Embed Size (px)

Citation preview

ARTICLE IN PRESS

Energy Policy 37 (2009) 1834–1841

Contents lists available at ScienceDirect

Energy Policy

0301-42

doi:10.1

� Corr

E-m

journal homepage: www.elsevier.com/locate/enpol

Valuation of marginal CO2 abatement options for electric power plantsin Korea

Hojeong Park a,�, Jaekyu Lim b

a Department of Food and Resource Economics, College of Life Sciences and Biotechnology, Korea University, Anam-Dong, Seongbuk-Gu, Seoul 136-701, Republic of Koreab Korea Energy Economics Institute, Euiwang-si, Kyonggi-do 437-713, Republic of Korea

a r t i c l e i n f o

Article history:

Received 19 November 2008

Accepted 12 January 2009Available online 3 March 2009

Keywords:

CO2 marginal abatement cost

Emission allowance

Real option

15/$ - see front matter & 2009 Elsevier Ltd. A

016/j.enpol.2009.01.007

esponding author. Tel.: +82 2 3290 3039; fax:

ail address: [email protected] (H. Park)

a b s t r a c t

The electricity generation sector in Korea is under pressure to mitigate greenhouse gases as directed by

the Kyoto Protocol. The principal compliance options for power companies under the cap-and-trade

include the application of direct CO2 emission abatement and the procurement of emission allowances.

The objective of this paper is to provide an analytical framework for assessing the cost-effectiveness of

these options. We attempt to derive the marginal abatement cost for CO2 using the output distance

function and analyze the relative advantages of emission allowance procurement option as compared to

direct abatement option. Real-option approach is adopted to incorporate emission allowance price

uncertainty. Empirical result shows the marginal abatement cost with an average of h14.04/ton CO2 for

fossil-fueled power plants and confirms the existence of substantial cost heterogeneity among plants

which is sufficient to achieve trading gains in allowance market. The comparison of two options enables

us to identify the optimal position of the compliance for each plant. Sensitivity analyses are also

presented with regard to several key parameters including the initial allowance prices and interest rate.

The result of this paper may help Korean power plants to prepare for upcoming regulations targeted

toward the reduction of domestic greenhouse gases.

& 2009 Elsevier Ltd. All rights reserved.

1 Along with the cap-and-trade system, the baseline-and-credit system is

under consideration as a short-term policy. In addition, several notable issues have

been discussed. For example, as for an initial allocation mechanism of CO2

allowances, there were many discussions on an incentive auction that allows

1. Introduction

The electricity generation sector in Korea is under significantpressure to reduce emission of greenhouse gases (GHGs). AlthoughKorea is not currently listed in the Annex I countries under theKyoto Protocol, it is generally expected to become an obligatoryreduction country after the first commitment period of2008–2012, as Korea is one of the biggest CO2 emitters in theworld, ranking 9th in terms of 2005 emission. If such expectationmaterializes, the electricity generation sector will be the firsttarget to be controlled, as it accounts for more than 25% ofdomestic GHG emission in Korea. In order to achieve theabatement goals effectively, the fossil-fueled power plants thatare responsible for approximately 60% of electricity generation inKorea are considering emission trading as a cost-effective measure.

Korean government is also in a track to design a domesticemission trading mechanism which scheme will be partiallysimilar to the emission trading scheme (ETS) currently beingactive in EU. In particular, the cap-and-trade program appearsmost likely to be introduced among the various proposals so farassessed by extensive numbers of researchers and practitioners in

ll rights reserved.

+82 2 3290 3030.

.

Korea (KEEI, 2007).1 Since, the major compliance tools underthe cap-and-trade program are, as well known, the applicationof direct abatement of CO2 emissions and the procurement ofemission allowances, power plants need to be well informed ofbenefits and costs of these two compliance measures. Afterwards,deliberate decision-making on allowance trades could be based onthis information in order to prevent possible imprudent tradesthat may undermine firm’s financial condition. Thus, the initialtask for the fossil-fueled power plants is to identify their positionsregarding the abatement decisions by examining potential gainsfrom abatement and allowance procurement.

This paper attempts to provide an analytical framework toquantify benefits and costs associated with abatement andemission allowance procurement by analyzing micro-level firm-specific data of fossil-fueled plants in Korea. One way to measurethe value of abatement activity is to compare the abatement cost

participating firms to bid competitively for funds provided by government as

rewards for the abatement. Banking of residual allowances may be allowed

whereas borrowing from the future is expected to be prohibitive. However, the

detail structure of the scheme for the domestic trading system is not yet officially

determined (KEEI, 2007).

ARTICLE IN PRESS

H. Park, J. Lim / Energy Policy 37 (2009) 1834–1841 1835

with the value of allowances that can be additionally gainedthrough the emission reduction. However, uncertainty regardingthe allowance price makes this seemingly straightforwardanalysis more complicated one, because the level of allowanceprice once suitable for the abatement may decrease with positiveprobability, thereby reducing the value of abatement. As recentactivity of EU carbon markets has evidenced, considerablevolatility of allowance price would influence firms’ financialposition associated with CO2 allowance trading. The financialengineering technique is an appropriate model to take intoaccount this uncertain aspect and to provide information valuableto risk management.

