Embed Size (px)

Citation preview

U.S. Navy Shipbuilding and Ship Procurement

Presented at the Conference on Shipbuilding and Ship Procurement Strategy for Canada

November, 2009

2

What is RAND?

• An independent, non-profit research institution

• A provider of objective analysis and effective solutions that address the challenges facing public and private sectors around the world

• A center for education and training in policy analysis

• Neither a university nor a management consultancy — but with the capabilities of both

3

Our Research Is TypicallyCharacterized by . . .

Issues that involve:

• Competing objectives and perspectives

• Intersection of public/ private interests

• "Messy" data, major uncertainties

• Implications for the future

An analytic approach that is:

• Integrative, collaborative, and multidisciplinary

• Empirical, with technical depth and methodological rigor

• Innovative, but informedby past findings

• Buttressed by demanding standards of quality and objectivity

RAND strives to build long-termrelationships with its clients

4

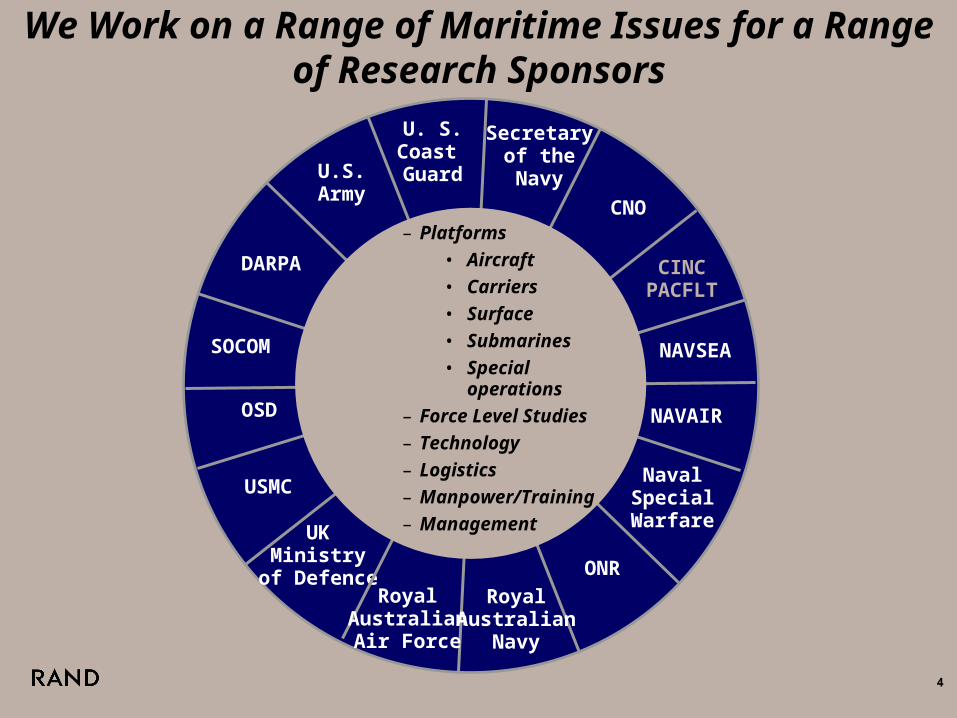

We Work on a Range of Maritime Issues for a Range of Research Sponsors

CNO

CINCPACFLT

USMC

OSD NAVAIR

ONR

NavalSpecialWarfare

SOCOM

DARPA

U.S.Army

U. S. Coast Guard

UKMinistry

of Defence

NAVSEA

Secretaryof theNavy

RoyalAustralianAir Force

RoyalAustralian

Navy

– Platforms

• Aircraft

• Carriers

• Surface

• Submarines

• Special operations

– Force Level Studies

– Technology

– Logistics

– Manpower/Training

– Management

5

Results of Our Research Are Typically Published

www.rand.org

6

Topics for Discussion

• U.S. Navy Ship Procurement Plans

• U.S. Shipbuilding Industrial Base

• Issues in U.S. Navy Shipbuilding

7

Navy Has Specific Goals in Ship Programs

• Ship designs that provide greater attention to life cycle costs

• Given a design, lower procurement costs

• Given a design, faster delivery

• Reliability in design, cost, and schedule goals

• Responsiveness to unexpected, emerging requirements

Current acquisition strategies fall short in achieving these goals

8

Any Acquisition Strategy Must Consider the Goals of Other Participants

• Shipbuilders– Enhanced cash flow– High return on investment– Order stability and predictability– Above average profits

