Embed Size (px)

Citation preview

TRUSTEE INVESTMENT PLANNING

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

• The reasons to incorporate trustee investment as part of your service delivery under adviser charging

• Trustee investment fundamentals

• Putting it into practice: Case study

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

These slides and the presentation in which they are used are put forward for general

consideration only. They are based on fictitious persons. No action must be taken or refrained from based on their content. Accordingly, neither Technical Connection

Limited nor any of its officers or employees can accept any responsibility for any loss arising of whatever nature to any person. Professional advice based on

the facts of each case is essential.

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

WHY WILL CLIENTS PAY FOR ADVICE?(HOWEVER IT’S DELIVERED)

Recognition of the limits of their own knowledge

The adviser has expertise that the consumer doesn’t possess or can’t get by “googling”

The adviser makes them aware of the need/risk/opportunity

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

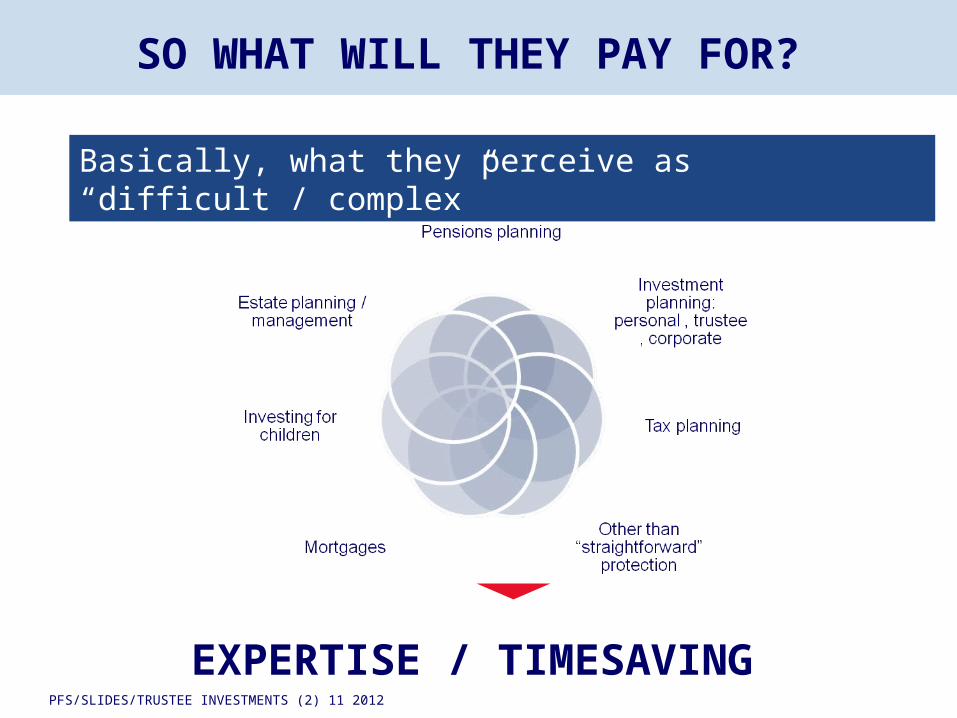

SO WHAT WILL THEY PAY FOR?

Basically, what they perceive as “difficult / complex”

EXPERTISE / TIMESAVING

SO WHAT WILL THEY PAY FOR?

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

AND IF WE ARE TALKING ABOUT TAX ….

You can’t have missed that it’s in the news

Tax and tax planning polarises opinions

Government committed to action

So……….

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

What’s going on?

Tax Avoidance

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

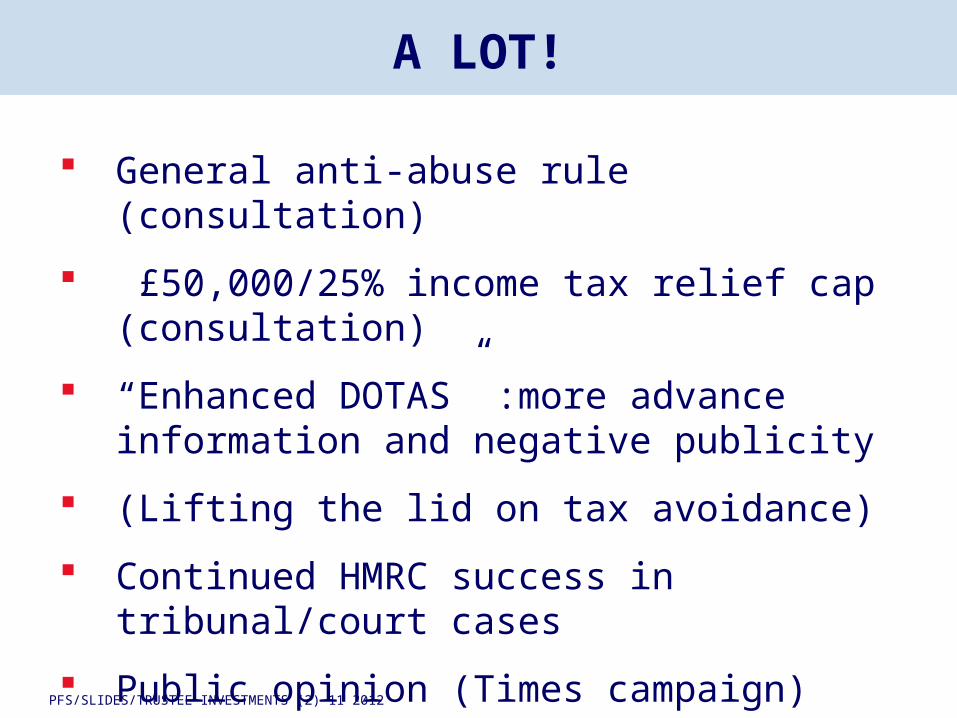

A LOT!

General anti-abuse rule (consultation)

£50,000/25% income tax relief cap (consultation)

“Enhanced DOTAS” :more advance information and negative publicity

(Lifting the lid on tax avoidance)

Continued HMRC success in tribunal/court cases

Public opinion (Times campaign)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

FINANCIAL PLANNING

GAAR should not affect “the centre ground of tax planning”

Opportunities to reinforce the power and effectiveness of “acceptable” financial planning for individuals ,

businesses and trustees

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TRUSTEE INVESTMENT ADVICE:A “PERFECT STORM”?

• High degree of difficulty

• Adviser charge justifiable

• Relatively high trustee tax rates

• Trusts are an essential part of estate

planning

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TRUSTEE INVESTMENT ADVICE :A “PERFECT STORM” ?

• Trustees must take investment advice

• Solicitors and accountants rarely have the necessary financial planning skills

• Strong collaboration potential for advisers

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

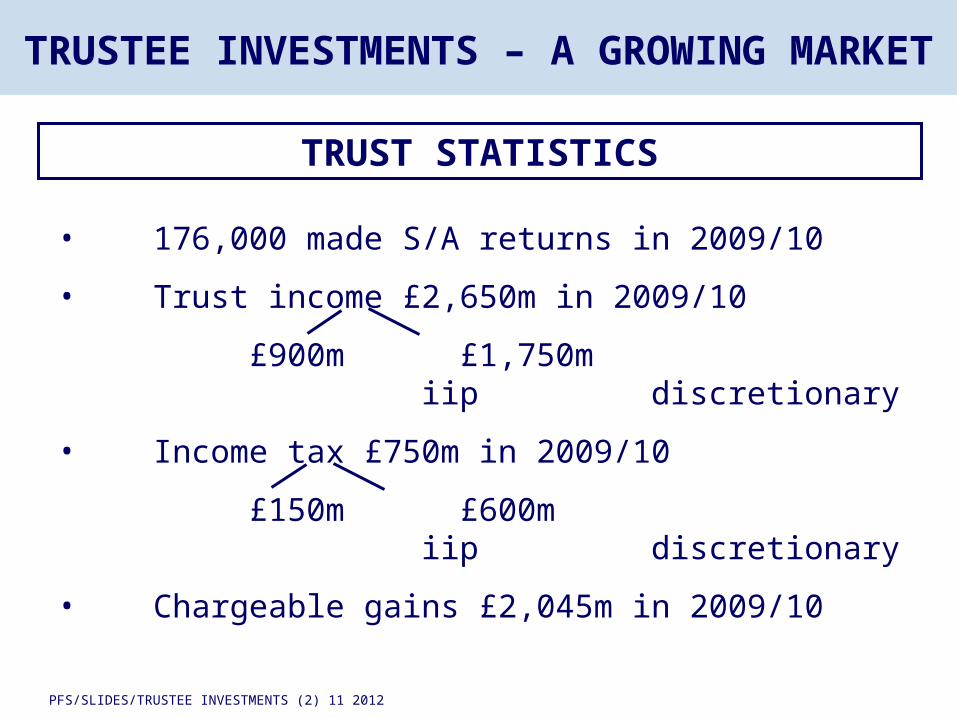

TRUSTEE INVESTMENTS – A GROWING MARKET

TRUST STATISTICS

• 176,000 made S/A returns in 2009/10

• Trust income £2,650m in 2009/10

£900m £1,750m iip discretionary

• Income tax £750m in 2009/10

£150m £600m iip discretionary

• Chargeable gains £2,045m in 2009/10

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

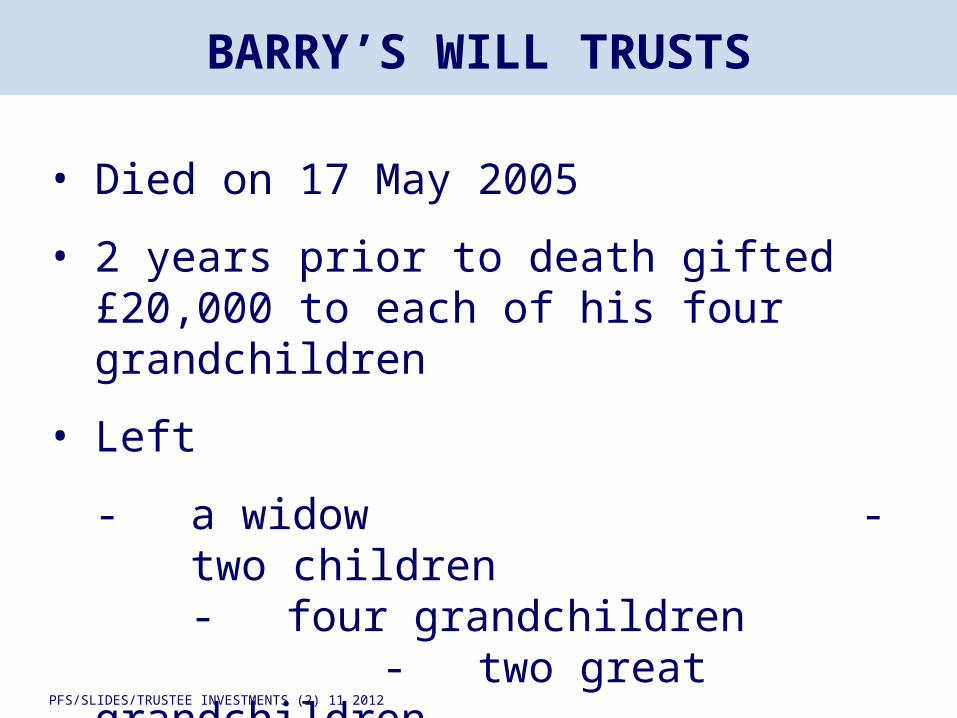

BARRY’S WILL TRUSTS

• Died on 17 May 2005

• 2 years prior to death gifted £20,000 to each of his four grandchildren

• Left

- a widow -two children -four grandchildren - two great grandchildren

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

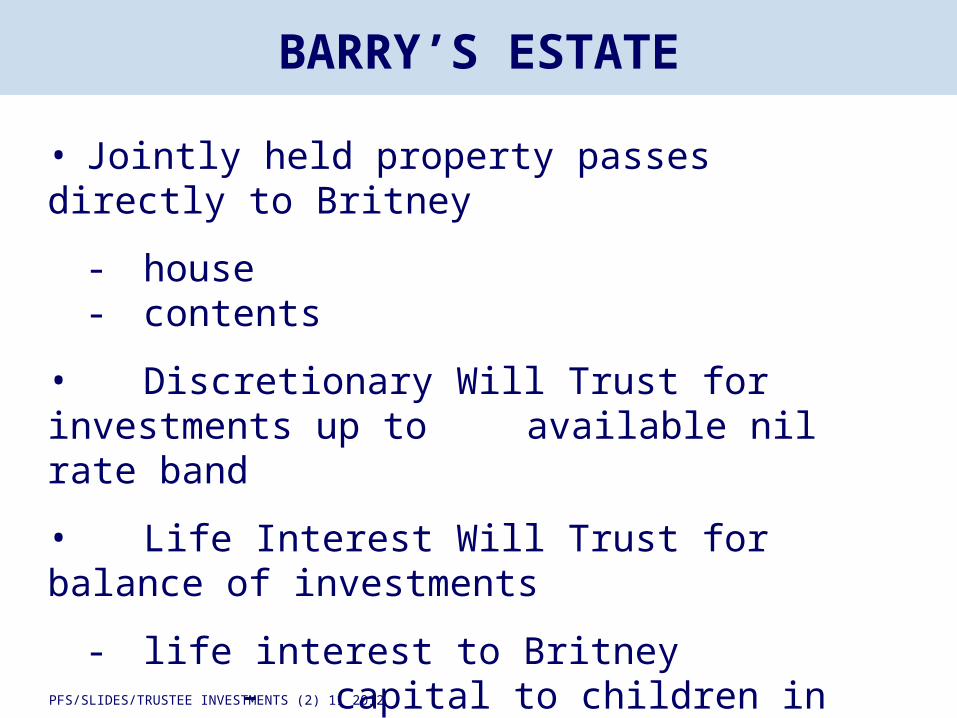

BARRY’S ESTATE

• Jointly held property passes directly to Britney

- house- contents

• Discretionary Will Trust for investments up to available nil rate band

• Life Interest Will Trust for balance of investments

- life interest to Britney- capital to children in equal shares

on Britney’s death

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

UNDERSTANDING THE FUNDAMENTALS

TRUSTEE ACT “IMPERATIVES”

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

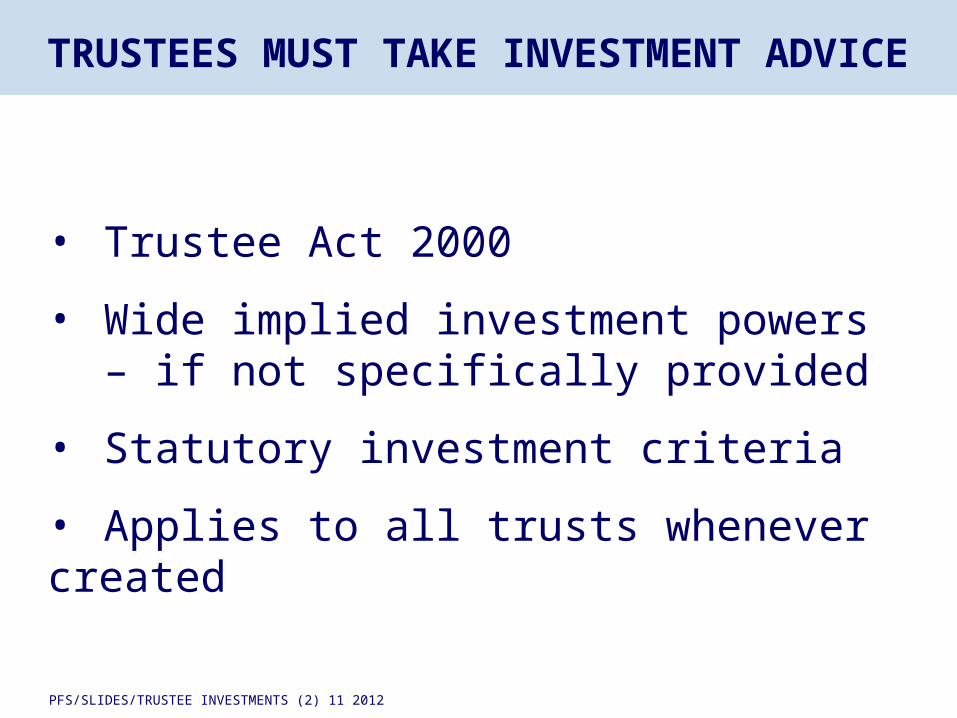

TRUSTEES MUST TAKE INVESTMENT ADVICE

• Trustee Act 2000

• Wide implied investment powers– if not specifically provided

• Statutory investment criteria

• Applies to all trusts whenever created

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

STATUTORY INVESTMENT CRITERIA

• Diversification

• Suitability

AND

• Obtain and consider proper advice

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

Advice of a person who the trustees reasonably believe to be qualified to give it by his (or her)

Ability in

+

Practical experience of financial + other matters

“PROPER ADVICE”

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

UNDERSTANDING THE FUNDAMENTALS

TRUST TAXATION

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

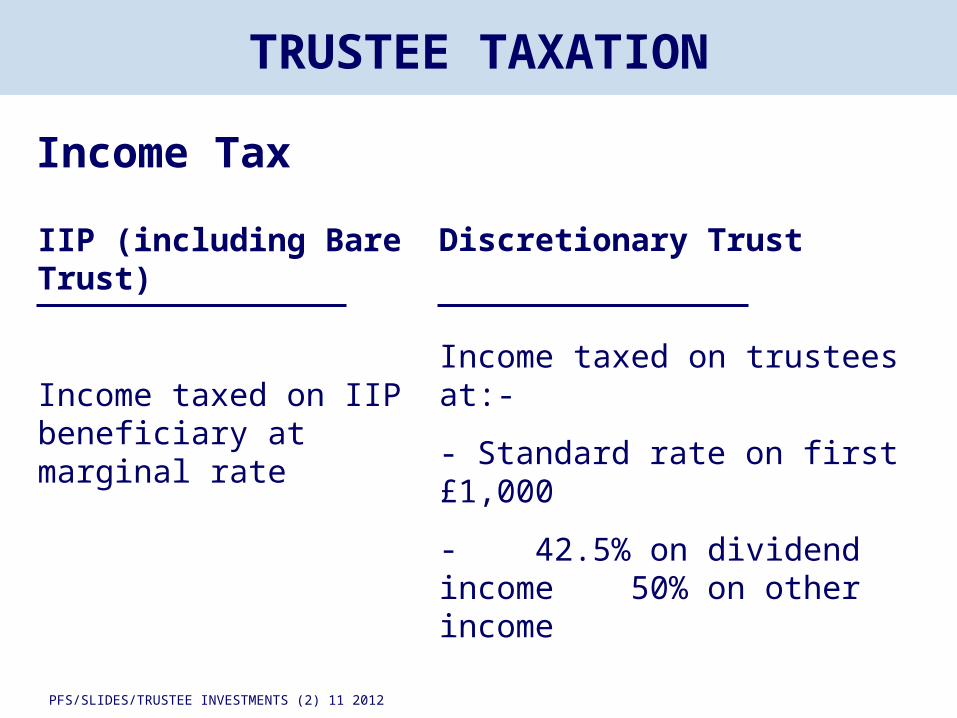

TRUSTEE TAXATION

Income Tax

IIP (including Bare Trust)

Income taxed on IIP beneficiary at marginal rate

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TRUSTEE TAXATION

Income Tax

IIP (including Bare Trust)

Income taxed on IIP beneficiary at marginal rate

Discretionary Trust

Income taxed on trustees at:-

- Standard rate on first £1,000

- 42.5% on dividend income 50% on other income

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

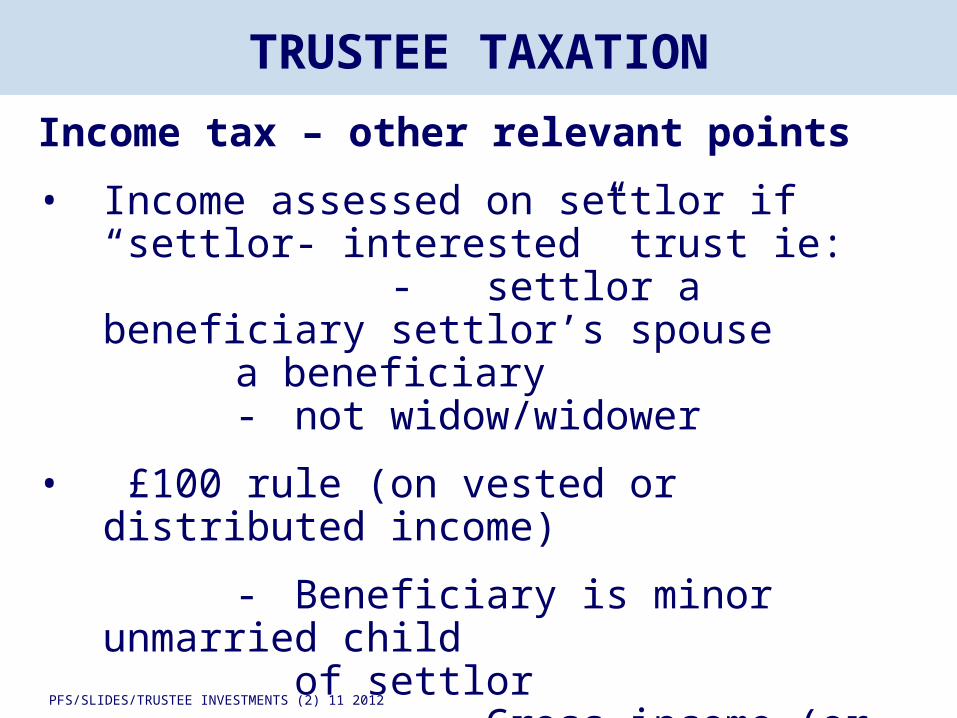

TRUSTEE TAXATION

Income tax – other relevant points

• Income assessed on settlor if“settlor- interested” trust ie:

- settlor a beneficiary settlor’s spouse a beneficiary

- not widow/widower

• £100 rule (on vested or distributed income)

- Beneficiary is minor unmarried child

of settlor- Gross income (or income

on all gifts) exceeds £100

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

DISCRETIONARY TRUST – INCOME TAX DETAIL

2 STAGE PROCESS

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

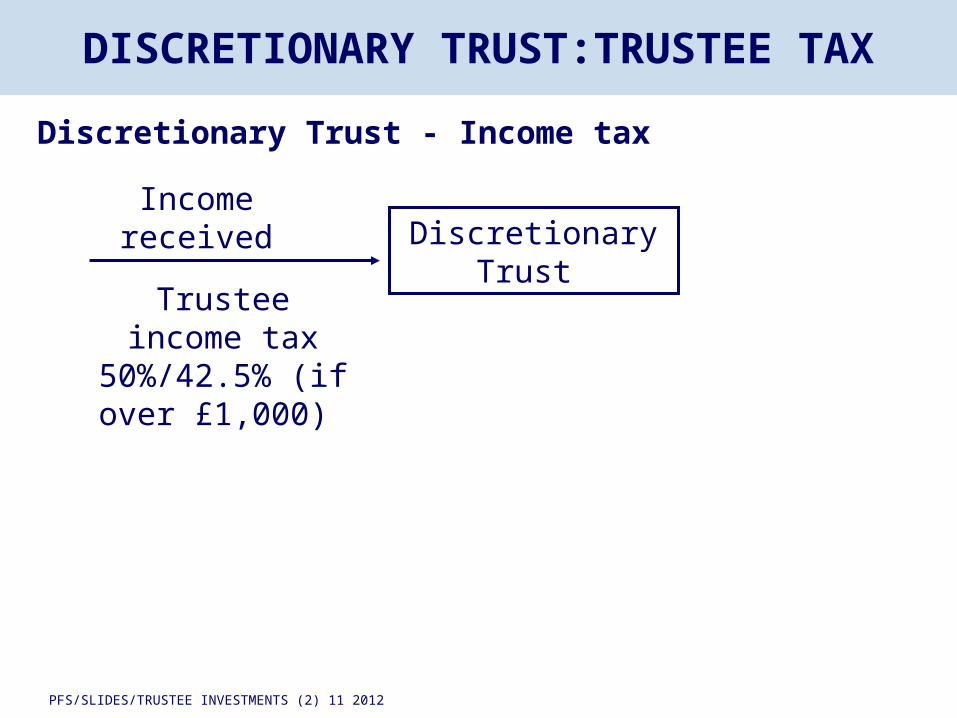

DISCRETIONARY TRUST:TRUSTEE TAX

Discretionary Trust - Income tax

Income received

Trustee income tax 50%/42.5% (if over £1,000)

