Embed Size (px)

Citation preview

Student loans in higher education 2. Asia

Report of an HEP educational forum

by Maureen Woodhall

Paris 1991

International Institute for Educational Planning (Established by Unesco)

Student loans in higher education

The views and opinions expressed in this volume are those of the authors and do not necessarily represent the views of Unesco or of the H E P . The designations employed and the presentation of material throughout this report do not imply the expression of any opinion whatsoever on the part of Unesco or H E P concerning the legal status of any country, territory, city or area or its authorities, or concerning its frontiers or boundaries.

The costs of the educational forum and of this report have been covered through a grant-in-aid offered by Unesco and voluntary contributions m a d e by several M e m b e r States of Unesco, the list of which will be found at the end of this volume.

This volume has been typeset using IIEP's computer facilities and has been printed in IIEP's printshop.

International Institute for Educational Planning 7 - 9 rue Eugene-Delacroix, 75116 Paris

©Unesco 1991

Contents

Preface vii

Executive summary l

Report of an H E P educational forum 4

I. Introduction 4

IL S u m m a r y of the forum discussion 7

III. B a c k g r o u n d orientation paper 20

IV. Annexes 35

A . Summaries of student support systems 35 I. Australia 37 II. People's Republic of China 41 III. Hong Kong 46 IV. India 51 V . Indonesia 57 VI. Japan 65 VII. The Republic of Korea 72 VIII. Malayasia 76 IX. Philippines 82 X . Singapore 85 XI. Thailand 89

B . Participants in the forum 93

v

Preface

This booklet is the second of a series which is reporting on Educational Forums being organized by the IIEP on the issue of student loans in higher education. The first booklet, published in 1990, examined the situation in Europe and the U S A . The present booklet reports on an educational forum held in Malaysia in November 1990 which focused on the situation of student loans in Asian countries; forums devoted to other regions of the world will follow.

The purpose of these meetings is to analyze the main issues raised by the introduction of student loans and discuss the ways these issues are being addressed both in industrialized and developing countries. Through open and candid discussion at the forums, and exchanges of experiences between countries, it is hoped to highlight the main implications for policy-making in higher education and draw some conclusions concerning the management of student loans in the future.

Each booklet in the series will normally include a report of the forum and summaries of the experiences of the countries represented. The IIEP, in embarking on this n e w initiative, hopes that the series will stimulate further co-operation in the form of exchanges of experiences among Unesco M e m b e r States.

Jacques Hallak Director, IIEP

vu

Executive summary

The International Institute for Educational Planning (HEP) held a forum in Gcnting, Malaysia in November 1990, to examine international experience of student loans in Asia. Participants from ten countries attended the meeting from 6 - 8 November, 1990 and discussed the provision of loans and other forms of student support in Australia, the People's Republic of China, H o n g Kong , India, Indonesia, Japan, Malaysia, the Philippines, Singapore and Thailand.

The forum was concerned with four main topics:

1. Existing patterns of finance for higher education and systems of student support

The countries represented at the forum differed considerably in patterns of finance and student support. Private sources of finance are very important in some countries, including Japan and the Philippines, where the majority of students attend private institutions and pay tuition fees. In the People's Republic of China and India, on the other hand, higher education is financed mainly by public expenditure. All the countries represented provide financial support for students, through scholarships, grants and, in some cases loans, but the proportion of students receiving assistance varies considerably.

Loans are the main form of financial support for students in Japan and H o n g Kong ; several countries provide a combination of grants, scholarships and loans and n e w loan schemes have recently been established in the People's Republic of China, Malaysia and the

1

Student loans in higher education

Philippines. Australia has no system of student loans, but has recently introduced a n e w Higher Education Contribution Scheme ( H E C S ) which provides an option for deferred payment of the required financial contribution, which will be collected after the student completes higher education, by means of the tax system. Thailand also proposes to increase tuition fees in public universities from 1991, as part of the Long Range Plan for Higher Education, and student loans will be introduced to help students pay the higher fees.

2. Reasons for interest in student loans

The meeting demonstrated strong interest in loans as a form of financial support for students in m a n y countries in Asia. There arc four main reasons for this interest:

(i) Financial pressures on public budgets, which mean that m a n y governments are seeking ways to increase private contributions to the costs of higher education.

(ii) Changing educational priorities have resulted in several governments giving higher priority to primary and secondary education, and trying to increase cost recovery in higher education, in order to free resources for lower levels of education.

(iii) Attempts to improve the efficiency of higher education. (iv) Concern about equity leads some advocates of loans to argue

that loans will result in a more equitable sharing of the costs of higher education than a system of grants, scholarships and free tuition, financed from government revenue.

3. Administration of loan programmes

A wide variety of schemes exist, with different forms of administration, levels of subsidy and repayment terms. A major concern in m a n y countries is h o w to reduce default, but while the proportion of loans that are actually repaid is low in India and in some other countries,

2

Executive summary

repayment rates are n o w very satisfactory in H o n g Kong, Japan and Singapore. While there are no simple solutions, countries can benefit from international experience, and the forum provided a valuable opportunity for an exchange of information.

4. Feasibility of student loans

Although governments in some countries (e.g. Australia) have concluded that loan schemes have too many disadvantages to be feasible, and in Indonesia the government has recently abolished a government subsidized loan programme, several Asian countries have successful loan schemes and there is evidence that loans are feasible in many countries and that obstacles can be overcome. However, the obstacles are more severe in large countries with a relatively low level of economic development, such as India, than in small countries with a buoyant economy, such as Singapore.

Nevertheless, despite the problems in some countries, student loans remain an important form of student support in the Asian region, and their importance is likely to grow in the future.

3

Student loans in higher education 2. Asia

Report of an H E P educational forum by Maureen Woodhall

I. Introduction

This report provides a summary of an educational forum held in Gcnting Highlands, Malaysia, from 6-8 November 1990, to discuss experience of student loans in Asia. This formed one of a series of meetings organized by the H E P on the subject of student loans as a means of financing higher education. The first meeting was held in Paris in September 1989, and a report of this was published by the H E P . 1 The educational forum on student loans in Asia was the second in this scries.

The purpose of the forum was to examine recent experience of student loan programmes in Asian countries, to explore arguments for and against loans as a means of providing financial support for students, and to understand the reasons w h y some countries in the region have adopted loans as a way of financing higher education, while others have rejected the idea.

Ten countries were represented at the meeting: Australia, the People's Republic of China, H o n g Kong , India, Indonesia, Japan, Malaysia, the Philippines, Singapore and Thailand.2 Seventeen participants attended the forum, including representatives of the ten Asian countries as well as specialists from the Asian Development Bank

1. Woodhall, M . (1990). Student loans in higher education : 1. Western Europe and the USA. Educational Forum Scries № . 1, H E P , Paris.

2 . Information was also received about the student loan system in the Republic of Korea, but the proposed participant was unable to attend the meeting.

4

Report of an HEP educational forum

( A D B ) , the World Bank (International Bank for Reconstruction and Development, I B R D ) and the International Institute for Educational Planning (HEP). All national participants provided information about student support in their countries in the form of descriptive papers and replies to a short questionnaire. Annex A provides a short summary of the student aid system in eleven Asian countries. A full list of participants is given in Annex B.

