Embed Size (px)

Citation preview

International Management Review Vol. 5 No. 2 2009

73

The Value Relevance of Fixed Asset Revaluation Reserves in International Accounting

Gyung Paik Brigham Young University, Provo, Utah, USA

[Abstract] The Securities and Exchange Commission (SEC) of the U.S. has recently proposed that all U.S. firms be required to issue financial statements in accordance with IFRS by 2014. Under IFRS, the rules for measurement of fixed assets are presented in IAS 16, which allows firms to choose either the cost model or the revaluation model. In this study, I investigate the effect of adopting the IFRS standard for fixed asset revaluation by examining the relationship between changes in revaluation reserves and stock prices. Out of the 15 countries used for the analyses, five countries have revaluation reserves that are statistically significant in explaining the market value of equity, suggesting that revaluation reserves are value relevant for those countries. I further break down the sample countries and categorize them based on the legal system to which they are subject, whether common law or code law. The results suggest that revaluation reserves of common law countries are value relevant, while those of code law countries are not. This study contributes to the international accounting literature by suggesting that the effect of adopting new IFRS rules, such as IAS 16, may differ in each country due to various legal, economic, cultural, and social forces.

[Keywords] International accounting; value relevance; asset revaluation; revaluation reserves

Introduction In August 2008, the Securities and Exchange Commission (SEC) of the U.S. outlined a “road map” promoting the acceleration of the convergence effort of US firms to adopt International Financial Reporting Standards (IFRS). It proposes that by 2014, all U.S. firms will be required to issue financial statements in accordance with IFRS (see SEC for Immediate Release 2008-184).

In this study, I investigate the effect of adopting the IFRS standard for fixed asset revaluation (IAS 16) using companies in the countries where firms follow IFRS and are able to choose either the cost method or the fair value method to value their long-term fixed assets. If firms choose the fair value method, they revalue their fixed assets annually as measured by market value, and the revaluation reserves of fixed assets affect the equity value of the firms. In this study, I specifically investigate the relationship between changes in revaluation reserves and stock prices in various countries.

The sample for this study includes 15 countries, each with at least 30 companies that have valid revaluation reserves data for the year 2005. Using multivariate analyses, which examine the relationship between the amount of revaluation reserves and the market value of equity, I find that five of the 15 countries selected in the sample have revaluation reserves that are statistically significant in explaining the market value of equity, suggesting that revaluation reserves are value relevant for those countries. The revaluation reserves for the other 10 countries are not statistically significant, signifying that for those countries, revaluation reserves are not considered for investment decisions and are, therefore, not value relevant.

I further examine the value relevance of revaluation reserves by partitioning the sample countries into two different country groups. I categorize countries based on their legal system to which they are subject, whether common law or code law, as suggested by Radebaugh, Sidney, and Black (2006) and Shenkar and Luo (2008). The results suggest that revaluation reserves of common law countries are value relevant, while those of code law countries are not.

This paper contributes to the existing knowledge on the value relevance of asset revaluations by examining equity valuation based on variables other than those commonly used, such as net income and the book value of equity for various countries. By doing so, this study contributes to the

International Management Review Vol. 5 No. 2 2009

74

international accounting literature by suggesting that the effect of adopting new IFRS rules, including IAS16, may differ due to the legal, cultural, and social differences of each country. This study also makes predictions regarding the value relevance of revaluation reserves for US firms once they are required to adopt IFRS and are, thus, allowed to report fixed assets based on fair market value.

The rest of the paper is organized as follows: I discuss the background of IFRS, international accounting rules for fixed assets, and the review of prior research regarding fixed asset revaluations in section two. In section three, I discuss the research questions of this study and explain the hypotheses. I discuss the data collection procedures and methodology in section four. In section five, I discuss the main results and the general implications of the results. Finally, in section six, I make concluding remarks.

