Embed Size (px)

Citation preview

U.S. Regulatory/Compliance Orientation for

International Bankers

Anti-Money Laundering and U.S. ComplianceConference of State Bank Supervisors & Institute of International Bankers

New York City, New York

July 28, 2009

Carol R. Van Cleef

U.S. Regulatory/Compliance Orientation for International Bankers2

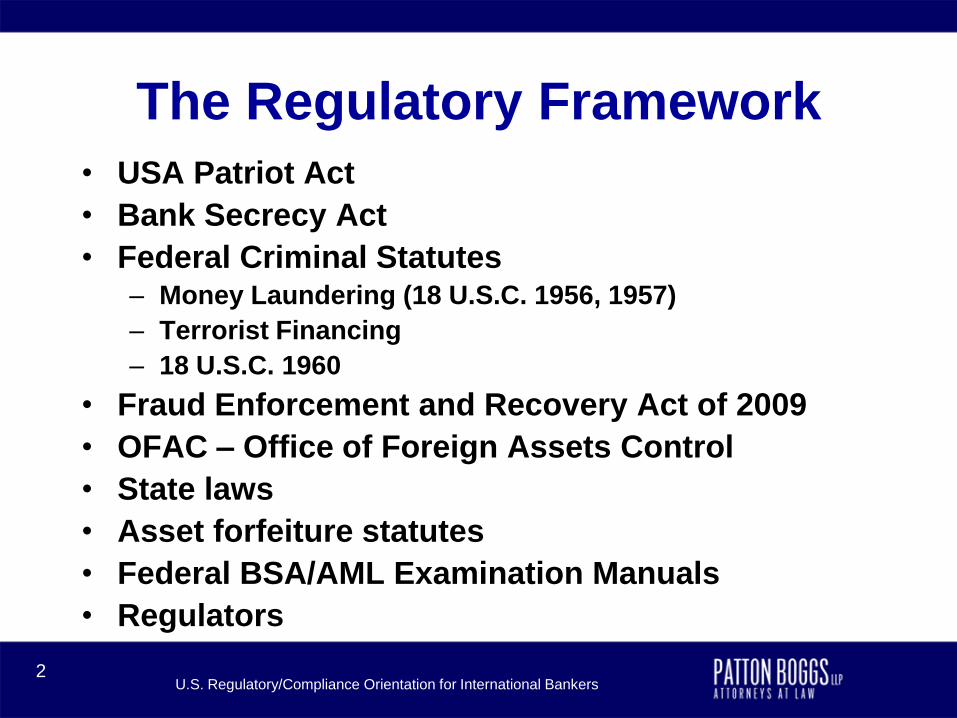

The Regulatory Framework

• USA Patriot Act

• Bank Secrecy Act

• Federal Criminal Statutes – Money Laundering (18 U.S.C. 1956, 1957)

– Terrorist Financing

– 18 U.S.C. 1960

• Fraud Enforcement and Recovery Act of 2009

• OFAC – Office of Foreign Assets Control

• State laws

• Asset forfeiture statutes

• Federal BSA/AML Examination Manuals

• Regulators

U.S. Regulatory/Compliance Orientation for International Bankers3

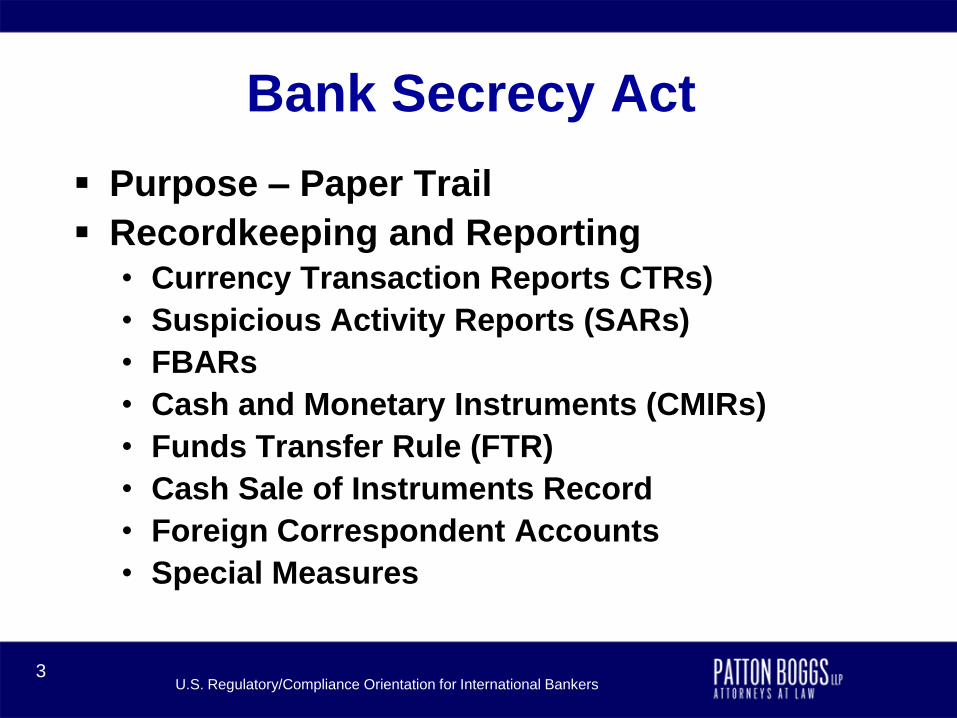

Bank Secrecy Act

Purpose – Paper Trail

Recordkeeping and Reporting• Currency Transaction Reports CTRs)

• Suspicious Activity Reports (SARs)

• FBARs

• Cash and Monetary Instruments (CMIRs)

• Funds Transfer Rule (FTR)

