Embed Size (px)

Citation preview

Research www.rics.org

Corporate Professional Local

Understanding construction consortia:theory, practice and opinions

RICS Research paper seriesVolume 6, Number 1 March 2006

Stephen Gruneberg and Will HughesUniversity of Reading

Stephen Gruneberg, BSc, MSc, PhD, FRSAis a research fellow in the School of ConstructionManagement and Engineering at the University of Reading. He is an economist specialising in theconstruction industry and is an experienced lecturer. He has written and co-written a number of books on the economic theory of construction. His recent research has covered productivity in construction,training, and the relationship between planning data and construction demand.

Will Hughes, MCIOB, BSc, PhD is a Reader in Construction Management and Economics and Headof the School of Construction Management andEngineering, University of Reading, having started hiscareer as a joiner in the West Midlands. His PhD was on organisational analysis of building projects and hehas researched and published extensively in this topic.His current research interests are in the costs of thecommercial processes in construction and contractingbased upon paying for the performance of a building,rather than for what it is made of. He is editor of the international refereed journal ConstructionManagement and Economics, and is an active memberof the Association of Researchers in ConstructionManagement, having completed two years as chairman(1998-2000), and remains responsible for developing and maintaining their information resources forresearchers in this field.

Understanding constructionconsortia: theory, practiceand opinions

Volume 6, Number 1March 2006

Stephen Gruneberg and Will Hughes,University of Reading

© RICS

March 2006ISSN 1464-648XISBN 1842 192 485

Published by:

RICS12 Great George StreetLondon SW1P 3ADUnited Kingdom

The views expressed by theauthor(s) are not necessarily thoseof the RICS nor any bodyconnected with it. Neither theauthor(s), nor the RICS accept anyliability arising from the use of thispublication.

This paper can be copied free ofcharge for teaching and researchpurposes, provided that:

• the permission of the RICS issought in advance

• the copies are not subsequentlyresold

• the RICS is acknowledged

Malcolm BellLeeds Metropolitan UniversityEngland

Alistair BlythUniversity of WestminsterEngland

Thomas BohnUniversity of LeipzigGermany

Paul BowenUniversity of Cape TownSouth Africa

Terry BoydQueensland University ofTechnologyAustralia

S E CheungCity University of Hong KongHong Kong

Chris CloeteUniversity of PretoriaSouth Africa

Charles CowapHarper Adams University CollegeEngland

Hoffie CruywagenAssociation of Quantity Surveyors inSouth AfricaSouth Africa

Christopher FortuneHeriot-Watt UniversityScotland

Karen GiblerGeorgia State UniversityUnited States of America

Andy HamiltonUniversity of SalfordEngland

John HenneberryUniversity of SheffieldEngland

Michael HoxleyAnglia Ruskin UniversityEngland

Will HughesUniversity of ReadingEngland

Eddie HuiHong Kong Polytechnic UniversityHong Kong

Norman HutchisonUniversity of AberdeenScotland

Aims and scope of the RICSResearch Paper Series

The aim of the RICS ResearchPaper Series is to provide an outletfor the results of research relevantto the surveying profession. Papersrange from fundamental researchwork through to innovative practicalapplications of new and interestingideas. Papers combine academicrigour with an emphasis on theimplications in practice of thematerial presented. The Series ispresented in a readable and lucidstyle which stimulates the interestof all the members of the surveyingprofession.

Managing editor

Stephen BrownHead of ResearchRICS12 Great George StreetLondon SW1P 3ADUnited [email protected]

Tel: +44 (0)20 7334 3725

Editorial board

Adarkwah AntwiUniversity of WolverhamptonEngland

Tim DixonOxford Brookes UniversityEngland

Les RuddockUniversity of SalfordEngland

Clive WarrrenUniversity of QueenslandAustralia

Christine WhiteheadLondon School of EconomicsEngland

Panel of refeees

Akintola AkintoyaGlasgow Caledonian UniversityScotland

Ghassan AouadUniversity of SalfordEngland

David BaldryUniversity of SalfordEngland

Ramin KeivaniOxford Brookes UniversityEngland

Andrew KnightNottingham Trent UniversityEngland

Richard LaingRobert Gordon’s UniversityScotland

S M LoCity University of Hong KongHong Kong

David LoweUniversity of ManchesterEngland

William McCluskeyUniversity of UlsterNorthern Ireland

John MansfieldNottingham Trent UniversityEngland

Jacob OpadeyiUniversity of the West IndiesTrinidad and Tobago

Rob PickardUniversity of NorthumbriaEngland

David ProverbsUniversity of WolverhamptonEngland

Rainer SchultzUniversity of AberdeenScotland

Martin SextonUniversity of SalfordEngland

Low Sui PhengNational University of SingaporeSingapore

Francois VirulyUniversity of WitwatersrandSouth Africa

Peter WyattUniversity of the West of EnglandEngland

Contents

1 Introduction 5

2 Construction consortia in general 10

3 Results from the interviews 23

4 Contrasting views of consortia 35

5 Conclusions 47

Acknowledgements 49

References 50

Appendix A: Interview questions 52

RICS research paper series 54

Understanding construction consortia:theory, practice and opinions

Stephen Gruneberg and Will Hughes (University of Reading, UK)

Abstract

Firms form consortia in order to win contracts. Once a project has been awarded to a consortium each member then concentrates

on his or her own contract with the client. Therefore, consortia are marketing devices, which present the impression of team-

working, but the production process is just as fragmented as under conventional procurement methods. In this way, the consortium

forms a barrier between the client and the actual construction production process.

l Firms form consortia, not as a simple development of normal ways of working, but because the circumstances for specific

projects make it a necessary vehicle. These circumstances include projects that are too large or too complex to undertake alone

or projects that require on-going services which cannot be provided by the individual firms in-house.

l It is not a preferred way of working, because participants carry extra risk in the form of liability for the actions of their partners in

the consortium.

l The behaviour of members of consortia is determined by their relative power, based on several factors, including financial

commitment and ease of replacement.

l The level of supply chain visibility to the public sector client and to the industry is reduced by the existence of a consortium

because the consortium forms an additional obstacle between the client and the firms undertaking the actual construction work.

Supply chain visibility matters to the client who otherwise loses control over the process of construction or service provision,

while remaining accountable for cost overruns. To overcome this separation there is a convincing argument in favour of adopting

the approach put forward in the Project Partnering Contract 2000 (PPC2000) Agreement.

l Members of consortia do not necessarily go on to work in the same consortia again because members need to respond flexibly

to opportunities as and when they arise.

l Decision-making processes within consortia tend to be on an ad hoc basis.

l Construction risk is taken by the contractor and the construction supply chain but the reputational risk is carried by all the firms

associated with a consortium.

l There is a wide variation in the manner that consortia are formed, determined by the individual circumstances of each project; its

requirements, size and complexity, and the attitude of individual project leaders. However, there are a number of close working

relationships based on generic models of consortia-like arrangements for the purpose of building production, such as the

Housing Corporation Guidance Notes and the PPC2000.

Contact

Stephen Gruneberg Will HughesSchool of Construction Management and Engineering School of Construction Management and EngineeringUniversity of Reading University of ReadingPO Box 219 PO Box 219Whiteknights WhiteknightsReading RG6 6AW Reading RG6 6AWUNITED KINGDOM UNITED KINGDOM

Tel: +44 (0) 118 378 5416 Tel: +44 (0)118 378 5416Email: [email protected] Email: [email protected]

The contractual environment

onstruction consortia arise in severaldifferent forms. They are one of manyways in which traditionally separate

parts of the construction procurement processmight be integrated. Sometimes, thisintegration involves a single firm taking onobligations wider than it is capable ofundertaking alone, and then subcontractingelements of the work; at other times, groups offirms get together to act as a consortium tomeet the needs of a client.

An example of such arrangements, which mayinvolve a number of firms with different areasof expertise, is design-build-finance-operate(DBFO). DBFO essentially provides acomplete private sector service (or theservices of a building), which the public sectoragrees to purchase over an extended period.In DBFO projects the commercial risk isnominally taken by the private sector operator.The public sector client only undertakes topurchase the output over a given period. Atthe end of the contract, the assets remain withthe operator. Similar arrangements mayinvolve the transfer of the built assets to thepublic sector client at the end of an agreedperiod, such as build-own-operate-transfer(BOOT), which has long been used to realisemajor construction projects, especially in lessdeveloped countries.

Public sector procurement andthe construction sectorConstruction procurement by the public sectorhas long been seen as a problematic. A recentreport (Office of the Deputy Prime Minister2003: 12) expressed concern over traditional

approaches to procurement by localauthorities. According to the Office of theDeputy Prime Minister (ODPM), the traditionalinterface between clients and contractors andthe management of contracts often causedproblems, which constrained innovation andinhibited the use of external suppliers. For highvalue and high risk projects, the ODPM (2003:p18) suggested that local government mightadopt partnering as an alternative approach.

Firms often form consortia to provide largeand complex public sector projects. Theseappear to be relatively efficient and effective.Hence, once a public sector client has decidedthat a major project is needed, it will oftenengage a consortium with sufficient financialbacking and technical expertise in constructionto carry out the work.

It seems reasonable to assume that, by using aconsortium, a team could be employed whichwould work together to solve problems, reducecosts and lower risks. At the same time,quality issues could be addressed; all thiscould be achieved in a shorter period than withtraditional procurement methods. Moreover,not only could the consortium carry out thebuilding work, the same arrangement could beused to deliver services, including facilitiesmanagement, after the construction phase.One of the purposes of this report is to testthe validity of such aspirations, and the extentto which they are matched in practice.

Government has encouraged constructionfirms to work in teams and has involved privatesector finance in the funding process throughits Private Finance Initiative (PFI). In responseto this approach, Special Purpose Vehicles

1 Introduction

RICS Research l 5www.rics.org/research

Understanding construction consortia: theory, practice and opinions

cc

(SPVs) are set up to structure the deliveryonce a contract has been agreed. But beforea contract can be agreed, informal consortiamay be formed, combining banking, propertyand construction companies. Only when oneof these informal consortia wins a bid is anSPV formally established. Several methods ofpublic procurement have emerged under theumbrella of PFI, including Prime Contractingfor MoD projects, Procure 21 for NHS projectsand Framework Agreements for schools andother types of building.

These initiatives usually involve structures thatpenetrate the supply chain. In PrimeContracting there are clusters of firmssupplying the cluster group leader or PrimeContractor. Each of the clusters has clustersof other firms supplying the specialist firms.Under Procure 21, Primary Supply ChainPartnerships (PSCPs) have been set up.These PSCPs are construction consortia,which have pre-qualified for NHS projects.There are only 12 PSCPs for the whole ofEngland. However, in a case study of Procure21 carried out by Proverbs and Riley (2003),caution was expressed. Proverbs and Rileyfound little awareness among NHS Trust staffof the supply chain companies and althoughNHS Estates advertised Procure 21 widely,individual members of staff were not generallyprepared for the new system of procurementwhen it was launched.

