Embed Size (px)

Citation preview

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20140

2015

UNAUDITED INTERIM RESULTSFOR THE SIX MONTHS ENDED 31 DECEMBER 2014

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20141

AGENDA

02GROUP OVERVIEW 08FINANCIAL

REVIEW 24DIVISIONALREVIEW 39QUESTIONS

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20142

02GROUP OVERVIEW

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20143

GROUP OVERVIEW

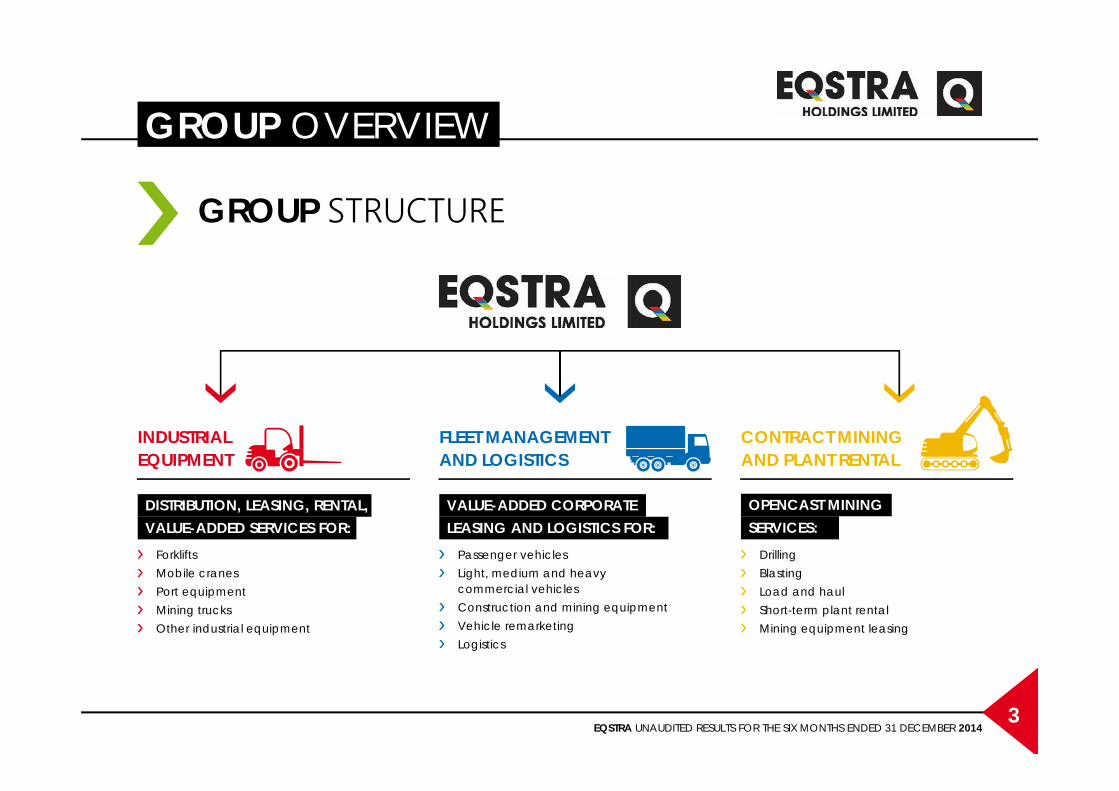

GROUP STRUCTURE

DISTRIBUTION, LEASING, RENTAL,VALUE-ADDED SERVICES FOR:

INDUSTRIALEQUIPMENT

ForkliftsMobile cranesPort equipmentMining trucksOther industrial equipment

VALUE-ADDED CORPORATELEASING AND LOGISTICS FOR:

FLEET MANAGEMENTAND LOGISTICS

Passenger vehiclesLight, medium and heavycommercial vehiclesConstruction and mining equipmentVehicle remarketingLogistics

OPENCAST MININGSERVICES:

CONTRACT MININGAND PLANT RENTAL

DrillingBlastingLoad and haulShort-term plant rentalMining equipment leasing

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20144

BUSINESS MODEL

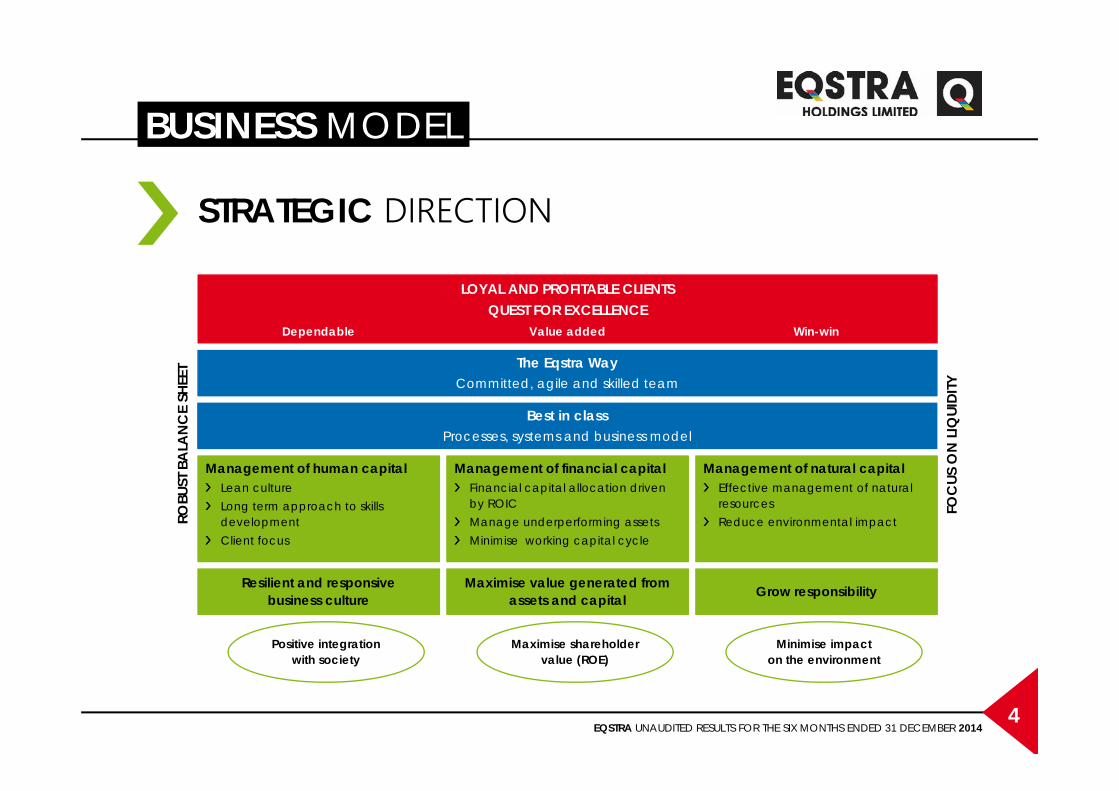

STRATEGIC DIRECTION

Management of human capitalLean cultureLong term approach to skills developmentClient focus

Management of financial capitalFinancial capital allocation drivenby ROICManage underperforming assetsMinimise working capital cycle

Management of natural capitalEffective management of natural resourcesReduce environmental impact

LOYAL AND PROFITABLE CLIENTSQUEST FOR EXCELLENCE

The Eqstra WayCommitted, agile and skilled team

Best in classProcesses, systems and business model

Resilient and responsivebusiness culture

Maximise value generated fromassets and capital Grow responsibility

ROBU

ST B

ALA

NC

E SH

EET

FOC

US O

N L

IQUI

DITY

Dependable Value added Win-win

Positive integrationwith society

Maximise shareholder value (ROE)

Minimise impacton the environment

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20145

STRATEGIC DIRECTION

Moved from a “growth” strategy to a “cash preservation and balance sheet strengthening” strategy

Dividend payments only to resume once the targeted capital adequacy, the debt market and company liquidity are normalised

Increase the capital adequacy in the common monetary area from 21% to 23%by June 2016 and 25% by June 2017

Reduce contract mining in an orderly fashion to ensure that the revenue generating asset base is less than 30% of the group’s asset base

Reduce interest-bearing borrowings by approximately R400m by June 2015

Consider alternative business models that will be sustainable in the long-term

ROBUST BALANCE SHEET

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20146

STRATEGIC DIRECTION

The collapse and the down grade of certain SA banks have largely contributed to the liquidity squeeze for corporate issuance in the capital market towards the end of 2014

Eqstra recognises that due to above it may not be able to raise new debt in the capital market in the short to medium term, therefore making the following provision:› Suspension all uncommitted expansion capital expenditure while maintaining

the integrity of the existing revenue generating asset base› Sale of certain non-core assets› Implement alternative sources of long term funding outside the South African

market, i.e. export credit (ECA) funding› Increasing the group’s liquidity buffer from 10% to a target of more than 15%› Will consider issuing a bond offshore if required

