Embed Size (px)

Citation preview

Thursday

March 23, 2017

March 23, 2017

Fed's Yellen, Kashkari, Kaplan Speak; New Home SalesBy Ben Baris and Geoff King

What to Watch: At 8:45 a.m., U.S. Federal Reserve Chair gives the Janet Yellenopening speech at the Fed’s two-day Community Development Research Conference in Washington. The meeting convenes policy makers to consider the economic future of children and communities. Minneapolis Fed President speaks at the Neel Kashkarisame event at 12:30 p.m. Dallas Fed President will speak at the Robert KaplanChicago Council on Global Affairs in a moderated Q&A session on the U.S. economic outlook and monetary policy at 7 p.m.

Economics: U.S. are forecast to decline to 240,000 in the weekinitial jobless claims ended March 18 from 241,000 the week prior, according to the consensus estimate of economists surveyed by Bloomberg, 8:30 a.m. are expected to have New home sales risen 1.6 percent in February from a month earlier to a 564,000 seasonally adjusted annualized rate, following a 3.7 percent advance in January, 10 a.m. The International

holds a two-day conference on “Gender and Macroeconomics” to Monetary Funddiscuss research and policy implications in Washington.

Government: French Republican presidential candidate gives a two-Francois Fillonhour television interview at 4 p.m.

Markets: A global selloff that spurred the biggest drop in shares since equitiesPresident ’s election eased as investors stepped back before a key U.S. Donald Trumpvote on health care. The halted a seven-day rally and retreated.yen gold

(All times local for New York.)

Full story with live chart on the Bloomberg .terminal

Commentary in This Issue

Credit-default swap traders may be more pessimistic about Mexico, Chile, Italy and France than the big three rating creditagencies: Michael McDonough (pictured) and Felipe Hernandez.

The spike in housingdemand at the beginning of the yearappears to be fading:Yelena Shulyatyeva and Carl Riccadonna.

Quote of the Day

"We believe that populism’s role in shaping economic conditions will probably be more powerful than classic monetary and fiscal policies." — Bridgewater Associates founder Ray Dalio

and three colleagues in a “Daily

Observations” report

Jay Clayton, the Wall Street lawyer nominated by President Donald Trump to lead the Securities and Exchange Commission, he sees said“meaningful room for improvement” to make U.S. markets more appealing to businesses and investors. (Link to terminal)

151 Billion Cubic Feet

The amount America’s natural gasstockpiles fell by in the seven days ended March 17, based on estimates compiled by Bloomberg. That would be the biggest decline ever for the third week of March, data from theU.S. Energy Information Administration show. (Link to terminal)

Sovereign Debt

Trump Trade Turns Chump Trade as Bullish Dollar Bets Sour

Dollar bears are back from the wilderness. The currency slid to the lowest since November on March 22, and options show investors are becoming more pessimistic on the greenback versus the euro and yen. The dollar has almost erased its gains from the so-called Trump Trade, as pro-growth policies from the presidential administration have yet to materialize. UBS AG’s wealth-management unit recommended selling the dollar against the euro, and JPMorgan Chase & Co., the world’s second-biggest currency trader, advised clients to ditch bullish bets in the short term. “The case has become more compelling” to short the dollar, said Constantin Bolz, an FX strategist at UBS in Zurich. The bullish dollar consensus since President Donald Trump’s election in November “is turning step by step” as markets question U.S. policies and their effectiveness.

