

Heineken Asia Pacific Pty Ltd - 25%

Free-float 8% 6%

Total 100% 100%

The Board

APU called an extraordinary shareholders meeting on 25th January 2018 to

appoint new board members reflecting the new shareholding structure. APU

has 9 board seats of which 3 are independent.

The Management

We expect senior management appointment from Heineken to assist with the

integration process and international sales.

ERDENEBILEG Tseveenjav, CEO: in position since 2008. Received Master’s

degree in Engineering from Technical University of Kiev. Prior working

experience includes 6 years at various management positions at Gobi JSC, 7

years as CEO at Erdenet Carpet JSC.

ENKHBILEG Gonchig, COO: MBA La Trobe University of Australia, CPA and

the Council of Certified Tax Accountants of Mongolia. Prior work experience

include, Chief Accountant in number of private companies and Finance Director

at Capital Group LLC.

TUVSHIN Banzragch, CFO: MBA from MIB University of Italy, CPA and CTA.

Prior experience includes 2 years as Economist at Trade Development Bank of

Mongolia, 3 years as Chief Accountant at Erel Bank.

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 3

INDUSTRY OVERVIEW

The domestic alcoholic beverage market showed signs of maturity in the past 3

years with CAGR of negative 2% after a decade of high growth of 15% CAGR.

The industry growth expectations are therefore below the GDP growth outlook

of 5% CAGR. The dairy products and soft drink markets, on the other hand, are

still growing with a potential for double digit growth in the next 5 years (CAGR

of 10% for both segments). APU plans to offset the slow growth in the alcoholic

beverage market by exporting to neighbouring countries, our preliminary

analysis indicate that such move could potentially be very lucrative line of

business for APU.

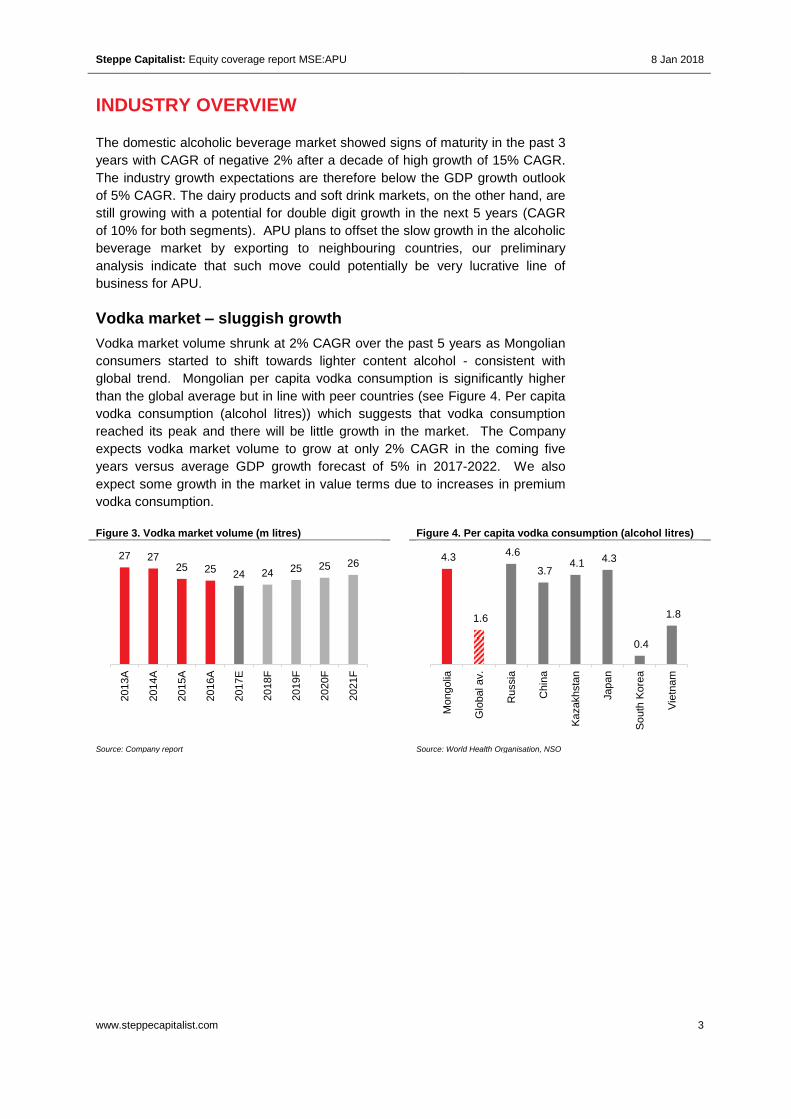

Vodka market – sluggish growth

Vodka market volume shrunk at 2% CAGR over the past 5 years as Mongolian

consumers started to shift towards lighter content alcohol - consistent with

global trend. Mongolian per capita vodka consumption is significantly higher

than the global average but in line with peer countries (see Figure 4. Per capita

vodka consumption (alcohol litres)) which suggests that vodka consumption

reached its peak and there will be little growth in the market. The Company

expects vodka market volume to grow at only 2% CAGR in the coming five

years versus average GDP growth forecast of 5% in 2017-2022. We also

expect some growth in the market in value terms due to increases in premium

vodka consumption.

Figure 3. Vodka market volume (m litres) Figure 4. Per capita vodka consumption (alcohol litres)

Source: Company report Source: World Health Organisation, NSO

27 27 25 25

24 24 25 25 26

2013A

2014A

2015A

2016A

2017E

2018F

2019F

2020F

2021F

4.3

1.6

4.6

3.7 4.1 4.3

0.4

1.8

Mo

ngolia

Glo

bal av.

