Embed Size (px)

Citation preview

THE INSTITUTE OF CHARTERED ACCOUNTANTS

OF NIGERIA

NOVEMBER 2010 PROFESSIONAL EXAMINATION II

Question Papers

Suggested Solutions

Plus

Examiners‟ Reports

PATHFINDER

2

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

FOREWORD

This issue of the PATHFINDER is published principally, in response to a growing

demand for an aid to:

(i) Candidates preparing to write future examinations of the Institute of Chartered

Accountants of Nigeria (ICAN);

(ii) Unsuccessful candidates in the identification of those areas in which they lost

marks and need to improve their knowledge and presentation;

(iii) Lecturers and students interested in acquisition of knowledge in the relevant

subjects contained herein; and

(iv) The profession; in improving pre-examinations and screening processes, and

thus the professional performance of candidates.

The answers provided in this publication do not exhaust all possible alternative

approaches to solving these questions. Efforts had been made to use the methods,

which will save much of the scarce examination time. Also, in order to facilitate

teaching, questions may be altered slightly so that some principles or application of

them may be more clearly demonstrated.

It is hoped that the suggested answers will prove to be of tremendous assistance to

students and those who assist them in their preparations for the Institute‟s

Examinations.

NOTES

Although these suggested solutions have been published

under the Institute‟s name, they do not represent the views of

the Council of the Institute. The suggested solutions are

entirely the responsibility of their authors and the Institute

will not enter into any correspondence on them.

PATHFINDER

3

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

TABLE OF CONTENTS

SUBJECT PAGES

FINANCIAL REPORTING AND ETHICS 4 – 27

STRATEGIC FINANCIAL MANAGEMENT 28 – 59

ADVANCED TAXATION

PUBLIC SECTOR ACCOUNING & FINANCE

59 – 90

60 - 91

MULTI-DISPINARY CASE STUDY 92 - 178

PATHFINDER

4

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

ICAN/102/Q/2 EXAMINATION NO...................................

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF NIGERIA

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

FINANCIAL REPORTING AND ETHICS

SECTION A: Attempt All Questions

PART I MULTIPLE- CHOICE QUESTIONS (20 MARKS)

1. Which of the following options is excluded from the class of rational agents, and

hence cannot be subjected to moral judgement?

(i) Moral minors

(ii) The insane

(iii) The senile

A. (i) and (ii) only

B. (ii) and (iii) only

C. (i) and (iii) only

D. (ii) only

E. (i), (ii) and (iii)

2. An action is good if only it promotes happiness for the greatest number of

people. This is an example of which ONE of these ethical theories?

A. Contractarianism

B. Utilitarianism

C. Majoritarian Morality

D. Ethical Considerationism

E. Sympathetic Morality

3. Government grants available to an enterprise are considered for inclusion in the

accounts

A. if the grant is not a financing device.

B. if it is to enable the government participate in the ownership.

C. if the grant is recognised as government assistance to the organization.

D. where there is reasonable assurance that the enterprise will comply with

the conditions attached to them.

E. where contingency related to a government grant is recognised.

PATHFINDER

5

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

4. The amount of contract revenue may increase or decrease from one period to

the next in all of the following, EXCEPT

A. a contractor and a customer may agree variations of claims in the period

subsequent to that which the contract was initially agreed.

B. the amount of revenue agreed in a fixed price contract may increase as a

result of cost escalation clauses.

C. the amount of contract revenue may decrease as a result of penalties

arising from delay caused by the contractor.

D. when a fixed price contract involves a fixed price per unit of output,

contractor revenue increases as the number of units is increased.

E. negotiations have reached an advanced stage such that the customer will

accept the claim.

5. Undisclosed assets revaluation surplus in the Financial Statements of a

company is known as

A. revaluation reserve.

B. capital reserve.

C. secret/hidden reserve.

D. asset revaluation reserve.

E. contingency reserve.

6. All the following are forms of business combinations, EXCEPT

A. merger.

B. acquisition.

C. amalgamation.

D. absorption.

E. joint Venture.

PATHFINDER

6

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

7. The theory that holds that it is morally acceptable for one to do what one feels

is in one‟s self-interest, is an example of which of these moral theories?

A. Selfish Immorality

B. Humanistic Morality

C. Ethical Egoism

D. Ethical Altruism

E. Unethical Egoism

8. The claim that there is only one correct moral code or system of moral principle

which supplies the single correct answer to every moral question, is attributed

to which of these?

A. Moral Subjectivism

B. Moral Objectivism

C. Moral Totality

D. Moral Globalization

E. Moral Uniqueness

9. The statement that there is no such thing as correct or incorrect moral code for

human conduct, is ascribed to which of these?

A. Moral Relativism

B. Moral Universalism

C. Moral Non-Wrongness

D. Moral Nihilism

E. Moral Incorrigibility

10. Which of these moral theories that holds that human nature determines the

correct moral laws of nature that human beings should follow?

A. Moral Fellowship

B. Natural Morality

C. Natural Law Theory

D. Natural Egoism

E. Ethical Naturalism

PATHFINDER

7

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

11. The following statements are true of a parent company, EXCEPT

A. the financial statements of a group are presented as those of a single

economic entity.

B. control is the power to govern the financial and operating policies of an

entity so as to obtain benefits from its activities.

C. a group is a parent and all its subsidiaries.

D. non-controlling interest is the equity in a subsidiary not attributable

directly or indirectly to a parent.

E. a parent is an entity that must have at least three subsidiaries.

12. The following are the generally recognised potential problems of using ratios

for comparison purposes, EXCEPT

A. inconsistent definition of ratios.

B. financial statements that have been deliberately manipulated.

C. different companies may adopt different accounting policies.

D. different managerial policies e.g. different companies offer customers

different payment terms.

E. profit for the year may result in higher cash flow.

13. Potential users of financial reports do NOT include ONE of the following:

A. Equity investors

B. Educationists

C. Creditors

D. Suppliers

E. Employees

14. In using the accounting ratios, comparison is commonly made between all BUT

ONE of the following:

A. Previous accounting periods

B. Other companies (mostly in the same type of business)

C. Budget and expectations

PATHFINDER

8

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

D. Government statistics

E. Emolument of the chief executive

15. The integration of social and ethical criteria into investors‟ investment decision

is known as

A. ethical Investing.

B. social Investing.

C. moral Investing.

D. socio-ethical Investing.

E. socio-moral Investing.

16. The use of ethical, social and environmental criteria in the selection and

management of investment, generally consisting of company shares is known as

A. ethical investment.

B. social investment.

C. moral investment.

D. socio-ethical investment.

E. socio-moral investment.

17. One of the fundamental precepts of Corporate Social Responsibility which

requires business leaders to acknowledge and accept the legitimate claims,

rights and needs of other groups in society is known as

A. Voluntary Social Responsibility.

B. Involuntary Social Responsibility.

C. Unlimited Social Responsibility.

D. Limited Social Responsibility.

E. Liberal Social Responsibility.

PATHFINDER

9

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

18. The basic principles of a good corporate governance system include:

i. Transparency

ii. Competence

iii. Integrity

iv. Proper alignment of interests and allocation of responsibilities

A. i and iv only

B. ii and iii only

C. i, ii and iii only

D. i, ii, iii and iv

E. ii, iii and iv only

19. The framework for ethical decision making that is useful for exploring ethical

dilemmas and identifying ethical courses of action does NOT include ONE of the

following:

A. Recognition of an ethical issue

B. Evaluation of alternative actions

C. Making a decision and testing it

D. Acting and reflecting on the outcome

E. Engaging a professional person for consultation

20. Which of the following is ordinarily computed and reported as part of the

financial statements of a large organisation?

A. Current ratio

B. Return on assets

C. Book value per share

D. Earnings per share

E. Price earnings ratio

PATHFINDER

10

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

PART II SHORT-ANSWER QUESTIONS (20 MARKS)

1. Responsibility is divided into Retrospective Responsibility and ………..

Responsibility.

2. The action that purports to benefit others primarily without any form of egoism

is ……………...

3. A risk management technique that mixes a wide variety of investments within a

portfolio is called ..........................

4. The duration between the purchase of a firm‟s inventory and the collection of

account receivable for a sale of that inventory is known as .........................

5. Kabir Ventures Ltd. had sales last year of N530 million including cash sales of

N50 million. If its average collection period was 40 days, its ending account

receivable is closest to ..............................

6. A scheme approved by the court in which the nominal value of a company‟s

paid up share capital is reduced is termed ......................

7. The process through which a person learns the values and behaviour patterns

considered appropriate by an organisation or group is called …....…………..

8. The Utilitarian theory of justice ties the question of economic distribution to the

promotion of ………......……

9. An approach to Business Ethics that attempts to change economic concepts with

the aim of facilitating moral action is termed ....…………….

10. The Libertarian associates justice with ........………….

11. Payments made to a parent company by a subsidiary out of pre-acquisition

profits are known as ...........................

12. The Institute of Chartered Accountants of Nigeria (ICAN) requires that its

members who are in Public Practice take up insurance policy with reputable

insurance companies. What is the name of the insurance policy required?

13. A component of an entity that engages in business activities from which it may

earn revenue and incur expenses is described by IFRS 8 as ..........................

PATHFINDER

11

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

14. The organisation which is empowered by law to incorporate, register and wind-

up companies in Nigeria is called ....................................

15. Two features of a business entity are .......................... and .................................

16. The standards of behaviour that groups expect of their members is referred to as

................................

17. Ethics must be promoted and institutionalized in an organization in order to

build credibility and ...............................

18. The ethical challenge in companies is often triggered by .............................

19. A method of accounting whereby an interest in a jointly controlled entity is

initially recorded at cost and adjusted thereafter for the post-acquisition change

in the venture‟s share of net assets of the jointly controlled entity is called

..........

20. The bringing together of separate entities or businesses into one operating

entity is called ...............................

PATHFINDER

12

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

SECTION B – ATTEMPT QUESTION ONE AND ANY OTHER THREE (60 MARKS)

QUESTION 1 –CASE STUDY

Topic: Variance Reporting

Characters: Olabisi, Director of Manufacturing and Computer Services

Tunde, Manager, Manufacturing Department 207

Bose, Supervisor, Manufacturing Department 201

Olabisi has been with Peace Auto Parts Manufacturing Company for 23 years. Recently,

he was appointed Director of Manufacturing and Computer Services. In just six weeks

in this new position, he has moved to reduce the amount of information provided to

manufacturing department managers by 60 percent. He argues that excess data is

distracting, expensive to provide and usually unused.

Tunde has been the Department Manager for 12 years. During a coffee break with

some of his department production supervisors, Tunde is quite vocal about the change.

“Who‟s this guy Olabisi to tell us what data we need? He needs to be out here for a few

weeks to find out what it‟s like. Keep it quiet, but I‟ve got a contact in Computer

Services who‟ll get me all the data analysis I want for just a N3,000 bill each month.

It‟s a good deal, and Olabisi will never know. How does he expect us to make good

decisions about those variances without enough data? This guy in Computer Services

can get any of you data, if you need it.”

Bose, overhearing Tunde, is shocked. “Is that ethical, Tunde? Do you really need that

extra data? Can‟t you get the information without going around Olabisi? I sure don‟t

want to pay for anything Mr. Olabisi doesn‟t want me to have.”

“Bose , you've only been a supervisor for six months,” Tunde replies. “It‟s just how the

firm operates. Try it, and you'll see it‟s worth the N3,000. You can't make good

decisions with the stuff Olabisi gives us now.” Bose doesn't respond, and the coffee

break ends with people returning to their jobs.

Later that evening, Bose begins to think about what Tunde said. She knows that he is a

good manager, but she does not want to have to buy information to do her job

correctly. Tomorrow, she is scheduled for a staff meeting with Mr. Olabisi. She is

uncertain about what to do or say, if anything.

PATHFINDER

13

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

Required

(a) What are the relevant facts? (3 marks)

(b) What are the ethical issues? (2 marks)

(c) Applying the Kant‟s Categorical Imperative, advise Bose on the

action(s) she should take. (10 marks)

(Total 15 marks)

QUESTION 2

a) Explain briefly Ethical Issues in business. (5 marks)

b) State TWO examples each of ethical issues relating to the following areas:

i. Society

ii. Internal and industry practice

iii. Marketing

iv. Product

v. Supply chain (10 marks)

(Total 15 marks)

QUESTION 3

a) Explain the term “conflict of interest”. (7 marks)

b) Situate conflict of interest within the accounting profession, especially as an

external auditor to a firm (8 marks)

(Total 15 marks)

QUESTION 4

Why should an accountant get involved in the study of ethics, given that all human

beings, including accountants, have moral beliefs they follow? .. (15 Marks)

PATHFINDER

14

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

QUESTION 5

a) State the meaning of the following terms as contained in IAS 27 - Consolidated and

Separate Financial Statements:

i. Consolidated Financial Statements

ii. Subsidiary

iii. Non controlling interest

iv. Control (6 Marks)

b) Explain briefly THREE of the disclosure requirements in Consolidated Financial

Statements. (9 marks)

(Total 15 Marks)

QUESTION 6

Identify and explain FIVE potential users of financial reports and their information

needs (Total 15 marks)

PATHFINDER

15

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

SECTION A

PART I: SOLUTIONS TO MULTIPLE CHOICE QUESTIONS

1. E

2. B

3. D

4. E

5. C

6. E

7. C

8. B

9. D

10. C

11. E

12. E

13. B

14. E

15. A

16. B

17. A

18. D

19. E

20. D

EXAMINERS‟ REPORT

The questions test various aspects of the syllabus. The candidates demonstrated clear

understanding of them. This translated into good performance by most candidates.

