Embed Size (px)

Citation preview

© ICSA, 2013 Page 1 of 21

Strategy in Practice November 2012

Suggested answers and examiner’s comments Important notice When reading these answers, please note that they are not intended to be viewed as a definitive ‘model’ answer, as in many instances there are several possible answers/approaches to a question. These answers indicate a range of appropriate content that could have been provided in answer to the questions. They may be a different length or format to the answers expected from candidates in the examination. Examiner’s general comments Overall, the performance for the November 2012 session of Strategy in Practice was lower than the June 2012 session. The answers that scored the highest marks focused on the question, dealt with the key issues that were raised, and contained references to the case study or examples (as appropriate) to support all the points made, whichever question was answered. As stated in past suggested answers, the Strategy in Practice paper is not divided into sections and four questions can be chosen from any of the six questions. However, there are two groups of questions – questions 1 to 4 are based on the pre-released case study and questions 5 and 6 are more general in character and may require application to an organisation of your choice, exploration of information given in the question, or a critical review of material from the syllabus. So a key point is that candidates will always have to answer at least two questions, and may answer all the questions, based on the case study. This is an important part of candidates’ preparation for the exam. A pre-released case study gives candidates time to consider and reflect on the strategic issues it raises for the organisation, research the context and subsequently to apply this in answer to the exam questions. What was encouraging in this session was that a few candidates showed clear evidence of having done some research on the context of the case study and then used this in their answers. On the whole, candidates also made better use of the facts of the case in their answers. Another key point noted for previous exam sessions is that, in preparing for the exam, it is important to use the models and frameworks from the syllabus to take an analytical view of your own organisation, the case organisation and others, so that you are able to use the information in the exam. This is something that can be done beforehand in preparing for the exam itself. Models were used well in this session, although it is important that candidates make sure they understand them and can use them clearly and accurately in the answers.

© ICSA, 2013 Page 2 of 21

Case Study

Stefi’s On the menu of Stefi’s Italian restaurants are the proud words ‘since 1964’. The UK-based restaurant chain has been operating for nearly half a century, which means that Stefi’s started business two years before the first ‘Pizza Rapido’ (a major chain and a competitor of Stefi’s), and decades before any other major Italian restaurant chain became a contender in the market. Pizza Rapido now has a site in every high street in the country and is considering expanding internationally. With the head start that it had, it might have been expected that Stefi’s would also be a highly lucrative business with its own major high street presence. But things have not quite worked out that way. While Pizza Rapido is to be found in over 400 locations across the country, and four other major chains also compete in what is now a fairly saturated Italian mid-market restaurant category, Stefi’s expansion has been more limited by comparison. Luigi Riva (‘Luigi’), the founder of Stefi’s, carefully expanded the company throughout the 1970’s and 1980’s as a business believing in family values, working hard to maintain the feel of small family restaurants preparing food ‘like mamma makes’. He wanted their offering to appeal to all. Luigi’s belief was that, “Italian food is accessible. If you’re a vegetarian you’re going to be OK. A meat lover is OK – there’s something for everyone.’’ Luigi’s son, Peter Riva (‘Peter’), became the owner and Chief Executive of the company after his father’s death in 2007. On taking over the business Peter said, “Italian restaurants went from zero to saturation and we weren’t there during the growth. We were at a crossroads. Others had been opening and building Italian restaurant groups and we just got left behind and failed to face the reality of what was happening.” In 2007, the company employed over 360 people and served around four million customers each year. But customer research suggested that few people had heard of the chain. The company operated at only 15 sites, comprising two stand-alone flagship Stefi restaurants in London and 13 smaller restaurant-cum-cafés in towns primarily in the south-west of England and at a single large retail centre. With Italian restaurant and coffee-bar brands competing for market share all over the country and the economy facing recession, it seemed a strange time to attempt to carve out a new niche in the market. But that is exactly what Peter planned to do by re-furbishing the two flagship London restaurants, renewing an emphasis on ‘regionality’, tapping into the rise of the casual-food concept, and seeking to develop the ‘next generation’ Stefi brand. The London flagship restaurants were given a major overhaul in 2009, transforming them from canteen-style cafés to ‘sit-down’ restaurants. “It was very old fashioned,” recalls Peter, “…it was time for a major overhaul.” So far the signs are encouraging. The two flagship London Stefi’s were taking £20,000 a week, but the figure has jumped to around £45,000 following the changes. Staff turnover is down considerably. What makes Stefi’s more than a copy of the competition is its regional orientation – the region in question being ‘Emilia-Romagna’ in the north of Italy. This was always part of Luigi’s concept and it seemed a sensible choice considering the recognisable Italian foods that come from the region, including Parma ham, Parmigiano Reggiano cheese, ‘real’ balsamic vinegar from Modena and pasta dishes such as tortellini and lasagne. Peter is seeking to emphasise this in the new strategy, which has been trialled in the London flagship restaurants, and said, “We feel that we are more regional than the others. Our wine, pasta and antipasti all come from the same region, and not just anywhere in Italy.” At Stefi’s, this regionality fits with a desire to differentiate the brand further by operating in what Peter calls the ‘upper mid-market’ with food more akin to that found at chains run by leading ‘celebrity chefs’ rather than by the more mainstream chains. Pricing will be keen, undercutting the larger, more established chains by 15% to 20%.

© ICSA, 2013 Page 3 of 21

“You must have fantastic quality ingredients and not mess about with them,” says Peter. “We are about upper casual dining, using the best ingredients, chosen and imported from carefully selected suppliers. From 2009, staff training for our chefs has included an exchange programme with catering colleges in Northern Italy where we not only exchange students but ideas as well.’’ There is evidence that this is increasing staff satisfaction too. Peter finally believes the idea of emphasising regionality trialled in the flagship London restaurants is ready to roll out across the chain. Peter also admits that the 13 remaining, smaller Stefi’s were a bit out of date. For these smaller units, Peter developed another proposition. A further feature of the Stefi’s brand is its experience in all-day operations. Having previously been café-style restaurants, the two London flagship Stefi’s already had well-established morning trades as well as a strong afternoon tea business. So seven of the 13 smaller Stefi’s are being refurbished and re-branded under the ‘Caffè Modena’ logo. So far, four have been converted with the remainder scheduled to switch over within the next 18 months. Here the concept is different, with a wide range of salads, sandwiches, soups and omelettes alongside the more traditional pizza and pasta dishes. ‘Dwell’ times are shorter, with the customer in and out within around 15 minutes if they wish, compared with an average stay of 30 to 45 minutes in Stefi’s, and an average spend of around £8 per person, half of that at the full-service restaurants. Peter says, “Caffè Modena appeals to a very different market from Stefi’s and is doing well in those units already converted. Italian meals are often seen as a slow, sit-down process, but Caffè Modena serves good Italian food quickly in busy environments. It is a business model I have a lot of hope for. The ultimate goal, after the rebranding and refurbishment programme is complete, is for the two concepts (Stefi’s and Caffè Modena) to grow and sit side by side in certain locations”. Herein lies a key challenge for the company: securing sites to facilitate growth. The company aims to open at least two more Stefi’s in the next 18 months on sites of 2,500 to 3,000 square feet. Peter is considering opening in the three largest UK cities outside London. In particular, he is looking at opening outlets in new retail developments, which usually means competing with established brands which have a great deal more leverage in the property market. “Our aim in the future is to move into airports and train stations with Caffè Modena, and then to work with their owners to introduce Stefi’s. I’d like to think that, if there was an opportunity, the Airports Authority and Rail Authority would give us a chance with the Stefi’s concept too.” It is going to be a hard battle but Peter is undeterred. He believes there is still sufficient of the consumer’s purse to go round. “Twenty years ago there were no restaurant brands. Now there’s a plethora. Soon it will go the other way again. People will look for something a bit more individualistic, and that’s what we are.”

