Embed Size (px)

Citation preview

DTI ECONOMICS PAPER NO. 3

UK Competitiveness: moving to the next stage

BY PROFESSOR MICHAEL E PORTERAND CHRISTIAN H M KETELS

INSTITUTE OF STRATEGY ANDCOMPETITIVENESS, HARVARD BUSINESS SCHOOL

MAY 2003

The DTI drives our ambition of‘prosperity for all’ by working to createthe best environment for businesssuccess in the UK. We help peopleand companies become moreproductive by promoting enterprise,innovation and creativity.

We champion UK business at homeand abroad. We invest heavily inworld-class science and technology.We protect the rights of workingpeople and consumers. And westand up for fair and open markets in the UK, Europe and the world.

ECONOMIC & SOCIALRESEARCH COUNCIL

The ESRC is the UK’s largest fundingagency for research and postgraduatetraining relating to social and economicissues. It provides independent, high-quality, relevant research to business,the public sector and Government. The ESRC invests more than £76 million every year in social scienceand at any time is supporting some2,000 researchers in academicinstitutions and research policyinstitutes. It also funds postgraduatetraining within the social sciences tonurture the researchers of tomorrow. More at http://www.esrc.ac.uk

DTI ECONOMICS PAPER NO. 3

UK Competitiveness: moving to the next stage

BY PROFESSOR MICHAEL E PORTERAND CHRISTIAN H M KETELS

INSTITUTE OF STRATEGY ANDCOMPETITIVENESS, HARVARD BUSINESS SCHOOL

MAY 2003

1UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

ForewordThe persistence of the productivity gap with our main competitors is a key issue in UKeconomic policy-making. In order to understand this problem better, the DTI and theESRC asked Professor Michael Porter, of the Institute of Strategy and Competitiveness atHarvard Business School, to investigate the current state of UK competitiveness.

Professor Porter points to the UK’s recent success in raising prosperity. He demonstratesthe UK’s strengths in terms of science and engineering, its supportive market framework,and its improved macroeconomic environment. However, he highlights continuedweaknesses in terms of skills, clusters of interconnected companies and innovation.

The most valuable message is that the UK needs a new conception of competitiveness.In the past, the UK has been very successful in implementing key market-based reforms:deregulation, privatisation and competition. But these aspects of industrial policy are nowrunning into diminishing returns.

Professor Porter argues that the UK now needs an approach focussed on improving skills,stimulating innovation and fostering enterprise. It is only by building such capacity, thatwe will be able to move to the next stage of improving competitiveness and achievesustained higher levels of prosperity.

In addition to his policy recommendations, Professor Porter has set out an ambitiousresearch agenda for the UK. Both the DTI and ESRC are committed to improving thestate of knowledge about the UK economy in order to provide a robust evidence base forfuture policy development. Much of this work will be carried out through AIM, themanagement research initiative supported by the ESRC and led by Professor Anne Huff.Other investments by the ESRC will also make a significant contribution.

We hope Professor Porter's analysis will stimulate debate and form part of a widerdialogue involving the DTI, ESRC and all with an interest in the economic performanceof the UK.

Vicky Pryce Frances CairncrossChief Economist and Chair, Economic andDirector-General Economics, Social Research CouncilDTI

2

DTI Economics Papers

The reviews of the DTI in Autumn 2001 placed analysis at the heart of policy-making. Aspart of this process the Department has decided to make its analysis and evidence basemore publicly available through the publication of a series of DTI Economics Papers thatwill set out the thinking underpinning policy development. Previous titles include:

Bundling, Tying and Portfolio Effects, Professor Barry Nalebuff (Yale University),February 2003

A Comparative Study of the British and Italian Clothing and Textile Industries,

Nicholas Owen (DTI), Alan Canon Jones (London College of Fashion), April 2003

The views expressed within DTI Economics Papers are those of the authors and shouldnot be treated as Government policy. We welcome feedback on the issues raised by theDTI Economics Papers, and comments should be sent to [email protected]

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

3

Contents

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

1 Introduction 4

a) Project Background 4

b) Key Findings 5

2 Overall Performance of the UK Economy 7

a) Prosperity 7

b) Productivity 9

c) Internationalisation, Innovation and Productivity Growth 13

3 Competitiveness and the UK BusinessEnvironment: Summary of the Evidence 18

a) Macroeconomic, Political, Social, and Legal Context 18

b) Microeconomic Business Environment 19

c) Clusters 27

d) Roles, Institutions, and Processes 30

e) Influences of Different Geographical Levels 32

4 Competitiveness and UK CompanyBehaviour: The Role of Management 34

a) UK Company Performance 34

b) UK Company Operations and Strategy: Competitive Assessment 35

c) Understanding UK Company Behaviour 38

5 Implications for Policy and Future Research 42

a) UK Competitiveness at the Transition to a New Stage 43

b) The UK Competitiveness Agenda 2003 45

c) Implications for UK Competitiveness Research 47

References and Data Sources 49

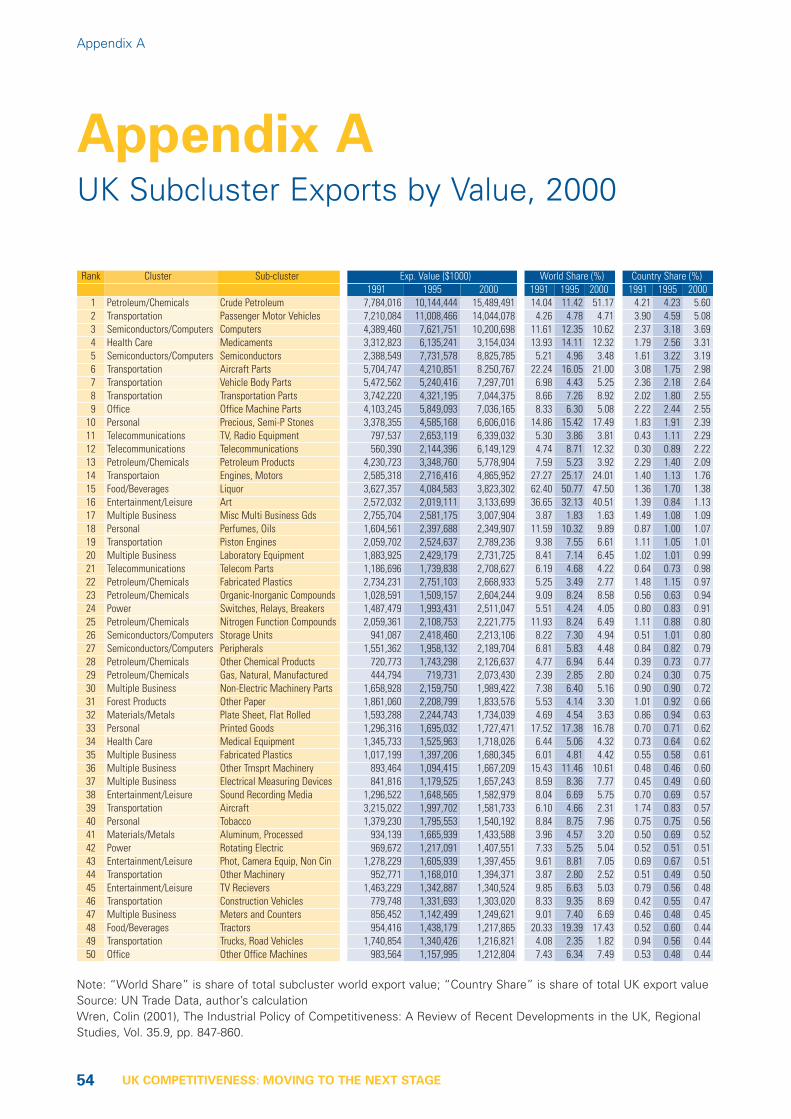

Appendix A: UK Subcluster Exports by Value, 2000 54

Appendix B: Convergence or Divergence Among Regions - Selected Countries 55

4 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

1

Introduction

a) Project Background

In October 2002, the Economic and Social Research Council (ESRC) appointed ProfessorMichael Porter and his team to conduct a brief, three-month review of the existingevidence on UK competitiveness. The effort was funded jointly by the ESRC and theDepartment of Trade and Industry (DTI). The London School of Economics and PoliticalScience (LSE) graciously served as the UK-based academic sponsor of the project.

The objective of this review is to synthesise, interpret, and draw implications from theavailable evidence on the competitiveness of the United Kingdom, applying the Portercompetitiveness framework and drawing on the learning from dozens of nationalcompetitiveness projects over the last decade. The ESRC asked that special attention bepaid to the role of management in UK competitiveness.

The review is based primarily on existing, and sometimes conflicting, research by others.We have also analysed existing detailed data from the Global Competitiveness Report(GCR) that has not been previously published, but we have not created any new primarydata. Our findings build on the existing research on UK competitiveness and confirmmany of its findings. We aim to provide an integrative framework that can aid scholarsand decision makers in the public and private sectors to set priorities and identifymissing pieces in the UK competitiveness agenda.

The integrative framework provided by the Porter microeconomic approach tocompetitiveness goes beyond a growth accounting decomposition of economicperformance to identify the probable causes underlying UK economic performance. Italso offers a holistic way of assessing their interrelationships and the changingconstraints on UK productivity and prosperity growth over time. We hope that thisframework will enable a more informed policy debate in the UK on how to manage thetransition to the next stage of competitiveness.

This review is decidedly not a comprehensive study of UK competitiveness but isintended to provide high-level guidance to policy makers on broad priorities, and to assistin defining a priority research agenda for the ESRC. In particular, this review will bemade available to the ESRC initiative on management headed by Professor Anne Huff.

A preliminary version of this report was delivered by Professor Michael E. Porter in apublic lecture at the LSE on January 22nd 2003. This report also draws upon discussions

5UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

during and after the lecture and the comments made in a closed policy workshop withparticipants invited by DTI.

b) Key Findings

Pessimism and the lack of an overall strategic perspective characterise much of thecurrent public discussion about UK competitiveness. Attention is focused on theprosperity and productivity gap that remains with the United States and primaryEuropean rivals Germany and France. This performance gap persists despite the UK’s farreaching economic policy reforms of the last two decades. A search for explanations hasso far not reached a clear consensus.

Looking at the UK’s future competitiveness, concerns dominate as well. A recent surveyof UK business leaders reported a significantly more negative view on the future versuscurrent UK competitiveness.1 Changing priorities in UK economic policy are perceived tothreaten the achievements of the past two decades, e.g. low levels of regulation andtaxation. Also, other countries are seen as having matched many of the reforms thatgave the UK a competitive edge in the past.

Our findings agree on many of the specifics, but are different in overall tone. The UK hasin fact achieved a remarkable success in halting the economy’s protracted downwardeconomic trajectory of the pre-1980 period. On many indicators of economicperformance, the UK has kept pace with, if not outpaced, competing locations, especially in Europe.2 This success in terms of economic performance is directly linked to the far-reaching economic policy reforms by successive UK governments that havefundamentally changed the macroeconomic and, more importantly, the microeconomiccontext for competition.

However, the UK currently faces a transition to a new phase of economic development.The old approach to economic development is reaching the limits of its effectiveness,and government, companies, and other institutions need to rethink their policy priorities.This rethinking is not a sign of the past strategy’s failure; it is a necessary part ofgraduating to the new stage. A public consensus on the direction of the transition and onthe next stage of the country’s competitiveness would help to manage the uncertaintiesof this process. The absence of such a consensus at a time when the old policyapproach is running its course explains much of the puzzlement and even pessimism inthe current UK debate.

We find that the competitiveness agenda facing UK leaders in government and businessreflects the challenges of moving from a location competing on relatively low costs ofdoing business to a location competing on unique value and innovation. This transitionrequires investments in different elements of the business environment, upgrading ofcompany strategies, and the creation or strengthening of new types of institutions.

As to management, we find that the role of management cannot be separated from the

Intoduction

6 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

Introduction

overall competitiveness issues facing the country. Management and its decisions areboth an input and a result of the business environment. Thus UK managementperformance in many ways either reflects weaknesses in the business environment orinvolves decisions that are consistent with the current business environment eventhough they do not improve competitiveness. Management practices, then, are not atthe core of the UK competitiveness challenge; however, there is always room forimprovement. As part of the overall effort to upgrade UK competitiveness there is a clearrole for management. Efforts to upgrade management will not however be sufficient toachieve a sustained improvement in UK competitiveness.

References

1 CBI (2002)

2 European Commission (2002)

7UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

2

Overall Performanceof the UK Economy

Competitiveness remains a concept that is not well understood, despite widespreadacceptance of its importance.3 To understand competitiveness, the starting point mustbe the sources of a nation’s prosperity. A nation’s standard of living is determined by theproductivity of its economy, which is measured by the value of goods and servicesproduced per unit of the nation’s human, capital and natural resources. Productivitydepends both on the value of a nation’s products and services, measured by the pricesthey can command in open markets, and the efficiency with which they can beproduced. True competitiveness then, is measured by productivity. Productivity allows anation to support high wages, a strong currency and attractive returns to capital, andwith them a high standard of living.

The UK economy has performed well on the most important economic metrics in thelast two decades, and the awareness of competitiveness issues has increased markedly.Prosperity has improved in absolute terms and has also increased relative to many otheradvanced economies. Prosperity gains relative to other locations benefited from asignificant increase in the level of labour force utilisation in the economy (hours workedper employee, employment rate, and labour force participation rate). Labour productivitygrowth has been good, but not significantly above the level in other economies. Otherintermediate measures of competitiveness, such as the UK’s world export market shareand FDI attraction, have been stable.