PART II: SOLUTIONS TO SHORT ANSWER QUESTIONS

1. Prospective

2. Altruism

3. Diversification

4. Cash conversion cycle or Cash operating cycle

5. N52.6million or N53million {(40/365 x (530-50) million}

6. Capital reduction

PATHFINDER

16

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

7. Socialization or Societalisation

8. Social Well-being/Happiness

9. Prescriptive or Normative

10. Liberty or Individual right or Entitlement

11. Pre-acquisition dividends

12. Professional Indemnity Insurance Policy

13. Operating segment or Reportable segment

14. Corporate Affairs Commission (CAC)

15. Legal status, Ownership of assets and Profit oriented (any two)

16. Group norms or Code of Conduct or Professional Ethics

17. Public trust/Confidence

18. Financial problems

19. Equity method

20. Business combination.

EXAMINERS‟ REPORT

The questions test most areas of the syllabus with particular emphasis on effective use

of terminologies in Ethics.

The performance of candidates was fair. Candidates are advised to make use of their

Study Packs and recommended texts on the subject to improve on their performance in

future.

SOLUTIONS TO SECTION B

QUESTION 1 – CASE STUDY

(a) Relevant facts about the Case:

(i) Olabisi has reduced the amount of data on Reports sent to departments.

(ii) Tunde secretly buys data from someone in the Computer Services

Department to supplement the variance report he receives.

(iii) Bose knows of Tunde practice of buying data, thinks it is unethical, but

does not know what to do about it.

(iv) Olabisi, the Director of Manufacturing and Computer Services is a long

standing employee of the organisation for the past 23 years.

PATHFINDER

17

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

(v) Olabisi was recently appointed as the Director of Manufacturing and

Computer Services.

(vi) He has moved to reduce the amount of information provided to Managers

by 60%.

(vii) Tunde has been the Departmental Manager of the Organisation for 12

years, and he advised Bose to obtain information at a cost.

(viii) Bose is the Supervisor, Manufacturing Department, and she is in a

dilemma as to whether she should yield to Tunde‟s advice or not.

(b) Ethical Issues Involved:

(i) Should Tunde buy data for his use in managing his Department?

(ii) Should Bose tell Olabisi (or any one else) what Tunde is doing?

(iii) Should Bose use the data source in Computer Services?

(iv) The appropriateness of disobeying a superior officer‟s instruction.

(v) The superior‟s intention of obtaining the information without cost from

undisclosed source.

(c) Emmanuel Kant made a major contribution to Ethics of duty. For him, the moral

values of actions, decisions and propositions are not dependent on a particular

situation or on the consequences of the action. Rather, morality was simply a

question of certain eternal, abstract and unchangeable principles that humans

should apply to all ethical problems.

To be moral, therefore, one must consciously act according to rules previously

calculated by „reason‟ to be right or just, and the motive for observing those

rules must be respected for duty alone. He, however, articulated the categorical

imperative as a theoretical framework to guide our commitment to duty. By this

he meant that this theoretical framework should be applied to every moral issue

regardless of who is involved, profits and who is harmed by the principles once

applied in specific situations.

The „categorical imperative‟ consists mainly of three formulations. We would

make use of the first two formulations in this case.

The first formulation states, “Act only according to that maxim by which you can

at the same time will that it should become a universal law.”

This means that for any action to be morally right, it must be capable of being

consistently universalisable. By implication, if any action is moral for me, it

must be moral for anyone else; everyone should be able to follow the same

underlying principle, it gives no room for any exceptions.

PATHFINDER

18

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

The second formulation otherwise referred to as the principle of humanity goes

thus: “Act so that you treat humanity, whether is your own person or in that of

another, always as an end and never as a means only.”

Kant‟s emphasis here is on the rational nature of humans as free, intelligent

and self directing beings. This nature of rationality is the basis for his/her value

as an end in itself. Because of this, “a rational being is worthwhile, has dignity

and is worthy of respect. Hence each person should be treated by every person

as an end, with respect and dignity …” This formulation forbids us to „use‟

people and manipulate them merely as means to our own ends.

Consider the different possible alternative actions that Bose can take, which

may include:

(i) Telling Mr. Olabisi of the situation when she meets with him tomorrow.

(ii) Asking Tunde to stop his data purchases.

(iii) Turning Tunde in to Mr. Olabisi‟s anonymously.

(iv) Buying information for herself if and when she needs it.

(v) Do nothing.

Given the main tenets of Kant‟s Categorical Imperative, Bose has a duty to tell

the truth always, to uncover any unethical practice in her organisation not

minding who will be affected and to protect another person from any form of

manipulations for selfish interests.

The best option, therefore, would be for Bose to first confront Tunde and ask

him to stop his data purchases. The reason is that, a lot of frictions and crises

could be avoided if Tunde heeds to this advice.

But Bose should be smart enough to decipher and discern what Tunde‟s

reaction would likely be so that she would not have failed to prevent any harm

being done on Olabisi. By implication, she would have to tell Olabisi what

Tunde‟s is. Going by Kant‟s first formulation of the Categorical Imperative, this

would be a good option because if she were Olabisi, she would have wished

that someone exposes such unethical intent to her.

Finally, I will strongly advise Bose against turning Tunde in to Olabisi

anonymously. The reason being because, it would be difficult for her to remain

anonymous since she had earlier on kicked against Tunde‟s decisions.

PATHFINDER

19

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

EXAMINERS‟ REPORT

The question tests candidates‟ understanding of Kant‟s Categorical Imperative

principles in Ethics. It also tests candidates‟ ability to identify ethical issues in the Case

Study.

The overall performance of the candidates was poor.

The commonest pitfalls of the candidates include:

(i) Lack of awareness of Kant‟s Categorical Imperative and its application.

(ii) Inability to identify ethical issues in the Case Study.

It is important for candidates to appreciate that examiners would continue to examine

questions which require application of ethical principles; hence, they are advised to

make use of recommended texts and journals on ethics. These would expose them to

relevant ethical principles and how they can be applied within the context of the

accounting profession.

QUESTION 2

(a) Ethical issues are problems, situations, or opportunities that require a person or

organisation to choose among several actions that must be evaluated as right or

wrong. Most ethical issues relate to conflicts of interest, fairness and honesty,

communications, or organisational relationship both internal and external.

In general, businesses seem to be more concerned with ethical issues that could

hurt the firm through negative publicity, such as bribery, and issues related to

consumers and the general public, such as environmental impact. Scandals related

to bribes, deceptive communications, and ecological disasters have severely

damaged public trust in business institutions and have helped to focus attention on

activities that could do further harm.

Therefore, studying ethical issues helps to prepare us to identify potential problems

within an organisation and to understand alternatives and ethical solutions to the

problem.

PATHFINDER

20

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

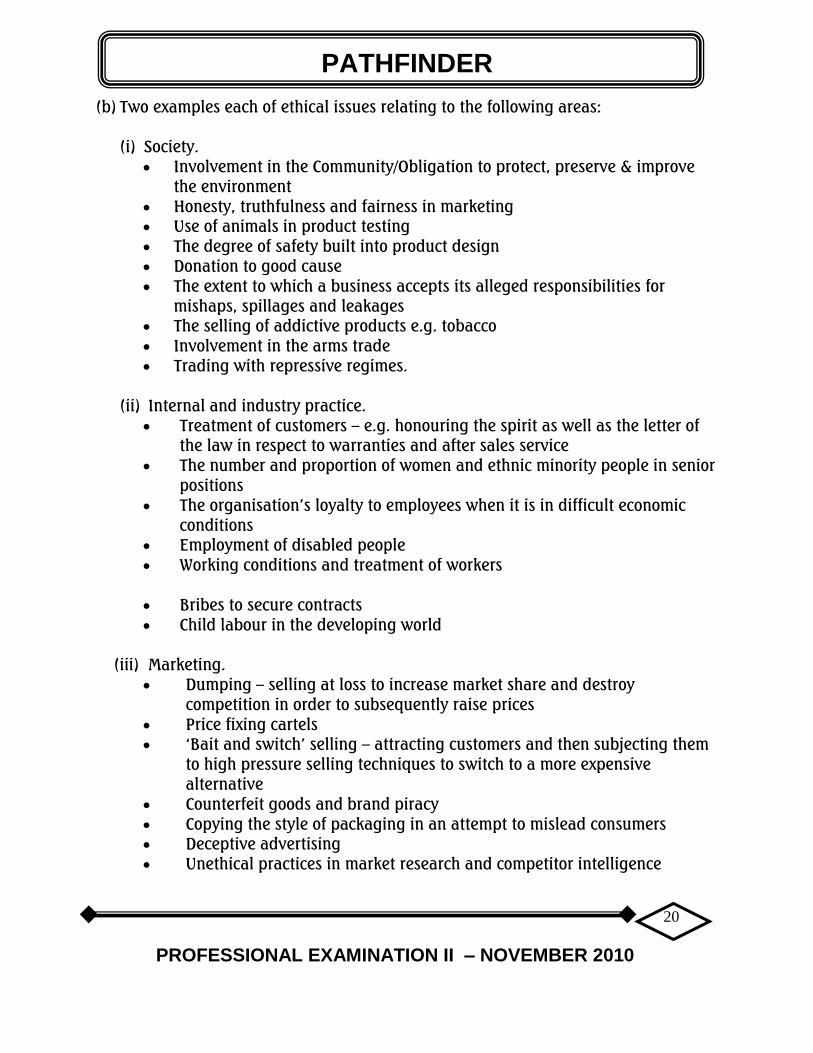

(b) Two examples each of ethical issues relating to the following areas:

(i) Society.

Involvement in the Community/Obligation to protect, preserve & improve

the environment

Honesty, truthfulness and fairness in marketing

Use of animals in product testing

The degree of safety built into product design

Donation to good cause

The extent to which a business accepts its alleged responsibilities for

mishaps, spillages and leakages

The selling of addictive products e.g. tobacco

Involvement in the arms trade

Trading with repressive regimes.

(ii) Internal and industry practice.

Treatment of customers – e.g. honouring the spirit as well as the letter of

the law in respect to warranties and after sales service

The number and proportion of women and ethnic minority people in senior

positions

The organisation‟s loyalty to employees when it is in difficult economic

conditions

Employment of disabled people

Working conditions and treatment of workers

Bribes to secure contracts

Child labour in the developing world

(iii) Marketing.

Dumping – selling at loss to increase market share and destroy

competition in order to subsequently raise prices

Price fixing cartels

„Bait and switch‟ selling – attracting customers and then subjecting them

to high pressure selling techniques to switch to a more expensive

alternative

Counterfeit goods and brand piracy

Copying the style of packaging in an attempt to mislead consumers

Deceptive advertising

Unethical practices in market research and competitor intelligence

PATHFINDER

21

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

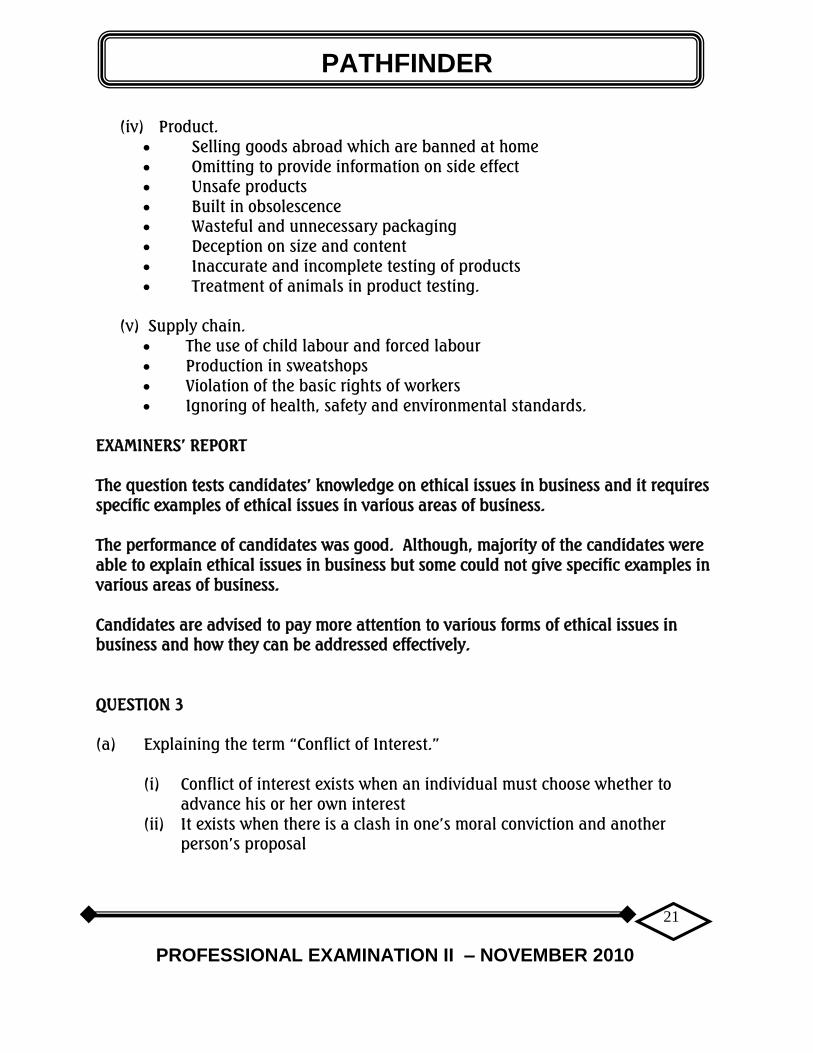

(iv) Product.