© ICSA, 2013 Page 4 of 21

Questions Questions 1 – 4, below, are connected to the pre-released case study. 1. (a) Using an appropriate framework, assess the competitive environment of the

industry sector or sectors in the case study. (17 marks)

Suggested answer Most candidates used Porter’s five forces analysis to answer this question but credit was given for using other suitable frameworks, such as strategic groups. Porter’s five forces analysis is a long-established model that is widely used as a framework for analysing the structure and dynamics of the competitive environment of an industry sector. Although developed as a rational model for calculating the profitability of firms in different industries, it also offers a useful analytical framework for organisations. It is still important to recognise though that his work applies to sectors, and not simply to individual organisations. Porter argued there are five main forces affecting the profitability of industries: (i) the overall industry structure, which reflects the intensity of competition between current

competitors, and is affected by: (ii) the threat of new entrants; (iii) the bargaining power of customers; (iv) the bargaining power of suppliers; and (v) the threat of substitute products or services. Many candidates represented these diagrammatically and the best answers used that diagram to present their analysis. It is important that, to be of most value, a five forces analysis needs to be carried out at the strategic business unit (SBU) level. If the analysis is at a more generalised level, the variety of influences in the environment will be so great as to reduce the value of the analysis. For Stefi’s, there could be analysis required of the upper-middle restaurant market and perhaps a separate analysis for the cafes. The ‘fast-food’ sector’s market could be quite different. Credit was given for making this point and applying the analysis to the correct level. Applying the five forces to the case study:

Intensity of competition (industry structure) – Porter suggests this depends on a number of factors including the number and strength of competitors; the rate of market growth; similarity of products (making it simple and easy for consumers to switch from one brand to another); and the level of fixed costs.

In the restaurant sector there are many competitors, but Stefi’s is seeking to differentiate

and compete in a narrower market that still comprises independents, large chains and ‘celebrity chef’ chains. There is still a significant number of competitors whose strength is greater than Stefi’s. Despite the recession there is a sign that this market is growing. Peter certainly thinks so. Much depends on Italian food, particularly from a specific region, remaining popular. Fixed costs are moderate but can be high in some locations, particularly in airports and retail centres where Stefi’s is seeking to compete head-to-head. There are few exit barriers.

Threat of new entrants – This depends on the extent to which there are barriers to entry, which most typically are: economies of scale, government policy, the capital requirement of entry, access to distribution channels, cost advantages independent of size (for example, if there is an established operator who knows the market well, has good relationships with

© ICSA, 2013 Page 5 of 21

the key buyers and suppliers, and knows how to overcome market and operating problems), and differentiation (for example, a reputation for reliability and quality underpinned by staff training.)

In Stefi’s market there are certain economies of scale, perhaps in management and

administration as the chain grows, though there can be dangers for Stefi’s (recognised by Peter) if this produces ‘corporate’ standardisation. Capital costs are not that high although they can be in expensive centres where there is much competition for sites and this will affect Stefi’s. Access to distribution channels is straightforward, although dependent on sites. Government policy will cause little restraint and differentiation is high with competitors seeking to position themselves in the marketplace. Stefi’s might seek to do as Marks and Spencer did historically through quality ingredients and training.

The bargaining power of customers and suppliers – All organisations have to obtain resources and provide goods or services, but the relationship of buyers and sellers can have similar effects in constraining the strategic freedom of an organisation.

Supplier power is likely to be high when there is a concentration of suppliers rather than a

fragmented source of supply or when ‘switching costs’ from one supplier to another are high. In the restaurant and catering sector supplier power is generally low, although there may be fewer suppliers of the highest quality products. Customer power is high in this sector as there are so many options with a large brand presence. Many struggle to hold, let alone gain, market share.

The threat of substitute products or services – The threat of substitution may take different forms including product-for-product and substitution of need rendering an existing product or service superfluous. Generic substitution occurs where products or services compete for need, for example, restaurants compete for available household expenditure, which also means people may do without.

The availability of substitutes can place a ceiling on prices, or make inroads into the

market and so reduce its attractiveness. The key questions are whether or not a substitute provides a higher perceived benefit or value and the ease with which buyers can switch to substitutes. For Stefi’s, the problem is one of generic substitution and doing without, as the economic climate has an impact on discretionary expenditure. It appears that the best quality competitors are doing well as are those who are keenly priced.

The value of Porter’s five forces model as an analytical framework is to assist the organisation to become more aware of events in its near environment – events that it cannot control but may be able to influence. It is possible that collaboration between organisations may be a more sensible route to achieving advantage than competing – an approach unlikely to suit Steffi’s. Identifying opportunities for collaboration nonetheless requires an understanding of the structure of industries, and the framework can be used for this purpose. Examiner’s comments This was a very popular question. Most candidates used Porter’s five forces analysis and some candidates provided very good analytical answers using the framework. Weaker answers showed an incomplete or incorrect understanding of the framework, did not apply it sufficiently or, in a few cases, used an inappropriate framework (such as SWOT or PESTLE). Some candidates could have gained more marks by providing an appropriate introduction and conclusion to their answers.

© ICSA, 2013 Page 6 of 21

(b) Identify the key questions that emerge for Stefi’s from your analysis.

(8 marks) Suggested answer Five forces analysis is a useful means of identifying the forces that affect the level of competition in an industry, and that might help businesses such as Stefi’s to identify bases of competitive strategy. Johnson, Scholes and Whittington (2011) proposed the following key questions arising from five forces analysis:

What are the key forces at work in the competitive environment? For example, Peter’s perception that there is a move towards ‘regionality’.

Are there underlying forces? These might include the desire for quality fast foods and quality ingredients.

Is it likely that the forces will change, and if so, how? As Peter said, “twenty years ago there were no restaurant brands. Now there’s a plethora. Soon it will go the other way again. People will look for something a bit more individualistic, and that’s what we are.”

How do particular competitors stand in relation to these competitive forces? For example, what are Stefi’s strengths and weaknesses in relation to the key forces at work? Perhaps the main issue is that they lack scale and it will take a long time to build it.

What can management do to influence the competitive forces affecting the business unit? For example, can barriers be built to entry, or power over suppliers or buyers increased?

Are some industries more attractive than others? Some industries are intrinsically more profitable than others because, for example, entry is more difficult, or buyers and suppliers are less powerful. Considering this could see Stefi’s move into what it perceives as a neglected area such as vegetarian Italian food.

Examiner’s comments Some candidates took this requirement rather too literally and just offered questions in their answers. Although this part of the question only represents a third of the total marks, some sense of how these key questions apply to Stefi’s was required. The very best answers also offered a sense of priority.