FOCUS ON LIQUIDITY

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20147

GROUP OVERVIEW

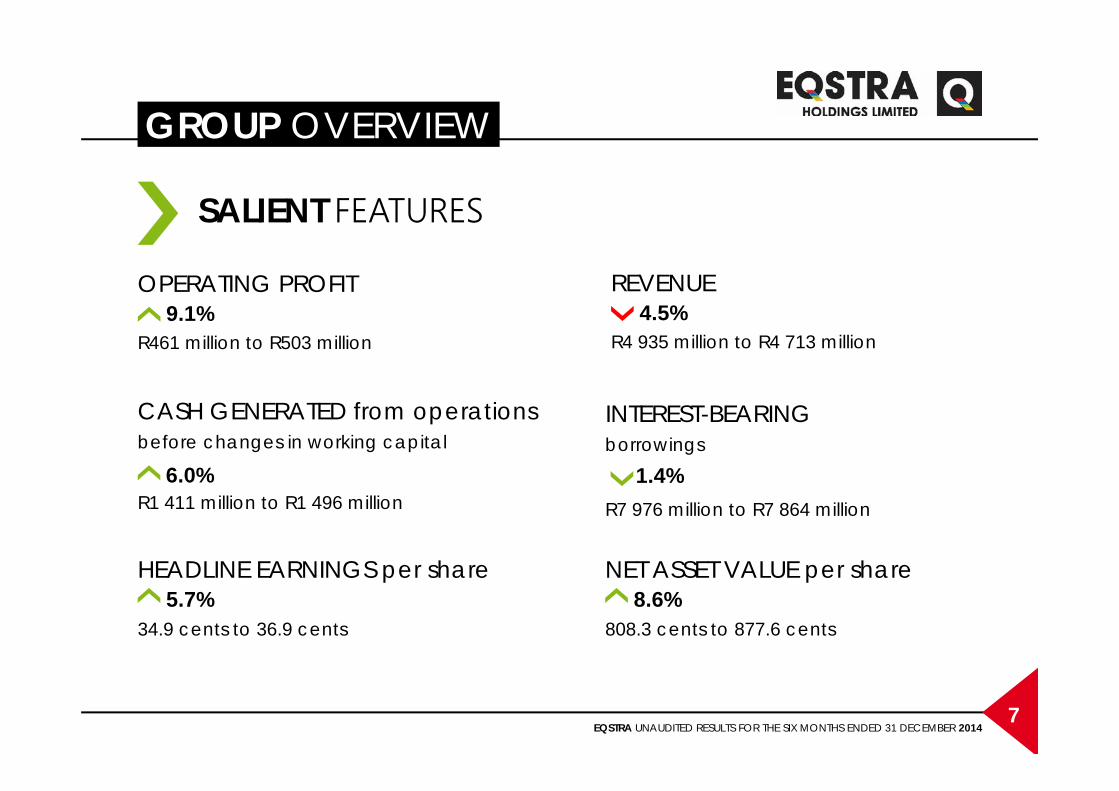

SALIENT FEATURES

OPERATING PROFIT9.1%

R461 million to R503 million

6.0%R1 411 million to R1 496 million

CASH GENERATED from operations before changes in working capital

34.9 cents to 36.9 cents

HEADLINE EARNINGS per share5.7%

REVENUE4.5%

R4 935 million to R4 713 million

1.4%R7 976 million to R7 864 million

808.3 cents to 877.6 cents

NET ASSET VALUE per share 8.6%

INTEREST-BEARING borrowings

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20148

08FINANCIAL REVIEW

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 20149

FINANCIAL REVIEW

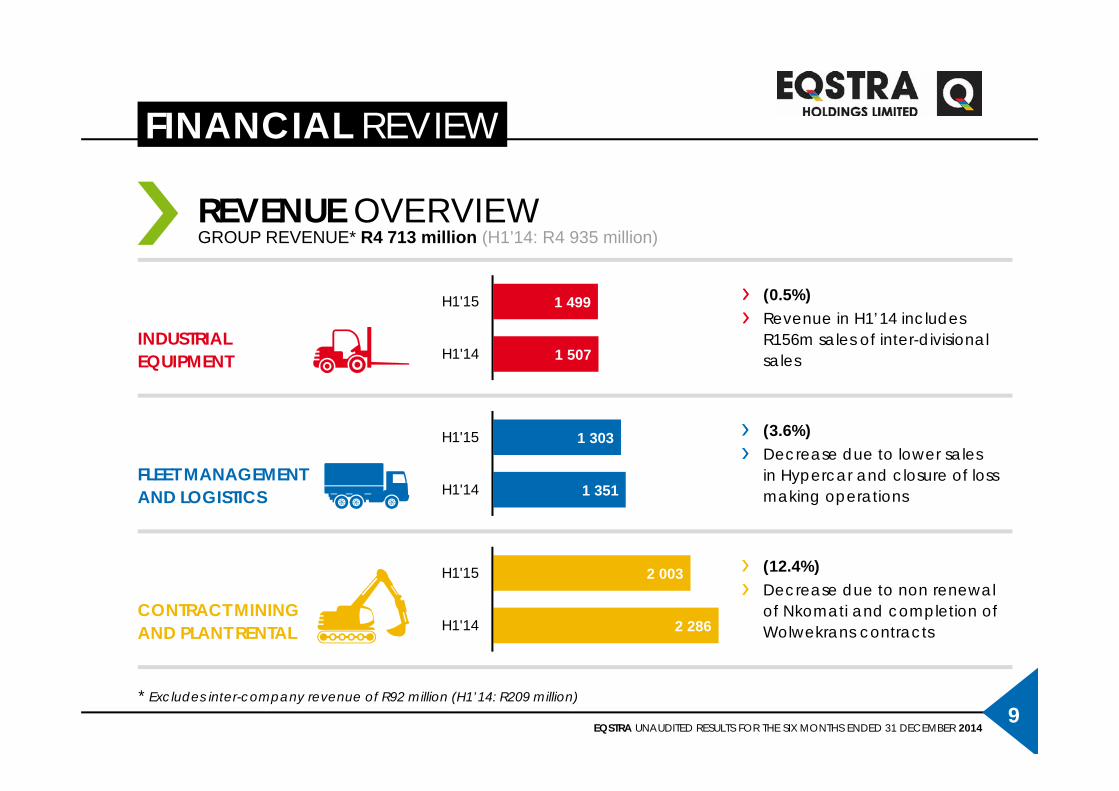

* Excludes inter-company revenue of R92 million (H1’14: R209 million)

REVENUE OVERVIEWGROUP REVENUE* R4 713 million (H1’14: R4 935 million)

INDUSTRIALEQUIPMENT

FLEET MANAGEMENTAND LOGISTICS

CONTRACT MININGAND PLANT RENTAL

1 507

1 499

H1'14

H1'15 (0.5%)Revenue in H1’14 includes R156m sales of inter-divisional sales

1 351

1 303

H1'14

H1'15 (3.6%)Decrease due to lower salesin Hypercar and closure of loss making operations

2 286

2 003

H1'14

H1'15 (12.4%)Decrease due to non renewal of Nkomati and completion of Wolwekrans contracts

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201410

FINANCIAL REVIEW

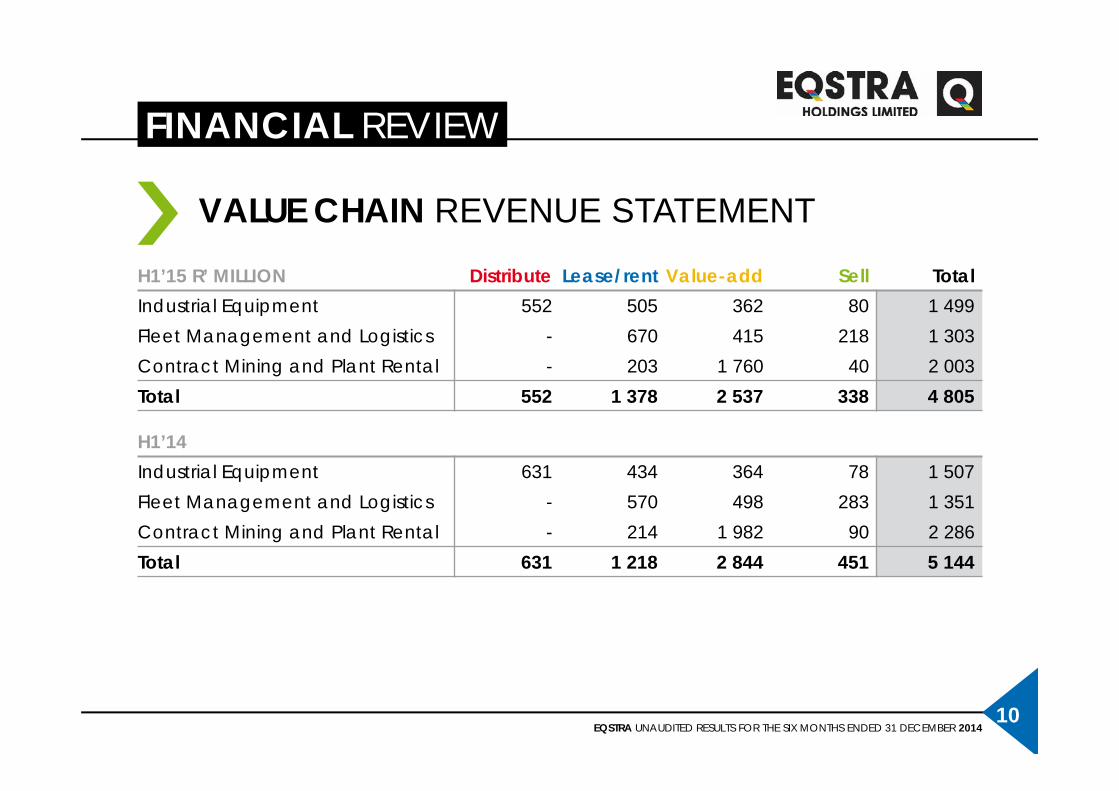

VALUE CHAIN REVENUE STATEMENT

H1’15 R’ MILLION Distribute Lease/rent Value-add Sell TotalIndustrial Equipment 552 505 362 80 1 499Fleet Management and Logistics - 670 415 218 1 303Contract Mining and Plant Rental - 203 1 760 40 2 003Total 552 1 378 2 537 338 4 805

H1’14Industrial Equipment 631 434 364 78 1 507Fleet Management and Logistics - 570 498 283 1 351Contract Mining and Plant Rental - 214 1 982 90 2 286Total 631 1 218 2 844 451 5 144

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201411

FINANCIAL REVIEW

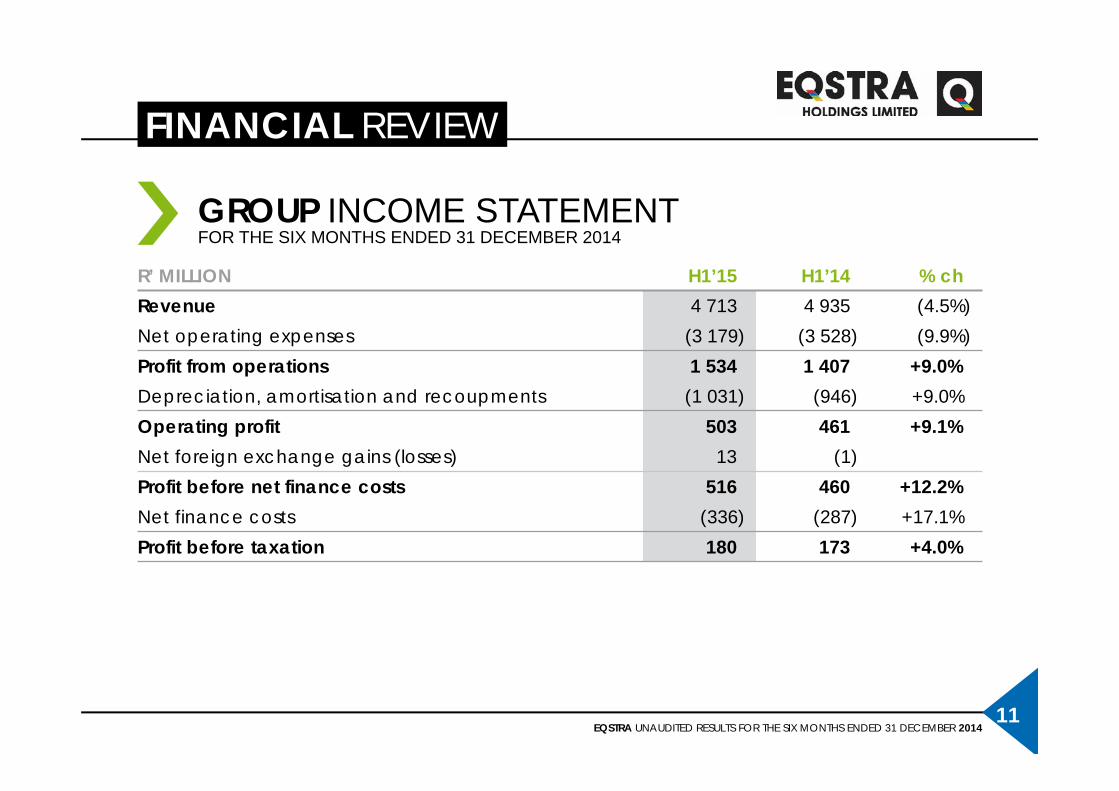

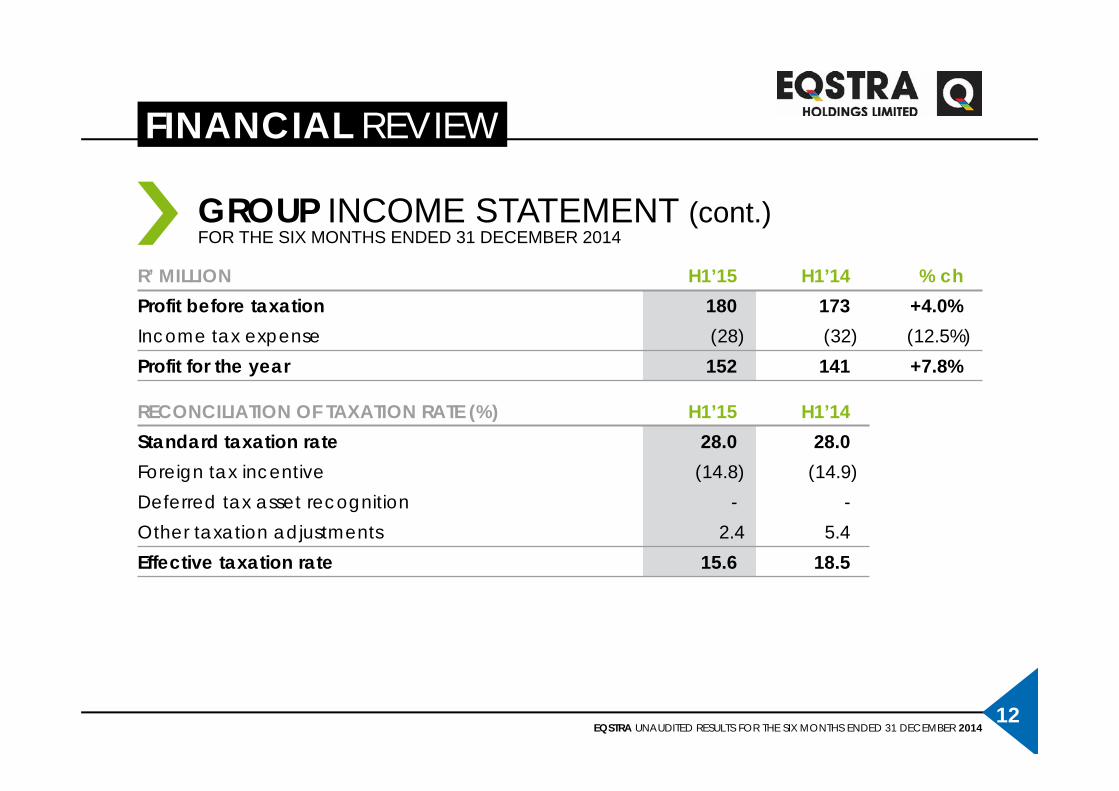

GROUP INCOME STATEMENT

R’ MILLION H1’15 H1’14 % chRevenue 4 713 4 935 (4.5%)Net operating expenses (3 179) (3 528) (9.9%)Profit from operations 1 534 1 407 +9.0%Depreciation, amortisation and recoupments (1 031) (946) +9.0%Operating profit 503 461 +9.1%Net foreign exchange gains (losses) 13 (1)Profit before net finance costs 516 460 +12.2%Net finance costs (336) (287) +17.1%Profit before taxation 180 173 +4.0%

FOR THE SIX MONTHS ENDED 31 DECEMBER 2014

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201412

FINANCIAL REVIEW

GROUP INCOME STATEMENT (cont.)