Student loans are used quite extensively in Asia to provide financial support for students in higher education, to enable them to pay the costs of tuition and/or living expenses. In Japan, loan schemes for students have existed for over 100 years and loans are n o w the main form of student support. A loan programme was established in India in the 1950s and more recently loan schemes have been set up in the People's Republic of China, H o n g K o n g , Indonesia, the Republic of Korea, Malaysia, the Philippines and Singapore. Australia has recently introduced a Higher Education Contribution Scheme, under which students have an option to defer payment until after they leave higher education, when it will be collected through the tax system. Thailand does not yet have a loan programme, apart from a few small-scale loans offered by institutions or private banks in the case of financial hardship. There have been proposals to introduce loans in Thailand, however, and the meeting heard that the government of Thailand plans to introduce student loans in 1991, as part of a general reform of higher education finance.

The subject of student loans, and the problems associated with this form of finance, is of considerable interest to policy-makers in all the countries represented at the forum as well as in other countries in the region, including Pakistan, which has a small loan scheme, Papua N e w Guinea, which considered the feasibility of loans a few years ago, Macau , which has a system of loans and has recently introduced changes, Sri Lanka, which had a loan scheme which was regarded as unsuccessful and eventually abandoned, and Vietnam, where a recent World Bank report identified scholarships and living stipends for university students as an area "where reducing subsidization and increasing the contributions of beneficiaries might be possible".

5

Student loans in higher education

The forum was concerned with four main topics:

(i) Existing sources and methods of finance for higher education and systems of financial support for students,

(ii) Reasons w h y countries have introduced, or arc considering the introduction of student loans, and arguments for and against loans as a means of financing higher education,

(iii) The design and administration of student loan programmes, including particularly: • h o w to determine eligibility,

• choice of administrative agency, • terms of loans and their repayment.

(iv) The feasibility of student loans and ways of overcoming problems or obstacles.

This report includes:

S u m m a r y of the forum discussions

Background orientation paper

Annexes: Annex A : Summaries of student support systems in Australia, the People's Republic of China, Hong Kong , India, Indonesia, Japan, the Republic of Korea, Malaysia, the Philippines, Singapore and Thailand. These summaries of student loans and other forms of student support arc edited extracts from country papers provided by the participants of the Education Forum. More detailed and extended versions of some of these papers will be published in a future edition of the journal, 'Higher Education'. For comparative purposes, figures are shown both in local currencies and in U S $ (converted on the basis of exchange rates in March 1991. Annex B : List of participants in the forum.

6

II. Summary of the forum discussions

Discussions took place over two and a half days and were informative and lively. A great diversity of experience was reviewed. Economic and educational conditions varied considerably in the countries represented at the forum, which ranged in size from India, with a student population of over 9 million in all forms of higher education, and Japan with over 3 million students, to Hong K o n g and Singapore with enrolment of only about 55,000. The countries included the People's Republic of China, with a system of Communist government and central planning, and Japan and Singapore, with a strong commitment to market economies. Private universities are important in the Philippines and Japan, and non-existent in the People's Republic of China. It was clear from the start that there was no 'right answer' to the issues being discussed. Indeed, one of the main purposes of the meeting was to encourage an exchange of ideas and experiences from very different systems.

1. Existing patterns of financial support for students

The meeting started with participants describing the systems of higher education, finance and student support in their countries. This information is summarised briefly here and Annex A presents more details about the system of student support in each country.

Loans are the main form of financial support for students in Japan and H o n g Kong , a combination of loans, grants and scholarships are used in several countries, including the Republic of Korea and Singapore and n e w schemes have recently been established in the People's Republic of China, Malaysia and the Philippines.

The most important source of financial assistance for students in Japan is the Japanese Scholarship Foundation which provides loans for both secondary school pupils and students in higher education. T w o kinds of loans are available, interest-free loans for students from low-income families and loans at 3 per cent (Category II loans) for those

7

Student loans in higher education

w h o are not eligible for interest-free loans. Altogether, about 14 per cent of Japanese students receive loans from the Japanese Scholarship Foundation,

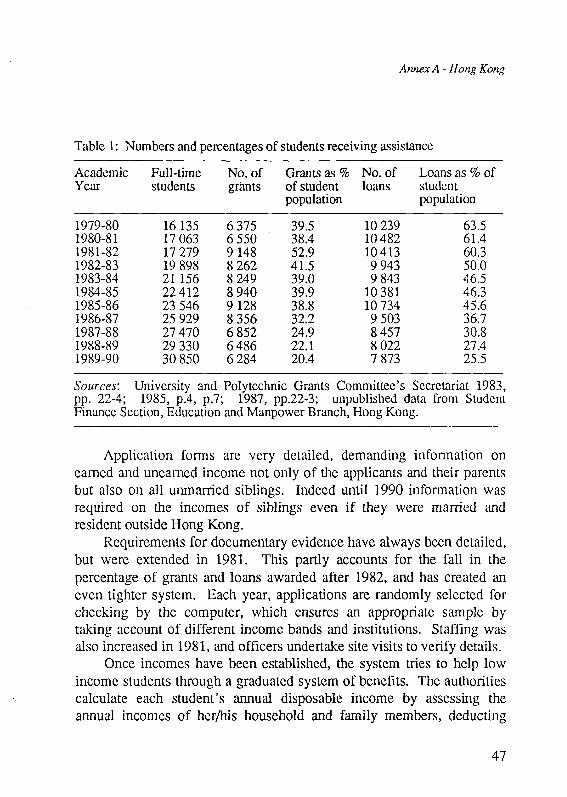

In Hong Kong students receive grants towards tuition costs and loans to help finance living expanses. The loan scheme was established in 1969 to help students in financial need. A strict means test is applied and the proportion of students receiving loans has fallen sharply from 63 per cent in 1979 to 26 per cent in 1989. The scheme is popular and is regarded in H o n g K o n g as efficient and as contributing significantly to equity of access to higher education.

In the Republic of Korea, commercial banks provide loans, but the government subsidizes the interest rate, so that instead of paying 11 per cent, which would be required by the banks, students pay only 5.5 per cent, and the balance is financed by the government. In addition, there are a number of scholarship schemes for academically gifted and low-income students and the National Agricultural Co-operative Federation offers both short-term and long-term loans for children of members.

Singapore has two loan programmes: the Student Loan Fund, which has existed for some time and the newly established Tuition Fee Loan, introduced in 1989. In addition, the Central Provident Fund (CPF), which is a national insurance/pension fund n o w allows parents to draw on their C P F contributions, in order to finance their children's education. Singapore is a small country with a buoyant economy and well developed banking system. These features help to explain the scheme's success, and the very low default rate on student loans in Singapore.

Malaysia relied entirely on scholarships for needy students until 1987, when a n e w loan programme was established. This provides two kinds of loan: (1) an ordinary loan scheme for a small proportion of students and (2) a convertible loan, under which students w h o achieve high examination grades get part of their loan converted to a grant.

Private institutions are particularly important in the Philippines, where 85 per cent of all enrolments are in private universities or colleges. A n e w Private Education Student Financial Assistance

8

Summary of the forum discussions

Programme (PESA) has been established after new legislation, the government Assistance to Students and Teachers in Private Education Act, was passed in 1989. Previously, there was a small scheme, the Student Loan Fund, which was established in 1976, but only a very small proportion of students were able to benefit from loans.

