Embed Size (px)

Citation preview

Canadian Investment Funds Course

www.ifse.ca © 2007

4-1

Unit 4: Types of Mutual Funds Welcome to Types of Mutual Funds. This unit gives you an overview of the types of mutual funds available. Before providing your client with an investment solution, you need to know what products are available, and what products are most appropriate. This unit takes approximately 1 hour and 15 minutes to complete. You will learn about the following topics:

• Three Categories of Funds • Income Funds • Growth Funds • Combination Growth and Income Funds • Comparing the Funds

To start with the first lesson, click Three Categories of Funds on the table of contents.

Lesson 1: Three Categories of Funds

www.ifse.ca © 2007

4-2

Lesson 1: Three Categories of Funds Welcome to Three Categories of Mutual Funds lesson. In this lesson, you will review the three main categories of mutual funds, and the objectives of each one. Before providing your client with an investment solution, you need to know what products are available, and how they work. This lesson takes 15 minutes to complete. At the end of this lesson, you will be able to do the following:

• list the three categories of mutual funds • describe the investment objectives of each category of fund

Canadian Investment Funds Course

www.ifse.ca © 2007

4-3

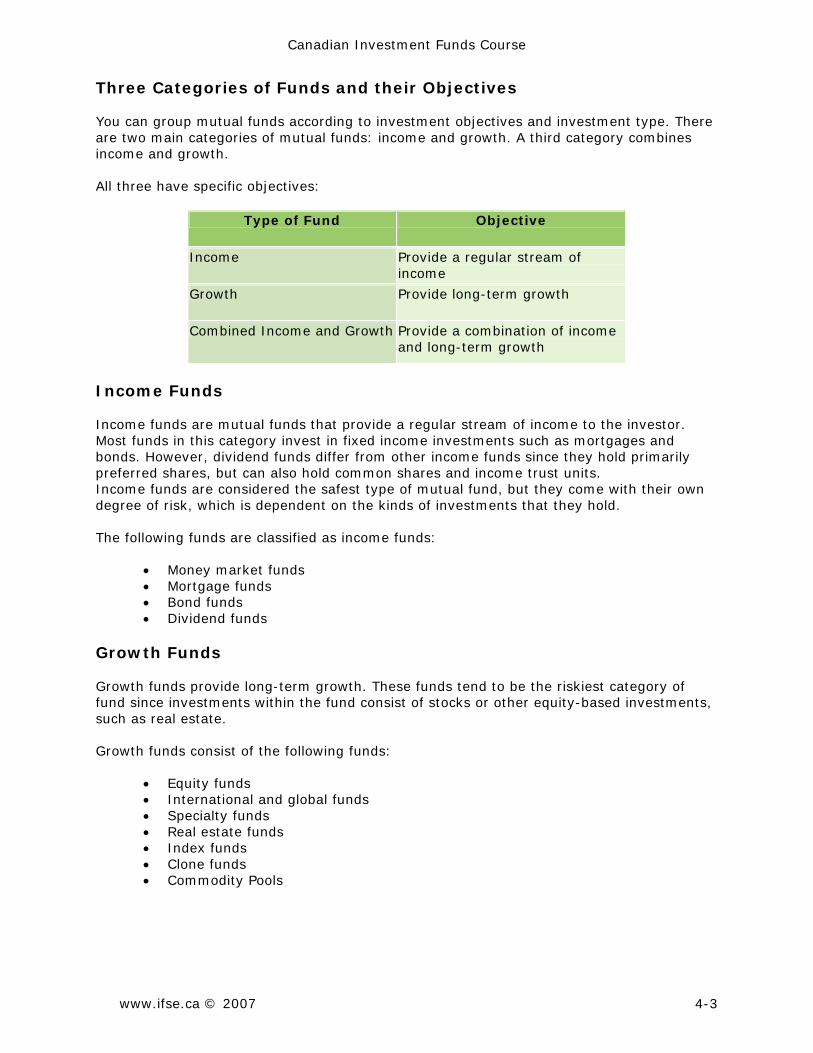

Three Categories of Funds and their Objectives You can group mutual funds according to investment objectives and investment type. There are two main categories of mutual funds: income and growth. A third category combines income and growth. All three have specific objectives:

Type of Fund Objective

Income Provide a regular stream of income

Growth Provide long-term growth

Combined Income and Growth Provide a combination of income and long-term growth

Income Funds Income funds are mutual funds that provide a regular stream of income to the investor. Most funds in this category invest in fixed income investments such as mortgages and bonds. However, dividend funds differ from other income funds since they hold primarily preferred shares, but can also hold common shares and income trust units. Income funds are considered the safest type of mutual fund, but they come with their own degree of risk, which is dependent on the kinds of investments that they hold. The following funds are classified as income funds:

• Money market funds • Mortgage funds • Bond funds • Dividend funds

Growth Funds Growth funds provide long-term growth. These funds tend to be the riskiest category of fund since investments within the fund consist of stocks or other equity-based investments, such as real estate. Growth funds consist of the following funds:

• Equity funds • International and global funds • Specialty funds • Real estate funds • Index funds • Clone funds • Commodity Pools

Lesson 1: Three Categories of Funds

www.ifse.ca © 2007

4-4

Combined Income and Growth Funds that provide a combination of income and growth hold a mix of fixed income and equity investments. These funds are considered moderate risk since they provide the investor with a level of stability along with the potential for capital growth. The following funds would fit into this category:

• Balanced funds • Asset allocation funds

Exercise: Three Categories of Funds

Canadian Investment Funds Course

www.ifse.ca © 2007

4-5

Lesson 2: Income Funds Welcome to the Income Funds lesson. In this lesson, you will learn about the different types of income funds available to investors. You will learn which instruments these funds hold, how they work, and for whom they are suitable. This lesson takes 15 minutes to complete. At the end of this lesson, you will be able to do the following:

• describe how a money market fund works • describe how a mortgage fund works • describe how a bond fund works • describe how a dividend fund works

Lesson 2: Income Funds

www.ifse.ca © 2007

4-6

Money Market Funds Definition Money market funds hold money market investments (cash and cash-type investments) that are short-term (less than one year). A money market fund portfolio contains the following investments:

• treasury bills (T-bills) • bankers' acceptances • commercial paper • provincial and municipal short-term paper

How it works Money market funds have terms to maturity of less than one year. By law they must have a weighted term to maturity of 90 days or less so any monies invested are returned quickly. Although the investments within the fund fluctuate with general interest rate levels, the funds are managed in such a way that the fund price remains constant (although it may fluctuate under rare circumstances), typically $1 or $10. In practice the investor does not experience any loss of invested capital. Money market funds pay interest on a monthly basis. You can reinvest the interest automatically or receive it as income. Returns move in the same direction as general interest rates and are usually better than on a traditional bank account. Risk profile Money market funds invest in low-risk securities and therefore have the lowest risk and pay lower returns. Client suitability The goal of money market funds is to provide income for the investor with a low risk to capital. These funds are suitable for investors who want to protect their investments, but also want some return. They are not typically a good investment for long-term goals, but they can be a smart choice for short-term goals, such as saving for a rainy day fund or parking money while deciding on long-term investments. Mortgage Funds Definition Mortgage funds contain mortgages, which are fixed income investments. Like other fixed income investments, mortgage fund prices rise when interest rates fall, and mortgage fund prices fall when interest rates rise. Returns increase in times of falling interest rates and decrease in times of rising interest rates.

Canadian Investment Funds Course

www.ifse.ca © 2007

4-7

How it works Most people are familiar with mortgages as borrowers, but when mortgage fund managers purchase mortgages they are acting as lenders. Most mortgage funds hold NHA insured mortgages. By investing in these mortgages, mutual funds reduce the risk of defaults by borrowers, which can lessen the return on a fund. Cash flow to the mortgage funds come from both the repayment of mortgage principal and interest payments. The mortgage fund in turn, distributes only the interest to unitholders on a monthly basis. There may also be capital gains distributions from the funds to unitholders at the end of the year. Just like other mutual funds, these funds do not pass on any capital losses to the investor. A monthly return of capital and interest stabilizes the price of mortgage fund units. This is achieved by having more capital available to invest in new mortgages at current interest rates. For example, every month when a borrower makes a mortgage payment, part of the payment goes towards the principal, and part of it goes towards interest. The interest portion is first sent to the lender, and then the lender flows it to the investor (mutual fund unitholder). This is how a mortgage fund supplies a steady stream of interest income. The principal portion is retained in the fund and used to purchase new mortgages. Risk profile Mortgage funds are a low-risk investment, although certainly not as low-risk as money market funds. Mortgage funds are less volatile than bond funds because mortgages have terms of less than five years. Investors should be aware of the risk of early repayment of principal, which can result in a potential loss of interest payments at higher interest rates. However, this risk is partially offset by the requirement of the borrower to pay a penalty for any unscheduled prepayments. Client suitability Mortgage funds are suitable for clients who want to protect their capital, require a steady stream of income, and do not have an immediate need for the invested funds. Younger people, who are already earning an adequate income, do not necessarily need income from their investments to support themselves. But fixed income funds (money market, bond, and mortgage) can help them diversify their portfolios. Exercise: Money Market and Mortgage Funds

