Embed Size (px)

Citation preview

Teachers’ Background & Capacity to TeachPersonal Finance:

Results of a National Study

Wendy L. Way, Ph.D., Professor & Associate DeanSchool of Human Ecology, University of Wisconsin-Madison

Karen Holden, Ph.D., ProfessorSchool of Human Ecology & Robert M. La Follette School of Public Affairs, University of Wisconsin-Madison

Ue full report is available at www.nefe.org/tntfinalreport.

©2010 National Endowment for Financial Education. All rights reserved.

2

Introduction

Teachers are pivotal to the success of financial education efforts. And while public awareness ofthe need for financial education has been growing rapidly in recent years, very little is knownabout the needs and characteristics of the teachers who are called upon to deliver this educationin the classroom.

Since a single accepted certification to teach financial education does not exist, teachers fromdiverse backgrounds—from elementary education teachers to secondary teachers specializing invocational/technical education, social studies, or math—are being tapped to teach financialeducation topics that they may know very little about. In addition, it is widely recognized thatteacher salaries are generally lower than other professionals with comparable education andresponsibilities, adding a personal economic challenge to those individuals who are charged withteaching financial education to our nation’s youth.

How do these financial issues affect our K–12 teachers? And how prepared are these educatorsfrom diverse backgrounds to teach personal finance?Uese are the questions that Wendy L. Way,Ph.D., and Karen Holden, Ph.D., from the University of Wisconsin-Madison, examined in “Teachers’Background and Capacity to Teach Personal Finance,” a two-year national study funded by theNational Endowment for Financial Education® (NEFE®) and completed in March 2009.

Highlights of Findings

2

80 percent ofstates haveadoptedpersonalfinanceeducationstandards orguidelines ofsome kind, upfrom 42 percentin 1998

63.8 percentof teachersfeel unqualifiedto utilizetheir state’sfinancialliteracystandards

89 percentof teachersagree orstrongly agreethat studentsshould takea financialliteracy courseor pass a testfor high schoolgraduation

Only29.7 percentof teachersare teachingfinancialeducation inany way—in existingclasses orspecial classeson financetopics

Only37 percentof K–12teachershad takena collegecoursein personalfinance

Only11.6 percentof K–12teachershad takena workshopon teachingpersonalfinance

Less than20 percentof teachersreportedfeeling verycompetentto teach anyof the sixpersonalfinancetopicssurveyed

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

3

About this Study

More than 1,200 K–12 teachers, prospective teachers currently enrolled in teacher educationprograms, and teacher education faculty completed online surveys for this study. Respondentswere asked 30 multi-part questions about their training and education in personal finance, theiropinions about the importance of financial education, and their capacity to teach these topics.Respondents also were asked about their own personal financial concerns and their experience indealing with personal finance issues outside the classroom.

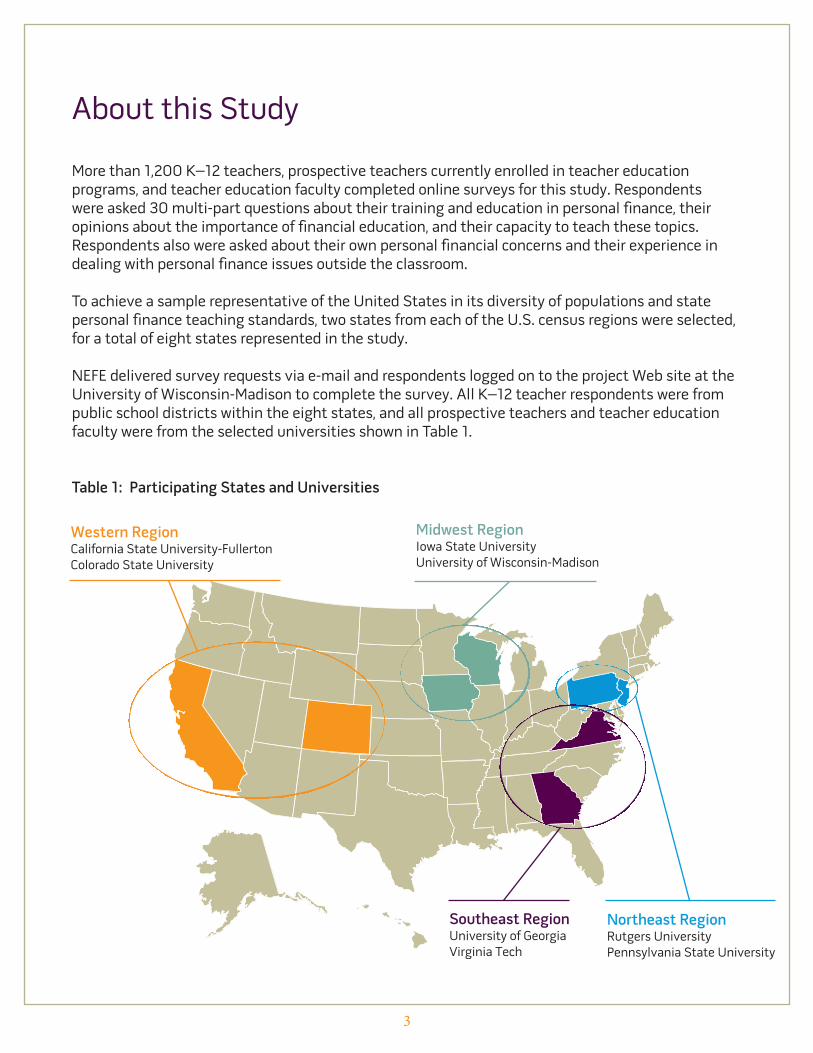

To achieve a sample representative of the United States in its diversity of populations and statepersonal finance teaching standards, two states from each of the U.S. census regions were selected,for a total of eight states represented in the study.

NEFE delivered survey requests via e-mail and respondents logged on to the project Web site at theUniversity of Wisconsin-Madison to complete the survey. All K–12 teacher respondents were frompublic school districts within the eight states, and all prospective teachers and teacher educationfaculty were from the selected universities shown in Table 1.

Table 1: Participating States and Universities

Western RegionCalifornia State University-FullertonColorado State University

Midwest RegionIowa State UniversityUniversity of Wisconsin-Madison

Northeast RegionRutgers UniversityPennsylvania State University

Southeast RegionUniversity of GeorgiaVirginia Tech

4

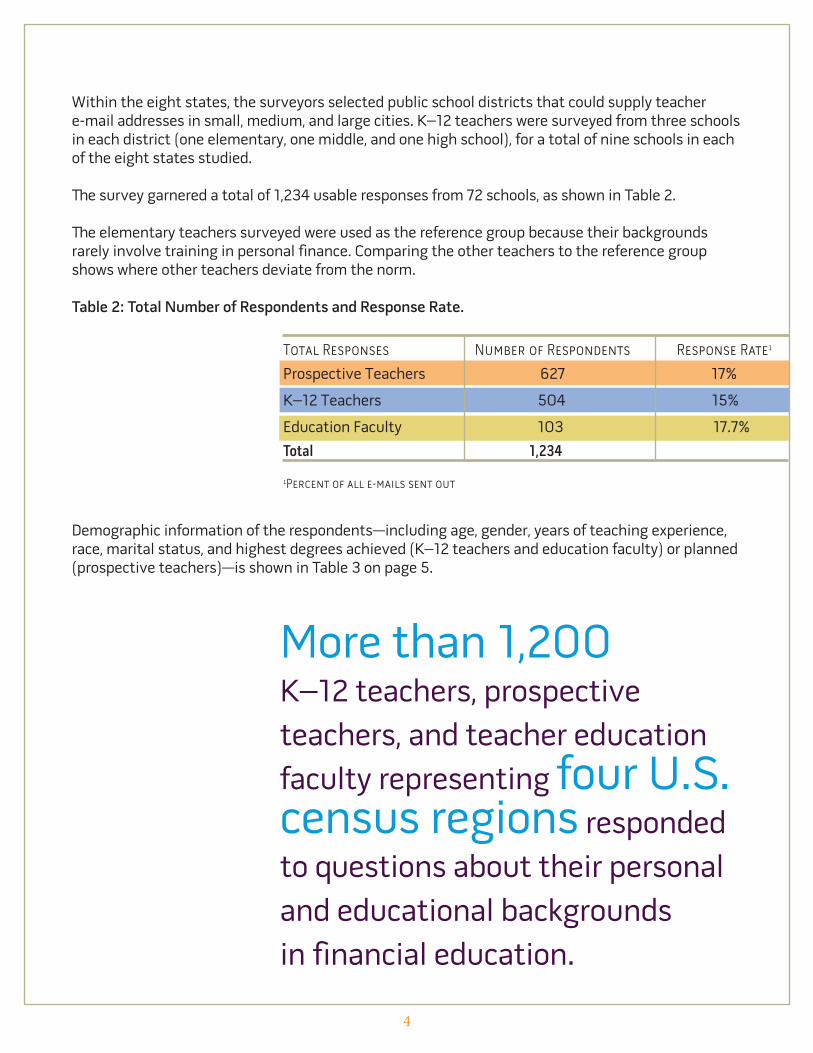

Within the eight states, the surveyors selected public school districts that could supply teachere-mail addresses in small, medium, and large cities. K–12 teachers were surveyed from three schoolsin each district (one elementary, one middle, and one high school), for a total of nine schools in eachof the eight states studied.

Ue survey garnered a total of 1,234 usable responses from 72 schools, as shown in Table 2.

Ue elementary teachers surveyed were used as the reference group because their backgroundsrarely involve training in personal finance. Comparing the other teachers to the reference groupshows where other teachers deviate from the norm.

Table 2: Total Number of Respondents and Response Rate.

