Embed Size (px)

DESCRIPTION

Value Creation Strategies

Citation preview

European Management Journal Vol. 18, No. 5, pp. 463–475, 2000 2000 Elsevier Science Ltd. All rights reservedPergamon

Printed in Great Britain0263-2373/00 $20.00PII: S0263-2373(00)00036-0

Strategies for ValueCreation in E-Commerce:Best Practice in EuropeCHRISTOPH ZOTT, INSEAD, FranceRAPHAEL AMIT, The Wharton School, University of Pennsylvania, USAJON DONLEVY, INSEAD, France

This paper investigates strategies for value creationof e-commerce companies. Our main assumption isthat e-commerce fundamentally affects the waybusiness is conducted across many industries. Tosupport this insight, we discuss the unique charac-teristics of ‘virtual markets’ brought on by the Inter-net. Based on a survey of 30 European e-commercecompanies, we then identify two main strategies forvalue creation in e-commerce — the efficiency thate-commerce business models exhibit, and thedegree to which they create ‘stickiness.’ To illus-trate these two strategies, we give examples of Euro-pean companies that can be considered ‘best prac-tice’ companies. 2000 Elsevier Science Ltd. Allrights reserved

Keywords: E-commerce, Value Creation, Best Prac-tice, Virtual Markets, Strategic Management

E-Commerce in Europe

The year 1999 was one of explosive growth for e-commerce in Europe. Revenue from European e-com-merce sales grew 200 per cent, compared to 145 percent for the US (IDC, 2000). The Boston ConsultingGroup (2000) predicted that the European on-linemarket would be worth over 45 billion euros by 2002.Jupiter Communications (1999) expects the upwardgrowth trend for the number of Europeans buyingon-line to continue exponentially, from 13.5 per centof the online population at present to 43 per cent bythe year 2003. Nonetheless, before 1999, in theshadow of the booming US economy, e-commerce inEurope had been overlooked and underestimated,not often commanding the same level of attention.Historically, European Internet penetration, andtherefore e-commerce, has lagged behind that of the

European Management Journal Vol 18 No 5 October 2000 463

US for many reasons, including the high connectioncosts resulting from the slow deregulation of the Eur-opean telecommunications industry, restrictive Euro-pean trade and legal regulations, and language andcultural differences across Europe. Consequently,while e-commerce became a phenomenon in the USduring the latter half of the 1990s, it is just beginningto attract attention in Europe.

