Embed Size (px)

Citation preview

Do

Not

Cop

y

2004, ICFAI Knowledge Center. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by any means – electronic or mechanical, without permission. To order copies, call 0091-40-2343-0462/63/64 or write to ICFAI Center for Management Research, Plot # 49, Nagarjuna Hills, Hyderabad 500 082, India or email [email protected]. Website: www.icmrindia.org

BSTA - 029

Tata Tea: Managing the Tetley Acquisition Introduction Tata Tea Limited (TTL), the second largest tea company in India (behind Hindustan Lever Ltd.), had a significant presence in over 35 countries. In 2003, TTL recorded revenue of $711.0 million and a net income of $17.5 million. Branded teas contributed 88% of the consolidated turnover of the group, with the remaining 12% coming from bulk tea, spices and investment activities. In 2000, TTL had acquired Tetley a major UK tea manufacturer. Analysts had expressed doubts whether the deal would be managed successfully. Three years after the takeover, things seemed to be improving. But there were still concerns whether TTL could service the huge debt burden resulting from the deal and whether the synergies projected before the merger could be realized.

Tata Tea’s Vision “Challenging for leadership in tea around the world” Challenging… A state of mind throughout the organisation, never being satisfied with the status quo, constantly striving to be better and to do new things, in new ways And a principle by which we manage our brands in the marketplace, creating relevant differentiation and confidently projecting clear brand identities. Leadership… Not just in size, but more importantly in the eyes of our customers and consumers, through our thoughts, ideas, behaviour and achievements. Through innovation, which will enable us to build stronger relationships with our existing consumers, reach out to new consumers and keep the category vibrant. Tea... The product scope of our vision, encompassing the widest definition of the category; the production and marketing of black and green teas, specialty fruit and herbal teas, ready-to-drink teas, tea serving systems and retailing of tea. The World... The geographic scope of our vision; building a global business by leveraging and building our brands and forging partnerships to mutual advantage.

Source: www.tatatea.com

Do

Not

Cop

y

2

Tata Tea’s Values We believe that our customers and consumers define the success of our organisation and that they should be top-of-mind in everything that we do. We believe that our people are at the heart of our organisation; and that we should give them the freedom to achieve, through clarity of direction and the creation of an informal, barrier-free culture. We believe in tea and in our products, and their role in adding to the well-being of people the world over. We believe in earning the respect of all those who know us. We believe in making a positive contribution to the people and communities our business touches. We believe that by striving to deliver our vision and by living our values we shall create more valuable business and hence over the long term increase returns to our shareholders.

Source: www.tatatea.com

Background Note

TTL’s operations spanned the entire value-chain in the tea business, including research and development, tea cultivation, manufacture of black tea, branding and distribution. The company owned 51 tea estates in India. TTL had an area of 26,500 hectares under tea cultivation and produced around 60 million kgs of black tea and two million kgs of instant tea annually. It operated nine modern packaging units across the country. TTL’s growth strategy had been multi-pronged - strengthening its business in existing geographies, expanding into new geographies and entering new product categories. TTL’s brands were found in the Middle East, West Asia, North Africa, Kazakhstan, the US and Canada. Joint venture companies had been set up in Bangladesh and Pakistan for marketing the Tetley brand. TTL had six major brands in the Indian market - Tata Tea, Tetley, Agni, Kanan Devan, Chakra Gold and Gemini, which spanned effectively every price point from Premium to Economy. In 2004, TTL had four major subsidiaries:

• The Tetley Group, headquartered in UK, owner of one of the best known International Brands of Tea - "Tetley".

• Tata Coffee Limited, India - a subsidiary that was Asia's largest coffee company. • Tata Tea Inc., USA - a subsidiary company with significant interests in instant tea in the

world's premier economy. • Watawala Plantations Limited, Sri Lanka - a joint venture with significant interest in the

tea estates, rubber and oil palm.