Despite these improvements, the levels of productivity and prosperity in the UK still lagmany other advanced economies. With labour force utilisation already at a high level,only further catch-up in labour productivity will be able to reduce the gap. Labourproductivity can increase through higher skill labour inputs, higher capital intensity, andhigher total factor productivity (technology). In all three areas the UK currently lagsbehind important competitors such as the United States, France and Germany. It willneed to close these gaps to finally achieve prosperity catch-up. This will requiresustained improvements in the microeconomic business environment.

a) Prosperity

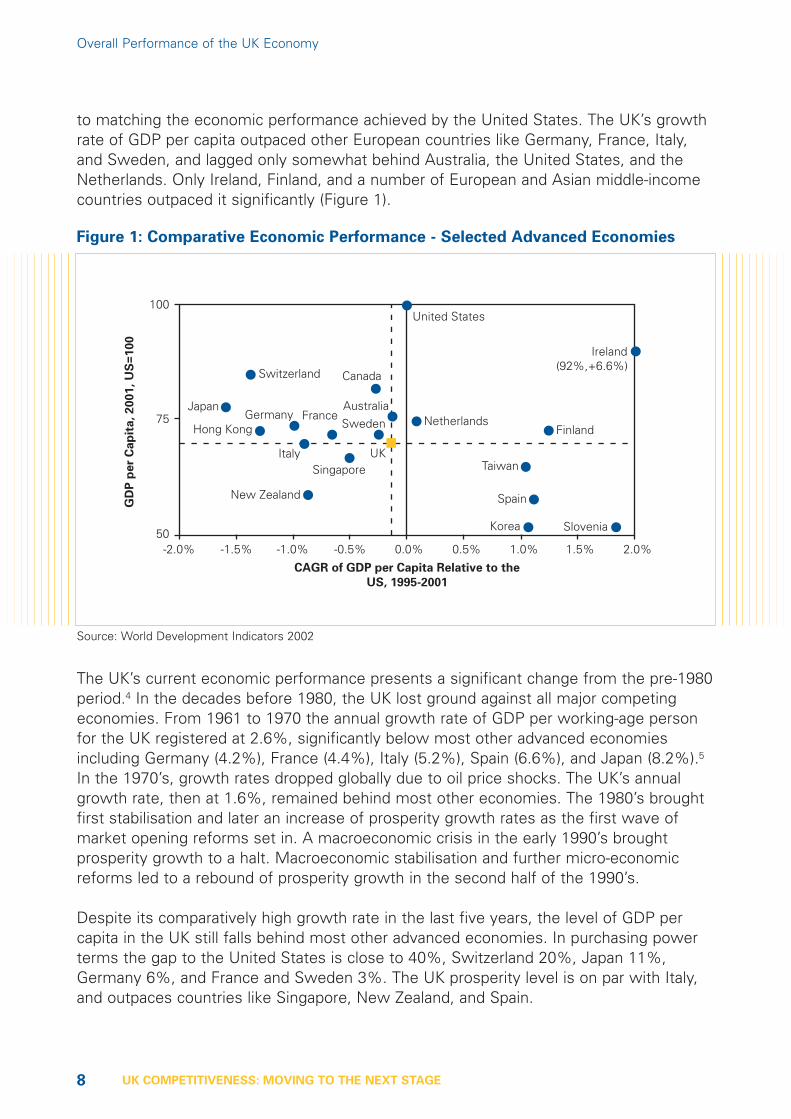

In the last five years, the UK was one of the few advanced economies that came close

8

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

to matching the economic performance achieved by the United States. The UK’s growthrate of GDP per capita outpaced other European countries like Germany, France, Italy,and Sweden, and lagged only somewhat behind Australia, the United States, and theNetherlands. Only Ireland, Finland, and a number of European and Asian middle-incomecountries outpaced it significantly (Figure 1).

The UK’s current economic performance presents a significant change from the pre-1980period.4 In the decades before 1980, the UK lost ground against all major competingeconomies. From 1961 to 1970 the annual growth rate of GDP per working-age personfor the UK registered at 2.6%, significantly below most other advanced economiesincluding Germany (4.2%), France (4.4%), Italy (5.2%), Spain (6.6%), and Japan (8.2%).5

In the 1970’s, growth rates dropped globally due to oil price shocks. The UK’s annualgrowth rate, then at 1.6%, remained behind most other economies. The 1980’s broughtfirst stabilisation and later an increase of prosperity growth rates as the first wave ofmarket opening reforms set in. A macroeconomic crisis in the early 1990’s broughtprosperity growth to a halt. Macroeconomic stabilisation and further micro-economicreforms led to a rebound of prosperity growth in the second half of the 1990’s.

Despite its comparatively high growth rate in the last five years, the level of GDP percapita in the UK still falls behind most other advanced economies. In purchasing powerterms the gap to the United States is close to 40%, Switzerland 20%, Japan 11%,Germany 6%, and France and Sweden 3%. The UK prosperity level is on par with Italy,and outpaces countries like Singapore, New Zealand, and Spain.

GD

P p

er

Cap

ita

, 2

00

1,

US

=1

00

CAGR of GDP per Capita Relative to the

US, 1995-2001

75

50

100

Switzerland

Japan

Hong Kong

New Zealand

SingaporeItaly

Germany

Canada

FranceSweden

UK

Australia

United States

Netherlands

Taiwan

Spain

Korea Slovenia

Finland

Ireland

-2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0%

(92%,+6.6%)

Figure 1: Comparative Economic Performance - Selected Advanced Economies

Source: World Development Indicators 2002

9

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

The UK has, according to 1996 data, a high level of poverty relative to other Europeancountries at similar levels of prosperity.6 The existence of such pockets of povertyindicates an untapped potential for productivity growth as well as a social challenge. It isalso a signal for remaining weaknesses in the business environment, such as lack oftraining, discrimination, a low level of local government responsibility, and the separationof social and economic policies. The efforts of the last few years to address this problemmay have already led to an improvement in the situation, but no consistent data on thisis currently available.

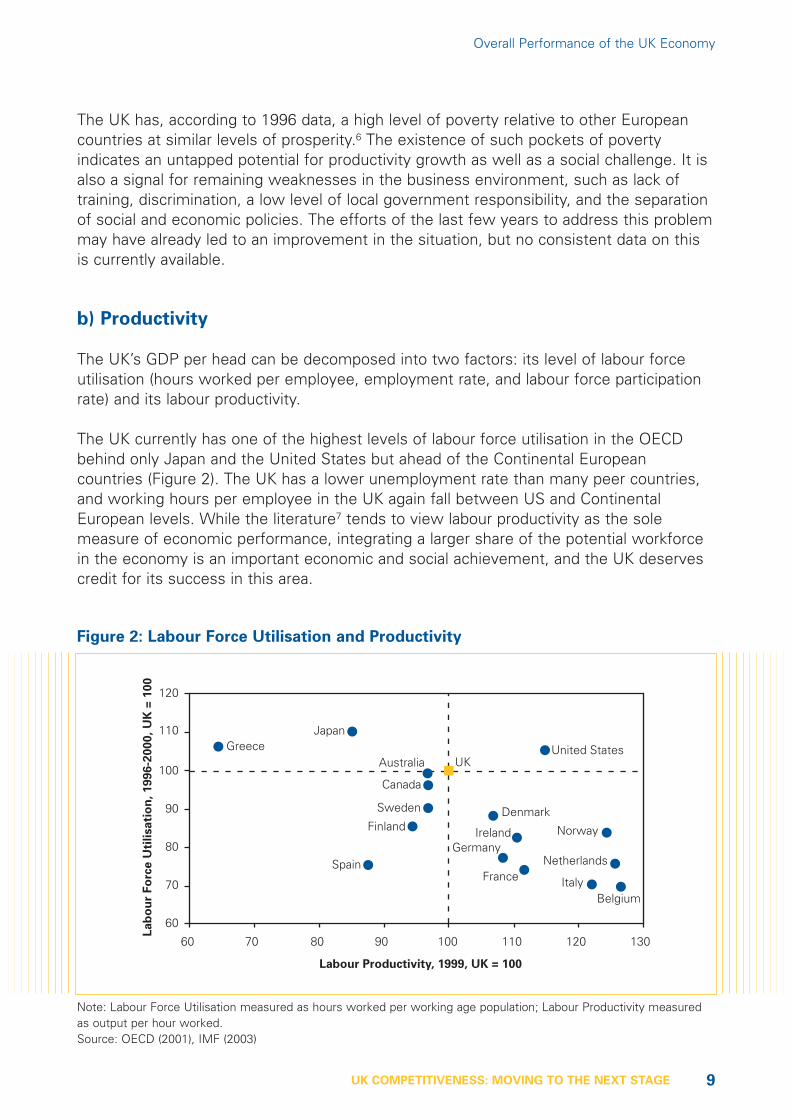

b) Productivity

The UK’s GDP per head can be decomposed into two factors: its level of labour forceutilisation (hours worked per employee, employment rate, and labour force participationrate) and its labour productivity.

The UK currently has one of the highest levels of labour force utilisation in the OECDbehind only Japan and the United States but ahead of the Continental Europeancountries (Figure 2). The UK has a lower unemployment rate than many peer countries,and working hours per employee in the UK again fall between US and ContinentalEuropean levels. While the literature7 tends to view labour productivity as the solemeasure of economic performance, integrating a larger share of the potential workforcein the economy is an important economic and social achievement, and the UK deservescredit for its success in this area.

Lab

ou

r Fo

rce U

tilisati

on

, 1996-2

000,

UK

= 1

00

JapanGreece

ItalyBelgium

Germany

Canada

France

Sweden

UKAustraliaUnited States

Netherlands

Norway

DenmarkFinland

Spain

Ireland

Labour Productivity, 1999, UK = 100

60

60

70

80

90

100

110

120

70 80 90 100 110 120 130

Figure 2: Labour Force Utilisation and Productivity

Note: Labour Force Utilisation measured as hours worked per working age population; Labour Productivity measuredas output per hour worked.Source: OECD (2001), IMF (2003)

10

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

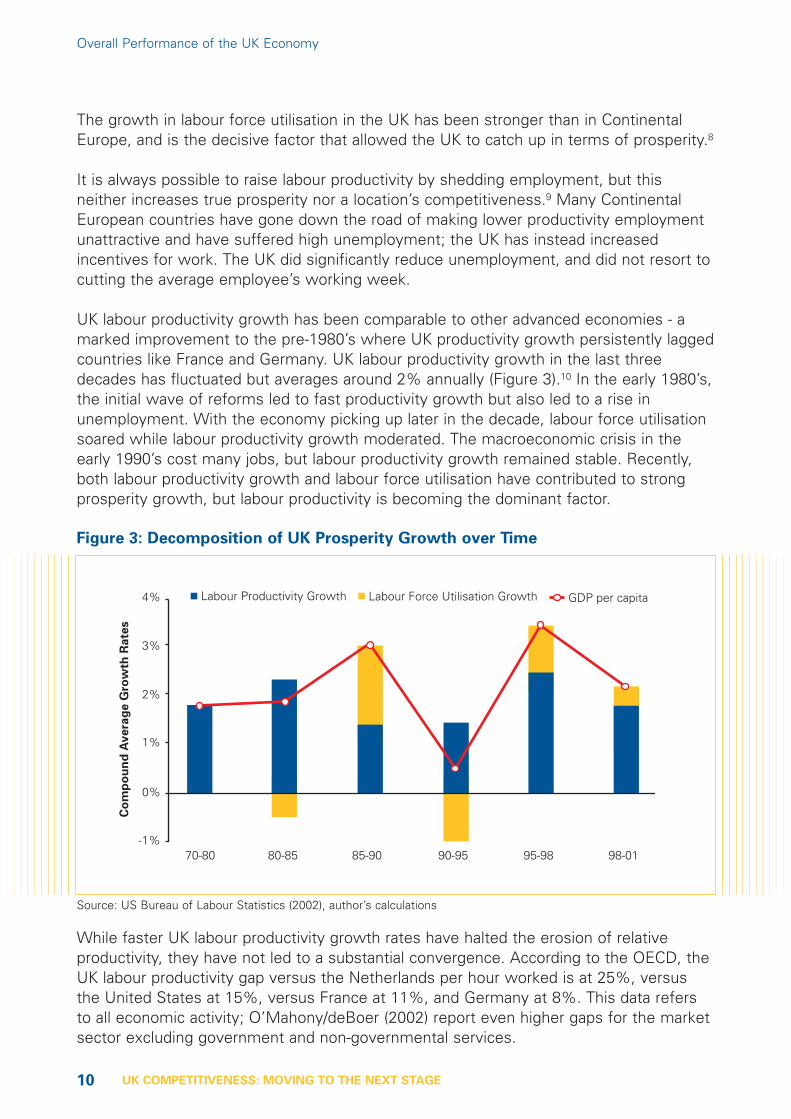

The growth in labour force utilisation in the UK has been stronger than in ContinentalEurope, and is the decisive factor that allowed the UK to catch up in terms of prosperity.8

It is always possible to raise labour productivity by shedding employment, but thisneither increases true prosperity nor a location’s competitiveness.9 Many ContinentalEuropean countries have gone down the road of making lower productivity employmentunattractive and have suffered high unemployment; the UK has instead increasedincentives for work. The UK did significantly reduce unemployment, and did not resort tocutting the average employee’s working week.

UK labour productivity growth has been comparable to other advanced economies - amarked improvement to the pre-1980’s where UK productivity growth persistently laggedcountries like France and Germany. UK labour productivity growth in the last threedecades has fluctuated but averages around 2% annually (Figure 3).10 In the early 1980’s,the initial wave of reforms led to fast productivity growth but also led to a rise inunemployment. With the economy picking up later in the decade, labour force utilisationsoared while labour productivity growth moderated. The macroeconomic crisis in theearly 1990’s cost many jobs, but labour productivity growth remained stable. Recently,both labour productivity growth and labour force utilisation have contributed to strongprosperity growth, but labour productivity is becoming the dominant factor.

While faster UK labour productivity growth rates have halted the erosion of relativeproductivity, they have not led to a substantial convergence. According to the OECD, theUK labour productivity gap versus the Netherlands per hour worked is at 25%, versusthe United States at 15%, versus France at 11%, and Germany at 8%. This data refersto all economic activity; O’Mahony/deBoer (2002) report even higher gaps for the marketsector excluding government and non-governmental services.

Co

mp

ou

nd

Avera

ge G

row

th R

ate

s

Labour Force Utilisation GrowthLabour Productivity Growth GDP per capita

70-80 80-85 85-90 90-95 95-98 98-01-1%

0%

1%

2%

3%

4%

Figure 3: Decomposition of UK Prosperity Growth over Time

Source: US Bureau of Labour Statistics (2002), author’s calculations

11

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

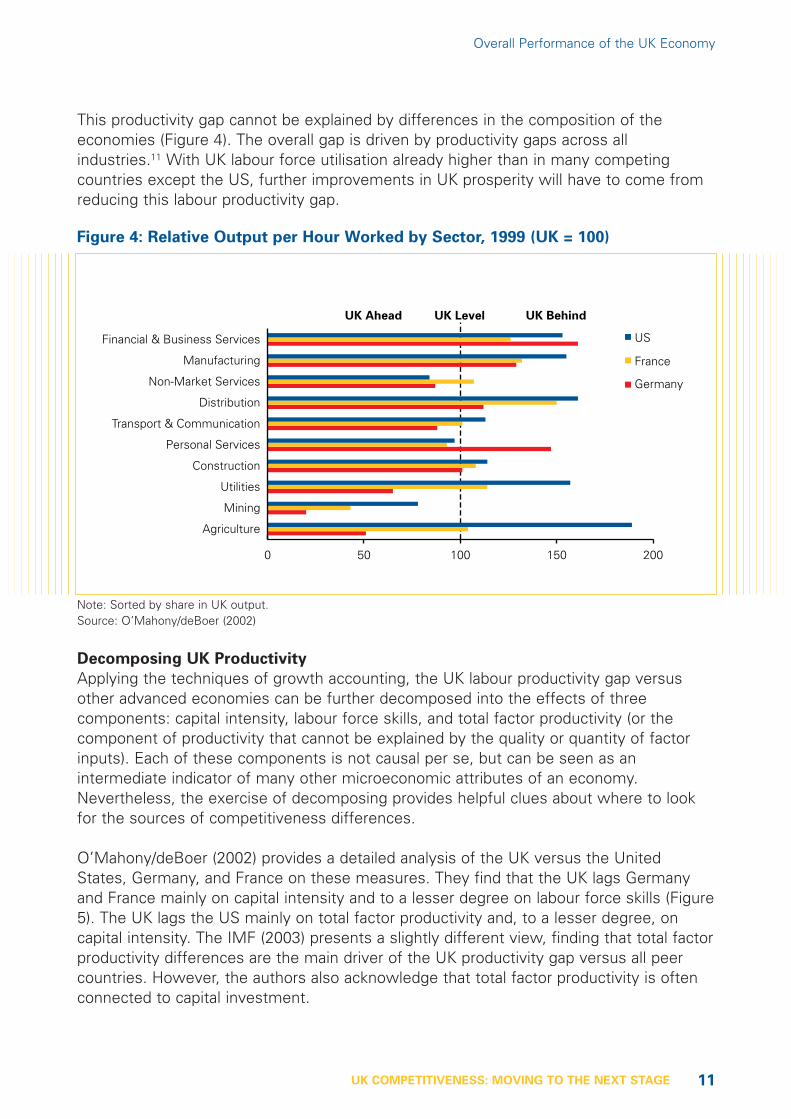

This productivity gap cannot be explained by differences in the composition of theeconomies (Figure 4). The overall gap is driven by productivity gaps across allindustries.11 With UK labour force utilisation already higher than in many competingcountries except the US, further improvements in UK prosperity will have to come fromreducing this labour productivity gap.