Discretionary Trust

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

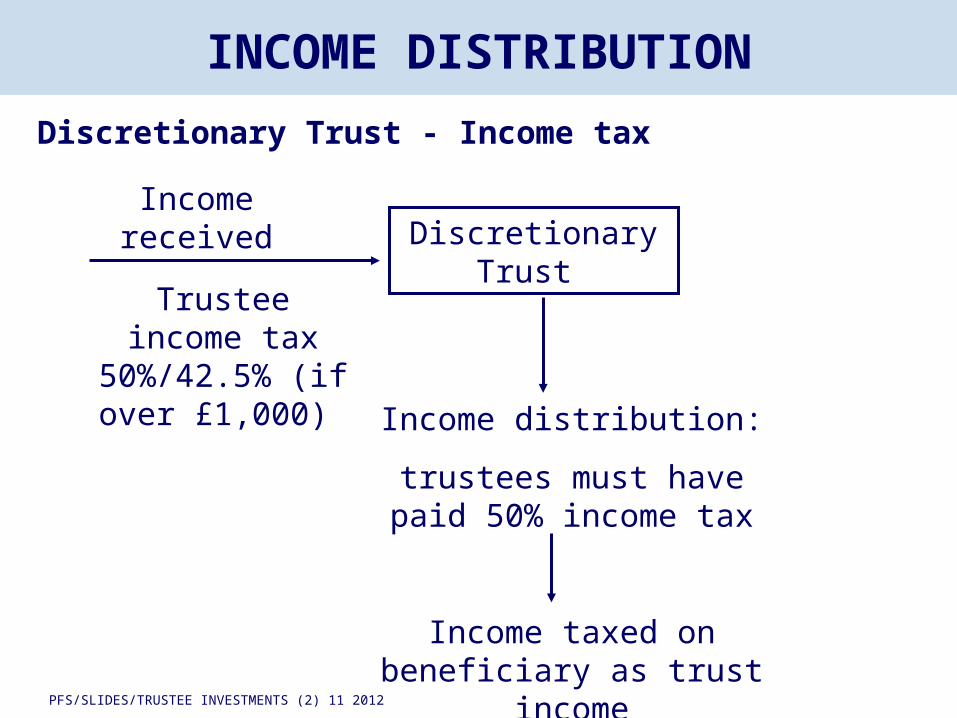

INCOME DISTRIBUTION

Discretionary Trust - Income tax

Income received

Trustee income tax 50%/42.5% (if over £1,000)

Discretionary Trust

Income distribution:

trustees must have paid 50% income tax

Income taxed on beneficiary as trust

income

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

DISCRETIONARY TRUST – INCOME TAX DETAIL

STAGE 1:

RECEIPT OF INCOME

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

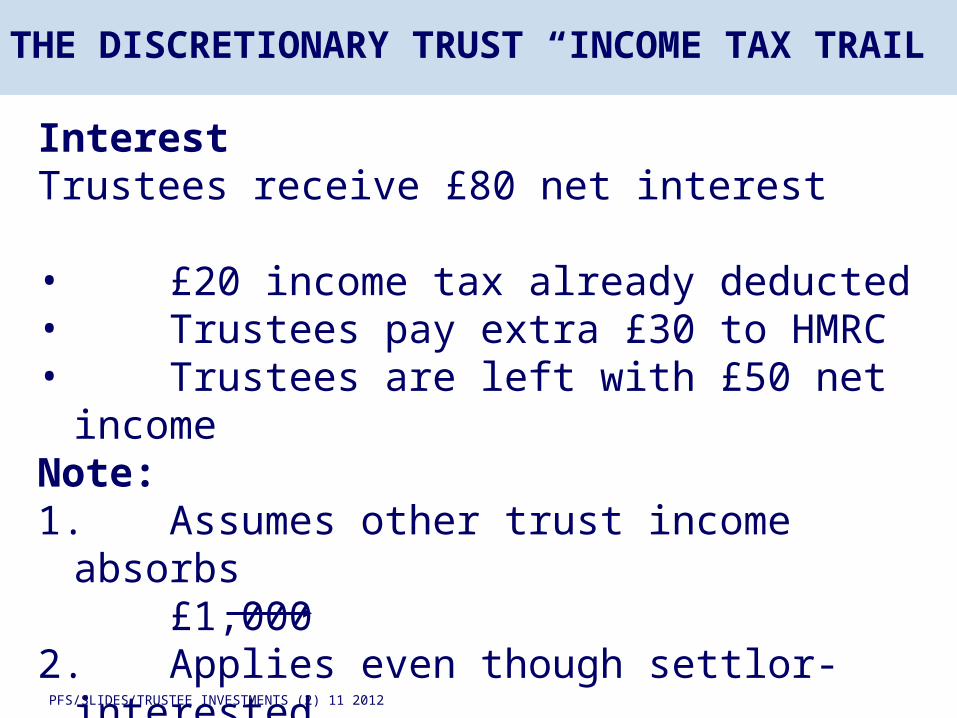

THE DISCRETIONARY TRUST “INCOME TAX TRAIL”

Interest Trustees receive £80 net interest • £20 income tax already deducted• Trustees pay extra £30 to HMRC• Trustees are left with £50 net incomeNote:1. Assumes other trust income absorbs

£1,0002. Applies even though settlor-

interestedtrust

3. 50% 45% from 6.4.2013

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

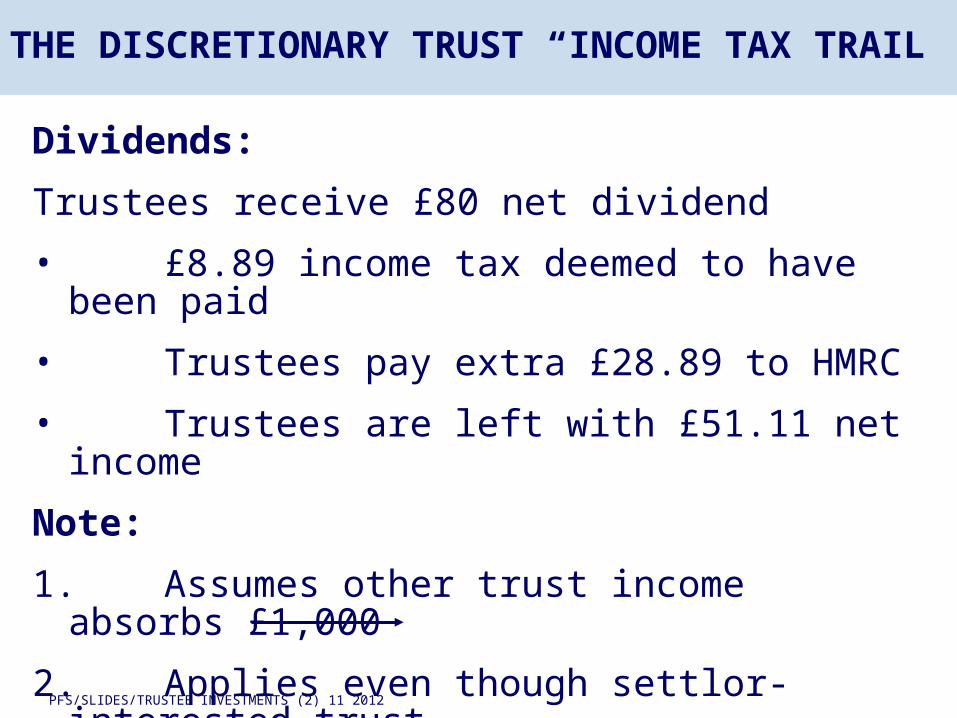

THE DISCRETIONARY TRUST “INCOME TAX TRAIL”

Dividends:

Trustees receive £80 net dividend

• £8.89 income tax deemed to have been paid

• Trustees pay extra £28.89 to HMRC

• Trustees are left with £51.11 net income

Note:

1. Assumes other trust income absorbs £1,000

2. Applies even though settlor-interested trust

3. 42.5% 37.5% from 6.4.2013

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

DISCRETIONARY TRUST – INCOME TAX DETAIL

STAGE 2:

INCOME DISTRIBUTION

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

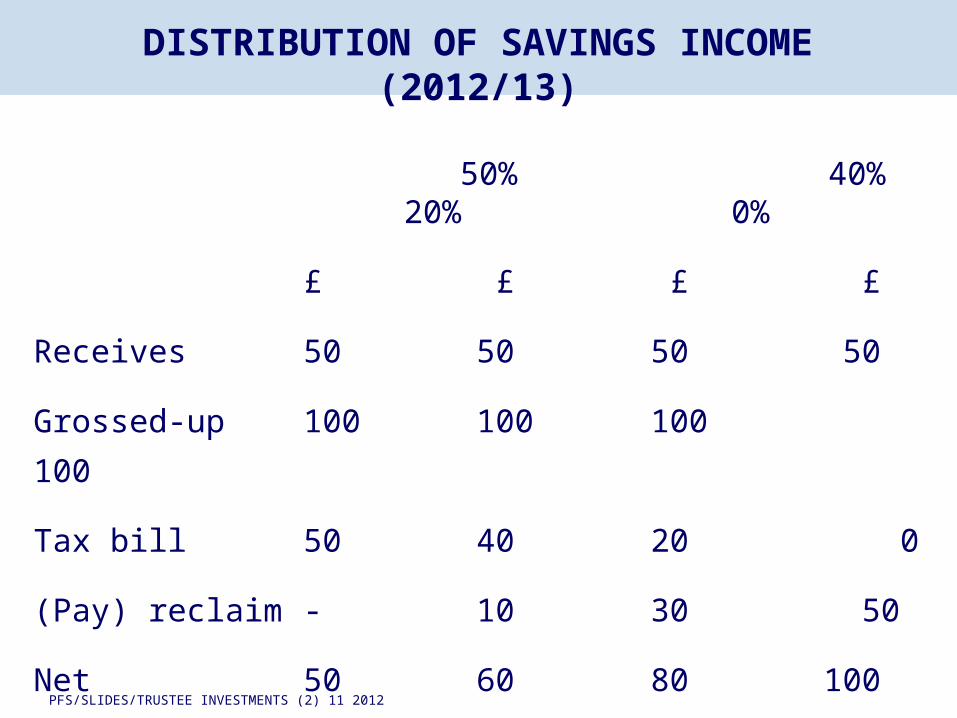

50% 40% 20% 0%

£ £ £ £

Receives 50 50 50 50

Grossed-up 100 100 100 100

Tax bill 50 40 20 0

(Pay) reclaim - 10 30 50

Net 50 60 80 100

DISTRIBUTION OF SAVINGS INCOME (2012/13)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

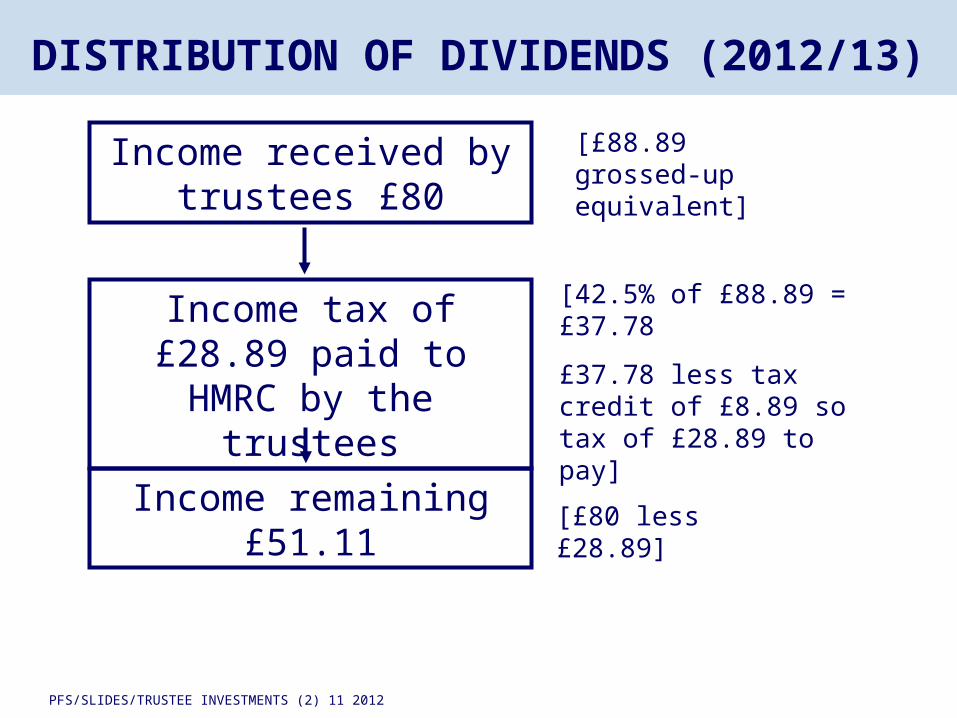

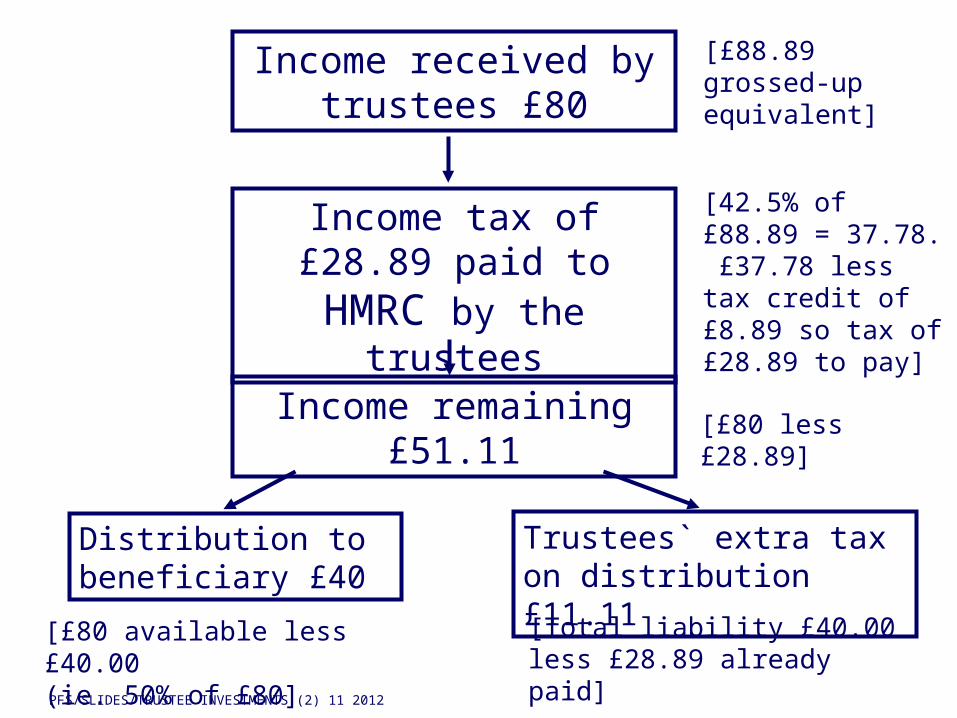

Income received by trustees £80

Income tax of £28.89 paid to HMRC by the

trustees

Income remaining £51.11

[£88.89 grossed-up equivalent]

[42.5% of £88.89 = £37.78

£37.78 less tax credit of £8.89 so tax of £28.89 to pay]

[£80 less £28.89]

DISTRIBUTION OF DIVIDENDS (2012/13)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

Distribution to beneficiary £40

Trustees` extra tax on distribution £11.11

[£80 available less £40.00(ie. 50% of £80]

[Total liability £40.00 less £28.89 already paid]

Income received by trustees £80

Income tax of £28.89 paid to HMRC by the

trustees

Income remaining £51.11

[£88.89 grossed-up equivalent]

[42.5% of £88.89 = 37.78. £37.78 less tax credit of £8.89 so tax of £28.89 to pay]

[£80 less £28.89]

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

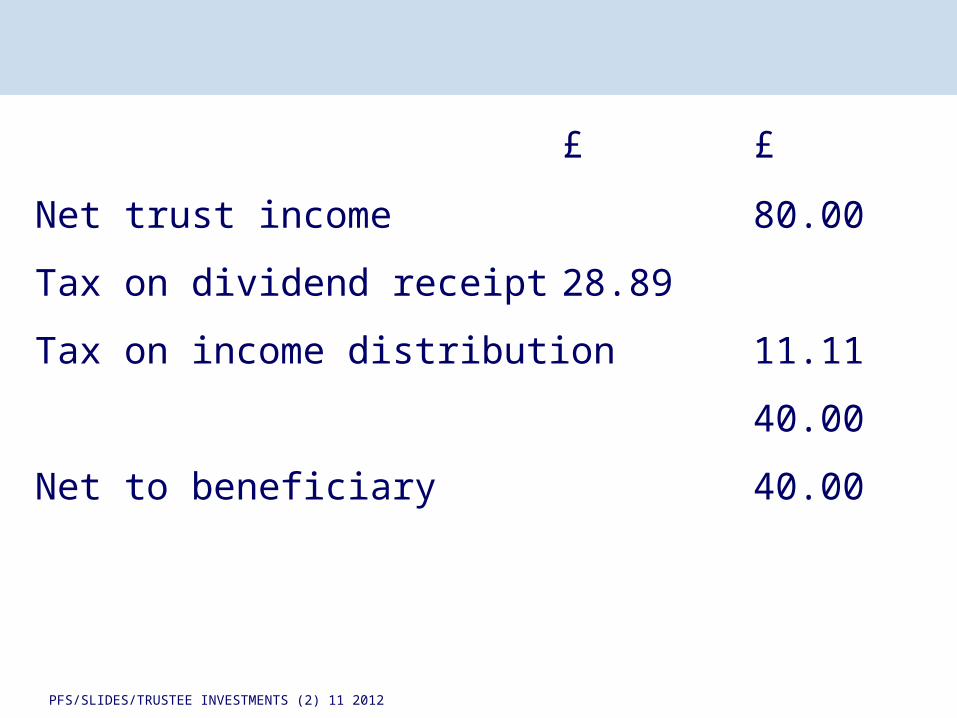

£ £

Net trust income 80.00

Tax on dividend receipt 28.89

Tax on income distribution 11.11

40.00

Net to beneficiary 40.00

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

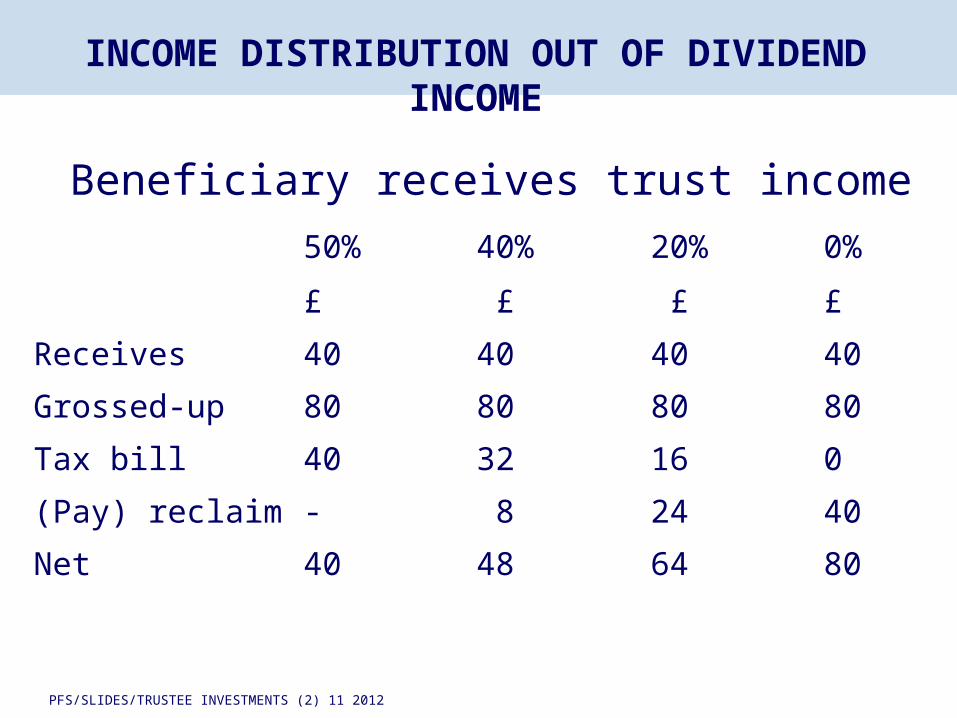

Beneficiary receives trust income

50% 40% 20% 0%

£ £ £ £

Receives 40 40 40 40

Grossed-up 80 80 80 80

Tax bill 40 32 16 0

(Pay) reclaim - 8 24 40

Net 40 48 64 80

INCOME DISTRIBUTION OUT OF DIVIDEND INCOME

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

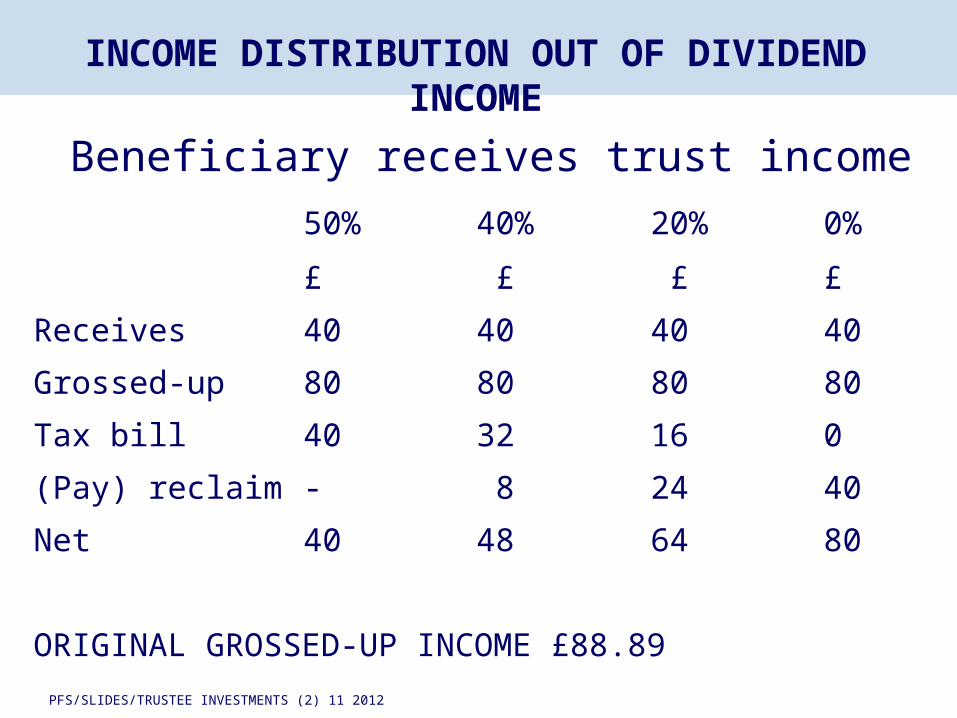

Beneficiary receives trust income

50% 40% 20% 0%

£ £ £ £

Receives 40 40 40 40

Grossed-up 80 80 80 80

Tax bill 40 32 16 0

(Pay) reclaim - 8 24 40

Net 40 48 64 80

ORIGINAL GROSSED-UP INCOME £88.89

INCOME DISTRIBUTION OUT OF DIVIDEND INCOME

PFS/SLIDES/TRUSTEE INVESTMENTS 10 2012

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

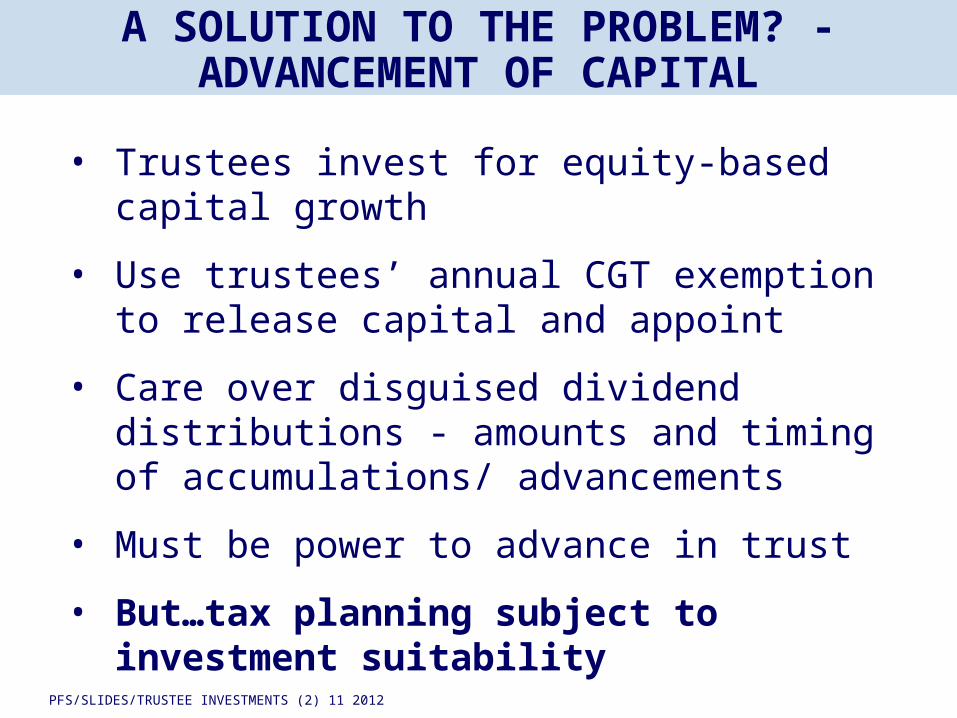

A SOLUTION TO THE PROBLEM? - ADVANCEMENT OF CAPITAL

• Trustees invest for equity-based capital growth

• Use trustees’ annual CGT exemption to release capital and appoint

• Care over disguised dividend distributions - amounts and timing of accumulations/ advancements

