Embed Size (px)

Citation preview

Page | 1

‘The influence of CEO power on CEO compensation’

Master’s thesis

Executive Programme in Management Studies – Strategy Track

Author: Marjolein Kennedy

Student number: 10733426

Date of submission: 30-06-2016

Final version

Supervisor: Dr. Daniel Wäger

Page | 2

Statement of Originality

This document is written by Student Marjolein Kennedy who declares to take full

responsibility for the contents of this document.

I declare that the text and the work presented in this document is original and that no

sources other than those mentioned in the text and its references have been used in

creating it.

The Faculty of Economics and Business is responsible solely for the supervision of

completion of the work, not for the contents.

Page | 3

Table of contents Abstract ........................................................................................................................................................ 5

Introduction ................................................................................................................................................. 6

Literature review ........................................................................................................................................ 9

CEO power and compensation .............................................................................................................. 9

Duality ................................................................................................................................................ 11

Board independence .......................................................................................................................... 12

Tenure ................................................................................................................................................ 12

CEO gender ........................................................................................................................................... 14

Country income inequality ................................................................................................................... 17

Data and method ....................................................................................................................................... 20

CEO compensation ............................................................................................................................... 21

Duality .................................................................................................................................................... 22

Tenure .................................................................................................................................................... 22

Board independence .............................................................................................................................. 22

CEO Gender .......................................................................................................................................... 23

GINI Index ............................................................................................................................................. 23

Control variables ................................................................................................................................... 24

Results ........................................................................................................................................................ 26

Findings for duality ............................................................................................................................... 34

Findings for tenure ............................................................................................................................... 34

Findings for board independence ........................................................................................................ 35

Findings for CEO gender ..................................................................................................................... 35

Findings for country inequality / GINI index ..................................................................................... 36

Other findings........................................................................................................................................ 36

Discussion .................................................................................................................................................. 38

Conclusions and suggestions for further research ................................................................................. 40

References .................................................................................................................................................. 42

Page | 4

Table of contents for tables and figures

Figure 1 Conceptual model……………………………………….…………………………....16

Table 1 Descriptive statistics for continuous variables…………………………………........23

Table 2 Descriptive statistics for categorical variables……………………………………....24

Table 3 Correlation matrix…………………………………………………………………….26

Table 4 Multiple regression results for independent variable duality………………………28

Table 5 Multiple regression results for independent variable tenure…………………….…29

Table 6 Multiple regression results for independent variable board independence...……..30

Page | 5

Abstract

CEO compensation is a topic that has gained an increased interest in the last few decades from

researchers in the field of governance, business ethics, psychology, and (behavioral) economics.

Researchers have looked into myriad of determinants of CEO compensation, of which one is

CEO power. CEO power is a multidimensional construct which measures the amount of

influence or power a CEO has, with regard to managerial discretion or persuasion of the board

for example. This concept is used as the independent variable in this study, and is divided into

three underlying variables; duality, tenure and board independence, in order to provide an

adequate measure for this multidimensional construct. This paper empirically tests to what extent

CEO power has an impact on CEO compensation, and furthermore looks at the moderating effect

of (in)equality associated with gender and with geographical location of the firms. Results from

the regression analyses show that CEO power has a very small effect on CEO compensation.

Gender does not seem to have any moderating effect, however country income equality

moderates the relationship between CEO power and CEO compensation for the variable of

duality. Regardless of the lack of support for the hypotheses as proposed in this paper, multiple

interesting findings are presented and suggestions for further research are provided at the end of

this paper.

Page | 6

Introduction

CEO compensation has been a topic of interest for several decades, and is often connected to

income inequality. Income inequality has increased greatly over the last decades and has come to

reach almost historic heights (Alvaredo, Atkinson, Piketty, & Saez, 2013, cf: Wernicke,

forthcoming). The income-related gap in society has recently become a more popular topic of

interest and has been the catalyst for protests against for example ‘the 1%’, referencing the 1% of

population that is extremely rich and continues to grow even richer as we speak. CEO

compensation in particular has not been shied away from in the media either, such as the Enron

scandal of 2001 or that of HP in 2010 to name but a few stories that were covered in great detail

in the media. Every year, new articles pop up describing yet another outrageous CEO pay

increase in time of crisis, or an exorbitant golden parachute rewarded to a CEO who has failed,

naturally often causing enragement of the public.

Not only is CEO compensation the source of often heated public debates on the ethics of

unwarranted remuneration packages and golden parachutes, but it has also attracted researchers

in governance, business ethics and firm performance alike, trying to figure out what factors

influence CEO compensation and under what circumstances these factors might be of more

significance (Belliveau et al., 1996; Brick et al., 2006; Cordeiro et al., 2003; Hill et al., 1991;

Johnston, 2002; Mohan et al., 2003; Sauerwald et al., 2014).

Much of the extant literature has predominantly had a focus on the combination of CEO

compensation and firm performance; trying to answer the question of whether higher

compensation is equal to higher performance (Adams et al., 2005; Brick et al., 2006; Hambrick,

2007). Through years of research, the answers to this question have been diverse and opinions

seem to remain mixed. More in the background has been the research on what ought to be, in my

Page | 7

opinion, researched first to try to understand CEO compensation; namely, what actually

constitutes CEO compensation, which attributes of CEOs themselves influence CEO

compensation and under what circumstances they do so more or less strongly? This paper aims

to add to this growing body of literature and studies the influence of CEO power, by trying to

answer the research question: ‘to what extent does CEO power have an impact on CEO

compensation?’.

There has also been an increasing interest in gender equality in the realm of

compensation. It is commonly known that the average wage of females is lower than their male

counterparts in comparable job positions. Females are often assumed to be other-regarding, and

to hold fairness into higher regard than males (Eagly & Wood, 1999). As stipulated by Hambrick

and Mason’s upper echelons theory, personal characteristics can be a proxy for managerial

characteristics influence strategic choice and decision-making (Hambrick & Mason, 1984). I

therefore believe it would be interesting to see whether gender has a moderating effect when

looking at the relationship between CEO power and CEO compensation. It would be insightful if

there is data available indicating a similar level of CEO power, however with a different impact

on executive compensation due to gender. This paper is unique in this sense, because gender and

equality in respect to compensation are certainly research areas which are understudied.

Especially matching CEO power with CEO gender and the underlying assumption of equality is

a topic that is novel and thus a valuable add-on to existing literature.

Another large influence of equality can be sought in culture; certain cultures value

fairness and equality more than others. In order to dig deeper into the role that regard for equality

plays in rewarding CEOs, the moderating role of equality per geographical region is also

researched in this paper. Both moderators are based on the same idea, namely that the influence

Page | 8

of CEO power should be lower when there is a higher concern for equality within a firm. I thus

theorize that the aversion to inequality is higher in firms led by female CEOs or in firms

headquartered in countries with low income inequality.

Both gender and geographical region with regard to equality in CEO compensation are

understudied research areas. This paper will thus create new insights and open up avenues for

future research.

The dataset used in this paper include the 500 companies as specified in the Financial

Times Global 500. The use of this specific global dataset creates a novel viewpoint, as most

extant literature limits itself to the North American market.

In the first part of this paper, a concise literature review including the proposed

hypotheses is presented. In the second part, the empirical research is presented by further

reviewing the dataset, variables, and study design, followed by the empirical results. Finally,

conclusions are offered and suggestions for future research are given.

Page | 9

Literature review

Executive compensation has been a topic of research interest for a very long time, and hundreds

of empirical studies have been done to define the key determinants of CEO compensation,

however mostly with mixed outcomes (Finkelstein & Boyd, 1998). Starting from an economics-

based viewpoint, the research has started shifting to a more social, political, and strategic focus

(Baker, Jensen & Murphy, 1988; cf. Finkelstein & Boyd, 1998).

CEO power and compensation

Agency theory has been, and still is, the main argument in explaining CEO compensation; the

conflict of interest between shareholders and the CEO is a perfect example of an agent-principal

problem. In light of self-interest, shareholders are assumed to want maximized stock returns,

where the CEO would want maximized private returns. Their demands clash, and according to

agency theory, only a monitor can solve this problem (Alchian & Demsetz, 1972). Yet still, a

monitoring board does not necessarily solve the problem. As has been shown in extant literature,

there are mixed empirical findings on the actual impact of the board and their monitoring, and it

has been suggested there are other contingencies that determine CEO compensation (Brick et al.,

2006; Ryan et al., 2004; Sauerwald et al., 2014).

Williamson’s model of managerial discretion (1964) is the forerunner of the principal-

agent problem (which was developed in the 70s) and laid the foundation theory for the self-

interested manager whose aim it is not to maximize company profit but their own utility. Agency

theory however does not account for differences between individuals. As stipulated by Alvesson

(2004), agency theory certainly has a few drawbacks, but most importantly he criticizes the

either/or situation in agency theory, there is always only one contract in agency theory. Instead,

Alvesson argues that there is always a combination of controls at the same time. This notion can

Page | 10

also be applied to CEO compensation; it is fair to say that there is a principal-agent relationship

between shareholders and the CEO, however this is likely not to be the only determinant of the

level of compensation. What about other situational, geographical, or social factors? Behavioral

economists have been moving away from the idea that everyone is self-interested, giving leeway

to new theories.