© ICSA, 2013 Page 7 of 21

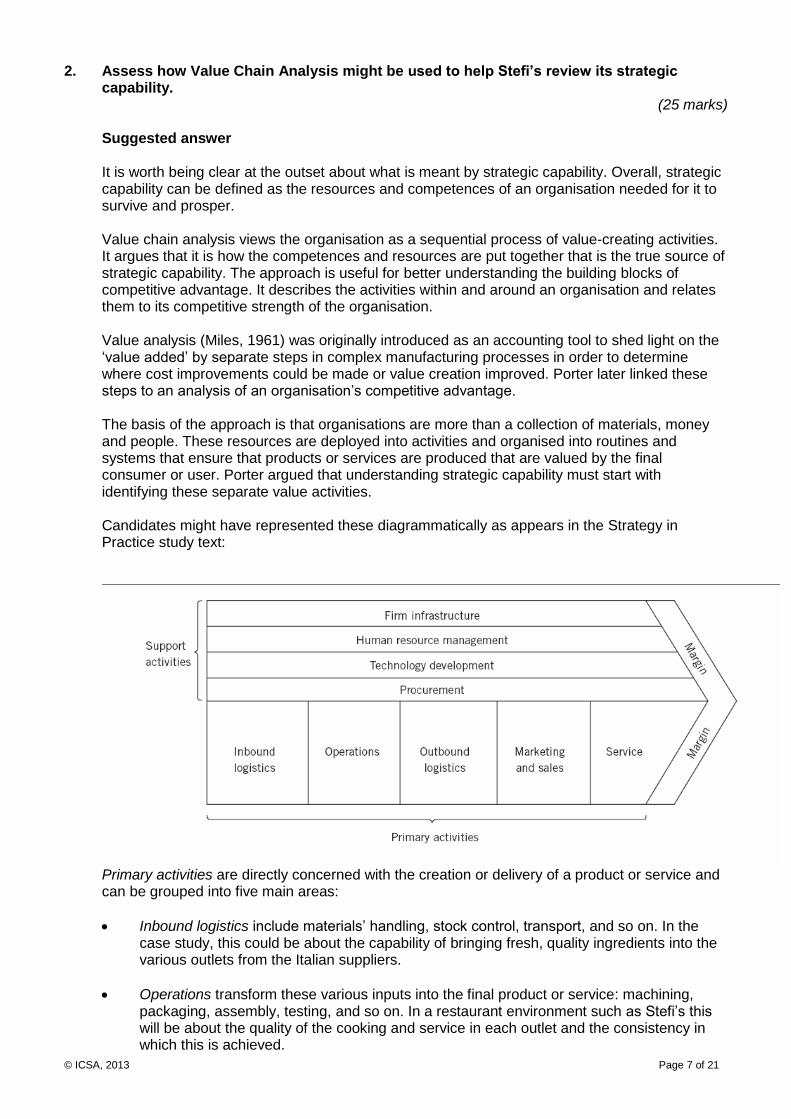

2. Assess how Value Chain Analysis might be used to help Stefi’s review its strategic capability.

(25 marks)

Suggested answer It is worth being clear at the outset about what is meant by strategic capability. Overall, strategic capability can be defined as the resources and competences of an organisation needed for it to survive and prosper. Value chain analysis views the organisation as a sequential process of value-creating activities. It argues that it is how the competences and resources are put together that is the true source of strategic capability. The approach is useful for better understanding the building blocks of competitive advantage. It describes the activities within and around an organisation and relates them to its competitive strength of the organisation. Value analysis (Miles, 1961) was originally introduced as an accounting tool to shed light on the ‘value added’ by separate steps in complex manufacturing processes in order to determine where cost improvements could be made or value creation improved. Porter later linked these steps to an analysis of an organisation’s competitive advantage. The basis of the approach is that organisations are more than a collection of materials, money and people. These resources are deployed into activities and organised into routines and systems that ensure that products or services are produced that are valued by the final consumer or user. Porter argued that understanding strategic capability must start with identifying these separate value activities. Candidates might have represented these diagrammatically as appears in the Strategy in Practice study text:

Primary activities are directly concerned with the creation or delivery of a product or service and can be grouped into five main areas:

Inbound logistics include materials’ handling, stock control, transport, and so on. In the case study, this could be about the capability of bringing fresh, quality ingredients into the various outlets from the Italian suppliers.

Operations transform these various inputs into the final product or service: machining, packaging, assembly, testing, and so on. In a restaurant environment such as Stefi’s this will be about the quality of the cooking and service in each outlet and the consistency in which this is achieved.

© ICSA, 2013 Page 8 of 21

Outbound logistics include warehousing, transport, and so on. In the case of services, they may be more concerned with arrangements for bringing customers to the service rather than the other way around. In the restaurant example, this is to do partly with the attractiveness of sites and the ease with which customers can find them, for example, whether they are well located. This could become significant should Stefi’s decide to diversify into the outside catering market.

Marketing and sales provide the means whereby consumers/users are made aware of the product or service and are able to purchase it. For example, how is Stefi’s approaching the market and advertising itself? We know from the case that the chain is not well known.

Service includes those activities that enhance or maintain the value of a product or service, such as staff training at Stefi’s.

Support activities help to improve the effectiveness or efficiency of primary activities. They can be divided into four areas:

Procurement – The processes for acquiring the various resource inputs to the primary activities. Stefi’s goes to some trouble to source its ingredients from a particular region of Italy. If that process is not working well then it could result in supply issues and high cost. Given how Stefi’s seeks to differentiate itself, this is a critical process.

Technology development – All value activities have a ‘technology’ even if it is simply ‘know-how’. In this case, this is the capability in the kitchen and delivering service.

Human resource management – Recruiting, managing, training, developing and rewarding people. We know, for example, that Stefi’s chefs all spend time training in Italy to ensure that they are appropriately trained to deliver the regional cuisine.

Infrastructure – The systems of planning, finance, information management and the routines within the culture. There seems to have been a significant change to the processes for strategy-making, for example, to the extent that Stefi’s is now seeking to catch up with those it perceives as its rivals.

The value chain is about more than just supply chain management. Most organisations are part of a wider value system – a value network that is linked to customer and supplier value chains. The value network is the set of inter-organisational links and relationships necessary to create a product or service. Indeed, it is often this specialisation that underpins excellence in creating value for money. Much of the value creation occurs in the supply and distribution chains, and this whole process needs to be analysed and understood. For example, the quality of Stefi’s offering when it reaches the final purchaser is not only influenced by the activities undertaken within the company itself. The quality of ingredients from suppliers also determines it. The value chain helps the analysis of the strategic position of an organisation in two ways: (i) As generic descriptions of activities that can help managers understand if there is a cluster

of activities providing benefit to customers located within particular areas of the value chain. Perhaps a business is especially good at outbound logistics linked to its marketing and sales operation and supported by its technology development. It might be less good in terms of its operations and its inbound logistics. The value chain also prompts managers to think about the role different activities play. For example, in a family-run restaurant chain, is cooking or service best thought of as ‘operations’ or as ‘marketing and sales’, given that its reputation and appeal may rely on the social relations between customers and waiting staff? Arguably it is ‘operations’ if done badly but ‘marketing and sales’ if done well.

© ICSA, 2013 Page 9 of 21

(ii) In terms of the cost and value of activities. Value chain analysis can be used as a way of identifying what to focus upon on in developing a more profitable business model. This can be seen in the re-design of the traditional establishments and setting up the new Caffè Modena concept.

Examiner’s comments This was another popular question but it was not always answered as well as it might have been. An encouraging number of candidates started with a definition of strategic capability as part of a short introduction. The most notable weaknesses in answers were not explaining the elements of value chain analysis and not applying it to the case study.