A long-established loan scheme exists in India, but this also provides loans for a very small proportion of all students in higher education. The total number of students has grown from 1.3 million in 1963, when the scheme was set up, to 9.2 million in 1988, but the annual number of loans provided under the National Loan Scholarship Scheme has remained fixed at 20,000. The Indian scheme is not regarded as very successful, in view of the high rate of default, and there have been a number of proposals to change the scheme or even abolish it.

The government of Indonesia has recently abolished a subsidized government student loan programme, Kredit Mahasiswa Indonesia (KMI) which was set up in 1982. The abolition of this scheme in 1990 was part of a n e w policy on banking deregulation, and a number of government subsidized credit programmes were abolished, including export credits and programmes for farmers and small-scale industry. The idea was to shift responsibility for loans to commercial banks, but so far the only n e w scheme to be set up by private banks is a small Professional Student Loan Programme (PSL) for post graduates taking professional courses, particularly in business administration. This is a small elite group of students with excellent employment prospects, and therefore the loans are considered by the banks to be a sound commercial investment.

While the Indonesian government has abolished its students loan scheme, other countries have recently established new programmes, for example Malaysia and the People's Republic of China, and others are intending to introduce loans, for example Thailand.

In the People's Republic of China, all levels of education have been free since the People's Republic was established in 1949, and until the 1980s all students in higher education received grants to cover their living expenses. In 1983, however, grants towards living costs were restricted to those in real financial need, although tuition and

9

Student loans in higher education

accommodation remained free for all students. A loan scheme was introduced, on an experimental basis, in 1987. U p to 30 per cent of students in each institution m a y apply for a loan if they are unable to finance their living costs. The loans are strictly means-tested and are interest-free. So far 383,000 students have been granted loans.

So far in Thailand, student support has been mainly in the form of scholarships, with only a few 'emergency loans' provided by institutions for students with urgent financial problems. The government has recently signalled a change of policy, however, as a result of a review of higher education policy and the completion of a long-term plan for higher education in the next fifteen years. The plan emphasizes the need for universities to become self-reliant, through the development of new sources of finance, including the raising of tuition fees. A student loan scheme has been proposed to assist students with the payment of higher fees.

The only country represented at the meeting that has no student loan programme is Australia, but a newly established Higher Education Contribution Scheme ( H E C S ) provides the option of deferred payment of the required contribution, through the income tax system. There has been considerable interest in m a n y countries in the new Australian system, which is often referred to as a 'graduate tax', although the Australian government emphasizes it is not, strictly speaking, a tax, and indeed it has certain resemblances to an income-contingent student loan. From 1989, all students in higher education in Australia must pay the Higher Education Contribution, which is roughly equivalent to 20 per cent of the average costs of a degree course. Students have a choice between paying an 'up-front' lump sum contribution, with a 15 per cent discount, or deferring payment until after completion of their course, in which case they will pay between 2 and 4 per cent of their income each year until the debt is discharged.

This brief review of current systems of finance and student support demonstrates a high level of interest in student loans, whether on the part of governments with well-established programmes or governments considering reforms of existing patterns of finance and the introduction of loans as a means of cost recovery. The first item for discussion,

10

Summary of the for um discussions

therefore, was what were the arguments for and against loans in countries that have recently introduced n e w programmes or considered the option of student loans.

2. Reasons for interest in student loans in Asia

There was general agreement that countries had introduced or were considering student loans for four main reasons:

Financial pressures on public budgets, which mean that m a n y governments are seeking ways to increase private contributions to higher education costs. Changing educational priorities m e a n that in several cases, governments are n o w giving higher priority to primary and lower secondary education, and see increased cost recovery in higher education as one option that m a y free resources for lower levels of education. Increased efficiency in higher education is a major goal in m a n y countries and some governments believe that a system of loans can improve student motivation and completion rates and help to reduce drop-out. A more equitable distribution of higher education costs can be achieved through loans, according to some advocates of student loans.

In Thailand, the government is proposing to increase fees and introduce loans because of growing pressure on government spending, the high priority given to increasing compulsory education from 6 to 9 years, which will require a reduction in government subsidies for public universities and a belief that it is equitable to expect those w h o will enjoy a substantial private return from university education to contribute to its cost. There are three routes to higher education in Thailand: 18 public universities which operate selective admission policies, two open universities with unrestricted admissions, and 27 private universities. Competition for places at the 18 selective public universities is intense, and students w h o are able to gain a place enjoy a very substantial

11

Student loans in higher education

subsidy, while those w h o study part-time at the open universities or w h o pay full-cost fees at private universities, contribute a far higher proportion of the costs of their education. Considerations of social justice, as well as financial pressure on the government budget, have led to a re-examination of the whole system of finance and subsidies for students. A n e w policy of increased cost recovery in public selective universities, and an emphasis on financial self-reliance, has been proposed by the committee responsible for the Long-term Plan. The committee considered the option of a shift towards full-cost fees for public, as well as private universities, but this was rejected in favour of a gradual increase in fees over the 15-year period, until fees in public selective universities will cover 50 per cent of costs, instead of 5-10 per cent as at present. T o help students from poor families to meet these increased costs, the Government will introduce a loans scheme, as well as increasing scholarships.

In the People's Republic of China, also, the introduction of loans was part of a policy shift which requires greater private contributions towards the costs of education as a result of financial pressure on government budgets and high priority being given to improving primary and secondary education. A n Education Reform announced in 1985 aims to universalize 9 years of compulsory education, and state and provincial governments are concerned about the high proportion of their limited education budgets being allocated to higher education. The introduction of loans in 1987 was seen as one w a y to increase revenue for universities without increasing the burden on public spending. Universities are allocated funds for loans to students, and are responsible for selecting needy recipients and collecting repayments. W h e n the loan is repaid, the university is not required to reimburse the provincial or state government, but can use the funds to improve teaching conditions. So far, the scheme is very limited, but it is an interesting innovation for students to be given loans rather than grants, in a Socialist country, committed to public ownership.

Because of differences in political ideology, it is perhaps surprising to find the People's Republic of China and Thailand adopting a similar approach to student support. Whereas the idea of student loans has been

12

Summary of the forum discussions

justified in Thailand, and in Singapore, by evidence of the high private rate of return to university education, the concept of the rate of return which individuals will enjoy as a result of investment in higher education is almost unknown in the People's Republic of China. In Japan, on the other hand, higher education is recognised as a profitable investment for the individual student and his or her family, and there is a strong belief that financial support for students should be in the form of loans, rather than grants. In the 1970s, government subsidies for higher education were increased, including subsidies for private as well as public universities. In the 1980s, pressures on government spending have led to a shift towards higher private contributions again, and the creation of a n e w kind of Category II student loan in 1984 can be seen as part of this trend. Students with Category II loans must pay interest, whereas the older Category I loans are interest free.

The idea that loans can help improve efficiency in higher education has been expressed in both Indonesia and Malaysia. The introduction of loans in Indonesia in 1982, was seen as one way of using the government's newly increased oil revenues to improve efficiency in higher education by providing financial support for students to help reduce their length of study. Under the K M I scheme, loans were available for students in their final years of study, to help them to complete their degree course. It was hoped that this would reduce dropout. However, problems of default, concerns about the difficulties of administering the loan scheme and decreased government revenues as a result of the fall in oil prices, led to the abolition of the scheme in 1990.

In Malaysia, also, the government hopes that the newly established loan scheme can increase efficiency by improving student motivation. Students w h o receive a convertible loan k n o w that if they complete their course of study in the stipulated period of time, and achieve high grades in their final examination, part of their debt will be cancelled.

