Embed Size (px)

DESCRIPTION

This Report identifies the recent progress and key ongoing challenges facing Turkey’s National Innovation System and draws on international experience to outline potentialissues for further analysis.

Citation preview

June 2009

Document of the World Bank

Report No. 48755-TR

TurkeyNational Innovation and Technology System

Europe and Central Asia Region

Recent Progress and Ongoing Challenges

Report N

o. 48755-TR

Turkey N

ational Innovation and Technology System

Pub

lic D

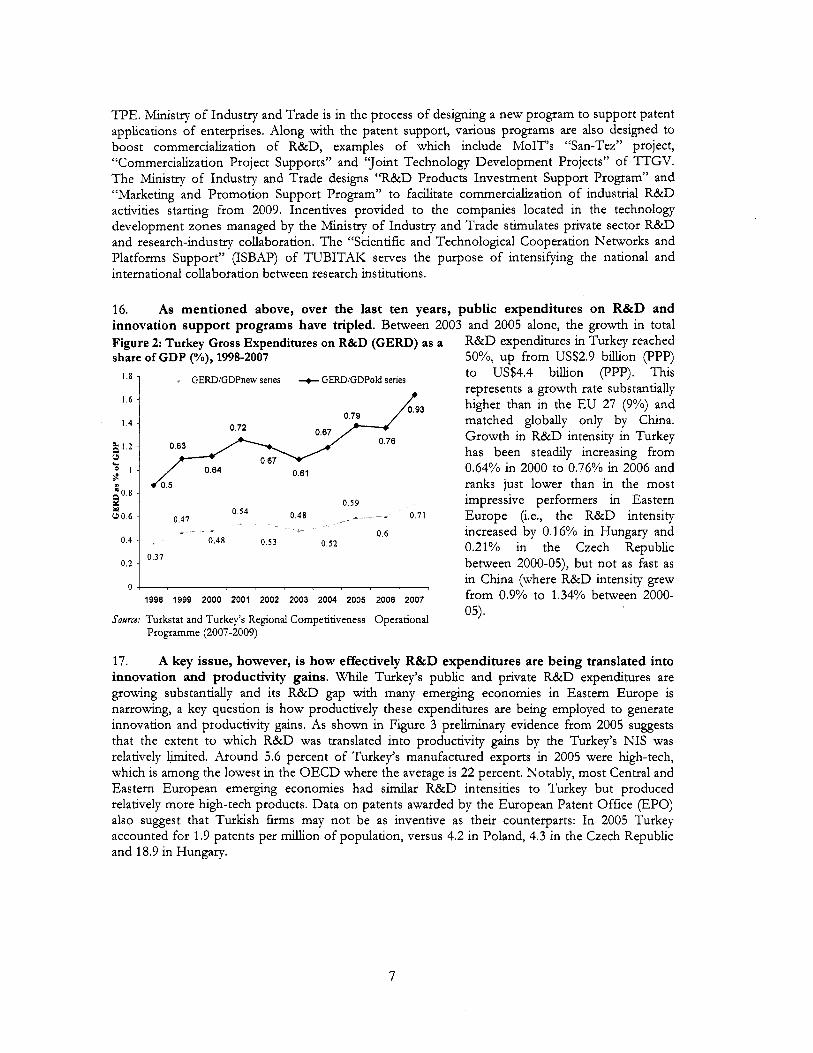

iscl

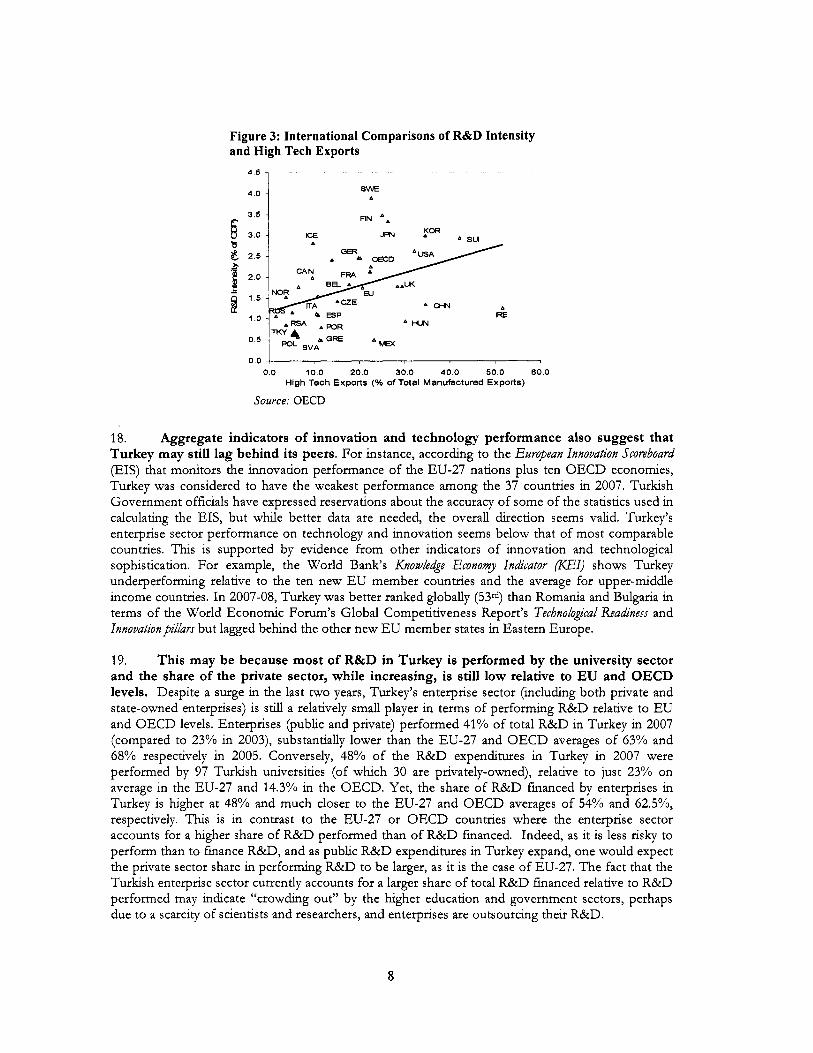

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Abbreviations and Acronyms

B E E P S BTYK CEM CMB CPS EBRD EPO ERA EU E U - 1 5

E U - 8 E U - 2 5 EU-27 FDI GDP GERD HR K O S G E B ICA ICs ICT IPR I S 0 ITP KE M&E MAM MARA M I S MoF MoIT M S I M S T Q OECD N I S NGO R&D RDI S&T S M E S SPO TAEA TARAL TDF TEKMER TEP TOBB

Business Environment and Enterprise Performance Survey Supreme Council of Science and Technology Country Economic Memorandum Capital Markets Board Country Partnership Strategy European Bank for Reconstruction and Development European Patent O f f i c e European Research Area European Union Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, Spain, Sweden, United Kingdom Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Slovakia, Slovenia E U - 1 5 plus the ten Member States that jo ined in May 2004 E U - 1 5 plus E U - 8 plus Romania and Bulgaria Foreign D i r e c t Investment Gross Domestic Product Gross Expenditures on R&D Human Resources Smal l and Medium Industry Development Organization Investment Climate Assessment Investment C h a t e Survey Information and Communication Technology Intel lectual Property Rtghts International Standards Organization Industrial Technology Pro ject Knowledge-based Economy Monitoring and Evaluation Marmara Research Center Ministry of Agriculture and Rural Affairs Management Information Systems M i n i s t r y of Finance Ministry of Indus t r y and Trade Mdlennium Science Init iat ive Metrology, Standards, Testing and Quality Organization for Economic Cooperation and Development Nat ional Innovation (and Technology) System N on-Governmental Organization Research and Development Research and Development Institution Science and Technology Smal l and Medium-Size Enterpr ises State Planning Organization Turhsh Atomic Energy Authority Turhsh Research Area Technology Development Financing Center of Technology Building Total Factor Product iv i ty Union of Chambers of Industry and Commerce

Abbreviations and Acronyms (Cont’d.)

TPE TTGV TRY T S E TTO TUBA TUBITAK TURKAK UFT UME U S A M P us UT VAT vc VCITs YOK

Turkish Patent Inst i tu te Technology Development Foundation of Turkey New Turkish Li ra Turhsh Standards Institution Technology Transfer Off ice Turkish Academy of Sciences Scientif ic a n d Technological Research Council o f Tu rkey Turkish Accredltation Agency Undersecretariat o f Foreign Trade National Metrology Ins t i t u te University-Industry Joint Research Centers Program United States Undersecretariat o f Treasury Value Added Tax Venture Capital Venture Capital Investment T r u s t s Council o f Higher Education

Table o f Contents

Executive Summary ................................................................................................................................................... i I . Introduction .................................................................................................................................................. 1

Turkey’s National Innovation System ........................................................................................................ 4

B . Intellectual Proper ty Rights Regime ......................................................................................................... 10 C . Collaboration between the Enterprise and Research Sectors .............................................................. 12 D . Innovation Finance: Venture Capital and Business Angels ................................................................. 15

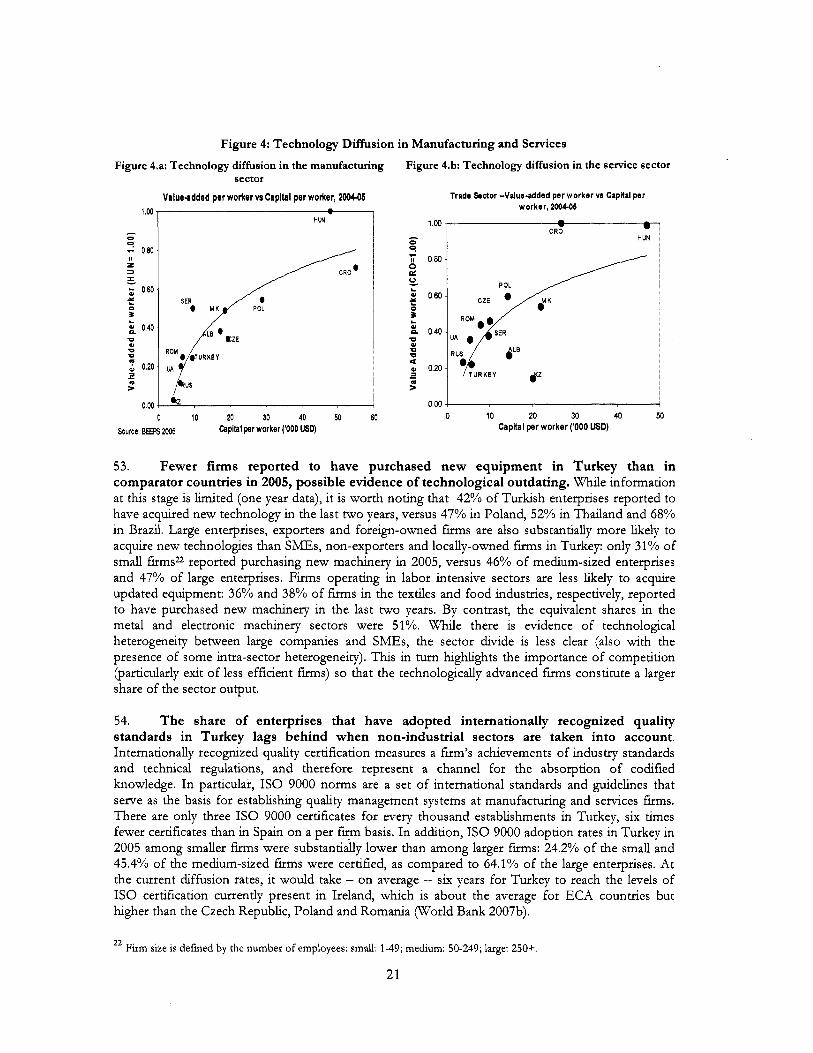

Technology Upgrading and Innovation by the Enterpr ise Sector ..................................................... 20

B . International Technology Transfer .......................................................................................................... 23 C . Innovation and R&D at the Enterprise-Level ....................................................................................... 25