Framework Agreements are deemed to becontracts in order to comply with EU directives.The framework sets up arrangements forsuppliers to work together over a period, orover a number of building projects. Theseagreements enable firms to undertake a seriesof smaller projects, such as school building, on

6 l RICS Research

In construction there has always been co-operationand a problem solving ethos; otherwise buildngscould never have been built.

behalf of the same client body or localauthority.

The use of consortia in construction does notnecessarily mean that construction firms couldnot work together outside consortia. Inconstruction there has always been co-operation and a problem-solving ethos;otherwise buildings could never have beenbuilt. Indeed, as reported below, oneinterviewee argued that, in view of thistraditional method of firms working together, itwould be difficult to find any advantages insetting up consortia in construction: in anycase, the incentives in consortia are in all thewrong places. For example, one of the majorcontradictions facing construction firmsworking in consortia with long-termundertakings is that building contractors, andeven many property developers, only have ashort-term interest in any project, up to theend of the construction phase, and then theysell it on.

Nevertheless, the management of risk may beone factor leading to the formation ofconsortia. In construction projects it is alwayspossible to find someone else to blame. Itmight be argued that one of the main reasonsfor the formation of a consortium is because itis not possible to parcel up risks. Themembers of a consortium are forced into theposition of trusting others to make commercialdecisions on their behalf, which they are goingto be held to, because in principle, though notnecessarily, they are all jointly and severallyliable. In practice, ultimately, the client orindividual parties carry the risks at present.For this reason consultancy firms and otherscarry professional indemnity insurance.

Issues and questionsThe Office of the Deputy Prime Minister(2003: p24) identified a number of methods ofprocurement of particular relevance to localgovernment, including potential partnershipmodels, that required further study andresearch. Partnership models are examples ofconsortia in construction. The questions raisedin this discussion concern the formation,composition and operation of consortia inconstruction. Are construction consortiaindeed effective and efficient or are theypurely marketing devices adding little value tothe process? This study examines questionsabout the working of consortia in public sectorprojects. The main objectives of the researchare to:

l examine the formation of consortia in theconstruction industry,

l examine the roles and relationships of themembers of consortia,

l understand the motives and strategies offirms in construction consortia,

l examine the working practices of firms inconsortia,

l examine the manner in which consortia areused to mobilise productive resources,

l examine risk and sources of conflict in construction consortia, and

l consider the operational differencesbetween integrated supply teams andconsortia.

RICS Research l 7www.rics.org/research

Understanding construction consortia: theory, practice and opinions

This study focuses on those situations inwhich several firms combine to provide abuilding or structure as a complete contract, oras part of a contract to provide services togovernment acting as client on behalf of thepublic. This would include those projectsinvolving construction either financed throughtraditional public sector funding means orthrough PFI.

The public sector work undertaken by theconstruction industry shares many of theeconomic characteristics of the constructionindustry in general. Hillebrandt (1984) pointsout that the construction sector has manyeconomic features, which it shares with otherindustries but in combination, distinguish itfrom them. Raftery (1991) points out thebulkiness and low value-to-weight ratio ofmaterials, the high labour content of output,the low levels of fixed costs and the high levelof subcontracting in construction. Gruneberg(2000) highlights the size of constructionprojects relative to the turnover of contractors.Each project is therefore an opportunity togenerate profits but is also a threat to the

survival of the firm if problems emerge. Ifproblems emerge, such as cost overruns,delays, technical difficulties, and late payment,losses on any one project can be greater thanthe profits of a firm’s other projects and itscapital assets. These characteristics oftenform barriers to building efficiently andeffectively both in the public and privatesectors. Several public sector projects(Portcullis House and the British Library arebut two examples of some of the largerprojects) have encountered management andfunding difficulties. These characteristics areoften the main reason for cost over-runs andbuilding delays especially in the public sector.There is no reason why they cannot bemanaged, but as yet they have often appearedto involve intractable difficulties.

One feature of the building production processof particular relevance to public sectorconstruction procurement is that largeconstruction projects are usually carried out bya number of construction firms, often as manyas 30-40 specialists, and sometimes morethan 70. Moreover, the size of projects often

8 l RICS Research

requires a number of firms to contribute riskcapital and arrange debt financing. It is theseequity-contributing firms that are seen as thebuilding consortium, but constructioncontractors usually remain outside the realconsortium, being members of the consortiumin name only, for marketing purposes.

Banks and property developers with jointcontractual financial arrangements mayparticipate in the management and productionof projects by being partners in a constructionconsortium. But they are only part of themanagement and production of projects. Theactual building production is undertaken by asupply chain of a number of firms. Theconsortium forms a buffer between the publicsector clients and the technology andresources used in the process. In consideringthe formation, nature and behaviour ofcollaboration, and the risks associated withjoint ventures in construction, our approach isto examine consortia in the context of theirbuilding projects as a whole.

Research methodThe method of study in this report is based ona literature review reinforced with interviewswith a number of leading practitioners.Interviews with selected practitioners from thedemand side and the supply side of consortiahave enabled us to develop clear explanationsand answers to the research questions. Theinterviewees represent a public sector client, adeveloper, a bank, a financial consultancy, anindependent project manager, a constructionindustry consultant, two main contractors, aspecialist subcontractor and a legal advisor.The size of firms approached ranged fromsmall consultancies to relatively large firms,

such as Bovis Lend Lease, Symonds andEMCOR Drake and Scull. However, theresponses of only one main contractor,randomly selected from those interviewed, areused in the tables to maintain a balance. Theviews expressed do not necessarily reflect theviews of the firms and named organisations.

It is important to state that the intervieweeswere not randomly selected and are notnecessarily representative of the industry as awhole or even their particular specialisms.However their views on consortia inconstruction were not known before theinterviews took place. The interviews should beseen as indicative of some opinions held in theindustry concerning consortia. Far moreinterviews would of course be needed to findstatistically significant results.

The interviews were divided into an opendiscussion of construction consortia and aseries of specific questions designed tohighlight particular issues. The questionscovered two areas of interest; first, the settingup and operation of consortia and second, themanagement of risk and decision-making.

Eight full interviews were conducted, along thelines indicated in Appendix A. In addition, twofurther interviews were carried out for thepurposes of dealing with some specificoutstanding issues. While these additionalinterviews are reported in the next section,they are not included in the systematic, tabularanalysis shown in this section.

RICS Research l 9www.rics.org/research

Understanding construction consortia: theory, practice and opinions

Terminology and definitionsSeveral longer-term or strategic relationshipswithin the construction industry have emergedin the last few years, including consortia, jointventures, partnering, special purpose vehicles,strategic alliances and supply chainmanagement. They are all examples ofconstruction and property syndicates.Unfortunately the terms are often used looselyor interchangeably by practitioners and thisleads to confusion over the definition of theterms in practice. Fortunately, the businesscontext invariably makes the meaning clear.Nevertheless, it may be useful to proposesome operational definitions for these terms inthis report.

In this paper a consortium is defined as anarrangement between several firms, in whicheach firm contributes an equity stake in theform of risk capital or payment in kind in orderto qualify as a member. Remuneration ofconsortium members may be calculated as ashare of the net profits of the consortium.

A joint venture is characterised by a numberof firms collaborating on a project, or a numberof distinct projects, with a view to sharing theprofits, each firm being paid on the basis of itsagreed contribution in kind or in financialterms.

A partnering agreement involves a number offirms, usually including the client, working co-operatively to achieve a given output over oneor a number of projects. Remuneration isusually based on contract terms andcontribution to the work.

A special purpose vehicle (SPV) is aformal accounting and contractualarrangement set up by one or more firms toundertake a project or a series of projectsseparate from the accounts of the firm(s)comprising the special purpose vehicle. Thus,not all SPVs are consortia. However, consortiainvariably set up SPVs after being selected tocarry out specific work, and the members ofthe consortium become shareholders of theSPV.

The distinctions between consortia, jointventures and partnering arrangements are,however, not as clear in practice wherevariants and ad hoc arrangements necessarilyblur and confuse the boundaries of the termsbecause of the need to tailor relationships inresponse to the needs of each project.Moreover, different interviewees interpretedthe terms differently, often depending on theirrole in the property and development process.

Furthermore, not all construction firms workingclosely together are necessarily workingtogether using any of the above arrangements.Strategic alliances are formed by firms whoseek to work together on an on-going basis asand when the members of the alliance winwork from different clients, provided thespecialist skills are required. Another exampleof closer working relationships between firmsin the construction industry appeared in abriefing paper to the members of theSpecialist Engineering Contractors’ Group(2003). According to this briefing paper, Egan(1998) suggested that the Defence Estates,NHS Estates, the Highways Agency and otherpublic sector building procurers shouldencourage the industry to form integrated

2 Construction consortia in general

10 l RICS Research

project teams (IPT), which are not consortia.IPTs should consist of all those involved withthe design, manufacture, assembly, installation,operation and maintenance of the building.These IPTs are thus intended to work closelywith the client over the whole process with aview to achieving the customer’s businessobjectives. The SEC Group favour theselection of IPTs based on best value ratherthan lowest price. This is seen as providingparticipating firms with opportunities to providecost-effective solutions, enhance their ownprofit margins and secure greater continuity ofwork.

The Egan Report does not mention IPTs, assuch, but does discuss integrating the(construction) process and the team aroundthe product, (Egan 1998: 16). This integrationdoes not necessarily imply the formation ofnew entities, such as consortia, to undertakethe work but does imply the need for greaterco-operation and understanding. Supply chainmanagement is one response, which seeks toreinforce the continuum of relationshipsformed by working on a project throughgreater communication and understandingbetween all the parties involved, extendingupstream to include building componentsuppliers, where necessary.

Types of consortiaAlthough some construction consortia mayappear to include contractors, many PFI bidsare assembled by developers and financiers,only using a contractor to present a technicalinput to the client. In practice, the constructioncontractors are kept at arm’s length and arenot full participating members of theconsortium. There is no one form that defines

construction consortia. On the contrary thereare several types of consortia: developer-financial consortia, developer-financial-contractor consortia, client-developer consortiaand single-type-organisation consortia. Someare involved in the essential commercial risk-taking of projects while others are involved inthe building production process and somecombine commercial risk, construction andservice provision. Variants of the consortiumconcept also depend on the relative size, skillsand financial inputs of the various partiesneeded to meet the specific demands of eachproject, building or service requirement.

It is not always possible to distinguish ex antethe type of consortium adopted in any givenproject, especially where contractors areinvolved at an early stage. Contractors areoften used at an early stage to demonstratethe existence of a team, but at this stage thecontractor may have made very littlecommitment to the consortium. According toone contractor interviewed for this study, themembership of consortia can change betweenthe initial presentation and the actual work onsite. Much depends on the workingrelationships between the actual peopleforming the consortium.