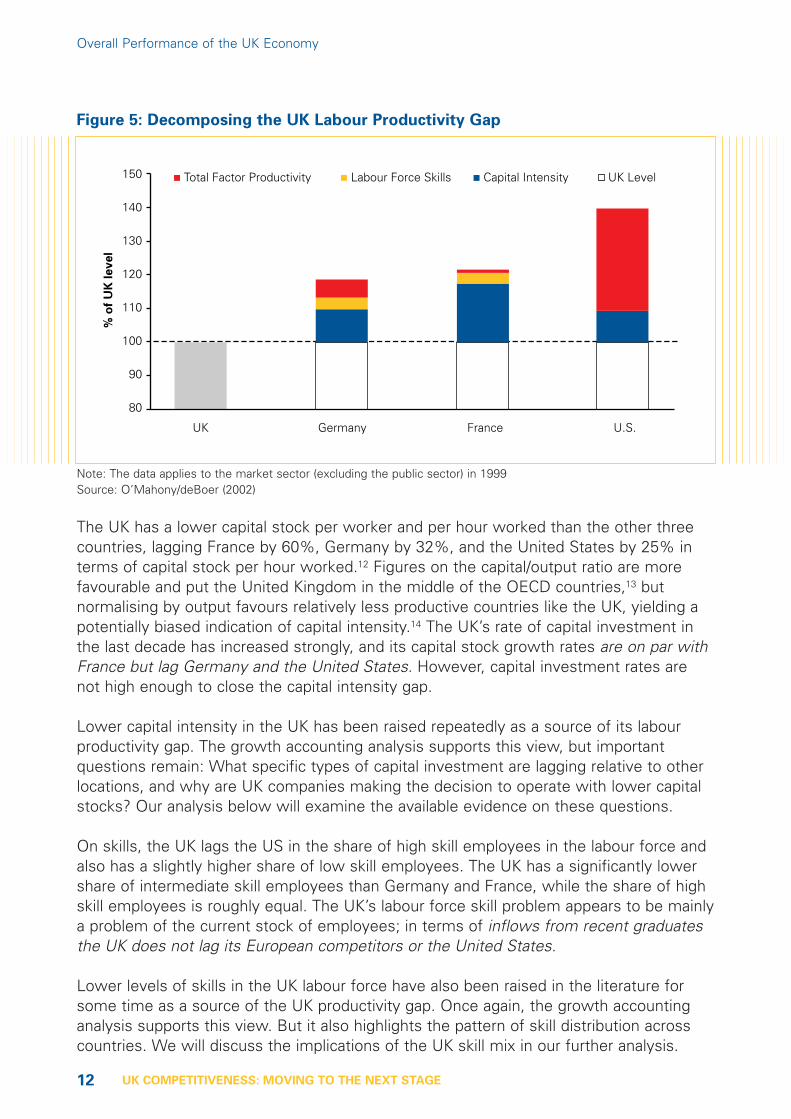

Decomposing UK Productivity

Applying the techniques of growth accounting, the UK labour productivity gap versusother advanced economies can be further decomposed into the effects of threecomponents: capital intensity, labour force skills, and total factor productivity (or thecomponent of productivity that cannot be explained by the quality or quantity of factorinputs). Each of these components is not causal per se, but can be seen as anintermediate indicator of many other microeconomic attributes of an economy.Nevertheless, the exercise of decomposing provides helpful clues about where to lookfor the sources of competitiveness differences.

O’Mahony/deBoer (2002) provides a detailed analysis of the UK versus the UnitedStates, Germany, and France on these measures. They find that the UK lags Germanyand France mainly on capital intensity and to a lesser degree on labour force skills (Figure5). The UK lags the US mainly on total factor productivity and, to a lesser degree, oncapital intensity. The IMF (2003) presents a slightly different view, finding that total factorproductivity differences are the main driver of the UK productivity gap versus all peercountries. However, the authors also acknowledge that total factor productivity is oftenconnected to capital investment.

0 50 100 150 200

Germany

France

US

Agriculture

Mining

Utilities

Construction

Personal Services

Transport & Communication

Distribution

Non-Market Services

Manufacturing

Financial & Business Services

UK Ahead UK Level UK Behind

Figure 4: Relative Output per Hour Worked by Sector, 1999 (UK = 100)

Note: Sorted by share in UK output.Source: O’Mahony/deBoer (2002)

12

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

The UK has a lower capital stock per worker and per hour worked than the other threecountries, lagging France by 60%, Germany by 32%, and the United States by 25% interms of capital stock per hour worked.12 Figures on the capital/output ratio are morefavourable and put the United Kingdom in the middle of the OECD countries,13 butnormalising by output favours relatively less productive countries like the UK, yielding apotentially biased indication of capital intensity.14 The UK’s rate of capital investment inthe last decade has increased strongly, and its capital stock growth rates are on par withFrance but lag Germany and the United States. However, capital investment rates arenot high enough to close the capital intensity gap.

Lower capital intensity in the UK has been raised repeatedly as a source of its labourproductivity gap. The growth accounting analysis supports this view, but importantquestions remain: What specific types of capital investment are lagging relative to otherlocations, and why are UK companies making the decision to operate with lower capitalstocks? Our analysis below will examine the available evidence on these questions.

On skills, the UK lags the US in the share of high skill employees in the labour force andalso has a slightly higher share of low skill employees. The UK has a significantly lowershare of intermediate skill employees than Germany and France, while the share of highskill employees is roughly equal. The UK’s labour force skill problem appears to be mainlya problem of the current stock of employees; in terms of inflows from recent graduatesthe UK does not lag its European competitors or the United States.

Lower levels of skills in the UK labour force have also been raised in the literature forsome time as a source of the UK productivity gap. Once again, the growth accountinganalysis supports this view. But it also highlights the pattern of skill distribution acrosscountries. We will discuss the implications of the UK skill mix in our further analysis.

Total Factor Productivity Labour Force Skills Capital Intensity UK Level

U.S.

150

140

130

120

110

100

90

80

France

% o

f U

K l

ev

el

GermanyUK

Figure 5: Decomposing the UK Labour Productivity Gap

Note: The data applies to the market sector (excluding the public sector) in 1999Source: O’Mahony/deBoer (2002)

13

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

In total factor productivity (TFP), the part of labour productivity that cannot be directlyattributed to factor inputs, the UK falls in the lower middle group of advanced economies.The UK lags the US, the global leader, by roughly 50%, France by 10%, and is comparableto Germany; based on OECD data for the 1995-1998 period.15 The data on the growth ofTFP is somewhat conflicting: the US Bureau of Labour Statistics reports UK TFP growthto be high in the early phase of microeconomic reforms in the 1980’s, but falling back to alevel similar to other advanced economies more recently.16 The IMF instead reports UKTFP to be lower than in peer countries except the United States not only throughout the1970’s but also the 1980’s, and increasing in the first half of the 1990’s. As do othersources, the IMF reports falling UK TFP growth towards the end of the 1990’s.17

Lower levels of TFP indicate inefficiencies unrelated to the level and quality of factorinputs and reflect low levels of innovation, broadly defined, and less effective use oftechnology. Deficits in TFP are especially problematic for an advanced economy like theUK, because TFP becomes increasingly important for labour productivity as an economyseeks higher levels of prosperity. We will examine various measures of innovation andprobable explanations for UK innovation performance in our further analysis.

c) Internationalisation, Innovation and Productivity Growth

Productivity growth is underpinned by trade, foreign investment, and innovative activity.Here we examine these three areas as additional indications of the trajectory of the UKeconomy. In general, we find that the UK’s export position is stable; that itsattractiveness for foreign direct investment is high but decreasing; and that its innovationperformance is weak.

Exports

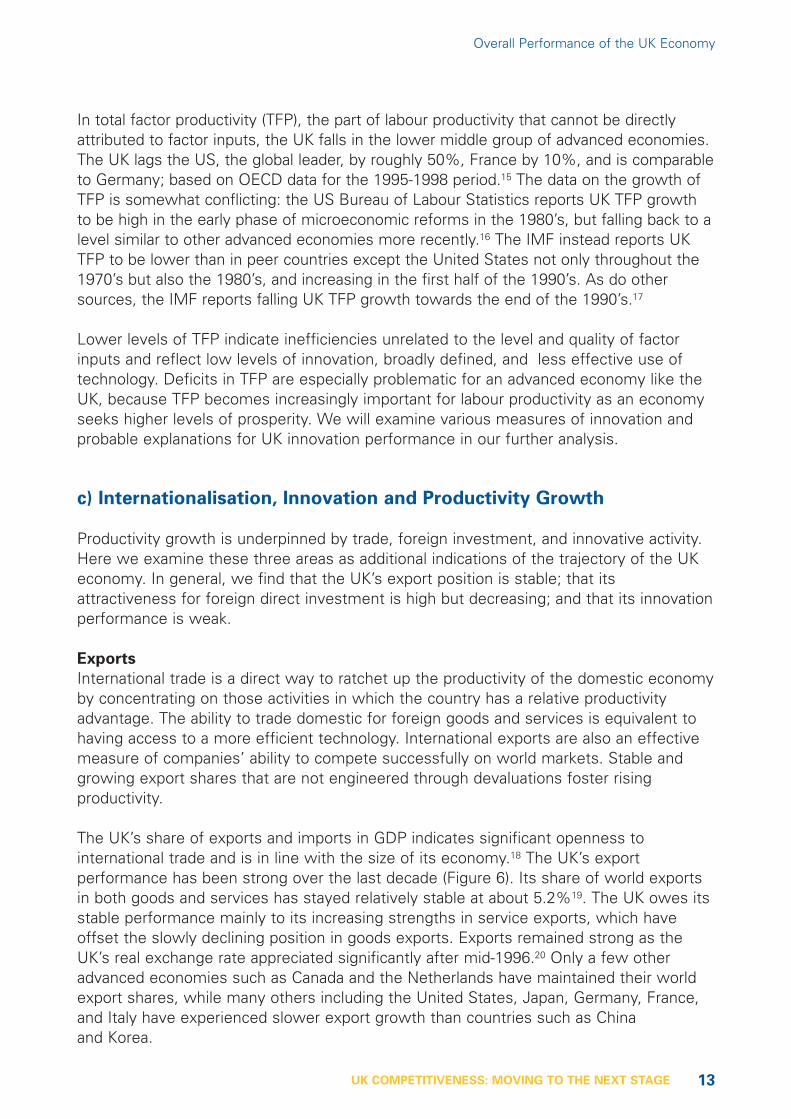

International trade is a direct way to ratchet up the productivity of the domestic economyby concentrating on those activities in which the country has a relative productivityadvantage. The ability to trade domestic for foreign goods and services is equivalent tohaving access to a more efficient technology. International exports are also an effectivemeasure of companies’ ability to compete successfully on world markets. Stable andgrowing export shares that are not engineered through devaluations foster risingproductivity.

The UK’s share of exports and imports in GDP indicates significant openness tointernational trade and is in line with the size of its economy.18 The UK’s exportperformance has been strong over the last decade (Figure 6). Its share of world exportsin both goods and services has stayed relatively stable at about 5.2%19. The UK owes itsstable performance mainly to its increasing strengths in service exports, which haveoffset the slowly declining position in goods exports. Exports remained strong as theUK’s real exchange rate appreciated significantly after mid-1996.20 Only a few otheradvanced economies such as Canada and the Netherlands have maintained their worldexport shares, while many others including the United States, Japan, Germany, France,and Italy have experienced slower export growth than countries such as Chinaand Korea.

14

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

Foreign Direct Investment (FDI)

Inward foreign investment improves the business environment by elevating the level ofdomestic competition, and raising the level of buyer sophistication through theprocurement standards and choices of foreign multinationals. And it also provides aneconomy with an inflow of new technologies, operational practices, and other knowledgedeveloped elsewhere. Foreign investors have capabilities otherwise not available in thedomestic economy; that is the reason they can compete in a location they otherwiseknow less well.21 These superior capabilities are reflected in the higher productivity offoreign-owned companies relative to the average domestic company, typical in all leadingeconomies.22

Outward foreign investment enables an economy to grow areas of the economy withhigh relative productivity, hence raising productivity growth. Outward FDI also amplifiesthe competitive position of UK-based firms allowing them to tap into low cost resourcesfor activities not requiring UK-level skills. Also, outward foreign investments allowcompanies to deepen their positions in foreign markets through providing local serviceand product customisation. Higher value activities still remain in the home country, andexperience suggests that the improvements in competitive position abroad can actuallyexpand home country jobs at the same time as some activities are moved abroad.Finally, outward FDI may sometimes be a necessity to preserve the very vitality of thehome country organisation.

