Embed Size (px)

Citation preview

TAURON Group’s H1 2013 financial results

Warsaw, August 22, 2013

Legal disclaimer

2

This presentation serves for information purposes only and should not be treated as investment-related advice.

This presentation has been prepared by TAURON Polska Energia S.A. (“the Company”).

Neither the Company nor any of its subsidiaries shall be held accountable for any damage resulting from the use

of this presentation or a part thereof, or its contents or in any other manner in connection with this presentation.

The recipients of this presentation shall bear exclusive responsibility for their own analyses and market

assessment as well as evaluation of the Company‟s market position and its potential results in the future based on

information contained in herein.

To the extent this presentation contains forward-looking statements related to the future, in particular such terms

as ”designed”, ”planned”, ”anticipated”, or other similar expressions (including their negation), they shall be

connected with the known and unknown risks, uncertainty and other factors which might result in actual results,

financial situation, actions and achievements being materially different from any future results, actions or

achievements expressed in such forward-looking statements.

Neither the Company nor any of its subsidiaries shall be obliged to provide the recipients of this presentation with

any additional information or to update this presentation

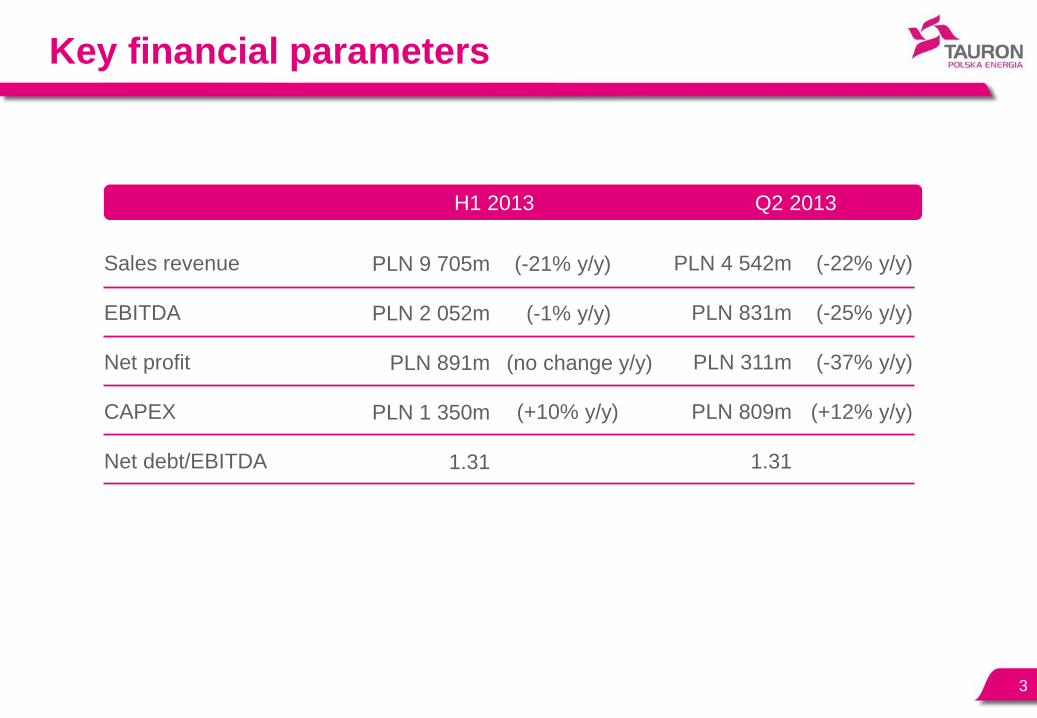

Key financial parameters

Sales revenue

EBITDA

Net profit

CAPEX

Net debt/EBITDA

3

H1 2013 Q2 2013

PLN 9 705m

PLN 2 052m

PLN 891m

PLN 1 350m

1.31

(-21% y/y)

(-1% y/y)

(no change y/y)

(+10% y/y)

PLN 4 542m

PLN 831m

PLN 311m

PLN 809m

1.31

(-22% y/y)

(-25% y/y)

(-37% y/y)

(+12% y/y)

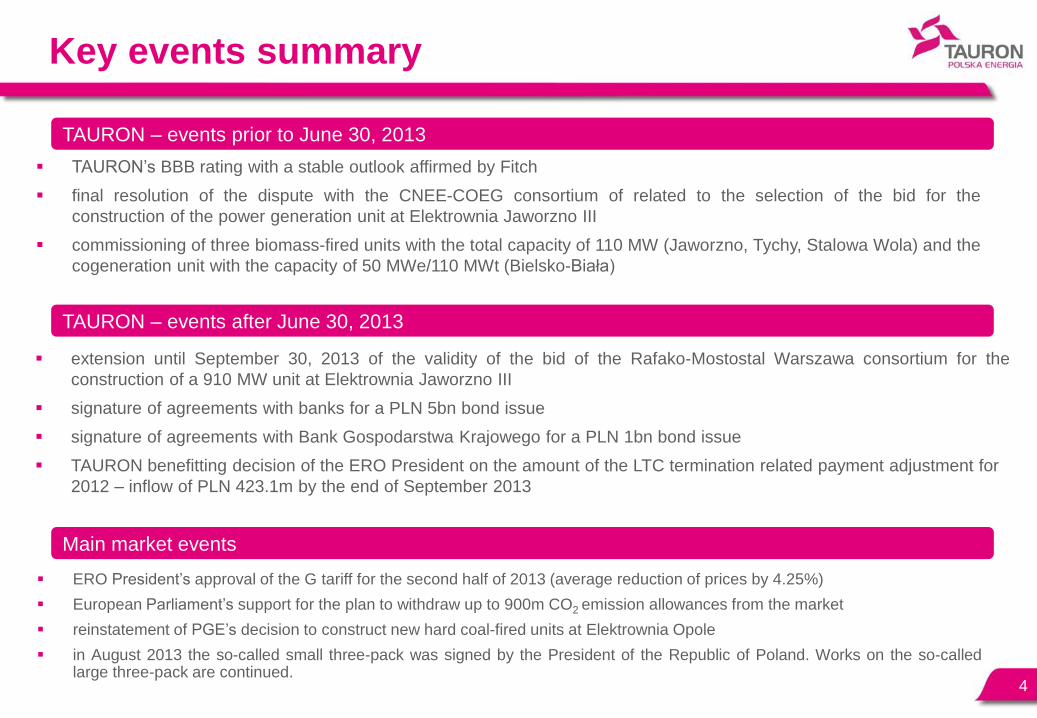

Key events summary

ERO President‟s approval of the G tariff for the second half of 2013 (average reduction of prices by 4.25%)

European Parliament‟s support for the plan to withdraw up to 900m CO2 emission allowances from the market

reinstatement of PGE‟s decision to construct new hard coal-fired units at Elektrownia Opole

in August 2013 the so-called small three-pack was signed by the President of the Republic of Poland. Works on the so-called large three-pack are continued.

4

TAURON‟s BBB rating with a stable outlook affirmed by Fitch

final resolution of the dispute with the CNEE-COEG consortium of related to the selection of the bid for the

construction of the power generation unit at Elektrownia Jaworzno III

commissioning of three biomass-fired units with the total capacity of 110 MW (Jaworzno, Tychy, Stalowa Wola) and the

cogeneration unit with the capacity of 50 MWe/110 MWt (Bielsko-Biała)

extension until September 30, 2013 of the validity of the bid of the Rafako-Mostostal Warszawa consortium for the

construction of a 910 MW unit at Elektrownia Jaworzno III

signature of agreements with banks for a PLN 5bn bond issue

signature of agreements with Bank Gospodarstwa Krajowego for a PLN 1bn bond issue

TAURON benefitting decision of the ERO President on the amount of the LTC termination related payment adjustment for

2012 – inflow of PLN 423.1m by the end of September 2013

Main market events

TAURON – events prior to June 30, 2013

TAURON – events after June 30, 2013

Macroeconomic and market situation

5

0%

1%

2%

3%

4%

5%

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

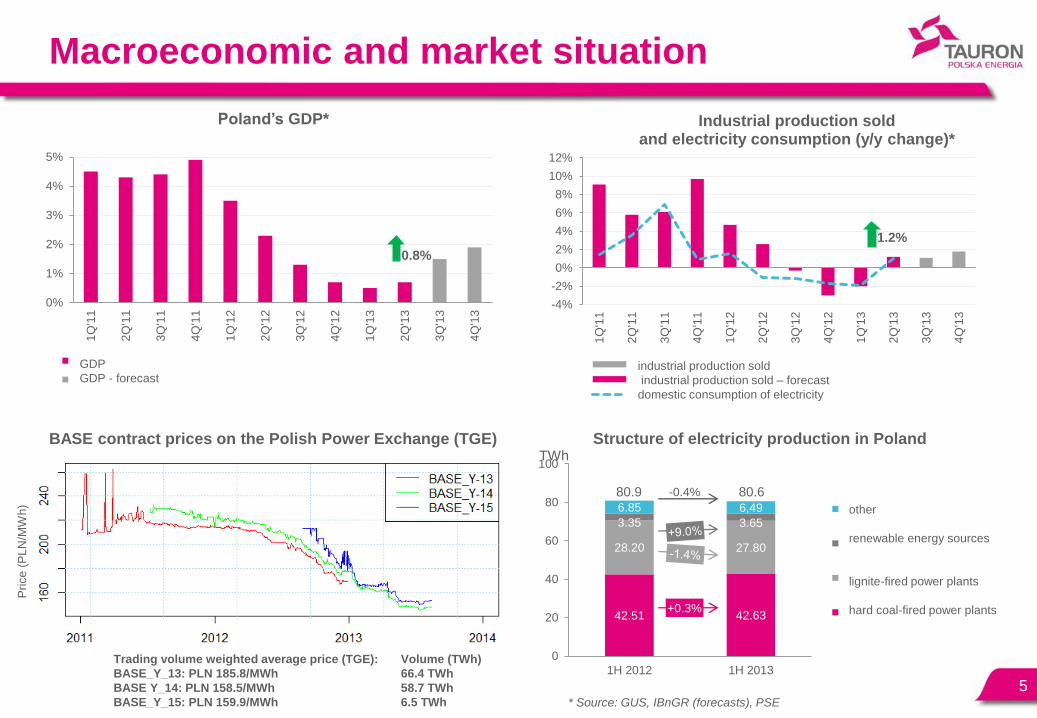

Poland’s GDP*

PKB

PKB - prognoza

GDP

GDP - forecast

42.51 42.63

28.20 27.80

3.35 3.65

6.85 6,49

0

20

40

60

80

100

1H 2012 1H 2013

Structure of electricity production in Poland

pozostałe

odnawialne źródła energii

el. cieplne na węgielbrunatny

el. cieplne na węgielkamienny

80.6 80.9

* Source: GUS, IBnGR (forecasts), PSE

TWh

+0.3%

-0.4%

0.8%

BASE contract prices on the Polish Power Exchange (TGE)

Trading volume weighted average price (TGE): Volume (TWh)

BASE_Y_13: PLN 185.8/MWh 66.4 TWh

BASE Y_14: PLN 158.5/MWh 58.7 TWh

BASE_Y_15: PLN 159.9/MWh 6.5 TWh

1.2%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

1Q

'11

2Q

'11

3Q

'11

4Q

'11

1Q

'12

2Q

'12

3Q

'12

4Q

'12

1Q

'13

2Q

'13

3Q

'13

4Q

'13

Industrial production sold and electricity consumption (y/y change)*

produkcja sprzedana przemysłu - prognoza

produkcja sprzedana przemysłu

krajowe zużycie energii elektrycznej

industrial production sold

industrial production sold – forecast

domestic consumption of electricity

other

renewable energy sources

lignite-fired power plants

hard coal-fired power plants

Pri

ce

(P

LN

/MW

h)