© ICSA, 2013 Page 10 of 21

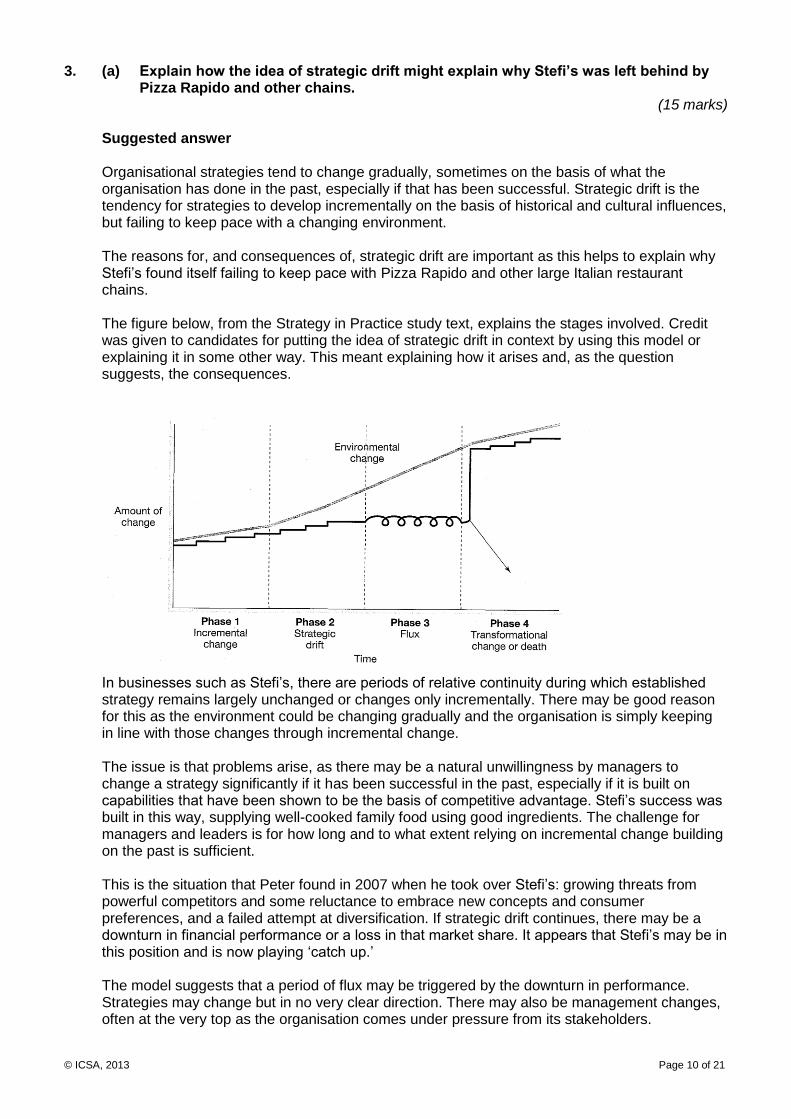

3. (a) Explain how the idea of strategic drift might explain why Stefi’s was left behind by Pizza Rapido and other chains.

(15 marks)

Suggested answer Organisational strategies tend to change gradually, sometimes on the basis of what the organisation has done in the past, especially if that has been successful. Strategic drift is the tendency for strategies to develop incrementally on the basis of historical and cultural influences, but failing to keep pace with a changing environment. The reasons for, and consequences of, strategic drift are important as this helps to explain why Stefi’s found itself failing to keep pace with Pizza Rapido and other large Italian restaurant chains. The figure below, from the Strategy in Practice study text, explains the stages involved. Credit was given to candidates for putting the idea of strategic drift in context by using this model or explaining it in some other way. This meant explaining how it arises and, as the question suggests, the consequences.

In businesses such as Stefi’s, there are periods of relative continuity during which established strategy remains largely unchanged or changes only incrementally. There may be good reason for this as the environment could be changing gradually and the organisation is simply keeping in line with those changes through incremental change. The issue is that problems arise, as there may be a natural unwillingness by managers to change a strategy significantly if it has been successful in the past, especially if it is built on capabilities that have been shown to be the basis of competitive advantage. Stefi’s success was built in this way, supplying well-cooked family food using good ingredients. The challenge for managers and leaders is for how long and to what extent relying on incremental change building on the past is sufficient. This is the situation that Peter found in 2007 when he took over Stefi’s: growing threats from powerful competitors and some reluctance to embrace new concepts and consumer preferences, and a failed attempt at diversification. If strategic drift continues, there may be a downturn in financial performance or a loss in that market share. It appears that Stefi’s may be in this position and is now playing ‘catch up.’ The model suggests that a period of flux may be triggered by the downturn in performance. Strategies may change but in no very clear direction. There may also be management changes, often at the very top as the organisation comes under pressure from its stakeholders.

© ICSA, 2013 Page 11 of 21

The model also suggests that the outcome will be one of three possibilities: the organisation may die; it may get taken over by another organisation; or it may go through a period of transformational change. This may involve multiple changes related to strategy such as a change in product offering, or market focus, changes of capabilities on which the strategy is based, changes in the top management and perhaps the way the organisation is structured. Transformational change does not take place frequently in organisations and is usually the result of a major downturn in performance. This could happen at Stefi’s if the current approach of refreshing the brand and competing directly for prime sites does not work. Examiner’s comments This was another very popular question. Candidates needed to begin by defining strategic drift and then going on to explain how this applies to the facts of the Stefi’s case study. Some answers did not show a full understanding of strategic drift and it was not always well applied to the case study. If a diagram is used to illustrate an answer, it is important that it is accurate. (b) Discuss the nature of a change agent and apply this to the role of Peter at Stefi’s. (10 marks)

Suggested answer A change agent is the individual or group that effects change in an organisation. These may be at the top of the organisation, but might also come from elsewhere. The creator of a strategy may rely on others to bring the change into effect. It may also be that there is a group of change agents from within the organisation or perhaps from outside, such as consultants, who have a whole team working on a project, together with managers from within the organisation. Personal traits of change agents are relevant. The successful change agent will need:

To be sensitive to the external context of change – the triggers in the environment that give rise to change, or the pressure from external stakeholders. Peter is showing signs in what he says of sensitivity in this area. He mentions, realistically, what has happened and is happening in the market.

To be sensitive to organisational context, building on or relating to the values and beliefs of those in or around the organisation who advocate or feel sympathy towards the need for change and the history of the organisation. Despite his recognition of the need for change, Peter also continues to stress the values upon which the business was founded: ‘family values’ and the ‘food like mama makes.’

To understand the overall strategy and therefore the magnitude and type of change necessary.

To use an appropriate style of managing change, adapting that style to the circumstances rather than imposing his or her style without regard for the specific context of change. It is arguably in these last two areas that Peter may not be performing as effectively as a change agent. He may not be recognising the scale of the change required if Stefi’s is to compete and may need to enlist external help.

In addition to this framework, candidates might point out that the literature on leadership argues that change agents have visionary capacity, are good at team-building and team-playing, are self-analytical, good at self-learning and have mental agility, and are also self-directed and self-confident. There is a tendency to overemphasise such personal attributes but managing change certainly places special demands on change agents. Peters and Waterman (1982) argue that the successful manager of change in organisations masters two ends of the spectrum. By this they mean that the change agent is simultaneously able to cope with potentially conflicting ways of managing:

© ICSA, 2013 Page 12 of 21

They have an ability to undertake or understand detailed analysis and, at the same time, to be visionary about the future. They need to be seen as having insight about the future, and yet action-oriented about making things happen.

In challenging the status quo in an organisation, they need an ability to maintain credibility and carry people with the change, while attacking the taken-for-granted and current ways of doing things.