Selling goods abroad which are banned at home

Omitting to provide information on side effect

Unsafe products

Built in obsolescence

Wasteful and unnecessary packaging

Deception on size and content

Inaccurate and incomplete testing of products

Treatment of animals in product testing.

(v) Supply chain.

The use of child labour and forced labour

Production in sweatshops

Violation of the basic rights of workers

Ignoring of health, safety and environmental standards.

EXAMINERS‟ REPORT

The question tests candidates‟ knowledge on ethical issues in business and it requires

specific examples of ethical issues in various areas of business.

The performance of candidates was good. Although, majority of the candidates were

able to explain ethical issues in business but some could not give specific examples in

various areas of business.

Candidates are advised to pay more attention to various forms of ethical issues in

business and how they can be addressed effectively.

QUESTION 3

(a) Explaining the term “Conflict of Interest.”

(i) Conflict of interest exists when an individual must choose whether to

advance his or her own interest

(ii) It exists when there is a clash in one‟s moral conviction and another

person‟s proposal

PATHFINDER

22

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

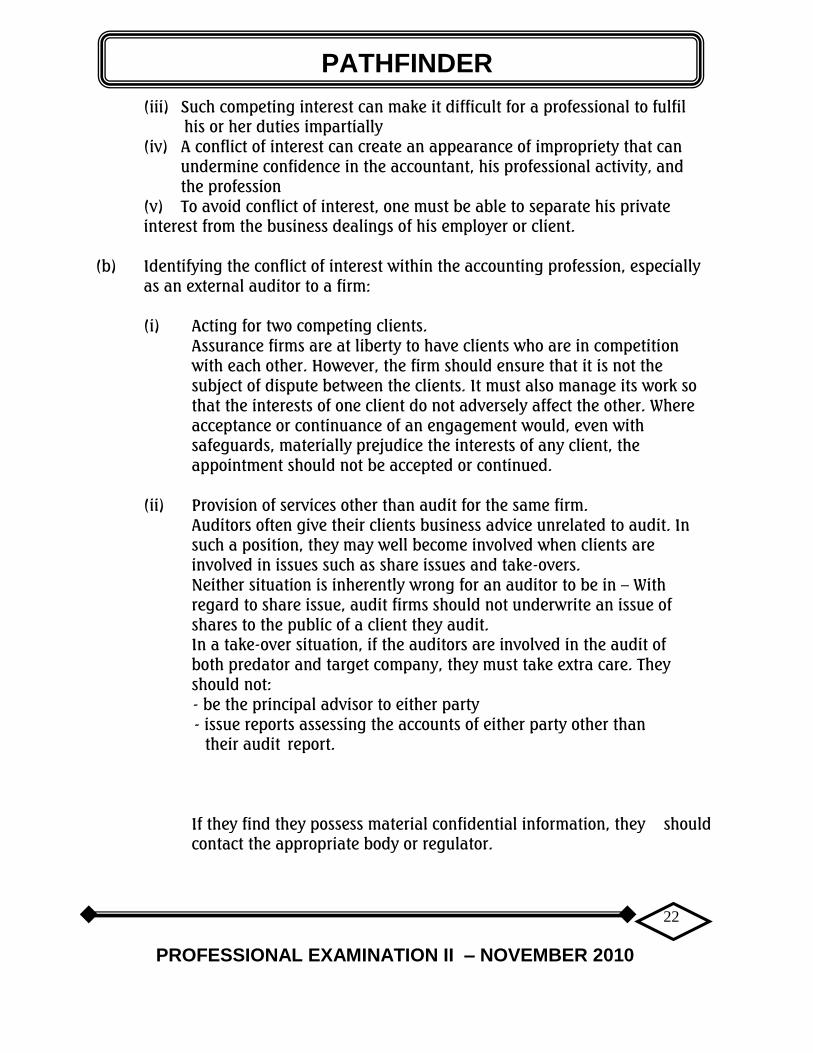

(iii) Such competing interest can make it difficult for a professional to fulfil

his or her duties impartially

(iv) A conflict of interest can create an appearance of impropriety that can

undermine confidence in the accountant, his professional activity, and

the profession

(v) To avoid conflict of interest, one must be able to separate his private

interest from the business dealings of his employer or client.

(b) Identifying the conflict of interest within the accounting profession, especially

as an external auditor to a firm:

(i) Acting for two competing clients.

Assurance firms are at liberty to have clients who are in competition

with each other. However, the firm should ensure that it is not the

subject of dispute between the clients. It must also manage its work so

that the interests of one client do not adversely affect the other. Where

acceptance or continuance of an engagement would, even with

safeguards, materially prejudice the interests of any client, the

appointment should not be accepted or continued.

(ii) Provision of services other than audit for the same firm.

Auditors often give their clients business advice unrelated to audit. In

such a position, they may well become involved when clients are

involved in issues such as share issues and take-overs.

Neither situation is inherently wrong for an auditor to be in – With

regard to share issue, audit firms should not underwrite an issue of

shares to the public of a client they audit.

In a take-over situation, if the auditors are involved in the audit of

both predator and target company, they must take extra care. They

should not:

- be the principal advisor to either party

- issue reports assessing the accounts of either party other than

their audit report.

If they find they possess material confidential information, they should

contact the appropriate body or regulator.

PATHFINDER

23

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

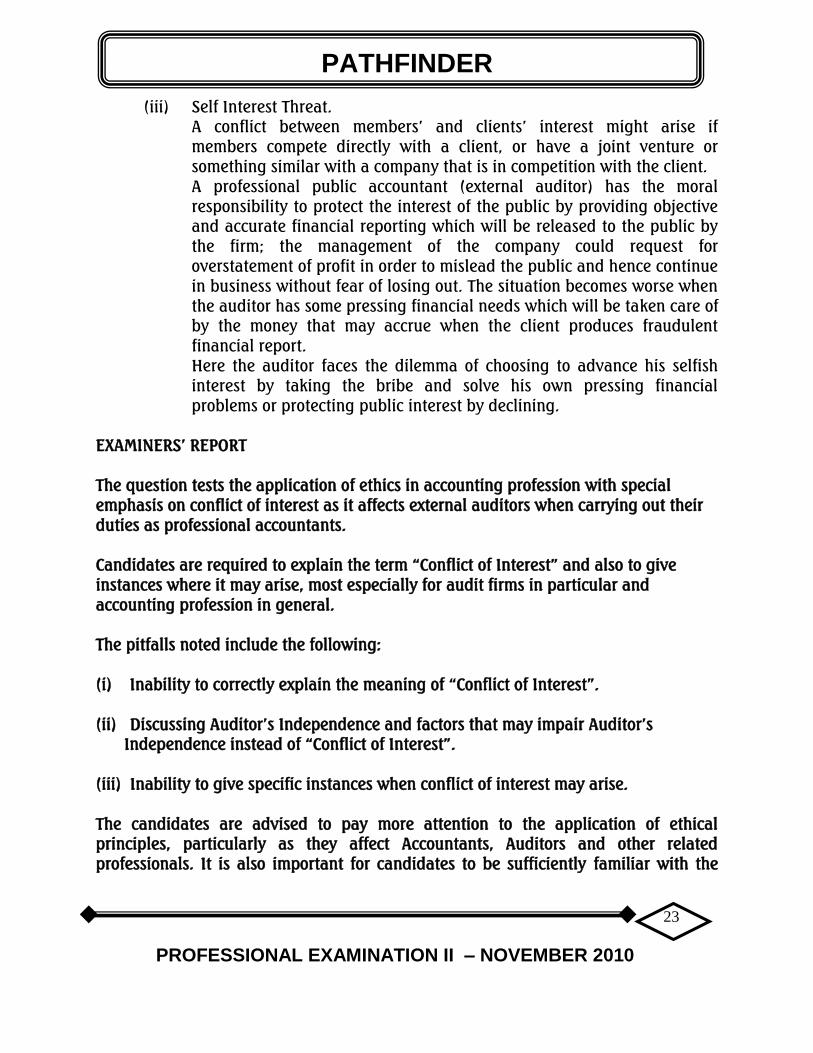

(iii) Self Interest Threat.

A conflict between members‟ and clients‟ interest might arise if

members compete directly with a client, or have a joint venture or

something similar with a company that is in competition with the client.

A professional public accountant (external auditor) has the moral

responsibility to protect the interest of the public by providing objective

and accurate financial reporting which will be released to the public by

the firm; the management of the company could request for

overstatement of profit in order to mislead the public and hence continue

in business without fear of losing out. The situation becomes worse when

the auditor has some pressing financial needs which will be taken care of

by the money that may accrue when the client produces fraudulent

financial report.

Here the auditor faces the dilemma of choosing to advance his selfish

interest by taking the bribe and solve his own pressing financial

problems or protecting public interest by declining.

EXAMINERS‟ REPORT

The question tests the application of ethics in accounting profession with special

emphasis on conflict of interest as it affects external auditors when carrying out their

duties as professional accountants.

Candidates are required to explain the term “Conflict of Interest” and also to give

instances where it may arise, most especially for audit firms in particular and

accounting profession in general.

The pitfalls noted include the following:

(i) Inability to correctly explain the meaning of “Conflict of Interest”.

(ii) Discussing Auditor‟s Independence and factors that may impair Auditor‟s

Independence instead of “Conflict of Interest”.

(iii) Inability to give specific instances when conflict of interest may arise.

The candidates are advised to pay more attention to the application of ethical

principles, particularly as they affect Accountants, Auditors and other related

professionals. It is also important for candidates to be sufficiently familiar with the

PATHFINDER

24

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

basic ethical problems that can arise as they carry out their professional duties as

Accountants.

QUESTION 4

Accountants cannot afford not to study ethics for the following reasons:

(i) Possibility of conflicting ethical principles:

Due to conflicting ethical principles it may be difficult to determine what to do

in certain circumstances. In this case, ethics can provide insights into how to

adjudicate between conflicting principles and show why certain courses of action

are more desirable than others.

(ii) Individual Accountant may hold some inadequate beliefs or cling to inadequate

values.

Subjecting those beliefs or values to ethical analysis may show their inadequacy.

It could be that at one time you thought some things were wrong but now you

think they are acceptable, or vice versa. For instance, some would claim that

while accounting firms operate within the letter of the law in attesting to the fact

that companies followed Generally Accepted Accounting Principles (GAAP), they

had an ethical obligation to encourage more realistic financial pictures. Also, at

one time accountants thought it unacceptable to advertise. Today, it seems a

justifiable practice. So, ethical reflection can make us more knowledgeable and

conscientious in moral matters.

(iii) Development of abilities needed to deal with ethical conflicts.

The study of ethics helps us to understand whether and why our opinions are

worth holding on to. As an Accountant, what do I do when I need to choose

between keeping a job and violating professional responsibilities? Ethics

provides the Accountant with the likely thing to do when his responsibility to his

family conflicts with his professional responsibility.

(iv) Recognition of issues in accounting that have ethical implications.

Some moral beliefs an individual accountant holds may be inadequate because

they are simple beliefs about complex issues. The study of ethics can help in

sorting out these complex issues, by seeing what principles operate in those

cases.

PATHFINDER

25

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

(v) Identification and application of basic ethical principles.

The final reason for studying ethics is to learn to identify the basic ethical

principles that can be applied to action. That should help develop the skill of

determining what should be done and an understanding of why it should be

done. When faced with trying to decide what to do in a difficult situation, it is

often helpful to have a checklist for basic questions or considerations that need to

be raised and applied to the situation to help determine what the outcome

should be. Just as one learns the principles of accounting in order to apply them

to specific situations, one also needs to learn the principles of ethics that govern

human behaviour in order to apply them when faced with difficult ethical

situations. The study of ethics makes us aware of the number and types of moral

principles that can be used in determining what should be done in a situation

involving ethical matters.

EXAMINERS‟ REPORT

The question tests the purpose of studying ethics by Accountants. It also tests the

importance of ethics to the accountancy profession in general.

Candidates are required to explain possibility of conflicting ethical principles, and also

to state the reasons why some Accountants may hold inadequate beliefs when faced

with issues in accounting that have ethical implications.

Most candidates demonstrated inadequate understanding of the question and

performance was generally poor.

The major pitfall was that candidates misinterpreted the question and they were

discussing ICAN Code of Conduct instead of answering the question.

Candidates are advised to study questions properly before answering them.

It is also important for candidates to appreciate that Ethics is an important aspect of

this paper; therefore, special attention must be paid to this part of the Syllabus for

better performance in future.

PATHFINDER

26

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

QUESTION 5

(a). (i) Consolidated Financial Statements are the financial statements of a

group presented as those of a single economic entity.

(ii) A Subsidiary is an entity, including an unincorporated entity that is

controlled by another entity known as the parent.

(iii) Non-controlling interest is the equity in the subsidiary not attributable

directly or indirectly to a parent.

(iv) Control is the power to govern the financial and operating policies of

an entity so as to obtain benefits from its activities.

(b) The following disclosures shall be made in Consolidated Financial Statements,

according to Schedule II paragraph 68 of CAMA:

(i) The nature of the relationship between the parent and subsidiary when

the parent does not own, directly or indirectly through subsidiaries, more

than half of the voting power.

(ii) The reasons why the ownership, directly or indirectly through

subsidiaries, of more than half of the voting or potential voting power

of an investee does not constitute control.

(iii) The end of the reporting period of the financial statements of a

subsidiary when such financial statements are used to prepare

consolidated financial statements and are as of a date or for a period

that is different from that of the parent‟s financial statements, and the

reason for using a different date or period.