— Lananh Nguyen and Robert Fullem

Economics 2 March 23, 2017

Sovereign Debt

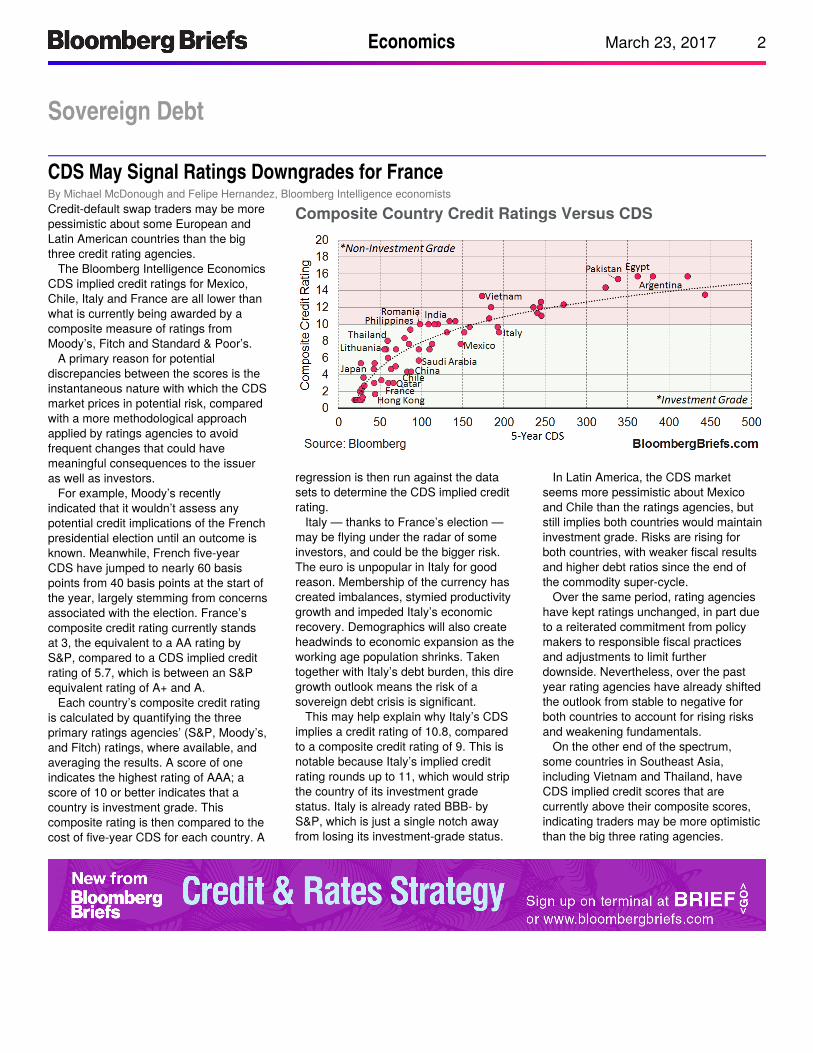

CDS May Signal Ratings Downgrades for FranceBy Michael McDonough and Felipe Hernandez, Bloomberg Intelligence economistsCredit-default swap traders may be more pessimistic about some European and Latin American countries than the big three credit rating agencies.

The Bloomberg Intelligence Economics CDS implied credit ratings for Mexico, Chile, Italy and France are all lower than what is currently being awarded by a composite measure of ratings from Moody’s, Fitch and Standard & Poor’s.

A primary reason for potential discrepancies between the scores is the instantaneous nature with which the CDS market prices in potential risk, compared with a more methodological approach applied by ratings agencies to avoid frequent changes that could have meaningful consequences to the issuer as well as investors.

For example, Moody’s recently indicated that it wouldn’t assess any potential credit implications of the French presidential election until an outcome is known. Meanwhile, French five-year CDS have jumped to nearly 60 basis points from 40 basis points at the start of the year, largely stemming from concerns associated with the election. France’s composite credit rating currently stands at 3, the equivalent to a AA rating by S&P, compared to a CDS implied credit rating of 5.7, which is between an S&P equivalent rating of A+ and A.

Each country’s composite credit rating is calculated by quantifying the three primary ratings agencies’ (S&P, Moody’s, and Fitch) ratings, where available, and averaging the results. A score of one indicates the highest rating of AAA; a score of 10 or better indicates that a country is investment grade. This composite rating is then compared to the cost of five-year CDS for each country. A

regression is then run against the data sets to determine the CDS implied credit rating.

Italy — thanks to France’s election — may be flying under the radar of some investors, and could be the bigger risk. The euro is unpopular in Italy for good reason. Membership of the currency has created imbalances, stymied productivity growth and impeded Italy’s economic recovery. Demographics will also create headwinds to economic expansion as the working age population shrinks. Taken together with Italy’s debt burden, this dire growth outlook means the risk of a sovereign debt crisis is significant.

This may help explain why Italy’s CDS implies a credit rating of 10.8, compared to a composite credit rating of 9. This is notable because Italy’s implied credit rating rounds up to 11, which would strip the country of its investment grade status. Italy is already rated BBB- by S&P, which is just a single notch away from losing its investment-grade status.

In Latin America, the CDS market seems more pessimistic about Mexico and Chile than the ratings agencies, but still implies both countries would maintain investment grade. Risks are rising for both countries, with weaker fiscal results and higher debt ratios since the end of the commodity super-cycle.