They need an ability to encapsulate often quite complex issues in everyday ways that people can understand.

Candidates might also have referred to the example of Cable and Wireless from the Strategy in Practice study text, which used the following competency description for a change agent:

Willingness to challenge paradigms / status quo.

Resilient in the face of resistance.

Understands and articulates the positive effects of change.

Champions change and new ideas.

Plans for change, including management of risk, setting levels and managing relationships. However, change agency is often directly linked to the role of a strategic leader. Kotter (1990) and other writers describe leadership as being about the management of change. Leaders are often categorised in two ways (Kets De Vries, 1994): (i) Charismatic or transformational leaders, who are mainly concerned with building a vision

for the organisation and motivating people to achieve it. These leaders have particularly beneficial impact on performance when people see the organisation facing uncertainty (Waldman et al., 2001).

(ii) Instrumental or transactional leaders, who focus more on designing systems and controlling the organisation’s operational activities.

The most successful strategic leaders are able to tailor their style to the situation (see for example Tannenbaum and Schmidt, 1973; Goleman, 2000). Indeed, it could be a problem if they cannot, as some styles might well lead to approaches to change not suited to the particular needs of the specific change context. In the case of Stefi’s, whilst Peter has not been entirely transformational in his approach, he is likely to have been working within the grain of the Stefi’s context. Examiner’s comments There were some very good answers to this question and the majority of candidates demonstrated a good understanding of the notion of change agency. The key thing was to explore it in the context of the case study.

© ICSA, 2013 Page 13 of 21

4. The business press has commented that Stefi’s lacks a clear strategic direction.

(a) Discuss how a clear vision might help the business to achieve a clear strategic direction.

(12 marks)

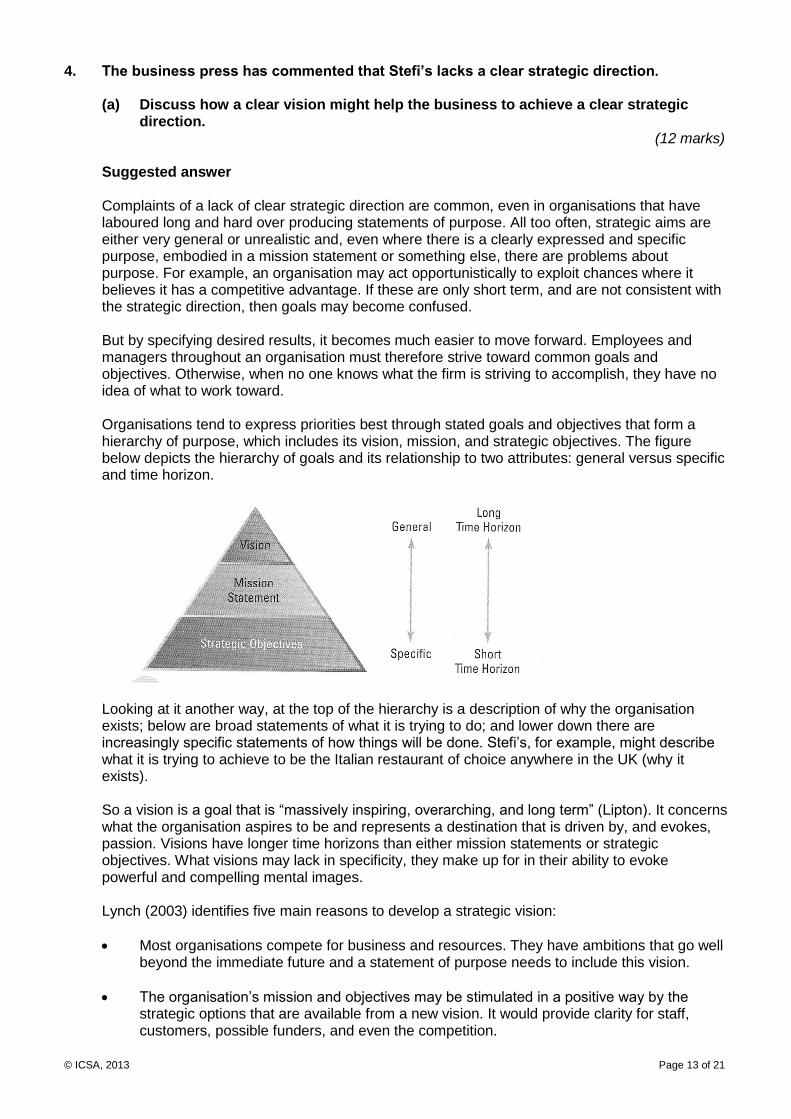

Suggested answer Complaints of a lack of clear strategic direction are common, even in organisations that have laboured long and hard over producing statements of purpose. All too often, strategic aims are either very general or unrealistic and, even where there is a clearly expressed and specific purpose, embodied in a mission statement or something else, there are problems about purpose. For example, an organisation may act opportunistically to exploit chances where it believes it has a competitive advantage. If these are only short term, and are not consistent with the strategic direction, then goals may become confused. But by specifying desired results, it becomes much easier to move forward. Employees and managers throughout an organisation must therefore strive toward common goals and objectives. Otherwise, when no one knows what the firm is striving to accomplish, they have no idea of what to work toward. Organisations tend to express priorities best through stated goals and objectives that form a hierarchy of purpose, which includes its vision, mission, and strategic objectives. The figure below depicts the hierarchy of goals and its relationship to two attributes: general versus specific and time horizon.

Looking at it another way, at the top of the hierarchy is a description of why the organisation exists; below are broad statements of what it is trying to do; and lower down there are increasingly specific statements of how things will be done. Stefi’s, for example, might describe what it is trying to achieve to be the Italian restaurant of choice anywhere in the UK (why it exists). So a vision is a goal that is “massively inspiring, overarching, and long term” (Lipton). It concerns what the organisation aspires to be and represents a destination that is driven by, and evokes, passion. Visions have longer time horizons than either mission statements or strategic objectives. What visions may lack in specificity, they make up for in their ability to evoke powerful and compelling mental images. Lynch (2003) identifies five main reasons to develop a strategic vision:

Most organisations compete for business and resources. They have ambitions that go well beyond the immediate future and a statement of purpose needs to include this vision.

The organisation’s mission and objectives may be stimulated in a positive way by the strategic options that are available from a new vision. It would provide clarity for staff, customers, possible funders, and even the competition.

© ICSA, 2013 Page 14 of 21

There may be major strategic opportunities from exploring new development areas that go beyond the existing market boundaries and organisational resources. These require a vision of the future that deserves careful exploration and development. For example, Stefi’s re-branding of part of its business to Caffè Modena.

Simple market and resource projections for the next few years will miss the opportunities opened up by a whole new range of possibilities, such as sites in retail developments. Extrapolating the current picture is unlikely to be sufficient.

Vision provides a challenge for managers. Vision is therefore a backdrop for the development of the purpose and strategy of the organisation. It is the leadership’s role to develop and implement a vision. Vision has little meaning unless it can be successfully shared with those working in the organisation, since it is they who will have to realise it. In addition, as the boundary between organisations blurs, there will increasingly be groups of workers associated with many companies and organisations, such as part-time workers and suppliers, who also need to feel committed to such a vision. Examiner’s comments Question 4 was the least popular question concerning the pre-released case study. On the whole, part (a) was well answered although, in some cases, there was confusion about the distinction between mission and vision and other ways of expressing purpose. (b) Discuss how strategic pathways could be used to put such a vision into practice.