In the paper, two step procedures are selected to identify theoptimal compliance measures under uncertain environment: themarginal abatement cost is estimated in the first stage and thenthe second state will compare the marginal abatement cost withthe cost of allowance procurement. More specifically, in the firststage, the output distance function is adopted in order to estimatethe marginal abatement costs, i.e., the shadow value of CO2

emission. This approach is particularly relevant in analyzing CO2

abatement costs as there are far few commercially feasibleabatement technology in place in the electricity generationprocess. In this regard, the shadow price approach has beenwidely used to analyze the cases in which internal pollutionabatement activity may be implicitly embedded in the electricitygeneration process (Coggins and Swinton, 1996; Fare et al., 2005;Vardanyan and Noh, 2006).

In the second stage, given the marginal abatement costsestimated by the output distance function, cost-effective mea-sures are selected by comparing the procurement costs ofemission allowances and abatement costs. In the paper, a real-option approach is adopted to incorporate the volatility of the CO2

market price. From the conventional notion of the optionapproach, the value of abatement strategies for electric utilitiesexhibits a call-option property in a sense that the abatementactivity increases the number of residual allowances that canbe sold later (Herbelot, 1992; Laurikka and Koljonen, 2006:Szolgayova et al., 2008). Thus, for each one unit of abatementoption, the underlying asset is the CO2 allowance that is acquiredvia an abatement activity, and the exercise price is the marginalabatement cost. On the contrary, the value of allowance procure-ment strategy can be analyzed in a framework of a put option inwhich emission allowance price is cost whereas the abatementcost is saved to the extent of the number of allowances in thebalance. We compare the relative advantages for the marginalabatement and allowance procurement options to quantify theconsequential compliance costs.

Power plants are able to choose the timing of abatement orallowance purchase until the specified deadline under the cap-and-trade system. Because, these options may be exercised earlierthan the specified expiry date, we have typical American styleoption problems as well known in the finance literature.Numerical procedures are taken in the paper due to the so-calledfree-boundary problem in American option since it does notprovide analytical solutions. As the power sector which has beenrecognized as a major CO2 emitter is expected to be phased intothe CO2 trading system in the near future, the analytical frame-work and consequential implications presented in the paper maycontribute for Korean power plants to prepare proper compliancemeasures by helping them to identify the optimal positionsregarding the abatement.

The paper is organized as follows. Section 2 providestheoretical models adopted in the paper. Section 3 presents theempirical estimation of the CO2 marginal abatement costs and thevalues of options for abatement and procurement strategies.Finally, Section 4 concludes the analysis.

2. Analytical framework

2.1. Output distance function model

The electric utility is the major contributive source of CO2

which is considered to be an undesirable bad commodity onenvironment. One approach that has been extensively employedto compute the shadow prices of bad commodities from electricutilities is the distance function method (Kwon and Yun, 1999;Swinton, 2002; Fare et al., 2005). This technique allows us to treatthe underlying production process as a non-separable productiontechnology within an axiomatic framework with the considera-tion of goods and bad outputs simultaneously. The marginalabatement cost is measured by the shadow price of pollutantsemitted from underlying production technology that is defined bythe output distance function.

An explicit model is introduced to accommodate the pollutingtechnology as a non-separable process of production. Supposethat a fossil fuel-fired electric power plant produces a vector ofoutputs using a vector of inputs. More specifically, individualproducer uses the N-dimensional input x ¼ (x1,y, xN)AR+

N in orderto produce the M-dimensional output vector y ¼ (y1,y, yM)AR+

M

which may include bad outputs (pollutants) as well as goodoutputs (electricity) at the same time. Following the usualnotation, the output set defined on the closed and boundedcompact space is represented by P(x) ¼ {yAR+

M: x can produce y},which denotes all output vectors that are technically feasiblegiven the input vector x. To establish more formal model, severalassumptions are introduced as follows: (i) P(0) ¼ {0}, (ii) x0Xx)

P(x0)+P(x), and (iii) yAP(x) and 0plp1 implies lyAP(x). Theassumption (i) represents the so-called no free lunch assumptionwhich implies a null output with no inputs. The assumption (ii) isfree disposability, indicating that the output set is non-shrinkingwith increasing inputs. The assumption (iii) concerns weaklydisposability, implying the feasibility of the proportional contrac-tion of outputs. That is, it is possible to reduce bad outputs bysimultaneously reducing some of the desirable outputs. Theoutput distance function is denoted as

Doðx; yÞ ¼ minyfy40jðy=yÞ 2 PðxÞg (1)

for all xAR+N. Note that Do(x,y) provides the maximum output

attainable given the production technology. By definition, thefollowing correspondence between technology and distancefunction can be verified in a straightforward manner: yAP(x) ifand only if Do(x,y)p1. The quantitative characteristics of technol-ogy represented by Do(x,y) rely on the input and output data usedin analysis. Additional feasible gains may result from theelimination of technological inefficiency. Regular properties ofthe distance function are summarized as is shown below

(a)

Do(0,y) ¼ +N for yX0 and Do(x,0) ¼ 0 for all xAR+N(b)

Do(x,ly) ¼ lDo(x,y) for l40 (c) x0Xx implies Do(x0,y)pDo(x,y) (d) y0Xy implies Do(x,y0)XDo(x,y)Two properties in (a) imply no free lunch and possibility ofinaction, respectively. Property (b) implies the positive linearhomogeneity. Property (c) indicates an inverse relationshipbetween inputs and efficiency given the output vector. Lastly,property (d) implies that the output distance function is non-decreasing. However, it must be noted that the output distancefunction is either non-increasing or -decreasing in emissions(Hetemaki, 1994; Kwon and Yun, 1999).