Background and Prior Research on Revaluation Reserves

Difference between US GAAP and IFRS on Fixed Asset Valuation

To facilitate the need for comparability and to reduce the cost of financial statement reporting, the European Union (EU) adopted IFRS in 2005. Many non-EU countries around the world have also adopted IFRS or have outlined incremental steps for convergence in an effort to increase accessibility to foreign sources of equity capital. In the U.S., the government and regulatory bodies, as well as accounting standards setters, have made commitments and set agendas to reduce the differences between U.S. GAAP and IFRS to move closer to convergence. In 2002 at a meeting in Norwalk, Connecticut, the IASB and the FASB agreed to harmonize their agendas and to work toward reducing the differences between IFRS and U.S. GAAP (the Norwalk Agreement). Beginning in 2008, foreign private issuers are permitted to file financial statements in accordance with IFRS without reconciliation to U.S. GAAP. In August 2008, the SEC outlined a “roadmap” that allows the early adoption of IFRS for some U.S. companies in 2010 and requires all companies to use IFRS in 2014 (Johnson 2009).

Under U.S. GAAP, the current rules and guidelines for measurement of long-term fixed assets, including property, plant, and equipment are presented in SFAS 144. When fixed assets are acquired, they are initially recorded at cost. In subsequent years, when an asset’s book value deviates from market value, an accounting adjustment is required to reflect this change. SFAS 144 states that an impairment loss must be recognized when the sum of future undiscounted cash flows of the asset is less than its carrying amount. When this occurs, the asset is written down to its fair value, or discounted future cash flows, and the loss is recognized in the income statement. However, no upward revaluation is permitted when the market value of the asset rises above its carrying book value, and, therefore, no adjustments are made to the financial statements.

Under IFRS, the rules for measurement of fixed assets are presented in IAS 16, which allows two valuation models for measurement of fixed assets: (1) The cost model and (2) The revaluation model. Under the cost model, fixed assets are carried at historical cost less accumulated depreciation and impairments. Under the revaluation model, fixed assets are carried at fair market value at the date of revaluation less accumulated depreciation. Revaluations are to be made so that the carrying amount does not differ significantly from fair value. At the revaluation date, when the market value is higher than the carrying book value, the amount that the market value exceeds the book value is recognized as “revaluation surplus.” This surplus bypasses the income statement and is credited directly to revaluation reserves in owner’s equity on the balance sheet in the year that the assets are revalued.

In sum, under US GAAP, when the market value of fixed assets rises above the book value at each reporting date, no adjustment needs to be made on the financial statements. However, under IFRS, an upward revaluation equal to the amount by which the market value exceeds the carrying book value is recognized and credited to the revaluation reserve account in owners’ equity on the balance sheet.

Prior Research on Revaluation Reserves Stock Price Relevance. Easton, Eddy, and Harris (1993) use a sample of 100 large Australian

International Management Review Vol. 5 No. 2 2009

75

firms from 1981 to 1990 to examine the value relevance of revaluation reserves. They find that changes in asset revaluation reserves statistically explain stock price returns over the traditional earnings and earnings change variables, and that the level of revaluation reserves has significant explanatory power for price-to-book ratios. Similarly, Barth and Clinch (1998) show that revalued assets are value relevant to stock prices, and the revalued amount correlates to the firm’s profitability in the future based on a sample of 776 companies in Australia during 1996.

In the discussion paper of Easton, Eddy, and Harris (1993), Bernard (1993) points out that a market-based test provides only indirect evidence about the relation between revaluation reserves and future operating performance. Following Bernard’s suggestion, Aboody, Barth, and Kasznik (1999) examine a sample of UK firms and show that asset revaluations are significantly and positively related to changes in future performance, measured by operating income and cash flows from operations. Jaggi and Tsui (2001) examined fixed asset revaluation in Hong Kong from 1991 to 1995 and found a significant positive relationship between revaluation and future operating income, signaling the usefulness and relevance of the fair market value of assets to financial statement users. In addition, Cotter and Zimmer (1999) obtained a sample of Australian firms from 1987 to 1993 and found that the propensity to revalue fixed assets was related to the degree of management certainty that the value increase will be realized in future cash flows.