Demographic information of the respondents—including age, gender, years of teaching experience,race, marital status, and highest degrees achieved (K–12 teachers and education faculty) or planned(prospective teachers)—is shown in Table 3 on page 5.

More than 1,200K–12 teachers, prospectiveteachers, and teacher educationfaculty representing four U.S.census regions respondedto questions about their personaland educational backgroundsin financial education.

Total Responses Number of Respondents Response Rate1

Prospective Teachers 627 17%

K–12 Teachers 504 15%

Education Faculty 103 17.7%

Total 1,234

1Percent of all e-mails sent out

5

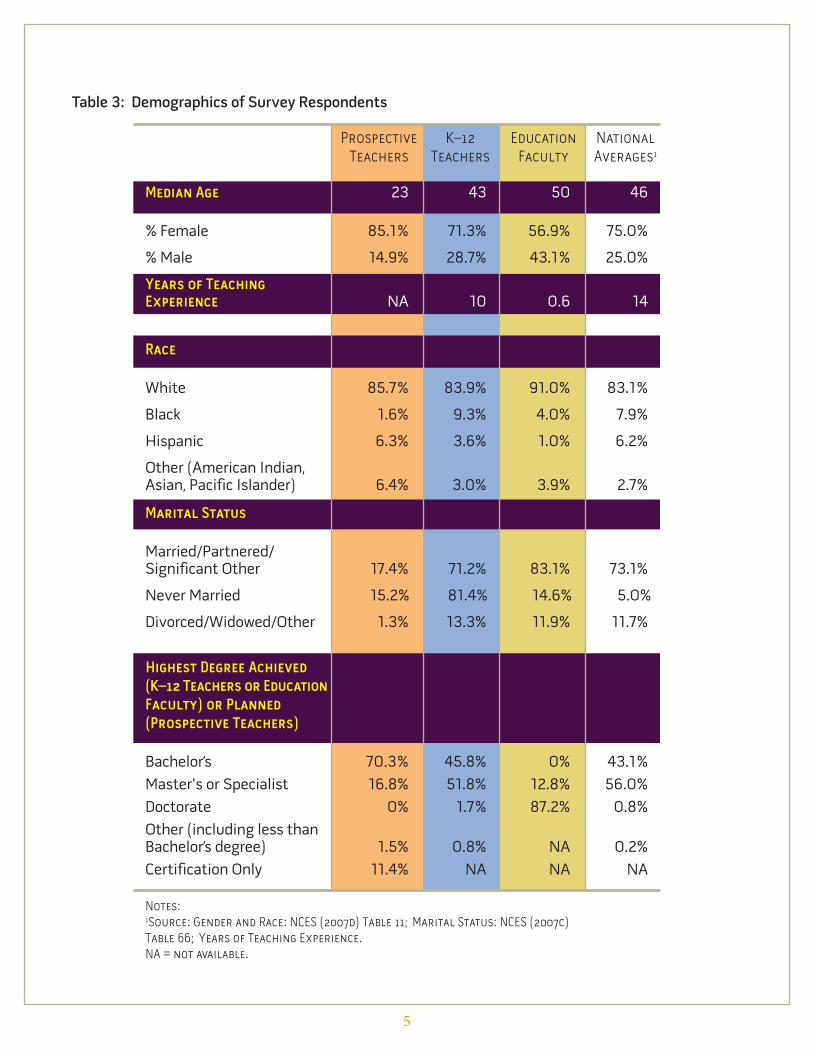

Table 3: Demographics of Survey Respondents

Prospective K–12 Education NationalTeachers Teachers Faculty Averages1

Median Age 23 43 50 46

% Female 85.1% 71.3% 56.9% 75.0%

%Male 14.9% 28.7% 43.1% 25.0%

Years of TeachingExperience NA 10 0.6 14

Race

White 85.7% 83.9% 91.0% 83.1%

Black 1.6% 9.3% 4.0% 7.9%

Hispanic 6.3% 3.6% 1.0% 6.2%

Other (American Indian,Asian, Pacific Islander) 6.4% 3.0% 3.9% 2.7%

Marital Status

Married/Partnered/Significant Other 17.4% 71.2% 83.1% 73.1%

Never Married 15.2% 81.4% 14.6% 5.0%

Divorced/Widowed/Other 1.3% 13.3% 11.9% 11.7%

Highest Degree Achieved(K–12 Teachers or EducationFaculty) or Planned(Prospective Teachers)

Bachelor’s 70.3% 45.8% 0% 43.1%Master's or Specialist 16.8% 51.8% 12.8% 56.0%Doctorate 0% 1.7% 87.2% 0.8%Other (including less thanBachelor’s degree) 1.5% 0.8% NA 0.2%Certification Only 11.4% NA NA NA

Notes:1Source: Gender and Race: NCES (2007d) Table 11; Marital Status: NCES (2007c)Table 66; Years of Teaching Experience.NA = not available.

6

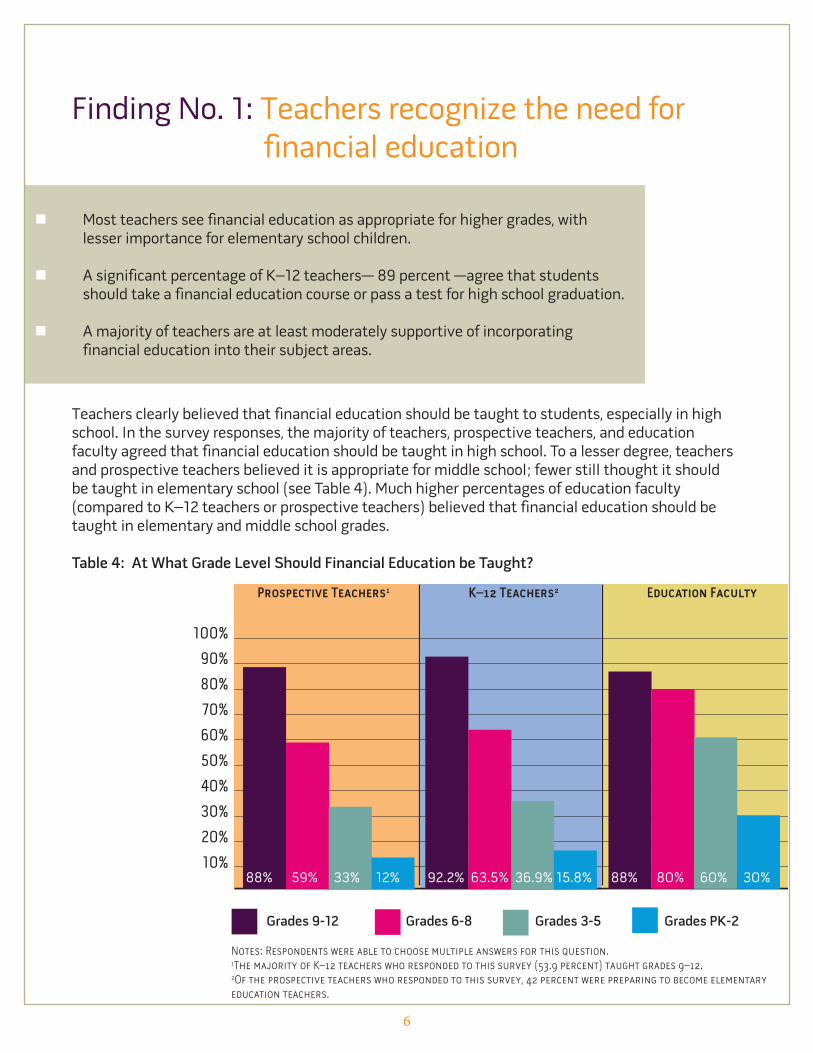

Finding No. 1: Teachers recognize the need forfinancial education

Teachers clearly believed that financial education should be taught to students, especially in highschool. In the survey responses, the majority of teachers, prospective teachers, and educationfaculty agreed that financial education should be taught in high school. To a lesser degree, teachersand prospective teachers believed it is appropriate for middle school; fewer still thought it shouldbe taught in elementary school (see Table 4). Much higher percentages of education faculty(compared to K–12 teachers or prospective teachers) believed that financial education should betaught in elementary and middle school grades.

Table 4: At What Grade Level Should Financial Education be Taught?

� Most teachers see financial education as appropriate for higher grades, withlesser importance for elementary school children.

� A significant percentage of K–12 teachers— 89 percent —agree that studentsshould take a financial education course or pass a test for high school graduation.

� A majority of teachers are at least moderately supportive of incorporatingfinancial education into their subject areas.