Finally, loans have been advocated in some countries as a way of increasing equity. The aim of the student loan programme in Hong Kong, for example, is to ensure that no eligible student w h o has been offered a place in an institution of tertiary education will be unable to accept it for lack of means. M a n y countries attempt to achieve this by making higher

13

Student loans in higher education

their living expenses, but advocates of loans argue that repayable loans are a more equitable form of finance than grants, scholarships and free tuition. There is evidence in m a n y countries that those most likely to benefit from higher education are the children of upper-income or at least well-to-do parents. Free tuition and grants, at the expense of taxpayers, m e a n a transfer of income from those w h o pay taxes but do not benefit from higher education to those w h o , in the future, will enjoy high incomes, as a result of their education. For this reason, 'social justice' is given as one of the main justifications for an increase in fees and the introduction of loans in Thailand. Similarly, in the Philippines a 'socialised tuition scheme' has been proposed in the University of the Philippines, under which students will be expected to pay tuition fees in accordance with paying capacity, which will mean that children of wealthy parents will pay fees, while poor students will receive financial assistance.

The Higher Education Contribution Scheme in Australia, was also proposed on grounds of increasing equity. The Committee on Higher Education Funding, under the chairmanship of Neville Wran , reported:

"The Committee found that access to higher education in Australia continues to be inequitable. People w h o make most use of the Australian higher education system tend to be, or become, privileged and affluent members of the community... Society in general benefits from higher education, but considerable private benefits accrue to those w h o have the opportunity to participate. Graduates typically get better jobs, experience very little unemployment and earn relatively high incomes over their lifetime, compared with non-graduates... ...Taxpayers carry most of the burden of the cost of higher education. However, most taxpayers are not privileged members of society and neither use nor directly benefit from higher education". (Committee on Higher Education Funding, 1988 p.x).

14

Summary of the forum discussions

The Committee therefore proposed the Higher Education Contribution, payable by all w h o participate in higher education, as a "funding partnership in which the beneficiaries m a k e a direct and fair contribution to the cost of higher education, to supplement the funds provided by taxpayers". The Committee considered loans as an alternative option, but concluded that overseas experience with student loan schemes demonstrated a number of serious problems, including:

"default claims for more than nine per cent of all student loans, high administrative and legal costs, rising student indebtedness and falling participation amongst financially and other disadvantaged groups". (Committee on Higher Education Funding, 1988, p.27.)

These arguments touched on two main items for discussion at the Malaysia Forum: (i) actual experience with the administration of loan schemes, and (ii) their feasibility in developing countries. The following two sections examine these in turn.

3. Design and administration of student loans

Existing loan programmes in Asia are subject to considerable variations in the terms and conditions of loans and the w a y in which they are administered. Discussion focused on four main topics:

administrative responsibility for loans, conditions for eligibility, interest rates and required repayment periods,

e success or failure in collecting repayments and minimising defaults.

There is no single pattern in the region. In m a n y countries, scholarships and loans are administered by a government agency, such as the 'Japan Scholarship Foundation', or a government department, such as the Education and M a n p o w e r Branch in Hong Kong, or the Public Service Department in Malaysia. M a n y participants felt that only a public department or agency would have the necessary expertise and

15

Student loans in higher education

objectivity. O n the other hand, commercial banks have responsibility in some countries, or other types of financial institution, such as the 'Central Provident Fund ' in Singapore.

Clearly, the choice of administrative agency will depend on the objectives of the scheme and the existing infrastructure in a country. In some countries, the banking system is not sufficiently developed and lacks a national network, while in others, commercial banks already operate a wide range of credit programmes. In several countries, higher education institutions themselves have a key role in selecting those w h o are eligible for assistance, and in some cases institutions have responsibility for disbursement and collection of loans.

Most countries select loan recipients using a combination of academic and financial criteria. The most detailed scrutiny is exercised in Hong Kong, where applicants must provide very detailed information, not only on the level of parental income and assets, but the income of other members of the family. A sample of applications is checked by computer and applicants are interviewed, to check the accuracy and reliability of data provided, and ensure that only those in genuine financial need receive the highly subsidized loans.

In several other countries, however, there are doubts about whether such detailed scrutiny of students' financial means is either feasible or desirable. In India and the Philippines, for example, where only a very small proportion of the population pays income tax, there is doubt about the reliability of income data and this is also a key question in Japan.

Governments want to select students w h o are most deserving in terms of academic merit and most needy in terms of family income or other financial indicators. In Indonesia, the government-subsidised K M I programme was available only to students in their final years of study, in the belief that these are more likely to be successful, but this often meant that those from the lowest income categories could not enter higher education or dropped out after only one or two years. Thus, efficiency and equity criteria m a y conflict w h e n limited funds are allocated between m a n y applicants.

The terms of loans vary considerably, particularly the interest charged (if any) and the length of repayment. Loans are interest free in

16

Summary of the forum discussions

the People's Republic of China and India; Japan Category I loans are interest free, while Category II loans, which are provided on less strict criteria require payment of 3 per cent interest. O n the other hand, students in the Philippines must pay 6 per cent. There was considerable discussion about the appropriate rate of interest for student loans. Most governments provide some interest subsidy in order to overcome resistance to loans and help low-income students. But it is n o w recognised in m a n y countries that this represents a substantial hidden grant and some analysts believe that it is more efficient to provide loans to all applicants, at interest rates close to market rates, but to provide grants, scholarships or bursaries for those from the lowest income families. If governments do chose to provide subsidies then the selection of loan recipients becomes a crucial issue. There are few examples of completely unsubsidized loans, although in Indonesia the newly established loans operated by private banks involve payment of 18 per cent interest.

The other main differences lie in length of repayment, which amounts to 3 years or less for some loans in Singapore, but 15 years in Japan. It was clear in discussion that there is no single right answer, but the choice will depend on the labour market for graduates, the extent of unemployment and similar factors.

In Australia, the Higher Education Contribution is payable by means of a fixed proportion of graduates' income, ranging from 2 to 4 per cent, depending on the level of income. Those with incomes below a specified m i n i m u m can postpone repayment, to ensure that the burden of debt does not become too heavy.

The possibility of postponement of loan repayments in cases of low income is important from the point of view of default. Experience with default rates varies widely, with Japan, Hong Kong and Singapore enjoying very low default, while India and Indonesia (under the K M I scheme) had very high levels of default. Participants felt that a strong political commitment to collecting repayments was essential, and helped to explain w h y repayment rates are high in Japan and Hong Kong, but very low in India. Various strategies have been attempted to minimise

17

Student loans in higher education

default, including the publication of lists of names of defaulters, or using the support of immigration and emigration officials, as in Hong Kong.

4. Feasibility of student loans and ways of overcoming obstacles

Student resistance was seen as a major obstacle in some countries, particularly in a region where students have strong political influence. However , the introduction of loans had encountered very little resistance in Malaysia and Singapore, and was not expected to do so in Thailand. O n e reason was that in all these countries, loans represented a net addition to the total level of financial support for students, and scholarships and bursaries would continue to be available. Countries where loans will partially replace grants or scholarships, as in the United Kingdom at present, are far more likely to encounter strong student opposition.