• Cash Sale of Instruments Record

• Foreign Correspondent Accounts

• Special Measures

U.S. Regulatory/Compliance Orientation for International Bankers4

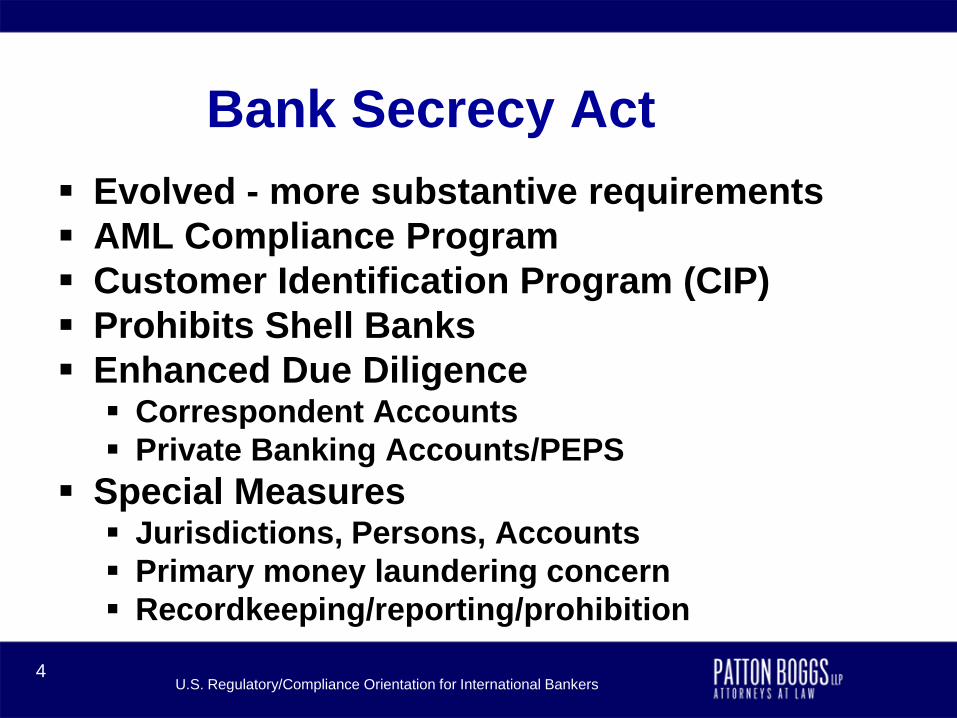

Bank Secrecy Act

Evolved - more substantive requirements

AML Compliance Program

Customer Identification Program (CIP)