Sauerwald et al. (2014) do a very good job in explaining the power that a CEO could

have over a board in their article on board social capital and excess CEO returns, using a well

thought out theory cross-over from agency theory and social capital theory. They argue that

boards have to comply with normative pressures from both their external and internal social

networks. These normative pressures however, may not always be in the best interest of the

shareholders. Powerful CEOs may enhance or constrain these normative pressures, as they

influence the director selection process, so they may magnify certain norms favoring excess CEO

returns. Powerful CEOs may thus alter normative pressures to follow managerial preferences and

go against the shareholder’s interest, because CEOs have the power to refuse to recommend

board directors to other firms and to ensure that they will not easily be hired somewhere else

(Sauerwald et al., 2014).

Wernicke (forthcoming) borrows from social comparison theory to argue why inequality

has grown, CEOs look at the pay of peers and take that as the norm, this creates a vicious cycle

of increasing pay. The information era we live in further allows this comparison, according to

Wernicke as executive compensation information is often easily accessible. Wernicke attempts to

look at the true social factors that influence executive pay (inequality), however social

comparison theory fails to answer the question why social forces do not have the power to curb

Page | 11

excessive pay inequality. Rationally, you would argue that the influence of social force should be

much larger as information is quite readily available to anyone (Wernicke, forthcoming).

CEO power will be measured in this paper by a combination of proxies, as is typical in

the large stream of extant research (Coles, Daniel, and Naveen, 2008; Haynes and Hillman,

2010; Zhang and Rajagopalan, 2003; cf. Sauerwald et al., 2014). The measures for CEO power

that I will use in my paper are the following, CEO tenure, CEO duality, the number of board

members the CEO has appointed. These measures are among the most widely used and studied

proxies to measure CEO power (Zhang and Rajagopalan, 2003). CEO power has been used as a

control variable or a mediator role in past research (Sauerwald, 2014), in this paper however it

will be the main topic of the research question in this paper: ‘To what extent does CEO power

have an impact on executive compensation?’.

Duality

As Boyd (1995) mentions, duality offers direction of a single leader. As you might expect, this

comes with advantages and disadvantages. What is however incontestable, is that with duality

also a certain sense of power is created. Whereas a CEO may be overruled by the board in a

situation where the CEO does not simultaneously chair the board, this can become a problem

when the CEO does carry out this tandem job. The chair of a board naturally has the right to

veto, thus this could imply great impact. Furthermore, the argument that has been carried

forward by Sauerwald et al. (2014) that a CEO may hire board members which creates CEO

power, is even more magnified when the CEO is simultaneously chair of the board. As is further

stipulated by Finkelstein et al. (1994) CEO duality furthers entrenchment, and thus diminishes

board monitoring effectiveness.

Based on these arguments, I propose hypothesis 1a.

Page | 12

H1a: CEO compensation is higher for firms, in which the CEO is also chairman of the board of

directors.

Board independence

Ryan & Wiggins (2004) note that it is generally accepted that a more independent board is better

for corporate governance, and independent boards are more willing to monitor the CEO

(Hermalin & Weisbach, 1998). Ryan & Wiggins pose that in situations with a higher degree of

board independence, the CEO has less of an influence on decisions with regard to board directors

to continue to serve on the board or to serve on another board. Independent board members are

less reliant on the CEO’s decision, and they even have a better bargaining position with the CEO

compared to insider board members (Ryan & Wiggins, 1998). It is thus fair to argue that when

the degree of board independence is lower, the CEO has more influence and consequently more

power. The degree of board independence is often set in company policy, however board

independence might also link to CEO tenure. As is further stipulated below, over the course of a

CEO’s tenure, a CEO may gain increasing power and is sometimes even able to circumvent the

system and the monitoring of the board. Over time, a CEO might personally appoint an

increasing amount of board members, which increases their power and weakens the board

monitoring. I thus propose hypothesis 1b.

H1b: The higher the number of board members the CEO has appointed, the higher her/his

compensation.

Tenure

Hill et al. (1991) look at the specific feature of tenure as a determinant of pay, and

provide several interesting findings. In their expectations, multiple sound reasons corroborated

by previous literature, are provided as to why tenure would increase a CEO’s power. A CEO

Page | 13

who has been in a position longer can appoint new board members throughout the years of tenure

(Finkelstein & Hambrick, 1989, cf: Hill et al. 1991). Secondly, as tenure increases, they can

learn to work the system and influence internal information flows, making it possible to withhold

information (Coughlan & Schmidt, 1985, cf: Hill et al. 1991) or to even change the board agenda

and to cast themselves in the most favorable light. These reasons combined, make for tenure to

be an often-used proxy to determine the power a CEO has over their board, and thus over their

compensation packages. According to Hill et al. (1991), agency theory enforces a link between

pay and stock returns to satisfy shareholders. They find in their research that this relationship

between CEO pay and stock returns weakens with tenure, providing evidence that tenure indeed

influences CEO power in the sense that a CEO could over time circumvent the monitoring of the

board and strengthen their position with the shareholders (Hill et al., 1991). Johnston (2002)

finds further evidence that CEO compensation is linked to tenure, he however links the level of

pay to a reward for earlier successful performance reached in the CEO’s tenure with the

company. Results from Johnston’s 2005 research show that tenure is negatively related to the

awarding of share options and the total value of remuneration packages, however longer tenure is

associated with higher baseline salaries.

Based on the abovementioned arguments, I propose hypothesis 1c:

H1c: As a CEO’s tenure increases, their executive compensation also increases.

Another interesting addition from outside of the field of management, is that of Peterson

et al. (2003). They posit that a CEO’s personal characteristics influence the dynamics of the top

management team, which henceforth influences the firm’s performance. Peterson et al.’s article

provides a valuable addition to the implications that the upper echelons theory has for corporate

Page | 14

governance, as they point to the high influence a CEO’s personality may have on their followers

in the top management team. They suggest that the board of directors should play a larger role in

monitoring the climate of the top management team as created by the CEO. This is a fair

warning, but one that may be obsolete, or just too simple of a solution. As Hill et al. (1991)

rightfully point out, a CEO may be able to even circumvent the monitoring board of directors

through the use of information and by ‘playing the system’, by using their tenure as a source of

CEO power; a managerial characteristic.

As described, CEO power is widely researched, and can be considered a managerial

characteristic worth looking at in terms of compensation. CEO power is thus the key determinant

in this paper, which aims to answer the research question: ‘to what extent does CEO power have

an impact on CEO compensation?’.

Carpenter et al. (2004) further note that indirect effects may as well be observed with

regard to socially constructive, normative standards, suggesting that executive effects may in fact

reflect the firm’s and its management’s embeddedness in a broader institutional environment

(Carpenter et al., 2004: pg 29). Drawing on this conclusion, country (in)equality is introduced in

this paper as moderating variables. Furthermore, drawing on the upper echelons theory, CEO

gender is used as a moderating variable.

CEO gender

According to Croson & Gneezy (2004), the two main empirical results in the labor market that

signify a gender difference are 1) the gender gap, referring to the average wage gap between

males and females, and 2) wage discrimination, referring to lower wages for workers with

similar characteristics but different gender. Eagly and Wood (1999) delve deeper into the

behavioral differences between sexes and the reasons for these differences. In their article they

Page | 15

examine two theories; psychological disposition and social structure. Naturally, as men and

women hold different sex-specific evolved mechanisms, they tend to occupy different social

roles due to psychological differences. Social structure on the other hand argues the other way

around; because men and women occupy different social roles, they become psychologically

different so as to adjust to these roles (Eagly & Wood, 1991: pg 408). Important to note here, is

that the social structure is a structure created by mankind and boosted by societal and cultural

circumstances. Eagly and Wood (1999) further stipulate that the behavioral differences between

the sexes cannot be explained by a simple nature versus nurture, but instead we should think in a

more hybrid form of nature and nurture, as the importance of both factors cannot be negated by

the other. The archetypal family and economic roles of men and women, can even today still

largely be described as that of resource provider and homemaker. According to social structure

theory, men and women seek to accommodate to these roles in terms of psychological attributes

and social behavior, creating a distinction between agentic behavior, typically attributed to men,

and communal behavior, typically attributed to women (Eagly & Wood, 1999). Women, for

example, are expected to be more other-regarding and compassionate than men. In general,

women are more often associated, whether stereotypical or not, with personality traits including

trust, fairness, reciprocity, and altruism.

Gender differences with effect on wage have also been looked at from an economic point

of view, mostly through economic games. In Solnick’s 2001 article on gender differences in the

ultimatum game, she looks at different outcomes of different game set-ups and finds specific

differences between the sexes. Also Eckel and Grossman (2001) specifically look at gender as a

variable in the ultimatum game. They find differences between the sexes as well, based on their

findings they posit that women have different social norms regarding fairness and equality than

Page | 16

men do (Eckel & Grossman, 2001; cf. Solnick, 2001). Solnick (2001) adds to this notion of

fairness, by concluding that it is likely that female players are reluctant to reject an offer and

cause both players to gain nothing when the other player is visible, however when the impact is

less obvious female players mostly adhere to their wish of receiving their fair share.