Russia

Chin

a

Ka

zakhsta

n

Jap

an

So

uth

Kore

a

Vie

tnam

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 4

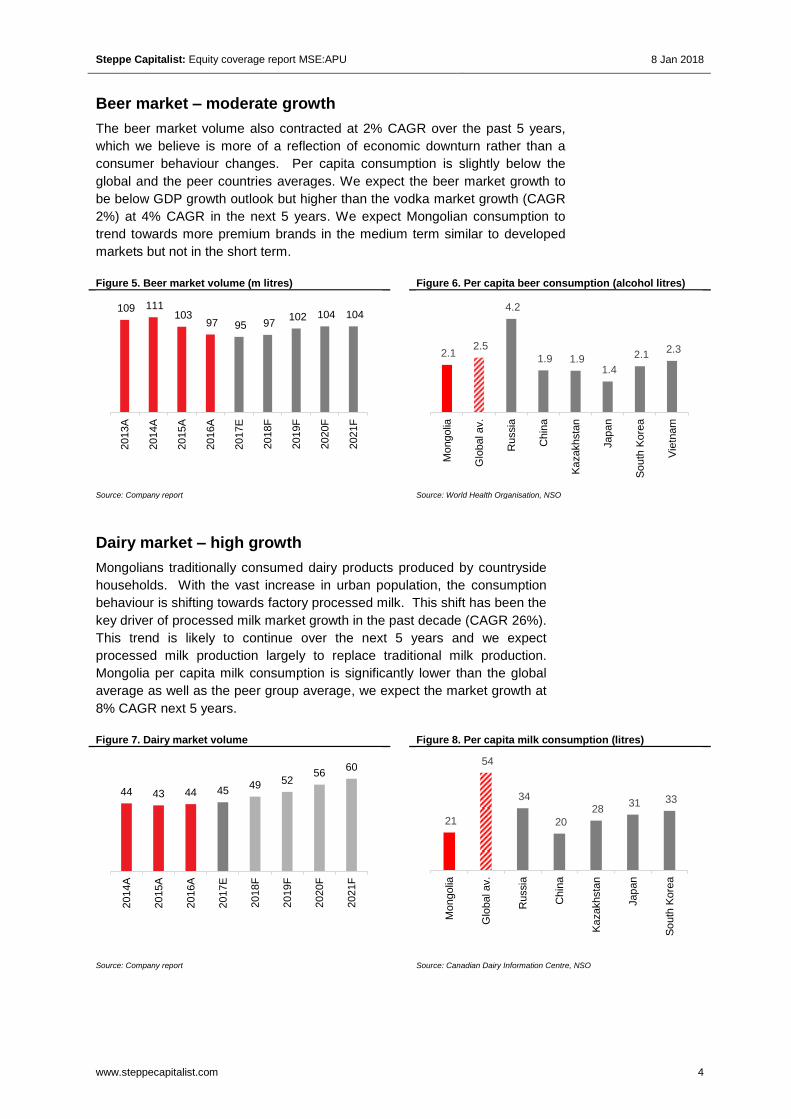

Beer market – moderate growth

The beer market volume also contracted at 2% CAGR over the past 5 years,

which we believe is more of a reflection of economic downturn rather than a

consumer behaviour changes. Per capita consumption is slightly below the

global and the peer countries averages. We expect the beer market growth to

be below GDP growth outlook but higher than the vodka market growth (CAGR

2%) at 4% CAGR in the next 5 years. We expect Mongolian consumption to

trend towards more premium brands in the medium term similar to developed

markets but not in the short term.

Figure 5. Beer market volume (m litres) Figure 6. Per capita beer consumption (alcohol litres)

Source: Company report Source: World Health Organisation, NSO

Dairy market – high growth

Mongolians traditionally consumed dairy products produced by countryside

households. With the vast increase in urban population, the consumption

behaviour is shifting towards factory processed milk. This shift has been the

key driver of processed milk market growth in the past decade (CAGR 26%).

This trend is likely to continue over the next 5 years and we expect

processed milk production largely to replace traditional milk production.

Mongolia per capita milk consumption is significantly lower than the global

average as well as the peer group average, we expect the market growth at

8% CAGR next 5 years.

Figure 7. Dairy market volume Figure 8. Per capita milk consumption (litres)

Source: Company report Source: Canadian Dairy Information Centre, NSO

109 111 103

97 95 97 102 104 104

2013A

2014A

2015A

2016A

2017E

2018F

2019F

2020F

2021F

2.1 2.5

4.2

1.9 1.9 1.4

2.1 2.3

Mo

ngolia

Glo

bal av.

Russia

Chin

a

Ka

zakhsta

n

Jap

an

So

uth

Kore

a

Vie

tnam

44 43 44 45 49 52

56 60

2014A

2015A

2016A

2017E

2018F

2019F

2020F

2021F

21

54

34

20

28 31 33

Mo

ngolia

Glo

bal av.

Russia

Chin

a

Ka

zakhsta

n

Jap

an

So

uth

Kore

a

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 5

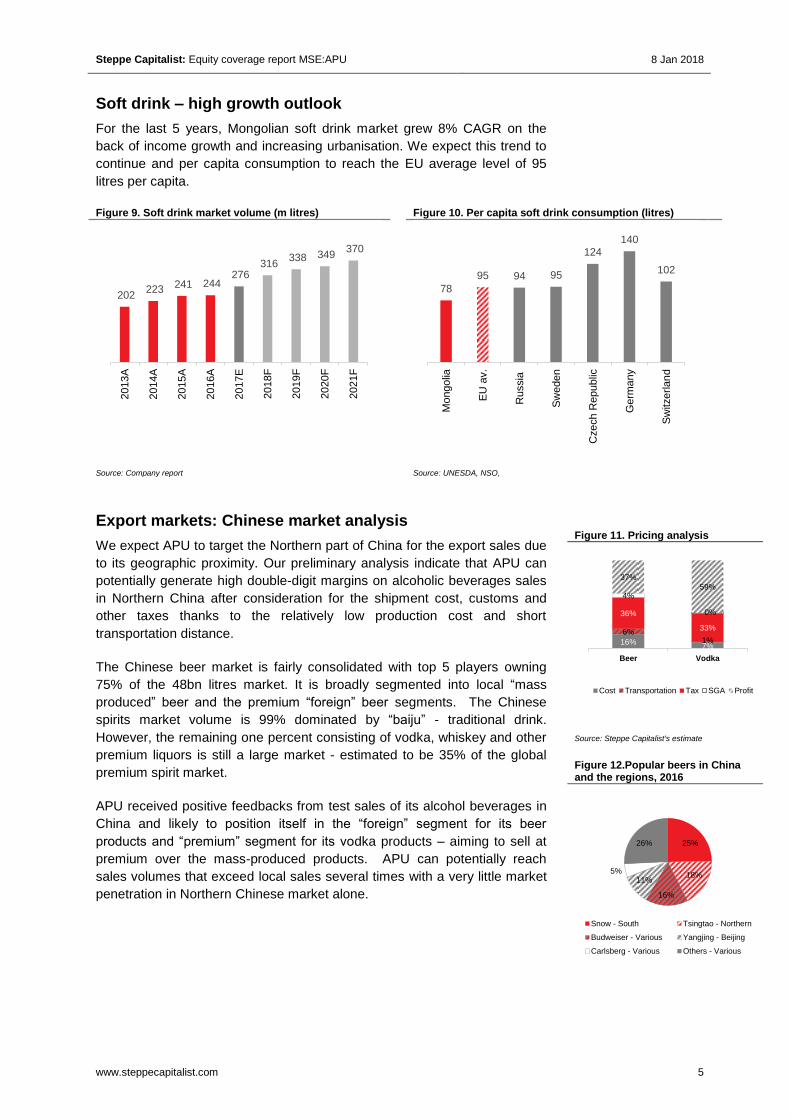

Soft drink – high growth outlook

For the last 5 years, Mongolian soft drink market grew 8% CAGR on the

back of income growth and increasing urbanisation. We expect this trend to

continue and per capita consumption to reach the EU average level of 95

litres per capita.