The UK is an economy with strong inward and outward investment flows, with netoutward FDI balances. The role of foreign-owned companies in UK manufacturing iscomparable to France and significantly higher than in Germany or the United States.23

0

1

2

3

4

5

6

7

8

9

Wo

rld

ex

po

rt s

ha

re i

n %

1991 1992 1993 1994 1995 1996 1997 1998 1999 2001 2002

UK Goods UK Services UK Total

Figure 6: UK World Export Market Shares over Time

Source: WTO (2002), author’s calculations

15

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

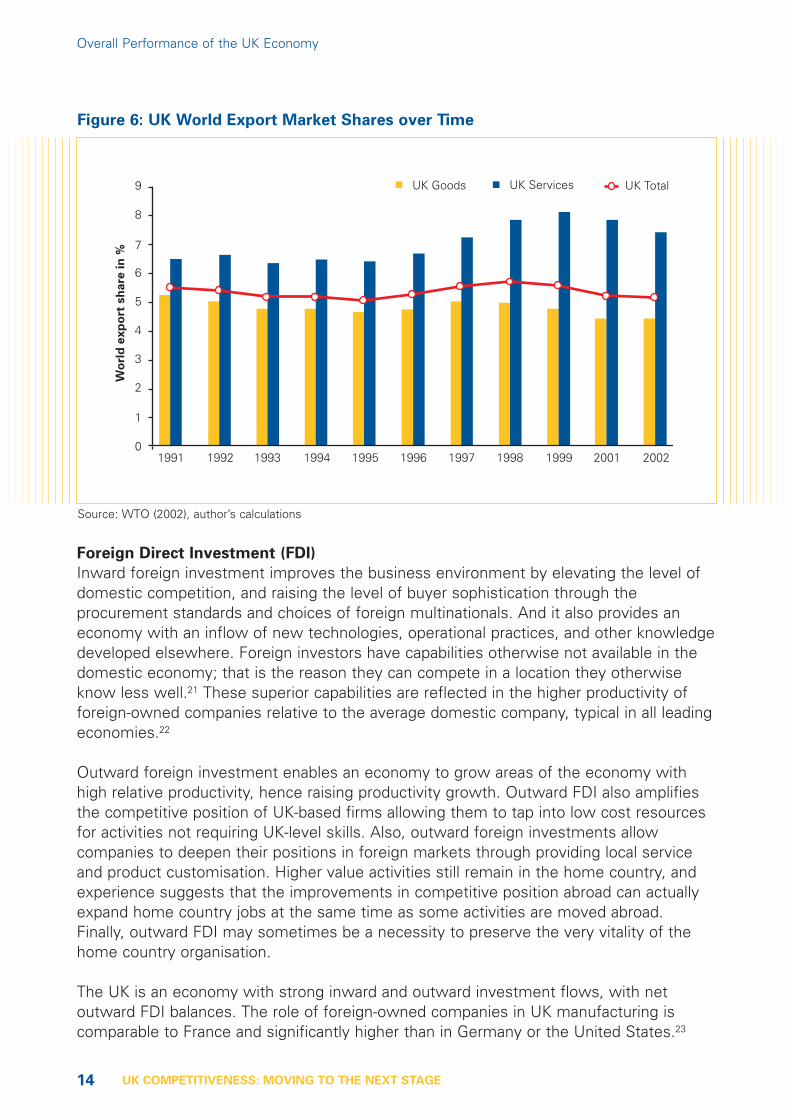

With a few exceptions the UK outperforms other advanced and emerging economies interms of FDI inflows as well as in stocks of FDI relative to GDP (Figure 7).24 In the years1998-2000 the UK’s share of world inward FDI stood at 7.8%, exceeding its share ofworld GDP by 80%, down from an even larger margin.

The UK also outperforms most countries in terms of outward FDI. UK companies have asignificant investment stock abroad; the value of their foreign investments stood at$942bn in 2001, about 14% of all countries foreign investment combined.25 They alsocontinue to invest heavily outside the UK: in 2000, UK company investments outside theUK exceeded their investments in the UK for the first time.

Innovation

The creation and commercialisation of new knowledge is a final, and crucial source ofdynamic improvements in productivity. For advanced economies, innovation is a matterof pushing the world frontier of knowledge. For developing countries technologyassimilation is the central challenge.

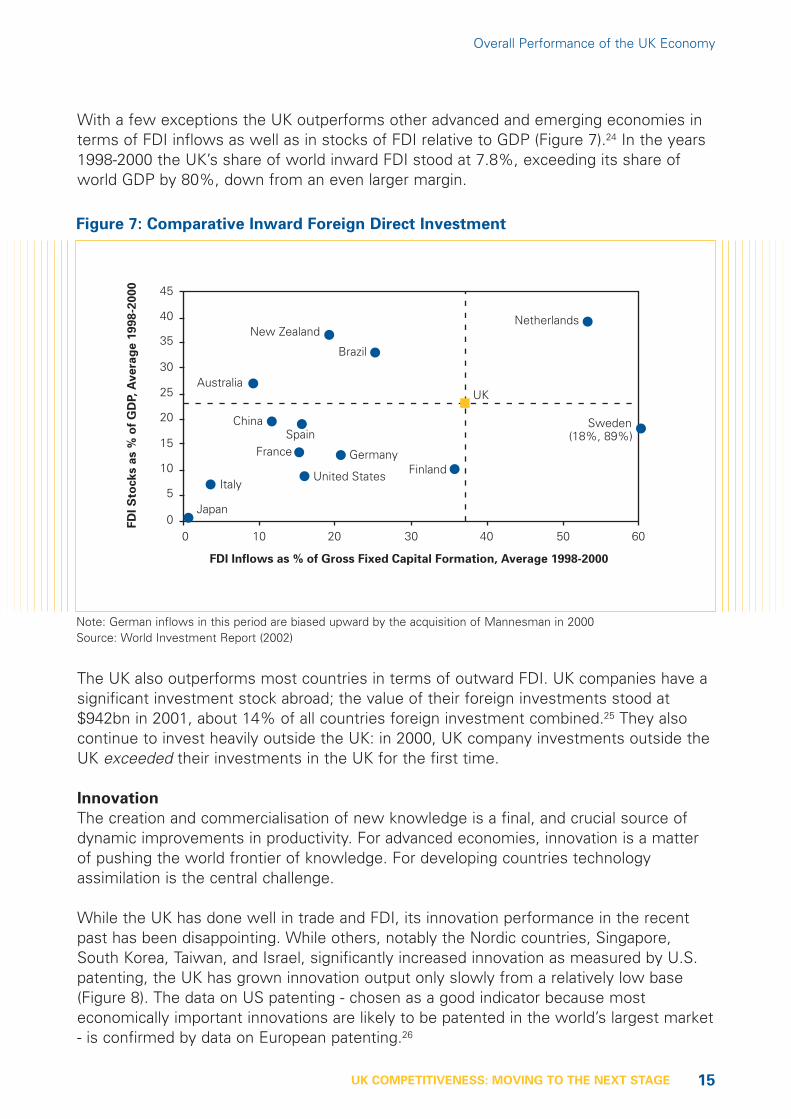

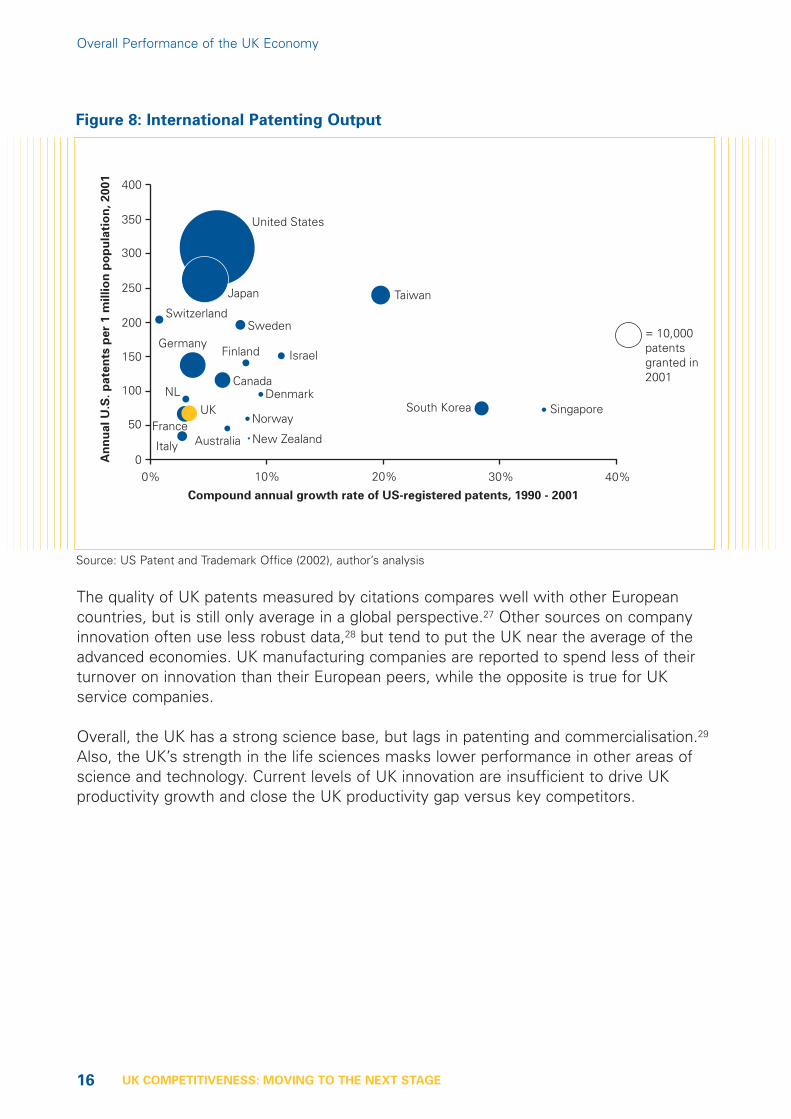

While the UK has done well in trade and FDI, its innovation performance in the recentpast has been disappointing. While others, notably the Nordic countries, Singapore,South Korea, Taiwan, and Israel, significantly increased innovation as measured by U.S.patenting, the UK has grown innovation output only slowly from a relatively low base(Figure 8). The data on US patenting - chosen as a good indicator because mosteconomically important innovations are likely to be patented in the world’s largest market- is confirmed by data on European patenting.26

FD

I S

tocks a

s %

of

GD

P, A

ve

rag

e 1

99

8-2

00

0

Japan

Italy

GermanyFrance

Sweden

UKAustralia

New Zealand

Brazil

China

United States

Netherlands

Finland

Spain

FDI Inflows as % of Gross Fixed Capital Formation, Average 1998-2000

0 10 20 30 40 50 600

10

15

20

25

30

35

40

45

5

(18%, 89%)

Figure 7: Comparative Inward Foreign Direct Investment

Note: German inflows in this period are biased upward by the acquisition of Mannesman in 2000Source: World Investment Report (2002)

16

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

The quality of UK patents measured by citations compares well with other Europeancountries, but is still only average in a global perspective.27 Other sources on companyinnovation often use less robust data,28 but tend to put the UK near the average of theadvanced economies. UK manufacturing companies are reported to spend less of theirturnover on innovation than their European peers, while the opposite is true for UKservice companies.

Overall, the UK has a strong science base, but lags in patenting and commercialisation.29

Also, the UK’s strength in the life sciences masks lower performance in other areas ofscience and technology. Current levels of UK innovation are insufficient to drive UKproductivity growth and close the UK productivity gap versus key competitors.

Compound annual growth rate of US-registered patents, 1990 - 2001

0% 10% 20% 30% 40%

An

nu

al

U.S

. p

ate

nts

pe

r 1

mil

lio

n p

op

ula

tio

n,

20

01

= 10,000patentsgranted in2001

0

50

100

150

200

250

300

350

400

Singapore

United States

Japan

SwitzerlandSweden

GermanyFinland

NL

UKFrance

Italy Australia New Zealand

Norway

DenmarkCanada

Israel

Taiwan

South Korea

Figure 8: International Patenting Output

Source: US Patent and Trademark Office (2002), author’s analysis

17

Overall Performance of the UK Economy

UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

References

3 Porter (2002a)

4 For other discussions of recentUK economic performance seeNickell (2002), Nickell/VanReenen (2002), andCard/Freeman (2002). For amore long-term perspective seeMaddison (2001).

5 IMF (2003)

6 OECD (2002), Nickell (2002a)

7 For example IMF (2003) andEuropean Commission (2002).

8 Card/Freeman (2002), OECD(2002a), IMF (2003)

9 The same is true for reducingworking time and thusincreasing the intensity of workin the remaining hours.

10 Bureau of Labour Statistics(2002), IMF (2003)

11 O’Mahoney/deBoer (2002)

12 Recent work by the IMF (2003)relates this gap in overall capitalintensity to lower investmentsin non-residential construction.UK investments in machinery,however, are comparable toother OECD countries.

13 IMF (2003)

14 Oughton (1997)

15 The IMF (2003) reportssomewhat different gaps for theaverage of the 1996 - 2000period with the UK lagging theUnited States by 33%, Franceby 25%, and Germany by 12%.

16 US Bureau of Labour Statistics(2002)

17 IMF (2003)

18 DTI (2002)

19 WTO (2002)

20 IMF (2002)

21 Given this logic, it should be nosurprise that multinationalcompanies are everywheremore productive than their localcompetitiors. See, for example,Ashworth (2001),Griffith/Simpson (2000).

22 Pain (2000)

23 OECD (2001)

24 UNCTAD (2002)

25 UNCTAD (2002)

26 European Commission (2001)

27 National Science Foundation(2000) cited in Porter/Van Opstel(2001)

28 Nickell/Van Reenen (2002)discuss the quality of theEuropean Innovation Survey

29 Nickell/Van Reenen (2002)

18 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

3

Competitiveness and theUK Business Environment:Summary of the Evidence

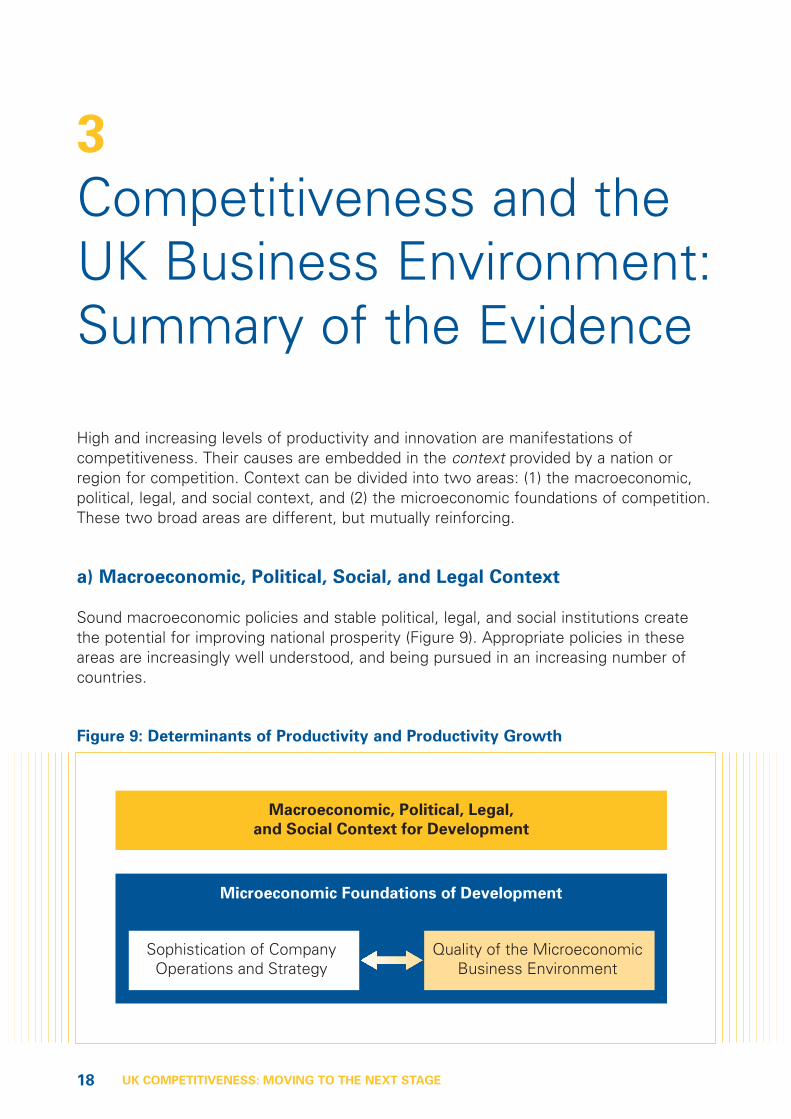

High and increasing levels of productivity and innovation are manifestations ofcompetitiveness. Their causes are embedded in the context provided by a nation orregion for competition. Context can be divided into two areas: (1) the macroeconomic,political, legal, and social context, and (2) the microeconomic foundations of competition.These two broad areas are different, but mutually reinforcing.

a) Macroeconomic, Political, Social, and Legal Context

Sound macroeconomic policies and stable political, legal, and social institutions createthe potential for improving national prosperity (Figure 9). Appropriate policies in theseareas are increasingly well understood, and being pursued in an increasing number ofcountries.