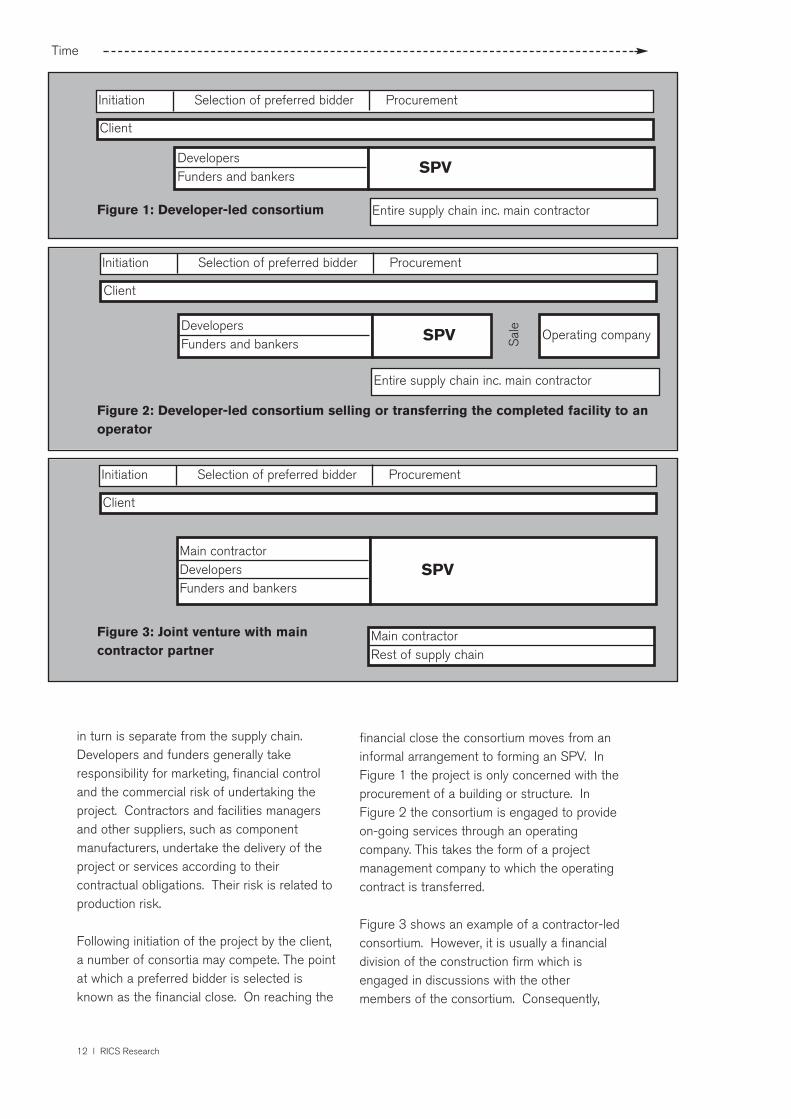

Figures 1 to 3 show the relationships ofdifferent parties, where private sector financeis involved, during three distinct phasesbeginning with the initiation of the project, theselection process and ending with theprocurement of the building and services.Figure 1 shows a developer-led consortiumcomprising a developer and a funder. Theclient is involved throughout the process butremains separate from the consortium, which

RICS Research l 11www.rics.org/research

Understanding construction consortia: theory, practice and opinions

in turn is separate from the supply chain.Developers and funders generally takeresponsibility for marketing, financial controland the commercial risk of undertaking theproject. Contractors and facilities managersand other suppliers, such as componentmanufacturers, undertake the delivery of theproject or services according to theircontractual obligations. Their risk is related toproduction risk.

Following initiation of the project by the client,a number of consortia may compete. The pointat which a preferred bidder is selected isknown as the financial close. On reaching the

financial close the consortium moves from aninformal arrangement to forming an SPV. InFigure 1 the project is only concerned with theprocurement of a building or structure. InFigure 2 the consortium is engaged to provideon-going services through an operatingcompany. This takes the form of a projectmanagement company to which the operatingcontract is transferred.

Figure 3 shows an example of a contractor-ledconsortium. However, it is usually a financialdivision of the construction firm which isengaged in discussions with the othermembers of the consortium. Consequently,

12 l RICS Research

Client

Initiation Selection of preferred bidder Procurement

Client

Initiation Selection of preferred bidder Procurement

Client

Initiation Selection of preferred bidder Procurement

DevelopersFunders and bankers

SPV

DevelopersFunders and bankers

SPV Operating companySal

e

Main contractorDevelopersFunders and bankers

SPV

Main contractorRest of supply chain

Figure 1: Developer-led consortium

Figure 2: Developer-led consortium selling or transferring the completed facility to anoperator

Figure 3: Joint venture with maincontractor partner

Entire supply chain inc. main contractor

Entire supply chain inc. main contractor

Time

the bid vehicle comprises the contractor’sfinancial division, funders, the developer andthe main contractor. After financial close(when a bidder is selected) the SPV is formedand the main contractor becomes both amember of the SPV and a separate member ofthe supply chain. As the main contractor ispart of the joint venture, part of the supplychain is included in the SPV, but not all. Thecontractor may be a shareholder of the SPVbut is also one of its suppliers.

Figures 1 to 3 illustrate the barrier formed byconstruction consortia, because the entiresupply chain is separated from the clientmaking it difficult for contractors and clients tocommunicate. This is dealt with in greaterdetail below.

Relationships between firms inconsortiaApart from the very smallest of jobs,construction projects invariably involve anumber of firms, each providing specialistknowledge and skills. In their advice to localauthorities the Office of the Deputy PrimeMinister (2003) recommend a number ofprocurement routes or delivery models toorganise the construction process, includingpartnering. Partnering models include publicsector consortia, PFI and other forms of DBFOcontracts, partnering contracts, joint venturecompanies and framework agreements(incremental partnering). This proliferation ofterms leads to confusion but it is clear thatevery construction project requires a relativelylarge number of firms to collaborate in oneway or another in order to organise the supplychain.

In their paper discussing a survey of supplychains, Akintoye, McIntosh, and Fitzgerald(2000) point out that although they foundimprovements in planning and purchasing, anumber of barriers remained which inhibitedcollaborative working. They found a hostileculture in the industry, a lack of commitment tosupply chain management (SCM) amongstsenior managers in the top constructioncontractors they interviewed andorganisational structures which failed toencourage collaboration. They also felt therewas a general lack of knowledge andunderstanding of SCM. If SCM is taken asone form of consortium in construction, inwhich the contractors and suppliers co-operate closely, it is clear that the managers offirms have a first loyalty to their owncompanies rather than the SPV or the otherfirms in the supply chain. We consider thisaspect of the behaviour of firms can best beexplained in terms of game theory, which isdiscussed below.

Consequently, we believe consortia do notnecessarily lead to vertically integratedprocesses in construction but simply addanother layer of contractual arrangements.However, a greater degree of co-operationbetween main and specialist contractorswould, according to Egan (1998), also reducethe adversarial nature of the process.However, in practice the underlyingrelationships seem to have remainedessentially unchanged.

Nevertheless, it might be argued thatintegrated teams might reduce duplication ofeffort through improvements in communicationbetween the various parties, but at a cost and

RICS Research l 13www.rics.org/research

Understanding construction consortia: theory, practice and opinions

this cost may be high, if firms take advantageof preferences offered by being a member ofthe integrated team. It is the consortiumnature of construction, according to Pearce(2003: 23), which creates major difficultiesbetween the various participants in thebuilding process and adds to the transactioncosts of delivering ‘consistent work patternsand effective communication’.

These difficulties may also vary depending onthe extent to which a consortium is an equityalliance, with consortium members sharingfinancial risk or a non-equity alliance. In a non-equity alliance the firms simply collaborateclosely on a contract as in a supply chain orpartnering arrangement. One area of difficultyis trust between the participants. Langfield-Smith (2005) examines trust within alliances

or consortia. According to Langfield-Smith,where there is a high level of uncertainty,control is more easily achieved if firms haveequity at risk or have invested in theconsortium. Langfield-Smith uses transactioncost theory and concepts of trust to describegoodwill trust and competence trust in thecontext of construction consortia. Againtransaction costs are discussed in more detailbelow.

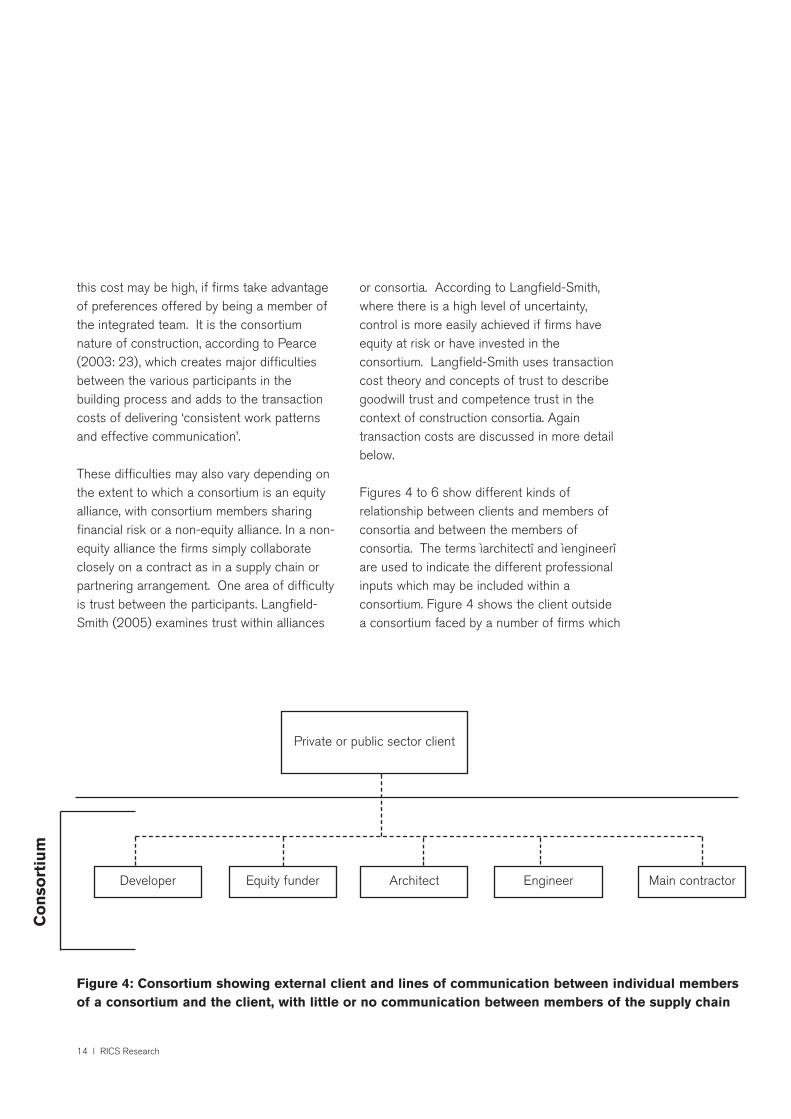

Figures 4 to 6 show different kinds ofrelationship between clients and members ofconsortia and between the members ofconsortia. The terms ìarchitectî and ìengineerîare used to indicate the different professionalinputs which may be included within aconsortium. Figure 4 shows the client outsidea consortium faced by a number of firms which

14 l RICS Research

Private or public sector client

Developer Equity funder Architect Engineer Main contractor

Co

nso

rtiu

m

Figure 4: Consortium showing external client and lines of communication between individual membersof a consortium and the client, with little or no communication between members of the supply chain

combine to negotiate with the client but do notnecessarily have close working relations withthe other members of the consortium.Nevertheless the consortium presents aunified approach to the client in order to winthe tender process although the arrangementsbetween the consortium members remaininformal until financial close.