Hambrick and Mason (1984) proposed that demographics of executives can be used as a

proxy to measure personal characteristics, which are very hard to measure. The key notions in

Hambrick and Mason’s theory are around the characteristics of executives or top management

teams, and their respective influence on decision-making within the firm. These characteristics

cover cognitions, values and norms, and perceptions of the person at stake (Hambrick & Mason

1984). According to Hambrick and Mason’s research, these characteristics influence the way in

which strategic decisions are made. As most determinants in their model are hard to measure

(such as cognitions and values), Hambrick and Mason rely on previous research on demography

and suggest that it is sufficient to measure managerial characteristics in order to get a view of

differences in cognition, perception and values (Carpenter et al., 2004). Specific demographic

characteristics such as age, education, tenure, etc. are used as proxies for psychological behavior

or constructs which shape your idea about the world and thus shape the strategic choices you

make (Carpenter et al., 2004).

Prior research has shown that Hambrick & Mason’s 1984 upper echelons theory can be

used very broadly and can be applied to multiple constructs, further linking it to firm

performance as opposed to strategic profiles, and also using it different firm contexts by

introducing new variables to the model (Carpenter et al., 2004). Their research has also provided

building blocks for further theory for the benefits of not only management, but also psychology

and mainstream economics (Carpenter et al., 2004). Recent interesting upper echelons research

Page | 17

in economics, finds valuable information to be used in management, however. Bertrand and

Schoar (2003) posit that top managers have a significant influence on how company resources,

such as investments, acquisitions, and other expenditures, are allocated. They find in their 2003

paper that manager fixed effects matter in decision-making, and moreover they propose several

patterns in managerial decision-making, explaining different managerial styles in similar

economic situations by attributing this to managerial (upper echelon) characteristics such as birth

cohort and educational experience. One of the interesting findings of Bertrand and Schoar’s 2003

paper with regard to compensation, is that manager fixed effects is related to manager

compensation levels, attributing this to management styles more prone to create value (initially

influenced by managerial upper echelon characteristics).

Following Hambrick & Mason’s Upper Echelons Theory (1984; 2007), executives'

experiences, values, and personalities influence their perceptions and interpretations, and thus

choices. I theorize that possibly due to certain character traits that are more commonly assigned

to women in the work field, such as a high regard of equality and fairness, there is a moderating

effect to be seen that weakens the direct effect of CEO power on CEO compensation. Thus,

‘female CEO’ is used as a moderating variable, and I suggest the following hypothesis:

H2: The relationship between CEO power and CEO compensation is moderated by the CEO

gender; when the CEO is female this direct relationship is weaker.

Country income inequality

Institutional theory was introduced in the late 1970s as a new field in organizational sociology.

The initial general argument within this theory was that formal organizational structure did not

just reflect technological imperatives and resource dependencies, but instead it reflected

institutional forces such as norms and values among other things (Scott, 2008). Over the last few

Page | 18

decades, institutional theory developed into a more well-defined and concrete theory.

Institutional theory states that institutions are forces on individuals and organizations, by creating

social pressures and setting the standard of what is considered acceptable and what is not. This

divide creates pressures, which have been divided into three pillars, namely normative, coercive,

and mimetic (DiMaggio & Powell, 1983). Income inequality could be placed in these social

pressures, and may become a social pressure through isomorphism. Firms often look to each

other for guidance, which might create a homogeneity based on a norm. Normative pressure

deals with social patterns and they become a pressure for organizations or individuals to comply

with norms or to act in a way that is regarded as normal or expected. This creation of a

homogeneity is referred to as isomorphism (Dimaggio & Powell, 1983).

Institutional theory does not only focus on individual organizations, but there is a large

sub-set of the literature focusing on the organizational field, which is characterized by a number

of organizations participating in the same cultural and social sub-system (Dimaggio & Powell,

1983). Organizations are key players in shaping the environment (Scott & Davis, 2007; cf. Scott,

2008), thus heavily influencing norms and values. One could argue that there is a vicious cycle

with organizations shaping the environment and the environment shaping organizations through

mimicking norms and values. What is however indisputable is that organizations and the

environment are closely related and thus influence each other heavily.

In this paper, I build on the institutional theory, and hypothesize that in countries where

there are higher levels of income equality, the CEO compensation will be lower even though the

CEO has considerable power. This will be tested through the following hypothesis:

H3: The relationship between CEO power and CEO compensation is weaker when there are

lower levels of inequality in the country where the firm is headquartered.

Page | 19

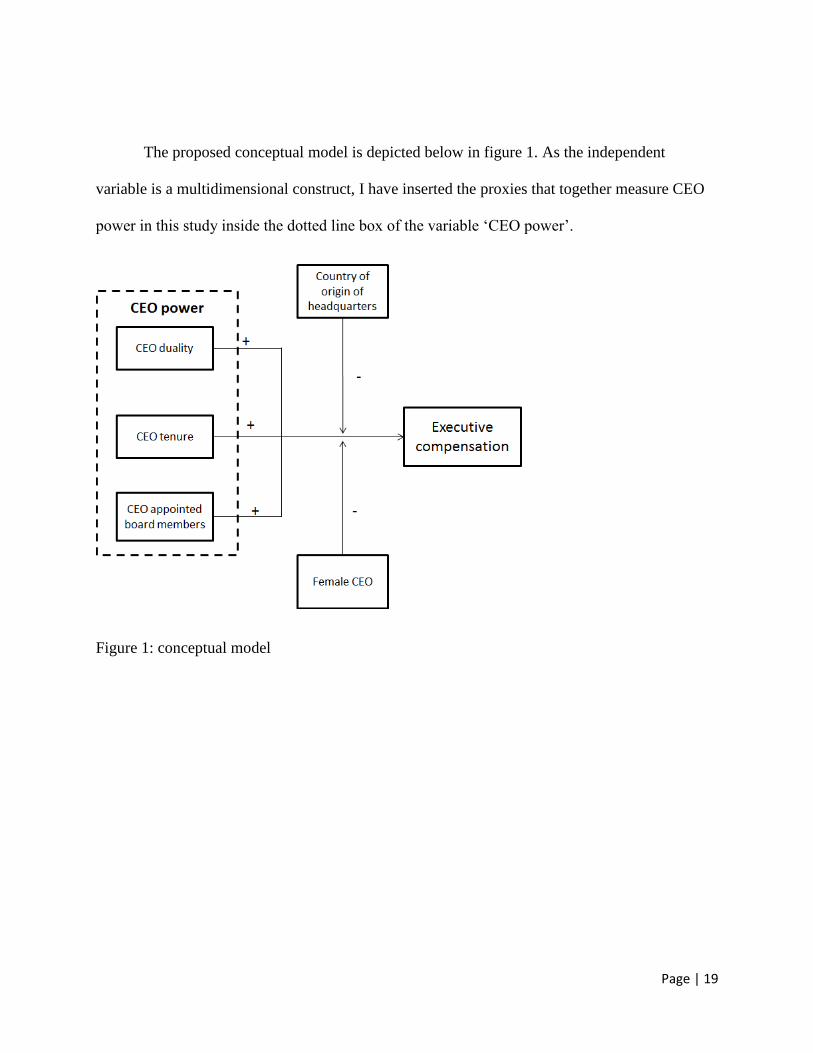

The proposed conceptual model is depicted below in figure 1. As the independent

variable is a multidimensional construct, I have inserted the proxies that together measure CEO

power in this study inside the dotted line box of the variable ‘CEO power’.

Figure 1: conceptual model

Page | 20

Data and method

As Sauerwald et al. (2014) point out, CEO power is a multidimensional construct, that is

typically measured through a combination of two or more individual measures. Following

existing research, I will measure commonly used features to measure CEO power, these are 1)

CEO tenure, 2) CEO duality, and 3) the amount of directors in the board that have been

appointed by the current CEO (in this paper, this variable is interchangeably named ‘board

independence’). These three variables all measure CEO power within the firm, as opposed to

other forces which could be an external boost to or constraint on CEO power (such as for

example media coverage).

For the independent variables (CEO power), and the moderating and control variables,

data from the year 2012 has been collected. For the dependent variable (CEO compensation) data

from the year 2013 has been collected. The data is limited to these years, in order to ensure that

the dependent variable indeed is the outcome of the independent variable, and furthermore this

will reflect the current environment.

Moreover, certain control variables will be added to the analysis in order to correct for

unwanted effects and to ensure validity. I will control only for the most salient factors such as

industry, geographical region (continent), and financial performance of the firm, and firm size.

The sample as used in this paper consists of the 500 companies which are included in the

Financial Times Global 500. This index provides an overview of the top 500 companies

worldwide, ranked on the value of their market capitalization. The market capitalization is

measured by multiplying the share price and number of shares issued, thus the greater the stock

market value of a firm, the higher it is listed. The main reason that the Financial Times Global

500 was used as a dataset, is because as the name already mentions it is global. Much, if not

Page | 21

most, of the extant research on CEO compensation focuses on North American companies only,

as this data is generally more easily retrievable due to legislation. However, to extend current

research it is of high value to look at this topic from a global angle versus isolated to one

geographical region. Having global data allows you to gain a valuable insight into possibly

replicating and extending earlier findings that only applied to North America for example.