If output prices are known, it is feasible to estimate the shadowprices of outputs using the duality between technology and

ARTICLE IN PRESS

H. Park, J. Lim / Energy Policy 37 (2009) 1834–18411836

revenue. Let p ¼ (p1,y, pM)AR+M denote the price vectors for the

outputs. The revenue function can be represented as

Rðx; pÞ ¼ maxyfpy : Doðx; yÞp1g (2)

Note that (2) is equivalent to Do(x,y) ¼maxp{py:R(x,p)p1}according to the duality established by Shephard (1970). Thisproperty is used to derive the shadow price vector of outputs. Inparticular, the shadow prices of bad outputs are interpreted as thenegative values of the marginal abatement costs. Assumption ondifferentiability of the revenue and distance functions isemployed in order to derive the shadow prices of outputs (Fareet al., 1993). In addition, it is assumed that the price of at least oneof the desirable output is known. Accordingly, the shadow pricefor the jth output when the price of the mth output is given iscalculated as follows:

qj ¼ pm

@Doðx; yÞ=@yj

@Doðx; yÞ=@ym

(3)

Eq. (3) implies that the shadow price of CO2 is measured by thevalue of electricity that is forgone in order to reduce one unit ofCO2, reflecting trade-off between the desirable and undesirableoutputs.

The next task for the estimation of CO2 shadow price is toconstruct the appropriate functional form for the distancefunction. For the estimation purpose, the distance function isassumed to follow the translog functional form

ln D0ðx; yÞ ¼ a0 þXMi¼1

ai ln yi þXN

j¼1

bj ln xj þ1

2

XMi¼1

XMi0¼1

aii0 ðln yiÞðln yi0 Þ

þ1

2

XN

j¼1

XN

j0¼1

bjj0 ðln xjÞðln xj0 Þ þXMi¼1

XN

j¼1

gij ln yi

� �ln xj

� �(4)

In our specific case, we focus on the desirable output(electricity), y1, and one bad output (CO2), y2. Eq. (4) is estimatedusing a non-stochastic linear programming, following the methodsuggested in Fare et al. (1993) and Coggins and Swinton (1996).The estimation process requires regular constraints including thenon-negativity condition, as well as the symmetry and homo-geneity conditions: (i) ln Do(x,y)p0, implying that the outputdistance function cannot exceed unity, (ii) q ln Do(x,y)/q ln y1X0 forthe strong disposability of electricity, q ln Do(x,y)/q ln y2p0 for theweak disposability of CO2 pollutant, (iii) aii0 ¼ ai0 i and bii0 ¼ bi0i forsymmetry for all i,i0,j and j0 and (iv)

Piai ¼ 1 and

Pi0aii0 ¼

1P

igij ¼ 0 for the homogeneity. GAUSS is used for the programalong with the coupled CO library. The BFGS algorithm is selectedto ensure the convergence stability. As the resultant shadowvalues tend to be somewhat sensitive to the electricity price, weperform a bootstrapping by randomizing electricity price in orderto examine the statistical properties of the shadow value.

2.2. Valuing marginal abatement and procurement options

The purpose of this section is to present a model framework toanalyze the option values associated with abatement andallowance procurement activities. The allowance is traded at theprice of s(t) at time t and the price is assumed to follow thestochastic process of geometric Brownian motion

dsðtÞ ¼ assðtÞdt þ sssðtÞdz (5)

where dz is the Wiener process with the property of E(dz) ¼ 0 andVar(dz) ¼ dt. as and as are the drift and volatility parameters,respectively. From the perspective of individual power plant, thevalue of marginal CO2 abatement is positively related to the priceof CO2 emission allowance. Let MAC denote the marginal

abatement cost estimated by the distance function approach asdescribed in the previous section.

When V(t,s) denotes the option value of marginal abatement,the option value at each point in the (t,s) must be larger than orequal to the immediate payoff from the option exercise

Vðt; sÞXmaxfsðtÞ �MAC;0g (6)

The structure of Eq. (6) resembles an American call optionwherein MAC corresponds to the strike price and s(t) is interpretedas the price of the underlying asset. That is, upon the exercise of thisoption, the plant acquires additional one unit of residual allowancethat carries the value of s(t) at the cost of MAC. The power plantchooses when to exercise the option within the remaining period ofDT ¼ T�t given the expiry date T. Similarly, the option value ofallowance procurement strategy, W(t,s), is represented by thefollowing specification which is analogous to the put option

Wðt; sÞXmaxfMAC � sðtÞ;0g (7)

Eq. (7) indicates that, upon the exercise of this option, the plantpays an emission allowance price for the procurement whereas themarginal abatement cost is saved.

Because, the free-boundary problem emerges as one of thetypical difficulties in pricing an American option due to thepossibility of the early exercise, finite difference method isemployed to numerically solve (6) and (7) (Wilmott et al., 1995).Considering V(t,s), the application of Ito’s lemma yieldsrV(t,s) ¼ Vi(t,s)+assVs(t,s)+0.52as

2s2Vss(t,s) where the subscript de-notes the partial derivative. The procedure to solve this partialdifferential equation requires a discrete grid that is set withrespect to t and s(t). Denote smax as a choke price of emissionallowance which cannot be reached by s(t) within the timehorizon. Then, the grid is represented by points (t,s) such thatt ¼ 0,dt,2dt,y, Ndt ¼ T and s ¼ 0,ds,2ds,y, Mds ¼ smax where d isan increment parameter. Let Vij ¼ V(idt,jds) for simplification.Then, we take symmetric differences for the first and secondderivatives in the partial differential equation. After computing Vij

for all i and j, the validity of early exercise is checked. Bycombining the Crank–Nicolson method to enhance the accuracy ofthe finite difference method and to prevent possible failure ofconvergence, we have the following grid equation with thecombination of forward, backward and central differences:

Vij � Vi�1;j

dtþ

rjds

2

Vi�1;jþ1 � Vi�1;j�1

2ds

� �þ

rjds

2

Vi;jþ1 � Vi;j�1

2ds

� �

þs2j2ðdsÞ2

4

Vi�1;jþ1 � 2Vi�1;j þ Vi�1;j�1

ðdsÞ2

!