(iv) The nature and extent of any significant restrictions on the ability of

subsidiaries to transfer funds to the parent in the form of cash

dividends or to repay loans or advances.

PATHFINDER

27

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

(v) A schedule that shows the effects of any changes in a parent‟s

ownership interest in a subsidiary that does not result in a loss on the

equity attributable to owners of the parent.

(vi) If control of a subsidiary is lost, the parent shall disclose the gain or

loss, if any.

(vii) A list of investment in subsidiaries, jointly controlled entities and

associates including the name and country of incorporation.

(viii) Where separate financial statements are prepared by a jointly

controlled entity or an investor, in an associate, the reason for

preparing separate financial statements, the list of significant

investment and country of incorporation of the investee must be

disclosed.

EXAMINERS‟ REPORT

The question tests candidates‟ understanding of the requirements of IAS 27 on

Separate Financial Statements as well as disclosure requirements when preparing

Consolidated Financial Statements.

The performance of the candidates was fair.

Most candidates were able to define the basic terms in accordance with the

International Accounting Standard No. 27, but they displayed inadequate

understanding of the disclosure requirements.

Candidates are advised to pay more attention to Statements of Accounting Standards.

PATHFINDER

28

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

QUESTION 6

Financial reporting is not an end in itself. It is a means of communicating to the users

of the financial reports. Information is useful in making choices among alternative

uses of scarce resources, though, the objective stems largely from the needs and

interests of those users.

Potential users of financial reports and their information needs include:

(a) Equity investors.

Equity investors in an entity are interested in the entity‟s ability to generate net

cash inflows because their decisions relate to the amounts, timing, and

uncertainties of those cash flows. To an equity investor, an entity is a source of

cash in the form of dividends (or other cash distributions) and increases in the

prices of shares or other ownership interests. Equity investors are directly

concerned with the ability of the entity to generate net cash inflows and with

how the perception of that ability affects the prices of its equity interests.

They are also interested in the ability of the company to issue scrip, which

will increase their shareholding and consequently increase their cash inflow.

(b) Creditors, including purchasers of trade debt instruments.

These provide finance to an entity by lending cash (or other assets) to it.

Like investors, creditors are interested in the amounts, timing and uncertainty

of an entity‟s future cash flows. To a creditor, an entity is a source of cash in the

form of interest, repayments of borrowings and increase in the prices of debt

securities.

(c) Suppliers.

They provide services rather than financial capital. They are interested in

assessing the likelihood that amounts an entity owes them will be paid as at

when due.

(d) Employees.

They provide services to equity; employees and their representatives are

interested in evaluating the stability, profitability, and growth of their

employer. They are interested in information that helps them to assess the

entity‟s continuing ability to pay salaries and wages and to provide incentive

payments and retirement and other benefits.

PATHFINDER

29

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

(e) Customers.

To its customers, an entity is a source of goods and services. Customers are

interested in assessing the entity‟s ability to continue to provide those goods or

services, especially if they have a long-term involvement with, or are dependent

on the entity.

(f) Governments and their agencies and regulatory bodies.

These are interested in the activities of an entity because they are in various

ways responsible for seeing that economic resources are allocated efficiently.

They also need information to help in regulating the activities of entities,

determining and applying taxation policies, preparing national income and

similar statistics.

(g) Management.

This requires financial reports to obtain financial information among others to

effectively perform their function of planning and controlling the operation of

the enterprise.

(h) Financial Analyst.

This like Accountants, Stockbrokers, etc. will need the financial information to

determine the performance of the entity in order to give constructive advice as

to whether their clients should invest in a particular company or not.

(i) Competitors.

Competitors require the financial statements of companies in the same line of

business or the same industry for the purpose of comparison. This will make

them know their position and facilitate effective analysis of their strengths,

weaknesses, opportunities and threats within the industry. This will also enable

competing companies know how they are faring among their peers and make

them evolve appropriate policies and/or actions for improvement.

(j) Researchers.

Researchers require financial information for inter-firm and inter-period

comparisons to guide students and consultants.

EXAMINERS‟ REPORT

The question tests candidates‟ knowledge on users of financial statements and their

individual information needs.

Majority of the candidates understood the question and the performance was good.

PATHFINDER

30

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

ICAN/ EXAMINATION NO...................................

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF NIGERIA

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

STRATEGIC FINANCIAL MANAGEMENT

Time allowed – 3 hours

SECTION A: Attempt All Questions

PART 1 MULTIPLE-CHOICE QUESTIONS (20 Marks)

1. Which of the following functions is NOT performed at a lower management level?

A. Supervision of cash receipts and payments.

B. Safeguarding cash balances

C. Record keeping and reporting

D. Custody and safeguarding securities and valuable papers

E. Planning and control of funds

2. The following are the characteristics of strategic decision EXCEPT they

A. are concerned with the scope of the organisation‟s activities.

B. match the organisation‟s activities to the environment in which it operates.

C. match an organisation‟s activities to its resource capability.

D. involve major decisions about the allocation or re-allocation of resources.

E. affect the short-term direction that the organisation takes.

3. Which of the following short-term investment opportunities is NOT available to

companies?

A. Treasury bills

B. Commercial papers

C. Certificates of deposits

D. Bonds

E. Bank deposits

PATHFINDER

31

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

4. Baumol‟s model on cash management is not based on ONE of the following

assumptions.

A. A firm is able to forecast its cash needs with certainty.

B. A firm‟s cash payments occur uniformly over a period of time.

C. The opportunity cost of holding cash is known and it does not change over

time.

D. The firm will incur the same transaction cost whenever it converts securities

to cash.

E. The net cashflow is normally distributed with a zero mean and standard

deviation.

5. Which of the following simplifying assumptions is NOT commonly made in

examining the relationship between capital structure and cost of capital?

A. There is no income tax

B. The firm pursues a policy of paying all its earnings as dividends

C. Investors have identical subjective probability distributions of operating

income

D. The operating income is expected to be static

E. A firm can change its capital structure almost instantaneously without

incurring transaction costs

6. Which of the following reasons for valuing securities is NOT correct?

A. To determine the purchase consideration in an absorption or merger scheme

B. To ascertain the total amount of the estate of a deceased investor

C. To determine the fair price at which shares of a company could be

purchased

D. To meet the stock exchange requirements

E. To estimate the break-up value of a company in liquidation

PATHFINDER

32

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

7. Given the following data in respect of Alariwo Plc, calculate the P/E ratio:

Share Price N5.00; and

EPS N0.82

A. 4.10

B. 6.10

C. 6.12

D. 6.14

E. 6.22

8. Which of the following statements may NOT be a reason for issuing bonus shares?

A. Bonus shares tend to bring the market price per share within a more

popular range

B. Bonus shares increase the number of outstanding shares

C. The rate of dividend tends to increase

D. Issuing of bonus shares improves the prospects of raising additional funds

E. The share capital base increases and the company may achieve a more

respectable size in the eyes of the investing community

9. Which of the following is NOT one of the core decision areas in financial

management?

A. Investment decision

B. Finance decision

C. Dividend decision

D. Liquidity decision

E. Credit management decision

10. The traditional approach to the valuation of a company assumes that

A. the gearing of a company is changed immediately by issuing debts to

purchase equity or vice-versa.

B. all earnings are distributed in form of dividend.

C. business risk fluctuates regardless of how the company invests its funds.

D. taxation is ignored.

E. earnings are assumed to have zero growth into perpetuity.

PATHFINDER

33

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

11. An integrated approach to the strategy making process provides a framework

which consists of the following parts EXCEPT

A. analysing the present internal and external conditions.

B. identifying and evaluating the present strategy.

C. searching for strengths and weaknesses within the present strategy and

environment.

D. considering changes in the existing strategy.

E. choosing the strategy that best satisfies the objectives.

12. Mr Adeyemi obtained a three-year loan of N10,000 @ 9% from his employer to

buy a motorcycle. The loan is expected to be repaid in three equal end-of-year

instalments. What is the annual instalment?

A. N3,905

B. N3,921

C. N3,951

D. N3,975

E. N3,981.

13. An investor expects a perpetual sum of N500 annually from his investment. What

is the present value of this perpetuity if his interest rate is 10%?

A. N5,000

B. N5,200

C. N5,300

D. N5,400

E. N5,500.

14. The following are relevant factors in taking a decision to raise money through

loan stock EXCEPT

A. issue costs.

B. capital repayment.

C. control.

D. servicing costs.

E. interest repayment.

PATHFINDER

34

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

15. Who has the overall responsibility for the attainment of corporate governance objectives

in an organisation?

A. Top executive officer

B. Shareholders

C. Work force

D. Audit Committee

E. Board of Directors

16. Which of the following is an aspect of the intermediation functions in the Nigerian

financial system?

A. Denomination intermediation

B. Maturity intermediation

C. Risk Intermediation

D. Interest rate intermediation

E. Liquidity intermediation

17. Strategic planning serves the following purposes in an organisation EXCEPT

A. clear definition of the purpose of the organisation and establishment of realistic

goals and objectives consistent with that mission in a definite time frame.

B. communication of those goals and objectives to the organisation‟s constituents.

C. development of a sense of ownership of the company‟s plan.

D. reflecting on how a specific function will contribute to the achievement of a

department‟s corporate priorities and defence tasks.

E. provision of a base from which progress can be measured and establishment of a

mechanism for informed change when needed.

18. Which of the following does NOT explain the essence of corporate planning?

A. The probability of future outcome of events is unknown

B. Predictions are susceptible to errors

C. The future is unpredictable

D. Decision makers cannot be assertive on future events

E. Decision relating to corporate planning rests on hunches

PATHFINDER

35

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

19. In relation to capital investment, a managerial option

A. applies only to new projects.

B. limits the flexibility of management‟s decision-making.

C. limits the downside risk of an investment project.

D. limits the profit potential of a proposed project.

E. extends the risk of executed projects.

20. Which of the following is NOT a limitation of capital rationing?

A. The assumption that projects are infinitely divisible may not always be true in

practice

B. An investment policy outcome may be less than optimal

C. The risk associated with the different projects and managements attitude to risk

are not considered

D. The linearity relationship can be faulted

E. If there is capital rationing in more than one year and more than two projects are

involved, ranking by discounted profitability index is not adequate

PATHFINDER

36

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

PART II – SHORT-ANSWER QUESTIONS (20 Marks)

1. Strategy formulation is ultimately the responsibility of............................

2. The secondary goal of a corporate organisation is................................

3. The two main theories relating to the effect of capital structure on the value of

the company are....................... and ..............................

4. A schedule statement of projected cash inflows and cash outflows over some

period is known as........................

5. What is the name given to an income received by the firm for goods and

services, to be supplied in future?

6. A financial instrument which entitles an investor to buy new shares of a

company during a specified period in future, at a price determined now, is

called...............................

7. Issue of shares of new companies are usually offered to the public for

subscription at........................value.

8. The process of guaranteeing to buy new public or rights issues if the issues are

NOT fully subscribed by the public is called................................

9. The development of financial strategy in an organization is the responsibility of

the...................................

10. The process of policy formulation, establishment of goals and objectives and the

development of strategies is known as ...........................

11. The level at which an order should be placed to replenish inventory is known

as...........................

12. Offers to the existing shareholders to subscribe cash for additional shares in the

proportion of their existing shareholdings at a price which is appreciably below

the current market price are referred to as .......................

.

13. The formula for determining the rate of return on a single asset is given

as...............................

PATHFINDER

37

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

14. The technique used in determining the viability, time of completion, costs and

resources of rescheduling alternative strategies is called.............................

15. The company‟s objective of maximising market price per share is synonymous

with …………………..

16. When a listed company delays or fails to notify the Stock Exchange of any new

development which may substantially affect the price of its security, an investor

can out-perform the market thereby resulting in …………….. capital market.

17. The process of developing and maintaining a strategic fit between the

organisation‟s goals and capabilities and its changing marketing opportunities

is the responsibility of the …………………..

18. A continuous process whereby people make decisions about how outcomes are

to be accomplished, what products will be produced, how success is measured

and evaluated and how budgetary resources are allocated is known

as………………..

19. Whenever there is a budget ceiling or a constraint on the amount of funds that

can be invested during a specific period, there will be need

for………………………

20. The terminology used to describe the value of a project‟s asset when sold

externally is known as …………………….

PATHFINDER

38

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

SECTION B -ANSWER QUESTION ONE AND ANY OTHER THREE (60 Marks)

QUESTION 1 - CASE STUDY

LAPEKUN LIMITED

Lapekun Limited is considering the purchase of a locally manufactured machine for N3

million. In view of the fact that the shares of the company are not quoted, it finds it

difficult to raise money through the issue of shares. The purchase of this machine

becomes absolutely necessary if the sales target given to the sales manager is to be

achieved. In order to ensure that the machine is purchased, the domineering

proprietor of the company and the accountant met informally to decide on how to

source for funds.

Many finance options were considered and they eventually agreed to negotiate for a

loan from Microfinance Bank Ltd. The bank agreed to give the company a loan of N2.5

million, which means that the company will have to source for the balance of N0.5

million elsewhere. However, the company has no tangible collateral with which to

secure additional loan to cover the balance of the value of the machine. In view of this

difficulty, the finance officer offered to advance the shortfall. The proprietor graciously

accepted this offer.

The duration of the loan is 20 years with an interest rate of 12% per annum. The

annual interest charge is to be calculated on the balance outstanding at the beginning

of each year. Repayment is to be made in 20 equal annual instalments. Each

instalment will include both interest and capital. A working capital of N250,000 will

be required at the beginning of the year. The amount will be sourced internally. The

machine is expected to generate net cashflows of N540,000 per annum for FIVE

consecutive years from its predominantly local sales.