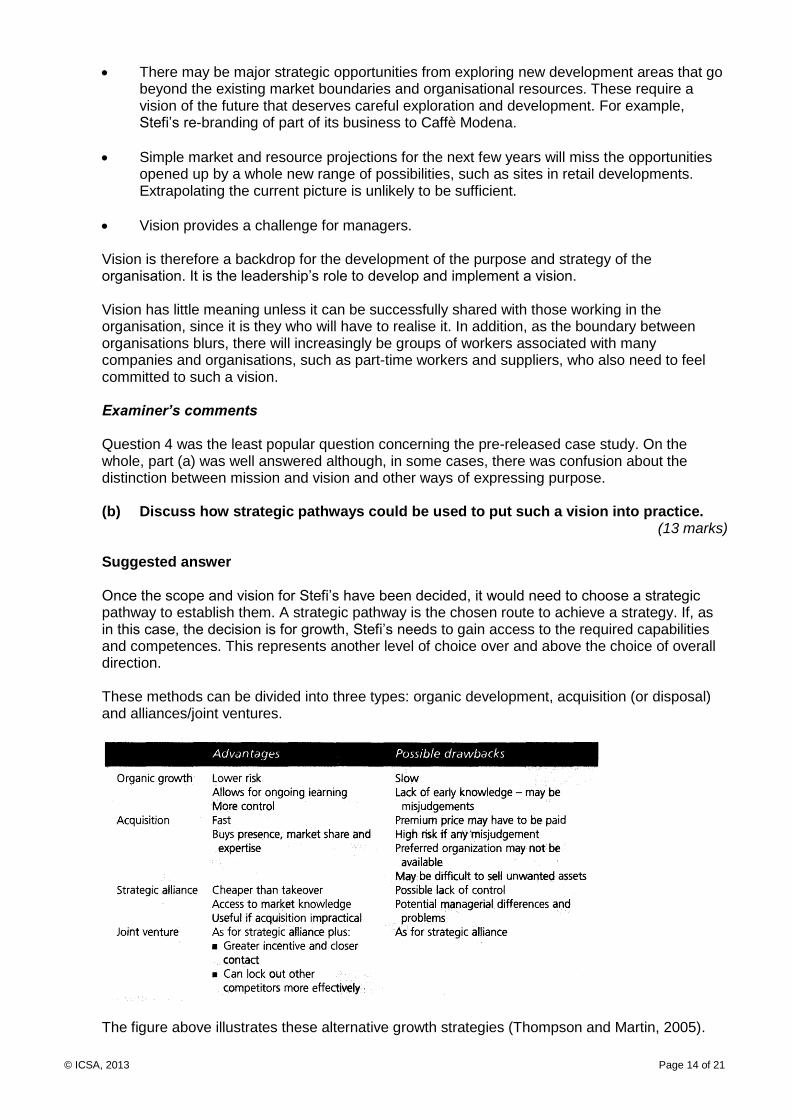

(13 marks) Suggested answer Once the scope and vision for Stefi’s have been decided, it would need to choose a strategic pathway to establish them. A strategic pathway is the chosen route to achieve a strategy. If, as in this case, the decision is for growth, Stefi’s needs to gain access to the required capabilities and competences. This represents another level of choice over and above the choice of overall direction. These methods can be divided into three types: organic development, acquisition (or disposal) and alliances/joint ventures.

The figure above illustrates these alternative growth strategies (Thompson and Martin, 2005).

© ICSA, 2013 Page 15 of 21

Organic development The first growth strategy, organic development (also known as internal development), involves building up the organisation’s own resource base and competences to develop strategy. This has been the approach at Stefi’s. There are some compelling reasons for this, especially the chance to spread costs. The final cost of developing new activities internally may be greater than that of acquiring other companies, but spreading these costs over time may be a better option. Stefi’s may not have the resources for major investments. The slower rate of change of organic development may also minimise the disruption to other aspects of the business and avoid the problems of acquisition integration that can occur. In fact, there may be few opportunities for acquisitions, other than in a piecemeal fashion of individual restaurants. The main advantages of organic development are that there is likely to be minimal change to continuing activities and there are unlikely to be the cultural problems associated with either an acquisition or an alliance. The main disadvantage is that it is likely to be slower than if an acquisition had been used, and probably slower than developing an alliance. Acquisition An acquisition is where an organisation takes ownership of another organisation, whereas a merger implies a mutually agreed decision for joint ownership between organisations. In practice, few acquisitions are hostile and few mergers are the joining of equals. If Stefi’s really wanted to move quickly now and signal its intentions clearly to stakeholders, then a series of acquisitions of individual restaurants or the acquisition of a small chain might dispense with the accusations of lacking strategic direction. The advantage that a series of acquisitions might offer includes high-speed access to resources for Stefi’s that could take years to establish through internal development. There is also less likelihood of retaliation from competitors. An acquisition only changes ownership and thus does not alter the capacity of the competitive arena as successful internal development would. Thus less reaction from competitors might be expected. The overriding problem with an acquisition lies in the ability to integrate the new company into the activities of the old, which often centres around problems of cultural fit. Where an acquisition is being used to acquire new competences, this ‘clash of cultures’ may simply arise because the organisational routines are so different in each organisation. Alliances/joint ventures A third option for Stefi’s might be a strategic alliance or joint venture with another chain. This is where two or more organisations share resources and activities to pursue a strategy. They vary from simple two-partner alliances coproducing a product, to one with multiple partners providing complex products and solutions. According to Johnson et al., motives for such alliances are of three main types: the need for critical mass, co-specialisation (allowing each partner to concentrate on activities that best match its capabilities), and learning from partners and developing competences that may be more widely exploited elsewhere. Stefi’s needs critical mass and perhaps more quickly than can be achieved by internal development. It might also be able to learn about consistency, for example, from the acquisition of one of the other restaurant chains. Examiner’s comments As noted above, this was not a popular question and answers to part (b) generally showed a limited understanding of the notion of strategic pathways.

© ICSA, 2013 Page 16 of 21

Questions 5 and 6, below, are not connected to the pre-released case study. 5. Analyse how the nature of the governance chain influences strategy-making by using

examples from organisations with which you are familiar. (25 marks)

Suggested answer The board of directors is the elected representative of the shareholders. It is charged with ensuring that the interests and motives of management are aligned with those of the owners (i.e. shareholders). For example, Intel Corporation is widely recognised as an excellent example of sound governance practices. Its board of directors has established guidelines to ensure that its members are independent (i.e. not members of the executive management team and do not have close personal ties to top executives) so that they can provide proper oversight, it has explicit guidelines on the selection of director candidates (to avoid ‘cronyism’), and it provides detailed procedures for formal evaluations of both directors and the firm’s top officers. Such guidelines serve to ensure that management is acting in the best interests of shareholders. The governance chain extends the roles and relationships of different groups involved in the governance of an organisation. In large, publicly quoted organisations, there are extra layers of management internally, while being publicly quoted introduces more investor layers as well. Individual investors (the ultimate beneficiaries) often invest in public companies through collective funds, such as pension funds, which then invest in a range of companies on their behalf. Funds are typically controlled by trustees, with day-to-day investment activity undertaken by investment managers. So the ultimate beneficiaries may not even know the companies in which they have a financial stake and may have little power to influence the companies’ boards directly. The relationships in such governance chains can be understood in terms of the principal-agent model (Eisenhardt, 1989). Here ‘principals’ pay ‘agents’ to act on their behalf. For example, company boards are principals, with senior executives their agents in managing the company. The issue for strategy in practice is that there are many layers of agents between ultimate principals and the managers at the bottom, with the reporting mechanisms between each layer liable to be imperfect. In large companies board members and other managers driving strategy are likely to be very remote from the ultimate beneficiaries of the company’s performance. The result may be that decisions are taken that are not in the best interests of the final beneficiary. This is just what has happened in the case of many of the corporate scandals of recent years. In this context, the governance chain helps highlight important issues that affect the management of strategy:

Responsibility to whom? A fundamental question in large corporations is whether executives should regard themselves as solely responsible to shareholders, or as trustees of the assets of the corporation acting on behalf of a wider range of stakeholders. Practice varies across the world.

