Embed Size (px)

Citation preview

The US Wine IndustryThe US Wine IndustryLiz BorodofskyLiz Borodofsky

John DaltonJohn DaltonJohn RoederJohn Roeder

James VineyardJames Vineyard

Table Of ContentsTable Of Contents

BackgroundBackground Market InformationMarket Information Nature Of CustomersNature Of Customers CompetitionCompetition Company ProfilesCompany Profiles Other Environmental InformationOther Environmental Information SourcesSources

BackgroundBackground

Industry HistoryIndustry History

American wine first gained prominence in the American wine first gained prominence in the 1919thth century. century.

Ohio was the first state to successfully grow Ohio was the first state to successfully grow wine grapes.wine grapes.

Spanish missionaries brought grapes to Spanish missionaries brought grapes to California and Texas.California and Texas.

The wine industry has not regained its size The wine industry has not regained its size prior to prohibition.prior to prohibition.

Wine in the USWine in the US

Wine competes with several substitute Wine competes with several substitute beverages in the US, primarily other alcoholic beverages in the US, primarily other alcoholic beverages.beverages.

The American culture historically has seen The American culture historically has seen wine as a luxury beverage, not suitable for wine as a luxury beverage, not suitable for consumption on a daily basis.consumption on a daily basis.

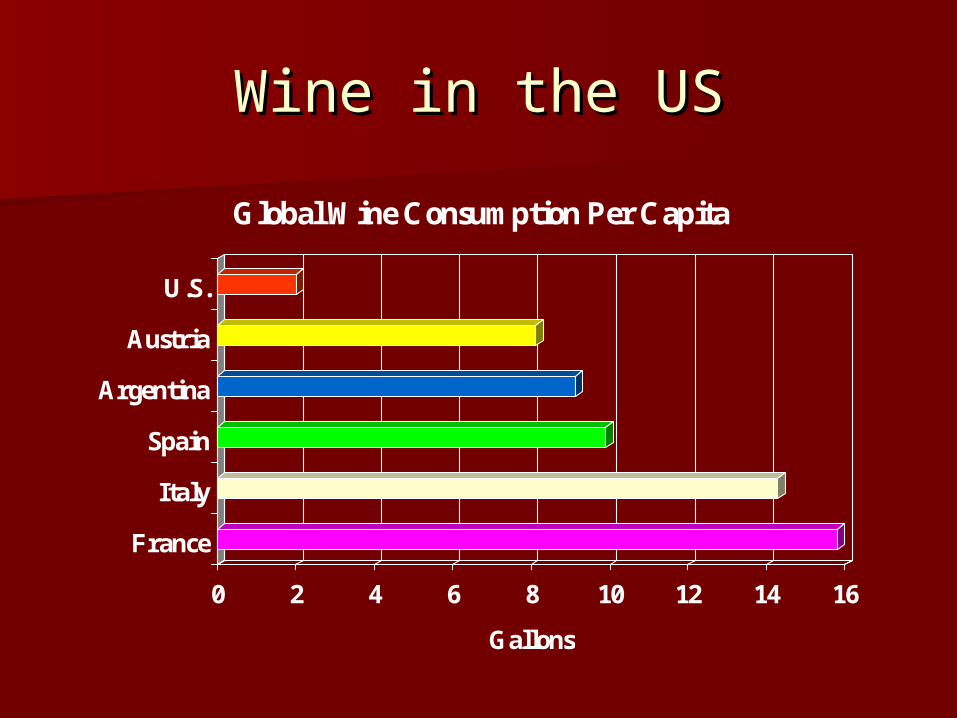

Wine in the USWine in the US

0 2 4 6 8 10 12 14 16

Gallons

France

Italy

Spain

Argentina

Austria

U.S.

Global Wine Consumption Per Capita

Market InformationMarket Information

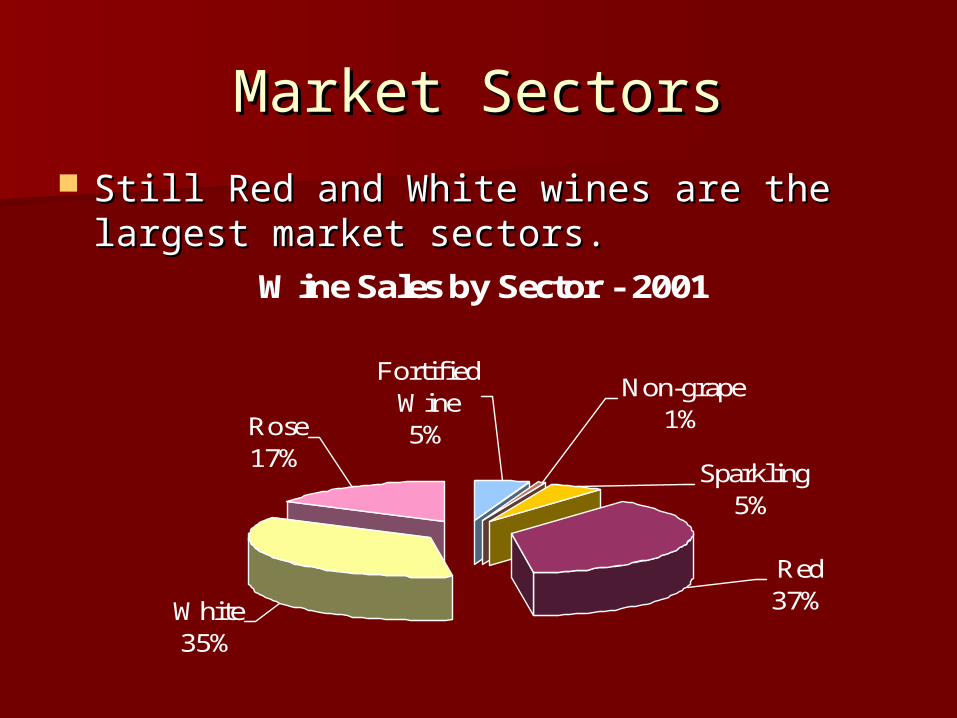

Market SectorsMarket Sectors

Wine Sales by Sector - 2001

White35%

Red37%

Sparkling5%

Non-grape1%

Fortified Wine5%Rose

17%

Still Red and White wines are the largest market Still Red and White wines are the largest market sectors.sectors.