7

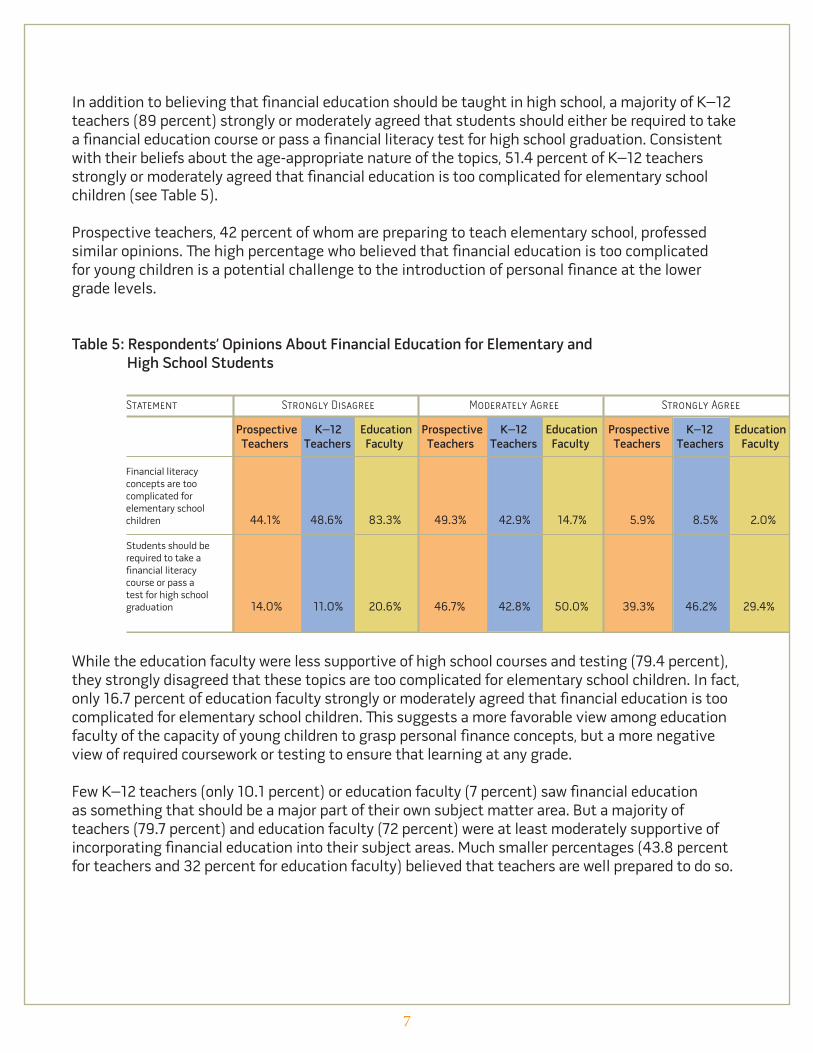

In addition to believing that financial education should be taught in high school, a majority of K–12teachers (89 percent) strongly or moderately agreed that students should either be required to takea financial education course or pass a financial literacy test for high school graduation. Consistentwith their beliefs about the age-appropriate nature of the topics, 51.4 percent of K–12 teachersstrongly or moderately agreed that financial education is too complicated for elementary schoolchildren (see Table 5).

Prospective teachers, 42 percent of whom are preparing to teach elementary school, professedsimilar opinions. Ue high percentage who believed that financial education is too complicatedfor young children is a potential challenge to the introduction of personal finance at the lowergrade levels.

Table 5: Respondents’ Opinions About Financial Education for Elementary andHigh School Students

While the education faculty were less supportive of high school courses and testing (79.4 percent),they strongly disagreed that these topics are too complicated for elementary school children. In fact,only 16.7 percent of education faculty strongly or moderately agreed that financial education is toocomplicated for elementary school children. Uis suggests a more favorable view among educationfaculty of the capacity of young children to grasp personal finance concepts, but a more negativeview of required coursework or testing to ensure that learning at any grade.

Few K–12 teachers (only 10.1 percent) or education faculty (7 percent) saw financial educationas something that should be a major part of their own subject matter area. But a majority ofteachers (79.7 percent) and education faculty (72 percent) were at least moderately supportive ofincorporating financial education into their subject areas. Much smaller percentages (43.8 percentfor teachers and 32 percent for education faculty) believed that teachers are well prepared to do so.

8

Finding No. 2: Few teachers currently are teachingfinancial literacy

� Only 29.7 percent of K–12 teachers have taught financial education topics.

� Having taken a personal finance course for credit is an important predictor ofteaching personal finance.

� Only 37 percent of K–12 teachers had taken a college course with financialeducation–related topics.

� Most financial education is delivered by integration into other disciplinarycourses, rather than in separate, stand-alone courses.

� Teachers with backgrounds in vocational/technical education, social studies,and math are more likely than others to teach financial education topics.

Prospectiveteachers are nomore likely to havetaken a course infinancial educationthan teachers whohave completedtheir degrees manyyears earlier.

9

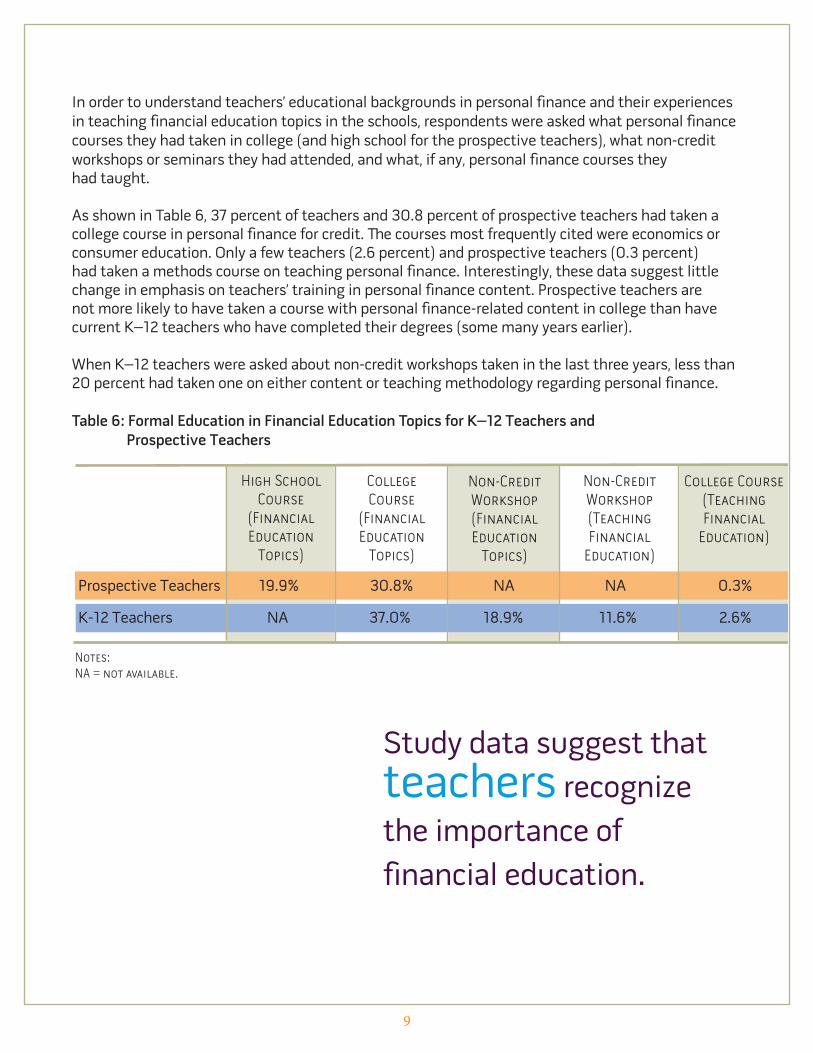

In order to understand teachers’ educational backgrounds in personal finance and their experiencesin teaching financial education topics in the schools, respondents were asked what personal financecourses they had taken in college (and high school for the prospective teachers), what non-creditworkshops or seminars they had attended, and what, if any, personal finance courses theyhad taught.

As shown in Table 6, 37 percent of teachers and 30.8 percent of prospective teachers had taken acollege course in personal finance for credit. Ue courses most frequently cited were economics orconsumer education. Only a few teachers (2.6 percent) and prospective teachers (0.3 percent)had taken a methods course on teaching personal finance. Interestingly, these data suggest littlechange in emphasis on teachers’ training in personal finance content. Prospective teachers arenot more likely to have taken a course with personal finance-related content in college than havecurrent K–12 teachers who have completed their degrees (some many years earlier).

When K–12 teachers were asked about non-credit workshops taken in the last three years, less than20 percent had taken one on either content or teaching methodology regarding personal finance.

Table 6: Formal Education in Financial Education Topics for K–12 Teachers andProspective Teachers

Study data suggest thatteachers recognizethe importance offinancial education.

Prospective Teachers K–12 Teachers

Financial EducationConsulted with professional financial planner 11.8% 50.4%

Consulted benefits specialist at work 5.6% 33.8%

Attended workplace presentation on financial topic 9.4% 23.3%

10

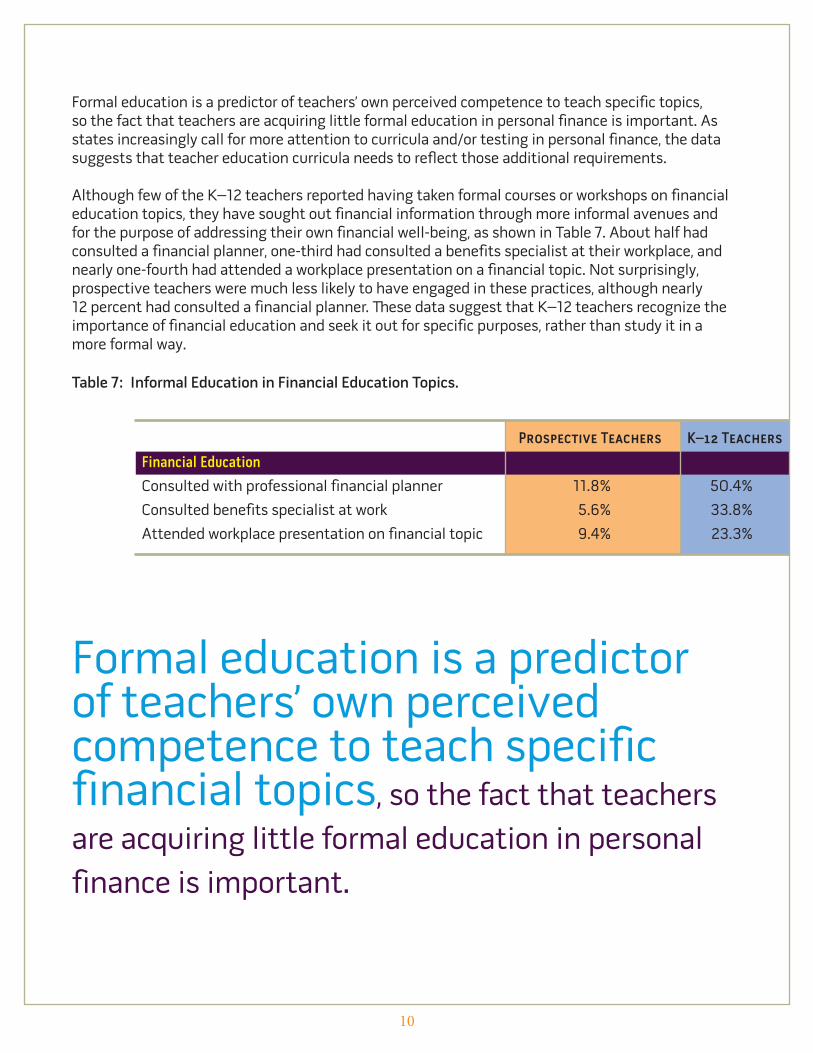

Formal education is a predictor of teachers’ own perceived competence to teach specific topics,so the fact that teachers are acquiring little formal education in personal finance is important. Asstates increasingly call for more attention to curricula and/or testing in personal finance, the datasuggests that teacher education curricula needs to reflect those additional requirements.