þs2j2ðdsÞ2

4

Vi;jþ1 � 2Vi;j þ Vi;j�1

ðdsÞ2

!¼

r

2Vi�1;j þ

r

2Vij

More simply, we may express this as follows:

�ajV i�1;j�1 þ ð1� bjÞVi�1;j � gjVi�1;jþ1 ¼ ajVi;j�1 þ ð1þ bjÞVij þ gjVi;jþ1

(8)

where aj ¼ dt(s2j2�rj)/4, bj ¼ �dt(s2j2+r)/2 and gj ¼ dt(s2j2+rj)/4.The appropriate boundary conditions are given by V(t,smax) ¼ 0.Based on the Gauss–Seidel method with overrelaxation, we adoptthe iterative scheme

V ðkþ1Þi1 ¼max g1;V

ðkÞi1 þ

o1�b1½r1 � ð1� b1ÞV

ðkÞi1 þ g1V ðkÞi2 �

n o;

V ðkþ1Þi2 ¼max g2;V

ðkÞi2 þ

o1�b2½r2 þ a2V ðkþ1Þ

i1 � ð1� b2ÞVðkÞi2 þ g2V ðkÞi3 �

n o...

V ðkþ1Þi;M�1 ¼max gM�1;V

ðkÞi;M�1 þ

o1�bM�1

½rM�1 þ aM�1V ðkþ1Þi;M�2 � ð1� bM�1ÞV

ðkÞi;M�1�

n o

for I ¼ 1,y, N. Note that k is the iteration count indicator,gj denotes the intrinsic value when s ¼ jds and o is the

ARTICLE IN PRESS

Table 1Specification of fossil fuel power plants.

Code Name Capacity (MW) CO2 (ton) Fuel type

1 Samchonpo Thermal Power 3240 6,412,520 Bituminous coal

2 Youngdong Thermal Power 325 443,127 Anthracite coal

3 Yosu Thermal Power 528 326,294 Oil

4 Bundang Combined Cycle power 900 501,612 LNG

5 Dangjin Thermal Power 2000 3,891,344 Bituminous coal

6 Honam Thermal Power 500 1,024,246 Bituminous coal

7 Donghae Thermal Power 400 596,121 Anthracite coal

8 Ulsan Thermal and Combined Cycle 3000 1,693,114 Oil-combined cycle

9 Ilsan Combined Cycle 900 433,102 LNG-combined cycle

10 Taean Thermal Power 3000 5,056,083 Bituminous coal

11 Pyeongtaek Thermal and Combined Cycle 1880 1,488,055 Bunker-C, LNG

12 Seoincheon Thermal Power 1300 814,119 Oil, LNG

13 Boryeong Thermal and Combined Cycle 3800 6,122,038 LNG and bituminous coal

14 Seoul Thermal Power 388 163,084 LNG

15 Seocheon Thermal Power 400 518,814 Anthracite coal

16 Jeju Thermal Power 215 209,781 Oil

17 Hadong Thermal Power 3000 5,735,354 Bituminous coal

18 Youngnam Thermal Power 400 319,628 Bunker-c, orimulsion

19 Shinincheon Combind Cycle 1800 1,146,047 LNG

20 Namjeju Thermal Power 60 17,589 Bunker-C

H. Park, J. Lim / Energy Policy 37 (2009) 1834–1841 1837

overrelaxation parameter. The convergence criterion we employ isJVij

(k+1)�Vij

(k)Joe where e denotes a tolerance parameter.

3. Empirical analysis

Under the cap-and-trade system, individual power plants mayabate CO2 emission by reducing electricity generations. Alterna-tively, the simplest option is to expand the amount of holdingallowances up to the point of emission level. Since bothalternatives involve some costs, we need to identify relativelymore efficient compliance method for power plants. For thispurpose, this section covers empirical studies on the abatementcosts for major fossil-fueled power plants in Korea and thepotential benefits of abatement and allowance procurementstrategies.

The empirical data is based on a utility-level survey compiledby the Korea Electric Power Corporation (KEPCO). KEPCO wasderegulated into six power companies in 2001 as the result ofgovernment efforts to extend public deregulation: South EastPower Co., East West Power Co., Western Power Co., MidlandPower Co., Southern Power Co. and Korea Hydro & Nuclear PowerCo. (KHNP). Except for the KHNP that consists of CO2 non-emittingtechnology relying on the hydro and nuclear power, the remainderof power companies is utilizing various fossil fuels such as oil, coaland natural gas. Therefore, after excluding hydro/pumping-uppower generations and nuclear power plants that are notresponsible for CO2 emission, basic specification for remaining20 fossil-fueled power plants are listed in Table 1.2 Most of largescale power plants with over 2000 MW nameplate capacity areusing coals that have been acknowledged as severe precursors ofCO2 emission. Partial list includes Samchonpo Power (code 1),Dangjin Thermal Power (code 5), Taean Thermal Power (code 10)and Handong Thermal Power (code 17).