Australia is an interesting example of a country that has introduced a system of student contributions where none previously existed. This might be expected to provide strong opposition, but the meeting heard that the Australian Government had been successful in winning support for the idea of H E C S by emphasizing that it would improve equity, undertaking to monitor the scheme to ensure that it did not discourage participation by low income students, and using the funds generated by the scheme to increase higher education opportunities, rather than reduce expenditure on higher education. All these factors helped to ensure that opposition, though initially strong in some quarters, was short-lived.

In the People's Republic of China, the Government relies on employers to collect repayments and it was felt that this m a y help to reduce the problem of default. Other countries rely heavily on universities and other higher education institutions to help select loan recipients and generally administer the scheme. This m a y help overcome obstacles, but it m a y also lead to opposition on the part of institutions.

The general conclusion of the discussions was that student loans are feasible under certain conditions, particularly in small, highly organized

18

Summary of the forum discussions

societies as in such countries as Hong Kong or Singapore. In very large and geographically dispersed countries, such as India and Indonesia, problems of securing repayment and other administrative difficulties seem to represent serious obstacles. A strong administrative framework is also essential, though whether this is best provided by commercial banks, government agencies, or the tax system (as in Australia) will depend on the state of the economy and society. Other important factors influencing the success or failure include the labour market for graduates and whether the private returns to higher education are significant. If they are, this is likely to lead to strong private demand for higher education, and greater acceptance of the idea that students should invest in their o w n future by means of loans.

Finally, strong political commitment to a reallocation of resources through increased cost recovery and the tapping of n e w sources of funds is another factor likely to lead to successful introduction and implementation of loan schemes. The emphasis on self-reliance in the n e w long-range plan for higher education in Thailand is one example of such strong political commitment, as is the Australian Government's determination to increase equity in the financing of education.

The introduction and implementation of systems of student loans is never easy. It m a y well encounter obstacles and opposition, and there m a y be problems, such as default and high administrative costs. Nevertheless, Asian experience suggests that loans are feasible, particularly w h e n combined with other forms of student support, and their use is likely to increase, as more governments face the problem of h o w to expand access to higher education, in response to private demand, while public expenditure is subject to increasing financial constraints.

19

III. Background orientation paper

The Role of Student Loans by Maureen Woodhall

Introduction3

Student loans have been widely advocated as a way of financing the private costs of investing in higher education and more than 30 countries n o w have loan programmes which enable students to borrow from government agencies or commercial banks in order to finance their tuition fees or living expenses, and to repay the loans after graduation. Most loan schemes offer government guarantees and some form of interest subsidy, and in many countries students receive financial support through a combination of loans, grants, scholarships or bursaries.

In some countries small-scale loan programmes were introduced 60 or 70 years ago but loans were established on a significant scale in the 1950s and 1960s in many developed countries (Canada, Denmark, Sweden and the U S A , for example) and in a few developing countries (Colombia and India both set up loan schemes in the 1950s). A review of international experience with student loans (Woodhall 1983) found examples of student loan programmes in Western Europe, North America, Japan, Latin America and Asia and a few in Africa. More recently there has been a new upsurge of interest in student loans in both developed and developing countries and significant changes have been introduced or proposed in several countries with established loan

3. This is an edited version of a paper prepared for a Conference on Private Provision of Social Services, organized by the World Bank and the Rockefeller Foundation, held at Bellagio, 22-26 October 1990.

20

Background orientation paper

programmes (Germany, Sweden, and the Netherlands, for example); a n e w loan programme has been established in the United Kingdom; and Australia has introduced a Higher Education Contribution, collected through a graduate tax. At the same time, a number of developing countries are n o w seriously considering student loans as a means of financing higher education; the World Bank has strongly advocated loans on grounds of both efficiency and equity (World Bank 1986 and 1988) and the Commonwealth Secretariat and the World Bank have published guidelines for developing countries considering h o w to design a student loan programme (Woodhall 1987a and b).

The time is therefore ripe to evaluate international experience with student loans, to assess the effects of the changes currently taking place and to share more widely information about what works and what does not. The International Institute for Educational Planning (HEP) has embarked on a series of seminars on student loans in higher education. The first Educational Forum on Student Loans was held in Paris in September 1989 and was concerned with recent experience in Western Europe and the United States. (For a summary of the discussion see Woodhall 1990). This report summarizes the forum held in Asia in November 1990, and plans are underway to hold forums in Africa and Latin America in 1991 and 1992. These will provide a useful opportunity to collect information about student loan programmes, to share experiences and to examine a number of issues, including the effects of loans on access and participation in higher education, the feasibility of loans in developing countries and problems of designing and administering loan programmes, particularly questions of whether loans are best administered by government agencies or commercial banks, what interest rate should be charged, h o w to minimize default, and the implications of graduate unemployment and the 'brain drain'.

The purpose of this paper is to explore some of these issues in greater depth in order to evaluate student loans as a means of financing higher education and to examine more widely the role of loans in the provision of social services. The paper is organized in terms of eight main issues which require systematic study. It is to be hoped that an evaluation of existing loan programmes will allow both developed and

21

Student loans in higher education

developing countries to learn from the wealth of international experience that is n o w available.

1. T h e role of student loans in cost-sharing in higher education

A basic issue in m a n y countries at present is h o w the costs and the benefits of education are and should be shared. Johnstone (1986) in a comparative study of student aid systems in five developed countries (France, Germany, Sweden, the United Kingdom and the U S A ) examines h o w the costs of higher education are shared between four partners: (i) students, (ii) parents, (iii) taxpayers and (iv) institutional and philanthropic donors. H e points out that regardless of the system, society or country, the direct costs of tuition and the indirect costs of student maintenance and earnings forgone must be shared by some combination of these four sources of revenue. H e concludes that despite differences in the balance between public and private contributions, and in the mechanisms of funding higher education in different countries, all the countries included in his study rely on a combination of these four sources, and he details various attempts in recent years to shift part of the burden of costs from one partner to another, for example by increasing fees, which shift costs from taxpayers to students or parents, or changing the balance between grants and loans.

At the time of his study (1985-86) three of the five countries (Germany, Sweden and the U S A ) relied partly on loans to finance higher education, but his analysis shows that the repayment terms of student loans in Sweden and Germany were so generous that there was a substantial 'hidden grant' in the form of interest subsidies which increase the contribution of taxpayers and reduce the students' share of the costs. Since his study was published there have been significant changes in several of the countries examined by Johnstone.

In 1989 both Sweden and Germany decided to change the balance between grants and loans (for an account of these changes see Woodhall 1989) and the British Government announced the introduction of student loans from 1990, but on terms which also constitute a substantial 'hidden grant', since loan repayments will be interest-free. In Sweden, the

22

Background orientation paper

government has increased the proportion of student aid provided in the form of a grant, but at the same time changed the repayment terms of loans so that the 'hidden grant' is reduced, while explicit grants are increased from less than 5 per cent to 30 per cent of total student aid. This policy change was partly influenced by economic analysis which demonstrated the effects of interest subsidies on the sharing of costs between students and taxpayers and by the argument of economists that explicit grants are more efficient than hidden subsidies.

