Embed Size (px)

DESCRIPTION

The Emergence of the Euro Zone An I nformal Euro Standard as a First Step for EMU Membership of the CEE Countries Gunther Schnabl Universität Tübingen & Katholieke Universiteit Leuven Observatoire Français des Conjonctures Èconomique Paris, February 2002 E-mail: [email protected]. - PowerPoint PPT Presentation

Citation preview

Dr. Gunther Schnabl, Tübingen University 1

The Emergence of the Euro ZoneAn Informal Euro Standard as a First Step

for EMU Membership of the CEE Countries

Gunther SchnablUniversität Tübingen & Katholieke Universiteit Leuven

Observatoire Français des Conjonctures ÈconomiqueParis, February 2002

E-mail: [email protected]

Dr. Gunther Schnabl, Tübingen University 2

Table of Content

1. Introduction2. A Shift towards more Exchange Rate

Flexibility in Central and Eastern Europe (CEE)?

3. The Shift towards a Euro Zone in Central and Eastern Europe

4. An Informal Euro Standard as an Optimal Exchange Rate Strategy

5. Conclusion

Dr. Gunther Schnabl, Tübingen University 3

1. Introduction

• The exchange rate strategies in Central and Eastern Europe are currently (officially) very heterogeneous:

– (tight) pegs to the euro: Bulgaria, Estonia, Hungary, Lithuania

– currency basket arrangement: Latvia (€, $, ¥)

– crawling peg: Romania– (officially) floating: Czech Republic, Poland,

Slovak Republic, Slovenia

• Is a more homogenous exchange rate strategy the better choice?

Dr. Gunther Schnabl, Tübingen University 4

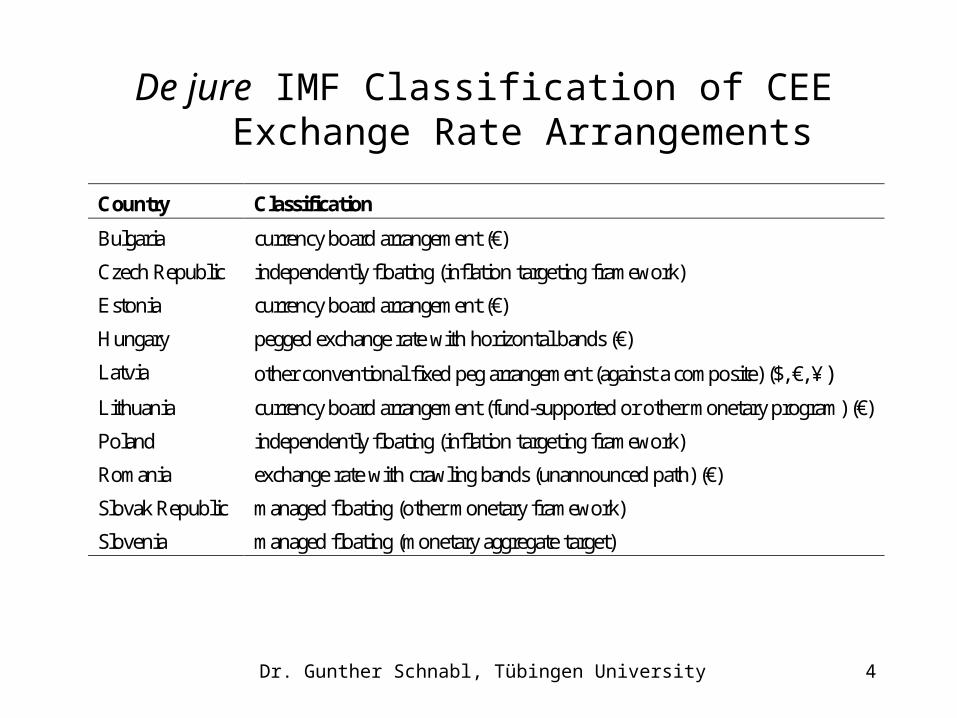

De jure IMF Classification of CEE Exchange Rate Arrangements

Country Classification

Bulgaria currency board arrangement (€)

Czech Republic independently floating (inflation targeting framework)

Estonia currency board arrangement (€)

Hungary pegged exchange rate with horizontal bands (€)

Latvia other conventional fixed peg arrangement (against a composite) ($, €, ¥)

Lithuania currency board arrangement (fund-supported or other monetary program) (€)

Poland independently floating (inflation targeting framework)

Romania exchange rate with crawling bands (unannounced path) (€)

Slovak Republic managed floating (other monetary framework)

Slovenia managed floating (monetary aggregate target)