Prohibits Shell Banks

Enhanced Due Diligence Correspondent Accounts

Private Banking Accounts/PEPS

Special Measures Jurisdictions, Persons, Accounts

Primary money laundering concern

Recordkeeping/reporting/prohibition

U.S. Regulatory/Compliance Orientation for International Bankers5

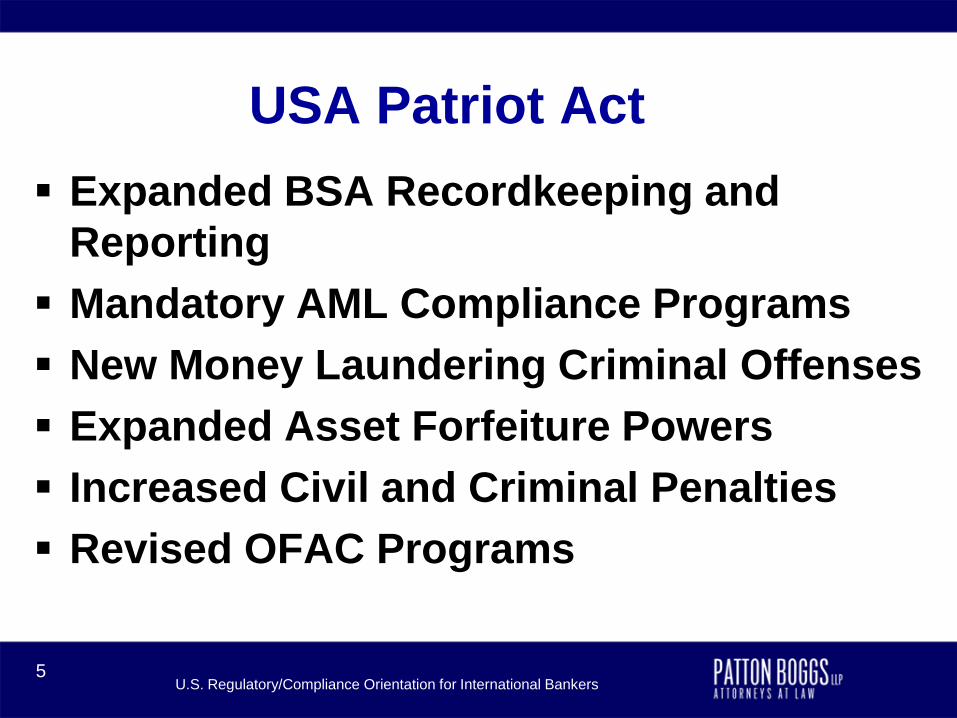

USA Patriot Act

Expanded BSA Recordkeeping and

Reporting

Mandatory AML Compliance Programs

New Money Laundering Criminal Offenses

Expanded Asset Forfeiture Powers

Increased Civil and Criminal Penalties

Revised OFAC Programs

U.S. Regulatory/Compliance Orientation for International Bankers6

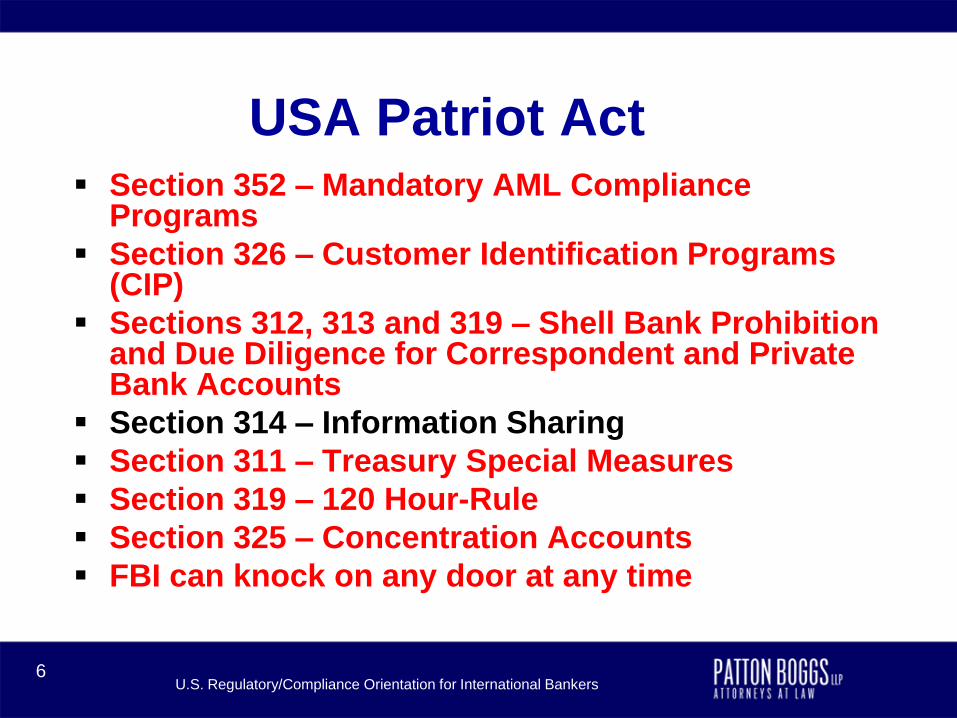

USA Patriot Act Section 352 – Mandatory AML Compliance

Programs

Section 326 – Customer Identification Programs (CIP)

Sections 312, 313 and 319 – Shell Bank Prohibition and Due Diligence for Correspondent and Private Bank Accounts

Section 314 – Information Sharing

Section 311 – Treasury Special Measures

Section 319 – 120 Hour-Rule

Section 325 – Concentration Accounts

FBI can knock on any door at any time

U.S. Regulatory/Compliance Orientation for International Bankers7

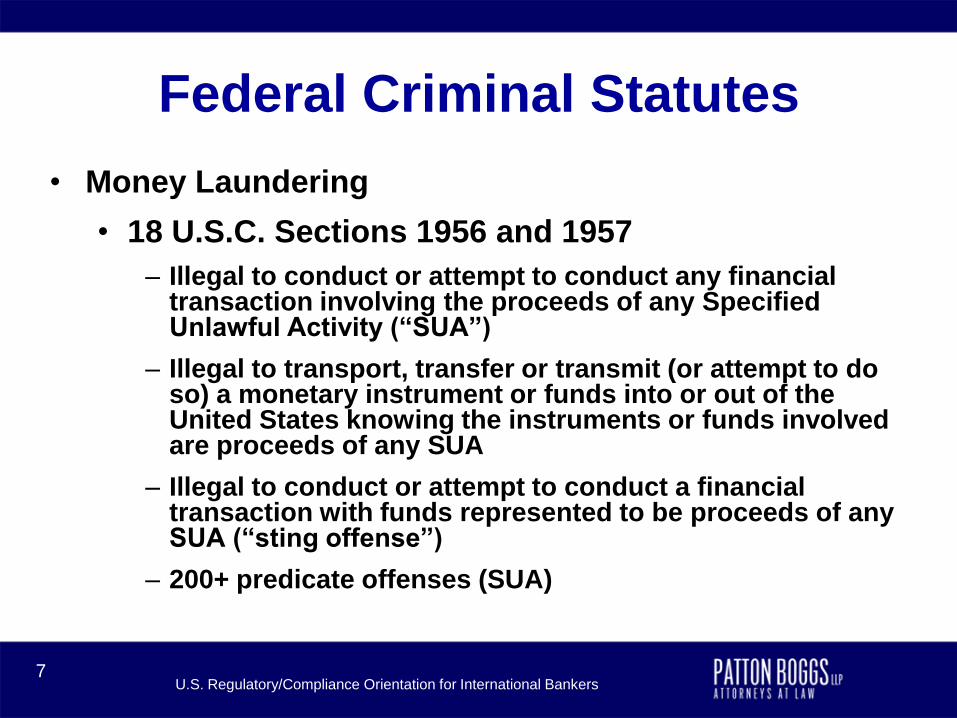

Federal Criminal Statutes

• Money Laundering

• 18 U.S.C. Sections 1956 and 1957

– Illegal to conduct or attempt to conduct any financial transaction involving the proceeds of any Specified Unlawful Activity (“SUA”)

– Illegal to transport, transfer or transmit (or attempt to do so) a monetary instrument or funds into or out of the United States knowing the instruments or funds involved are proceeds of any SUA

– Illegal to conduct or attempt to conduct a financial transaction with funds represented to be proceeds of any SUA (“sting offense”)

– 200+ predicate offenses (SUA)