• Congress– Stability in local jobs– No long-term commitments– Perceived contribution to the defense mission

of TOA committed to ships

It may be difficult to find acquisition strategies that are agreeable to all three parties

9

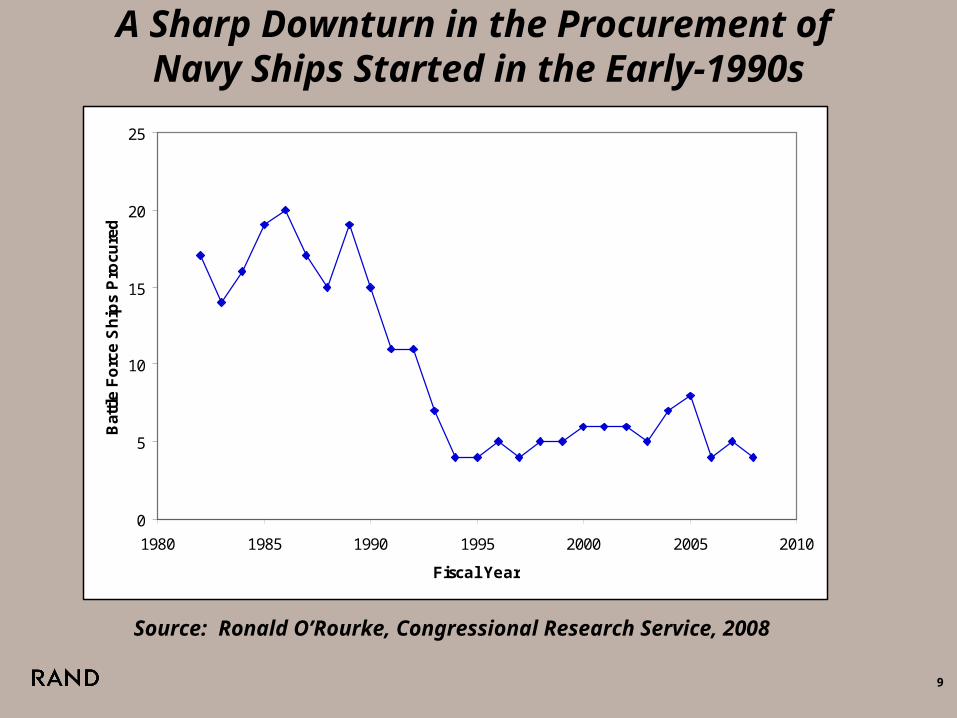

A Sharp Downturn in the Procurement of Navy Ships Started in the Early-1990s

Source: Ronald O’Rourke, Congressional Research Service, 2008

0

5

10

15

20

