Embed Size (px)

Citation preview

Total Retail 2015: Retailers and the age of disruption

Based on PwC’s annual global survey of shopping behaviour across channels, this year’s report reveals major trends that are ‘disrupting’ the retail model as we know it.

Contents

0304

2106

23

Foreword

Methodology

Waves of disruption

Future of modern retail in India

About Retail and Consumer practice

Continuing with PwC’s global exercise from last year, our firms across the world have evaluated consumer shopping behaviours and the use of different channels in the retail industry. In an expanded, comprehensive survey, we cover more than 19,000 respondents in 19 countries across six continents. In India, our team obtained more than a 1,000 completed responses that have provided data to analyse and evaluate at great depth the changing retail landscape in the country.

The results from this year’s survey highlight the India retail industry in the throes of cost pressures and increased competition and and, at the same time, devising strategies which could potentially disrupt competitor business.

Last year, our report on Total Retail discussed key trends for the ‘total retailer’ to take note of while enhancing customer experience that would blur the lines between online and in-store channels. This year, we have looked at how disruptions–be it e-tailers with innovative campaigns or physical stores attempting to reinvent themselves to stay relevant- are changing the landscape.

This year, our survey recognises the ‘disruptors’ in the Indian retail industry:

• The price war• Exclusivity in products• Greater convenience for shoppers• Mobile and related technologies• Evolving nature of the physical store

The disruption strategy adopted by the online retail industry has resulted in successful sales. Although the numbers amounted to only about 0.5% of the overall retail trade, not only were online retailers able to clock in sales amounting to 5.3 billion USD, their innovative marketing and aggressive expansion strategies invited growing interest from investors in India and outside.

Despite the success of e-commerce and e-tail companies, traditional large-format retailers have been persevering under the pressure of trying to match their competitors’ every step of the way by promoting discounts and adopting technologies to enhance in-store experiences.

In this report, we discuss how the role of the physical store will continue to evolve into a sleeker, more customised and less transactional model. As online shopping continues to grow at the expense of store visits, the premium in the future will be on creating unique, brand-defining store experiences that keep customers coming back for more.

For the first time, we also asked respondents if they had heard of virtual currencies such as bitcoin and if they see themselves using them in the future. The result though not surprising, since 71% of them said yes, is extremely telling of the fact that we are still not over with the discussion around disruptors coming in the way of the retailers.

Rachna NathLeader, Retail and Consumer PwC India

Foreword

4 PwC

PwC’s Global Retail and Consumer practice, in conjunction with the International Survey Unit (ISU), administered a global survey to understand and compare consumer shopping behaviours and the use of different retail channels across 19 territories–Australia, Belgium, Brazil, Canada, Chile, China/Hong Kong, Denmark, France, Germany, India, Italy, Japan, the Middle East, Russia, South Africa, Switzerland, Turkey, the UK and the US.

A team of subject matter specialists representing each participating territory developed the survey based on last year’s survey. The final survey for 2014 includes updated questions and answer options in addition to new questions on payment methods. Where possible and appropriate, last year’s questions have been retained in order to conduct year-on-year comparisons. Research Now, an external provider, carried out the survey in August and September 2014, resulting in over 1,000 completed responses in every territory.

19,068 online interviews were conducted

across 19 territories during August/September 2014.