You are required to determine

(a) the amount to be paid in each year on the loan; (5 Marks)

(b) the NPV of the machine and advise on its viability; and (5 Marks)

(c) identify FIVE features of small scale enterprises. (5 Marks)

(Total 15 Marks)

PATHFINDER

39

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

QUESTION 2

(a) Explain the term “rights issue”. (2 Marks)

(b) Differentiate between “rights issue” and “public issue”. (3 Marks)

(c) (i) Rapala Plc is about to make a one-for-three rights issue. Its current capital

structure is as follows:

6 million Ordinary shares of N1 each (current market value is N6.20 per

share)

15% Debentures (Redeemable at par in 10 years time) – N6 million.

(ii) The money raised from the rights issue may be used to execute the

following;

Buy back all the 15% debentures at their current market value. It is

expected that this investment will be priced to offer investors a yield of

9% which is the current market-yield on debenture loan.

Finance a new project costing N1.6 million.

You are required to determine the

(i) finance required to redeem the debentures and finance the new project.

(5 Marks)

(ii) issue price per share; (1 Mark )

(iii) theoretical ex-rights price; and (2 Marks)

(iv) theoretical nil paid value of a right per share (2 Marks)

NOTE:

The total finance required for (i) and (ii) should be rounded up to the next

N100,000 for the purpose of the rights issue.

(Total 15 Marks)

QUESTION 3

(a) State the formula for calculating the rate of return on equity shares

(2 Marks)

(b) Calculate the rate of return on equity share using the following information:

Price at the beginning of the year N60.00

PATHFINDER

40

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

Dividend paid at the end of the year N2.40

Price at the end of the year N69.00 (3 Marks)

(c) Explain FIVE areas in which the financial management in a business

organisation can benefit from information and communication technology.

(10 Marks)

(Total 15 Marks)

QUESTION 4

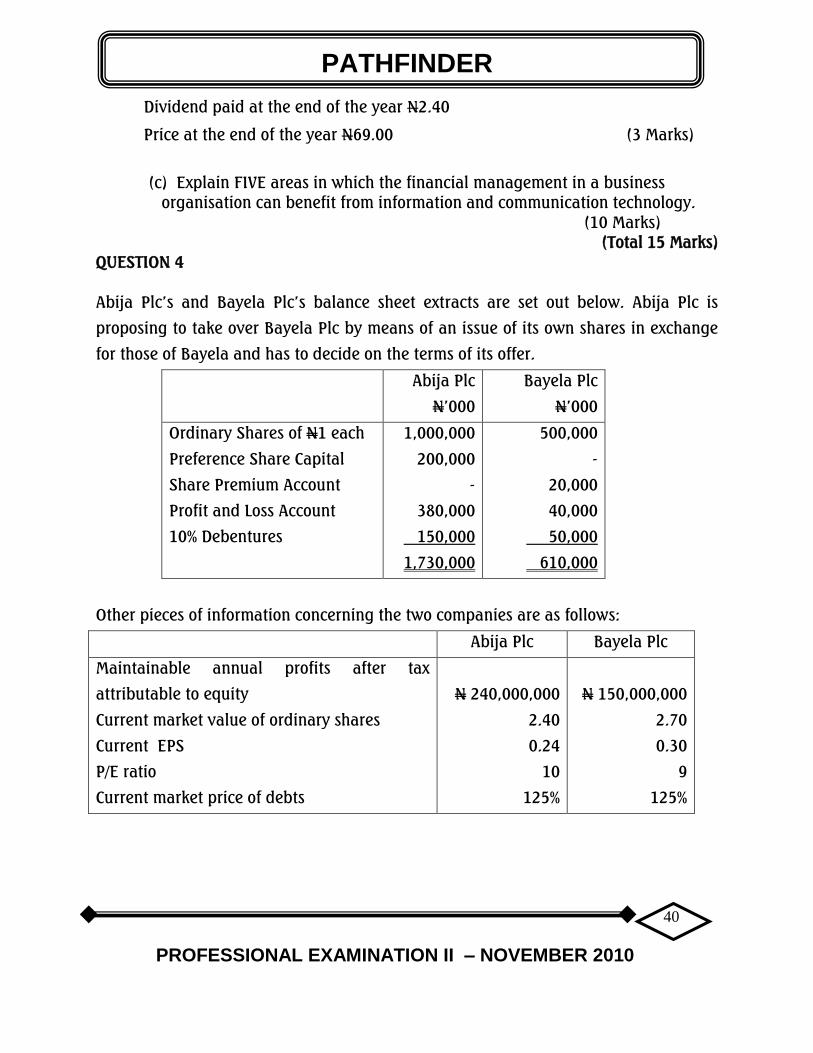

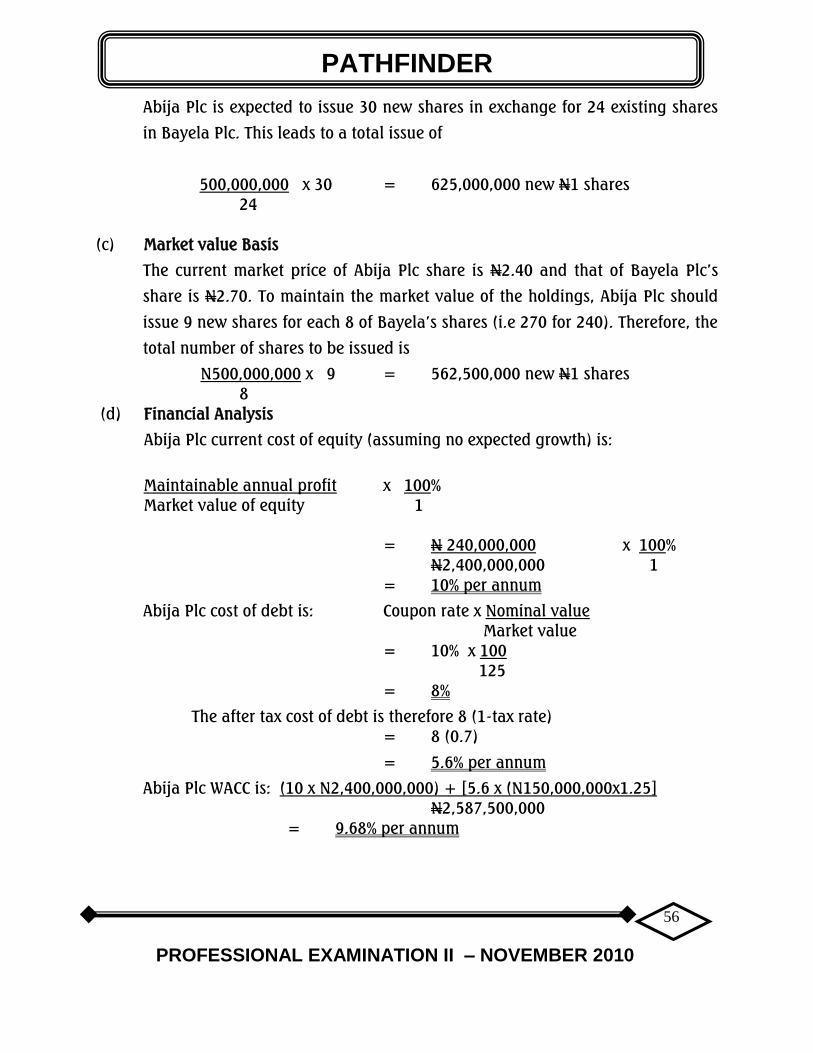

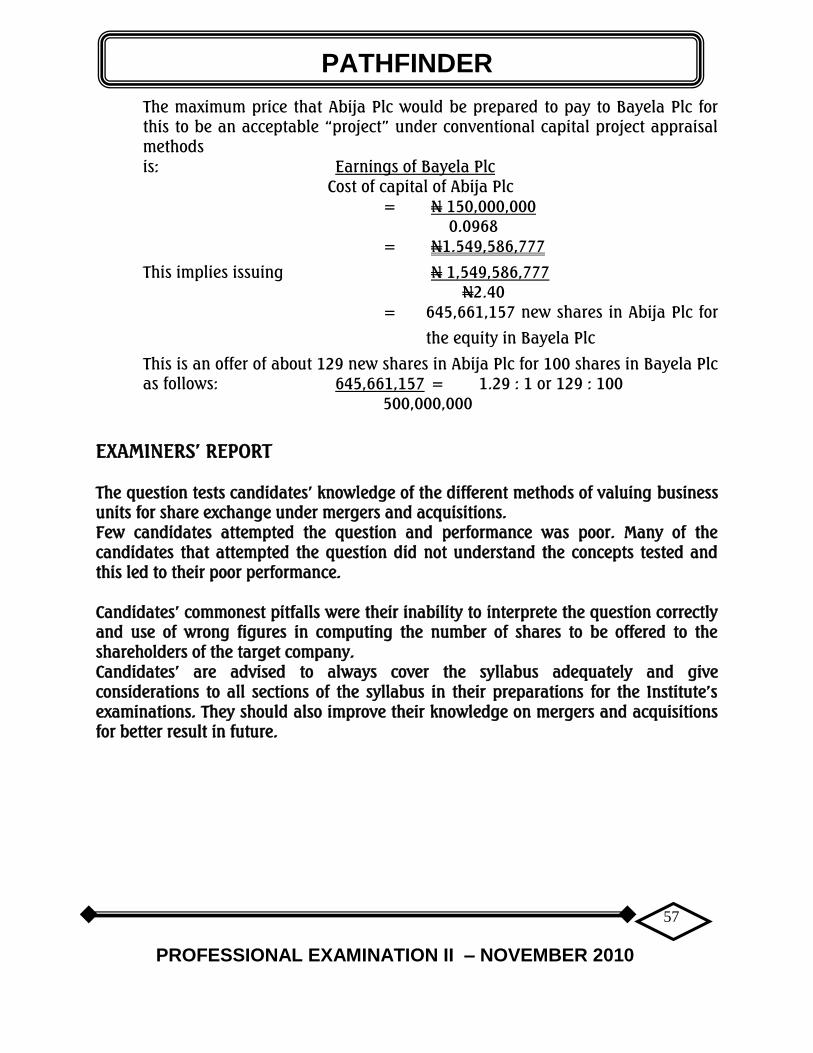

Abija Plc‟s and Bayela Plc‟s balance sheet extracts are set out below. Abija Plc is

proposing to take over Bayela Plc by means of an issue of its own shares in exchange

for those of Bayela and has to decide on the terms of its offer.

Abija Plc

N‟000

Bayela Plc

N‟000

Ordinary Shares of N1 each

Preference Share Capital

Share Premium Account

Profit and Loss Account

10% Debentures

1,000,000

200,000

-

380,000

150,000

1,730,000

500,000

-

20,000

40,000

50,000

610,000

Other pieces of information concerning the two companies are as follows:

Abija Plc Bayela Plc

Maintainable annual profits after tax

attributable to equity

Current market value of ordinary shares

Current EPS

P/E ratio

Current market price of debts

N 240,000,000

2.40

0.24

10

125%

N 150,000,000

2.70

0.30

9

125%

PATHFINDER

41

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

Required:

Determine the offer which the directors of Abija Plc would make to the shareholders of

Bayela Plc on each of the following bases:

a) Net Asset (3 Marks)

b) Earnings (4 Marks)

c) Market value (2 Marks)

d) Financial analysis (6 Marks)

The company‟s income tax rate is 30%.

