Embed Size (px)

Citation preview

Tax Effi cient Review

EditorMartin ChurchillBSc (Econ) FCA

www.taxeffi cientreview.com

September 2016

Venture Capital Trust

Early Stage Generalist VCT with track record

Octopus Titan VCT

This communication is provided for informational purposes only. This information does not constitute advice on investments within the meaning of Article 53 of the Financial Services and Markets Act (Regulated Activities) Order 2001. Should investment advice be required this should be sought from a FCA authorised person

Reprinted for the use of Octopus Investments Limited

Tax Efficient Review reviews are completely independent and providers do not pay for inclusion in Tax Efficient Review

Providers who wish to distribute their review as part of their marketing can do so for a standard fee

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 201622

Review of Early Stage Generalist VCT with track record

Tax Efficient Review is published by Tax Efficient Review Ltd

35 The ParkLondon

NW11 7ST Tel: +44 (0)20 8458 9003

VCT RISK WARNINGS

RISK WARNINGS AND DISCLAIMERS

GENERAL RISK WARNINGS

Fluctuations in Value of-Investments

Suitability

Past performance

Legislation

Taxation

ADDITIONAL RISK WARNINGS

This communication is provided for informational purposes only. This informa-tion does not constitute advice on investments within the meaning of Article 53 of the Financial Services and Markets Act (Regulated Activities) Order 2001. Should in-vestment advice be required this should be sought from a FCA authorised person

Tax Effi cient Review’ (the “Review”) is issued by Tax Effi cient Review Limited (“TER”). The Review is provided for information purposes only and should not be construed as an off er of, or as solicitation of an off er to purchase, investments or investment advisory services. The investments or investment services provided by TER may not be suitable for all readers. If you have any doubts as to suitability, you should seek advice from TER. No investment or investment service mentioned in the Review amounts to a personal recommendation to any one investor.

Your attention is drawn to the following risk warnings which identify some of the risks associated with the investments which are mentioned in the Review:

The value of investments and the income from them can go down as well as up and you may not get back the amount invested.

The investments may not be suitable for all investors and you should only invest if you understand the nature of and risks inherent in such investments and, if in doubt, you should seek professional advice before eff ecting any such investment.

Past performance is not a guide to future performance.

Changes in legislation may adversely aff ect the value of the investments.

The levels and the bases of the reliefs from taxation may change in the future. You should seek your own professional advice on the taxation consequences of any investment.

Venture Capital Trusts1. An investment in a VCT carries a higher risk than many other forms of investment.2. A VCT’s shares, although listed, are likely to be diffi cult to realise.3. You should regard an investment in a VCT as a long term investment, particularly as regards a

VCT’s investment objectives and policy and the fi ve year period for which shareholders must hold their ordinary shares to retain their initial income tax reliefs.

4. The investments made by VCTs will normally be in companies whose securities are not publicly traded or freely marketable and may therefore be diffi cult to realise and investments in such companies are substantially riskier than those in larger companies.

5. If a VCT loses its Inland Revenue approval tax reliefs previously obtained may be lost. 6. No investment can made by the VCT in a company whose fi rst commercial sale was more than

7 years prior to date of investment, except where previous State Aid Risk Finance was received by the company within 7 years (10 years for a ‘knowledge intensive’ company) or where a turnover test is satisfi ed; and

7. No funds received from an investment by the VCT into a company can be used to acquire another existing business or trade.

Copyright © 2016 Tax Efficient Review Ltd. All Rights Reserved. The information, data and opinions (“Information”) expressed and con-tained herein: (1) are proprietary to Tax Efficient Review Ltd and/or its content providers and are not intended to represent investment advice or recommendation to buy or sell any security; (2) may not normally be copied or distributed without express license to do so; and (3) are not warranted to be accurate, complete or timely. Tax Efficient Review Ltd reserves its rights to charge for access to these reports. Tax Efficient Review Ltd is not responsible for any damages or losses arising from any use of the reports or the Information contained therein. The copyright in this publication belongs to Martin Churchill, all rights reserved, and for a fee the author has granted Octopus Investments Limited an unlimited non-exclusive and royalty free licence to use the publication

33 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

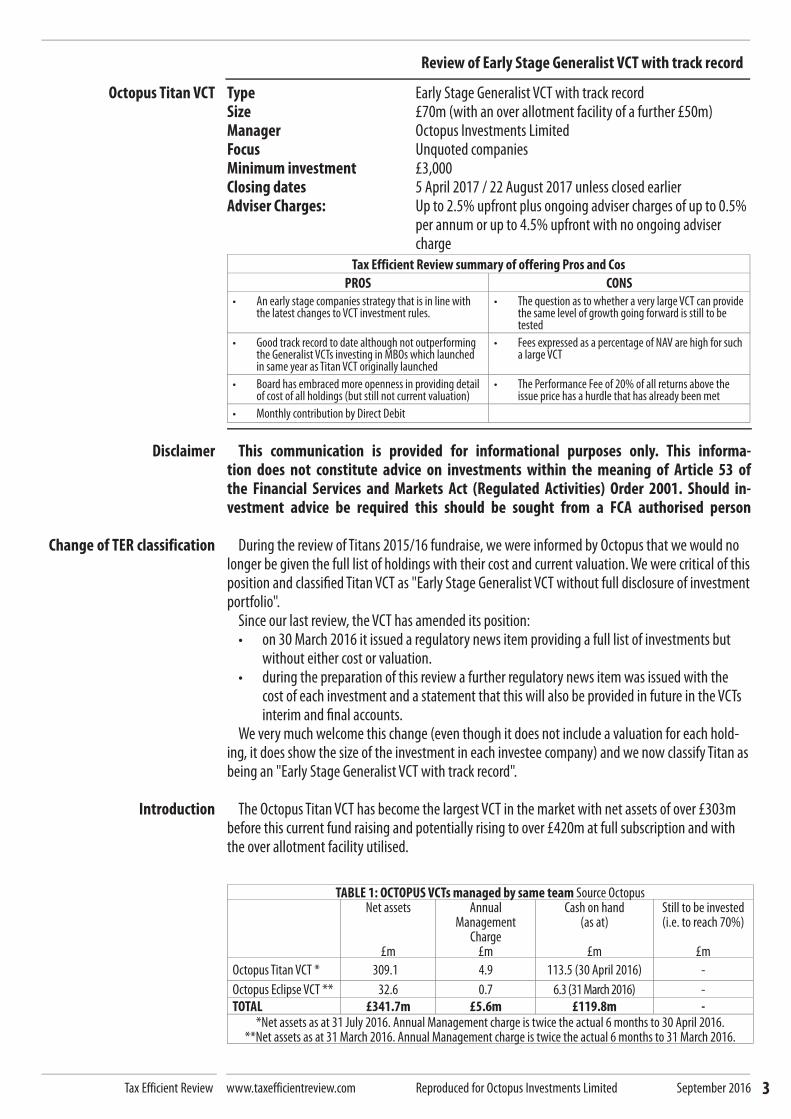

Octopus Titan VCT

Disclaimer

Change of TER classification

Introduction

Type Early Stage Generalist VCT with track recordSize £70m (with an over allotment facility of a further £50m)Manager Octopus Investments LimitedFocus Unquoted companiesMinimum investment £3,000Closing dates 5 April 2017 / 22 August 2017 unless closed earlierAdviser Charges: Up to 2.5% upfront plus ongoing adviser charges of up to 0.5%

per annum or up to 4.5% upfront with no ongoing adviser charge

Tax Efficient Review summary of offering Pros and Cos

PROS CONS

• An early stage companies strategy that is in line with the latest changes to VCT investment rules.

• The question as to whether a very large VCT can provide the same level of growth going forward is still to be tested

• Good track record to date although not outperforming the Generalist VCTs investing in MBOs which launched in same year as Titan VCT originally launched

• Fees expressed as a percentage of NAV are high for such a large VCT

• Board has embraced more openness in providing detail of cost of all holdings (but still not current valuation)

• The Performance Fee of 20% of all returns above the issue price has a hurdle that has already been met

• Monthly contribution by Direct Debit

This communication is provided for informational purposes only. This informa-tion does not constitute advice on investments within the meaning of Article 53 of the Financial Services and Markets Act (Regulated Activities) Order 2001. Should in-vestment advice be required this should be sought from a FCA authorised person

During the review of Titans 2015/16 fundraise, we were informed by Octopus that we would no longer be given the full list of holdings with their cost and current valuation. We were critical of this position and classifi ed Titan VCT as "Early Stage Generalist VCT without full disclosure of investment portfolio".

Since our last review, the VCT has amended its position:• on 30 March 2016 it issued a regulatory news item providing a full list of investments but

without either cost or valuation.• during the preparation of this review a further regulatory news item was issued with the

cost of each investment and a statement that this will also be provided in future in the VCTs interim and fi nal accounts.

We very much welcome this change (even though it does not include a valuation for each hold-ing, it does show the size of the investment in each investee company) and we now classify Titan as being an "Early Stage Generalist VCT with track record".

The Octopus Titan VCT has become the largest VCT in the market with net assets of over £303m before this current fund raising and potentially rising to over £420m at full subscription and with the over allotment facility utilised.

TABLE 1: OCTOPUS VCTs managed by same team Source OctopusNet assets

£m

Annual Management

Charge£m

Cash on hand (as at)

£m

Still to be invested (i.e. to reach 70%)

£m

Octopus Titan VCT * 309.1 4.9 113.5 (30 April 2016) -

Octopus Eclipse VCT ** 32.6 0.7 6.3 (31 March 2016) -

TOTAL £341.7m £5.6m £119.8m -*Net assets as at 31 July 2016. Annual Management charge is twice the actual 6 months to 30 April 2016.