Methodology

Total Retail 2015: Retailers and the age of disruption 5

31%

25%

20%

13%

9%

2%

0%

5%

10%

15%

20%

25%

30%

35%

18 - 24 25 - 34 35 - 44 45 - 54 55 - 64 65+

Age

0%0%0%0%0%0%0%0%0%0%0%0%

1%1%1%1%1%

2%2%2%

3%4%4%

6%6%

9%9%

10%10%

12%13%

0% 5% 10% 15%

TripuraSikkim

NagalandMizoramManipur

Daman and DiuMeghalaya

Arunachal PradeshJammu and Kashmir

UttarakhandHimachal Pradesh

GoaAssam

ChhattisgarhChandigarhJharkhand

BiharOrissa

HaryanaPunjab

Madhya PradeshKerala

RajasthanGujarat

West BengalDelhi

KarnatakaAndhra Pradesh

Uttar PradeshTamil Nadu

Maharashtra

Region

4%

17%

3%

4%

3%

2%

4%

3%

4%

5%

4%

9%

12%

19%

8%

0% 10% 20%

Prefer not to disclose

Over 500,000 INR

460,000 to 499,999 INR

420,000 to 459,999 INR

380,000 to 419,999 INR

340,000 to 379,999 INR

300,000 to 339,999 INR

260,000 to 299,999 INR

220,000 to 259,999 INR

180,000 to 219,999 INR

140,000 to 179,999 INR

100,000 to 139,999 INR

60,000 to 99,999 INR

20,000 to 59,999 INR

Under 20,000 INR

Household income

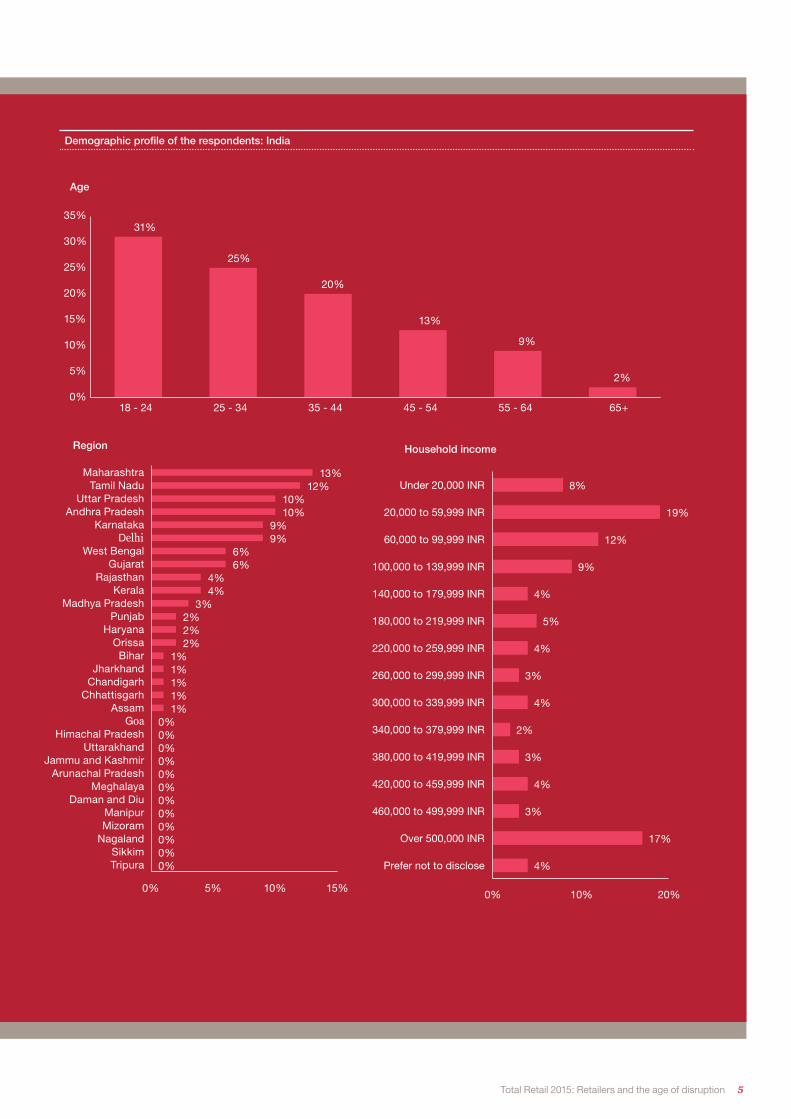

Demographic profile of the respondents: India

6 PwC

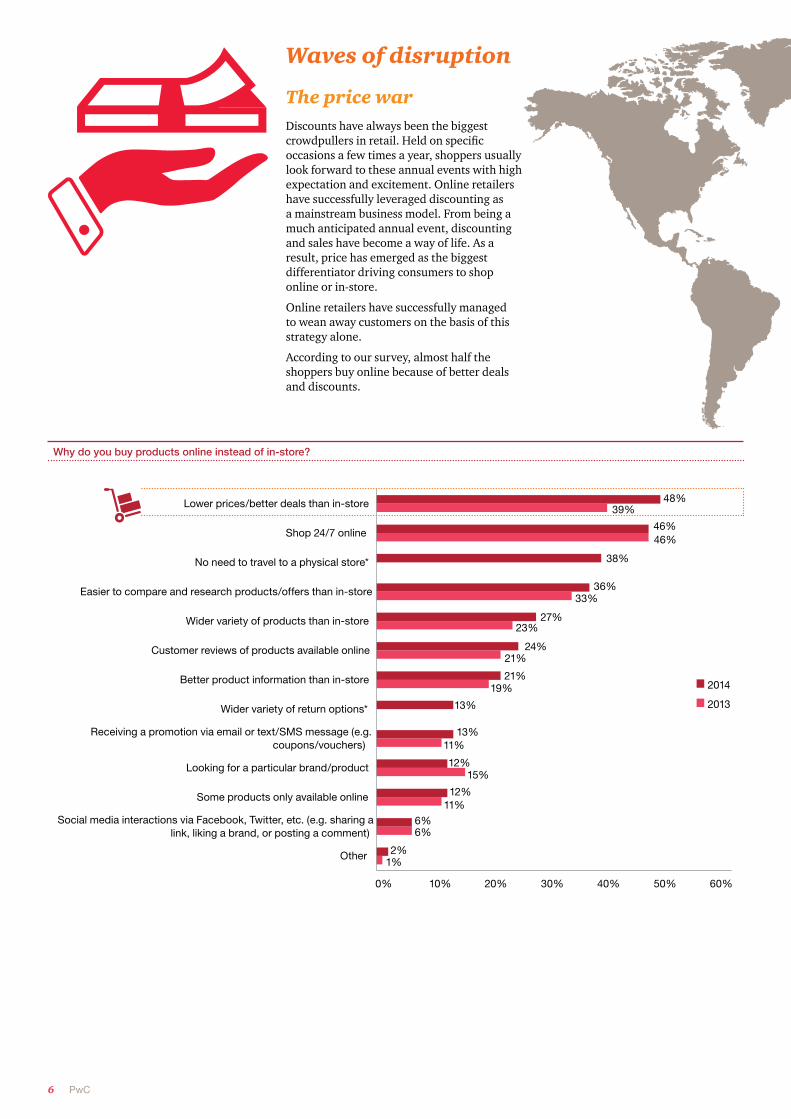

Waves of disruption

The price warDiscounts have always been the biggest crowdpullers in retail. Held on specific occasions a few times a year, shoppers usually look forward to these annual events with high expectation and excitement. Online retailers have successfully leveraged discounting as a mainstream business model. From being a much anticipated annual event, discounting and sales have become a way of life. As a result, price has emerged as the biggest differentiator driving consumers to shop online or in-store.

Online retailers have successfully managed to wean away customers on the basis of this strategy alone.

According to our survey, almost half the shoppers buy online because of better deals and discounts.

Why do you buy products online instead of in-store?

1%

6%

11%

15%

11%

19%

21%

23%

33%

46%

39%

2%

6%

12%

12%

13%

13%

21%

24%

27%

36%

38%

46%

48%

0% 10% 20% 30% 40% 50% 60%

Other

Social media interactions via Facebook, Twitter, etc. (e.g. sharing alink, liking a brand, or posting a comment)

Some products only available online

Looking for a particular brand/product

Receiving a promotion via email or text/SMS message (e.g.coupons/vouchers)

Wider variety of return options*

Better product information than in-store

Customer reviews of products available online

Wider variety of products than in-store

Easier to compare and research products/offers than in-store

No need to travel to a physical store*

Shop 24/7 online

Lower prices/better deals than in-store

2014

2013

Total Retail 2015: Retailers and the age of disruption 7

8 PwC

8%

11%

18%

15%

16%

18%

21%

18%

19%

28%

26%

38%

41%

8%

12%

15%

15%

15%

15%

16%

17%

17%

18%

20%

26%

28%

31%

37%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Flyer or recommendation in-store

Because I shop with them

Had a good or bad experience and wanted to provide feedbackthrough social media

To learn about and provide feedback on brand'ssocial/environmental commitment*

Brand contacted me through social media

The opportunity to influence product design*

The brand provides customer service through social media

Interested in interacting with the brand and its online followers

Opportunity to participate in competitions through social media

Received a promotion via email or text/SMS message

Advertising (e.g. TV, outdoor, newspaper/magazine, website)

To research products before buying

Friend's or expert's recommendation

Interested in new product offerings

Attractive deals/promotions/sales

2014

2013

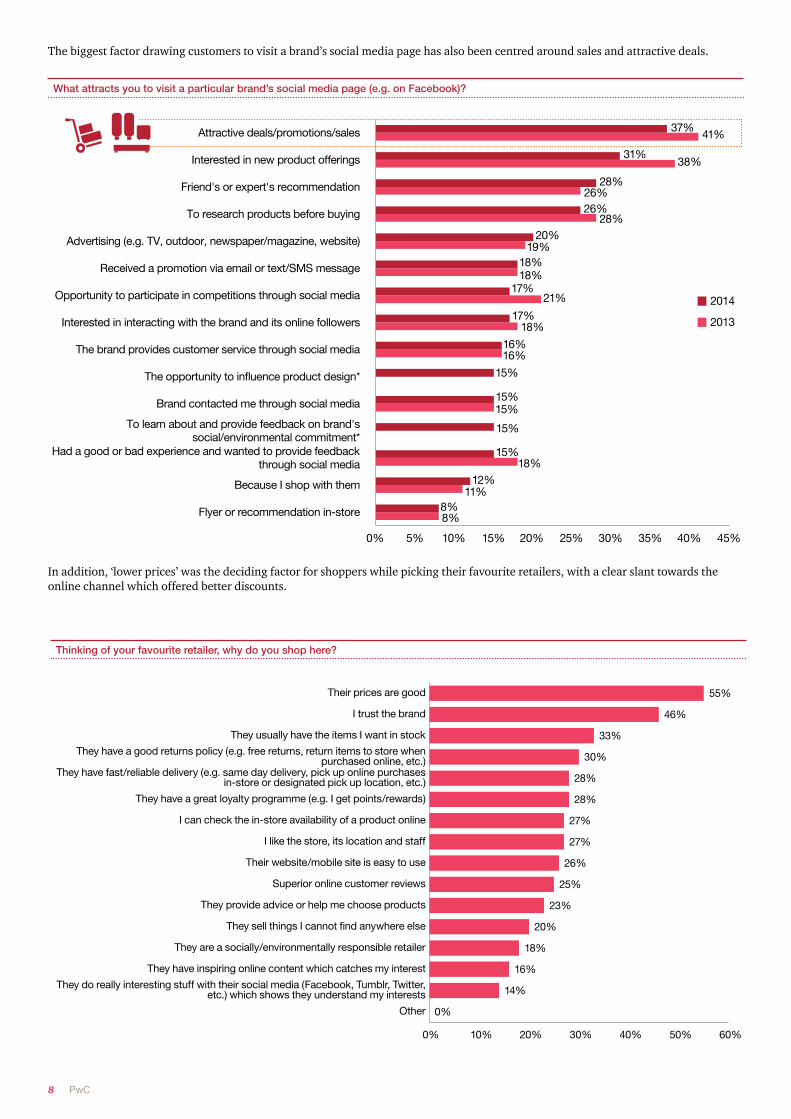

The biggest factor drawing customers to visit a brand’s social media page has also been centred around sales and attractive deals.

In addition, ‘lower prices’ was the deciding factor for shoppers while picking their favourite retailers, with a clear slant towards the online channel which offered better discounts.

What attracts you to visit a particular brand’s social media page (e.g. on Facebook)?

Thinking of your favourite retailer, why do you shop here?

0%

14%

16%

18%

20%

23%

25%

26%

27%

27%

28%

28%

30%

33%

46%

55%

0% 10% 20% 30% 40% 50% 60%

Other

They do really interesting stuff with their social media (Facebook, Tumblr, Twitter,etc.) which shows they understand my interests

They have inspiring online content which catches my interest

They are a socially/environmentally responsible retailer

They sell things I cannot find anywhere else

They provide advice or help me choose products

Superior online customer reviews

Their website/mobile site is easy to use

I like the store, its location and staff

I can check the in-store availability of a product online

They have a great loyalty programme (e.g. I get points/rewards)

They have fast/reliable delivery (e.g. same day delivery, pick up online purchasesin-store or designated pick up location, etc.)