Over the same period, rating agencies have kept ratings unchanged, in part due to a reiterated commitment from policy makers to responsible fiscal practices and adjustments to limit further downside. Nevertheless, over the past year rating agencies have already shifted the outlook from stable to negative for both countries to account for rising risks and weakening fundamentals.

On the other end of the spectrum, some countries in Southeast Asia, including Vietnam and Thailand, have CDS implied credit scores that are currently above their composite scores, indicating traders may be more optimistic than the big three rating agencies.

Housing Market

Composite Country Credit Ratings Versus CDS

Economics 3 March 23, 2017

Housing Market

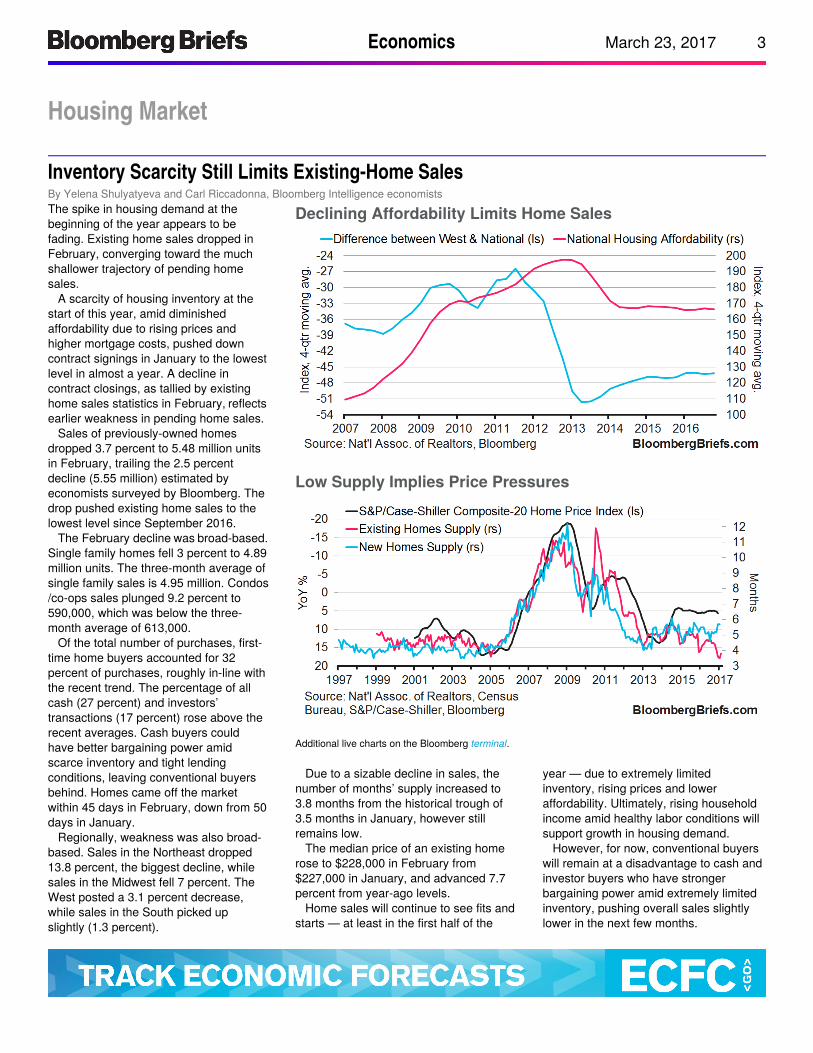

Inventory Scarcity Still Limits Existing-Home SalesBy Yelena Shulyatyeva and Carl Riccadonna, Bloomberg Intelligence economists The spike in housing demand at the beginning of the year appears to be fading. Existing home sales dropped in February, converging toward the much shallower trajectory of pending home sales.

A scarcity of housing inventory at the start of this year, amid diminished affordability due to rising prices and higher mortgage costs, pushed down contract signings in January to the lowestlevel in almost a year. A decline in contract closings, as tallied by existing home sales statistics in February, reflectsearlier weakness in pending home sales.

Sales of previously-owned homes dropped 3.7 percent to 5.48 million units in February, trailing the 2.5 percent decline (5.55 million) estimated by economists surveyed by Bloomberg. The drop pushed existing home sales to the lowest level since September 2016.

The February decline was broad-based.Single family homes fell 3 percent to 4.89 million units. The three-month average of single family sales is 4.95 million. Condos/co-ops sales plunged 9.2 percent to 590,000, which was below the three-month average of 613,000.