• Must be power to advance in trust

• But…tax planning subject to investment suitability

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

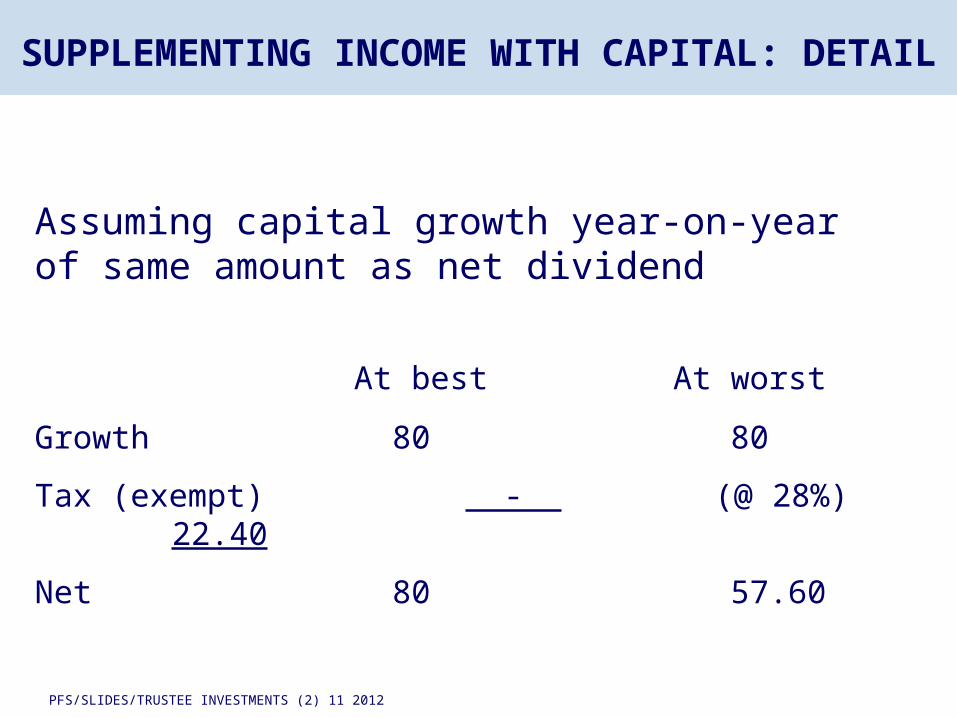

SUPPLEMENTING INCOME WITH CAPITAL: DETAIL

Assuming capital growth year-on-year of same amount as net dividend

At best At worst

Growth 80 80

Tax (exempt) - (@ 28%) 22.40

Net 80 57.60

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

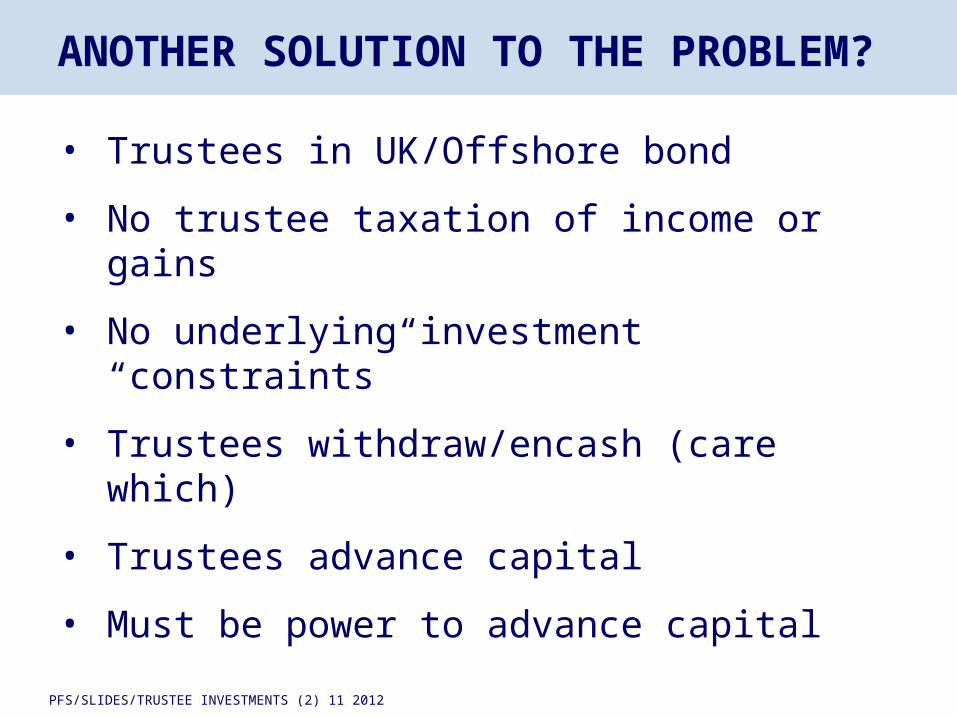

ANOTHER SOLUTION TO THE PROBLEM?

• Trustees in UK/Offshore bond

• No trustee taxation of income or gains

• No underlying investment “constraints”

• Trustees withdraw/encash (care which)

• Trustees advance capital

• Must be power to advance capital

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

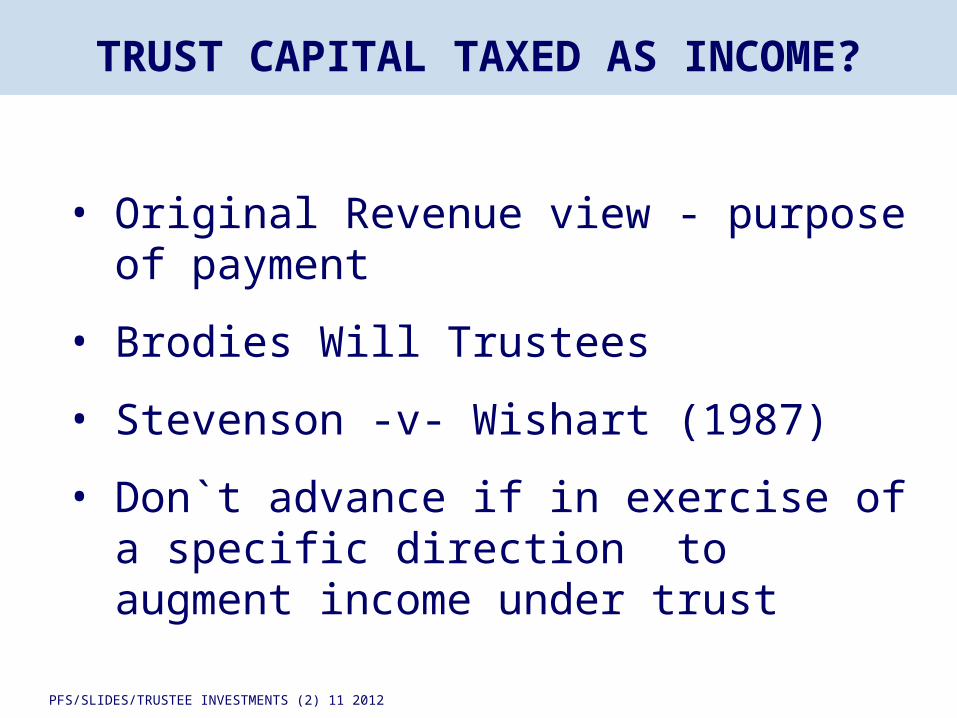

TRUST CAPITAL TAXED AS INCOME?

• Original Revenue view - purpose of payment

• Brodies Will Trustees

• Stevenson -v- Wishart (1987)

• Don`t advance if in exercise of a specific direction to augment income under trust

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

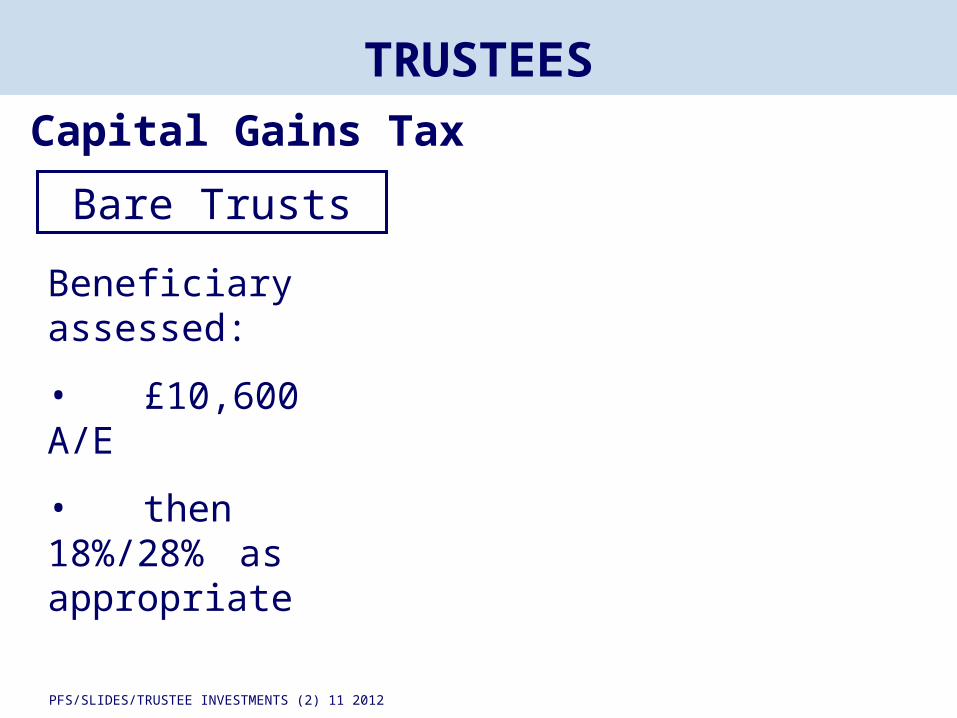

TRUSTEESCapital Gains Tax

Bare Trusts

Beneficiary assessed:

• £10,600 A/E

• then 18%/28% as appropriate

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

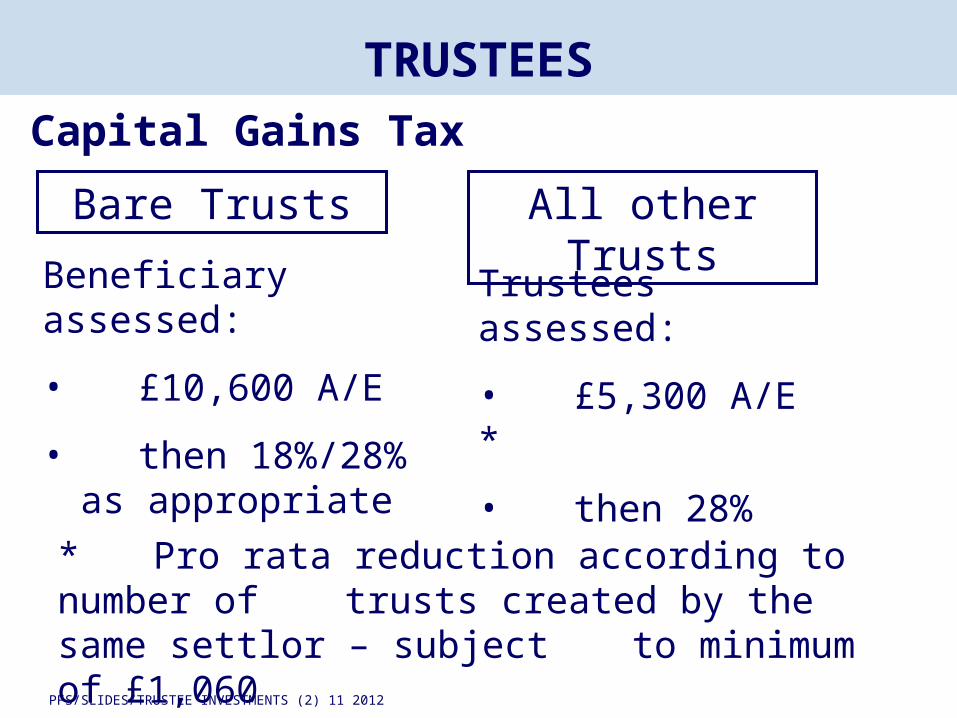

TRUSTEESCapital Gains Tax

Bare Trusts All other Trusts

Beneficiary assessed:

• £10,600 A/E

• then 18%/28% as appropriate

Trustees assessed:

• £5,300 A/E *

• then 28%

* Pro rata reduction according to number of trusts created by the same settlor – subject to minimum of £1,060

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

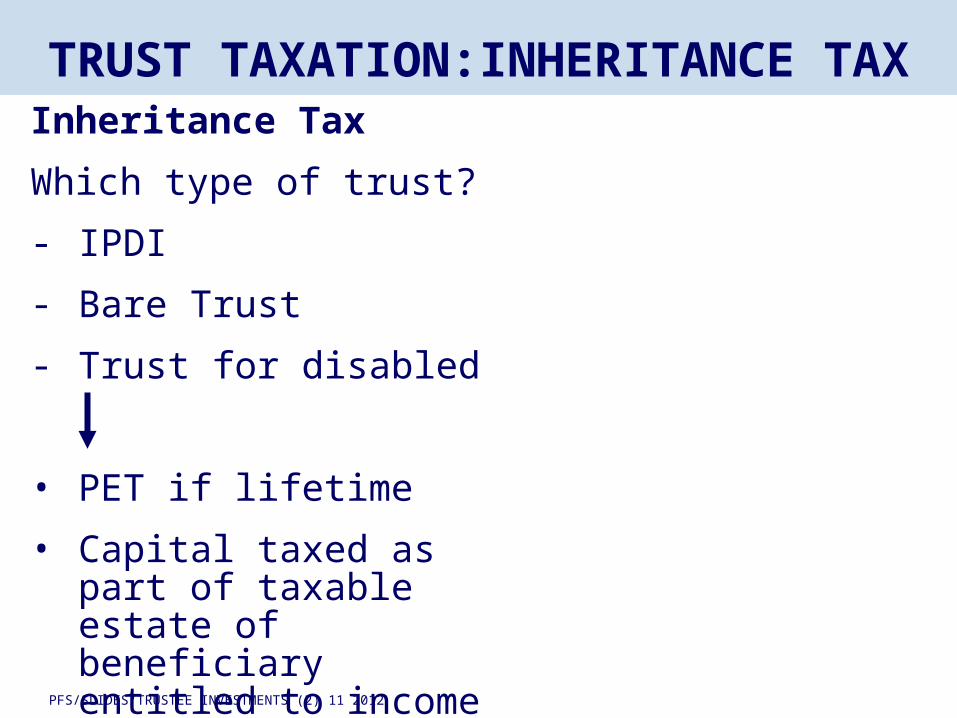

TRUST TAXATION:INHERITANCE TAXInheritance Tax

Which type of trust?

- IPDI

- Bare Trust

- Trust for disabled

• PET if lifetime

• Capital taxed as part of taxable estate of beneficiary entitled to income

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

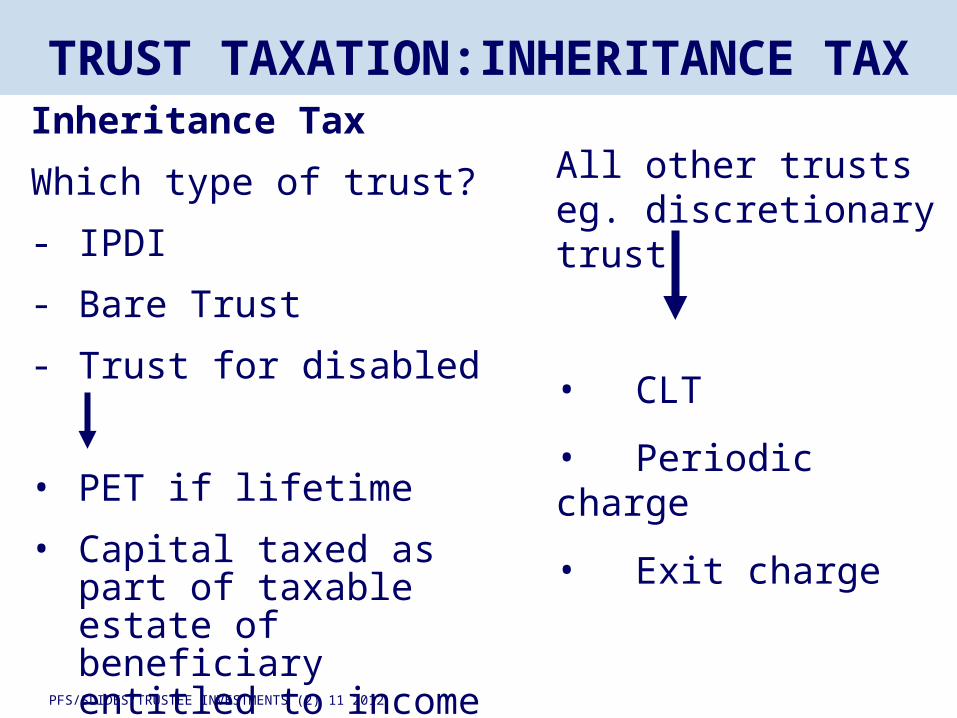

TRUST TAXATION:INHERITANCE TAXInheritance Tax

Which type of trust?

- IPDI

- Bare Trust

- Trust for disabled

• PET if lifetime

• Capital taxed as part of taxable estate of beneficiary entitled to income

All other trusts eg. discretionary trust

• CLT

• Periodic charge

• Exit charge

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

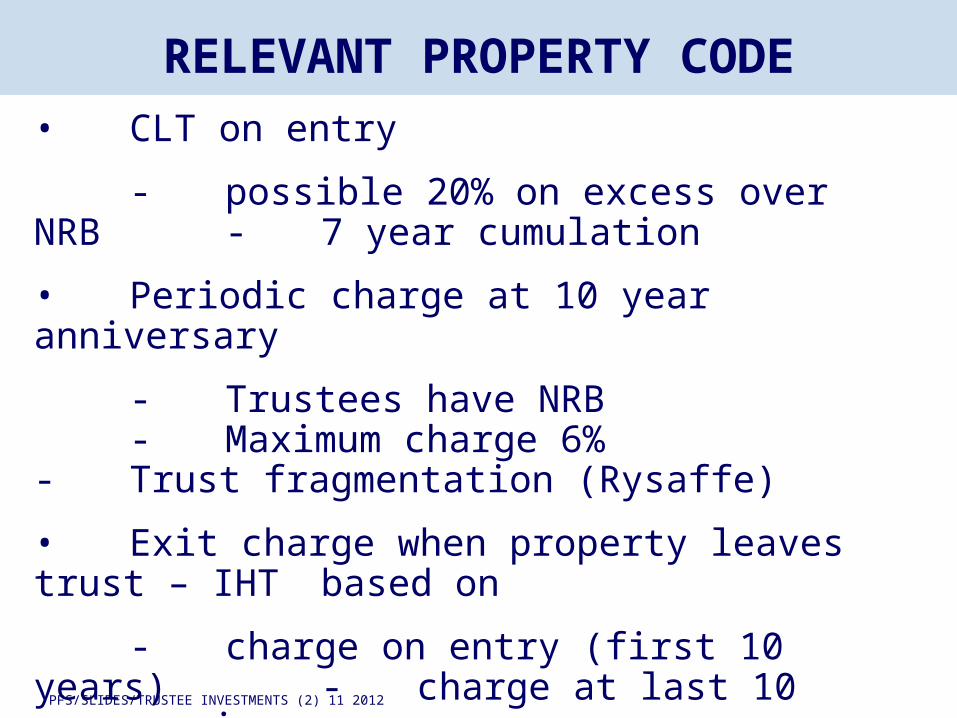

RELEVANT PROPERTY CODE• CLT on entry

- possible 20% on excess over NRB- 7 year cumulation

• Periodic charge at 10 year anniversary

- Trustees have NRB- Maximum charge 6%- Trust fragmentation (Rysaffe)