They have a good returns policy (e.g. free returns, return items to store whenpurchased online, etc.)

They usually have the items I want in stock

I trust the brand

Their prices are good

Total Retail 2015: Retailers and the age of disruption 9

A majority of e-commerce players are start-ups and therefore, are working towards rapidly scaling up their market share. They have been aggressively planning and implementing discounting strategies which would make the customer sit up and take notice. Besides, with strong backing from investors, online retailers have been doling out discounts and special offers to happy customers like never before, even at the cost of hitting their business bottomline.

According to a survey by Associated Chambers of Commerce and Industry (ASSOCHAM), online shopping growth is projected to increase to 350% during peak festival seasons resulting in plummeting footfalls in brick-and-mortar retail shops. During Diwali 2014, online shopping has been estimated to cross 10,000 crore INR and going forward, the trend will not only continue but grow dramatically to cross 100,000 crore INR over the next four years.

Home-grown Black Friday?

The Great Online Shopping Festival which was hosted for the third time in 2014 has given us our very own version of the American Black Friday sale which is known for the best deals on products and is also the biggest sale in the US. With participation from nearly all e-commerce players as well as major FMCG and consumer durables brands, the festival has been a huge success.

Special sales during special occasions such as Diwali, Republic Day, Holi, etc. and occasions created specifically to drive traffic like the ‘Big Billion Day’ generated a sale of 100 million USD in 10 hours as claimed by the e-tailer. These sales have disrupted the ‘sales calendar’ for the in-store retailer and the industry is seeing sales becoming a norm throughout the year rather than being special events. In fact, so fierce is the competition, that e-tailers are also clearly seen trying to outdo each other by offering steeper discounts as often as possible.

The following is a lowdown on sales that generated the most attention in the past year.

Big Billion Day and the Savings Day Sale

During these sales, which were launched by two major e-tailers in the country, deep discounts were offered on most product categories from consumer electronics such as laptops, mobile phones, cameras to apparel, footwear, homeware, kitchenware et al.

With aggressive marketing leading up to these daylong sales events, e-tailers spent a whopping 100 crore INR on advertising to ensure that they were a resounding success. Much excitement was generated with over a million downloads of the mobile app in one day. Claims by certain retailers indicated single-day sales of over 600 crore INR, notwithstanding widespread complaints

about technological hiccups and frustrated consumer experiences.

Sales for sales’ sake

Online retailers also experimented with the appetite of the burgeoning e-customers in India. Apart from planning sales coinciding with the usual holidays, some have announced sales on non-traditional days and have found success. Examples of this trend are the End of Reason Sale and the Republic Day sales,which took place recently.

January is not traditionally spending time for the customer. But the creation of mega sales like the two mentioned above have forced customers to consider spending during this off season.

The fundamental principle of the End of Reason Sale was to compress the traditional six- to- seven-week format traditional format of an end-of-season sale that spans six to seven weeks into just two days.

The catchy title and the attention-grabbing advertisements on television are good examples of online retailers’ aggressive discount strategy to enhance the nascent customer base. The underlying business strategy was to create customer habits and dependencies resulting in increased customer lifetime value.

Having received an overwhelming response, and just like in the case of its predecessors, the e-tailer soon ran out of stocks and in some cases, even

5%

36%

25%

74%

31%

25%

66%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Next-generation wearables

Online via mobile phone or smartphone

Online via tablet

Online via PC

TV shopping

Catalogue/magazine

In-store

Thinking of your favourite retailer, please specify if you have purchased something through the following shopping channels.

10 PwC

had to procure additional stock from fellow online retailers. This proved that customers are conscious and receptive to these ad hoc discounting strategies.

The Republic Day sale is another example of the online industry taking advantage of a long weekend. An interesting point of difference is that this sale had several offline retailers hosting sales as well.

Repercussions on offline retailers

Customer buying habits have undergone a drastic change due to the round-the-year discounts across product categories.

Offline retail sales have taken a severe hit because many smart buyers prefer shopping online where prices are lower and deliveries dependable. Consumers today have become wiser and ensure that they have researched all their options before shopping.

Naturally, offline retailers have been up in arms over beating online prices. The interpretation of government regulations for e-commerce companies has been a major source of discontent among offline retailers.

While e-commerce companies don’t have to deal with overhead costs such as rent for real estate, they have also been getting away with selling products way below the maximum retail price, without factoring in even profit margins, thus raising questions about predatory pricing practices. Further, although online retailers say they simply deliver goods from the seller to the customer and therefore do not pay VAT, this business model has been repeatedly questioned by offline competitors.

Besides, the discounting model has been taking a toll on the brands associated with these sales too. It may not always be viable for a brand to participate in a sale. Apart from taking a hit on their margins, premium brands with a presence in online retail are concerned about the deep discounts hurting their brand value as well.

Total Retail 2015: Retailers and the age of disruption 11

3%

51%

53%

59%

72%

86%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Other

To seek advice from store staff

The item was not in stock in store

It is more convenient to have the item delivered to

me rather than carry from the store

I wanted to see/touch/try the merchandise before ordering online

Better prices online

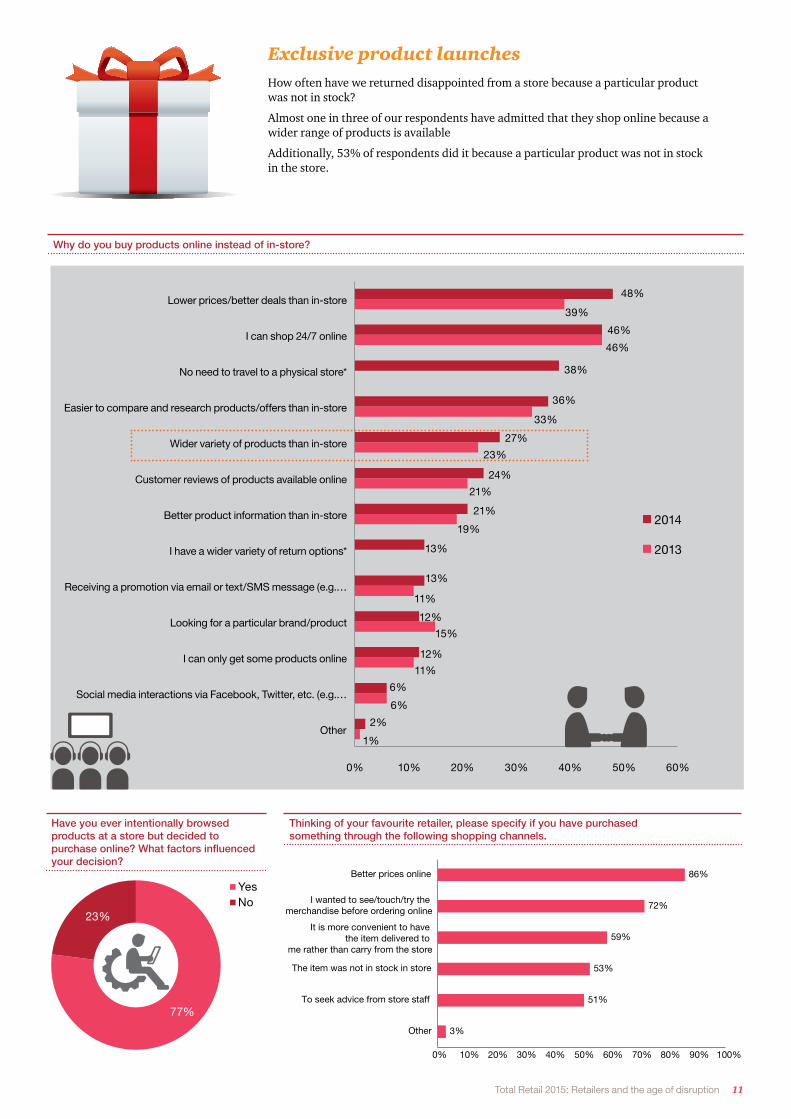

Exclusive product launchesHow often have we returned disappointed from a store because a particular product was not in stock?

