Embed Size (px)

Citation preview

TheInsightTheInsight

The Institute of Chartered Accountants of India(Setup by an Act of Parliament)

BARODA BRANCH OF

WESTERN INDIA CHARTERED ACCOUNTANTS

STUDENTS ASSOCIATION OF

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(WICASA)

VOL. X NOVEMBER 2012l

“Leveraging Strength, Catalyzing Tomorrow”

e-NewsLettere-NewsLetter

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “You only live once, but if you do it right, once is enough.”

PRINTED AND PUBLISHED BY

Designed at

“ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012.

Telefax : +91 (265) 2680593, 2681115 E-mail: [email protected] Web : www.baroda-icai.org

Multiprints, 30/B, Gandhi Oil Mill Compound,

Near BIDC, Gorwa, Vadodara - 390 016.

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

WESTERN INDIA CHARTERED ACCOUNTANTS STUDENTS

ASSOCIATION

BARODA BRANCH OF WICASA

ICAI Bhawan, Post Box No. 7100, Indraprastha Marg,

New Delhi - 110002. Tel. : +91 (11) 39893989

E-mail : [email protected] Website : www.icai.org

ICAI Bhawan, 27, Cuffe Parade, Post Box No. 6081, Colaba,

Mumbai - 400 005. Tel. : +91 (22) 39893989

Email : [email protected] Website : www.wirc-icai.org

“ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012.

Telefax : +91 (265) 2681115, 2680593

E-mail: [email protected] Web : www.baroda-icai.org

�

�

�

Managing Committee Members

CA. Ashish Parikh Chairman 9825231545

Mr. Sharukh Pathan Vice Chairman 8905094384

Ms. Hiral Jethva Secretary 9714778552

Mr. Mehul Thakkar Treasurer 8905564940

CA. Nayan Kothari Ex-officio 9824433445

Mr. Kanji Hadiya Member 9687969764

Mr. Mohd.Atiq Qureshi Member 9998570095

Mr. Dipesh Thakkar Member 9898940652

CA. Ashish Parikh Editor

Mr. Mohd.Atiq Qureshi Joint Editor

Ms. Hiral Jethva Member

Editorial Board

DISCLAIMER :

WICASA COMMUNITY :

STUDENTS’ STUDY CIRCLE :

BRAIN TRUST SESSION :

SPORTS ACTIVITIES:

WICASA HELPLINE :

The views and opinion expressed or implied in the Newsletter are those of the

authors/contributors and do not necessarily reflect those of ICAI. Unsolicited articles and

transparencies are sent at the owner's risk and the publisher accepts no liability for loss or

damage. Material in this publication may not be reproduced, whether in part or in whole, without

the consent of ICAI.

Students are requested to kindly send article / paper of interest to [email protected].

The same may be published in the newsletter subject to availability of space & editing.

Be a part of the “WICASA Baroda” now also on FACEBOOK Community. Exchange views and

news. Be updated about forthcoming events of WICASA.

Join now .... where in students can exchange knowledge with the help of group discussion.

Contact Mr.Kanji Hadiya-9687969764

Join now… where a group of students can discuss on predetermine questions and moderator

(from CA fraternity) will elaborate the discussion and conclude. Contact Ms. Hiral Jethva-

9714778552

Join now…where in students can participate in Indoor-Outdoor games for overall development.

Contact Mr. Dipesh Thakkar-9898940652

Students are invited to send their feedback suggestions or grievances to

[email protected] or contact Mr. Sharukh Pathan-8905094384, Mr. Mehul Thakkar-

8905564940

Dear Students,

I hope and wish that all your hard work, patience and

sacrifices must have helped in boosting your performance in

your examinations. But I know that all of you will try to make it

achievable. As a student you have put in all your best efforts

for performing at your best in examination. Now it is time to

go ahead and put your efforts in different perspectives like

apply your all theoretical knowledge in practical issues or

occupy yourself in other activities.

Coming to the Baroda Branch of WICASA-2012 event of

November 2012, it has organized numerous of programs like

Study Circle Meeting, Industrial Visits and Career Counseling

Programs & to aid the students for acquiring utmost benefit

we organized 1 RRC at Caravan Serai Resort, Jambughoda,

Gujarat.

In this month of festivals give us an opportunity to celebrate

and provide us an opportunity to rejoice in community. Our

elders used to say: Joy when shared increases and pain when

shared decreases. Joy and pain are actually relative, and

absence of either of the two will result in a loss of the other.

These require frames of reference to exist. We have already

learnt that we cannot celebrate our joy in isolation, and that

sharing is quite innate to happiness.

Best wishes

st

CA. Ashish Parikh

“Sometimes life knocks you ! Happiness is not the absence of

problems; it's the ability to deal with them.”

May the spirit of our festivals envelop our soul and provide

us strength and courage to do something for the welfare of

our society!

Chairman’sCommunication

2

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Sometimes the questions are complicated and the answers are simple.”

Forthcoming EventsForthcoming Events

3

Lecture Meeting

Study Circle Meetings

Date & Day :

Time :

Topic :

Speaker :

Venue :

Date & Day :

Time :

Topic :

Speaker :

26-11-2012, Monday

18:30 hrs. to 20:30 hrs.

Cyber Crime

CA. Sanjeev Shah

ICAI Bhawan

27-11-2012, Tuesday

18:30 hrs. to 20:30 hrs.

Reverse Charge Mechanism

Mr. Karan Shah

Venue : ICAI Bhawan

Date & Day :

Time :

Topic :

Speaker :

Venue :

Date & Day :

Time :

Topic :

Speaker :

Venue :

Date & Day :

Time :

Topic :

Speaker :

Venue :

07-11-2012, Wednesday

16:00 hrs. to 18:00 hrs.

"GST" - a precusor

Mr. Milind Joshi

ICAI Bhawan

08-11-2012, Thursday

17:00 hrs. to 18:30 hrs.

TDS - Provision

Mr. Brijesh Pitroda

ICAI Bhawan

10-11-2012, Saturday

18:30 hrs. to 20:30 hrs.