Although few of the K–12 teachers reported having taken formal courses or workshops on financialeducation topics, they have sought out financial information through more informal avenues andfor the purpose of addressing their own financial well-being, as shown in Table 7. About half hadconsulted a financial planner, one-third had consulted a benefits specialist at their workplace, andnearly one-fourth had attended a workplace presentation on a financial topic. Not surprisingly,prospective teachers were much less likely to have engaged in these practices, although nearly12 percent had consulted a financial planner. Uese data suggest that K–12 teachers recognize theimportance of financial education and seek it out for specific purposes, rather than study it in amore formal way.

Table 7: Informal Education in Financial Education Topics.

Formal education is a predictorof teachers’ own perceivedcompetence to teach specificfinancial topics, so the fact that teachersare acquiring little formal education in personalfinance is important.

11

According to the study, some teachers shape their ideas of what personal finance is andshould be through their own personal financial experiences, rather than through professionaldevelopment focused on how to teach with methods and materials appropriate for the diversebody of K–12 students.

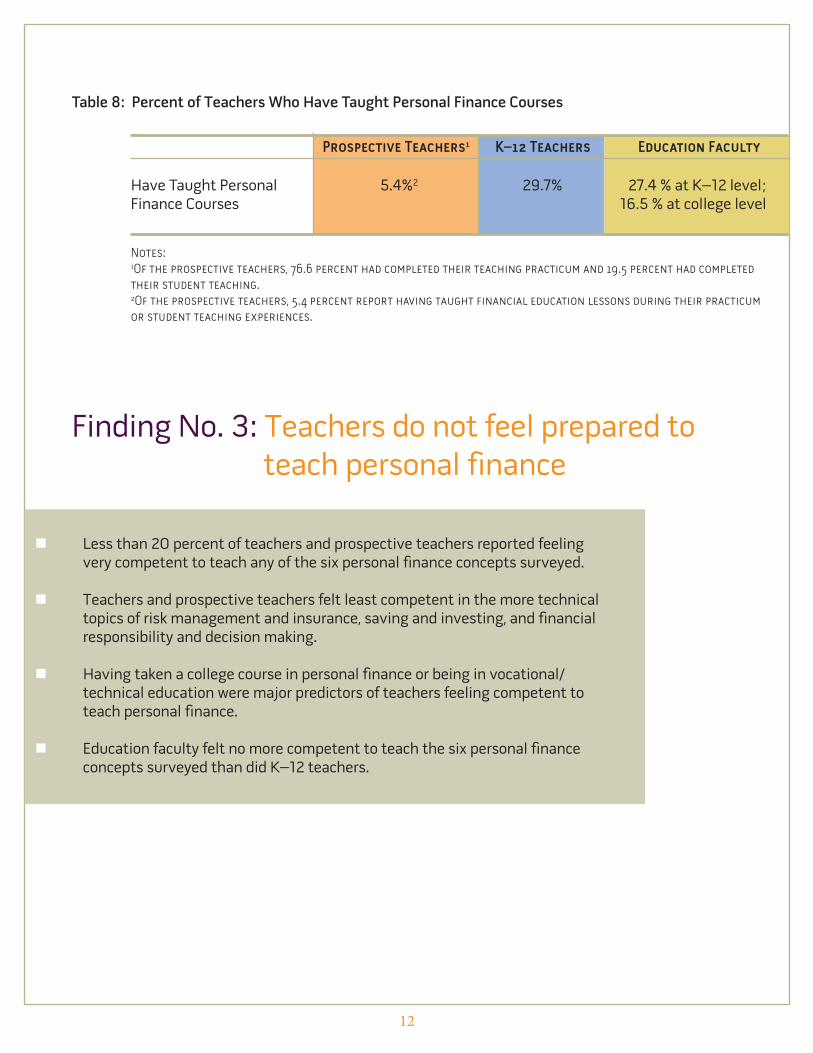

Ue percentage of K–12 teachers and education faculty who have taught a course in personalfinance are similar: 29.7 percent for K–12 teachers and 27.4 percent for education faculty (seeTable 8). Of the K–12 teachers who have taught financial education topics, 25.5 percent reportedthat they integrated financial education topics into a regularly offered credit course rather thanoffering a separate, stand-alone course.

How does a teacher’s background relate to the likelihood that he or she will take or teach a formalcourse with personal finance content? Gender and subject matter background are the onlystatistically significant predictors of the probability of having taken a for-credit course withpersonal finance content:

• Female teachers were about half as likely as male teachers to have taken a formal courserelated to personal finance.

• Social studies teachers were more than three- and-a-half times more likely than the referencegroup to have taken a formal course related to personal finance.

• Vocational/technical education teachers were nearly five times more likely than the referencegroup of elementary education teachers to have taken such a course.

• Ue concentration in vocational/technical education and social studies is consistent with thetraditional expectation that those teachers would teach in the content areas of personal finance.

• In terms of teaching, those who have taken a personal finance course for credit, regardless of theirdiscipline, were more than three times more likely to teach a personal finance course.

• Uose with backgrounds in vocational/technical education and social studies were more likely toteach a personal finance course, just as they had been more likely to take one.

• Teachers of math also were more likely toteach a personal finance course, even thoughthey were no more likely to have taken one.

• Females were no less likely to teach personalfinance topics, even though they were lesslikely to have taken one.

Table 8: Percent of Teachers Who Have Taught Personal Finance Courses

Finding No. 3: Teachers do not feel prepared toteach personal finance

12

� Less than 20 percent of teachers and prospective teachers reported feelingvery competent to teach any of the six personal finance concepts surveyed.

� Teachers and prospective teachers felt least competent in the more technicaltopics of risk management and insurance, saving and investing, and financialresponsibility and decision making.

� Having taken a college course in personal finance or being in vocational/technical education were major predictors of teachers feeling competent toteach personal finance.

� Education faculty felt no more competent to teach the six personal financeconcepts surveyed than did K–12 teachers.

Prospective Teachers1 K–12 Teachers Education Faculty

Have Taught Personal 5.4%2 29.7% 27.4 % at K–12 level;Finance Courses 16.5 % at college level

Notes:1Of the prospective teachers, 76.6 percent had completed their teaching practicum and 19.5 percent had completedtheir student teaching.2Of the prospective teachers, 5.4 percent report having taught financial education lessons during their practicumor student teaching experiences.

13

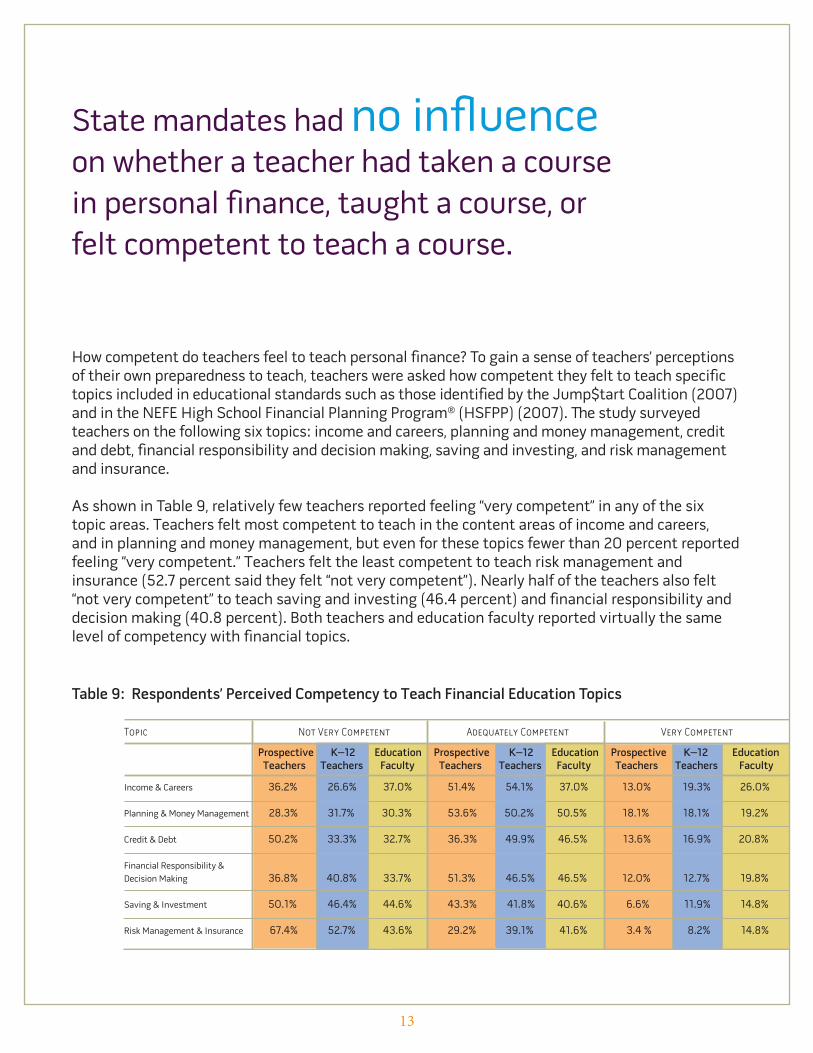

How competent do teachers feel to teach personal finance? To gain a sense of teachers’ perceptionsof their own preparedness to teach, teachers were asked how competent they felt to teach specifictopics included in educational standards such as those identified by the Jump$tart Coalition (2007)and in the NEFE High School Financial Planning Program® (HSFPP) (2007). Ue study surveyedteachers on the following six topics: income and careers, planning and money management, creditand debt, financial responsibility and decision making, saving and investing, and risk managementand insurance.