R’ MILLION H1’15 H1’14 % chProfit before taxation 180 173 +4.0%Income tax expense (28) (32) (12.5%)Profit for the year 152 141 +7.8%

RECONCILIATION OF TAXATION RATE (%) H1’15 H1’14Standard taxation rate 28.0 28.0Foreign tax incentive (14.8) (14.9)Deferred tax asset recognition - -Other taxation adjustments 2.4 5.4Effective taxation rate 15.6 18.5

FOR THE SIX MONTHS ENDED 31 DECEMBER 2014

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201413

FINANCIAL REVIEW

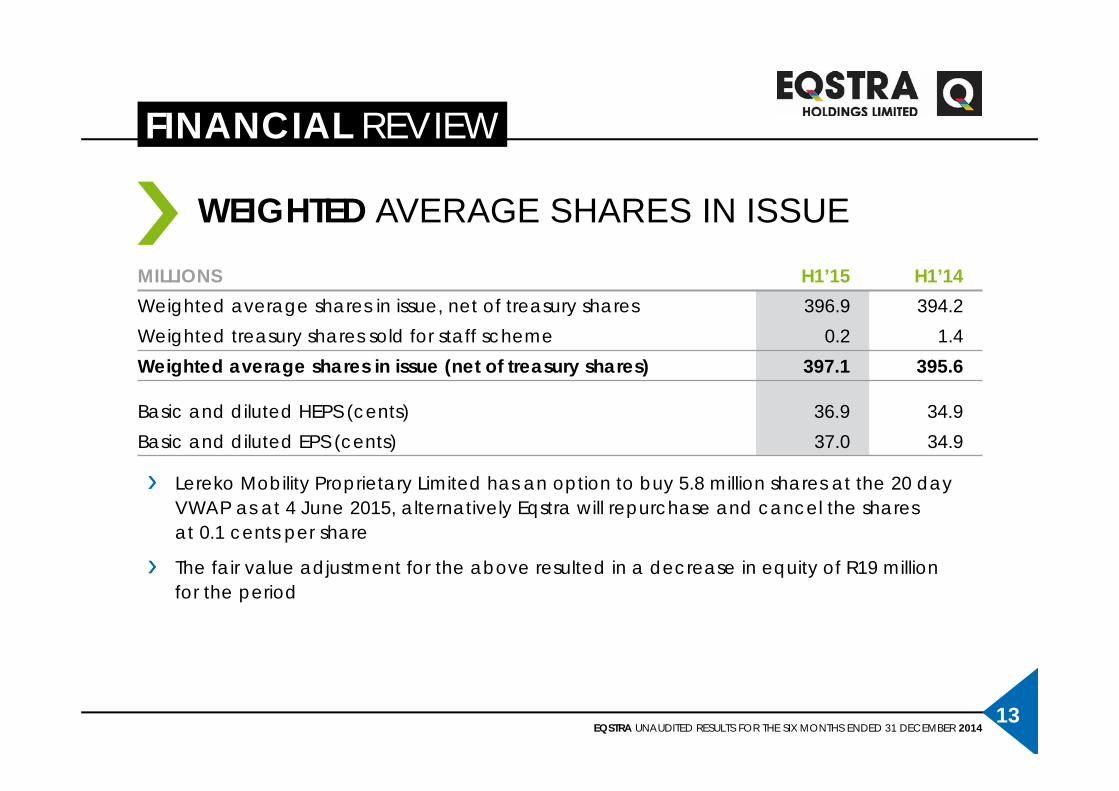

Lereko Mobility Proprietary Limited has an option to buy 5.8 million shares at the 20 day VWAP as at 4 June 2015, alternatively Eqstra will repurchase and cancel the sharesat 0.1 cents per share

The fair value adjustment for the above resulted in a decrease in equity of R19 millionfor the period

WEIGHTED AVERAGE SHARES IN ISSUE

MILLIONS H1’15 H1’14Weighted average shares in issue, net of treasury shares 396.9 394.2Weighted treasury shares sold for staff scheme 0.2 1.4Weighted average shares in issue (net of treasury shares) 397.1 395.6

Basic and diluted HEPS (cents) 36.9 34.9Basic and diluted EPS (cents) 37.0 34.9

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201414

FINANCIAL REVIEW

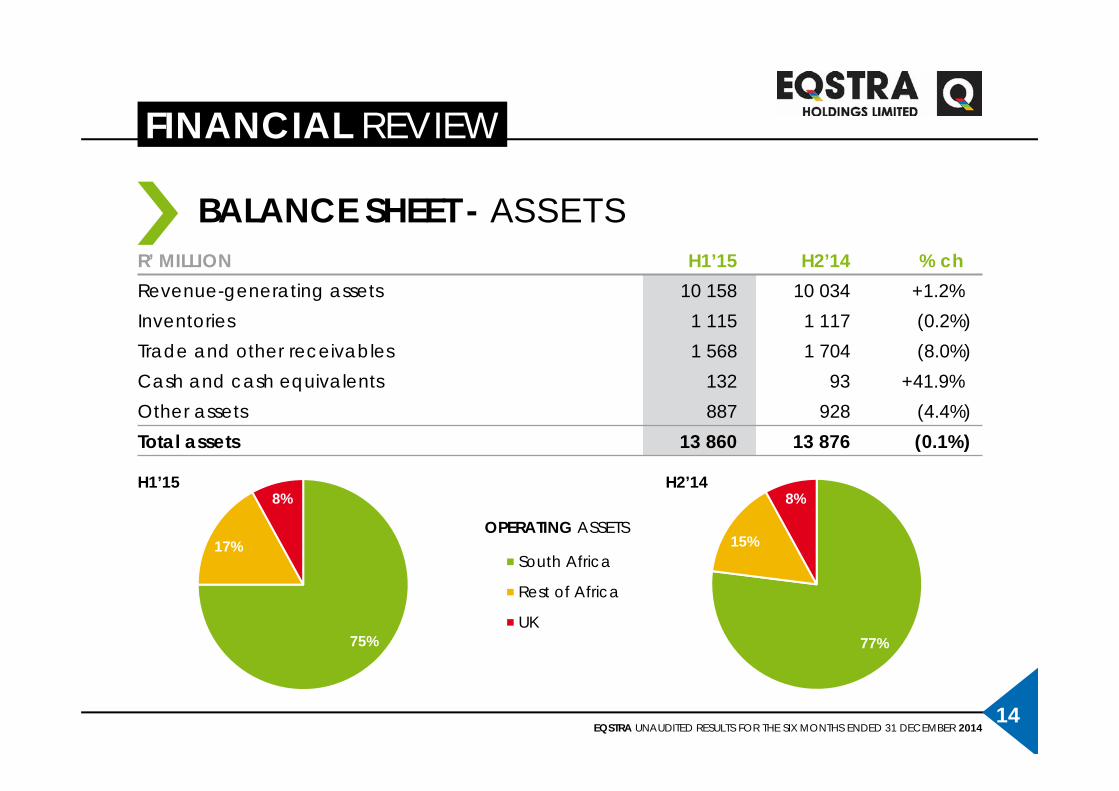

BALANCE SHEET - ASSETSR’ MILLION H1’15 H2’14 % chRevenue-generating assets 10 158 10 034 +1.2%Inventories 1 115 1 117 (0.2%)Trade and other receivables 1 568 1 704 (8.0%)Cash and cash equivalents 132 93 +41.9%Other assets 887 928 (4.4%)Total assets 13 860 13 876 (0.1%)

75%

17%

8%

South Africa

Rest of Africa

UK77%

15%

8%H1’15 H2’14

OPERATING ASSETS

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201415

FINANCIAL REVIEW

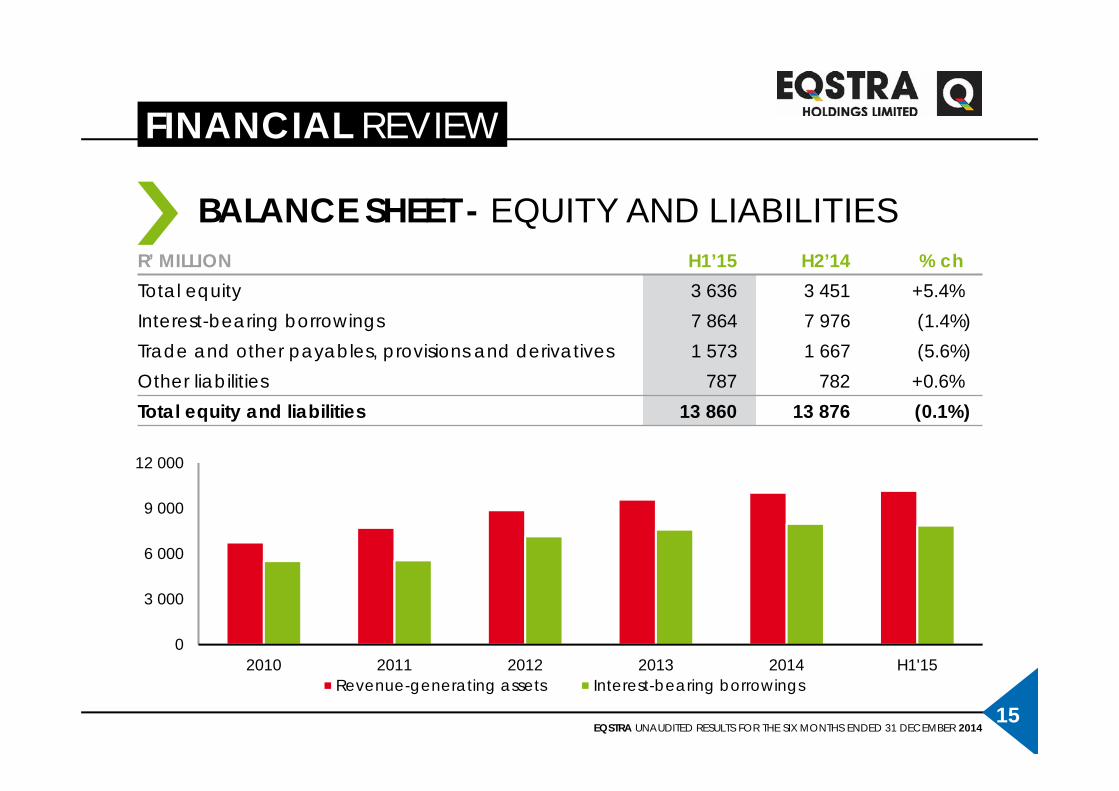

BALANCE SHEET - EQUITY AND LIABILITIESR’ MILLION H1’15 H2’14 % chTotal equity 3 636 3 451 +5.4%Interest-bearing borrowings 7 864 7 976 (1.4%)Trade and other payables, provisions and derivatives 1 573 1 667 (5.6%)Other liabilities 787 782 +0.6%Total equity and liabilities 13 860 13 876 (0.1%)

0

3 000

6 000

9 000

12 000

2010 2011 2012 2013 2014 H1'15Revenue-generating assets Interest-bearing borrowings