The Evolution of India’s largest tea company

Incorporated in 1962, TTL was controlled by the House of Tatas, one of India’s largest and most respected business groups. The formal coming together of two large business houses, namely the Tatas and James Finlay PLC in early 1960 led to the formation of a fledging company named Tata Finlay Limited. Tata Finlay, incorporated in 1962, envisaged the setting up of two business operations- the Packet tea division at Bangalore and the Instant tea operation at Munnar. James Finlay had the know how for the manufacture of Instant Tea powder - the fully soluble solids of Tea - which was the new and fast growing product in a resurgent American market. TTL

Do

Not

Cop

y

3

commenced operations in 1964 with the manufacture of packaged tea. The instant tea plant started in 1965. Tata Tea acquired the business of James Finlay, UK, and its seven associated tea companies operating in India, with effect from 1976. The technical and financial collaboration with James Finlay expired in 1971.

The Tatas had a 40 per cent stake in Tata Finlay Ltd. Subsequent to the expiry of the collaboration agreement, the overseas company sold off its entire stake to Tata Industries in 1982. After the sale of equity holdings, the name of the company was changed to Tata Tea during 1983. During 1985, the company set up a tea factory at Chundavurrai tea estate in Kerala to process black tea. In 1984, it floated an investment company, as a 100 per cent owned subsidiary called Bambino Investment & Trading Co Pvt Ltd. In 1986, Tata Tea set up a 100 per cent subsidiary in the US, Tata Tea Inc, after acquiring the instant tea processing facilities of Tritea Inc, USA. During 1990-91, Consolidated Coffee Ltd, along with its two subsidiaries, became subsidiaries of Tata Tea. In 1993, Tata Tea set up Tata Tetley Ltd, a joint venture company with the Lyons Tetley group of UK, in Cochin. In March 2000, Tata Tea acquired the worldwide tea business of UK based tea major Tetley Tea. In the same month, Tata Tea made its Global Depository Receipt issue for part- funding this acquisition. The company also set up a wholly owned subsidiary, Tata Tea, Great Britain for the purpose of acquiring the UK firm. Tata Tea's acquisition of Tetley was expected to provide the company access to markets in North America, Europe and Australia. Tata Tea had 6 major brands in the Indian market - Tata Tea, Tetley, Agni, Kanan Devan, Chakra Gold and Gemini. The company had a joint venture with the Hitachi Group, Japan, to market beverages in that country. It also had a joint venture arrangement with the Tetley Group with a production unit in Kochi, India, supplying tea bags to the Russian and Polish markets. In addition, the company had formed a joint venture in Sri Lanka through which it had acquired a controlling interest in the Watawala Plantations Ltd., with tea, rubber and oil palm estates.