(Total 15 Marks)

QUESTION 5

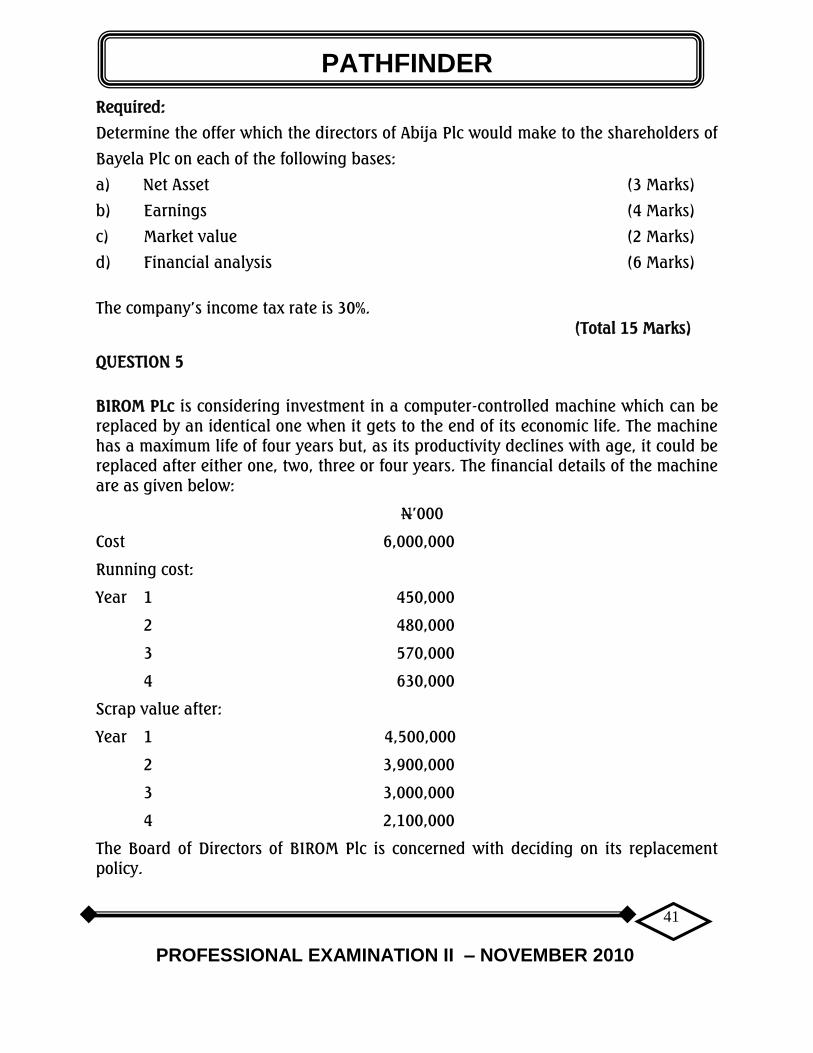

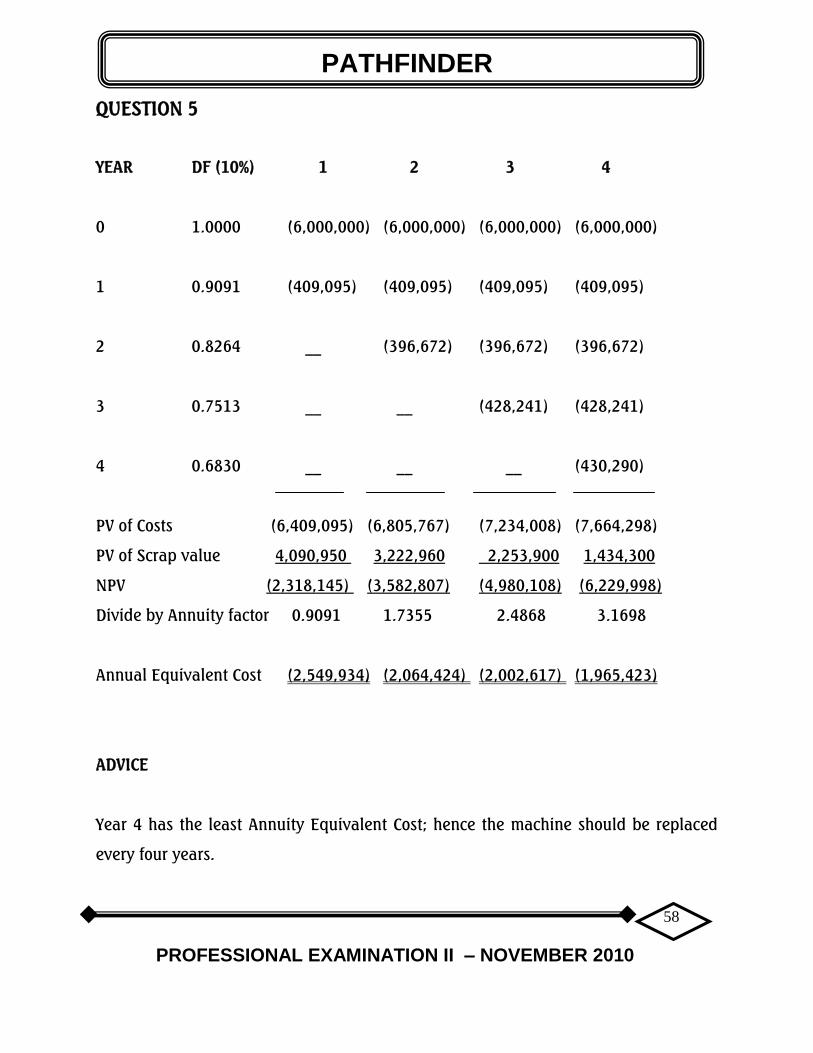

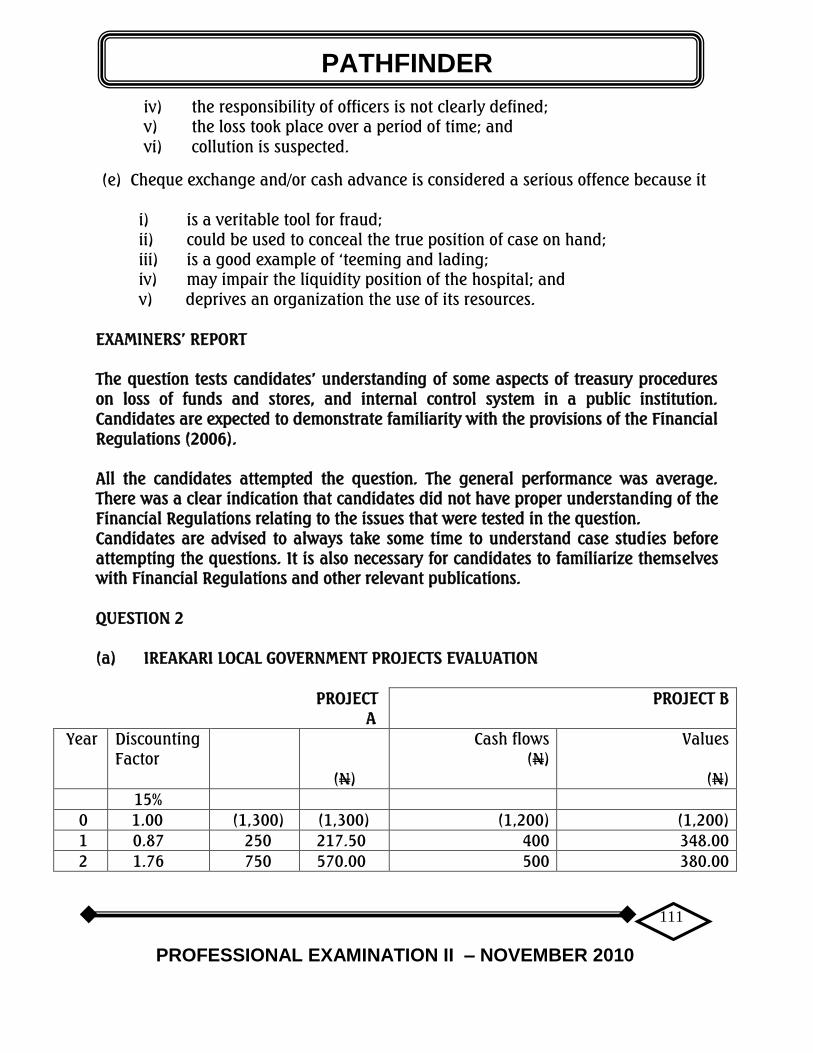

BIROM PLc is considering investment in a computer-controlled machine which can be

replaced by an identical one when it gets to the end of its economic life. The machine

has a maximum life of four years but, as its productivity declines with age, it could be

replaced after either one, two, three or four years. The financial details of the machine

are as given below:

N‟000

Cost 6,000,000

Running cost:

Year 1 450,000

2 480,000

3 570,000

4 630,000

Scrap value after:

Year 1 4,500,000

2 3,900,000

3 3,000,000

4 2,100,000

The Board of Directors of BIROM Plc is concerned with deciding on its replacement

policy.

PATHFINDER

42

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

As the financial manager of the company, you are required to advise the board on the

optimal replacement policy of the machine assuming that the company‟s cost of

capital is 10%.

(15 Marks)

QUESTION 6

“The role of planning cannot be over emphasised in the attainment of corporate

objectives”:

(a) In relation to the above statement, explain each of the following concepts:

(i) Operational planning;

(ii) Tactical planning; and

(iii) Strategic planning.

(6 Marks)

(b) State Three functions of each of the following:

(i) Central Securities Clearing System (CSCS); and

(ii) Securities and Exchange Commission (SEC)

(9 Marks)

(Total 15 Marks)

PATHFINDER

43

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

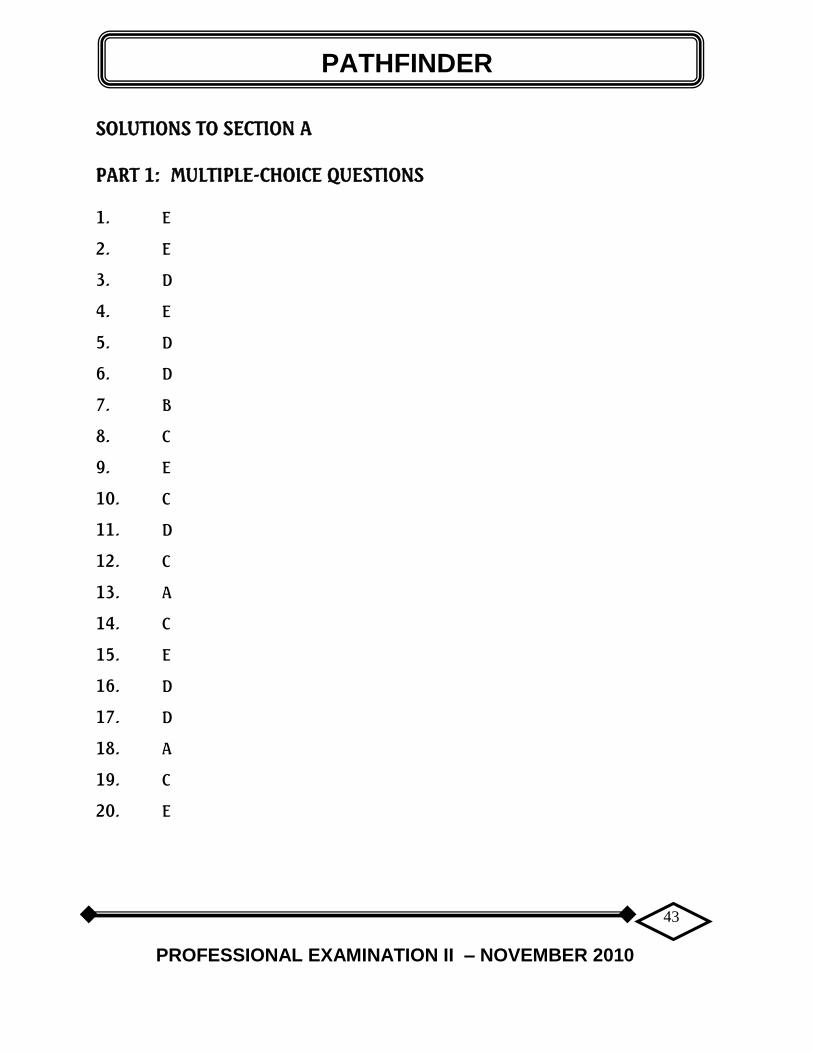

SOLUTIONS TO SECTION A

PART 1: MULTIPLE-CHOICE QUESTIONS

1. E

2. E

3. D

4. E

5. D

6. D

7. B

8. C

9. E

10. C

11. D

12. C

13. A

14. C

15. E

16. D

17. D

18. A

19. C

20. E

PATHFINDER

44

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

Tutorials

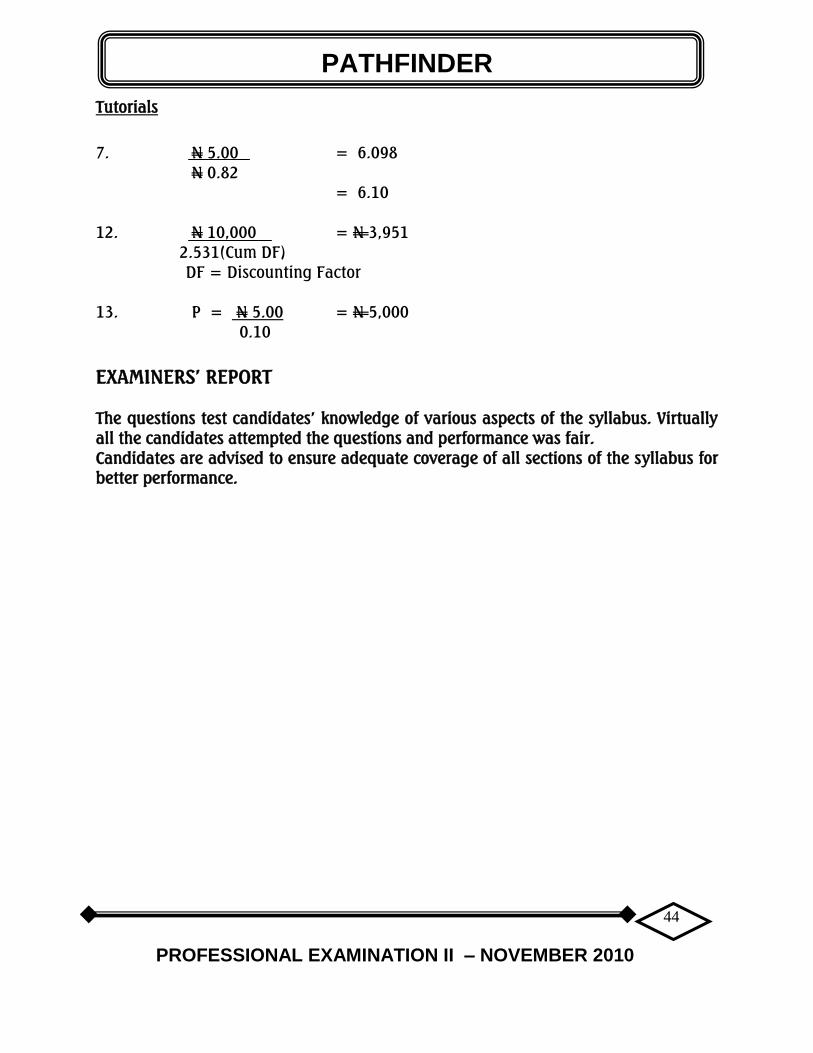

7. N 5.00 = 6.098

N 0.82

= 6.10

12. N 10,000 = N 3,951

2.531(Cum DF)

DF = Discounting Factor

13. P = N 5.00 = N 5,000

0.10

EXAMINERS‟ REPORT

The questions test candidates‟ knowledge of various aspects of the syllabus. Virtually

all the candidates attempted the questions and performance was fair.