25

1980 1985 1990 1995 2000 2005 2010

Fiscal Year

Bat

tle

Fo

rce

Sh

ips

Pro

cure

d

10

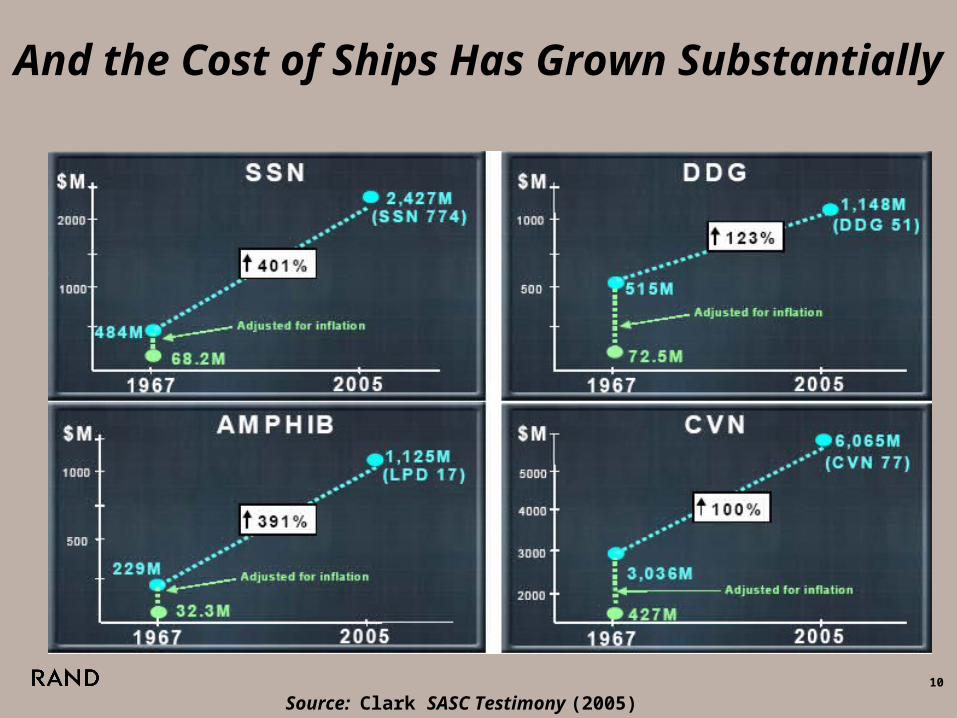

And the Cost of Ships Has Grown Substantially

Source: Clark SASC Testimony (2005)

11

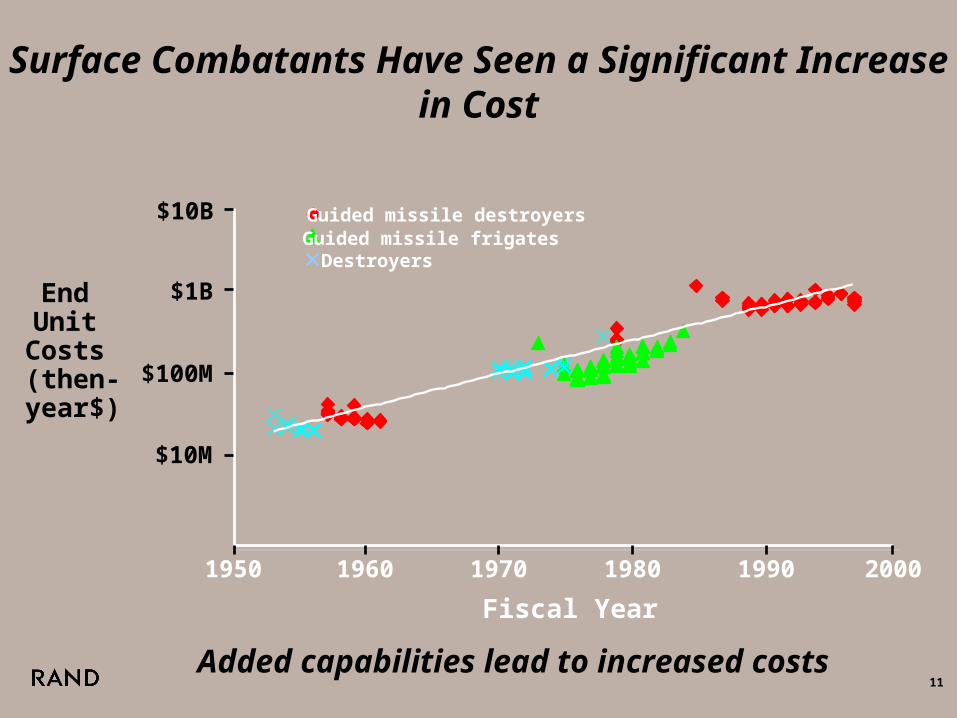

Surface Combatants Have Seen a Significant Increase in Cost

Added capabilities lead to increased costs

$10M

$100M

$1B

$10B

End Unit

Costs (then-year$)