Almost one in three of our respondents have admitted that they shop online because a wider range of products is available

Additionally, 53% of respondents did it because a particular product was not in stock in the store.

Have you ever intentionally browsed products at a store but decided to purchase online? What factors influenced your decision?

77%

23%

YesNo

1%

6%

11%

15%

11%

19%

21%

23%

33%

46%

39%

2%

6%

12%

12%

13%

13%

21%

24%

27%

36%

38%

46%

48%

0% 10% 20% 30% 40% 50% 60%

Other

Social media interactions via Facebook, Twitter, etc. (e.g.…

I can only get some products online

Looking for a particular brand/product

Receiving a promotion via email or text/SMS message (e.g.…

I have a wider variety of return options*

Better product information than in-store

Customer reviews of products available online

Wider variety of products than in-store

Easier to compare and research products/offers than in-store

No need to travel to a physical store*

I can shop 24/7 online

Lower prices/better deals than in-store

2014

2013

Why do you buy products online instead of in-store?

Thinking of your favourite retailer, please specify if you have purchased something through the following shopping channels.

12 PwC

With an increasing number of customers preferring online shopping to in-store, several brands are entering into exclusive distribution tie-ups with online retailers. This trend has been observed across all product categories. Through exclusive tie-ups, Indian as well as international brands are taking advantage of the extensive reach of online retailers.

In 2014, certain food and beverage products also saw exclusive online pilot launches. With the consistent popularity of books on the online channel, pre-orders of certain books were only available online.

The continuing popularity of consumer electronics through the online retail channel has motivated several smartphone brands to give exclusive distribution rights to the large online retailers. Brands have claimed sales of as much as 20,000 units within a few hours.

International fashion brands are also using this platform as the initial step in their foray into the Indian market. Exporting their merchandise to online retailers has helped them avoid dealing with India’s complex regulations that tend to delay market entry. Besides, these brands end up saving on the costs of investing in real estate, among several other overheads.

From a offline retailer’s perspective, this has been a disturbing trend. Launching long anticipated products following their success in foreign markets has always been a crowdpuller, regardless of how premium the brand. While the brand can use the online launch to test demand, a second launch in physical stores might or might not garner as much attention, especially in the case of already popular products.

Industry reaction

There has been uproar among traditional big format retailers as far as exclusive online product launches are concerned. For the original equipment manufacturer (OEM), most sales still come from traditional channels but since e-commerce has been a profitable channel to get to customers, they grapple with establishing balance between the two. On their part, big format offline retailers have even gone so far as to refuse to stock products which were first launched online. Demarcations have been established, disallowing the sale of certain ‘experience’ products online since it may lead to brand dilution and customer mindscape disconnect. Consumer electronics companies, part of the bestselling category in online retail, have especially faced this problem.

This is another addition to the episode of the battle between the incumbent and the challengers.

Total Retail 2015: Retailers and the age of disruption 13

Greater convenience for shoppers

Assuming you have free basic delivery, which of the following other delivery options would you be willing to pay for?

2%

27%

39%

47%

49%

49%

69%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Other

Locker/box collection (e.g. Amazon lockers)

Can pick up purchase from a convenient location (e.g. local

convenience store/FedEx)

90-minute delivery for store-based purchase

Specific agreed-upon time frame for delivery (e.g. Monday 8:00-8:30am)

One/two day delivery

Same day delivery

Although 43% of our respondents said that they preferred shopping in-store in order to get immediate delivery, a whopping 69% said they are willing to pay for same-day delivery and 49% are willing to pay for delivery between a specific agreed-upon timeframe.

Given the supply chain issues in our country, the most challenging prospect that online retailers face today has been fulfilling its most fundamental proposition–transcending physical boundaries to deliver a variety of products to the customer’s doorstep. Negligible or zero delivery charges, doorstep delivery, traceability solutions and convenient reverse logistics have become the most important elements of differentiation for e-tailers. While the concept of same-day deliveries has been around for some time now, Indian online shoppers today expect the product to be delivered within hours of placing an order.

‘Convenience for shoppers’ is being given a whole new meaning by e-tailers while trying to win the loyalty of their customers. E-tailers are trying to ensure that shoppers are not only able to shop anytime and anywhere but also receive their deliveries at a time and place most convenient to them.

The country’s major e-commerce players are attempting to improve on how they can deliver products, in some cases, even in as little as three hours. With several e-tailers also operating in the food and beverages category, a more efficient supply chain will be a gamechanger.

With growing investment in delivery and logistics teams, e-commerce companies are working towards providing quick and reliable delivery services to its vast customer base. Benefitting from this potential, third-party logistics (3PL) companies in India are also gearing up to meet the increasing demands of the e-tailing industry. This will help realise the huge potential offered by faster deliveries.

E-tailers’ plans for future expansion, and a key role in it for third-party delivery firms, have also contributed to higher valuations of the existing 3PL companies. Logistics companies have gained up to 80% this past year, making logistics among the top-5 industries in India.

14 PwC

Mobile and related technologies Smartphone penetration in the country is growing at over 150% year on year. With internet connectivity through smartphones on the rise, more and more mobile users are expected to shop online.

As compared to last year, there has been a 7% increase in the number of mobile users who shop via their mobile phones or smartphones on a weekly basis.

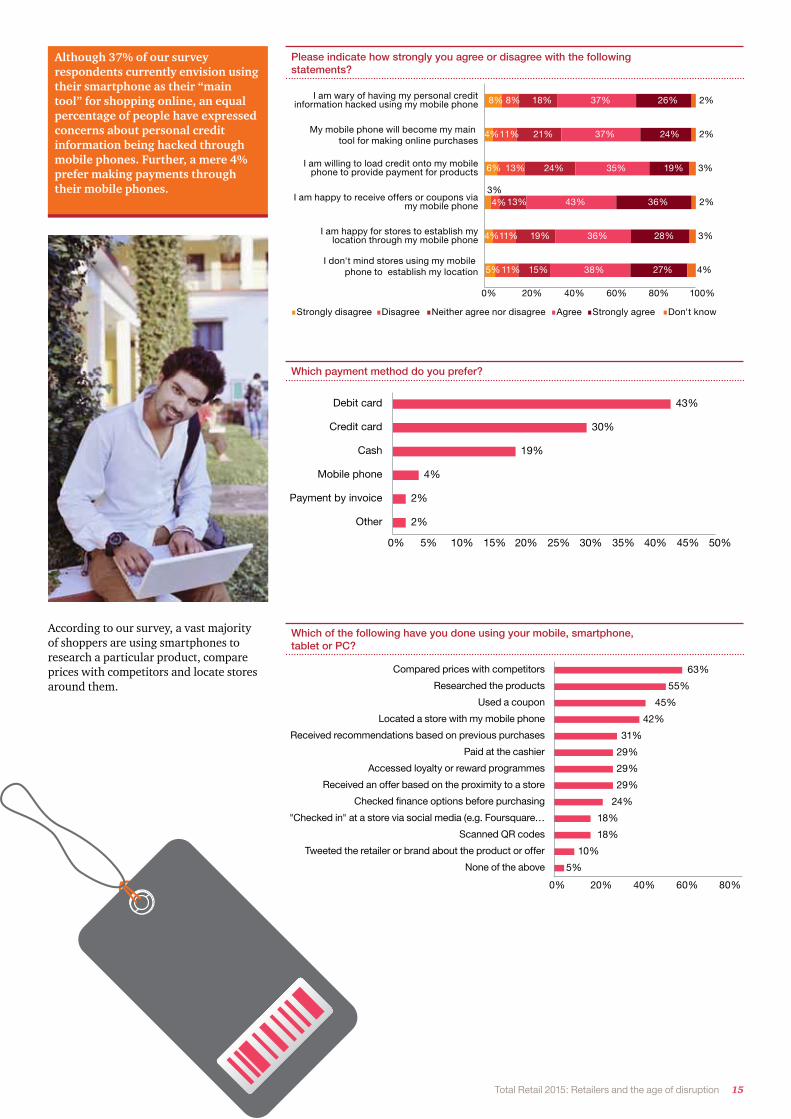

Although 37% of our survey respondents currently envision using their smartphone as their ‘main tool’ for shopping online, an equal percentage of people have expressed concerns about personal credit information being hacked through mobile phones. Further, a mere 4% prefer making payments through their mobile phones.