Candidates are advised to ensure adequate coverage of all sections of the syllabus for

better performance.

PATHFINDER

45

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

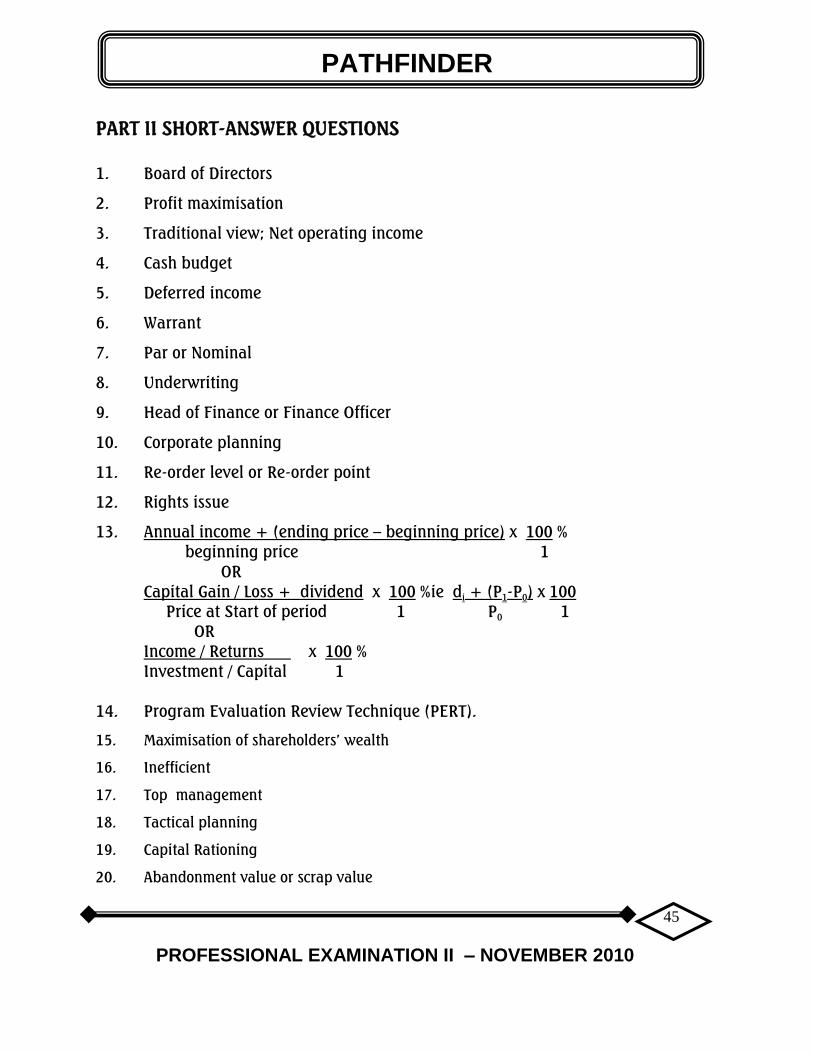

PART II SHORT-ANSWER QUESTIONS

1. Board of Directors

2. Profit maximisation

3. Traditional view; Net operating income

4. Cash budget

5. Deferred income

6. Warrant

7. Par or Nominal

8. Underwriting

9. Head of Finance or Finance Officer

10. Corporate planning

11. Re-order level or Re-order point

12. Rights issue

13. Annual income + (ending price – beginning price) x 100 %

beginning price 1

OR

Capital Gain / Loss + dividend x 100 % ie di + (P

1-P

0) x 100

Price at Start of period 1 P0

1

OR

Income / Returns x 100 %

Investment / Capital 1

14. Program Evaluation Review Technique (PERT).

15. Maximisation of shareholders‟ wealth

16. Inefficient

17. Top management

18. Tactical planning

19. Capital Rationing

20. Abandonment value or scrap value

PATHFINDER

46

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

EXAMINERS‟ REPORT

The questions test candidates‟ knowledge of various aspects of the syllabus.

Candidates‟ performance was average.

Candidates are advised to study extensively and adequately to cover the syllabus

when preparing for the examinations of the Institute for better result.

PATHFINDER

47

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

SOLUTIONS TO SECTION B

QUESTION 1 - CASE STUDY

LAPEKUN LIMITED

(a) Calculation of the annual repayment

A = [1-(1 + r)-n

]

r

= 1 –( 1.12)-20

0.12

= 7.4694

: . Annual repayment = N2,500,000

7.4694

= N 334,698.90

(b) Calculation of the NPV of the machine

Year NCF

(N)

DF@

12%

PV

(N)

0 (3,000,000) 1.0000 (3,000,000)

0 (250,000) 1.0000 (250,000)

1-5 540,000 3.6048 1,946,592

5 250 0.5674 141,850

NPV -1,161,558

Advice:

The machine should not be bought, as its purchase would result in the

reduction of the shareholders‟ wealth by N1,161,558.

PATHFINDER

48

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

(c) Features of small-scale enterprises.

These include:

i. The ownership of the firm and its control are not often separated, that is,

both are in most cases in the hands of a few closely related people,

probably within the same family.

ii. The companies‟ shares are usually not quoted on the stock market;

iii. The informal relationship among employees in the organization dominates

the formal relationship;

iv. In most cases, their inputs are locally sourced;

v. Management structure is uncomplicated, hence there is a speedy decision-

taking process;

vi. They contribute to the domestic capital formation;

vii. Low setup costs;

viii. Accelerating rural development and contributing to stemming urban

immigration and problems of congestion in large cities through employment

generation;

ix. Provide links between agriculture and industries; and

x. Supplying parts and components to large scale industries.

EXAMINERS‟ REPORT

Part „a‟ of the question tests candidates‟ knowledge of annuity while part „b‟ tests

candidates‟ understanding of one of the techniques of investment appraisal. Part „c‟ of

the question, however, tests candidates‟ knowledge of the features of Small Scale

Enterprises (SMEs).

Over 80% of the candidates attempted the question and most of them did well in part

„b‟ but demonstrated lack of adequate understanding of parts „a‟ and „c‟, hence

performance was average.

Candidates‟ commonest pitfall in part „a‟ was their inability to remember the annuity

formula, hence they were unable to calculate the annual „loan repayment.

PATHFINDER

49

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

Their pitfall in part „b‟ was their inability to compute the projects Net Present Value

(NPV) correctly owing to their failure to recognise the recovery of working capital at

the end of the project‟s life. However, in part „c‟, candidates focused on the features of

sole proprietorship instead of Small Scale Enterprises (SMEs).

Candidates are advised to read wide, understand and interprete questions

appropriately before attempting them. They should also make effort to remember key

formulae.

QUESTION 2

(a) Rights Issue –This is an offer to the existing shareholders of securities listed in the

primary market to subscribe for additional shares in the proportion of their

existing shareholdings at a price lower than the current market price of the

shares. It is the most common method of raising capital by private and public

companies.

(b) Differences between “rights issue” and “public issue”

(i) Rights issue is usually more successful than public issue because it is made

to investors who are familiar with the operations of the company.

(ii) A rights issue involves selling of ordinary shares to the existing shareholders

while a public issue involves raising of share capital directly from the

public.

(iii) The flotation costs of a rights issue are significantly lower than those of a

public issue because a rights issue is not underwritten.

(iv) A rights issue may be made by private companies as well as public

companies whereas a public issue can only be made by public companies.

(v) A rights issue does not lead to dilution of control except the rights are not

fully taken up by the shareholders whereas a public issue can lead to

dilution of control.

PATHFINDER

50

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

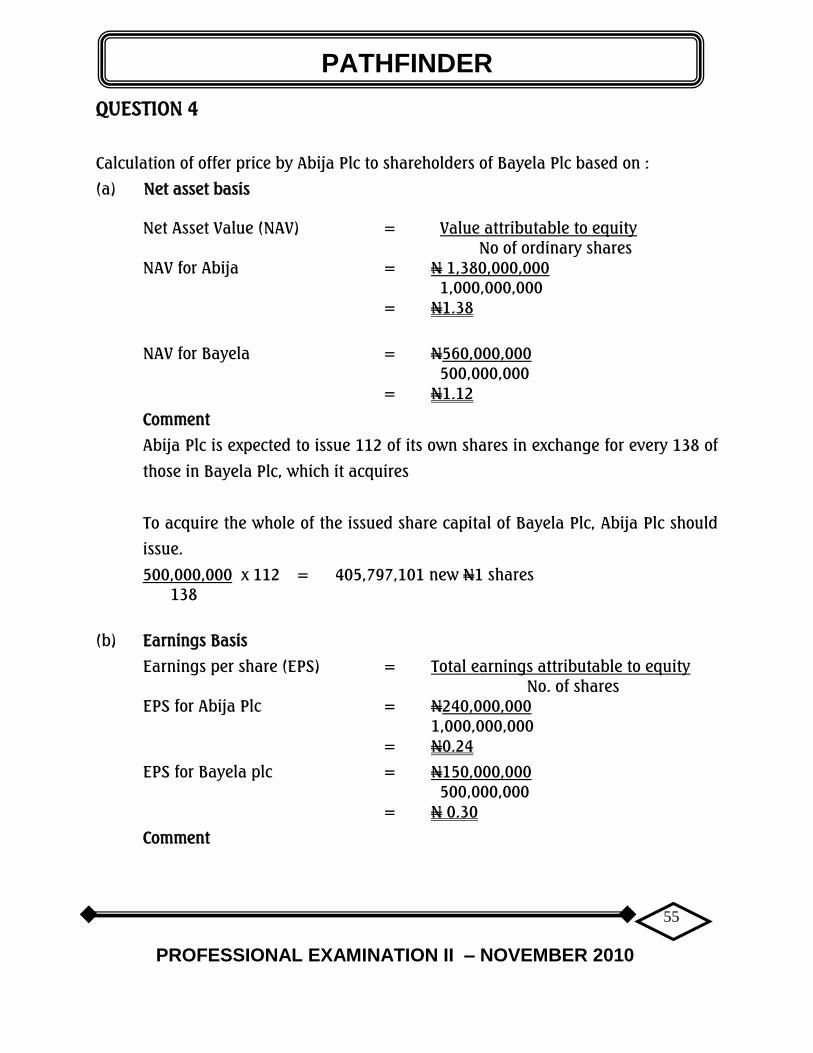

(b) (i) Finance required:

The finance required to redeem the debenture and finance the new project is

the addition of the current price of the debenture and the cost of the new

project. This is obtained as follows:

Calculation of the current value of the debenture

15% Redeemable debenture = N 6,000,000

Annual interest = N 900,000

Year Item Cashflow

N

DCF @

9%

PV

(N)

1 – 10 Interest 900,000 6.4177 5,775,930

10 Debt

redeemed

6,000,000 0.4224 2,534,400

Current value 8,310,330

Current value of the 15% redeemable debenture = N 8,310,330

Cost of the proposed project (given) = N 1,600,000

Therefore, the finance required is = N 9,910,330

= N10,000,000 approx.

(ii) Calculation of issue price per share

Finance required = N 10,000,000 (c (i) above)

No of shares issued (6,000,000/3) = 2,000,000 shares

Issue price = N10,000,000

2,000,000

= N5.00

PATHFINDER

51

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

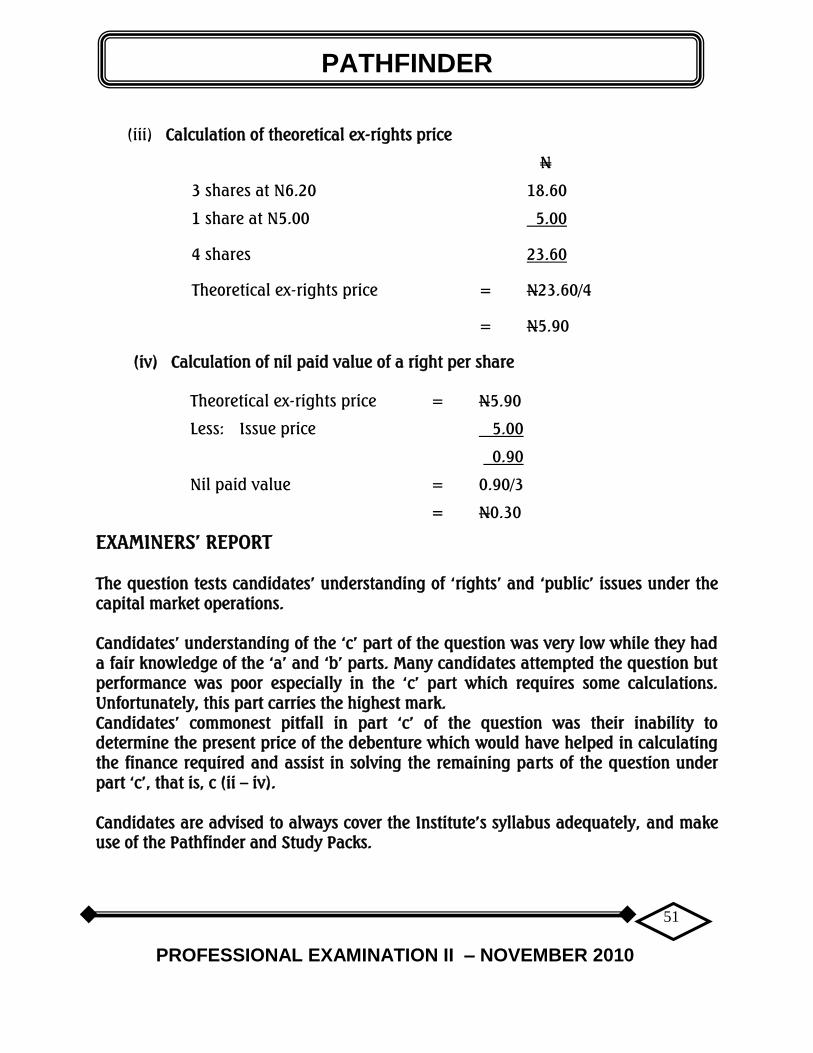

(iii) Calculation of theoretical ex-rights price

N

3 shares at N6.20 18.60

1 share at N5.00 5.00

4 shares 23.60

Theoretical ex-rights price = N23.60/4

= N5.90

(iv) Calculation of nil paid value of a right per share

Theoretical ex-rights price = N5.90

Less: Issue price 5.00

0.90

Nil paid value = 0.90/3

= N0.30

EXAMINERS‟ REPORT

The question tests candidates‟ understanding of „rights‟ and „public‟ issues under the

capital market operations.