**Net assets as at 31 March 2016. Annual Management charge is twice the actual 6 months to 31 March 2016.

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 201644

Review of Early Stage Generalist VCT with track record

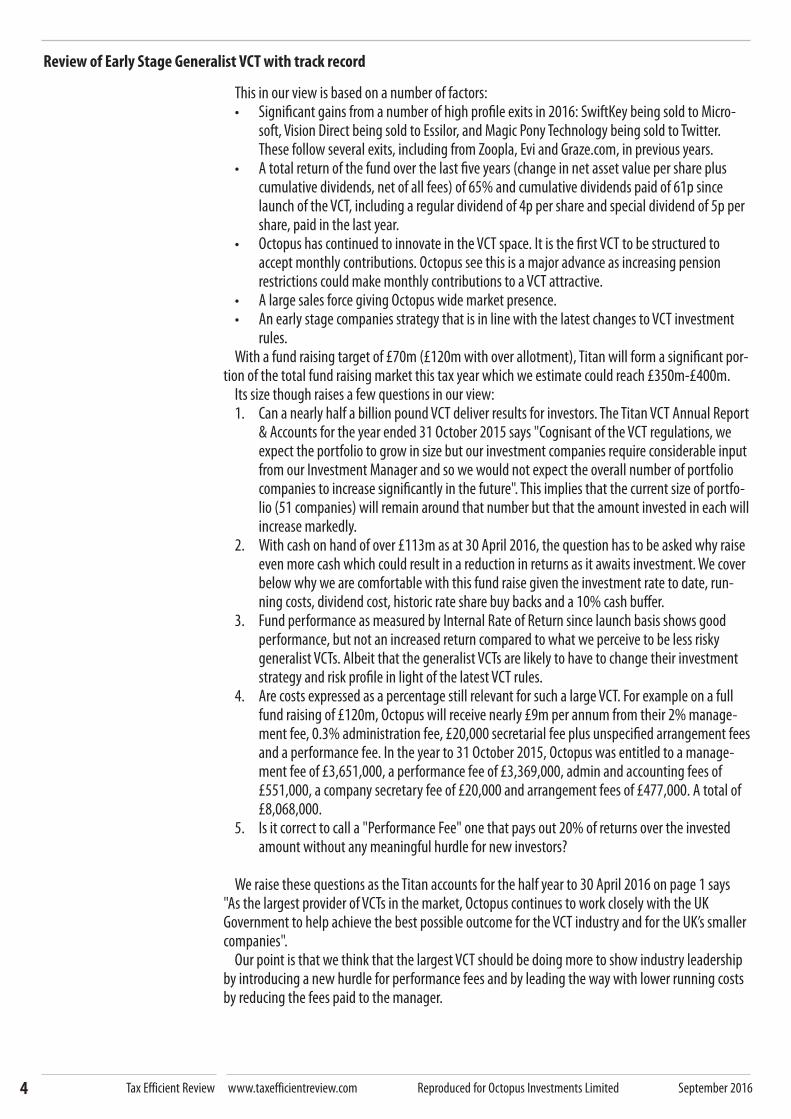

This in our view is based on a number of factors:• Signifi cant gains from a number of high profi le exits in 2016: SwiftKey being sold to Micro-

soft, Vision Direct being sold to Essilor, and Magic Pony Technology being sold to Twitter. These follow several exits, including from Zoopla, Evi and Graze.com, in previous years.

• A total return of the fund over the last fi ve years (change in net asset value per share plus cumulative dividends, net of all fees) of 65% and cumulative dividends paid of 61p since launch of the VCT, including a regular dividend of 4p per share and special dividend of 5p per share, paid in the last year.

• Octopus has continued to innovate in the VCT space. It is the fi rst VCT to be structured to accept monthly contributions. Octopus see this is a major advance as increasing pension restrictions could make monthly contributions to a VCT attractive.

• A large sales force giving Octopus wide market presence.• An early stage companies strategy that is in line with the latest changes to VCT investment

rules.With a fund raising target of £70m (£120m with over allotment), Titan will form a signifi cant por-

tion of the total fund raising market this tax year which we estimate could reach £350m-£400m.Its size though raises a few questions in our view:1. Can a nearly half a billion pound VCT deliver results for investors. The Titan VCT Annual Report

& Accounts for the year ended 31 October 2015 says "Cognisant of the VCT regulations, we expect the portfolio to grow in size but our investment companies require considerable input from our Investment Manager and so we would not expect the overall number of portfolio companies to increase signifi cantly in the future". This implies that the current size of portfo-lio (51 companies) will remain around that number but that the amount invested in each will increase markedly.

2. With cash on hand of over £113m as at 30 April 2016, the question has to be asked why raise even more cash which could result in a reduction in returns as it awaits investment. We cover below why we are comfortable with this fund raise given the investment rate to date, run-ning costs, dividend cost, historic rate share buy backs and a 10% cash buff er.

3. Fund performance as measured by Internal Rate of Return since launch basis shows good performance, but not an increased return compared to what we perceive to be less risky generalist VCTs. Albeit that the generalist VCTs are likely to have to change their investment strategy and risk profi le in light of the latest VCT rules.

4. Are costs expressed as a percentage still relevant for such a large VCT. For example on a full fund raising of £120m, Octopus will receive nearly £9m per annum from their 2% manage-ment fee, 0.3% administration fee, £20,000 secretarial fee plus unspecifi ed arrangement fees and a performance fee. In the year to 31 October 2015, Octopus was entitled to a manage-ment fee of £3,651,000, a performance fee of £3,369,000, admin and accounting fees of £551,000, a company secretary fee of £20,000 and arrangement fees of £477,000. A total of £8,068,000.

5. Is it correct to call a "Performance Fee" one that pays out 20% of returns over the invested amount without any meaningful hurdle for new investors?

We raise these questions as the Titan accounts for the half year to 30 April 2016 on page 1 says "As the largest provider of VCTs in the market, Octopus continues to work closely with the UK Government to help achieve the best possible outcome for the VCT industry and for the UK’s smaller companies".

Our point is that we think that the largest VCT should be doing more to show industry leadership by introducing a new hurdle for performance fees and by leading the way with lower running costs by reducing the fees paid to the manager.

55 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

Major changes since last review

Summary

Major changes since our last review in Issue 227 in September 2015 are:• Three exits as per above• Payment of further dividends – regular and special• Opening of a US Offi ce• Titan is nearing the threshold for AIFMD (Alternative Investment Fund Managers Directive

2011/61/EU law on the fi nancial regulation of hedge funds, private equity, real estate funds, and other "Alternative Investment Fund Managers") so the manager may at some stage have to address the stricter rules

• Changes to the investment strategy driven by, the prospectus says, the continuing evolution of early stage investment environment and recent changes in VCT legislation, the Company feels it is appropriate to refresh the investment policy- changes to the terminology it applies to the investment sectors. Instead of defi ning separately: Technology, Media, Telecoms, Consumer Lifestyle and Well-being, and Environ-ment, the Company has simplifi ed this to "a range of technology sectors" which it believes is simpler to communicate and more refl ective of the way the Company thinks about its investments, both historic and future. The underlying portfolio has not changed and the type of companies the Company will invest in will not change. - The Company has also made changes to the types of non-Qualifying Investments it will make to align with recent VCT legislative changes. The Company has also increased the top range of the % of Qualifying Investments that it will aim to hold from 85% to 90%. This, again, is refl ective of changes in legislation restricting non-Qualifying Investments, meaning that the balance may shift slightly towards holding more Qualifying Investments.- The most signifi cant change is the removal of the passage restricting the use of borrowing to make investments. The Company now has the power in its articles of association to borrow up to 50% of its net assets. The prospectus says that the Company has no intention to make use of borrowing for this purpose in the immediate future; however it would like to align the investment policy with the Articles and remove any constraints placed upon it by this clause to provide more fl exibility into the future should any such need or desire arise.

• A reduction in the minimum investment amount that an investor can invest from £5,000 to £3,000

• For the fi rst time, investors can now purchase the Company's shares by monthly contribution. Investors simply need to complete the ‘direct debit’ section in the application form. Octopus will collect this amount from an investors bank account via direct debit on or around day 14 of every month. At roughly three-monthly intervals, this money will be used to purchase New Shares. Share and tax certifi cates will be sent shortly after the regular share allotment dates which are currently scheduled for: December, March, June and August

This is the tenth year that Octopus has off ered a fund raising into Octopus Titan VCT, or at least one of the fi ve Titan VCT funds that merged to form the single Titan VCT in November 2014. In recognition that it off ers a unique early stage high risk / potential high return approach to investing, it remains in a sub-category of Generalist called "Early Stage Generalist VCT with track record ". At present, the Octopus Titan VCT is the only fund in this group, which Octopus believes is an advan-tage in that it is fully aligned with both the UK Government’s and The European Union's intentions for the VCT industry – to support young UK businesses and help kick-start the economy.

This new share off er provides investors with an opportunity to invest in what is now the biggest VCT in the UK with assets of £303m as at 31 August 2016 and nearly twice the size of the second largest (Baronsmead Venture Trust at £174m at 31 March 2016). Octopus Titan VCT has a portfolio which includes investee companies at varying stages of maturity which should help provide diver-sity. Octopus say that there is continued evidence that many of the investee companies are making demonstrable progress, shown by the increase in Total Return (NAV plus cumulative dividends paid, currently 154.7p per share) and most tangibly by the cumulative dividends paid to date by Octopus Titan VCT (formerly Octopus Titan VCT 2), which now totals 61p per share. However, as we explore

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 201666

Review of Early Stage Generalist VCT with track record

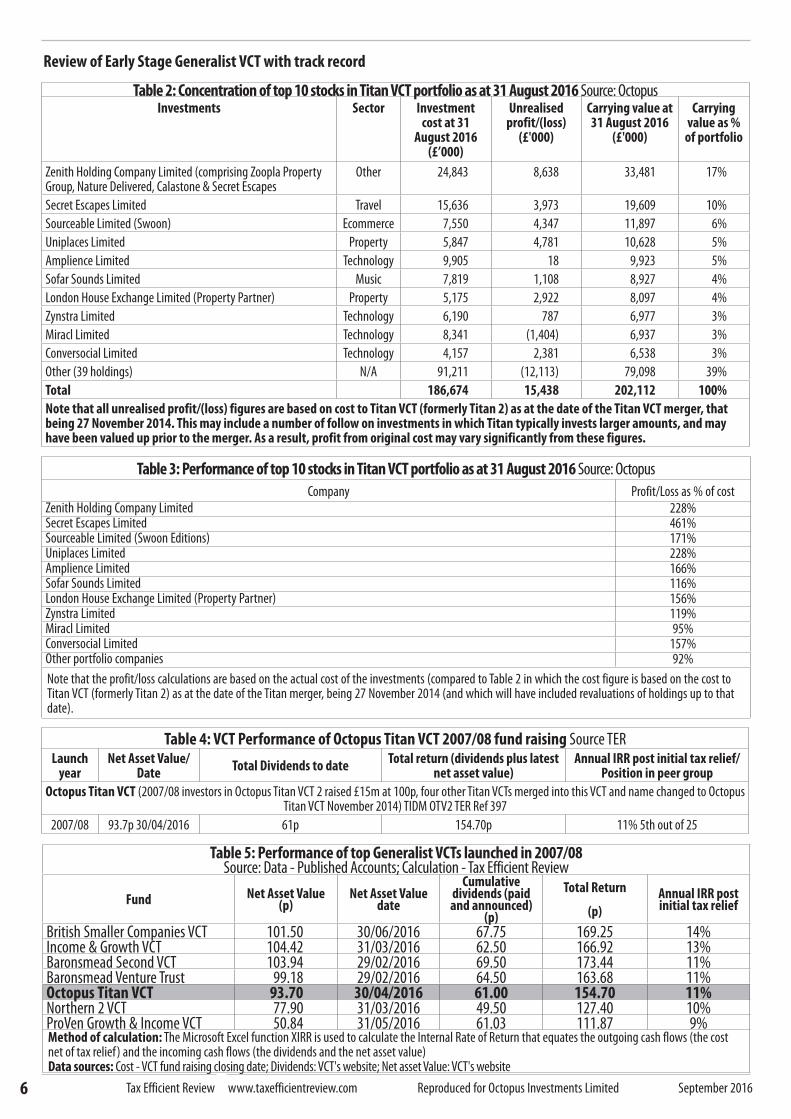

Table 2: Concentration of top 10 stocks in Titan VCT portfolio as at 31 August 2016 Source: OctopusInvestments Sector Investment

cost at 31 August 2016

(£’000)