How often do you buy products using the following shopping channels?

17%

7%6%

8%6%

8%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Daily

32%

22%

12%

25%

16%19%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Weekly

31%

21%

16%

31%

18%18%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Monthly

17%19%20%

27%

18%22%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

A few times a year

2%

10%

15%

5%8%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once a year

1%

20%

31%

3%

35%

25%

41%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Never

In-store Catalogue/magazine

TV shopping Online via PC

Online via tablet Online via mobile phone or smartphone

Next generation wearables (watch, glasses, pens)

17%

7%6%

8%6%

8%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Daily

32%

22%

12%

25%

16%19%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Weekly

31%

21%

16%

31%

18%18%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Monthly

17%19%20%

27%

18%22%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

A few times a year

2%

10%

15%

5%8%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once a year

1%

20%

31%

3%

35%

25%

41%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Never

In-store Catalogue/magazine

TV shopping Online via PC

Online via tablet Online via mobile phone or smartphone

Next generation wearables (watch, glasses, pens)

17%

7%6%

8%6%

8%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Daily

32%

22%

12%

25%

16%19%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Weekly

31%

21%

16%

31%

18%18%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Monthly

17%19%20%

27%

18%22%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

A few times a year

2%

10%

15%

5%8%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once a year

1%

20%

31%

3%

35%

25%

41%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Never

In-store Catalogue/magazine

TV shopping Online via PC

Online via tablet Online via mobile phone or smartphone

Next generation wearables (watch, glasses, pens)

17%

7%6%

8%6%

8%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Daily

32%

22%

12%

25%

16%19%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Weekly

31%

21%

16%

31%

18%18%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Monthly

17%19%20%

27%

18%22%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

A few times a year

2%

10%

15%

5%8%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once a year

1%

20%

31%

3%

35%

25%

41%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Never

In-store Catalogue/magazine

TV shopping Online via PC

Online via tablet Online via mobile phone or smartphone

Next generation wearables (watch, glasses, pens)

17%

7%6%

8%6%

8%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Daily

32%

22%

12%

25%

16%19%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Weekly

31%

21%

16%

31%

18%18%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Monthly

17%19%20%

27%

18%22%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

A few times a year

2%

10%

15%

5%8%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once a year

1%

20%

31%

3%

35%

25%

41%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Never

In-store Catalogue/magazine

TV shopping Online via PC

Online via tablet Online via mobile phone or smartphone

Next generation wearables (watch, glasses, pens)

17%

7%6%

8%6%

8%5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Daily

32%

22%

12%

25%

16%19%

11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Weekly

31%

21%

16%

31%

18%18%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Monthly

17%19%20%

27%

18%22%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

A few times a year

2%

10%

15%

5%8%

9%11%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Once a year

1%

20%

31%

3%

35%

25%

41%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Never

In-store Catalogue/magazine

TV shopping Online via PC

Online via tablet Online via mobile phone or smartphone

Next generation wearables (watch, glasses, pens)

In-store

TV shopping

Online via tablet

Next generation wearables (watch, glasses , pens)

Catalogu e/magazine

Online via PC

Online via mobile phone or smartphone

Total Retail 2015: Retailers and the age of disruption 15

According to our survey, a vast majority of shoppers are using smartphones to research a particular product, compare prices with competitors and locate stores around them.

5%

4%

3%

6%

4%

8%

11%

11%

4%

13%

11%

8%

15%

19%

13%

24%

21%

18%

38%

36%

43%

35%

37%

37%

27%

28%

36%

19%

24%

26%

4%

3%

2%

3%

2%

2%

0% 20% 40% 60% 80% 100%

I don't mind stores using my mobile phone to establish my location

I am happy for stores to establish mylocation through my mobile phone

I am happy to receive offers or coupons viamy mobile phone

I am willing to load credit onto my mobilephone to provide payment for products

My mobile phone will become my main tool for making online purchases

I am wary of having my personal creditinformation hacked using my mobile phone

Strongly disagree Disagree Neither agree nor disagree Agree Strongly agree Don't know

2%

2%

4%

19%

30%

43%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Other

Payment by invoice

Mobile phone

Cash

Credit card

Debit card

Please indicate how strongly you agree or disagree with the following statements?

Which payment method do you prefer?

Which of the following have you done using your mobile, smartphone, tablet or PC?

5%

10%

18%

18%

24%

29%

29%

29%

31%

42%

45%

55%

63%

0% 20% 40% 60% 80%

None of the above

Tweeted the retailer or brand about the product or offer

Scanned QR codes

"Checked in" at a store via social media (e.g. Foursquare…

Checked finance options before purchasing

Received an offer based on the proximity to a store

Accessed loyalty or reward programmes

Paid at the cashier

Received recommendations based on previous purchases

Located a store with my mobile phone

Used a coupon

Researched the products

Compared prices with competitors

Although 37% of our survey respondents currently envision using their smartphone as their “main tool” for shopping online, an equal percentage of people have expressed concerns about personal credit information being hacked through mobile phones. Further, a mere 4% prefer making payments through their mobile phones.

16 PwC

About 42% of our respondents said that they do not mind sharing their location via their smartphones.

Mobile phones are fast emerging as the main drivers of interaction between retailers and customers, which is in turn leading to growth in sales. Depending on the agility of the retailers, both offline and online, to adapt to this third major retail channel, it could be the next biggest disruptor in modern retail in India.

Mobile search advertising

As illustrated in the graph above, 55% of our survey respondents admitted to using their smartphones for researching products on the go before making a purchase. Retailers and e-tailers could benefit from search engine optimisation, which would influence shopping behaviour among potential customers.

According to an article published in the Forbes magazine, mobile advertising volume in India grew by a record 260% since July 2013, the fastest in the world. Further, mobile apps which pick up data from customers’ online activity are able to provide customised results that show detailed information regarding the store or establishment that the customers are researching.

Real-time transparency into available inventory

When asked about technologies that would enhance their in-store shopping experience, 38% of the respondents voted for having the ability to check other stores or online stock instantly.

The ability to have real-time insight into the available inventory would not only drive sales across multiple channels of a particular retailer, but also allow it to push various discounts and sales on a personalised basis, which is the second most important factor for our survey respondents.

For instance, a shopper should be able to check if a particular product is available in the store nearest to him or her, using the mobile application of the retailer in question. Based on this search, retailers would be able to push personalised deals to the shoppers, thus enhancing customer engagement.

Although Big Data analytics offers many ways for the front office to customise marketing and sales, the back office of most retailers still faces a serious challenge in managing an increasingly complex supply chain.

But pinpointing inventory throughout the store network, right down to the pallet, store and shelf will be harder for large retail chains. Overcoming this hurdle in the back office would actively help retain customers by driving personalised offers based on the customers’ search history.

Location-based marketing services

Please indicate how strongly you agree or disagree with the following statements?

5%

4%

3%

6%

4%

8%

11%

11%

4%

13%

11%

8%

15%

19%

13%

24%

21%

18%

38%

36%

43%

35%

37%

37%

27%

28%

36%

19%

24%

26%

4%

3%

2%

3%

2%

2%

0% 20% 40% 60% 80% 100%

I am happy to store my payment anddelivery information in an app on my

mobile phone

I am happy for stores to establish mylocation through my mobile phone

I am happy to receive offers or coupons viamy mobile phone

I am willing to load credit onto my mobilephone to provide payment for products

My mobile phone will become my main toolfor which to purchase items

I am wary of having my personal creditinformation hacked using my mobile phone

Strongly disagree Disagree Neither agree nor disagree Agree Strongly agree Don't know

Which of the following in-store technologies would make your shopping experience better?

55% indicated real-time personalised offers

Several mobile applications are allowing users to “check in” to their place of business and reward them with points each time they check in. About 18% of our survey respondents were accustomed to using their smartphones to check into applications like Foursquare, Swarm, Facebook, Zomato and Google Places.

The stores then reward such customers by offering freebies, discount coupons or virtual titles and badges such as ‘shopper of the day’ and ‘virtual ambassador’. Such gamification would not only attract more customers, but also drive passive marketing through brand endorsements by these customers.

Total Retail 2015: Retailers and the age of disruption 17

Micro-location based marketing services

Retailers will be able to make use of mobile iBeacons from Apple phones or similar bluetooth-enabled low-energy devices to push specific advertising and marketing campaigns when the customer is in a specific aisle in the store.