TDS - Case Studies

Ms. Rutvi Solanki

ICAI Bhawan

An Initiative to Save Environment

Day Light Saving Day

Industrial Visit

Childrens Day Celebration

Career Counselling Program

CPT Mock Test

Date & Day :

Time :

Venue :

Date & Day :

Time :

Venue :

Date & Day :

Time :

Venue :

Date & Day :

Time :

Venue :

Date & Day :

Time :

Venue :

Date & Day :

Time :

Fees :

Venue :

02-11-2012, Friday

Full day

ICAI Bhawan

04-11-2012, Sunday

Full day

ICAI Bhawan

07-11-2012, Wednesday

08.00 hrs. to 10.00 hrs.

Goraj Cancer Hospital

14-11-2012, Wednesday

09:30 hrs. to 12:00 hrs.

ICAI Bhawan

21-11-2012, Wednesday

09:30 hrs. to 12:00 hrs.

St. Kabir School

25-11-2012, Sunday

10:00 hrs. to 17:00 hrs.

Rs. 200/-

ICAI Bhawan

Past Events : October 2012Past Events : October 2012DATE NAME OF EVENT ATTEN.

01-10-2012 Full Day Seminar on Accounting (Amalgamation, Absorption & Reconsutruction) by CA Mayur Thakkar 44

02-10-2012 Half Day Seminar on CAPITAL GAIN by CA.Nirav Shah 60

03-10-2012 Half Day Seminar on Financial Management by CA. AMIT SHAH 50

04-10-2012 Half Day Seminar on VAT by CA.Nirav Shah 45

05-10-2012 Half Day Seminar on Income Tax by CA. Nirav shah 58

05-10-2012 Half Day Seminar on Financial Management by CA. AMIT SHAH 45

06-10-2012 Full Day Seminar on Taxation by CA.Nirav Shah 49

07-10-2012 Full Day Seminar on Account by Dr.J.K.Pandya 76

09-10-2012 Half Day Seminar on Income Tax by CA. NIRAV SHAH 46

12-10-2012 Full Day Seminar on Costing by CA Anu Agrawal, Mumbai 46

13-10-2012 Full Day Seminar on Costing by CA Anu Agrawal, Mumbai 47

13-10-2012 Motivation Lecture - How to Face CA Exams by Hemadri Sinha 47

14-10-2012 Half Day Seminar on Costing ( Capital Budgeting) by CA. AMIT SHAH 46

15-10-2012 Mock Test - CA Final (Group I) : Financial Reporting 10

15-10-2012 Mock Test - CA IPCE (Group I) : Accounting 37

15-10-2012 Mock Test - CA PCC (Group I) : Advanced Accounting 5

16-10-2012 Mock Test - CA Final (Group I) : Strategic Financial Management 10

16-10-2012 Mock Test - CA IPCE/PCC (Group I) : Business Laws, Ethics & Communication 37

17-10-2012 Mock Test - CA Final (Group I) : Advanced Auditing and Professional Ethics 10

17-10-2012 Mock Test - CA IPCE/PCC (Group I) : Costing and Financial Managaement 37

18-10-2012 Mock Test - CA Final (Group I) : Corporate and Allied Laws 10

18-10-2012 Mock Test - CA IPCE (Group I) : Taxation 37

18-10-2012 Half Day Seminar on Computer Network & Network security Mr. Manish Shukla 70

19-10-2012 Half Day Seminar on Flow Chart, Decision Table & Internet and other technologies Mr. Manish Shukla 56

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Always do your best, success follow’s actions.”4

The term, Forensic Accounting was coined by Maurice Paulobet

in 1946. Worldwide, Sherlock Holmes is considered to be the

first forensic accountant. However, in India, Kautilya was the

first person to mention the famous forty ways of embezzlement

in his book Arthashastra during the ancient times. He was the

first economist, who openly recognized the need of the forensic

accountants. Similarly, Birbal was the Scholar in the time of King

Akbar. He used various tricks to investigate various crimes. Some

of his stories give the fraud examiner a brief idea about the

Litmus test of investigation.

The modern digital and complex environment offers new

opportunities for both perpetrators and investigators of fraud

i.e. Satyam scam, CWG and 2G. In many ways, it has reformed

the way fraud examiners conduct investigations, the methods

forensic accountant use to plan and complete work, and the

approaches take to assess risk and perform task. Forensic

Accounting is essentially required in wake of growing frauds e.g.

Rapid use of complex information technology

environment

Growing Cyber crime

Increase in number of Corporate Scams.

Failure of regulators to track the securities scams

H e l p i n g t o

Government in

a c h i e v i n g

c o m p l i a n c e

with var ious

f o r m &

regulation.

It's

a good quote that

every auditor should

know. This quote

makes the definition of Forensic accountants even simpler. The

forensic Accountant is a bloodhound of Bookkeeping. These

bloodhounds sniff out fraud and criminal transactions in bank,

corporate entity or from any other organization's financial

�

�

�

�

�

"Auditor should be

watchdog and not be

the bloodhound".

Need of Forensic Accounting

Forensic Accountants

DATE NAME OF EVENT ATTEN.

20-10-2012 Half Day Seminar on Accounting Standard by CA Mayur Thakkar 44

22-10-2012 Mock Test - CA Final (Group II) : Advanced Management Accounting 5

22-10-2012 Mock Test - CA IPCE (Group II) : Advance Accounting 20

22-10-2012 Mock Test - CA PCC (Group II) : Taxation 5

23-10-2012 Mock Test - CA Final (Group II) : Information Systems Control and Audit 5

23-10-2012 Mock Test - CA IPCE/PCC (Group II) : Auditing and Assurance 20

24-10-2012 Mock Test - CA Final (Group II) : Direct Tax Laws 5

24-10-2012 Mock Test - CA IPCE/PCC (Group II) : Information Technology and Strategic Management 20

25-10-2012 Mock Test - CA Final (Group II) : Indirect Tax Laws 5

29-10-2012 Study Circle Meeting on "Limited Liability Partnership" by Vahid Langawala 11

31-10-2012 Visit to Trade Fair at Sir Sayajirao Nagar gruh 6

Forensic AccountingContributed by : (CA Final Student)Prateek Patel

Forensic – ‘belonging to, used in or suitable to courts of

judicature or to public discussion or debate’.