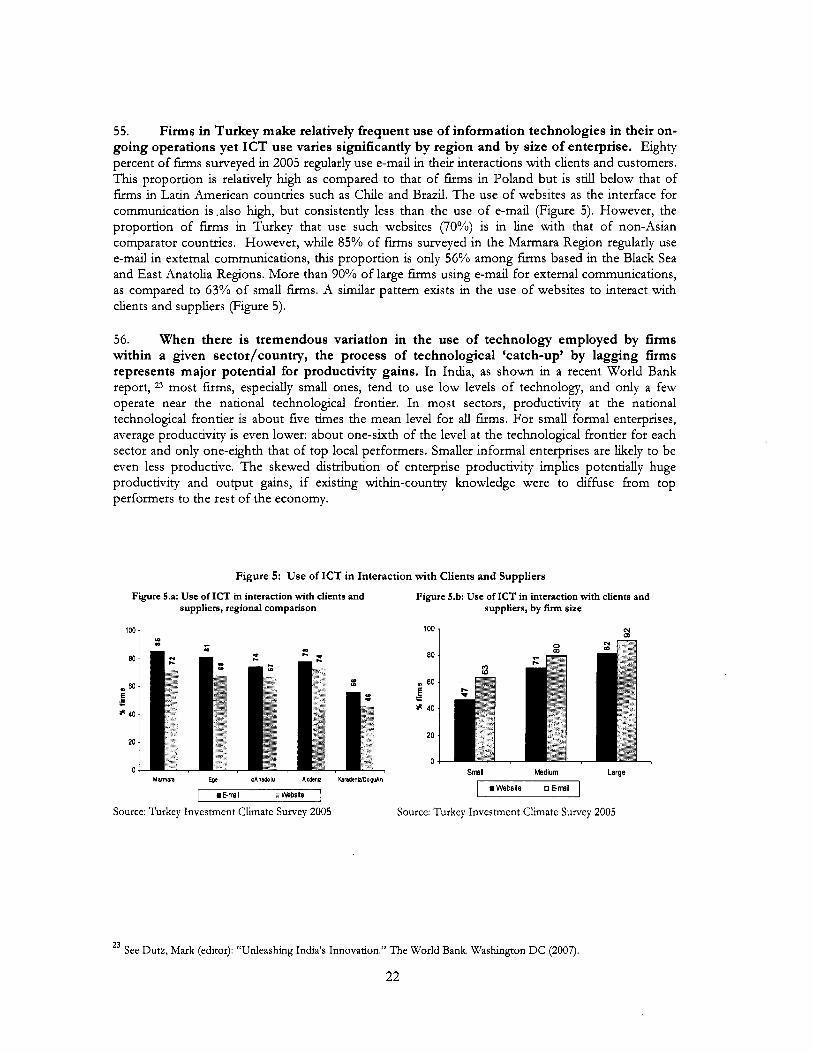

Summary and Conclusions ....................................................................................................................... 29

11 . A . Overview of Institutions, Policies and Programs ..................................................................................... 4

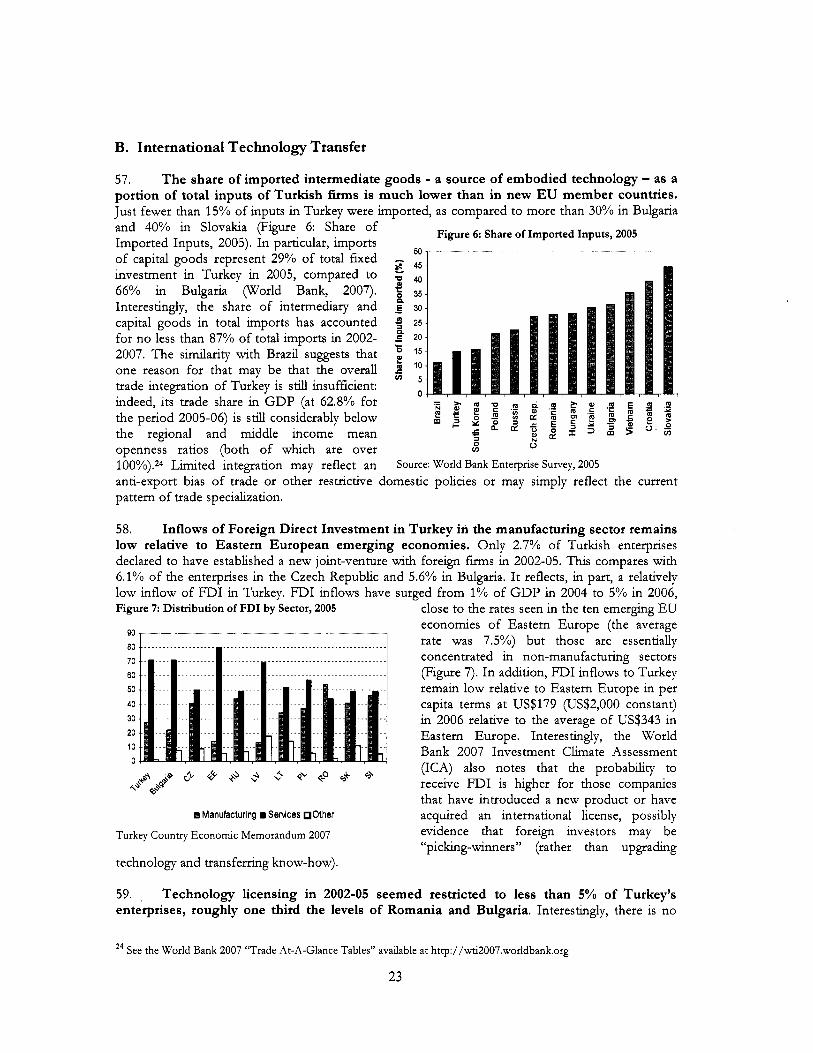

E . Human Resources: Sk i l l s and Education ................................................................................................ 1 8

A . Technology Adoption and Diffusion ..................................................................................................... 20 I11 .

.

D . Possible Causes for Low Technology Diffusion ................................................................................... 26 E . Enterprise Case Studies ............................................................................................................................. 27

IV . V . References ............................................................................................................................................... 3 2

ANNEXES

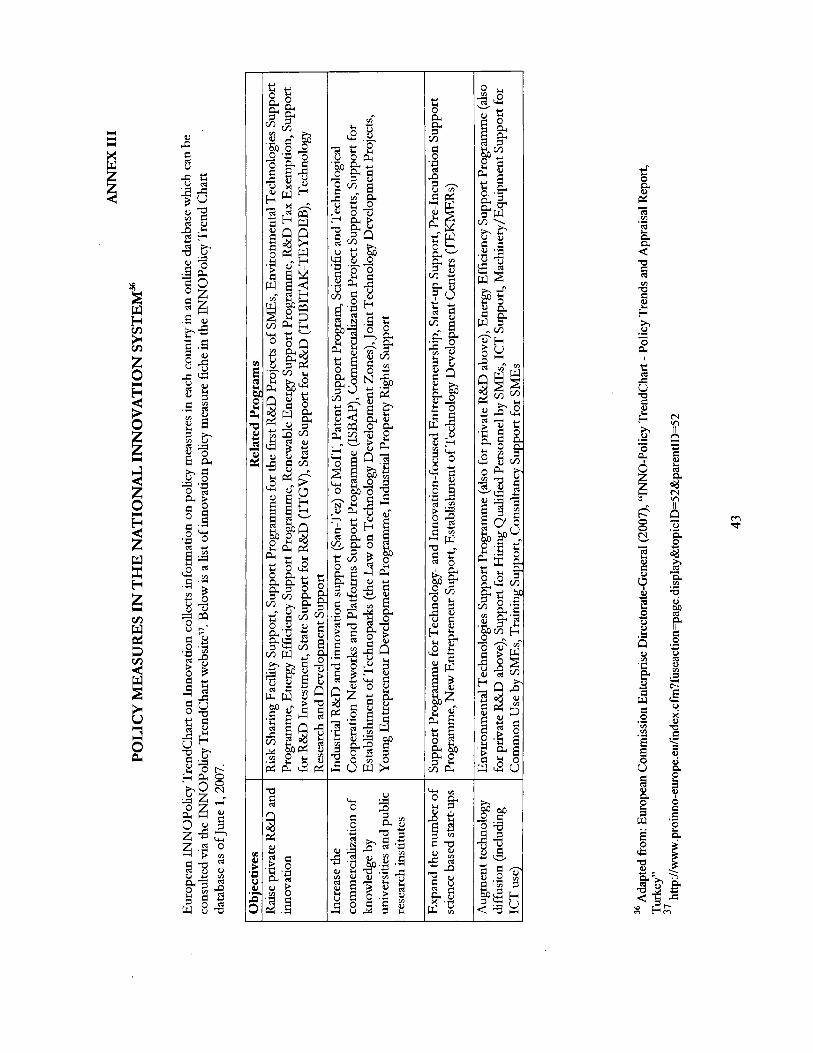

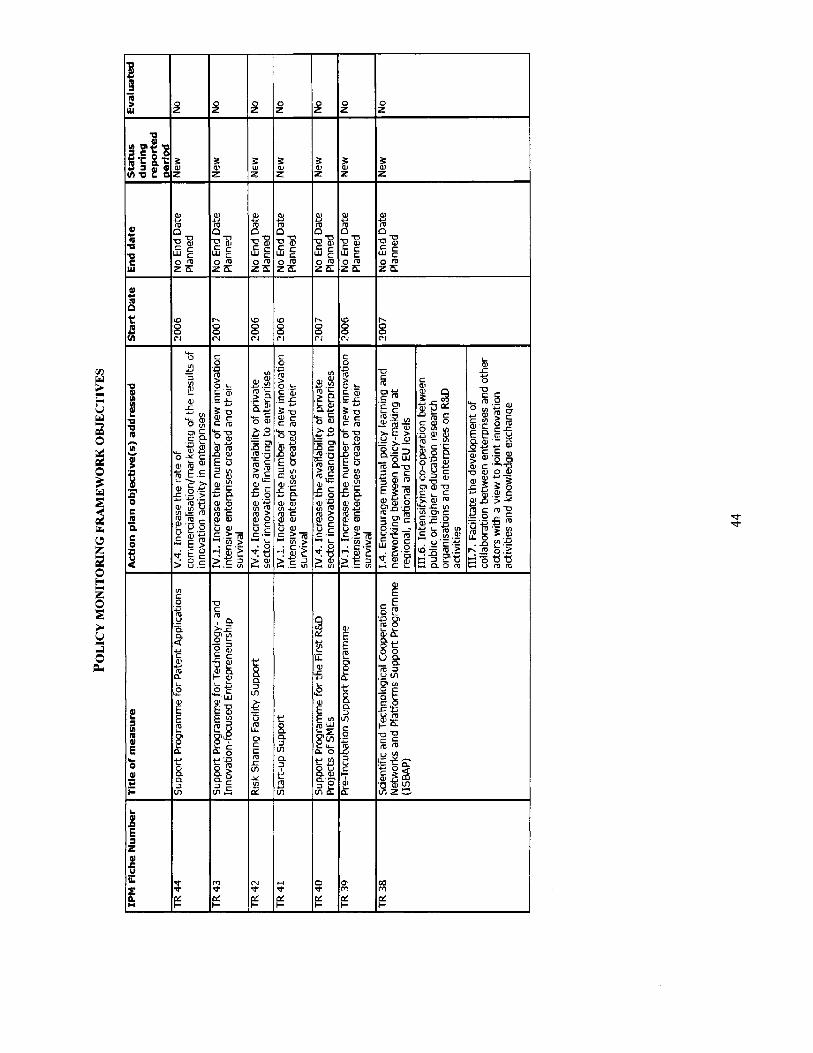

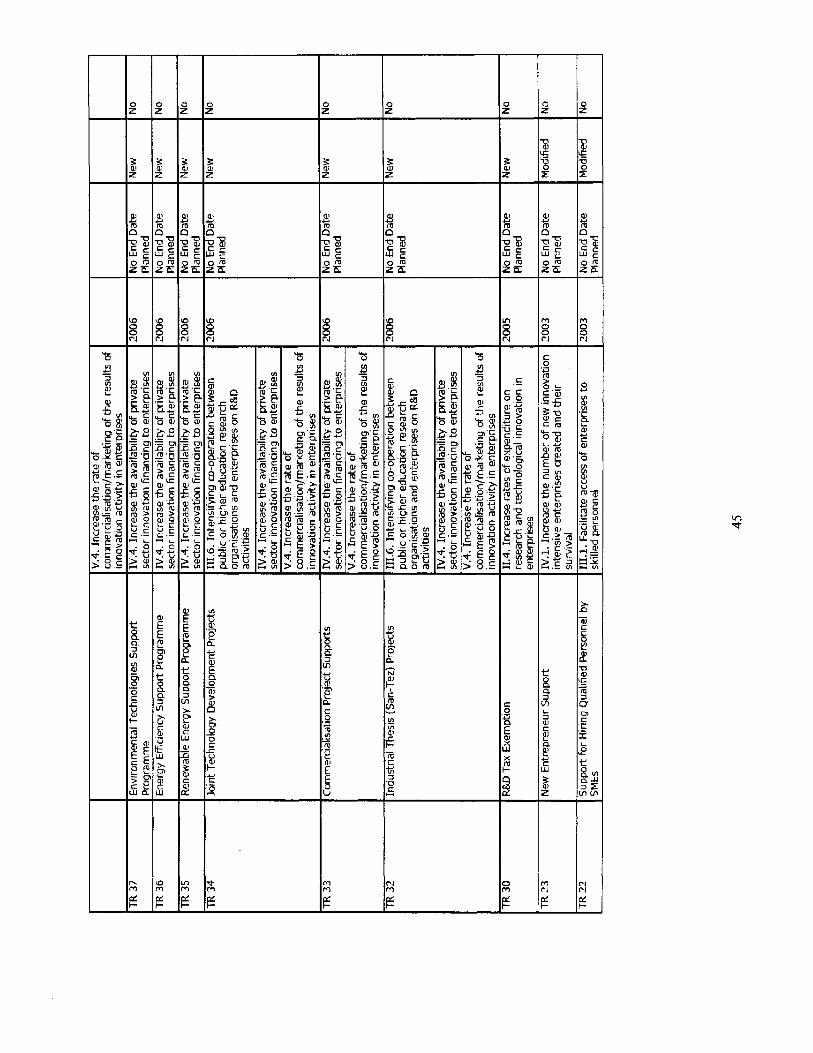

Annex I: Key Actors o f the National Innovation System ......................................................................... 33 Annex 11: Main Implementing Agencies of Public R&D Suppor t Programs ......................................... 41 Annex 111: Policy Measures in the National Innovation System ................................................................. 43 Annex IV: Summary of Main R&D Related Legislation .............................................................................. 52 Annex V: Innovation Suppor t Programs in Turkey .................................................................................... 53