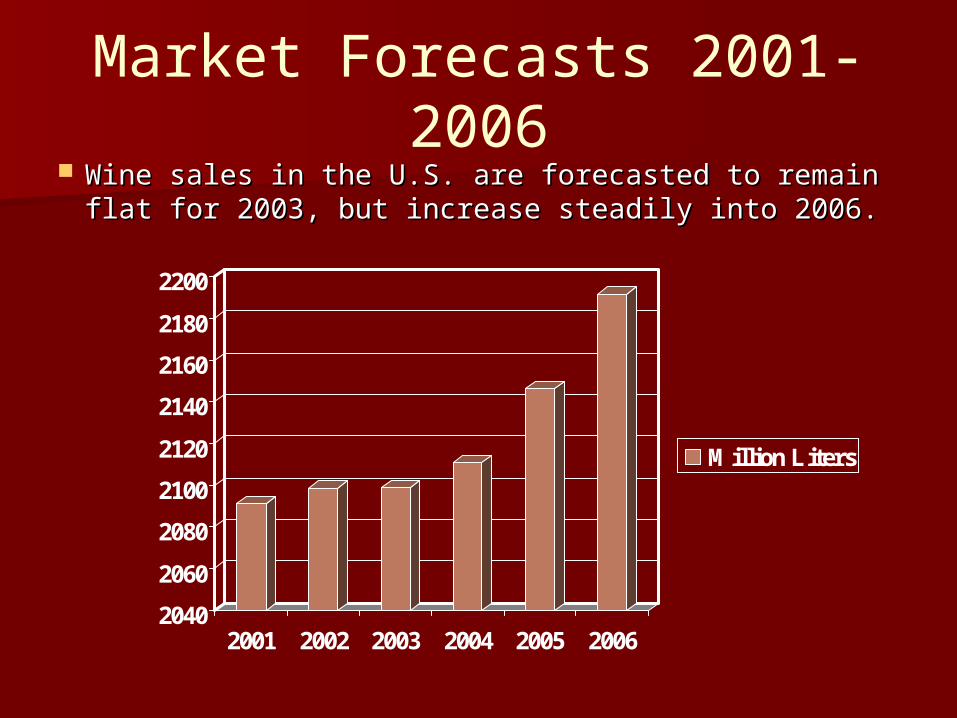

Market Forecasts 2001-2006

2040

2060

2080

2100

2120

2140

2160

2180

2200

2001 2002 2003 2004 2005 2006

Million Liters

Wine sales in the U.S. are forecasted to remain flat Wine sales in the U.S. are forecasted to remain flat for 2003, but increase steadily into 2006.for 2003, but increase steadily into 2006.

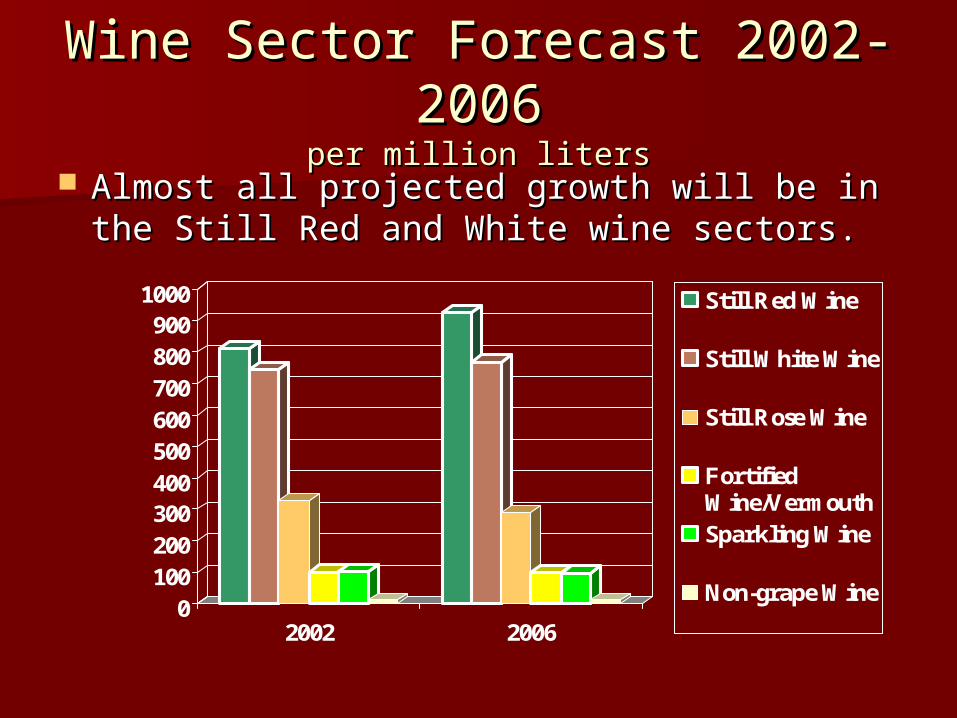

Wine Sector Forecast 2002-Wine Sector Forecast 2002-20062006

per million litersper million liters

0100200300400500600700800900

1000

2002 2006

Still Red Wine

Still White Wine

Still Rose Wine

FortifiedWine/VermouthSparkling Wine

Non-grape Wine

Almost all projected growth will be in the Still Red Almost all projected growth will be in the Still Red and White wine sectors.and White wine sectors.