In partnering arrangements, the firms agree inprinciple to form a partnering arrangement atthe pre-tender stage. If the consortium issuccessful, the bidders are joined by the client.Figure 5 illustrates the assumption that allparties to the project, ranging from the clientto specialist contractors, are able tocommunicate freely. Only a relatively fewunimportant contractors may remain outsidethe partnering arrangement. This specific

arrangement appears to model the socialhousing sector where Housing Associationswork with private sector developers andcontractors to build social housing and housesfor sale. This also appears to be the modelassumed in the PPC2000: Project PartneringContract (Mosey 2000) .

PPC2000 requires the active involvement ofthe client with full and open communicationbetween all parties. As shown in Figure 5,lines of communication are seen to existbetween all members of the partneringagreement and especially between themembers of the supply chain and the client.However, this mode of working is not commonin projects for public sector clients. Moregenerally, in recent consortia which have beenestablished to serve public sector clients, the

RICS Research l 15www.rics.org/research

Understanding construction consortia: theory, practice and opinions

Public sector client

Developer Equity funder

Architect EngineerContractors in the

supply chain

Figure 5: Project Partnering Contract showing the client within the contractarrangements and lines of communication between individual members of aconsortium and the client and between members of the supply chain

Su

pp

ly c

hain

Pro

ject

Part

neri

ng

Co

ntr

act

client is not contractually part of theconsortium.

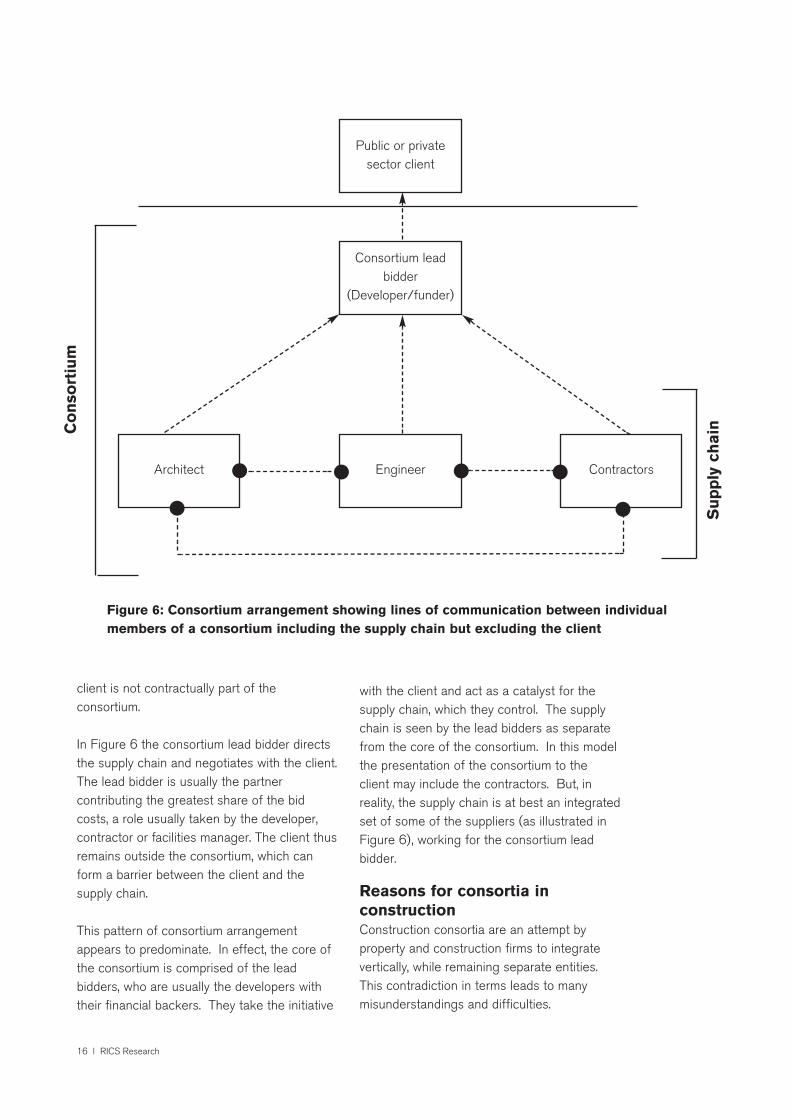

In Figure 6 the consortium lead bidder directsthe supply chain and negotiates with the client.The lead bidder is usually the partnercontributing the greatest share of the bidcosts, a role usually taken by the developer,contractor or facilities manager. The client thusremains outside the consortium, which canform a barrier between the client and thesupply chain.

This pattern of consortium arrangementappears to predominate. In effect, the core ofthe consortium is comprised of the leadbidders, who are usually the developers withtheir financial backers. They take the initiative

with the client and act as a catalyst for thesupply chain, which they control. The supplychain is seen by the lead bidders as separatefrom the core of the consortium. In this modelthe presentation of the consortium to theclient may include the contractors. But, inreality, the supply chain is at best an integratedset of some of the suppliers (as illustrated inFigure 6), working for the consortium leadbidder.

Reasons for consortia inconstructionConstruction consortia are an attempt byproperty and construction firms to integratevertically, while remaining separate entities.This contradiction in terms leads to manymisunderstandings and difficulties.

16 l RICS Research

Public or privatesector client

Consortium leadbidder

(Developer/funder)

Architect Engineer Contractors

Su

pp

ly c

hainC

on

sort

ium

Figure 6: Consortium arrangement showing lines of communication between individualmembers of a consortium including the supply chain but excluding the client

Nevertheless it is an attempt to respond tomarket pressures caused by the size andcomplexity of projects put to the industry thatrequire more than a specified building oncompletion. The continuity of responsibilityafter the construction phase, and into thebuilding-in-use phase, has led to a need ordesire to integrate the firms engaged in theprovision of the built environment.

This section deals with the reasons that firmsmay choose to work in consortia rather than asfully vertically integrated firms providing a fullconstruction and facilities management servicein-house.

Many consortia are formed in anticipation ofclient requirements or in response to pre-contract qualification criteria set by the client.There may be several reasons for the belief inthe efficacy of consortia both from the clients’point of view and from the point of view of themembers of the consortia. Indeed the Office ofthe Deputy Prime Minister (2003: p35)suggests a number of benefits to be gained bylocal authorities from partnering arrangements,defined as the ‘the creation of sustainable,collaborative relationships with suppliers in thepublic, private, social enterprise and voluntarysectors to deliver services, carry out majorprojects or acquire supplies and equipment.’Although the ODPM do not say so in theirreport, it could be argued that theseadvantages may also be applied to consortia ingeneral. According to the ODPM report, thesebenefits include better designed solutions,integration of services for customers, accessto new and scarce skills, economies of scaleand scope and investment. However, noevidence is given in support of these

assertions in the report.

Size of firms relative to projectsOne reason for the existence of consortia inconstruction is given by Pearce (2003: 23),who shows that one of the consequences ofthe predominantly small size of specialist firmsin construction is that they must co-operatewith other small firms in order to undertakerelatively large building projects. For firmsentering consortia-type arrangements theshortage of in-house expertise and the highcost of tendering can lead firms to collaborateon projects.

Risk managementA second reason for forming consortia inconstruction is implied by Hayes, et al. (1987),who discuss risk management from thecontractors’ point of view. Although Hayes etal. are not concerned with the issue ofconsortia they discuss the issue of riskmanagement, arguing that an appropriatecontract strategy involves consideration of theorganisational structure needed to control bothdesign and construction and the relationshipbetween them. The allocation of risk betweenthe various parties may not be best served bytraditional contracting arrangements inundertaking high risk complex projects. Whendifficulties arise on site or when there aremajor cost overruns it may be too late to avoidthe costs of delay, arbitration or litigation. Theyadvocate ‘active management of a risk by allparties.’ (Hayes et al. 1987: 24)

We argue that the idea of active riskmanagement should be taken further inproposing that a construction project shouldbegin with an analysis of the main objectives

RICS Research l 17www.rics.org/research

Understanding construction consortia: theory, practice and opinions

and risks in a project, followed by theidentification of roles and responsibilities, andonly then the identification of contractualterms which bind the parties in legalrelationships. This is the opposite of the moreusual practice of starting with a standard-formcontract and adapting it to suit particularcircumstances. Consortia may be viewed asorganisational structures which take risk intoaccount at the earliest stages in a projectrather than waiting for problems to arise at alater stage. They therefore signal a clear moveaway from traditional approaches to theprocurement of construction work. An evenmore direct approach to dealing with the earlyidentification of risk and design issues may beprovided by recent developments in partneringarrangements as defined by the PPC2000partnering contract which is discussed below.

The management of risk through the use ofconsortia may be viewed as an industryresponse to demand put to it by the publicsector and very large private sector clients.Demand is put to the industry in the form ofproject proposals. These projects tend to bevery large and complex. At any one timeconstruction firms hold a portfolio of discreteprojects on which they are working. Only firmsof a certain capacity can undertake work overa certain size or complexity. When theworkload exceeds that size firms have nooption but to seek partners. Otherwise theexposure to risk represented by one projectcontradicts the need to balance risk in thefirm’s portfolio of projects. In this way therelative commitment of any one firm to anyparticular project is limited. Few firms woulddevote all of their resources to one project.Nevertheless, each project still constitutes

both a source of revenue for the firm and athreat to its profitability and even its continuedsurvival.