Unrealised profit/(loss)

(£'000)

Carrying value at 31 August 2016

(£'000)

Carrying value as %

of portfolio

Zenith Holding Company Limited (comprising Zoopla Property Group, Nature Delivered, Calastone & Secret Escapes

Other 24,843 8,638 33,481 17%

Secret Escapes Limited Travel 15,636 3,973 19,609 10%

Sourceable Limited (Swoon) Ecommerce 7,550 4,347 11,897 6%

Uniplaces Limited Property 5,847 4,781 10,628 5%

Amplience Limited Technology 9,905 18 9,923 5%

Sofar Sounds Limited Music 7,819 1,108 8,927 4%

London House Exchange Limited (Property Partner) Property 5,175 2,922 8,097 4%

Zynstra Limited Technology 6,190 787 6,977 3%

Miracl Limited Technology 8,341 (1,404) 6,937 3%

Conversocial Limited Technology 4,157 2,381 6,538 3%

Other (39 holdings) N/A 91,211 (12,113) 79,098 39%

Total 186,674 15,438 202,112 100%

Note that all unrealised profit/(loss) figures are based on cost to Titan VCT (formerly Titan 2) as at the date of the Titan VCT merger, that being 27 November 2014. This may include a number of follow on investments in which Titan typically invests larger amounts, and may have been valued up prior to the merger. As a result, profit from original cost may vary significantly from these figures.

Table 4: VCT Performance of Octopus Titan VCT 2007/08 fund raising Source TERLaunch

yearNet Asset Value/

DateTotal Dividends to date

Total return (dividends plus latest net asset value)

Annual IRR post initial tax relief/Position in peer group

Octopus Titan VCT (2007/08 investors in Octopus Titan VCT 2 raised £15m at 100p, four other Titan VCTs merged into this VCT and name changed to Octopus Titan VCT November 2014) TIDM OTV2 TER Ref 397

2007/08 93.7p 30/04/2016 61p 154.70p 11% 5th out of 25

Table 3: Performance of top 10 stocks in Titan VCT portfolio as at 31 August 2016 Source: Octopus

Company Profit/Loss as % of cost

Zenith Holding Company Limited 228%Secret Escapes Limited 461%Sourceable Limited (Swoon Editions) 171%Uniplaces Limited 228%Amplience Limited 166%Sofar Sounds Limited 116%London House Exchange Limited (Property Partner) 156%Zynstra Limited 119%Miracl Limited 95%Conversocial Limited 157%Other portfolio companies 92%

Note that the profit/loss calculations are based on the actual cost of the investments (compared to Table 2 in which the cost figure is based on the cost to Titan VCT (formerly Titan 2) as at the date of the Titan merger, being 27 November 2014 (and which will have included revaluations of holdings up to that date).

Table 5: Performance of top Generalist VCTs launched in 2007/08 Source: Data - Published Accounts; Calculation - Tax Efficient Review

Fund Net Asset Value(p)

Net Asset Value date

Cumulative dividends (paid and announced)

(p)

Total Return

(p)

Annual IRR post initial tax relief

British Smaller Companies VCT 101.50 30/06/2016 67.75 169.25 14%Income & Growth VCT 104.42 31/03/2016 62.50 166.92 13%Baronsmead Second VCT 103.94 29/02/2016 69.50 173.44 11%Baronsmead Venture Trust 99.18 29/02/2016 64.50 163.68 11%Octopus Titan VCT 93.70 30/04/2016 61.00 154.70 11%Northern 2 VCT 77.90 31/03/2016 49.50 127.40 10%ProVen Growth & Income VCT 50.84 31/05/2016 61.03 111.87 9%Method of calculation: The Microsoft Excel function XIRR is used to calculate the Internal Rate of Return that equates the outgoing cash flows (the cost net of tax relief) and the incoming cash flows (the dividends and the net asset value)Data sources: Cost - VCT fund raising closing date; Dividends: VCT's website; Net asset Value: VCT's website

77 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

Strategy

later in this review, this does not put them in top position in Generalist VCT returns in their fi rst year of launch.

The key question for investors of course is given the continued expansion of the portfolio, funded both by further very large fundraises such as this current off er and realisations from the older com-panies in the portfolio, can the VCT provide strong performance going forward or will its giant size prove to be a limiting factor.

This fundraise aims to ensure the VCT is able to continue increasing exposure to those portfolio companies that are developing "well" (as categorised by the investment team) and also selectively making investments into new companies where the investment team believes there is an exciting opportunity. This follows the team’s investment model of continuing to fund the ‘winners’ within their portfolio whilst minimising additional funding to the poorer performing companies.

Octopus claim that this should mean that investors are getting in at a stage when the fund is a) de-risked to the extent that it is already partially invested, b) has built a diverse portfolio operating in a variety of sectors, and c) has already refl ected earlier losses in the NAV of the fund. Octopus Titan VCT is a generalist fund managed by the Ventures Team within Octopus. The team

has been together for over a decade, has signifi cant investment and business experience between them and includes a number of former entrepreneurs. The team is bolstered by their Venture Part-ners (including those formerly known as Entrepreneurs in Residence and Strategic Advisers).

The Ventures Team invests into early stage unquoted companies, with follow on investments providing development and growth capital. The team looks to invest in “high growth businesses” that can “scale explosively to create, transform or dominate an industry”. They will not invest into a company unless they think the company has the potential to deliver a 5-10X return from the initial investment. The fund is targeting an annual regular dividend of 5p per share with the potential for special dividends to be paid in addition to this, typically following a signifi cant realisation from one or more of the underlying portfolio companies.

In our view, there are two aspects of Octopus Titan VCTs off ering that diff erentiate it from the rest of the generalist VCTs currently available:

• The “Octopus Venture Partners” approach to investing and • The focus on early stage, expansion and development investments.The ‘Octopus Venture Partners’ are an exclusive group of around 90 leading entrepreneurs and

business angels who can introduce investment opportunities, assist with due diligence, and off er support to and co-investment into the companies in Octopus Titan VCT. The members pay an annual fee of £3,000 to be shown investment opportunities in which they can co-invest if they so wish. The Octopus Venture Partners are able to invest on the same terms as Octopus Titan VCT and Octopus will not typically invest if members of the Venture Partners are not also prepared to invest their own money alongside the VCT. This provides added comfort that each investment opportunity is strong enough on its own merit for trusted industry experts to “put their money where their mouth is.”

Octopus has commented as follows about its relationship with the Octopus Venture Partners and the additional resource that this provides them.

“Often early-stage companies need more than just access to funding. After we’ve made an investment, we help by:Off ering a range of comprehensive services – such as a network of professional contacts, as-sisting with key staff recruitment as well as any necessary consulting, coaching and mentoring support.Providing access to the Octopus Venture Partners – a valuable resource of entrepreneurs and business experts.Usually one of the Ventures team sits on the Board of the companies Octopus Titan VCT invests in. This allows them to play a prominent role in the company’s ongoing development.The Octopus Venture Partners are a network of around 90 entrepreneurs and business people who typically have the opportunity to invest alongside Octopus Titan VCT. Some even work

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 201688

Review of Early Stage Generalist VCT with track record

with the Ventures team at Octopus to help provide hands-on support, practical advice and professional connections to the companies we invest in. Our Venture Partners include past and present senior management from companies such as Google, Innocent Drinks, Betfair, Orange, PayPal UK, Virgin, Vodafone, IBM, and Paddy Power.”

In summary, the Octopus Venture Partners contribute to the investment process in a number of ways:

• Some Venture Partners bring high quality deal fl ow to Octopus, typically on a proprietary basis.

• Discrete Venture Partners may help in the due diligence carried out by the Ventures Team. Octopus tells us that the Venture Partners have deep industry knowledge and expertise having developed their own businesses in their industry sectors, which enables the Fund Managers, who may not have the same depth of specialised industry experience, to leverage this knowledge. Venture Partners who have experience in the relevant sector, can be invited in to help with due diligence. This enables the Octopus team to consider a far wider range of sectors for the portfolios.

• Prior to Octopus investing into a company, the Venture Partners usually endorse the invest-ment decision made by the Octopus team in an investment process which may include the potential investee company presenting directly to a group of the Venture Partners, followed by the Venture Partners investing, typically 5-20% of the total Octopus investment.

• Post-investment, Octopus works actively with its portfolio companies in order to maximise the value from each investment. The Venture Partners can provide a valuable resource in this process. A Venture Partner may in some cases sit on the Board of an investee company or act as an observer/monitor for Octopus within that company alongside a member of the invest-ment team.