Lesson 2: Income Funds

www.ifse.ca © 2007

4-8

Bond Funds Definition Bond funds invest in bonds. Some bond funds invest exclusively in one type of bond — for instance, government bonds — while others may hold a combination of bond types. How it works The main objective of bond funds is to produce income in the form of interest, which is usually paid to unitholders on a monthly basis. However, capital gains may also be derived from the trading of bonds in the portfolio. Bond funds can also experience capital losses when bond prices drop. These losses are not distributed but held in the fund to offset capital gains. Since bond funds hold a portfolio of bonds, portfolio managers can minimize some of the risks associated with bonds, such as interest rates and issuers, with diversification. Portfolio managers can adjust the bond maturities to take advantage of different stages in the economic cycle. Longer maturities can be used when interest rates are low or falling and shorter maturities can be used for periods of high or rising rates. If permitted by the investment objectives, portfolio managers can also diversify their portfolio by the type of bond issuers. For instance, they may hold bonds from the federal and provincial government as well as corporate bonds. Risk profile Bond funds are considered low to moderate risk investments. They tend to be more volatile than mortgage funds because they hold securities with longer maturities, which are often 20 years or more. The longer the maturity of a bond, the more it will be affected by interest rate changes. Longer-term bonds rise in value more when interest rates fall, and drop in value more when interest rates rise. Bond funds that invest in corporations or foreign governments may be riskier than ones that invest in domestic bonds since there may be a higher possibility of default. Client suitability Bond funds are suitable for investors who want to protect their capital, but also require a stream of income for living. Dividend Funds Definition Dividend funds provide investors with periodic income from dividend-paying investments, as well as the potential to earn capital gains through growth. The majority of the investments are preferred shares of Canadian corporations, and to a lesser extent, the common shares of dividend-paying corporations. These corporations are large, established companies with a history of steady dividend payment on their common shares. These companies are usually referred to as blue chip.

Canadian Investment Funds Course

www.ifse.ca © 2007

4-9

How it works These investments enable dividend funds to generate tax-preferred income. Investors in these funds benefit from the dividend tax credit. This credit reduces the amount of tax payable by investors who receive dividends distributed by Canadian corporations. Returns from dividend funds consist of a combination of income and capital appreciation (or depreciation) of shares. Therefore, returns are dependent on both the direction of interest rates — which have an inverse relationship to prices of preferred shares — and the general direction of stock markets. Although corporations do not have to pay dividends, blue chip corporations generally do issue dividends in order to ensure market and investor confidence. Therefore, dividend funds are less risky than equity funds that often hold equity investments that rarely or never pay dividends. Risk profile Dividend funds are a moderate risk investment. They are riskier than bond and mortgage funds, because the market value of the preferred and common shares fluctuates as market conditions change. Client suitability Dividend funds are suitable for investors with a moderate risk profile who would like a steady stream of tax-preferred income, but would also like the opportunity to earn some capital gains through growth of the investments. Investors should be able to tolerate some decline in the value of their investments. Exercise: Income Funds

Lesson 3: Growth Funds

www.ifse.ca © 2007

4-10

Lesson 3: Growth Funds Welcome to the Growth Funds lesson. In this lesson, you will learn about the different types of growth funds available to investors. You will learn the financial instruments these funds hold, how they work and for whom they are suitable. This lesson takes 20 minutes to complete. At the end of this lesson, you will be able to do the following:

• describe how an equity fund works • describe how an international and global fund works • describe how a specialty fund works • describe how a real estate fund works • describe how an index fund works • describe how a commodity pool works