Dr. Gunther Schnabl, Tübingen University 5

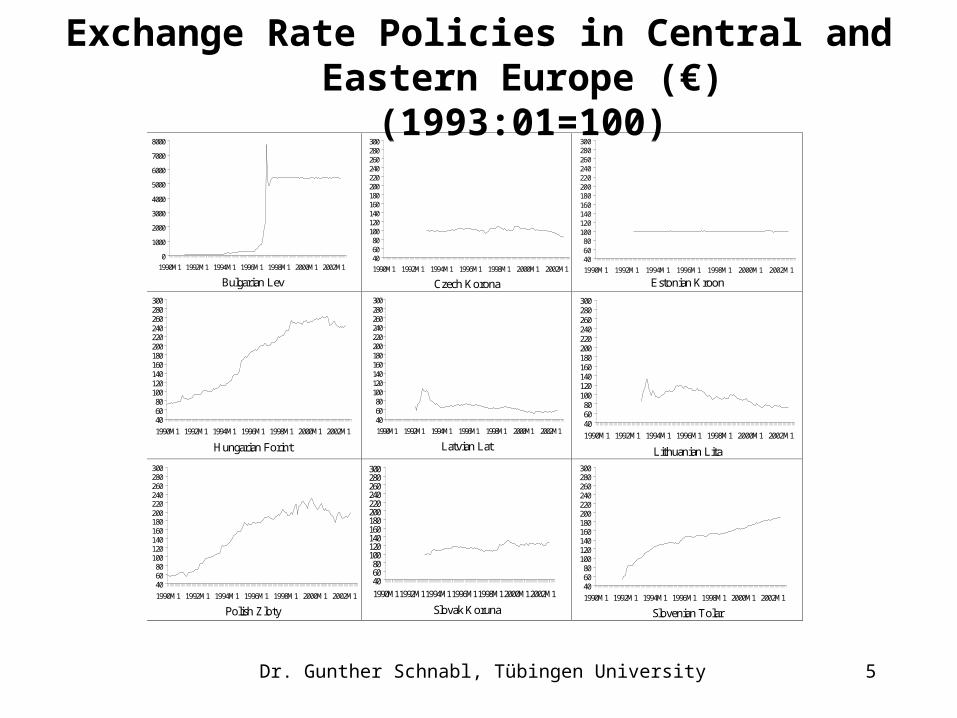

Exchange Rate Policies in Central and Eastern Europe (€)

(1993:01=100)

0

1000

2000

3000

4000

5000

6000

7000

8000

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Bulgarian Lev

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Czech Korona

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1 Estonian Kroon

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Hungarian Forint

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Latvian Lat

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Lithuanian Lita

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Polish Zloty

406080

100120140160180200220240260280300

1990M11992M11994M11996M11998M12000M12002M1

Slovak Koruna

406080

100120140160180200220240260280300

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Slovenian Tolar

Dr. Gunther Schnabl, Tübingen University 6

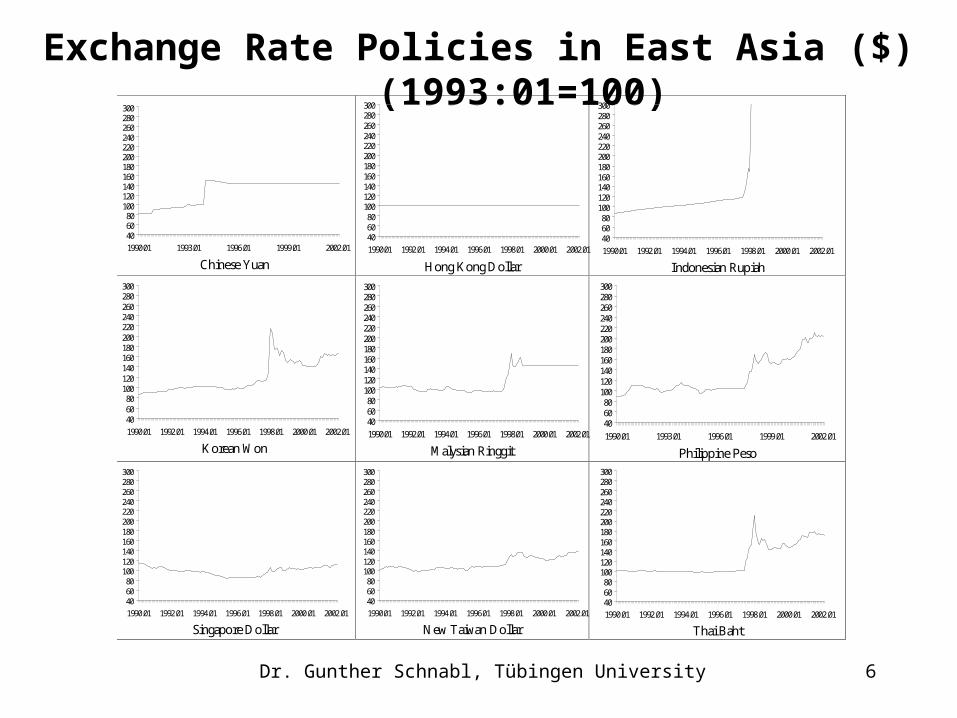

Exchange Rate Policies in East Asia ($) (1993:01=100)

406080

100120140160180200220240260280300

1990.01 1993.01 1996.01 1999.01 2002.01

Chinese Yuan

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

Hong Kong Dollar

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

Indonesian Rupiah

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

Korean Won

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

Malysian Ringgit

406080

100120140160180200220240260280300

1990.01 1993.01 1996.01 1999.01 2002.01

Philippine Peso

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

Singapore Dollar

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

New Taiwan Dollar

406080

100120140160180200220240260280300

1990.01 1992.01 1994.01 1996.01 1998.01 2000.01 2002.01

Thai Baht

Dr. Gunther Schnabl, Tübingen University 7

2. More Exchange Rate Flexibility in Central and Eastern Europe?

• Soft pegs in emerging markets open to international capital flows are prone to crisis (Fischer 2001). The IMF recommends that emerging markets open to international capital flows should pursue (more) flexible exchange rate regimes.