As shown in Table 9, relatively few teachers reported feeling “very competent” in any of the sixtopic areas. Teachers felt most competent to teach in the content areas of income and careers,and in planning and money management, but even for these topics fewer than 20 percent reportedfeeling “very competent.” Teachers felt the least competent to teach risk management andinsurance (52.7 percent said they felt “not very competent”). Nearly half of the teachers also felt“not very competent” to teach saving and investing (46.4 percent) and financial responsibility anddecision making (40.8 percent). Both teachers and education faculty reported virtually the samelevel of competency with financial topics.

Table 9: Respondents’ Perceived Competency to Teach Financial Education Topics

State mandates had no influenceon whether a teacher had taken a coursein personal finance, taught a course, orfelt competent to teach a course.

14

According to the survey results, teachers who had taken a personal finance course in college aremore comfortable teaching financial education concepts. In fact, these teachers were 50 percentmore likely to rate themselves as competent in teaching financial literacy. Teachers in vocational/technical education fields were significantly more likely than elementary education teachers(the reference group) to feel competent to teach in each of the six topic areas. Teachers in stateswith and without educational testing or course mandates expressed no difference in teachingcompetency.

Finding No. 4: Teachers do not feel qualifiedto use state standards

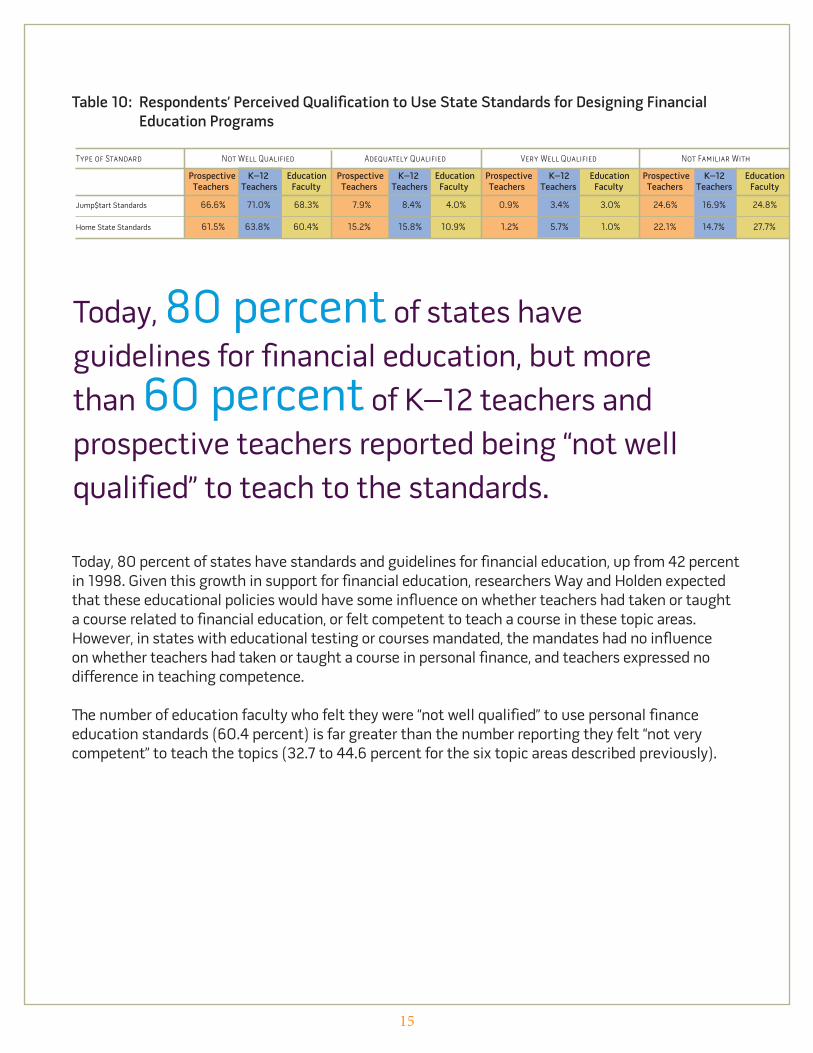

While the number of states with financial education standards and guidelines has almost doubledin the last decade, a majority of K–12 teachers (63.8 percent), prospective teachers (61.5 percent),and education faculty (60.4 percent) reported feeling “not well qualified” to teach to thesestandards. Even higher percentages of K–12 teachers, prospective teachers, and education facultyreported feeling “not well qualified” to use the Jump$tart standards (Jump$tart Coalition, 2007)(see Table 10). In addition to those reporting they were not well qualified to use their statestandards, 14.7 percent of K–12 teachers, 22.1 percent of prospective teachers, and 27.7 percentof education faculty reported not feeling familiar with their state standards in the first place.

� Today, 80 percent of states have adopted personal financial education standardsor guidelines, up from 42 percent in 1998.

� In those states, 63.8 percent of teachers and 61.5 percent of prospective teachersdo not feel qualified to teach to their state’s financial education standards.

� State mandates had no influence on whether a teacher had taken a course inpersonal finance, taught a course, or felt competent to teach a course.

� Education faculty were no more familiar with state financial education standardsthan K–12 teachers.

Table 10: Respondents’ Perceived Qualification to Use State Standards for Designing FinancialEducation Programs

Today, 80 percent of states have standards and guidelines for financial education, up from 42 percentin 1998. Given this growth in support for financial education, researchers Way and Holden expectedthat these educational policies would have some influence on whether teachers had taken or taughta course related to financial education, or felt competent to teach a course in these topic areas.However, in states with educational testing or courses mandated, the mandates had no influenceon whether teachers had taken or taught a course in personal finance, and teachers expressed nodifference in teaching competence.

Ue number of education faculty who felt they were “not well qualified” to use personal financeeducation standards (60.4 percent) is far greater than the number reporting they felt “not verycompetent” to teach the topics (32.7 to 44.6 percent for the six topic areas described previously).

15

Today, 80 percent of states haveguidelines for financial education, but morethan 60 percent of K–12 teachers andprospective teachers reported being “not wellqualified” to teach to the standards.

16

Finding No. 5: Teachers do not feel qualified infinancial education pedagogy

� More than half of K–12 teachers, prospective teachers, and education facultyreported feeling “not well qualified” to design curricula, employ instructionalstrategies, or address learner needs for financial education.

� Teachers view team teaching and collaborating with parents and the localfinancial services community as positive strategies to employ for teachingfinancial education.

Overall, respondentswere open to variousteaching methods,including teamteaching andcollaborationwith parentsand the localfinancialservicescommunity.

17

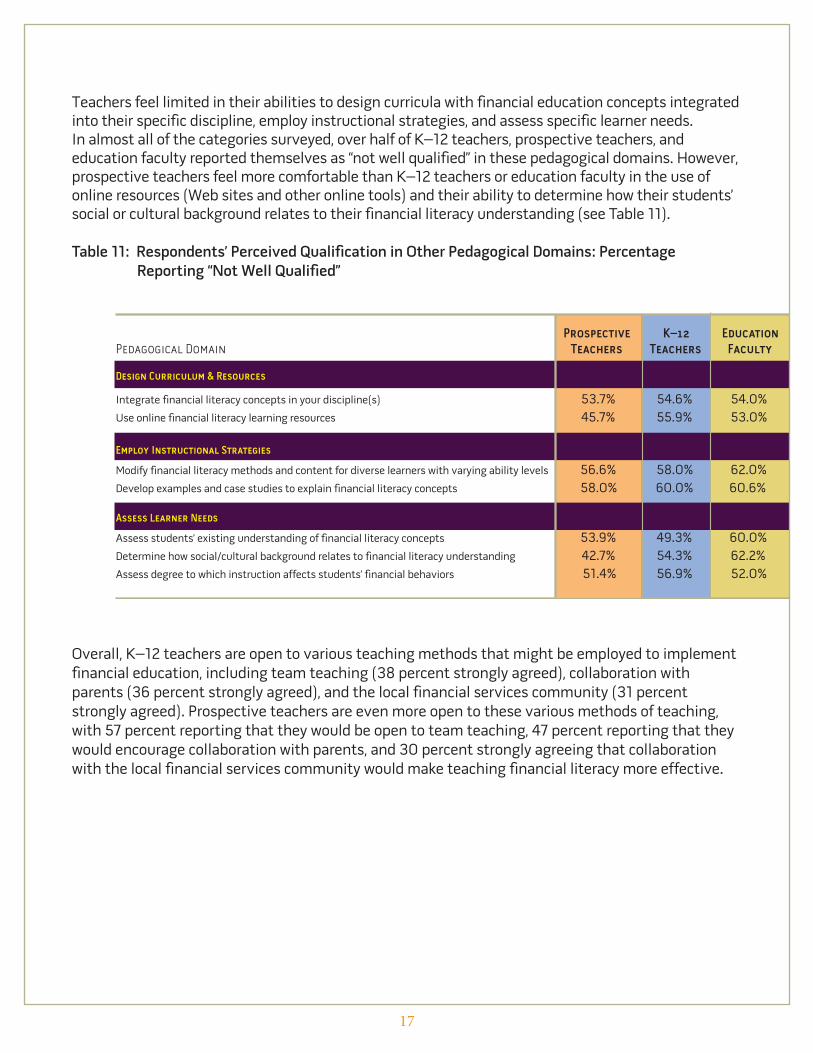

Teachers feel limited in their abilities to design curricula with financial education concepts integratedinto their specific discipline, employ instructional strategies, and assess specific learner needs.In almost all of the categories surveyed, over half of K–12 teachers, prospective teachers, andeducation faculty reported themselves as “not well qualified” in these pedagogical domains. However,prospective teachers feel more comfortable than K–12 teachers or education faculty in the use ofonline resources (Web sites and other online tools) and their ability to determine how their students’social or cultural background relates to their financial literacy understanding (see Table 11).