Furthermore, it allows you to compare and contrast CEO compensation per geographical region,

providing a unique insight.

The hypotheses will be tested by running three hierarchical multiple regressions, one for

each independent variable. By running different regressions for the independent variables, it is

possible to gauge whether one or more proxies has a different effect than the others.

CEO compensation

Information on CEO compensation has been retrieved from the Thomson One Asset 4 database.

This database includes objective data on environmental, social, and governance information,

based upon myriad KPIs and datapoints. The variable used to measure the CEO compensation, is

described as ‘the value of the highest yearly remuneration package in dollars within the

company’, and is numerical. The data for CEO compensation has been collected for the year

2013, in order to be able to correctly measure the effect of the independent variables. CEO

compensation data was available for 326 out of the 500 Financial Times Global 500 companies.

This creates a large enough and representative sample in order to run the necessary statistical

tests.

Page | 22

Duality

Duality is used as one of the proxies to measure CEO power in this paper. Duality signifies the

‘double position’ a CEO can be in, by simultaneously being the CEO of a company and the

chairman of the board of that same company. Duality is considered a binary variable in this

paper, either CEO is also the chairman of the board, signified by a 1, or they are not, signified by

a 0. For statistical purposes, in order to be able to correctly run a regression test, the binary

variable is treated as a numerical variable.

Tenure

Tenure, the amount of years the CEO has been in their current position, is the second measure

used to gauge CEO power. This variable is numerical, and is measured by simply adding up the

years this person has been the CEO of the company he/she works for now. Data for this variable

is collected for the year 2012, and has been manually collected from company websites and

generic company index websites such as Bloomberg and Reuters. In the case a CEO was

appointed in the year 2012 itself, a tenure of 0 years was registered. The information of CEO

tenure has been collected for 431 CEOs, with years of service ranging from 0 years to a stunning

55 years. This wide range in tenure created some issues with skewedness in the data, which has

been dealt with accordingly as presented in the Results section of this paper.

Board independence

Board independence is the third variable that concludes the independent variables which are used

to measure CEO power within the firm. This variable stands for the amount of board members

that have been appointed by the current CEO. The data is collected from the Thomson One Asset

Page | 23

4 database, which reports the percentage of independent board members as reported by the

company.

CEO Gender

As a first moderating variable to possibly have effect on the relation between CEO power and

CEO compensation, CEO gender is measured. There has been some research on gender

differences in compensation (Adams et al., 2007; Mohan et al., 2003; Shin, 2012) but empirical

results seem mixed and have not developed a proven theoretical structure for this possible

difference. Gender has been chosen as a moderator in this paper, because there is theory

suggesting that women value fairness and equality more than men (Eagly & Wood, 1999). This

would suggest that females would accept a lower compensation than their male counterparts. For

the CEOs in the dataset, I verified whether this person is male or female. A male CEO is codified

as 0 in the sample, and a female CEO is codified as 1, creating another binary variable which is

treated as a numerical variable. After codifying the data, it can easily be said that male CEOs

dominate the sample by far, with 412 male CEOs against 18 female CEOs.

GINI Index

To continue in the realm of equality, I will assess whether the country where the headquarters is

based, could have a moderating effect on the relationship between CEO power and CEO

compensation. Geographical region is thus theorized to have a moderating impact on this

relationship.

The level of equality, is measured by using the GINI index. This index measures how the

distribution of income within a certain economy compares to a perfectly equal distribution. The

Page | 24

GINI Index on equality is a score ranging of 0 to 100, indicating the level of equality of salaries

among the whole workforce of that specific country, where 100 signifies perfect equality and a

score of 0 indicating perfect inequality. The GINI index is calculated by plotting the cumulative

percentages of total income received against the cumulative number of recipients on a Lorenz

curve, starting with the poorest individual or household

(http://data.worldbank.org/indicator/SI.POV.GINI). These plots provide a score ranging from 0

to 100, 0 representing perfect equality and 100 implying perfect inequality.

GINI index scores from the host countries of headquarters have been collected from the

year 2012, with the exception of the United States of America for which a GINI index score for

the year 2013 has been collected due to missing data for this country for the year of 2012.

Control variables

In order to correct for unwanted effects and to ensure validity, control variables are used. I will

control only for the most salient factors such as industry, geographical region (continent), firm

performance, and the firm size. Firm financial performance will be measure by Return on Assets

(ROA), which is the net income divided by total assets. Following extant research, total assets

seems to be most commonly used to measure firm size, as opposed to number of employees for

example.

Two of the control variables, industry and geographical region, are categorical, and were

therefore recoded into dummy variables. The geographical regions are divided into the six

continents: North America, South America, Europe, Africa, Asia, and Australia. North America

serves as the baseline group in this dummy variable, since it represents the majority of the

Page | 25

sample (N=166) for continent North America). Industry types have been classified according to

the Industry Classification Benchmark (ICB), as typified and maintained by FTSE International

Limited, and used at the majority of global stock markets. This index divides all industries in ten

overarching categories: financials, consumer goods, consumer services, basic materials,

healthcare, telecommunication, technology, oil & gas, and utilities. Financials serve as the

baseline group for this dummy variable, as it represents the majority of the sample (N = 64 for

industry financials)

Page | 26

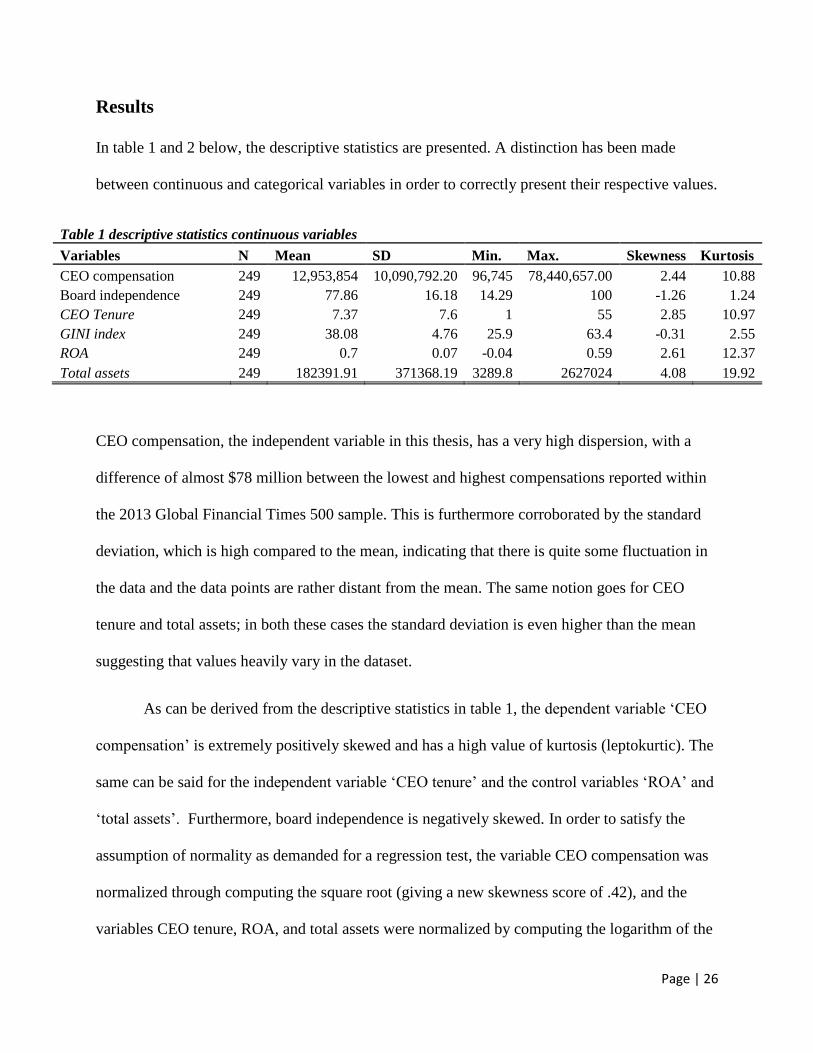

Results

In table 1 and 2 below, the descriptive statistics are presented. A distinction has been made

between continuous and categorical variables in order to correctly present their respective values.

Table 1 descriptive statistics continuous variables

Variables N Mean SD Min. Max. Skewness Kurtosis

CEO compensation 249 12,953,854 10,090,792.20 96,745 78,440,657.00 2.44 10.88

Board independence 249 77.86 16.18 14.29 100 -1.26 1.24

CEO Tenure 249 7.37 7.6 1 55 2.85 10.97

GINI index 249 38.08 4.76 25.9 63.4 -0.31 2.55

ROA 249 0.7 0.07 -0.04 0.59 2.61 12.37

Total assets 249 182391.91 371368.19 3289.8 2627024 4.08 19.92

CEO compensation, the independent variable in this thesis, has a very high dispersion, with a

difference of almost $78 million between the lowest and highest compensations reported within

the 2013 Global Financial Times 500 sample. This is furthermore corroborated by the standard

deviation, which is high compared to the mean, indicating that there is quite some fluctuation in

the data and the data points are rather distant from the mean. The same notion goes for CEO

tenure and total assets; in both these cases the standard deviation is even higher than the mean

suggesting that values heavily vary in the dataset.