Figure 9. Soft drink market volume (m litres) Figure 10. Per capita soft drink consumption (litres)

Source: Company report Source: UNESDA, NSO,

Export markets: Chinese market analysis

We expect APU to target the Northern part of China for the export sales due

to its geographic proximity. Our preliminary analysis indicate that APU can

potentially generate high double-digit margins on alcoholic beverages sales

in Northern China after consideration for the shipment cost, customs and

other taxes thanks to the relatively low production cost and short

transportation distance.

The Chinese beer market is fairly consolidated with top 5 players owning

75% of the 48bn litres market. It is broadly segmented into local “mass

produced” beer and the premium “foreign” beer segments. The Chinese

spirits market volume is 99% dominated by “baiju” - traditional drink.

However, the remaining one percent consisting of vodka, whiskey and other

premium liquors is still a large market - estimated to be 35% of the global

premium spirit market.

APU received positive feedbacks from test sales of its alcohol beverages in

China and likely to position itself in the “foreign” segment for its beer

products and “premium” segment for its vodka products – aiming to sell at

premium over the mass-produced products. APU can potentially reach

sales volumes that exceed local sales several times with a very little market

penetration in Northern Chinese market alone.

202 223 241 244

276 316

338 349 370

2013A

2014A

2015A

2016A

2017E

2018F

2019F

2020F

2021F

78

95 94 95

124

140

102

Mo

ngolia

EU

av.

Russia

Sw

eden

Cze

ch R

epublic

Germ

any

Sw

itzerlan

d

Figure 11. Pricing analysis

Source: Steppe Capitalist's estimate

Figure 12.Popular beers in China and the regions, 2016

Source: Nikkei

16% 7%

6% 1%

36%

33%

4%

0%

37%

59%

Beer Vodka

Cost Transportation Tax SGA Profit

25%

18%

16%

11% 5%

26%

Snow - South Tsingtao - Northern

Budweiser - Various Yangjing - Beijing

Carlsberg - Various Others - Various

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 6

GROWTH STRATEGY AND MERGER

APU strategy: growth through international markets

Having successfully positioned itself in the local market APU is now

strategically focusing on international markets. As the local alcoholic drink

market has limited growth prospects, international sales will be an important

part of the APU’s long term growth. This strategy is aligned with the

Heineken’s objective to increase its footprint in Asian market. APU’s

expertise in producing high quality vodka (World Vodka Award 2016) and its

geographic proximity to China combined with Heineken’s marketing

expertise can competitively position APU in Chinese market, in particular the

premium vodka and beer segments in the Northern region. The Company

estimates to generate MNT 25bn of additional EBITDA from export sales

from 2018 to 2021. Export sales will increase the current plant utilisation rate

(c.60%) and reduce production costs.

Transaction details

The Merger transaction is between APU and Evergreen International LLC

(Evergreen) and was initiated 3 years ago. Evergreen is a holding company

that owns Heineken’s assets in Mongolia as well as the distributor (APU

trading LLC or APU Trading) and the spirits suppliers (Natur Agro LLC

and UB Spirits LLC or Spirits Suppliers). The transaction is, therefore, not

only a vertical integration between the largest (APU) and the second largest

producers (MBC of Heineken) of alcoholic beverage but also a vertical

integration of APU’s supply chain (APU Trading and Spirits Suppliers).

In the return for merging the assets with book value of MNT 338bn APU will

issue additional 321,304,553 shares to the shareholders of Evergreen

(Heineken Asia Pacific Pte Ltd - 83% and Mongolian Beverage Investments

LLC-17%) at valuation of MNT 1052 per share. As a result Heineken will

become the second largest shareholder of APU with 25% ownership.

Also as part of APU’s general re-organization process, the Company is

separating the dairy products operation under a new wholly-owned

subsidiary (APU Dairy LLC) with over MNT 55bn of assets. This move

suggests that the Company is planning a spin-off of its dairy business. This

makes a lot of sense given the dairy business could be worth more as a

separate business rather than a part of the whole as the dairy market has

high growth potential than alcohol and beverages markets and the synergy

between dairy and alcohol businesses is limited.

We expect a smooth integration process as the Merger was agreed with the

full support from both sides and the shareholders are aligned and committed

to the growth strategy going forward.