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201416

FINANCIAL REVIEW

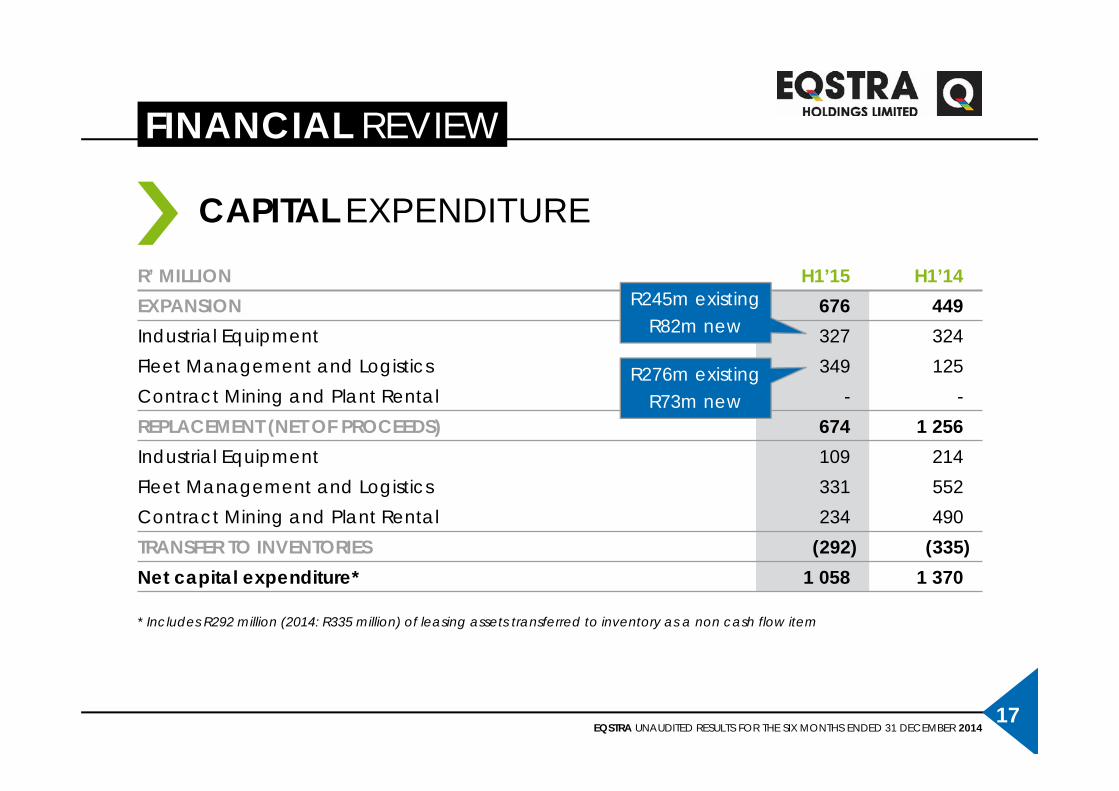

* Includes R292 million (2014: R335 million) of leasing assets transferred to inventory as a non cash flow item

CASH FLOW STATEMENT

R’ MILLION H1’15 H1’14 % chCash generated from operationsbefore working capital movements 1 496 1 411 +6.0%Working capital movements* 409 257 +59.1%Cash generated from operations 1 905 1 668 +14.2%Cash flows from interest and taxation (348) (298) +16.8%Net cash flows from operating activities 1 557 1 370 +13.6%Net cash flows from investing activities (1 356) (1 702) (20.3%)Net cash flows from financing activities (169) 96Net increase (decrease) in cash and cash equivalentsbefore effect of exchange rate 32 (236)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201417

FINANCIAL REVIEW

* Includes R292 million (2014: R335 million) of leasing assets transferred to inventory as a non cash flow item

CAPITAL EXPENDITURE

R’ MILLION H1’15 H1’14EXPANSION 676 449Industrial Equipment 327 324Fleet Management and Logistics 349 125Contract Mining and Plant Rental - -REPLACEMENT (NET OF PROCEEDS) 674 1 256Industrial Equipment 109 214Fleet Management and Logistics 331 552Contract Mining and Plant Rental 234 490TRANSFER TO INVENTORIES (292) (335)Net capital expenditure* 1 058 1 370

R245m existingR82m new

R276m existingR73m new

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201418

FINANCIAL REVIEW

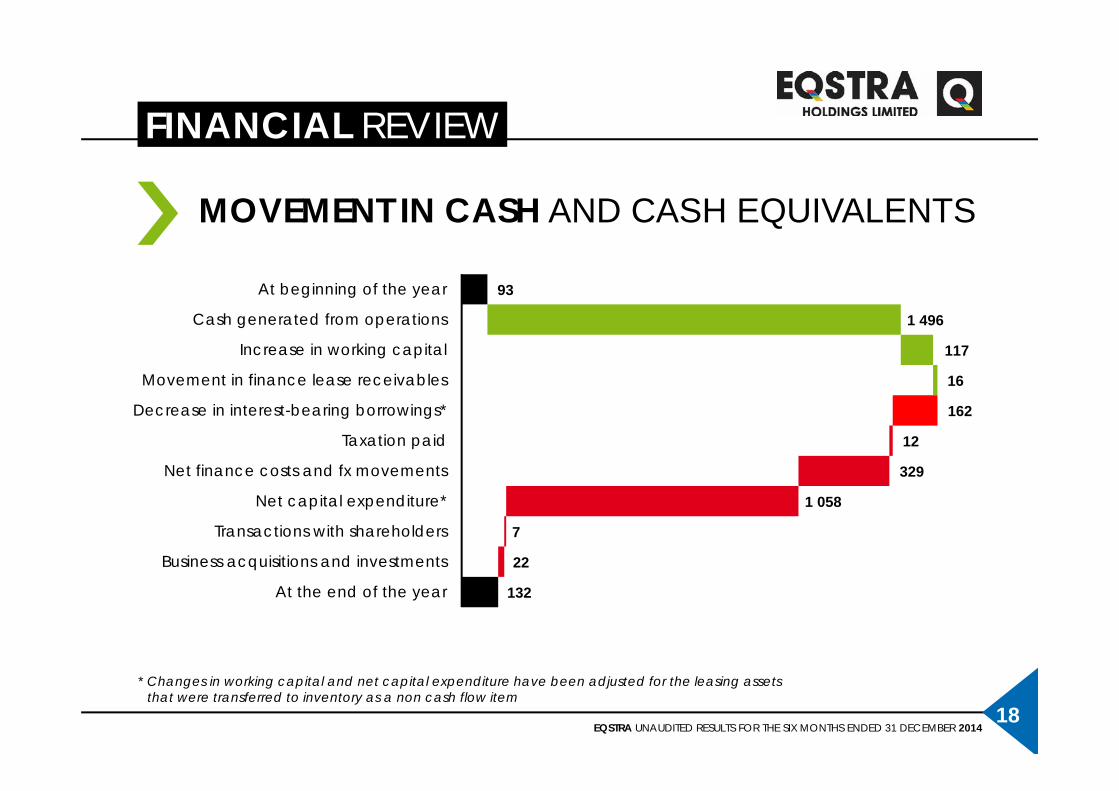

* Changes in working capital and net capital expenditure have been adjusted for the leasing assetsthat were transferred to inventory as a non cash flow item

MOVEMENT IN CASH AND CASH EQUIVALENTS

93

1 496

117

16

162

12

329

1 058

7

22

132

At beginning of the year

Cash generated from operations

Increase in working capital

Movement in finance lease receivables

Decrease in interest-bearing borrowings*

Taxation paid

Net finance costs and fx movements

Net capital expenditure*

Transactions with shareholders

Business acquisitions and investments

At the end of the year

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201419

FINANCIAL REVIEW

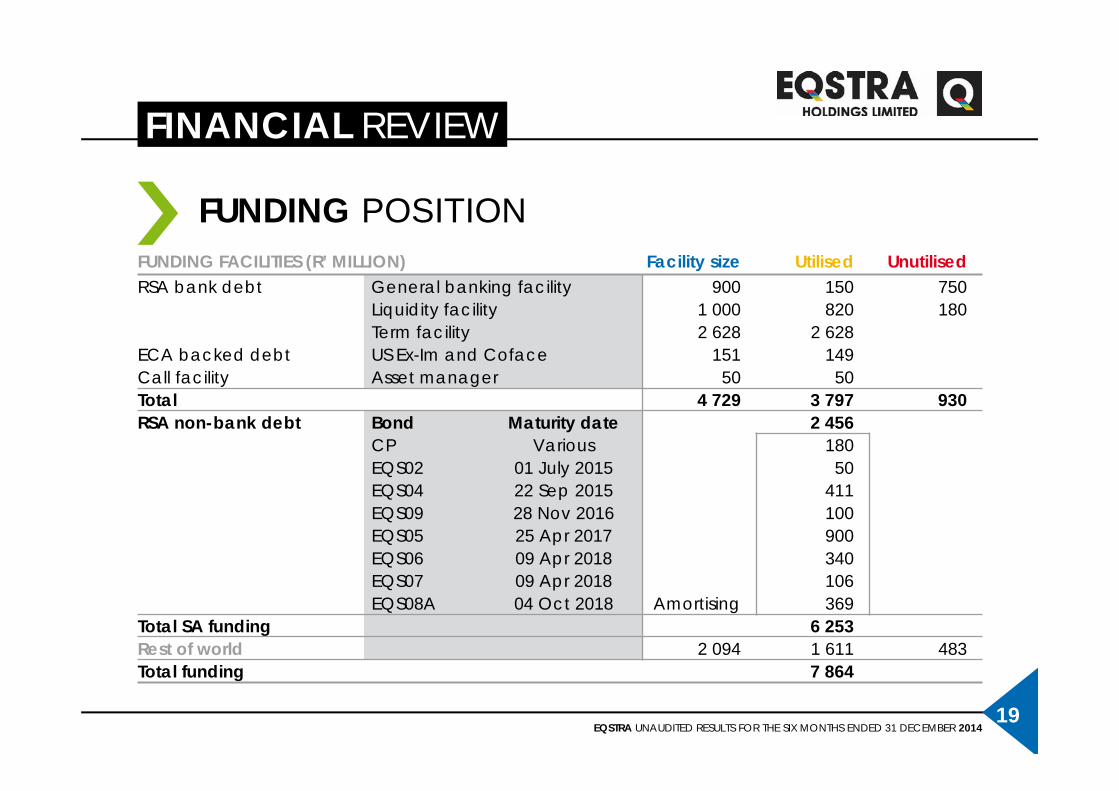

FUNDING POSITION FUNDING FACILITIES (R’ MILLION) Facility size Utilised UnutilisedRSA bank debt General banking facility 900 150 750

Liquidity facility 1 000 820 180Term facility 2 628 2 628

ECA backed debt US Ex-Im and Coface 151 149Call facility Asset manager 50 50Total 4 729 3 797 930RSA non-bank debt Bond Maturity date 2 456

CP Various 180EQS02 01 July 2015 50EQS04 22 Sep 2015 411EQS09 28 Nov 2016 100EQS05 25 Apr 2017 900EQS06 09 Apr 2018 340EQS07 09 Apr 2018 106EQS08A 04 Oct 2018 Amortising 369