Of the total number of purchases, first-time home buyers accounted for 32 percent of purchases, roughly in-line with the recent trend. The percentage of all cash (27 percent) and investors’ transactions (17 percent) rose above the recent averages. Cash buyers could have better bargaining power amid scarce inventory and tight lending conditions, leaving conventional buyers behind. Homes came off the market within 45 days in February, down from 50 days in January.

Regionally, weakness was also broad-based. Sales in the Northeast dropped 13.8 percent, the biggest decline, while sales in the Midwest fell 7 percent. The West posted a 3.1 percent decrease, while sales in the South picked up slightly (1.3 percent).

Additional live charts on the Bloomberg .terminal

Due to a sizable decline in sales, the number of months’ supply increased to 3.8 months from the historical trough of 3.5 months in January, however still remains low.

The median price of an existing home rose to $228,000 in February from $227,000 in January, and advanced 7.7 percent from year-ago levels.

Home sales will continue to see fits and starts — at least in the first half of the

year — due to extremely limited inventory, rising prices and lower affordability. Ultimately, rising household income amid healthy labor conditions will support growth in housing demand.

However, for now, conventional buyers will remain at a disadvantage to cash and investor buyers who have stronger bargaining power amid extremely limited inventory, pushing overall sales slightly lower in the next few months.

Data & Events

Declining Affordability Limits Home Sales

Low Supply Implies Price Pressures

Economics 4 March 23, 2017

Data & Events

TIME COUNTRY EVENT SURVEY PRIOR

7:00 Brazil FGV CPI IPC-S 0.38% 0.35%

7:00 U.K. CBI Retailing Reported Sales 4 9

7:00 U.K. CBI Total Dist. Reported Sales 20 25

8:30 U.S. Revisions: Initial Jobless Claims — —

8:30 U.S. Initial Jobless Claims 240k 241k

8:30 U.S. Continuing Claims 2040k 2030k

9:45 U.S. Bloomberg Consumer Comfort — 51

10:00 U.S. New Home Sales 564k 555k

10:00 U.S. New Home Sales MoM 1.60% 3.70%

10:00 Mexico Bi-Weekly CPI YoY 5.28% 5.02%

10:00 Mexico Bi-Weekly CPI 0.33% 0.25%

10:00 Mexico Bi-Weekly Core CPI 0.30% 0.23%

11:00 U.S. Kansas City Fed Manf. Activity 14 14

11:00 Euro Area Consumer Confidence -5.9 -6.2Source: Bloomberg. Surveys updated at 5:05 a.m. in New York.

Full story with live chart on the Bloomberg .terminal

Calendar

Click on the to see the full range of economists' forecasts on the terminal. highlighted releases

Overnight

British exporters are in a post-referendum and pre-Brexit “sweet spot,” according to Bank of England Deputy Governor — Ben Broadbentbut it may not last. While sterling has fallen sharply since the vote to leave the EU, benefiting U.K. exporters, the country’s trading rules “are for the time being unchanged,” Broadbent said today in a speech at Imperial College in London. “The result is that the costs and ease of exports are unchanged but the returns to it significantly higher.

The bought Swiss National Bankforeign currencies worth 67.1 billion francs ($67.6 billion) last year as it sought to contain the strength of its currency. The sum, published today in the central bank’s annual report, compares with a 2015 tally of 86.1 billion francs and a record of 188 billion spent in 2012.

The Philippine central bank left its benchmark at a record interest rate low, judging it didn’t need to respond immediately to inflation pressures even as the economy expands strongly. Bangko Sentral ng

kept the overnight reverse Pilipinasrepurchase rate at 3 percent, it said today, as predicted by 19 of 21 economists surveyed by Bloomberg. This is the first time in two years that economists weren’t unanimous in their forecasts, with two calling for an increase.

Taiwan held its benchmark interest steady for a third straight quarter rate

as inflation pressure remains moderate and the growth outlook improves. Policy makers held the discount rate for banks at a six-year low of 1.375 percent, the central

said today in a statement after banka meeting in Taipei. All but one of 29 economists in a Bloomberg survey predicted the decision.