FIGURES

Figure 1: Innovation Conceptual Framework ....................................................................................... 2 Figure 2: Turkey Gross Expenditures on R&D (GERD) as a share of GDP (YO), 1998-2007 ............... 7 Figure 3: International Comparisons o f R&D Intensity and High Tech Exports ............................... 8 Figure 4: Technology Diffusion in Manufacturing and Services .......................................................... 21 Figure 5: U s e of I C T in Interaction with Clients and Suppliers .......................................................... 22 Figure 6: Share o f Imported Inputs, 2005 ........................................................................................... 23 Figure 7: Distribution of FDI by Sector, 2005 .................................................................................... 23 Figure 8: International Comparisons of Firms Developing and Upgrading Products ......................... 25

TABLES

Table 1: Public Expenditures on Innovation and Technology Programs ...................................................... 6 Table 2: Public R&D Suppor t to Turkish Enterprises ...................................................................................... 6 Table 3: Key Findings from Case Studies of S M E s in Labor-Intensive Sectors ......................................... 27

Acknowledgements

T h i s repo r t was prepared, in col laboration with the Turkish Government , by a World B a n k T e a m l e d by Paulo Correa (TTL) and compr ised by Vinod K. Goel, Chris J. Uregian, S i r i n Elci, I r e m Guceri, I a n Cooper, A lasdak Reid, I hsan Karatayli, D o h a Cebotari, Naotaka Sawada and D o n a t o de Rosa. T h e repo r t has been prepared in the context of the “Turkey: N a t i o n a l I n n o v a t i o n and Technology System (NIS) Assessment” Study be ing conducted jointly by the Turkish Governmen t and the World Bank. T h e repo r t reviews the recent progress a n d ongoing challenges of Turkey’s Na t iona l I n n o v a t i o n a n d Technology System a n d identi f ies potent ia l areas for fur ther analysis.

Special thanks are g iven to U h c h Zachau (Country Director , ECCU6), Fernando Montes-Negret (Director, ECSPF) a n d L a l i t Raina (Sector Manager, ECSPFi) who suppor ted the team in the preparat ion and comp le t i on of t h i s report. T h e team i s grateful to Car l D a h l m a n (Georgetown University), M a r k A D u t z (World Bank), a n d Maureen McLaugh l tn (World Bank) who were peer reviewers for t h i s paper.

Executive Summary

I n Januay 2008, the Turkish Government has requested the World Bank to j o i n t 4 undertake an assessment of its National Innovation System in order to help guide the Turkish Government’s ongoing eforts to deepen innovation in the Turkish economy. The World Bank/ T u r k y Country Partnership Strategv (CPJ) 2008-20 I 1 ident$es ‘Improved Competitiveness and Employment Opportunities” as one of the ky areas of engagement, and within this context, recommendr studies related to technolog adoption, R&D and innovation. This document is a first attempt to address this request. It focuses on the recent progress and ongoing challenges ofthe Turkish NIS, p a r t i d r b in terms of developing innovation and techno logv policies that enable sustainedgrowth andjob creation.

1. Turkey’s Ninth Development Plan (NDP, 2007-2013) envisages doubling nominal per capita income and raising employment by 2.7% per year during the 2007-2013 period. To sustain rapid growth in the years ahead, Turkey will also need among other things (boosting ICT, labor ski l ls, innovation etc) to raise labor productivity, which i s currently at less t han 40% o f the EU- 25 average (or 29% of the us). 2. Innovation and technology diffusion can be critical factors for enhancing productivity gains that underpin competitiveness, growth and employment generation. Innovation and technology diffusion lead to more eff ic ient processes and lower costs of production for new (or higher quality) products, thereby raising overall levels of productivity. T h e National Innovation System (NIS determines innovation and technology diffusion in an economy and thus i s indrectly related to labor productivity.

3. T h e Turkish Government recognizes the importance o f technology diffusion and innovation, having set ambitious targets with a focus on the enterprise sector. These targets include (i) increasing total R&D expenditures from less than 0.6% to 2% of GDP; (i) raising the share o f privately real ized R&D from 29% to 60% of t h e total; (ii) expanding the number of researchers from under 24,000 to 80,000; and (iv) augmenting the internet penetration rate from 20% to 60%.

4. Accordingly, public expenditures on Science and Technology have increased substantially in recent years. T h e Government increased the allocation of funds for R&D in recent years, especially since 2005, with more than US$1.5 billton allocated to the Scientif ic and Technological Research Council of Turkey (TUBITAK) alone for 2005-08. Total R&D expenditures as a share of GDP in Turkey rose from 0.67% in 2002 to 0.76% in 2006. T h i s trend i s expected to continue.

5. In addition, fourteen new policy measures and programs have been introduced. Most of these measures a im to facihtate industry-researcher cooperation and to support innovative start-up companies. More broadly, systematic efforts to improve Turkey’s innovation and technology performance have been made throughout the last decade, including the creation of Technology Development Zones and the alignment of the intellectual p roper t y rights (IPR) regime with t h e European Union.

6. Turkey’s National Innovation System i s fairly well developed by international standards. Nevertheless, some challenges remain to be addressed. These challenges are particularly relevant in order to position Turkey’s Innovation and Technology policies to contribute effectively to sustaining economic growth and raising employment. For that purpose i t i s important to understand the obstacles for the transformation of knowledge into product iv i ty gains and innovation.

7. T h e private sector‘s share o f total R&D expenditures has been increasing steadily. Total R&D expenditures in Turkey rose by 50% between 2003 and 2005, up from US$2.9 bLUton (FPP) to US$4.4 billion (PPP). T h i s reflects the highest growth rate globally (with China) and i s substantially higher than in the E U - 2 7 countries (9”/0). From 2003 to 2006, the share of total R&D financed by the

enterprise sector (that includes pub l i c a n d private f m s ) also increased significantly by 10% to reach 46% of to ta l expenditures.

8. However, R&D i s largely performed by Universities and Research and Development Institutes (RDIs) with public financing. Despi te steady increases, the enterprise sector per formed a smaller share o f R&D in Turkey (37%) than the OECD average (62.5%), a n d foreign f inancing of R&D i s m u c h l o w e r than in emerging economy comparators. Risk-aversion may b e one reason against greater R&D financing by the enterprise sector, along with the possible “crowding-out” effect of publ ic ly f inanced R&D due to a scarcity of researchers. T h e n e w R&D Law, enacted in February 2008, i s expected to increase both fore ign a n d local private par t ic ipat ion in R&D activities.

9. Turkey’s intellectual property rights framework i s broadly aligned with the EU but implementation needs to be strengthened. Notw i ths tand ing certain divergences, the IPR legislative f ramework i s in h e with EU standards, yet imp lemen ta t i on a n d enforcement m o s t notably in the area of indust r ia l p roper t y rights, needs to b e strengthened to reach EU levels. T h i s requires legislative changes, capacity building of key institutions (IP courts, Turkish Patent Institute) and greater cooperat ion between the public, private and non-governmenta l actors.

10. T h e Government i s increasing measures to further collaboration between the enterprise and research sectors, but progress i s slow. L i m i t e d col laboration between publ ic research institutes, universit ies a n d the enterprise sector contr ibutes to the low product iv i ty of Turkey’s N I S . O n e cause i s the regulatory f ramework that creates disincentives for researchers to o f fe r consult ing services to enterprises (university revo lv ing fund regulations) a n d to establish start-ups, a n d for universit ies to commercial ize research (distribution of royalty rights). In addition, the quanti ty and quali ty of m a n y impor tan t N I S intermediaries (technology transfer offices, venture capital) that facilitate col laboration between industry and research institutes can b e raised and the Turkish G o v e r n m e n t i s ma lung efforts in t h i s direction, most no tab ly with the expansion of technology transfer offices in m a j o r universities.

11. Scarcity o f human capital i s another critical bottleneck. There are 2.0 researchers p e r thousand of to ta l employed in Turkey, w h i c h i s l ower than the EU-27 average of 5.8. O n e of the m a i n reasons for this scarcity i s a brain-drain that claims a significant share of Turkish researchers who reside abroad upon complet ion of their PhDs. To tackle this problem, TUBITAK, the M i n i s t r y o f Na t iona l Educa t ion and the M i n i s t r y of Industry a n d T rade have developed programs, and Governmen t efforts to modern ize the h igher education system are in place.

12. A lack of innovation finance due to the underdevelopment o f the venture capital (VC) and business angel sector i s another constraint to the performance of Turkey’s N I S . There are only three Venture Capital Investment Trusts in Turkey, with annual investments l ower than US$lOO d o n . T h e regulatory f ramework a n d government incentives to the financial sector constrain development of these services. In addition, the demand (deal flow) for VC and business angels’ services i s also low, fur ther constraining development o f t h s sector.

13. Currently, technology adoption in Turkey i s low. T h e World B a n k Enterprise Survey o f 2005 reveals that Turkish firms generally choose to purchase machinery and equipment, rather than developing and adapting their own technology. In addltion, fewer Turkish firms repor t to have purchased n e w machinery in the preceding year than those in comparator countries. In 2005, 42% o f firms in Turkey repor ted the acquisit ion o f n e w machinery, w h i c h i s a l ower technology acquisit ion rate than in many other emerging economies such as B raz i l (68%).

14. Technology transfer from abroad remains relatively limited as well. T h e n u m b e r of joint ventures established with foreign f m s , a m a j o r source o f technology upgrading for developing countries, seems to b e lower in Turkey than comparator countries. Furthermore, a l though Fore ign D i r e c t Investment (FDI) inflows have increased significantly in recent years, manufactur ing sectors did not get the largest share o f t h i s increase and levels o f investment seem m u c h lower than in most n e w EU member states. There i s also scope to increase g lobal knowledge transfer to Turkey v ia the large Turhsh Diaspora.

ii

15. Both large-scale survey data and case studies show that firm-level innovation i s limited, especially in labor-intensive sectors. T h e percentages of firms in t roduc ing a n e w product, or upgradmg their products, remain b e l o w those of comparators such as Brazil, Thailand, Chi le a n d Poland. On the other hand, pr ivate R&D intensity i s similar to comparators: expendltures on R&D as a share of sales are 0.3%, about the same as a selection o f comparable economies.

16. Case studies of S M E s in certain sectors suggest that the main constraints to upgrading innovation and technology in the enterprise sector are deficient labor skills, limited access to credit, and a lack of knowledge transfer. These factors, a long with addit ional costs incurred by Turhsh firms such as high prices a n d inconsistent supply of energy as w e l l as high tax rates, negatively affect the capacity o f enterprises to innovate a n d adop t technology, hurting their global competiveness.

17. These findings suggest areas for further analysis. At the strategic level, there are impor tan t questions related to the emphasis o f the nat ional i nnova t ion po l i cy f ramework a n d the interaction between NIS institutions. These questions include: (i) I s the balance between pub l i c support for R&D in industry vs. a g c u l t u r e optimum, given the large share of emp loymen t in agriculture and service sectors in Turkey?; (ii) Could the recent surge in pub l i c R&D expenditures b e “crowding-out” private R&D?; a n d (iii) A r e there mechanisms employed in N I S systems in OECD economies that cou ld b e used in Turkey to he lp i m p r o v e po l i cy coord inat ion a n d enhance communicat ion and knowledge sharing between the d i f ferent N I S actors?