U.S. Regulatory/Compliance Orientation for International Bankers8

Federal Criminal Statutes

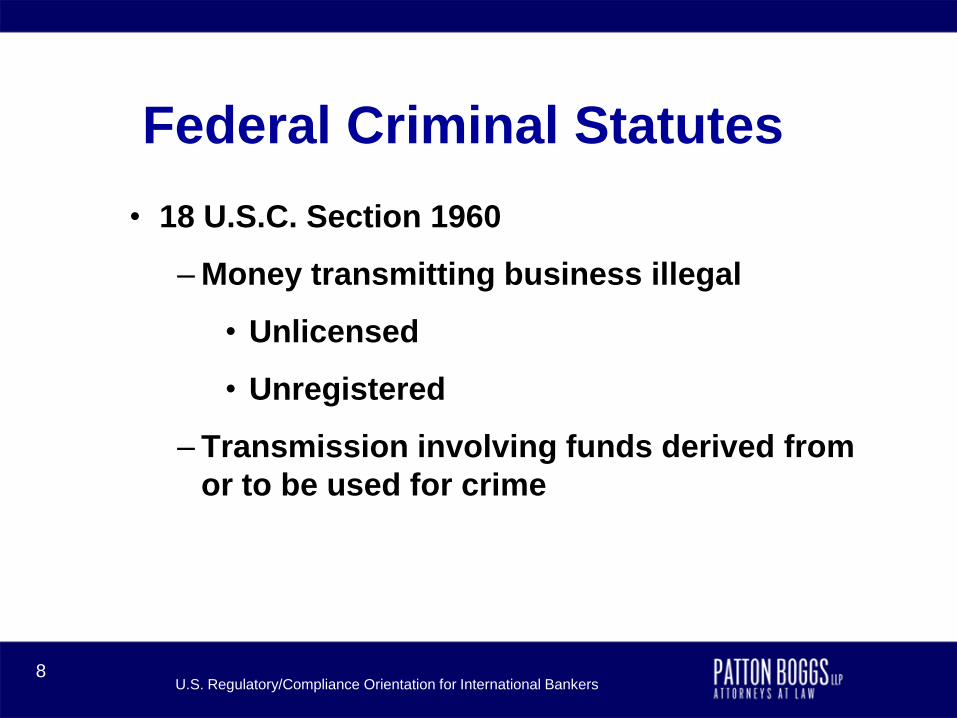

• 18 U.S.C. Section 1960

– Money transmitting business illegal

• Unlicensed

• Unregistered

– Transmission involving funds derived from

or to be used for crime

U.S. Regulatory/Compliance Orientation for International Bankers9

Federal Criminal Statutes

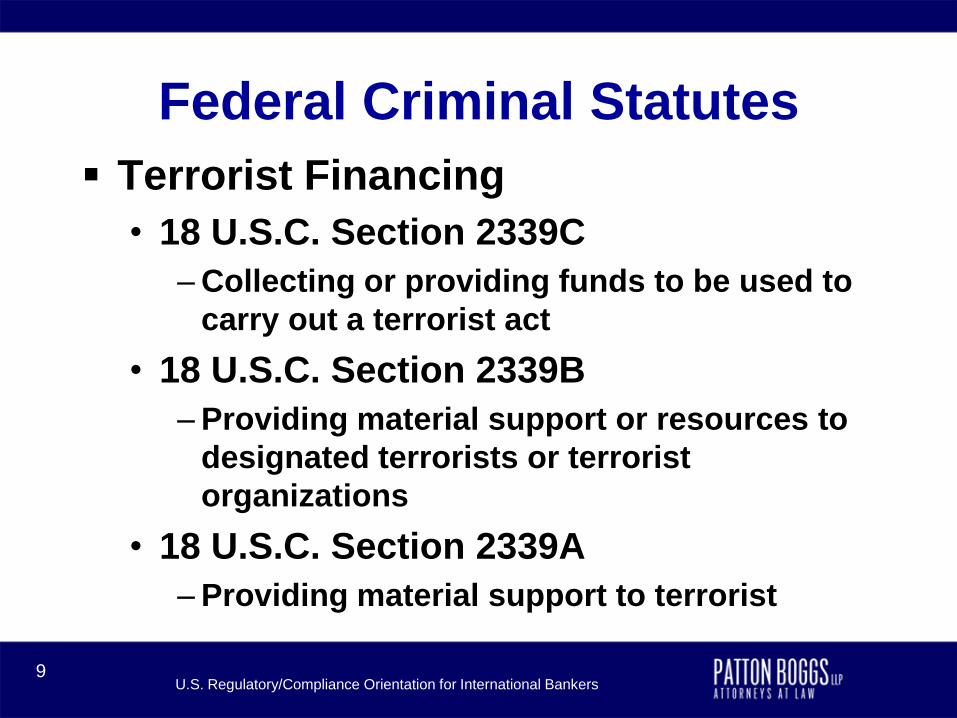

Terrorist Financing

• 18 U.S.C. Section 2339C

– Collecting or providing funds to be used to

carry out a terrorist act

• 18 U.S.C. Section 2339B

– Providing material support or resources to

designated terrorists or terrorist

organizations

• 18 U.S.C. Section 2339A

– Providing material support to terrorist

U.S. Regulatory/Compliance Orientation for International Bankers10

Fraud Enforcement and Recovery

Act of 2009 (FERA)• Mortgage lending business now financial

institution in criminal code– Defined as both financing and refinancing debt

secured by interest in real estate

– Includes subsidiaries

– Affects interstate or foreign commerce

• False statements in applications include those of mortgage brokers and agents of MLBs

• Broadens criminal provisions to include TARP funds and other stimulus, recovery or rescue funding

U.S. Regulatory/Compliance Orientation for International Bankers11

Fraud Enforcement and Recovery

Act of 2009 (FERA)• Proceeds of criminal activity = property derived

from or obtained or retained through unlawful activity

• Sense of Congress on limited use of 18 U.S.C 1956 and 1957

• Additional funding to pursue financial crime– Includes mortgage, securities and commodities and

financial institution fraud

– Also frauds related to federal assistance and relief programs

• False Claims Act

• Financial Crisis Inquiry Commission– Examine causes of current financial and economic crisis

– Criminal referrals

a

U.S. Regulatory/Compliance Orientation for International Bankers12

Office of Foreign Assets Control

Within U.S. Department of the Treasury

Administers 29+ programs

Foreign policy and national security

objectives

List of Specifically Designated Nationals

and Blocked Persons (SDN)