1950 1960 1970 1980 1990 2000

Fiscal Year

Guided missile destroyersGuided missile frigatesDestroyers

12

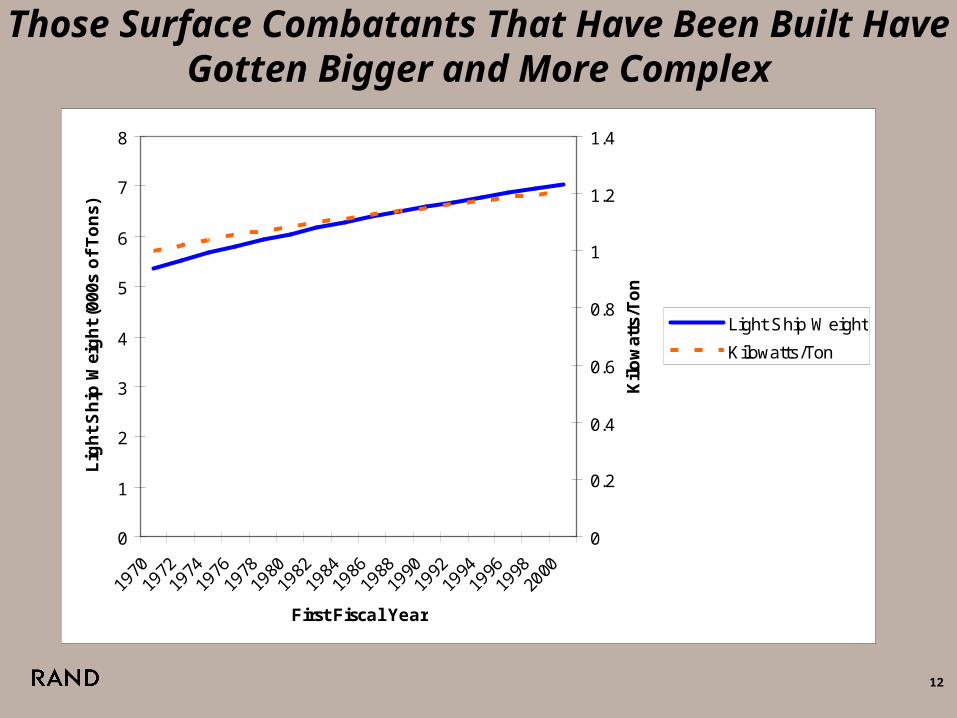

Those Surface Combatants That Have Been Built Have Gotten Bigger and More Complex

0

1

2

3

4

5

6

7

8

First Fiscal Year

Lig

ht

Sh

ip W

eig

ht

(000

s o

f T

on

s)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Kil

ow

atts

/To

n

Light Ship Weight

Kilowatts/Ton

13

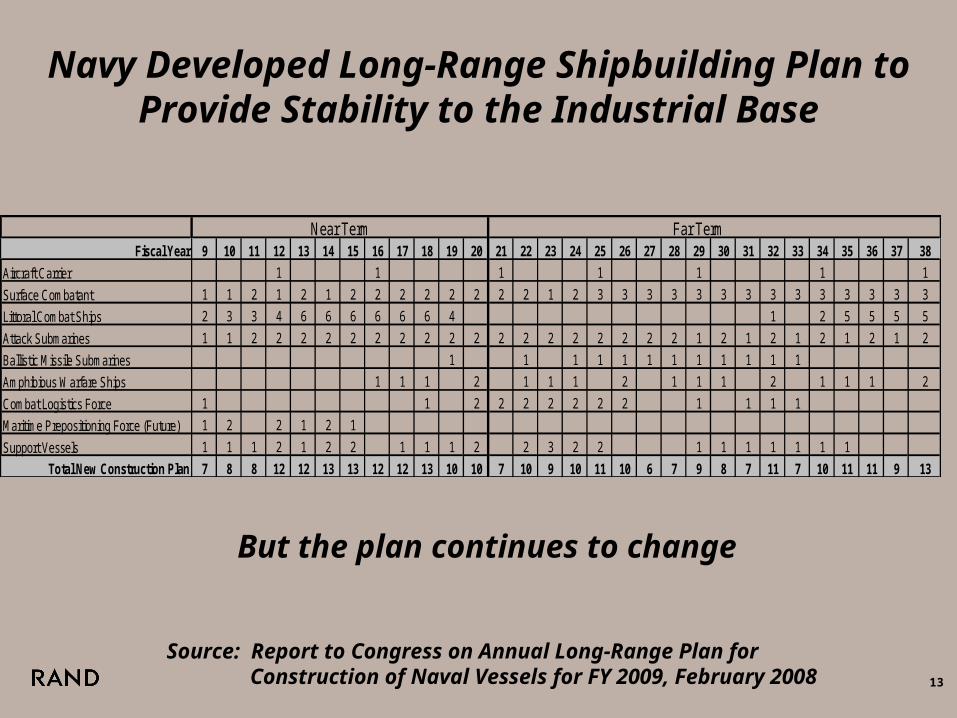

Navy Developed Long-Range Shipbuilding Plan to Provide Stability to the Industrial Base