Firm Characteristics and Asset Revaluations. Prior studies have examined what firm characteristics are related to the decision of revaluing fixed assets. Brown, Izan, and Loh (1992) selected a sample of 204 Australian firms during 1974-1977 (higher inflation) and 206 Australian firms from 1984-1986 (lower inflation), and have shown that firms revaluing long-term assets are large in size, have high leverage, and are close to violation of debt covenants. Cotter and Zimmer (1995) and Whittred and Chan (1992) used Australian firm data, and showed that management incentives for asset revaluation were closely associated with declining cash flows from operations and corresponded to the demand of creditors for collateral borrowings.

Missonier-Piera (2007) uses a sample of industrial and commercial firms in Sweden during 1994, 1997, 2000, and 2005 to show that asset revaluation improves creditworthiness of companies relying on debt financing and has the effect of increasing companies’ borrowing capacity. Similarly, Nichols and Buerger (2002) find that German banks give significantly higher loans to companies valuing fixed assets using the fair value method. In sum, prior studies have provided strong evidence of a relationship between the decision of revaluing fixed assets and firms’ financing need.

Additionally Lin and Peasnell (2000) examined a sample of UK firms that revalued fixed assets during 1989 to 1991 and found that upward revaluation was associated with depletion of equity, indebtedness, poor liquidity, size, and fixed asset intensity. Gaeremynck and Veugelers (1999) used a sample of Belgian industrial companies from 1989 to 1994 to show that successful firms in those industries with a high variance in performance or with low equity-to-debt ratios, are less likely to revalue assets, and that firms that move closer to technical default or violate covenants are more likely to revalue assets.

Regarding superiority between the fair value method and the cost method, Herrmann, Saudagaran, and Thomas (2006) find that for long-term assets, fair value is superior to historical cost because of the characteristics of predictive value, feedback value, timeliness, neutrality, representational faithfulness, comparability, and consistency. Cotter and Richardson (2002) use a sample of Australian firms during the period from 1981 to 1999 and find that asset revaluations are more reliable from independent appraisers than from the company’s board of directors, with reliability being measured as upward revaluation write-downs in subsequent years.

Hypotheses The focus of this study is to examine whether the annual revaluation reserves of fixed assets are value relevant to firm equity values. Because assets by definition are probable future economic benefits to entities, the upward asset revaluation to fair value must be due to an increase in probable future benefit.

International Management Review Vol. 5 No. 2 2009

76

I predict that the event of an upward asset revaluation is positively correlated with stock price because of the perceived increase in value of assets and the probable future cash flows associated with the higher fixed asset value. My first hypothesis, therefore, is H1: Revaluation reserves are value relevant.

Furthermore, revaluation reserves are positively related to stock prices. I further partition countries into two different country groups, and test the value relevance of

revaluation reserves. I categorize countries based on their legal system—countries subject to a common law system and countries subject to a code law system (Radebaugh, et al., 2006). Common law refers to a legal system in which court decisions are based on prior authority of similar cases or precedent. Code law, on the other hand, refers to a legal system that is based on statutes enacted by the legislature. Countries included in common law or code law groups are presented in Table 1.

Table 1. Common vs. Code Law Country Classification

Common Law Code Law

Australia BrazilBermuda Cayman Islands

Great Britain GreeceHong Kong Indonesia

India JapanMalaysia Korea

Philippines ThailandSingapore

I predict that in a common law system, the reliance on precedents results in relatively precise guidance on terms of contract and expectations of performance, and, therefore, stock markets operating under it will provide information that is relatively transparent and complete. In contrast, companies in a code law system may not fully disclose financial information when there is no precedent to be based upon because the probability of potential violation of the law is assessed to be low. Therefore, stock markets operating under a code law system may be less efficient and less information transparent than those under a common law system. Therefore, I predict that stock markets operating under a common law system are more efficient and reliable than those operating under a code law system to the extent that the information of fixed asset revaluation reserves in countries under a common law system are to be more informative for creditors and investors. My second hypothesis, therefore, is H2: Revaluation

reserves are more value relevant in countries under common law than in those under code law.