Macroeconomic, Political, Legal,

and Social Context for Development

Microeconomic Foundations of Development

Sophistication of CompanyOperations and Strategy

Quality of the MicroeconomicBusiness Environment

Figure 9: Determinants of Productivity and Productivity Growth

19UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

However, competitiveness ultimately depends on firms and the way they compete.Hence, a sound macroeconomic, political, legal, and social context is necessary forachieving competitiveness, but not sufficient.30

The UK’s political and legal system is stable and not a barrier to economic development.The UK has in recent years achieved a higher level of macroeconomic stability than inany other period after 1945. Before 1980, deteriorating public finances, a high level ofinflation, and an erosion of the value of the pound hampered the economy. In the earlyphase of the post-1980 reforms the focus was on reducing the size of government andstabilising public finances. Monetary policy, however, remained volatile and growtherratic. In the last decade, however, fiscal and monetary policy have become much morestable, especially after the independence of the Bank of England. There remainsuncertainty about Economic Monetary Union (EMU) membership, but this uncertainty isin itself unlikely to be an important factor affecting the UK’s competitiveness.

Progress on social issues has been more mixed, and the UK still faces significanteconomic disparities across regions and population groups. So far, poverty has beenseen as more a social than an economic problem, but the demographic shift could in thefuture increase the economic costs of these social problems.

b) Microeconomic Business Environment

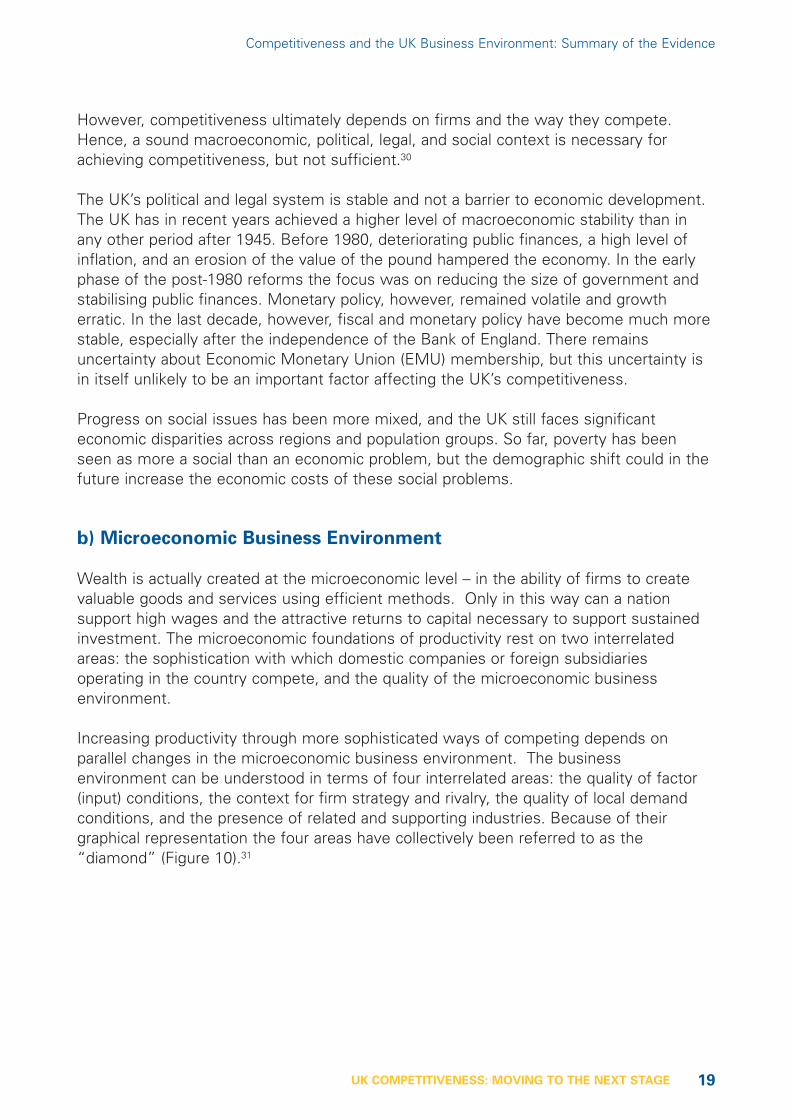

Wealth is actually created at the microeconomic level – in the ability of firms to createvaluable goods and services using efficient methods. Only in this way can a nationsupport high wages and the attractive returns to capital necessary to support sustainedinvestment. The microeconomic foundations of productivity rest on two interrelatedareas: the sophistication with which domestic companies or foreign subsidiariesoperating in the country compete, and the quality of the microeconomic businessenvironment.

Increasing productivity through more sophisticated ways of competing depends onparallel changes in the microeconomic business environment. The businessenvironment can be understood in terms of four interrelated areas: the quality of factor(input) conditions, the context for firm strategy and rivalry, the quality of local demandconditions, and the presence of related and supporting industries. Because of theirgraphical representation the four areas have collectively been referred to as the“diamond” (Figure 10).31

Competitiveness and the UK Business Environment: Summary of the Evidence

20 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

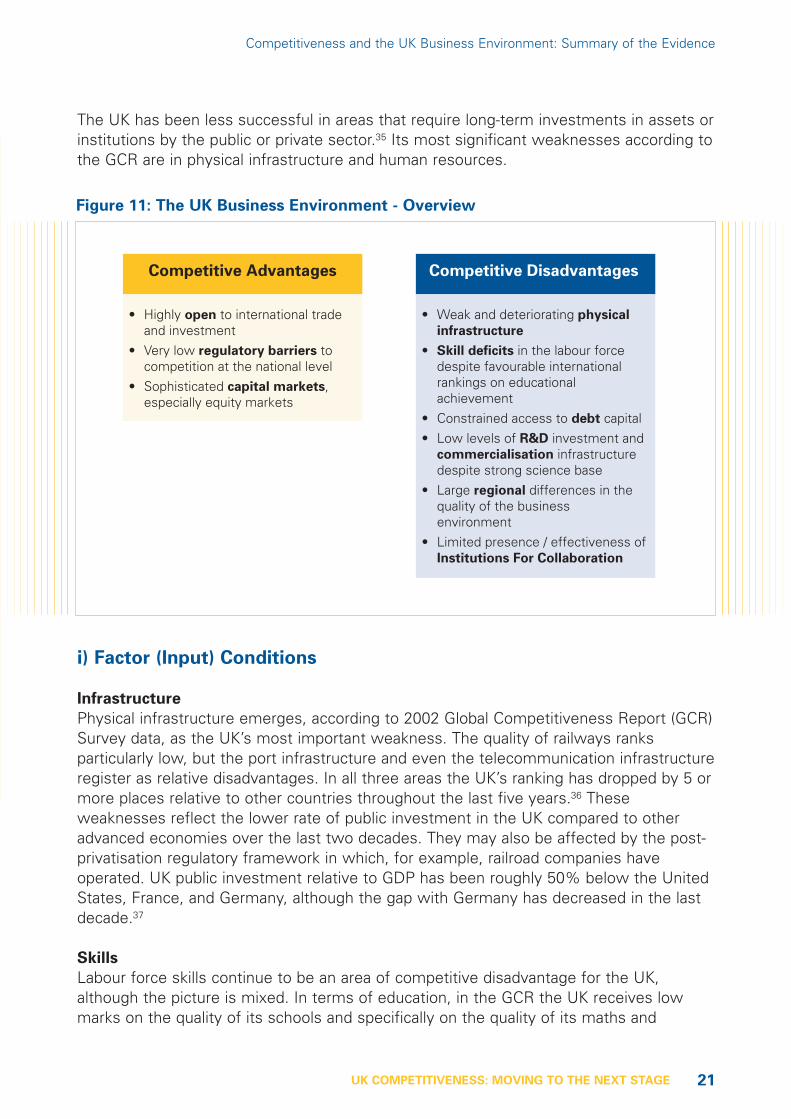

The UK business environment has been fundamentally upgraded in the last twodecades.32 This has been the result of significant changes in policy starting in the late1970’s,33 which have made the UK a much more attractive place to do business and haveenabled companies located there to achieve much higher levels of productivity.

Overall, the UK has been successful in reducing unproductive roles and distortions ofgovernment in the competitive process (Figure 11). In the Global Competitiveness Report(GCR),34 the UK performs especially well in measures of competitive vitality and marketincentives; it also performs well on demand conditions and capital markets.

Competitiveness and the UK Business Environment: Summary of the Evidence

Context for Firm

Strategy and Rivalry

The context shaping the extent of corporate

investment, the types of strategies employed, and the

intensity of local rivalry

Factor (Input) Conditions

The efficiency, quality, and specialisation of underlying inputs that firms draw in in

competing• human resources• capital resources• physical infrastructure• administrative infrastructure• scientific and technological

infrastructure• natural resources

Related and

Supporting Industries

The availability and quality of local suppliers and related industries, and the state of development of clusters

Demand

Conditions

The sophistication of home demand and the pressure

from local buyers to upgrade products and services

Figure 10: Productivity and the Business Environment

21UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

The UK has been less successful in areas that require long-term investments in assets orinstitutions by the public or private sector.35 Its most significant weaknesses according tothe GCR are in physical infrastructure and human resources.

i) Factor (Input) Conditions

Infrastructure

Physical infrastructure emerges, according to 2002 Global Competitiveness Report (GCR)Survey data, as the UK’s most important weakness. The quality of railways ranksparticularly low, but the port infrastructure and even the telecommunication infrastructureregister as relative disadvantages. In all three areas the UK’s ranking has dropped by 5 ormore places relative to other countries throughout the last five years.36 Theseweaknesses reflect the lower rate of public investment in the UK compared to otheradvanced economies over the last two decades. They may also be affected by the post-privatisation regulatory framework in which, for example, railroad companies haveoperated. UK public investment relative to GDP has been roughly 50% below the UnitedStates, France, and Germany, although the gap with Germany has decreased in the lastdecade.37

Skills

Labour force skills continue to be an area of competitive disadvantage for the UK,although the picture is mixed. In terms of education, in the GCR the UK receives lowmarks on the quality of its schools and specifically on the quality of its maths and

Competitiveness and the UK Business Environment: Summary of the Evidence

Competitive Advantages

• Highly open to international trade and investment

• Very low regulatory barriers to competition at the national level

• Sophisticated capital markets, especially equity markets

Competitive Disadvantages

• Weak and deteriorating physical

infrastructure

• Skill deficits in the labour force despite favourable international rankings on educational achievement

• Constrained access to debt capital• Low levels of R&D investment and

commercialisation infrastructure despite strong science base

• Large regional differences in the quality of the business environment

• Limited presence / effectiveness of Institutions For Collaboration

Figure 11: The UK Business Environment - Overview

22 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

science education. This is consistent with the comparatively low spending on educationin the UK; on a per student basis the UK ranks 15th among all OECD countries on thismeasure. However, UK students have performed well in the recent PISA study oneducational performance across countries where the UK ranks between 4 and 6 ondifferent educational areas.38

In terms of general labour force skills, the UK still falls behind competing economies,especially because of a high share of the population with low levels of educationalattainment.39 UK companies report significant skill shortages that are consistent withthese deficits.40

In terms of advanced skills, the UK ranks well in the GCR on management education, anarea in which the country attracts many foreign students. The UK receives low GCRmarks on the availability of scientists and engineers. The UK has, however, registered ahigher increase in the number of researchers per employees in the workforce than mostother advanced economies, although it still is at a low level.41

Financial markets

The City of London is one of the most competitive financial services clusters in theworld. The UK ranks 1 in the GCR on the sophistication of its financial markets. Its equitymarkets in particular are rated highly, although there is anecdotal evidence of companiesgoing private to avoid the markets short-term scrutiny.42 Venture capital availability is thehighest in Europe behind the Netherlands,43 although some observers are concernedabout the relatively greater focus on later stage investments. While equity financing iscompetitive, it tends to be more expensive than debt financing. There are signs that theenvironment for debt financing is not as competitive: Investments of UK companiesreact more strongly to cash-flow changes, indicating constrained access to externalfinancing.44 This would be particularly harmful to the growth prospects of small andmedium sized companies.