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 7

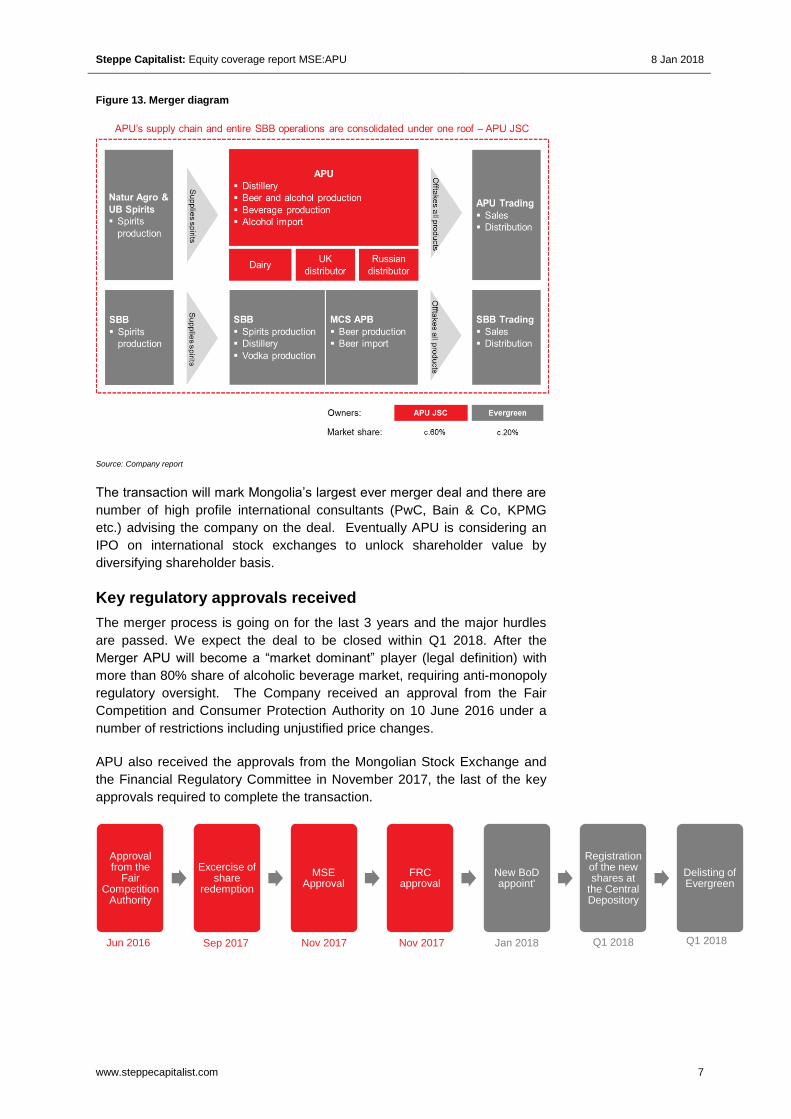

Figure 13. Merger diagram

Source: Company report

The transaction will mark Mongolia’s largest ever merger deal and there are

number of high profile international consultants (PwC, Bain & Co, KPMG

etc.) advising the company on the deal. Eventually APU is considering an

IPO on international stock exchanges to unlock shareholder value by

diversifying shareholder basis.

Key regulatory approvals received

The merger process is going on for the last 3 years and the major hurdles

are passed. We expect the deal to be closed within Q1 2018. After the

Merger APU will become a “market dominant” player (legal definition) with

more than 80% share of alcoholic beverage market, requiring anti-monopoly

regulatory oversight. The Company received an approval from the Fair

Competition and Consumer Protection Authority on 10 June 2016 under a

number of restrictions including unjustified price changes.

APU also received the approvals from the Mongolian Stock Exchange and

the Financial Regulatory Committee in November 2017, the last of the key

approvals required to complete the transaction.

Approval from the

Fair Competition

Authority

Excercise of share

redemption

MSE Approval

FRC approval

New BoD appoint'

Registration of the new shares at

the Central Depository

Delisting of Evergreen

Q1 2018 Q1 2018 Jan 2018 Nov 2017 Sep 2017 Nov 2017 Jun 2016

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 8

FINANCIAL OUTLOOK

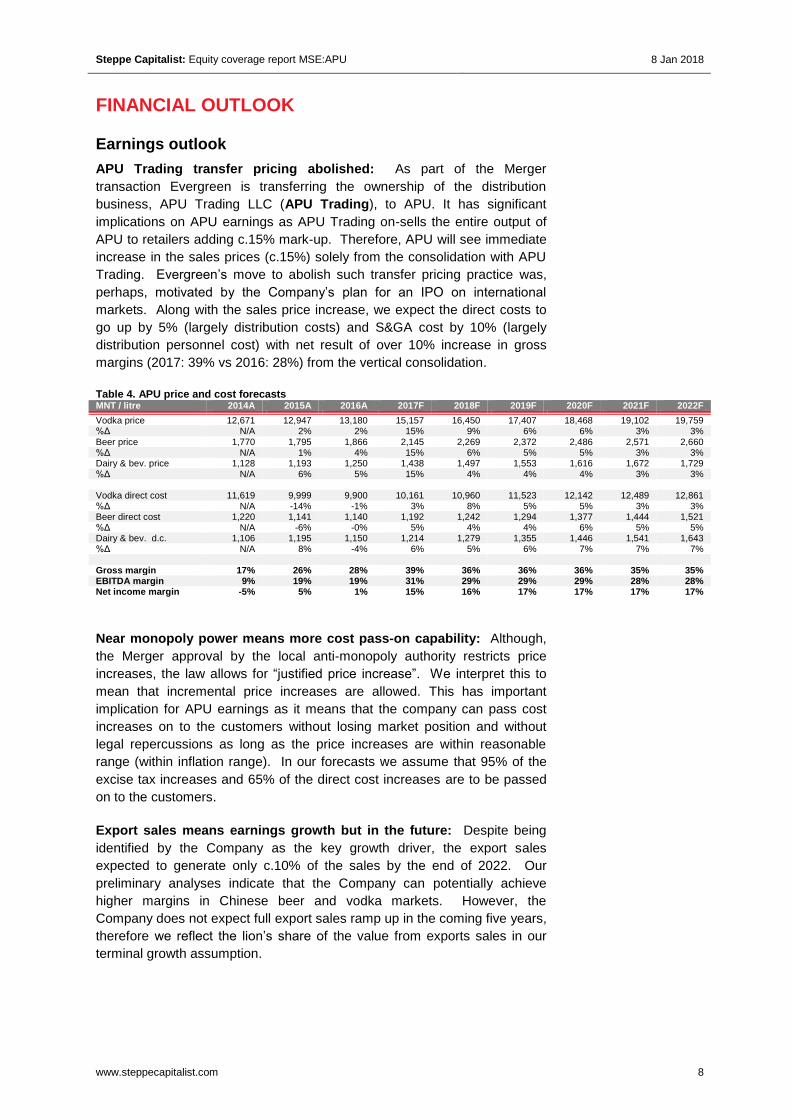

Earnings outlook

APU Trading transfer pricing abolished: As part of the Merger

transaction Evergreen is transferring the ownership of the distribution

business, APU Trading LLC (APU Trading), to APU. It has significant

implications on APU earnings as APU Trading on-sells the entire output of

APU to retailers adding c.15% mark-up. Therefore, APU will see immediate

increase in the sales prices (c.15%) solely from the consolidation with APU

Trading. Evergreen’s move to abolish such transfer pricing practice was,

perhaps, motivated by the Company’s plan for an IPO on international

markets. Along with the sales price increase, we expect the direct costs to

go up by 5% (largely distribution costs) and S&GA cost by 10% (largely

distribution personnel cost) with net result of over 10% increase in gross

margins (2017: 39% vs 2016: 28%) from the vertical consolidation.