Table 11: Respondents’ Perceived Qualification in Other Pedagogical Domains: PercentageReporting “Not Well Qualified”

Overall, K–12 teachers are open to various teaching methods that might be employed to implementfinancial education, including team teaching (38 percent strongly agreed), collaboration withparents (36 percent strongly agreed), and the local financial services community (31 percentstrongly agreed). Prospective teachers are even more open to these various methods of teaching,with 57 percent reporting that they would be open to team teaching, 47 percent reporting that theywould encourage collaboration with parents, and 30 percent strongly agreeing that collaborationwith the local financial services community would make teaching financial literacy more effective.

18

Finding No. 6: A majority of teachers areopen to further education infinancial literacy

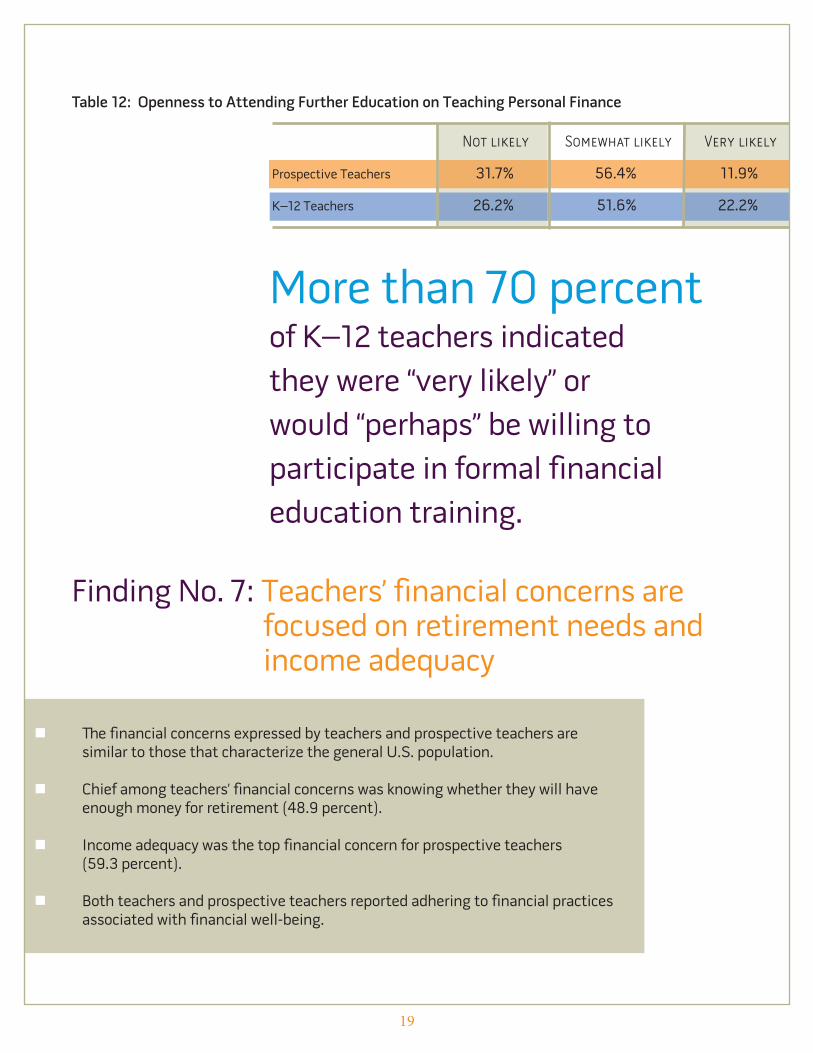

When asked about their willingness to participate in additional training, close to one-fourth ofteachers (22.2 percent) said they would be “very likely” to do so and another 51.7 percent said“perhaps” they would. Teachers who had taken a college course for credit related to personal financeare nearly twice as likely to express this willingness to participate in further education related toteaching personal finance. Vocational/technical education teachers are nearly four times more likelythan others to say they would be “very likely” to participate in professional development activitiesrelated to financial education.

As shown in Table 12, a little more than two-thirds of prospective teachers said they would be willingto attend additional training (beyond what was required for their program) on teaching financialeducation. Twice as many K–12 teachers as prospective teachers said they would be “very likely”to do so. Prospective teachers who have backgrounds in social studies were nearly three times aslikely, and those who have backgrounds in vocational education were nearly six times as likely asthe reference group (elementary education teachers), to say they were “very likely” to attend furthereducation on teaching personal finance. Uis is consistent with the fact that social studies andvocational education teachers traditionally have been responsible for teaching personalfinance topics.

� A little more than two-thirds of prospective teachers and nearly three-quarters ofteachers said they would be “somewhat likely” to participate in further educationon teaching financial literacy.

� Teachers and prospective teachers who would be interested in additional trainingare those who have had a college course in personal finance or who have back-grounds in vocational education or social studies.

19

More than 70 percentof K–12 teachers indicatedthey were “very likely” orwould “perhaps” be willing toparticipate in formal financialeducation training.

� Ue financial concerns expressed by teachers and prospective teachers aresimilar to those that characterize the general U.S. population.

� Chief among teachers’ financial concerns was knowing whether they will haveenough money for retirement (48.9 percent).

� Income adequacy was the top financial concern for prospective teachers(59.3 percent).

� Both teachers and prospective teachers reported adhering to financial practicesassociated with financial well-being.

Not likely Somewhat likely Very likely

Prospective Teachers 31.7% 56.4% 11.9%

K–12 Teachers 26.2% 51.6% 22.2%

Table 12: Openness to Attending Further Education on Teaching Personal Finance

Finding No. 7: Teachers’ financial concerns arefocused on retirement needs andincome adequacy

Prospective K–12Percent Who Have Ever: Teachers Teachers

Purchased real estate property for personal use 9.0% 83.4%Taken out a mortgage 8.1% 82.7%Contributed to voluntary employer-sponsored retirement account 13.4% 73.4%Applied for a bank or credit union loan other than a mortgage 26.9% 72.9%Contributed to another retirement plan such as an IRA 14.2% 71.0%Often/always planned and set goals for financial future 48.5% 70.0%Refinanced a mortgage or home loan 4.8% 65.4%Purchased stocks, bonds, mutual funds apart from retirement accounts 23.8% 54.5%Developed a financial recordkeeping system 39.5% 54.2%Created a legal financial will and/or estate plan 4.1% 34.8%

20

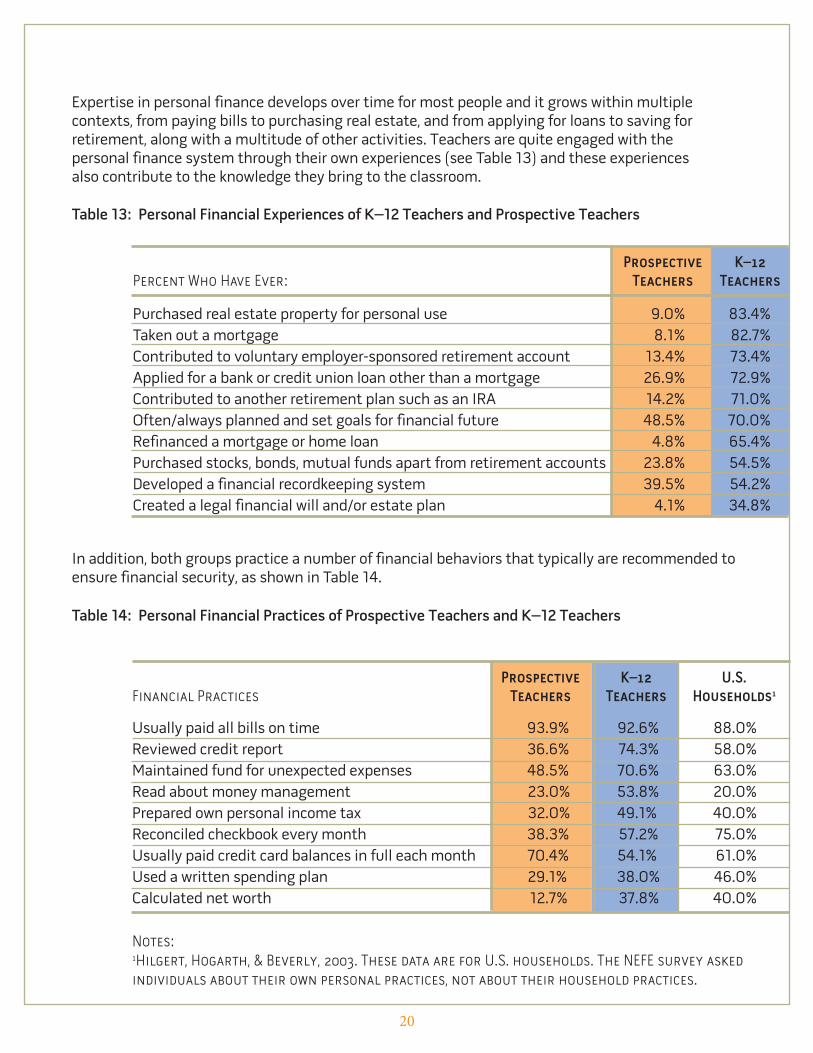

Expertise in personal finance develops over time for most people and it grows within multiplecontexts, from paying bills to purchasing real estate, and from applying for loans to saving forretirement, along with a multitude of other activities. Teachers are quite engaged with thepersonal finance system through their own experiences (see Table 13) and these experiencesalso contribute to the knowledge they bring to the classroom.