18. There are also other issues in the policy and institutional framework that would benefit from further analysis, such as IPR protection, enterprise-research-university sector collaboration, and the innovation finance industry. G i v e n the recent surge in n e w support programs in the Turkish N I S , usefu l insights c o u l d b e gained from the establishment o f monitoring and evaluation mechanisms for key programs, using techniques c o m m o n in OECD economies. T h e key programs that cou ld b e assessed inc lude pr ivate R&D suppor t schemes (tax incentives, soft loans and m a t c h n g grants), Technopark incentives, a n d technology diffusion programs. In addltion, further analysis of f irm-level surveys a n d case-study data c o u l d p r o v i d e a deeper understanding o f the relative constraints to innova t ion a n d technological upgrading in the Turkish enterprise sector, a n d thus improve fu ture pub l i c po l i cy design a n d implementation.

iii

Turkey- National Innovation and Technology System

Recent Progress and Ongoing Challenges

I. Introduction

1. In January 2008, the Turkish Government requested the World Bank to jointly undertake an assessment of its National Innovation System in order to help guide i ts ongoing efforts to deepen the role of innovation (and i ts performance) in the Turkish economy. T h e World Bank /Tu rkey Country Partnership Strategy (CPS) 2008-201 1 identif ies the enhancement o f technology adop t ion and innova t ion as a key priority for engagement within the context of improving competit iveness a n d employment opportunit ies. U n d e r the CPS framework, a series of analytical studies are planned, i nc lud ing one focused on technology adoption, R&D a n d innova t ion for t h e 2008-2009 period. T h e G o v e r n m e n t requested t h i s Study in order to p rov ide crit ical input to i t s efforts in this area a n d t h i s Repor t has been prepared in the context of t h i s Study.

2. Sustaining economic growth, expanding employment and raising labor productivity i s a key development challenge in Turkey. To sustain r a p i d growth in the years ahead, Tu rkey will need to a m o n g o the r things raise l abo r productivi ty, w h i c h i s currently a t less than 40% of the EU-25 average (or 29% of the US). As indicated in the World Bank‘s 2007 Tu rkey E c o n o m i c M e m o r a n d u m (CEM), raising labo r p roduc t i v i t y wdl require increasing to ta l factor product iv i ty (TFP) and the amoun t o f capital pe r worker . T h i s , in turn, entails the challenge of raising investment levels wh i l e addressing the savings-investment gap a n d Turkey’s structurally high current account deficit. Despi te strong economic growth since 2002, employment has not been increasing commensurately. Generat ing m o r e a n d bet ter jobs i s the pr inc ipa l channel for distributing the benefits of economic growth to Turhsh citizens. E m p l o y m e n t g rew by a n annual average o f about 0.7% in 2002-2006, considerably l o w e r than the requi red level to keep pace with the r a p i d expansion o f the working age populat ion. Turkey’s employment rate in 2006 was 46%, b e l o w al l EU countries and the Lisbon Agenda target of 70%.

3. A favorable investment climate enables the private sector investment and productivity improvements needed to sustain long-term competiveness, growth and employment generation.’ A good investment clunate i s compr ised of a n u m b e r of fundamental factors that determine the pr ivate sector’s capacity to invest a n d i m p r o v e productivi ty. These factors include: macroeconomic stabdity; sound legal institutions a n d ru le of l a w that ensure predictable contract a n d p roper t y rights enforcement; a n d compet i t ive p r o d u c t markets support by strong compe t i t i on a n d open trade policies. A regulatory env i ronmen t a n d tax regime that are not over ly burdensome also p lay an i m p o r t a n t ro le on f m s ’ incentives to invest. O t h e r impor tan t factors inc lude eff icient f inancial markets that a l l ow firms to get access to funding for their ventures a n d good infrastructure that enables fEms to connect with their customers and suppliers and helps t h e m take advantage of m o d e r n p r o d u c t i o n techniques. Finally, f lexible l abo r market institutions that a l l ow f m s to respond to marke t changes wh i l e he lp ing workers deal with change and a skil led work fo rce are essential for f m s to adop t new, m o r e product ive technologies.

4. Innovation and technology diffusion can be critical factors for enhancing productivity gains that underpin competitiveness, growth and employment generation.2

A Better Investment Chate for Everyone,” World Development Report 2005, World Bank, Washington DC I ( <

For economic theory and empincal evidence of the links between compemon, innovation, producuvity growth, and overall cconomic growth, sce Aghion (2006), Aghion, Bloom, and others (2005), and Aghion, Blundcll, and otherq (2006)

1

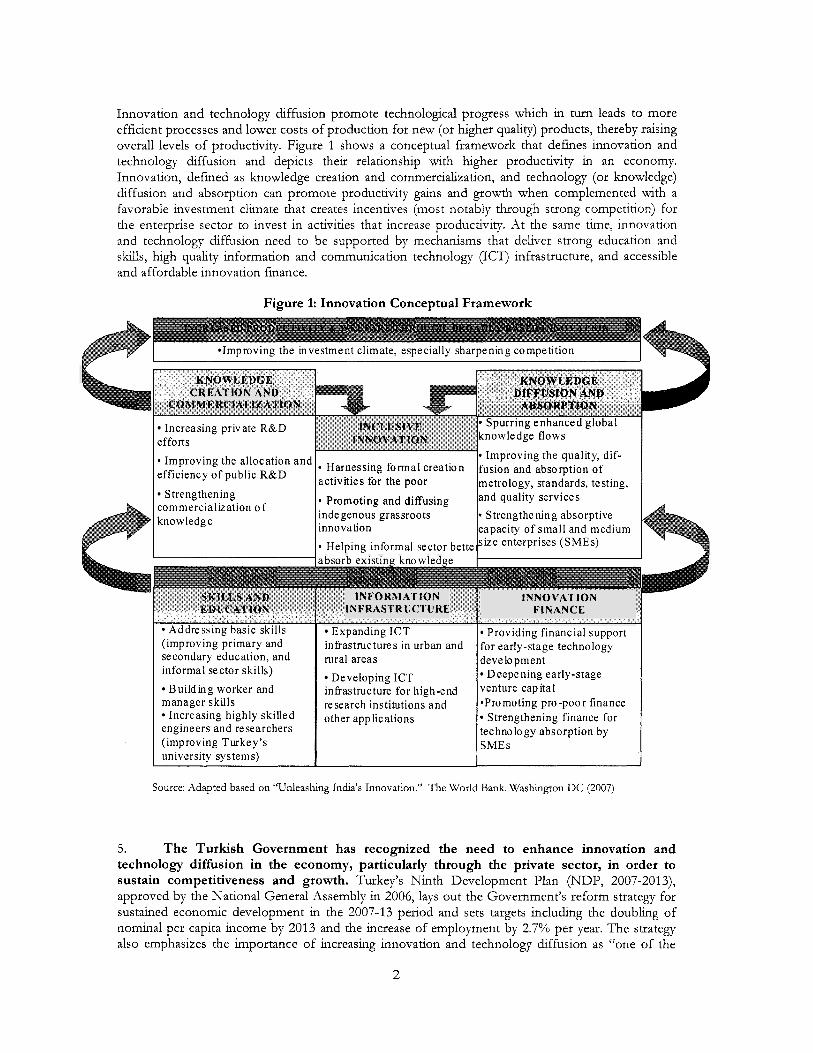

I n n o v a t i o n a n d technology d f f u s i o n p r o m o t e technological progress w h i c h in turn leads to m o r e eff icient processes and lower costs of p roduc t i on for n e w (or h igher quality) products, thereby raising overal l levels o f productivi ty. F igure 1 shows a conceptual f ramework that defines i nnova t ion and technology diffusion and depicts their relat ionship with higher p roduc t i v i t y in an economy. Innovat ion, def ined as knowledge creation and commercialization, and technology (or knowledge) diffusion and absorpt ion can p r o m o t e product iv i ty gains a n d growth w h e n complemented with a favorable investment climate that creates incentives (most notably through strong competit ion) for the enterprise sector to invest in activities that increase product iv i ty . At the same time, innovat ion and technology Qffusion need to b e supported by mechanisms that deliver strong education and s l d s , hgh quali ty i n fo rma t ion a n d communicat ion technology (ICT) infrastructure, and accessible and affordable i nnova t ion finance.

Figure 1: Innovation Conceptual Framework

CREATIOK AND

Increasing private R&D efforts

* Improving the allocation and efficiency o f public R&D

Strengthening commercialization o f knowledge

(improving primary and secondary education, and informal sector ski l ls)

Bui lding worker and manager sk i l l s

Increasing highly skilled engineers and researchers (improving Turkey’s university systems)

Harnessing formal creation

Promoting and diffusing

ictivities for the poor

ndegenous grassroots nnovation

Helping informal sector bette . -

INFO RRI A’r ION INFRASI’RIIC‘I‘tIHE

Expanding I C T infrastructures in urban and rural areas

Developing ICT infrastructure for high-end research institutions and other applications

KNOW LEDGE DIFFUSION AND

ABSORPTION 1 Y Spurring enhanced global inowledge flows

1 Improving the quality, dif- Yusion and absorption o f netrology, standards, testing, 2nd quality services t Strengthening absorptive :apacity o f small and medium size enterprises (SMEs)

I N N O\‘ A T 1 ON FINANCE

Providing financial support for early-stage technology development

Deepening early-stage venture capital *Promoting pro-poor finance

Strengthening finance for technology absorption by SMEs

Source: Adapted based on “Unleashing India’s Innovation.” The World Bank. Washington D C (2007)

5. T h e Turkish Government has recognized the need to enhance innovation and technology diffusion in the economy, particularly through the private sector, in order to sustain competitiveness and growth. Turkey’s Ninth Deve lopmen t P lan (NDP, 2007-2013), approved by the N a t i o n a l Genera l Assembly in 2006, lays out the Government’s r e f o r m strategy for sustained economic development in the 2007-13 per iod and sets targets i n c l u d m g the doubling of nomina l pe r capita i n c o m e by 2013 and the increase o f employment by 2.7% p e r year. T h e strategy also emphasizes the impor tance of increasing innovat ion and technology Qffusion as “one of the

2

most impor tan t factors” for Turkey’s competit iveness a n d sets the following targets for the pe r iod 2007-2013: (i) increase to ta l R&D expenditures from less than 0.7 to 2% of GDP; (ii) raise the share o f privately real ized R&D from less than 30% to 60% of the total; (iii) expand the number of researchers from u n d e r 24,000 to 80,000; a n d (iv) augment the in ternet penetrat ion rate from 20% to 60%. To achieve these targets, the Turkish G o v e r n m e n t has in recent years substantially increased publ ic expendltures on R&D a n d o the r programs supporting innova t ion a n d technology diffusion and implemented a n u m b e r of inst i tu t ional and legislative reforms. Since late 2006, 14 n e w measures have been introduced, most of w h i c h have been a imed p r imar i l y a t strengthening col laboration between the enterprise sector a n d the research community, a n d increasing investments in innovat ion by the enterprise sector, most no tab ly by supporting the creation of h igh- tech start-up companies.

6. The Turkish Government requested the World Bank to jointly undertake an assessment of the National Innovation System in order to help guide i t s ongoing efforts to improve the economy’s innovation and technology performance. T h e N a t i o n a l I nnova t ion System PIS) relates to the institutions, policies a n d programs that underlay the in teract ion o f public, private a n d non-profit sectors that dr ive i nnova t ion a n d technology/knowledge dlffusion.3 T h e pub l i c sector has a key r o l e in al l of these components, p r imar i l y in terms of creating the appropriate po l icy a n d regulatory f ramework but in some cases also by providing financial support through programs. T h e G o v e r n m e n t recognizes that in order to maximize returns on publ ic ly funded R&D investments, and to i m p r o v e the economy’s i nnova t ion a n d technology performance, i t needs to further r e f o r m i ts N I S in l ine with EU standards and international best practices. In order to p rov ide analytical input into these r e f o r m efforts, the Turkish G o v e r n m e n t a n d the World B a n k are jointly u n d e r t a h n g an analytical study assessing the Na t iona l I n n o v a t i o n System. W h i l e recognizing the broader elements of the Turkish N I S , the Turkish G o v e r n m e n t requested the World B a n k to focus the Study on three main areas of i t s N I S : (i) the innova t ion policy, legal a n d inst i tu t ional framework; (ii) the evaluation o f selected i nnova t ion a n d technology support programs; a n d (iii) a rev iew of private sector i nnova t ion a n d technology per formance a n d potent ia l determinants.

7. This Report identifies the recent progress and key ongoing challenges facing Turkey’s National Innovation System and draws on international experience to outline potential issues for further analysis. T h e n e x t section prov ides an overv iew of the inst i tut ional structure, po l icy f ramework a n d main programs of Turkey’s N I S a n d identi f ies issues in three main areas that h inder i nnova t ion performance: the intellectual p roper t y right (IPR) regme, col laboration between the research and enterprise sectors, and innova t ion finance. T h e third section uses available i n fo rma t ion (aggregate a n d f irm-level data a n d a set of 20 case studies) to p r o v i d e a rev iew o f the i nnova t ion and technology per formance of the enterprise sector in T u r k e y a n d prel iminari ly address i t s possible determinants. Areas for fur ther potent ia l study and analysis are ident i f ied based on the key findlngs in each section.

As defined in P. Patel and K. Pavitt (1994): “National Innovation Systems: Why They Are Important, And How They 3

Might Be Measured And Compared.” Economics ofInnovation andNew Technolog, Volume 3, Issue 1 1994, pages 17 - 95.