The amount of CO2 emitted from the electricity generationsector is calculated on the basis of the IPCC guideline. According tothe IPCC (1996), there are two recommendable methods, that is,Tiers 1 and 2, so as to calculate CO2 emissions in electricitygeneration sector. Two methods are distinct depending on the

2 As for several combined-cycle plants, they are reported along with the steam

engine power plants simultaneously adopted in the utility, thereby disaggregating

the variables of interest by technology type is impossible.

types of electricity generations and required level of datacomplexity. The Tier 1 method is relatively simple in that itcalculates the amount of emission via the multiplication of fuelinputs and the corresponding greenhouse emission coefficients.On the other hand, the Tier 1 method has disadvantages in thatthere may be some overestimation of greenhouse gases whenmitigation technology is embedded into the electricity generationprocess. The Tier 2 method applies different emission factors toeach type of utility generation. Compared to the Tier 1, thismethod is relatively accurate but requires more complex data.Thus, the Tier 2 result tends to be sensitive to the underlyingtechnology and estimation uncertainty might increase. We use theemission coefficients provided by the Tier 1 in the IPCC guidelines,‘Revised 1996 IPCC Guidelines for National Greenhouse GasInventories, IEA/OECD’. The following formula is suggested: CO2

emission ¼P

(EFab�ACTIVITYab) where EF is the emission coeffi-cient (kg/TOE), ACTIVITY is the fuel inputs (TOE), a is the fuel type,and b is the generation activity for each plant. In order to obtainthe amount of fuel consumption for each fuel, we require thegeneration efficiency data for each fuel and electricity–petroleumconversion factor. Table 2 presents the generation efficiency datafor each source of fossil fuels between 2001 and 2004, showingthat, on average, anthracite generation has an efficiency of 39.17%,bituminous generation has an efficiency of 34.07%, gas generationhas an efficiency of 36.14% and residual fuel oil generation has anefficiency of 37.51%. Note that the anthracite which is produced indomestic region exhibits relatively high generation efficiencycompared to the imported bituminous coal.

Several input variables including fuel usage and generatingcapacity are compiled at the generating unit level, while the laborand capital variables are made at the plant level. Our modelcorresponds to one good (electricity) and one bad (CO2 emissions)model. Electricity output is measured with kilowatt-hours peryear and electricity prices are expressed in the Euro per kWh,which values are averaged for each plant for each year.3 The meanvalues for electricity generation and CO2 emission are 8010�106

kWh per year and 1813�103 tons per year, respectively. Laborinput variable is measured by the numbers employed whereas the

3 Since, the estimated marginal abatement cost is compared to the CO2

allowance price that is measured by Euro, we convert Korean won to Euro to

facilitate the comparison. The exchange rate 1,305.23 Korean won per Euro is used

to ensure consistency of the following analysis on option analysis.

ARTICLE IN PRESS

Table 3The estimates of the translog distance function.

Parameter Value

P01 6.1321

P02 �1.1168

P03 2.1168

P04 �2.7707

P05 2.1093

P06 1.9144

P07 0.3444

P08 0.3444

P09 �2.6033

P10 2.3614

P11 6.9778

P12 6.9778

P13 22.8982

P14 �5.6467

P15 12.2205

P16 �9.4307

P17 2.8569

Table 2Generation efficiency by fuel types.

Anthracite Bituminous Gas Residual fuel oil

2001 39.30 33.93 35.42 37.71

2002 39.30 34.66 36.10 37.59

2003 39.16 34.51 36.37 37.58

2004 39.25 34.74 36.09 37.40

Source: KEEI (2006).Unit: %.

Table 4CO2 marginal abatement costs of power plants.

Plant code Value Std. dev.

1 14.12 1.05

2 12.30 1.06

3 12.94 1.38

4 10.11 1.64

5 12.46 1.05

6 13.52 0.94

7 10.25 1.00

8 16.85 1.58

9 9.92 1.52

10 15.74 1.27

11 15.78 1.58

12 13.04 1.87

13 15.13 1.17

14 13.19 1.50

15 12.49 1.27

16 8.51 1.12

17 13.43 1.08

18 11.54 1.29

19 12.38 1.91

20 8.65 0.97

Unit: h/ton CO2.

H. Park, J. Lim / Energy Policy 37 (2009) 1834–18411838

capital variable is measured by the Euro per kWh that is derivedfrom the investment cost with the application of annualdepreciation rate 5%. The mean values for labor and capital are311 per year and h783.77/kWh, respectively.

The first step in empirical investigation is to estimate Eq. (4)using the total 80 observations to calculate the marginalabatement costs. The resulting parameter estimates reported inTable 3 are used to compute the marginal abatement cost of CO2

as is shown in Eq. (3), after obtaining the four-year averagedistance function values for each power plant. As the marginalabatement cost of CO2 may be sensitive to the electricity prices,1000 numbers of simulations are conducted by randomizing theelectricity price from the benchmark level, i.e., h0.05/kWh.Afterwards, the average values are adopted for the remaininganalysis.