Total SA funding 6 253Rest of world 2 094 1 611 483Total funding 7 864

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201420

FINANCIAL REVIEW

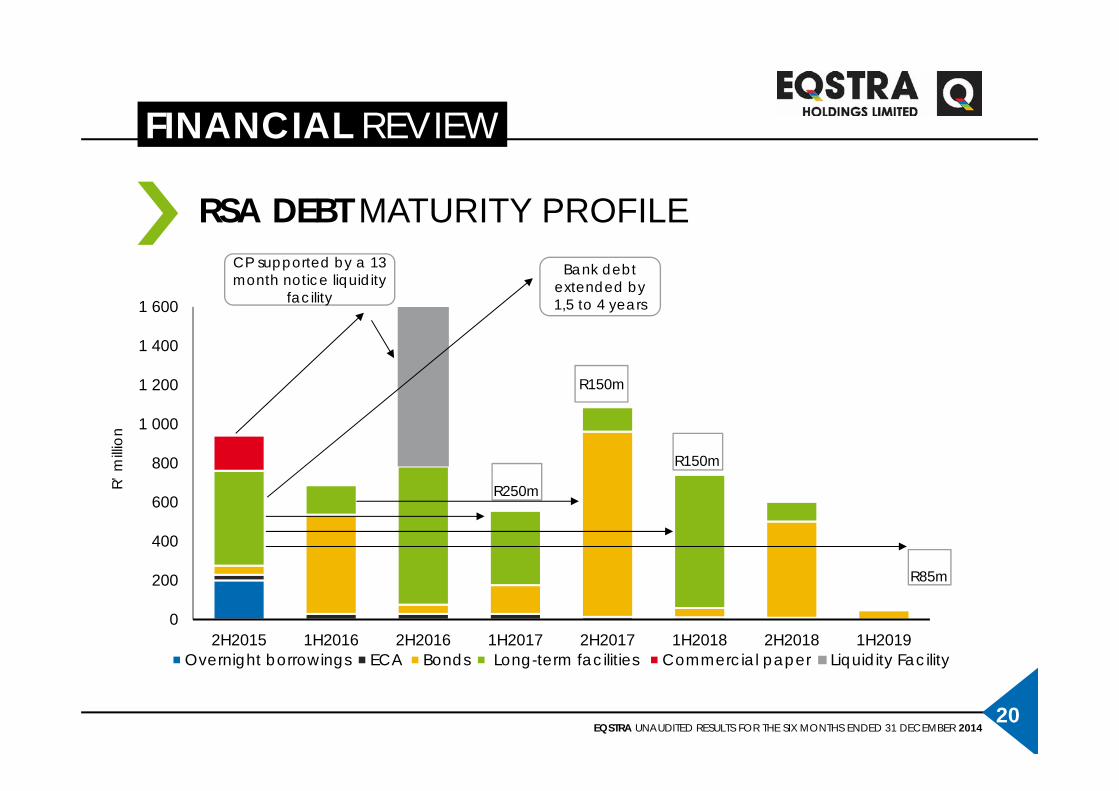

RSA DEBT MATURITY PROFILE

0

200

400

600

800

1 000

1 200

1 400

1 600

2H2015 1H2016 2H2016 1H2017 2H2017 1H2018 2H2018 1H2019

R’ m

illion

Overnight borrowings ECA Bonds Long-term facilities Commercial paper Liquidity Facility

Bank debt extended by 1,5 to 4 years

CP supported by a 13 month notice liquidity

facility

R250m

R150m

R150m

R85m

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201421

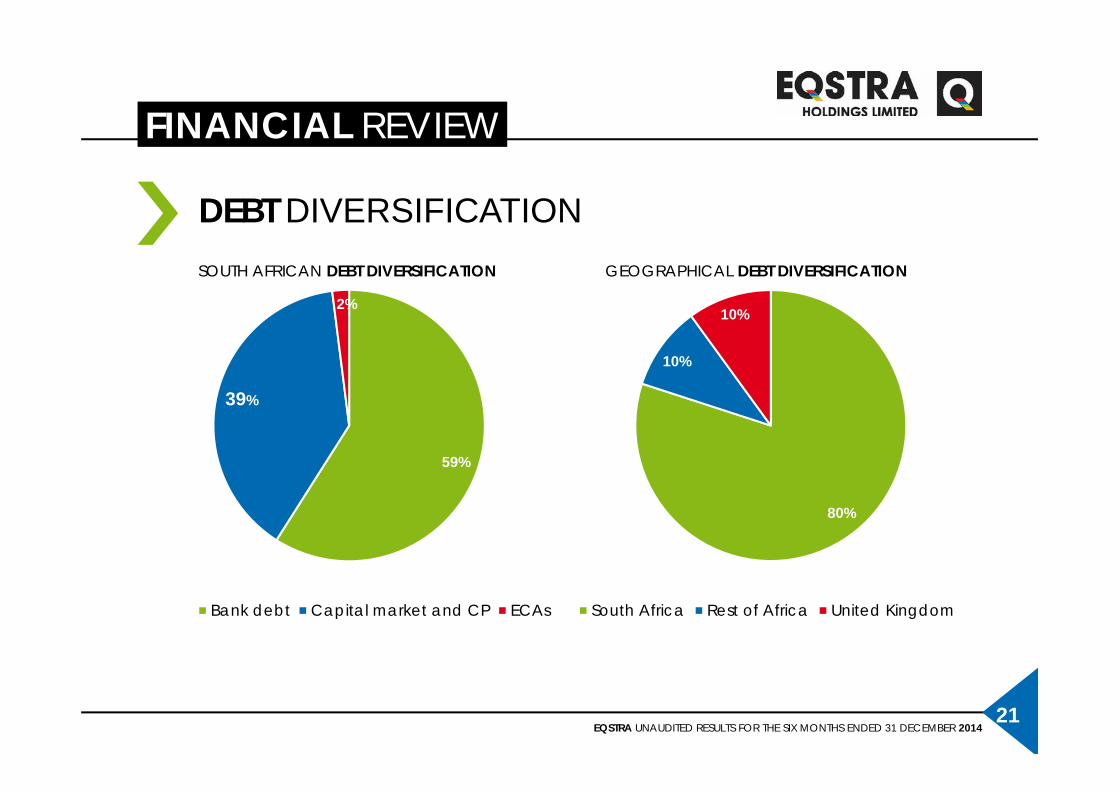

FINANCIAL REVIEW

DEBT DIVERSIFICATIONSOUTH AFRICAN DEBT DIVERSIFICATION

80%

10%

10%

South Africa Rest of Africa United Kingdom

GEOGRAPHICAL DEBT DIVERSIFICATION

59%

39%

2%

Bank debt Capital market and CP ECAs

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201422

FINANCIAL REVIEW

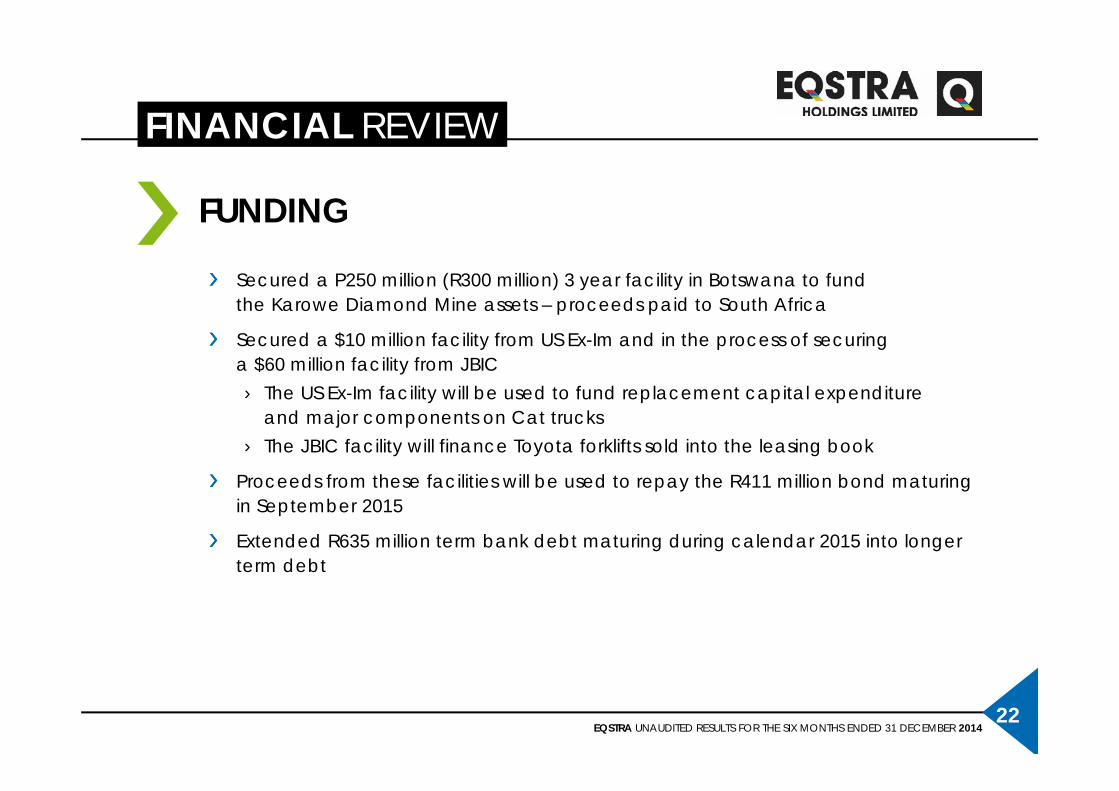

FUNDING

Secured a P250 million (R300 million) 3 year facility in Botswana to fundthe Karowe Diamond Mine assets – proceeds paid to South Africa

Secured a $10 million facility from US Ex-Im and in the process of securinga $60 million facility from JBIC› The US Ex-Im facility will be used to fund replacement capital expenditure

and major components on Cat trucks› The JBIC facility will finance Toyota forklifts sold into the leasing book

Proceeds from these facilities will be used to repay the R411 million bond maturing in September 2015

Extended R635 million term bank debt maturing during calendar 2015 into longer term debt

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201423

FINANCIAL REVIEW

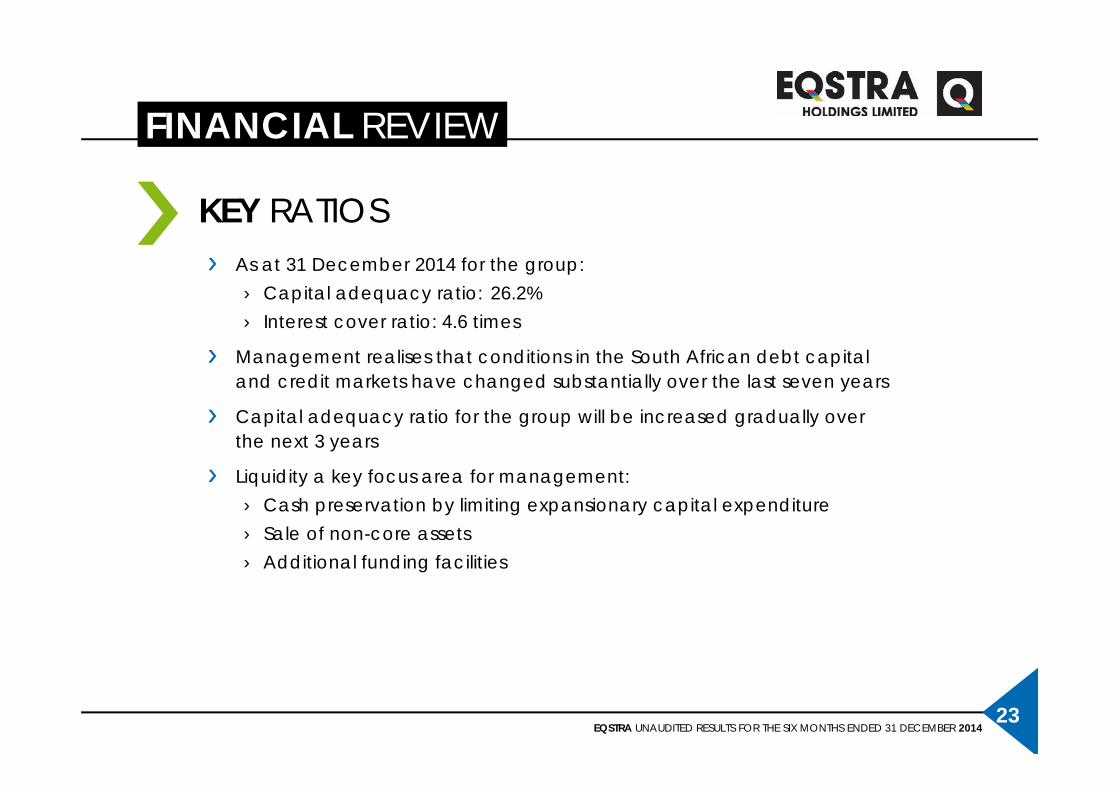

As at 31 December 2014 for the group:› Capital adequacy ratio: 26.2%› Interest cover ratio: 4.6 times

Management realises that conditions in the South African debt capitaland credit markets have changed substantially over the last seven years

Capital adequacy ratio for the group will be increased gradually overthe next 3 years

Liquidity a key focus area for management: › Cash preservation by limiting expansionary capital expenditure› Sale of non-core assets› Additional funding facilities