3

11. Turkey’s Nat ional Innovation System

A. Overview o f Institutions, Policies and Programs

8. N I S at the macro-level. The key findings are that:

This section summarizes the main institutions, policies and programs of the Turkish

. T u r k e y has a well-developed N I S structure that encompasses most of the actors and institutions existent in OECD economies; . T h e scope of pub l i c programs supporting innova t ion a n d technology i s large; . T h e r e have been inst i tu t ional improvements recently, however there i s s t i l l some level o f fragmentation a n d overlap in institutions a n d programs and, as in most countries, coord inat ion a m o n g N I S players i s challenge; . Independen t evaluation a n d in ternat ional benchmark ing o f institutions a n d programs i s in the process of evolvement; . Following the EU experience, T u r k e y i s currently interested in raising the impac t of i nnova t ion policies on the development of regions.

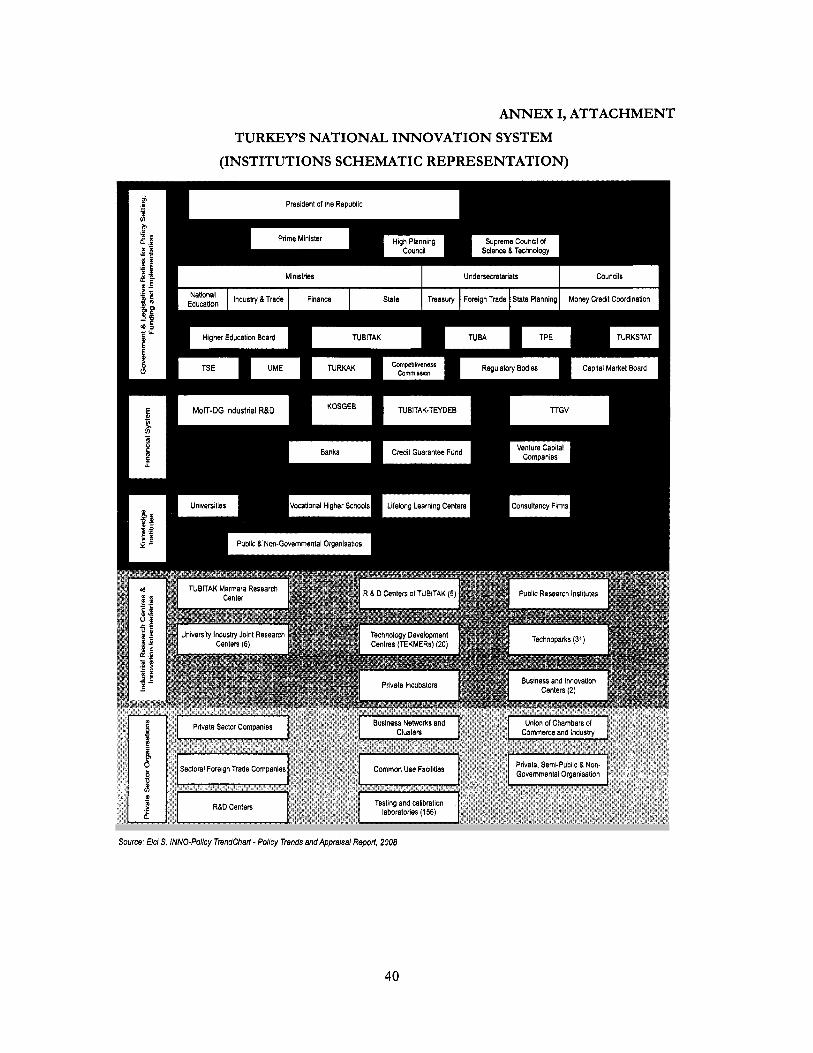

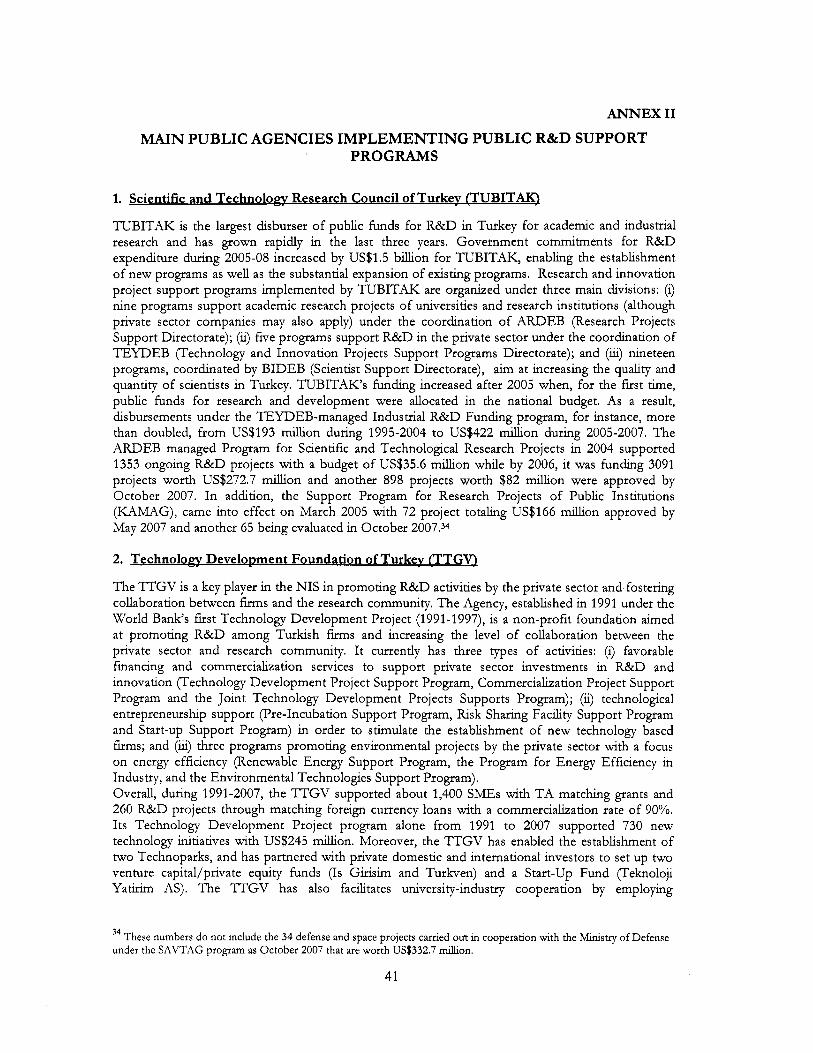

9. Main Institutions of Innovation Policy Formulation. A p a r t from the Turkish Nat iona l General Assembly a n d the Counc i l of Ministers, the main actors in the formulat ion o f Science and Technology Policies in Turkey are the Supreme Counc i l of Science a n d Technology (BTYK), the Scientif ic and Technologica l Research Counc i l of T u r k e y (TUBITAK), the State Planning Organizat ion (SPO), a n d the Counc i l of H i g h e r Educa t ion (YOIC, a n d Universit ies. BTYK i s the highest body for designing, coord inat ing a n d monitoring science a n d research policy a n d in addi t ion prov ides advisory support to the G o v e r n m e n t in the fo rmu la t i on of long- term innova t ion strategy pol icy. I t s meetings take place semi-annually a n d are chaired by the Pr ime-Min is ter and composed o f representatives of the government, universities, industry a n d NGOs. TUBITAK functions as the Secretariat to BTYK a n d i s t he central player in the N I S with several key responsibhties: (i) formulat ing a n d coord inat ing implementat ion of Turkey’s science, technology and innova t ion policies that are decided by the Supreme Counc i l o f Science a n d Technology; (ii) imp lemen t ing science, technology a n d innova t ion support programs; (iii) managing the “Turlush Research Area” (TARAL), a p l a t f o r m for public, private a n d NGO stakeholders to coordinate fu ture R&D priori t ies a n d collaboration, a n d to integrate i t with the European Research A rea (ERA); and (iv) owning and operating a n e t w o r k o f publ ic R&D institutions PIS) a n d other organizations such as Marmara Research Center (MAW, N a t i o n a l Me t ro logy Inst i tu te (UME), Elect ron ics Inst i tu te a n d others. O t h e r impor tan t actors inc lude the Technology Deve lopmen t Founda t ion o f Tu rkey (TTGV), the Turkish Patent Inst i tu te (TPE), the Turkish Standards Institution (TSE), the M i n i s t r y of Industry and T rade (MoIT); the Ministry of A p c u l t u r e a n d Rura l Affairs (MARA); the Undersecretariat of Fo re ign Trade (UFT); the Undersecretariat o f Treasury (UT); the M i n i s t r y o f Finance (MoF), the Small and Medium-Sized Enterprises Deve lopmen t Organizat ion (KOSGEB); the Turlush A t o m i c Energy Authority (TAEA); a n d the Turkish Academy of Sciences (TUBA). These institutions have sector specific po l i cy roles (as in the cases of MoIT a n d MARA), imp lemen t certain support programs (MoF, UlT a n d ‘ITGV) whi le TUBITAK also pe r fo rms R&D activities through i t s 14 institutes. T h e Turhsh N I S also includes technology intermedlaries such as incubators, Technoparks, venture-capital funds, other knowledge institutions and the enterprise sector (Annex I).

10. The Turkish Government has made strong efforts to strengthen key institutions of the N I S in recent years. In the past decade, the G o v e r n m e n t has modern ized several N I S institutions inc lud ing the Turkish Standards Institution, TUBITAK’s Marmara Research Centre and Na t iona l Me t ro logy Inst i tute, the Turkish Patent I ns t i t u te a n d suppor ted establishment of the TTGV. T h e Marmara Research Center, the largest pub l i c sector R&D organization, has been restructured a n d now i s one o f the most active contract research centers in the country. I t provides

4

extensive services (both R&D and other services) to industry and currently earns 50-60% of i t s expenses from contract work. However, a major i ty o f i t s work i s focused on the public sector. TLJBITAK also has f ive more R&D Inst i tu tes in the areas of information technologies and electronics, defense, cryp tology, bio- technology, and gene tics.

11. TUBITAK’s funding increased after 2005 (US$1.5 billion during 2005-08) when, for the first time, public funds were allocated in the national budget specifically for R&D. As a result, disbursements under the TEYDEB-managed Industrial R&D Funding program, for instance, more than doubled, from US$193 d o n during 1995-2004 to US$422 million during 2005-2007. T h e ARDEB managed Program for Scientif ic and Technological Research Projects in 2004 supported 1353 ongoing R&D projects with a budget of US$35.6 d o n while by 2006 i t was fundmg 3091 projects worth US$272.7 million and another 898 projects worth US$82 d o n were approved by October 2007. In addition, the Suppor t Program for Research Projects o f Public Institutions (KAMAG) came into effect on March 2005 with 7 2 projects totaling US$166 d o n approved by May 2007 and another 65 being evaluated in October 2007.4

12. The overarching policy framework for Innovation, Science and Technology in Turkey i s outlined in a set of publications composed of the Ninth Development Plan for 2007- 13, the Medium T e r m Program for 2008-2010 (prepared under the coordination of SPO) and the decisions of the Supreme Council, including the National Science and Technology Strategy (2005- 2010) and the “National Innovation Strategy 2008-2010” (prepared by TUBITAK). T h i s policy framework i s completed by the following documents: “Industrial Policy for Turkey” (towards EU Membership), “ S M E Strategy and Action Plan”, and “Vision 2023” (includmg the preparation of a Technology Foresight Project, a National Technology Competences Inventory Project, a Researcher Information System Pro ject and a National Research Infrastructure Information System Pro ject with the objective o f identifying strategic technologies for Turkey under t h e coordination o f TUBITAK). Anchored in the challenge o f raising employment by 2.7% per year and sustaining economic growth at 7’10, the Ninth Development Plan establishes the following complementary goals in the field of Innovation and Technology for t h e 2007-13 period: (i) increase R&D expenditures from less then 0.7 to 2% o f GDP; (ii) raise the share o f privately financed R&D from less than 30% to 60%; (iii) expand the number of researchers from under 24,000 to 80,000; and (iv) augment the internet penetration rate from 20% to 60%.

13. The documents that constitute the basis for the National Innovation Policy framework converge around four main policy objectives: (i) increase the rates of expenditures on research and technological diffusion (particularly ICT) by enterprises; (ii) strengthen co-operation between public or higher education research organizations and enterprises on R&D activities; (iii) increase the number of new innovation intensive enterprises created and their survival; and (iv) increase the rate o f commercial izat ion of R&D activities by the research sector. Until late 2006, innovation policy measures in Turkey were very h t e d in scope, focused primarily on the f i r s t two objectives. T h e large number of new measures introduced since then (doubling the previous total) have primarily been aimed at addressing the last two categories outlined above, substantially enriching the policy mix.

14. Main Public Innovation Support Programs. T h e Turkish Government’s investments in public innovation and technology support programs have r isen substantially in recent years and are pro jected to continue to increase. As mentioned earlier, during the 2005-08 period, the Government allocated a significant amount of additional resources (over U S $ l . 5 billion) from i t s budget, pr imardy to TUBITAK. Public resources allocated to innovation and technology support programs have more than tripled in the last ten years with public R&D expenditures as a share o f GDP rising from 0.67%

These numbers do not include the 34 defense and space projects carried out in cooperation with the Ministry of Defense under the SAVTAG program, as of October 2007 that are worth US$332.7million.