• Exit charge when property leaves trust – IHT based on

- charge on entry (first 10 years)- charge at last 10 year anniversary

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

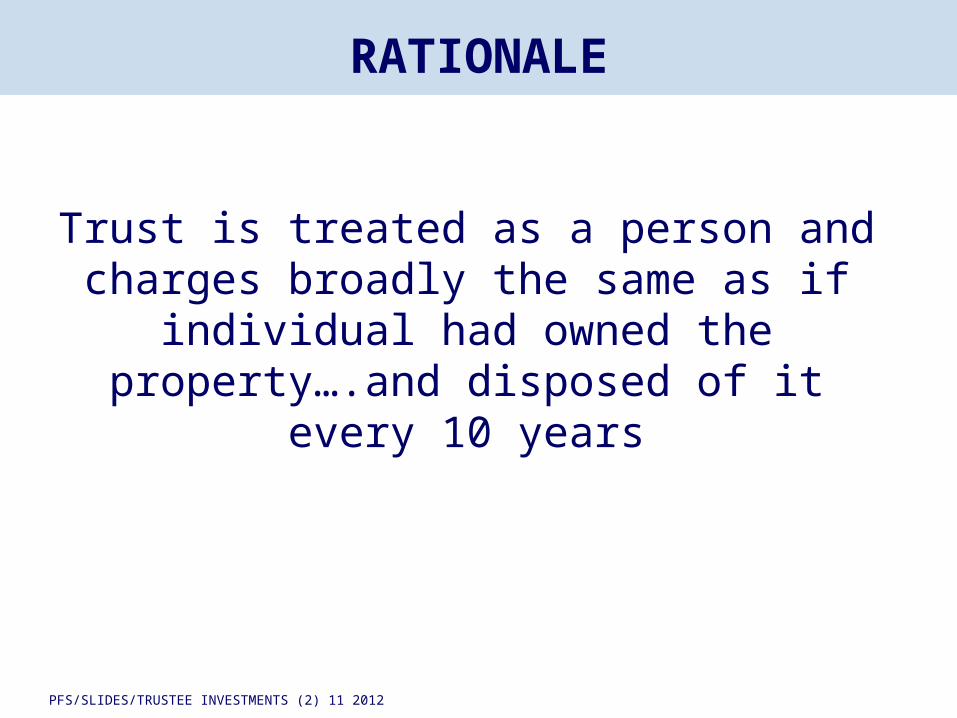

RATIONALE

Trust is treated as a person and charges broadly the same as if individual had

owned the property….and disposed of it every 10 years

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

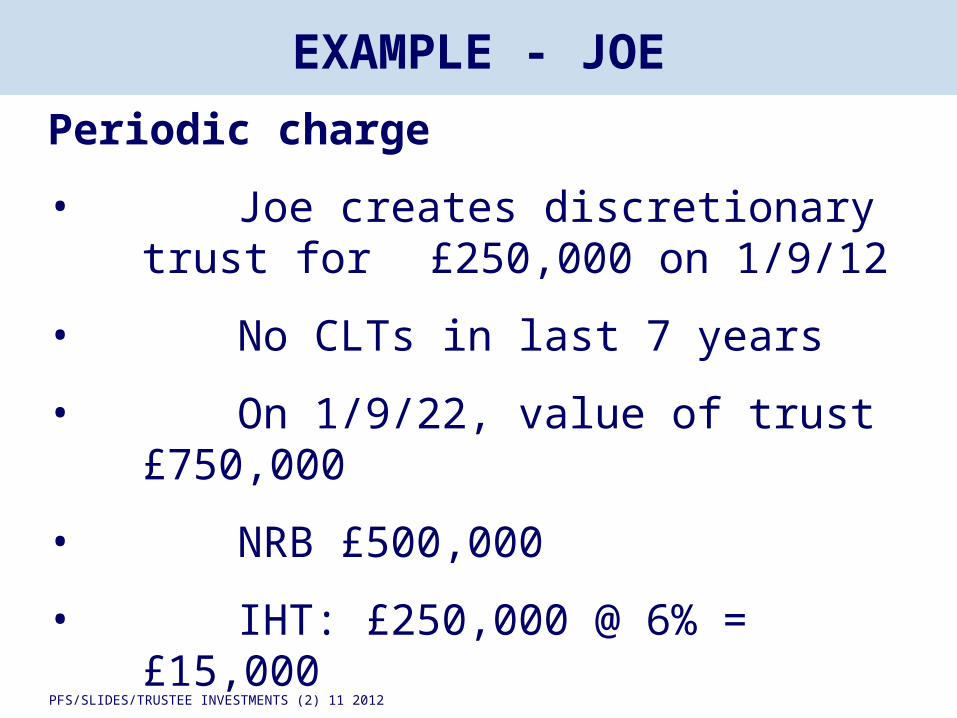

EXAMPLE - JOE

Periodic charge

• Joe creates discretionary trust for £250,000 on 1/9/12

• No CLTs in last 7 years

• On 1/9/22, value of trust £750,000

• NRB £500,000

• IHT: £250,000 @ 6% = £15,000

• Equates to 2% on £750,000

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

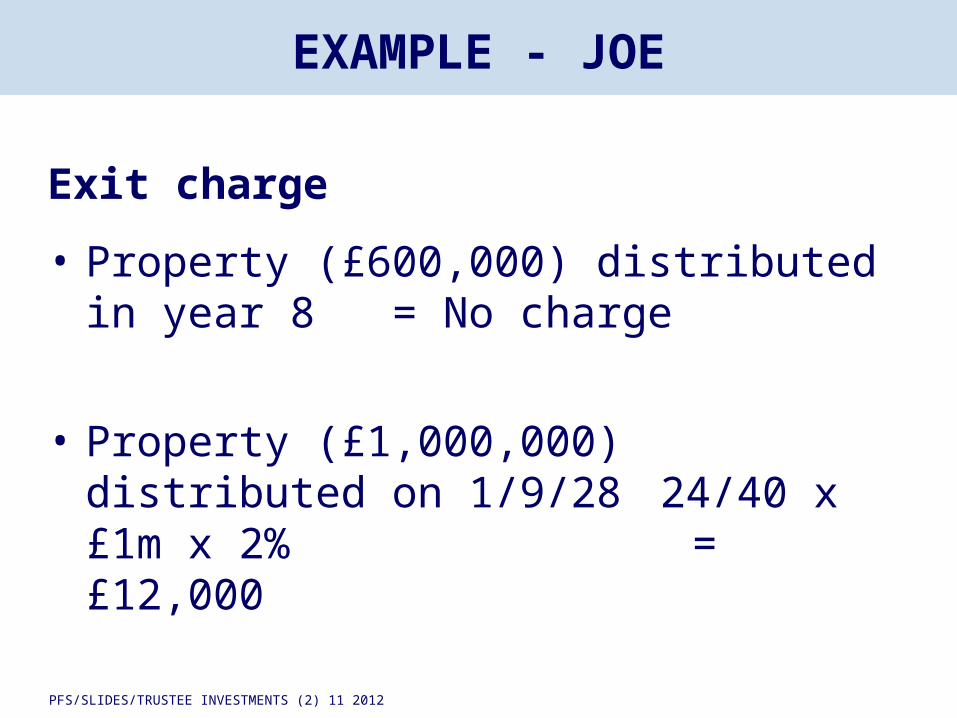

EXAMPLE - JOE

Exit charge

• Property (£600,000) distributed in year 8 = No charge

• Property (£1,000,000) distributed on 1/9/28 24/40 x £1m x 2%

= £12,000

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

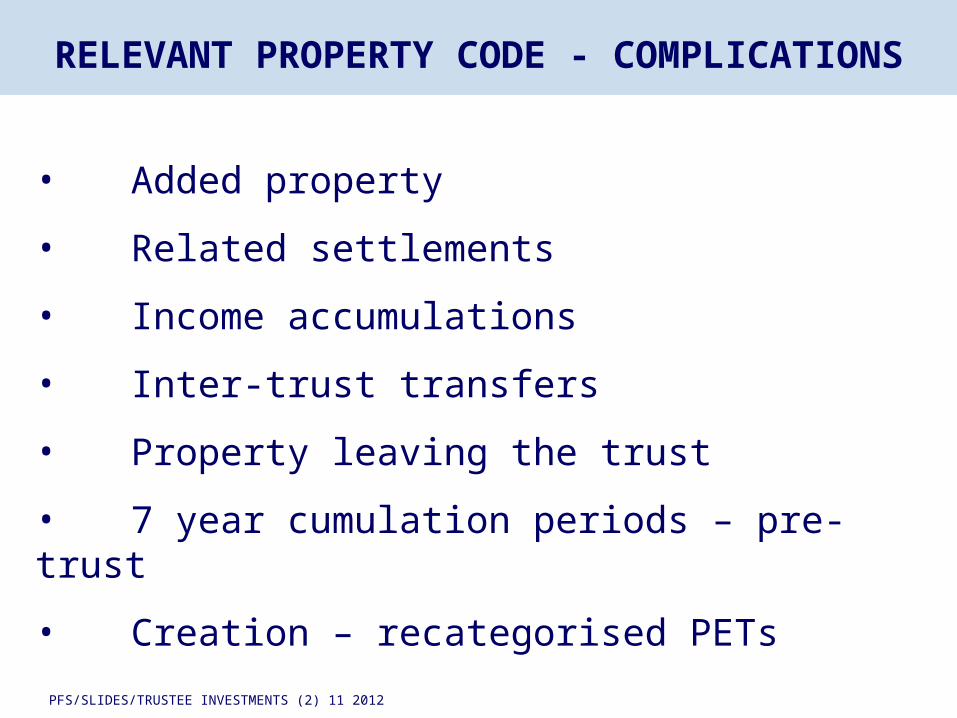

RELEVANT PROPERTY CODE - COMPLICATIONS

• Added property

• Related settlements

• Income accumulations

• Inter-trust transfers

• Property leaving the trust

• 7 year cumulation periods – pre-trust

• Creation – recategorised PETs

PFS/SLIDES/TRUSTEE INVESTMENTS 10 2012

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

UNDERSTANDING THE FUNDAMENTALS

MAKING THE MOST OF THE NIL RATE BAND

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

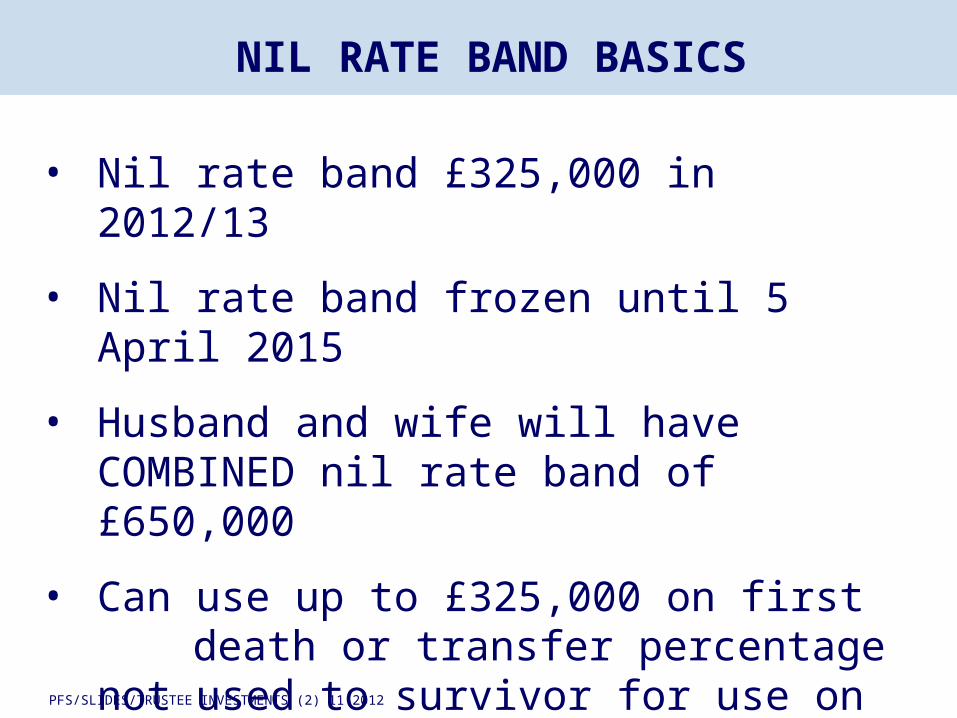

NIL RATE BAND BASICS

• Nil rate band £325,000 in 2012/13

• Nil rate band frozen until 5 April 2015

• Husband and wife will haveCOMBINED nil rate band of £650,000

• Can use up to £325,000 on first death or transfer percentage not used to survivor for use on second death

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

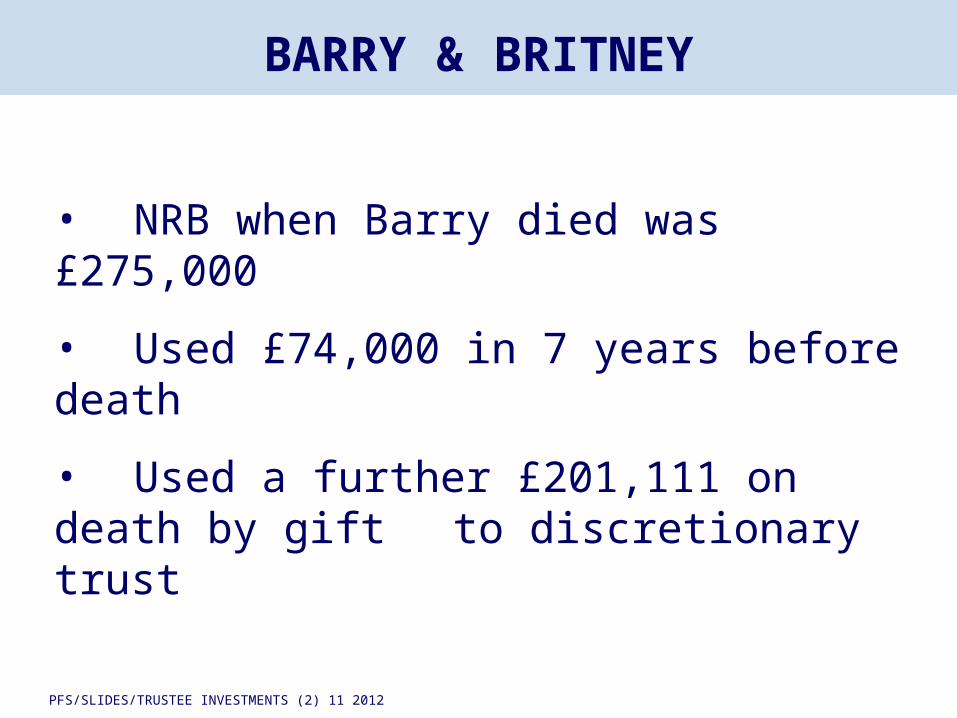

• NRB when Barry died was £275,000

• Used £74,000 in 7 years before death

• Used a further £201,111 on death by gift to discretionary trust

BARRY & BRITNEY

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

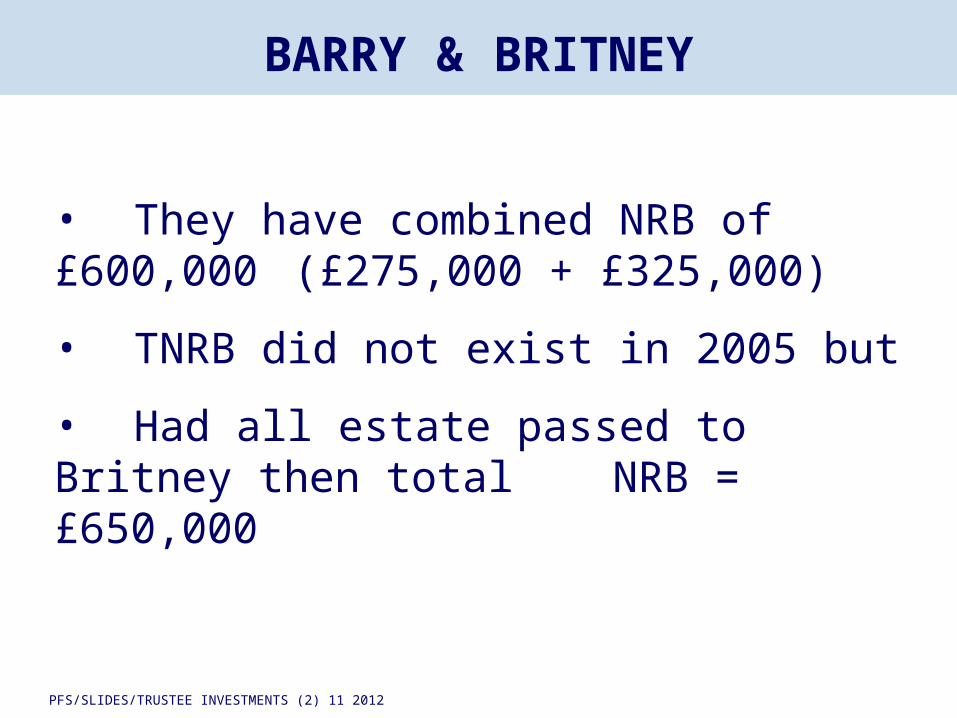

• They have combined NRB of £600,000 (£275,000 + £325,000)

• TNRB did not exist in 2005 but

• Had all estate passed to Britney then total NRB = £650,000

BARRY & BRITNEY

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

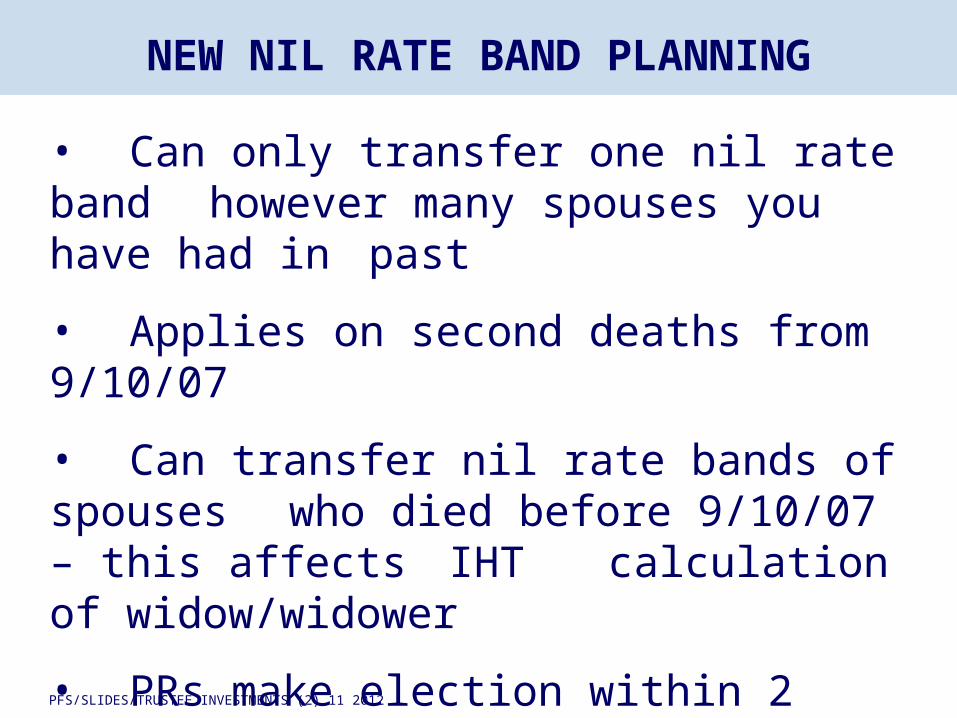

• Can only transfer one nil rate band however many spouses you have had in past

• Applies on second deaths from 9/10/07

• Can transfer nil rate bands of spouses who died before 9/10/07 – this affects IHT calculation of widow/widower

• PRs make election within 2 years of second death

NEW NIL RATE BAND PLANNING

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

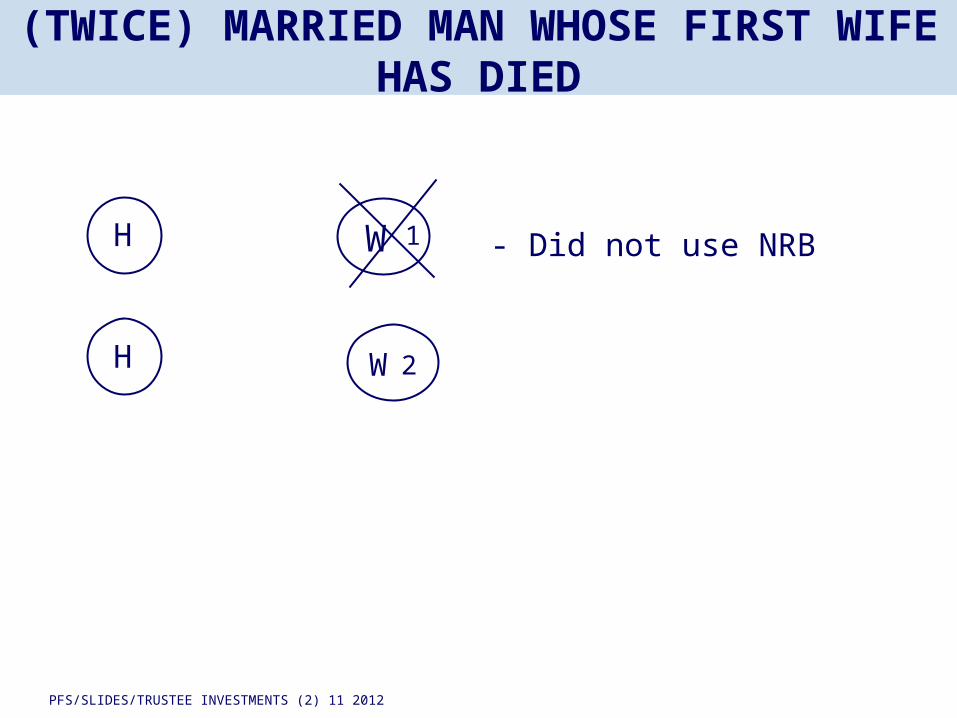

H

(TWICE) MARRIED MAN WHOSE FIRST WIFE HAS DIED

W

2W

1H - Did not use NRB

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

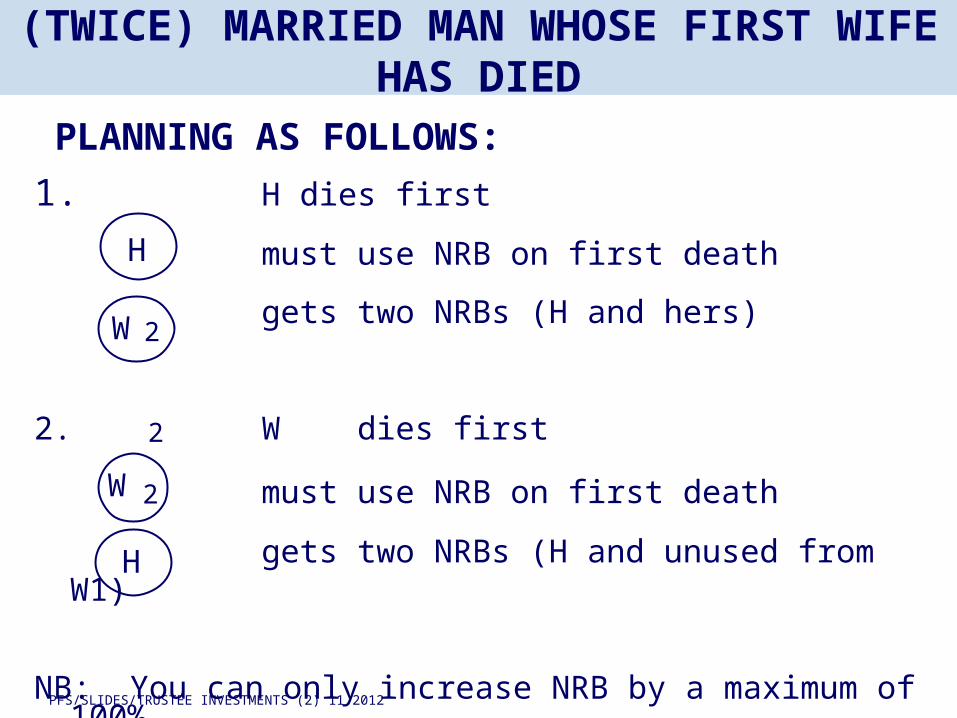

(TWICE) MARRIED MAN WHOSE FIRST WIFE HAS DIED

1. H dies first

must use NRB on first death

gets two NRBs (H and hers)

2. W dies first

must use NRB on first death

gets two NRBs (H and unused from W1)

NB: You can only increase NRB by a maximum of 100%

H

2W

H

W

PLANNING AS FOLLOWS:

2

2

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

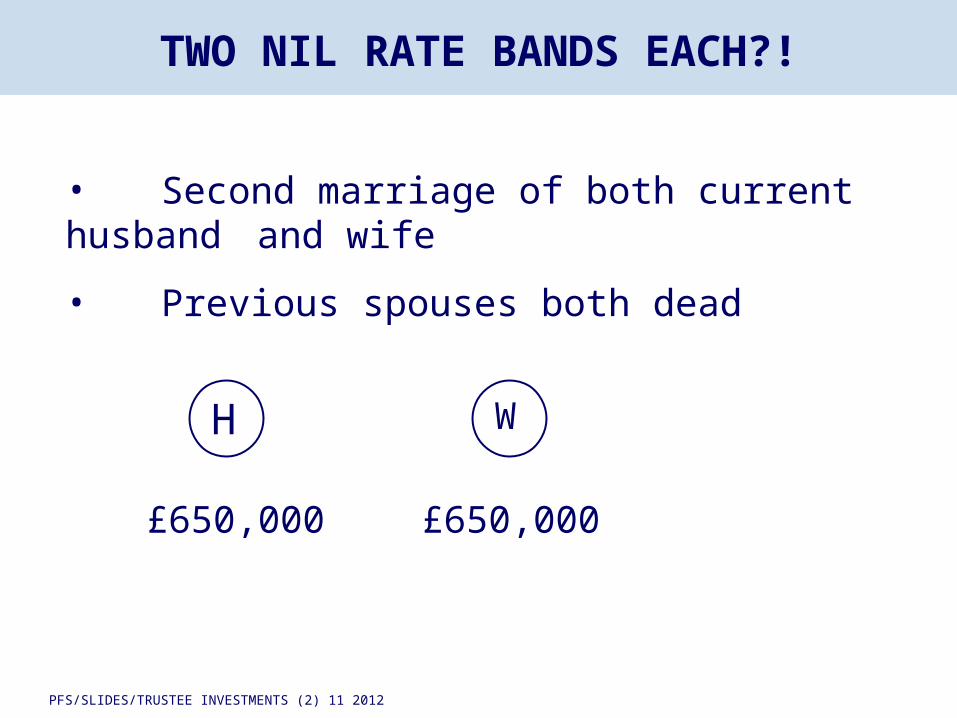

TWO NIL RATE BANDS EACH?!