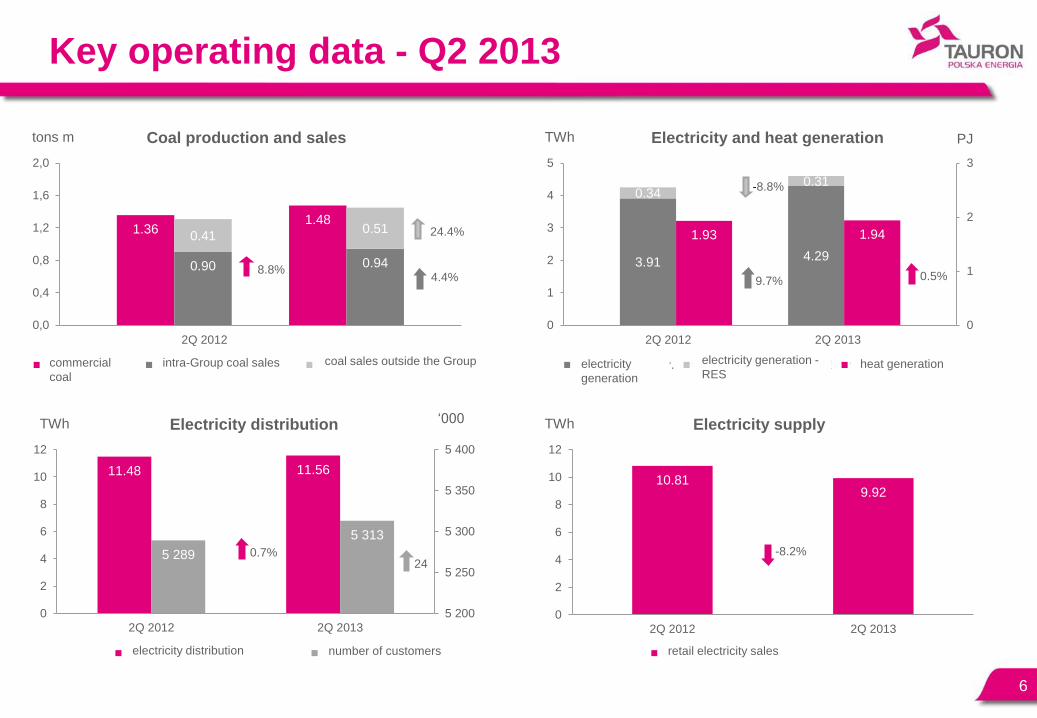

1.36 1.48

0.90 0.94

0.41 0.51

0,0

0,4

0,8

1,2

1,6

2,0

Coal production and sales

węgiel handlowy sprzedaż węgla do Grupy sprzedaż węgla poza Grupę

tons m

4.4%

24.4%

8.8%

Key operating data - Q2 2013

3.91 4.29

0.34 0.31

1.93 1.94

0

1

2

3

0

1

2

3

4

5

2Q 2012 2Q 2013

Electricity and heat generation

wytw.energii elektr. wytw. energii elektr. - OZE wytwarzanie ciepła

TWh PJ

0.5% 9.7%

-8.8%

6

11.48 11.56

5 289

5 313

5 200

5 250

5 300

5 350

5 400

0

2

4

6

8

10

12

2Q 2012 2Q 2013

Electricity distribution

dystrybucja energii elektrycznej liczba klientów

TWh „000

0.7% 24

2Q 2012 2Q 2013

10.81 9.92

0

2

4

6

8

10

12

2Q 2012 2Q 2013

Electricity supply

sprzedaż detaliczna energii elektrycznej

TWh

-8.2%

2Q 2012 2Q 2013

coal sales outside the Group commercial

coal

intra-Group coal sales heat generation electricity

generation

electricity generation -

RES

retail electricity sales electricity distribution

number of customers

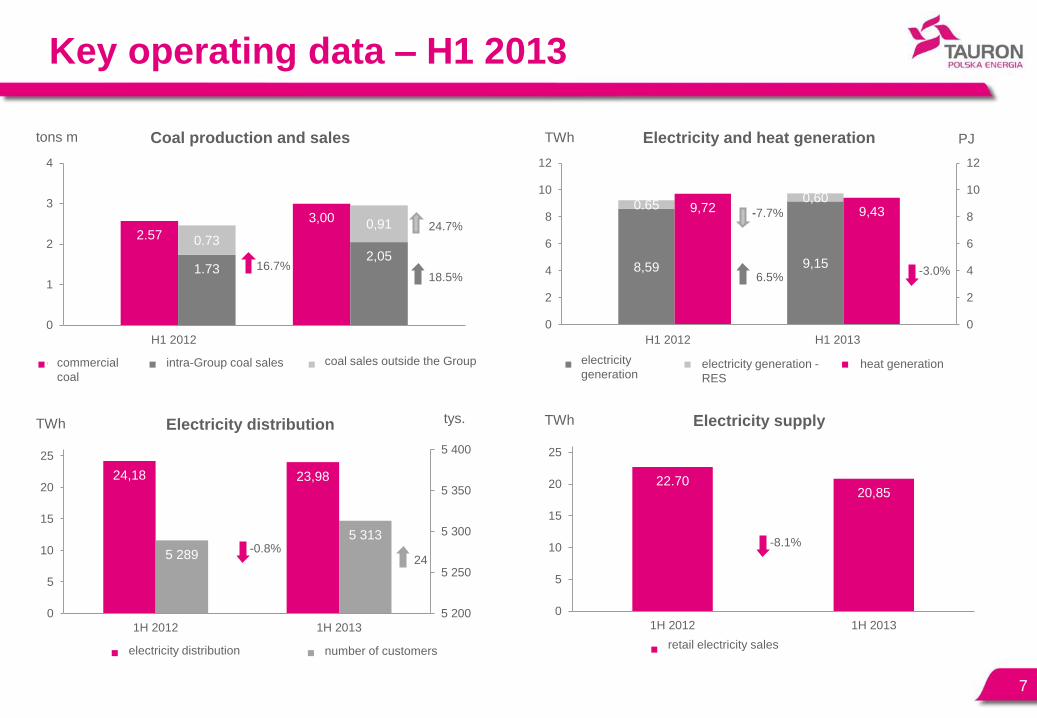

Key operating data – H1 2013

2.57

3,00

1.73 2,05

0.73

0,91

0

1

2

3

4

Coal production and sales

węgiel handlowy sprzedaż węgla do Grupy sprzedaż węgla poza Grupę

tons m

H1 2012 H1 2013

18.5%

24.7%

16.7% 8,59 9,15

0.65 0,60

9,72 9,43

0

2

4

6

8

10

12

0

2

4

6

8

10

12

1H 2012 1H 2013

Electricity and heat generation

wytw.energii elektr. wytw. energii elektr. - OZE wytwarzanie ciepła

TWh PJ

-3.0% 6.5%

-7.7%

electricity

generation

electricity generation -

RES

heat generation

7

24,18 23,98

5 289

5 313

5 200

5 250

5 300

5 350

5 400

0

5

10

15

20

25

1H 2012 1H 2013

Electricity distribution

dystrybucja energii elektrycznej liczba klientów

TWh tys.

-0.8% 24

H1 2012 H1 2013

22.70 20,85

0

5

10

15

20

25

1H 2012 1H 2013

Electricity supply

sprzedaż detaliczna energii elektrycznej

TWh

-8.1%

retail electricity sales

commercial

coal

intra-Group coal sales

coal sales outside the Group

electricity distribution

number of customers

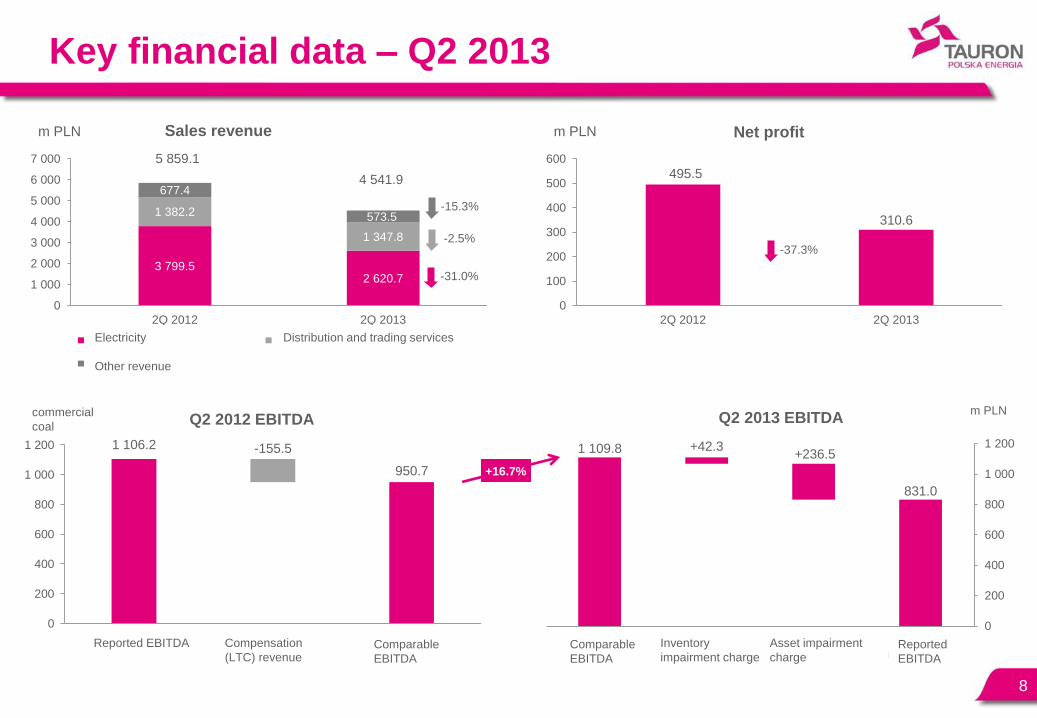

Key financial data – Q2 2013

3 799.5 2 620.7

1 382.2

1 347.8

677.4

573.5

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

2Q 2012 2Q 2013

Sales revenue

Energia elektryczna Usługi dystrybucyjne i handlowe

Pozostałe przychody

m PLN

5 859.1

4 541.9

-31.0%

-15.3%

-2.5%

Electricity

Other revenue

Distribution and trading services

8

495.5

310.6

0

100

200

300

400

500

600

2Q 2012 2Q 2013

Net profit m PLN

-37.3%

831.0

+236.5 +42.3 1 109.8

0

200

400

600

800

1 000

1 200

EBITDAraportowana

Odpis aktualizującywartość aktywów

Odpis aktualizującywartość zapasów

EBITDAporównywalna

Q2 2013 EBITDA m PLN

1 106.2 -155.5

950.7

0

200

400

600

800

1 000

1 200

EBITDAraportowana

Przychody z tytułurekompensaty (KDT)