As can be derived from the descriptive statistics in table 1, the dependent variable ‘CEO

compensation’ is extremely positively skewed and has a high value of kurtosis (leptokurtic). The

same can be said for the independent variable ‘CEO tenure’ and the control variables ‘ROA’ and

‘total assets’. Furthermore, board independence is negatively skewed. In order to satisfy the

assumption of normality as demanded for a regression test, the variable CEO compensation was

normalized through computing the square root (giving a new skewness score of .42), and the

variables CEO tenure, ROA, and total assets were normalized by computing the logarithm of the

Page | 27

respective values (giving new values of -.06, -.27, and .56 respectively). Board independence

was normalized by computing higher powers (giving a new value of -.75). After normalizing, the

skewness and kurtosis values were all reduced to acceptable numbers in order to continue with

the statistical tests.

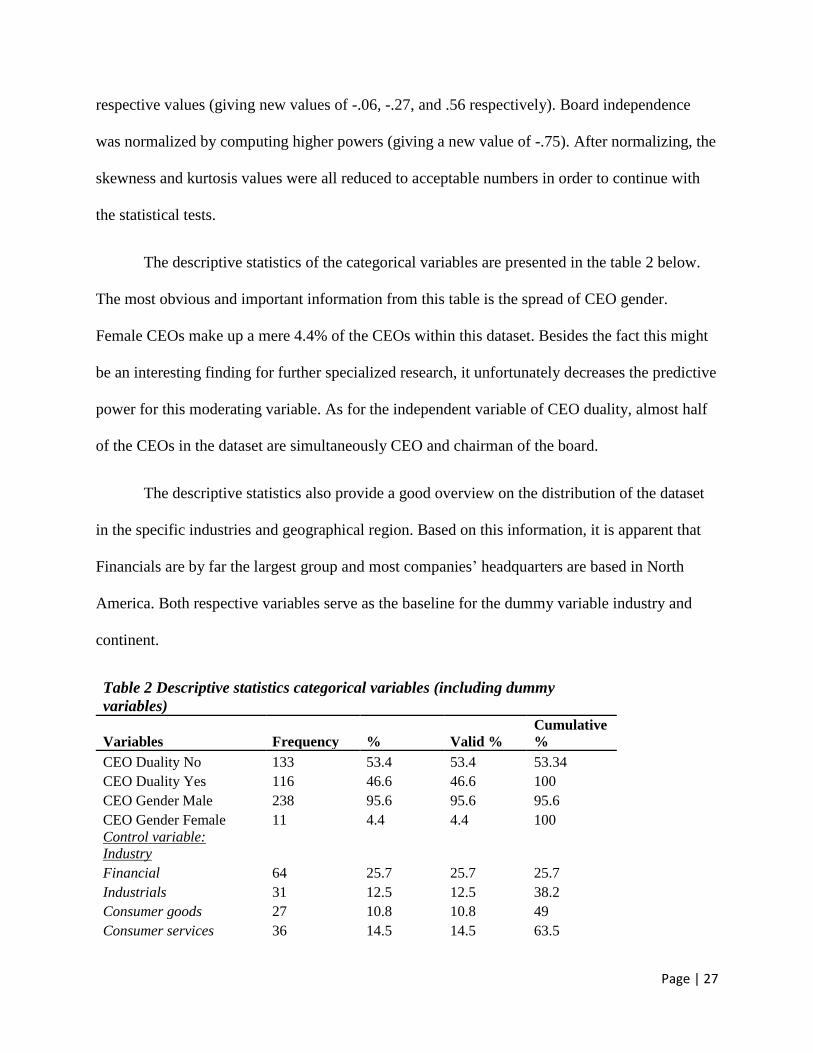

The descriptive statistics of the categorical variables are presented in the table 2 below.

The most obvious and important information from this table is the spread of CEO gender.

Female CEOs make up a mere 4.4% of the CEOs within this dataset. Besides the fact this might

be an interesting finding for further specialized research, it unfortunately decreases the predictive

power for this moderating variable. As for the independent variable of CEO duality, almost half

of the CEOs in the dataset are simultaneously CEO and chairman of the board.

The descriptive statistics also provide a good overview on the distribution of the dataset

in the specific industries and geographical region. Based on this information, it is apparent that

Financials are by far the largest group and most companies’ headquarters are based in North

America. Both respective variables serve as the baseline for the dummy variable industry and

continent.

Table 2 Descriptive statistics categorical variables (including dummy

variables)

Variables Frequency % Valid %

Cumulative

%

CEO Duality No 133 53.4 53.4 53.34

CEO Duality Yes 116 46.6 46.6 100

CEO Gender Male 238 95.6 95.6 95.6

CEO Gender Female 11 4.4 4.4 100

Control variable:

Industry

Financial 64 25.7 25.7 25.7

Industrials 31 12.5 12.5 38.2

Consumer goods 27 10.8 10.8 49

Consumer services 36 14.5 14.5 63.5

Page | 28

Basic materials 11 4.4 4.4 67.9

Technology 19 7.6 7.6 75.5

Oil & gas 21 8.4 8.4 83.9

Healthcare 24 9.7 9.7 93.6

Utilities 5 2 2 95.6

Telecommunications 11 4.4 4.4 100

Control variable:

continent

Africa 1 0.4 0.4 0.4

Asia 19 7.6 7.6 8

Australia 9 3.6 3.6 11.6

Europe 54 21.7 21.7 33.3

South America 0 0 0 33.3

North America 166 66.7 66.7 100

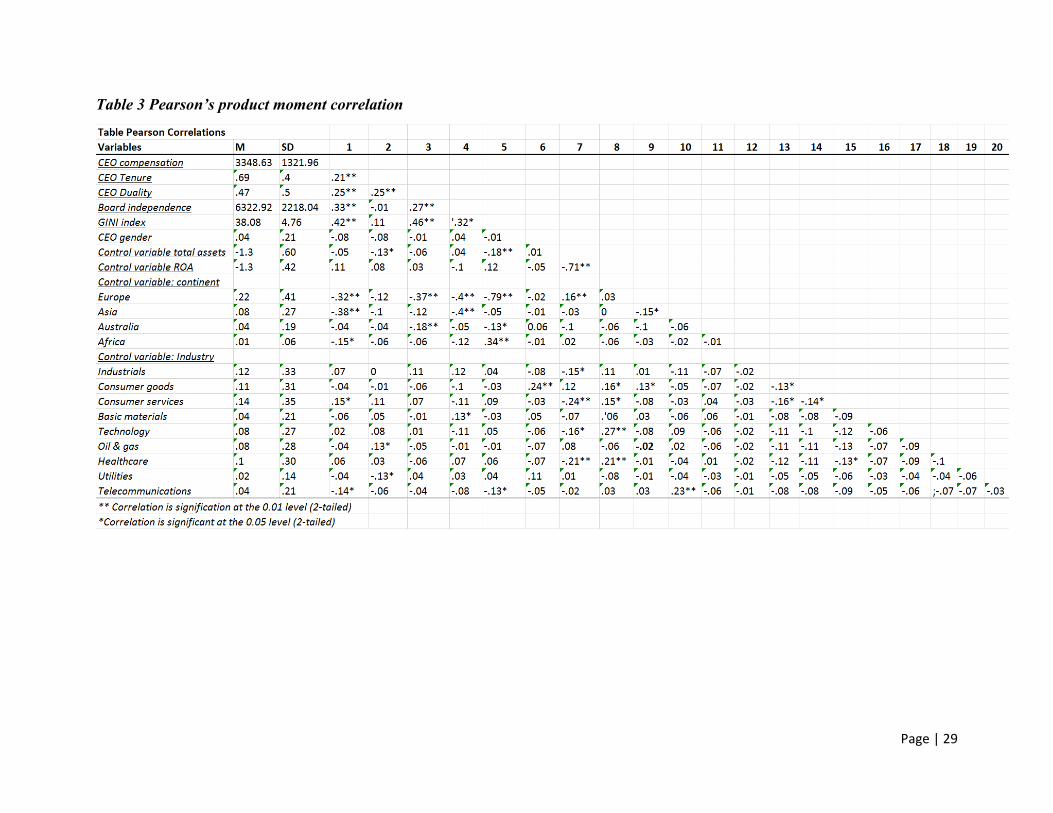

In order to quantify the strength of the linear relationship between the variables, a

Pearson’s product moment correlation was performed, using the transformed variables. The

results of this correlation analysis can be found below in table 3. As can be seen in the output

table the linear relation between the independent variables CEO duality, tenure and board

independence were all three statistically significant, however only indicating a weak to moderate

positive correlation to the dependent variable CEO compensation. The moderating variable of

gender is not statistically significant, and thus this correlation score may be disregarded as

potentially caused by mere chance. The second moderating variable GINI index, shows to have

the highest positive correlation among all variables to CEO compensation, albeit still a moderate

correlation.

Page | 29

Table 3 Pearson’s product moment correlation

Page | 30

As a Pearson’s product moment correlation merely tests the strength of a linear

relationship between variables, a multiple regression was performed in order to better assess the

strength of the relationship between the variables and to see which predictors add most variance

to the model.