Capitalising on the selfie craze

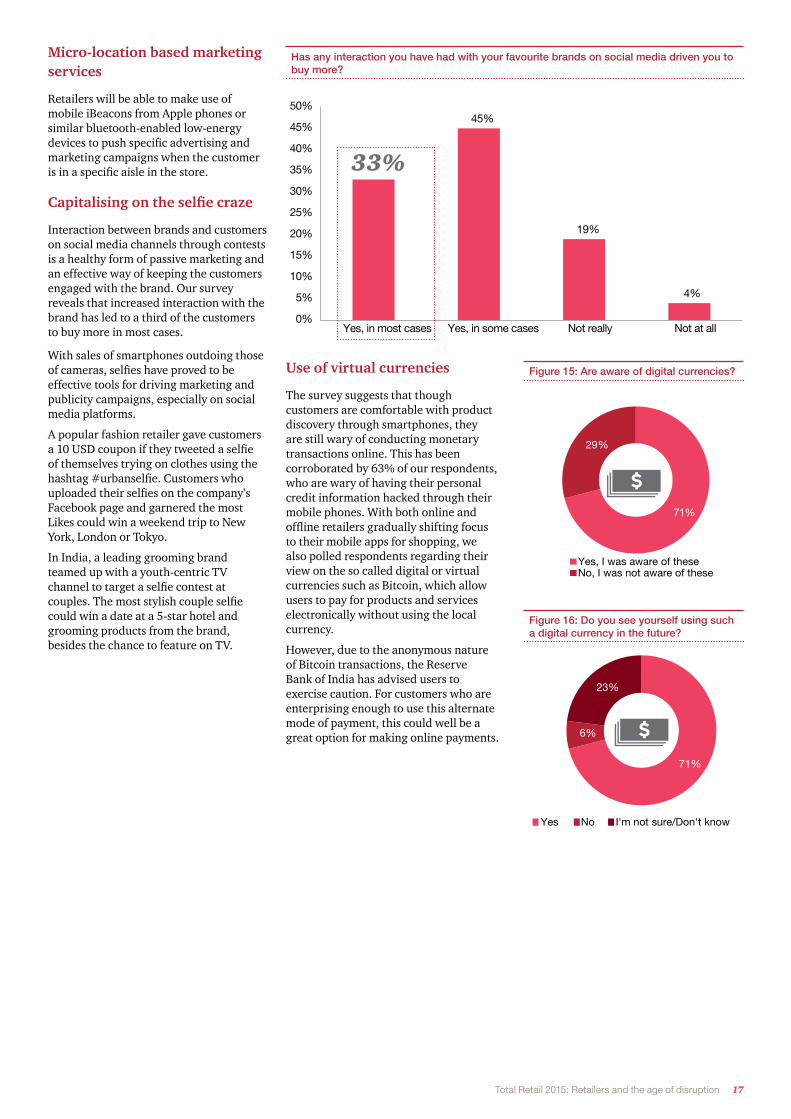

Interaction between brands and customers on social media channels through contests is a healthy form of passive marketing and an effective way of keeping the customers engaged with the brand. Our survey reveals that increased interaction with the brand has led to a third of the customers to buy more in most cases.

With sales of smartphones outdoing those of cameras, selfies have proved to be effective tools for driving marketing and publicity campaigns, especially on social media platforms.

A popular fashion retailer gave customers a 10 USD coupon if they tweeted a selfie of themselves trying on clothes using the hashtag #urbanselfie. Customers who uploaded their selfies on the company’s Facebook page and garnered the most Likes could win a weekend trip to New York, London or Tokyo.

In India, a leading grooming brand teamed up with a youth-centric TV channel to target a selfie contest at couples. The most stylish couple selfie could win a date at a 5-star hotel and grooming products from the brand, besides the chance to feature on TV.

Use of virtual currencies

The survey suggests that though customers are comfortable with product discovery through smartphones, they are still wary of conducting monetary transactions online. This has been corroborated by 63% of our respondents, who are wary of having their personal credit information hacked through their mobile phones. With both online and offline retailers gradually shifting focus to their mobile apps for shopping, we also polled respondents regarding their view on the so called digital or virtual currencies such as Bitcoin, which allow users to pay for products and services electronically without using the local currency.

However, due to the anonymous nature of Bitcoin transactions, the Reserve Bank of India has advised users to exercise caution. For customers who are enterprising enough to use this alternate mode of payment, this could well be a great option for making online payments.

33%

45%

19%

4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Yes, in most cases Yes, in some cases Not really Not at all

Has any interaction you have had with your favourite brands on social media driven you to buy more?

Figure 15: Are aware of digital currencies?

Figure 16: Do you see yourself using such a digital currency in the future?

71%

29%

Yes, I was aware of theseNo, I was not aware of these

71%

6%

23%

Yes No I'm not sure/Don't know

33%

18 PwC

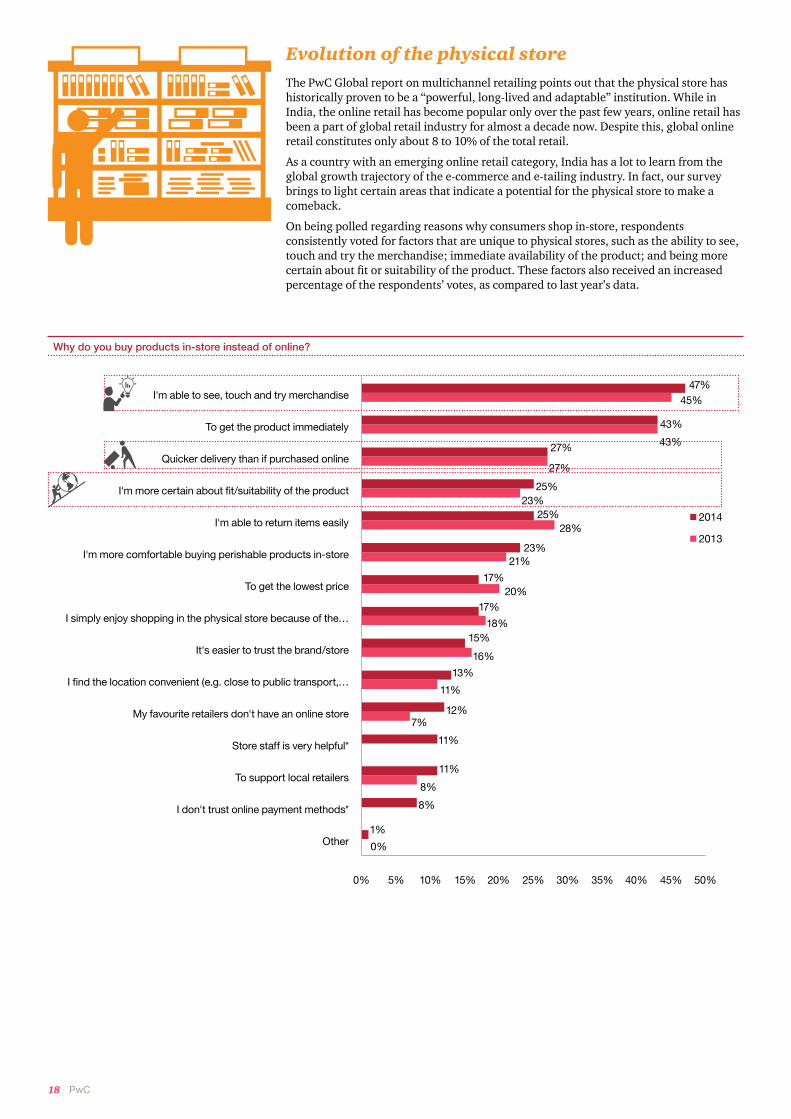

Evolution of the physical store The PwC Global report on multichannel retailing points out that the physical store has historically proven to be a “powerful, long-lived and adaptable” institution. While in India, the online retail has become popular only over the past few years, online retail has been a part of global retail industry for almost a decade now. Despite this, global online retail constitutes only about 8 to 10% of the total retail.

As a country with an emerging online retail category, India has a lot to learn from the global growth trajectory of the e-commerce and e-tailing industry. In fact, our survey brings to light certain areas that indicate a potential for the physical store to make a comeback.