Do

Not

Cop

y

4

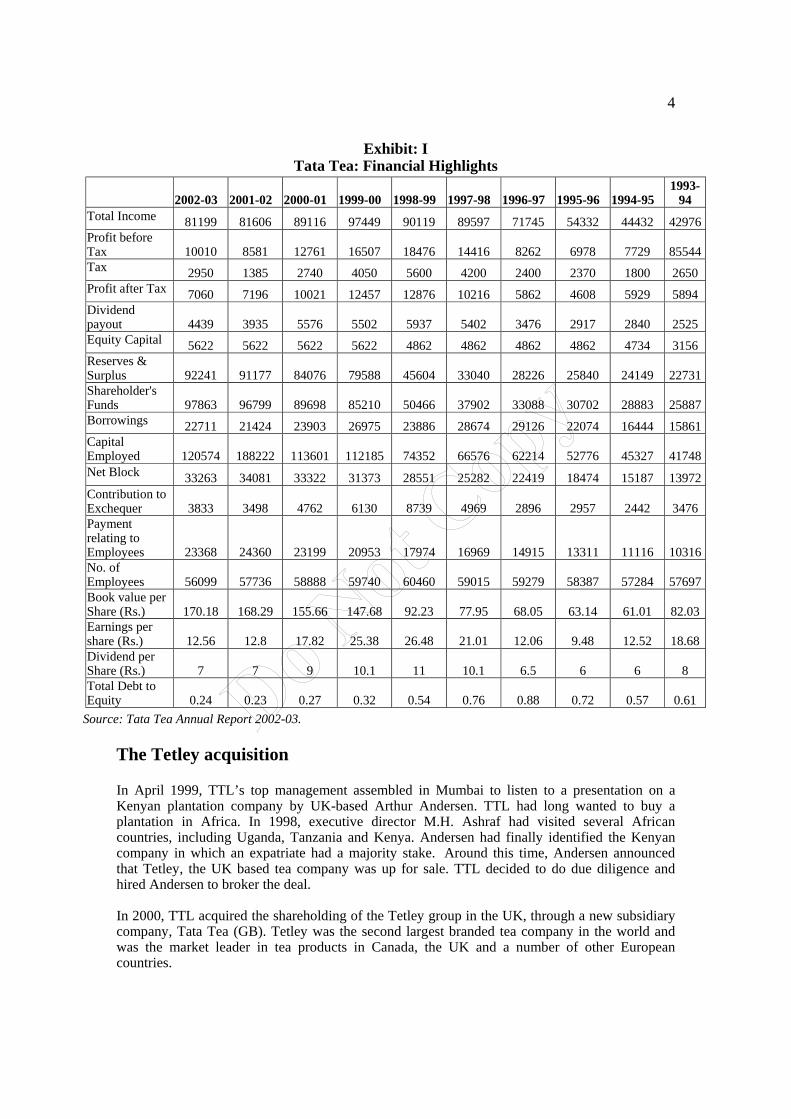

Exhibit: I Tata Tea: Financial Highlights

2002-03 2001-02 2000-01 1999-00 1998-99 1997-98 1996-97 1995-96 1994-95 1993-

94 Total Income 81199 81606 89116 97449 90119 89597 71745 54332 44432 42976 Profit before Tax 10010 8581 12761 16507 18476 14416 8262 6978 7729 85544 Tax 2950 1385 2740 4050 5600 4200 2400 2370 1800 2650 Profit after Tax 7060 7196 10021 12457 12876 10216 5862 4608 5929 5894 Dividend payout 4439 3935 5576 5502 5937 5402 3476 2917 2840 2525 Equity Capital 5622 5622 5622 5622 4862 4862 4862 4862 4734 3156 Reserves & Surplus 92241 91177 84076 79588 45604 33040 28226 25840 24149 22731 Shareholder's Funds 97863 96799 89698 85210 50466 37902 33088 30702 28883 25887 Borrowings 22711 21424 23903 26975 23886 28674 29126 22074 16444 15861 Capital Employed 120574 188222 113601 112185 74352 66576 62214 52776 45327 41748 Net Block 33263 34081 33322 31373 28551 25282 22419 18474 15187 13972 Contribution to Exchequer 3833 3498 4762 6130 8739 4969 2896 2957 2442 3476 Payment relating to Employees 23368 24360 23199 20953 17974 16969 14915 13311 11116 10316 No. of Employees 56099 57736 58888 59740 60460 59015 59279 58387 57284 57697 Book value per Share (Rs.) 170.18 168.29 155.66 147.68 92.23 77.95 68.05 63.14 61.01 82.03 Earnings per share (Rs.) 12.56 12.8 17.82 25.38 26.48 21.01 12.06 9.48 12.52 18.68 Dividend per Share (Rs.) 7 7 9 10.1 11 10.1 6.5 6 6 8 Total Debt to Equity 0.24 0.23 0.27 0.32 0.54 0.76 0.88 0.72 0.57 0.61

Source: Tata Tea Annual Report 2002-03.