H W

• Second marriage of both current husband and wife

• Previous spouses both dead

£650,000 £650,000

PFS/SLIDES/TRUSTEE INVESTMENTS 10 2012

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

A TNRB ALTERNATIVE /FORERUNNER

THE DISCRETIONARY WILL TRUST

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

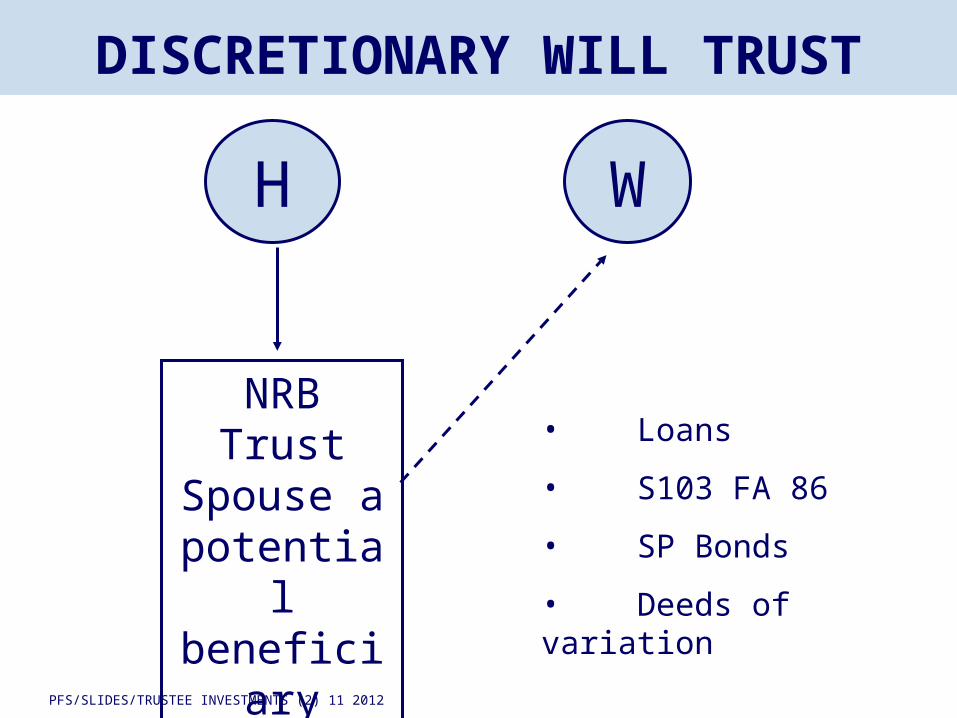

H W

NRB Trust Spouse a potential beneficiar

y

DISCRETIONARY WILL TRUST

• Loans

• S103 FA 86

• SP Bonds

• Deeds of variation

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

H

EXISTING WILL INCLUDES TRUST

Will Trust

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

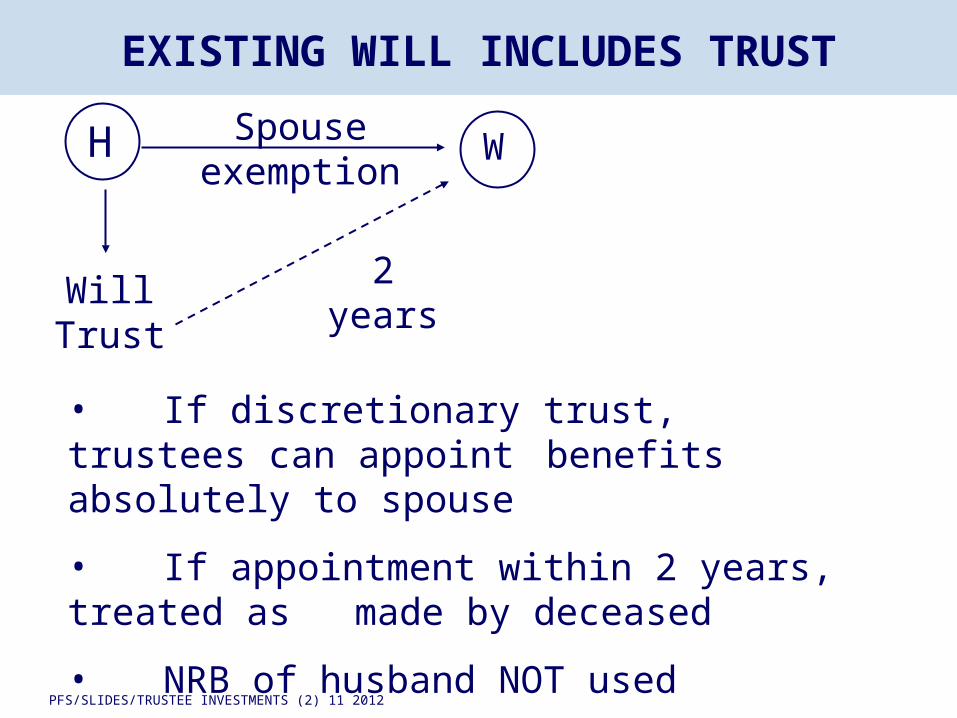

H

EXISTING WILL INCLUDES TRUST

Will Trust

WSpouse exemption

2 years

• If discretionary trust, trustees can appoint benefits absolutely to spouse

• If appointment within 2 years, treated as made by deceased

• NRB of husband NOT used

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

Does the transferable nil rate band make IHT planning on death of the first of a couple

to die unnecessary?

TNRB

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

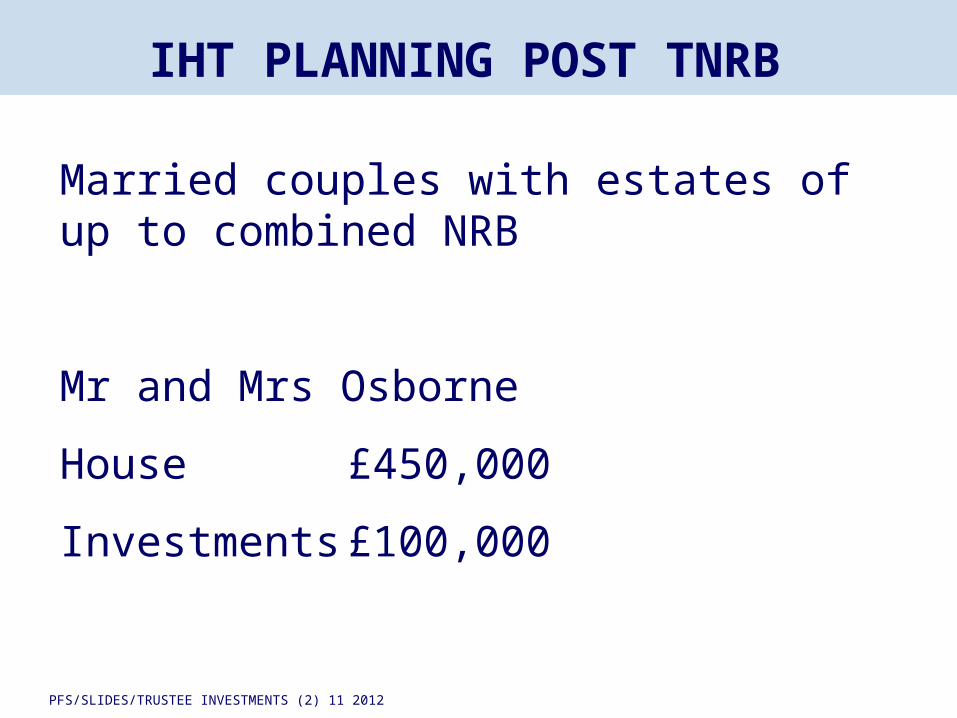

IHT PLANNING POST TNRB

Married couples with estates of up to combined NRB

Mr and Mrs Osborne

House £450,000

Investments £100,000

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

MR AND MRS OSBORNE

• No lifetime planning necessary

• No NRB first death planning generally necessary

UNLESS………………

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

REASONS TO USE NRB ON FIRST DEATH

• Second marriage and different children to benefit from half share on second death

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

REASONS TO USE NRB ON FIRST DEATH

• Second marriage and different children to benefit from half share on second death

• Desire to move assets away from surviving spouse (local authority care charge)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

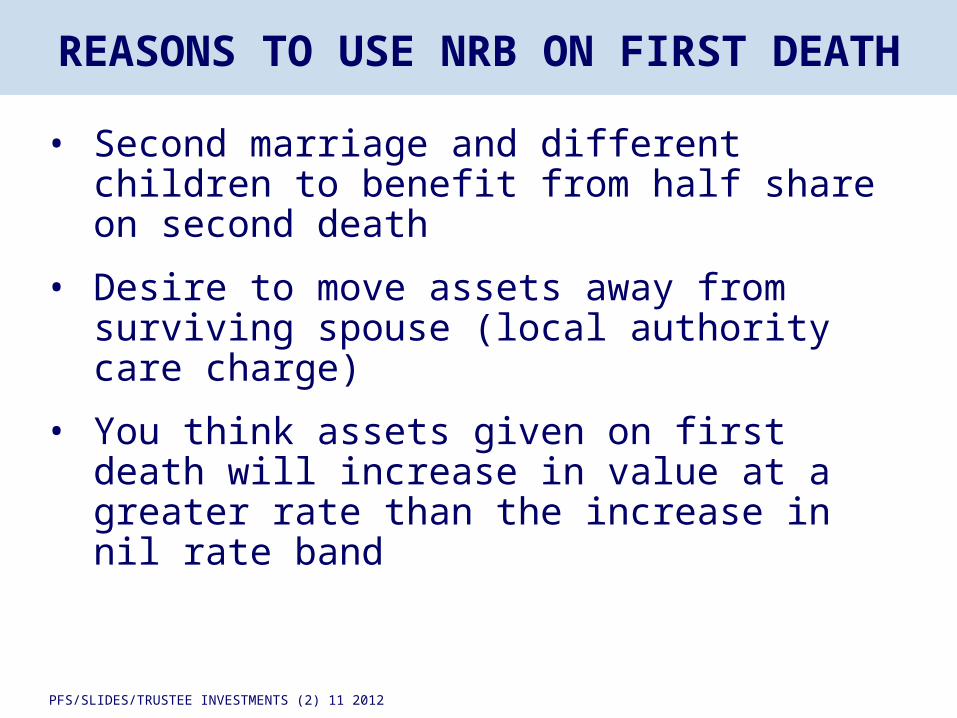

REASONS TO USE NRB ON FIRST DEATH

• Second marriage and different children to benefit from half share on second death

• Desire to move assets away from surviving spouse (local authority care charge)

• You think assets given on first death will increase in value at a greater rate than the increase in nil rate band

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

REASONS TO USE NRB ON FIRST DEATH

• Second marriage and different children to benefit from half share on second death

• Desire to move assets away from surviving spouse (local authority care charge)

• You think assets given on first death will increase in value at a greater rate than the increase in nil rate band

• Divorce /insolvency protection for children

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

REASONS TO USE NRB ON FIRST DEATH

• Second marriage and different children to benefit from half share on second death

• Desire to move assets away from surviving spouse (local authority care charge)

• You think assets given on first death will increase in value at a greater rate than the increase in nil rate band

• Divorce /insolvency protection for children

• You qualify for double NRB despite still being married

PFS/SLIDES/TRUSTEE INVESTMENTS 10 2012

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

• It can be complicated because need to secure survivor’s tenancy but avoid an IIP

• Use IOUs or Charge Scheme

USING MAIN RESIDENCE IN FIRST DEATH PLANNING

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

SPOUSAL PLANNING ON FIRST DEATH; A SUMMARY

• Consider transferable nil rate band first: effective and simple

• Consider alternatives if circumstances dictate

• Remember , first death planning with residential property “fraught”

• The most common objection to using TNRB is lack of control over “asset destination”….there is an answer………

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

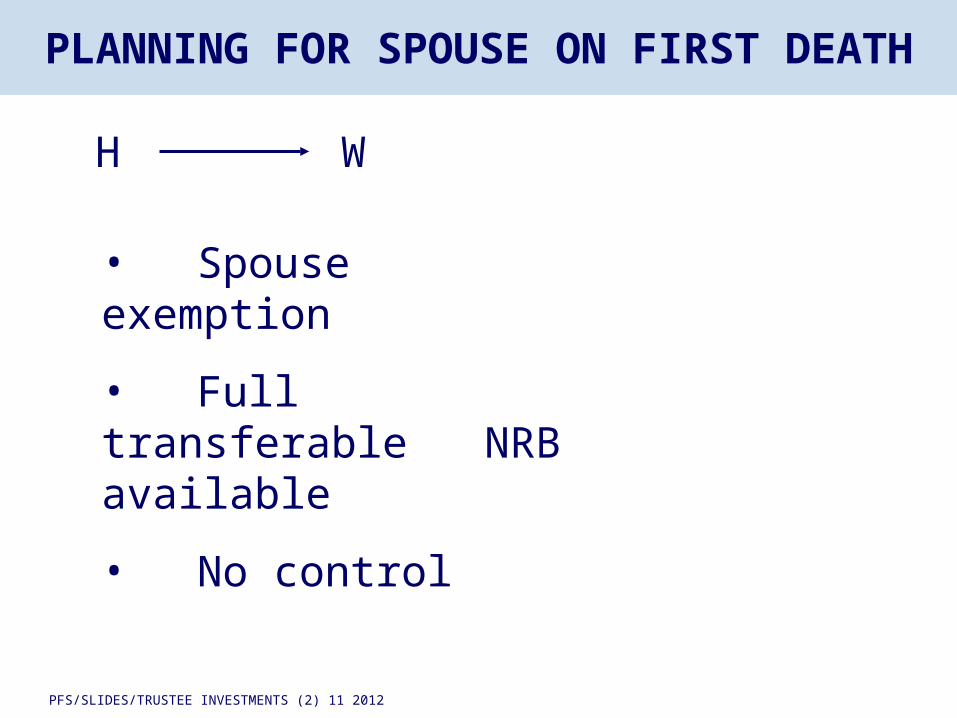

H W

• Spouse exemption

• Full transferable NRB available

• No control

PLANNING FOR SPOUSE ON FIRST DEATH

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

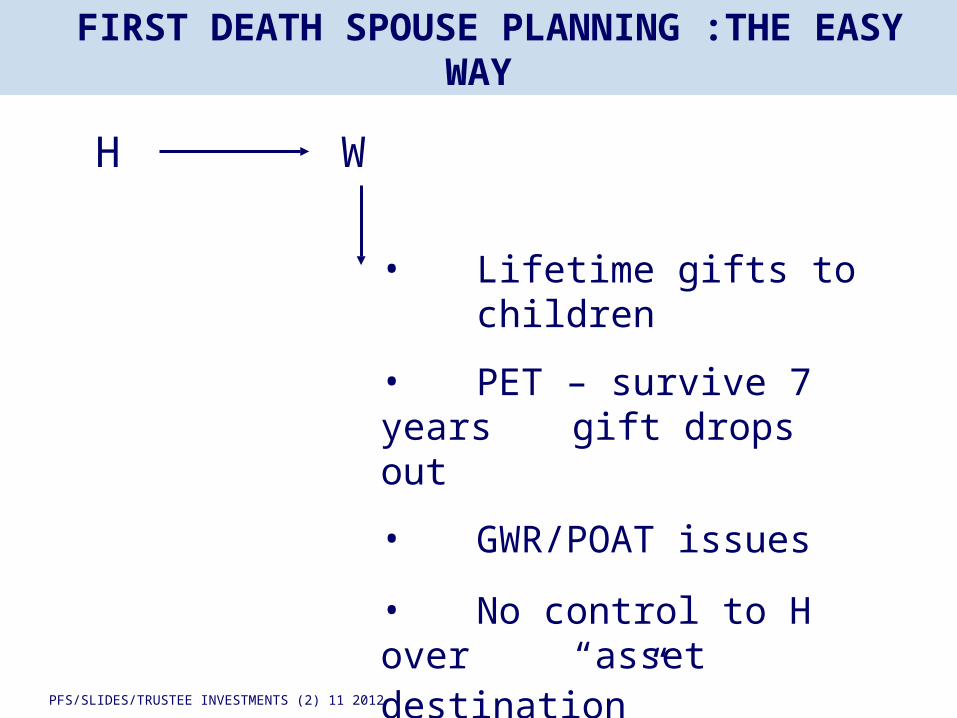

H W

• Lifetime gifts to children

• PET – survive 7 years gift drops out

• GWR/POAT issues

• No control to H over “asset destination”

FIRST DEATH SPOUSE PLANNING :THE EASY WAY

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

• Can you keep control – even after death?

• Yet use the transferable nil rate band?

OVERCOMING THE “NO CONTROL” OBJECTION

THE QUESTION

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

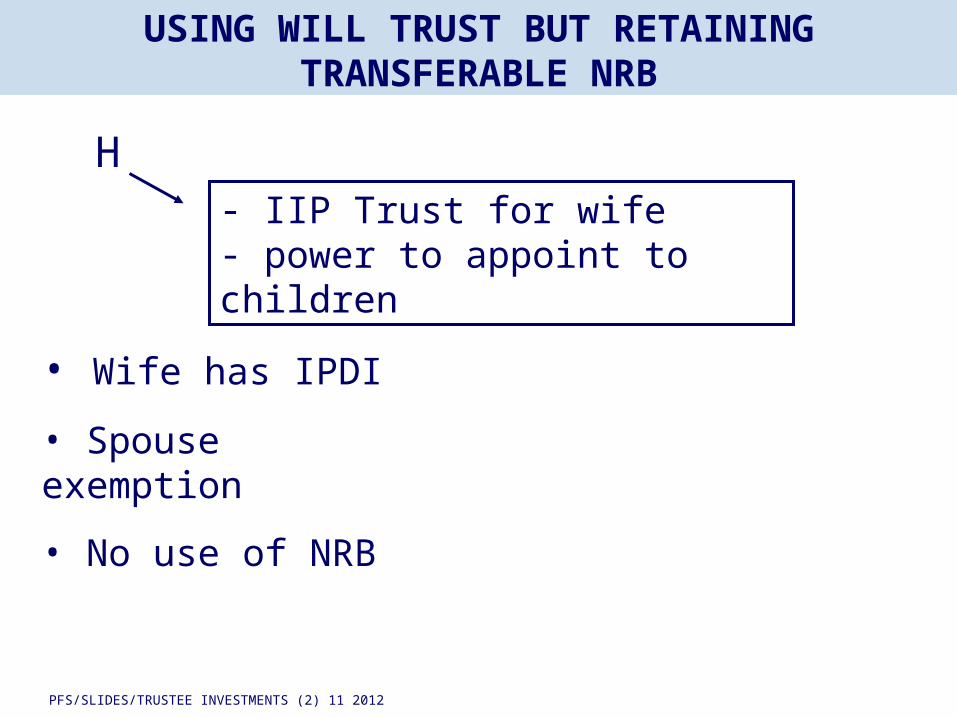

USING WILL TRUST BUT RETAINING TRANSFERABLE NRB

H- IIP Trust for wife- power to appoint to children

• Wife has IPDI

• Spouse exemption

• No use of NRB

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

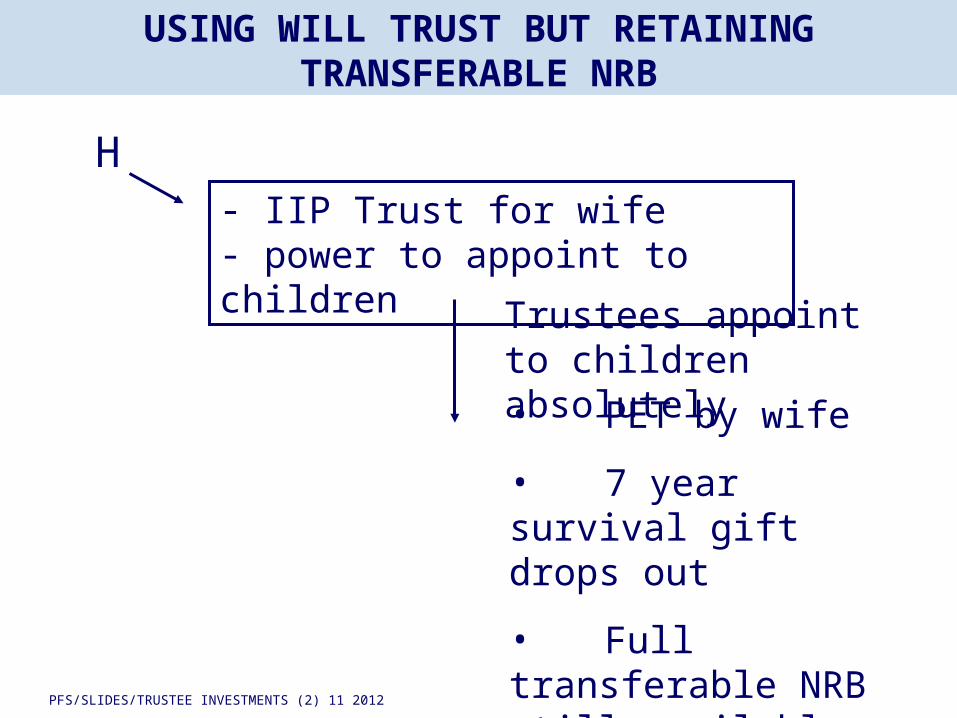

USING WILL TRUST BUT RETAINING TRANSFERABLE NRB

H- IIP Trust for wife- power to appoint to children

Trustees appoint to children absolutely• PET by wife

• 7 year survival gift drops out

• Full transferable NRB still available

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TRUSTEE INVESTMENT ADVICE:A “PERFECT STORM”?

• High degree of difficulty

• Adviser charge justifiable

• Relatively high trustee tax rates

• Trusts are an essential part of estate planning

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TRUSTEE INVESTMENT ADVICE:A “PERFECT STORM”?

• Trustees must take investment advice

• Solicitors and accountants rarely have the necessary financial planning skills

• Strong collaboration potential for advisers

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

LSA2007 : WHAT ARE THE RISKS FOR LAWYERS?

• Impact from greater competition with strong national brands eg. Co-op

• Fall in market share for established legal firms

• Smaller, non-progressive firms may go out of business

• Dual authorisation and complex compliance requirements may make ABSs prohibitive….so…..