Fiscal Year 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38

Aircraft Carrier 1 1 1 1 1 1 1

Surface Combatant 1 1 2 1 2 1 2 2 2 2 2 2 2 2 1 2 3 3 3 3 3 3 3 3 3 3 3 3 3 3

Littoral Combat Ships 2 3 3 4 6 6 6 6 6 6 4 1 2 5 5 5 5

Attack Submarines 1 1 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 1 2 1 2 1 2 1 2 1 2

Ballistic Missile Submarines 1 1 1 1 1 1 1 1 1 1 1 1

Amphibious Warfare Ships 1 1 1 2 1 1 1 2 1 1 1 2 1 1 1 2

Combat Logistics Force 1 1 2 2 2 2 2 2 2 1 1 1 1

Maritime Prepositioning Force (Future) 1 2 2 1 2 1

Support Vessels 1 1 1 2 1 2 2 1 1 1 2 2 3 2 2 1 1 1 1 1 1 1

Total New Construction Plan 7 8 8 12 12 13 13 12 12 13 10 10 7 10 9 10 11 10 6 7 9 8 7 11 7 10 11 11 9 13

Far TermNear Term

Source: Report to Congress on Annual Long-Range Plan for Construction of Naval Vessels for FY 2009, February 2008

But the plan continues to change

14