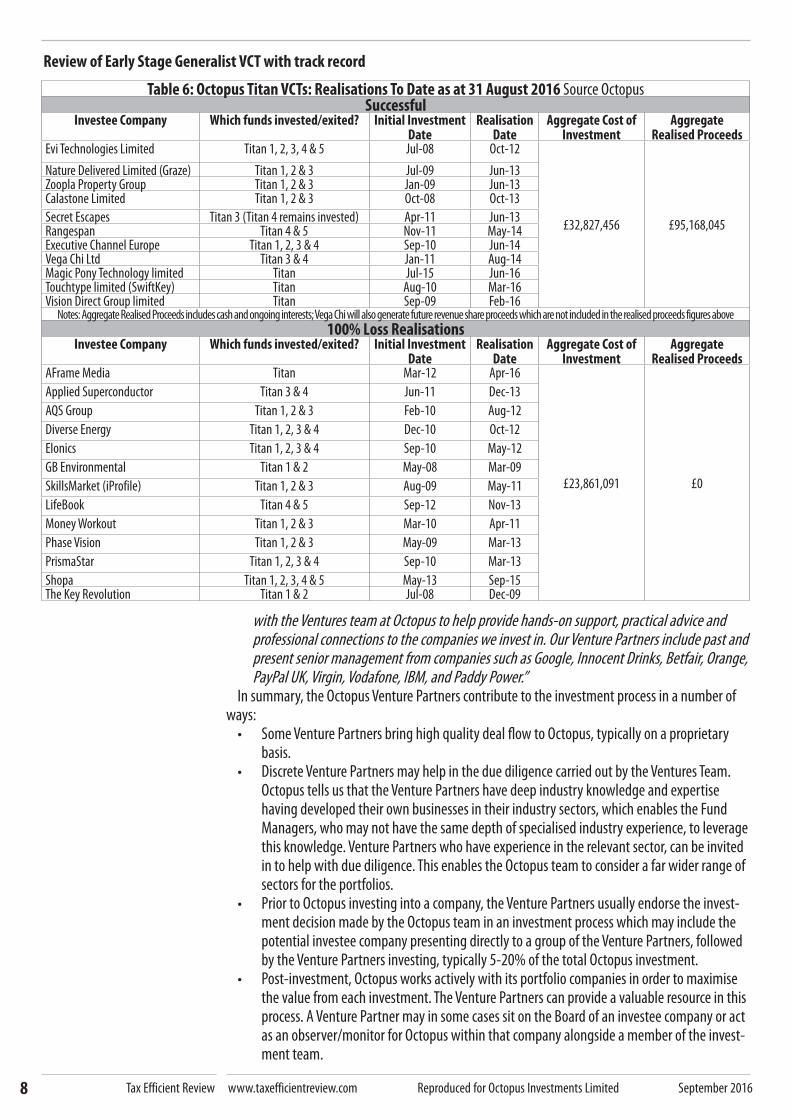

Table 6: Octopus Titan VCTs: Realisations To Date as at 31 August 2016 Source Octopus Successful

Investee Company Which funds invested/exited? Initial Investment Date

Realisation Date

Aggregate Cost of Investment

Aggregate Realised Proceeds

Evi Technologies Limited Titan 1, 2, 3, 4 & 5 Jul-08 Oct-12

£32,827,456 £95,168,045

Nature Delivered Limited (Graze) Titan 1, 2 & 3 Jul-09 Jun-13Zoopla Property Group Titan 1, 2 & 3 Jan-09 Jun-13Calastone Limited Titan 1, 2 & 3 Oct-08 Oct-13

Secret Escapes Titan 3 (Titan 4 remains invested) Apr-11 Jun-13Rangespan Titan 4 & 5 Nov-11 May-14Executive Channel Europe Titan 1, 2, 3 & 4 Sep-10 Jun-14Vega Chi Ltd Titan 3 & 4 Jan-11 Aug-14Magic Pony Technology limited Titan Jul-15 Jun-16Touchtype limited (SwiftKey) Titan Aug-10 Mar-16Vision Direct Group limited Titan Sep-09 Feb-16

Notes: Aggregate Realised Proceeds includes cash and ongoing interests; Vega Chi will also generate future revenue share proceeds which are not included in the realised proceeds figures above

100% Loss Realisations Investee Company Which funds invested/exited? Initial Investment

DateRealisation

DateAggregate Cost of

InvestmentAggregate

Realised ProceedsAFrame Media Titan Mar-12 Apr-16

£23,861,091 £0

Applied Superconductor Titan 3 & 4 Jun-11 Dec-13

AQS Group Titan 1, 2 & 3 Feb-10 Aug-12

Diverse Energy Titan 1, 2, 3 & 4 Dec-10 Oct-12

Elonics Titan 1, 2, 3 & 4 Sep-10 May-12

GB Environmental Titan 1 & 2 May-08 Mar-09

SkillsMarket (iProfile) Titan 1, 2 & 3 Aug-09 May-11

LifeBook Titan 4 & 5 Sep-12 Nov-13

Money Workout Titan 1, 2 & 3 Mar-10 Apr-11

Phase Vision Titan 1, 2 & 3 May-09 Mar-13

PrismaStar Titan 1, 2, 3 & 4 Sep-10 Mar-13

Shopa Titan 1, 2, 3, 4 & 5 May-13 Sep-15The Key Revolution Titan 1 & 2 Jul-08 Dec-09

99 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

Track record

• The Venture Partner co-investment model also works along with Octopus’ own team skills, its diverse portfolio approach and the active portfolio management style to mitigate the risk associated with early stage investing wherever possible.

Tax Effi cient Review Strategy rating: 29 out of 30

The other aspect of Octopus Titan VCT which is diff erent from other VCTs on the market is the focus on venture capital investing in early stage unquoted companies, with follow on investments funding development and growth capital. Early stage investments had been mainly avoided by other VCTs until the Octopus Titan VCTs launched as they were deemed too risky. VCTs generally moved up into Management Buy Out (MBO) and Management Buy In (MBI) deals although these have recently been restricted by recent changes to VCT legislation. This puts Octopus Titan VCT in a unique position in the market as it doesn’t have to adapt its strategy to fi t new legislation unlike many other VCTs.

Octopus claims it has some strong risk mitigation approaches in place that have enabled it to perform very well in this sector over the last fi ve years. As well as having a diverse portfolio of around 50 companies they cite the Venture Partner investment model as being a signifi cant factor in mitigating risk, alongside its philosophy of investing a small amount initially before providing further funding where a business proves its investment case.

The Ventures Team at Octopus claim to have realised circa 20% of the businesses (by number of companies) invested into by Titan at a loss (equivalent to less than 14% of capital invested by the fund) against an industry average of 50% or more (source: RSA Growing Pains report, October 2014). Additionally, because of the increased maturity of the off er compared to a new fund launch, Octopus say that a signifi cant proportion of the portfolio investors will be accessing are already delivering signifi cant capital growth. This has resulted in Octopus Titan VCT having paid 61p of divi-dends since launch, resulting in a Total Return (NAV plus cumulative dividends paid) of 154.7p per share as at 15 August 2016. The circa 50 companies in the portfolio (as at 31 August 2015, and in-cluding those which the Titan VCT still has an interest in through the Zenith transaction) employed over 800 additional people in the year to April 2016 and have grown revenues by nearly £150m in calendar year 2015. A third of the portfolio is grew revenues at more than 50% in the year.

Octopus Titan VCT is invested in a diversifi ed portfolio of investments in early stage unquoted companies with a focus on technology-enabled businesses which operate in almost any sector. Now that the Company is through its initial Qualifying Investment period and has been invested above the 70% qualifying holdings threshold for a number of years, the investment profi le is expected to be approximately 75% to 90% in Qualifying Companies, and 10% to 25% in cash, money market securities and other funds managed by Octopus Investments. Prior to investment of the funds raised in this off er, the funds are held in cash or cash equivalents, or other funds managed by Octopus Investments. The directors provide a share buyback scheme to provide a degree of liquidity for investors, at a price no less than 95% of the prevailing net asset value.

The Octopus Titan VCTs have invested into 71 businesses since inception, of which: 24 have been realised, in whole or in part, consisting of:- ten with positive realisations (of which four are part realisations)- fourteen have been realised at a loss (all of which is refl ected in the current NAV)As at 31 August 2016, there were 51 companies in the Octopus Titan VCT portfolio (including the

companies which Titan still has an interest in through the Zenith transaction), of these:• Twenty six are currently being held at a value which is higher than the investment cost (typi-

cally due to follow on funding rounds taking place at a higher value)• Ten are currently valued at the investment cost• The remaining fi fteen are currently being held at a value which is less than the investment

cost, including one that has been written off entirely (yet to be realised but already account-ed for in the current NAV).

Interestingly this is the same size portfolio (51 companies) as at our last review date in September 2015.

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 20161010

Review of Early Stage Generalist VCT with track record

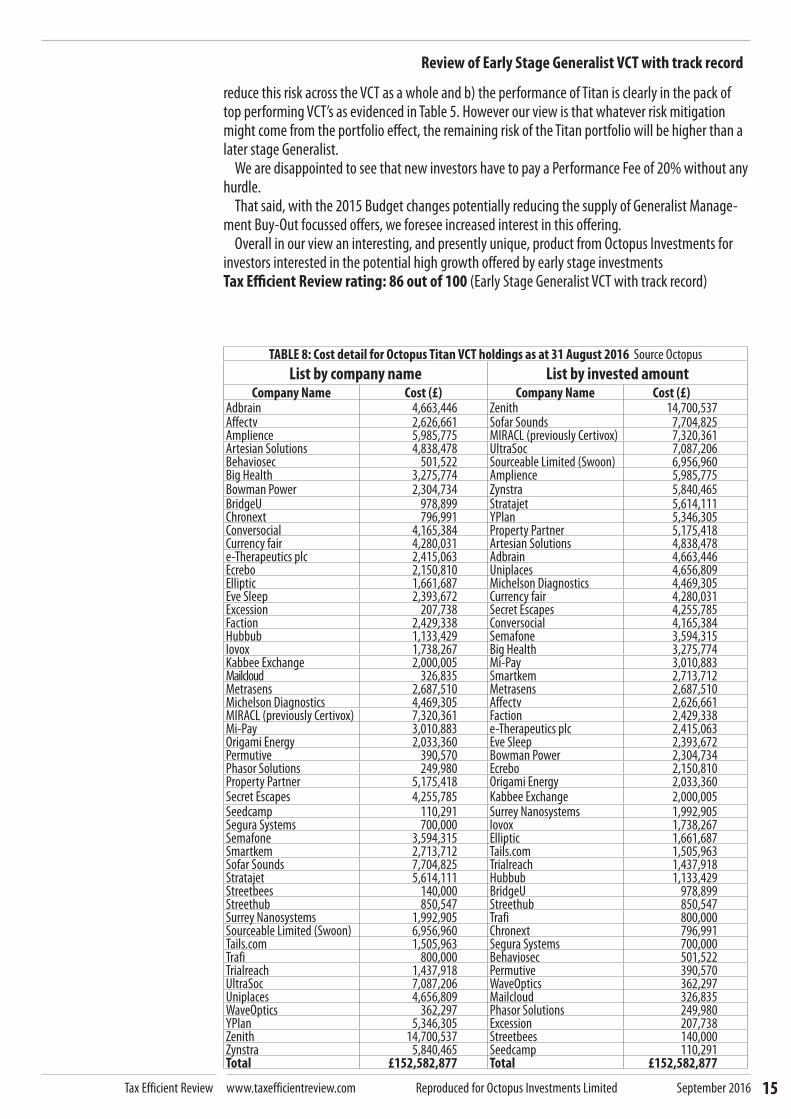

As mentioned at the beginning of this review, Octopus have not provided valuation details on any individual holdings outside the top ten.