Sample Selection and Methodology Sample I include all countries available in the Global Industrial/Commercial database found in the Compustat Global database. I collect data for revaluation reserves, net income, and the book value of equity for the year 2005. To obtain the 2005 annual revaluation reserve amounts, I collect data for the ending balance of revaluation reserve for both 2004 and 2005 and then subtract the ending reserve balance of 2004 from 2005 to arrive at annual revaluation reserve amounts for 2005. Many countries in the database have no revaluation reserve balance for 2004 or 2005 either because they were not permitted to revalue their fixed assets upward under their accounting rules or because no deviation of book value from the market value existed at the balance sheet date. I exclude these companies from my analysis. I further exclude 65 countries from my analysis due to their small sample size of companies and I am left with 15 countries that have a sample size of at least 30 companies.

Firms’ market values are calculated by multiplying stock price by the number of shares outstanding. I collect stock price and common shares outstanding data from Global Security Daily found in the Compustat Global database. I use stock price three months after the company’s fiscal year end and the number of shares at that date because I, along with many prior value-relevance studies

International Management Review Vol. 5 No. 2 2009

77

(see for example, Barlev, et al., 2007), assume that the market takes an average of three months to absorb information regarding changes in asset values for pricing firm’s securities.

Methods

I use the regression model to conduct the value relevance analysis on fixed asset revaluation. I include annual change in revaluation reserves as well as net income and the book value of equity as independent variables to control for their effect on price. All independent variables are scaled (divided) by number of shares. I then run the regression against the dependent variable, the stock price three months after fiscal year end. Revaluation reserve is my variable of interest as I analyze its market value relevance. The equation of the regression model is:

Price = a1NI + a2BV + a3RR + ε

Where: NI is the net income reported by companies at fiscal year end. BV is the book value of shareholders’ equity on the balance sheet date. RR is the annual change in the revaluation reserve balance that adjusts the book value of fixed assets to market value