Candidates‟ understanding of the „c‟ part of the question was very low while they had

a fair knowledge of the „a‟ and „b‟ parts. Many candidates attempted the question but

performance was poor especially in the „c‟ part which requires some calculations.

Unfortunately, this part carries the highest mark.

Candidates‟ commonest pitfall in part „c‟ of the question was their inability to

determine the present price of the debenture which would have helped in calculating

the finance required and assist in solving the remaining parts of the question under

part „c‟, that is, c (ii – iv).

Candidates are advised to always cover the Institute‟s syllabus adequately, and make

use of the Pathfinder and Study Packs.

PATHFINDER

52

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

QUESTION 3

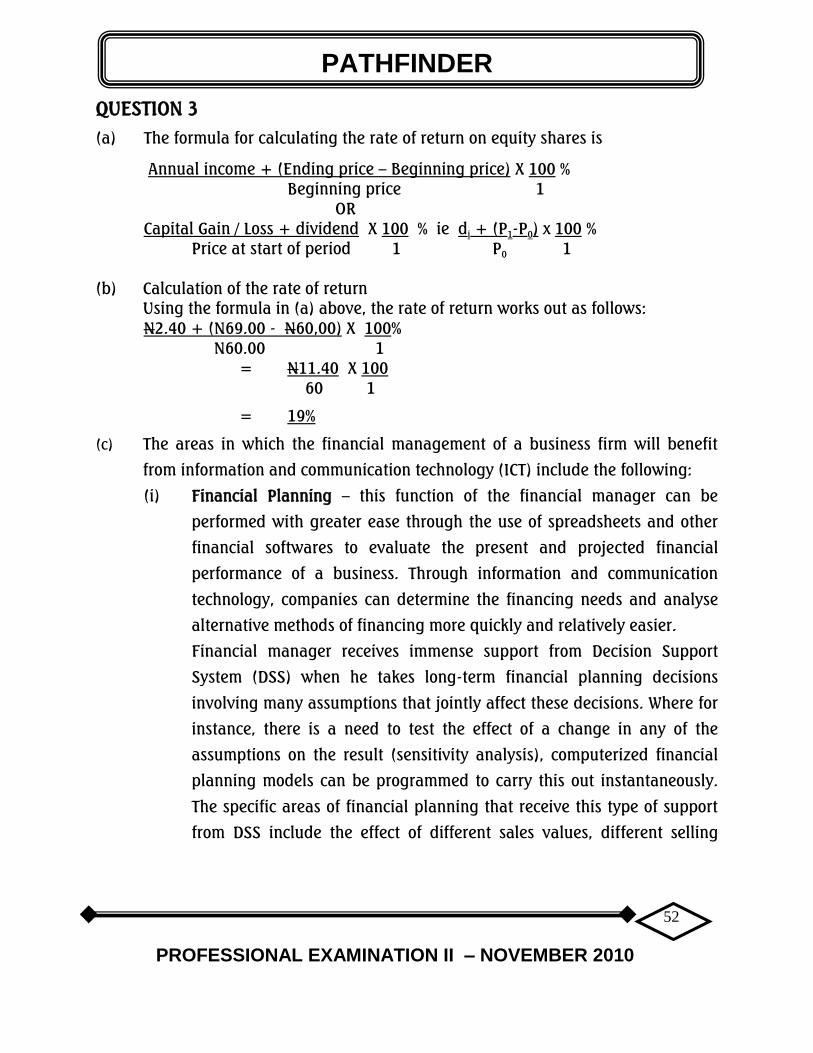

(a) The formula for calculating the rate of return on equity shares is

Annual income + (Ending price – Beginning price) X 100 %

Beginning price 1

OR

Capital Gain / Loss + dividend X 100 % ie di + (P

1-P

0) x 100 %

Price at start of period 1 P0 1

(b) Calculation of the rate of return

Using the formula in (a) above, the rate of return works out as follows:

N2.40 + (N69.00 - N60,00) X 100%

N60.00 1

= N11.40 X 100

60 1

= 19%

(c) The areas in which the financial management of a business firm will benefit

from information and communication technology (ICT) include the following:

(i) Financial Planning – this function of the financial manager can be

performed with greater ease through the use of spreadsheets and other

financial softwares to evaluate the present and projected financial

performance of a business. Through information and communication

technology, companies can determine the financing needs and analyse

alternative methods of financing more quickly and relatively easier.

Financial manager receives immense support from Decision Support

System (DSS) when he takes long-term financial planning decisions

involving many assumptions that jointly affect these decisions. Where for

instance, there is a need to test the effect of a change in any of the

assumptions on the result (sensitivity analysis), computerized financial

planning models can be programmed to carry this out instantaneously.

The specific areas of financial planning that receive this type of support

from DSS include the effect of different sales values, different selling

PATHFINDER

53

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

prices, and different input costs on the forecast figure in the projected

financial statements.

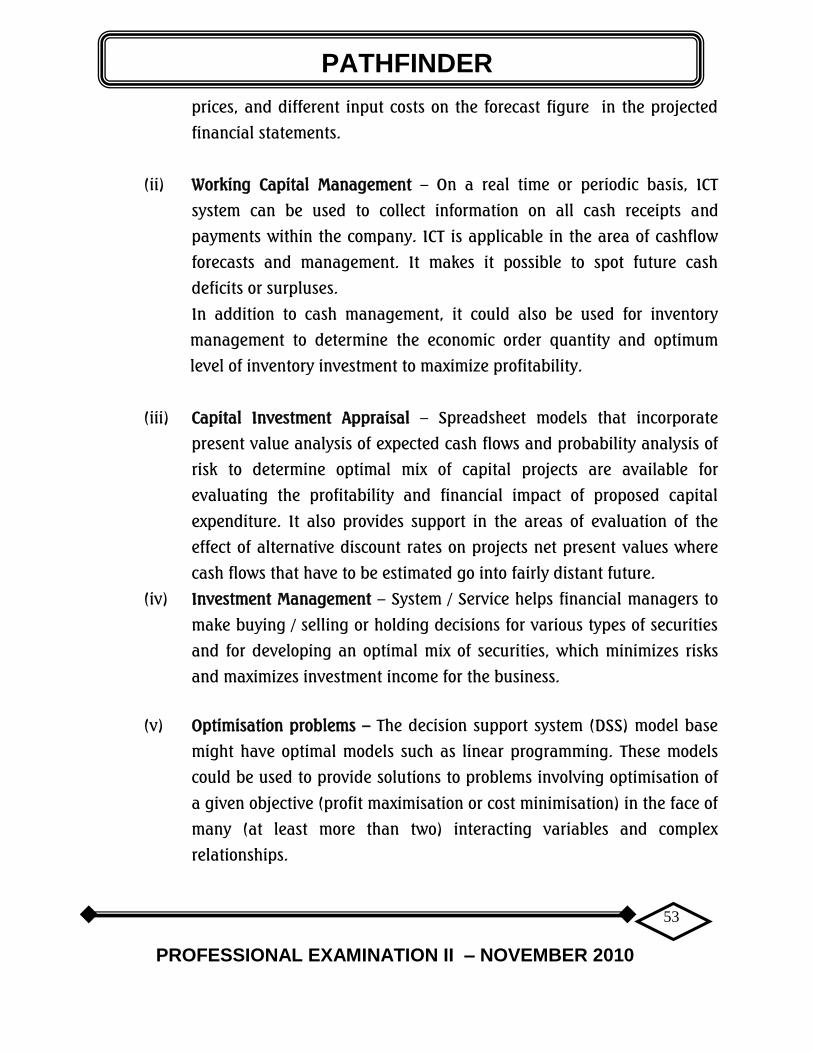

(ii) Working Capital Management – On a real time or periodic basis, ICT

system can be used to collect information on all cash receipts and

payments within the company. ICT is applicable in the area of cashflow

forecasts and management. It makes it possible to spot future cash

deficits or surpluses.

In addition to cash management, it could also be used for inventory

management to determine the economic order quantity and optimum

level of inventory investment to maximize profitability.

(iii) Capital Investment Appraisal – Spreadsheet models that incorporate

present value analysis of expected cash flows and probability analysis of

risk to determine optimal mix of capital projects are available for

evaluating the profitability and financial impact of proposed capital

expenditure. It also provides support in the areas of evaluation of the

effect of alternative discount rates on projects net present values where

cash flows that have to be estimated go into fairly distant future.

(iv) Investment Management – System / Service helps financial managers to

make buying / selling or holding decisions for various types of securities

and for developing an optimal mix of securities, which minimizes risks

and maximizes investment income for the business.

(v) Optimisation problems – The decision support system (DSS) model base

might have optimal models such as linear programming. These models

could be used to provide solutions to problems involving optimisation of

a given objective (profit maximisation or cost minimisation) in the face of

many (at least more than two) interacting variables and complex

relationships.

PATHFINDER

54

PROFESSIONAL EXAMINATION II – NOVEMBER 2010

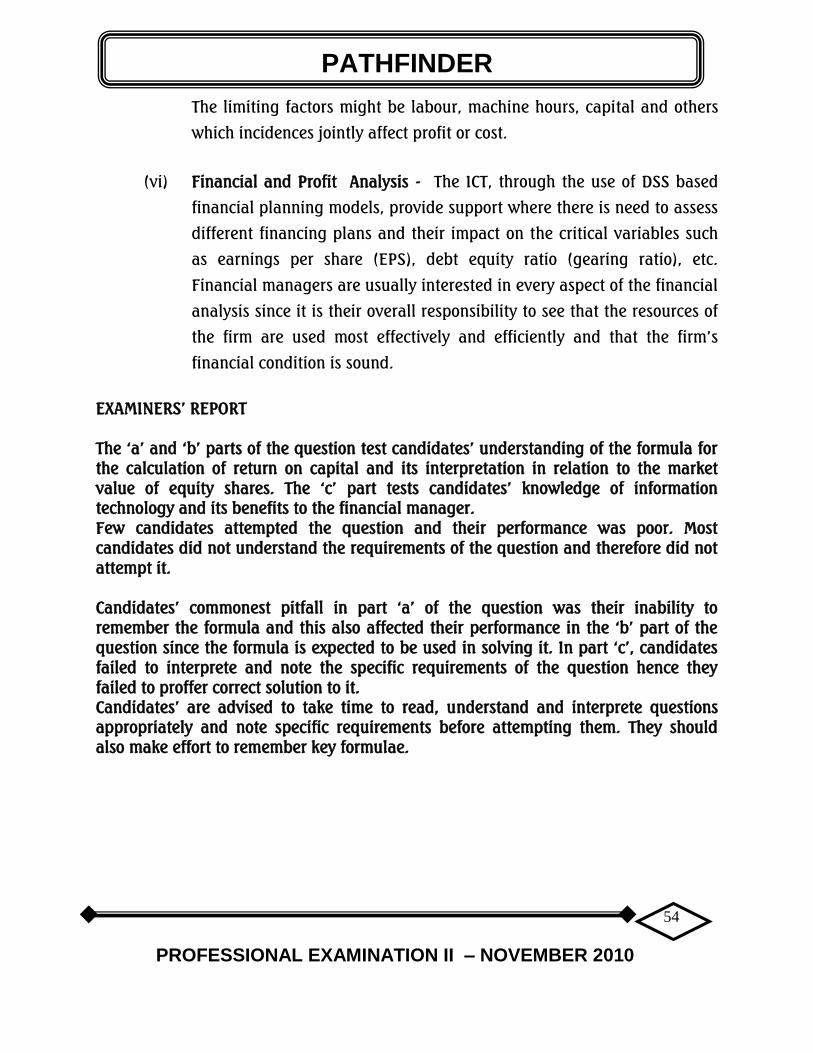

The limiting factors might be labour, machine hours, capital and others

which incidences jointly affect profit or cost.

(vi) Financial and Profit Analysis - The ICT, through the use of DSS based

financial planning models, provide support where there is need to assess

different financing plans and their impact on the critical variables such

as earnings per share (EPS), debt equity ratio (gearing ratio), etc.

Financial managers are usually interested in every aspect of the financial

analysis since it is their overall responsibility to see that the resources of