Forensic accounting intends to “investigate” the possibilities of

criminal intent in the conduct of the transaction. Forensic

accounting is the specialty practice area of accounting that

defines activities, which result from real or anticipated

litigation. Broadly speaking, these engagements fall into one of

three categories:

economic damages,

assurance as to fraud in accounts or inventories, or

the presentation thereof, and business valuation.

However forensic accounting is a gross area of tasks of which

fraud examination is a small part.

Emphasis of Forensic Accounting is on scrutinizing and

interpreting white collar crimes such as securities fraud and

embezzlement, bankruptcies and contract disputes, and other

complex and possibly criminal financial transactions, such as

money laundering by organized criminals. Forensic accountants

combine their knowledge of accounting, industry practice, and

finance with law and investigative techniques in order to

determine if illegal activity is going on. It can be identified as

integrity of accounting, auditing and investigative skills to

secure a particular result. It is use of intelligence gathering

techniques and accounting and business skills to develop

information.

�

�

�

According to AICPA, “Forensic Accounting is the application of

accounting principles, theories and discipline to facts or

hypothesis at issues in a legal dispute and encompasses every

branch of accounting knowledge.”

“Thinking beyond the numbers and Thinking out of Box.”

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “The Ultimate Thinking Tool That Will Change Your Life”5

records. They hound for the conclusive evidences.

Forensic Accountant has to become thief-in-virtual-sense. A

capable Forensic Accountant should have the following

characteristics:

curiosity;

persistence;

creativity;

discretion;

organization;

confidence;

sound professional judgment;

Interpersonal and communication skills, which aid in

disseminating information about the company’s ethical

policies.

Knowledge and Experience in:

Financial Statements & Audit

Internal Controls and Operational Processes

Fraud Schemes

Investigation and Legal Elements of Fraud

Psychology of the White Collar Criminal

A Forensic Accountant must be open to consider all alternatives,

scrutinize the fine details and at the same time see the big

picture. In addition, a Forensic Accountant must be able to listen

effectively and communicate clearly and concisely. Forensic

accountants, in fact, utilize an understanding of business

information and financial reporting systems, accounting and

auditing standards and procedures, evidence gathering and

investigative techniques, and litigation processes and

procedure to perform their work. Forensic accountants are also

increasingly playing more ‘proactive’ risk reduction roles by

designing and performing extended procedures as part of the

statutory audit, acting as advisors to audit committees, and

assisting in investment analyst research.

The involvement of the forensic accountant is almost always

reactive – they primarily respond to complaints arising in

criminal matters, statements of claim arising in civil litigation

and rumors and enquiries arising in corporate investigations.

Forensic Accountants become involved in a wide range of

investigations, spanning many different industries. The practical

and in-depth analysis that a Forensic Accountant will bring to a

case helps uncover trends that bring to light the relevant issues.

Forensic accountants are trained to look beyond numbers and

deal with the business like situation. Forensic accountants are

also increasingly playing more 'proactive' risk reduction roles by

designing and performing extended procedures as part of the

statutory audit, acting as advisors to audit committees, and

assisting in investment analyst research.

Investigating and analyzing financial evidence;

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

Assignments which Forensic Accountant can perform?

A Forensic Accountant is often involved in the following:

�

�

�

Developing computerized applications to assist in the

analysis and presentation of financial evidence;

Communicating their findings in the form of reports,

exhibits and collections of documents; and

Assisting in legal proceedings, including testifying in court

as an expert witness and preparing visual aids to support

trial evidence.

Detailed below are various areas in which a Forensic Accountant

will often become involved;

Professional slackness: Forensic accountants also take up cases

relating to professional negligence. Whenever there is a breach

of generally accepted accounting standards (GAAS) or ethical

codes of any profession, forensic accountants are required to

quantify the loss resulting from such professional negligence or

deficiency in service.

Detection of fraud: This often involves procedures to determine

the existence, nature and extent of fraud or embezzlement and

may concern the identification of a perpetrator. These

investigations often entail interviews of personnel who had

access to the funds and a detailed review of the documentary

evidence.

Criminal investigation: Where the matter under investigation

involves financial implications, the investigation department,

law society, and etc. avail of the services of a forensic

accountant. The report of an accountant is very much useful in

preparing and presenting evidence.

Personal Injury Claims / Motor Vehicle Accidents: A Forensic

Accountant is often asked to quantify the economic losses

resulting from a motor vehicle accident. A Forensic Accountant

needs to be familiar with the legislation in place, which pertains

to motor vehicle accidents. Cases of medical malpractice and

wrongful dismissal often involve similar issues in calculating the

resulting economic damages.

Business economic losses: Assignments involving business

economic losses include; contract disputes, construction claims,

product liability claims, trademark and patent infringements

and losses stemming from a breach of a non-competition

agreement.

Review of the factual situation and provision of

suggestions regarding possible courses of action.

Assistance with the protection and recovery of assets.

Co-ordination of other experts, including:

Private investigators;

Forensic document examiners;

Consulting engineers.

Assistance with the recovery of assets by way of civil action

or criminal prosecution.

Assistance in obtaining documentation necessary to

�

�

�

�

�

�

�

�

Investigative Accounting:

Litigation Support:

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Never Give Up: Relentless Determination to Overcome Life's Challenges”6

support or refute a claim.

Review of the relevant documentation to form an initial

assessment of the case and identify areas of loss.

Assistance with Examination for Discovery including the

formulation of questions to be asked regarding the

financial evidence.

Attendance at the Examination for Discovery to review the

testimony; assist with understanding the financial issues

and to formulate additional questions to be asked.

Review of the opposing expert's damages report and

reporting on both the strengths and weaknesses of the

positions taken.

Assistance with settlement discussions and negotiations.

Attendance at trial to hear the testimony of the opposing

expert and to provide assistance with cross-examination.