Science & Technology

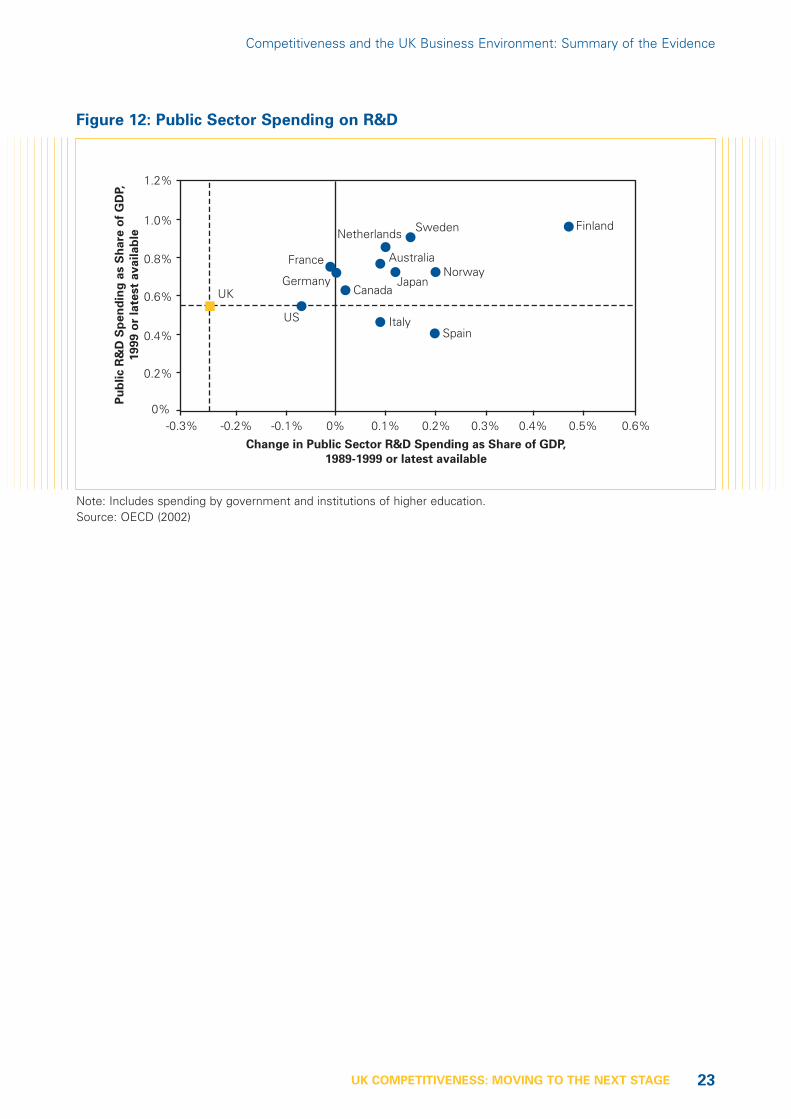

The UK has in the recent past invested less public sector money into R&D than mostother advanced economies. And over the last decade, the UK’s position on public R&Dspending relative to GDP has worsened (Figure 12).45 Recent policy changes have startedto address this, and the government budgets for the next few years register a significantramping up of public sector R&D spending. It will take a while, however, until theaccumulated effect of years of under investment in, for example, the universityinfrastructure, will have been overcome.46

Competitiveness and the UK Business Environment: Summary of the Evidence

23UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

Competitiveness and the UK Business Environment: Summary of the Evidence

Pu

bli

c R

&D

Sp

en

din

g a

s S

ha

re o

f G

DP,

19

99

or

late

st

av

ail

ab

le

Finland

Norway

Sweden

SpainItaly

Canada

Netherlands

Australia

Japan

France

Germany

US

UK

Change in Public Sector R&D Spending as Share of GDP,

1989-1999 or latest available

-0.3% -0.2% -0.1% 0% 0.1% 0.2% 0.3% 0.4% 0.5% 0.6%0%

1.2%

1.0%

0.8%

0.6%

0.4%

0.2%

Figure 12: Public Sector Spending on R&D

Note: Includes spending by government and institutions of higher education.Source: OECD (2002)

24 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

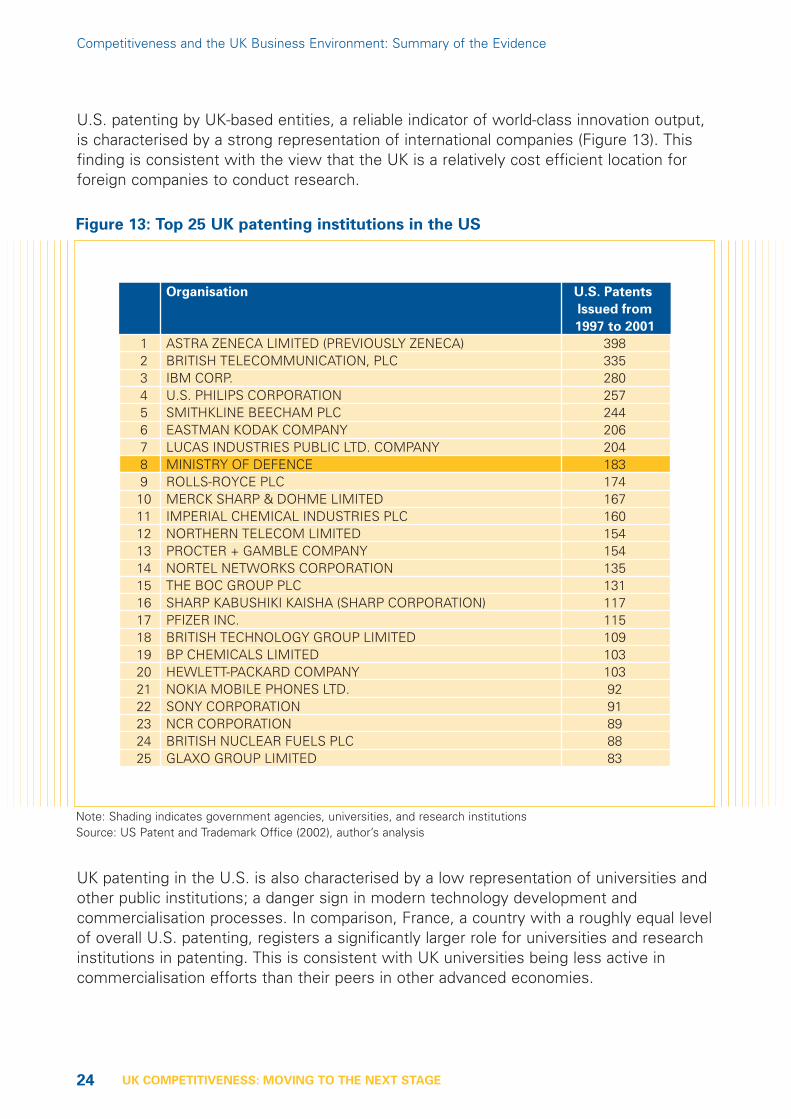

U.S. patenting by UK-based entities, a reliable indicator of world-class innovation output,is characterised by a strong representation of international companies (Figure 13). Thisfinding is consistent with the view that the UK is a relatively cost efficient location forforeign companies to conduct research.

UK patenting in the U.S. is also characterised by a low representation of universities andother public institutions; a danger sign in modern technology development andcommercialisation processes. In comparison, France, a country with a roughly equal levelof overall U.S. patenting, registers a significantly larger role for universities and researchinstitutions in patenting. This is consistent with UK universities being less active incommercialisation efforts than their peers in other advanced economies.

Competitiveness and the UK Business Environment: Summary of the Evidence

Organisation U.S. Patents

Issued from

1997 to 2001

1 ASTRA ZENECA LIMITED (PREVIOUSLY ZENECA) 3982 BRITISH TELECOMMUNICATION, PLC 3353 IBM CORP. 2804 U.S. PHILIPS CORPORATION 2575 SMITHKLINE BEECHAM PLC 2446 EASTMAN KODAK COMPANY 2067 LUCAS INDUSTRIES PUBLIC LTD. COMPANY 2048 MINISTRY OF DEFENCE 1839 ROLLS-ROYCE PLC 17410 MERCK SHARP & DOHME LIMITED 16711 IMPERIAL CHEMICAL INDUSTRIES PLC 16012 NORTHERN TELECOM LIMITED 15413 PROCTER + GAMBLE COMPANY 15414 NORTEL NETWORKS CORPORATION 13515 THE BOC GROUP PLC 13116 SHARP KABUSHIKI KAISHA (SHARP CORPORATION) 11717 PFIZER INC. 11518 BRITISH TECHNOLOGY GROUP LIMITED 10919 BP CHEMICALS LIMITED 10320 HEWLETT-PACKARD COMPANY 10321 NOKIA MOBILE PHONES LTD. 9222 SONY CORPORATION 9123 NCR CORPORATION 8924 BRITISH NUCLEAR FUELS PLC 8825 GLAXO GROUP LIMITED 83

Figure 13: Top 25 UK patenting institutions in the US

Note: Shading indicates government agencies, universities, and research institutionsSource: US Patent and Trademark Office (2002), author’s analysis

25UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

ii) Context for Firm Strategy and Rivalry47

Market openness

The UK traditionally is an open economy with low barriers to foreign trade andinvestment, especially towards neighbouring European countries. As a member of theEuropean Union, it falls under the general rules of the common market and the commontrade policy.48 According to the GCR, the UK has an overall low level of tariffs but someremaining non-tariff barriers to trade.

Domestically, the reforms of the last two decades have left the UK with very lowadministrative costs for new business formation relative to other countries. However,while the rate of new business formation is high, UK start-ups have a significantly lowerlikelihood to survive the initial years than their peers in other European countries and theUnited States.49

Government regulations

The UK has the lowest level of product and labour market regulations in the OECD. Thelevel of distortive government subsidies in the UK is low, and the subsidies paid tend tobe horizontal rather than industry specific.50 While the UK outperforms many otherEuropean countries on the level of distortive government subsidies, it ranks only 12 inthe global comparison of the GCR. Specific local regulations, such as zoning laws, arealso mentioned as barriers to more investment and productivity.51 There is also someconcern in the business community about an increasing level of European Union-drivenregulation that the UK will be subject to.

Incentives

The UK has a generally competitive system of business taxation with incentives for R&Dinvestments and investments in economically distressed areas. The overall level oftaxation is slightly lower than in many other advanced economies; this relative advantageof the UK has, however, decreased in recent years.52 According to the GCR survey data,the UK has very strong intellectual property rights protection, providing a goodenvironment for innovation and technology transfer.

Competition

Relatively low levels of competitive intensity in some parts of the UK economy arerepeatedly mentioned in the literature. The examples often tend to be in the non-tradedsector of the economy. Reasons mentioned include the effects of past privatisation thatare argued to have been driven too heavily by fiscal considerations. The competitionpolicy in the UK was historically perceived to be more lenient than in other OECDcountries.53 Recent policy changes have markedly improved the policy context but willtake considerable time to be fully reflected in companies competitive behaviour.54

Competitiveness and the UK Business Environment: Summary of the Evidence

26 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

While there is no conclusive data, there is evidence that UK price levels in many sectorsare higher than in other European countries and, in some sectors, above US levels aswell.55 The lower UK ranking on GDP per capita measured by purchasing power parityversus by current exchange rate is consistent with this view (Figure 14). However, thedata is not conclusive: the divergence between purchasing power parity and exchangerate could be explained by other factors unrelated to the level of competition in the UK.

iii) Demand Conditions

The importance of advanced and sophisticated domestic demand grows as advancedeconomies progress. Sophisticated local customers educate local companies aboutfuture needs and pressure them to produce superior goods and services. Home demandis influenced not only by consumers and corporate customers but also by the stringencyof local regulatory standards in areas such as energy, safety, and environmental impacts.Given the priority for the UK to overcome current weaknesses in innovation, demandconditions are an increasingly important influence on the country’s competitiveness.

Demand sophistication

The UK ranks high on overall buyer sophistication in the GCR. Specific examples are

Competitiveness and the UK Business Environment: Summary of the Evidence

Rank Country by 2001 Country by 2001

GDP per Capita GDP per Capita

(FX) (PPP)

1 US US2 Norway Ireland3 Switzerland Norway4 Japan Switzerland5 Denmark Iceland6 Iceland Denmark7 Ireland Canada8 Netherlands Netherlands9 UK Austria10 Sweden Belgium11 Finland Australia12 Austria Japan13 Germany Germany14 Belgium Italy15 Canada Finland16 France Sweden17 Italy UK18 Australia France19 Spain Spain20 New Zealand New Zealand

Figure 14: The Effect of Purchasing Power on National Prosperity

Source: OECD (2002)

27UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

related to individual clusters such as oil & gas, financial services, media, and others, butthere is little hard data available.

Standards and regulations

The regulatory context in the UK provides average incentives for companies to addresssophisticated consumer needs. On environmental regulations, for example, the UKperforms less well than Scandinavia, Germany, or France, but still outperforms theaverage of the advanced economies.56

Government procurement

The UK ranks low on the sophistication of government procurement in the GCR. There islittle other hard data available on this subject.

c) Clusters

Clusters constitute one facet of the diamond, but they are best seen as a manifestationof the interaction of all the diamond’s elements.57 Clusters are geographically proximategroups of interconnected companies, suppliers, service providers, and associatedinstitutions in a particular field, linked by commonalities and complementarities. Clusterssuch as IT in Silicon Valley or high performance cars in Southern Germany can beconcentrated in a particular region within a larger nation, and sometimes in a singletown. Other clusters are national and sometimes stretch across borders into adjacentcountries, such as Southern Germany and German-speaking Switzerland. Proximity mustbe sufficient to allow efficient interaction and flow of goods, services, ideas, and skillsacross the cluster.

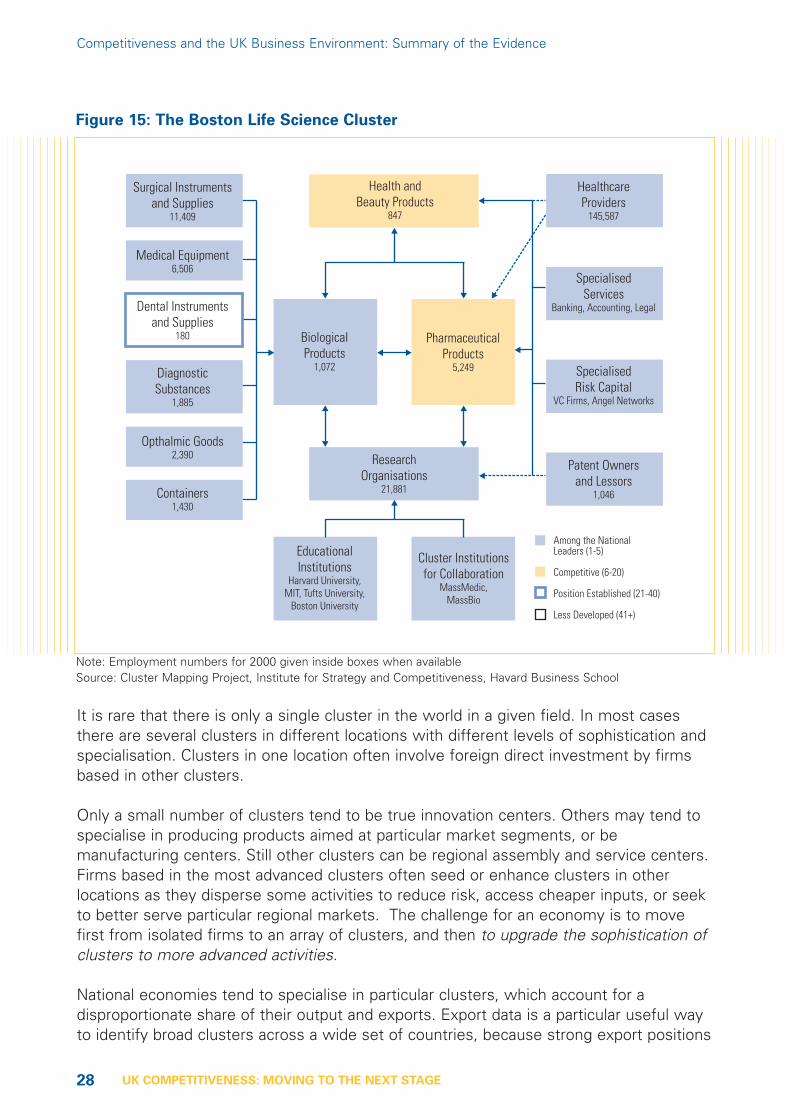

Clusters affect competitiveness in three broad ways: First, clusters increase the level ofproductivity at which constituent firms can operate. Firms can, for example, operate withlower levels of stock due to the local presence of suppliers. And they can reducedowntime in cases of technical failures in the production process due to the quickaccess to local service providers that can solve such problems quickly. Second, clustersincrease the capacity for innovation and productivity growth. In the Boston Life SciencesCluster (Figure 15), for example, the presence of world-class research universities,teaching hospitals, competing biotech companies, and cluster institutions that facilitateinteraction among all these foster the dissemination of knowledge and provide a fertileground for new ideas: Boston has between 1996 and 2000 generated the highestnumber of life science patents of all economic areas in the United States. Third, clustersstimulate and enable new business formation that further supports innovation andexpands the cluster. In Boston, the availability of highly experienced researchers andlaboratory technicians, the access to specialized Venture Capital providers and lawyers,and the many options for employment in other cluster companies in case of failure allreduce the costs and risks of starting a new life sciences company.