EBITDAporównywalna

Q2 2012 EBITDA m PLN commercial

coal

+16.7%

Reported EBITDA Comparable

EBITDA

Compensation

(LTC) revenue Comparable

EBITDA

Reported

EBITDA

Inventory

impairment charge

Asset impairment

charge

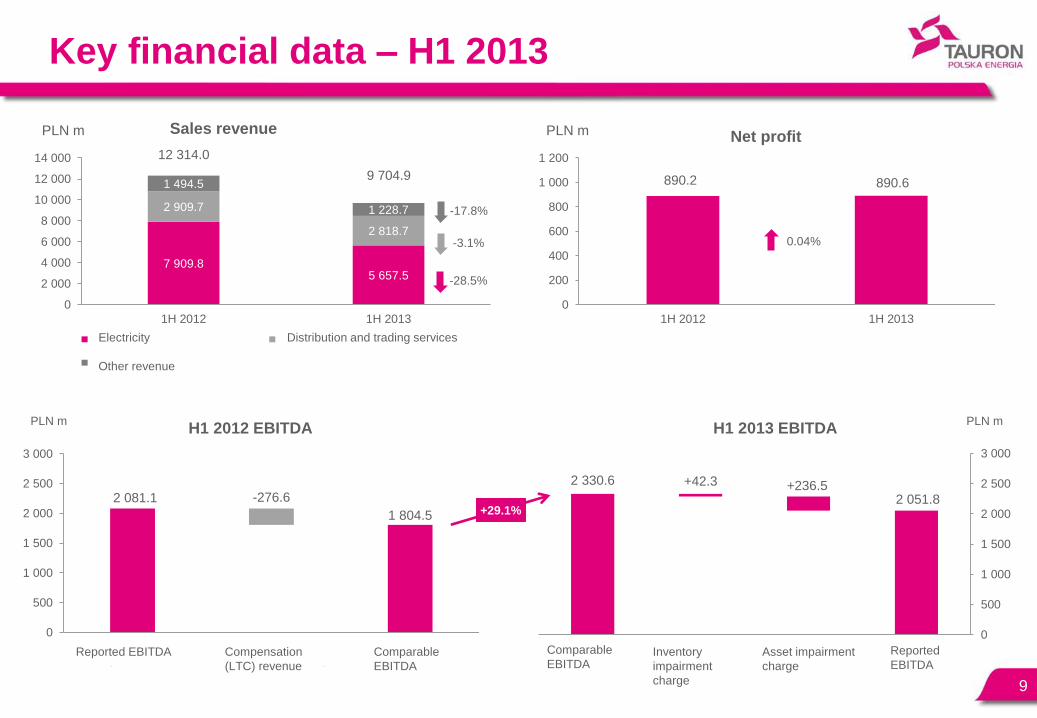

Key financial data – H1 2013

7 909.8 5 657.5

2 909.7

2 818.7

1 494.5

1 228.7

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

1H 2012 1H 2013

Sales revenue

Energia elektryczna Usługi dystrybucyjne i handlowe

Pozostałe przychody

PLN m

12 314.0

9 704.9

-28.5%

-17.8%

-3.1%

9

890.2 890.6

0

200

400

600

800

1 000

1 200

1H 2012 1H 2013

Net profit PLN m

0.04%

2 051.8 +236.5 +42.3 2 330.6

0

500

1 000

1 500

2 000

2 500

3 000

EBITDAraportowana

Odpis aktualizującywartość aktywów

Odpis aktualizującywartość zapasów

EBITDAporównywalna

H1 2013 EBITDA PLN m

2 081.1 -276.6

1 804.5

0

500

1 000

1 500

2 000

2 500

3 000

EBITDAraportowana

Przychody z tytułurekompensaty (KDT)

EBITDAporównywalna

H1 2012 EBITDA PLN m

+29.1%

Electricity

Other revenue

Distribution and trading services

Reported EBITDA Comparable

EBITDA Compensation

(LTC) revenue

Comparable

EBITDA

Reported

EBITDA Inventory

impairment

charge

Asset impairment

charge

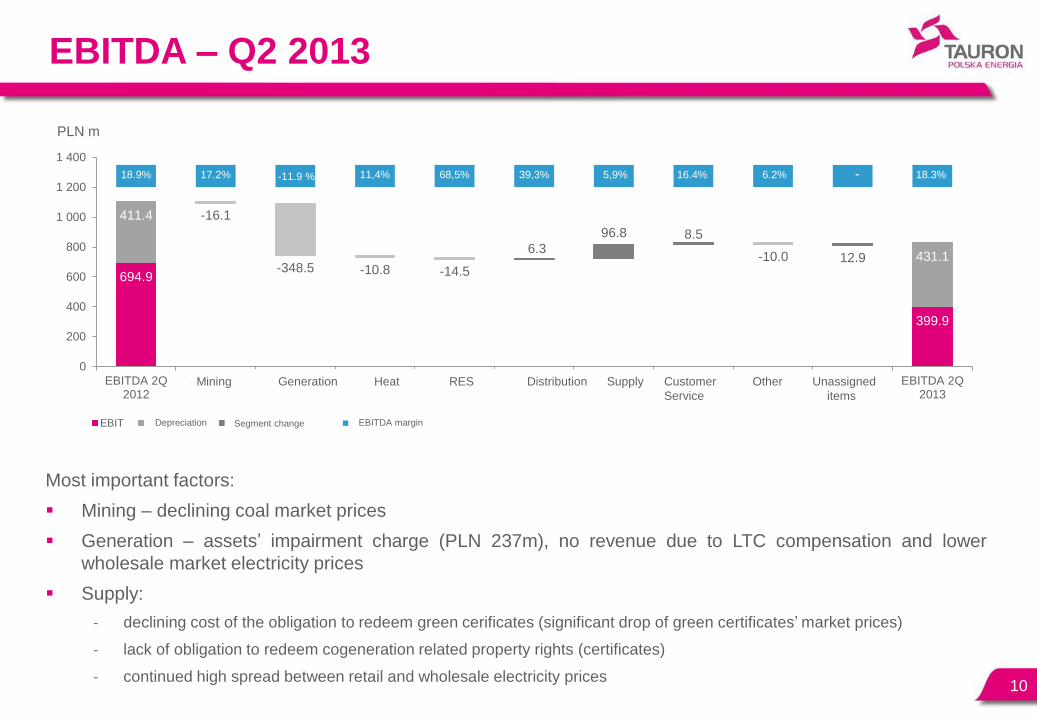

EBITDA – Q2 2013

Most important factors:

Mining – declining coal market prices

Generation – assets‟ impairment charge (PLN 237m), no revenue due to LTC compensation and lower

wholesale market electricity prices

Supply:

- declining cost of the obligation to redeem green cerificates (significant drop of green certificates‟ market prices)

- lack of obligation to redeem cogeneration related property rights (certificates)

- continued high spread between retail and wholesale electricity prices 10

694.9

399.9

411.4

431.1

-16.1

-348.5 -10.8 -14.5

6.3

96.8 8.5

-10.0 12.9

18.9% 17.2% 11,4% 68,5% 39,3% 5,9% 16.4% 6.2% 18.3%

0

200

400

600

800

1 000

1 200

1 400

EBITDA 2Q2012

Wydobycie Wytwarzanie Ciepło OZE Dystrybucja Sprzedaż Obsługaklienta

Pozostałe Pozycjenieprzypisane

EBITDA 2Q2013

EBIT Amortyzacja Zmiana w segmencie Marża EBITDA

PLN m

- -11.9 %

Mining Generation Heat RES Distribution Supply Customer Other Unassigned

Service items

Depreciation Segment change EBITDA margin

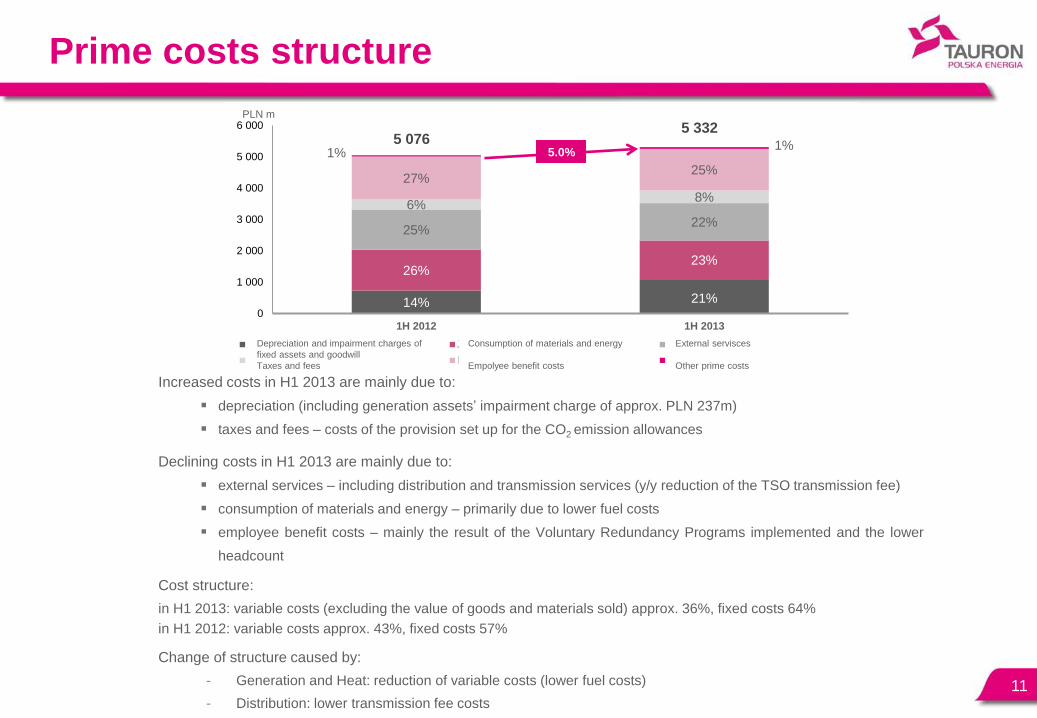

Prime costs structure

11

Increased costs in H1 2013 are mainly due to:

depreciation (including generation assets‟ impairment charge of approx. PLN 237m)

taxes and fees – costs of the provision set up for the CO2 emission allowances

Declining costs in H1 2013 are mainly due to:

external services – including distribution and transmission services (y/y reduction of the TSO transmission fee)

consumption of materials and energy – primarily due to lower fuel costs

employee benefit costs – mainly the result of the Voluntary Redundancy Programs implemented and the lower

headcount

Cost structure:

in H1 2013: variable costs (excluding the value of goods and materials sold) approx. 36%, fixed costs 64%

in H1 2012: variable costs approx. 43%, fixed costs 57%

Change of structure caused by:

- Generation and Heat: reduction of variable costs (lower fuel costs)

- Distribution: lower transmission fee costs

14% 21%

26% 23%

25% 22%

6% 8%

27% 25%

1% 1%

0

1 000

2 000

3 000

4 000

5 000

6 000

1H 2012 1H 2013

PLN m

Amortyzacja i odpisy aktualiz. ŚT i WN Zużycie materiałów i energii Usługi obce

Podatki i opłaty Koszty świadczeń pracowniczych Pozostałe koszty rodzajowe

5 076 5 332

5.0%

Depreciation and impairment charges of

fixed assets and goodwill

Taxes and fees

Consumption of materials and energy

Empolyee benefit costs

External servisces

Other prime costs

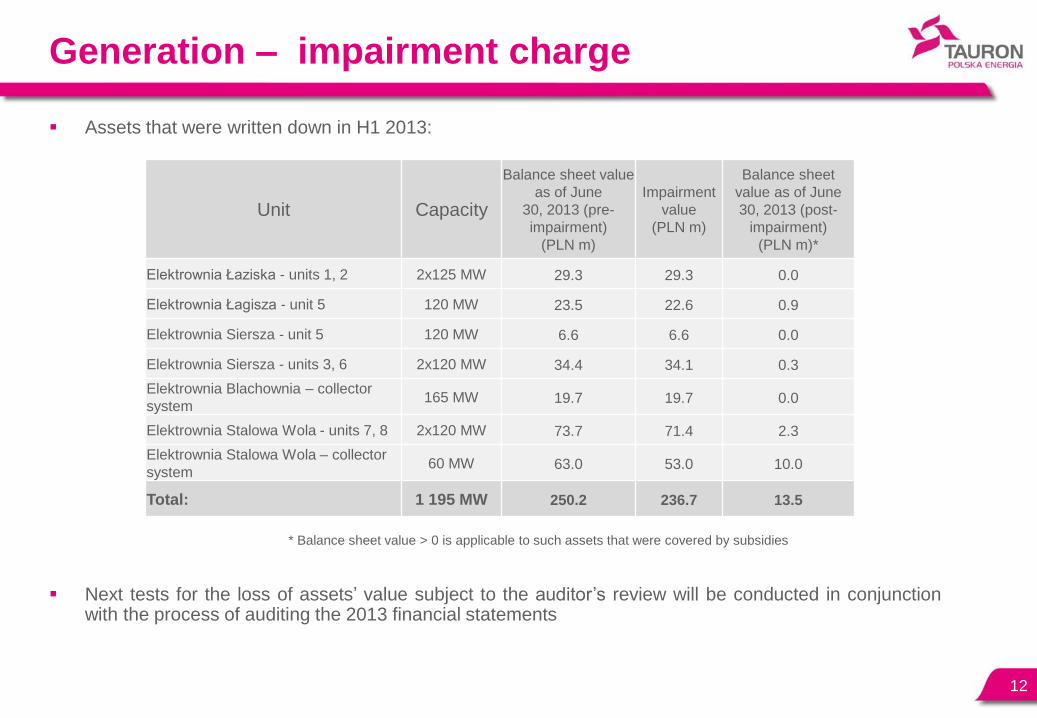

Generation – impairment charge

Assets that were written down in H1 2013:

* Balance sheet value > 0 is applicable to such assets that were covered by subsidies

Next tests for the loss of assets‟ value subject to the auditor‟s review will be conducted in conjunction with the process of auditing the 2013 financial statements

12

Unit Capacity

Balance sheet value

as of June

30, 2013 (pre-

impairment)

(PLN m)

Impairment

value

(PLN m)

Balance sheet

value as of June

30, 2013 (post-

impairment)

(PLN m)*

Elektrownia Łaziska - units 1, 2 2x125 MW 29.3 29.3 0.0

Elektrownia Łagisza - unit 5 120 MW 23.5 22.6 0.9

Elektrownia Siersza - unit 5 120 MW 6.6 6.6 0.0

Elektrownia Siersza - units 3, 6 2x120 MW 34.4 34.1 0.3

Elektrownia Blachownia – collector

system 165 MW 19.7 19.7 0.0

Elektrownia Stalowa Wola - units 7, 8 2x120 MW 73.7 71.4 2.3

Elektrownia Stalowa Wola – collector

system 60 MW 63.0 53.0 10.0

Total: 1 195 MW 250.2 236.7 13.5

Generation – prospects for 2013

13

Factors that may have a positive impact on the

earnings in H2 2013:

• decline of electricity market prices – realizing a higher margin

on electricity trading

• higher rate of utilizing the capacity of the 460 MW unit at

Elektrownia Łagisza

• increasing prices of property rights to certificates of origin for

electricity generated in RES

• lower per unit costs of hard coal and biofuels consumption

(PLN/GJ)

Factors that may have a negative impact on the

earnings in H2 2013:

• higher fixed costs (upgrades, external services, labor costs)

• higher costs of the provision for CO2

• lower heat sales

• lower margin on the EUA/CER/ERU exchange transactions

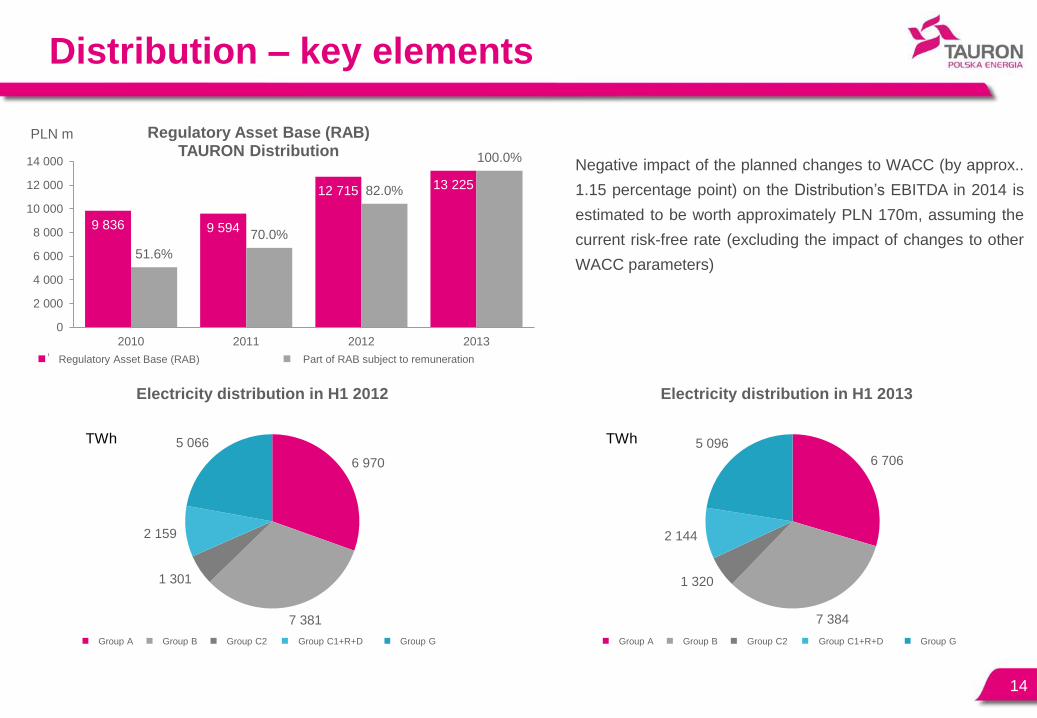

Distribution – key elements

14

9 836 9 594

12 715 13 225

51.6%

70.0%

82.0%

100.0%

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

2010 2011 2012 2013

Regulatory Asset Base (RAB) TAURON Distribution

Wartość regulacyjna aktywów (WRA) Udział WRA podlegający wynagradzaniu

PLN m

6 706

7 384

1 320

2 144

5 096

Electricity distribution in H1 2013

Grupa A Grupa B Grupa C2 Grupa C1+R+D Grupa G

TWh

6 970

7 381

1 301

2 159

5 066

Electricity distribution in H1 2012

Grupa A Grupa B Grupa C2 Grupa C1+R+D Grupa G

TWh

Negative impact of the planned changes to WACC (by approx..

1.15 percentage point) on the Distribution‟s EBITDA in 2014 is

estimated to be worth approximately PLN 170m, assuming the

current risk-free rate (excluding the impact of changes to other

WACC parameters)

Group A Group A Group B Group B Group C2 Group C2 Group C1+R+D Group C1+R+D Group G Group G

Regulatory Asset Base (RAB) Part of RAB subject to remuneration

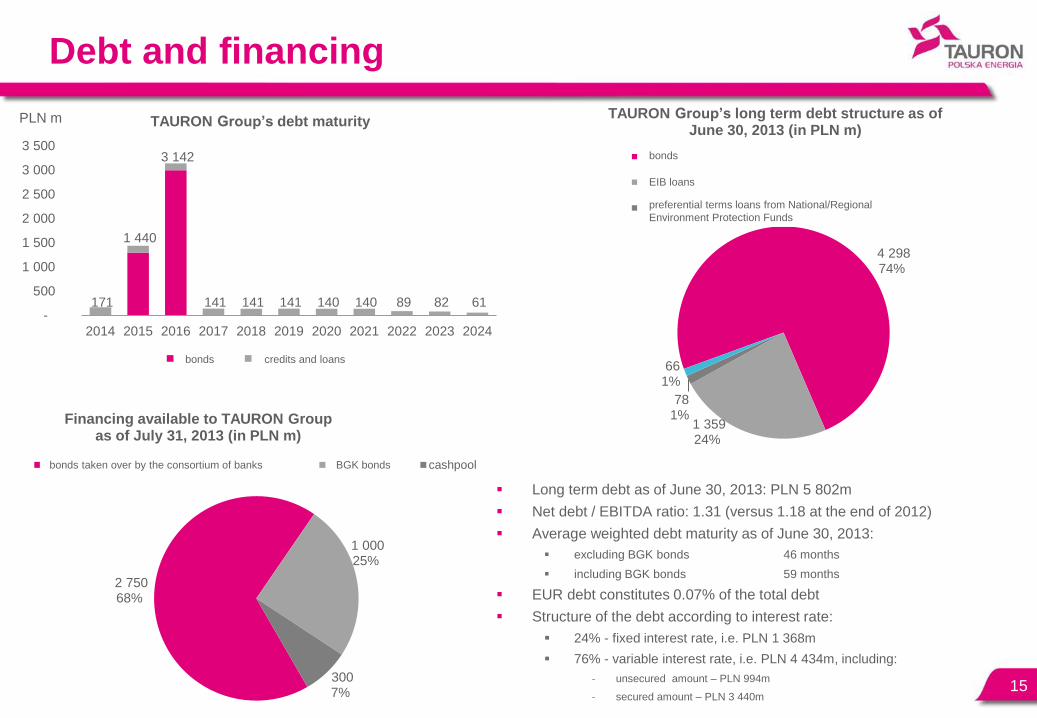

Debt and financing

15

171

1 440

3 142

141 141 141 140 140 89 82 61 -

500

1 000

1 500

2 000

2 500

3 000

3 500

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

TAURON Group’s debt maturity

obligacje kredyty i pożyczki

PLN m

4 298 74%

1 359 24%

78 1%

66 1%

TAURON Group’s long term debt structure as of June 30, 2013 (in PLN m)

obligacje

kredyty z EBI

pożyczki preferencyjne zNFOŚiGW/WFOŚiGW

2 750 68%

1 000 25%

300 7%

Financing available to TAURON Group as of July 31, 2013 (in PLN m)

obligacje obejmowane przez konsorcjum banków obligacje BGK cashpool

Long term debt as of June 30, 2013: PLN 5 802m

Net debt / EBITDA ratio: 1.31 (versus 1.18 at the end of 2012)

Average weighted debt maturity as of June 30, 2013:

excluding BGK bonds 46 months

including BGK bonds 59 months

EUR debt constitutes 0.07% of the total debt

Structure of the debt according to interest rate:

24% - fixed interest rate, i.e. PLN 1 368m

76% - variable interest rate, i.e. PLN 4 434m, including:

- unsecured amount – PLN 994m

- secured amount – PLN 3 440m

bonds credits and loans

bonds

EIB loans

preferential terms loans from National/Regional

Environment Protection Funds

bonds taken over by the consortium of banks BGK bonds

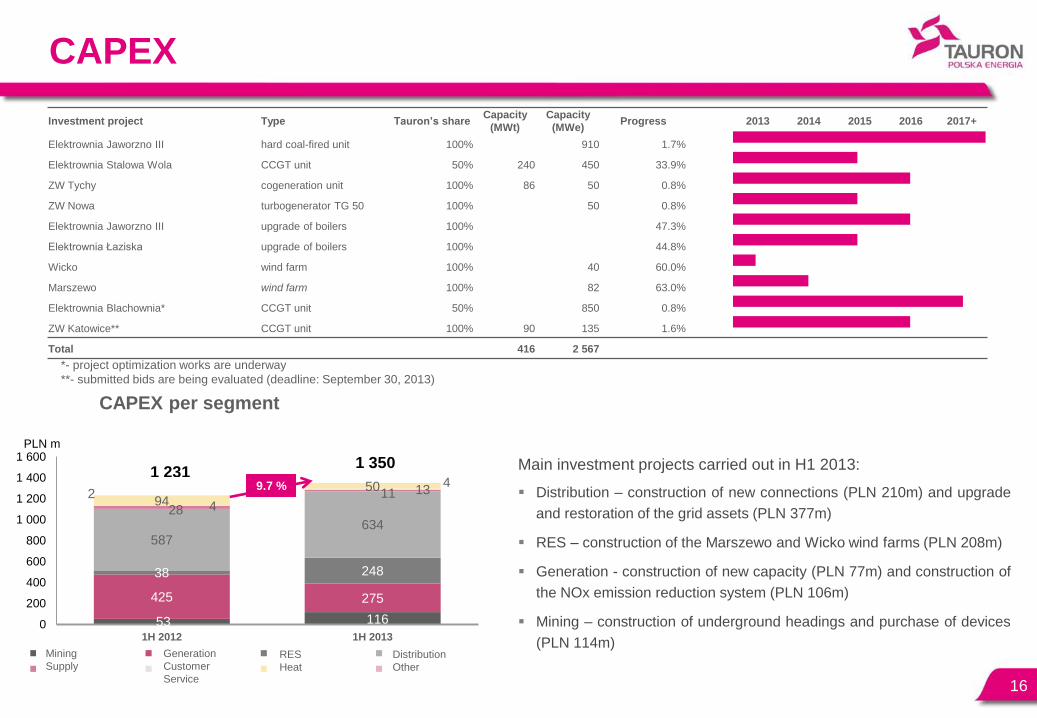

CAPEX

CAPEX per segment

16

Main investment projects carried out in H1 2013:

Distribution – construction of new connections (PLN 210m) and upgrade

and restoration of the grid assets (PLN 377m)

RES – construction of the Marszewo and Wicko wind farms (PLN 208m)

Generation - construction of new capacity (PLN 77m) and construction of

the NOx emission reduction system (PLN 106m)

Mining – construction of underground headings and purchase of devices

(PLN 114m)

Investment project Type Tauron’s share Capacity

(MWt)

Capacity

(MWe) Progress 2013 2014 2015 2016 2017+

Elektrownia Jaworzno III hard coal-fired unit 100% 910 1.7%

Elektrownia Stalowa Wola CCGT unit 50% 240 450 33.9%

ZW Tychy cogeneration unit 100% 86 50 0.8%

ZW Nowa turbogenerator TG 50 100% 50 0.8%

Elektrownia Jaworzno III upgrade of boilers 100% 47.3%

Elektrownia Łaziska upgrade of boilers 100% 44.8%

Wicko wind farm 100% 40 60.0%

Marszewo wind farm 100% 82 63.0%

Elektrownia Blachownia* CCGT unit 50% 850 0.8%

ZW Katowice** CCGT unit 100% 90 135 1.6%

Total 416 2 567

*- project optimization works are underway

**- submitted bids are being evaluated (deadline: September 30, 2013)

53 116

425 275

38 248

587 634

28

11 4

13 94

50 2

4

0

200

400

600

800

1 000

1 200

1 400

1 600

1H 2012 1H 2013

Wydobycie Wytwarzanie OZE Dystrybucja

Sprzedaż Obsługa Klienta Ciepło Pozostałe

PLN m

1 231 1 350

9.7 %

Mining

Supply

Generation

Customer

Service

RES

Heat

Distribution

Other

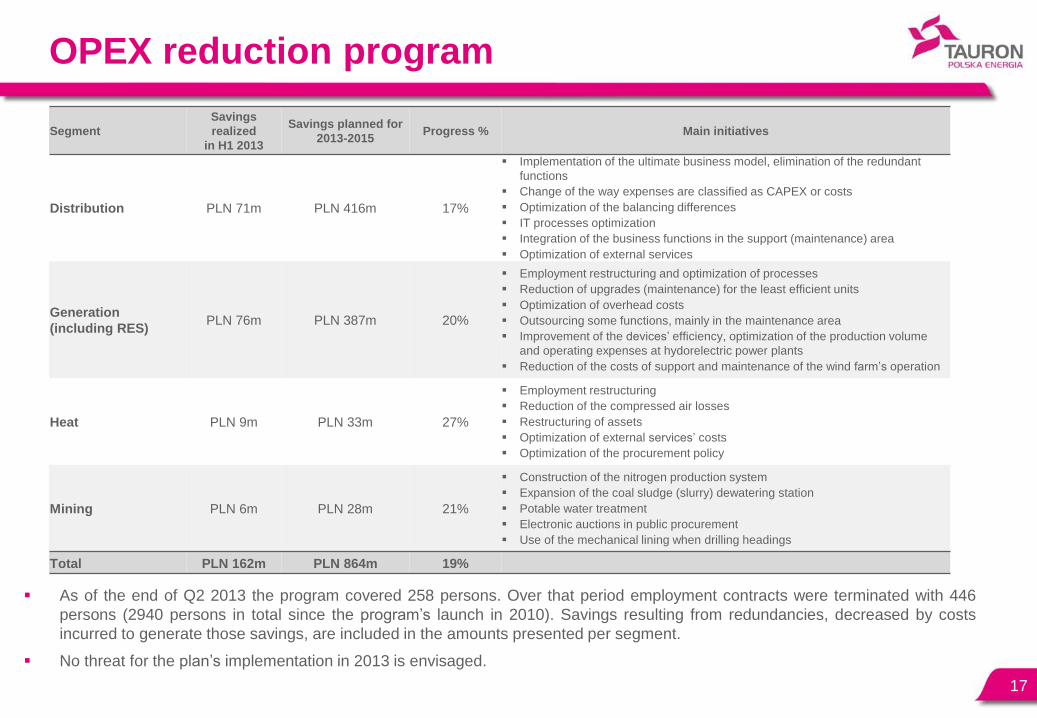

OPEX reduction program

As of the end of Q2 2013 the program covered 258 persons. Over that period employment contracts were terminated with 446

persons (2940 persons in total since the program‟s launch in 2010). Savings resulting from redundancies, decreased by costs

incurred to generate those savings, are included in the amounts presented per segment.

No threat for the plan‟s implementation in 2013 is envisaged.

17

Segment

Savings

realized

in H1 2013

Savings planned for

2013-2015 Progress % Main initiatives

Distribution PLN 71m PLN 416m 17%

Implementation of the ultimate business model, elimination of the redundant

functions

Change of the way expenses are classified as CAPEX or costs

Optimization of the balancing differences

IT processes optimization

Integration of the business functions in the support (maintenance) area

Optimization of external services

Generation

(including RES) PLN 76m PLN 387m 20%

Employment restructuring and optimization of processes

Reduction of upgrades (maintenance) for the least efficient units

Optimization of overhead costs

Outsourcing some functions, mainly in the maintenance area

Improvement of the devices‟ efficiency, optimization of the production volume

and operating expenses at hydorelectric power plants

Reduction of the costs of support and maintenance of the wind farm‟s operation

Heat PLN 9m PLN 33m 27%

Employment restructuring

Reduction of the compressed air losses

Restructuring of assets

Optimization of external services‟ costs

Optimization of the procurement policy

Mining PLN 6m PLN 28m 21%

Construction of the nitrogen production system

Expansion of the coal sludge (slurry) dewatering station

Potable water treatment

Electronic auctions in public procurement

Use of the mechanical lining when drilling headings

Total PLN 162m PLN 864m 19%

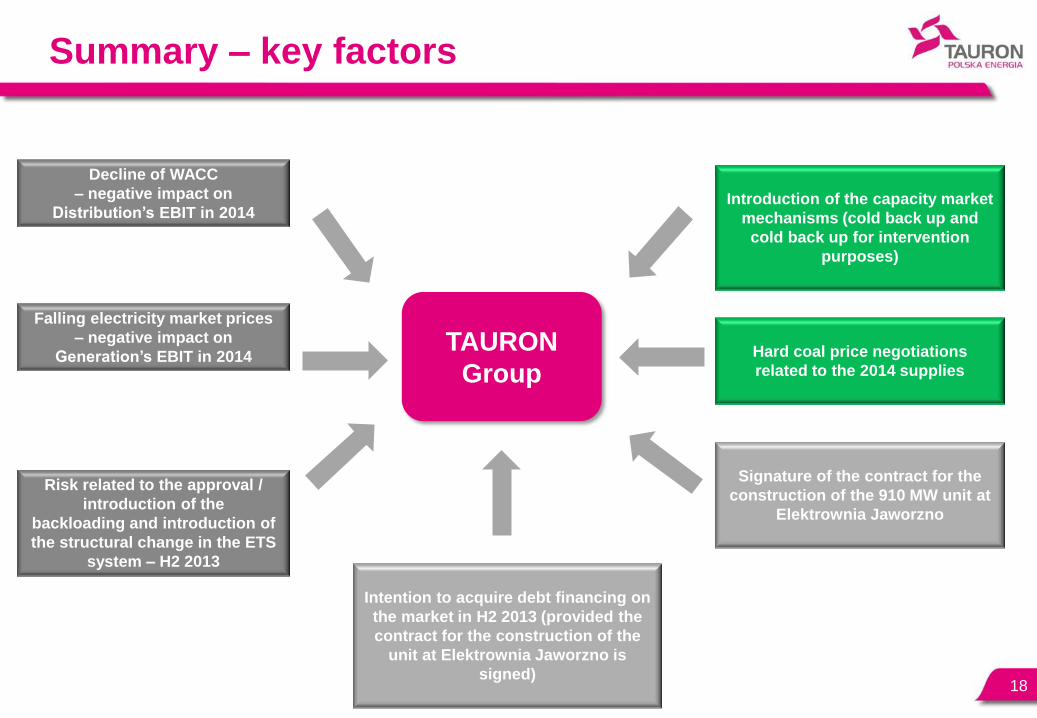

Summary – key factors

18

Decline of WACC

– negative impact on

Distribution’s EBIT in 2014

Falling electricity market prices

– negative impact on

Generation’s EBIT in 2014

Intention to acquire debt financing on

the market in H2 2013 (provided the

contract for the construction of the

unit at Elektrownia Jaworzno is

signed)

Signature of the contract for the

construction of the 910 MW unit at

Elektrownia Jaworzno

Hard coal price negotiations

related to the 2014 supplies

Introduction of the capacity market

mechanisms (cold back up and

cold back up for intervention

purposes)

TAURON

Group

Risk related to the approval /

introduction of the

backloading and introduction of

the structural change in the ETS

system – H2 2013

Thank you – Q&A

19

Investor Relations Office

Marcin Lauer

tel. + 48 32 774 27 06

Paweł Gaworzyński

tel. + 48 32 774 25 34

Magdalena Wilczek

tel. + 48 32 774 25 38

Mining

20

Lower average hard coal sales price, mainly declining price

of coal sludges sold intra-Group

Revenue drop partly compensated by increased sales

volume, along with the stronger growth of sales outside

TAURON Group versus the intra-Group sales

1.21

1.36

1.52 1.48 1.52 1.48

0,0

0,4

0,8

1,2

1,6

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Commercial coal production tons m

357.2 375.6

80.6 64.5 54.6

38.5

0

50

100

150

200

250

300

350

400

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

54,6

4,5 -19,1

0,2 -1,8 38,5

0

10

20

30

40

50

60

70

EBIT 2Q 2012 Wolumen sprzedażywęgla

Cena sprzedażywęgla

Jedn. koszt własnysprzedanego węgla

Pozostałeprzychody/koszty

EBIT 2Q 2013

EBIT bridge PLN m

Sales revenue Coal sales Coal sales Own per unit Other

volume price cost of coal sold revenue/

costs

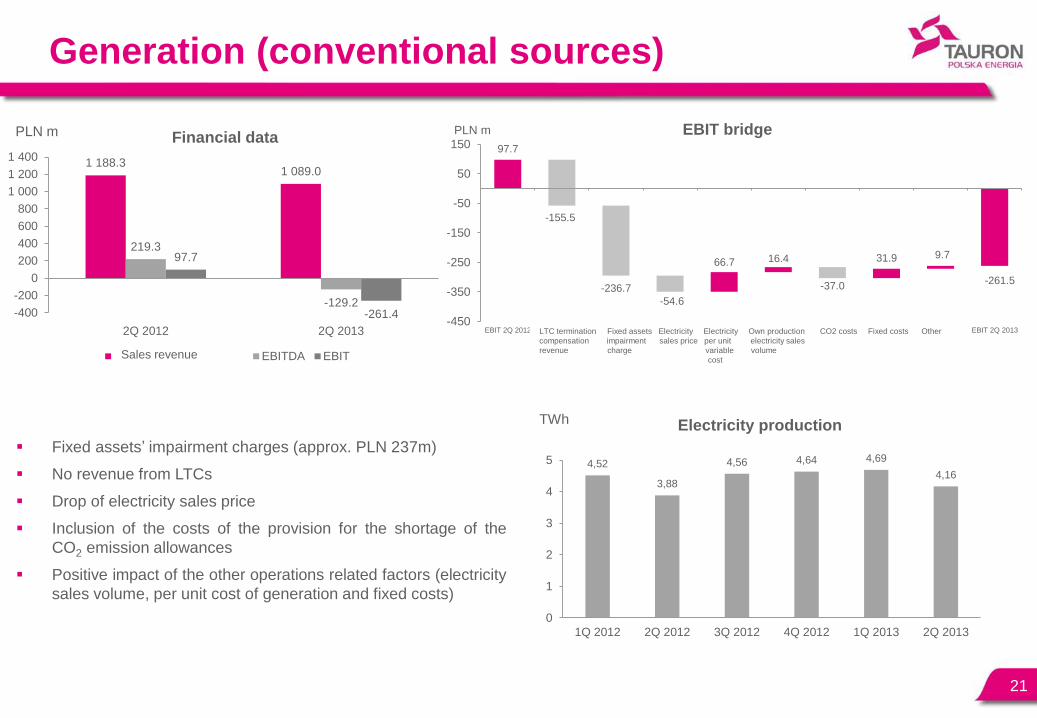

Generation (conventional sources)

21

Fixed assets‟ impairment charges (approx. PLN 237m)

No revenue from LTCs

Drop of electricity sales price

Inclusion of the costs of the provision for the shortage of the

CO2 emission allowances

Positive impact of the other operations related factors (electricity

sales volume, per unit cost of generation and fixed costs)

1 188.3 1 089.0

219.3

-129.2

97.7

-261.4 -400

-200

0

200

400

600

800

1 000

1 200

1 400

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

4,52

3,88

4,56 4,64 4,69

4,16

0

1

2

3

4

5

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Electricity production TWh

97.7

66.7 16.4 31.9 9.7

-155.5

-236.7

-54.6

-37.0 -261.5

-450

-350

-250

-150

-50

50

150

EBIT 2Q 2012 Przychody z tyt.rekompensaty

KDT

Odpisaktualizującyaktywa trwałe

Cena sprzedażyenergii

Jednostkowykoszt zmienny

energii el.