And much more…

U.S. Regulatory/Compliance Orientation for International Bankers13

State Laws

Criminal Money Laundering

BSA

• Incorporated by reference

• Look-alike

• File BSA reports

OFAC-like

U.S. Regulatory/Compliance Orientation for International Bankers14

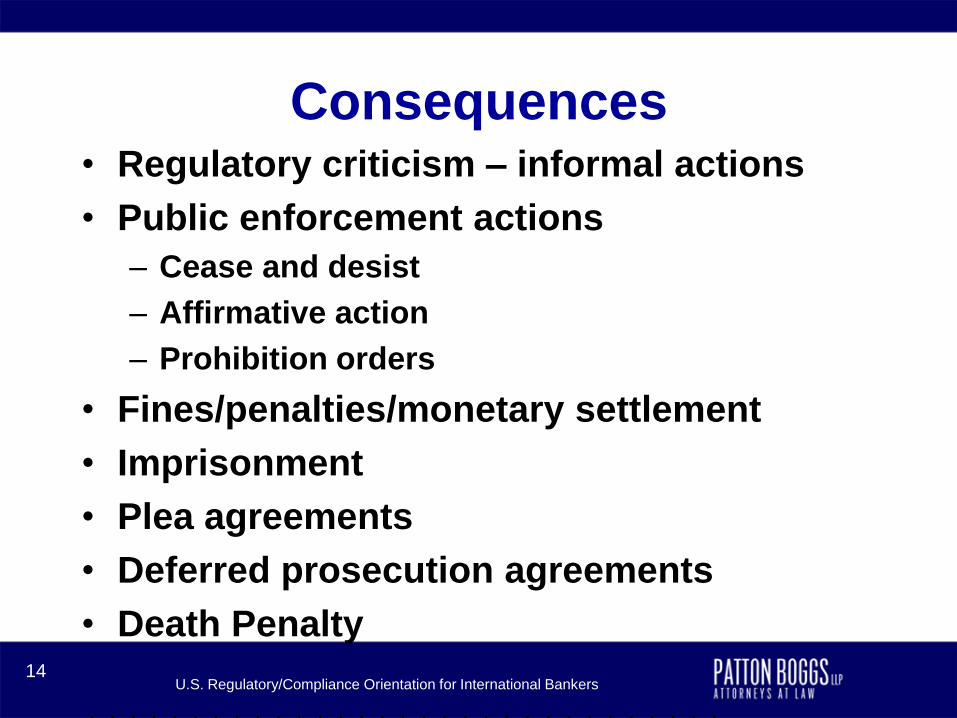

Consequences• Regulatory criticism – informal actions

• Public enforcement actions

– Cease and desist

– Affirmative action

– Prohibition orders

• Fines/penalties/monetary settlement

• Imprisonment

• Plea agreements

• Deferred prosecution agreements

• Death Penalty

$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$$

U.S. Regulatory/Compliance Orientation for International Bankers15

Someone is Always Watching

• Federal and state bank regulators

• Foreign regulatory community

• Law Enforcement

– Federal, State and Local AND Foreign

– FBI, ICE, Secret Service, DEA

• Intelligence community–US and Foreign

• Prosecutors – federal, state, local

• Federal Trade Commission

• Criminals

U.S. Regulatory/Compliance Orientation for International Bankers16

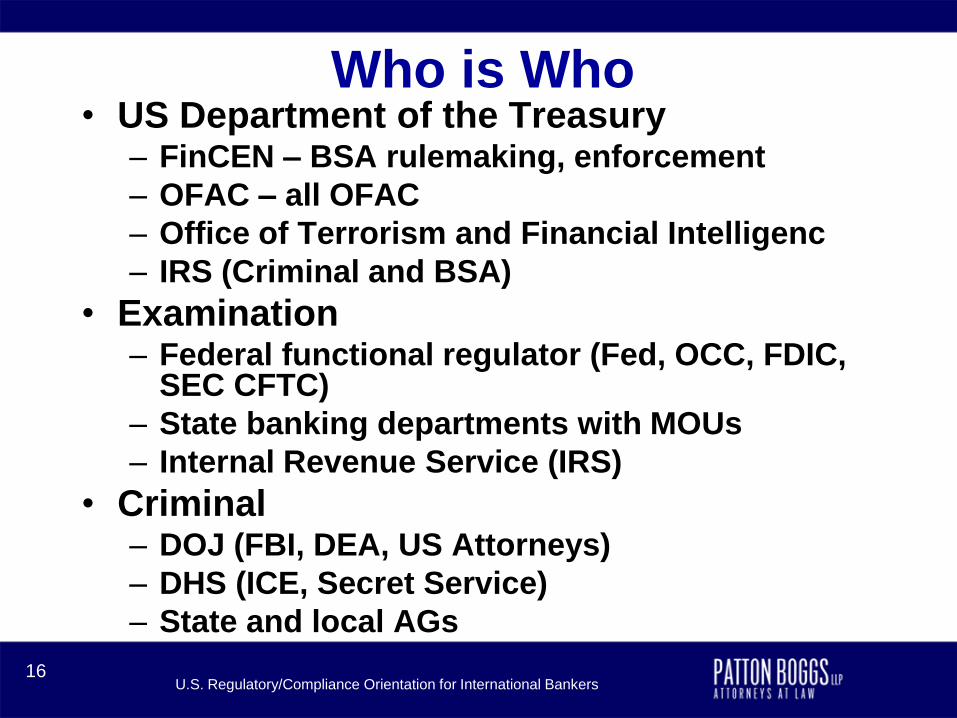

Who is Who• US Department of the Treasury

– FinCEN – BSA rulemaking, enforcement

– OFAC – all OFAC

– Office of Terrorism and Financial Intelligenc

– IRS (Criminal and BSA)

• Examination– Federal functional regulator (Fed, OCC, FDIC,

SEC CFTC)

– State banking departments with MOUs

– Internal Revenue Service (IRS)

• Criminal– DOJ (FBI, DEA, US Attorneys)

– DHS (ICE, Secret Service)