5

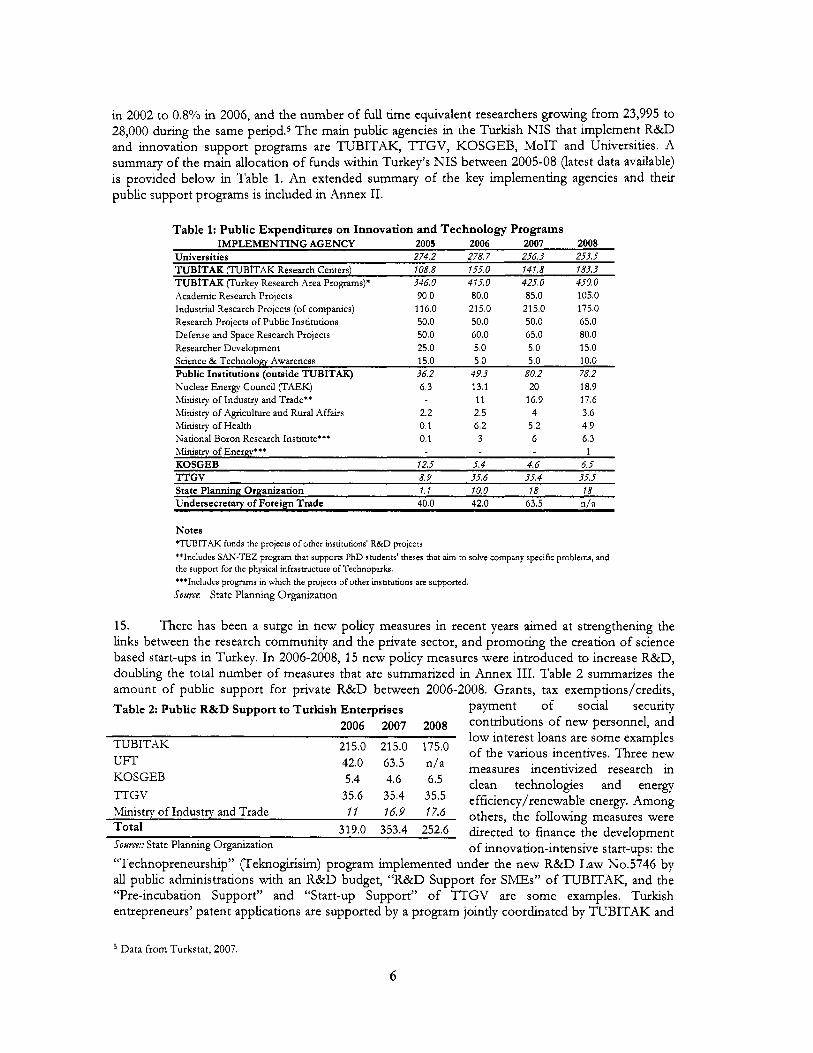

in 2002 to 0.8% in 2006, and the number o f full t ime equivalent researchers growing from 23,995 to 28,000 during the same period.5 T h e main public agencies in the Turlush N I S that implement R&D and innovation support programs are TUBITAK, TTGV, K O S G E B , MoIT and Universit ies. A summary of the main allocation of funds within Turkey’s N I S between 2005-08 (latest data available) i s provided below in Table 1. An extended summary o f the key implementing agencies and their public support programs i s included in Annex 11.

Table 1: Public Expenditures on Innovation and Technology Programs IMPLEMENTING AGENCY 2005 2006 2007 2008

Universities 274.2 278.7 256.3 253.5 TUBfTAK (TUBITAK Research Centers) 108.8 155.0 141.8 183.3 TUBITAK Furkey Research Area Programs)* 346 0 415.0 425.0 450.0 Academic Research Projects 90.0 80.0 85.0 105.0 Industrial Research Projects (of companies) 116.0 215.0 215.0 175.0 Research Projects of Public Institutions 50.0 50.0 50.0 65.0 Defense and Space Research Projects 50.0 60.0 65.0 80.0 Researcher Development 25.0 5.0 5.0 15.0

Public Institutions (outside TUBITAK) 36.2 49.3 80.2 78.2 Nuclear Energy Council (TAEK) 6.3 13.1 20 18.9 Ministry of Industry and Trade** 11 16.9 17.6 Ministry of Agriculture and Rural Affairs 2.2 2.5 4 3.6

National Boron Research Institute*** 0.1 3 6 6.3

Science & Technology Awareness 15.0 5.0 5.0 10.0

Ministry of Health 0.1 6.2 5.2 4.9

M i n i s t r y of Energy*** 1 KOSGEB 12.5 5.4 4.6 6.5 TTGV 8.9 35.6 35.4 35.5 State Planning Organization 1. I 10.0 18 18 Undersecretary of Foreign Trade 40.0 42.0 63.5 n/a

Notes *TUBITAK funds the projects of other institutions’ R&D projects **Includes SAN-TEZ program that supports PhD students’ theses that aim to solve company specific problems, and the support for the physical infrastructure of Technoparks. ***Includes programs in which the projects of other institutions are supported. Source: State Planning Organization

15. There has been a surge in new policy measures in recent years aimed at strengthening the links between the research c o m m u n i t y and the private sector, and promoting the creation of science based start-ups in Turkey. In 2006-2008, 15 new policy measures were introduced to increase R&D, doubling the total number o f measures that are summarized in Annex 111. Table 2 summarizes the amount of public support for private R&D between 2006-2008. Grants, tax exemptions/credits, Table 2: Public R&D Support to Turkish Enterprises payment of social security

2006 2007 2008 contributions of new personnel, and low interest loans are some examples

215’0 215’0 175’0 of the various incentives. Th ree new TUBITAK

42.0 63.5 n’a measures incentivized research in UFT

5’4 4.6 6.5 clean technologies and energy KOSGEB TI’GV 35.6 35s4 35*5 efficiency/renewable energy. Among Miustry o f Industry and Trade ‘ I ’Ii.’ “a6 others, the following measures were

319.0 353.4 252.6 h e c t e d to finance the development Total Source:: State Planning Organization o f innovation-intensive start-ups: the “Technopreneurship” (Teknogirisim) program implemented under the new R&D Law No.5746 by al l public administrations with an R&D budget, “R&D Suppor t for S M E s ” of TUBITAK, and the “Pre-incubation Support” and “Start-up Support” of TTGV are some examples. Turkish entrepreneurs’ patent applications are supported by a program jo int ly coordinated by TUBITAK and

Data from Turkstat, 2007

6

TPE. Ministry o f Industry and Trade i s in the process o f designing a new program to support patent applications of enterprises. Along with the patent support, various programs are also designed to boost commercial izat ion o f R&D, examples of which include MoIT’s “San-Tez” project, “Commercial izat ion Pro ject Supports” and “Joint Technology Development Projects” of ‘ITGV. T h e Ministry of Industry and Trade designs “R&D Products Investment Suppor t Program’’ and “Marketing and Promotion Suppor t Program” to facilitate commercial izat ion o f industrial R&D activit ies starting from 2009. Incentives provided to the companies located in the technology development zones managed by the M i n i s t r y of Industry and Trade stimulates private sector R&D and research-industry collaboration. T h e “Scientific and Technological Cooperation Networks and Platforms Suppor t ” (ISBAP) o f TUBITAK serves the purpose of intensifylng the national and international collaboration between research institutions.

1 8 -

1 6 -

1 4 -

g12-

2 0 I - ;e VI

io8- Y

0 0 6 -

0 4 -

0 2 -

0 ,

to US$4.4 billion (PPP). T h i s represents a growth rate substantially higher than in the EU 27 (9Yo) and matched globally only by China. Growth in R&D intensity in Turkey has been s t e a d y increasing from 0.64% in 2000 to 0.76% in 2006 and

0 59 impressive performers in Eastern 0 54 0 48 0 71 Europe @e., the R&D intensity

increased by 0.16% in Hungary and 0 52 0.21% in the Czech Republic

between 2000-05), but not as fast as in China (where R&D intensity grew

GERD/GDPnew senes + GERD/GDPold series

ranks just lower than in the most

0 47 0 6

0 48 0 53 0 37

17. A key issue, however, i s how effectively R&D expenditures are being translated into innovation and productivity gains. W e Turkey’s public and private R&D expenditures are growing substantially and i t s R&D gap with many emerging economies in Eastern Europe i s narrowing, a key question i s how productively these expenditures are being employed to generate innovation and product iv i ty gains. As shown in Figure 3 preliminary evidence from 2005 suggests that the extent to which R&D was translated into productivity gains by the Turkey’s N I S was relatively limited. Around 5.6 percent of Turkey’s manufactured exports in 2005 were high-tech, which i s among the lowest in the OECD where the average i s 22 percent. Notably, most Central and Eastern European emerging economies had s d a r R&D intensities to Turkey but produced relatively more high-tech products. Data on patents awarded by the European Patent Off ice (EPO) also suggest that Turkish f m s may not be as inventive as their counterparts: In 2005 Turkey accounted for 1.9 patents per million of population, versus 4.2 in Poland, 4.3 in the Czech Republic and 18.9 in Hungary.

7

Figure 3: International Comparisons of R&D Intensity and High Tech Exports

s w A

FIN A A 3 5

I? B 3.0

& 2.5

2.0

b

r ii 1.8

1 .o

0.5

0.0 10.0 20.0 30.0 40.0 50.0 80.0 High Tech Exports (% of Total Manufactured Exports)

Source: OECD

18. Aggregate indicators of innovation and technology performance also suggest that Turkey may still lag behind its peers. For instance, accordmg to the Etlropean Innovation Scoreboard (EIS) that monitors the i nnova t ion per formance of the EU-27 nations plus ten OECD economies, T u r k e y was considered to have the weakest per formance a m o n g the 37 countries in 2007. Turlush Governmen t off icials have expressed reservations abou t the accuracy of some o f the statistics used in calculating the EIS, but wh i l e better data are needed, the overal l d i rect ion seems valid. Turkey's enterprise sector per formance on technology a n d innova t ion seems b e l o w that o f most comparable countries. This i s suppor ted by evidence from other indicators of i nnova t ion and technological sophistication. For example, the World Bank's Knowledge Economy Indicator (KEI) shows Turkey underper forming relative to the ten n e w EU m e m b e r countr ies and the average for upper-middle i n c o m e countries. In 2007-08, T u r k e y was better ranked global ly ( 5 3 9 than Romania and Bulgaria in terms o f the World E c o n o m i c Forum's G l o b a l Competit iveness Report's Technological Readiness and Innovationpillars but lagged b e h m d the other n e w EU m e m b e r states in Eastern Europe.

19. This may be because most of R&D in Turkey i s performed by the university sector and the share of the private sector, while increasing, i s st i l l low relative to EU and OECD levels. Despi te a surge in the last two years, Turkey's enterprise sector ( including both pr ivate and state-owned enterprises) i s s t i l l a relatively small player in terms of p e r f o r m i n g R&D relative to EU a n d OECD levels. Enterprises (public and private) p e r f o r m e d 41% o f to ta l R&D in T u r k e y in 2007 (compared to 23% in 2003), substantially l o w e r than the EU-27 and OECD averages o f 63% a n d 68% respectively in 2005. Conversely, 48% o f the R&D expendtures in Turkey in 2007 were p e r f o r m e d by 97 Turlush universit ies (of w h i c h 30 are privately-owned), relative to j u s t 23% on average in the EU-27 and 14.3% in the OECD. Yet, the share o f R&D financed by enterprises in T u r k e y i s higher a t 48% and m u c h closer to the EU-27 a n d OECD averages o f 54% a n d 62.5%, respectively. T h i s i s in contrast to the EU-27 or OECD countries where the enterprise sector accounts for a higher share of R&D per fo rmed than of R&D financed. Indeed, as it i s less risky to p e r f o r m than to finance R&D, a n d as pub l i c R&D expenditures in Turkey expand, one would expect t he private sector share in p e r f o r m i n g R&D to b e larger, as i t i s the case o f EU-27 . T h e fact that the Turkish enterprise sector currently accounts for a larger share o f to ta l R&D financed relative to R&D p e r f o r m e d may indicate "crowding out'' by the h igher education a n d government sectors, perhaps due to a scarcity of scientists a n d researchers, a n d enterprises are outsourc ing their R&D.