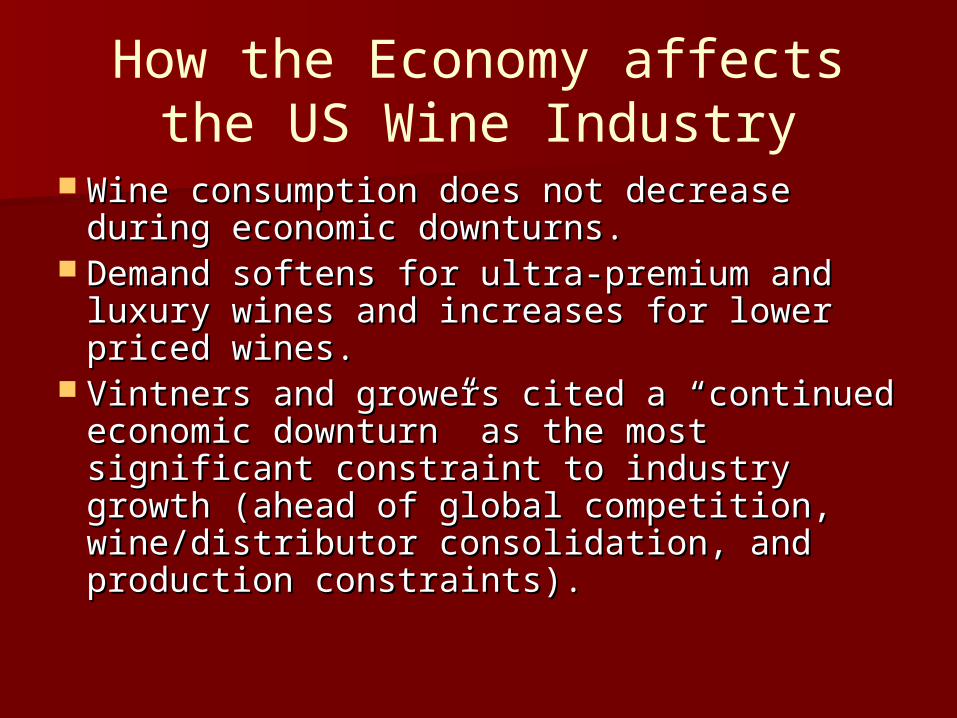

How the Economy affects the US Wine Industry

Wine consumption does not decrease during Wine consumption does not decrease during economic downturns.economic downturns.

Demand softens for ultra-premium and luxury Demand softens for ultra-premium and luxury wines and increases for lower priced wines.wines and increases for lower priced wines.

Vintners and growers cited a “continued Vintners and growers cited a “continued economic downturn” as the most significant economic downturn” as the most significant constraint to industry growth (ahead of global constraint to industry growth (ahead of global competition, wine/distributor consolidation, competition, wine/distributor consolidation, and production constraints).and production constraints).

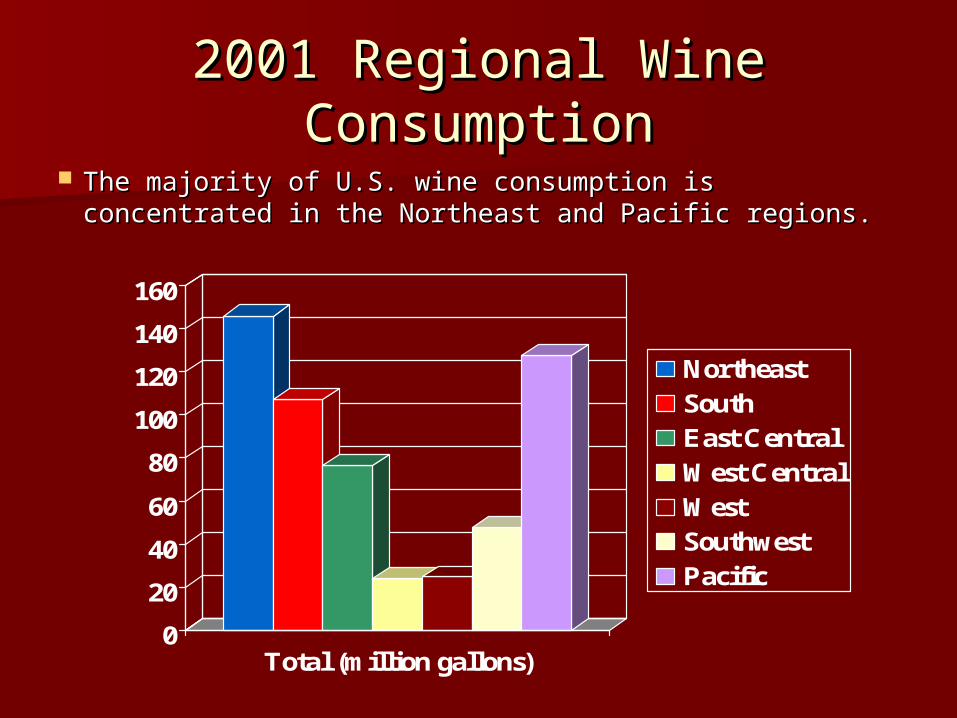

2001 Regional Wine 2001 Regional Wine ConsumptionConsumption

0

20

40

60

80

100

120

140

160

Total (million gallons)