– State and local AGs

U.S. Regulatory/Compliance Orientation for International Bankers17

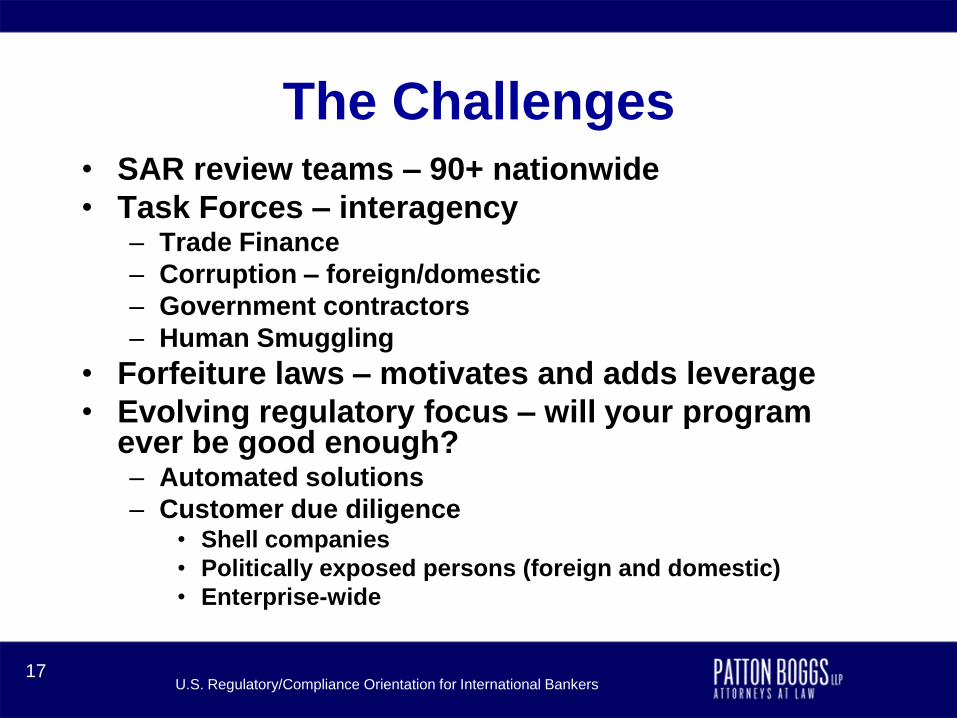

The Challenges• SAR review teams – 90+ nationwide

• Task Forces – interagency– Trade Finance

– Corruption – foreign/domestic

– Government contractors

– Human Smuggling

• Forfeiture laws – motivates and adds leverage

• Evolving regulatory focus – will your program ever be good enough?– Automated solutions

– Customer due diligence• Shell companies

• Politically exposed persons (foreign and domestic)

• Enterprise-wide

U.S. Regulatory/Compliance Orientation for International Bankers18

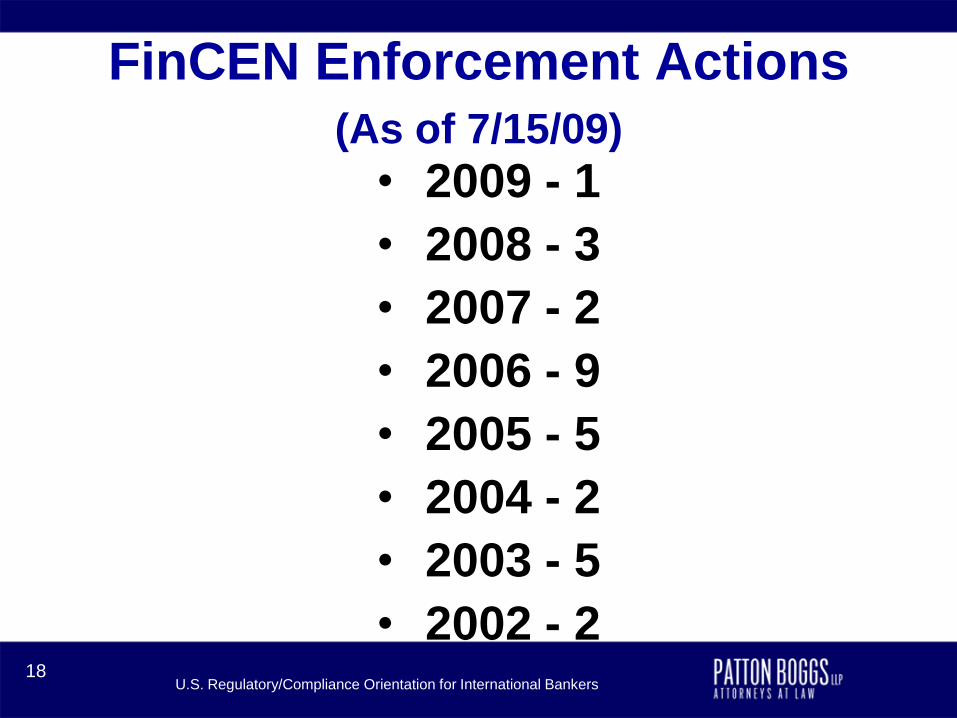

FinCEN Enforcement Actions

(As of 7/15/09)