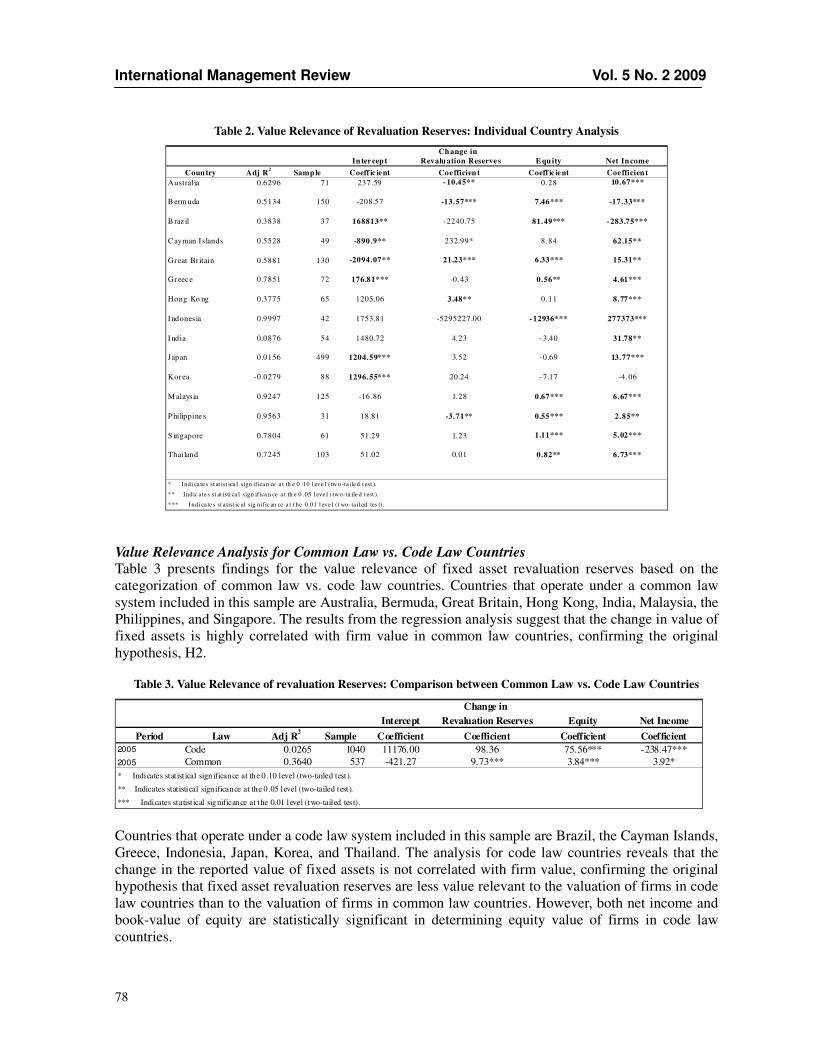

Results Value Relevance Analysis for Each Country Table 2 presents findings for the value relevance of revaluation reserves, net income, and book value of equity for each country. It reveals that the revaluation reserves for Great Britain and Bermuda are statistically significant at the 1 percent level in explaining stock prices, and the revaluation reserves for Australia, Hong Kong, and the Philippines are statistically significant at the 5 percent level. However, revaluation reserves for the other ten countries are not value relevant. Also the signs of the coefficients of revaluation reserves for Australia, Bermuda, and the Philippines are opposite of the predictions. The negative significant coefficients of revaluation reserves may indicate that regardless of the upward revaluation of fixed assets, the market pays more attention to other negative financial and accounting performance of revaluating companies. In sum, only two countries, Great Britain and Hong Kong, support my hypothesis, H1.

For each of the five countries with value-relevant revaluation reserves, their reported net income numbers are also value relevant (the net income for these five countries are statistically significant at least at the 5 percent level). However, the book-value of equity is not always value relevant; the book value of equity for Hong Kong and Australia is not value relevant.

International Management Review Vol. 5 No. 2 2009

78

Table 2. Value Relevance of Revaluation Reserves: Individual Country Analysis

Ch ange in

In ter cep t Revalu ation Reserve s E qu ity Net In come

Coun try Adj R2

Samp le Coeff ic ie nt Coe fficien t Coeff ic ie nt Coe fficien t

Australia 0.6296 71 237.59 - 10.45** 0.28 10.67***

B erm uda 0.5134 150 -208.57 -13.57*** 7.46*** -17.33***

B raz il 0.3838 37 168813** - 2240.75 81.49*** -283.75***

C ayman I slands 0.5528 49 -890.9** 232.99* 8.84 62.15**

Great Br itain 0.5881 130 -2094.07** 21.23*** 6.33*** 15.31**

Greec e 0.7851 72 176.81*** -0.43 0.56** 4.61***

Hong Ko ng 0.3775 65 1205.06 3.48** 0.11 8.77***

I ndonesia 0.9997 42 1753.81 -5295227.00 - 12936*** 277373***

I ndia 0.0876 54 1480.72 4.23 - 3.40 31.78**

Japan 0.0156 499 1204.59*** 3.52 - 0.69 13.77***

Korea -0.0279 88 1296.55*** 20.24 - 7.17 -4.06

M alaysia 0.9247 125 -16.86 1.28 0.67*** 6.67***

P hilippine s 0.9563 31 18.81 -3.71** 0.55*** 2.85**

S ingapore 0.7804 61 51.29 1.23 1.11*** 5.02***

Thailand 0.7245 103 51.02 0.01 0.82** 6.73***

* Indi ca te s st at ist ica l sign if ican ce a t th e 0 .10 l eve l ( tw o-ta iled t est ).