Business Valuation Services: Forensic accountants are often

hired to perform valuation services for clients. The AICPA

defines business valuation services as follows:

“Business valuations generally arise in the context of one or

more of the following three categories: (1) transactions; (2)

litigation; and (3) taxes (or estate planning). Transaction

appraisals include acquisitions, mergers, leveraged buy-outs,

initial public offerings, ESOPs, buy-sell agreements, and many

other engagements.

Valuations may arise in a litigation context in connection with

marital dissolution, bankruptcy, breach of contract, dissenting

shareholder and minority oppression cases, economic damages

computations, and other cases. Valuations may also be

conducted for tax reasons, including gift and estate taxes, estate

planning, family limited partnerships, ad valorem taxation, and

other tax-related reasons. The Business Valuation resource

section presents guidance on performing valuations of closely-

held businesses and intangible assets, including an overview of

the valuation process, the factors to consider before accepting

the valuation engagement, and the various methods of

valuation. Additionally, it includes tools and aids that would

facilitate the business valuation process.”

Benford’s Law works because nature produces more small

things than large things. There are more insects than large

mammals, more small houses than large ones, and more

small lakes than large bodies of water. Similarly,

businesses produce more transactions with small

amounts than with large amounts. It is a mathematical

tool used in determining whether a variable under study is

a case of mistake or fraud. Once the variable is decided,

the left most digit of the variable is extracted and

summarized for entire population. The summarization is

done by classifying the first digit field and calculating its

observed count percentage. Then Benford’s set is applied.

�

�

�

�

�

�

Techniques used by Forensic Accountants

� Digital Analysis / Benford’s Law;

�

�

�

�

�

Trending;

Outlier Detection;

Data Mining

Analytical Tools

External Research

In addition to comparing same period numbers from

different vendors, employees, or customers, fraud can be

discovered by comparing numbers over time. Because

almost all perpetrators are greedy, fraud increases

exponentially over time. Forensic accountant can easily

spot an increasing trend on a line chart.

One of the primary methods of detecting fraud is

discovering data values that are outside the normal course

of business. For example, a kickback scheme might be the

reason purchases from one vendor are twice as high as

similar purchases from another vendor.

Forensic accountants find patterns through database

searches and statistical algorithms. Benford's Law, for

example, reveals false invoices by identifying activities

such as recurring fixed expenses. The law states that

"certain digits appear more frequently than others in data

sets." flag discrepancies in key performance ratios such as

debt to equity. Outer detection, which highlights amounts

that appear to be abnormally high, shows unusual

spending habits and possible kickbacks. Also used in credit

card fraud investigations, the Luhn algorithms, validates

account numbers.

Forensic accountants use trending to study financial

figures over a period of time. They conduct ratio analyses

of indicators, such as inventory turnover and working

capital to identify fraudulent financial statements.

The advent of the Internet has enabled forensic

accountants to quickly compile information on individuals

and companies. Software packages that bypass passwords

to access suspect computer hard drives and programs that

detect embedded information enhance their investigative

ability.

Finally, forensic accounting is a relatively ingenious field. As the

services of forensic accountants are not used or essential within

the everyday activity of an individual it’s not at all unusual fairly

little is known about the occupation. Upon investigation

forensic accounting is in fact broad in scope and covers many

different roles. What is interesting to note is the fact that despite

the difference between general accounting and forensic

accounting, the services connected with each are frequently

provided by exactly the same company. In other words it will

often be the case a chartered accountant can cater for not only

your general accounting needs but also your forensic

accounting requirements, in the event you so need them.

Conclusion

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Don't cry because it's over, smile because it happened.”7

Non-XBRL Filing

XBRL Filing

The Ministry issued General Circular No.30/2012 Dated

28.09.2012, In order to ensure smooth filing and to avoid last

minute rush, the due date of filing of e-forms 23AC(Non-XBRL)

and 23ACA (Non XBRL) as per new schedule VI is extended in

following manner without any additional fee :-

Company holding AGM or whose due date for holding AGM is on

or before 20.09.2012, the time limit will be 03.11.2012 or due

date of filing, whichever is later.

Company holding AGM or whose due date for holding AGM is on

or after 21.09.2012, the time limit will be 22.11.2012 or due date

of filing, whichever is later.

As per General Circular No. 16/2012 issued by the Ministry of

Corporate Affairs on 6 July 2012, all companies referred in para

2 of the said circular will be allowed to file their financial

statements in XBRL mode without any additional fee/ penalty up

to15 November, 2012 or within 30 days from the date of their

AGM, whichever is later.

XBRL filing for the financial year 2011-12 is not enabled by MCA

as yet since the validation tool is still under finalization. Recently,

MCA has come out with the beta version of the validation tool

which is likely to be made effective from 14 October 2012.

MCA XBRL Validation Tool ensures that only those XBRL

documents; that satisfy the requirements of Taxonomy and

Business Rules, are filed with MCA under section 220 of the

Companies Act, 1956. MCA Validation Tool is an important mean

for improving the quality of financial information/disclosures in

XBRL. Successful validation of the instance document is a pre-

requisite before filing the balance sheet and profit & loss account

on MCA portal.

It may, however, be noted that mere successful validation of an

XBRL document by the MCA Validation Tool does not mean that

the provisions under section 211 of the Companies Act, 1956

have fully been complied with. It is important to ensure that this

‘validated’ XBRL document also provides a true and fair view of

the state of affairs of the company as per financial statements

adopted in the AGM. MCA XBRL Validation Tool also provides the

‘human-readable’ pdf version of the XBRL document for ease in

th

th

th

XBRL Filing of Financial StatementsContributed by : (CA Final Student)Ms. Rutvi Solanki

XBRL is the acronym for Extensible Business Reporting Language.

As the name itself suggests, it is a language for presentation of

data which permits easy analysis and interpretation thereby

reducing cost, time and effort. It promotes paperless reporting

and thus is in line with the green initiatives being promoted

world over.