Table 4 shows the final estimation results of CO2 marginalabatement costs as well as standard deviations from thesimulation. This result confirms the existence of substantialheterogeneity among electric utilities with regard to the marginalabatement cost, implying that significant improvement of eco-nomic efficiency via emission trading may be realized. Theweighted average price of a marginal abatement in CO2 emissionis h14.04/ton CO2. Note that this value reveals great disparity ascompared to Kwon and Yun (1999) which reported an averageprice of h2.91 during the early 1990s. Such difference seems to bemainly due to the increase of electricity price, since then, becausethe energy portfolio has been significantly altered by loweringcoal dependency in the power-generation sector while increasingrelatively expensive fuels such as LNG. In addition, unlike Kwonand Yun (1999) which used the nameplate capacity as the capitalvariable, this paper employs more explicit data on the capitalinvestment cost directly supplied by the KEPCO. Such differencemakes a direct comparison of two results difficult. It must benoted that the result in this paper is more consistent with other

related study. For example, according to Rezek and Campbell(2007) that analyzed a panel data of U.S. electric power plants in1998, the average price per CO2 ton is USD 18.10–20.62, orequivalently h16.14–18.38.

The average marginal abatement costs differ by technologysuch that coal-fired plants recorded an average of h13.04/ton CO2

while plants with oil and natural gas-fired units maintained anaverage of h12.45/ton CO2 and h11.40/ton CO2, respectively. Mostnotably, Youngdong, Donghae and Seocheon power plants (code 2,7 and 15) using the domestic anthracite coal exhibit the lowermarginal abatement cost (h11.68/ton CO2 on average) compared toplants using the imported bituminous coal (h13.85/ton CO2 onaverage). Based on this finding, each power plant may decide at itsmarginal point whether to implement an abatement strategy or topurchase emission allowances in CO2 market. For instance, thecase when the marginal abatement cost is significantly lower thanthe emission allowance price induces the plant to choose theabatement option. Thus, the next step is to calibrate the optionvalues of the marginal abatement and allowance procurement asformally defined in (6) and (7). We first begin with the non-stationary test to confirm the process of geometric Brownianmotion for the CO2 allowance price. The allowance price data inthe paper covers the period from January 31, 2005 to June 13,2005 which belongs to the early period of EU-ETS. The averageallowance price is h13.85 during that period. The AugmentedDickey–Fuller (ADF) test shows �0.1205 for the level data, whichdisallow the rejection of the null hypothesis of unit root at 1–5% ofsignificance. However, in case of the first difference series, ADFstatistics is �5.2632, implying stable time series. Therefore, due toa non-stable property of AR(1), the geometric Brownian motioncan be used to describe the trends of allowance price.

Then, we estimate the volatility parameter by letting yt ¼ lnst�ln st�1 where st is the CO2 allowance price. According to Tsay(2002), if st follows the geometric Brownian motion (5), the meanand variance of st are given by (as�as

2/2)D and as2D, respectively,

where D is the equally spaced time interval. Hence, the value of ss

is provided by s:dy=ffiffiffiffiDp

, where s:d ¼ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiPT

t¼1ðyt � yÞ2=ðT � 1Þq

.

By importing the shadow values of CO2 estimated in theprevious procedure, the marginal abatement option values forplants are computed. For the benchmark level, the annual interestrate r is set to 0.05 and the estimated value of ss is 0.3083. In the

ARTICLE IN PRESS

H. Park, J. Lim / Energy Policy 37 (2009) 1834–1841 1839

numerical procedures for the finite difference method, it isassumed that T ¼ 5.12, dt ¼ T/150, smax ¼ 100, s0 ¼ 13.85 ando ¼ 1.2 with a tolerance level of 0.001.

The second and fifth columns in Table 5 report the optionvalues of CO2 marginal abatement, which show that some powerplants (code # 4, 7, 9, 16 and 20) maintain the position where thedirect CO2 abatement is more cost-effective than the allowanceprocurement. This result was anticipated to some degrees as themarginal abatement cost for them is considerably lower than theemission allowance spot price which was then set at the level ofh13.85. In addition, such relative advantages for abatement wouldincrease further if the allowance price is expected to increase withgreater volatility, because increasing allowance price reflectslarger chances for arbitrage by selling the residual allowancesacquired through the abatement activity. Table 5 shows that mostof combined-cycle power plants (code #8, 10 and code 13) havethe marginal abatement option values below h0.7, implying thelarger opportunity costs of CO2 abatement. This indicates thatthese power plants are better to place them in allowance

Table 5Comparison of abatement and procurement options.

Plant code Abatement option Procurement option

1 1.04 1.37

2 2.02 0.53

3 1.62 0.78

4 3.77 0.09

5 1.92 0.59

6 1.32 1.04

7 3.64 0.10

8 0.31 3.37

9 3.94 0.07

10 0.53 2.47

11 0.52 2.50

12 1.57 0.82

13 0.69 2.03

14 1.49 0.89

15 1.90 0.60

16 5.29 0.01

17 1.36 1.10

18 2.56 0.31

19 1.97 0.56

20 5.15 0.01

Unit: h/ton CO2.

8 10 12 14 16 180

1

2

3

4

5

6

MAC

Mar

gina

l Aba

tem

ent O

ptio

n V

alue

(uni

t: E

uro)

Fig. 1. The relationship between the option v

procurement strategy rather than to abate CO2 as a means forcompliance.