• Since 1997 three CEE countries have moved towards (more) exchange rate flexibility: Czech Republic (1997), the Slovak Republic (1999), and Poland (2001). Romania and Slovenia were (official) free floaters even before 1997.

• The flexible exchange rate strategies are not sustainable in emerging markets in general (McKinnon/Schnabl 2002) and in Central and Eastern Europe in specific (ECOFIN 2000).

Dr. Gunther Schnabl, Tübingen University 8

Reasons for the „Fear of Floating“ in Emerging Markets

• macroeconomic stabilization– inflation – government expenditure

• foreign exchange risk for international trade– trade of emerging markets is invoiced in $, € or ¥

• original sin (Eichengreen and Hausmann 1999)– international debt denominated in foreign currency

depreciations and exchange rate fluctuations put balance sheets at risk

– foreign exchange risk of short-term international payment flows (McKinnon and Schnabl 2002)

Dr. Gunther Schnabl, Tübingen University 9

Reasons for Exchange Rate Stabilization with Respect to EU Accession

• macroeconomic stabilization is a prerequisite for EU, ERM2 and EMU membership

– monetary convergence (inflation, interest rates)– fiscal discipline

• further growing trade integration after EU accession– euro invoicing

• accelerated integration into the euro capital markets– foreign exchange risk of (inter-)national (euro

denominated) debt vanishes– foreign exchange risk of short-term international

capital flows disappears• expected ERM2 membership adds an additional

need to redirect exchange rates to the euro

Dr. Gunther Schnabl, Tübingen University 10

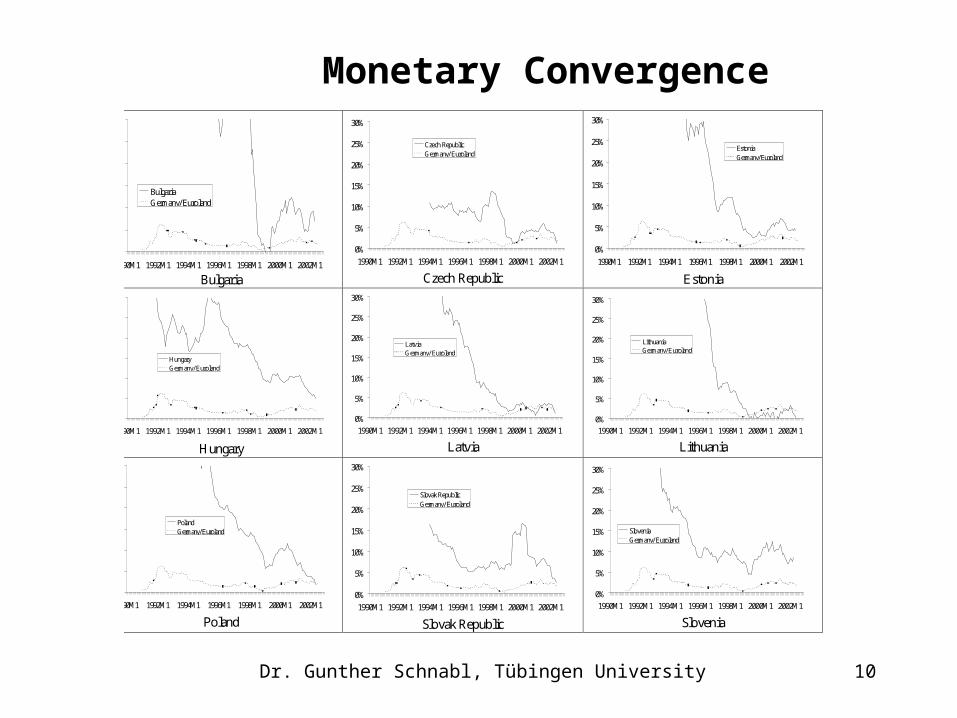

Monetary Convergence

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

BulgariaGermany/Euroland

Bulgaria

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Czech RepublicGermany/Euroland

Czech Republic

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

EstoniaGermany/Euroland

Estonia

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

HungaryGermany/ Euroland

Hungary

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

LatviaGermany/ Euroland

Latvia

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

LithuaniaGermany/Euroland

Lithuania

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

PolandGermany/Euroland

Poland

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Slovak RepublicGermany/Euroland