XBRL is only a method of presentation or reporting. It does not

attempt to make any changes in the content to be reported. The

idea behind XBRL is simple. Instead of treating financial

information as a block of text - as in a standard internet page or a

printed document - it provides an identifying label (tag) for each

individual line item of data. This data then becomes computer

readable.

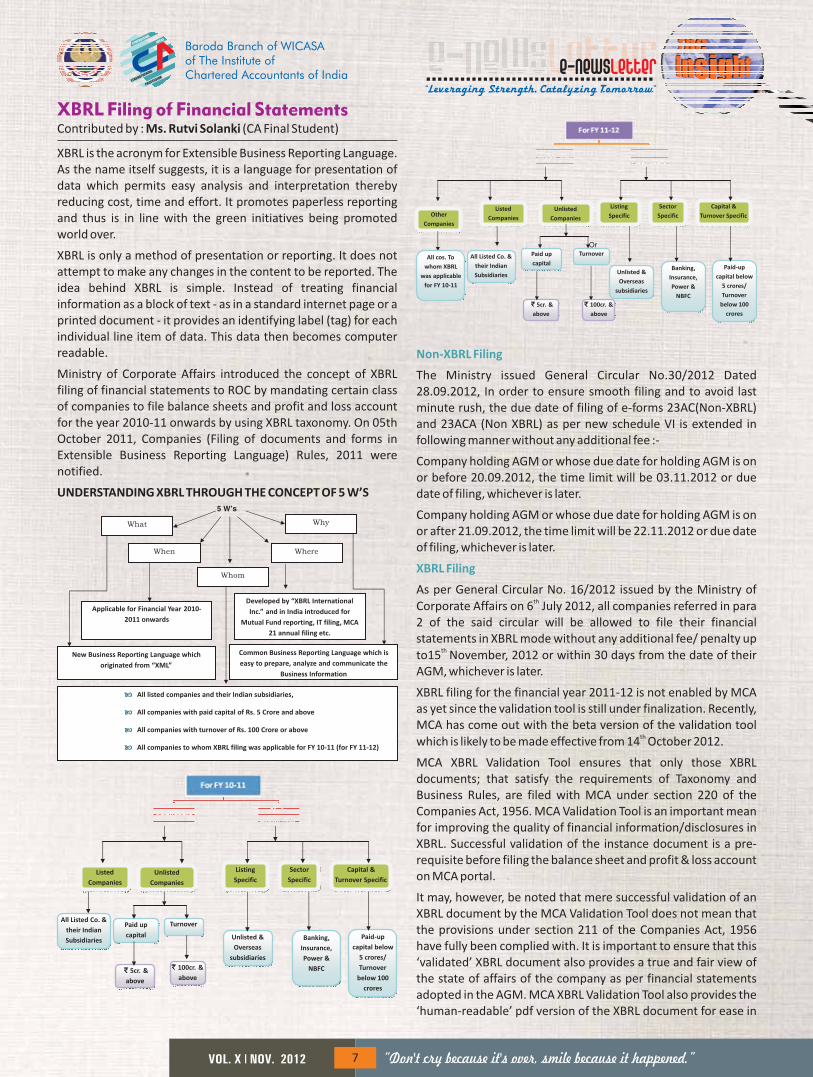

Ministry of Corporate Affairs introduced the concept of XBRL

filing of financial statements to ROC by mandating certain class

of companies to file balance sheets and profit and loss account

for the year 2010-11 onwards by using XBRL taxonomy. On 05th

October 2011, Companies (Filing of documents and forms in

Extensible Business Reporting Language) Rules, 2011 were

notified.

UNDERSTANDING XBRL THROUGH THE CONCEPT OF 5 W’S

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “There is no failure except in no longer trying.”8

authentication and certification of the XBRL document being

filed by the company to MCA.

Ministry of Corporate Affairs have come out with a number of

circulars and notifications in the recent times relating to

maintenance of Cost Accounting Records and Cost Audit. These

circulars and notifications have not only brought remarkable

changes in the applicability of cost accounting and audit rules

but have introduced a number of new requirements like

obtaining of Cost Compliance Report, filing of reports in XBRL

mode, fees for appointment of cost auditor etc.

These announcements and changes have created a lot of

perplexity in the minds of the readers regarding the applicability

of the revised rules. Moreover, since the onus of compliance has

been shifted from the legislator to the company, it becomes even

more vital to understand the changes and their implications.

For ease of understanding, we have divided this section into 2

parts –

1. Maintenance of Cost Accounting Records and Filing of Cost

Compliance Report

2. Appointment of Cost Auditor and filing of Cost Audit

Report

The Companies (Cost Accounting Records) Rules, 2011

were notified on 3 June 2011 vide notification no. G.S.R.

429(E), issued by the Ministry of Corporate Affairs in

exercise of the powers conferred by section 642(1)(b) read

with section 209(1)(d) of the Companies Act, 1956. These

rules are in supersession of all Cost Accounting Record

Rules issued so far.

These rules shall apply to every company, including a

foreign company as defined under section 591 of the Act

which is engaged in the production, processing,

manufacturing, or mining activities and which satisfies any

one of the following criteria

• A company which is a body corporate governed by any

special Act

• Activities or products covered in any of the following

Industry Specific rules:

(a) Cost Accounting Records (Bulk Drugs) Rules, 1974

(b) Cost Accounting Records (Formulations) Rules, 1988

rd

These rules shall not apply to the following class of companies :

XBRL FILING OF COST AUDIT AND COMPLIANCE REPORT

Maintenance of Cost Accounting Records and Filing of Cost

Compliance Report

�

�

Notification

Applicability

(c) Cost Accounting Records (Fertilizers) Rules, 1993

(d) Cost Accounting Records (Sugar) Rules, 1997

(e) Cost Accounting Records (Industrial Alcohol) Rules, 1997

(f) Cost Accounting Records (Electricity Industry) Rules, 2001

(g) Cost Accounting Records (Petroleum Industry) Rules, 2002

(h) Cost Accounting Records (Telecommunications) Rules,

2002

• Whole sale of retail trading activities.