Wolumensprzed. energii z

własnej prod.

Koszty CO2 Koszty stałe Pozostałe EBIT 2Q 2013

EBIT bridge PLN m

Sales revenue

LTC termination Fixed assets Electricity Electricity Own production CO2 costs Fixed costs Other

compensation impairment sales price per unit electricity sales

revenue charge variable volume

cost

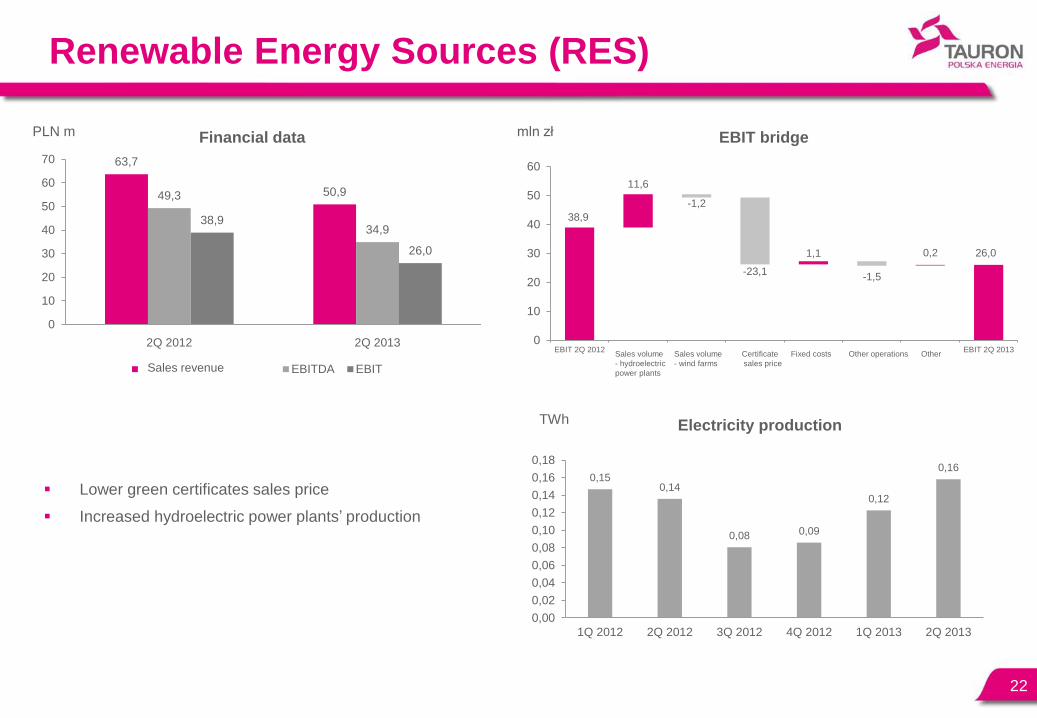

Renewable Energy Sources (RES)

22

Lower green certificates sales price

Increased hydroelectric power plants‟ production

63,7

50,9 49,3

34,9 38,9

26,0

0

10

20

30

40

50

60

70

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

0,15 0,14

0,08 0,09

0,12

0,16

0,00

0,02

0,04

0,06

0,08

0,10

0,12

0,14

0,16

0,18

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Electricity production TWh

38,9

11,6

-1,2

-23,1

1,1

-1,5

0,2 26,0

0

10

20

30

40

50

60

EBIT 2Q 2012 Wolumensprzedaży - el.

wodne

Wolumensprzedaży -el.wiatrowe

Cena sprzedażycertyfikatu

Koszty stałe Pozostaładziałalnośćoperacyjna

Pozostałe EBIT 2Q 2013

EBIT bridge mln zł

Sales revenue

Sales volume Sales volume Certificate Fixed costs Other operations Other

- hydroelectric - wind farms sales price

power plants

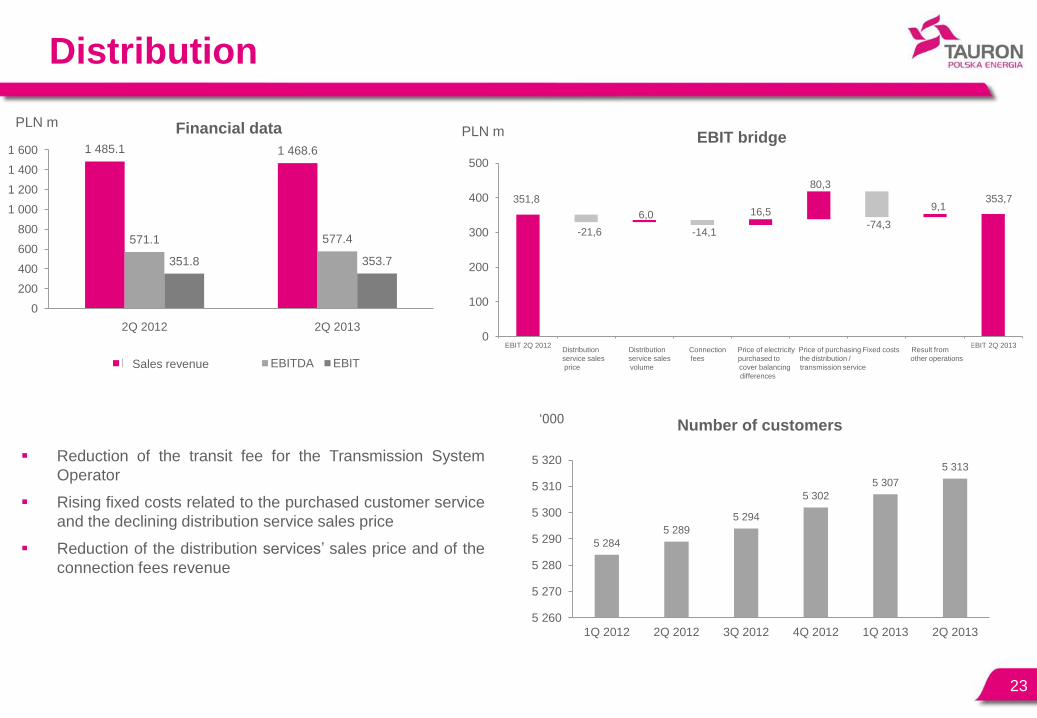

Distribution

23

Reduction of the transit fee for the Transmission System

Operator

Rising fixed costs related to the purchased customer service

and the declining distribution service sales price

Reduction of the distribution services‟ sales price and of the

connection fees revenue

1 485.1 1 468.6

571.1 577.4

351.8 353.7

0

200

400

600

800

1 000

1 200

1 400

1 600

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

351,8

-21,6

6,0

-14,1

16,5

80,3

-74,3

9,1 353,7

0

100

200

300

400

500

EBIT 2Q 2012 Cena sprzedażyuslugi

dystrybucyjnej

Wolumensprzedaży usługi

dystrybucyjnej

Opłatyprzyłączeniowe

Cena zakupuenergii na

pokrycie różnicybilansowej

Cena zakupuusługi

dystrybucyjnej /przesyłowej

Koszty stałe Wynik na pozost.działalności

EBIT 2Q 2013

EBIT bridge PLN m

5 284

5 289

5 294

5 302

5 307

5 313

5 260

5 270

5 280

5 290

5 300

5 310

5 320

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Number of customers „000

Sales revenue

Distribution Distribution Connection Price of electricity Price of purchasing Fixed costs Result from

service sales service sales fees purchased to the distribution / other operations

price volume cover balancing transmission service

differences

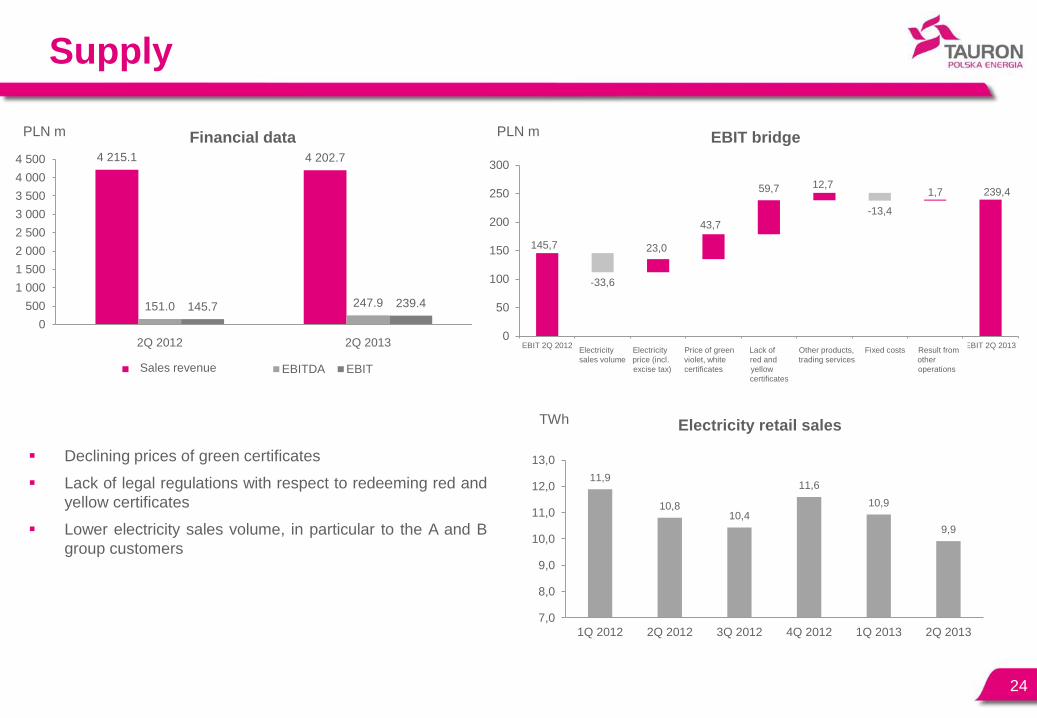

Supply

24

Declining prices of green certificates

Lack of legal regulations with respect to redeeming red and

yellow certificates

Lower electricity sales volume, in particular to the A and B

group customers

4 215.1 4 202.7

151.0 247.9 145.7 239.4

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

145,7

-33,6

23,0

43,7

59,7 12,7

-13,4

1,7 239,4

0

50

100

150

200

250

300

EBIT 2Q 2012 Wolumensprzedaży

energii

Cena energii (zakcyzą)

Cena PMzielonych,

fioletowych,białych

Brak PMczerwonych i

żółtych

Pozostałetowary, usługi

handlowe

Koszty stałe Wynik napozost.

działalności

EBIT 2Q 2013

EBIT bridge PLN m

11,9

10,8 10,4

11,6

10,9

9,9

7,0

8,0

9,0

10,0

11,0

12,0

13,0

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Electricity retail sales TWh