Slovak Republic

0%

5%

10%

15%

20%

25%

30%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

SloveniaGermany/Euroland

Slovenia

Dr. Gunther Schnabl, Tübingen University 11

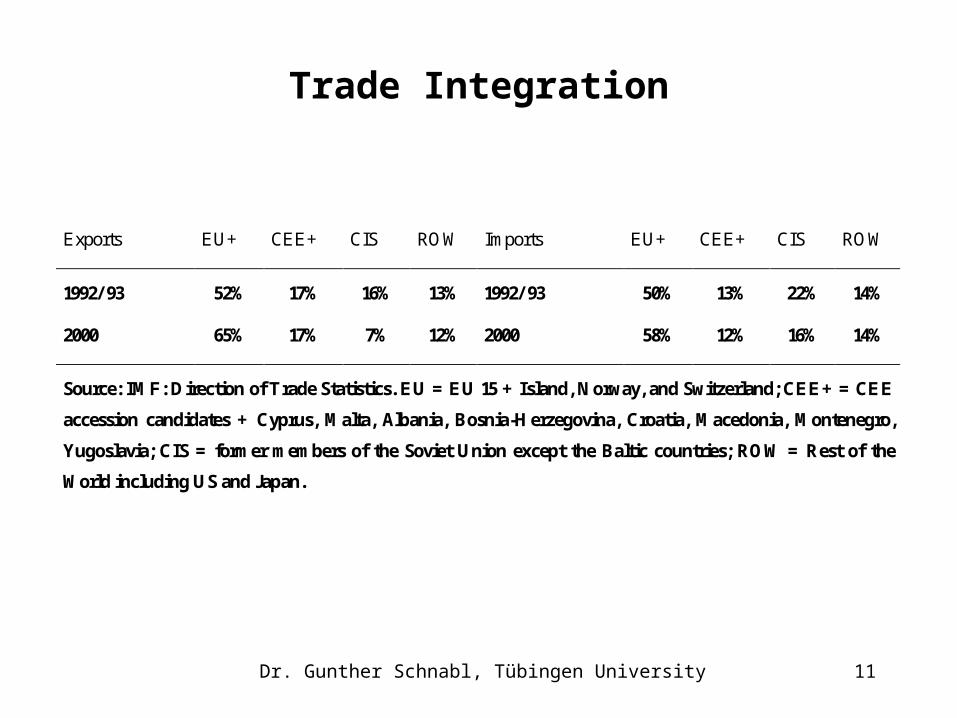

Trade Integration

Exports EU+ CEE+ CIS ROW Imports EU+ CEE+ CIS ROW

1992/ 93

2000

52%

65%

17%

17%

16%

7%

13%

12%

1992/ 93

2000

50%

58%

13%

12%

22%

16%

14%

14%

Source: IMF: Direction of Trade Statistics. EU = EU 15 + Island, Norway, and Switzerland; CEE+ = CEE

accession candidates + Cyprus, Malta, Albania, Bosnia-Herzegovina, Croatia, Macedonia, Montenegro,

Yugoslavia; CIS = former members of the Soviet Union except the Baltic countries; ROW = Rest of the

World including US and Japan.

Dr. Gunther Schnabl, Tübingen University 12

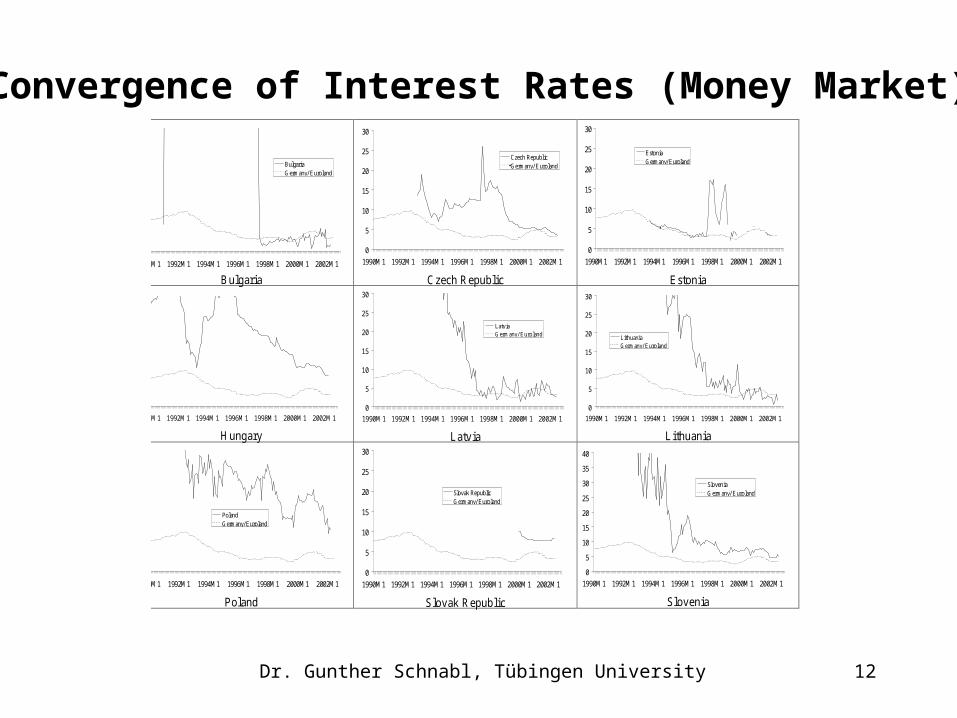

Convergence of Interest Rates (Money Market)

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

BulgariaGermany/ Euroland

B ulgaria

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Czech RepublicGermany/ Euroland