• Banking, financial, leasing, investment, Insurance,

education, healthcare, tourism, travel, hospitality,

recreation, transport services, business/professional

consultancy, IT & IT enabled services, research &

development, postal/courier services, etc. unless any of

these have been specifically covered under any other Cost

Accounting Records Rules.

• Companies engaged in rendering job work operations or

contracting/sub-contracting activities, and are paid only

the job work or conversion charges, such as tailoring,

baking, repairing, painting, printing, constructing,

servicing, etc.

• Companies engaged in the production, processing,

manufacturing or mining activities till such time they

commence their commercial operations.

• Ancillary products/activities of companies incidental to

their main operations (i.e. products/activities that do not

constitute their main line of business) and wherein the

total turnover from the sale of each such ancillary

products/activities do not exceed 2% of the total turnover

of the company or Rs.20 crores, whichever is lower.

� Maintenance of Records

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Lack of time is actually lack of priorities.”9

�

�

�

�

Filing of Compliance Report

Due date for filing under XBRL mode

Format of Compliance Report and Form for filing

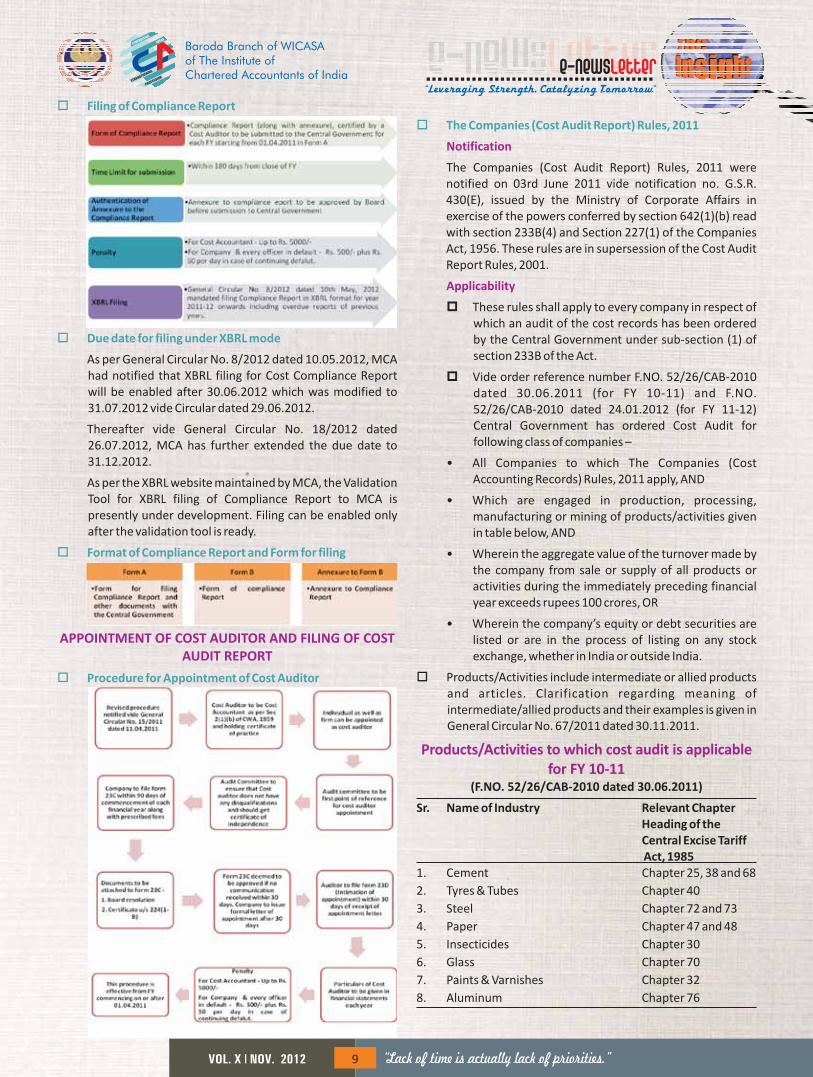

Procedure for Appointment of Cost Auditor

As per General Circular No. 8/2012 dated 10.05.2012, MCA

had notified that XBRL filing for Cost Compliance Report

will be enabled after 30.06.2012 which was modified to

31.07.2012 vide Circular dated 29.06.2012.

Thereafter vide General Circular No. 18/2012 dated

26.07.2012, MCA has further extended the due date to

31.12.2012.

As per the XBRL website maintained by MCA, the Validation

Tool for XBRL filing of Compliance Report to MCA is

presently under development. Filing can be enabled only

after the validation tool is ready.

APPOINTMENT OF COST AUDITOR AND FILING OF COST

AUDIT REPORT

� The Companies (Cost Audit Report) Rules, 2011

Notification

Applicability

Products/Activities to which cost audit is applicable

for FY 10-11(F.NO. 52/26/CAB-2010 dated 30.06.2011)

Sr. Name of Industry Relevant Chapter

Heading of the

Central Excise Tariff

Act, 1985

The Companies (Cost Audit Report) Rules, 2011 were

notified on 03rd June 2011 vide notification no. G.S.R.

430(E), issued by the Ministry of Corporate Affairs in

exercise of the powers conferred by section 642(1)(b) read

with section 233B(4) and Section 227(1) of the Companies

Act, 1956. These rules are in supersession of the Cost Audit

Report Rules, 2001.

These rules shall apply to every company in respect of

which an audit of the cost records has been ordered

by the Central Government under sub-section (1) of

section 233B of the Act.

Vide order reference number F.NO. 52/26/CAB-2010

dated 30.06.2011 (for FY 10-11) and F.NO.

52/26/CAB-2010 dated 24.01.2012 (for FY 11-12)

Central Government has ordered Cost Audit for

following class of companies –

• All Companies to which The Companies (Cost

Accounting Records) Rules, 2011 apply, AND

• Which are engaged in production, processing,

manufacturing or mining of products/activities given

in table below, AND

• Wherein the aggregate value of the turnover made by

the company from sale or supply of all products or

activities during the immediately preceding financial

year exceeds rupees 100 crores, OR

• Wherein the company’s equity or debt securities are

listed or are in the process of listing on any stock

exchange, whether in India or outside India.