The Tetley acquisition

In April 1999, TTL’s top management assembled in Mumbai to listen to a presentation on a Kenyan plantation company by UK-based Arthur Andersen. TTL had long wanted to buy a plantation in Africa. In 1998, executive director M.H. Ashraf had visited several African countries, including Uganda, Tanzania and Kenya. Andersen had finally identified the Kenyan company in which an expatriate had a majority stake. Around this time, Andersen announced that Tetley, the UK based tea company was up for sale. TTL decided to do due diligence and hired Andersen to broker the deal. In 2000, TTL acquired the shareholding of the Tetley group in the UK, through a new subsidiary company, Tata Tea (GB). Tetley was the second largest branded tea company in the world and was the market leader in tea products in Canada, the UK and a number of other European countries.

Do

Not

Cop

y

5

TTL reported a turnover of Rs 901 crore and post-tax profits of Rs 129 crore in 1998-99 and Tetley clocked a worldwide turnover of £320 million (Rs 2,240 crore) and profits of about £26 million (Rs 182 crore) in 1998. TTL realized that if it clinched the deal, it would become a Rs 3,141 crore company. TTL bid £260-270 million (Rs 1,820-1,890 crore, minus its US-based coffee operations, valued at £30-40 million) -- making this one of the biggest ever overseas deals involving an Indian company.

Exhibit: II

Tata Tea: Product Wise Information Product/Services Product-wise Turnover

2002/03 2001/02

Quantity (Kgs/lakhs)

Value (Rs/lakhs)

Quantity (Kgs/lakhs)

Value (Rs/lakhs)

Tea 679.4 71083.57 665.87 73145.22

Coffee 4.0 165.40 8.06 335.43

Spices & Others 36.98 3321.95 26.51 2491.62

Services Rendered 112.02 161.13

Total 74682.94 76133.4

Source: Tata Tea Annual report 2002-03. Tetley sold tea bags in 44 countries, had a presence in India (it has a Kochi-based, export-oriented joint venture with TTL), Canada, the US, Australia and Europe, and was the world's second largest tea brand (Lipton is the largest). It was also the UK's top tea bag brand. In a survey of 50 top British brands in April 1998, AC Nielsen, the market research agency, ranked Tetley 17th, well ahead of rival Unilever's PG Tips (26th). Tetley bought over two million pounds of tea every week at the world's major auctions, including Calcutta, Chittagong, Colombo and Mombasa. These teas came from up to 35 different countries and from some 10,000 tea estates around the globe. Tetley offered a variety of tea bags (the "single-chamber" tea bag, the "double-chamber" bag, the "long" bag). Tetley also produced flavored (black currant, strawberry, lemon, apple cinnamon -- the flavour was added via small granules and released when boiling water was poured over the tea bag) teas, herbal teas and iced tea.

In the sixties, Tetley had been bought by the UK based food and beverage conglomerate, Allied Domecq1. In July 1995, Allied Domecq decided to put it on the auction block. A host of bidders expressed interest, including food multinationals Nestle SA and Sara Lee. By then, TTL had its joint venture with Tetley in place, and knew the Allied Domecq and Tetley top brass. So it appointed investment bank J.P. Morgan as its financial advisor and put in a bid of well under £200 million. Krishna Kumar recalled, "We decided that we would finance it by raising funds in

1 Allied Domecq is a £5.5 billion, multinational food and beverage manufacturer and retailer headquartered

in the UK. It is the second largest distiller of spirits in the world and the fourth largest international retailer with 13,000 outlets worldwide. AD is the company responsible for many world-famous brands, including Beefeater, Canadian Club, Kahlua, Dunkin' Donuts, Baskin-Robbins, Carlsberg, and Tetley.