NortheastSouthEast CentralWest CentralWestSouthwestPacific

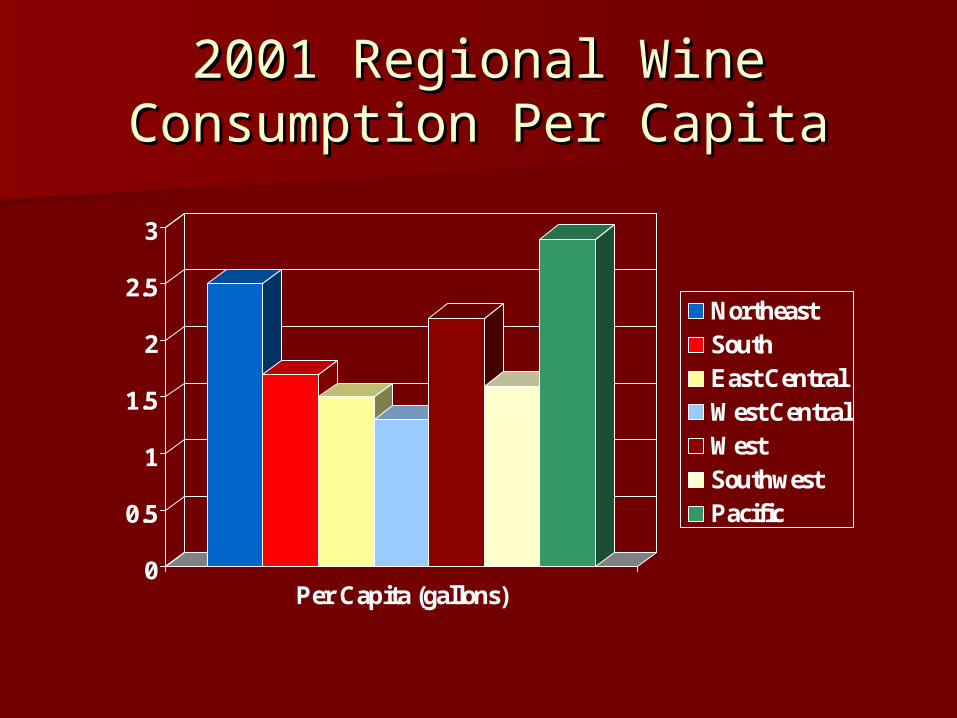

The majority of U.S. wine consumption is The majority of U.S. wine consumption is concentrated in the Northeast and Pacific regions.concentrated in the Northeast and Pacific regions.

2001 Regional Wine 2001 Regional Wine Consumption Per CapitaConsumption Per Capita

0

0.5

1

1.5

2

2.5

3

Per Capita (gallons)