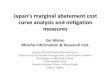

Optimal choices for power plants can be clarified by comparingtwo options, V(t,s) and W(t,s), the marginal abatement andallowance procurement options, respectively. The third and sixthcolumns in Table 5 shows the option value associated withallowances procurement. Fig. 1 illustrates the relationship ofmarginal option values with the variation of the marginalabatement cost. One example is provided to facilitate under-standing the results of Table 4 and Table 5: As for the SamchonpoThermal Power (code 1) with the marginal abatement cost ofh14.12/ton CO2, the option value of marginal abatement is lessthan the option value of allowance procurement, thereby implyingthat it is more desirable to hold its allowance procurementposition instead of trying to abate CO2 emission directly. Thisrelation still holds even after considering the possibility that theallowance price may exceed the marginal abatement cost. On theother hand, for example, the marginal abatement cost of DonghaeThermal Power (code 7) is substantially lower than the underlyingallowance price and thus its abatement option value significantlyexceeds the allowance procurement option value. Thus, DonghaeThermal Power is more likely to function as a seller of theCO2 allowance to the extent that the relationship of the abatementoption larger than procurement option is sustained. Fig. 2illustrates the values of V(t,s)�W(t,s) for 20 power plants whichcorrespond to the values of relative advantages of marginalabatement to allowance procurement. In particular, the powerplants having code numbers 1, 8, 10, 11 and 13 seem to be inpositions suitable for allowance procurement whereas the rest ofplants are profitable to abate CO2.

In the real option literature (Dixit and Pindyck, 1994), thewaiting value of exercising the option exists when V(t,s)�(s�MAC)40 in a sense that the value of keeping option is largerthan the payoff from the immediate exercise of the option. In thepresence of such positive waiting value, it is recommended todelay the option exercise. Sensitivity analyses on the waitingvalues are provided regarding several key parameters. Firstly, aswell known in the real-option analysis, it is immediate to find anincrease of waiting value of the marginal abatement option whenthe marginal abatement cost increases. In addition, starting fromthe current allowance price that allows for either abatementposition or allowance procurement position for each power plant,it is worthwhile to derive the threshold level of allowance price atwhich the original position is reversed to another position. Fig. 3

8 10 12 14 16 180

0.5

1

1.5

2

2.5

3

3.5

4

MAC

Mar

gina

l Pro

cure

men

t Opt

ion

Val

ue (u

nit:

Eur

o)

alues and the marginal abatement cost.

ARTICLE IN PRESS

H. Park, J. Lim / Energy Policy 37 (2009) 1834–18411840

provides a visualized information on the exact magnitudes ofallowance price gap which prompts option switching. For example,if there is a price change of h0.38 that increases allowance pricefrom h13.85 to h14.23, it would be better for Samchonpo ThermalPower (code 1) to alter its allowance procurement position byadopting a direct abatement policy, since its marginal abatementcost becomes significantly lower than the allowance price. Inparticular, visual investigation reveals that Jeju and Namjeju plants(codes 16 and 20) maintain robust positions, implying that theyare unlikely to switch their original positions unless there aresufficient price changes for the allowance price.

Combined with the interest rate, the expiry date performs aninteresting role in option valuation under the cap-and-tradesystem, since the flexibility for power plants to adjust theirpositions tends to be more limited as the remaining period untilthe expiry date decreases. Fig. 4 illustrates the sensitivity analysisof the abatement option value for Namjeju Thermal Power withregard to the expiry date, showing that, if the expiry date comesearlier, the option value for abatement increases. This is intuitivebecause the marginal abatement cost of Namjeju Thermal Power(h8.65/ton CO2) is relatively lower than the allowance pricecurrently evaluated (h13.85/ton CO2) and its chances are fairly lowfor the allowance price to fall below the marginal abatement

0 2 4 6 8 10 12 14 16 18 20-4

-3

-2

-1

0

1

2

3

4

5

6

Plant Code Number

V-W

(uni

t:Eur

o)

Abatement Regime

Procurement Regime

Fig. 2. The values of relative advantages of marginal abatement.

0 2 4 6 8 10 12 14 16 18 20-6

-5

-4

-3

-2

-1

0

1

2

3

4

Plant Code Number

Eur

o

Fig. 3. Threshold allowance price gaps for option switching.

cost with the short-time window until the expiry date. Inaddition, Fig. 4 shows an inverse relationship between theabatement option value and the interest rate which yields areduction in waiting value. This implies that higher interest ratesinduce earlier abatement action, as the rate of return from thesales of residual allowances obtained from the abatementincreases and accordingly the waiting value of option exercisedecreases. Similarly, Fig. 5 provides a graph on the sensitivityof option value for Ulsan Thermal and Combined-Cycle plant(code 8) which marginal abatement cost is relatively high.

4. Conclusion

The electricity generation sector in Korea, being responsible formore than 25% of domestic GHG emission, is expected to be amajor target for emission control after the first commitmentperiod of 2008–2012 under the Kyoto Protocol. Since fossil fueldependency in Korea remains still high in spite of increasingefforts to expand nuclear power generation, it is criticallyimportant to evaluate and identify comparative advantages forfossil-fueled power plants by empirically examining costs andbenefits associated with CO2 reduction.

0.10.2

0.30.4

0.5

01

23

45

x 10-3

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Expiry DateInterest Rate

Aba

tem

ent O

ptio

n V

alue

(uni

t: E

uro)

Fig. 5. Sensitivity analysis of option value with respect to T and r: Ulsan plant.

0.10.20.30.40.5

0 1 2 3 4 5x 10-3

4.945

4.95

4.955

4.96

4.965

4.97

4.975

4.98

4.985

4.99

Expiry DateInterest Rate

Aba

tem

ent O

ptio

n V

alue

(uni

t: E

uro)

Fig. 4. Sensitivity analysis of option value with respect to T and r: Namjeju plant.