The total portfolio of the VCT is diversifi ed with the top investment, Zenith (a Cayman Islands registered company which holds stakes in 4 companies) representing 10.83% and the top ten investments (including Zenith) representing 37.40% of the portfolio by carrying value (not cost) as at 30 April 2016. In total, these Top 10 holdings represent twelve underlying companies, given that Zenith holds stakes in 4 companies, including Secret Escapes which is also held directly by Octopus Titan VCT.

The performance as at 30 April 2016 for the earliest Titan off er (2007/08) is detailed in Table 4.We think the two key questions for potential investors are:• Does the return compensate for the higher risk involved in investing in early stage

companies as evidenced by the large number of complete write-off s. Taking the launch year 2007/08, the top ten VCT launches returns are in Table 5 and show that to date, in our view, whilst performing well, the Titan off er has not produced a return that compensates for what we perceive to be the higher risk involved, in comparison to Generalist VCTs focussing on Growth funding and/or Management Buy-Outs. Although we do acknowledge that govern-ment restrictions on VCTs doing management buy outs may mean that others have no choice but to move into Titan’s space and take more risk.

• Is there growth potential left in the circa 50 holdings (including the established hold-ings within Zenith Holding Company (which holds stakes in four companies)) as well as the newer companies still held at cost, in order to compensate for any future potential write-off s from amongst the large number of stocks held at cost. It is worth noting that two of the previous top ten holdings at the time of this report being published in 2015, have since been realised at signifi cant profi t for Titan (SwiftKey (aka TouchType Ltd) being sold to Microsoft and Vision Direct being sold to Essilor. There has also been a third profi table exit with Magic Pony Technology being sold to Twitter, all in 2016).

Octopus was unable to disclose details of all of the various exits that have occurred due to com-mercial confi dentiality terms agreed with the acquirers. However, it has provided some details where possible (see Table 6) and included some background on the Zenith transaction that provided partial exits for four of the holdings. This is covered in our previous analysis of this transaction (published May 2013) which is reproduced at the end of this review.

A number of full or partial exits have now been achieved from unquoted companies in the portfolio to date. These exits include Evi Technologies (acquired by Amazon), Nature Delivered Limited (graze.com, which the Octopus Titan VCT continues to have a holding in via Zenith Holding Company), Rangespan (reported in the press as being acquired by Google), Zoopla Property Group (which again continues to be held via Zenith Holding Company),Vega Chi (acquired by Liquidnet, the global institutional trading network) and ECNlive (the digital display network providing live content and connecting brands with executive audiences in the corporate environment). The most recent exits include SwiftKey (aka TouchType Ltd, acquired by Microsoft for a reported $250m), Vision Direct (sold to Essilor International), and Magic Pony Technology (acquired by Twitter, for a reported $150m), all of which have completed in 2016.

Focusing on just one of these, Octopus fi rst made a seed investment from Titan VCT into Swift-Key (TouchType Ltd) in 2010 prior to the launch of the company’s fi rst product. SwiftKey’s fl agship mobile app adapts to the way you type, so you spend less time correcting typos the more you use it and more time saying what you really mean. SwiftKey’s launch was a success, and the management team impressive in its ambition and ability to execute its plans well. The app went on to be available in multiple languages and was Google’s most successful ‘paid for’ app for two years running before it was launched on Apple’s operating system in 2014, where it rapidly became Apple’s number-one free app. By 2016, SwiftKey users across 300 million mobile devices had saved an estimated 10 trillion keystrokes across 100 diff erent languages, while the company had grown to employ around 160 people. This expansion was supported by additional funding at key stages of its growth, includ-ing from Titan VCT. In February 2016, SwiftKey announced it was acquired by Microsoft, at a later

1111 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

reported valuation of $250m. The realisation resulted in strong returns for Titan VCT and a special dividend of 5p per share was subsequently paid to Titan shareholders in April 2016.

Octopus values its portfolio companies in accordance with International Private Equity and Venture Capital Guidelines. The valuation of the investments is typically at the price of the most recent funding round unless it has failed to successfully meet its business plan since the last fund-ing round in which case a provision is taken against the valuation, usually by increments of 25%. For any investee company which is more than 12 months from the latest funding round, several triangulated valuation methodologies will be used to inform the valuation and may adjust up or down accordingly.

This new fundraise provides an opportunity for new and existing investors to invest into Octopus Titan VCT. This report and Octopus have previously described the ‘J curve’ a number of times in the past, a trend typically seen by venture funds in which those businesses that fail do so prior to the successful businesses delivering their returns, meaning the value of a portfolio will fall before it rises again. Overall, Octopus tell us that a signifi cant part of the Titan portfolio can probably now be said to be through this dip in the curve.

The fact that the new off er invests into a fund, part of which has progressed along the ‘J’ curve could mean that investors can benefi t from existing developing businesses as they exit through the payment of dividends. This is evidenced by the dividends announced to date, and the fact that Octopus Titan VCT is targeting an annual regular dividend of 5p per share. In addition, the VCT continues to aim to pay special dividends when there are signifi cant gains from the sale of portfolio holdings.

Investors will also be buying into the VCT at a price based on its current net asset value which takes into account both the losses realised to date and also any write downs in the valuations of any under-performing assets in the current portfolio.

The Titan off ering sits within the pack, but not at the top, of top performing VCTs from a returns perspective as shown in Table 5, which considers IRR since launch. However, whilst performance is inline with the best performing VCTs, we are not convinced on results to date that what we perceive to be the extra risk involved in the Titan off ering is compensated for by any extra return. As noted above though most other VCTs will have to take more risk than they have previously because of the changed VCT rules.Tax Effi cient Review Track Record rating: 32 out of 40

Octopus Investments is a specialist fund management company, with over £5.8 billion of funds under management across its range of products. It manages more than £600 million of VCT money on behalf of over 25,000 investors, more money than any other VCT manager, providing fi nance across the small and medium size enterprise spectrum. It has been voted ‘VCT Provider of the Year’ at the Professional Adviser awards on a number of occasions in recent years. The Titan VCT won VCT of the Year at the Investor AllStar awards 2014 and Best VCT at the 2015 Which Investment awards, and is managed by the Ventures Team at Octopus. The team has an excellent track record of invest-ing in early stage companies such as Zoopla Property Group, Graze, Secret Escapes and SwiftKey (TouchType Ltd). Since its formation, the Ventures team has invested £400 million into companies like these.

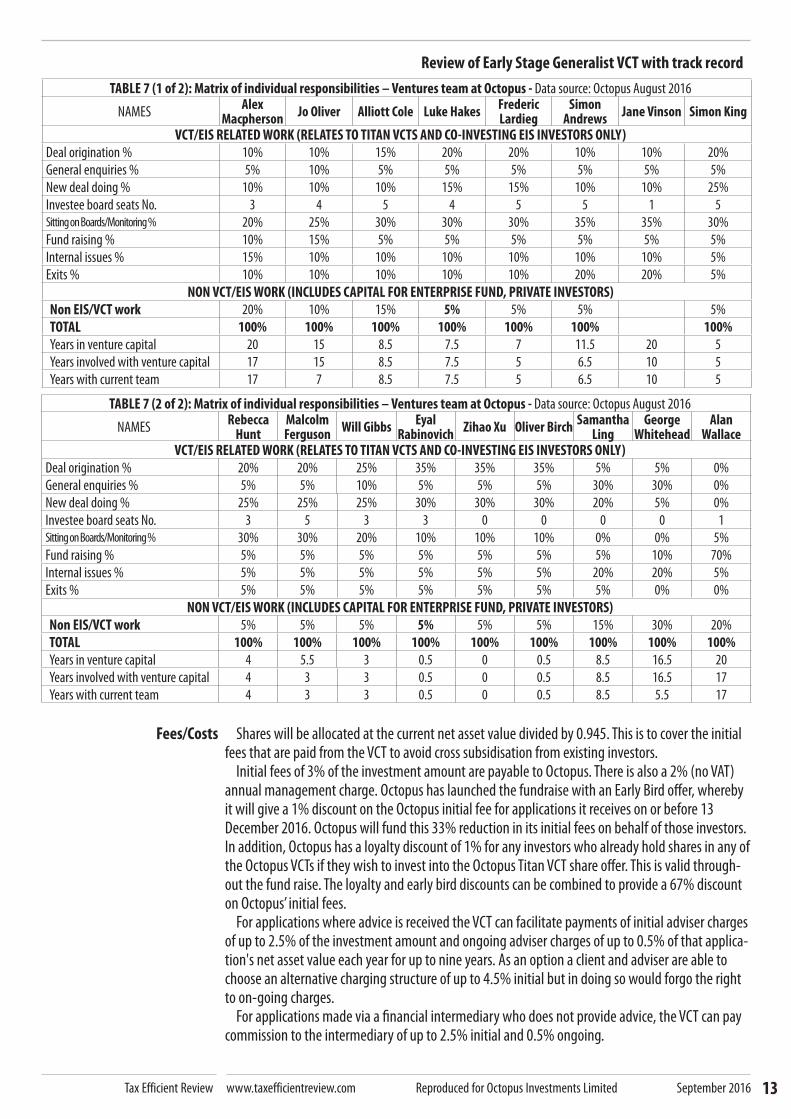

The Ventures investment team is in Table 7.The ventures investment team which manages Octopus Titan VCT, alongside Octopus Eureka EIS

Portfolio Service and Octopus Eclipse VCT is currently 17 strong, featuring investment professionals, investor relations specialists and investment support, plus fi ve Operating Venture Partners spend-ing the equivalent of 6.9 man years per annum on investing the funds (5.9 man years from "Deal origination" and "New deal doing" rows in Table 7 plus some Venture Partner time). The average deal size to date is around £2,000,000 and in our view unquoted deals take around four months on average to complete.

As part of our VCT reviews we try to gauge how the size of a team relates to the amount of deal

Manager

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 20161212

Review of Early Stage Generalist VCT with track record

doing capacity that is needed to invest funds raised. We do this by asking providers to complete a time breakdown for team members to quantify the time spent initiating and transacting new deals in order to arrive at a man-year equivalent for executives seeking out and executing new deals. This together with a TER assumption on maximum deals per executive per year (three based on industry input) and the average deal size (from past investments) helps to give an estimate of deal doing capability within the team. We then compare this to funds still to invest from past fund raisings, funds being raised in current fund raising and an estimate of cash proceeds from future realisations that also needs reinvesting.