KEY RATIOS

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201424

24DIVISIONAL REVIEW

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201425

DIVISIONAL REVIEW

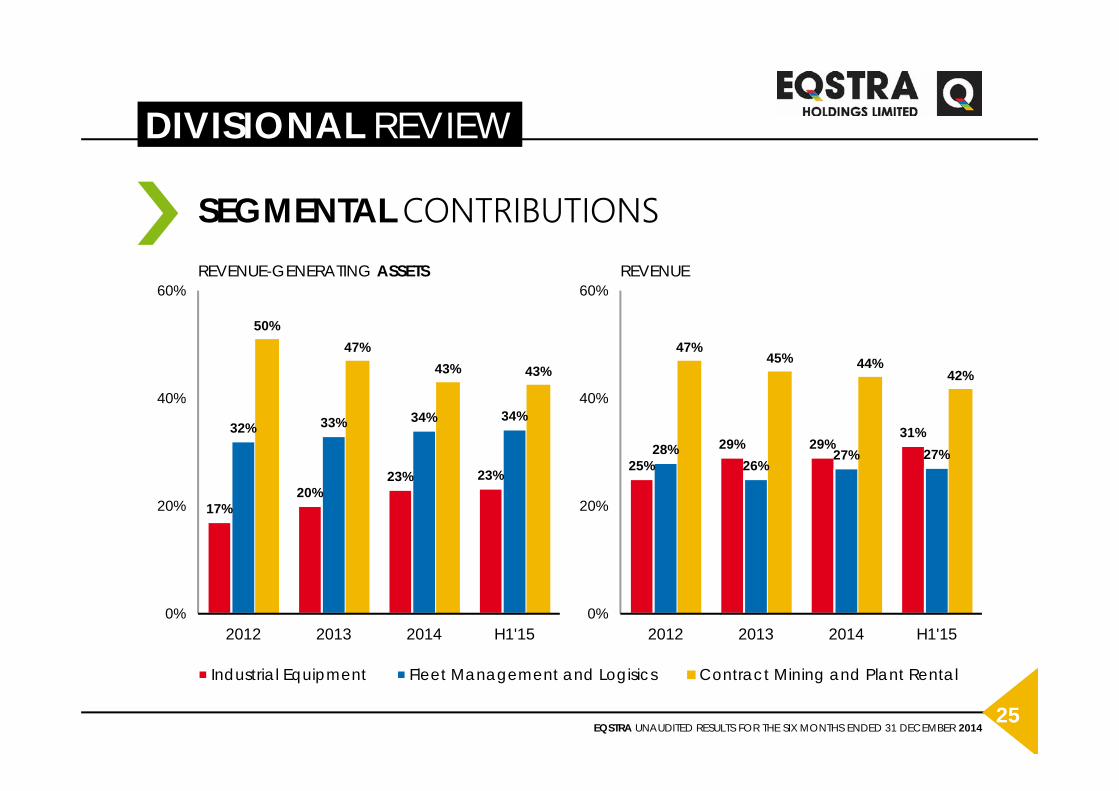

SEGMENTAL CONTRIBUTIONS

17%20%

23% 23%

32% 33% 34% 34%

50%47%

43% 43%

0%

20%

40%

60%

2012 2013 2014 H1'15

Industrial Equipment Fleet Management and Logisics Contract Mining and Plant Rental

REVENUE-GENERATING ASSETS

25%29% 29%

31%28%

26%27% 27%

47%45% 44%

42%

0%

20%

40%

60%

2012 2013 2014 H1'15

REVENUE

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201426

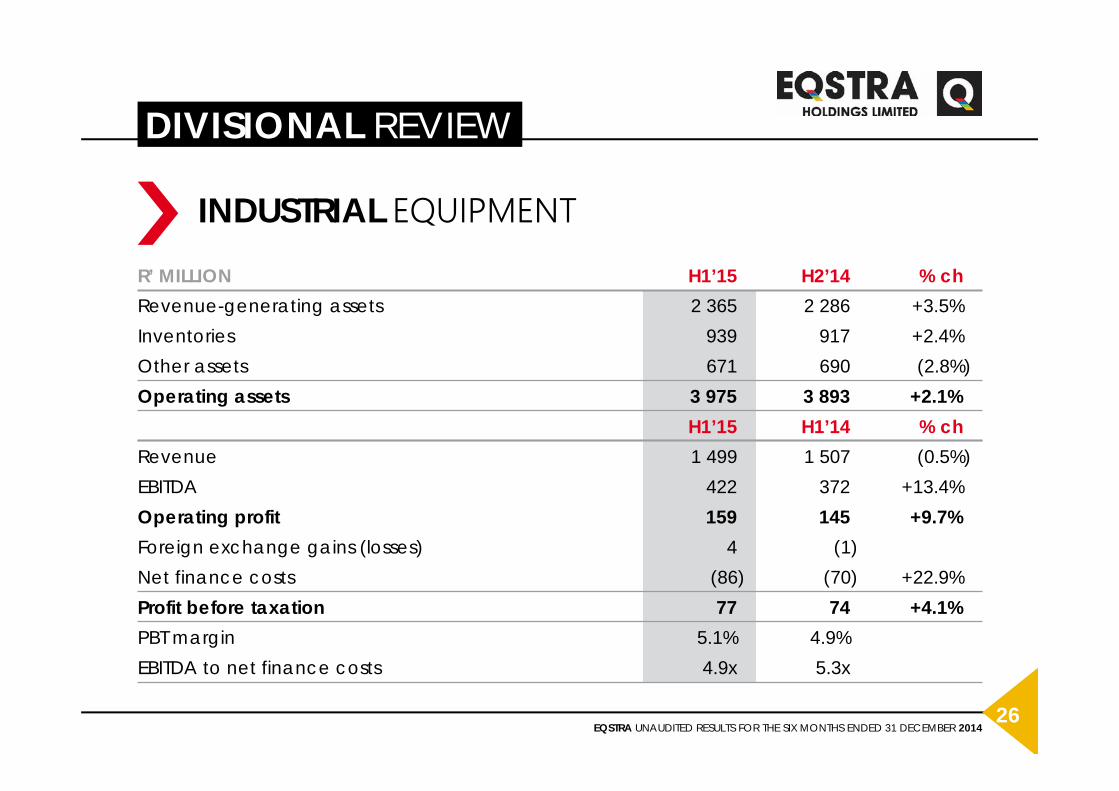

DIVISIONAL REVIEW

INDUSTRIAL EQUIPMENTR’ MILLION H1’15 H2’14 % chRevenue-generating assets 2 365 2 286 +3.5%Inventories 939 917 +2.4%Other assets 671 690 (2.8%)Operating assets 3 975 3 893 +2.1%

H1’15 H1’14 % chRevenue 1 499 1 507 (0.5%)EBITDA 422 372 +13.4%Operating profit 159 145 +9.7%Foreign exchange gains (losses) 4 (1)Net finance costs (86) (70) +22.9%Profit before taxation 77 74 +4.1%PBT margin 5.1% 4.9%EBITDA to net finance costs 4.9x 5.3x

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201427

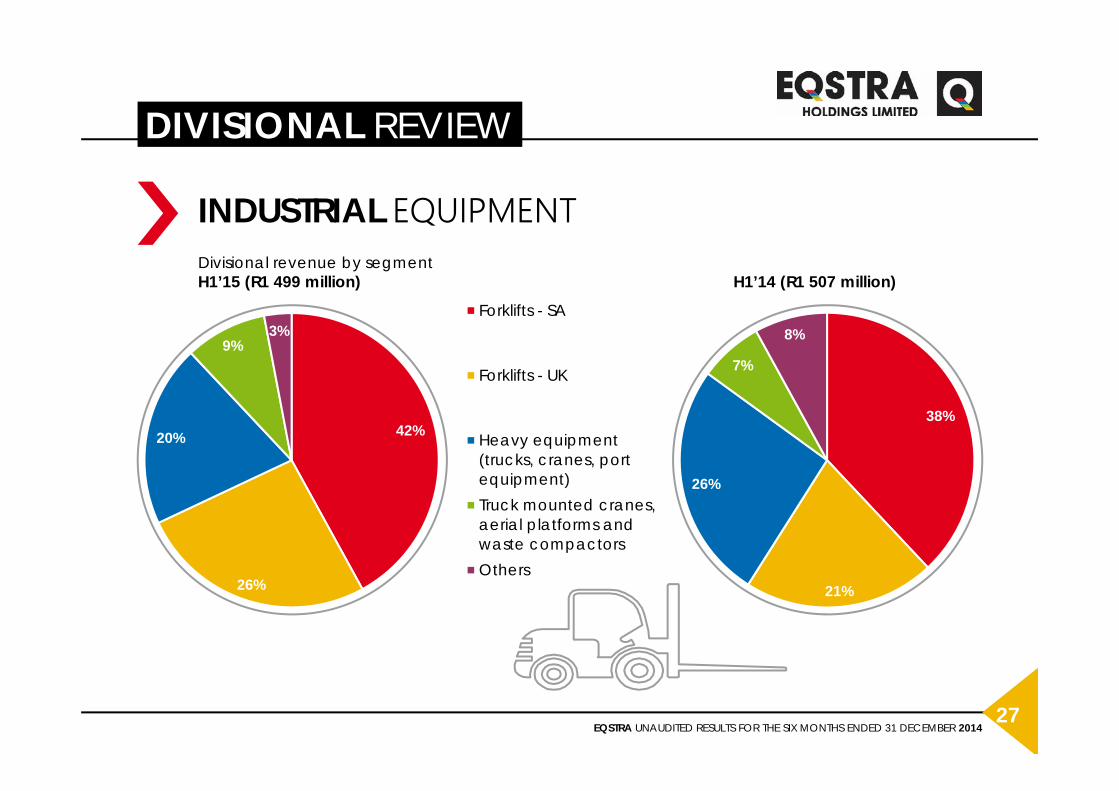

DIVISIONAL REVIEW

INDUSTRIAL EQUIPMENT

42%

26%

20%

9%3%

38%

21%

26%

7%

8%Forklifts - SA

Forklifts - UK

Heavy equipment(trucks, cranes, portequipment)Truck mounted cranes,aerial platforms andwaste compactorsOthers

Divisional revenue by segment H1’15 (R1 499 million) H1’14 (R1 507 million)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201428

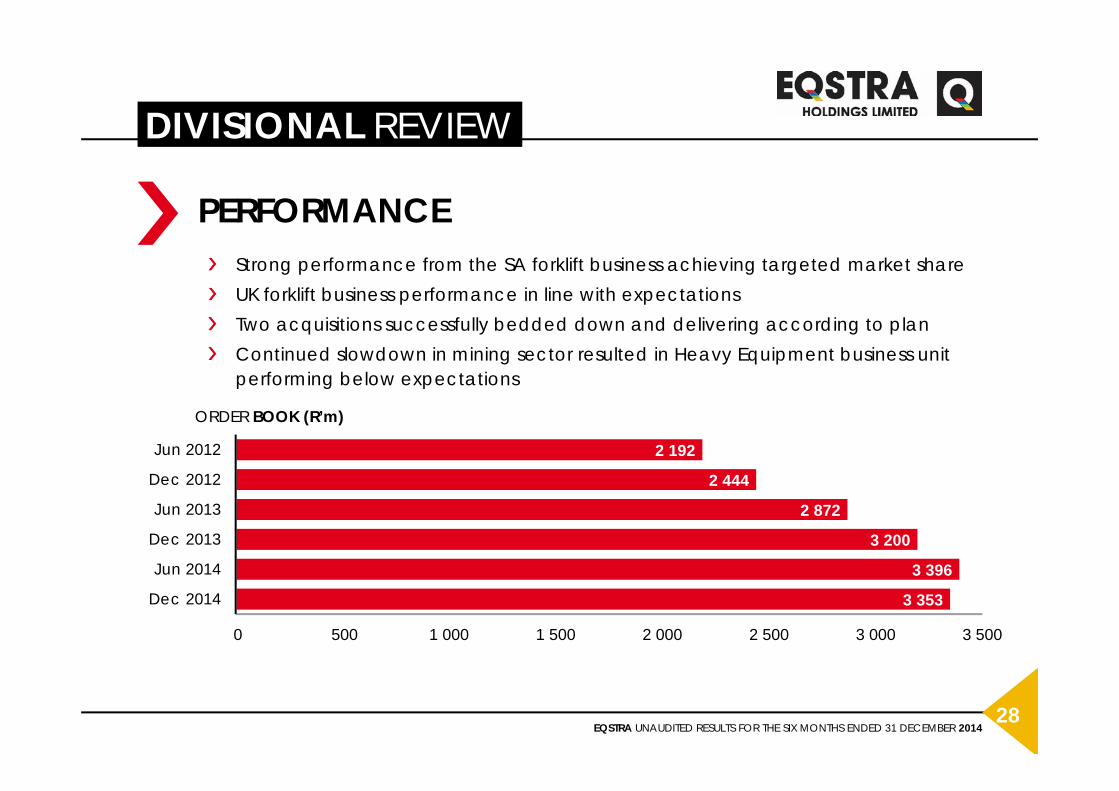

DIVISIONAL REVIEW

Strong performance from the SA forklift business achieving targeted market share UK forklift business performance in line with expectationsTwo acquisitions successfully bedded down and delivering according to planContinued slowdown in mining sector resulted in Heavy Equipment business unit performing below expectations