• Joint ventures may offer similar benefits within a simpler operating model

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

OPPORTUNITIES FOR FINANCIAL ADVISERS

• Potential to offer legal services or become part of a firm that offers ‘one stop shop’ services

• Collaborations become easier• Scope for increased referrals from a

broader client range• Introduction of Legal Ombudsman

heightens need for trustee investment advice

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

INTRODUCTIONS AND REFERRALS FOR FINANCIAL ADVICE POST-RDR

The new “post RDR” adviser categorisation (Independent /

Restricted) has led professional bodies to review stance on referral

guidelines

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

INTRODUCTIONS AND REFERRALS FROM ACCOUNTANTS

• Institute of Chartered Accountants for England and Wales (ICAEW) will allow accountants to refer to restricted advisers

• Must first make a ‘case-by-case’ assessment of suitability (not necessary for referral to an ‘independent’ adviser)

• Consistent with existing code of ethics

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

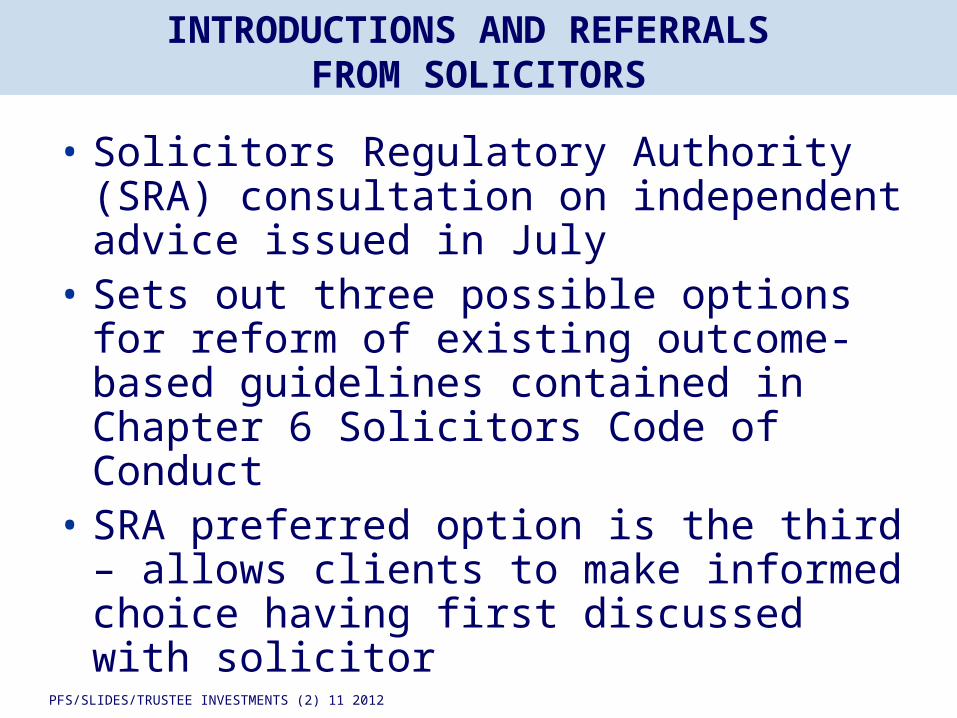

• Solicitors Regulatory Authority (SRA) consultation on independent advice issued in July

• Sets out three possible options for reform of existing outcome-based guidelines contained in Chapter 6 Solicitors Code of Conduct

• SRA preferred option is the third – allows clients to make informed choice having first discussed with solicitor

INTRODUCTIONS AND REFERRALS FROM SOLICITORS

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

ADVISER CHARGING AND TRUSTS

A FEW THOUGHTS ON THE POTENTIAL TAXATION IMPLICATIONS IN RELATION TO ADVISER CHARGING ON PRODUCTS

IN TRUST

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

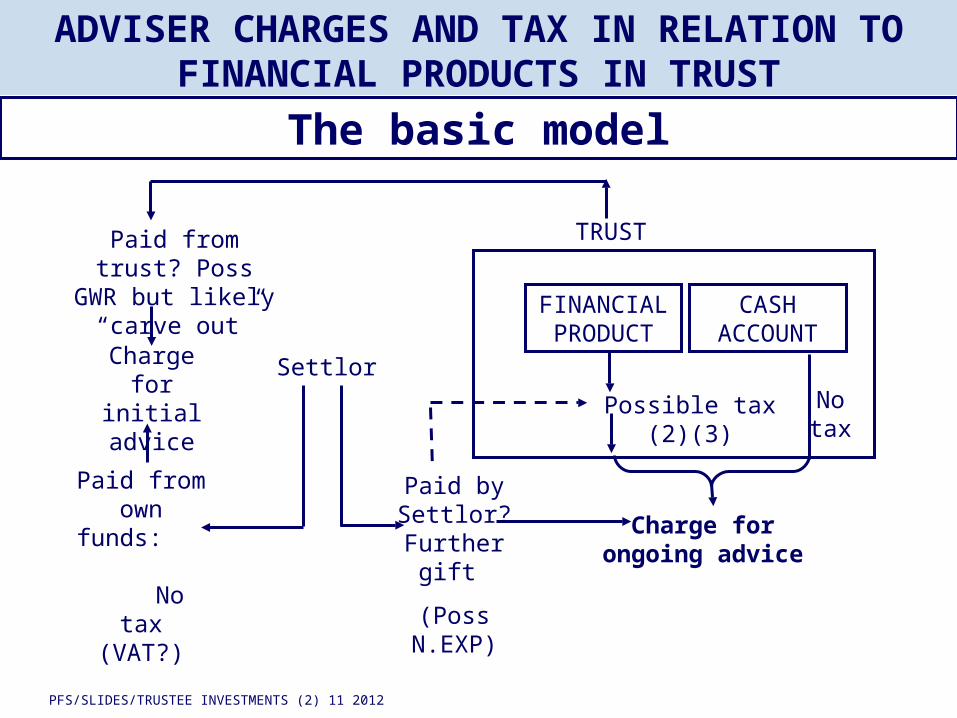

ADVISER CHARGES AND TAX IN RELATION TO FINANCIAL PRODUCTS IN TRUST

The basic model

Paid from trust? Poss GWR but likely “carve

out”Charge

for initial advice

Paid from own funds:

No tax (VAT?)

Paid by Settlor?

Further gift

(Poss N.EXP)

Charge for ongoing advice

TRUST

FINANCIAL PRODUCT

CASH ACCOUNT

Possible tax (2)(3)

SettlorNo tax

PFS/SLIDES/TRUSTEE INVESTMENTS 10 2012

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TRUSTEE INVESTMENT:CASE STUDY

PUTTING IT INTO PRACTICE:

APPLIED EXPERTISE

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

BARRY’S WILL TRUSTS

• Died on 17 May 2005

• 2 years prior to death gifted £20,000 to each of his four grandchildren

• Left

- a widow- two children- four grandchildren

- two great grandchildren

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

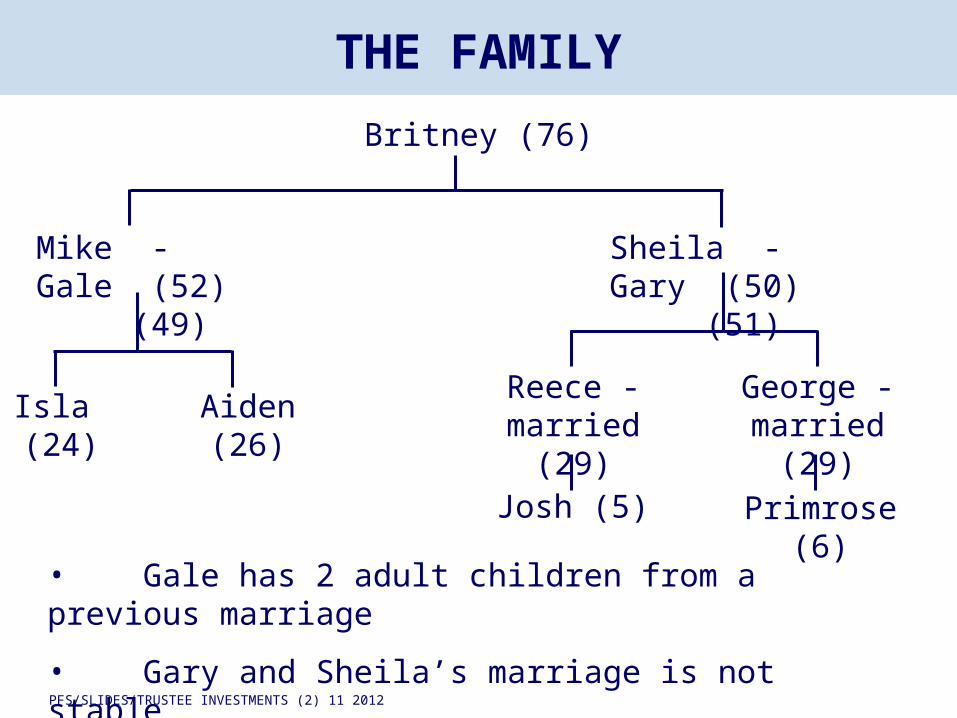

THE FAMILY

Britney (76)

Mike - Gale (52) (49)

Isla (24)

Aiden (26)Reece -

married (29)George -

married (29)

Josh (5) Primrose (6)

• Gale has 2 adult children from a previous marriage

• Gary and Sheila’s marriage is not stable

Sheila - Gary (50) (51)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

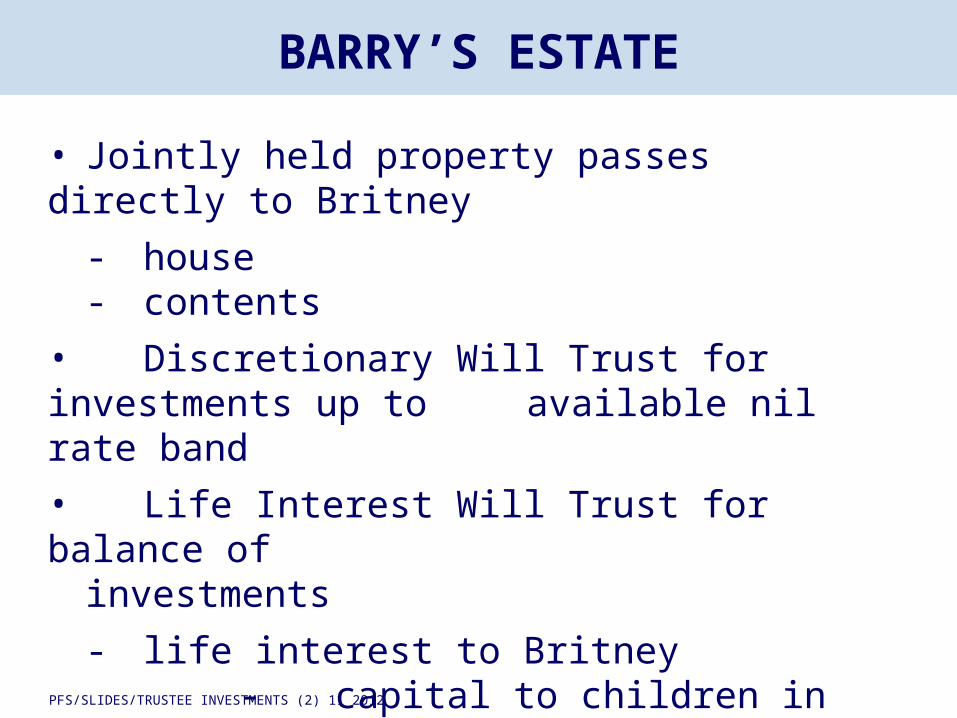

BARRY’S ESTATE

• Jointly held property passes directly to Britney

- house- contents

• Discretionary Will Trust for investments up to available nil rate band

• Life Interest Will Trust for balance ofinvestments

- life interest to Britney- capital to children in equal shares

on Britney’s death

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

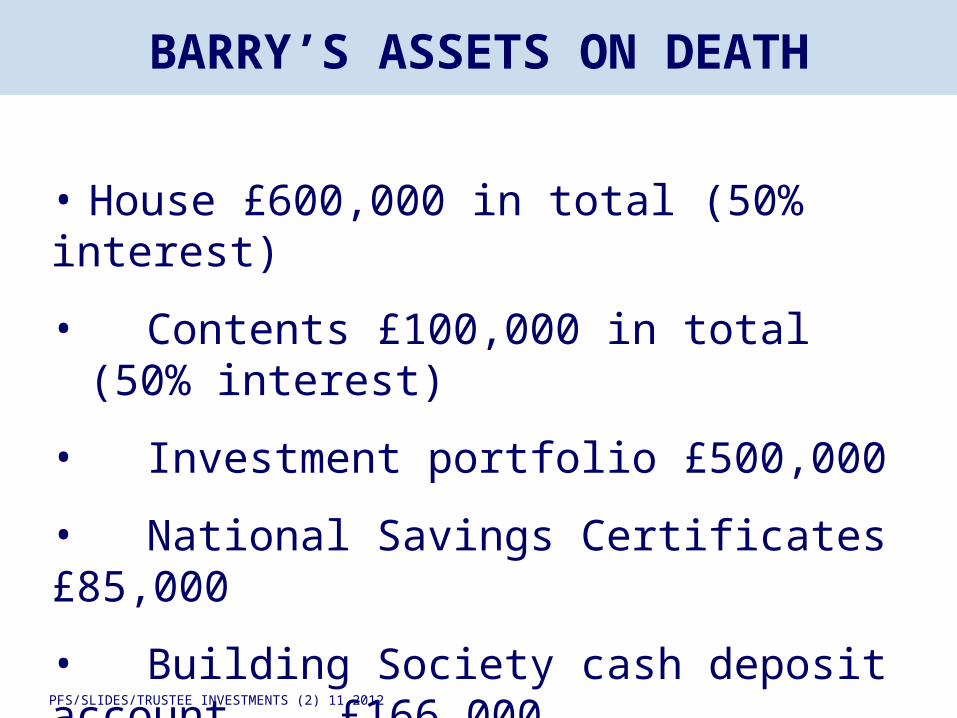

BARRY’S ASSETS ON DEATH

• House £600,000 in total (50% interest)

• Contents £100,000 in total(50% interest)

• Investment portfolio £500,000

• National Savings Certificates £85,000

• Building Society cash deposit account £166,000

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

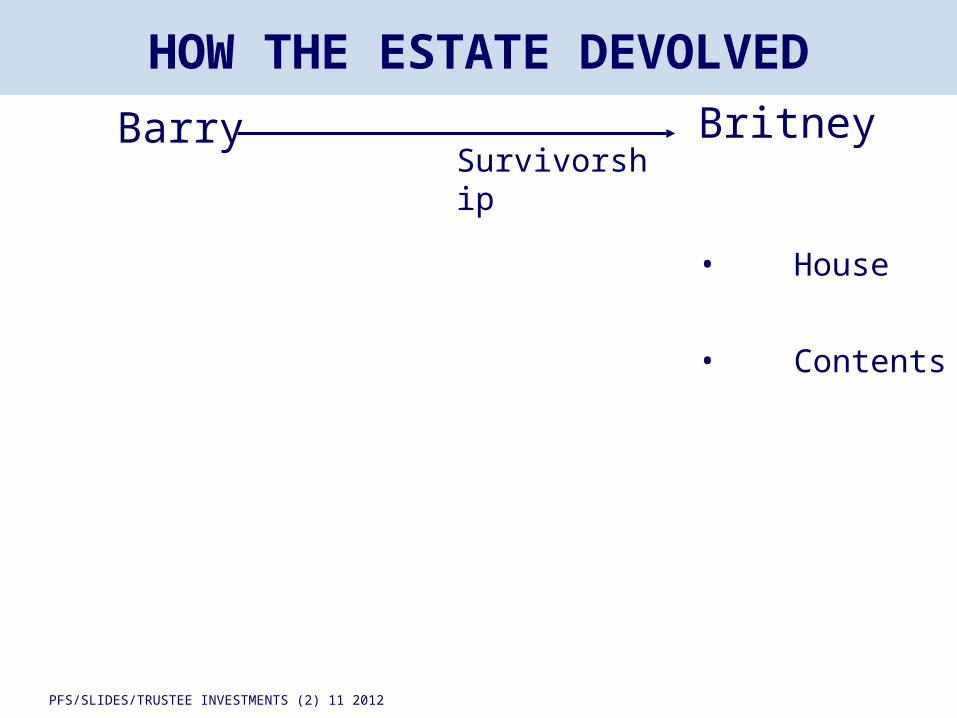

HOW THE ESTATE DEVOLVED

Barry Britney

• House

• Contents

Survivorship

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

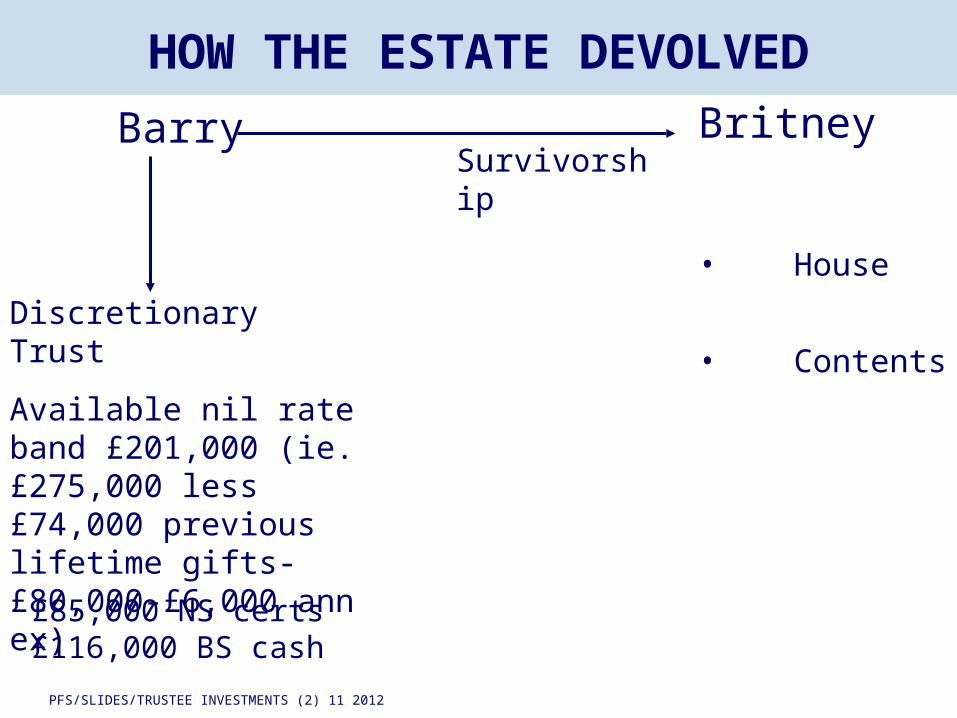

HOW THE ESTATE DEVOLVED

Barry

Discretionary Trust

Available nil rate band £201,000 (ie. £275,000 less £74,000 previous lifetime gifts-£80,000-£6,000 ann ex)

Britney

• House

• Contents

Survivorship

£85,000 NS certs £116,000 BS cash

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

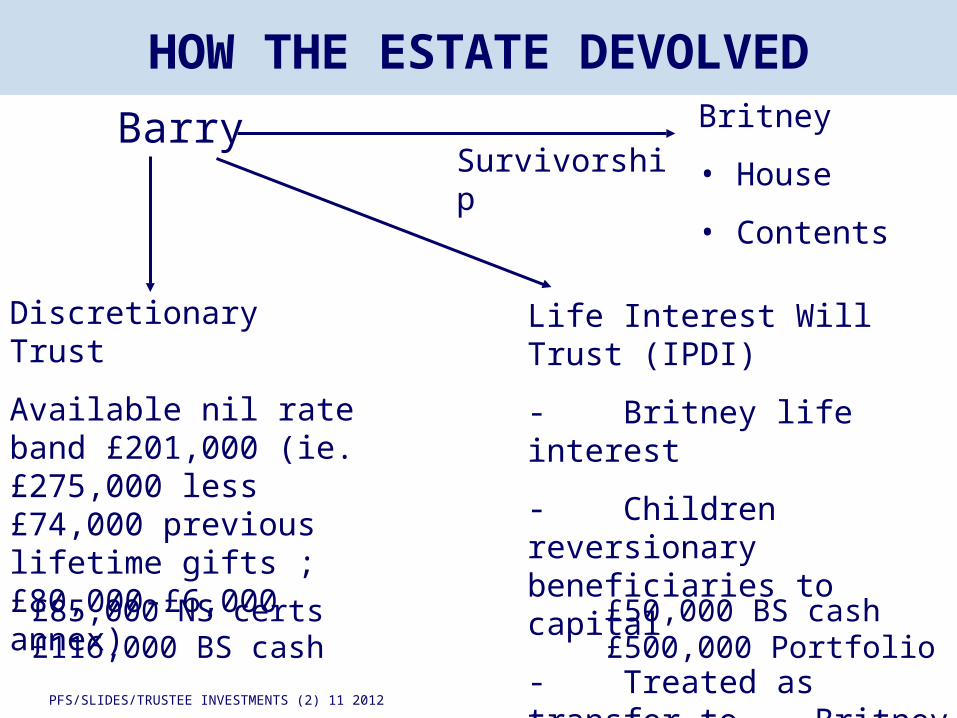

HOW THE ESTATE DEVOLVED

Barry

Discretionary Trust

Available nil rate band £201,000 (ie. £275,000 less £74,000 previous lifetime gifts ;£80,000-£6,000 annex)

Life Interest Will Trust (IPDI)

- Britney life interest

- Children reversionary beneficiaries to

capital

- Treated as transfer to Britney for IHT

Britney

• House

• Contents

Survivorship

£85,000 NS certs £50,000 BS cash £116,000 BS cash £500,000 Portfolio

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

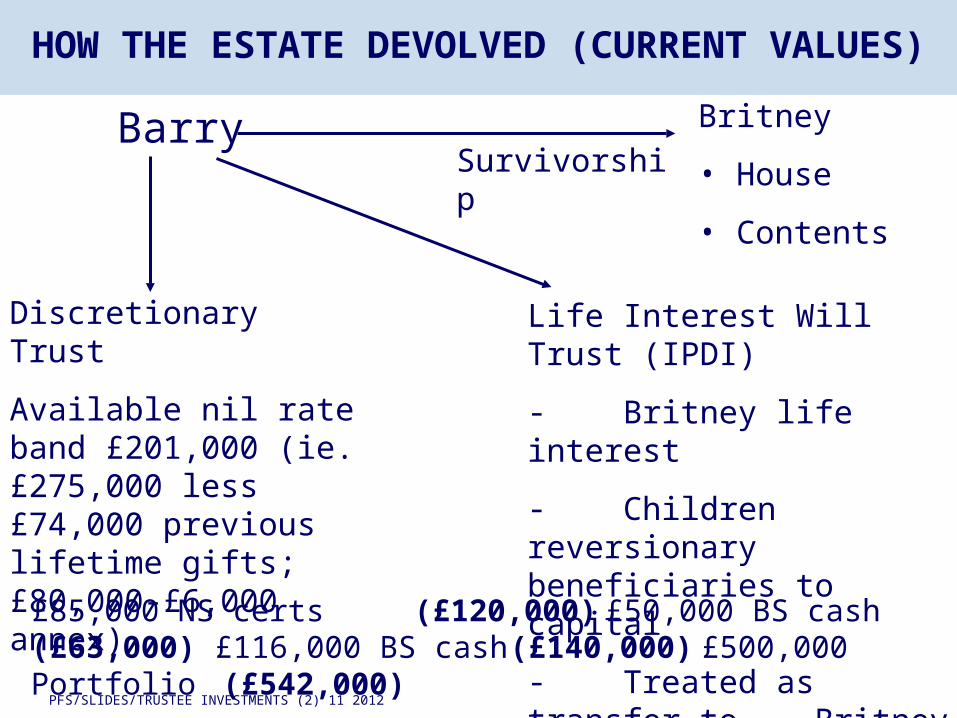

HOW THE ESTATE DEVOLVED (CURRENT VALUES)

Barry

Discretionary Trust

Available nil rate band £201,000 (ie. £275,000 less £74,000 previous lifetime gifts; £80,000-£6,000 annex)

Life Interest Will Trust (IPDI)

- Britney life interest

- Children reversionary beneficiaries to

capital

- Treated as transfer to Britney for IHT

Britney

• House

• Contents

Survivorship

£85,000 NS certs (£120,000)£50,000 BS cash(£63,000) £116,000 BS cash (£140,000)£500,000 Portfolio (£542,000)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