C zech R epublic

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

EstoniaGermany/ Euroland

Estonia

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

H ungary

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

LatviaGermany/ Euroland

Latvia

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

LithuaniaGermany/ Euroland

Lithuania

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

PolandGermany/ Euroland

Poland

0

5

10

15

20

25

30

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Slovak RepublicGermany/ Euroland

Slovak R epublic S lovenia

0

5

10

15

20

25

30

35

40

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

SloveniaGermany/ Euroland

Dr. Gunther Schnabl, Tübingen University 13

3. The Shift towards a Euro Zone in Central and Eastern Europe

• The euro bloc is continuously growing.• Formal tests:

– Calvo-Reinhart criteria– standard deviations of daily exchange rate

returns• Estonia (1992), Bulgaria (1997), Hungary (2000)

and Lithuania (2002) form the core of the euro zone.

• Informally, the Czech Republic and Slovenia have also joined the euro club.

• Poland, the Slovak Republic, Romania and partially Latvia (still) remain outside.

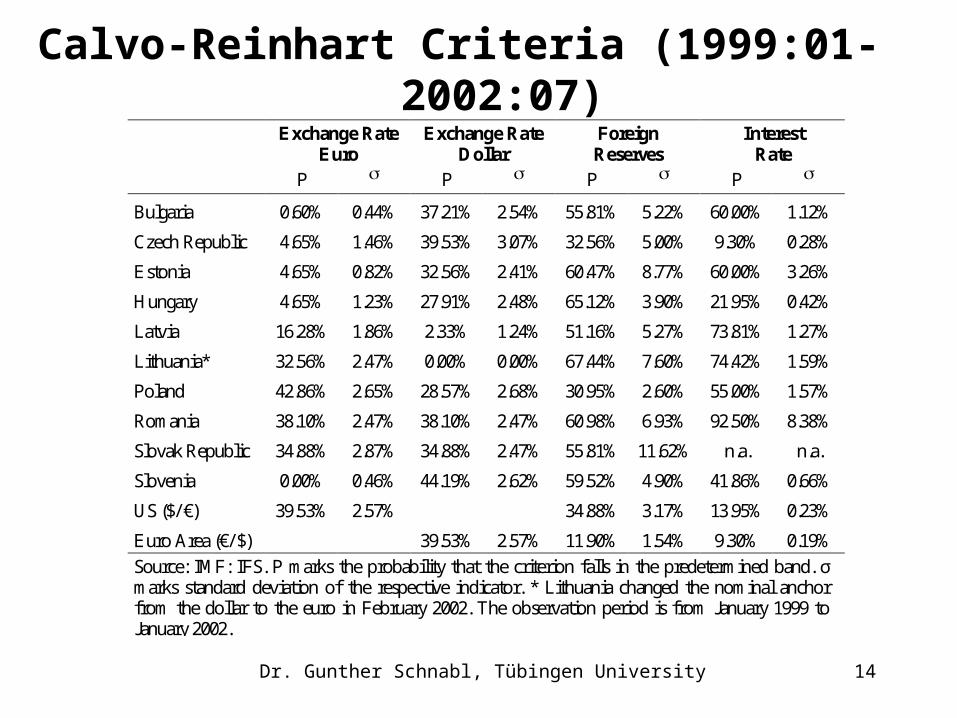

Dr. Gunther Schnabl, Tübingen University 14

Calvo-Reinhart Criteria (1999:01-2002:07) Exchange Rate

Euro Exchange Rate

Dollar Foreign Reserves

Interest Rate

P P P P

Bulgaria 0.60% 0.44% 37.21% 2.54% 55.81% 5.22% 60.00% 1.12%

Czech Republic 4.65% 1.46% 39.53% 3.07% 32.56% 5.00% 9.30% 0.28%

Estonia 4.65% 0.82% 32.56% 2.41% 60.47% 8.77% 60.00% 3.26%

Hungary 4.65% 1.23% 27.91% 2.48% 65.12% 3.90% 21.95% 0.42%

Latvia 16.28% 1.86% 2.33% 1.24% 51.16% 5.27% 73.81% 1.27%

Lithuania* 32.56% 2.47% 0.00% 0.00% 67.44% 7.60% 74.42% 1.59%

Poland 42.86% 2.65% 28.57% 2.68% 30.95% 2.60% 55.00% 1.57%

Romania 38.10% 2.47% 38.10% 2.47% 60.98% 6.93% 92.50% 8.38%

Slovak Republic 34.88% 2.87% 34.88% 2.47% 55.81% 11.62% n.a. n.a.

Slovenia 0.00% 0.46% 44.19% 2.62% 59.52% 4.90% 41.86% 0.66%

US ($/ €) 39.53% 2.57% 34.88% 3.17% 13.95% 0.23%

Euro Area (€/ $) 39.53% 2.57% 11.90% 1.54% 9.30% 0.19% Source: IMF: IFS. P marks the probability that the criterion falls in the predetermined band. σ marks standard deviation of the respective indicator. * Lithuania changed the nominal anchor from the dollar to the euro in February 2002. The observation period is from January 1999 to January 2002.