Tables 4, 5 and 6 report standardized beta values and standard errors of the multiple

regression, furthermore at the bottom line of the table in the notes, the R2 and R2 change is

included for each model. Four steps have been run in this hierarchical multiple regression,

consistently adding a new variable to each step in order to gain an overall insight into the

specific effects of individual variables and their contribution to the model as a whole, and to

understand the relationship between the independent variable and the dependent variable and

their potential moderators. In the first step only control variables have been included in the

regression in order to account for any fixed effects caused by auxiliary variables. In the second

step, in the second column of the table, the independent variable has been added to the model.

Thirdly, the first moderating variable CEO gender and the interaction term for the independent

variable times CEO gender has been added to the model, and finally the second moderator

geographical region/GINI index value and its correspondent interaction term has been added to

complete the model and its constituent variables. Overall, I find that only tenure of the

independent variables that constitute CEO power altogether is statistically significant in

explaining the variance in CEO compensation, albeit with a low β value. Similar results are

found for the moderator CEO gender, implying no difference has been found between

compensation for male and female CEOs. The second moderator of country inequality does show

some significant findings. In the paragraphs below, the results and their implications for each

multiple regression is considered in further detail.

Page | 31

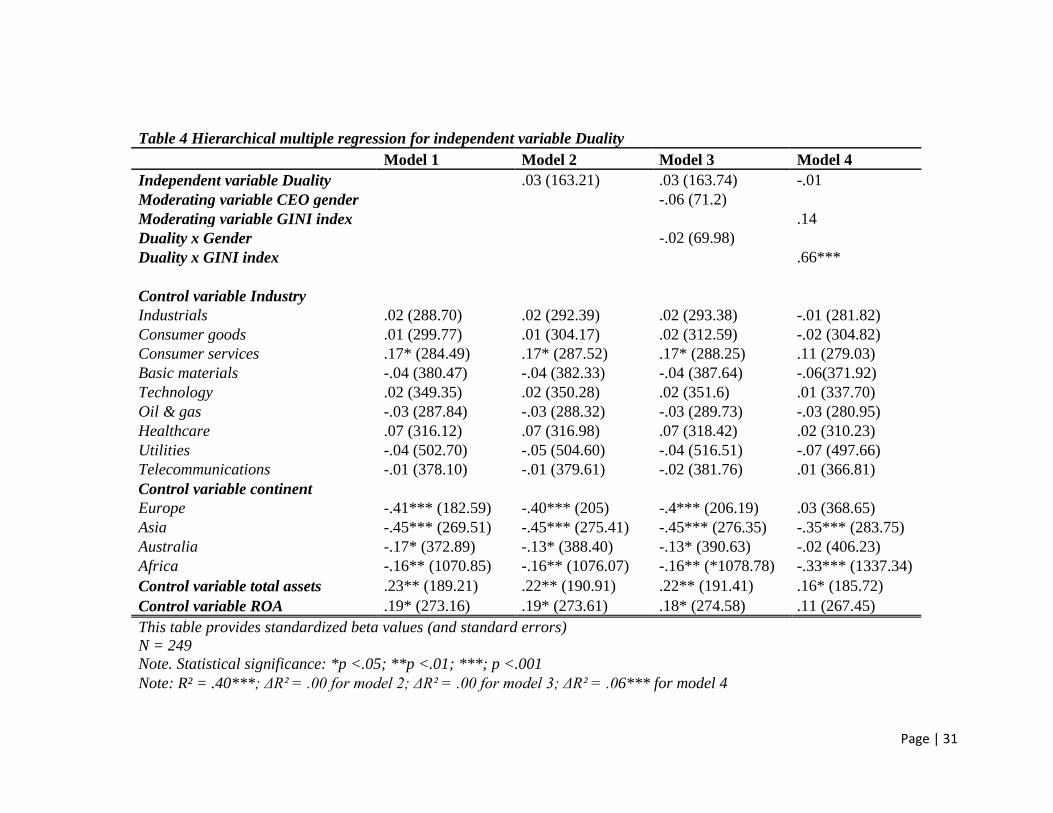

Table 4 Hierarchical multiple regression for independent variable Duality

Model 1 Model 2 Model 3 Model 4

Independent variable Duality .03 (163.21) .03 (163.74) -.01

Moderating variable CEO gender -.06 (71.2)

Moderating variable GINI index .14

Duality x Gender -.02 (69.98)

Duality x GINI index .66***

Control variable Industry

Industrials .02 (288.70) .02 (292.39) .02 (293.38) -.01 (281.82)

Consumer goods .01 (299.77) .01 (304.17) .02 (312.59) -.02 (304.82)

Consumer services .17* (284.49) .17* (287.52) .17* (288.25) .11 (279.03)

Basic materials -.04 (380.47) -.04 (382.33) -.04 (387.64) -.06(371.92)

Technology .02 (349.35) .02 (350.28) .02 (351.6) .01 (337.70)

Oil & gas -.03 (287.84) -.03 (288.32) -.03 (289.73) -.03 (280.95)

Healthcare .07 (316.12) .07 (316.98) .07 (318.42) .02 (310.23)

Utilities -.04 (502.70) -.05 (504.60) -.04 (516.51) -.07 (497.66)

Telecommunications -.01 (378.10) -.01 (379.61) -.02 (381.76) .01 (366.81)

Control variable continent

Europe -.41*** (182.59) -.40*** (205) -.4*** (206.19) .03 (368.65)

Asia -.45*** (269.51) -.45*** (275.41) -.45*** (276.35) -.35*** (283.75)

Australia -.17* (372.89) -.13* (388.40) -.13* (390.63) -.02 (406.23)

Africa -.16** (1070.85) -.16** (1076.07) -.16** (*1078.78) -.33*** (1337.34)

Control variable total assets .23** (189.21) .22** (190.91) .22** (191.41) .16* (185.72)

Control variable ROA .19* (273.16) .19* (273.61) .18* (274.58) .11 (267.45)

This table provides standardized beta values (and standard errors)

N = 249

Note. Statistical significance: *p <.05; **p <.01; ***; p <.001

Note: R² = .40***; ΔR² = .00 for model 2; ΔR² = .00 for model 3; ΔR² = .06*** for model 4

Page | 32

Table 5 Multiple regression for independent variable Tenure

Model 1 Model 2 Model 3 Model 4

Independent variable Tenure .12* (181.93) .12* .11

Moderating variable CEO gender -.05

Moderating variable GINI index .51***

Tenure x Gender -.01

Tenure x GINI .06

Control variable Industry

Industrials .02 (288.70) .03 (286.24) .03 (287.75) -.02 (278.97)

Consumer goods .01 (299.77) .02 (297.53) .03 (303.62) -.03 (297.79)

Consumer services .17* (284.49) .17* (281.89) .17* (282.75) .11 (276.52)

Basic materials -.04 (380.47) -.04 (377) -.04 (379.14) -.06 (366.61)

Technology .02 (349.35) .02 (346.16) .02 (347.25) -.01 (337.19)

Oil & gas -.03 (287.84) -.01 (288.28) -.01 (289.5) -.03 (278.66)

Healthcare .07 (316.12) .08 (313.49) .08 (314.6) .02 (308.18)

Utilities -.04 (502.70) -.02 (504.97) -.02 (520.93) -.05 (506.82)

Telecommunications -.01 (378.10) 0 (375.23) 0 (376.68) .01 (363.48)

Control variable continent

Europe -.41*** (182.59) -.40*** (181.64) -.40***(182.52) .01 (365.15)

Asia -.45*** (269.51) -.44*** (269.25) -.44*** (270.1) -.36 (274.51)

Australia -.17* (372.89) -.13* (370.53) -.12* (376.25) -.02 (402.38)

Africa -.16** (1070.85) -.15** (1064.67) -.15** (1067.99) -.3*** (1367.16)

Control variable total assets .23** (189.21) .23** (187.61) .23** (188.19) .19* (183.14)

Control variable ROA .19* (273.16) .18* (270.74) .18* (272.07) .13 (263.5)

This table provides standardized beta values (and standard errors)

Note: Statistical significance: *p <.05; ** p <.01; ***; p<.001

N = 249

Note: R² =.40***; ΔR² = .01* for model 2; ΔR² = .00 for model 3; ΔR² = .05*** for model 4