8

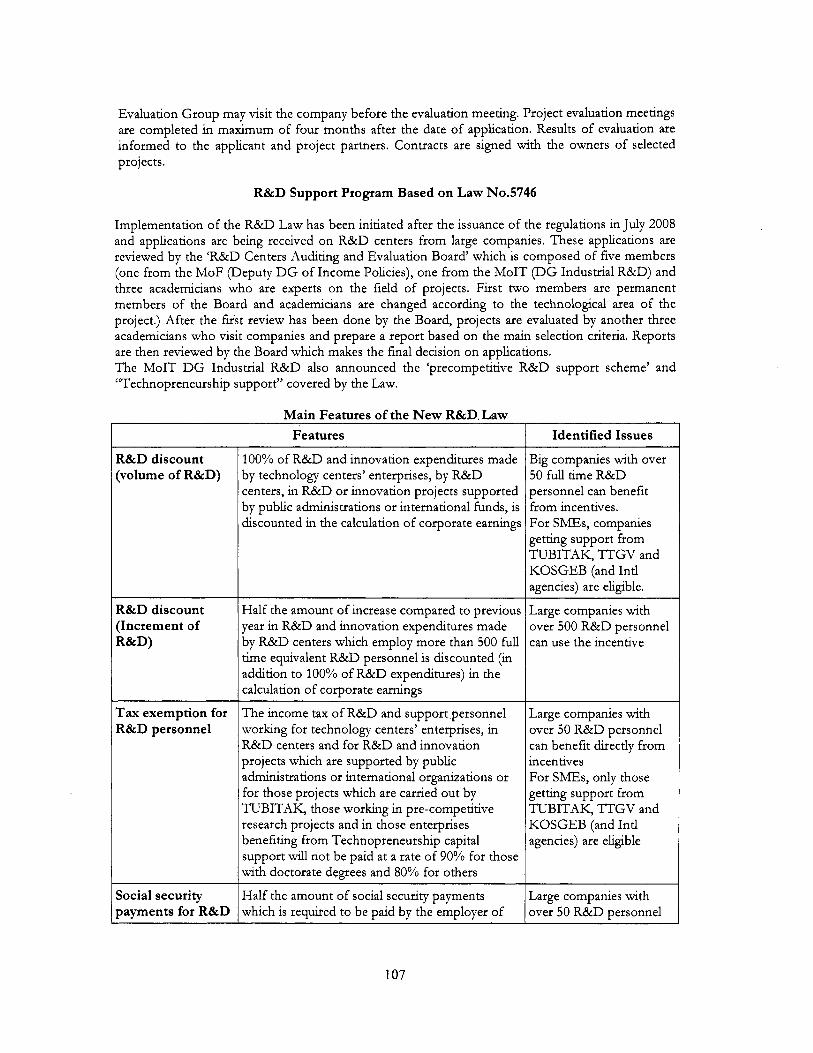

20. Also, the share of multinational’s R&D in the total private R&D in Turkey appears to be small compared to its peer countries. In 2000, Turkey was a m o n g the group of countries for w h i c h business R&D was essentially l e d by local enterprises with mul t i -nat ional corporations (MNCs) playing a secondary role. W h i l e this i n f o r m a t i o n needs to b e updated, the possibllity to attract large fore ign drrect investments i s welcome. A c c o r d i n g to OECD Science and Technology Indicators, in 2006 only 0.5% of to ta l R&D expenditures in T u r k e y were f inanced by fore ign sources, versus 7.6% in Russia and 10.7% in Hungary in 2005. In p a r t to change t h i s situation, in February 2008, the G o v e r n m e n t approved a n e w L a w on “Support ing Research a n d Deve lopmen t Activit ies” (Law No. 5746), imp lemen ted by the DG Indus t r i a l R&D of the M i n i s t r y o f Industry and Trade, that provides a range o f fiscal incentives for R&D activities by the pr ivate sector, (as we l l as for projects suppor ted by publ ic agencies a n d international institutions). T h e Governmen t hopes to induce a concentrat ion of R&D activities that will enable gains from economies of scale as we l l as attract R&D-intensive FDI. A summary o f the key R&D-related legislations i s presented in A n n e x IV.

21. The impact of Turkey’s innovation policy and programs may be enhanced with more coordination amongst the key players as well regular monitoring and evaluation of institutions, programs and policies. In v i e w of the significant changes a n d developments in the Turkish N I S in a relatively short p e r i o d of time, a n u m b e r of stakeholders men t ioned the need to develop the necessary inst i tu t ional set-ups, procedures a n d practices for agenda sett ing and priori t izat ion, implementat ion a n d policy learn ing between the d i f ferent pub l i c N I S institutions. In ternat ional experience suggests that the increased impor tance a n d complex i ty o f i nnova t ion policy and inst i tut ional arrangements of N I S can b reed n e w challenges that m a y affect po l i cy and inst i tut ional coherence a n d effectiveness (OECD 2005). This does not only relate to publ ic institutions but also refers to the establishment o f an effect ive a n d systematic n e t w o r k o f communicat ion between a l l N I S actors. A n o t h e r i m p o r t a n t t rend in m a n y OECD economies i s the establishment of systematic monitoring a n d evaluation systems for N I S institutions, programs a n d policies. In Turkey, such practices are s t i l l l i m i t e d but c o u l d b e increasingly relevant as publ ic expenditures are rising rapid ly towards EU standards and n e w policy init iatives are being designed a n d implemented.

22. In light of these findings, future analysis could include the in-depth benchmarking of institutional mechanisms, policies and programs within the Turkish N I S against EU and international best practices: Some areas that cou ld b e addressed include:

G i v e n the current emphasis on pub l i c support for industr ial R&D, should relatively m o r e support b e p r o v i d e d to the agriculture and service sectors (given their larger employment share)?

In the context o f a scarce supply o f h u m a n resources in the research sector, cou ld rising publ ic R&D expenditures b e possibly “crowding-out” private R&D?

W h a t i s the i m p a c t of the main support programs promoting R&D a n d technology diffusion in Turkey versus international practices a n d can their impac t b e increased through changes in design and /o r implementat ion? K e y programs inc lude pr ivate R&D tax exemptions, TfGV’s soft loans, TUBITAK’s match ing grant schemes, K O S G E B ’ s I C T up-grading and machinery improvemen t support, etc.

A r e there mechanisms employed in N I S systems in OECD economies that cou ld b e used in Turkey’s N I S that m a y i m p r o v e policy coord inat ion a n d enhance commun ica t i on a n d knowledge sharing between the various N I S actors?

9

B. Intellectual Property Rights Regime

23. This section compares Turkey’s IPR regime to that of the EU and identifies legislative and institutional issues that limit the protection of intellectual property and thus may hinder incentives for R&D and innovation activities. K e y findings include:

T h e legislative f ramework for intel lectual p roper t y rights i s broadly aligned with EU, no tw i ths tand ing certain divergences, most notably in the area o f indust r ia l p roper t y rights. T h e imp lemen ta t i on a n d enforcement o f IPR legislation in T u r k e y however has not reached EU levels, in te rms of legislative changes, capacity of key inst i tu t ions (IP courts, TPE) and cooperation be tween public, private and non-profit sectors. . T h e lack o f a u t o n o m y of the Turkish Patent Inst i tu te i s a f fect ing the quali ty o f i t s services.

.

24. Turkey’s IPR legislative framework i s broadly in line with the EU but the enforcement of the IPR framework in Turkey st i l l needs to be strengthened to reach EU levels. Overall, t he European Commission’s most recent T u r k e y Progress Repor t found that Turkey’s legislative f ramework in the area o f IPR i s broadly al igned with EU6 and the Governmen t i s currently prepar ing four m a i n pieces of IPR legislation in l ine with the EU requirements expected to b e rat i f ied by 2008.’ T h e r e are s t d l certain requi red legislative changes outstanding for w h i c h there i s no clear imp lemen ta t i on plan, i nc lud ing a n e w TPE Establ ishment L a w to ensure i t s autonomy, a legislative f ramework for industr ial p roper t y rights8 and legislation to establish a professional society for patent and trademark attorneys. T h e key issue h igh l ighted by the European Commission’s Progress Repor t re la t ing to the IPR regime i s enforcement. A c c o r d i n g to OECD data, Tu rkey was the fourth highest origin of seized counterfeit and p i ra ted products into the EU in 2006 (accounting for 7% of seized goods) after China (38%), Tha i l and (loyo) a n d Hong Kong (8%).9 Enfo rcemen t i s impa i red by three m a i n factors: an inadequate regulatory f ramework for enforcement @articularly in the case of indust r ia l p roper t y rights), weak capacity of enforcement institutions, and insuff icient cooperation a m o n g d i f ferent players.

25. The regulatory framework for the enforcement both commercial and industrial property rights legislation can be improved. T h e Turkish G o v e r n m e n t has made changes to the “Law on Intel lectual a n d Ar t is t ic Works ” to give m o r e incentives to copyr ight enforcement in l ine with EU law, but there rema in some problemat ic aspects, i nc lud ing inaccurate terminology, incompat ibht ies with other relevant Turkish legislation, a n d omissions relative to EU and international laws ( i.e. no articles for digital l i terary and artistic works). T h e implementat ion and enforcement of indust r ia l p roper t y rights i s even m o r e problemat ic as there are “severe deficiencies” in the regulatory framework.fO For example, the pol ice can currently take ex-off icio act ion in case o f copyr ight v io la t ion but not in cases of trademark infr ingement. As a result, there are infr ingements to we l l - known trade marks (registered packaging a n d three-dimensional trade marks) by Turkish companies that have negative externalities on technology diffusion a n d the abil ity o f other f m s to absorb advanced fore ign technology as foreign firms are discouraged from transferr ing technology.

26. Building the capacity of key institutions in the IPR regime i s critical to ensure better enforcement. A c c o r d i n g to the above men t ioned European Commission report, Turkey’s

“Turkey 2007 Progress Report”, Chapter 7: Intellectual Property Law, European Commission, November 2007. ’ These pieces of legislation include adjustments to the Laws on Geographical indications, Industrial Design, and Trade Marks and a new Patent and Intellectual Property Law. a T h e “Law Amending the Treaty on Granting European Patents”, which regulates the procedures of European Patents within the Member States of the European Patent Organisation, entered into force and the Law on the accession of Turkey to the Protection of New Varieties of Plants (UPOV) Convention was ratified and published.

“The Economic Impact o f Counterfeiting and Piracy,” OECD (2008). “Turkey 2007 Progress Report”, Chapter 7: Intellectual Property Law, European Commission, November 2007.

10

administrat ive capacity remains insuf f ic ient to ensure the level o f enforcement required by the EU Customs Union Decision, due to regular inconsistencies between TPE a n d IPR speciahzed courts. This relates to t h e small n u m b e r a n d weak capacity o f IP Courts: there are just 20 specialized IP courts located in the three main cities (13 in Istanbul, 5 in Ankara and 2 in Izm i r ) and a shortage o f judges trained in IPR (of the 7 judges who have received some IP training, only three are currently active, and others need further training). In cities without specialization courts, IPR cases are handled by the First Instance Civil and First Instance Cr im ina l Courts where the judges and prosecutors do not have suff icient knowledge in the IPR field, resul t ing in delays (appeals can take up to 2 years) and inconsistencies. T h e lack o f suitable training a n d experience amongst prosecutors and expert witnesses i s also a p r o b l e m as i t leads to the i n i t i a t i on o f c o u r t proceedings in instances w h e n it i s not appropriate and reduce confidence in the cou r t judgments a n d wider IPR regime. In order to overcome these problems, the Turkish Patent Inst i tu te a n d the Ministry o f Justice currently organize t ra in ing programs and international workshops for judges in cooperat ion with the European Patent O f f i c e (EPO), a n d are also trying to establish expert witness training activities. In addi t ion to these activities, to fur ther i m p r o v e the consistency between TPE a n d IP cour t judgments, n e w joint inst i tu t ional mechanisms for knowledge sharing a n d evaluation o f nat ional and international developments in IPR l a w (particularly in the f ie ld o f indust r ia l p roper t y rights) are p lanned between the TPE and Ministry of Justice that need to b e adequately designed, funded a n d implemented.

27. Coordination and cooperation amongst different stakeholders to improve enforcement has been strengthened but further progress i s required, particularly in the enforcement of copyright and related rights. A Coordmat ion B o a r d has been established in Turkey for the enforcement of intellectual p roper t y rights, with a specific mandate to ensure cooperat ion and coordmat ion a m o n g related agencies includes representatives from the Ministry of Justice, Ministry of Interior, Ministry of Cul ture a n d Tourism Copyrights and Cinema Directorate General, Customs Under-secretariat a n d various other pub l i c agencies. Strategies have been designed to i m p r o v e coord inat ion with posi t ive results but ongoing ef for ts are needed, for example with the cooperat ion between pol ice and customs. In addition, greater e f for ts need to b e made in ensuring eff icient p ro tec t i on o f intellectual p roper t y rights of Turkish enterprises a n d in enhancing pub l i c awareness of intellectual proper ty right protection.