Who are the shareholders? If managers see themselves as primarily responsible to shareholders, what does this mean in terms of the governance chain? Final beneficiaries are often far removed from the managers, so for many managers responsibility to such beneficiaries is notional. Strategists within a firm face a difficult choice, even if they espouse primary responsibility to shareholders. Do they develop strategies they believe to be in the best interest of a highly fragmented group of unknown shareholders? Or to meet the needs and aspirations of the investment managers for example? A similar problem exists for public sector managers. They may see themselves as developing strategies for the public good, but they may face direct scrutiny from an agency acting on behalf of the

© ICSA, 2013 Page 17 of 21

government. Is the strategy to be designed for the general public good, or to meet the scrutiny of the agency? For example, managers and doctors in the UK health service are dedicated to the well-being of their patients. But how they manage their services has been governed by the targets placed upon them by a government department, which presumably also believes it is acting in the public good.

The role of institutional investors. The role of institutional investors differs according to governance structures around the world. However, a common issue is the extent to which they do or should actively seek to influence strategy. Historically in the UK they have exerted their influence simply through buying and selling shares rather than engaging with the company on strategic issues. However, investors are becoming more actively involved in strategies (Davies et al., 2006). Johnson et al. suggest that there is evidence that institutional investors that seek to work proactively with boards to develop strategy do better for their beneficiaries.

Scrutiny and control. Given recent concerns about governance, there has been an increase in scrutiny and control of the activities of ‘agents’ in the chain to safeguard the interests of the final beneficiaries. There are increasing statutory requirements as well as voluntary codes placed upon boards to disclose information publicly and regulate their activities. Nevertheless, managers are still left with a great deal of discretion as to what information to provide to whom and what information to require of those who report to them. For example, how specific should a chief executive be in explaining future strategy to shareholders in public statements such as annual reports? Are the typical accountancy measures (such as return on capital employed) the most appropriate or should measures be specifically designed to fit the needs of particular strategies or particular stakeholder/shareholder expectations? How managers answer these questions depends both on what they decide the strategic purpose of the organisation is, and their view about to whom they see themselves responsible.

A key point is that strategists and managers need to be aware that the governance chain typically operates imperfectly as a result of:

a lack of clarity concerning the end beneficiaries;

unequal division of power between the different ‘players’ in the chain;

with different levels of access to information available to them;

potentially agents in the chain pursuing their own self-interest; and

using measures and targets reflecting their own interests rather than those of end beneficiaries.

In such circumstances it is not surprising that governance structures are changing around the world and there have been reforms to corporate governance. These are well known to chartered secretaries. Dess et al. (2008) focus on three important mechanisms to ensure effective corporate governance: an effective and engaged board of directors, shareholder activism, and proper managerial rewards and incentives. In addition to these internal controls, a key role is played by various external control mechanisms. These include the auditors, banks, analysts, an active financial press, and the threat of hostile takeovers. Examiner’s comments Questions 5 and 6 were the least popular questions and question 5 was the least well answered. The answer required an explanation of the nature of governance chains and their impact on strategy but, within this context, there was scope about how to answer the question. Credit is always given for appropriate answers that don’t necessarily follow the suggested answer.

© ICSA, 2013 Page 18 of 21

6. (a) Using examples from an organisation with which you are familiar, distinguish the nature of strategic decisions from other decisions an organisation makes. (15 marks)

Suggested answer The detailed answer to both parts of Question 6 depended on the context of the candidate’s chosen organisation. The key thing was that appropriate examples were aligned to illustrate the characteristics of strategic decisions and the nature of levels. What distinguishes strategic decisions from other decisions being taken in the organisation? According to Johnson, Scholes and Whittington (2008) these are concerned with:

The long-term direction of an organisation rather than the short-term.

The scope of an organisation’s activities. The issue of scope of activity is fundamental to strategic decisions because it concerns the way in which those responsible for managing the organisation see its boundaries and what they want the organisation to be like and to be about.

Securing advantage. Strategic decisions are normally about trying to achieve some advantage for the organisation over the competition or providing higher quality, value-for-money services than others in the public or third sector.

Strategic fit with the environment. Strategy can be seen as the matching of the activities of an organisation to the environment in which it operates. For example, locating in particularly favourable markets or seeking to appeal to particular market segments.

The organisation’s resources and competences. Strategy can also be seen as exploiting the strategic capability of an organisation in terms of its resources and competencies to provide competitive advantage or yield new opportunities. IKEA, for example, has built up its logistics expertise over many years and provided a distinct way of operating, greatly appreciated by customers.

Values and expectations. The strategy of an organisation is affected not only by environmental forces and resource availability, but also by the values and expectations of those who have power in and around it. For example, whether a company is expansionist or more concerned with consolidation may say much about the values and attitudes of those who influence strategy – the stakeholders of the organisation. These include: shareholders or financial institutions; management and the workforce, buyers and perhaps suppliers; and the local community.

These characteristics mean that strategic decisions are likely to:

Be complex in nature, especially in organisations with a wide geographical scope, such as multinational firms, or with a wide range of products or services.

Be made in situations of uncertainty, where it is impossible for managers to be sure. At a company such as Yahoo!, the internet environment is one of constant innovation that is hard to predict.

Be linked to operational decisions, for example, the internationalisation of IKEA required a whole series of decisions at operational level. Management and control structures to deal with the geographical spread of the firm had to change. HR policies and practices had to be reviewed. This link between overall strategy and operational aspects of the organisation has two highly significant implications:

© ICSA, 2013 Page 19 of 21

(i) If the operational aspects of the organisation are not in line with the strategy then, no matter how well considered the strategy is, it will not succeed.

(ii) It is at the operational level that real strategic advantage can be achieved. Companies have succeeded not only because of a good strategic concept, but also because of the detail of how the concept is put into effect.

Demand an integrated approach to managing the organisation. Managers have to cross-functional and operational boundaries to deal with strategic problems and come to agreements with other managers with different interests and priorities.

Require the management of relationships and networks outside the organisation, for example, with suppliers, distributors and customers. Strategic decisions may also involve change in organisations that is difficult both to plan and implement.

Strategic change is a critical component of strategy. As such it can be difficult because of the existing resources and culture. Candidates might also have used Mintzberg’s 5 P’s to explain the nature of strategic decisions. Examiner’s comments Question 6 was answered well, on the whole, by those who attempted it. Good answers to part (a) showed a clear understanding of the nature of strategic decisions and looked at consequences and implications of these.

(b) Explain the concept of levels of strategy and why these might vary.