Transaction costsA third reason for consortia in constructionconcerns the cost of transactions. Williamson(1975), Dietrich (1994), Winch (1989) andGruneberg and Ive (2000) refer to a numberof hidden expenses subsumed in thetransaction process. Transaction costs arecaused by a number of different factors, whichimpinge on decisions to buy or sell. Thesefactors include ‘bounded rationality’ whichrefers to the complexity and uncertaintyassociated with decision making. Secondly,‘information impactedness’ refers to the limitedknowledge of the parties to a transactionwhich denies them the ability to make correctpurchasing or selling decisions. Williamsonrefers to opportunism, which occurs wheneverfirms take advantage of the informationimpactedness of the co-transactor. Winch alsonotes the existence of asset specificity whichrefers to specialised plant and other capitalequipment which may only occasionally berequired in unique circumstances. The problemof costing the use of specialised plant inunusual conditions allows firms to takeadvantage of the lack of an established marketprice.

Transaction costs occur even when consortiaare engaged. One symptom of hightransaction costs associated with the ChannelTunnel project, for example, was the fact that,according to figures in The Sunday Times of 8October 1989, there were approximately 400men actually digging the tunnel and at least800 people monitoring their progress in the

18 l RICS Research

headquarters of Transmanche Link, Eurotunneland Atkins/Setec, the Maitre d'Oeuvre. Therewere also several advisors to the 200 banksfunding the project.

Nevertheless the formation of consortia maybe seen as a rational response to theeconomic and commercial environment inwhich firms operate. Production processes inconstruction are highly fragmented andspecialised. Many separate firms must cometogether in order to construct and operatebuildings. These complex relationships aredetermined by the markets for the variousservices and components needed: design,management, piling, steel erecting, cladding,facilities management and many otherspecialisms. Before a contract can be signedthe product or service must be defined andunderstood by both parties; both sides to thedeal must have confidence that the order willbe carried out and duly paid for. A consortiumis often seen as one solution for discussingand overcoming the uncertainties which mayarise and for facilitating negotiations with theclient. However, in reality the process remainsfragmented; both within consortia and throughthe supply chain. Indeed, the discussionsbetween the consortium members and theclient rarely, if ever, include members of thesupply chain.

Nevertheless, von Branconi and Loch (2004)provide a strategic checklist-framework fordealing with transaction cost aspects whichmay arise in project contracts before moredetailed considerations are discussed. Thischecklist consists of eight key areas, namely:

l Technical specifications, including use,

operation and maintenance

l Price, consistent with the technicalspecifications allowing for contingenciesand profit margins

l Payment terms which recognise the cashflow issues facing contractors

l Schedule with key milestones clearly definedand understood

l Performance guarantees including those tobe undertaken by the client

l The period of warranties specifying the re-performance of services and or thereplacement or repair of building defects

l Limitation of liability to protect contractor byproviding a maximum exposure

l Securities, such as bank guarantees, may beused to offer a limited degree of assuranceto both or either party

Von Branconi and Loch (2004) argue thatthese key areas are all sources of transactioncost, with associated areas of uncertainty asdescribed by Williamson (1992), Jarillo (1988)and Stinchcombe and Heimer (1985). Thefirst four key areas specify the project whilethe second four give assurances to both sides.

Jarillo (1988) discusses strategic networks ofpartners, which require partners to agree theirgoals through continuous collaboration andinterdependency. As construction involvesdiscrete projects, with future collaboration

RICS Research l 19www.rics.org/research

Understanding construction consortia: theory, practice and opinions

uncertain, if not unlikely, firms may be temptedto take advantage of short term opportunities.Stinchcombe and Heimer (1985) discuss apossible solution to transaction costs causedby clients’ changing requirements during aproject’s construction. They suggest that therelationships between the separate firmsshould be organised much more along thelines of relationships found insideorganisations. A higher degree of co-ordination and information-flow between thefirms should help a network of companies tobe more responsive to changes. Indeed, thepractical operation of construction consortiaprovides the very command structures,authority systems, dispute resolutionprocedures, standard operation systems andincentive schemes that are called for by thosewho seek to improve inter-firm collaboration.

Game theoryWe have noted that project size andcomplexity influence the way firms collaborate.This response is an application of game theory.According to Hargreaves, Heap and Varoufakis(1995) the situation facing firms in theconstruction and property sectors appears tocomply with the conditions of game theory.These conditions are that there should only bea limited number of players, that the playersexpect the behaviour of the other players to bebased on a similar rationality to their own andthat the actions of one player impact on theother players.

Three types of game may be identified: hawk-dove, co-ordination and prisoners’ dilemma. Inthe hawk-dove game, the share of profits isunequal but all lose if the players fight. In the

game of co-ordination, if firms co-operate theywin but if they fight they all lose. In theprisoner’s dilemma, individual firms act in theirown interest but are worse off as a result.

In brief, different games are played out inconstruction consortia. The different scenariosof winners and losers depend on the termsand conditions affecting the project that eachconsortium undertakes. The advantages of co-operation may be the initial driver towardssetting up consortia.

It may be assumed by firms and organisationsthat the members of a consortium combine totheir mutual advantage in a form of co-ordination game. However, unexpected eventsmay adversely affect all the parties and cancreate conflicts, which lead firms intoconfrontation, to their mutual detriment. Analternative game is presented by the prisoners’dilemma in which the members of theconsortium each act in their own interests withthe result that the gains from the consortiumare lower than they would have been had thefirms been able to co-operate. In the hawk-dove scenario firms combine to form consortiabut some members are far more powerful thanothers and are in a position to take advantageof their position. The result is that some firmsare worse off than they would have been, hadsome members not taken advantage of theirrelative strength. From this brief summary ofapplied game theory it is clear that conflict isinherent even within consortia, even where co-ordination games are being played, due to theimpossibility of predicting all the eventualitiesthat may arise.

20 l RICS Research

Conflict and dissent in theproduction processConsortia are formed by a number of diverseorganisations in order to undertake projects.These projects are therefore shared amongstthe members of the consortium. However, Iveand Gruneberg (2000) argue that members ofjoint ventures do not share the same goals. Inconstruction projects it is typical for eachmember of the team to have distinct goalsoften in conflict with the other members(Murdoch and Hughes, 2000). Moreover, notall members of the team are of equalimportance or have equalpower (Greenwood, 2002).

Nevertheless, a consortium(as distinct from the projectitself) may be deemedsuccessful if participation inthe joint venture issufficiently profitable foreach member and eachmember perceives his orher reward to becommensurate with his orher contribution. Butwhere firms collaborate,these conditions arealmost impossible to find.In the course of anyproject, disagreementsbetween the partiesinvariably emerge asdisputes arise overpayments for unplanned,unexpected or unavoidableadditional work. Ofnecessity these disputesmust arise as each

organisation seeks to promote its owninterests within the context of a zero sumgame, in which one party can benefit only atthe expense of another.

This is not to say that conflict is necessarilydestructive. Indeed conflict may be expectedand even welcomed as part of a creativeprocess or as a result of care, passion andinvolvement by people representing differentfirms. For example, it is quite possible that aquantity surveyor (QS) may be concerned withcontrolling costs while the contractors are

www.rics.org/research

Understanding construction consortia: theory, practice and opinions

....conflict may be expected and even welcomed aspart of the creative process....

concerned with delivering a building accordingto specifications. If costs are escalating to thepoint where cost overruns become inevitable,then the conflict between the QS and thecontractor may be used to find a compromisesolution.

Management of conflictLawrence and Lorsch (1967) suggest threemethods for dealing with dissent withincomplex business organisations, namely:confrontation, smoothing and force. Theterminology of Lawrence and Lorsch can beapplied to disputes withinconsortia. Confrontationinvolves presenting therelevant facts and seekinga solution to a problemthrough discussion andnegotiation. Smoothingrelies on emphasising thecommonalities betweenthe parties to a disputeand the costs of failure toboth parties. The thirdmethod is force anddepends on the relativepower of the firms indispute. One of theproblems with firmsadopting force is that they may benefitthemselves at the expense of the totality ofthe consortium. Unfortunately, the use offorce in construction disputes is common.Consortium members may use these threemethods to achieve their individual objectivesbut the resolution of any argument depends onthe relative economic power of theparticipants. For this reason the use ofconfrontation and force will tend to be more

effective than smoothing, as Lawrence andLorsch showed in their empirical work. Thedanger to be avoided is a tendency not toleave forcing as the technique of last resort,with the effect of impairing openness and trustbetween the parties in a consortium.

22 l RICS Research

One of the problemswith firms adopting

force is that theymay benefit

themselves at theexpense of thetotality of theconsortium

The formation of consortiaFour of the eight interviewees questioned forthis report had long-term consortiumrelationships, four did not. Those who tendedto have long-term relationships, such as thefinancial consultant, were not the majorspeculative risk takers, whereas those whotook on the major financial risks, such as thedeveloper and funder, tended to rely on newarrangements for each project. Consultantsmay have long-term relationships with theirclients but as consultants would not generallybe expected to take on financial risks. Theymay however, hold a relatively small proportionof the equity unless their commitment to theconsortium was based on payment followingfinal account, and success. Consultants do notgenerally invest any risk capital in consortiawith which they are involved.

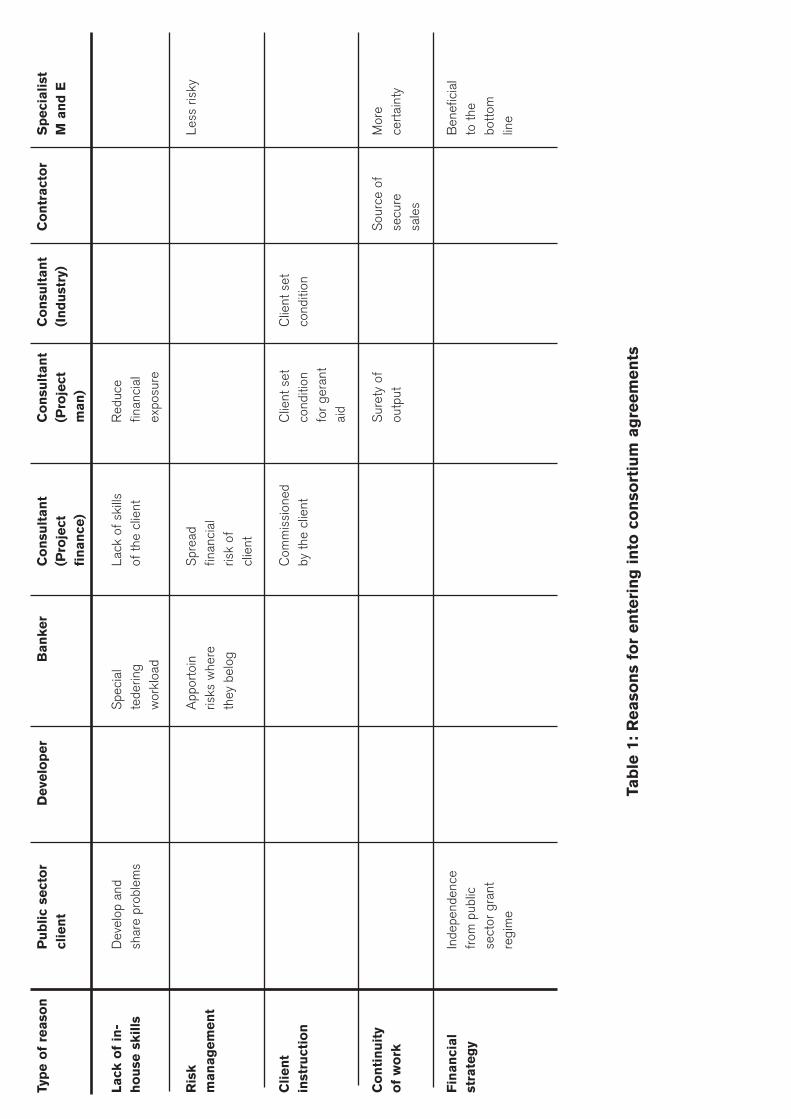

In Table 1 the reasons for entering intoconsortia are given vertically according to eachpoint of view and grouped horizontally byapproximate type of reason. The main reasonsfor entering into construction consortia,whether on a one-off basis or on an on-goingbasis, are related to a lack of skills in-house,the need to engage specialists at an earlyhigh-risk stage when projects were still highlyspeculative, and the need to apportion riskswhere they belonged. Moreover clients oftenrequire firms to enter into consortiaarrangements, which therefore improved thelikelihood of sales and increased their profitmargins. From the point of view of publicsector clients, consortia provide access toprivate sector funding as an alternative sourceof finance to grants funded by the Treasury.