NortheastSouthEast CentralWest CentralWestSouthwestPacific

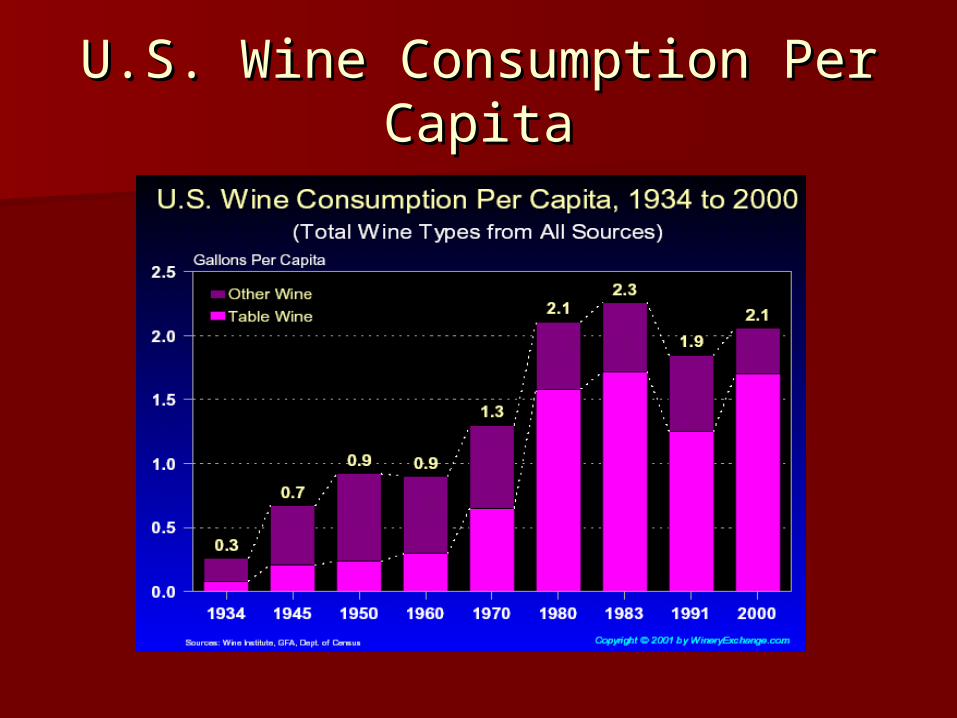

U.S. Wine Consumption Per U.S. Wine Consumption Per CapitaCapita

Nature of CustomersNature of Customers

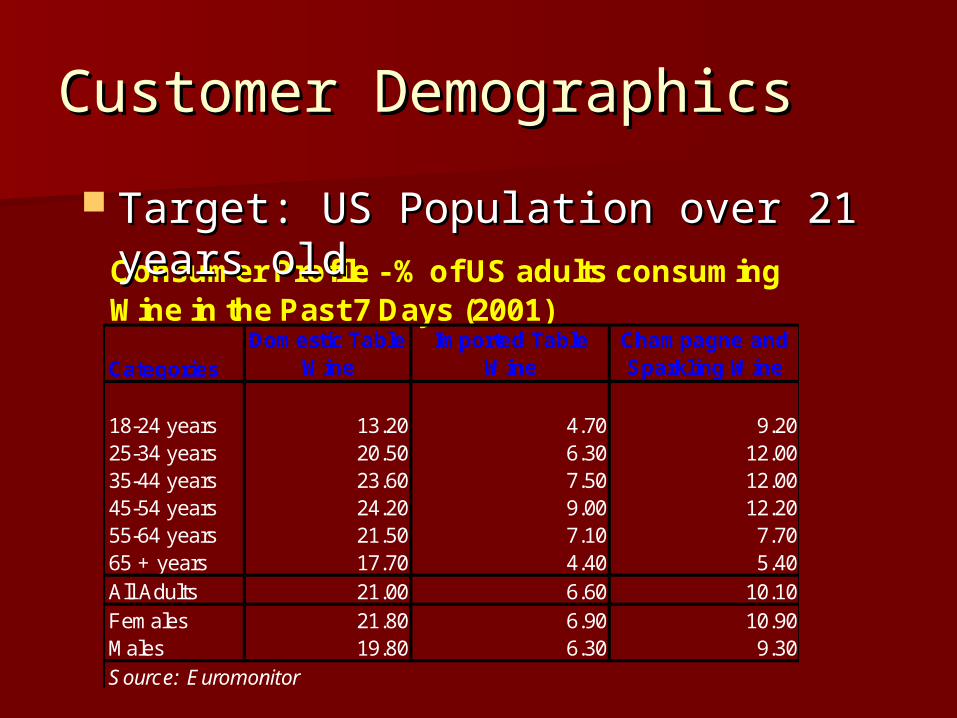

Customer DemographicsCustomer Demographics

Consumer Profile - % of US adults consumingWine in the Past 7 Days (2001)

CategoriesDomestic Table

WineImported Table

WineChampagne and Sparkling Wine

18-24 years 13.20 4.70 9.2025-34 years 20.50 6.30 12.0035-44 years 23.60 7.50 12.0045-54 years 24.20 9.00 12.2055-64 years 21.50 7.10 7.7065 + years 17.70 4.40 5.40All Adults 21.00 6.60 10.10Females 21.80 6.90 10.90Males 19.80 6.30 9.30Source: Euromonitor