Products/Activities include intermediate or allied products

and articles. Clarification regarding meaning of

intermediate/allied products and their examples is given in

General Circular No. 67/2011 dated 30.11.2011.

1. Cement Chapter 25, 38 and 68

2. Tyres & Tubes Chapter 40

3. Steel Chapter 72 and 73

4. Paper Chapter 47 and 48

5. Insecticides Chapter 30

6. Glass Chapter 70

7. Paints & Varnishes Chapter 32

8. Aluminum Chapter 76

�

�

�

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Life isn’t about finding yourself. Life is about creating your-self.”10

Products/Activities to which cost audit is applicable for FY 11-12

F.NO. 52/26/CAB-2010 dated 24.01.2012

1. Jute, cotton, silk, Chapters 50 to 63

woolen or blended fibers/

textiles

2. Edible oil Chapters 12 and 15

seeds and Oils (incl.vanaspati)

3. Packaged food products Chapters 2 to 25 (except

Chapters 5,6,14, 23 & 24)

4. Organic & Inorganic Chemicals Chapters 28,29,32,38& 39

5. Coal & Lignite Chapter 27

6. Mining & Metallurgy Chapters 26 and 74 to 83

of ferrous & (except Chapters 76 and

non‐ferrous metals 77)

7. Tractors & other motor Chapters 84, 85 and 87

vehicles (incl. automotive

components)

8. Plantation Products Chapters 8, 9, 21 and 40,

9. Engineering machinery Chapters 84 and 85

(incl. electrical

& electronic products)

These rules shall not apply to the following class of companies –

• Generation of electricity for captive consumption

• Own manufactured products that are consumed

exclusively by the company for the sole purpose of

production, processing, manufacturing, or mining of its

other product or activities that are subject to cost audit.

• All units located in SEZs, EPZs, FTZs & 100% EOUs (refer

general Circular No. 11/2012 dated 25.05.2012 for more

details)

Ministry of Corporate Affairs has mandated filing of the

Cost Audit Report and Compliance Report from the

financial year 2011-12 onwards (including overdue reports

relating to any previous year) by using the XBRL taxonomy

Sr. Name of Industry Relevant Chapter

Heading of the Central

Excise Tariff Act, 1985

�

�

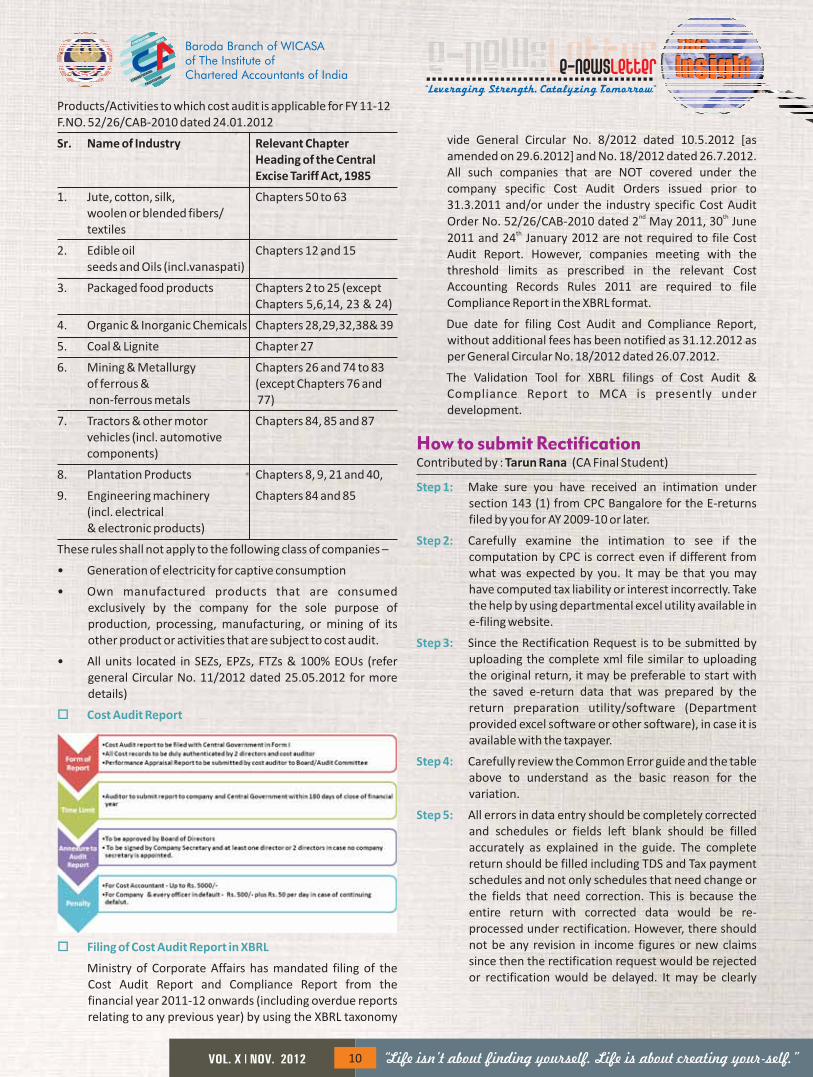

Cost Audit Report

Filing of Cost Audit Report in XBRL

vide General Circular No. 8/2012 dated 10.5.2012 [as

amended on 29.6.2012] and No. 18/2012 dated 26.7.2012.

All such companies that are NOT covered under the

company specific Cost Audit Orders issued prior to

31.3.2011 and/or under the industry specific Cost Audit

Order No. 52/26/CAB-2010 dated 2 May 2011, 30 June

2011 and 24 January 2012 are not required to file Cost

Audit Report. However, companies meeting with the

threshold limits as prescribed in the relevant Cost

Accounting Records Rules 2011 are required to file

Compliance Report in the XBRL format.

Due date for filing Cost Audit and Compliance Report,

without additional fees has been notified as 31.12.2012 as

per General Circular No. 18/2012 dated 26.07.2012.