Table 4. APU price and cost forecasts MNT / litre 2014A 2015A 2016A 2017F 2018F 2019F 2020F 2021F 2022F

Vodka price 12,671 12,947 13,180 15,157 16,450 17,407 18,468 19,102 19,759 %Δ N/A 2% 2% 15% 9% 6% 6% 3% 3% Beer price 1,770 1,795 1,866 2,145 2,269 2,372 2,486 2,571 2,660 %Δ N/A 1% 4% 15% 6% 5% 5% 3% 3% Dairy & bev. price 1,128 1,193 1,250 1,438 1,497 1,553 1,616 1,672 1,729 %Δ N/A 6% 5% 15% 4% 4% 4% 3% 3%

Vodka direct cost 11,619 9,999 9,900 10,161 10,960 11,523 12,142 12,489 12,861 %Δ N/A -14% -1% 3% 8% 5% 5% 3% 3% Beer direct cost 1,220 1,141 1,140 1,192 1,242 1,294 1,377 1,444 1,521 %Δ N/A -6% -0% 5% 4% 4% 6% 5% 5% Dairy & bev. d.c. 1,106 1,195 1,150 1,214 1,279 1,355 1,446 1,541 1,643 %Δ N/A 8% -4% 6% 5% 6% 7% 7% 7%

Gross margin 17% 26% 28% 39% 36% 36% 36% 35% 35% EBITDA margin 9% 19% 19% 31% 29% 29% 29% 28% 28% Net income margin -5% 5% 1% 15% 16% 17% 17% 17% 17%

Near monopoly power means more cost pass-on capability: Although,

the Merger approval by the local anti-monopoly authority restricts price

increases, the law allows for “justified price increase”. We interpret this to

mean that incremental price increases are allowed. This has important

implication for APU earnings as it means that the company can pass cost

increases on to the customers without losing market position and without

legal repercussions as long as the price increases are within reasonable

range (within inflation range). In our forecasts we assume that 95% of the

excise tax increases and 65% of the direct cost increases are to be passed

on to the customers.

Export sales means earnings growth but in the future: Despite being

identified by the Company as the key growth driver, the export sales

expected to generate only c.10% of the sales by the end of 2022. Our

preliminary analyses indicate that the Company can potentially achieve

higher margins in Chinese beer and vodka markets. However, the

Company does not expect full export sales ramp up in the coming five years,

therefore we reflect the lion’s share of the value from exports sales in our

terminal growth assumption.

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 9

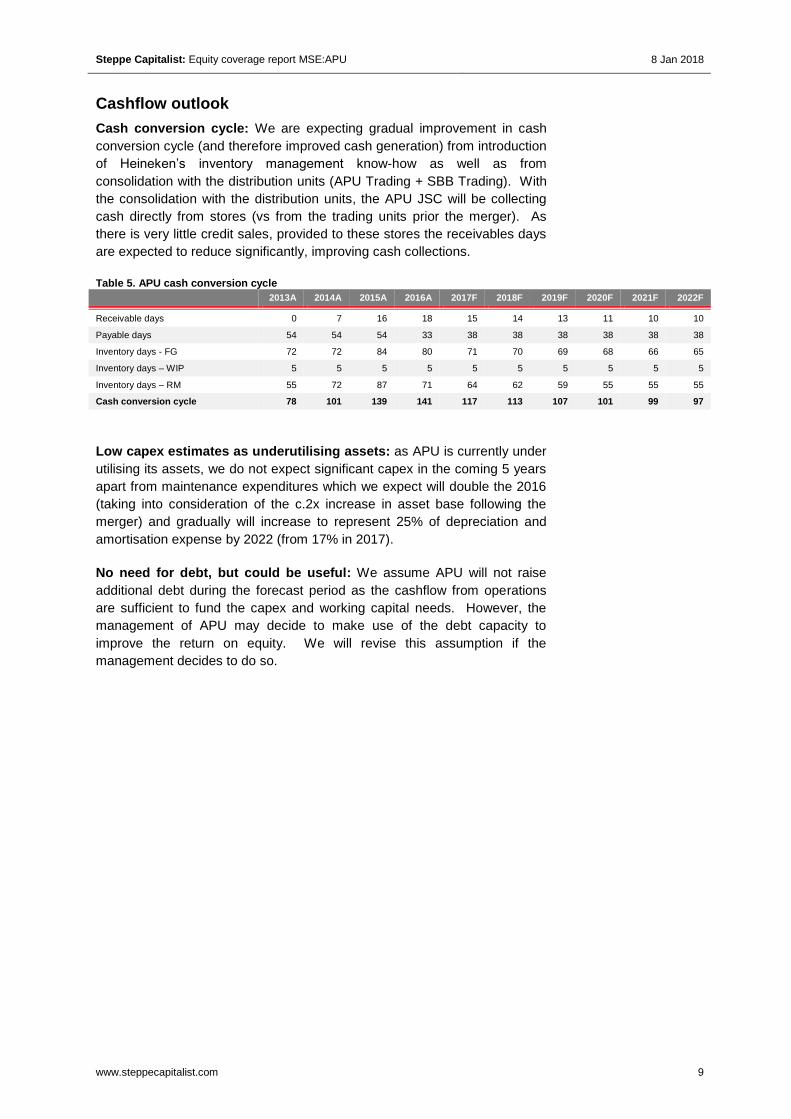

Cashflow outlook

Cash conversion cycle: We are expecting gradual improvement in cash

conversion cycle (and therefore improved cash generation) from introduction

of Heineken’s inventory management know-how as well as from

consolidation with the distribution units (APU Trading + SBB Trading). With

the consolidation with the distribution units, the APU JSC will be collecting

cash directly from stores (vs from the trading units prior the merger). As

there is very little credit sales, provided to these stores the receivables days

are expected to reduce significantly, improving cash collections.

Table 5. APU cash conversion cycle

2013A 2014A 2015A 2016A 2017F 2018F 2019F 2020F 2021F 2022F

Receivable days 0 7 16 18 15 14 13 11 10 10

Payable days 54 54 54 33 38 38 38 38 38 38

Inventory days - FG 72 72 84 80 71 70 69 68 66 65

Inventory days – WIP 5 5 5 5 5 5 5 5 5 5

Inventory days – RM 55 72 87 71 64 62 59 55 55 55

Cash conversion cycle 78 101 139 141 117 113 107 101 99 97

Low capex estimates as underutilising assets: as APU is currently under

utilising its assets, we do not expect significant capex in the coming 5 years

apart from maintenance expenditures which we expect will double the 2016

(taking into consideration of the c.2x increase in asset base following the

merger) and gradually will increase to represent 25% of depreciation and

amortisation expense by 2022 (from 17% in 2017).

No need for debt, but could be useful: We assume APU will not raise

additional debt during the forecast period as the cashflow from operations

are sufficient to fund the capex and working capital needs. However, the

management of APU may decide to make use of the debt capacity to

improve the return on equity. We will revise this assumption if the

management decides to do so.