Do

Not

Cop

y

6

the US bond market. To conclude the deal, we had to raise the funds in the high-interest rate bond market and pay the seller within an agreed period. We had a letter from J.P. Morgan expressing a high level of confidence that this would be done. But that was not acceptable to Allied Domecq."2 Meanwhile senior Tetley managers led by Leon Allen (who became Tetley chairman) and Roger Price (finance director), backed by a consortium of venture capital funds such as Prudential Capital and Schroeders, offered about £190 million, cash down, and bagged Tetley.

In 1998, Tetley decided to go public and raise £400 million -- more than double its valuation in the management buy-out. But the IPO backfired and was withdrawn. Under pressure from the other shareholders, Allen and Price resigned. At the same time, Prudential and Schroeders (both of which control some 33% each of Tetley's equity) and the smaller venture capital companies wanted to book profits by offloading their stakes. In early 1999, they sounded out Sara Lee, which reportedly offered some £220-225 million. But Tetley's owners were unwilling to settle for that sum. Unilever could not bid for Tetley due to the competition laws in the UK. So TTL was sounded out next. The Indian tea company had wrested an agreement that Tetley's owners would not talk to anyone else till TTL's offer was concluded, one way or the other. In June 1999, Krishna Kumar and Kidwai flew to London to meet Tetley's owners. And after months of talks, a TTL team of senior executives flew to London in September 1999 to start a due diligence exercise.

The Synergies

TTL believed the acquisition would not only open up several new opportunities but also fortify the company in an increasingly competitive environment. As Krishna Kumar noted, "Like many others in India, TTL had the protection of nobody being allowed to come and occupy the high ground in India. This will not continue. In less than four or five years, tea from Sri Lanka and anywhere in the world will come in."3 Rivals like Hindustan Lever Ltd (HLL) would be able to buy and import good quality lower-priced tea. Kenyan crush, tear and curl (CTC, or non-premium) tea, for instance, cost at least Rs 10 a kg less than comparable Indian CTC teas; the price gap was Rs 20 a kg for premium tea. TTL could draw on Tetley's expertise and infrastructure in sourcing teas worldwide for the Indian market. Indian tea companies had in recent years been slowly shifting from selling loose tea (the exception being high-quality teas that were still hawked in auctions at high prices) to branded and packaged teas. TTL realized that when the Indian tea market was opened to international competition, it would need global brands. "The battle is a battle of brands. We believe that brands cannot be confined to regions, and even India will be a region. The world tea market is going to be dominated by two or three brands,"4 explained Krishna Kumar. TTL believed it could effectively use Tetley as a vehicle to push its packet teas in the developing world, leaving developed markets for Tetley's tea bags. The Tata name would gain visibility by entering millions of households around the globe. The Tetley tea packets would carry the legend: "Tetley, from Tata." TTL also sensed an opportunity to launch "ready to drink" tea in a range of flavors and typically drunk cold. TTL had looked at introducing RTDs in India for a long time, but had postponed its plans as the company would then have to battle Coke and Pepsi. Moreover the Indian market was not developed enough for the product. Now with the Tetley deal, things would be different.

2 “The big bid,” Business world, 27th September 1999. 3 “The big bid,” Business world 27th September 1999. 4 “The big bid,” Business world 27th September 1999.

Do

Not

Cop

y

7

Despite these synergies, the acquisition of Tetley remained a major strategic decision for TTL. With its strong distribution network, TTL had been planning to become a fast moving consumer goods (FMCG) company, along the lines of HLL. TTL had been looking at diversification into edible oils, atta and Tata Salt. Indeed, TTL's proposed FMCG makeover was ambitious. For example, for the atta (wheat flour) project, it wanted to draw on group company Rallis India's ability to reach out to farmers, and offer them technical advice on growing special wheat. TTL also saw subsidiary Consolidated Coffee being merged with TTL one day, so that TTL would become an integrated beverage company. If the company bought Tetley, all these plans would, inevitably, be put on hold.