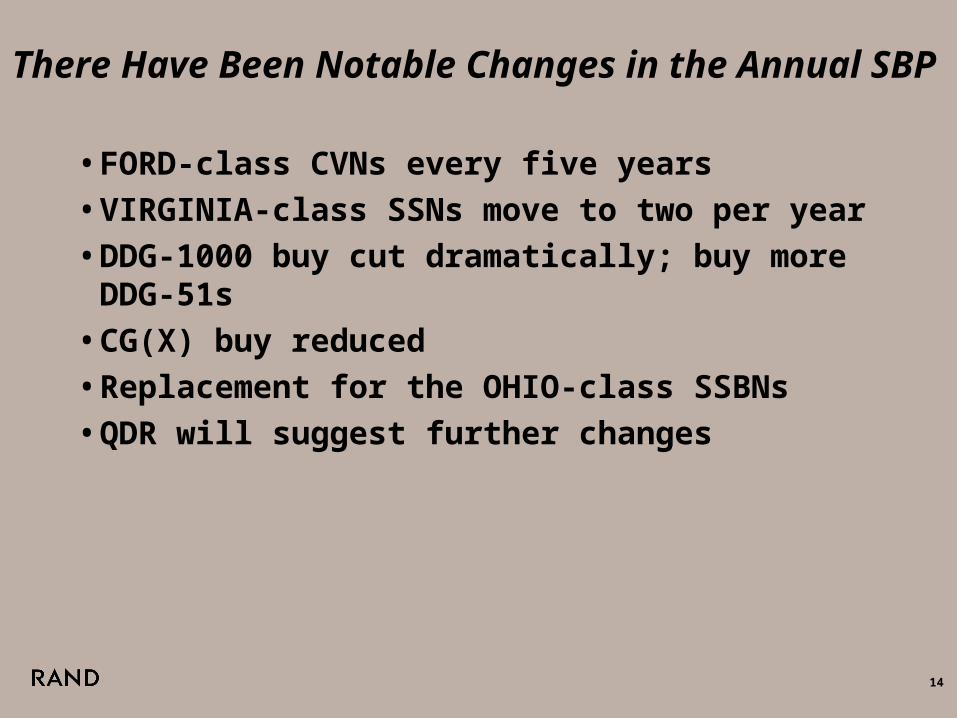

There Have Been Notable Changes in the Annual SBP

• FORD-class CVNs every five years

• VIRGINIA-class SSNs move to two per year

• DDG-1000 buy cut dramatically; buy more DDG-51s

• CG(X) buy reduced

• Replacement for the OHIO-class SSBNs

• QDR will suggest further changes

15

Topics for Discussion

• U.S. Navy Ship Procurement Plans

• U.S. Shipbuilding Industrial Base

• Issues in U.S. Navy Shipbuilding

16

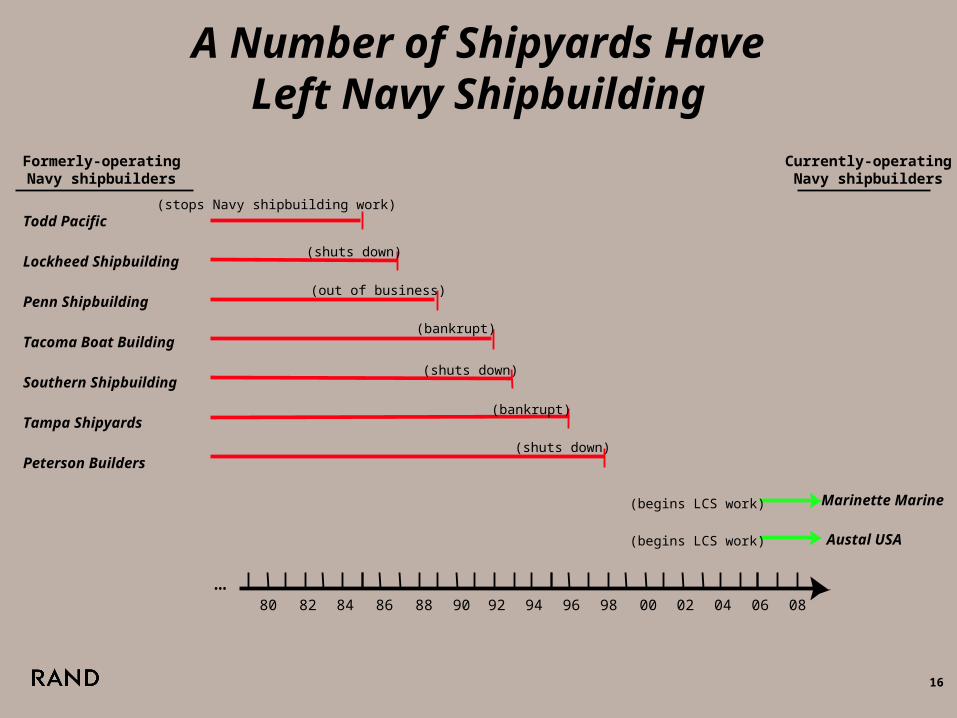

A Number of Shipyards HaveLeft Navy Shipbuilding

96 98 00 02 04 06 088280 84 86 88 90 92 94

…

Todd Pacific

Lockheed Shipbuilding

Penn Shipbuilding

Tacoma Boat Building

Southern Shipbuilding

Tampa Shipyards

Peterson Builders

Marinette Marine

Austal USA

(stops Navy shipbuilding work)

(shuts down)

(out of business)

(bankrupt)

(shuts down)

(bankrupt)

(shuts down)

(begins LCS work)

(begins LCS work)