** Indic a tes st at isti ca l sign if ica n ce a t th e 0 .05 l eve l ( two-ta ile d t est ).

*** Indi ca te s st a tist ic al sig nif ic an ce a t t he 0.01 l eve l ( t wo-ta il ed tes t) .

Value Relevance Analysis for Common Law vs. Code Law Countries

Table 3 presents findings for the value relevance of fixed asset revaluation reserves based on the categorization of common law vs. code law countries. Countries that operate under a common law system included in this sample are Australia, Bermuda, Great Britain, Hong Kong, India, Malaysia, the Philippines, and Singapore. The results from the regression analysis suggest that the change in value of fixed assets is highly correlated with firm value in common law countries, confirming the original hypothesis, H2.

Table 3. Value Relevance of revaluation Reserves: Comparison between Common Law vs. Code Law Countries

Change in

Intercept Revaluation Reserves Equity Net Income

Period Law Adj R2

Sample Coefficient Coefficient Coefficient Coefficient

2005 Code 0.0265 1040 11176.00 98.36 75.56*** -238.47***2005 Common 0.3640 537 -421.27 9.73*** 3.84*** 3.92** Indicates stat ist ical sign ificance at the 0 .10 level (two-tailed test).

** Indicates stat istical significance at the 0 .05 level (two-tailed test).

*** Indicates statist ical significance at the 0.01 level (two-tailed test). Countries that operate under a code law system included in this sample are Brazil, the Cayman Islands, Greece, Indonesia, Japan, Korea, and Thailand. The analysis for code law countries reveals that the change in the reported value of fixed assets is not correlated with firm value, confirming the original hypothesis that fixed asset revaluation reserves are less value relevant to the valuation of firms in code law countries than to the valuation of firms in common law countries. However, both net income and book-value of equity are statistically significant in determining equity value of firms in code law countries.

International Management Review Vol. 5 No. 2 2009

79

Conclusion As the U.S. gradually moves closer to adoption of IFRS, U.S. financial statement preparers and users need to know what impact the adoption will have. In this paper, I focus on the impact of the IFRS standard dealing with the valuation of fixed assets. Specifically, I examine how the IFRS accounting treatment of revaluation reserves of fixed assets impacts adjustments to firm market price. To do this, I select a sample of 15 countries that adopted IFRS before 2005 and regress fixed asset revaluation reserves on stock price for the companies in each country. I find that five of the sample countries have revaluation reserves that are value relevant to firm market value, and ten of the sample countries have revaluation reserves that are not value relevant to firm market value.

I also categorize the countries based on legal system and find that countries that are subject to a common law system have fixed asset revaluation reserves that are value relevant to firm value. On the other hand I find that countries that are subject to a code law system have fixed asset revaluation reserves that are not value relevant to firm value. In addition to the legal system categorization, I partition countries into four groups based on their accounting system—British-American Common, Continental, South American, and others.

Based on the findings of this study, some predictions can be derived regarding the value relevance of revaluation reserves for U.S. firms once they are required to adopt IFRS and are, thus, required to report fixed assets based on fair market value. The U.S. is known to have a common law legal system. Therefore, after adoption of IAS16, it is more likely than not the revaluation reserves of U.S. firms will be value relevant to stock prices. This study has examined how the adoption of IAS 16 will affect the stock prices of firms in different countries. Future research may examine the effect of other IFRS accounting rules, such as derivatives, deferred taxes, and leases on various countries.

References Aboody, D., Barth, M., & Kasznik, R. (1999). Revaluations of fixed assets and future firm performance:

Evidence from the UK. Journal of Accounting & Economics, 26, 149-178. Barlev, B., Fried, D., Haddad, J., & Livnat, J. (2007). Reevaluation of revaluations: A cross-country examination

of the motives and effects on future performance. Journal of Business Finance & Accounting, 34(7-8), 1025-1050.