Canadian Investment Funds Course

www.ifse.ca © 2007

4-11

Equity Funds Definition Equity funds invest primarily in the common shares of corporations. There are many types of equity funds, ranging from funds that invest in a variety of shares to funds that invest in shares of a specific economic sector or shares in foreign companies. Some may specialize in more secure, blue-chip stocks while others invest in smaller growth companies. How it works Canadian equity funds invest primarily in the shares of Canadian companies. Returns from these funds consist mainly of capital gains through share appreciation. Investors may also receive minimal dividends. Some equity funds concentrate on smaller companies and are known as small capitalization or small-cap funds. Others may concentrate on medium or large companies. Large, well-established companies are often referred to as “blue-chip”. U.S. equity funds invest primarily in shares of U.S. companies. As with Canadian equity funds, U.S. equity funds can hold a diversified portfolio of stocks or specialize in a particular sector, geographic area, or market capitalization. Returns from equity funds vary according to a number of factors:

• the industries in which the fund invests • the aggressiveness of investing • the proportion of domestic and foreign equities held • the skills of the fund managers in selecting stock market investments

Risk profile Generally, equity funds are higher-risk investments. Volatility is high because of the extreme variability of stock prices in general. The tradeoff, however, is the potential of far greater returns. Funds that invest in larger companies are considered lower risk than small-cap funds. Those stocks, especially blue-chip stocks, are larger, more established, and have a longer performance record and history of paying dividends. Their stock price tends to be less volatile, reflecting the market’s greater confidence. Equity funds tend to invest in stocks in different industry sectors. This diversification moderates the volatility of the funds in comparison to more specialized funds. Client suitability Equity funds are suitable for the moderate to high-risk investor who is seeking capital growth over the longer term. The investor would have to be prepared to see his or her investment decline in value in the short term.

Lesson 3: Growth Funds

www.ifse.ca © 2007

4-12

International and Global Funds Definition International funds invest almost exclusively in securities outside of Canada and North America, while Global Equity funds may invest in the Americas but must also invest in Asia and Europe. How it works These funds may specialize in one type of security, such as stocks, or invest in a variety of securities, such as stocks and bonds. Risk profile These funds are moderate to high risk. The returns and risks of these funds are dependent on the following factors:

• location of the investment • type of security • changes in currency exchange rates • type of investment • approach taken: conservative or aggressive

Client suitability International and global funds are suitable for investors who have a moderate to high-risk profile, and investors who are looking for international diversification. Specialty Funds Definition Specialty funds invest in the common shares of companies in a particular industrial or economic sector, or a defined geographic area. They are a subset of equity funds but are narrowly focussed. How it works Some of the equity funds, such as natural resource funds, can be considered specialty funds. Others include funds that invest in the securities of particular countries, such as Japan, or a specialty fund might invest in the securities of a larger region, such as the Far East or Europe. Specialty funds may invest in stocks, bonds, or other securities. Gold funds, for example, may invest in shares of mining companies in North America and abroad, as well as in gold bullion. Risk profile Specialty funds are usually high-risk investments. Many of these funds strive to earn high rates of return through capital gains. As a result, returns can be highly volatile. These funds offer the potential for large gains and large losses, and performance can vary widely from year to year.

Canadian Investment Funds Course

www.ifse.ca © 2007

4-13

Client suitability Specialty funds are suitable for investors who have a high-risk profile, and who are looking for long-term growth. Exercise: Equity, International, and Specialty Funds

Real Estate Funds Definition Real estate funds invest in real estate, usually in commercial and industrial properties. Some invest in the shares of real estate management companies or development companies. How it works Investor returns are in the form of rental and other income generated by properties in the fund's portfolio, plus capital gains if the properties are sold at a profit. In addition, real property holdings (any type of building) are depreciable for tax purposes. Consequently, they generate tax deductions for investors. These deductions, known as capital cost allowances, are deductible against rental income that is distributed to holders of units in real estate funds. When properties are sold, the fund and ultimately the investors may experience a recapture of capital cost allowance. In this situation, the recaptured amount is distributed amongst unitholders and included as income for tax purposes. This applies only to real estate funds that pass on the capital cost allowance to their investors; otherwise redemption proceeds are treated in the same manner as those for other types of funds. The rate and the conditions of these charges are clearly defined in the fund's prospectus. Real estate funds are valued on a different basis than most funds. Most mutual funds are valued daily to reflect constant changes in the prices of investments that are frequently bought and sold and for which there are defined prices. However, the valuation of real estate funds is based on appraisals of the properties in the fund's portfolio. These appraisals are used to calculate the fund's net asset value, which in turn is used to determine the price of fund units. As a result, unit prices are usually set monthly or quarterly. Because unit prices of real estate funds are set less frequently than other mutual funds; real estate fund units are less liquid. Investors may be able to redeem fund units only at specified times, and may have to give prior notice. It may also take considerable time to receive the proceeds of a redemption request. If the fund does not have enough cash on hand, redemption requests may be only partially filled.