Titan has made 26 investments totalling £39.6m in the ten months to end August 2016 of which all but fi ve were follow-on investments. With Titan accounting for 60% of the overall investments made by the venture team (with Eureka, Eclipse VCT and the Venture Partners accounting for the balance) over the period, this implies an annual investment rate capability of over nearly £80m per annum for the team (ie not just for Titan). In addition, the Manager has provided TER with detailed pipeline of future investments which supports that it has visibility on over £75m of deal fl ow over the next 12 months, with approximately 75% of this in to existing portfolio companies and 25% in to new investments.

How does this relate to the amount of investing needed to satisfy Titan VCT investors who will not wish to see cash-drag from too much fund-raising.

Table 1 shows that there was still roughly around £113.5m of cash in Titan VCT as at April 2016, which had reduced to circa £90m as at August 2016, including investments by Titan of £19m in the period. Based on earmarked Titan investments of nearly £50m in the period to April 2017, £12.5m of dividends and share buybacks, £4.5m deferred disposal proceeds and costs of £6.6m, the cash balance is expected to be approximately £27m as at the end of April 2017, excluding any infl ows from the current fundraising. This £27m is an appropriate cash buff er given the size of Titan, being less than 10% of the total net asset value. The funds raised in the current funding round are for deployment in the following period.

If this fund raising achieves its stretch target of £120m, the cash balance at the end of April 2017 would be approximately £140m (net of fundraising fees). Assuming running costs of mainly an-nual management fee and performance fee (which Octopus tell us will be around £15m, the bulk of which is paid to Octopus), the regular dividend (around £20m), historic rate share buy backs (around £12m) and a cash buff er of 10% of net asset value of the fund (equivalent to £40m for a £400m fund), only around £55m needs investing . Based on the investment rate year to date, the pipeline of the investments and the deal doing capacity of the team, this will be invested in less than a year, assuming that there are no realisations in the same period producing funds needing reinvesting.

The changes in legislation announced in 2015 generally do not seem to present a problem for Oc-topus Titan VCTs investment mandate which does not include MBOs and will not do so in the future. The average age of a company when Titan fi rst invests is under three years (source: Octopus) versus the cap of 7 years (or 10 years for knowledge intensive companies). The lifetime cap restricting investment of more than £12m in State Aid (which includes VCT & EIS funding) into a company over its lifetime (increasing to £20m in the case of ‘knowledge intensive’ companies) is the most relevant change to Octopus Titan VCT. Many of the companies in the portfolio will require a number of follow on investments prior to exit, which could see investment levels near the cap. However, Octopus believes many should also qualify as a ‘knowledge intensive’ company under the current guidance from HMRC meaning that the cap is signifi cantly higher. Any follow on investments will be subject to careful monitoring by Octopus and Titan’s advisers to ensure these limits are not breached.

Finally, we were also interested to note that the Octopus Ventures team has recently opened an offi ce in New York with the view to giving Titan’s portfolio companies a spring board into the US. Many of the portfolio companies see this as an attractive market to expand into so we are interested to see what the impact might be on future performance.Tax Effi cient Review Team and Deal fl ow rating: 18 out of 20

1313 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

Fees/Costs Shares will be allocated at the current net asset value divided by 0.945. This is to cover the initial fees that are paid from the VCT to avoid cross subsidisation from existing investors.

Initial fees of 3% of the investment amount are payable to Octopus. There is also a 2% (no VAT) annual management charge. Octopus has launched the fundraise with an Early Bird off er, whereby it will give a 1% discount on the Octopus initial fee for applications it receives on or before 13 December 2016. Octopus will fund this 33% reduction in its initial fees on behalf of those investors. In addition, Octopus has a loyalty discount of 1% for any investors who already hold shares in any of the Octopus VCTs if they wish to invest into the Octopus Titan VCT share off er. This is valid through-out the fund raise. The loyalty and early bird discounts can be combined to provide a 67% discount on Octopus’ initial fees.

For applications where advice is received the VCT can facilitate payments of initial adviser charges of up to 2.5% of the investment amount and ongoing adviser charges of up to 0.5% of that applica-tion's net asset value each year for up to nine years. As an option a client and adviser are able to choose an alternative charging structure of up to 4.5% initial but in doing so would forgo the right to on-going charges.

For applications made via a fi nancial intermediary who does not provide advice, the VCT can pay commission to the intermediary of up to 2.5% initial and 0.5% ongoing.

TABLE 7 (2 of 2): Matrix of individual responsibilities – Ventures team at Octopus - Data source: Octopus August 2016

NAMESRebecca

HuntMalcolm Ferguson

Will GibbsEyal

RabinovichZihao Xu Oliver Birch

Samantha Ling

George Whitehead

Alan Wallace

VCT/EIS RELATED WORK (RELATES TO TITAN VCTS AND CO-INVESTING EIS INVESTORS ONLY)

Deal origination % 20% 20% 25% 35% 35% 35% 5% 5% 0%

General enquiries % 5% 5% 10% 5% 5% 5% 30% 30% 0%

New deal doing % 25% 25% 25% 30% 30% 30% 20% 5% 0%

Investee board seats No. 3 5 3 3 0 0 0 0 1

Sitting on Boards/Monitoring % 30% 30% 20% 10% 10% 10% 0% 0% 5%

Fund raising % 5% 5% 5% 5% 5% 5% 5% 10% 70%

Internal issues % 5% 5% 5% 5% 5% 5% 20% 20% 5%

Exits % 5% 5% 5% 5% 5% 5% 5% 0% 0%

NON VCT/EIS WORK (INCLUDES CAPITAL FOR ENTERPRISE FUND, PRIVATE INVESTORS)

Non EIS/VCT work 5% 5% 5% 5% 5% 5% 15% 30% 20%

TOTAL 100% 100% 100% 100% 100% 100% 100% 100% 100%

Years in venture capital 4 5.5 3 0.5 0 0.5 8.5 16.5 20

Years involved with venture capital 4 3 3 0.5 0 0.5 8.5 16.5 17

Years with current team 4 3 3 0.5 0 0.5 8.5 5.5 17

TABLE 7 (1 of 2): Matrix of individual responsibilities – Ventures team at Octopus - Data source: Octopus August 2016

NAMESAlex

MacphersonJo Oliver Alliott Cole Luke Hakes

Frederic Lardieg

Simon Andrews

Jane Vinson Simon King

VCT/EIS RELATED WORK (RELATES TO TITAN VCTS AND CO-INVESTING EIS INVESTORS ONLY)

Deal origination % 10% 10% 15% 20% 20% 10% 10% 20%

General enquiries % 5% 10% 5% 5% 5% 5% 5% 5%

New deal doing % 10% 10% 10% 15% 15% 10% 10% 25%

Investee board seats No. 3 4 5 4 5 5 1 5

Sitting on Boards/Monitoring % 20% 25% 30% 30% 30% 35% 35% 30%

Fund raising % 10% 15% 5% 5% 5% 5% 5% 5%

Internal issues % 15% 10% 10% 10% 10% 10% 10% 5%

Exits % 10% 10% 10% 10% 10% 20% 20% 5%

NON VCT/EIS WORK (INCLUDES CAPITAL FOR ENTERPRISE FUND, PRIVATE INVESTORS)

Non EIS/VCT work 20% 10% 15% 5% 5% 5% 5%

TOTAL 100% 100% 100% 100% 100% 100% 100%

Years in venture capital 20 15 8.5 7.5 7 11.5 20 5

Years involved with venture capital 17 15 8.5 7.5 5 6.5 10 5

Years with current team 17 7 8.5 7.5 5 6.5 10 5

Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 20161414

Review of Early Stage Generalist VCT with track record

Conclusion

For direct applications the Octopus initial fee will be 5.5% (or 3.5% for existing shareholders under the Early Bird off er) and annual charges of 2.5%.

Annual running costs are capped at 3.2% of NAV (excluding VAT and trail commissions), and within that amount the annual Management Fee is 2% p.a. of NAV. Also within the 3.2% is an Administration Fee of 0.3%.

There is a performance fee structure for Octopus Titan VCT. The original VCT was launched in 2007, and in the years since, it has invested and subsequently sold stakes in a number of companies. Because of this, it has already met or exceeded various performance hurdles required to charge this fee. Octopus will take a performance fee – up to a maximum of 20% – on all future gains in perfor-mance, subject to a high watermark (which is currently 154.7p per share).

The combination of an industry standard annual 2% management fee (questionable given poten-tial economies of scale on a £280m VCT) and a Performance fee with no new hurdles beyond those already achieved, have reduced the score in this area.Tax Effi cient Review Costs rating: 7 out of 10

For VCT investors seeking potentially higher returns for taking on a higher level of risk, this is an opportunity to invest into the full portfolio built by what was originally fi ve Titan VCTs. Some of the oldest companies in the portfolio are so far performing very well, as demonstrated by the dividends paid by the VCT to date and its ability to meet the target of regular dividends, despite the diffi cult economic period over which it has been investing and in which the underlying companies have been trading.

Octopus also says that many of the companies added to the portfolio more recently are also making excellent progress. The NAV has remained close to the creation price of 94.5p, and the latest dividends paid announced by Titan increased the cumulative dividends paid to 61p.

Octopus claims that the progress of the ‘Star’ performers within the portfolio further vindicates the Venture Team’s investment model of continuing to fund the ‘winners’ within their portfolios whilst not providing additional funding to the poorer performing companies.

Octopus Titan VCT says it has a strong pipeline of both new investment opportunities, and op-portunities to invest further into existing portfolio companies. It is therefore seeking to raise £70m (with an over-allotment facility of a further £50m, to a total of £120m) in new funds to ensure the VCT is well positioned to capitalise at what Octopus say is a good time to invest, because of the lack of fi nance for smaller companies and the wealth of investment opportunities available.

The companies within Octopus Titan VCT portfolio are at varying diff erent stage of development although Octopus say that the fund could not be deemed to have ‘peaked’ as yet, with realisations only starting to come through (with three in the past twelve months), even from the earliest invest-ments.

The new share off er provides an opportunity to buy into a fund with proven performance, a portfolio of companies which has already made signifi cant progress, and which is valued at a price which factors in losses and write downs that have been incurred thus far.

Octopus Titan VCT is managed by a very well resourced and experienced team and off er, in our view, two unique features that set it apart from the rest of the off erings: the “Venture Partner” approach to investing and the focus on venture capital investing in early stage, expansion and development investments.

As a new fund raise opportunity into an existing diversifi ed fund, this represents a unique chance for investors to access the ‘star companies’ within an early stage portfolio that have demonstrated both growth and resilience in a tough economic climate.

With three exits from the portfolio in the last twelve months, cash or cash equivalents still to invest as at 30 April 2016 total £113m.