Table 13: Personal Financial Experiences of K–12 Teachers and Prospective Teachers

In addition, both groups practice a number of financial behaviors that typically are recommended toensure financial security, as shown in Table 14.

Table 14: Personal Financial Practices of Prospective Teachers and K–12 Teachers

Prospective K–12 U.S.Financial Practices Teachers Teachers Households1

Usually paid all bills on time 93.9% 92.6% 88.0%Reviewed credit report 36.6% 74.3% 58.0%Maintained fund for unexpected expenses 48.5% 70.6% 63.0%Read about money management 23.0% 53.8% 20.0%Prepared own personal income tax 32.0% 49.1% 40.0%Reconciled checkbook every month 38.3% 57.2% 75.0%Usually paid credit card balances in full each month 70.4% 54.1% 61.0%Used a written spending plan 29.1% 38.0% 46.0%Calculated net worth 12.7% 37.8% 40.0%

Notes:1Hilgert, Hogarth, & Beverly, 2003. These data are for U.S. households. The NEFE survey askedindividuals about their own personal practices, not about their household practices.

21

When asked about their top financial concerns, K–12 teachers and prospective teachers reported anumber of similar concerns. K–12 teachers’ top financial concerns were having enough money forretirement and other concerns about income adequacy and making wise investment choices:

• Knowing whether I will have enough money for retirement: 48.9 percent

• Determining ways to supplement my income as teacher: 40.8 percent

• Paying for my children’s college/university education: 39.4 percent

• Whether I am using the best strategies for investing my money: 38.0 percent

• Whether I am taking advantage of all of the tax laws that benefit me: 35.6 percent

• Not having sufficient income to meet my needs: 33.8 percent

Financial concerns for prospective teachers were:

• Determining ways to supplement my income as a teacher: 59.3 percent

• Not having sufficient income to meet my needs: 56.8% percent

• Having funds to buy a home or meet my mortgage payments: 54.4 percent

• Paying off my college/university loans: 53.6 percent

• Covering the cost of my continuing education requirements: 46.6 percent

• Whether I am using the best strategies for investing my money: 46.4 percent

• Knowing whether I will have enough money for retirement: 44.1 percent

K–12 and prospectiveteachers practice anumber of financial behaviorsthat typically help ensurefinancial security.

22

Financial concerns were more similar than different among teachers and prospective teachers,although some background characteristics such as age, marital status, gender, and race areimportant predictors of some specific concerns, such as paying for children’s education versuspaying off personal college loans. Uough the median age of teachers was 43 and the median age ofprospective teachers was 23, both teachers (48.9 percent) and prospective teachers (44.1 percent)reported similar concerns about having enough money for retirement. (By contrast, according to anABC News/Washington Post Poll on Feb. 19–22, 2009, of 1,001 adults nationwide, the number ofU.S. households concerned about having enough money for retirement exceeds 60 percent.)

Ue Road Ahead

As this study shows, there is a great need to expand educational opportunities in personal financefor teachers and prospective teachers in order to meet both their personal and professional needs.Ue researchers’ suggestions for expanded educational opportunities include:

Teachers’ Personal Financial Needs

Focused personal financial programs related to investment education. Having enough money forretirement was one of the chief financial concerns for K–12 teachers. Uey also were concernedwith related issues about investment strategies, supplementing their income, and paying fortheir children’s education. Prospective teachers’ top concerns were related to income adequacy(supplementing their income, not having sufficient income to meet their needs, having funds tobuy a home or meet mortgage payments, paying off college loans, etc.). While prospective teachers(median age 23) were on average far younger than K–12 teachers (median age 43), prospectiveteachers also were concerned about having enough money for retirement. Uese widespreadconcerns about income adequacy and retirement needs suggest that teachers and prospectiveteachers would benefit from programs focused on investment education.

Focused attention to financial planning for prospective teachers within the context of careerdevelopment. Helping future teachers explore career paths in education—and helping them pursuethose options—could enable prospective teachers to better pursue career and financial goals whilealso meeting state and school district continuing education requirements. Financial planningeducation for prospective teachers likely would be most effective if it focused on teachers’ specialcareer and financial circumstances and how they are related. Issues that add relevance to financialplanning instruction for this group include the typical nine-month employment schedules, districtand state continuing education requirements, options for covering costs of further education,career pathway/pay relationships and opportunities, and unique investment options for teachers.

23

Teachers’ Professional Education Needs

More learning opportunities in both financial education subject matter and pedagogy.All respondents (K–12 teachers, prospective teachers, and education faculty) reported feeling notwell qualified to teach most of the financial topics surveyed. A top priority of respondents issubject matter help in the topics of risk management and insurance, saving and investment,financial responsibility and decision making, and credit and debt. Ue survey showed that K–12teachers and prospective teachers are acquiring very little formal education in personal finance,either through credit-based courses or non-credit offerings. Since having formal education relatedto personal finance is a significant predictor of teachers’ own perceived competence to teachpersonal finance topics, teachers lack of education in this area is significant. In addition, only a fewteachers and a handful of prospective teachers had taken any formal course work in educationalmethods for teaching financial education. Given the increasing responsibility placed on individualsfor their own financial health, and the increasing diversity of the U.S. population, teachers withexpertise in both the content and pedagogy of financial education are critically needed.

Additional training for prospective teachers in teacher education programs. Education faculty mayneed to be made more aware of the importance of integrating this subject matter into the teachereducation curriculum. Education faculty felt no more competent to teach specific financial conceptsthan did K–12 teachers, and they were not more familiar with state financial education standards.

Help with how to use standards.While 80 percent of states now have standards or guidelines forfinancial education in their schools, a majority of K–12 teachers, prospective teachers, and educationfaculty reported feeling not well qualified to use those standards. In fact, 15 to 28 percent are notfamiliar with the standards. Uis suggests that much work needs to be done to ensure that thesestandards are incorporated into the curriculum for prospective teachers and that K–12 teachersget the training they need to use the standards.

Help with integration of financial concepts throughout multiple disciplines, beyond just vocational/technical education, social studies, and math.Most of the financial education currently taughtis through integrated—rather than stand-alone—curricula. Significant variations exist in teachers’perceived expertise in teaching personal finance based upon what they are teaching even at thetime of this study. In-service education organized around homogeneous teaching specialty groupsor tailored to include disciplinary-specific curricula and instruction examples within heterogeneousin-service groupings may be effective in expanding financial education beyond the areas where ittraditionally has been taught.

Help with understanding the developmental nature of financial reasoning, and learning how tomake financial concepts accessible at different ages, including the lower grade levels. Becausea majority of teachers see financial education as a subject that is appropriate primarily for highergrades, most teachers would benefit from learning more about the developmental nature offinancial reasoning, and from learning how to make financial concepts accessible at differentgrade levels. And given that few K–12 teachers or education faculty have taken financial educationmethods courses or workshops, and that much of their content-focused financial education hastaken place primarily through their own financial experience (which would be complex and adultfocused), it is likely that prospective teachers have not been exposed to the concept of personalfinancial education as a developmental process or to developmentally appropriate curricula andteaching/learning resources.

24

AcknowledgmentsUe National Endowment for Financial Education gratefully acknowledges the significantcontribution to the field of financial education research made by the study team of Wendy Way,Ph.D., and Karen Holden, Ph.D. Ueir thorough literature review, and collection and analysis of data,combined with their thoughtful presentation of teachers’ capabilities, attitudes, and interests inthe context of teachers’ own personal financial concerns presents a well-rounded perspective onthe current state and future prognosis for financial education in America’s K–12 classrooms.

Many other academic researchers, experts, and stakeholders also contributed to the significance ofthis project, including participating in its conception at a roundtable meeting at NEFE in April 2006,advising on the study while in process, and finally discussing the study’s implications at a Salonconducted at the University of Wisconsin campus in July 2009 where 15 priorities for establishingeffective financial education classrooms were identified. We gratefully acknowledge the followingindividuals who participated in one or more of the efforts that went into producing the study andthis report:

• Cheryl Achterberg, Dean, College of Human Sciences, Iowa State University (now Dean, College ofEducation and Human Ecology, Ohio State University)

• Diana Borth, Family and Consumer Education Teacher, Badger Ridge Middle School,Verona, Wisconsin

• Peter Chandler, Associate Director of Investor Education, FINRA

• Virginia Clark Johnson, Dean, College of Human Development & Education, North DakotaState University

• J. Michael Collins, Assistant Professor, Consumer Science, University of Wisconsin-Madison

• Donna Cooner, Director of Teacher Education, Colorado State University

• Warren Crown, Associate Dean of Academic Affairs, Graduate School of Education,Rutgers University

• Tim Davies, Interim Director, School of Education, Colorado State University

• Kathleen deMarrais, Associate Dean for Academic Programs, University of Georgia

• Robin Douthitt, Dean, School of Human Ecology, University of Wisconsin-Madison

• Jacqueline Edmondson, Associate Dean for Teacher Education and Undergraduate Programs,College of Education, Pennsylvania State University

• Cheryl Fedje, Professor Emerita, University of Wisconsin-Stevens Point and Family andConsumer Education Senior Lecturer, University of Wisconsin-Madison

• Michael Gutter, Assistant Professor and Financial Management State Specialist for theDepartment of Family, Youth, and Community Sciences, in the Institute for Food andAgricultural, University of Florida

• Philip Heckman, Director of Youth Programs, Credit Union National Association (CUNA)

25

• Karen Holden, Professor Emeritus of Public Affairs and Consumer Science, Faculty Affiliate,Institute for Research on Poverty, Center for the Demography and Health of Aging, Instituteon Aging, University of Wisconsin – Madison.