Lesson 3: Growth Funds

www.ifse.ca © 2007

4-14

Risk profile Real estate funds are high-risk investments because the fund is concentrated in one industry, the real estate industry. Investors also have less liquidity since the portfolio may hold real properties. Client suitability Real estate funds are suitable for investors who have a high-risk profile, who are looking for tax advantages, and who have a longer time horizon. Index Funds Definition An index fund matches its portfolio to that of a specific financial market index, such as the Standard & Poor's 500 Index (S&P 500). The value of fund units then fluctuates in tandem with those indexes. Although most popular index funds are growth oriented, they also can be income or a combination of income and growth oriented. How it works Index funds are considered passive funds because they do not require any analysis or specific expertise of the portfolio manager. To construct an index fund, the manager purchases all of the stocks in the particular index in exactly the same proportion in which those stocks are represented in the index. Therefore, the return of an index fund should mirror that of the underlying index. For example, if the total returns for the S&P 500 rise by 10% in one year, unit values of a fund based on this index should rise by the same percentage (less management fees). Some of the stocks in the index pay dividends that are passed on to the investor, but the primary income expectation of an index fund is capital gains through investment appreciation. Risk profile Index funds are of moderate to high risk. Because index funds move directly with the market index, there can be some pronounced movements in the fund value. These funds have more risk than dividend funds because there is not a focus on large, stable, dividend-paying companies. Client suitability Index funds are suitable for the investor with a moderate to high-risk profile who is not expecting a steady stream of income. The investor should have a relatively long time horizon since market indexes can vary in the short term, although over the long term there is a general upwards trend.

Canadian Investment Funds Course

www.ifse.ca © 2007

4-15

Commodity Pools Definition Commodity pools are mutual funds that are permitted to use or invest in specified derivatives and physical commodities beyond what is permitted by National Instrument 81-102. These funds are governed by Multilateral Instrument 81-104. In addition, commodity pools must be issued under a long form prospectus rather than the simplified prospectus permitted by National Instrument 81-101, and they must issue financial statements on a quarterly basis, rather than semi-annually. How it works Commodity pools are similar to other mutual funds except they are able to employ alternative trading strategies for their portfolios. Commodity pool managers attempt to increase their rate of return by investing in:

• specified derivatives • physical commodities

Some of the investments that may be found in a commodity pool are commodity futures and forward contracts for grains, meats, metals, energy products, and coffee. In addition, a commodity pool may invest more than 10% of its net assets with any one counterparty in one or more specified derivatives transactions. However, it is still subject to the 10% rule in relation to any securities of any issuers, for example, common shares of a counterparty or issuer. Risk profile Commodity pools can be highly speculative and hence, they are high risk investments. The very nature of derivative and commodity trading can lead to substantial losses. As a result, returns can be extremely volatile. You should review the risk factors outlined in the prospectus before recommending these products to a client. Client suitability These investments are suitable only for sophisticated investors willing to accept the high risk associated with commodity pools. Please be aware that your mutual fund license does not entitle you to sell these products. Contact your compliance department for information on the necessary licensing requirements. Exercise: Growth Funds

Lesson 4: Combination Growth and Income Funds

www.ifse.ca © 2007

4-16

Lesson 4: Combination Growth and Income Funds Welcome to the Combination Growth and Income Funds lesson. In this lesson, you will learn about the different types of combination growth and income funds available to investors. You will learn the financial instruments these funds hold, how they work, and for whom they are suitable. This lesson takes 15 minutes to complete. At the end of this lesson, you will be able to do the following:

• describe how a balanced fund works • describe how an asset allocation fund works