Dr. Gunther Schnabl, Tübingen University 15

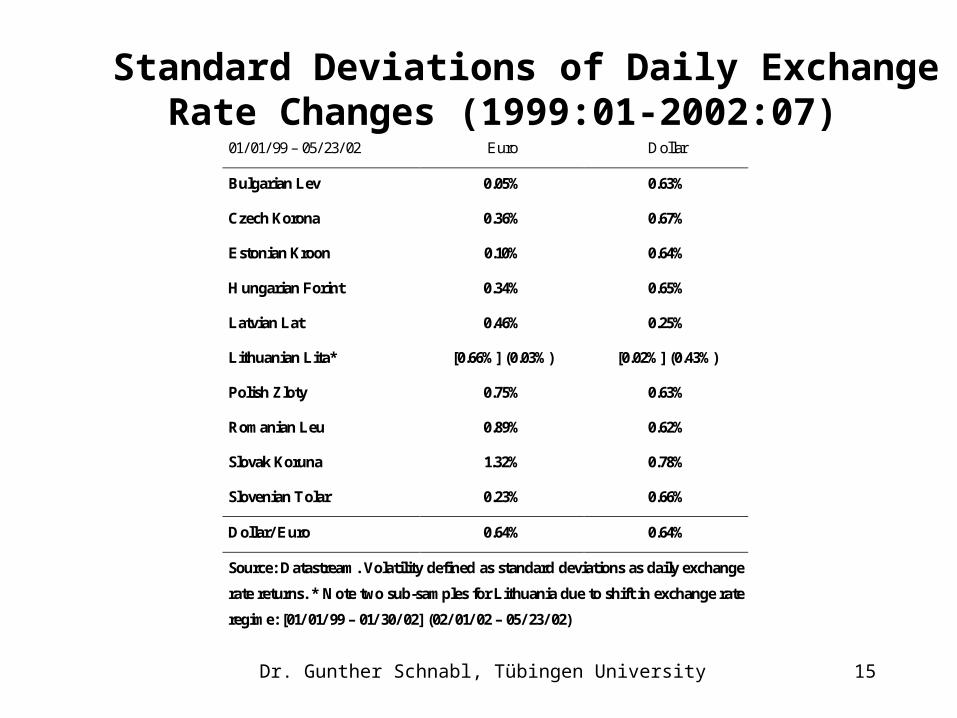

Standard Deviations of Daily Exchange Rate Changes (1999:01-2002:07)

01/ 01/ 99 – 05/ 23/ 02 Euro Dollar

Bulgarian Lev 0.05% 0.63%

Czech Korona 0.36% 0.67%

Estonian Kroon 0.10% 0.64%

Hungarian Forint 0.34% 0.65%

Latvian Lat 0.46% 0.25%

Lithuanian Lita* [0.66%] (0.03%) [0.02%] (0.43%)

Polish Zloty 0.75% 0.63%

Romanian Leu 0.89% 0.62%

Slovak Koruna 1.32% 0.78%

Slovenian Tolar 0.23% 0.66%

Dollar/ Euro 0.64% 0.64%

Source: Datastream. Volatility defined as standard deviations as daily exchange

rate returns. * Note two sub-samples for Lithuania due to shift in exchange rate

regime: [01/ 01/ 99 – 01/ 30/ 02] (02/ 01/ 02 – 05/ 23/ 02)

Dr. Gunther Schnabl, Tübingen University 16

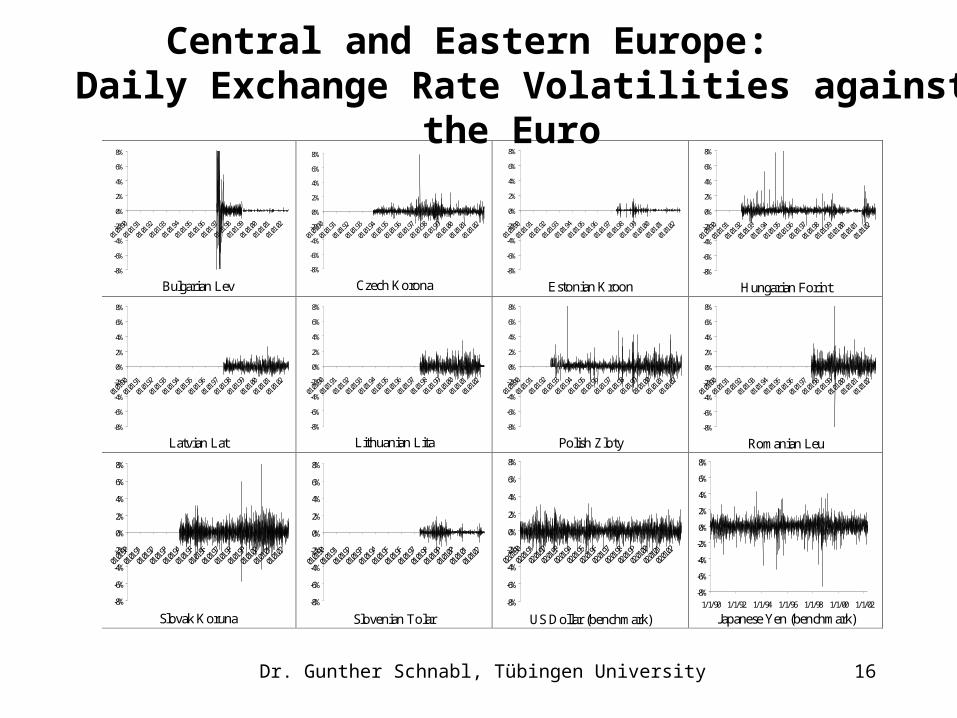

Central and Eastern Europe: Daily Exchange Rate Volatilities against

the Euro

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01.