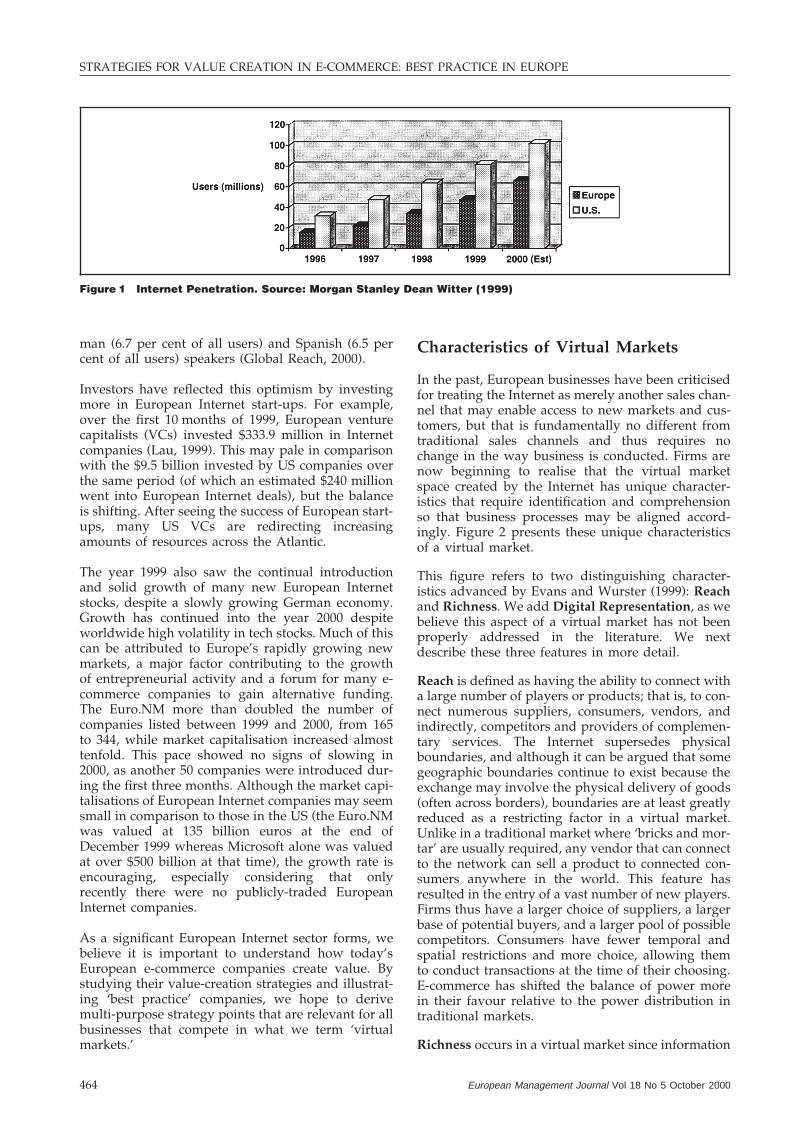

Events in the past year indicate that the e-commercelandscape in Europe is changing. Falling Internetaccess costs across the Continent, spurred by compe-tition in the telephone industry from a prolongedprice war, have created a surge in the number of Eur-opeans going on-line. From October to December1999, one out of every four Europeans reported hav-ing used the Internet (see Figure 1). While e-com-merce is still hindered by local call charges, whichlimit the amount of time spent on-line, many InternetService Providers (ISPs) are combating this. The UK’sFreeserve was the first ISP to offer ‘free Internetaccess’, where the consumer pays only the cost of theconnecting call, from which Freeserve shares a por-tion of the revenue. This model was soon imitatedacross the Continent. More recently, ISPs have beenoffering flat-rate subscriptions, where the consumerpays monthly or annual fees and can stay connectedfor unlimited periods of time. These efforts to keeppeople on-line are expected to be a major growthdriver of e-commerce.

In addition to changes in connection costs, there hasbeen a steady increase in the number of non-Englishlanguage web sites. This change has paralleled thegrowing Internet penetration into non-English-speak-ing markets. The market is driving this change — thenumber of non-English-speaking Internet users (48.7per cent of all users) is approaching that of English-speaking users (51.3 per cent of all users), led by Ger-

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

Figure 1 Internet Penetration. Source: Morgan Stanley Dean Witter (1999)

man (6.7 per cent of all users) and Spanish (6.5 percent of all users) speakers (Global Reach, 2000).

Investors have reflected this optimism by investingmore in European Internet start-ups. For example,over the first 10 months of 1999, European venturecapitalists (VCs) invested $333.9 million in Internetcompanies (Lau, 1999). This may pale in comparisonwith the $9.5 billion invested by US companies overthe same period (of which an estimated $240 millionwent into European Internet deals), but the balanceis shifting. After seeing the success of European start-ups, many US VCs are redirecting increasingamounts of resources across the Atlantic.

The year 1999 also saw the continual introductionand solid growth of many new European Internetstocks, despite a slowly growing German economy.Growth has continued into the year 2000 despiteworldwide high volatility in tech stocks. Much of thiscan be attributed to Europe’s rapidly growing newmarkets, a major factor contributing to the growthof entrepreneurial activity and a forum for many e-commerce companies to gain alternative funding.The Euro.NM more than doubled the number ofcompanies listed between 1999 and 2000, from 165to 344, while market capitalisation increased almosttenfold. This pace showed no signs of slowing in2000, as another 50 companies were introduced dur-ing the first three months. Although the market capi-talisations of European Internet companies may seemsmall in comparison to those in the US (the Euro.NMwas valued at 135 billion euros at the end ofDecember 1999 whereas Microsoft alone was valuedat over $500 billion at that time), the growth rate isencouraging, especially considering that onlyrecently there were no publicly-traded EuropeanInternet companies.

As a significant European Internet sector forms, webelieve it is important to understand how today’sEuropean e-commerce companies create value. Bystudying their value-creation strategies and illustrat-ing ‘best practice’ companies, we hope to derivemulti-purpose strategy points that are relevant for allbusinesses that compete in what we term ‘virtualmarkets.’