Canadian Investment Funds Course

www.ifse.ca © 2007

4-17

Balanced Funds Definition Balanced funds invest in a combination of cash, bonds, and stocks. How it works Bonds provide income and offer a measure of stability, while common shares provide growth and some dividend income. The fund manager adjusts the mix of bonds and common shares in a balanced fund's portfolio to reflect the changing conditions of financial markets. Most balanced funds are required to hold minimum percentages of each type of investment, according to objectives set out in the fund's prospectus. Usually, there is a range specifying the minimum and maximum limits for each asset category. For example, a fund may be required to hold no less than 30% of its portfolio in either stocks or bonds at any given time. Returns may be made up of interest, dividends, and capital gains. Risk profile Balanced funds are moderate risk investments. Returns from balanced funds are generally higher than those for bond funds but lower than those for equity funds. Client suitability Balanced funds are suitable for investors who match the moderate risk profile, and for investors who want to earn income and realize capital gains. Asset Allocation Funds Definition Unlike other balanced funds, asset allocation funds generally have no restrictions on the asset mix of the portfolio. Therefore, an asset allocation fund could have all of its assets in one type of investment at a particular time or have a mixture of investments. How it works Like balanced funds, managers of asset allocation funds vary the asset mix of the portfolio in response to changing market conditions. However, asset allocation portfolio managers have more freedom to adjust their portfolios. For example, if there is an anticipation that interest rates will decrease in the near future, a manager may decide to invest in equities to take advantage of this trend. A balanced fund manager may only invest in equities up to a maximum, such as 60% of the portfolio. However, an asset allocation manager does not have this restriction and if desired, he or she can invest greater than 60% of the fund's portfolio in equities.

Lesson 4: Combination Growth and Income Funds

www.ifse.ca © 2007

4-18

Risk profile The risk to investors in asset allocation funds varies greatly, depending on the fund's mandate and objectives. Most asset allocation funds would be moderate to high-risk. Client suitability Asset allocation funds are suitable for investors who match the moderate to high-risk profile, and investors who want to earn income and realize capital gains. Exercise: Balanced and Asset Allocation Funds

Canadian Investment Funds Course

www.ifse.ca © 2007

4-19

Lesson 5: Comparing the Funds Welcome to the Comparing the Funds lesson. In this lesson, you will learn about the relationship between volatility, risk, and return. Before providing your client with an investment solution, you need to know how this relationship works so you can match investments to risk comfort levels and return expectations. This lesson takes 10 minutes to complete. At the end of this lesson, you will be able to do the following:

• define and describe risk and volatility as they relate to returns • define and describe risk and volatility as they relate to each other