Finalizing the deal

International takeovers were tricky for Indian companies for various reasons. Big capital outflows abroad required various official approvals. Indian accounting rules did not allow consolidation of accounts of parent and subsidiaries, making it difficult to use the target company's balance sheet to raise funds for a takeover. Tetley's £271m (US$450m) price tag was nearly four times TTL's net worth of Rs5bn (US$114m). TTL could muster only about £70m-a quarter of the purchase price-in cash. This came from a global depository receipts (GDR) equity issue of £45m-expected within two months-sales of assets (such as stakes totaling US$9m in Tata Chemicals and Associated Cement), and existing cash resources, including a £10m contribution by American subsidiary Tata Tea Inc. The other £201m had to be borrowed. TTL could not borrow directly, or else it would result in a huge interest burden. So it planned to call on other Tata group companies to help it leverage Tetley's balance sheet indirectly. TTL and its US subsidiary pumped their £70m in cash into a Tata shell company in the UK. The resulting special-purpose vehicle (SPV) raised the required additional funds through an issue of subordinated debt and syndicated loans from European investors, secured by Tetley's assets. The SPV would then purchase Tetley, with the lion's share of Tetley’s profits over the first decade, going to pay off lenders.

Integration

Integration of the two companies posed major challenges. Tata and Tetley formed several groups comprising executives from both outfits. Two of these were, the tea procurement group (TPG) and the geographic expansion group (GEG). TPG examined sourcing of tea by Tetley from India, in general and from TTL, in particular. TTL had made a small beginning as a supplier of both North and South Indian teas to Tetley in 1999. The process had since stabilized. Obviously, the quantum depended on two factors, the incremental market share that could be gathered and the ability to make subtle changes in the blend so that the product quality, particularly in the existing markets, remained acceptable. GEG's principal responsibility was to coordinate forays into new markets. Tetley, which was predominantly into the tea bag business in 2002 (92 per cent of sales), was expected to look for growth in the packet tea segment. Russia and Kazakhstan had since been identified. TTL’s experience in marketing packet tea in India and in West Asia, would help Tetley's efforts. The premium tea bag offering of TTL, which contained fine Assams and a Sri Lankan component, launched in the last quarter of 2001-02, was brought under the Tetley brand.

Do

Not

Cop

y

8

The collaboration and coordination exercise also extended to R&D. TTL joined hands with the R&D wing of Tetley, to work in new areas like new products, packaging materials, improvement in tea quality and analytical methods. In India, a new area of collaboration, which was expected to happen at a later date, was the launch of ready-to-drink teas and flavored teas, in which Tetley already had experience.

Under the control of TTL, the UK outfit had already seen a phase of restructuring and consolidation. The relatively small Greenford tea factory in West London, which produced `Drawstring' tea bags, black tea bags and a range of speciality, fruit-flavored teas and fruit/herbal infusions, was de-commissioned in 2001. Its capacity was re-located at the large Eaglescliffe facility near Middlesborough in Northeast England.

In the course of 2001-02, the company `demised' the Tata Tetley brand in the domestic market and wound up its domestic market activity to enable the company to focus on exports. Its role in the domestic market was restricted to that of a tea bag converter for TTL. Tetley also decided to reposition the brand by not using the lovable Tetley tea folk5 (Gaffer, Sidney, Clarence and Archie) in its advertisements to shed its working-class image. Krishna Kumar explained,

"We wanted to get away from the old-fashioned tea folk and promote tea as a modern lifestyle choice which promotes good health.”6

The brand's new ambassador, Trainspotting and Moulin Rouge actor Ewan McGregor, could not be more different from the northern English working- class figures he replaced. After the takeover, Tata ring-fenced7 the debt within Tetley, leaving it with a debt/ equity ratio of 3:1, which by 2002, came down to about 1.7:1. TTL believed once it reached 1:1 the two companies would be ready to integrate their balance sheets and operations into a single operating company. But many analysts believed debt reduction remained a huge challenge.