Currently-operatingNavy shipbuilders

Formerly-operatingNavy shipbuilders

17

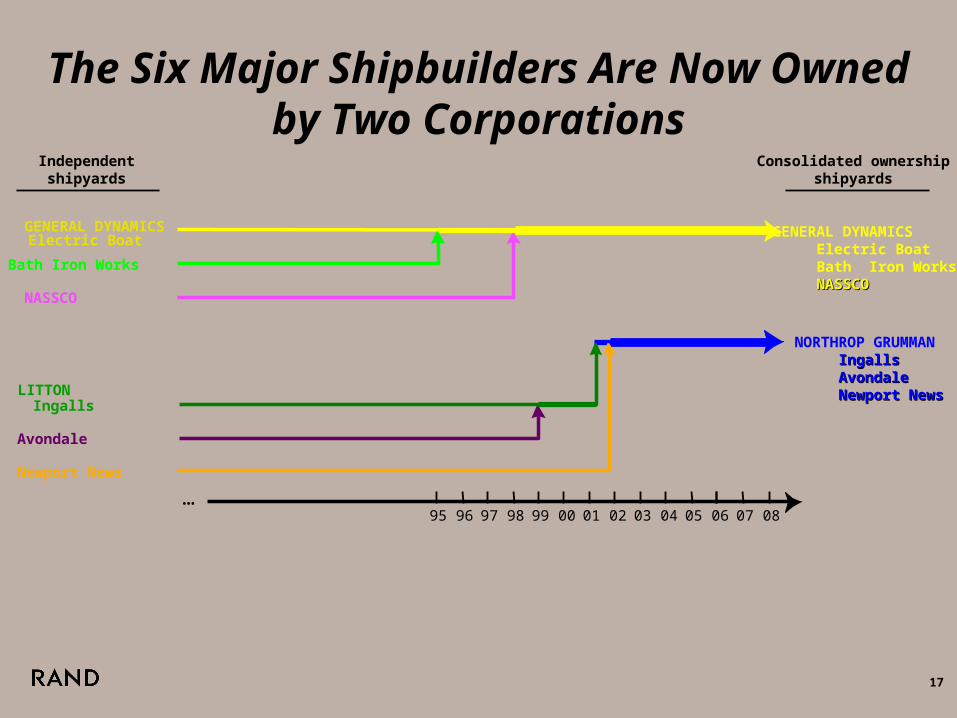

The Six Major Shipbuilders Are Now Ownedby Two Corporations

GENERAL DYNAMICSElectric Boat

Bath Iron Works

NASSCO

95 96 97 98 00 0199 02 03 04 05 06 07 08

GENERAL DYNAMICS Electric Boat Bath Iron Works NASSCONASSCO

LITTONIngalls

Avondale

Newport News

NORTHROP GRUMMAN IngallsIngalls AvondaleAvondale Newport NewsNewport News

…

Consolidated ownershipshipyards

Independentshipyards

18

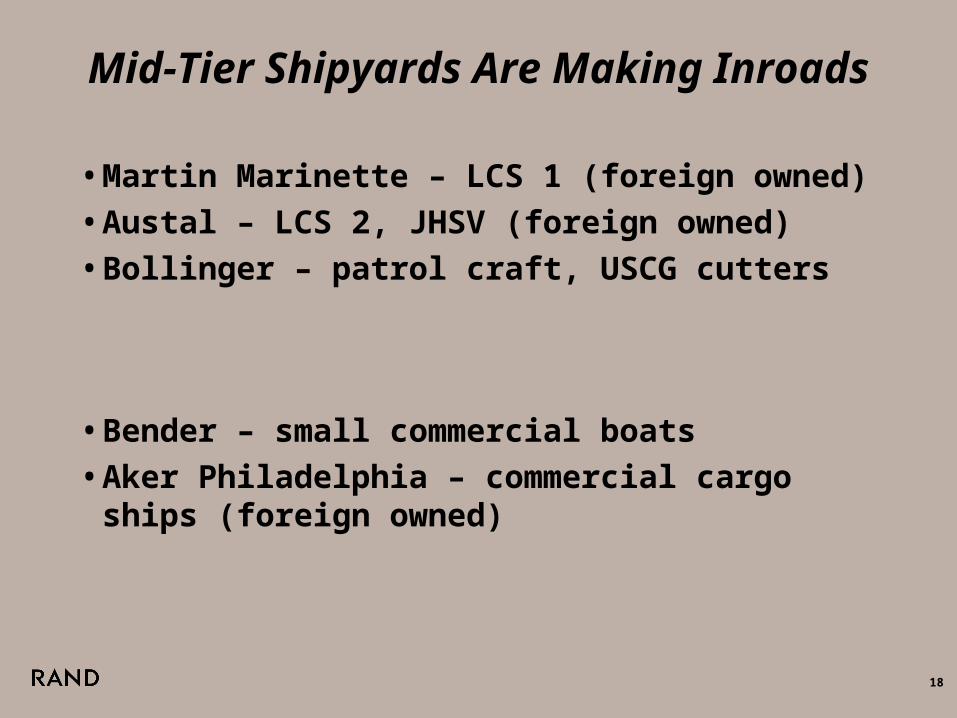

Mid-Tier Shipyards Are Making Inroads

• Martin Marinette – LCS 1 (foreign owned)