On the performance to date we are not yet convinced that the returns compensate for what we perceive to be the extra risk involved in the Titan off ering. Our position is that we see the Titan investments as individually higher risk than later stage ones pursued by other Generalists, although we do acknowledge that a) the effi cient portfolio management strategies employed should help

1515 Tax Efficient Review www.taxefficientreview.com Reproduced for Octopus Investments Limited September 2016

Review of Early Stage Generalist VCT with track record

TABLE 8: Cost detail for Octopus Titan VCT holdings as at 31 August 2016 Source Octopus

List by company name List by invested amountCompany Name Cost (£) Company Name Cost (£)

Adbrain 4,663,446 Zenith 14,700,537Affectv 2,626,661 Sofar Sounds 7,704,825Amplience 5,985,775 MIRACL (previously Certivox) 7,320,361Artesian Solutions 4,838,478 UltraSoc 7,087,206Behaviosec 501,522 Sourceable Limited (Swoon) 6,956,960Big Health 3,275,774 Amplience 5,985,775Bowman Power 2,304,734 Zynstra 5,840,465BridgeU 978,899 Stratajet 5,614,111Chronext 796,991 YPlan 5,346,305Conversocial 4,165,384 Property Partner 5,175,418Currency fair 4,280,031 Artesian Solutions 4,838,478e-Therapeutics plc 2,415,063 Adbrain 4,663,446Ecrebo 2,150,810 Uniplaces 4,656,809Elliptic 1,661,687 Michelson Diagnostics 4,469,305Eve Sleep 2,393,672 Currency fair 4,280,031Excession 207,738 Secret Escapes 4,255,785Faction 2,429,338 Conversocial 4,165,384Hubbub 1,133,429 Semafone 3,594,315Iovox 1,738,267 Big Health 3,275,774Kabbee Exchange 2,000,005 Mi-Pay 3,010,883Mailcloud 326,835 Smartkem 2,713,712Metrasens 2,687,510 Metrasens 2,687,510Michelson Diagnostics 4,469,305 Affectv 2,626,661MIRACL (previously Certivox) 7,320,361 Faction 2,429,338Mi-Pay 3,010,883 e-Therapeutics plc 2,415,063Origami Energy 2,033,360 Eve Sleep 2,393,672Permutive 390,570 Bowman Power 2,304,734Phasor Solutions 249,980 Ecrebo 2,150,810Property Partner 5,175,418 Origami Energy 2,033,360Secret Escapes 4,255,785 Kabbee Exchange 2,000,005Seedcamp 110,291 Surrey Nanosystems 1,992,905Segura Systems 700,000 Iovox 1,738,267Semafone 3,594,315 Elliptic 1,661,687Smartkem 2,713,712 Tails.com 1,505,963Sofar Sounds 7,704,825 Trialreach 1,437,918Stratajet 5,614,111 Hubbub 1,133,429Streetbees 140,000 BridgeU 978,899Streethub 850,547 Streethub 850,547Surrey Nanosystems 1,992,905 Trafi 800,000Sourceable Limited (Swoon) 6,956,960 Chronext 796,991Tails.com 1,505,963 Segura Systems 700,000Trafi 800,000 Behaviosec 501,522Trialreach 1,437,918 Permutive 390,570UltraSoc 7,087,206 WaveOptics 362,297Uniplaces 4,656,809 Mailcloud 326,835WaveOptics 362,297 Phasor Solutions 249,980YPlan 5,346,305 Excession 207,738Zenith 14,700,537 Streetbees 140,000Zynstra 5,840,465 Seedcamp 110,291Total £152,582,877 Total £152,582,877

reduce this risk across the VCT as a whole and b) the performance of Titan is clearly in the pack of top performing VCT’s as evidenced in Table 5. However our view is that whatever risk mitigation might come from the portfolio eff ect, the remaining risk of the Titan portfolio will be higher than a later stage Generalist.

We are disappointed to see that new investors have to pay a Performance Fee of 20% without any hurdle.

That said, with the 2015 Budget changes potentially reducing the supply of Generalist Manage-ment Buy-Out focussed off ers, we foresee increased interest in this off ering.

Overall in our view an interesting, and presently unique, product from Octopus Investments for investors interested in the potential high growth off ered by early stage investments Tax Effi cient Review rating: 86 out of 100 (Early Stage Generalist VCT with track record)

Tax Efficient Review www.taxefficientreview.com Issue 262 September 20161616

Review of Early Stage Generalist VCT with track record

Report issu

ed May 2013

Introduction

Summary

Reproduction of Briefi ng Note published May 2013. The transaction was approved by sharehold-ers on 21 June 2013.

This Briefi ng Note has been produced by Martin Churchill, editor of Tax Effi cient Review, and seeks to explain the key points behind the Zenith LP proposal that shareholders in the Titan VCTs will be asked to vote on at General Meetings on 3 June 2013.

No advice is off ered nor implied by the publication of this Briefi ng Note.It is based upon 1. A meeting with Alex MacPherson, the lead fund manager, and Paul Latham both of Octopus.2. A one hour phone call with John Hustler (Board Chairman for Titan 2), Mark Hawkesworth

(Board Chairman for Titan 3) and Alex MacPherson, the lead Octopus fund manager.3. A one hour phone call with Alex MacPherson, the lead Octopus fund manager.4. The Circular to the three Titan VCT shareholders dated 7 May 2013.5. A note prepared for Tax Effi cient Review by Octopus explaining in greater depth the rationale

behind the Zenith transaction

The proposal on which the Titan VCT shareholders are being asked to vote is complex, was not fl agged up as a potential transaction to the investors in the fund raising that ended three weeks before its announcement and in our view could have a major impact on the VCTs and their future perfor-mance.

Still awaited is HMRC confi rmation that the transaction will not adversely aff ect the status of the Titan VCTs.

It involves the VCTs exiting half their holdings in the four star performers in the three Titan portfo-lios to two new institutional investors by transferring the four companies into a Limited Partnership controlled by the two new institutional investors, DB Private Equity & Private Markets and Seligman Private Equity Select LLP, and managed by Octopus.

The proposal is summarised by the three VCT Board Chairmen in the Circular as "We are pleased to inform you that Titan 1, Titan 2 and Titan 3 (together the “Titan VCTs 1-3”) have been presented with an attractive opportunity to partially realise their investment in a number of underlying Portfolio Companies. This will generate significant cash, which will be used substantially to fund new and follow-on investments in Titan VCTs 1-3’s remaining port-folio investments but which will also be distributed to Shareholders through future dividends, an interim dividend expected to be declared by the Titan VCTs 1-3 when they present their half yearly reports for the 6 months ended 30 April 2013 and partly used to finance future share buy-backs. However, the Sale Proposals are structured so that Titan VCTs 1-3 will also retain a sizeable investment in these underlying Portfolio Companies, which will benefit from further capital investment from new investors through a new fund, Octopus Zenith LP (“Zenith”). Most importantly, it will safeguard the Titan VCTs 1-3’s VCT qualifying status, which is otherwise at risk, thereby ensuring that Shareholders’ tax reliefs are retained".

What does "Most importantly, it will safeguard the Titan VCTs 1-3’s VCT qualifying status, which is otherwise at risk, thereby ensuring that Shareholders’ tax reliefs are retained" actually mean?

VCT legislation requires the fund to hold 70% of its assets in qualifying holdings at all times and HMRC are clear that if you foresee an impending problem with the qualifi cation tests it is important to be proactive to mitigate the risk of a breach.

The test can create a problem for a VCT where a non qualifying investment is disposed of, although there are multiple ways in which transactions can be structured that might minimise any resulting problem.

Investments are either qualifying (meet certain size and trade tests) or non qualifying (do not meet the tests). Qualifying investments can become non qualifying as the investee company circumstances change as this is the case for two out of the four investments covered by this proposal (Zoopla and Nature Delivered known as Graze). The reason that two of the holdings are non-qualifying is that

1717 Tax Efficient Review www.taxefficientreview.com Issue 262 September 2016

Review of Early Stage Generalist VCT with track record

Report issu

ed May 2013

Conclusion

both Zoopla and Nature Delivered no longer meet the test under the Income Taxes Act Section 296(2) "The company must not be under the control of another company, or of another company and any other person or persons connected with that company". Zoopla Property Group Ltd is majority owned by A&N Media (a division of the Daily Mail and General Trust) and Graze is now controlled by Carlyle Europe Technology Partners (the pan-European growth capital & buyout fund).

If the VCT breaches the 70% rule then the VCT has the following time in which to lift its qualifying investment level back up over 70%:

• A qualifying investment – 6 months to rectify• A qualifying investment that has become non qualifying - Immediately in breach unless specifi c

dispensation sought and granted. No requirement for HMRC to grant.• A non qualifying investment - Immediately in breach unless specifi c dispensation sought and

granted. No requirement for HMRC to grant.So in our view the VCT rules are defi cient in not allowing qualifying investments that for good com-

mercial reasons have become non qualifying a period of grace to remedy the breach.To be clear neither Titan 1, 2 or 3 is in breach of the 70% rule at present, however the VCTs have a

duty to anticipate and proactively manage potential non-qualifi cation issues. The potential risk could come should a large investee company be sold or taken over and the transaction not structured in a way to mitigate this problem. This is no diff erent from every other VCT and as with all other VCTs part of the sale process is to plan how to mitigate any possible eff ect the disposal might have on the 70% rule.

It is our experience, over the seventeen years that we have reviewed VCTs, that HMRC are extremely supportive of the industry. A VCT that lost its VCT status would in our view kill the VCT market stone dead. Therefore we would expect that HMRC would aim to look to positively help in any situation involving a disposal of a large holding where the 70% test looks to be in jeopardy, particularly one where the investment started out as qualifying.

We asked Kathryn Robertson, Senior policy/technical advisor on Venture Capital Schemes at HM Revenue & Customs, for a general comment on HMRC’s general approach in this area:

“The regulations dealing with breaches of a VCT’s conditions for approval gives HMRC some discretion to overlook the breach if the breach is outside the control of the managers and the managers take steps to rectify it as soon as possible. HMRC has been in the habit of applying that discretion fl exibly and sympathetically and will continue to do so within the parameters which the legislation allows.”

We therefore take a diff erent view to that of the VCT Chairmen and do not understand how they can say "which is otherwise at risk" about their VCT qualifying status. We certainly think they are alarmist by saying "if the Sale Proposals do not proceed, the Titan VCTs 1-3 would immediately have to consider taking alternative actions and may be forced to dispose of part or all of these Portfolio Companies, potentially at a significant discount to their current value, in order to maintain their VCT status".