Target: US Population over 21 years oldTarget: US Population over 21 years old

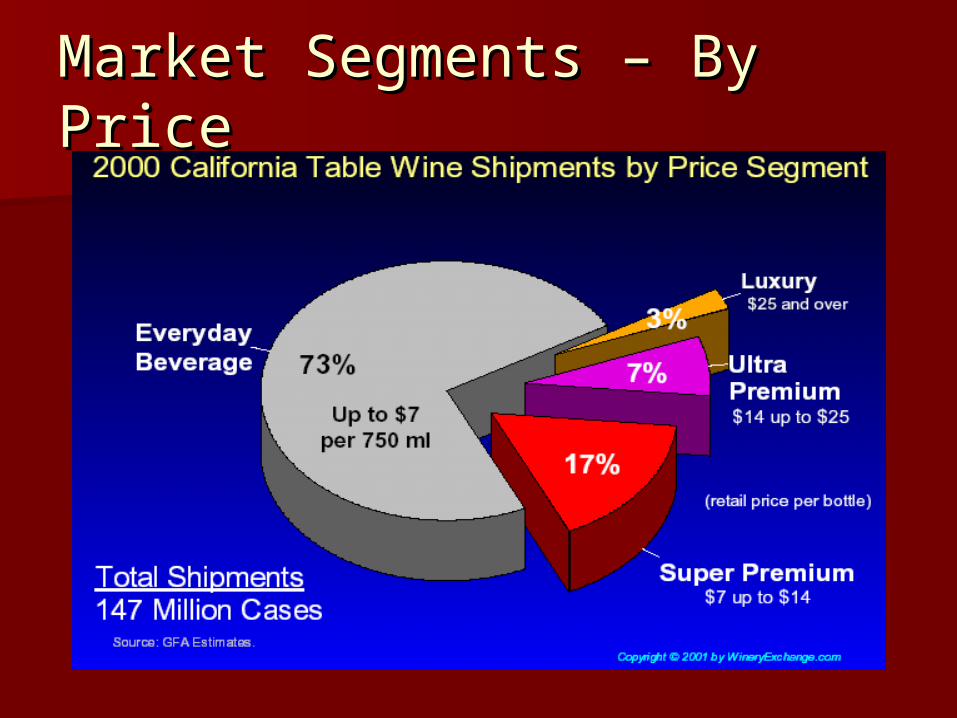

Market Segments – By PriceMarket Segments – By Price

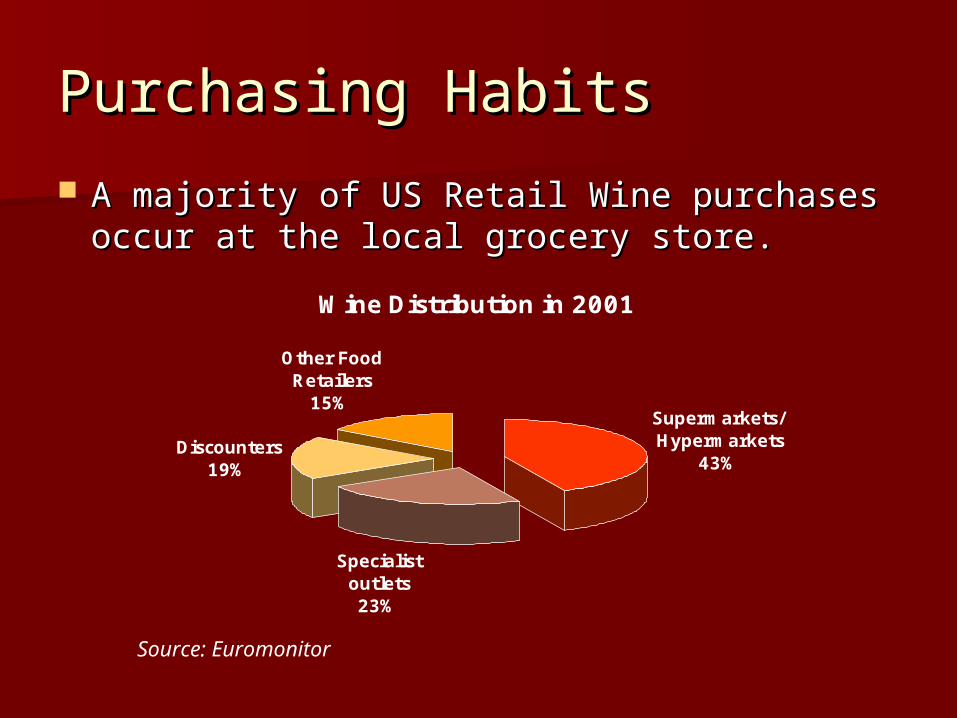

Purchasing HabitsPurchasing Habits

A majority of US Retail Wine purchases occur at the A majority of US Retail Wine purchases occur at the local grocery store.local grocery store.

Source: Euromonitor

Wine Distribution in 2001

Supermarkets/Hypermarkets

43%

Specialist outlets23%

Discounters19%

Other Food Retailers

15%

CompetitionCompetition

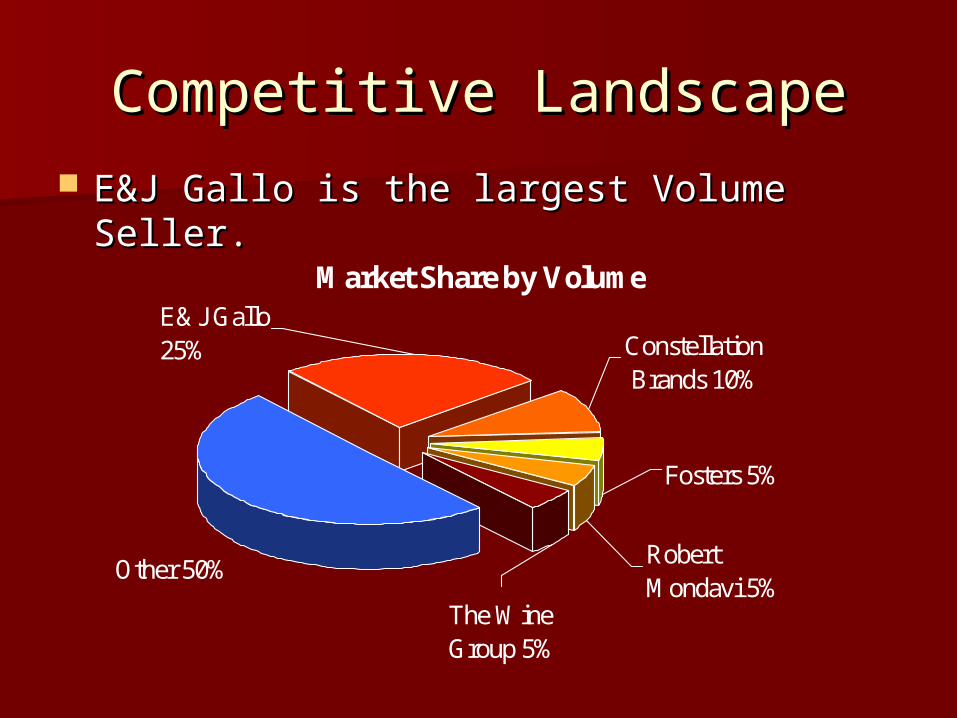

Competitive LandscapeCompetitive Landscape

Market Share by Volume

Other 50%

The Wine Group 5%

Fosters 5%

Robert Mondavi 5%

Constellation Brands 10%

E&J Gallo 25%

E&J Gallo is the largest Volume Seller.E&J Gallo is the largest Volume Seller.