In most other loan programmes there are still substantial interest subsidies, but several countries are considering changes in repayment terms that would result in an increase or reduction in 'hidden subsidies'. O n e question for further research is the effect of student loans on the relative cost burdens which are borne by students, parents, taxpayers and institutional or philanthropic donors in different countries, and the effects of different types of loan programmes on the incidence of costs. A change in student aid, such as the introduction of student loans in the United Kingdom, or the reintroduction of grants in Germany (so that from 1989 students receive aid in the form of 50 per cent grant and 50 per cent loan, rather than the 100 per cent loans that were provided between 1984 and 1989) involve a shift in relative cost burdens, and a change in the relation between private and social rates of return. Since so m a n y countries are currently changing their systems of student aid it is important to examine these changes from the perspective of cost sharing, and to compare the effects of the introduction of loans, or a change in the balance between loans and grants, with other financial changes such as the graduate tax introduced in Australia and advocated by some Vice Chancellors in the United Kingdom

2 . T h e effects of loans on access and participation in higher education

A key issue is the effect of student loans on access to higher education and on participation by particular categories of student, such as those from low-income families, minority groups, or w o m e n . Advocates of loans argue that by reducing the financial burden on public

23

Student loans in higher education

funds, loan programmes can lead to an increase in overall participation rates and that loans are also more equitable than grants or free tuition, since the benefits of publicly-funded higher education tend to be enjoyed disproportionately by students from upper-income families. Critics on the other hand argue that student loans will deter working class students, those from poor families w h o will be discouraged by the fear of debt, and w o m e n w h o will be afraid of incurring a 'negative dowry' .

Evidence so far shows that loans do not necessarily deter low-income students; indeed Perkins Loans in the U S A , which are heavily subsidized, are designed for low-income students, but there is some concern n o w in the U S A that loans m a y discourage ethnic minority students. Certainly w o m e n do not appear to be discouraged and in Sweden and the U S A which rely heavily on loans, rates of participation of w o m e n in higher education have increased faster than in the United Kingdom, which relied entirely on grants until this year. But with so m a n y countries introducing changes in student support in the 1990s, it will be extremely important to monitor the effects on participation rates by different social and income groups, by m e n and w o m e n , by rural and urban status and by different ethnic groups. It is particularly important to study this question in developing countries, since loans arc frequently advocated on equity grounds (sec, for example, Psacharopoulos 1977, World Bank 1986).

3. T h e effects of student loans on labour markets

Another area of controversy between advocates and critics of student loans is the implications of loans for labour markets, through their effects on subject and career choices. O n e of the arguments put forward by the British Government in favour of loans was that it would "increase economic awareness" on the part of students, with respect to choice of subject and careers. O n the other hand, critics argue that it will distort career choices and discourage students from entering high-cost courses, such as medicine, or low-paid jobs such as teaching. The effects of student loans on recruitment for courses with higher than average costs, such as medicine or engineering, is a particular concern in some

24

Background orientation paper

countries and special loan programmes have been designed for doctors and health care workers in the U S A , and m a n y states offer 'loan forgiveness' schemes to attract graduates into teaching, although experience shows that such programmes are not very effective in influencing career choices.

The idea of using 'loan forgiveness' or variable repayment terms to attract graduates into particular occupations or areas appears attractive in some developing countries, but m a y be extremely difficult to implement. In Barbados, a n e w scheme of 'loan grants' was introduced in 1983, under which part of a graduate's debt can be cancelled if he or she enters a 'shortage' occupation.

Such a scheme could be used to attract graduates to rural areas, or to meet other labour market objectives, but it will be vital to monitor such schemes carefully in order to evaluate whether they are successful in influencing career choices and whether they are more successful than alternatives, such as increasing salaries in shortage occupations. In general, the concept of 'bonded scholarships', under which students receive financial support in return for an undertaking to work in a particular field or job after graduation, is losing favour in most developing countries, but the effects of alternative types of student aid on career choices is an important area for research.

Another significant issue is the effect of student loans on the 'brain drain'. Critics of loans argue that it will be impossible to ensure repayment w h e n a high proportion of graduates work overseas, and that student loans m a y actually increase the brain drain, but it is very difficult to disentangle the effects of loans from the general effects of salary differentials and other labour market factors in influencing inflation.

4. Debt burdens and the problem of minimizing loan defaults

T w o problems that cause particular concern among critics of student loans are the burdens of debt faced by graduates and the problem of default by graduates w h o cannot or will not repay their debts. The question of what is an 'acceptable' burden of debt has no simple answer. Studies of debt burdens in the U S A (Hansen 1987 and 1989) show that

25

Student loans in higher education

there are widely differing definitions of what constitutes a 'reasonable' or 'manageable' burden of debt for graduates w h o have financed their higher education through loans.

Hansen (1989) argues that: "Facts are few; in this as in other aspects of student aid w e are unable to answer basic questions, such as h o w m u c h debt the typical borrower has upon college graduation or about h o w many students are borrowing at high levels. In this area, too, w e have failed to establish benchmarks, such as percentages of income that must be devoted to loan repayment, that would help us determine when w e are approaching danger. Studies of manageable debt burdens, for example, have ranged in their recommendation from 3 to 15 per cent of income, hardly useful for policy purposes even if w e had better information on what percentage of income student borrowers are devoting to loan repayment." (Hansen 1989, pp. 61-62).

Nevertheless, she concludes that "the data w e do have suggest that borrowing is not out of control and that most student borrowers have quite manageable debt burdens". In developing countries, however, very little is known about the average burden of debt faced by those w h o take out student loans and what can be regarded as a "reasonable" level of debt. Where private rates of return are high, then it m a y be reasonable to expect graduates to allocate a higher proportion of their income to loan repayments than in a country with lower private rates of return. In Sweden, for instance, graduates are expected to repay not more than 4 per cent of their gross income, but private rates of return to university education are very low in Sweden and in some occupations m a y actually be negative. In the U S A , on the other hand, where average private rates of return are higher than in Sweden, 10 per cent of a graduate's income m a y be needed to repay a student loan. M u c h more research is needed on levels of debt in relation to actual and expected graduate salaries, in order to understand the economic effects of student loans.

26

Background orientation paper

This is closely linked with the problem of default. In Sweden, where graduates are not expected to pay more than 4 per cent of their income in loan repayments, and those w h o are unemployed or have low earnings can automatically postpone repayment, actual default rates are extremely low. In the U S A default rates are currently causing great concern, but research suggests that very high rates of default are associated with particular types of courses (for example short vocational courses in private for-profit proprietary schools) rather than a general phenomenon. Hansen argues that while the costs of default have "skyrocketed", due to the huge expansion of student loans in the late 1970s and 1980s, the actual rate of default has increased only a little, and she concludes that "the evidence about w h o fails to repay and w h y indicates that it is not the large borrowers w h o default, but rather, students with relatively small debts w h o cannot repay". (Hansen 1989, p. 62).

There is very little evidence about default in developing countries, but the fear of high default rates is a major factor discouraging governments from introducing loan schemes in some developing countries. Closer examination of countries which have loan schemes with very high rates of default often shows that banks or other lenders have actually m a d e very little attempt to collect loan repayments. For example, Kenya introduced student loans in 1974, but very few graduates have as yet repaid their loans. The government n o w recognises, however, that this is largely due to the fact that virtually no effort was m a d e until very recently to collect loan repayments, and believes that the default rate will fall substantially n o w that strong efforts are being made to require employers to collect loan repayments from all graduate employees. Similarly, a study in Sri Lanka (Hemachandra 1982) found that high rates of default were partly due to failure on the part of the People's Bank, which administered the student loan programme, to collect loan repayments.

The whole question of default requires m u c h more research, both to establish the true extent and causes of default and to identify effective ways of dealing with the problem in countries such as Japan and H o n g K o n g , where default rates are extremely low.