European Management Journal Vol 18 No 5 October 2000464

Characteristics of Virtual Markets

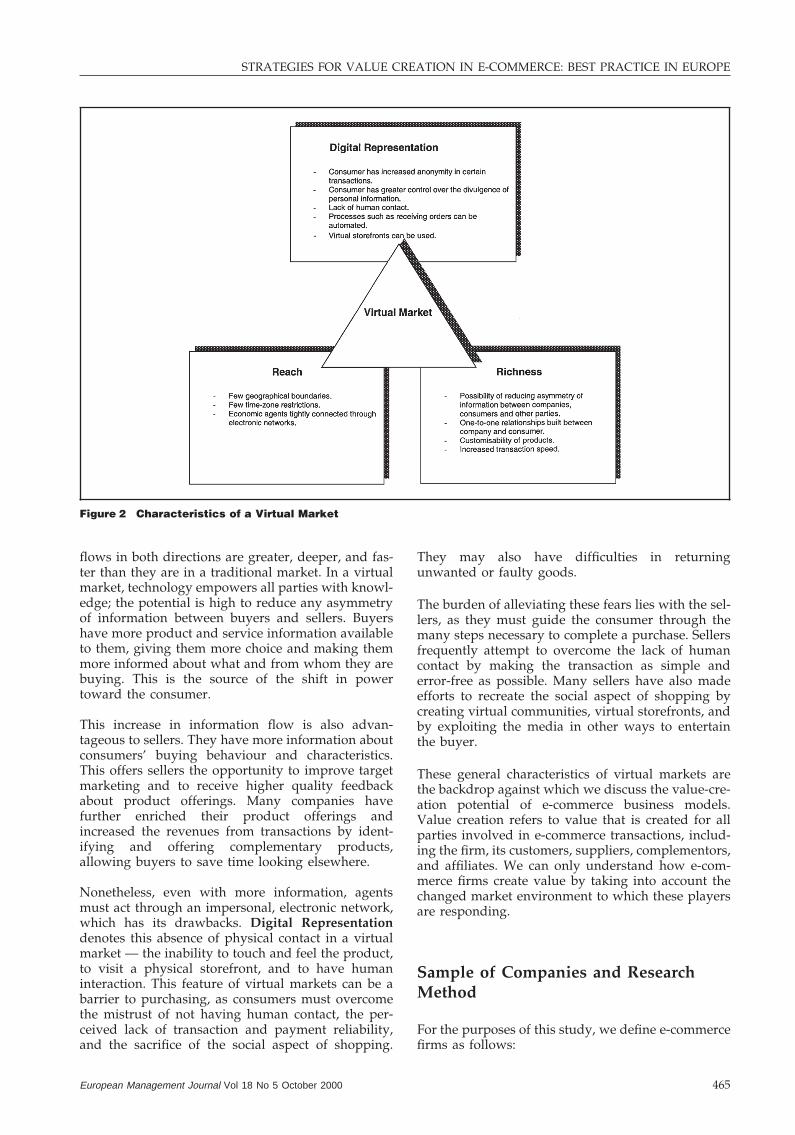

In the past, European businesses have been criticisedfor treating the Internet as merely another sales chan-nel that may enable access to new markets and cus-tomers, but that is fundamentally no different fromtraditional sales channels and thus requires nochange in the way business is conducted. Firms arenow beginning to realise that the virtual marketspace created by the Internet has unique character-istics that require identification and comprehensionso that business processes may be aligned accord-ingly. Figure 2 presents these unique characteristicsof a virtual market.

This figure refers to two distinguishing character-istics advanced by Evans and Wurster (1999): Reachand Richness. We add Digital Representation, as webelieve this aspect of a virtual market has not beenproperly addressed in the literature. We nextdescribe these three features in more detail.