Sales revenue

Electricity Electricity Price of green Lack of Other products, Fixed costs Result from

sales volume price (incl. violet, white red and trading services other

excise tax) certificates yellow operations

certificates

Heat

25

Impairment charges reducing the value of the red and yelow

certificates‟ inventory to zero

Positive impact of the operations related factors (heat

production, electricity production, heat price, per unit

vraiable generation costs, fixed costs)

221.8 235.8

37.8 27.0

14.6 1.0

0

50

100

150

200

250

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

14.6

1.0 0.7

-32.9

3.6

4.0 3.0

3.2

4.5

-25

-20

-15

-10

-5

0

5

10

15

20

EBIT 2Q 2012 Odpisaktualizujący

certyfikaty

Wolumensprzedaży energii

Cena sprzedażyciepła

Cena sprzedażydmuchu

wielkopiecowegoi sprężonego

powietrza

Jednostkowekoszty

wytwarzania

Koszty stałe Pozostałe EBIT 2Q 2013

EBIT bridge PLN m

3,9

0,9

0,5

3,1

4,0

1,1

0

1

2

3

4

5

1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013

Segment’s heat production PJ

Sales revenue Certificates‟ Electricity Heat sales Blast furnace Per unit Fixed costs Other

impairment sales price and compressed generation

charge volume air sales price costs

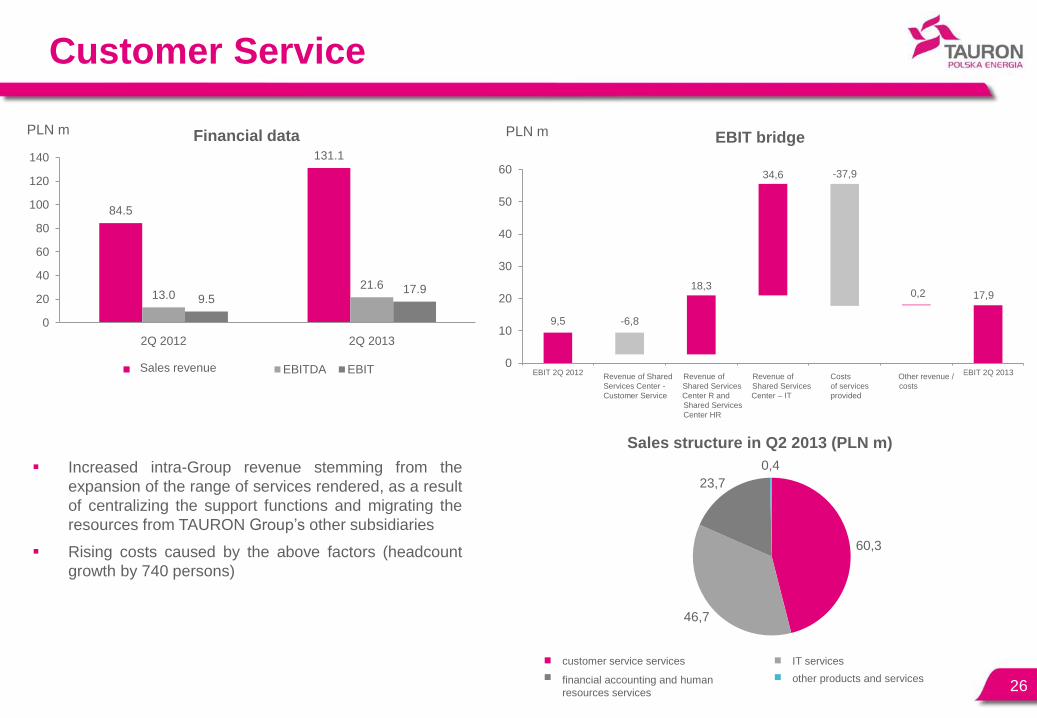

Customer Service

26

Increased intra-Group revenue stemming from the

expansion of the range of services rendered, as a result

of centralizing the support functions and migrating the

resources from TAURON Group‟s other subsidiaries

Rising costs caused by the above factors (headcount

growth by 740 persons)

84.5

131.1

13.0 21.6

9.5 17.9

0

20

40

60

80

100

120

140

2Q 2012 2Q 2013

Financial data

Przychody ze sprzedaży EBITDA EBIT

PLN m

60,3

46,7

23,7

0,4

Sales structure in Q2 2013 (PLN m)

usługi obsługi klienta usługi informatyczne

usługi finansowe księgowe i kadrowe pozostałe produkty i usługi

9,5 -6,8

18,3

34,6 -37,9

0,2 17,9

0

10

20

30

40

50

60

EBIT 2Q 2012 Przychody CUWOK

Przychody CUW R iCUW HR

Przychody CUW IT Kosztyświadczonych usług

Pozostałeprzychody/koszty

EBIT 2Q 2013

EBIT bridge PLN m

Sales revenue Revenue of Shared Revenue of Revenue of Costs Other revenue /

Services Center - Shared Services Shared Services of services costs

Customer Service Center R and Center – IT provided

Shared Services

Center HR

IT services

other products and services

customer service services

financial accounting and human

resources services

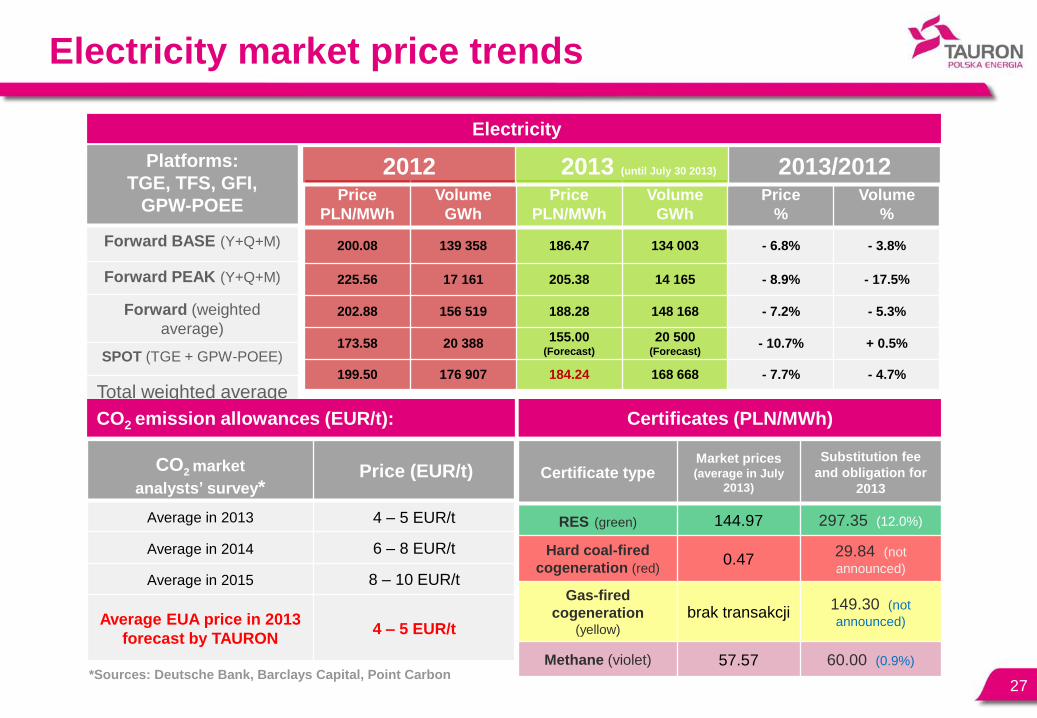

Electricity market price trends

27

Platforms:

TGE, TFS, GFI,

GPW-POEE

Forward BASE (Y+Q+M)

Forward PEAK (Y+Q+M)

Forward (weighted

average)

SPOT (TGE + GPW-POEE)

Total weighted average

Price

PLN/MWh

Volume

GWh

Price

PLN/MWh

Volume

GWh

Price

%

Volume

%

200.08 139 358 186.47 134 003 - 6.8% - 3.8%

225.56 17 161 205.38 14 165 - 8.9% - 17.5%

202.88 156 519 188.28 148 168 - 7.2% - 5.3%

173.58 20 388 155.00

(Forecast)

20 500 (Forecast)

- 10.7% + 0.5%

199.50 176 907 184.24 168 668 - 7.7% - 4.7%

Electricity

CO2 emission allowances (EUR/t): Certificates (PLN/MWh)

Certificate type Market prices (average in July

2013)

Substitution fee

and obligation for

2013

RES (green) 144.97 297.35 (12.0%)

Hard coal-fired

cogeneration (red) 0.47

29.84 (not

announced)

Gas-fired

cogeneration (yellow)

brak transakcji 149.30 (not

announced)

Methane (violet) 57.57 60.00 (0.9%)

2012 2013 (until July 30 2013) 2013/2012

CO2 market

analysts’ survey*

Price (EUR/t)

Average in 2013 4 – 5 EUR/t

Average in 2014 6 – 8 EUR/t

Average in 2015 8 – 10 EUR/t

Average EUA price in 2013

forecast by TAURON 4 – 5 EUR/t

*Sources: Deutsche Bank, Barclays Capital, Point Carbon

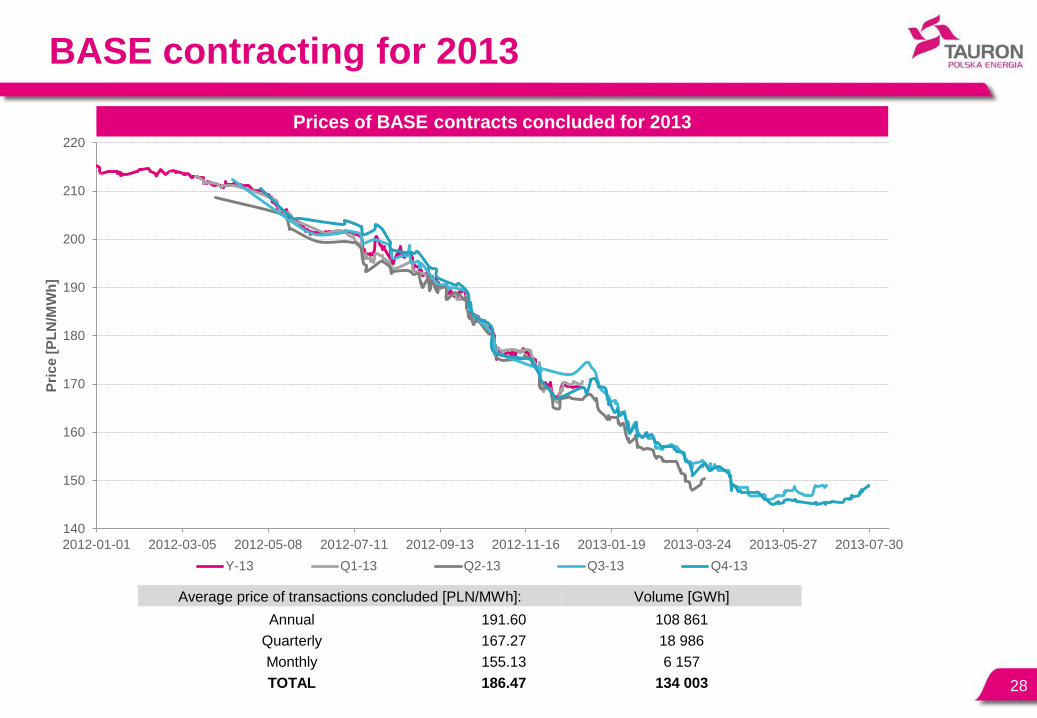

BASE contracting for 2013

28

140

150

160

170

180

190

200

210

220

2012-01-01 2012-03-05 2012-05-08 2012-07-11 2012-09-13 2012-11-16 2013-01-19 2013-03-24 2013-05-27 2013-07-30

Pri

ce

[P

LN

/MW

h]

Y-13 Q1-13 Q2-13 Q3-13 Q4-13

Prices of BASE contracts concluded for 2013

Average price of transactions concluded [PLN/MWh]: Volume [GWh]