27

Student loans in higher education

O n e proposal that has been strongly advocated by Barr (1989 and 1991 forthcoming) as a way to minimize default is income-contingent student loans, under which graduates undertake to repay a specific proportion of their income, rather than to repay their loans in a specific time, as in most 'mortgage type' loan programmes. Barr argues strongly that income-contingent loans are feasible, fair and administratively simple if collected through the National Insurance System. H e has advocated such a scheme in the United Kingdom without, however, convincing the government, whose system of 'top-up loans' announced in 1988 and introduced in 1990 (Department of Education and Science 1988) is a conventional 'mortgage type' loan to be repaid in 5 to 10 years. In the U S A , there has been some limited experience with income-contingent loans which is largely regarded as a failure, although in 1988 Reischaucr advocated a n e w Higher Education Loan Programme (HELP) to be based on income-related repayments, collected via the social security system (see Rcischauer's proposal in Gladieux (Ed) 1989).

The question of whether income-contingent loans arc "an idea whose time has come" as Barr argues (1991 forthcoming) or an impractical notion, as American critics believe, will continue to be debated on both sides of the Atlantic, but the implications of this idea for developing countries have hardly been addressed.

5. Administration of student loans: terms, conditions and administrative mechanisms

The first question to be determined in the design of a student loan programme is whether it should be administered by a government department or agency or by commercial banks. There are examples of the two models in both developed and developing countries, and several instances of changes, or proposals for change, from one model to another. In Sweden, for example, loans are administered by a government agency, the National Student Aid Board, whereas in the U S A commercial banks provide loans backed by government guarantees and interest subsidies. The British government initially hoped that

28

Background orientation paper

commercial banks would administer the n e w system of 'top-up loans' introduced in 1990, but the banks proved unwilling and the government has set up a Student Loan Company to operate the scheme. In the Netherlands the government has recently decided to privatize the loan programme and to use commercial banks instead of a government agency, and a similar decision has just been made in Indonesia. O n the other hand, in Kenya, which recently involved commercial banks for the first time, the government n o w wants to set up a government agency to administer student loans. There is considerable scope here for a comparative study of student loan programmes which compares government-administered programmes with those operated by commercial banks, in terms of costs of administration, efficiency of loan disbursement and collection of repayments, choice of recipients, etc.

Arguments put forward for government administration are that commercial banks would confine their lending to 'low risk' students, and that those from poor families would be denied access to the loans and that it would be more efficient, due to economies of scale. O n the other hand, advocates of loans operated by commercial banks argue that they have greater expertise in debt collection and that the burden on public funds will be reduced if the private sector can be persuaded to provide the finance for student loans. W h a t is the evidence on these issues? In the U S A there is evidence that commercial banks can operate student loan programmes efficiently, but that the cost to public funds, in terms of subsidies, guarantees and the 'special allowance' paid to banks to induce them to participate, is very high. O n the other hand, very little is known about relative advantages and disadvantages of government-administered programmes versus commercial banks in developing countries.

There is also a wide range of administrative issues that require further research, particularly in developing countries. In designing a student loan programme administrative issues to be resolved include:

(i) h o w to determine eligibility, through means test or other

mechanisms; (ii) what is an appropriate interest rate;

29

Student loans in higher education

(iii) the length of repayment and the length of a grace period during which graduates are excused repayment.

There m a y also be legal obstacles to effective administration of student loans in some countries, and the legal frameworks establishing loans and the obligation to repay the loans m a y merit further examination.

6. T h e effects of loans on internal efficiency

Critics of student loans often argue that they will lead to higher rates of drop-out and wastage, as students m a y withdraw from courses because of a fear of incurring excessive debts, whereas advocates of loan systems suggest that they will increase efficiency by giving students an incentive to complete their higher education as quickly as possible. There is very little evidence on such issues, particularly in developing countries, and any evaluation of student loans needs to look closely at the effects of loans on the average length of course, drop-out and repetition.

In some countries, loan schemes incorporate incentives to encourage students to complete their higher education in the m i n i m u m time. In Germany, for example, students w h o complete in the m i n i m u m period have part of their loan cancelled, but there has been no evaluation of the effectiveness of such incentives.

7 . T h e role of incentives: complexity versus simplicity

The question of incentives, and their effectiveness, raises the question of a possible trade-off between the flexibility of a student loan programme, and its complexity. It is perfectly possible to devise a very flexible programme, with different interest rates and different repayment periods for different categories of student, and which incorporates incentives to encourage students to complete quickly, or to enter particular occupations. Examples can be found of all such features. O n the other hand, such a programme will be extremely complex and likely to lead to high costs of administration. A simpler programme would be

30

Background orientation paper

easier to administer, but m a y be perceived as less fair to particular categories of students or graduates. In her review of the American experience, Hansen (1989) concludes that "in designing student aid programmes, there is an important trade-off to consider between minimizing complexity of administration and maximizing flexibility in meeting student needs". There is very little evidence on the extent of this trade-off in developing countries, and this issue would repay further research.

8. T h e political economy of student loans

Another important issue is that of the political economy of policy reform. This is particularly important in the area of cost recovery in higher education and the introduction or adoption of student loan programmes.

H o w was the Australian government able to introduce a graduate tax so quickly, in 1988-89, when the N e w Zealand government faced major obstacles to the introduction of student loans? Did the political factors that caused the government of Ghana to withdraw a student loan programme in the 1970s m e a n that the scheme was unworkable, or would student opposition to the loans have eventually been overcome? Such questions are extremely difficult to answer through research, and are politically sensitive, but it is clear that the whole idea of student loans raises such deep emotions on the part of both advocates and opponents, that the question of attitudes towards user charges and loans is crucial. The success or failure of student loans m a y ultimately depend on attitudes towards debt and obligations to repay loans. H o w can such attitudes be changed?

O n e factor that seems to be important in some countries is that the introduction of user charges or student loans was linked directly with proposals to expand higher education. Both students and taxpayers seem to have been persuaded in Australia, for example, that revenue generated from the Higher Education Contribution will be used to finance expansion, rather than to reduce public expenditure on higher education. In the United Kingdom, the government has argued that the introduction

31

Student loans in higher education

of student loans will permit expansion of higher education, but students and many parents remain unconvinced. The process whereby changes have been announced and implemented in systems of student support as well as levels of tuition fees and other user charges could be an interesting area for research.

Conclusion

This paper has attempted to outline some of the main questions and issues that remain to be resolved and that require research, if w e are to understand more fully the role of student loans in financing higher education in developing countries. The present time represents an ideal opportunity to hold a series of International Forums in this area, to leam from experience in different countries and regions. In 1989 and 1990 major changes in systems of student support were announced or introduced in Australia, Germany, Sweden and the United Kingdom, and fundamental reviews of student loans and other types of student aid programmes are being conducted in Canada and the U S A Several developing countries are considering or implementing changes in student loan programmes, including Indonesia and Kenya. There is strong interest in student loans in many African countries, and growing experience of loan programmes in Asia and Latin America.

The series of Educational Forums on Student Loans being organized by H E P in 1989-91 will help to provide and disseminate information about h o w loan schemes work in different countries and what are the major issues facing policy-makers.

32

Background orientation paper

References

Barr, N . (1989). Student loans: the next steps. Aberdeen: Aberdeen University Press for the David H u m e Institute, Edinburgh.