• 2009 - 1

• 2008 - 3

• 2007 - 2

• 2006 - 9

• 2005 - 5

• 2004 - 2

• 2003 - 5

• 2002 - 2

U.S. Regulatory/Compliance Orientation for International Bankers19

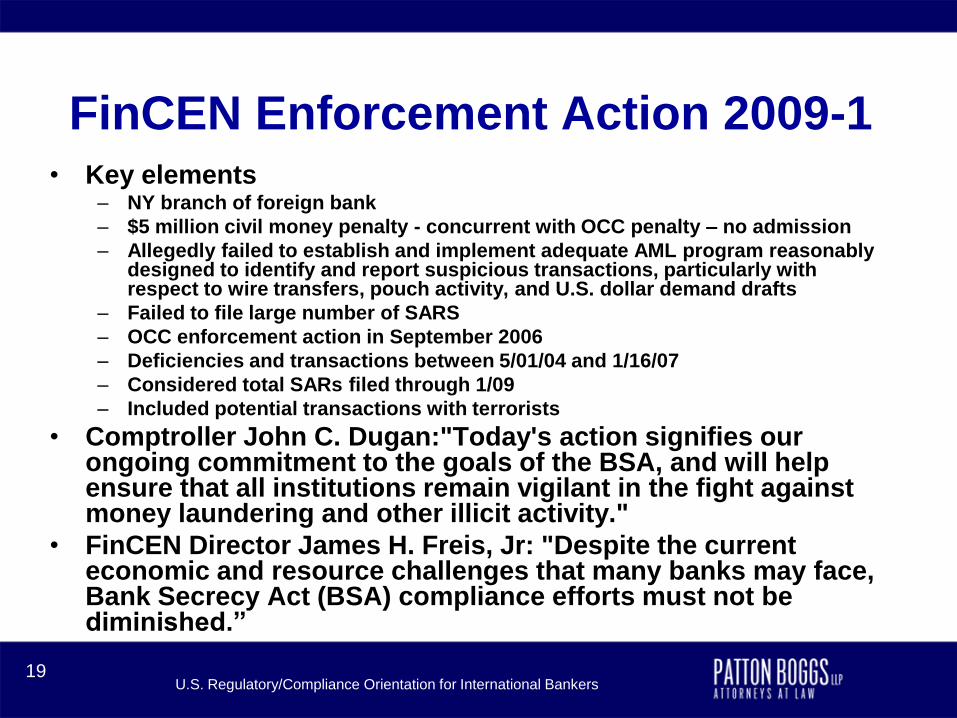

FinCEN Enforcement Action 2009-1• Key elements

– NY branch of foreign bank

– $5 million civil money penalty - concurrent with OCC penalty – no admission

– Allegedly failed to establish and implement adequate AML program reasonably designed to identify and report suspicious transactions, particularly with respect to wire transfers, pouch activity, and U.S. dollar demand drafts

– Failed to file large number of SARS

– OCC enforcement action in September 2006

– Deficiencies and transactions between 5/01/04 and 1/16/07

– Considered total SARs filed through 1/09

– Included potential transactions with terrorists

• Comptroller John C. Dugan:"Today's action signifies our ongoing commitment to the goals of the BSA, and will help ensure that all institutions remain vigilant in the fight against money laundering and other illicit activity."

• FinCEN Director James H. Freis, Jr: "Despite the current economic and resource challenges that many banks may face, Bank Secrecy Act (BSA) compliance efforts must not be diminished.”