Annual 191.60 108 861

Quarterly 167.27 18 986

Monthly 155.13 6 157

TOTAL 186.47 134 003

165

175

185

195

205

215

225

235

245

255

2012-01-01 2012-02-28 2012-04-26 2012-06-23 2012-08-20 2012-10-17 2012-12-14 2013-02-10 2013-04-09 2013-06-06 2013-08-03

Pri

ce

[P

LN

/MW

h]

Y-13 Q1-13 Q2-13 Q3-13 Q4-13

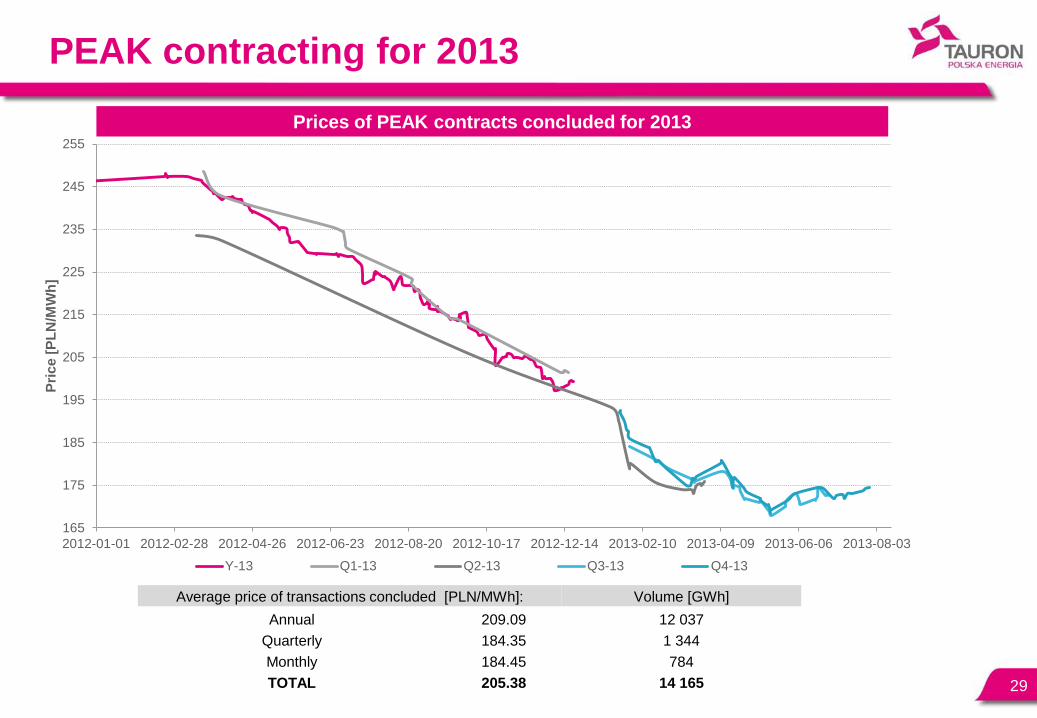

PEAK contracting for 2013

29

Prices of PEAK contracts concluded for 2013

Average price of transactions concluded [PLN/MWh]: Volume [GWh]

Annual 209.09 12 037

Quarterly 184.35 1 344

Monthly 184.45 784

TOTAL 205.38 14 165

Average price of transactions concluded [PLN/MWh]: Volume [GWh]

Annual 164.74 88 029

Quarterly 150.30 1 399

Monthly

TOTAL 164.52 89 428

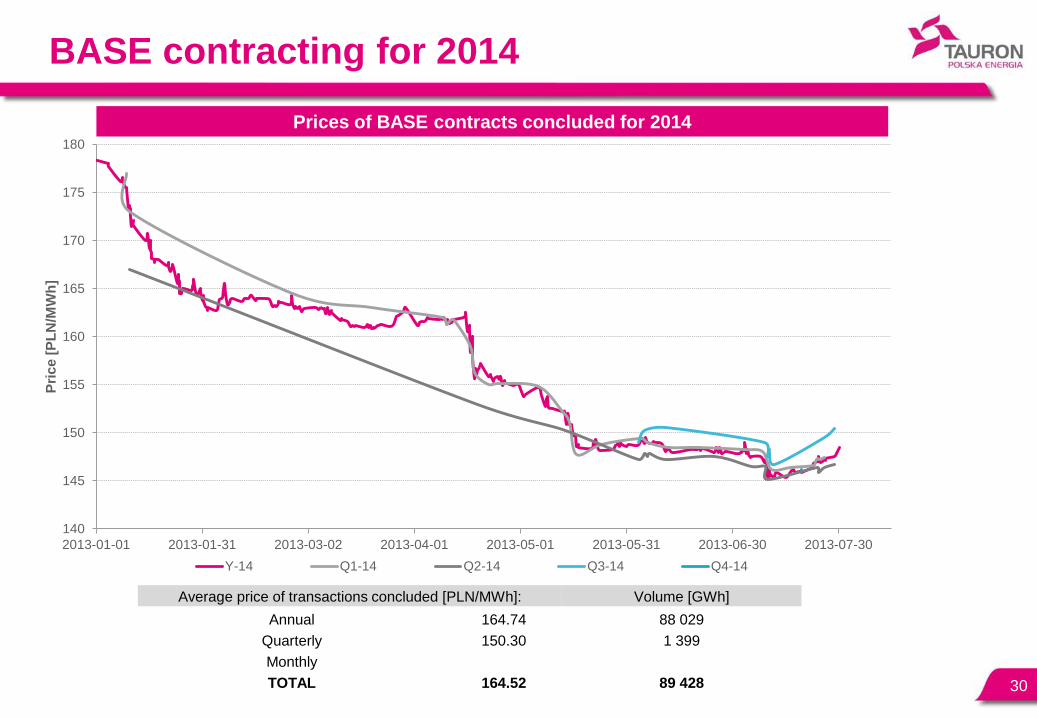

BASE contracting for 2014

30

140

145

150

155

160

165

170

175

180

2013-01-01 2013-01-31 2013-03-02 2013-04-01 2013-05-01 2013-05-31 2013-06-30 2013-07-30

Pri

ce

[P

LN

/MW

h]

Y-14 Q1-14 Q2-14 Q3-14 Q4-14

Prices of BASE contracts concluded for 2014

Average price of transactions concluded [PLN/MWh]: Volume [GWh]

Annual 176.52 5 186

Quarterly

Monthly

TOTAL 176.52 5 186

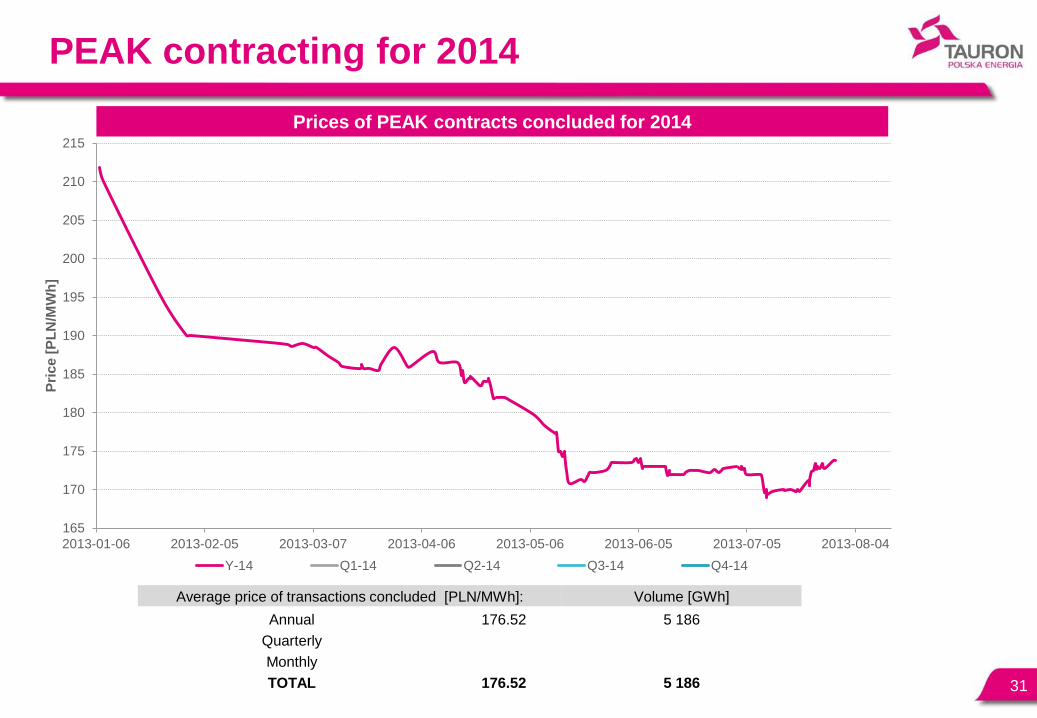

PEAK contracting for 2014

31

165

170

175

180

185

190

195

200

205

210

215

2013-01-06 2013-02-05 2013-03-07 2013-04-06 2013-05-06 2013-06-05 2013-07-05 2013-08-04

Pri

ce

[P

LN

/MW

h]

Y-14 Q1-14 Q2-14 Q3-14 Q4-14

Prices of PEAK contracts concluded for 2014

Average price of transactions concluded [PLN/MWh]: Volume [GWh]

Annual 162.52 10 670

Quarterly

Monthly

TOTAL 162.52 10 670

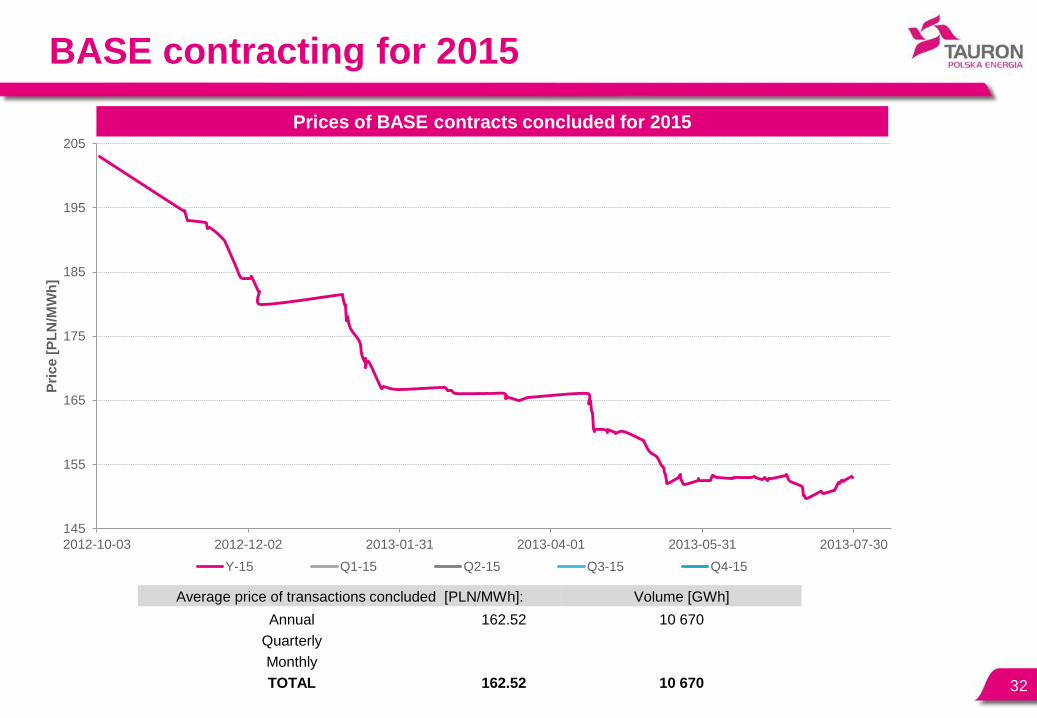

BASE contracting for 2015

32

145

155

165

175

185

195

205

2012-10-03 2012-12-02 2013-01-31 2013-04-01 2013-05-31 2013-07-30

Pri

ce

[P

LN

/MW

h]

Y-15 Q1-15 Q2-15 Q3-15 Q4-15

Prices of BASE contracts concluded for 2015