"Debt levels [in Tetley] remain very high and unless Tetley is able to generate the cash flow to repay the debt, the company will face trouble.”8

"Tea prices are already at a five-year low and that is already factored into the share price. Plus if you strip out the debt, Tetley's underlying performance is very strong.” 9

said a Bombay-based analyst who followed TTL. He added that he rated the stock as a good investment, despite the challenges ahead.

5 The Tetley Tea Folk were first used in television advertising for Tetley Tea Bags in

1973 and were originally envisaged as animated representations of Tetley’s quality control standards. 6 “Tea producer seeks a stronger brew,” Economist Intelligence Unit, viewswire database,

5th December 2002. 7 A 'ring fenced' fund is money raised for a particular activity. 8 “Tea producer seeks a stronger brew,” Economist Intelligence Unit, Viewswire database,

5th December 2002. 9 “Tea producer seeks a stronger brew,” Economist Intelligence Unit, Viewswire database,

5th December 2002.

Do

Not

Cop

y

9

With debt reduction already under way, the Tata and Tetley management began to hold regular meetings to devise common strategies on issues such as product development and new markets. Homi Khushrokhan, the (recently retired) TTL managing director explained, the push towards integration. “Our common strategy is to use Tetley as the flagship brand internationally and Tata will remain key to India. We've identified up to eight new markets for Tetley, including the Middle East and Russia…The legal merger of the two companies depended on getting the Tetley debt down to manageable levels - a debt/equity ratio of 1:1. That could be less than two years away. But in the meantime we're creating a common culture and a virtual joint management structure." 10

At the time of the takeover, cultural differences were a big hurdle. For example, Tata executives would complain about being kept waiting when visiting Tetley's UK head office, despite being the senior partners. Meanwhile, Tetley managers would complain about being run by the Tatas, who they felt knew only about India and nothing about Western markets.

TTL was more of a sleepy plantation-dependent company, whereas Tetley did not own a single plantation and sourced all its leaves. Then, there were other stumbling blocks such as compensation structures and overlap in functions. In January 2004, TTL announced that all its products marketed abroad would carry the words ‘A Tata Enterprise’ on product packs. Tetley, being a different legal entity, would pay the licence fee in due course after meeting all the conditions of the licence agreement of the Tata group. In order to be cost effective, Tetley had plans to have a few manufacturing hubs around the world. For example, Tetley, which had entered into two joint ventures — one in Bangladesh and the other in Pakistan — would help the company leverage its manufacturing and distribution networks for serving its other markets. In Australia, TTL closed its manufacturing facility and began to source its requirement from Tata Tetley Ltd, the joint venture company in Kochi. During 2002-03, Tetley restructured its operations in the US by selling its private label business, outsourcing its entire manufacturing operations to a joint venture company. It also set up another joint venture company to retain its presence in the food service sector. In line with its global ambitions, TTL looked at certain overseas markets where it had plans to introduce its brands through soft launches. These markets included the Middle East, the Gulf countries and the Far East. The Tetley group would continue to have a presence in most of the developed countries along with Russia, Bangladesh and Pakistan.

The Road Ahead

Tetley was expected to bring TTL volumes in the short term and greater opportunities in the long term. In 2003, in the UK and Canada, Tetley was the market leader with 29.4 per cent and 43.4 percent share, respectively. In Australia, it was the fastest-growing tea brand, and in the US it had 11.5 per cent of the black tea bag market. And after moving into Pakistan and Bangladesh, both big tea-consuming markets, Tetley was getting its act together in the Middle East, Africa, and

10 “Tea producer seeks a stronger brew,” Economist Intelligence Unit, Viewswire database, 5th December

2002.