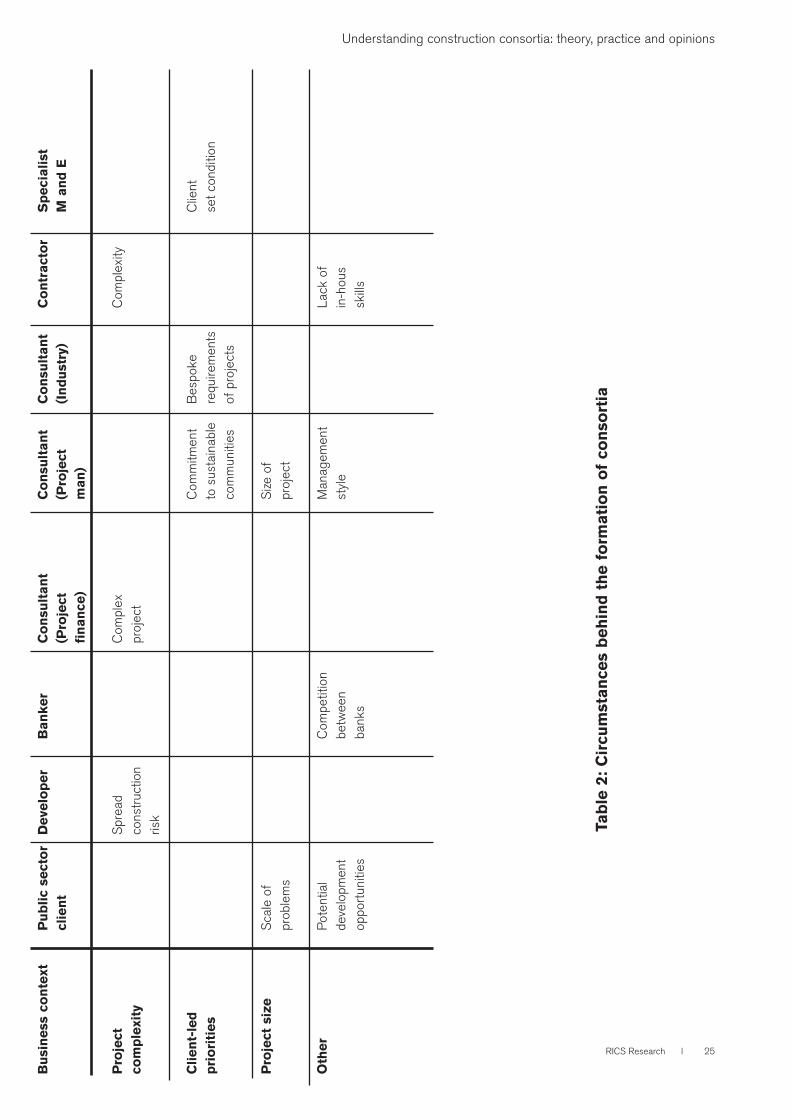

In Table 2, the circumstances that give rise tothe formation of consortia are shown verticallyaccording to each point of view and groupedhorizontally by approximate type of economicdriver. Consortia are often formed in responseto the complexity of development proposals,while the size of projects also plays animportant role in the need for firms tocollaborate. However, for banks, the drive toparticipate in consortia comes fromcompetition in financial markets. By joining aconsortium, banks can ensure a funding rolefor themselves before the project leadersrequire debt finance and approach financialcompetitors. One of the most importantconditions leading to the formation ofconsortia is the set of requirements of theclient. These may include specific terms andconditions relating to environmental provisionsor a requirement to demonstrate and providesustainable urban communities. Often theserequirements can only be met by closecollaboration of a number of firms, which thenrespond by forming a consortium.

In the social housing sector, the HousingCorporation Guidance Notes are frequentlyused as the basis for standard arrangements.However, in other construction sectors, whilemany firms may not use a standard partneringagreement, there is a general contract,PPC2000, available through the Association ofChartered Architects (ACA) and produced byTrowers and Hamlin. However, the contractualarrangements do not determine the economicinterests of the members of consortia beforethe consortium is formed. Rather, contractualagreements are determined by the economicinterests of the firms joining the consortium.

3 Results from the interviews

RICS Research l 23www.rics.org/research

Understanding construction consortia: theory, practice and opinions

Typ

e o

f re

aso

nP

ub

lic

sect

or

Deve

lop

er

Ban

ker

Co

nsu

ltan

tC

on

sult

an

tC

on

sult

an

tC

on

tract

or

Sp

eci

alist

clie

nt

(Pro

ject

(Pro

ject

(In

du

stry

)M

an

d E

fin

an

ce)

man

)

Lack

of

in-

Dev

elop

and

S

peci

alLa

ck o

f sk

ills

Red

uce

ho

use

skills

shar

e pr

oble

ms

tede

ring

of th

e cl

ient

finan

cial

wor

kloa

dex

posu

re

Ris

kA

ppor

toin

Spr

ead

Less

ris

kym

an

ag

em

en

tris

ks w

here

finan

cial

they

bel

ogris

k of

clie

nt

Clien

tC

omm

issi

oned

Clie

nt s

etC

lient

set

inst

ruct

ion

by th

e cl

ient

cond

ition

cond

ition

for

gera

ntai

d

Co

nti

nu

ity

Sur

ety

ofS

ourc

e of

Mor

eo

f w

ork

outp

utse

cure

ce

rtai

nty

sale

s

Fin

an

cial

Inde

pend

ence

Ben

efic

ial

stra

teg

yfr

om p

ublic

to th

e se

ctor

gra

ntbo

ttom

re

gim

elin

e

Tab

le 1

: R

easo

ns

for

en

teri

ng

in

to c

on

sort

ium

ag

reem

en

ts

Bu

sin

ess

co

nte

xtP

ub

lic

sect

or

Deve

lop

er

Ban

ker

Co

nsu

ltan

tC

on

sult

an

tC

on

sult

an

tC

on

tract

or

Sp

eci

alist

clie

nt

(Pro

ject

(Pro

ject

(In

du

stry

)M

an

d E

fin

an

ce)

man

)

Pro

ject

Spr

ead

Com

plex

Com

plex

ityco

mp

lexi

tyco

nstr

uctio

npr

ojec

tris

k

Clien

t-le

dC

omm

itmen

tB

espo

keC

lient

pri

ori

ties

to s

usta

inab

lere

quire

men

tsse

t con

ditio

nco

mm

uniti

esof

pro

ject

s

Pro

ject

siz

eS

cale

of

Size

of

prob

lem

spr

ojec

t

Oth

er

Pot

entia

lC

ompe

titio

nM

anag

emen

tLa

ck o

fde

velo

pmen

tbe

twee

nst

yle

in-h

ous

oppo

rtun

ities

bank

ssk

ills

RICS Research l 25

Understanding construction consortia: theory, practice and opinions

Tab

le 2

: C

ircu

mst

an

ces

beh

ind

th

e f

orm

ati

on

of

con

sort

ia

At the early stages of the formation of aconsortium, for example, banks rely on a loose,ad hoc memorandum of understanding ratherthan a rigid contract. The same may be said ofdevelopers.

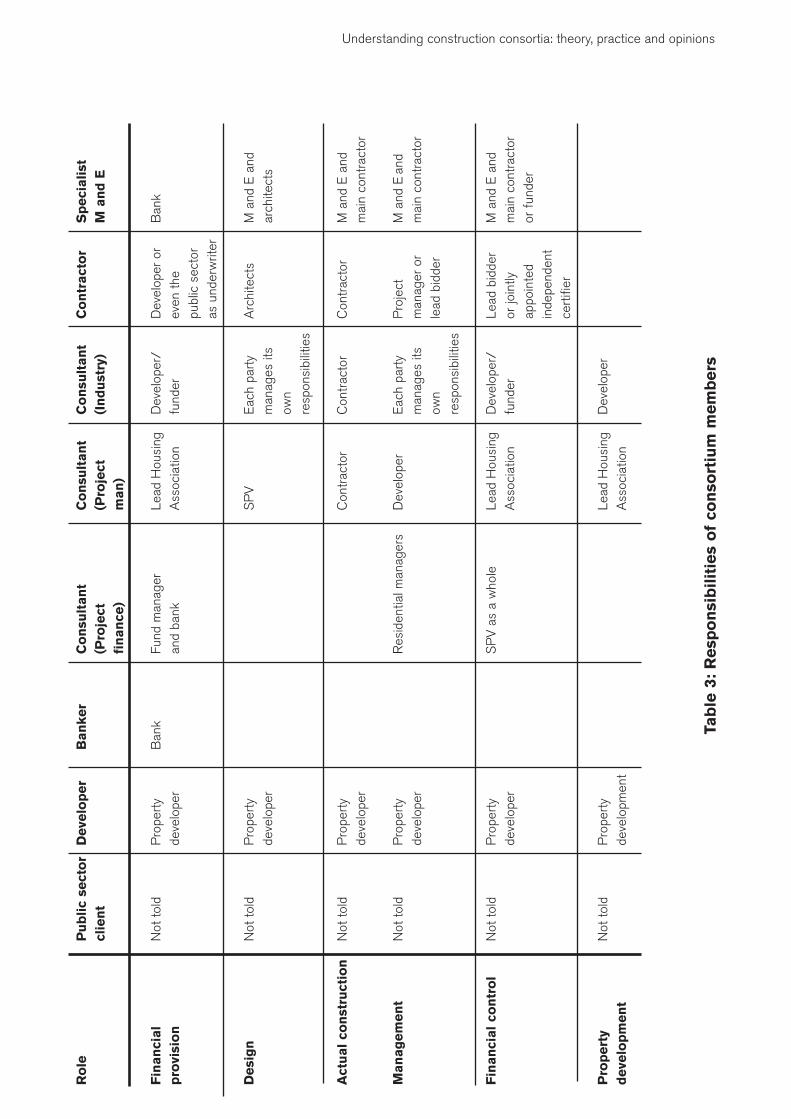

Participants and roles inconsortiaThe left hand column in Table 3 lists a numberof roles in the development process. Theresponsibility for each of these roles isallocated according to the responses givenvertically by each of the interviewees. There islittle consensus concerning the allocation of anumber of responsibilities. The table isindicative of a confusion of roles and a lack ofclear definition. This lack of prescribed rolesmay be one cause of conflict andmisunderstanding between firms withinconsortia. This is particularly the case withregards to design, management and financialcontrol, where responsibility for the functioncan be seen to range from the SPV, as awhole, to different individual members.However, responsibility for financial provision,property development and actual constructionare more clearly defined.