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 10

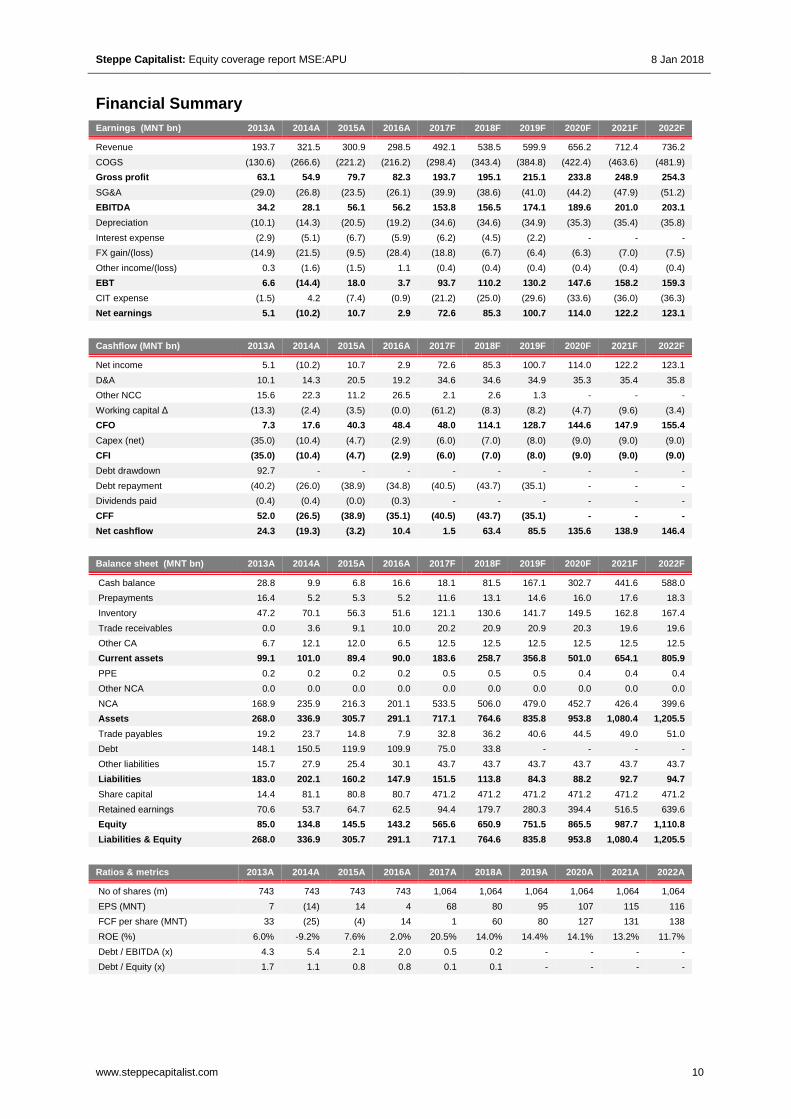

Financial Summary

Earnings (MNT bn) 2013A 2014A 2015A 2016A 2017F 2018F 2019F 2020F 2021F 2022F

Revenue 193.7 321.5 300.9 298.5 492.1 538.5 599.9 656.2 712.4 736.2

COGS (130.6) (266.6) (221.2) (216.2) (298.4) (343.4) (384.8) (422.4) (463.6) (481.9)

Gross profit 63.1 54.9 79.7 82.3 193.7 195.1 215.1 233.8 248.9 254.3

SG&A (29.0) (26.8) (23.5) (26.1) (39.9) (38.6) (41.0) (44.2) (47.9) (51.2)

EBITDA 34.2 28.1 56.1 56.2 153.8 156.5 174.1 189.6 201.0 203.1

Depreciation (10.1) (14.3) (20.5) (19.2) (34.6) (34.6) (34.9) (35.3) (35.4) (35.8)

Interest expense (2.9) (5.1) (6.7) (5.9) (6.2) (4.5) (2.2) - - -

FX gain/(loss) (14.9) (21.5) (9.5) (28.4) (18.8) (6.7) (6.4) (6.3) (7.0) (7.5)

Other income/(loss) 0.3 (1.6) (1.5) 1.1 (0.4) (0.4) (0.4) (0.4) (0.4) (0.4)

EBT 6.6 (14.4) 18.0 3.7 93.7 110.2 130.2 147.6 158.2 159.3

CIT expense (1.5) 4.2 (7.4) (0.9) (21.2) (25.0) (29.6) (33.6) (36.0) (36.3)

Net earnings 5.1 (10.2) 10.7 2.9 72.6 85.3 100.7 114.0 122.2 123.1

Cashflow (MNT bn) 2013A 2014A 2015A 2016A 2017F 2018F 2019F 2020F 2021F 2022F

Net income 5.1 (10.2) 10.7 2.9 72.6 85.3 100.7 114.0 122.2 123.1

D&A 10.1 14.3 20.5 19.2 34.6 34.6 34.9 35.3 35.4 35.8

Other NCC 15.6 22.3 11.2 26.5 2.1 2.6 1.3 - - -

Working capital Δ (13.3) (2.4) (3.5) (0.0) (61.2) (8.3) (8.2) (4.7) (9.6) (3.4)

CFO 7.3 17.6 40.3 48.4 48.0 114.1 128.7 144.6 147.9 155.4

Capex (net) (35.0) (10.4) (4.7) (2.9) (6.0) (7.0) (8.0) (9.0) (9.0) (9.0)

CFI (35.0) (10.4) (4.7) (2.9) (6.0) (7.0) (8.0) (9.0) (9.0) (9.0)

Debt drawdown 92.7 - - - - - - - - -

Debt repayment (40.2) (26.0) (38.9) (34.8) (40.5) (43.7) (35.1) - - -

Dividends paid (0.4) (0.4) (0.0) (0.3) - - - - - -

CFF 52.0 (26.5) (38.9) (35.1) (40.5) (43.7) (35.1) - - -

Net cashflow 24.3 (19.3) (3.2) 10.4 1.5 63.4 85.5 135.6 138.9 146.4

Balance sheet (MNT bn) 2013A 2014A 2015A 2016A 2017F 2018F 2019F 2020F 2021F 2022F

Cash balance 28.8 9.9 6.8 16.6 18.1 81.5 167.1 302.7 441.6 588.0

Prepayments 16.4 5.2 5.3 5.2 11.6 13.1 14.6 16.0 17.6 18.3

Inventory 47.2 70.1 56.3 51.6 121.1 130.6 141.7 149.5 162.8 167.4

Trade receivables 0.0 3.6 9.1 10.0 20.2 20.9 20.9 20.3 19.6 19.6

Other CA 6.7 12.1 12.0 6.5 12.5 12.5 12.5 12.5 12.5 12.5

Current assets 99.1 101.0 89.4 90.0 183.6 258.7 356.8 501.0 654.1 805.9

PPE 0.2 0.2 0.2 0.2 0.5 0.5 0.5 0.4 0.4 0.4

Other NCA 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

NCA 168.9 235.9 216.3 201.1 533.5 506.0 479.0 452.7 426.4 399.6

Assets 268.0 336.9 305.7 291.1 717.1 764.6 835.8 953.8 1,080.4 1,205.5

Trade payables 19.2 23.7 14.8 7.9 32.8 36.2 40.6 44.5 49.0 51.0

Debt 148.1 150.5 119.9 109.9 75.0 33.8 - - - -

Other liabilities 15.7 27.9 25.4 30.1 43.7 43.7 43.7 43.7 43.7 43.7

Liabilities 183.0 202.1 160.2 147.9 151.5 113.8 84.3 88.2 92.7 94.7

Share capital 14.4 81.1 80.8 80.7 471.2 471.2 471.2 471.2 471.2 471.2

Retained earnings 70.6 53.7 64.7 62.5 94.4 179.7 280.3 394.4 516.5 639.6

Equity 85.0 134.8 145.5 143.2 565.6 650.9 751.5 865.5 987.7 1,110.8

Liabilities & Equity 268.0 336.9 305.7 291.1 717.1 764.6 835.8 953.8 1,080.4 1,205.5