Reach is defined as having the ability to connect witha large number of players or products; that is, to con-nect numerous suppliers, consumers, vendors, andindirectly, competitors and providers of complemen-tary services. The Internet supersedes physicalboundaries, and although it can be argued that somegeographic boundaries continue to exist because theexchange may involve the physical delivery of goods(often across borders), boundaries are at least greatlyreduced as a restricting factor in a virtual market.Unlike in a traditional market where ‘bricks and mor-tar’ are usually required, any vendor that can connectto the network can sell a product to connected con-sumers anywhere in the world. This feature hasresulted in the entry of a vast number of new players.Firms thus have a larger choice of suppliers, a largerbase of potential buyers, and a larger pool of possiblecompetitors. Consumers have fewer temporal andspatial restrictions and more choice, allowing themto conduct transactions at the time of their choosing.E-commerce has shifted the balance of power morein their favour relative to the power distribution intraditional markets.

Richness occurs in a virtual market since information

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

Figure 2 Characteristics of a Virtual Market

flows in both directions are greater, deeper, and fas-ter than they are in a traditional market. In a virtualmarket, technology empowers all parties with knowl-edge; the potential is high to reduce any asymmetryof information between buyers and sellers. Buyershave more product and service information availableto them, giving them more choice and making themmore informed about what and from whom they arebuying. This is the source of the shift in powertoward the consumer.

This increase in information flow is also advan-tageous to sellers. They have more information aboutconsumers’ buying behaviour and characteristics.This offers sellers the opportunity to improve targetmarketing and to receive higher quality feedbackabout product offerings. Many companies havefurther enriched their product offerings andincreased the revenues from transactions by ident-ifying and offering complementary products,allowing buyers to save time looking elsewhere.

Nonetheless, even with more information, agentsmust act through an impersonal, electronic network,which has its drawbacks. Digital Representationdenotes this absence of physical contact in a virtualmarket — the inability to touch and feel the product,to visit a physical storefront, and to have humaninteraction. This feature of virtual markets can be abarrier to purchasing, as consumers must overcomethe mistrust of not having human contact, the per-ceived lack of transaction and payment reliability,and the sacrifice of the social aspect of shopping.

European Management Journal Vol 18 No 5 October 2000 465

They may also have difficulties in returningunwanted or faulty goods.

The burden of alleviating these fears lies with the sel-lers, as they must guide the consumer through themany steps necessary to complete a purchase. Sellersfrequently attempt to overcome the lack of humancontact by making the transaction as simple anderror-free as possible. Many sellers have also madeefforts to recreate the social aspect of shopping bycreating virtual communities, virtual storefronts, andby exploiting the media in other ways to entertainthe buyer.

These general characteristics of virtual markets arethe backdrop against which we discuss the value-cre-ation potential of e-commerce business models.Value creation refers to value that is created for allparties involved in e-commerce transactions, includ-ing the firm, its customers, suppliers, complementors,and affiliates. We can only understand how e-com-merce firms create value by taking into account thechanged market environment to which these playersare responding.

Sample of Companies and ResearchMethod

For the purposes of this study, we define e-commercefirms as follows:

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

e-commerce firms are firms that derive a significant or rap-idly growing proportion of their revenues from trans-actions over the Internet. (Amit and Zott, 2000)

While this definition is broad in the sense that itincludes, for example, ISPs, it is narrow in that itexcludes many providers of Internet-related hard-ware or software who facilitate e-commerce, but whodo not themselves engage in the activity. Above all,an e-commerce firm is one that is directly involved intransactions (the exchange of goods, services, and/orinformation) using the Internet as a medium.