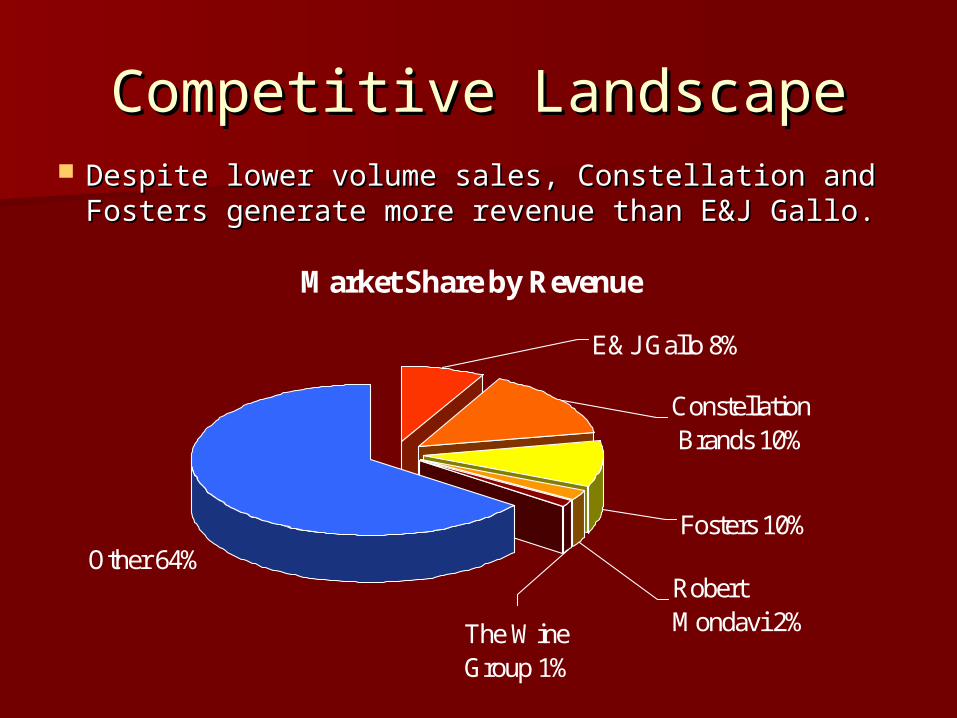

Competitive LandscapeCompetitive Landscape

Market Share by Revenue

Other 64%

The Wine Group 1%

Fosters 10%

Robert Mondavi 2%

Constellation Brands 10%

E&J Gallo 8%

Despite lower volume sales, Constellation and Despite lower volume sales, Constellation and Fosters generate more revenue than E&J Gallo.Fosters generate more revenue than E&J Gallo.

Industry TrendsIndustry Trends

Medium and large wineries are experiencing Medium and large wineries are experiencing significant consolidation while small wineries significant consolidation while small wineries proliferate (750+ in California alone).proliferate (750+ in California alone).

Worldwide grape-glut putting downward pressure Worldwide grape-glut putting downward pressure on prices.on prices.

Import wines gain market share. Wines from Italy Import wines gain market share. Wines from Italy and Australia, now represent 1 in 3 bottles sold in and Australia, now represent 1 in 3 bottles sold in supermarkets.supermarkets.

The Super Premium category ($7-$14) is The Super Premium category ($7-$14) is experiencing the highest growth.experiencing the highest growth.

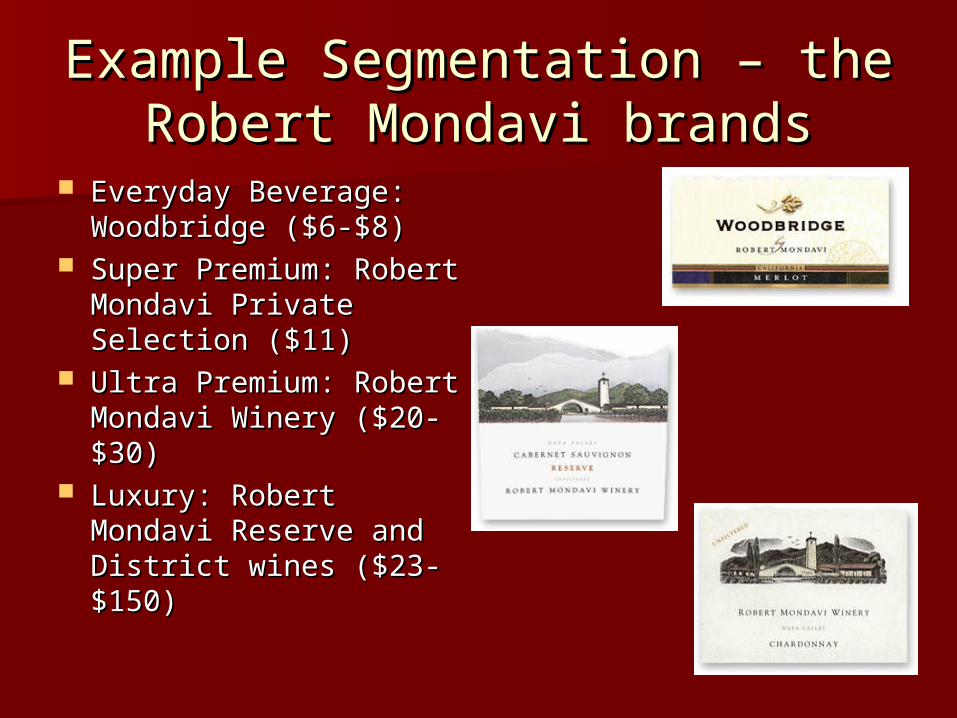

Example Segmentation – the Example Segmentation – the Robert Mondavi brandsRobert Mondavi brands

Everyday Beverage: Everyday Beverage: Woodbridge ($6-$8)Woodbridge ($6-$8)

Super Premium: Robert Super Premium: Robert Mondavi Private Selection Mondavi Private Selection ($11)($11)

Ultra Premium: Robert Ultra Premium: Robert Mondavi Winery ($20-$30)Mondavi Winery ($20-$30)

Luxury: Robert Mondavi Luxury: Robert Mondavi Reserve and District wines Reserve and District wines ($23-$150)($23-$150)

Company ProfilesCompany Profiles

Gallo is the worlds largest winemaker.Gallo is the worlds largest winemaker. Traditionally focused on lower price categories, particularly Traditionally focused on lower price categories, particularly

jug wines.jug wines. Newer brands such as Turning Leaf and Gallo of Sonoma Newer brands such as Turning Leaf and Gallo of Sonoma

are targeted at higher priced segments.are targeted at higher priced segments. 2001 Revenues of $1.65 billion.2001 Revenues of $1.65 billion. Major Brands: Carlo Rossi, Gallo, Gallo Reserve, Night Major Brands: Carlo Rossi, Gallo, Gallo Reserve, Night

Train, Ballatore, Rancho Zabaco.Train, Ballatore, Rancho Zabaco.