ARTICLE IN PRESS

H. Park, J. Lim / Energy Policy 37 (2009) 1834–1841 1841

In this paper, we have attempted to assess the overalleconomic efficiency of major fossil-fueled power plants byintegrating the distance function method and real-option ap-proach to quantify power plant’s marginal abatement cost and thepayoffs from the CO2 reduction activity. The volatility of CO2

allowance price as recently observed in the EU market wasincorporated into the analysis since the role of uncertainty iscrucial in making a decision for abatement activity.

The finding of this study indicates that the weighted averagemarginal abatement cost of CO2 for Korean fossil-fueled powerplants is h14.04/ton CO2 which is lower than the allowance spotprice, implying that some of power plants in Korean electric sectorseem not to be so vulnerable to the emission trading scheme asexpected earlier. Numerical illustrations showed that the marginalabatement cost is higher for coal-fired power plants than the casefor non-coal-fired power generation. In addition, the marginalabatement costs for domestic coal-fired plants are lower than themarginal abatement costs for power plants using the importedbituminous coal. Nevertheless, this does not necessarily meanthat electric sector has to expand the use of domestic coal for thegeneration purpose, because there are growing concerns on thereservoir of domestic anthracite coal near to the extinction pointwhich will obviously limit the fuel switching capacity. Theanalytical model presented in the paper is helpful from theperspective of individual fossil-fueled power plant to identifythe comparative advantages of the abatement activity. Overall, theresult would be of interest for making a cost-minimizingcompliance decision in the electric generation sector, since theelectricity generation sector in Korea is more likely to be the firsttarget for pilot domestic emission trading project.

Although the result in the paper enables us to quantify thevalue of abatement option, thereby verifying the strategicpositions regarding abatement activity, it does not permit the fullscale analysis regarding the abatement cost and benefits. This isan inherent shortcoming in the distance function approach whichprovides only the point estimates of the marginal abatement cost,not the entire marginal abatement cost curve. Therefore, thenumerical results reported in the paper must be interpreted in astatic context similar to Swinton (2002). In addition, currentanalysis does not investigate the CO2 emission outside the electricsector. Once if domestic CO2 emission trading scheme is launched,future study must include analysis which examines the structureof marginal abatement costs for the entire regulated industry inorder to study possible convergence between the market price ofallowance and the marginal abatement costs across plants (Rezekand Blair, 2005).

Acknowledgement

This work was financially supported by a Korea ResearchFoundation Grant funded by the Korean Government (KRF-2006-321-B00349).

References

Coggins, J.S., Swinton, J.R., 1996. The price of pollution: a dual approach to valuingSO2 allowances. Journal of Environmental Economics and Management 30,58–72.

Dixit, A., Pindyck, R., 1994. Investment under Uncertainty. Princeton UniversityPress, Princeton.

Fare, R., Grosskopf, S., Lovell, C.A.K., Yaisawarng, S., 1993. Derivation of shadowprices for undesirable outputs: a distance function approach. The Review ofEconomics and Statistics 75, 374–380.

Fare, R., Grosskopf, S., Noh, D-W., 2005. Characteristics of a polluting technology:theory and practice. Journal of Econometrics 126, 469–492.

Herbelot, O., 1992, Option valuation of flexible investments: the case ofenvironmental investments in the electric power industry, Ph.D. Dissertation,Department of Nuclear Engineering, MIT.

Hetemaki, L., 1994. Do environmental regulations lead firms into trouble? Evidencefrom a two-stage distance function model with panel data. The Finnish ForestResearch Institute, Helsinki.

IPCC, 1966, Revised 1996 IPCC Guidelines for National Greenhouse Gas Inventories,IEA/OECD.

KEEI, 2006. Annual Energy Statistics. Korea Energy Economics Institute.KEEI, 2007, Research on emission trading system and national electricity demand

and supply schedule incorporating CO2 allowance prices. Korea EnergyEconomics Institute and Korea Power Exchange (in Korean).

Kwon, O.S., Yun, W-C., 1999. Estimation of the marginal abatement costs ofairborne pollutants in Korea’s power generation sector. Energy Economics 21,547–560.

Laurikka, H., Koljonen, T., 2006. Emissions trading and investment decisions in thepower sector—a case study in Finland. Energy Policy 34, 1063–1074.

Rezek, J.P., Blair, B., 2005. Abatement cost heterogeneity in Phase 1 electric utilities.Contemporary Economic Policy 23 (3), 324–340.

Rezek, J.P., Campbell, R.C., 2007. Cost estimates for multiple pollutants: amaximum entropy approach. Energy Economics 29, 503–519.

Shephard, R.W., 1970. Theory of Cost and Production Functions. PrincetonUniversity Press, Princeton.

Szolgayova, J., Fuss, S., Obersteiner, M., 2008. Assessing the effects of CO2 price capson electricity investment—a real options analysis. Energy Policy 36,3974–3981.

Swinton, J.R., 2002. The potential for cost savings in the sulfur dioxide allowancemarket: empirical evidence from Florida. Land Economics 78 (3), 390–404.

Tsay, R.S., 2002. Analysis of Financial Time Series. Wiley-Interscience.Vardanyan, M., Noh, D.-W., 2006. Approximating the cost of pollution abatement

via alternative specifications of a multi-output production technology: a caseof the U.S. electric utility industry. Journal of Environmental Management 80,177–190.

Wilmott, P., Howison, S., Dewynne, J., 1995. The Mathematics of FinancialDerivatives. Cambridge University Press, Cambridge.