Ratios & metrics 2013A 2014A 2015A 2016A 2017A 2018A 2019A 2020A 2021A 2022A

No of shares (m) 743 743 743 743 1,064 1,064 1,064 1,064 1,064 1,064

EPS (MNT) 7 (14) 14 4 68 80 95 107 115 116

FCF per share (MNT) 33 (25) (4) 14 1 60 80 127 131 138

ROE (%) 6.0% -9.2% 7.6% 2.0% 20.5% 14.0% 14.4% 14.1% 13.2% 11.7%

Debt / EBITDA (x) 4.3 5.4 2.1 2.0 0.5 0.2 - - - -

Debt / Equity (x) 1.7 1.1 0.8 0.8 0.1 0.1 - - - -

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 11

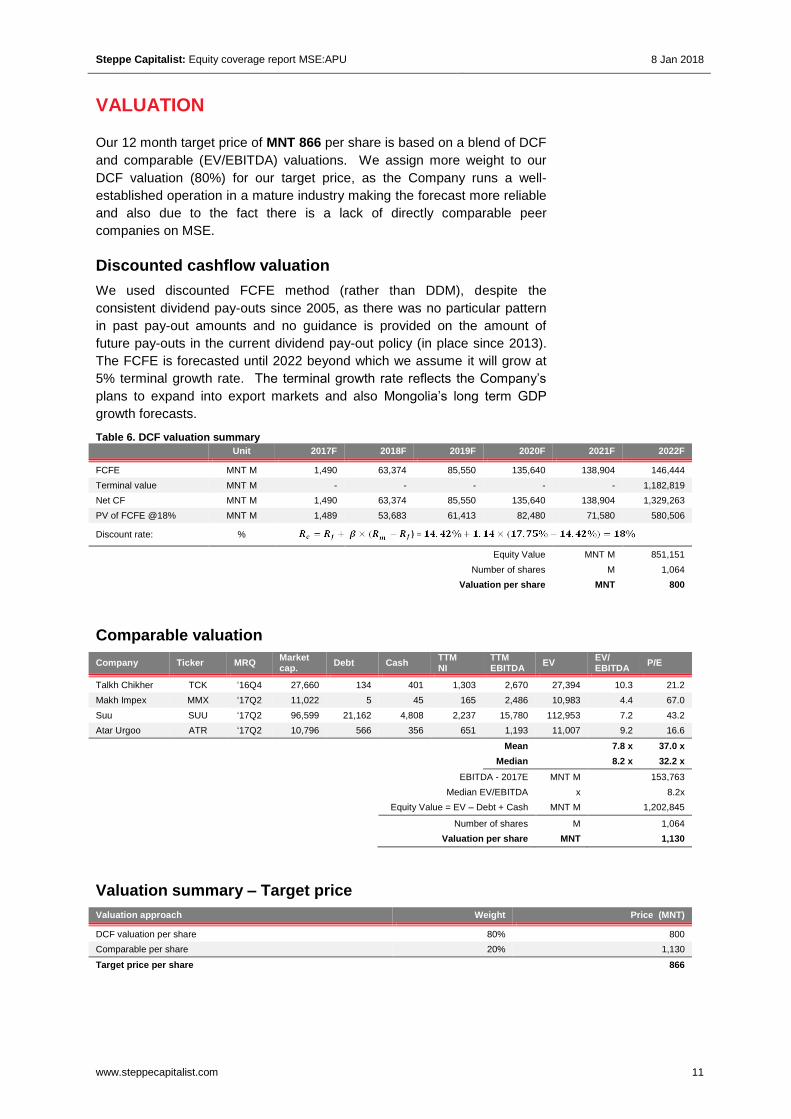

VALUATION

Our 12 month target price of MNT 866 per share is based on a blend of DCF

and comparable (EV/EBITDA) valuations. We assign more weight to our

DCF valuation (80%) for our target price, as the Company runs a well-

established operation in a mature industry making the forecast more reliable

and also due to the fact there is a lack of directly comparable peer

companies on MSE.

Discounted cashflow valuation

We used discounted FCFE method (rather than DDM), despite the

consistent dividend pay-outs since 2005, as there was no particular pattern

in past pay-out amounts and no guidance is provided on the amount of

future pay-outs in the current dividend pay-out policy (in place since 2013).

The FCFE is forecasted until 2022 beyond which we assume it will grow at

5% terminal growth rate. The terminal growth rate reflects the Company’s

plans to expand into export markets and also Mongolia’s long term GDP

growth forecasts.

Table 6. DCF valuation summary

Unit 2017F 2018F 2019F 2020F 2021F 2022F

FCFE MNT M 1,490 63,374 85,550 135,640 138,904 146,444

Terminal value MNT M - - - - - 1,182,819

Net CF MNT M 1,490 63,374 85,550 135,640 138,904 1,329,263

PV of FCFE @18% MNT M 1,489 53,683 61,413 82,480 71,580 580,506

Discount rate: %

Equity Value MNT M 851,151

Number of shares M 1,064

Valuation per share MNT 800

Comparable valuation

Company Ticker MRQ Market cap.