Barr, N . (1991). "Income-contingent student loans: an idea whose time

has come". In: Shaw, G . K . (Ed). Economics, Culture and Education: Essays in Honour of Mark Blaug. Aldershot: Edward Elgar (forthcoming).

Department of Education and Science (1988). Top-up loans for students. London: H M S O (Cm. 520).

Gladieux, L . (ed) (1989). Radical reform or incremental change? Student loan policy alternatives for the Federal Government. N e w York: College Entrance Examination Board.

Hansen, J. (1987). Student loans: are they overburdening a generation?

Washington D . C . : The College Board. Hansen, J. (1989). "Cost-sharing in higher education: the United States

experience". In: Woodhall, M . (Ed). Financial support for students:

grants, loans or graduate tax? London: Kogan Page 1989. Hemachandra, H . L (1982) University students loan scheme, Study Paper

N o . 46, Colombo: People's Bank, Sri Lanka. Johnstone, B . (1986). Sharing the costs of higher education: student

financial assitance in the UK, the Federal Republic of Germany, France, Sweden and the USA. N e w York: College Entrance Examination Board.

Psacharopolous, G . (1977). "The perverse effects of public subsidisation of education". In: Comparative Education Review, Vol. 21, N o . 1

(February) pp. 69-90. Reischauer, R . (1989)."HELP: A student loan program for the

twenty-first century". In: Gladieux, L . E . (Ed.). Radical Reform or

Incremental Change? Student loan policy alternatives for the Federal Government. N e w York: College Entrance Examination

Board.

33

Student loans in higher education

Woodhall, M . (1983). Student loans as a means of financing higher education: lessons from international experience. International Bank for Reconstruction and Development, World Bank Staff Working Paper N o . 599.

(1987a). Lending for learning: designing a student loan

programme for developing countries. London: Commonwealth Secretariat.

(1987b). Establishing student loans in developing countries: some guidelines. Washington D . C . : International Bank for Reconstruction and Development (World Bank), Report N o . E D T 8 5 .

(1989) (Ed). Financial support for students: grants, loans or graduate tax? London: Kogan Page, with the Institute of Education, University of London.

(1990). Student loans in higher education: 1. Western Europe and

the USA. Paris: International Institute for Educational Planning, Educational Forum Series, N o . 1.

World Bank (1986). Financing education in developing countries: an exploration of policy options. Washington D . C . : International Bank for Reconstruction and Development (World Bank).

(1988). Education in Sub-Saharan Africa: policies for adjustment, revitalization and expansion. Washington D . C . : International Bank for Reconstruction and Development (World Bank).

34

IV. Annexes

Annex A

Summaries of student support systems

I. Australia

In December 1987 the federal government issued a policy discussion paper on higher education in Australia. That paper, and the government policy statement which flowed from it in July 1988, identified as major government commitments:

expansion of the capacity and effectiveness of the higher education sector, improvement of access to higher education for groups then

under-represented.

This commitment had significant funding implications and the government decided it was necessary to consider sources of funding involving the direct beneficiaries. It therefore established a Committee, chaired by Neville Wran , to develop options and m a k e recommendations for possible schemes of funding which could involve contributions from students, graduates, their parents and employers. The Committee, generally referred to as the Wran Committee, was directed to have regard to the social and educational consequences of the schemes under consideration.

In the period leading up to the establishment of the Committee Australia had the following arrangements:

1945-1973: tuition fees representing some 15 per cent of course costs but with government scholarships, in particular, but also other arrangements resulting in only some 40 per cent of students paying fees. 1973-1986: no tuition fees. 1986-1988: a small compulsory Higher Education Administration Charge - A$.263 (US$207) in 1988 - was introduced for students to support the administrative costs associated with their enrolment. S o m e 40 per cent of full-time

37

Student loans in higher education

students were either exempted from the charge or received assistance to pay it through income support arrangements.

The Wran Committee reported in April, 19884 and its recommendations were largely adopted by the federal government and implemented in 1989. The principal outcome of the review was a scheme, called the Higher Education Contribution Scheme ( H E C S ) , for collecting a financial contribution from higher education students towards the costs of providing their education. This was seen as equitable since there was clear evidence that students themselves, as well as the community, benefitted from participation in higher education.

However, central to the government's objectives was the desire to minimize financial disincentives and obstacles to participation by all w h o were capable of successfully undertaking higher education. It is in addressing this objective that H E C S is most innovative.

With only very few exceptions, all students undertaking award courses in Commonwealth-funded higher education institutions incur a liability under H E C S . This is currently A$.l,882 (US$1,482) per annum or some 20 per cent of average course costs (with pro rata contributions for part-time students). The innovative feature of H E C S is that students can choose to meet their liability by making a lump sum payment each semester with a 15 per cent discount; or they can choose to pay the full amount through the taxation system in the same way that they pay income tax. Rates of repayment through the taxation system are 2 per cent, 3 per cent or 4 per cent of the personal taxable income of the student or graduate annually. If a person's taxable income is below a specified level in a given financial year no repayment is required in that year. (Currently that specified level is A$.35,469 (US$27,925), compared with current Adult Full-time Average Annual Earnings of some A$.28,000 (US$22,050). In 1989 the median starting salary for graduates was A$.24,000 (US$18,900).

4 . Report of the Committee on Higher Education Funding. Australian Government Publishing Service, Canberra, 1988.

38

Annex A - Australia

The annual charge, the outstanding liability and the threshold income levels are indexed each year to maintain their real value. However, no interest is charged.

Surveys and statistical analyses undertaken since the introduction of H E C S suggest it has had little effect on participation in higher education.

A disadvantage of the H E C S approach from a revenue raising perspective is that it takes some years before revenues become substantial. In 1989 total federal government expenditure on higher education was some A$.3.1 billion. In the same year H E C S liabilities incurred by students totalled A$.511 million (US$402 million). However, the following are actual and estimated H E C S receipts:

1988/89 1989/90 1990/91 1991/92

1992/93 1993/94

A $ 3 4 m A $ 1 0 0 m A $ 1 2 8 m (est.) A $ 1 9 2 m (est.) A $ 2 6 0 m (est.) A $ 3 4 8 m (est.)

In 1990 19 per cent of students elected to pay their H E C S contribution "up-front", by means of a lump sum payment.

The Wran Committee of course considered the option of combining fees with student loans but rejected it. The Committee's report states:

"In conclusion, fees schemes that have exemptions for the disadvantaged and commercially financed loans for other students can be expected to have an unacceptable impact on student demand and equity, and should be rejected. Schemes involving fees and government-financed loans are preferable because they can accommodate zero or low interest rates and 'easy start', or exit contingent repayment plans. However, in light of overseas experience, all schemes involving fees with loans should be rejected." (Reporto/the Committee ...,p.27.)

The Committee's review of overseas experience with student loans led it to conclude there were a number of serious problems, including:

39

Student loans in higher education

The Committee's review of overseas experience with student loans led it to conclude there were a number of serious problems, including:

"default claims for more than 9 per cent of all student loans; high administrative and legal costs, and the use of debt collection agencies, in taking action against defaulters; rising student indebtedness and falling participation amongst financially and other disadvantaged groups."

(Report ot the Committee..., p.27)

Clearly the government accepted the Committee's advice.

Income support

Since 1987 income support for higher education students has been provided through allowances available under the A U S T U D Y programme. The programme was introduced to simplify an earlier range of student allowance programmes and to remove the disincentive for young people from low-income families to participate.