On being polled regarding reasons why consumers shop in-store, respondents consistently voted for factors that are unique to physical stores, such as the ability to see, touch and try the merchandise; immediate availability of the product; and being more certain about fit or suitability of the product. These factors also received an increased percentage of the respondents’ votes, as compared to last year’s data.

0%

8%

7%

11%

16%

18%

20%

21%

28%

23%

27%

43%

45%

1%

8%

11%

11%

12%

13%

15%

17%

17%

23%

25%

25%

27% 43%

47%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Other

I don't trust online payment methods*

To support local retailers

Store staff is very helpful*

My favourite retailers don't have an online store

I find the location convenient (e.g. close to public transport,…

It's easier to trust the brand/store

I simply enjoy shopping in the physical store because of the…

To get the lowest price

I'm more comfortable buying perishable products in-store

I'm able to return items easily

I'm more certain about fit/suitability of the product

Quicker delivery than if purchased online

To get the product immediately

I'm able to see, touch and try merchandise

2014

2013

Why do you buy products in-store instead of online?

Total Retail 2015: Retailers and the age of disruption 19

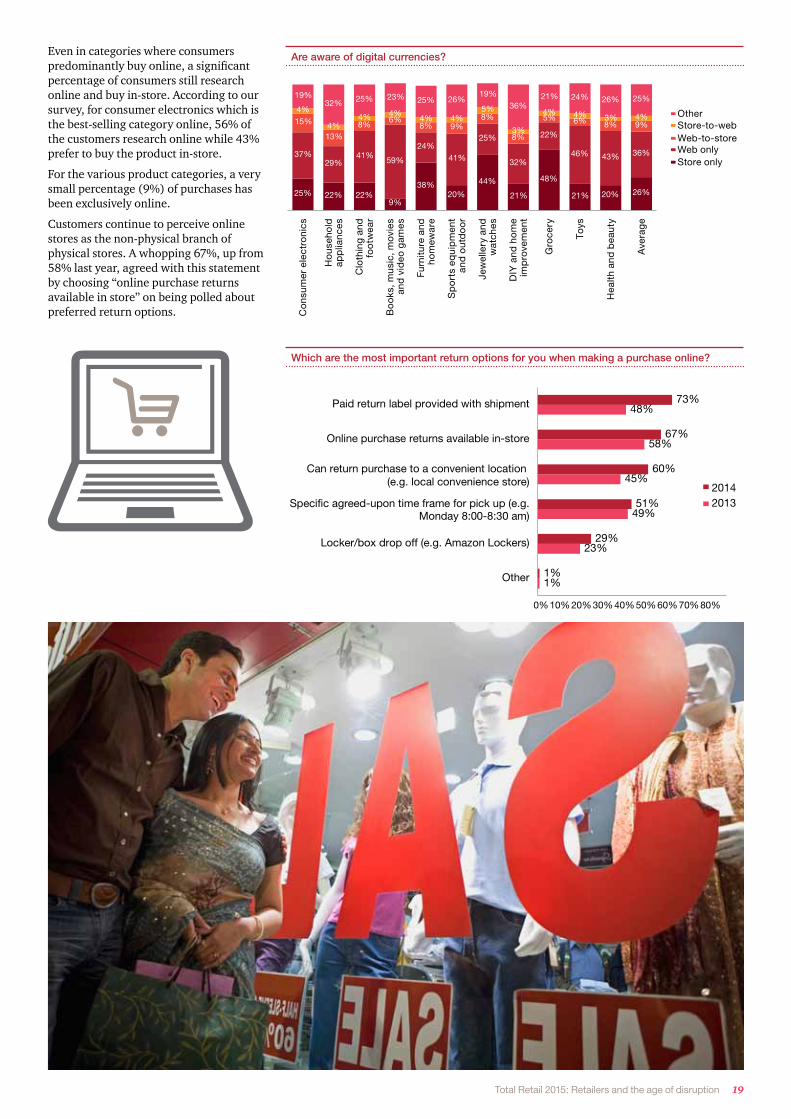

Even in categories where consumers predominantly buy online, a significant percentage of consumers still research online and buy in-store. According to our survey, for consumer electronics which is the best-selling category online, 56% of the customers research online while 43% prefer to buy the product in-store.

For the various product categories, a very small percentage (9%) of purchases has been exclusively online.

Customers continue to perceive online stores as the non-physical branch of physical stores. A whopping 67%, up from 58% last year, agreed with this statement by choosing “online purchase returns available in store” on being polled about preferred return options.

Are aware of digital currencies?

Which are the most important return options for you when making a purchase online?

25% 22% 22%9%

38%20%

44%

21%

48%

21% 20% 26%

37%29%

41%59%

24%41%

25%

32%

22%

46% 43% 36%

15%

13%8%

6%8% 9%

8%

8%

5% 6% 8% 9%

4%

4%4% 4%

4% 4%5%

3%

4% 4% 3% 4%

19%32% 25% 23% 25% 26%

19%36%

21% 24% 26% 25%

Co

nsum

er e

lect

roni

cs

Ho

useh

old

app

lianc

es

Clo

thin

g an

dfo

otw

ear

Bo

oks

, mus

ic, m

ovie

san

d v

ideo

gam

es

Furn

iture

and

hom

ewar

e

Sp

ort

s eq

uip

men

tan

d o

utd

oo

r

Jew

elle

ry a

ndw

atch

es

DIY

and

ho

me

imp

rove

men

t

Gro

cery

Toys

Hea

lth a

nd b

eaut

y

Ave

rag

e

OtherStore-to-webWeb-to-storeWeb onlyStore only

1%

23%

49%

45%

58%

48%

1%

29%

51%

60%

67%

73%

0%10%20%30%40%50%60%70%80%

Other

Locker/box drop off (e.g. Amazon Lockers)

Specific agreed-upon time frame for pick up (e.g.Monday 8:00-8:30 am)

Can return purchase to a convenient location (e.g. local convenience store)

Online purchase returns available in-store

Paid return label provided with shipment

20142013

20 PwC

Why do you buy products online instead of in-store?

Please indicate how strongly you agree or disagree with the following statements

1%

6%

11%

15%

11%

19%

21%

23%

33%

46%

39%

2%

6%

12%

12%

13%

13%

21%

24%

27%

36%

38%

46%

48%

0% 10% 20% 30% 40% 50% 60%

Other

Social media interactions via Facebook, Twitter, etc. (e.g.…

Some products are only available online

Looking for a particular brand/product

Receiving a promotion via email or text/SMS message (e.g.…

Wider variety of return options*

Better product information than in-store

Customer reviews of products available online

Wider variety of products than in-store

Easier to compare and research products/offers than in-store

No need to travel to a physical store*

I can shop 24x7 online

Lower prices or better deals than in-store

2014

2013

5%

4%

3%

6%

4%

8%

11%

11%

4%

13%

11%

8%

15%

19%

13%

24%

21%

18%

38%

36%

43%

35%

37%

37%

27%

28%

36%

19%

24%

26%

4%

3%

2%

3%

2%

2%

0% 20% 40% 60% 80% 100%

I am happy to store my payment anddelivery information in an app on my

mobile phone

I am happy for stores to establish mylocation through my mobile phone

I am happy to receive offers or coupons viamy mobile phone

I am willing to load credit onto my mobilephone to provide payment for products

My mobile phone will become my main toolfor which to purchase items

I am wary of having my personal creditinformation hacked using my mobile phone

Strongly disagree Disagree Neither agree nor disagree Agree Strongly agree Don't know

On the other hand, when questioned about why consumers shop online instead of in-store, only two reasons were found to be exclusive to online stores: a) I can shop 24x7 online, and b) No need to travel to a physical store. Interestingly, all other factors can be achieved by physical stores as well.

Thus, our findings prove that the physical store will continue to persevere as the preferred and more convenient channel for shopping for now, even in the wake of disruptors such as the ones discussed in this report. When looking for everyday items like milk and eggs or when looking for that perfect dress for the office gala, customers will still prefer to run to the nearest store.

Having said that, retailers are attempting to match e-tailers’ business strategies, every step of the way, if not outdoing them altogether.

A number of retailers have refuted the claim that everything available online is cheap. In fact, a number of online retailers have excluded product categories that do not provide an EBIDTA of more than 20%.