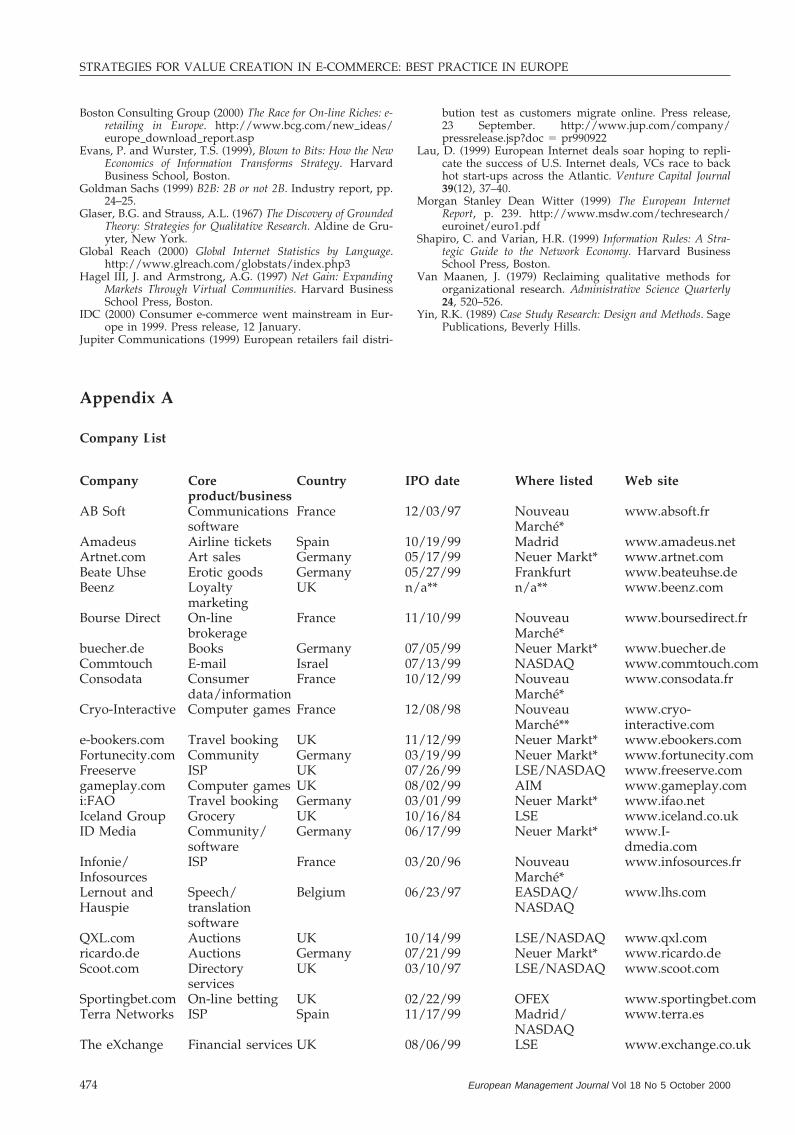

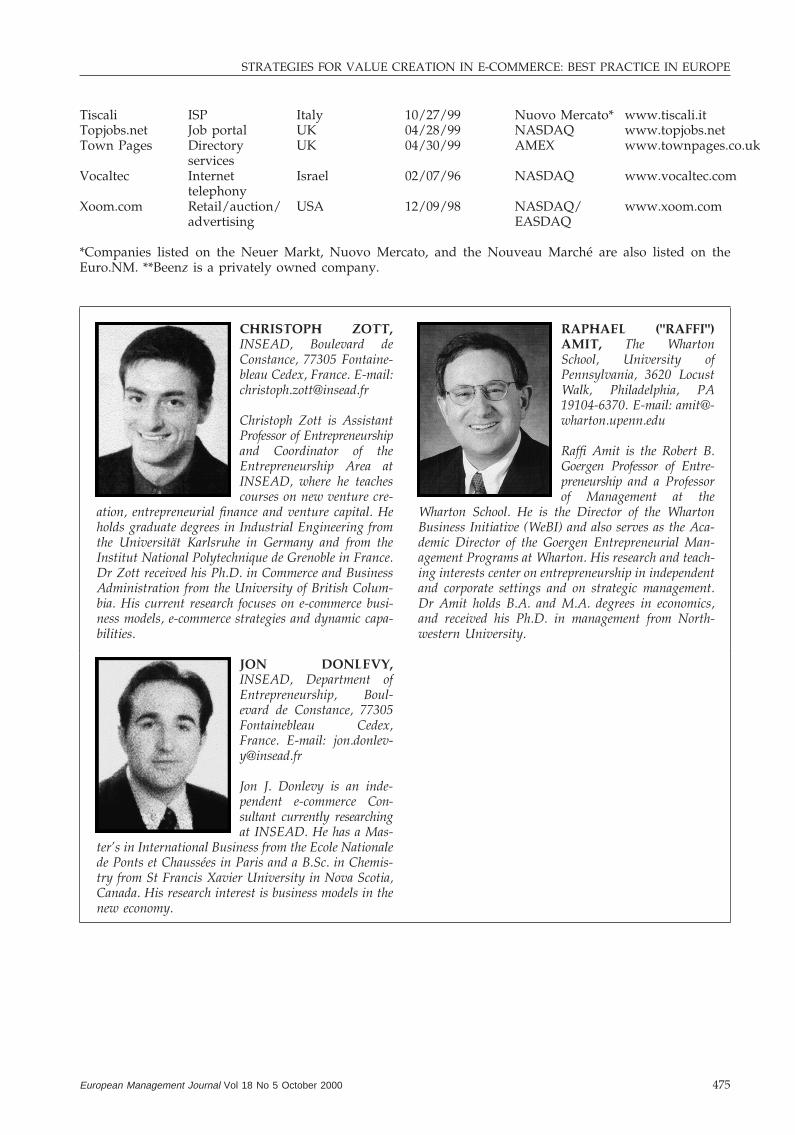

To uncover the business models of successful Euro-pean e-commerce firms, we studied the businesspractices of 30 European companies. To be includedin our sample, a firm had to:

(a) derive a significant or rapidly growing pro-portion of its revenues from the Internet(b) be a B-to-C, C-to-B, or C-to-C firm (see below)(c) be publicly listed(d) be European

The first criterion comes from our definition of an e-commerce firm. The second reflects our focus on e-commerce companies that involve the individualconsumer in the transaction. Such companies arereferred to as business-to-consumer (B-to-C), con-sumer-to-business (C-to-B) or consumer-to-consumer(C-to-C) companies (Goldman Sachs, 1999). Forexample, a C-to-C business is one that allows con-sumers to sell to other consumers (e.g. an auctionservice). We focused on these business types for asimple reason. When this project was undertaken,there were more mature public companies of thesetypes than there were of business-to-business (B-to-B) companies. These former firms comprised the firstwave of ‘dot-com’ companies that went public(Morgan Stanley Dean Witter, 1999).