Europe

Asia

Stock Pickers Can Thank Fed for Drop in Correlated Moves

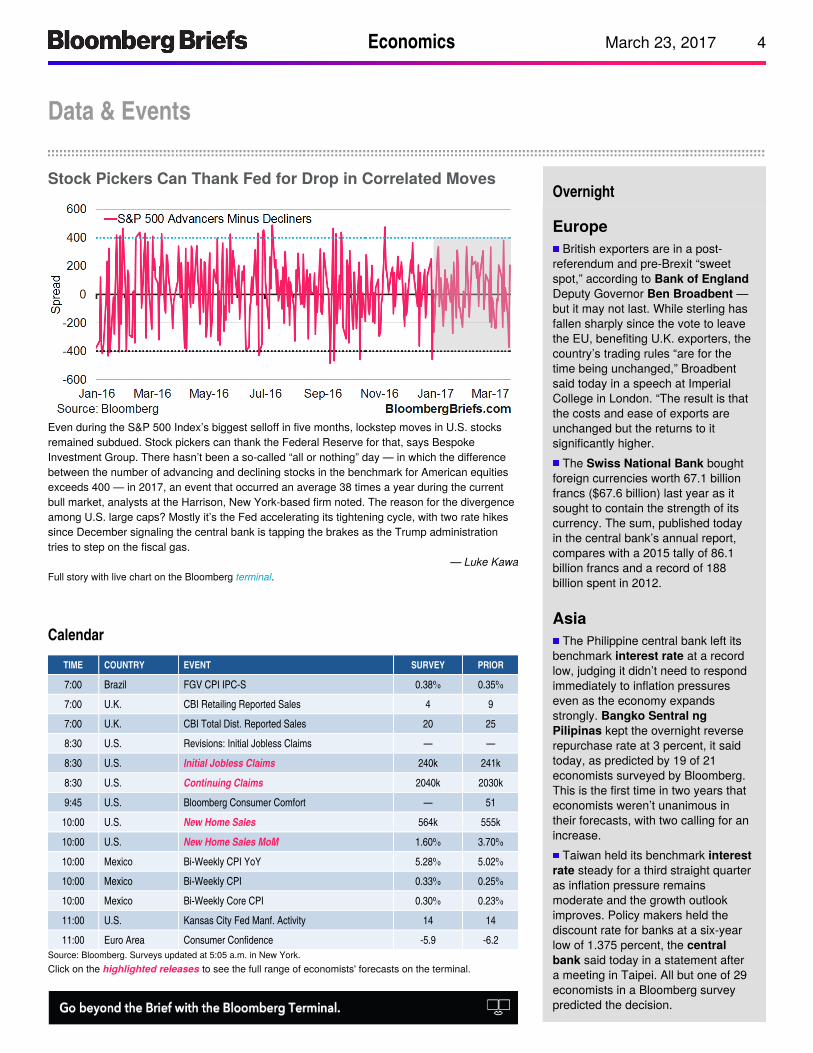

Even during the S&P 500 Index’s biggest selloff in five months, lockstep moves in U.S. stocks remained subdued. Stock pickers can thank the Federal Reserve for that, says Bespoke Investment Group. There hasn’t been a so-called “all or nothing” day — in which the difference between the number of advancing and declining stocks in the benchmark for American equities exceeds 400 — in 2017, an event that occurred an average 38 times a year during the current bull market, analysts at the Harrison, New York-based firm noted. The reason for the divergence among U.S. large caps? Mostly it’s the Fed accelerating its tightening cycle, with two rate hikes since December signaling the central bank is tapping the brakes as the Trump administration tries to step on the fiscal gas.

— Luke Kawa

Economics 5 March 23, 2017

Bloomberg Brief: Economics

Bloomberg Brief Managing Editor

Paul Smith

Economics Editors

Ben Baris

James Crombie

Global Director Economic

Research & Chief Economist

Michael McDonough

Chief U.S. Economist

Carl Riccadonna

U.S. Economists

Richard Yamarone

Yelena Shulyatyeva

Reprints & Permissions

Lori Husted

+1-717-505-9701 x2204

Marketing & Partnership Director

Courtney Martens

@bloomberg.netcmartens3

+1-212-617-2447

Advertising

Lucy Rosen

+1-212-617-6759

Economics Terminal Sales

Matthew Traum

+1-212-617-4671

Interested in learning more about

the Bloomberg terminal? Request a

free demo .here

© 2017 Bloomberg LP.

All rights reserved. This newsletter

and its contents may not be

forwarded or redistributed without

the prior consent of Bloomberg.

Please contact our reprints group

listed left for more information.