Debt Cash TTM NI

TTM EBITDA

EV EV/ EBITDA

P/E

Talkh Chikher TCK ‘16Q4 27,660 134 401 1,303 2,670 27,394 10.3 21.2

Makh Impex MMX ‘17Q2 11,022 5 45 165 2,486 10,983 4.4 67.0

Suu SUU ‘17Q2 96,599 21,162 4,808 2,237 15,780 112,953 7.2 43.2

Atar Urgoo ATR ‘17Q2 10,796 566 356 651 1,193 11,007 9.2 16.6

Mean 7.8 x 37.0 x

Median 8.2 x 32.2 x

EBITDA - 2017E MNT M 153,763

Median EV/EBITDA x 8.2x

Equity Value = EV – Debt + Cash MNT M 1,202,845

Number of shares M 1,064

Valuation per share MNT 1,130

Valuation summary – Target price

Valuation approach Weight Price (MNT)

DCF valuation per share 80% 800

Comparable per share 20% 1,130

Target price per share

866

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 12

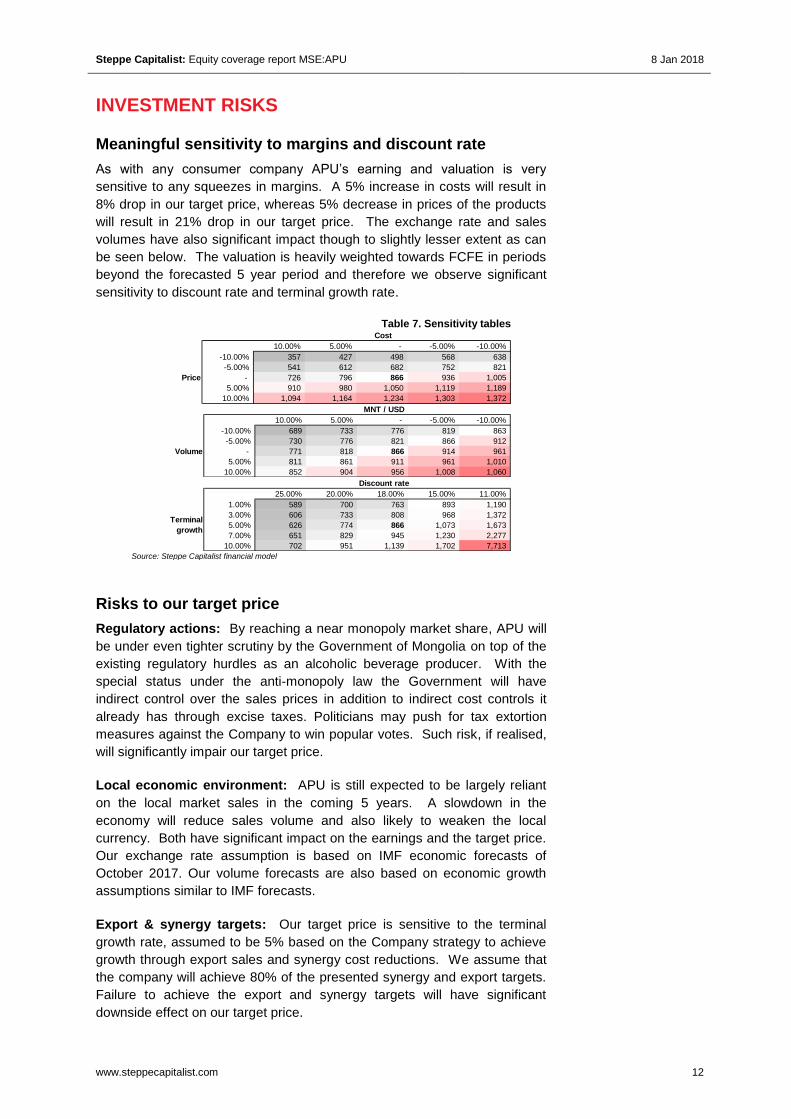

INVESTMENT RISKS

Meaningful sensitivity to margins and discount rate

As with any consumer company APU’s earning and valuation is very

sensitive to any squeezes in margins. A 5% increase in costs will result in

8% drop in our target price, whereas 5% decrease in prices of the products

will result in 21% drop in our target price. The exchange rate and sales

volumes have also significant impact though to slightly lesser extent as can

be seen below. The valuation is heavily weighted towards FCFE in periods

beyond the forecasted 5 year period and therefore we observe significant

sensitivity to discount rate and terminal growth rate.

Table 7. Sensitivity tables

Source: Steppe Capitalist financial model

Risks to our target price

Regulatory actions: By reaching a near monopoly market share, APU will

be under even tighter scrutiny by the Government of Mongolia on top of the

existing regulatory hurdles as an alcoholic beverage producer. With the

special status under the anti-monopoly law the Government will have

indirect control over the sales prices in addition to indirect cost controls it

already has through excise taxes. Politicians may push for tax extortion

measures against the Company to win popular votes. Such risk, if realised,

will significantly impair our target price.

Local economic environment: APU is still expected to be largely reliant

on the local market sales in the coming 5 years. A slowdown in the

economy will reduce sales volume and also likely to weaken the local

currency. Both have significant impact on the earnings and the target price.

Our exchange rate assumption is based on IMF economic forecasts of

October 2017. Our volume forecasts are also based on economic growth

assumptions similar to IMF forecasts.

Export & synergy targets: Our target price is sensitive to the terminal

growth rate, assumed to be 5% based on the Company strategy to achieve

growth through export sales and synergy cost reductions. We assume that

the company will achieve 80% of the presented synergy and export targets.

Failure to achieve the export and synergy targets will have significant

downside effect on our target price.

Cost

866 10.00% 5.00% - -5.00% -10.00%

-10.00% 357 427 498 568 638

-5.00% 541 612 682 752 821

Price - 726 796 866 936 1,005

5.00% 910 980 1,050 1,119 1,189

10.00% 1,094 1,164 1,234 1,303 1,372

MNT / USD

866 10.00% 5.00% - -5.00% -10.00%

-10.00% 689 733 776 819 863

-5.00% 730 776 821 866 912

Volume - 771 818 866 914 961

5.00% 811 861 911 961 1,010

10.00% 852 904 956 1,008 1,060

Discount rate

866 25.00% 20.00% 18.00% 15.00% 11.00%

1.00% 589 700 763 893 1,190

3.00% 606 733 808 968 1,372

5.00% 626 774 866 1,073 1,673

7.00% 651 829 945 1,230 2,277

10.00% 702 951 1,139 1,702 7,713

Terminal

growth

Steppe Capitalist: Equity coverage report MSE:APU 8 Jan 2018

www.steppecapitalist.com 13

IMPORTANT INFORMATION AND DISCLOSURES

This document/post is solely for information purposes and must not be

singularly used as the basis of any investment decision. Nothing in this

document should be construed as investment or financial advice. Please do

your own research as deem necessary to arrive at an independent

evaluation of an investment in the securities of the companies referred to in

this document/post.

The information and data in this document/post was obtained from publicly

available sources and other reliable sources. No information/data was

obtained from proprietary or non-public sources. We did not independently

verify all the information contained within this document, although best

efforts were taken.

Shareholding in the subject company

The authors of the document/post own the shares in the company referred

to in this document/post. The collective shareholding is below 0.01% of the

issued common shares.

Our ratings classifications

BUY – the target price is 30% or more above the current market price

HOLD – the target price is within -10-29% range of the current market

price

SELL – the target price is 10% or more below the current market price