Competitiveness and the UK Business Environment: Summary of the Evidence

28 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

It is rare that there is only a single cluster in the world in a given field. In most casesthere are several clusters in different locations with different levels of sophistication andspecialisation. Clusters in one location often involve foreign direct investment by firmsbased in other clusters.

Only a small number of clusters tend to be true innovation centers. Others may tend tospecialise in producing products aimed at particular market segments, or bemanufacturing centers. Still other clusters can be regional assembly and service centers.Firms based in the most advanced clusters often seed or enhance clusters in otherlocations as they disperse some activities to reduce risk, access cheaper inputs, or seekto better serve particular regional markets. The challenge for an economy is to movefirst from isolated firms to an array of clusters, and then to upgrade the sophistication ofclusters to more advanced activities.

National economies tend to specialise in particular clusters, which account for adisproportionate share of their output and exports. Export data is a particular useful wayto identify broad clusters across a wide set of countries, because strong export positions

Competitiveness and the UK Business Environment: Summary of the Evidence

ResearchOrganisations

21,881

Among the NationalLeaders (1-5)

Competitive (6-20)

Position Established (21-40)

Less Developed (41+)

HealthcareProviders

145,587

SpecialisedServices

Banking, Accounting, Legal

SpecialisedRisk Capital

VC Firms, Angel Networks

Patent Ownersand Lessors

1,046

Health andBeauty Products

847

BiologicalProducts

1,072

PharmaceuticalProducts

5,249

EducationalInstitutions

Harvard University,MIT, Tufts University,

Boston University

Cluster Institutionsfor Collaboration

MassMedic,MassBio

Opthalmic Goods2,390

Containers1,430

Dental Instrumentsand Supplies

180

Medical Equipment6,506

Surgical Instrumentsand Supplies

11,409

DiagnosticSubstances

1,885

Figure 15: The Boston Life Science Cluster

Note: Employment numbers for 2000 given inside boxes when availableSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Havard Business School

29UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

in specific clusters indicate a base of internationally competitive companies orsubsidiaries in these areas.

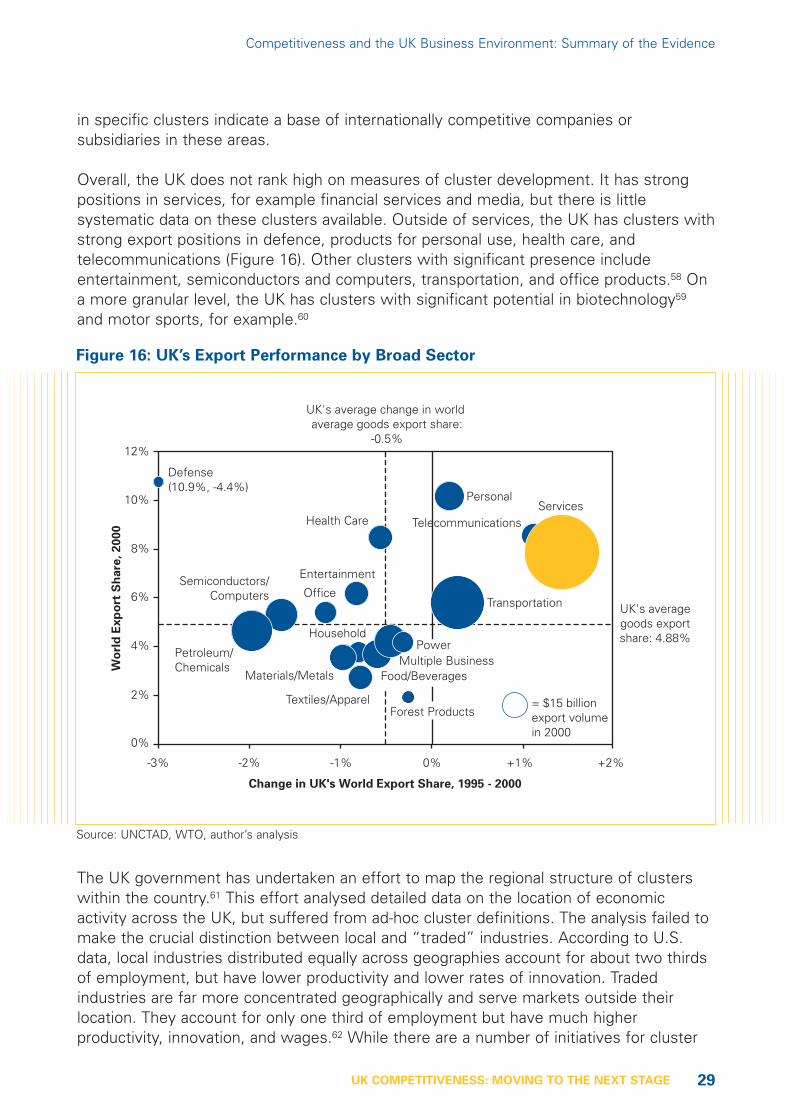

Overall, the UK does not rank high on measures of cluster development. It has strongpositions in services, for example financial services and media, but there is littlesystematic data on these clusters available. Outside of services, the UK has clusters withstrong export positions in defence, products for personal use, health care, andtelecommunications (Figure 16). Other clusters with significant presence includeentertainment, semiconductors and computers, transportation, and office products.58 Ona more granular level, the UK has clusters with significant potential in biotechnology59

and motor sports, for example.60

The UK government has undertaken an effort to map the regional structure of clusterswithin the country.61 This effort analysed detailed data on the location of economicactivity across the UK, but suffered from ad-hoc cluster definitions. The analysis failed tomake the crucial distinction between local and “traded” industries. According to U.S.data, local industries distributed equally across geographies account for about two thirdsof employment, but have lower productivity and lower rates of innovation. Tradedindustries are far more concentrated geographically and serve markets outside theirlocation. They account for only one third of employment but have much higherproductivity, innovation, and wages.62 While there are a number of initiatives for cluster

Competitiveness and the UK Business Environment: Summary of the Evidence

Change in UK's World Export Share, 1995 - 2000

-3% -2% -1% 0% +1% +2%

Wo

rld

Ex

po

rt S

ha

re,

20

00

UK's average change in world average goods export share:

-0.5%

UK's averagegoods exportshare: 4.88%

= $15 billionexport volumein 2000

0%

2%

4%

6%

8%

10%

12%

Defense(10.9%, -4.4%)

Health CareServices

Personal

Office

Entertainment

Household

Materials/Metals

Textiles/ApparelForest Products

Food/BeveragesMultiple Business

Power

Transportation

Telecommunications

Petroleum/Chemicals

Semiconductors/Computers

Figure 16: UK’s Export Performance by Broad Sector

Source: UNCTAD, WTO, author’s analysis

30 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

activation throughout the UK, often initiated by the Regional Development Agencies(RDA’s), the data provided by the existing cluster mapping effort seems to have had onlylimited practical value.

d) Roles, Institutions, and Processes

Competitiveness increasingly relies on a country’s appropriate structure of roles,institutions and processes to enable, organise, and drive efforts to improve businessenvironments and clusters. In the past, government, often at the national level, was incharge of improving competitiveness through policy decisions and incentives. Firmscompeted in the marketplace and took their environment as given. In moderncompetition, however, improving competitiveness becomes a collaborative processinvolving multiple levels of government, companies, educational institutions, andinstitutions for collaboration (IFC). At the microeconomic level a large number of factorsimpact on competitiveness and hence only a broad coalition can hope to improve anation’s foundations of competitiveness.

Government continues to play an important role because it affects many aspects of thebusiness environment. Government shapes factor conditions, for example, through itstraining and infrastructure policies and similar policy influences are present in allelements of the diamond. There are distinct roles for government in improving thebusiness environment at the national, state, and local level as well as amongneighbouring countries. Government at all levels also has a central role in convening andsupporting competitiveness efforts, even though these efforts will tend to be led by theprivate sector or other institutions. Without government involvement, initiatives lacklegitimacy and they fail to address those competitiveness issues government policy candirectly affect.

Companies play an increasingly important role for the competitiveness of their locations.Competitive advantage resides not only within the firm, but is also shaped by theexternal context firms operate in. Individual companies can improve their externalcontext by individual actions such as establishing schools, attracting suppliers, or definingstandards that not only benefit themselves but also improve the overall environment forcompetition. Companies can also take collective steps to enhance the ability of individualcompanies to improve operating practices and strategies, such as quality certificationprograms and manufacturing assistance centers.

Universities and other educational and research institutions have also becomeincreasingly important factors for national and regional competitiveness. Traditionally,they have been important in improving the skill base of the economy. But a shift in theway research and development (R&D) is organised is now also strengthening their role incommercial R&D. In the past, universities did basic science, while companies workedseparately on applications for commercial use. Today, these boundaries have blurred, andsuccessful R&D often involves cooperation throughout the innovation process.

Competitiveness and the UK Business Environment: Summary of the Evidence

31UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

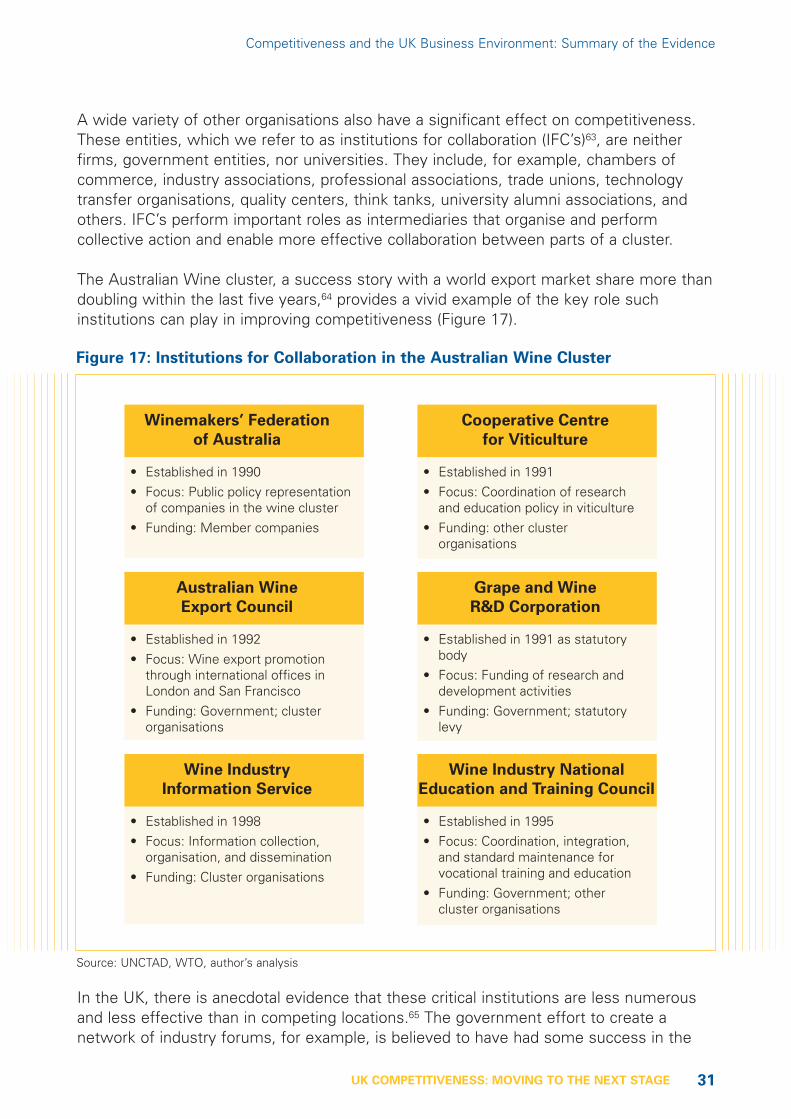

A wide variety of other organisations also have a significant effect on competitiveness.These entities, which we refer to as institutions for collaboration (IFC’s)63, are neitherfirms, government entities, nor universities. They include, for example, chambers ofcommerce, industry associations, professional associations, trade unions, technologytransfer organisations, quality centers, think tanks, university alumni associations, andothers. IFC’s perform important roles as intermediaries that organise and performcollective action and enable more effective collaboration between parts of a cluster.

The Australian Wine cluster, a success story with a world export market share more thandoubling within the last five years,64 provides a vivid example of the key role suchinstitutions can play in improving competitiveness (Figure 17).

In the UK, there is anecdotal evidence that these critical institutions are less numerousand less effective than in competing locations.65 The government effort to create anetwork of industry forums, for example, is believed to have had some success in the

Competitiveness and the UK Business Environment: Summary of the Evidence

Winemakers’ Federation

of Australia

• Established in 1990• Focus: Public policy representation

of companies in the wine cluster• Funding: Member companies

Cooperative Centre

for Viticulture

• Established in 1991• Focus: Coordination of research

and education policy in viticulture• Funding: other cluster

organisations

Australian Wine

Export Council

• Established in 1992• Focus: Wine export promotion

through international offices in London and San Francisco

• Funding: Government; cluster organisations

Grape and Wine

R&D Corporation

• Established in 1991 as statutory body

• Focus: Funding of research and development activities

• Funding: Government; statutory levy

Wine Industry

Information Service

• Established in 1998• Focus: Information collection,

organisation, and dissemination• Funding: Cluster organisations

Wine Industry National

Education and Training Council

• Established in 1995• Focus: Coordination, integration,

and standard maintenance for vocational training and education

• Funding: Government; other cluster organisations

Figure 17: Institutions for Collaboration in the Australian Wine Cluster

Source: UNCTAD, WTO, author’s analysis

32 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

automotive cluster, but little impact elsewhere. However, there is no systematicevidence on these efforts.

e) Influences of Different Geographical Levels

In the past, analysis of competitiveness has focused on the nation and national-levelpolicies. Increasingly it is becoming clear that this perspective is too limited:competitiveness is affected by assets and policies at many different geographic levels.These range from cross-national, e.g. the Baltic Rim or the European Union, to national,to regional, to local. Indeed, the most significant spillovers and interactions take place atthe regional and local level. A clear indication of the importance of regional businessenvironments is the sharp performance difference across regions within given countries,even though they are all exposed to the same national level policies.