Page | 33

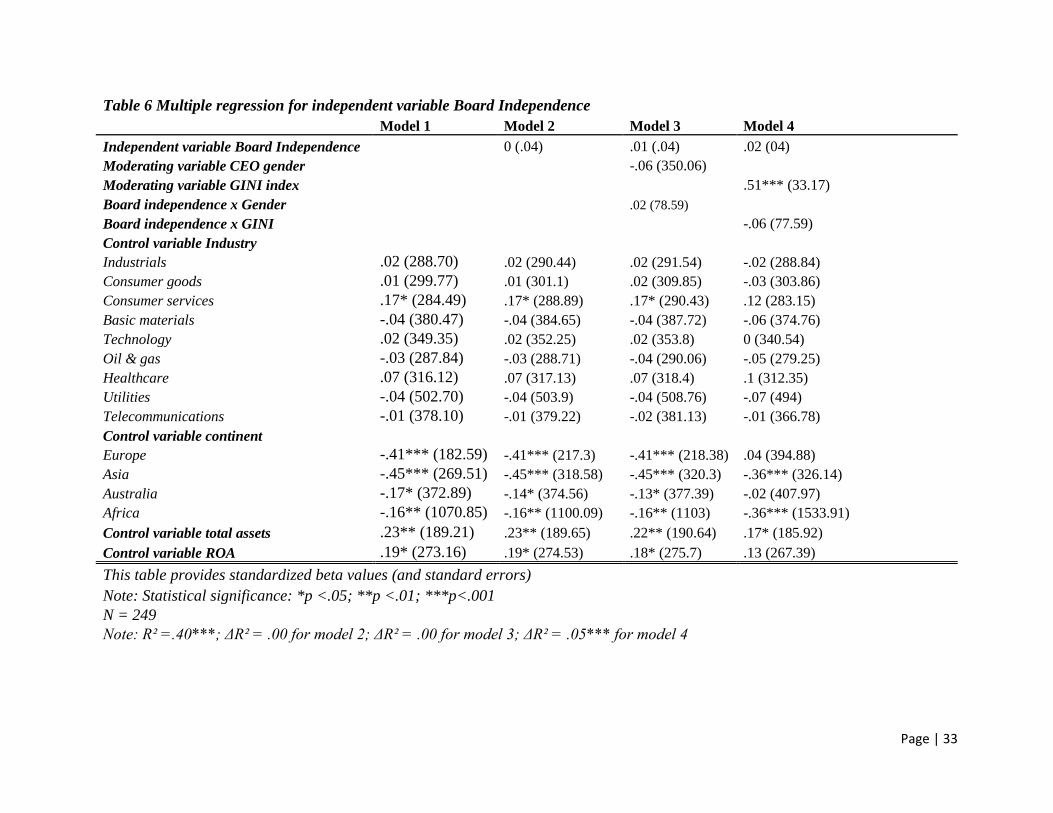

Table 6 Multiple regression for independent variable Board Independence

Model 1 Model 2 Model 3 Model 4

Independent variable Board Independence 0 (.04) .01 (.04) .02 (04)

Moderating variable CEO gender -.06 (350.06)

Moderating variable GINI index .51*** (33.17)

Board independence x Gender .02 (78.59)

Board independence x GINI -.06 (77.59)

Control variable Industry

Industrials .02 (288.70) .02 (290.44) .02 (291.54) -.02 (288.84)

Consumer goods .01 (299.77) .01 (301.1) .02 (309.85) -.03 (303.86)

Consumer services .17* (284.49) .17* (288.89) .17* (290.43) .12 (283.15)

Basic materials -.04 (380.47) -.04 (384.65) -.04 (387.72) -.06 (374.76)

Technology .02 (349.35) .02 (352.25) .02 (353.8) 0 (340.54)

Oil & gas -.03 (287.84) -.03 (288.71) -.04 (290.06) -.05 (279.25)

Healthcare .07 (316.12) .07 (317.13) .07 (318.4) .1 (312.35)

Utilities -.04 (502.70) -.04 (503.9) -.04 (508.76) -.07 (494)

Telecommunications -.01 (378.10) -.01 (379.22) -.02 (381.13) -.01 (366.78)

Control variable continent

Europe -.41*** (182.59) -.41*** (217.3) -.41*** (218.38) .04 (394.88)

Asia -.45*** (269.51) -.45*** (318.58) -.45*** (320.3) -.36*** (326.14)

Australia -.17* (372.89) -.14* (374.56) -.13* (377.39) -.02 (407.97)

Africa -.16** (1070.85) -.16** (1100.09) -.16** (1103) -.36*** (1533.91)

Control variable total assets .23** (189.21) .23** (189.65) .22** (190.64) .17* (185.92)

Control variable ROA .19* (273.16) .19* (274.53) .18* (275.7) .13 (267.39)

This table provides standardized beta values (and standard errors)

Note: Statistical significance: *p <.05; **p <.01; ***p<.001

N = 249

Note: R² =.40***; ΔR² = .00 for model 2; ΔR² = .00 for model 3; ΔR² = .05*** for model 4

Page | 34

Findings for duality

As stipulated in the notes of the multiple regression output as presented in table 4, 40% of the

variance (R2) in the model can be explained by the control variables industry, continent, and firm

performance, and firm size. Looking at the second and third step in the multiple regression, a

disappointing 0 R2 change (not statistically significant) is shown. Again, looking at the fourth

and last step, support is provided that country wage equality (GINI index) does influence CEO

compensation, and the model gains an additional 6% explanation of the variance.

The standardized beta for the independent variable duality is not statistically relevant, and

even if it would have been the value is so low that it is almost negligible. This rejects hypothesis

1a. The moderating values as predictor variables themselves are not statistically significant, and

neither is the interaction term for gender. However, the interaction term for duality and GINI

index is .66, statistically significant at the 0.001 level. This shows that country equality

moderates the relationship between duality and compensation. Thus when the CEO

simultaneously chairs the board, this has an impact on compensation, however when the level of

inequality in the country is higher, this further increases the CEO’s compensation.

Findings for tenure

The output of the multiple regression for tenure are presented in table 5. At a first glance, it can

already be noted that the findings here are quite similar to those of the first regression for duality.

Adding the independent variable in the second model adds a sheer 1% to the R2 , pointing out its

small contribution in accounting for the variability in the outcome. This is further corroborated

by the standardized beta value of .12 which points a small positive effect. Tenure however, is the

only independent variable that is a statistically significant predictor variable in regard to CEO

compensation. Albeit small, there is thus support for hypothesis 1c.

Page | 35

Looking at the moderators or in table 5, neither of the interaction terms are statistically

significant. Even if they would be significant, the values are of such low values that they are

almost negligible.

Findings for board independence

In table 6, the results from the regression for independent variable board independence is

presented. Most surprisingly, again the results are quite unexpected looking at their

insignificance. The coefficient of determination (R2) after adding the independent variable board

independence, does not change at all. This signifies the lack of any relationship between this

independent variable and the dependent variable. Furthermore, it indicates that board

independence does not account for any of the variability in CEO compensation. With regard to

the findings are presented in table 6, hypothesis 1b is thus rejected.

Furthermore, also the statistically insignificant and low interaction term values for the

moderators, show that there is no moderating effect of either variable.

Findings for CEO gender

In all three regressions, the β for the interaction term of ‘gender x duality’ is very small and is

not statistically significant ( -.02 in table 4, -.01 in table 5, and .01 in table 6). These results

imply that gender effectually does not moderate the relationship between any of the independent

variables and the dependent variable.

These findings, force me to have to reject hypothesis 2. It is however important to

mention that these findings might be convoluted by the dominance of male CEOs in this sample

(95.8% of the sample are male).

Page | 36

Findings for country inequality / GINI index

The interaction terms for country inequality, show that this variable only moderates the

relationship between duality and CEO compensation. In case of the other two independent

variables, the interaction term is not statistically significant. As there is moderation for one of

three independent variables, hypothesis 3 is partly supported.

Country of headquarters/GINI index, is however a statistically significant predictor in all

models and aside from this, also has the highest standardized beta value. This is quite surprising

and interesting, because geographic region has already been controlled for. This suggests that

country income inequality, as opposed to simply geographical region, has a significant additional

impact on CEO compensation.

Other findings

The control variables continent and firm size and performance are the only variables (besides the

GINI Index) which are consistently statistically relevant throughout the steps in the multiple

regressions. This proves their importance in explaining the variance measured for CEO

compensation. It is interesting when comparing these results to the findings for the industry

benchmark, which does not seem to have any impact on the level of CEO compensation.

Furthermore, as North America is the baseline for the dummy variable of continent, the

five other continents as shown in the tables above are a coefficient compared to North America.

This suggests that when the coefficient is positive, the level of CEO compensation is higher

compared to that in North America, and vice versa if the coefficient is negative. An interesting

result is that CEO compensation is lower than CEO compensation in North American for all

continents. These findings imply that CEO compensation in North America is the highest in the

Page | 37

world, which normally would raise ethical debates. This ethical issue could be an additional

explanation, besides the easy access to compensation data, as to why extant research has focused

on mostly North America up until now.

Below, a summary of the hypotheses is provided and whether they are supported by the

data or not:

H1a: When the CEO is also the chairman of the executive board (CEO duality), his or

her compensation will be higher than for those CEOs who are not.

Result: not supported.

H1b: When the CEO has appointed board members, CEO compensation will be higher

than when the board is independent. (Board independence)

Result: not supported.

H1c: As a CEO’s tenure increases, their executive compensation also increases.

Result: supported.

H2: The relationship between CEO power and CEO compensation is moderated by the

CEO gender; when the CEO is female this direct relationship is weaker.

Result: not supported.

H3: The relationship between CEO power and CEO compensation is weaker when there

are lower levels of inequality in the country where the firm is headquartered.

Result: partly supported.

Page | 38

Discussion

Multiple interesting findings have been presented in the previous chapter. The most obvious and

perhaps most surprising, is that only one of the three hypotheses pertaining to CEO power are

not supported by the data. Based on the results of the regressions and the outcome of these

hypotheses, the answer to the research question in this paper is that the extent of CEO power

only has a very small impact on CEO compensation.