92

01.01.

93

01.01

.94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.99

01.01.

00

01.01.

01

01.01.

02

Bulgarian Lev

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01

.90

01.01

.91

01.01.

92

01.01.

93

01.01.

94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.

99

01.01.

00

01.01.

01

01.01.

02

Czech Korona

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01.

92

01.01.

93

01.01

.94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.

99

01.01.

00

01.01.

01

01.01.

02

Estonian Kroon

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01.

92

01.01.

93

01.01.

94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.

99

01.01.

00

01.01.

01

01.01.

02

Hungarian Forint

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01

.92

01.01.

93

01.01.

94

01.01.

95

01.01.

96

01.01.

97

01.01

.98

01.01

.99

01.01.

00

01.01.

01

01.01.

02

Latvian Lat

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01.

92

01.01.

93

01.01

.94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.

99

01.01.

00

01.01.

01

01.01.

02

Lithuanian Lita

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01.

92

01.01.

93

01.01.

94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.

99

01.01.

00

01.01.

01

01.01.

02

Polish Zloty

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.

90

01.01.

91

01.01.

92

01.01.

93

01.01.

94

01.01.

95

01.01.

96

01.01.

97

01.01.

98

01.01.

99

01.01.

00

01.01.

01

01.01.

02

Romanian Leu

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.9

001.01.9101.01.9

201.01.9301.01.9401.01.95

01.01.9601.01.9

701.01.9801.01.9901.01.0

001.0

1.0101.01.0

2

Slovak Koruna

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01.01.9001.01.9101.01.9201.01.9

301.01.94

01.01.9501.01.9601.01.9701.01.9

801.01.9901.01.0

001.01.0101.01.0

2

Slovenian Tolar

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

02.01.9002.01.9102.01.9202.01.9302.01.9402.01.9502.01.9602.01.9702.01.9802.01.9902.01.0

0

02.01.0

102.01.02

US Dollar (benchmark)

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1/1/90 1/1/92 1/1/94 1/1/96 1/1/98 1/1/00 1/1/02

Japanese Yen (benchmark)

Dr. Gunther Schnabl, Tübingen University 17

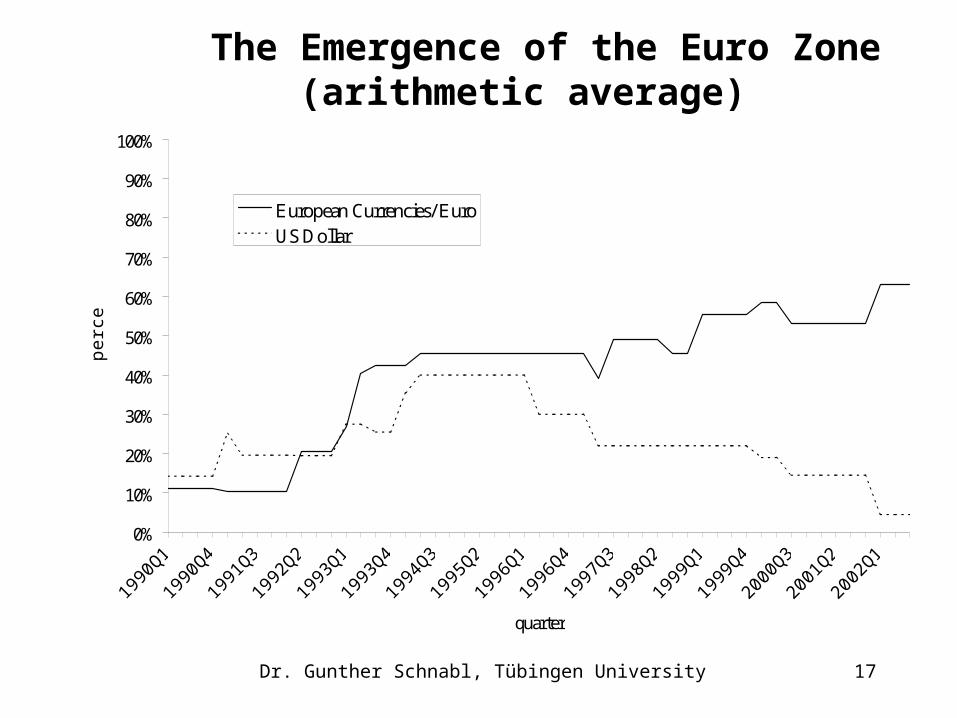

The Emergence of the Euro Zone (arithmetic average)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990

Q1

1990

Q4

1991

Q3

1992

Q2

1993

Q1

1993

Q4

1994

Q3

1995

Q2

1996

Q1

1996

Q4

1997

Q3

1998

Q2

1999

Q1

1999

Q4

2000

Q3

2001

Q2

2002

Q1

quarter

per

cen

t

European Currencies/ EuroUS Dollar

Dr. Gunther Schnabl, Tübingen University 18

4. An Informal Euro Standard as an Optimal Exchange Rate Strategy

• Latvia, Poland, the Slovak Republic and Romania should join the euro zone.