Lesson 5: Comparing the Funds

www.ifse.ca © 2007

4-20

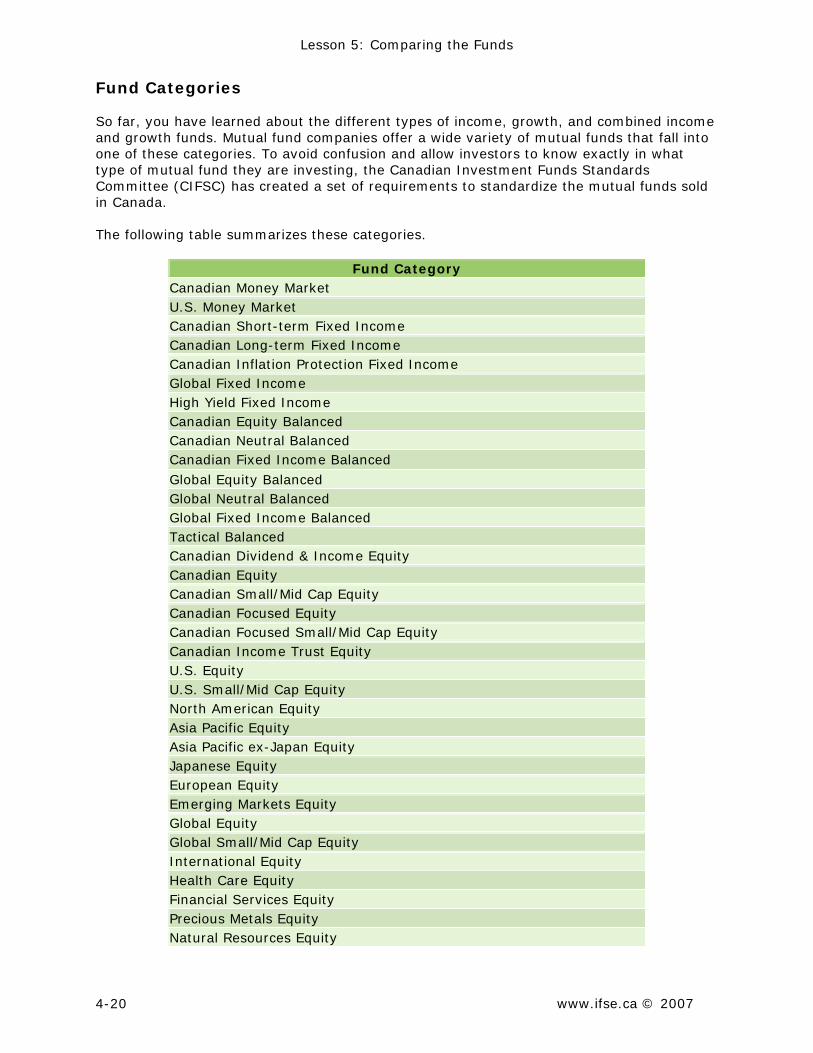

Fund Categories So far, you have learned about the different types of income, growth, and combined income and growth funds. Mutual fund companies offer a wide variety of mutual funds that fall into one of these categories. To avoid confusion and allow investors to know exactly in what type of mutual fund they are investing, the Canadian Investment Funds Standards Committee (CIFSC) has created a set of requirements to standardize the mutual funds sold in Canada. The following table summarizes these categories.

Fund Category Canadian Money Market U.S. Money Market Canadian Short-term Fixed Income Canadian Long-term Fixed Income Canadian Inflation Protection Fixed Income Global Fixed Income High Yield Fixed Income Canadian Equity Balanced Canadian Neutral Balanced Canadian Fixed Income Balanced Global Equity Balanced Global Neutral Balanced Global Fixed Income Balanced Tactical Balanced Canadian Dividend & Income Equity Canadian Equity Canadian Small/Mid Cap Equity Canadian Focused Equity Canadian Focused Small/Mid Cap Equity Canadian Income Trust Equity U.S. Equity U.S. Small/Mid Cap Equity North American Equity Asia Pacific Equity Asia Pacific ex-Japan Equity Japanese Equity European Equity Emerging Markets Equity Global Equity Global Small/Mid Cap Equity International Equity Health Care Equity Financial Services Equity Precious Metals Equity Natural Resources Equity

Canadian Investment Funds Course

www.ifse.ca © 2007

4-21

Fund Category Science & Technology Equity Real Estate Equity Retail Venture Capital Miscellaneous Alternative Strategies

Volatility, Risk, and Return To understand how mutual funds are categorized and how individual funds fit within those categories, it is important to understand how the concepts of risk and volatility apply to mutual funds.

To investors, risk is the chance that they are going to lose some or all of their investment. Volatility is the degree to which the price of an investment fluctuates, or increases and decreases over a period of time. Volatility indicates the amount of risk. The higher the volatility, the higher the risk, and the lower the volatility, the lower the risk. For example, if a fund drops 50% in value, it would have to increase by 100% before it returns to its starting point. These are some of the factors that cause investment prices to fluctuate:

• changes in interest rates • political upheaval • shifts in market expectations • changes in the credit rating of borrowers • time horizon

Return is the amount of money you earn on investments. Table: How the Funds Compare So far, you have reviewed the most common types of mutual funds, the types of products they hold, their characteristics, and their level of risk. This job aid provides a comparison of the most common funds. It will help you as you continue this lesson, as well as on the job.

Lesson 5: Comparing the Funds

www.ifse.ca © 2007

4-22

Rate by Risk The following is a generalization of the types of funds and their associated risks. The risk level of a particular fund will be dependent upon the fund manager and the assets within the fund itself.

Exercise: Influencing Factors

Canadian Investment Funds Course

www.ifse.ca © 2007

4-23

Review Let's look at the concepts covered in this unit:

• Three Categories of Funds • Income Funds • Growth Funds • Combination Growth and Income Funds • Comparing the Funds

You now have a good understanding of the types of mutual funds offered, their characteristics, and their level of risk. At this point in the course, you should be able to start to identify the best type of mutual fund to suit your client's objectives and attitude to risk. Click Assessment on the table of contents to test your understanding. Assessment Now that you have completed Unit 4: Types of Mutual Funds, you are ready to assess your knowledge. You will be asked a series of 20 questions. When you have finished answering the questions, click Submit to see your score. When you are ready to start, click the Go to Assessment link.