Looking at the specific determinants of CEO power; duality, tenure, and board

independence, only the findings on tenure support previous research (Hill et al., 1991; Johnston,

2002). This finding also lends further support to the use upper echelon theory in explaining CEO

power and that tenure may be a proxy for this managerial characteristic. Adversely, for duality

and board independence, upper echelon theory was used to explain the use of these proxies,

however with no significant results.

The results as presented in this paper do provide an interesting and novel take on equality

with regard to CEO compensation, which has been an understudied topic up to now. It provides

an unusual view on the influence the country where the firm is headquartered with regard to

levels of (in)equality of that specific country. Country income equality, measured by the GINI

index, moderates the relation between duality and compensation. Results indicate that the higher

the level of inequality, the higher the level of CEO compensation. The insignificant findings on

CEO gender are not in support of the upper echelon theory as described in the literature review,

however it is very possible that the findings as presented in this paper are not fully representative

due to the imbalance between the amount of male and female CEOs in this dataset.

Page | 39

Albeit unfortunate that most of the hypotheses were not supported by the data, this does

create opportunities for additional research and building on the upper echelon theory with regard

to (in)equality.

Page | 40

Conclusions and suggestions for further research

This paper adds to the literature on CEO compensation by testing a set of hypotheses using a

unique global dataset, as opposed to extant literature. It finds that, opposite of what is theorized,

CEO power does not have an impact on CEO compensation.

This paper aims to extend the upper echelon theory (Hambrick & Mason, 1984), by

proposing that CEO power is one of the managerial characteristics that influence strategic choice

and moreover influence strategic choices of the board of directors with regard to CEO

compensation. Furthermore, the upper echelon theory is extended by introducing fairness into the

theory. As certain characteristics and social norms influence strategic decision-making

(Hambrick & Mason, 1984), I propose that it is likely that female CEOs are willing to accept

lower compensations than their male counterparts, because of the social structure of a high

regard of fairness and equality that is often assigned to females (Eagly & Woord, 1999).

Although the findings for this specific proposition are not what was expected per se, it is

important to note that this topic in specific deserves further research with different datasets.

Suggestions for further research thus regard the topic of gender and CEO compensation.

As is presented in this paper, female CEOs made up a sheer 4.2% of the whole sample,

decreasing the predictive power of this variable. Results however, showed that the difference

between female and male CEO compensation was not statistically significant. It would be very

interesting to understand whether CEO compensation would be influenced by whether or not

there are females on the board. This could for example be done by researching whether there are

any or no females on the board, and measure the respective impact on CEO compensation. It

would however be more interesting to research the effects of the specific amount of females on

the board. The reason for the latter, is because it has been theorized that females only have a

Page | 41

specific influence when there is another female on their side, as they are less likely to speak up if

they are the only female in the room. It would be interesting to then see whether it would make

any difference if there are no females on the board, one female on the board, or more than one

female on the board. In the latter case, this should decrease the CEO’s compensation based on

the research on fairness and reciprocity as presented in this paper.

Page | 42

References

Adams, R. B., Almeida, H., & Ferreira, D. 2005. Powerful CEOs and their impact on corporate

performance. Review of Financial Studies, 18(4): 1403-1432.

Adams, S. M., Gupta, A., Haughton, D. M., & Leeth, J. D. 2007. Gender differences in CEO

compensation: Evidence from the USA. Women in Management Review, 22(3): 208-224.

Alchian, A. A., & Demsetz, H. 1972. Production, information costs, and economic organization.

The American Economic Review, 62(5): 777-795.

Belliveau, M. A., O'Reilly, C. A., & Wade, J. B. 1996. Social capital at the top: Effects of social

similarity and status on CEO compensation. Academy of management Journal, 39(6): 1568-

1593.

Bertrand, M., & Schoar, A. 2002. Managing with style: The effect of managers on firm policies.

Boyd, B. K. 1995. CEO duality and firm performance: A contingency model. Strategic

Management Journal, 16(4): 301-312.

Brick, I. E., Palmon, O., & Wald, J. K. 2006. CEO compensation, director compensation, and

firm performance: Evidence of cronyism? Journal of Corporate Finance, 12(3): 403-423.

Bugeja, M., Matolcsy, Z. P., & Spiropoulos, H. 2012. Is there a gender gap in CEO

compensation? Journal of Corporate Finance, 18(4): 849-859.

Page | 43

Carpenter, M. A., Geletkanycz, M. A., & Sanders, W. G. 2004. Upper echelons research

revisited: Antecedents, elements, and consequences of top management team composition.

Journal of management, 30(6): 749-778.

Carpenter, M. A., & Reilly, G. P. 2006. Constructs and construct measurement in upper echelons

research. Research methodology in strategy and management, 3: 17-35.

Conyon, M. J. 2006. Executive compensation and incentives. The Academy of Management

Perspectives, 20(1): 25-44.

Cordeiro, J. J., & Veliyath, R. 2003. Beyond pay for performance: A panel study of the

determinants of CEO compensation. American Business Review, 21(1): 56.

Eagly, A. H., & Wood, W. 1999. The origins of sex differences in human behavior: Evolved

dispositions versus social roles. American psychologist, 54(6): 408.

FIELDS, COLLECTIVE RATIONALITY IN ORGANIZATIONAL, Dimaggio, P., & Powell,

W. 1983. The iron cage revisited: Institutional isomorphism and collective rationality in

organizational fields. American Sociological Review, 48(2): 147-160.

Finkelstein, S. 1992. Power in top management teams: Dimensions, measurement, and

validation. Academy of Management journal, 35(3): 505-538.

Finkelstein, S., & Boyd, B. K. 1998. How much does the CEO matter? the role of managerial

discretion in the setting of CEO compensation. Academy of Management journal, 41(2): 179-

199.

Page | 44

Finkelstein, S., & D'aveni, R. A. 1994. CEO duality as a double-edged sword: How boards of

directors balance entrenchment avoidance and unity of command. Academy of Management

journal, 37(5): 1079-1108.

Grabke-Rundell, A., & Gomez-Mejia, L. R. 2002. Power as a determinant of executive

compensation. Human Resource Management Review, 12(1): 3-23.

Haleblian, J., & Finkelstein, S. 1993. Top management team size, CEO dominance, and firm

performance: The moderating roles of environmental turbulence and discretion. Academy of

Management journal, 36(4): 844-863.

Hambrick, D. C. 2007. Upper echelons theory: An update. Academy of management review,

32(2): 334-343.

Haynes, K. T., & Hillman, A. 2010. The effect of board capital and CEO power on strategic

change. Strategic Management Journal, 31(11): 1145-1163.

Hermalin, B. E., & Weisbach, M. S. 1998. Endogenously chosen boards of directors and their

monitoring of the CEO. American Economic Review: 96-118.

Hill, C. W., & Phan, P. 1991. CEO tenure as a determinant of CEO pay. Academy of

Management journal, 34(3): 707-717.

Johnston, J. 2002. Tenure, promotion and executive remuneration. Applied Economics, 34(8):

993-997.

Page | 45

Mohan, N., & Ruggiero, J. 2003. Compensation differences between male and female CEOs for

publicly traded firms: A nonparametric analysis. Journal of the Operational Research Society,

54(12): 1242-1248.

Mohan, N., & Ruggiero, J. 2007. Influence of firm performance and gender on CEO

compensation. Applied Economics, 39(9): 1107-1113.

Peterson, R. S., Smith, D. B., Martorana, P. V., & Owens, P. D. 2003. The impact of chief

executive officer personality on top management team dynamics: One mechanism by which

leadership affects organizational performance. Journal of Applied Psychology, 88(5): 795.

Ryan, H. E., & Wiggins, R. A. 2004. Who is in whose pocket? director compensation, board

independence, and barriers to effective monitoring. Journal of Financial Economics, 73(3):

497-524.

Ryan, H. E., & Wiggins, R. A. 2004. Who is in whose pocket? director compensation, board

independence, and barriers to effective monitoring. Journal of Financial Economics, 73(3):

497-524.

Sauerwald, S., Lin, Z. J., & Peng, M. W. 2014. Board social capital and excess CEO returns.

Strategic Management Journal.

Scott, W. R. 2008. Approaching adulthood: The maturing of institutional theory. Theory and

society, 37(5): 427-442.

Page | 46

Shin, T. 2012. The gender gap in executive compensation the role of female directors and chief

executive officers. The Annals of the American Academy of Political and Social Science,

639(1): 258-278.

Solnick, S. J. 2001. Gender differences in the ultimatum game. Economic inquiry, 39(2): 189.

Wernicke, G. forthcoming. Dad is in the news! CEO identities and the social constraint on

executive pay.

Zhang, Y., & Rajagopalan, N. 2003. Explaining new CEO origin: Firm versus industry

antecedents. Academy of Management Journal, 46(3): 327-338.

Zhang, Y., & Rajagopalan, N. 2003. Explaining new CEO origin: Firm versus industry

antecedents. Academy of Management Journal, 46(3): 327-338.

Websites:

Financial Times Global 500 methodology: http://www.ft.com/cms/s/2/1fda5794-169f-11e5-b07f-

00144feabdc0.html#axzz4CDMRLRme, accessed on 21/6/2016.

ICB industry definitions. http://www.icbenchmark.com/, accessed on 6/6/2016.