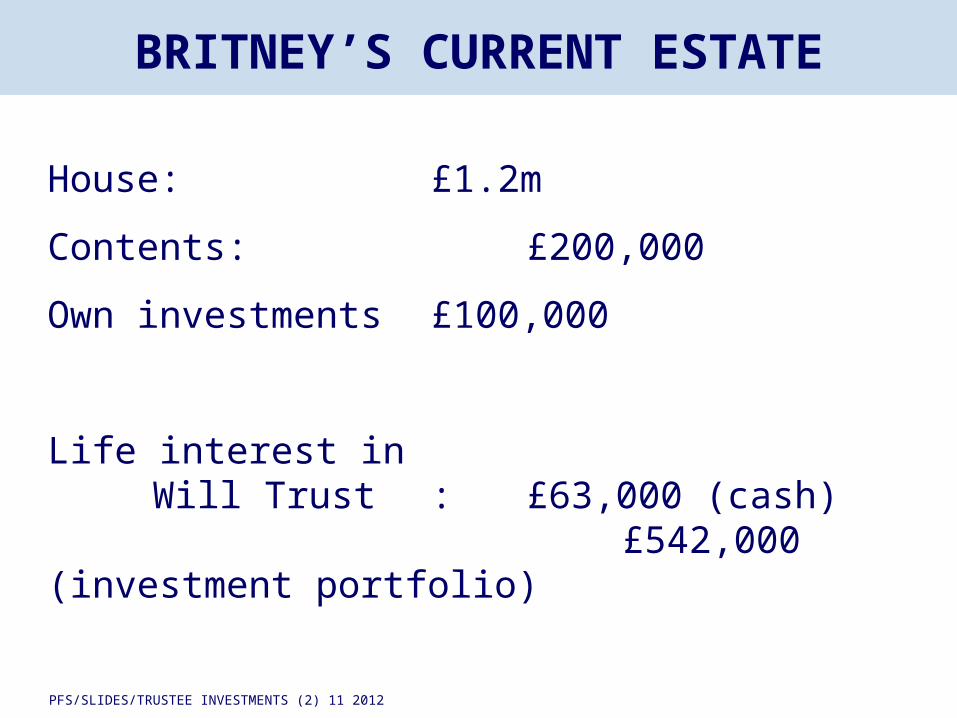

BRITNEY’S CURRENT ESTATE

House: £1.2m

Contents: £200,000

Own investments £100,000

Life interest in Will Trust : £63,000 (cash)

£542,000 (investment portfolio)

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

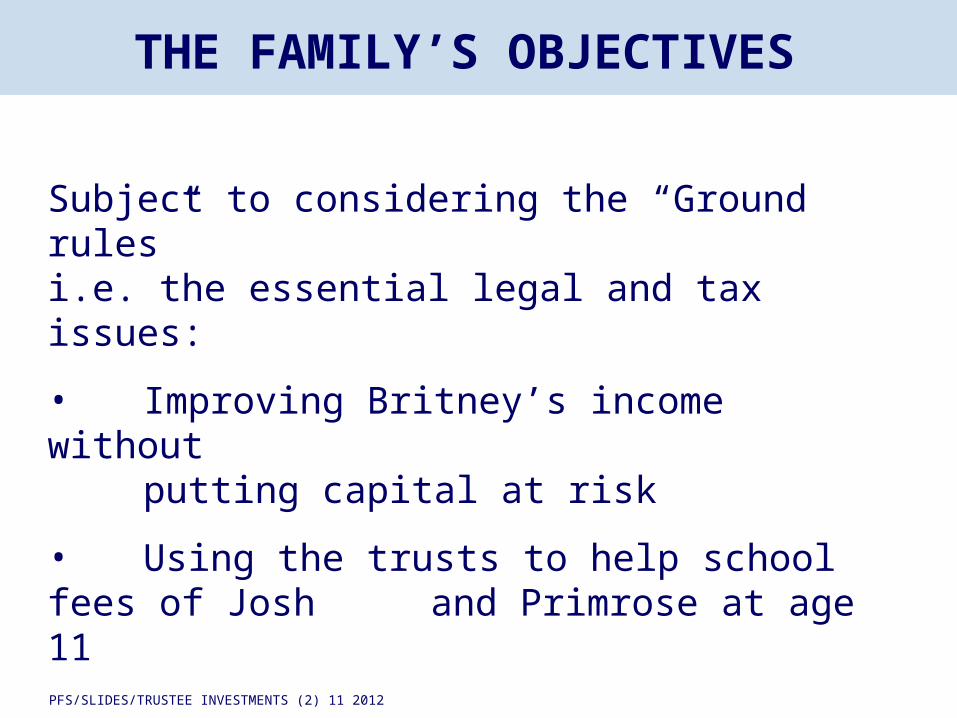

THE FAMILY’S OBJECTIVES

Subject to considering the “Ground rules”i.e. the essential legal and tax issues:

• Improving Britney’s income withoutputting capital at risk

• Using the trusts to help school fees of Josh and Primrose at age 11

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

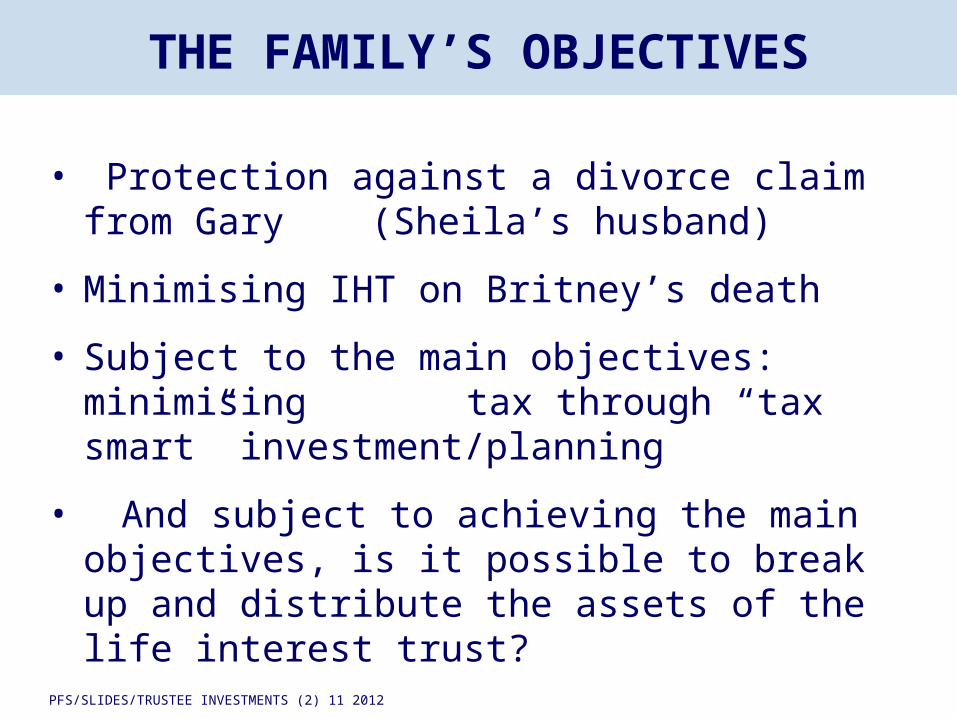

THE FAMILY’S OBJECTIVES

• Protection against a divorce claim from Gary (Sheila’s husband)

• Minimising IHT on Britney’s death

• Subject to the main objectives: minimising tax through “tax smart”

investment/planning

• And subject to achieving the main objectives, is it possible to break up and distribute the assets of the life interest trust?

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

MEETING OBJECTIVES

1. IMPORTANT AND LEGAL TAX ISSUES

Legal issues:

• Powers of investment? Wide

• Invest for the benefit of all beneficiaries

- discretionary trust- life interest trust

• SIC

- diversification- suitability- advice

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

MEETING OBJECTIVES

1. IMPORTANT AND LEGAL TAX ISSUES

Tax fundamentals:

Discretionary trust

- 50%/42.5% income tax - CGT annual exemption

(reduced) - then 28% CGT

IIP Trust:

- Income taxed on Britney - CGT annual exemption (reduced)

then 28% CGT

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

MEETING OBJECTIVES

In determining the strategy keep in mind:

• There are two trusts

• Desire not to put capital at risk

• Tax saving can deliver “Alpha”

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

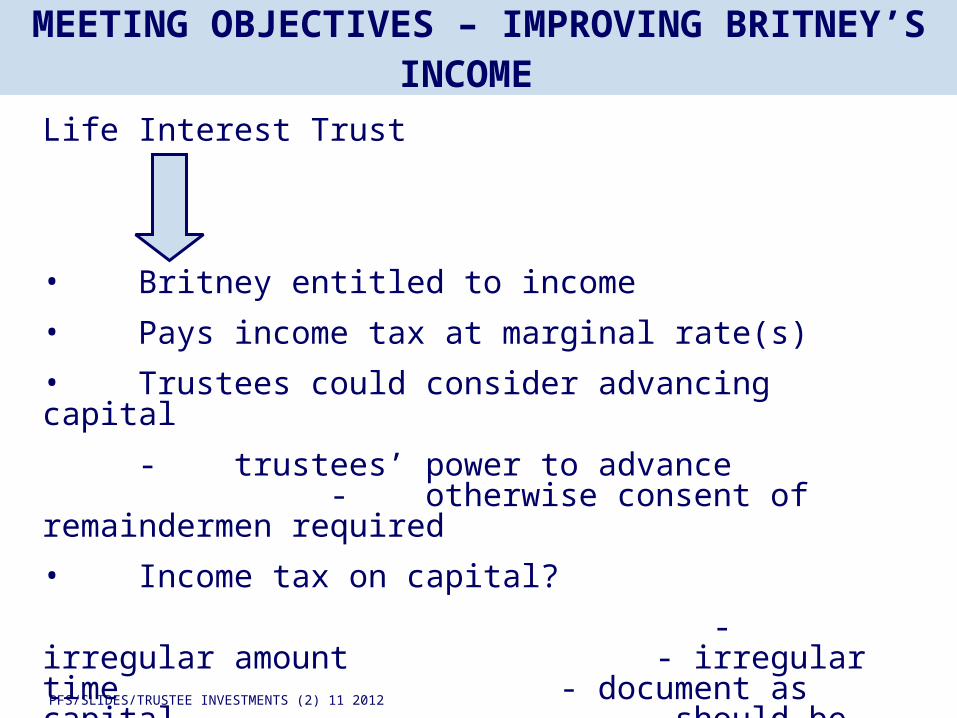

MEETING OBJECTIVES – IMPROVING BRITNEY’S INCOME

Life Interest Trust

• Britney entitled to income

• Pays income tax at marginal rate(s)

• Trustees could consider advancing capital

- trustees’ power to advance- otherwise consent of

remaindermen required

• Income tax on capital?

- irregular amount - irregular time -

document as capital - should be taxed as capital

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

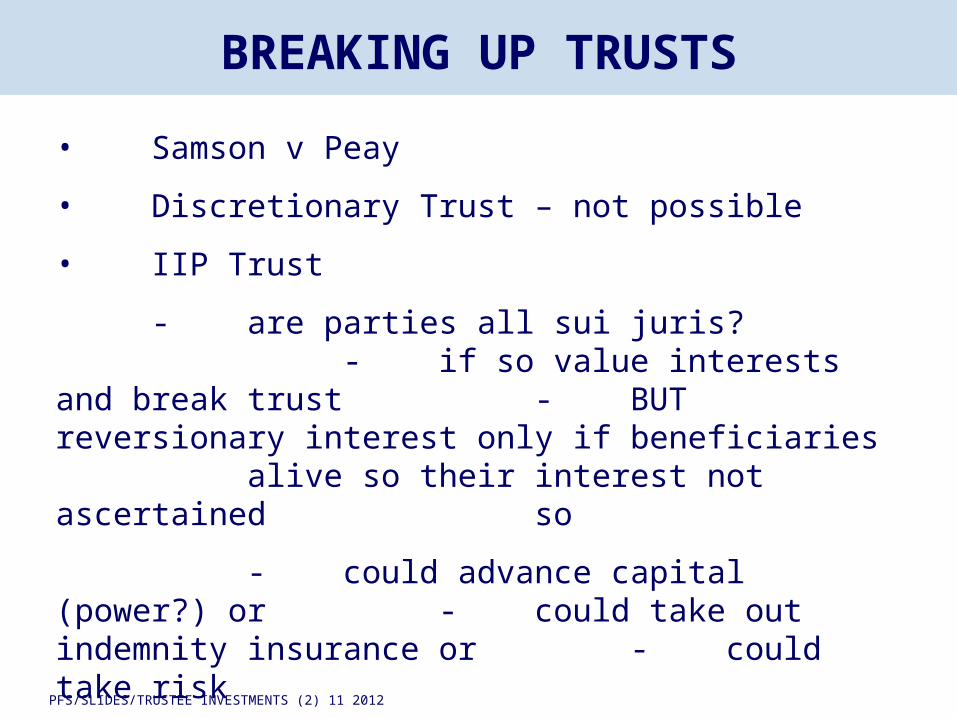

BREAKING UP TRUSTS

• Samson v Peay

• Discretionary Trust – not possible

• IIP Trust

- are parties all sui juris?- if so value interests and break trust- BUT reversionary interest only if

beneficiaries alive so their interest not ascertained so

- could advance capital (power?) or- could take out indemnity

insurance or - could take risk

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

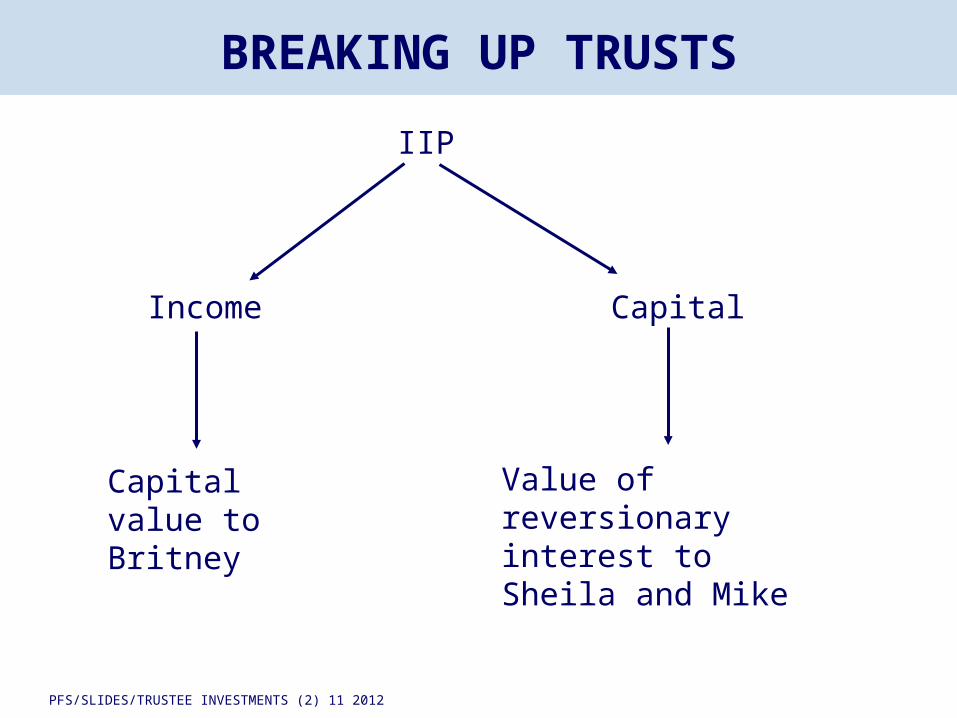

BREAKING UP TRUSTS

IIP

Income Capital

Capital value to Britney

Value of reversionary interest to Sheila and Mike

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

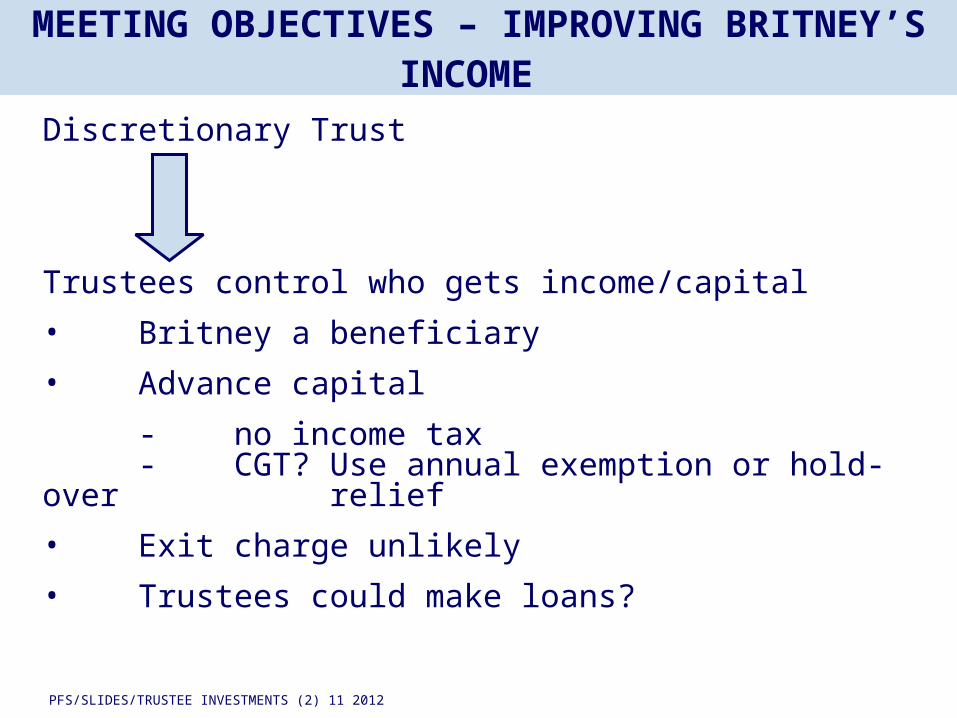

MEETING OBJECTIVES – IMPROVING BRITNEY’S INCOME

Discretionary Trust

Trustees control who gets income/capital

• Britney a beneficiary

• Advance capital

- no income tax- CGT? Use annual exemption or hold-

over relief

• Exit charge unlikely

• Trustees could make loans?

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

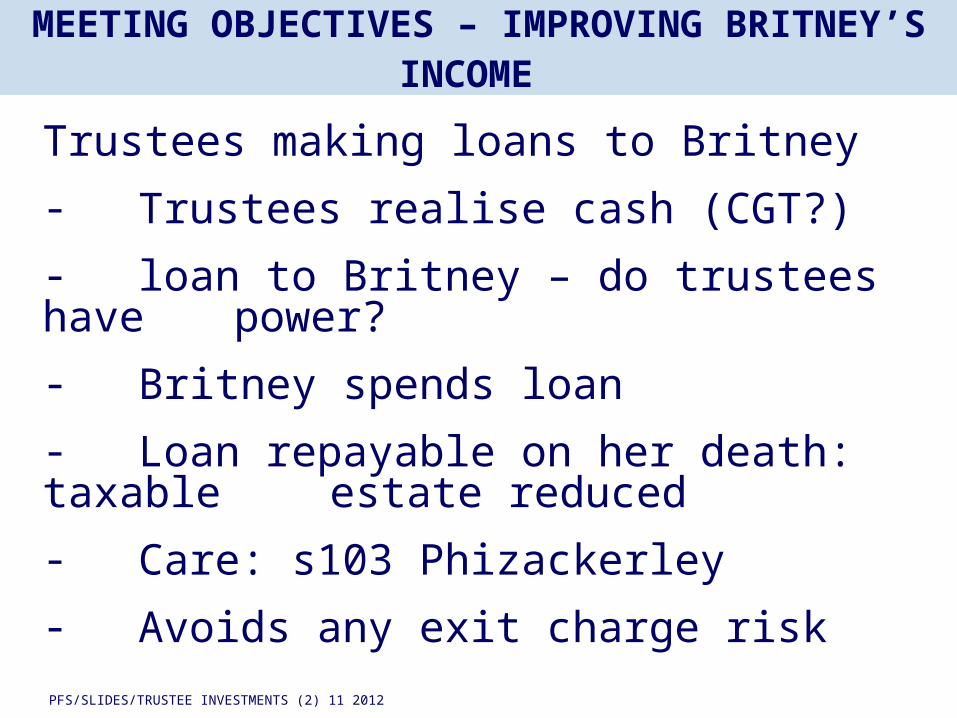

MEETING OBJECTIVES – IMPROVING BRITNEY’S INCOME

Trustees making loans to Britney

- Trustees realise cash (CGT?)

- loan to Britney – do trustees have power?

- Britney spends loan

- Loan repayable on her death: taxable estate reduced

- Care: s103 Phizackerley

- Avoids any exit charge risk

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

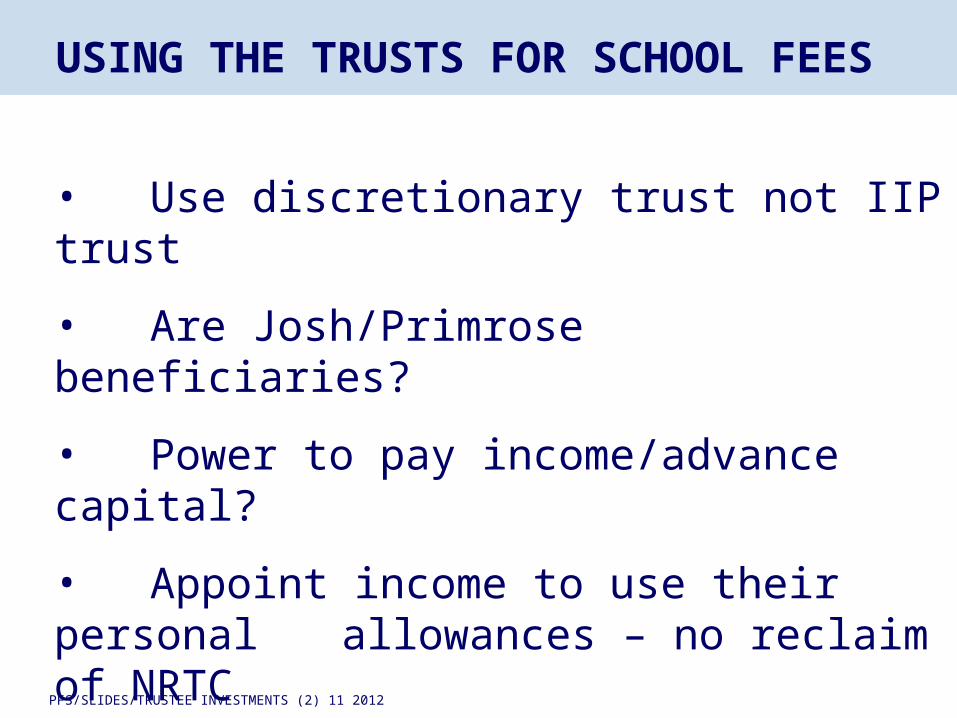

USING THE TRUSTS FOR SCHOOL FEES

• Use discretionary trust not IIP trust

• Are Josh/Primrose beneficiaries?

• Power to pay income/advance capital?