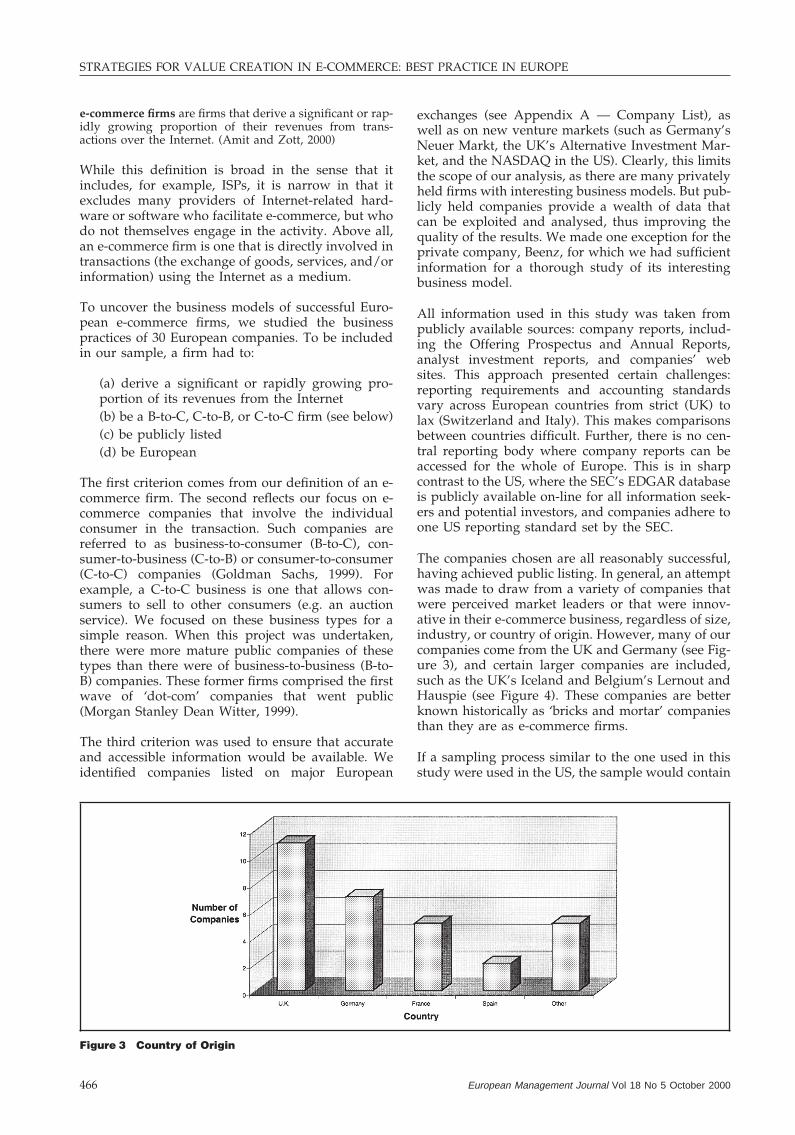

The third criterion was used to ensure that accurateand accessible information would be available. Weidentified companies listed on major European

Figure 3 Country of Origin

European Management Journal Vol 18 No 5 October 2000466

exchanges (see Appendix A — Company List), aswell as on new venture markets (such as Germany’sNeuer Markt, the UK’s Alternative Investment Mar-ket, and the NASDAQ in the US). Clearly, this limitsthe scope of our analysis, as there are many privatelyheld firms with interesting business models. But pub-licly held companies provide a wealth of data thatcan be exploited and analysed, thus improving thequality of the results. We made one exception for theprivate company, Beenz, for which we had sufficientinformation for a thorough study of its interestingbusiness model.

All information used in this study was taken frompublicly available sources: company reports, includ-ing the Offering Prospectus and Annual Reports,analyst investment reports, and companies’ websites. This approach presented certain challenges:reporting requirements and accounting standardsvary across European countries from strict (UK) tolax (Switzerland and Italy). This makes comparisonsbetween countries difficult. Further, there is no cen-tral reporting body where company reports can beaccessed for the whole of Europe. This is in sharpcontrast to the US, where the SEC’s EDGAR databaseis publicly available on-line for all information seek-ers and potential investors, and companies adhere toone US reporting standard set by the SEC.