• Catherine Huddleston-Casas, Assistant Professor, Family and Consumer Sciences Universityof Nebraska-Lincoln

• Julie Johnson, Chair, Family and Consumer Sciences, University of Nebraska-Lincoln

• Marjorie Kostelnik, Dean, College of Education and Human Sciences, University ofNebraska-Lincoln

• David Mancl, Director of the Office of Financial Literacy, State of Wisconsin, Madison, Wisconsin

• April Mason, Dean, College of Applied Human Sciences, Colorado State University

• Christine Mayfield, Instructor, College of Education, California State University-Fullerton

• Uomas McGowan, Chair of Teacher Education, University of Nebraska-Lincoln

• Members of the NEFE Teacher Development Task Force, who provided feedback during theirDenver meeting in August 2008

• Collin O’Rourke, Graduate Student, University of Wisconsin-Madison

• Ann Perkins, Assistant Professor, College of Human Development & Education, North DakotaState University

• Jane Schuchardt, National Program Leader, National Institute of Food and Agriculture (NIFA),United States Department of Agriculture

• Bridget Skelly, Education Student, University of Wisconsin-Madison

• Daisy L. Stewart, Associate Director, School of Education, Virginia Polytechnic Institute andState University

• Patricia Swanson, Extension Family Specialist, Human Development and Family Studies,Iowa State University

• Lois Vitt, Director, Institute for Socio-Financial Studies, Charlottesville, Virginia

• Wendy Way, Associate Dean, School of Human Ecology, University of Wisconsin-Madison

• David Whaley, Dean, School of Education, Colorado State University (now Associate Dean forTeacher Education, Iowa State University)

26

Reference ListUe following references are cited in this summary of the “Teachers’ Background & Capacity toTeach Personal Finance” study’s research findings. A complete reference list is in the full reportat www.nefe.org/tntfinalreport.

Hilgert, M.A, Hogarth, J.M., & Beverly, S.G., 2003. Household financial management:Ue connection between knowledge and behavior. Federal Reserve Bulletin, 89, 309–322.

Jump$tart Coalition for Personal Financial Literacy, 2007. National standards in K–12 personalfinance education, %ird edition. Accessed 2/1/2009 at: http://www.jumpstart.org/guide.html.

National Endowment for Financial Education, 2007. High School Financial Planning Program.Accessed 2/2/2009 at: http://www.nefe.org/HighSchoolProgram/tabid/146/Default.aspx.

National Center for Education Statistics (NCES) (2007). Status of education in rural America.Table 3.7. Number and percentage distribution of public elementary and secondary schoolteachers, by locale and selected characteristics: 2002–2003. Washington, D.C.: NationalCenter for Education Statistics, U.S. Department of Education. Retrieved Feb. 2, 2009, fromhttp://nces.ed.gov/pubs2007/ruraled/tables/tabl3_7.asp.

National Center for Education Statistics (NCES) (2008). Digest of education statistics. Table 69.Selected characteristics of public school teachers: Selected years, spring 1961 through spring 2001.Washington, D.C.: National Center for Education Statistics, U.S. Department of Education. RetrievedSept. 23, 2009, from http://nces.ed.gov/programs/digest/d08/tables/dt08_069.asp.

27

Top 15 Research Priorities for EstablishingEffective Financial Education inPreK–12 ClassroomsOn July 16, 2009, on the University of Wisconsin- Madison campus, NEFE convened a group ofparticipants representative of key stakeholders, including teacher education students, PreK–12teachers, education faculty, funders, and researchers, along with the research team and the study’sadvisors to discuss the project findings and its implications.Ee group developed the following Top 15Research Priorities:

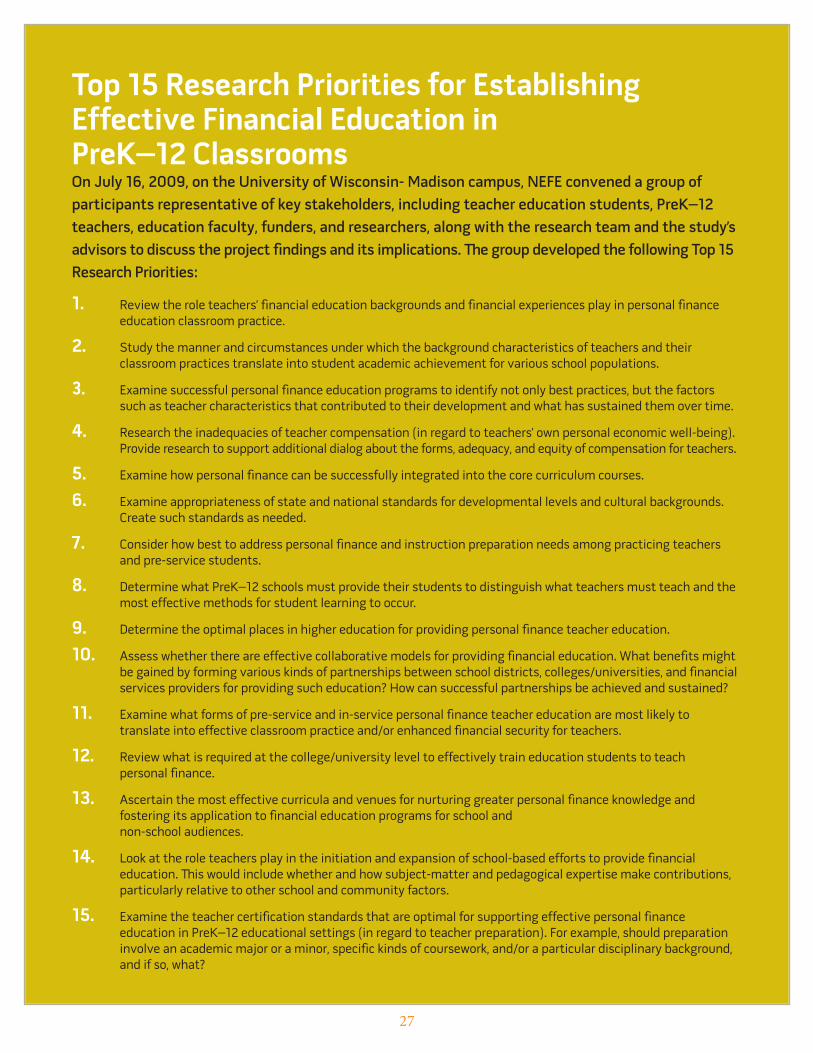

1. Review the role teachers’ financial education backgrounds and financial experiences play in personal financeeducation classroom practice.

2. Study the manner and circumstances under which the background characteristics of teachers and theirclassroom practices translate into student academic achievement for various school populations.

3. Examine successful personal finance education programs to identify not only best practices, but the factorssuch as teacher characteristics that contributed to their development and what has sustained them over time.

4. Research the inadequacies of teacher compensation (in regard to teachers’ own personal economic well-being).Provide research to support additional dialog about the forms, adequacy, and equity of compensation for teachers.

5. Examine how personal finance can be successfully integrated into the core curriculum courses.

6. Examine appropriateness of state and national standards for developmental levels and cultural backgrounds.Create such standards as needed.

7. Consider how best to address personal finance and instruction preparation needs among practicing teachersand pre-service students.

8. Determine what PreK–12 schools must provide their students to distinguish what teachers must teach and themost effective methods for student learning to occur.

9. Determine the optimal places in higher education for providing personal finance teacher education.

10. Assess whether there are effective collaborative models for providing financial education. What benefits mightbe gained by forming various kinds of partnerships between school districts, colleges/universities, and financialservices providers for providing such education? How can successful partnerships be achieved and sustained?

11. Examine what forms of pre-service and in-service personal finance teacher education are most likely totranslate into effective classroom practice and/or enhanced financial security for teachers.

12. Review what is required at the college/university level to effectively train education students to teachpersonal finance.

13. Ascertain the most effective curricula and venues for nurturing greater personal finance knowledge andfostering its application to financial education programs for school andnon-school audiences.

14. Look at the role teachers play in the initiation and expansion of school-based efforts to provide financialeducation. Uis would include whether and how subject-matter and pedagogical expertise make contributions,particularly relative to other school and community factors.

15. Examine the teacher certification standards that are optimal for supporting effective personal financeeducation in PreK–12 educational settings (in regard to teacher preparation). For example, should preparationinvolve an academic major or a minor, specific kinds of coursework, and/or a particular disciplinary background,and if so, what?

Ue full report is available at www.nefe.org/tntfinalreport.

![[Teach the Teachers]20101006 Stress relief_ppt](https://img.pdfslide.net/doc/110x75/55535e4bb4c905031f8b4a53/teach-the-teachers20101006-stress-reliefppt.jpg)