Barth, M. & Clinch, G. (1998). Revalued financial tangible and intangible assets: Association with share prices and non-market based estimates. Journal of Accounting Research, 36, 199-233.

Bartov, E. (1993). The timing of asset sales and earnings manipulation. The Accounting Review, 68, 840-855. Bernard, V. (1993). Discussion of an investigation of revaluations of tangible long-lived assets. Journal of

Accounting Research, 31, 39-45. Brown, P., Izan, H., & Loh, A. (1992). Fixed asset revaluations and managerial incentives. Abacus, 28(1) 36-57. Cotter, J., & Zimmer, I. (1995). Asset revaluations and assessment of borrowing capacity. Abacus, 31(2), 136-

151. Cotter, J., & Richardson, S. (2002). Reliability of asset revaluations: The impact of appraiser independence.

Review of Accounting Studies, 7(4), 435-457. Easton, P., Eddy, P., & Harris, T. (1993). An Investigation of revaluations of tangible long-lived assets. Journal

of Accounting Research, 31(3), 1-38. Financial Accounting Standards Board (FASB) (2001). Accounting for the impairment or disposal of long-lived

assets. Statement of Financial Accounting Standard No. 144, Norwalk, CT: FASB. Gaeremynck, A., & Veugelers, R. (1999). The revaluation of assets as a signaling device: a theoretical and an

empirical analysis. Accounting and Business Research, 29(2), 123–138. Herrmann, D., Saudagaran, S., & Thomas, W. (2005). The quality of fair value measure for property, plant and

equipment. Accounting Forum, 30, 43-59. International Accounting Standards Board (IASB). (1982). Accounting for property, plant, and equipment.

International Accounting Standard, 16. Jaggi, B., & Tsui, J. (2001). Management motivation and market assessment: revaluations of fixed assets.

Journal of International Financial Management and Accounting, 12(2), 160–187. Johnson, S. (2009). SEC pushes back IFRS roadmap. Retrieved Feb.4, 2009 from http://www. CFO.com Lin, Y., & Peasnell, K. (2000). Fixed asset revaluation and equity depletion in UK. Journal of Business Finance

International Management Review Vol. 5 No. 2 2009

80

and Accounting, 27(3–4), 359–394. Missonier-Piera, F. (2007). Motives for fixed-asset revaluation: An empirical analysis with Swiss data. The

International Journal of Accounting, 42(2), 186-205. Nichols, L., & Buerger, K. (2002). An investigation of the effect of valuation alternatives for fixed assets on the

decision of statement users in the United States and Germany. Journal of International Accounting

Auditing & Taxation, 11, 155–163. Radebaugh, L., Sidney, J., & Black, E. (2006). International accounting and multinational enterprises. John

Wiley & Sons, Inc. Securities and Exchange Commission (SEC). (2008). SEC proposes roadmap toward global accounting

standards to help investors compare financial information more easily. For Immediate Release 2008-

184, August 27. Shenkar, O., & Luo, Y. (2008). International business. Sage Publication, Inc. Whittred, G., & Chan, K. (1992). Asset revaluations and mitigations of underinvestment. Abacus, 28 (1), 58-74.

International Management Review Vol. 5 No. 2 2009

108

Contributing Authors Dr. Mary E. Malliaris is Associate Professor of Information Systems at Loyola University Chicago. Her research and teaching interests are in databases, data warehousing, data mining and healthcare informatics. She has published articles in The International Journal of Computational Intelligence and

Organizations, Neural Networks in Finance and Investing, Neurocomputing, Neurovest, and Applied

Intelligence among others. She has served as a reviewer for The Financial Review, The Journal of

Applied Business Research, Mitchell-McGraw Hill Publishers, Wall Data, IEEE, and Decision Sciences. She is currently the production editor for The Journal of Economic Asymmetries. Email:

[email protected]. Dr. Maria Pappas received her PhD in Counseling Psychology from Loyola University and a J.D. from Chicago-Kent College of Law. After careers in counseling, teaching and law, she entered politics. She served as a Commissioner of Cook County for two terms and is currently in her third term as the Treasurer of Cook County in Illinois. She also serves as the President of the Thorek Memorial Hospital Foundation in Chicago. Her research interests include financial issues in county government, teen pregnancy, and non-profit governance. She can be reached at 312-603-6202. Mr. Eddy Junarsin is a Fulbright scholar at the College of Business, Southern Illinois University at Carbondale. He was an assistant professor at the Faculty of Business and Economics, Gadjah Mada University and a visiting professor at the Faculty of Business and Law, Pforzheim University of Applied Sciences. His research interests cover business areas such as finance, creativity, and innovation. Dr. Piero Mella is full Professor of Business Economics and Administration at the Faculty of Economics at Pavia University, Italy since 1985. Dr. Mella served as Head of the Department of Business Research and later was elected as Dean of the Economics Faculty at the University of Pavia from 1987 till 1993. Dr. Mella has published widely and created the scientific Journal Economia

Aziendale on line at www.ea2000.it. His interests concern the fields of Complex and Holonic Systems, Networks, Systems Thinking, and Control Systems. In 1992, he proposed the Combinatory System Theory, described at the web site: www.ea2000.it/cst.

Dr. Paul Sicilian is Associate Professor of Economics in the Seidman College of Business at Grand Valley State University. He earned his B.A. degree at Tulane University and his M.S. and Ph.D. degrees at the University of Illinois, Urbana-Champaign. His teaching interests are in principles of microeconomics, labor economics, industrial organization, and econometrics. His primary research interest is in labor markets. His published papers have appeared in Southern Economic Journal, Applied Economics, Journal of Labor Research, and Quarterly Review of Economics and Finance.

Dr. Torki Mejhim Al-Fawwaz is Assistant Professor and holds a Ph.D of economics specialized in investment. Dr. Al-Fawwaz was appointed at Al.Balqa Applied Unviersity in 2000 as Vice Dean of Zarqa' University College and Head of Business and Financial Department. Morover, he is a member of many organisations such as Jordan Society for Scientific Research, Committees in Al-Balqa' Applied University Jordan and Member of Zarqa' University College Council, Al-Balqa' Applied University. As regard to publications and research, Al-Fawwaz has many published papers in different journals such as International Management Review (IMR) and European Journal of Social Sciences and of West Asian Studies and so on. He also actively involved in many international conferences. Dr. Gyung H. Paik earned his Ph.D. at the University of Illinois, Urbana-Champaign in 2001. Currently he is an assistant professor of accounting at Brigham Young University, Utah, USA. His research

International Management Review Vol. 5 No. 2 2009

109

interest is in financial accounting. Dr. Rodney Jean-Baptiste, CMA, Ph.D. has worked in accounting for more than 15 years including management positions for Fortune 500 companies, and has done many consulting assignments in ERP. He has also served in the adjunct faculty of many universities including Southern New Hampshire University. He is a CMA (certified management accountant) and a member of the IMA (Institute Of Management Accountants) since 1995. Received a B’S in Business with concentration in accounting at Worcester State College in 1988, an MBA from Anna-Maria College in 1992, and a Ph.D. in Organization and Management at Capella University in 2006. His areas of interest include ERP systems, accounting information systems, knowledge management, management accounting, and personal finance. He can be reached at [email protected] or [email protected] Dr. Wei Guo is Associate Professor of School of Management, Huazhong University of Science & Technology (HUST). He holds Ph.D of management. He finished his postdoctoral research during 2003-2005 in postdoctoral research center of Control Science & Engineering in Wuhan, China. He has published 53 papers in core journals in the areas of capital markets, real estate credit risk management, finance and accounting both in Chinese and in English. He is the vice secretary general of Wuhan System Engineering Society, a member of IEEE. Dr. Guo can be reached at [email protected]

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.