Although it might be argued that consortiumarrangements such as SPVs might be used tooffload risks and responsibilities, the developercan be seen as accepting overall responsibilityfor almost every aspect of the development, inreturn for the profit arising out of the project.The public sector client was not informedabout the allocation of responsibilities in theconsortia working for the local authority.Although developers may see themselves asthe main risk takers, according to the verticalcolumn labelled Developer in Table 3, the

consultants and contractors do not necessarilyshare this view. As far as responsibility fordesign, management and financial controlwere concerned; the consultants consideredrisks were shared between several parties. Infact, while overall responsibility may rest withthe developers, even the developer concededthat those in the supply chain, the contractors,took the construction risk.

The management of risk inconsortiaThis apparent contradiction arises out of theposition of the developer who is responsible tofunders for the delivery of a building as far asthe funders are concerned but then thedeveloper offloads that responsibility on to thecontractors. Similarly overall responsibility forthe project may be assumed by the projectlead banker, responsible for the financibilityand deliverability of the project because it isthe lead bank, which is responsible to theunderwriters of the finance. Again the bankprotects its exposure to risk by ensuring thedeveloper takes responsibility for the deliveryof the project. Thus each member of aconsortium fulfils both a supplier and apurchaser role. As a supplier, the memberundertakes a responsibility but then passesthe risk down the supply chain when it acts asa purchaser of its own inputs.

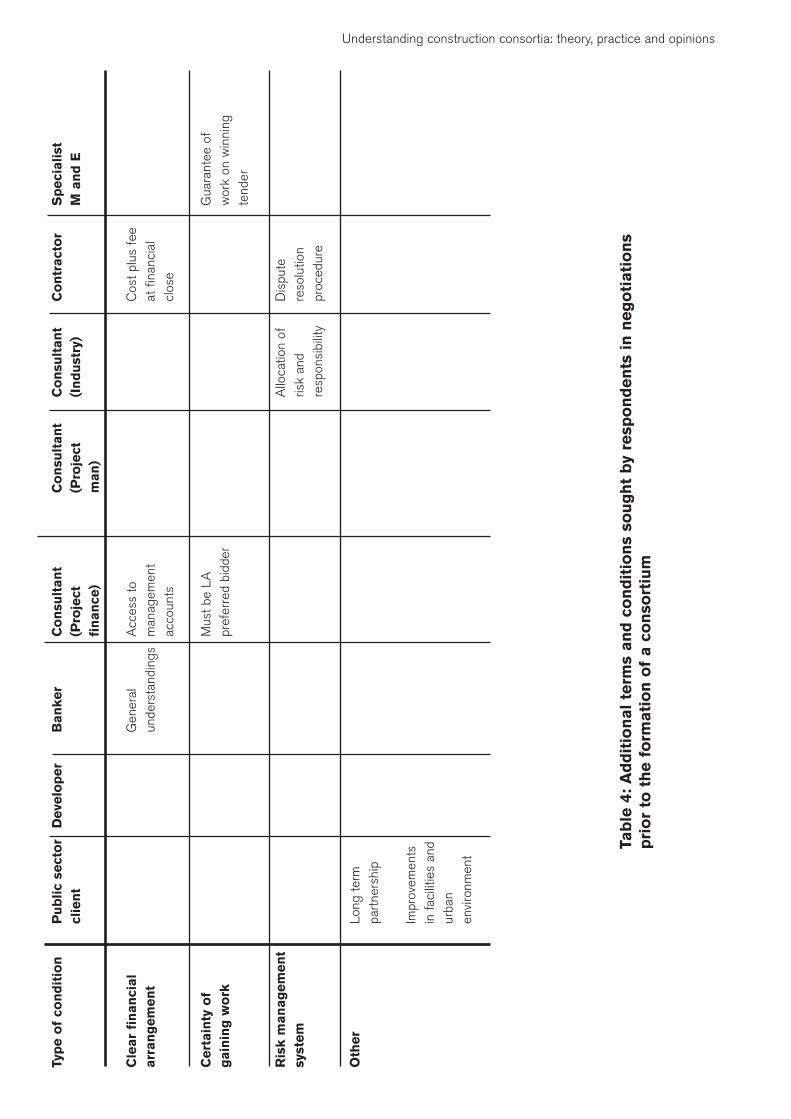

In the light of the difficulties of allocating riskand responsibilities after a consortium hasbeen formed, Table 4 shows the generalconditions sought by firms even beforeentering a consortium and before contractsare signed. These terms and conditions areshown vertically according to the point of viewof each interviewee and grouped

26 l RICS Research

Ro

leP

ub

lic

sect

or

Deve

lop

er

Ban

ker

Co

nsu

ltan

tC

on

sult

an

tC

on

sult

an

tC

on

tract

or

Sp

eci

alist

clie

nt

(Pro

ject

(Pro

ject

(In

du

stry

)M

an

d E

fin

an

ce)

man

)

Fin

an

cial

Not

told

Pro

pert

yB

ank

Fund

man

ager

Lead

Hou

sing

Dev

elop

er/

Dev

elop

er o

rB

ank

pro

visi

on

deve

lope

ran

d ba

nkA

ssoc

iatio

nfu

nder

even

the

publ

ic s

ecto

ras

und

erw

riter

Desi

gn

Not

told

Pro

pert

yS

PV

Eac

h pa

rty

Arc

hite

cts

M a

nd E

and

deve

lope

rm

anag

es it

sar

chite

cts

own

resp

onsi

bilit

ies

Act

ual

con

stru

ctio

nN

ot to

ldP

rope

rty

Con

trac

tor

Con

trac

tor

Con

trac

tor

M a

nd E

and

deve

lope

rm

ain

cont

ract

or

Man

ag

em

en

tN

ot to

ldP

rope

rty

Res

iden

tial m

anag

ers

Dev

elop

erE

ach

part

yP

roje

ct

M a

nd E

and

deve

lope

rm

anag

es it

sm

anag

er o

rm

ain

cont

ract

orow

n le

ad b

idde

rre

spon

sibi

litie

s

Fin

an

cial

con

tro

lN

ot to

ldP

rope

rty

SP

V a

s a

who

leLe

ad H

ousi

ngD

evel

oper

/Le

ad b

idde

rM

and

E a

ndde

velo

per

Ass

ocia

tion

fund

eror

join

tlym

ain

cont

ract

orap

poin

ted

or f

unde

rin

depe

nden

tce

rtifi

er

Pro

pert

y N

ot to

ldP

rope

rty

Lead

Hou

sing

Dev

elop

erd

eve

lop

men

tde

velo

pmen

tA

ssoc

iatio

n

Understanding construction consortia: theory, practice and opinions

Tab

le 3

: R

esp

on

sib

ilit

ies

of

con

sort

ium

mem

bers

horizontally by approximate type of condition.As the developer is usually the initiator of aconsortium, any terms and conditions agreedby the parties prior to setting up a consortiumwould be required as a concession made bythe developer. The developer does notgenerally begin the process with priorconditions as such, and therefore theDeveloper column in Table 4 is empty. Table 4also shows the diversity of requirementspartners might seek prior to joining aconsortium.

Before entering into a consortium commitmentwith other firms, the project finance advisorsuggested that firms should seek access tothe management accounts of key partners.This is seen as vital because of theinterdependence of the members of aconsortium and the shortcomings of thehistorical nature of annual accounts.

Up to the point when a group of firms biddingfor a contract is given preferred bidder status,partners are free to leave a consortium. In theearly stages agreements may be based ongeneral understandings as far as the bank isconcerned. Nevertheless contractors mayrequire more specific terms andunderstandings such as a commitment to costreimbursement during construction, plus a feeat financial close. Even at the beginning of thetender process, some firms, such as specialistcontractors undertaking detailed design workand seek guarantees that they will beappointed if the consortium wins the tender.

In the social housing sector one prerequisite isthat the consortium must be a local authority(LA) preferred bidder. Local authority

preferred bidders are housing associations andtheir partners, who have pre-qualified for LAgrant support. Local authorities may, for theirpart, seek consortia, which are willing toprovide improvements in facilities and theurban environment.