28. The lack of functional autonomy i s affecting the quality of services provided by the Turkish Patent Institute. In recent years the TPE has modern i zed i t s entire institution inc ludmg physical fachties, i m p r o v e d search systems, staff ing sk i l ls , in ternal and external IT structure, on l ine services a n d publ ic relations, and the establishment o f a n on-l ine trademarks application system. T h i s has i m p r o v e d significantly the speed a n d consistency o f i t s services and in 2007, the TPE carried out 83 patent research and investigation requests, a lmost three times the n u m b e r in 2005 (28). However , TPE does not have enough quali f ied permanent s ta f f to m a t c h the demand for i t s services a n d as a result i t does not have a solid reputat ion for consistent, t imely decision-mahng. Moreover , i t currently covers j u s t 40% o f the In ternat ional Patent Classifications (IPC), with the examination o f a lmost a l l Turkish patent applications (there were 1,838 applications in the f u s t 9 months of 2007) outsourced abroad (to Sweden, Denmark, Russia a n d Austria, a n d by the EPO). Patent applications that are outsourced overseas are up to 50% m o r e expensive than that of applications dealt with by the TPE b v e n the translation costs, preparation charges a n d h lgher fees o f foreign patent offices) and in a d d t i o n there are o f ten logistical delays. T h e TPE i s short-staffed, in part, because the L a w establishing the TPE sets l i m i t s on the number of s taf f to b e recru i ted for each cadre, restr ict ing the n u m b e r o f permanent s ta f f that can b e h i red to mee t the substantial rise in domestic demand for patents in recent years. In t h i s context, there i s a n urgent need to increase the n u m b e r o f technology areas where TPE patent specialists undertake patent researches and investigations, and patent specialists with appropriate qualif ications must b e employed and trained according to research areas.

.

11

29. Given these findings, issues that merit further analysis to guide reform include:

. How i m p o r t a n t i s the IPR regune in affect ing R&D investment decisions for d i f ferent types o f enterprises (SMEs, large, foreign) as w e l l as in the commercial izat ion of R&D? How m u c h does the IPR regime affect the inflow o f R&D-intensive FDI, the technology transfer from foreign f i r m s to domestic subsidiaries or partners, and the l icensing of proprietary foreign technology to domestic f i r m s ? W h a t i s the i m p a c t o f the IPR regime on innova t ion in key sectors such as agriculture, ICT /so f tware ( including financial services) and clean technology? How effective are government incentives for IPR enforcement relative to EU practices?

.

. C. Collaboration between the Enterprise and Research Sectors

30. between the enterprise and research sectors and identifies the following issues: . This section examines the institutional and regulatory fiamework for collaboration

Some regulations (e.g., the university revo lv ing fund regulations) create disincentives for researchers to p rov ide services to the enterprise sector a n d thus reduce the mobhty o f researchers. . T h e current IP laws favor researchers in the al location of royalties for commerciahzed research, h inder ing universit ies to commercial ize R&D outputs. . Incentives and support for universit ies a n d researchers to commercial ize R&D are weak. . T h e n u m b e r a n d impac t of in termediary institutions that encourage col laboration between the enterprise a n d research sectors c o u l d b e increased (e.g., techno-parks, technology transfer offices, early stage financing).

31. A central issue for the commercial outputs o f any N I S i s the collaboration between the private sector and the knowledge institutions. Turkey has a solid knowledge-base with well- known R D I s a n d universities, a n d scientif ic output has r isen substantially during 1990-2006 and, in particular, in the last f ive years, following changes in promotion criteria and greater pub l i c support for researchers. T h e n u m b e r o f publ ished articles by scientists p e r d o n inhabitants in Turkey rose from 95 in 2000 to 252 in 2006, the highest growth in the world, with Turkey’s world rank ing in output of scientif ic a n d technical articles i m p r o v e d from 34th to 19th.11 Similarly, patent applications and registrations by Turlush residents both domestically and overseas have grown quickly during this period, with patent applications to the European Patent O f f i c e growing by 360% during 2000-05 the second highest growth rate in the world. Y e t this growth stems par t ly from Turkey’s low base, as in 2006 1.9 EPO patents were granted to Turkey p e r million of populat ion, versus 18.9 to Hungary and 128 to the EU-27 as a whole. However , Turkey’s N I S per formance in commeniah@g (wing) knowledge i s .not following the same pace as i t s per formance in terms o f generating knowledge. Although data on spin-off start-ups a n d technology l icensing are not avadable, the i n fo rma t ion gathered in Section I11 suggest otherwise. I t i s thus impor tan t to consider whether the existing inst i tut ional and regulatory f ramework under ly ing the col laboration between these institutions and the private sector creates an appropriate conducive environment.

32. One o f the important elements affecting the collaboration between the public universities and the enterprise sector are the “University Revolving Fund Regulations.” Accord ing to the m o d i f i e d regulations issued by the M in i s t r y of Finance in 2004, academicians at publ ic universities who prov ide consultancy services have to pay 55% of their i ncome to the university, such that their n e t i n c o m e after tax amounts to 25% of the to ta l service income.12 In addition, a deduction i s made from the monthly salary of an academician i f he/she has been paid for

Thomson’s I S 1 Web of Science. University pays to the Treasury 15% of i t s 55% share (on January 24, 2008, the Minister of Finance announced that t h i s

share would be decreased from 15% to 5%).

12

a service in the respective month. To b e exempted from t h i s regulation, a company should b e located in a Technopark, following the provisions of the “2001 Technology Deve lopmen t Zones W Z ) Law.” In terv iews with the pr ivate sector revealed that the revo lv ing fund seems to work the same way as that a tax-wedge affects economic activity: limiting voluntary transaction and therefore reducing the gains from trade between researchers w i h g to supply technical sk i l l s a n d f i r m s willing to buy t h e m to t h e benef i t of a third par ty (university). W h i l e a closer assessment o f the revolv ing fund i s needed, i t s effect over the Technoparks industry was equivalent to a subsidy with the consequent expansion of the supply of Technoparks. As i t i s c o m m o n in the case of the provision of any subsidy, the hypothesis o f an over-supply of Technoparks can not b e rejected apkok.

33. T h e regulation o f the ownership o f commercialized inventions, and thus the distribution of royalties between the researcher and the host institution, i s also important. Current legislation allows the successful i nven to r to reap substantially m o r e of the benefits than his/her host inst i tut ion, with any legal rights obta ined as a result of research carried out in universit ies hosting the academicians.13 I f the results o f research are commercialized, the m a x i m u m amoun t o f royalties that can b e obta ined by universit ies i s h t e d to the amoun t of support they have p rov ided to the academician for the durat ion o f the research. T h i s i s seen as one possible reason for the lack of university investment a n d support for applied research a n d commercial izat ion services, i nc lud ing the support for patent applications, the cost of w h i c h i s too high for many researchers. T h e risk of under-investment from both sides, either the host institution or the researcher, i s a central p r o b l e m of the legal f ramework underp inn ing the contractual relat ionship between these two agents. Untd recently a t least, the OECD economies seemed to b e convergmg to an overal l design that, with some variation, m i r r o r e d the U n i t e d States’ Buyb-Dole Act (1980) that established a uniform patent po l i cy a m o n g the m a n y federal agencies that f unded research in the U S and w h i c h p roved highly successful in incent iv iz ing researchers to pursue applied research, develop intellectual property, a n d start their own companies or find other ways to commercial ize their research (i.e., l icensing to companies) and universit ies to develop inst i tu t ional mechanisms (licensing programs, technology transfer offices) to support researchers’ commercial izat ion efforts. The re are a variety of other mechanisms employed in nat ional IPR regunes to increase incentives for hinovators14 that Turkish policy-makers c o u l d consider a n d adapt to the T u r k i s h context to strengthen incentives among both researchers and universit ies to undertake m o r e applied research and m o r e impor tant ly with the enterprises to commercial ize it.

34. Another factor affecting the commercialization o f research i s the legal provision regulating the start-up o f new companies. M a n y universit ies throughout the OECD economies have repl icated the U S experience by al lowing scientists to f l oa t /own start-ups whde working at universities, as w e l l by providing “entrepreneurial” sabbaticals for researchers to start a business based on a n e w inven t ion instead of licensing it. V e r y o f t e n the sabbatical takes up to two years and re-entry i s guaranteed in case o f f d u r e . I t appears that, beyond the n o r m a l academic sabbatical, there are no s d a r provisions in Turkey. Mobihty between the academic a n d the business sectors i s supposed to b e encouraged through part icipation in joint-research projects in Technoparks. In addition, entrepreneurial (profit-oriented) activities are not always. w e l l accepted culturally by academicians and rules for promotion in universit ies re ly a lmost exclusively on academic achievement.

35. Rules regarding academic promotion do not encourage collaboration with the business sector, with the number o f scientific articles produced being the main criterion for career ascension. F e w pr ivate universit ies use R&D related indicators (such as the n u m b e r o f research projects, co-operation with the private sector, n u m b e r of patents, etc) in addi t ion to output

l3 Intellectual Property Law No 551, Article 41. l4 Austraha, for example, introduced an “innovation patent” system in 2001 to provide simple, inexpensive protection for inventions deemed insufficiently inventive to meet the threshold required for standard patents.

13

of articles.15 T h i s however m a y not b e sustainable on a compet i t ive basis if large pub l i c o w n e d institutes that do not place the same requirement are able to o f fe r equally attractive bonuses for researchers. Academicians with successful R&D commercial izat ion track records no te that there i s a strong culture within universit ies w h i c h does not favor prof i t -or iented research or a closer cooperat ion with the pr ivate sector. As a result, entrepreneurial activities, as those associated with the spi l l -over of invent ions and start-up of companies by fo rmer academicians, are also not favorably seen.

36. Under-investment in the commercialization o f research activities i s also reflected in the limited development o f key institutional intermediaries such as technology transfer offices. Technology transfer off ices (’TTOs) can p lay a n i m p o r t a n t coordmat ion ro le during the commercial izat ion stage of research, and in encouraging researchers and firms to init iate n e w col laborative projects. Researchers also need training a n d m e n t o r i n g on business p lanning and other key topics l ike IPR management a n d commercialization. T h e lack o f specialized institutions makes i t d i f f i cu l t for firms to b e aware o f scientif ic and technological experts as w e l l as research results and patented invent ions produced at universit ies that c o u l d b e usefu l to them. T h e absence o f a specialized organization to deal with technology transfer a n d commercial izat ion o f R&D outputs also leads to problems in sharing and the use of IPR. Recently TUBITAK a n d TPE have begun providing support to researchers for patenting, with the f i r s t , pilot “Patent a n d Technology Transfer O f f i ce ” be ing established at G a z i Univers i ty in Ankara. T h e r e are also attempts by a f e w universit ies to create technology transfer offices, as i l lustrated by the case of Inovent , a company created at Sabanci Univers i ty (in GOBS Technopark located in the Gebze Organized Indust r ia l Zone) to undertake technology transfer and commercial izat ion activities a n d the Turkish Governmen t has shown interest in supporting these efforts.16

37. Many universities and companies have expressed interest in establishing and joining, respectively, Technoparks in Turkey, but collaboration between f i rms and research sectors within the Technoparks and the creation o f high-tech start-ups i s low. By 2008, 31 Technoparks have been approved in Turkey by the MoIT (under the Technology Deve lopmen t Zones L a w o f 2003) with 18 of t h e m currently active a n d housing 890 companies (of w h i c h 32 are foreign) that emp loy 7,437 R&D staf f and 2,308 technical support personnel a n d imp lemen t 2,671 R&D projects (in ICT, electronics, defense, telecommunication, medical/bio-medical, advance materials, industr ial design and env i ronmenta l technologies) a n d account for some US$250 million of expor t revenues (US$144 million in 2006).17 Technoparks are supposed to encourage start-ups a n d spin-offs from universit ies and pub l i c R D I s by o f fe r i ng a comb ina t ion of infrastructure support a n d business development services in addi t ion to the natura l advantages o f proximity to the host research institution. In the case of Turkey, given the generosity of the tax incentives p rov ided by the Technology Deve lopmen t Zones Law, there i s a concern that the infrastructure-support side of the business has expanded to the det r iment of the provision of value-added services, w h i c h are very m u c h needed and are a key pa r t o f successful Technoparks a round the world. Indeed, ren t costs in m a n y Technoparks can b e up to three times the marke t rates. Further, Technoparks seem to b e dominated by the R&D departments of large companies seekmg to take advantage of the addit ional tax incentives, raising concerns about the addit ional i ty o f the scheme in terms of private R&D investment. As the n e w R&D L a w extends the benefi ts of p r o v i d e d by Technoparks to R&D activities larger than a certain threshold a n d thus will reduce, to some extent, the attractiveness of Technoparks for large companies. By law, the tax incentives for Technoparks were to b e phased out by 2013 but - as i t i s c o m m o n in such cases - there are segments of society, especially Technopark owners, arguing for the extension of the incentives until 2023. Desp i te al l these caveats, some

l5 I t should also be noted that there are different rules and practices applied for academic promotion at different universities, and even at different faculties of the same university in Turkey. l6 Inovent has evaluated over 1000 projects in the last 2 years from 7 universities, and has accepted 130 of these. Other universities moving in this direction include METLJ, Mersin, Yeditepe and Gazi that are taking steps to pilot 3 3 ’ 0 s . l7 Ministry of Industry and Trade, 2008.

14

potential ly interesting cases are identif iable, as i l lustrated by the nurturing of a v ib ran t software industry by Cyberpark a n d METUTECH that have started to o f f e r some value-added services to their tenants but this i s s t d l evo lv ing a n d has a long way to go in Turkey.

38. areas:

In light o f the findings of this section, future work could be taken in the following