Constellation BrandsConstellation Brands Formerly known as Canandaigua Wine Company (Now a subsidiary).Formerly known as Canandaigua Wine Company (Now a subsidiary). The Canandaigua arm focuses on the lower-priced segments while the The Canandaigua arm focuses on the lower-priced segments while the

Franciscan arms targets Super Premium and Luxury segments.Franciscan arms targets Super Premium and Luxury segments. Markets more than 125 brands, including beers, wines, and spirits.Markets more than 125 brands, including beers, wines, and spirits. 2001 Revenues of $3.2 billion, net income of $97.3 million.2001 Revenues of $3.2 billion, net income of $97.3 million. Major Brands: Ravenswood, Estancia, Simi, Inglenook, Almaden, Major Brands: Ravenswood, Estancia, Simi, Inglenook, Almaden,

Franciscan, Talus.Franciscan, Talus. Listed on the NYSE as STZ.Listed on the NYSE as STZ.

Robert MondaviRobert Mondavi Has ownership in luxury Has ownership in luxury

producing wineries like Opus One producing wineries like Opus One (California), Ornellaia (Italy), and (California), Ornellaia (Italy), and Sena (Chile).Sena (Chile).

Mondavi primarily targets price Mondavi primarily targets price segments over $8.segments over $8.

Markets brands in each price Markets brands in each price segment.segment.

2001 Revenues of $0.5 billion, 2001 Revenues of $0.5 billion, net income of $43 million.net income of $43 million.

Listed on the NASDAQ as Listed on the NASDAQ as MOND.MOND.

The Wine GroupThe Wine Group

Primarily owns low-end brands, but has recently Primarily owns low-end brands, but has recently acquired some higher-end brands.acquired some higher-end brands.

Major brands include Franzia, the leading box Major brands include Franzia, the leading box wine in the US, and Corbett Canyon.wine in the US, and Corbett Canyon.

2001 Revenues $300 million, down 14% from 2001 Revenues $300 million, down 14% from 2000.2000.

Formerly part of Coca Cola.Formerly part of Coca Cola. The Wine Group recently purchased the Glen The Wine Group recently purchased the Glen

Ellen and MG Vallejo brands from Diageo.Ellen and MG Vallejo brands from Diageo.

Other Environmental Other Environmental InformationInformation

Government RegulationsGovernment Regulations

The Bureau of Alcohol, Tobacco and Firearms The Bureau of Alcohol, Tobacco and Firearms (ATF) regulates the industry.(ATF) regulates the industry.

Wine is taxed at the state and federal levels.Wine is taxed at the state and federal levels. Individual States determine the regulations Individual States determine the regulations

regarding the sale, marketing, and shipping of regarding the sale, marketing, and shipping of alcoholic beverages.alcoholic beverages.

Sales occur through state owned and operated Sales occur through state owned and operated stores in some states.stores in some states.

Direct Shipping of WineDirect Shipping of Wine

• These restrictions are currently being debated at the state and federal levels.

Wine may not be shipped directly to Wine may not be shipped directly to customers in most US states.customers in most US states.

Direct Shipping of WineDirect Shipping of Wine

In 2002, US district judges overturned In 2002, US district judges overturned "discriminatory" interstate shipping bans in Virginia, "discriminatory" interstate shipping bans in Virginia, North Carolina, Texas, and even in New York.North Carolina, Texas, and even in New York.

In 2002, the US House and Senate passed a provision In 2002, the US House and Senate passed a provision into the Department of Justice Appropriations into the Department of Justice Appropriations Authorization Act allowing wine purchased while Authorization Act allowing wine purchased while visiting a winery, to be shipped to another state.visiting a winery, to be shipped to another state.

SourcesSources Euromonitor.comEuromonitor.com: Information concerning recent : Information concerning recent

trends in sectors, market segment data, forecasts, trends in sectors, market segment data, forecasts, market share information, customer demographics market share information, customer demographics and company profiles.and company profiles.

Business Source PremierBusiness Source Premier article “Moving Forward”: article “Moving Forward”: Regional data of US wine consumptionRegional data of US wine consumption

History-of-Wine.comHistory-of-Wine.com: Everything from the history of : Everything from the history of wine, wine production around the world, the wine, wine production around the world, the popularity of wine in various regionspopularity of wine in various regions

Winebusiness.comWinebusiness.com: Retail wine sales information : Retail wine sales information from the end of September 2002.from the end of September 2002.

SourcesSourcescont.cont.

Hoovers.com: Company Profiles WineryExchange.com: Market Segments RobertMondavi.com: Price Segment offering

information, company information Constellationbrands.com: Company Information Gallo.com: Company Information California Association of Winegrowers (cawg.org):

Industry News, per capita consumption statistics Forbes, January 6, 2003, p 118: “Seeing Stars.”:

Company information

SourcesSourcescont.cont.

Wineinstitute.orgWineinstitute.org Mindbranch.comMindbranch.com Wine Business MonthlyWine Business Monthly