(10 marks)

Suggested answer It is possible to identify three planning levels although, in practice, there may be more or fewer. Typical terms are strategic, intermediate and operational levels. Candidates might have captured the key distinctions in a diagram, for example:

Senior managers display a broader scope in their plans both in terms of areas of the business and the time span covered. This latter aspect is important. They have different planning horizons. The planning horizon is the time that elapses between making and executing a plan. Longer time horizons suggest that strategic planning means greater uncertainty than intermediate or tactical planning. Forecasts are likely to be less detailed over a longer period and there is more time for unexpected events to occur.

Planning level

Purpose

Managers

Time Horizon

Strategic

Achieving business objectives through making long-term relationships between the organisation and its environment; obtaining key resources.

General managers and heads of functions.

1 – 10 years or more

Intermediate

Giving direction to, and allocating resources among, sub-units and functions to give each clear objectives and to ensure co-ordination.

Middle managers working together and also with their departmental teams.

6 months –2 years

Operational

Accomplishing tasks with available resources to contribute to departmental objectives.

Operating unit managers, supervisors and individual staff.

A few hours – 1 year

© ICSA, 2013 Page 20 of 21

The plans at each level have different purposes. In general, senior managers are expected to incorporate the uncertainty of the environment into their planning. In giving directions to those at lower hierarchical levels, they seek to absorb some of this uncertainty. Intermediate and operational plans can be more specific and concrete because they cover shorter periods and relate (or at least should relate) to the objectives of the next higher level that should already have been clarified. Agreement over objectives reduces uncertainty for managers. Senior managers help to insulate the operating core of the organisation from environmental uncertainty. At the operations level, some linking, or boundary spanning, roles are assigned to specialist departments such as marketing or purchasing. Strategies therefore exist at a number of levels in an organisation. It is possible to distinguish at least three different levels of organisational strategy: (i) Corporate strategy

This is concerned with the overall purpose and scope of the organisation to meet the expectations of owners or major stakeholders and add value to the different parts of the enterprise. In the case of IKEA this took form in the way in which the firm was structured to maintain its independence according to the wishes of its founder. In publicly quoted businesses, corporate-level strategy is heavily influenced by the expectations of shareholders and the stock market. Being clear about this strategy forms the basis of other strategic decisions. It may well take form in an explicit or implicit ‘mission’ statement that reflects such expectations.

Corporate strategy is concerned with the question: ‘What businesses should we be in?’ (ii) Business unit strategy

This is about how to compete successfully in a particular market. The concerns are therefore with how to achieve advantage over competitors; what new opportunities can be identified or created in markets; which products or services should be developed in which markets; and the extent to which these meet customer needs to achieve the objectives of the organisation, whether long-term profitability or market growth.

Whereas corporate strategy concerns the organisation as a whole, strategic decisions at this level need to be related to a strategic business unit. This is a part of the organisation for which there is a distinct external market for goods or services.

At this level, strategic decisions are based on how customer or client needs can best be met to achieve some sort of competitive advantage for the organisation. It is therefore very important that a strategic business unit (SBU) understands the needs of its customers (or clients) and who its competitors are. So business unit strategy is concerned with the question: ‘How do we succeed in this particular business?’

(iii) Operational strategies

Operational strategies are concerned with how the component parts of the organisation in terms of resources, processes, people and their skills effectively deliver the corporate and business-level strategies. In most organisations, successful strategies depend to a large extent on activities that occur at the operational level. For example, in IKEA it is of crucial importance that design, store operations and sourcing operations dovetail into higher-level decisions about product range and market entry. The integration of operational decisions and strategy is of great importance. Functional/operational strategy is concerned with the question: ‘How does this function or operation contribute to the business strategy?’ Operational and functional strategies include: marketing strategies, production strategies that involve issues such as factory location, manufacturing techniques and subcontracting.

© ICSA, 2013 Page 21 of 21

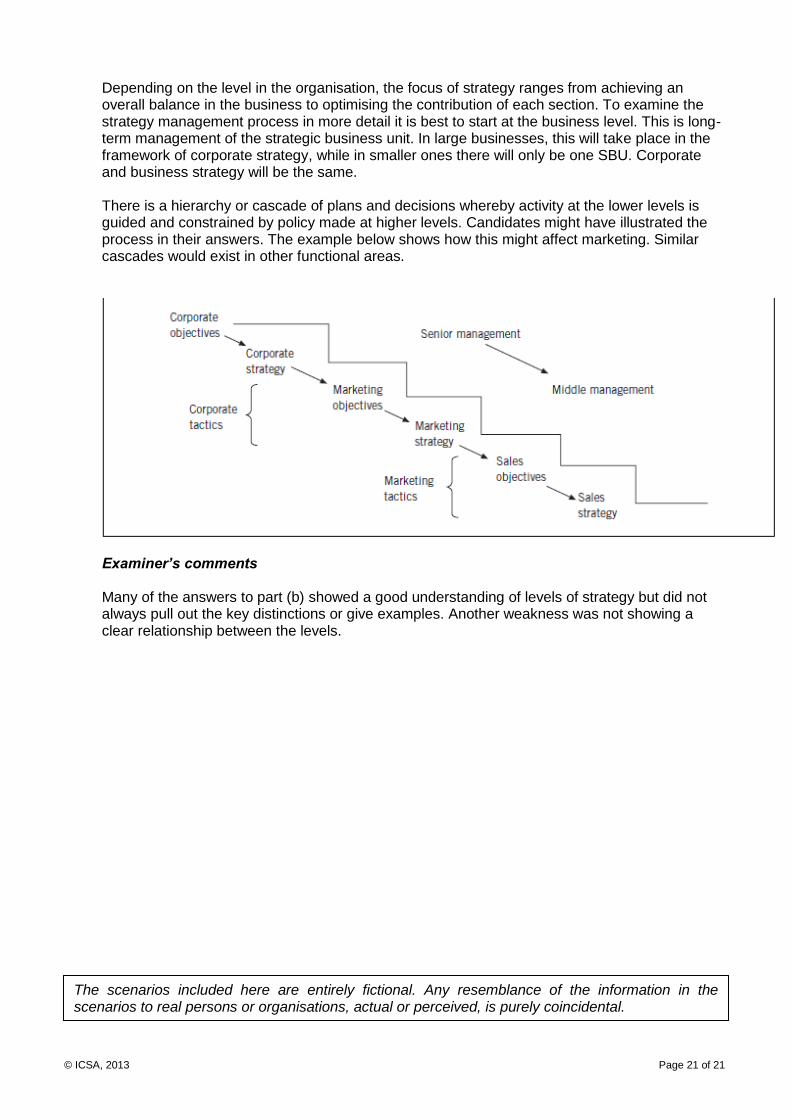

Depending on the level in the organisation, the focus of strategy ranges from achieving an overall balance in the business to optimising the contribution of each section. To examine the strategy management process in more detail it is best to start at the business level. This is long-term management of the strategic business unit. In large businesses, this will take place in the framework of corporate strategy, while in smaller ones there will only be one SBU. Corporate and business strategy will be the same. There is a hierarchy or cascade of plans and decisions whereby activity at the lower levels is guided and constrained by policy made at higher levels. Candidates might have illustrated the process in their answers. The example below shows how this might affect marketing. Similar cascades would exist in other functional areas.

Examiner’s comments Many of the answers to part (b) showed a good understanding of levels of strategy but did not always pull out the key distinctions or give examples. Another weakness was not showing a clear relationship between the levels.

The scenarios included here are entirely fictional. Any resemblance of the information in the scenarios to real persons or organisations, actual or perceived, is purely coincidental.