The in-store retailer at the same time is working on a number of factors like the in-store look and feel, value added services and customer engagement to ensure customers are in the store and buying. Retailers are also experimenting with innovative marketing and promotion campaigns especially through mobile phones. These include launching shopping apps, SMS alerts during sales and communication of discount codes or coupons. Validating this strategy, 79% of our respondents have admitted that they would be happy to receive offers or coupons via mobile phones.

For the physical store to maintain a competitive advantage, it will have to continue to reinvent itself in keeping with the changing times. With increased competition even in the offline space, retailers have to move beyond the “simply transacting” business model. It is imperative that they provide customers with an experience that would convince them that the new product would change their life. The trend of online retailers entering the physical space by opening offline stores only emphasises how multisensory customer experiences contribute immensely in building lasting relationships with the consumer.

Total Retail 2015: Retailers and the age of disruption 21

Future of modern retail in IndiaDisruptors are the order of the day. E-tailers are scrambling to differentiate themselves from the crowd in order to register the highest gross merchandise sales. Meanwhile, traditional offline retailers are also jostling to maintain their position in overall retail.

In the next stage of their evolution, how will the online and the offline retailers work? Do we see a possible amalgamation of the channels or at least collaborations to begin with?

E-commerce: the benevolent distributor for several small scale businesses

The success of the online marketplace has encouraged several entrepreneurs and small businesses to build their presence online. Not only have they benefitted from the extensive reach of the e-tailer in the country, but have also been able to piggyback on the existing supply chain infrastructure and marketing and advertising campaigns.

Be it saree weavers in Varanasi, handicrafts and curio makers or even local manufacturers of bags, small

manufacturers are finding it easier to grow and sustain their business on online marketplaces.

A more viable long-term strategy for growth

Offering lower prices will not be viable in the long term. Despite luring in customers in the initial stages, lower prices won’t be able to retain customers in the long run. While the discounting will continue for some more months, e-tailers are thinking beyond discounts to acquire customers and build loyalty.

The combined losses faced by e-tailing companies as a result of their discounting strategies now stand at almost 1,000 crore INR.

Further, with valuations of e-commerce companies skyrocketing, there is increasing pressure from investor firms to cut down on discounts and concentrate on making profits. The more mature firms in the business are gradually implementing this change in strategy.

As an alternative, customer data analytics and a host of other tools for customer engagement are helping e-tailers to offer tailor-made solutions on a large scale. Awareness campaigns linked with social issues have also contributed immensely to increasing topline sales of a leading online

retailer specialising in the sale of women’s lingerie.

Emergence of Tier II and III cities as consumption centres

The increasing sale of smartphones and the consequent increase in the internet user base has led to the emergence of small towns as e-commerce hubs. Retailers continue to face challenges like high real estate costs, labour, sourcing and supply chain along with the conditions on multi-brand and single-brand retail trading in India. E-tailing is therefore emerging as a viable alternative by which organised retail can expand its share in the total retail pie.

Keeping this in mind, traditional retailers are fast expanding into the online space.

Tie-ups between online and offline channels

Another model that can result from Tier II and Tier III cities driving consumption is that of collaborations between online and offline retailers.

According to our survey, customers pick their favourite retailers based on a number of factors that are characteristic of both the online and offline channels of retailing.

Why do you shop at your favourite retailer?

0%

14%

16%

18%

20%

23%

25%

26%

27%

27%

28%

28%

30%

33%

46%

55%

0% 10% 20% 30% 40% 50% 60%

Other

They do really interesting stuff with their social…

They have inspiring online content which catches my…

They are a socially/environmentally responsible…

They sell things I cannot find anywhere else

They provide advice or help me choose products

Superior online customer reviews

Their website/mobile site is easy to use

I like the store, its location and staff

I can check the in-store availability of a product online

They have a great loyalty programme (e.g. I get…

They have fast/reliable delivery (e.g. same day…

They have a good returns policy (e.g. free returns,…

They usually have the items I want in stock

I trust the brand

Their prices are good

22 PwC

Further, data from our survey states that respondents largely voted for a seamless shopping experience across the brick and mortar store, website and mobile application.

Cross-channel collaboration could create a win-win situation for both the customers as well as the retailers. The customers would enjoy the seamless shopping experience that they desire. Additionally, offline retail could benefit from the reach of online retail while online retail could capitalise on the presence of traditional retail in territories that were left uncovered. The objective would be to cover as many PIN codes as possible.

Over the last few months, several large format as well as specialist physical retail chains have forged partnerships with online companies to this end.

Mobile continues to attract new customers

As illustrated in this report, while mobile shopping still accounts for a small percentage of retail sales, an increasing number of customers now prefer shopping on their smartphones, thus validating our earlier view of mobile shopping being the next game changer.

One way of dealing with change is to embrace it and the future of modern retail seems to be ushering in an era of symbiotic co-existence between the multiple channels. In reality, e-tailers could do with the volumes of business that existing offline retailers possess whereas the latter, especially local businesses, can gain exponentially by harnessing the nationwide reach of the large e-commerce players.

What do you wish Indian online retailers would do to make you not just research or browse online but buy online as well?

Which product categories do you prefer to buy through your mobile?

72%

77%

83%

66%68%70%72%74%76%78%80%82%84%

Design better site functionality (well planned site, less clicks to buy, easy purchase process, etc)

Provide a seamless experience across the brick and mortar store, or online or on a mobile app

Provide the same product range across all their channels

32%

23%

34%

13%

24%

21%

16%

56%

44%

30%

37%

31%

28%

24%

19%

25%

28%

21%

64%

50%

31%

44%

0% 10% 20% 30% 40% 50% 60% 70%

Health and beauty (cosmetics)

Toys

Grocery

DIY and home improvement

Jewellery and watches

Sports and outdoor equipment

Furniture and homeware

Books, music, movies and video games

Clothing and footwear

Household appliances

Consumer electronics and computers

20142013

Total Retail 2015: Retailers and the age of disruption 23

About our Retail and Consumer practice

About PwC

The India Retail and Consumer practice boasts of having worked with the Fortune 500 companies.Developing the market entry strategy for global companies, location assessment based on the target audience, streamlining the supply chain and distribution system, deploying IT strategy, linking the customer data using analytics, managing the inventory and ensuring a delightful experience for the customer are among the gamut of services that we offer our clients to help them in their journey to success.

Our clients in the R&C goods sector operate in different formats ranging from supermarket chains to food and beverage manufacturers and from luxury goods retailers to consumer packaged-goods manufacturers, and agribusiness companies.

PwC’s globally renowned technical expertise, its unsurpassed tax capabilities, 19,000 professionals in118 countries serving the R&C companies, and the fact that it hosts the best talent worldwide makes it the best choice to help you overcome every challenge and optimally utilise all opportunities.

PwC helps organisations and individuals create the value they’re looking for. We’re a network of firms in 157 countries with more than 195,000 people who are committed to delivering quality in Assurance, Tax and Advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com.

In India, PwC has offices in these cities: Ahmedabad, Bangalore, Chennai, Delhi NCR, Hyderabad, Kolkata, Mumbai and Pune. For more information about PwC India’s service offerings, visit www.pwc.in

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

You can connect with us on:

facebook.com/PwCIndia

twitter.com/PwC_IN

linkedin.com/company/pwc-india

youtube.com/pwc

Rachna NathRetail and Consumer LeaderPwC IndiaEmail: [email protected]

Kalyani PalkarAnalyst, Retail and ConsumerPwC IndiaEmail: [email protected]

Additional contributions by

Debarghya DasManager, AdvisoryPwC IndiaEmail: [email protected]

Contacts

www.pwc.inData Classification: DC0

This publication does not constitute professional advice. The information in this publication has been obtained or derived from sources believed by PricewaterhouseCoopers Private Limited (PwCPL) to be reliable but PwCPL does not represent that this information is accurate or complete. Any opinions or estimates contained in this publication represent the judgment of PwCPL at this time and are subject to change without notice. Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication. PwCPL neither accepts or assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decisions readers may take or decide not to or fail to take.

© 2015 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Private Limited (a limited liability company in India having Corporate Identity Number or CIN : U74140WB1983PTC036093), which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity.

AK 315 - January 2015 Name of the report.inddDesigned by Corporate Communications, India