• Appoint income to use their personal allowances – no reclaim of NRTC

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

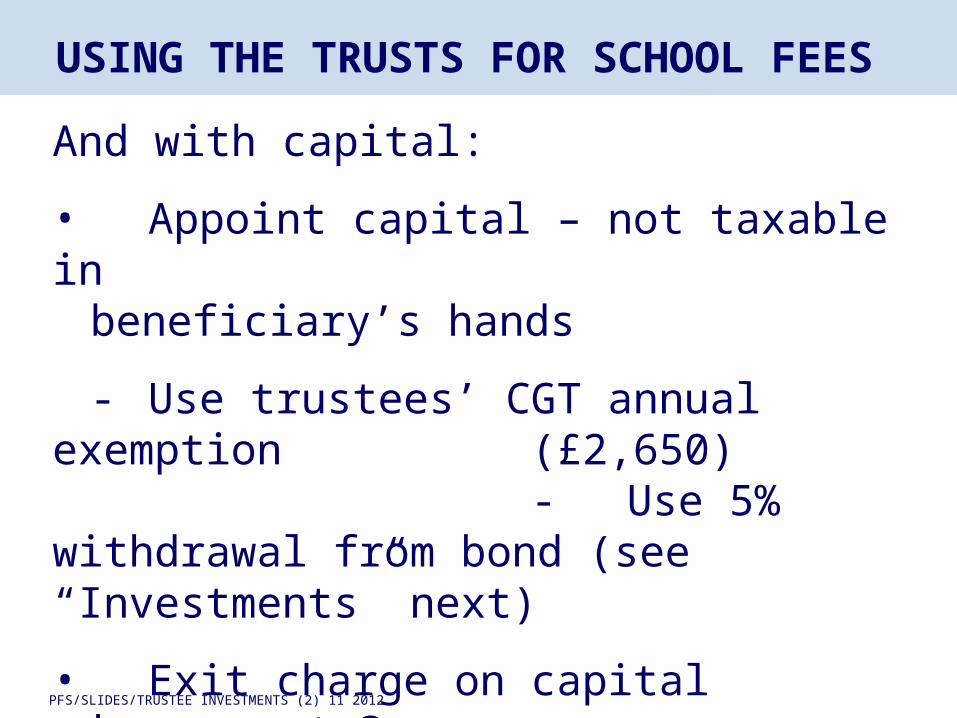

USING THE TRUSTS FOR SCHOOL FEES

And with capital:

• Appoint capital – not taxable inbeneficiary’s hands

- Use trustees’ CGT annual exemption (£2,650)

- Use 5% withdrawal from bond (see “Investments” next)

• Exit charge on capital advancement ?

IHT charge unlikely

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

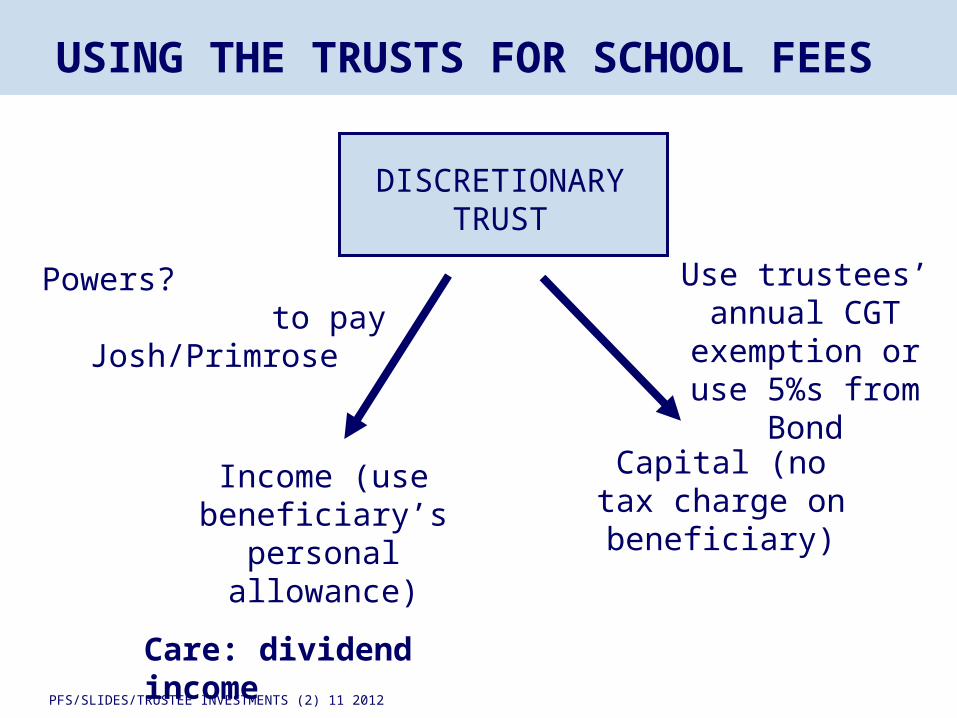

USING THE TRUSTS FOR SCHOOL FEES

DISCRETIONARY TRUST

Income (use beneficiary’s personal

allowance)

Care: dividend income

Capital (no tax charge on

beneficiary)

Use trustees’ annual CGT

exemption or use 5%s from

Bond

Powers? to pay Josh/Primrose

PFS/SLIDES/TRUSTEE INVESTMENTS 10 2012

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

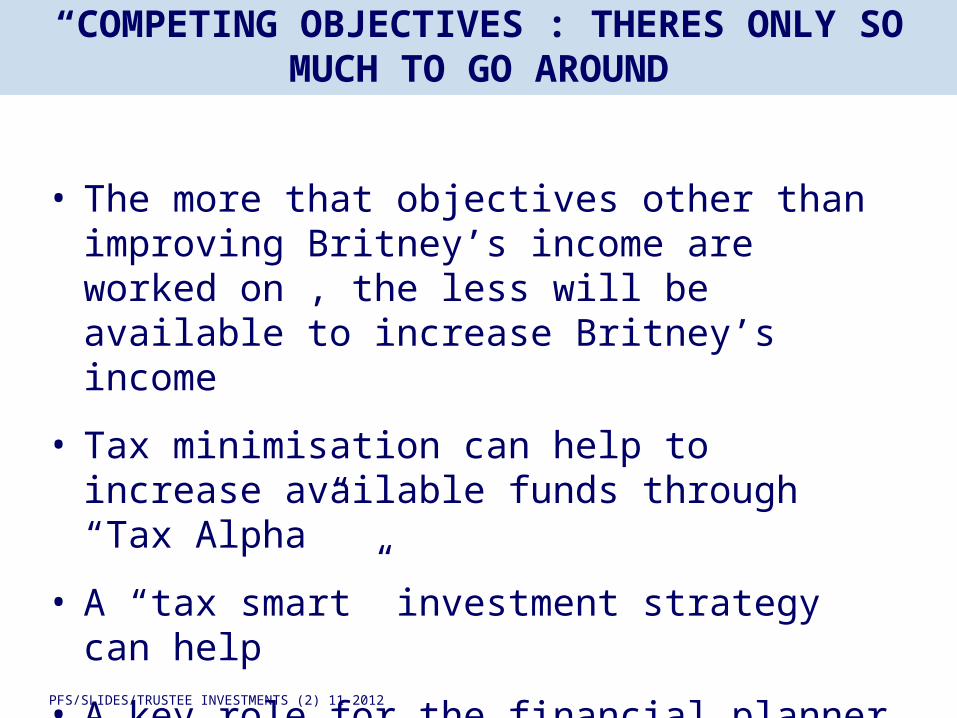

“COMPETING OBJECTIVES”: THERES ONLY SO MUCH TO GO AROUND

• The more that objectives other than improving Britney’s income are worked on , the less will be available to increase Britney’s income

• Tax minimisation can help to increase available funds through “Tax Alpha”

• A “tax smart” investment strategy can help

• A key role for the financial planner

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

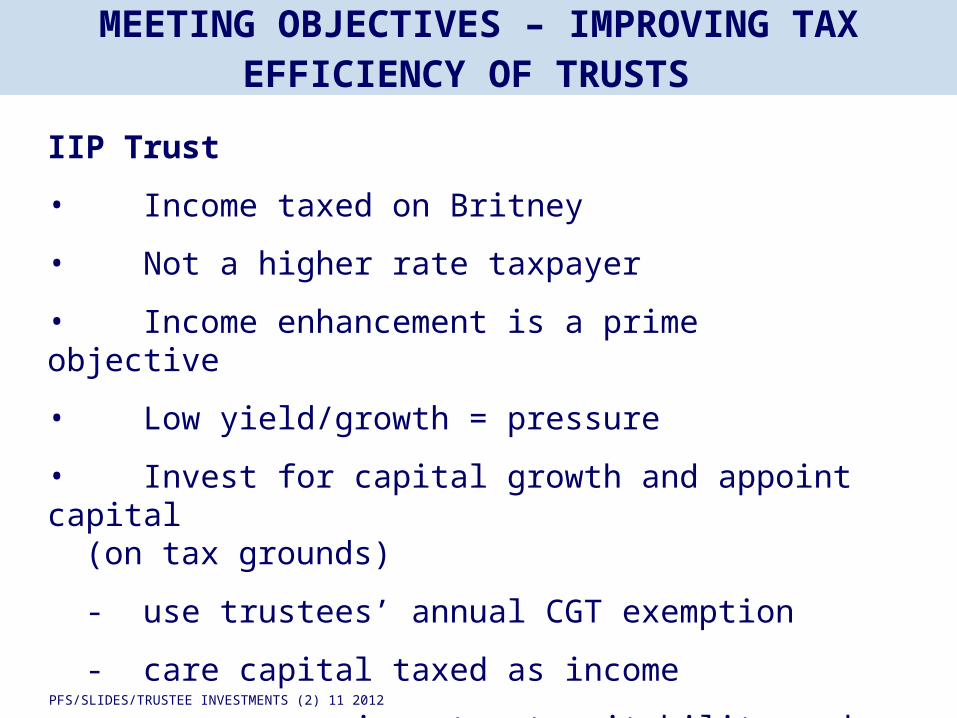

MEETING OBJECTIVES – IMPROVING TAX EFFICIENCY OF TRUSTS

IIP Trust

• Income taxed on Britney

• Not a higher rate taxpayer

• Income enhancement is a prime objective

• Low yield/growth = pressure

• Invest for capital growth and appoint capital(on tax grounds)

- use trustees’ annual CGT exemption

- care capital taxed as income

- care investment suitability and investment risk

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

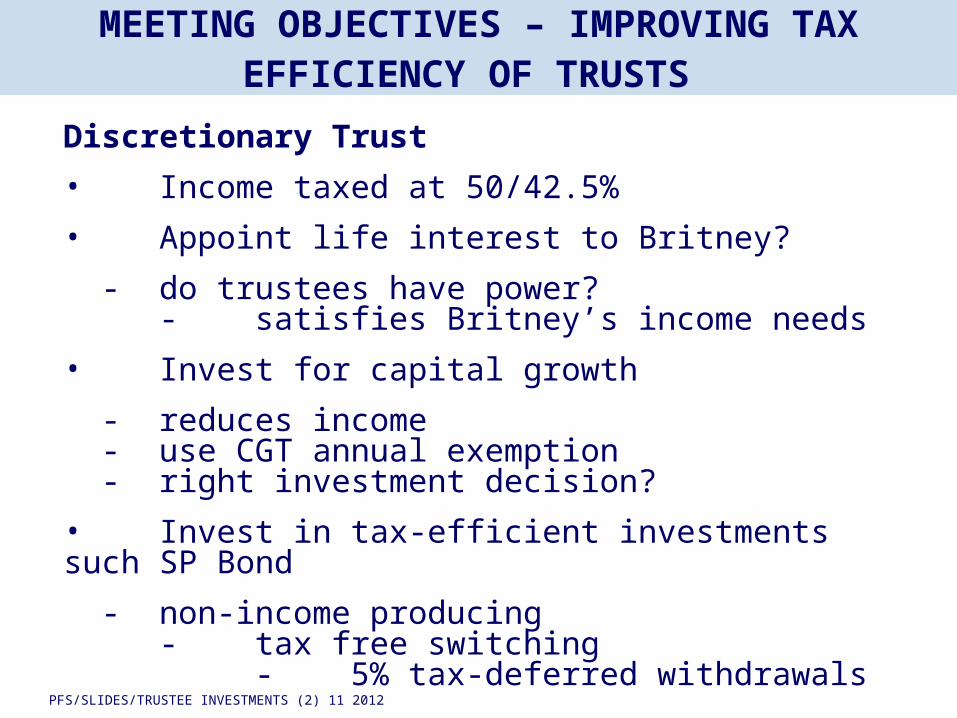

MEETING OBJECTIVES – IMPROVING TAX EFFICIENCY OF TRUSTS

Discretionary Trust

• Income taxed at 50/42.5%

• Appoint life interest to Britney?

- do trustees have power?- satisfies Britney’s income needs

• Invest for capital growth

- reduces income- use CGT annual exemption- right investment decision?

• Invest in tax-efficient investments such SP Bond

- non-income producing- tax free switching- 5% tax-deferred withdrawals

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

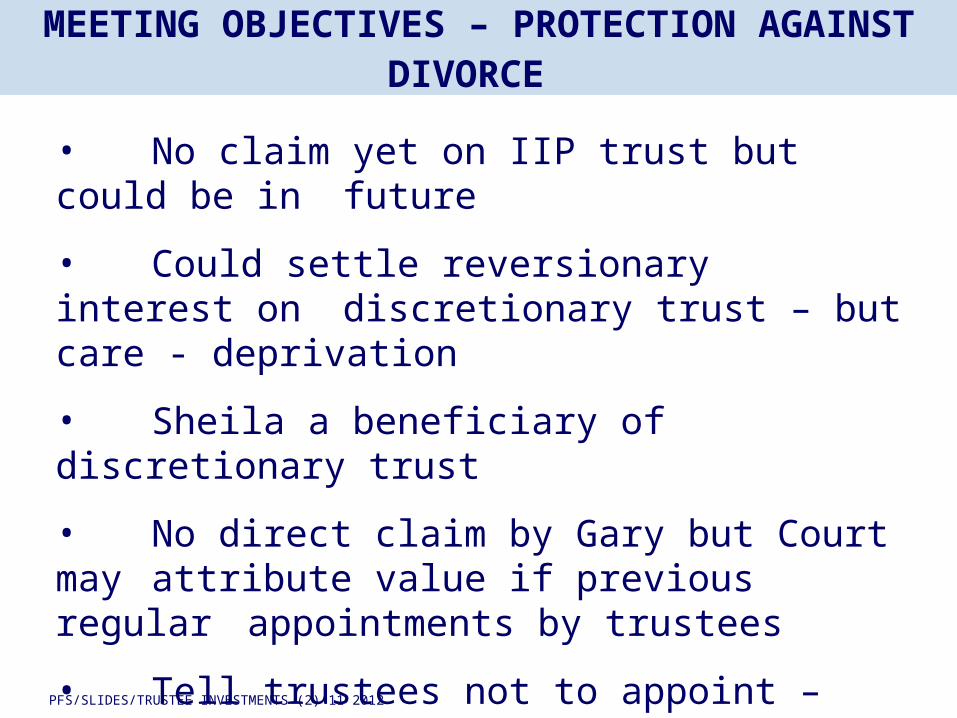

MEETING OBJECTIVES – PROTECTION AGAINST DIVORCE

• No claim yet on IIP trust but could be in future

• Could settle reversionary interest on discretionary trust – but care -

deprivation

• Sheila a beneficiary of discretionary trust

• No direct claim by Gary but Court may attribute value if previous regular

appointments by trustees

• Tell trustees not to appoint – perhapsappoint to children instead of to Sheila

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

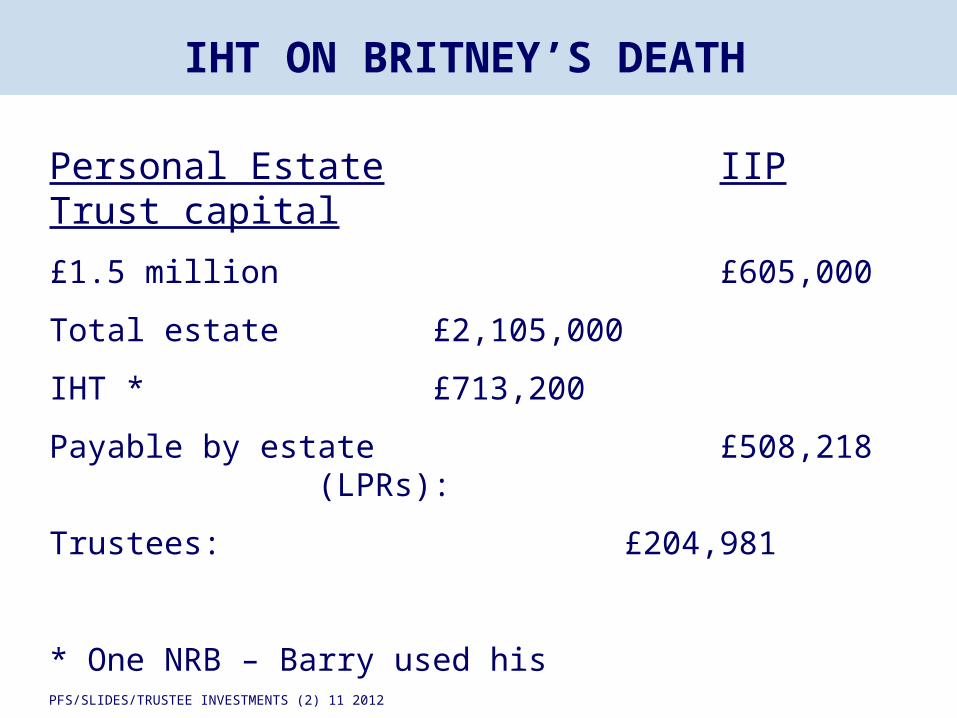

IHT ON BRITNEY’S DEATH

Personal Estate IIP Trust capital

£1.5 million £605,000

Total estate £2,105,000

IHT * £713,200

Payable by estate £508,218 (LPRs):

Trustees: £204,981

* One NRB – Barry used his

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

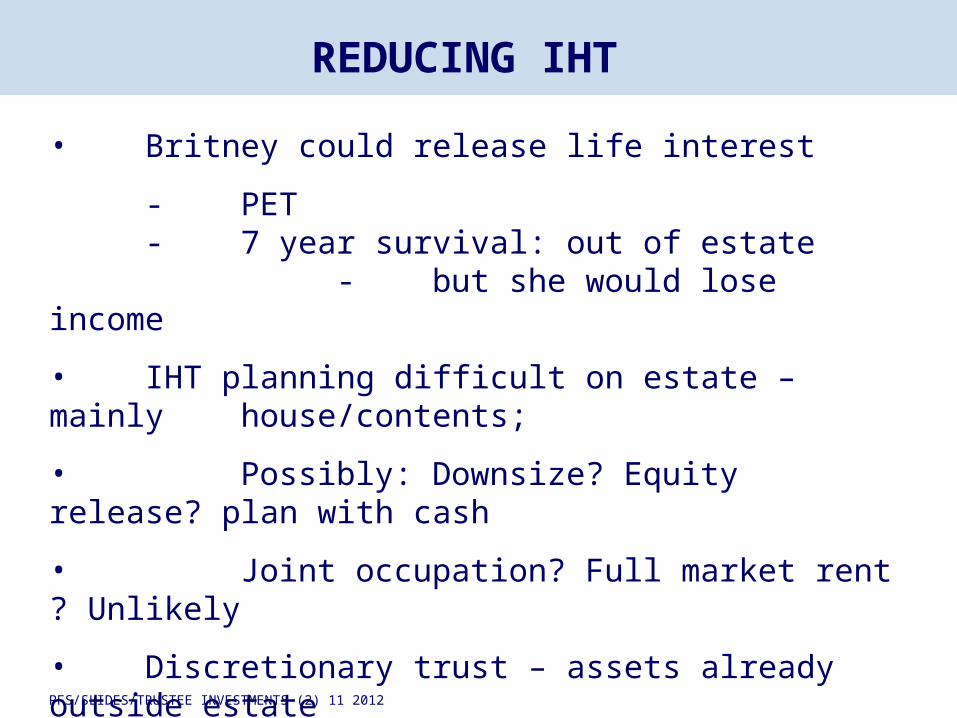

REDUCING IHT

• Britney could release life interest

- PET- 7 year survival: out of estate- but she would lose income

• IHT planning difficult on estate – mainly house/contents;

• Possibly: Downsize? Equity release? plan with cash

• Joint occupation? Full market rent ? Unlikely

• Discretionary trust – assets already outside estate

• Life cover : Care cost? Beneficiary funded? Keep

policy outside IIP trust.

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

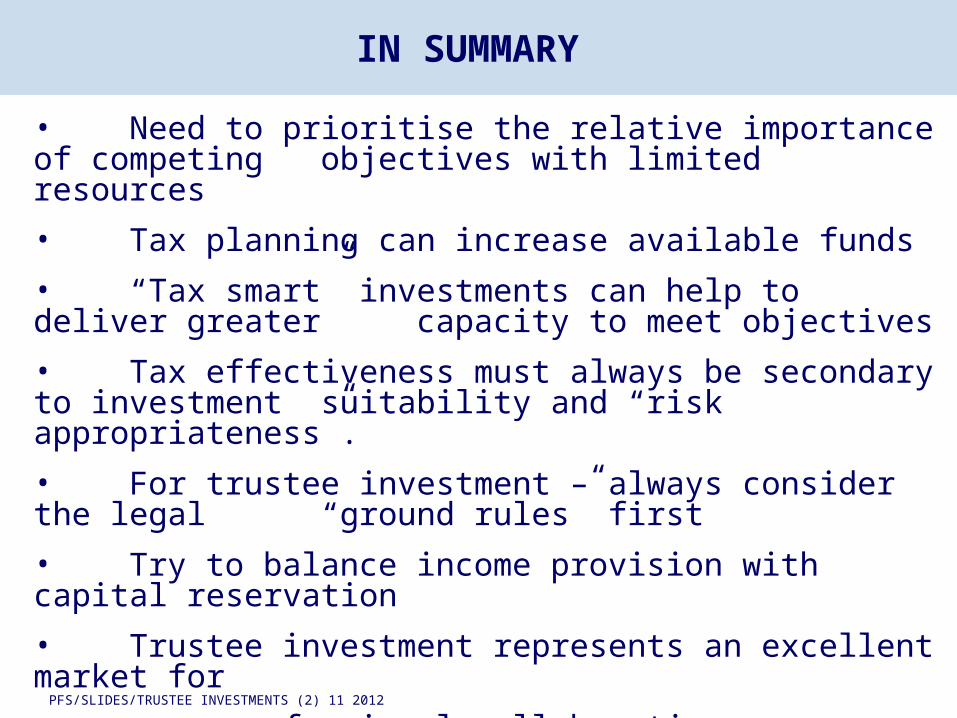

IN SUMMARY

• Need to prioritise the relative importance of competing objectives with limited resources

• Tax planning can increase available funds

• “Tax smart” investments can help to deliver greater capacity to meet objectives

• Tax effectiveness must always be secondary to investment suitability and “risk appropriateness”.

• For trustee investment – always consider the legal “ground rules” first

• Try to balance income provision with capital reservation

• Trustee investment represents an excellent market for

- professional collaboration - strongly justifiable (and profitable) adviser

charging

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

Comprehensive technical support and business generation for financial planners

• Techlink Professional • Accredited CPD• Advanced examination support• ASK; Case related technical support• Business Generation Initiatives• Techlink Communicator• Dynamic client facing website content for advised and non –advised markets.

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

Techlink professional

TECHLINK PROFESSIONAL

All you need to: Keep up to date professionally and technically Research the answers you need to your technical questions Secure business generation ideas Carry out, automatically track , record and test your technical CPD

DELIVERED THROUGH

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

TECHLINK COMMUNICATOR

Our complete communication service that enables you to keep in touch with, inform and inspire your clients and the professional advisers you do business with.

1. Quarterly Newsletters for your clients and professional (Accountants and Solicitors) contacts

"FYI” our bi-weekly , managed ,self select client email service.

3.2.

FYI Professional, bi-weekly managed e-mail to be sent to your professional connections.

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

CONTACT

www.technicalconnection.co.uk

www.techlink.co.uk

Tony Wickenden

0207 405 1600

PFS/SLIDES/TRUSTEE INVESTMENTS (2) 11 2012

![Australian EXP TRIATE...Australian Expatriate Superannuation Fund Investment Guide 3Disclaimer This Investment Guide was prepared by Tidswell Financial Services Ltd [Trustee/Tidswell],](https://img.pdfslide.net/doc/110x75/5fef1a9ccf89674f960337b0/australian-exp-triate-australian-expatriate-superannuation-fund-investment-guide.jpg)