• Austal – LCS 2, JHSV (foreign owned)

• Bollinger – patrol craft, USCG cutters

• Bender – small commercial boats

• Aker Philadelphia – commercial cargo ships (foreign owned)

19

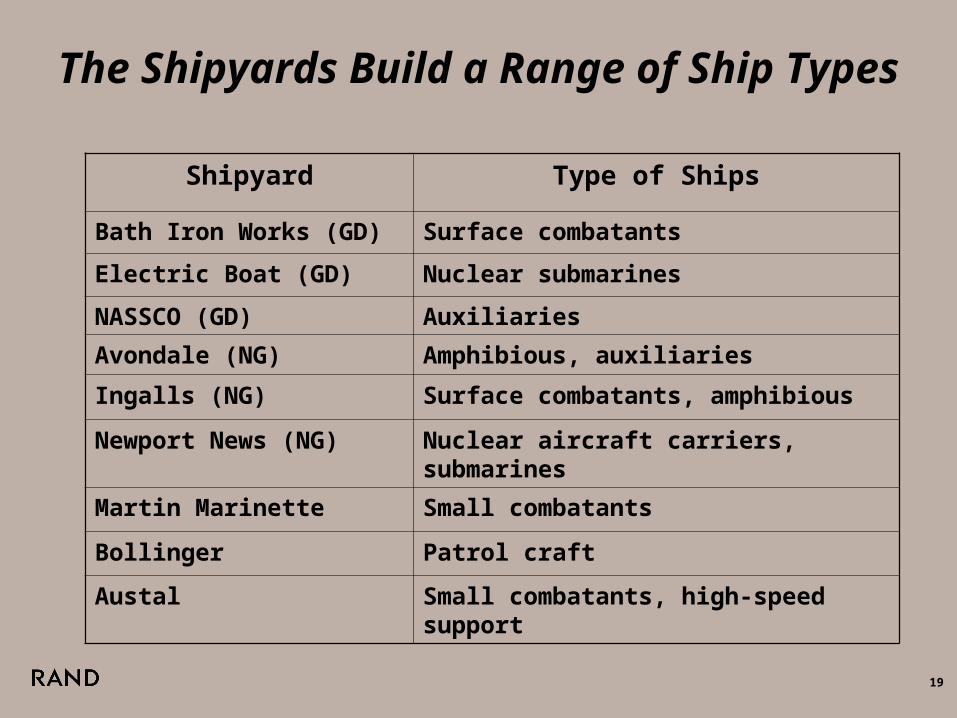

The Shipyards Build a Range of Ship Types

Shipyard Type of Ships

Bath Iron Works (GD) Surface combatants

Electric Boat (GD) Nuclear submarines

NASSCO (GD) Auxiliaries

Avondale (NG) Amphibious, auxiliaries

Ingalls (NG) Surface combatants, amphibious

Newport News (NG) Nuclear aircraft carriers, submarines

Martin Marinette Small combatants

Bollinger Patrol craft

Austal Small combatants, high-speed support

20

Topics for Discussion

• U.S. Navy Ship Procurement Plans

• U.S. Shipbuilding Industrial Base

• Issues in U.S. Navy Shipbuilding

21

Some Questions Facing U.S. Navy Ship Procurement

• Is the future shipbuilding plan affordable?– SCN budget is flat while future calls for more new ships– Many new designs, each with cost and schedule risk

• How can certain design skills be sustained?– Larger gaps in new program starts– Desire to reuse designs to reduce costs

• What will be the impact of new missions, such as BDM?– Choice between modifying a current platform or

designing a new platform– Uncertainty on the number of ships needed

• When and how should competition be used?– Sustaining the industrial base requires allocation of work– Congress can constrain the use of competition

22

Shipbuilder Competition Is Peculiar

• Since Navy requirements typically evolve, the shipbuilder probably believes it will not be bound by initial promises

– Shipbuilders generally become monopolists when competition is over and the Navy wants specification changes

– Even when a ship is built by two shipbuilders, it is probably not credible that workload will be removed entirely from a shipyard

• A shipbuilder’s motivation is to get the work through optimistic bidding

– Even “fixed-price” contracts are effectively cost-based• Changing Navy specifications are always an “out”• The Navy does not want the shipbuilder to default