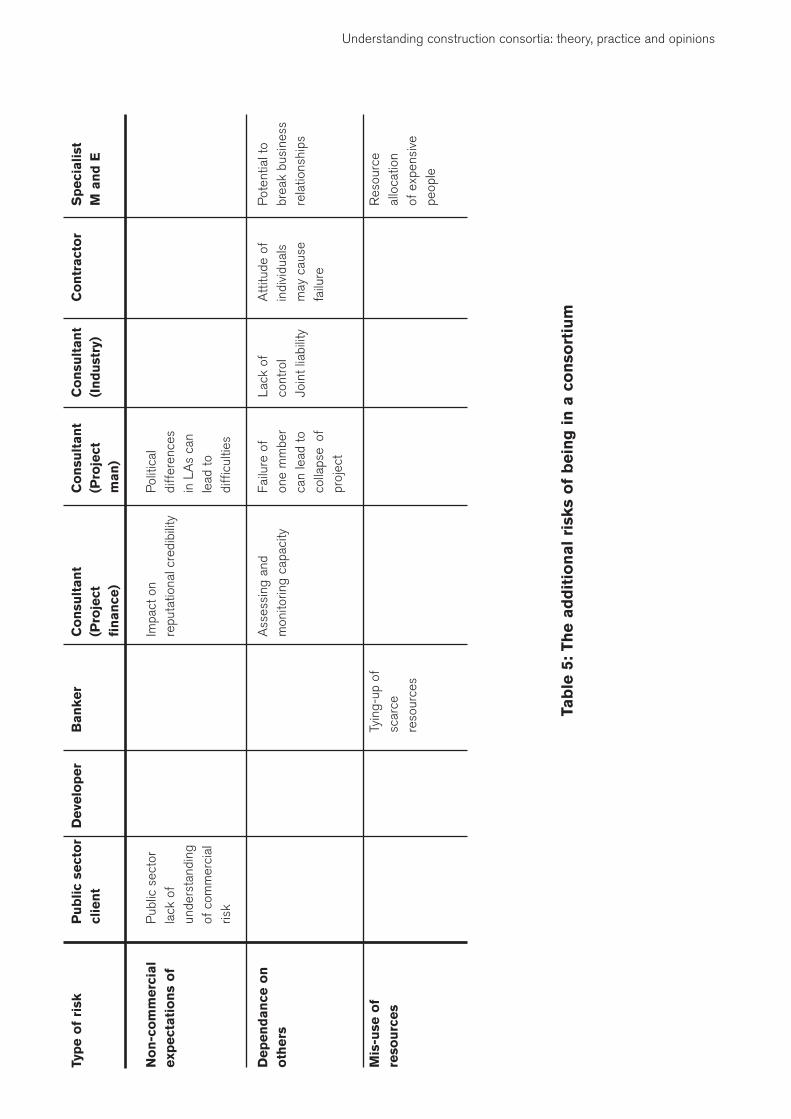

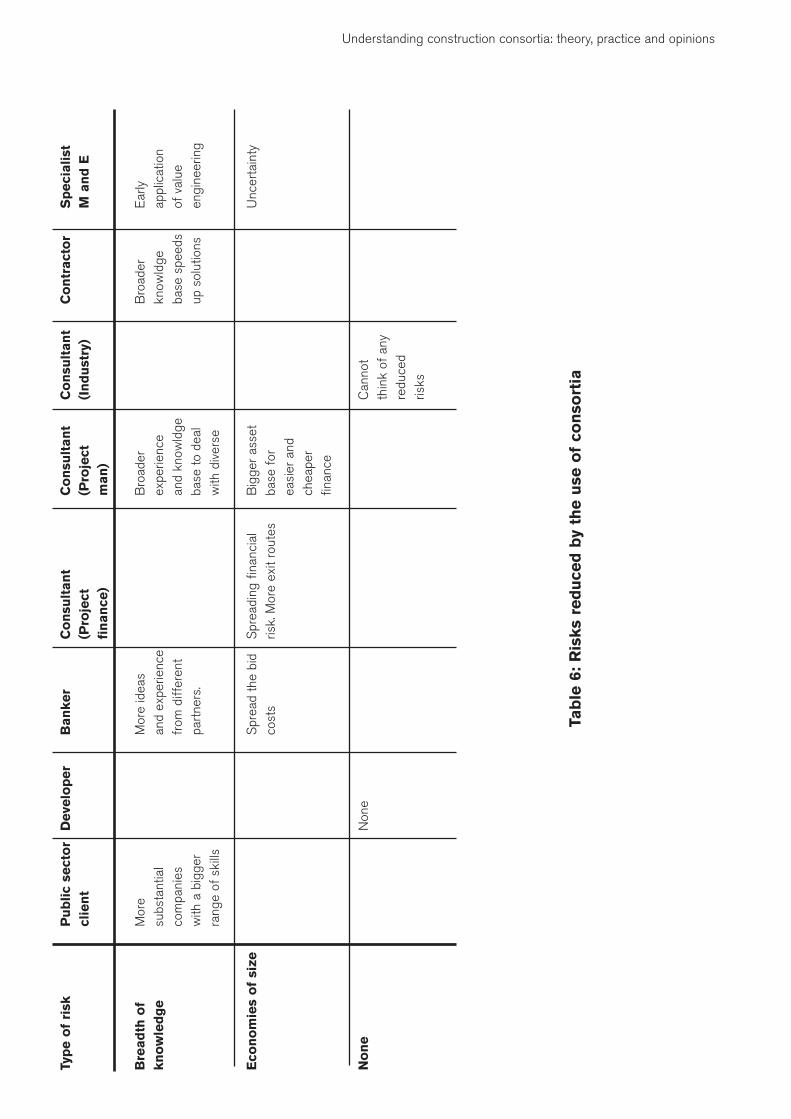

Additional risks in consortiaIt may be argued that consortia reduce risk.Different firms working together with differentspecialist skills, and more diverse managementexpertise than any single firm, appear to offerlower risk solutions. However, far fromreducing uncertainty, consortia can also beseen as increasing some firms’ exposure torisk. This apparent paradox can be resolvedby thinking in terms of overall risk reductionand individual firms’ risk exposure. While eachfirm may experience additional risk factors,many of these risks are part of a zero sumgame, in which the total risk to the client isreduced. For example, value engineeringimplies that solutions can be found whichreduce the total cost of construction. At thesame time, design changes brought about bythe value engineering exercise may mean thatone or more members of the consortium mayfind their services are no longer required.

Table 5 shows the additional risks faced bymembers of a consortium. The major group ofidentified risks is concerned with theimplications of working very closely with otherfirms or organisations. This area of riskassociated with consortia may be calledreputational risk. Reputational risk is notlimited. In any case all respondents stated thatlimited liability makes no difference wherelarge projects are concerned. In effect any

28 l RICS Research

Typ

e o

f co

nd

itio

nP

ub

lic

sect

or

Deve

lop

er

Ban

ker

Co

nsu

ltan

tC

on

sult

an

tC

on

sult

an

tC

on

tract

or

Sp

eci

alist

clie

nt

(Pro

ject

(Pro

ject

(In

du

stry

)M

an

d E

fin

an

ce)

man

)

Cle

ar

fin

an

cial

Gen

eral

Acc

ess

toC

ost p

lus

fee

arr

an

gem

en

tun

ders

tand

ings

man

agem

ent

at f

inan

cial

acco

unts

clos

e

Cert

ain

ty o

fM

ust b

e LA

Gua

rant

ee o

fg

ain

ing

wo

rkpr

efer

red

bidd

erw

ork

on w

inni

ngte

nder

Ris

k m

an

ag

em

en

tA

lloca

tion

ofD

ispu

tesy

stem

risk

and

reso

lutio

nre

spon

sibi

lity

proc

edur

e

Oth

er

Long

term

part

ners

hip

Impr

ovem

ents

in fa

cilit

ies

and

urba

nen

viro

nmen

t

Understanding construction consortia: theory, practice and opinions

Tab

le 4

: A

dd

itio

nal

term

s an

d c

on

dit

ion

s so

ug

ht

by

resp

on

den

ts i

n n

eg

oti

ati

on

sp

rio

r to

th

e f

orm

ati

on

of

a c

on

sort

ium

firm that fails to perform to the satisfaction ofits public sector clients will find it extremelydifficult to continue to supply services to publicsector organisations. Indeed if any firmconsistently underperformed, it would find itdifficult to win more work, especially in thepublic sector. This reduces demand for thefirm’s output, depending on the ratio of publicto private sector work the firm carries out.Even private sector clients may be deterred bya firm’s tainted reputation.

The interdependence of firms in consortia hasthe potential to break up working relationshipsbetween members, leading to a significant lossin a firm’s turnover. As consortia often workclosely with local authorities, an additional riskfacing firms is the lack of understanding ofcommercial risk by many in the public sector.Indeed political disputes between different

local authorities (where projects overlap intoneighbouring council territories) and betweenlocal authorities and central government canalso lead to difficulties for consortia members.

A further risk for firms in consortia is thechanging capacity of fellow firms to fulfil theirobligations to the consortium. Given that eachfirm is engaged on a number of projectsoutside the consortium and because of thelumpiness of demand facing any one firm inproperty and construction, each member firm’s

capacity available to the consortium can varywidely over the life of a consortium.

There are other soft issues, for example thetying up of resources, such as expensivesenior management, which interferes with thesmooth running of the organisation, especiallyas there is no guarantee of success. This

30 l RICS Research

A further risk forfirms in consortia is

the changingcapacity of fellowfirms to fulfil theirobligations to the

consortium

Typ

e o

f ri

skP

ub

lic

sect

or

Deve

lop

er

Ban

ker

Co

nsu

ltan

tC

on

sult

an

tC

on

sult

an

tC

on

tract

or

Sp

eci

alist

clie

nt

(Pro

ject

(Pro

ject

(In

du

stry

)M

an

d E

fin

an

ce)

man

)

No

n-c

om

merc

ial

Pub

lic s

ecto

rIm

pact

on

Pol

itica

lexp

ect

ati

on

s o

fla

ck o

fre

puta

tiona

l cre

dibi

lity

diff

eren

ces

unde

rsta

ndin

gin

LA

s ca

n of

com

mer

cial

lead

toris

kdi

ffic

ultie

s

Dep

en

dan

ce o

nA

sses

sing

and

Failu

re o

f La

ck o

fA

ttitu

deof

Pot

entia

l to

oth

ers

mon

itorin

g ca

paci

tyon

e m

mbe

rco

ntro

lin

divi

dual

sbr

eak

busi

ness

can

lead

toJo

int l

iabi

lity

may

cau

sere

latio

nshi

psco

llaps

eof

failu

repr

ojec

t

Mis

-use

of

Tyin

g-up

of

Res

ourc

ere

sou

rces

scar

ce

allo

catio

nre

sour

ces

of e

xpen

sive

peop

le

Understanding construction consortia: theory, practice and opinions

Tab

le 5

: Th

e a

dd

itio

nal

risk

s o

f b

ein

g i

n a

co

nso

rtiu

m

would also apply where no consortium isformed but selection for many public sectorprojects is not based on a single firm’sstrengths or offer, but on the combinedstrengths and merits of the consortium as awhole. Success, for example from aconsortium funder’s point of view, is alsodependent on the selection process, whichmay be based on design or facilitiesmanagement features and not just the bankingaspects of the bid.

Risks within consortia may be classed asattributable and non-attributable risks.Attributable risks may be taken by membersaccording to their skills and roles within theconsortium. Non-attributable risks may betaken by the consortium leader or the funder.

Although property developers may argue thatit is they, who accept responsibility for projects,risks are borne by those in the weakestnegotiating position as they can be most easilyreplaced. Therefore those who offer non-differentiated services are in the mostvulnerable position. The firms in the weakestnegotiating position are the contractors andtheir sub-contractors. Perceived risk is takenby the developers and constructional risk istaken by the contractors. Perceived risk, whichmay be speculative or commercial risk, isrewarded with the profits (net of constructioncosts). The constructional risk is therefore leftto contractors to price correctly and profitably(while still winning the auction for work).Risks are thus identified and allocated to thefirm best able to manage them. That firm thenowns the risk. Construction is seen as a highrisk, high volume and low-margin business.