In our view this can be seen by Titan shareholders in two ways: either as a creative way out of a real problem that VCT rules have imposed on the VCTs or as a way for Octopus to use the four growth stars in the Titan portfolios to seed a new vehicle that will allow Octopus to tap into lucrative institutional fund raising going forward.

In the Circular the Chairmen set out their view that the Sale Proposals are in the best interests of the Shareholders because they will:

1. Safeguard the Titan VCTs 1-3’s VCT qualifying status, thereby ensuring and that Shareholders retain their VCT tax reliefs;

2. Allow Titan VCTs 1-3 to part realise their investments in the Portfolio Companies at current NAV;3. Enable Titan VCTs 1-3 to retain an investment in the Portfolio Companies and thereby par-

ticipate in any future increase in their value, which will be enhanced by the follow on funds provided by DB PEPM and Seligman;

4. Generate proceeds for the Titan VCTs 1-3 that can finance new and follow on investments, be distributed to Shareholders as future dividends and also finance future share buy-backs;

Tax Efficient Review www.taxefficientreview.com Issue 262 September 20161818

Review of Early Stage Generalist VCT with track record

Report issu

ed May 2013

5. Enable Titan 1’s and Titan 2’s Shareholders to gain an investment in Secret Escapes;6. Provide a structure with institutional partners that can be replicated in the future; and7. Avoid an alternative solution which may necessitate the sale of some or all of the investments in

the Portfolio Companies prematurely, potentially at a price below their current value

As Octopus put it to us, they see one of the major benefi ts of this transaction as creating "a stra-tegic relationship with institutional investors that has the potential to benefi t Titan investors in the medium-long term in respect of further co-investment and follow-on funding into the Titan portfolios to accelerate their growth and optimise their value potential for Titan investors".

A less positive spin on the transaction is that Octopus are using the four "star" performers to seed an institutional fund.

In eff ect we see it as how much weight should be placed on either point 1 or point 6 and there are a number of key questions for shareholders arising from this proposal.

• What is the real risk of breaching the 70% rule?The three VCT Chairmen seem to be asserting that the main reason for this complex transaction is to "safeguard the Titan VCTs 1-3’s VCT qualifying status, thereby ensuring and [sic] that Share-holders retain their VCT tax reliefs" and to "avoid an alternative solution which may necessitate the sale of some or all of the investments in the Portfolio Companies prematurely, potentially at a price below their current value". It is vital for shareholders to keep in mind that Titan 1, 2 and 3 are undertaking this transaction in order to remove the risk of the Titan VCTs breaching VCT rules, not that there is an actual breach at present.In addition we believe that any risk of the VCT losing its VCT status (the VCT income tax relief can only be clawed back in the fi rst fi ve years since a shareholder invested) is completely overblown as we believe that HMRC will seek to help a VCT remedy any breach rather than rigidly enforce a rule. We do however concede that it is easier for us to make this comment as we are not at risk of shareholder complaint if our view of HMRCs' attitude proves not to be correct. We also accept the VCT Board directors have received specialist independent advice to assist them in their deci-sion as to the best course of action.

• Are the valuations reasonable? The Boards have commissioned an independent report on the valuations from a top ten UK accounting fi rm (based an 2012 Accountancy Age fi gures) which considers the valuations as reasonable as the portfolio companies are all the subject of recent transactions involving third parties injecting more funds into the companies.This raises a question: If there have been recent transactions, why could these not have been structured in such a way as to avoid any of the 70% test issues?

• Is the partial exit from the portfolio companies and the structure of the Limited Partnership and its sharing of profi ts/losses in the best interests of the VCT share-holders?There are downside protection features for the new shareholders in the structure (they receive distributions in fi rst place plus a 10% compound return before the VCTs start to receive distribu-tions) and we question why these are needed.

• Does the introduction of the new investors give Octopus a confl ict of interest? The answer has to be yes and we expect the Boards to properly represent the VCT investors in this matter.

Overall we see this transaction as one that benefi ts both the Titan shareholders and Octopus.The Titan shareholders exit half their investment in the four "star" holdings, retain the other half (although in a Limited Partnership structure with downside protection for the new investors) and the structure should help to avoid any future 70% qualifying assets test issues.

Octopus are able to seed a new fund raising vehicle that could prove attractive to institutional investors. In our view they are the outright winners in this transaction.

Not a transaction with too much to object to but we think the risk highlighted by the VCT Boards as to the danger posed from these large investments and the threat to the status of the VCTs is over-

1919 Tax Efficient Review www.taxefficientreview.com Issue 262 September 2016

Review of Early Stage Generalist VCT with track record

Report issu

ed May 2013

Background to VCT rules

HMRC value vs Economic Value

The Titan problem

exaggerated. We would be surprised if most Titan shareholders did not support the proposal.

Here is the background to the non-qualifying issue

First it is important to understand the diff erence between HMRC valuation and economic valua-tion.

• HMRC valuation is the cost price of the asset when purchased and remains constant until further shares are purchased at a diff erent price.

• Using Zoopla as the example the HMRC valuation represents 7% of Titan 1 – investment cost being £742k

• Economic valuation is the current valuation of the assets and the price which contributes to NAV. Zoopla’s economic valuation as a result in the rise in value of the shares is 25% of Titan 1 NAV – Fair value being £4,486k

The Titan funds invested into a portfolio of businesses from 2008 making qualifying investments over the period passing through the three year mark. However some of the businesses that were originally invested into have, as a result of success, become non qualifying assets for VCT purposes.

Companies which formed part of Zenith transaction in June 2013

AssetOriginal

investment dateQualifying on

purchase

Qualifying at time

of Zenith Transaction

Date went non qualifying

Reason for non qualifying

Zoopla Property Group

07/01/2009 Yes No May 2012Subsidiary of another company contrary to

Income Taxes Act Section 296(2)

Nature Delivered 30/06/2010 Yes No Nov 2012Calastone 29/10/2008 Yes Yes NA NA

Secret Escapes 18/04/2011 Yes Yes NA NA

At a VCT level circa 23% of Titan 1’s and 2's (they are mirror images of each other) current HMRC value is in non-qualifying assets. Zoopla constitutes 7% of the total HMRC value, and Nature Deliv-ered (Graze) 12%. In addition to these two assets there are also some additional unquoted holdings that are non-qualifying, taking the total to 23%.

VCT legislation requires the fund to hold 70% of its assets in qualifying holdings at all times. HMRC are clear that if you foresee an impending problem with the qualifi cation tests it is important to be proactive to mitigate the risk of a breach.

Octopus provided the following comment:"VCTs are a tremendous structures for taking businesses from the circa £10m valuation point to the £50m - £100m range. However, in order to build really signifi cant companies, further corporate action is often necessary and this has been the situation at both Zoopla (where the Digital Property Group assets merged with Zoopla) and Nature Delivered (Carlyle transaction last year). We regard both the DPG and Carlyle transactions as real positives and of real benefi t to Zoopla and Nature Delivered respectively and, therefore, the Titan investments in the businesses. However, both involved a corporate taking a majority stake in each business, which in turn resulted in both assets becoming immediately non-qualifying.The fi rst to occur was Zoopla in May 2012 when the merger with the Daily Mail Group Trust business, DPG, resulted in Zoopla being majority owned by a corporate. This makes the asset non-qualifying. The merger is of great benefi t to Zoopla and the right thing for the busi-ness to do to build a signifi cant company from which Titan investors have benefi ted and we believe will continue to benefi t.In its own right that was not a major issue for Titan 1 in respect of the 70% test, given Zoopla’s 7% HMRC valuation.

Tax Efficient Review www.taxefficientreview.com Issue 262 September 20162020

Review of Early Stage Generalist VCT with track record

Report issu

ed May 2013

What have the VCT Boards done to flag this problem to

shareholders

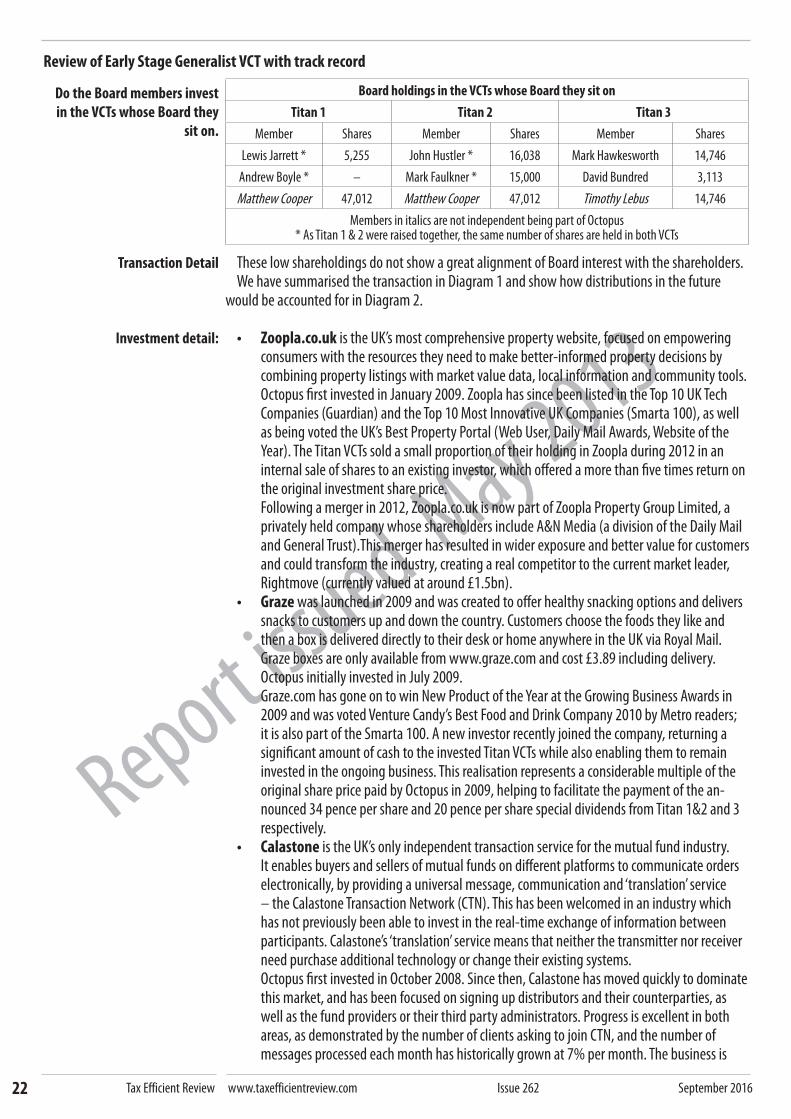

Are there no alternative options