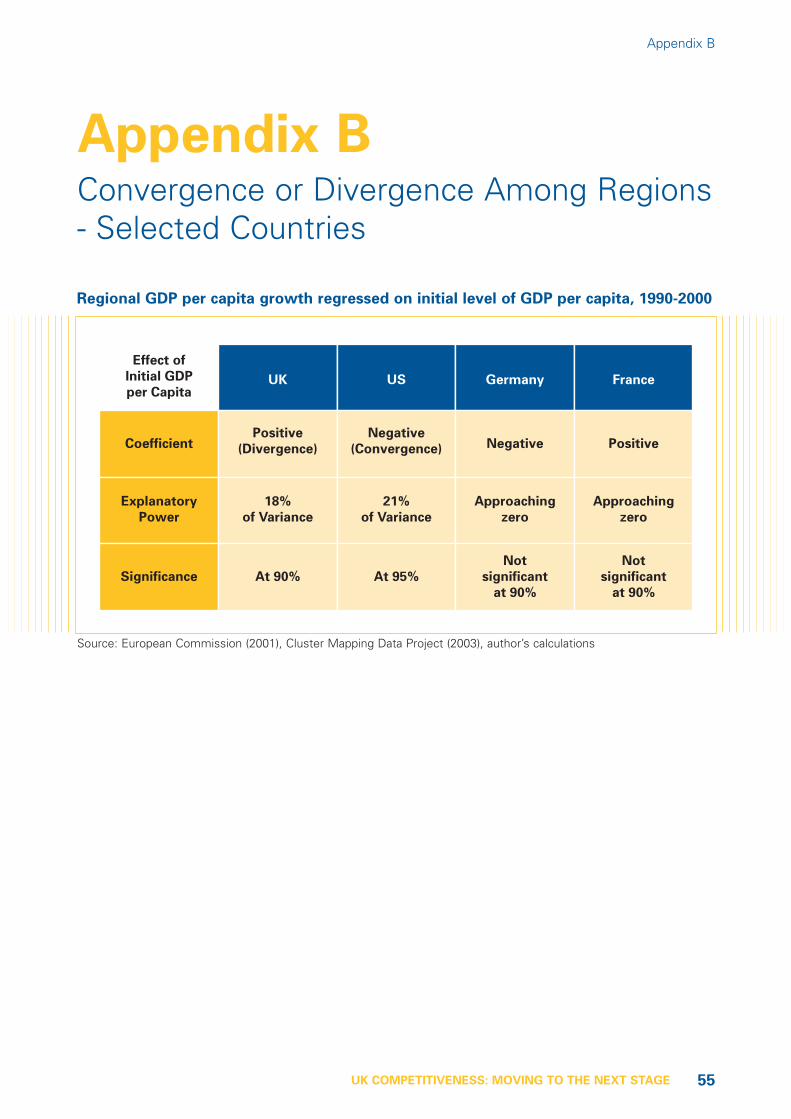

Across UK regions, as in many other countries, there are strong differences in regionaleconomic prosperity that are consistent with differences in the quality of regionalbusiness environments.66 In countries such as the United States there is convergence ofprosperity across regions. In the UK, there is divergence of regional prosperity.67 The richare getting richer and the poor are getting poorer. In France and Germany there is nosignificant relationship between regional prosperity and prosperity growth, or no changein dispersion of performance. While GDP per capita differences in UK regions appear tobe more persistent than in other European countries, unemployment rates in the UK aremore similar across regions.68 This is consistent with flexible labour markets in the UK.Labour mobility and wage flexibility are effective, and regional differences in incomereflect the quality of the regional business environments.

Strong regions and regional institutions - from mayors to elected regional and state leveladministrations with significant decision rights - have proven to be an increasinglyimportant factor for competitiveness in many other countries. Their importance has goneup, because there has been convergence on the policies controlled at the national level,such as macroeconomic policy, taxation, and overall government regulation. Theremaining differences in regional business environments affected by the decisions ofregional institutions have become more important. In the United States, for example,there is clear evidence that much of the relevant progress in improving themicroeconomic foundations of competitiveness occurs on the regional level.69

In the UK only about 25% of public sector expenditure is controlled by regional and localgovernments, below most other OECD countries including Germany (35%) and theUnited States (42%), but above France (18%).70 The UK’s centralised organisationalstructure for government has repercussions for competitiveness: Public spending isinevitably less well adapted to regional and local opportunities and needs. And privatesector leaders are less willing to engage in local and regional efforts, if importantdecisions affecting the quality of their business environment are made in the capital.

The Regional Development Agencies (RDA’s),71 established by order of the RegionalDevelopment Agencies Act of 1998, has created new institutions to address regional

Competitiveness and the UK Business Environment: Summary of the Evidence

33UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

competitiveness in the UK. The RDA’s are an innovative approach to strengthen regionalpolicy in the UK, but it will take more time to evaluate if they can overcome the inherentchallenges they face in the given structure of UK government.72

Competitiveness and the UK Business Environment: Summary of the Evidence

References

30 Porter (2002)

31 Porter (1998)

32 For a good overview on policyinitiatives and outcomes see DTI(2002) and OECD (2002)

33 Beath (2002) argues instead thatthere has been remarkableconsistency in much of themicroeconomic policies.

34 Porter (2002a)

35 The pharmaceutical sector andits ability to draw on the UKscience base is a notableexamples.

36 Global Competitiveness Report(2002), unpublished data.

37 OECD (2002a), IMF (2003). It isunclear if the higher level ofprivatization in the UK isimportant in explaining thisdifference.

38 OECD (2000)

39 OECD (2002a)

40 Hogarth/Wilson (2001)

41 OECD (2001)

42 Nickell/Van Reenen (2002)

43 European Commission (2002)

44 Ashworth et al. (2001)

45 OECD (2001)

46 JM Consulting (2001)

47 For general information onrecent policy changes see HMTreasury (2001a)

48 The research reviewed did notdistinguish more betweenopenness to EU members in thecommon market and opennessto countries outside the EU.

49 Bartelsmann et al. (2003)

50 European Commission (2001)

51 McKinsey (1998)

52 Bond/Chennells (2000)

53 Nickell (2002)

54 OECD (2002a)

55 European Commission (2001)

56 Porter/Esty (2001)

57 Porter (1998), Porter (2000)

58 In appendix A we have includeda more detailed ranking ofsubclusters by exportperformance.

59 There is a significant literature onthe UK biotechnology cluster.See DTI (1999) for thegovernment perspective. Seealso European Commission(2001) and OECD (2002b)

60 “Motorsport Valley” inOxfordshire is claimed to be

home to more than 700motorsport-related companies.

61 DTI (2001)

62 Porter (2003), Porter/Council onCompetitiveness/Monitor Group(2001).

63 Porter/Emmons (2003)

64 Porter/Sölvell (2003)

65 See, for example, the discussionof the Business Link-scheme inOughton (1997)

66 HM Treasury (2001b)

67 See the results of a statisticalanalysis in appendix B

68 Soltwedel (1999) quoted in IMF(2000).

69 Porter/Council onCompetitiveness/Monitor Group(2001), Porter (2001d)

70 OECD (2002a)

71 For more information on theRDA’s see www.dti.gov.uk/rda.Other regional efforts have beenundertaken with EU support inthe Innovating Regions in Europe(IRE) network. This effort ispromising, but lacks a consistentintellectual framework.

72 Cockerill (2002)

34 UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

4

Competitiveness andUK Company Behaviour:The Role of Management

The productivity of a country is ultimately set by the productivity of its companies, bothdomestic firms and the subsidiaries of foreign companies operating there. However, thesophistication of companies is inextricably intertwined with the quality of the nationalbusiness environment. More sophisticated company strategies require more highlyskilled people, better information, improved infrastructure, more capable suppliers, moreadvanced research institutions, and stronger competitive pressure, among other things.

Companies in a nation must upgrade their operating practices and strategies if successfuleconomic development is to occur. The competitive advantages of a nation’s companiesmust shift from comparative advantages (low-cost labour or natural resources) tocompetitive advantages arising from unique products and processes. Companies mustmove from tapping foreign distribution channels to building their own channels.

a) UK Company Performance

The UK is home to a significant number of large, internationally successful companies.Within Europe, the UK has an equal or higher number of companies in the Fortune 100relative to GDP than do Germany or France. Among multinational companies (MNC’s)with the largest foreign assets (classified as transnational companies by UNCTAD) theUK is home to 14 companies, behind only the United States and Japan and ahead ofGermany, France, Italy, and the Netherlands.73 In a dataset of 10,000 large companiesfrom Canada, Germany, Japan, the United States, and the United Kingdom, UKcompanies reported the highest return on equity in the 1997-2001 period.74

Productivity levels of UK multinationals are roughly in line with German and Frenchmultinationals, but lag US multinationals.75 Productivity of domestic UK companies islower than that of the MNC’s operating in that country, as in other countries. Thedifference in relative UK productivity across industries is consistent with theircompetitiveness as revealed in their export positions: strengths in services (retail,banking) and selected manufacturing (oil & gas, pharmaceuticals, food processing) and

35UK COMPETITIVENESS: MOVING TO THE NEXT STAGE

weaknesses in many other manufacturing industries.76 The hypothesis of a “long tail” ofunderperforming firms, i.e. the presence of a higher share of companies with very lowperformance in the UK relative to other countries, finds no support in current research.77

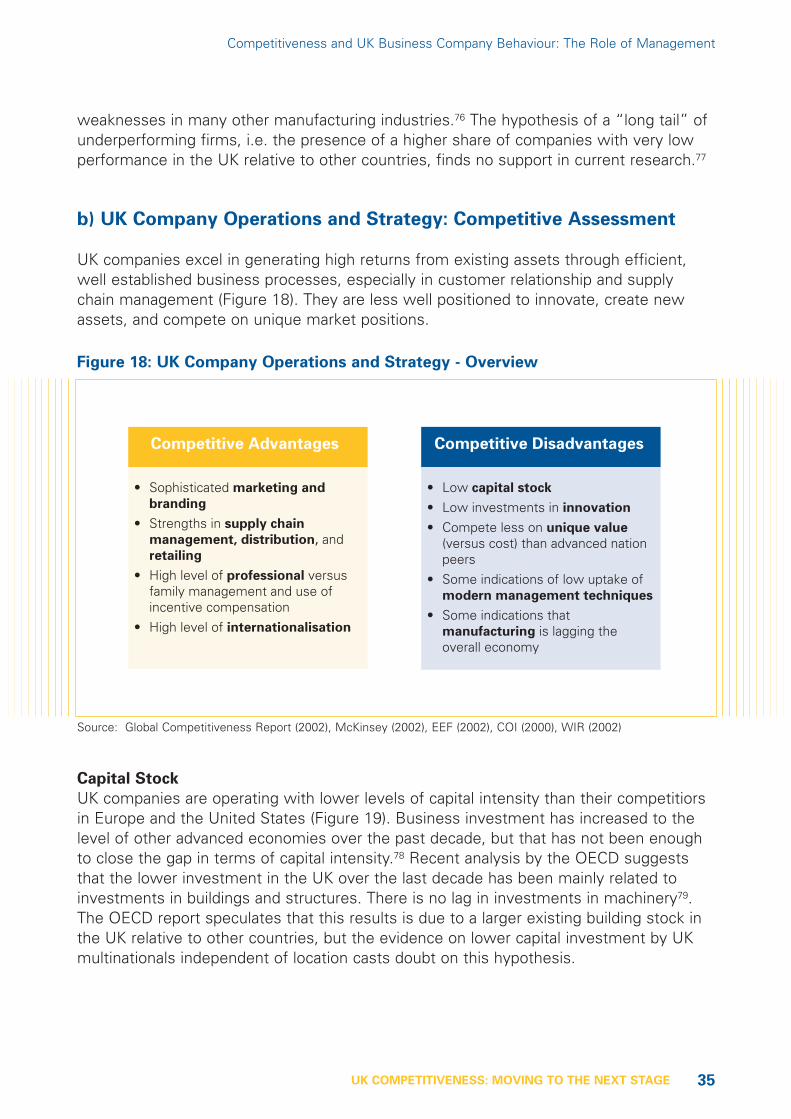

b) UK Company Operations and Strategy: Competitive Assessment

UK companies excel in generating high returns from existing assets through efficient,well established business processes, especially in customer relationship and supplychain management (Figure 18). They are less well positioned to innovate, create newassets, and compete on unique market positions.

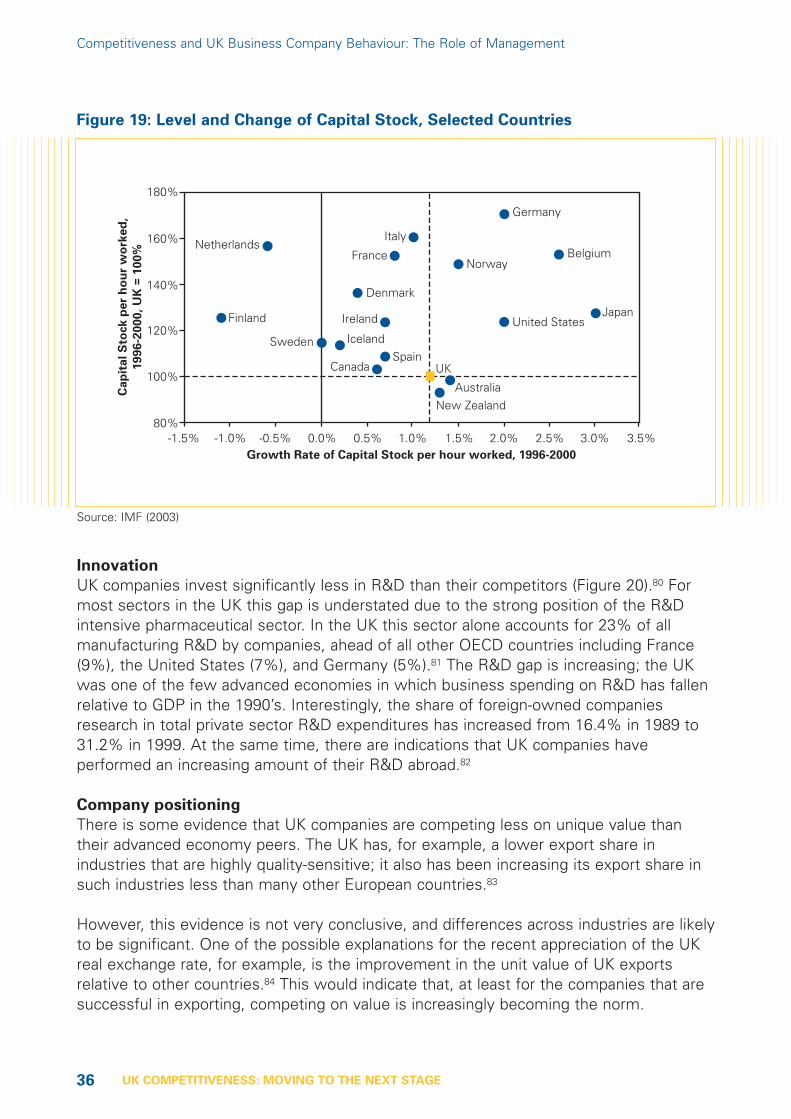

Capital Stock

UK companies are operating with lower levels of capital intensity than their competitiorsin Europe and the United States (Figure 19). Business investment has increased to thelevel of other advanced economies over the past decade, but that has not been enoughto close the gap in terms of capital intensity.78 Recent analysis by the OECD suggeststhat the lower investment in the UK over the last decade has been mainly related toinvestments in buildings and structures. There is no lag in investments in machinery79.The OECD report speculates that this results is due to a larger existing building stock inthe UK relative to other countries, but the evidence on lower capital investment by UKmultinationals independent of location casts doubt on this hypothesis.

Competitiveness and UK Business Company Behaviour: The Role of Management

• Sophisticated marketing and

branding

• Strengths in supply chain