The Validation Tool for XBRL filings of Cost Audit &

Compliance Report to MCA is presently under

development.

nd th

th

How to submit RectificationContributed by : (CA Final Student)Tarun Rana

Make sure you have received an intimation under

section 143 (1) from CPC Bangalore for the E-returns

filed by you for AY 2009-10 or later.

Carefully examine the intimation to see if the

computation by CPC is correct even if different from

what was expected by you. It may be that you may

have computed tax liability or interest incorrectly. Take

the help by using departmental excel utility available in

e-filing website.

Since the Rectification Request is to be submitted by

uploading the complete xml file similar to uploading

the original return, it may be preferable to start with

the saved e-return data that was prepared by the

return preparation utility/software (Department

provided excel software or other software), in case it is

available with the taxpayer.

Carefully review the Common Error guide and the table

above to understand as the basic reason for the

variation.

All errors in data entry should be completely corrected

and schedules or fields left blank should be filled

accurately as explained in the guide. The complete

return should be filled including TDS and Tax payment

schedules and not only schedules that need change or

the fields that need correction. This is because the

entire return with corrected data would be re-

processed under rectification. However, there should

not be any revision in income figures or new claims

since then the rectification request would be rejected

or rectification would be delayed. It may be clearly

Step 1:

Step 2:

Step 3:

Step 4:

Step 5:

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “I know nothing except the fact of my ignorance.”11

noted that this facility is only

for correct ing mistakes

apparent from record. Fill the

utility as if you are preparing a

new ITR.

After the Return data is

corrected then the xml can be

ge n e rate d . T h i s i s t h e

Rectification XML file.

Log in to

https://incometaxindiaefiling.

gov.in and go to My Account-

> Rectification-> Rectification

upload .

Fi l l in detai ls from the

intimation sheet which will be

verified to ascertain that only

the taxpayer in possession of

the Intimation from CPC would

b e a b l e t o s u b m i t a

rectification request.

Fill in details of Schedules

where changes have been

made and reasons for seeking

rectification. Fill in due date

for filing return, if incorrect as

per intimation sheet. Leave

blank if not applicable. Fill in

details which are not available

in the return form such as

details of 80G donations (not

available in ITR forms for 1, 2

and 3) and Quarter-wise

details of Capital Gains (all four

types- which is not available in

ITRs 2, 3, 4, 5 and 6) only if

applicable. Leave blank if not

applicable. Please note if your

address has been changed in

the rectification XML file, you

should check the address

changed checkbox to ensure

that the new address is

updated else the address as

per old e-return only will be

used.

Now upload the Rectification

XML file. Validations will be

done to ascertain that only

mistakes apparent from

record are sought to be

rectified.

Upon successful upload,

Rectification Request number

and acknowledgement will be

displayed.

Step 6:

Step 7:

Step 8:

Step 9:

Step 10:

Step 11:

on 24 & 25 of November 2012, Saturday - Sunday

Organised by

th th

WICASA Baroda 2012

FIRST STUDENT’SResidential Refresher Course (RRC)

at

Jambughoda, Gujarat.CARAVAN SERAI RESORT,

For registrations and further details, ContactICAI Bhawan, Atladra, Baroda.

Contact : 0265 2681115 / 2680593

DAY ONE – 24 November 2012

DAY TWO – 25 November 2012

th

th

Timing Activity

Timing Activity

09:00 to 10:00 hrs. - Breakfast

10:00 to 13:00 hrs. Technical Session – Discussion on Case Studies of Direct Taxes

13:00 to 14:00 hrs. Lunch

14:00 to 16:30 hrs. Group Discussion on a Technical Topic – Direct Taxes

16:30 to 18:30 hrs. Bush Trekking in Jungle /Flying Fox / Swimming / Cricket Match

/ Cycling Badminton

19:00 to 22:00 hrs. Pool side DJ Party

22:00 to 23:30 hrs. Camp Fire with Dinner

08:00 to 09:30 hrs. Swimming + Breakfast

09:30 to 11:00 hrs. Technical Session – Issues in Accounting Standards (AS 2, 9,

11, 17, 18 & 22)

11:00 to 12:30 hrs. Motivational Lecture

12:30 to 13:30 hrs. Lunch

13:30 to 17:30 Visit to Pavagadh & Champaner (Heritage Sites)

• Baroda Branch of WICASA 2012 is organising students Residential Refresher Course (RRC)

for the first time in history of Baroda, ICAI.

• Fees of Rs. 1000 /- per student is inclusive of Travelling, Accommodation, Food and all

other facilities.

-

-

-

-

-

-

-

-

-

-

-

e-NewsLetter“Leveraging Strength, Catalyzing Tomorrow”

Baroda Branch of WICASA

of The Institute of

Chartered Accountants of India

VOL. X NOV. 2012l “Glory is fleeting, but obscurity is forever."12

PHOTOFLASHPHOTOFLASH

CA Mayur Thakkar at Full Day Seminar on Accounting -

Amalgamation (01.10.2012)

CA Amit Shah at Half Day Seminar on

Financial Management (05.10.2012)

CA Nirav Shah at Full Day Seminar

on Taxation (06.10.2012)

Dr.J.K.Pandya at Full Day Seminar on

Accounts (07.10.2012)

Mr. Manish Shukla at Half Day Seminar

on Information Technology (18.10.2012)Visit to Trade Fair (31.10.2012)

CA Anu Agrawal at Full Day Seminar on Costing (12.10.2012) Mock Test - CA Final Students

Mock Test - CA IPCE & PCC Students Study Circle Meeting by Mr. Vahid Langawala on LLP (29.10.2012)

![C L GOLCHHA & ASSOCIATES [ CHARTERED ACCOUNTANTS ] Firm Profile Presentation CHARTERED ACCOUNTANTS C L GOLCHHA & ASSOCIATES](https://img.pdfslide.net/doc/110x75/5697c0301a28abf838cdac32/c-l-golchha-associates-chartered-accountants-firm-profile-presentation.jpg)