U.S. Regulatory/Compliance Orientation for International Bankers20

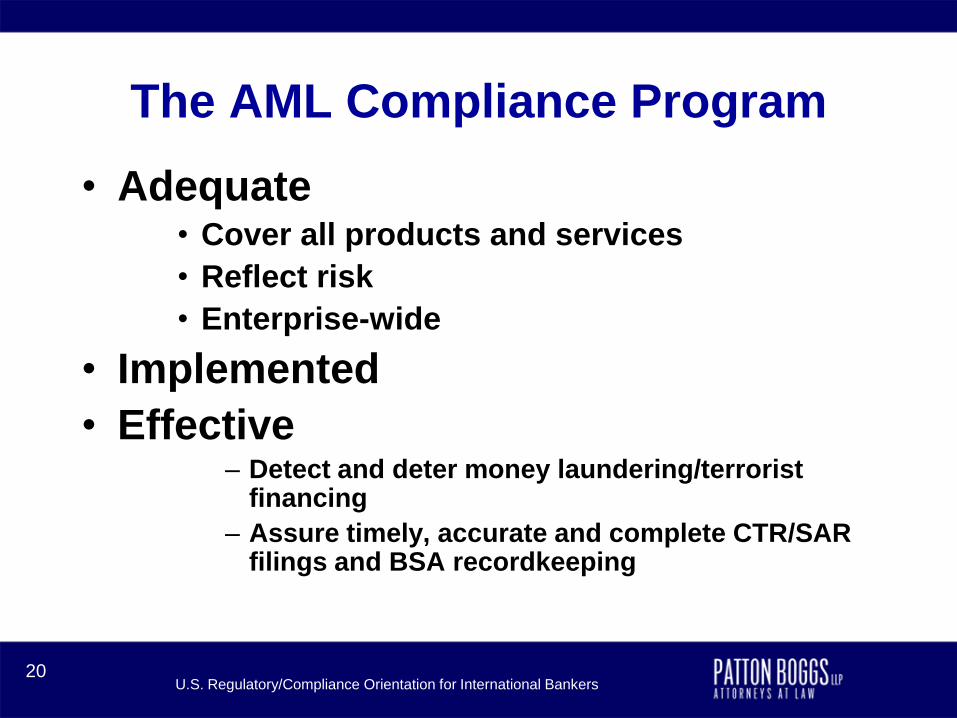

The AML Compliance Program

• Adequate• Cover all products and services

• Reflect risk

• Enterprise-wide

• Implemented

• Effective– Detect and deter money laundering/terrorist

financing

– Assure timely, accurate and complete CTR/SAR filings and BSA recordkeeping

U.S. Regulatory/Compliance Orientation for International Bankers21

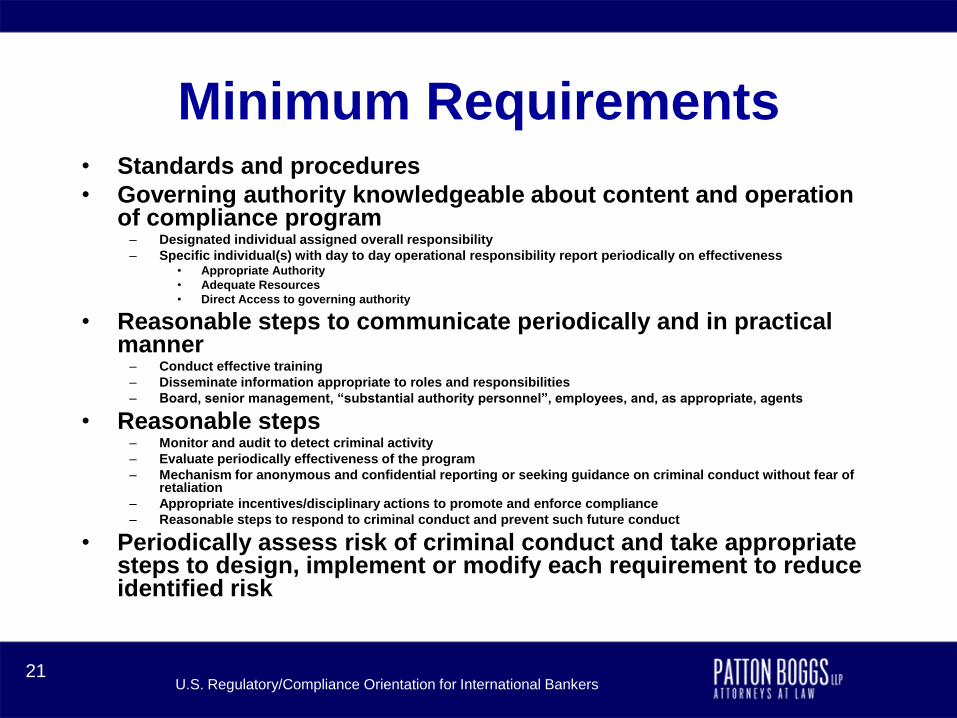

Minimum Requirements• Standards and procedures

• Governing authority knowledgeable about content and operation of compliance program

– Designated individual assigned overall responsibility

– Specific individual(s) with day to day operational responsibility report periodically on effectiveness• Appropriate Authority

• Adequate Resources

• Direct Access to governing authority

• Reasonable steps to communicate periodically and in practical manner

– Conduct effective training

– Disseminate information appropriate to roles and responsibilities

– Board, senior management, “substantial authority personnel”, employees, and, as appropriate, agents

• Reasonable steps– Monitor and audit to detect criminal activity

– Evaluate periodically effectiveness of the program

– Mechanism for anonymous and confidential reporting or seeking guidance on criminal conduct without fear of retaliation

– Appropriate incentives/disciplinary actions to promote and enforce compliance

– Reasonable steps to respond to criminal conduct and prevent such future conduct

• Periodically assess risk of criminal conduct and take appropriate steps to design, implement or modify each requirement to reduce identified risk

U.S. Regulatory/Compliance Orientation for International Bankers22

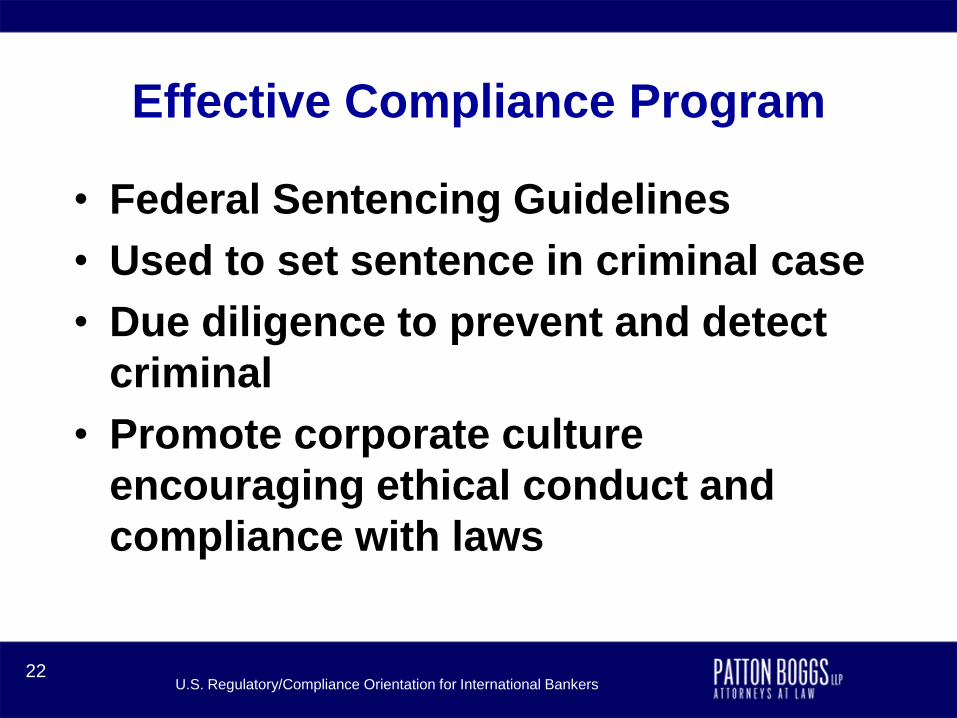

Effective Compliance Program

• Federal Sentencing Guidelines

• Used to set sentence in criminal case

• Due diligence to prevent and detect

criminal

• Promote corporate culture

encouraging ethical conduct and

compliance with laws

U.S. Regulatory/Compliance Orientation for International Bankers23

Anti-Money Laundering

Compliance - FinCEN

• MSB proposed regulation and stored

value card questions

• Mortgage fraud initiatives

• SAR confidentiality-disclosure/sharing

• Directive to act on prepaid cards

U.S. Regulatory/Compliance Orientation for International Bankers24

Managing BSA/AML/OFAC

Compliance

• AML compliance is not going away

• The bar continues to move higher

• Attitude is critical

• Respect your regulatory relationship

• Keep your eye on the rest of your audience

• An adequate program may not be effective

• You likely need more resources – even with the best technology

U.S. Regulatory/Compliance Orientation for International Bankers25

FURTHER INFORMATION

Carol R. Van CleefPartner

Patton Boggs LLP

2550 M. Street, NW

Washington, DC 20037

202-457-6435/571-643-1375

![Sustainable Regulatory Compliance[1]](https://img.pdfslide.net/doc/110x75/577cdd861a28ab9e78ad346d/sustainable-regulatory-compliance1.jpg)