• The case against the currency basket (Latvia):– A trade weighted currency basket reduces risk

against all basket currencies, but does not eliminate it.

– A hard peg to the euro eliminates the risk against the most important currency for trade and payment transactions and allows hedging against all other currencies via the euro capital markets—at low cost.

– A hard peg to the euro further prepares Latvia for ERM2 and EMU membership.

Dr. Gunther Schnabl, Tübingen University 19

The merits of an Informal Euro Standard with Respect to EMU Accession

• Poland, the Slovak Republic and Romania should the exchange rate towards the euro to enhance macroeconomic stability in the region.

• The common nominal anchor would – favour macroeconomic convergence with the Euro

Area and among the CEE countries,– reduce risk for international trade with the Euro

Area and among the CEE countries (competitive depreciations),

– accelerate the integration of the CEE countries in the euro capital markets.

• Economic stability by both macroeconomic stabilization and growing intra-regional trade and capital linkages would also reduce the risk of speculative attacks.

Dr. Gunther Schnabl, Tübingen University 20

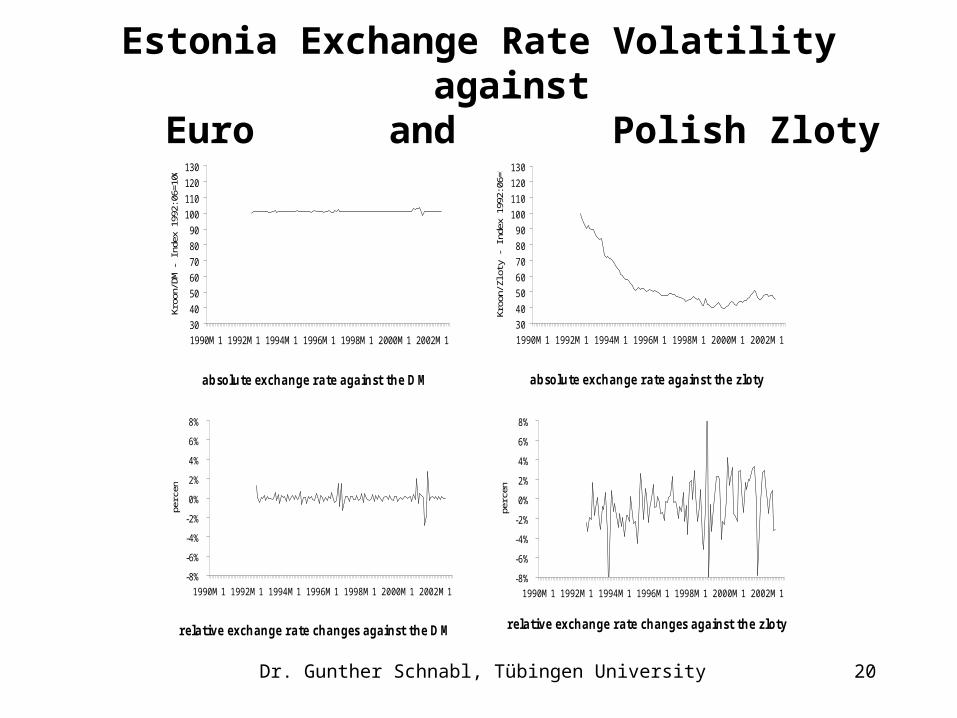

Estonia Exchange Rate Volatility against Euro and Polish Zloty

30

40

50

60

70

80

90

100

110

120

130

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Kro

on/D

M -

Inde

x 19

92:0

6=10

0

a b so lu te ex c h a n g e r a te a g a in st th e D M

30

40

50

60

70

80

90

100

110

120

130

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

Kro

on/Z

loty

- In

dex

1992

:06=

100

a b so lu te ex c h a n g e r a te a g a in st th e z lo ty

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

perc

ent

r e la t iv e e x ch a n g e r a te c h a n g e s a g a in st th e D M

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1990M1 1992M1 1994M1 1996M1 1998M1 2000M1 2002M1

perc

ent

r e la t iv e e x ch a n g e r a te c h a n g e s a g a in st th e z lo ty

Dr. Gunther Schnabl, Tübingen University 21

5. Conclusion

• The exchange rate policies of the CEE countries are still rather heterogeneous.

• As the EU accession and the intended ERM2 and EMU accession require macroeconomic convergence, Central and Eastern Europe are drifting toward a euro zone.

• The informal euro zone enhances economic stability, economic integration and—to this end—real convergence. Thus, it facilitates EMR2 and EMU accession.

• The informal euro standard does not necessitate a strictly unified hard peg to the euro but allows adjustments—for instance gradual appreciations in response to relative productivity gains (Balassa-Samuelson effect).