PERFORMANCE

3 353

3 396

3 200

2 872

2 444

2 192

0 500 1 000 1 500 2 000 2 500 3 000 3 500

Dec 2014

Jun 2014

Dec 2013

Jun 2013

Dec 2012

Jun 2012

ORDER BOOK (R’m)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201429

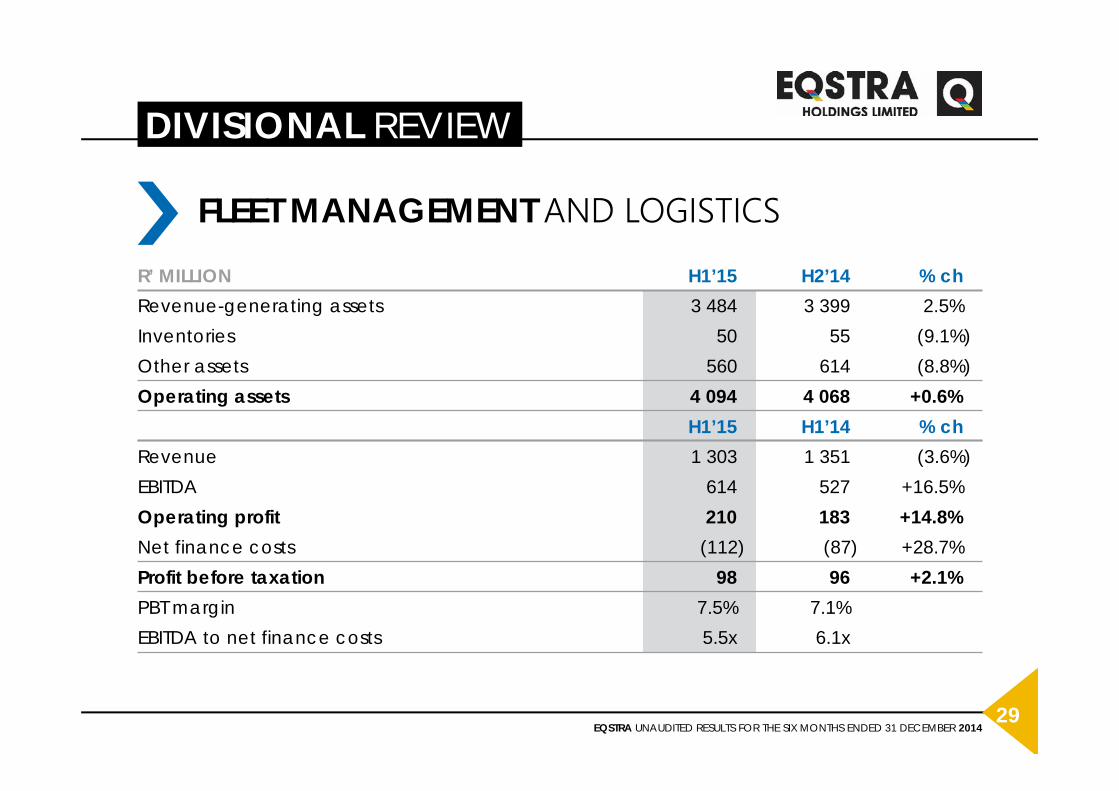

DIVISIONAL REVIEW

FLEET MANAGEMENT AND LOGISTICSR’ MILLION H1’15 H2’14 % chRevenue-generating assets 3 484 3 399 2.5%Inventories 50 55 (9.1%)Other assets 560 614 (8.8%)Operating assets 4 094 4 068 +0.6%

H1’15 H1’14 % chRevenue 1 303 1 351 (3.6%)EBITDA 614 527 +16.5%Operating profit 210 183 +14.8%Net finance costs (112) (87) +28.7%Profit before taxation 98 96 +2.1%PBT margin 7.5% 7.1%EBITDA to net finance costs 5.5x 6.1x

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201430

DIVISIONAL REVIEW

FLEET MANAGEMENT AND LOGISTICS

56%25%

9%

10%Fleet Management -passenger vehiclesFleet Management -commercial vehiclesLogistics

Fleet Management -Rest of Africa

45%

30%

17%

8%

Divisional revenue by segment H1’15 (R1 303 million)

Divisional revenue by segment H1’14 (R1 351 million)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201431

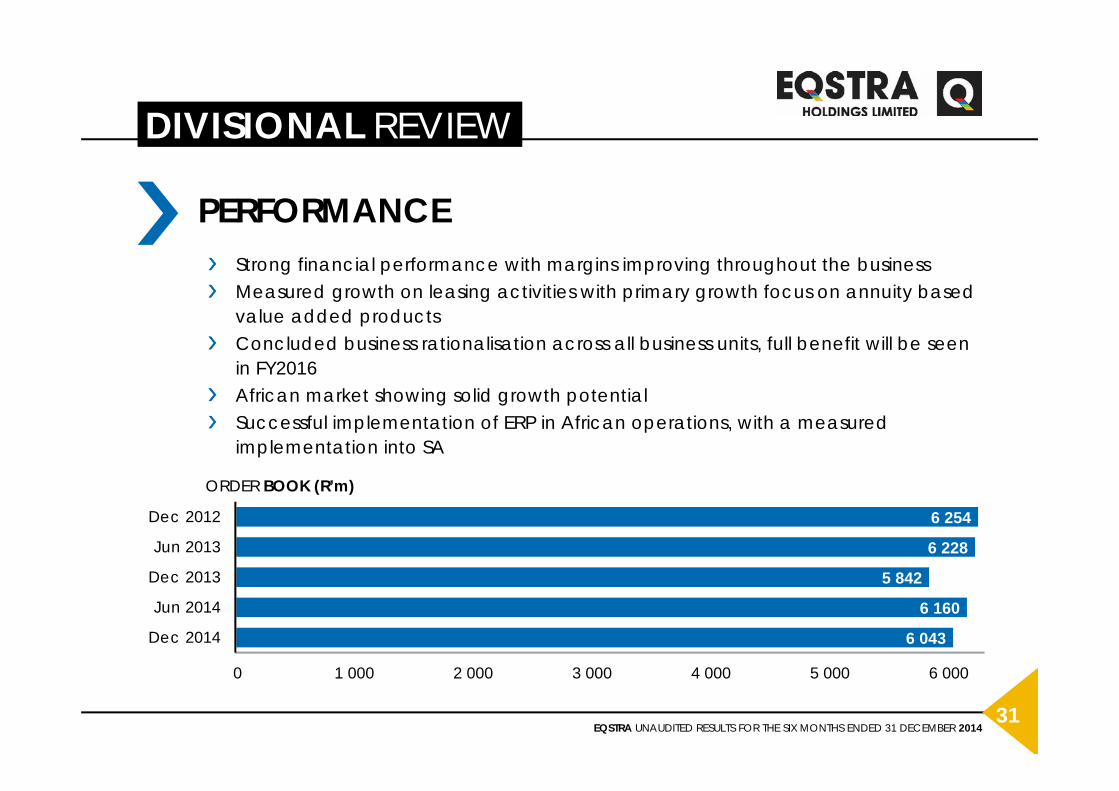

DIVISIONAL REVIEW

Strong financial performance with margins improving throughout the businessMeasured growth on leasing activities with primary growth focus on annuity based value added products Concluded business rationalisation across all business units, full benefit will be seen in FY2016 African market showing solid growth potentialSuccessful implementation of ERP in African operations, with a measured implementation into SA

PERFORMANCE

6 043

6 160

5 842

6 228

6 254

0 1 000 2 000 3 000 4 000 5 000 6 000

Dec 2014

Jun 2014

Dec 2013

Jun 2013

Dec 2012

ORDER BOOK (R’m)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201432

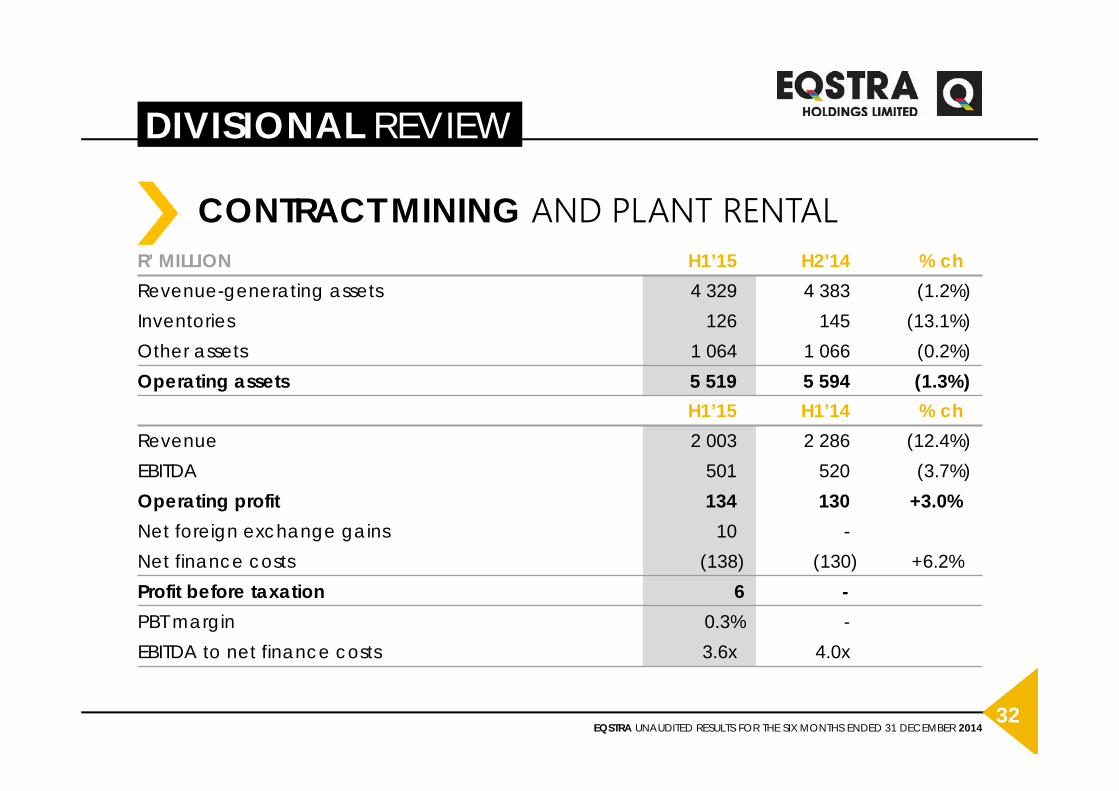

DIVISIONAL REVIEW

CONTRACT MINING AND PLANT RENTALR’ MILLION H1’15 H2’14 % chRevenue-generating assets 4 329 4 383 (1.2%)Inventories 126 145 (13.1%)Other assets 1 064 1 066 (0.2%)Operating assets 5 519 5 594 (1.3%)

H1’15 H1’14 % chRevenue 2 003 2 286 (12.4%)EBITDA 501 520 (3.7%)Operating profit 134 130 +3.0%Net foreign exchange gains 10 -Net finance costs (138) (130) +6.2%Profit before taxation 6 -PBT margin 0.3% -EBITDA to net finance costs 3.6x 4.0x