Do

Not

Cop

y

10

Russia, where it was giving the final touches to a new distribution network. The £6 million that it had freed up in annual cash flow would no doubt help beef up Tetley's operations in the new and existing key markets. But TTL realized that global expansion would not be possible with one common strategy across markets, even if they were on the same continent. For example, in the UK, tea was a beverage of every day consumption. But in France, tea was not only more expensive than coffee but was also treated as a drink for special occasions. Thus, while consumers in Britain were more price sensitive, those in France wanted more exclusive products and were prepared to pay a premium. The difference in consumption habits was one reason why Tetley wanted to grow its non-black tea bag business. In 2003, its flavored tea bags, fruit teas and herbal teas accounted for only 5-6 per cent (a market estimate that TTL would neither confirm nor deny) of its revenues. But Tetley's Managing Director, K. Pringle saw a huge market potential. In an analyst conference call early in 2003, he cited the $5-billion (Rs 22,500 crore) tea market in the US, where $3 billion (Rs 13,500 crore) of the market was for ready to drink tea, $1 billion (Rs 4,500 crore) for fruit and herbal, and only the remaining $1 billion, for black tea. Till November 2003, Tetley only sold black tea in the US. Therefore, to grow, Tetley had to do a good job of launching new drinks. Meanwhile, TTL had made some major decisive moves. It decided to close two manufacturing facilities in the UK, retaining just one. In the US, where capacity had been freed up after withdrawing from the private label business, TTL turned its facility in Marietta, Atlanta, into a joint venture with Harris Tea. A Melbourne-based unit was relocated to Cochin. According to TTL's Director (Finance) Anil Goel, the move was prompted by not so much the fact that Cochin was cheaper as the fact that the Melbourne facility was constrained for capacity. Instead of investing in a bigger plant in Australia, it made sense to relocate the unit to Cochin. By late 2003, the Tetley and TTL teams were working closely in several areas. There were management committees that Khusrokhan and Pringle headed jointly. Task forces had also been created in areas such as marketing, supply chain, and procurement. (Boston Consulting Group continues to help with the integration). TTL had even transferred specific skills, such as tea buying, sourcing, and blending from Tetley. For example, it had moved from a ''heritage system''-an old-world, touchy-feely system-to Tetley's uniform computerized rating system, Broadbrush. Siganporia explained: ''With Broadbrush, you don't have to be at the buying place physically, besides it is easier to assemble recipes. Both yield a huge jump in productivity.''11 But for TTL, there was still plenty of work to be done especially at home. Although TTL straddled the entire market spectrum from economy to premium, HLL was still the leader with a 33 per cent share (org data for April 2002-March 2003). Then there were regional brands and a clutch of small, nimble unbranded players who were undercutting their bigger rivals through aggressive pricing.

11 Abir Pal, “Tata's Tea Party,” Business Today, 23rd November 2003.

Do

Not

Cop

y

11

Bibliography

1. “The big bid,” Business World, 27th September 1999.

2. “Tata Tea buys Tetley,” Economist Intelligence Unit, Viewswire database,

29th February 2000.

3. “The beverages market is changing,” Economist Intelligence Unit, Viewswire database,

1st February 2002.

4. “Liberalizing tea and papers,” Economist Intelligence Unit, Viewswire database,

1st July 2002.

5. Rabindranath Sinha, “Tata Tea, Tetley: A `seamless' venture to expand market,” Business

Line, 24th September 2002.

6. “Tea producer seeks stronger brew,” Economist Intelligence Unit, Viewswire database,

5th December 2002.

7. “Tetley Tea, Lakson tie up for Pakistan market,” Economist Intelligence Unit, Viewswire

database, 9th June 2003.

8. “The Case Of Reviving Tea,” Business Today, 17th August 2003.

9. Abir Pal, “Tata's Tea Party,” Business Today, 23rd November 2003.

10. Sambit Datta, ‘Tata Products Abroad To Sport ‘A Tata Enterprise,” Financial Express,

12th January 2004.

11. “Tata Tea gets superbrand status,” Media Releases, 22nd August 2003.

12. Tata Tea Annual Report 2002-03.

13. www.indiainfoline.com.

14. www.tatatea.com