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201433

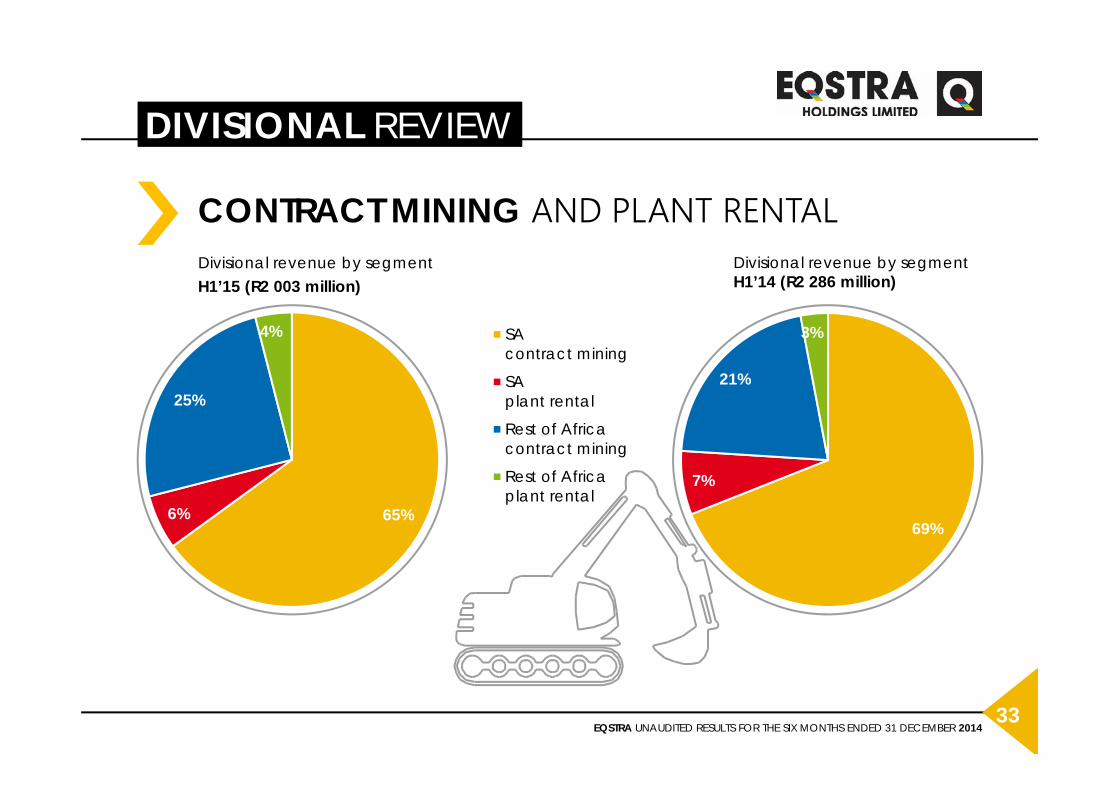

DIVISIONAL REVIEW

CONTRACT MINING AND PLANT RENTAL

65%6%

25%

4% SAcontract mining

SAplant rental

Rest of Africacontract mining

Rest of Africaplant rental

Divisional revenue by segmentH1’15 (R2 003 million)

69%

7%

21%

3%

Divisional revenue by segmentH1’14 (R2 286 million)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201434

DIVISIONAL REVIEW

New contracts commenced: Aganang (limestone), Karowe (diamonds) and Rockwell (diamonds)

Right sizing of business resulted in R15 million retrenchment and closure costs

Tharisa Minerals contract restructured toonly waste removal and finalising a further5 year extension

Closure of Nkomati finalised

CONTRACT MINING AND PLANT RENTAL

41%

36%

24%

25%

35%

63%

84%

43%

38%

45%

49%

37%

19%

16%

26%

31%

26%

28%

18%

16%

1H15

FY14

FY13

FY12

FY11

FY10

FY09

PGMs Energy Other & plant rental

COMMODITY DIVERSIFICATION

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201435

DIVISIONAL REVIEW

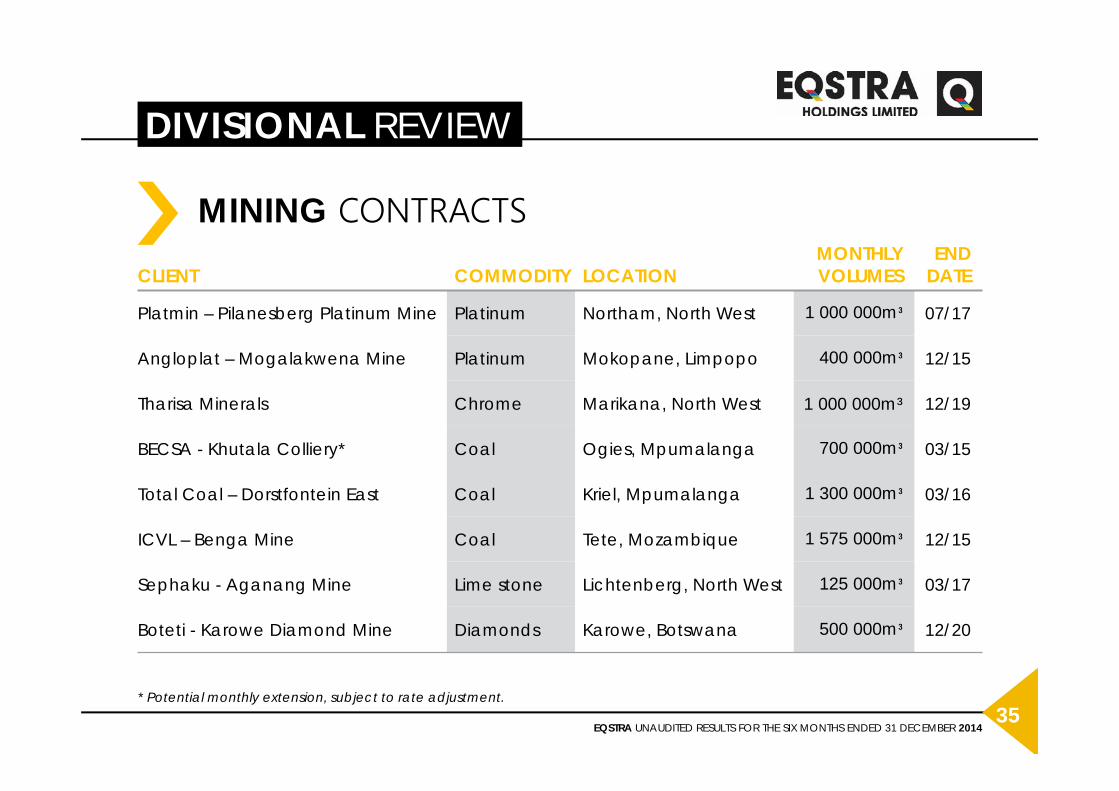

* Potential monthly extension, subject to rate adjustment.

MINING CONTRACTSCLIENT COMMODITY LOCATION

MONTHLY VOLUMES

END DATE

Platmin – Pilanesberg Platinum Mine Platinum Northam, North West 1 000 000m³ 07/17

Angloplat – Mogalakwena Mine Platinum Mokopane, Limpopo 400 000m³ 12/15

Tharisa Minerals Chrome Marikana, North West 1 000 000m³ 12/19

BECSA - Khutala Colliery* Coal Ogies, Mpumalanga 700 000m³ 03/15

Total Coal – Dorstfontein East Coal Kriel, Mpumalanga 1 300 000m³ 03/16

ICVL – Benga Mine Coal Tete, Mozambique 1 575 000m³ 12/15

Sephaku - Aganang Mine Lime stone Lichtenberg, North West 125 000m³ 03/17

Boteti - Karowe Diamond Mine Diamonds Karowe, Botswana 500 000m³ 12/20

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201436

DIVISIONAL REVIEW

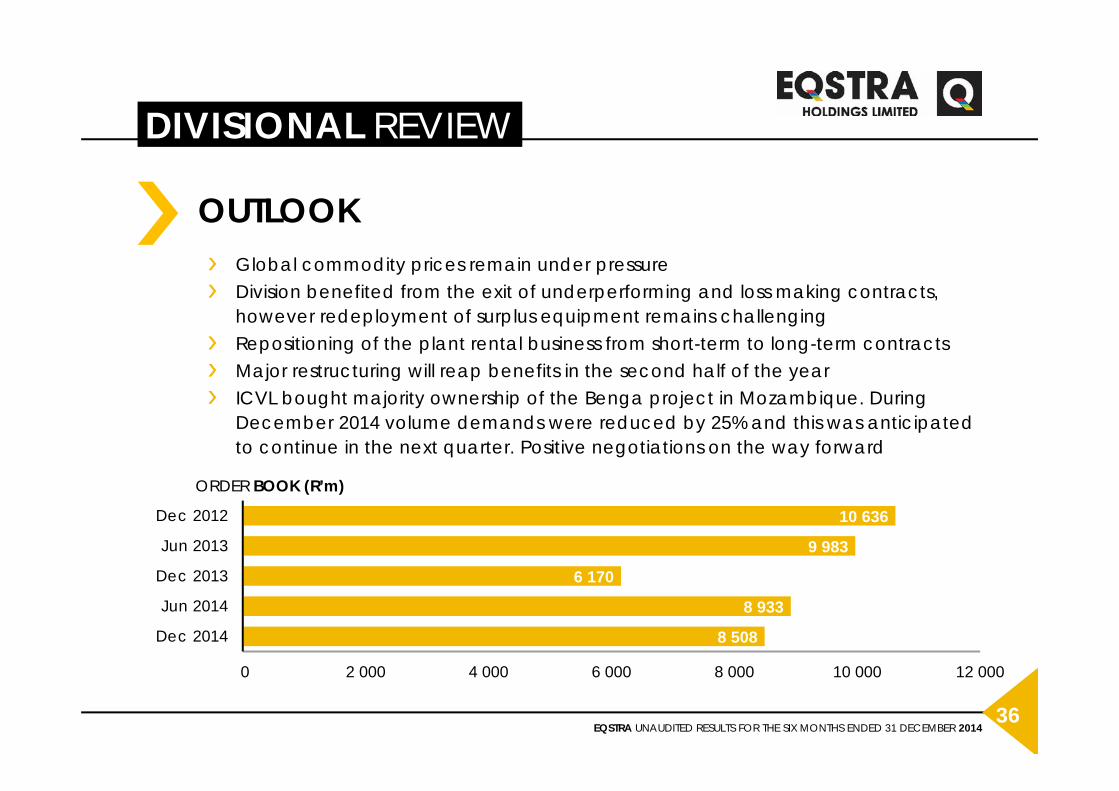

Global commodity prices remain under pressureDivision benefited from the exit of underperforming and loss making contracts, however redeployment of surplus equipment remains challengingRepositioning of the plant rental business from short-term to long-term contractsMajor restructuring will reap benefits in the second half of the yearICVL bought majority ownership of the Benga project in Mozambique. During December 2014 volume demands were reduced by 25% and this was anticipated to continue in the next quarter. Positive negotiations on the way forward

OUTLOOK

8 508

8 933

6 170

9 983

10 636

0 2 000 4 000 6 000 8 000 10 000 12 000

Dec 2014

Jun 2014

Dec 2013

Jun 2013

Dec 2012

ORDER BOOK (R’m)

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201437

GROUP REVIEW

Focus on liquidity improvement› Roll maturing bank debt› Secure additional funding from Coface and JBIC

Increase and maintain group capital adequacy ratioto a minimum of 25%

Curtail capital expansion at all divisions

Match maintenance spend to cash flows

Redeploy excess standing equipment

Focus on migrating short term rental contract to longer term lease contracts

Conclude the way forward with ICVL in Mozambique

MANAGEMENT FOCUS FOR THE NEXT 12 MONTHS

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201438

Industrial Equipment anticipates the SA forklift market to remain challenging with the UK market increasing marginally. Our aim to further balance the product portfolio and grow into sub-Sahara Africa and the UK, with a much stronger basket of products in place. A healthy order book for long-term rental and cash sales is in place to support annuity revenue growth.

Fleet Management and Logistics earnings from leasing activities are set to remain defensive however the ongoing low interest rates will continue to have a negative impact on earnings. We aim to drive value add products with measured expansion on leasing activities until the liquidity outlook improves.

Contract Mining and Plant Rental remains an important part of the asset mix of the group. The re-positioning of the division has already starting to show early signs of recovery under new management. The exit of underperforming contracts and improvement of asset utilisation positions the division adequately through the commodity cycle. Management continues to reduce the exposure to contract mining not exceeding 30% of the group’s revenue-generating assets. We continue to actively participate in the South Africa tender activities, but redeploying surplus assets could however be challenging.

DIVISIONAL REVIEW

OUTLOOK

EQSTRA UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 31 DECEMBER 201439

39QUESTIONS