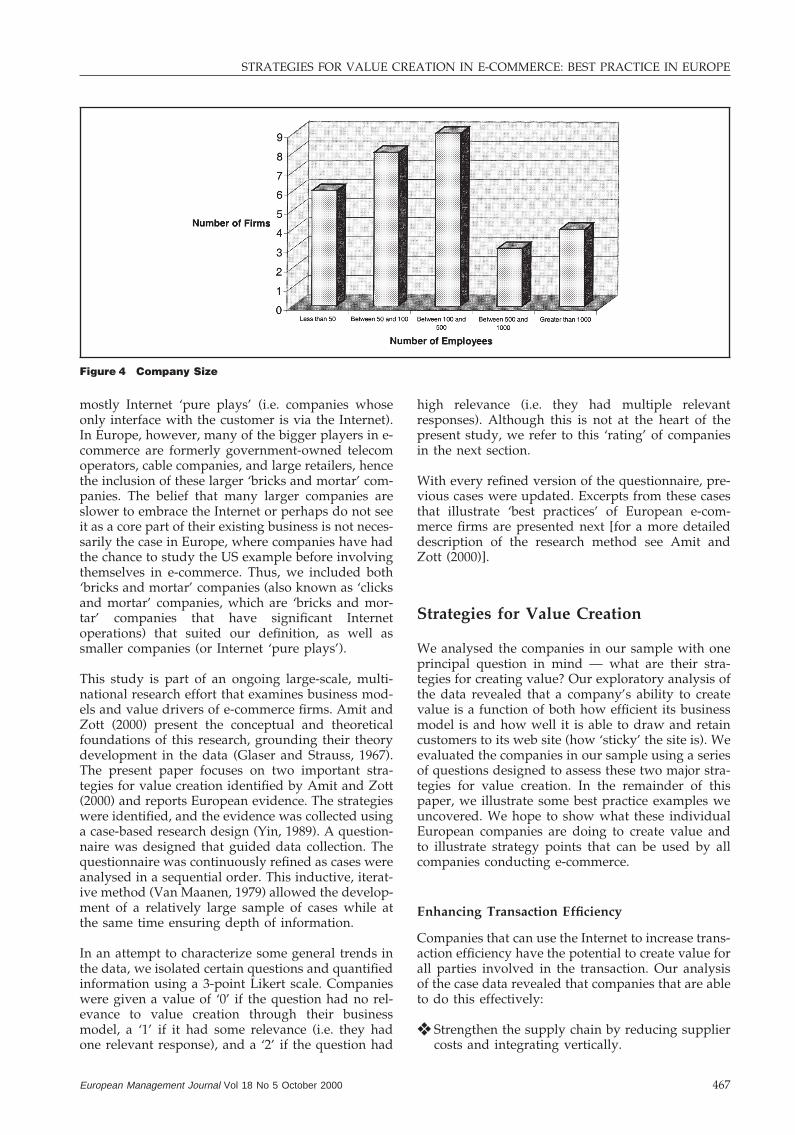

The companies chosen are all reasonably successful,having achieved public listing. In general, an attemptwas made to draw from a variety of companies thatwere perceived market leaders or that were innov-ative in their e-commerce business, regardless of size,industry, or country of origin. However, many of ourcompanies come from the UK and Germany (see Fig-ure 3), and certain larger companies are included,such as the UK’s Iceland and Belgium’s Lernout andHauspie (see Figure 4). These companies are betterknown historically as ‘bricks and mortar’ companiesthan they are as e-commerce firms.

If a sampling process similar to the one used in thisstudy were used in the US, the sample would contain

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

Figure 4 Company Size

mostly Internet ‘pure plays’ (i.e. companies whoseonly interface with the customer is via the Internet).In Europe, however, many of the bigger players in e-commerce are formerly government-owned telecomoperators, cable companies, and large retailers, hencethe inclusion of these larger ‘bricks and mortar’ com-panies. The belief that many larger companies areslower to embrace the Internet or perhaps do not seeit as a core part of their existing business is not neces-sarily the case in Europe, where companies have hadthe chance to study the US example before involvingthemselves in e-commerce. Thus, we included both‘bricks and mortar’ companies (also known as ‘clicksand mortar’ companies, which are ‘bricks and mor-tar’ companies that have significant Internetoperations) that suited our definition, as well assmaller companies (or Internet ‘pure plays’).

This study is part of an ongoing large-scale, multi-national research effort that examines business mod-els and value drivers of e-commerce firms. Amit andZott (2000) present the conceptual and theoreticalfoundations of this research, grounding their theorydevelopment in the data (Glaser and Strauss, 1967).The present paper focuses on two important stra-tegies for value creation identified by Amit and Zott(2000) and reports European evidence. The strategieswere identified, and the evidence was collected usinga case-based research design (Yin, 1989). A question-naire was designed that guided data collection. Thequestionnaire was continuously refined as cases wereanalysed in a sequential order. This inductive, iterat-ive method (Van Maanen, 1979) allowed the develop-ment of a relatively large sample of cases while atthe same time ensuring depth of information.

In an attempt to characterize some general trends inthe data, we isolated certain questions and quantifiedinformation using a 3-point Likert scale. Companieswere given a value of ‘0’ if the question had no rel-evance to value creation through their businessmodel, a ‘1’ if it had some relevance (i.e. they hadone relevant response), and a ‘2’ if the question had

European Management Journal Vol 18 No 5 October 2000 467

high relevance (i.e. they had multiple relevantresponses). Although this is not at the heart of thepresent study, we refer to this ‘rating’ of companiesin the next section.

With every refined version of the questionnaire, pre-vious cases were updated. Excerpts from these casesthat illustrate ‘best practices’ of European e-com-merce firms are presented next [for a more detaileddescription of the research method see Amit andZott (2000)].

Strategies for Value Creation

We analysed the companies in our sample with oneprincipal question in mind — what are their stra-tegies for creating value? Our exploratory analysis ofthe data revealed that a company’s ability to createvalue is a function of both how efficient its businessmodel is and how well it is able to draw and retaincustomers to its web site (how ‘sticky’ the site is). Weevaluated the companies in our sample using a seriesof questions designed to assess these two major stra-tegies for value creation. In the remainder of thispaper, we illustrate some best practice examples weuncovered. We hope to show what these individualEuropean companies are doing to create value andto illustrate strategy points that can be used by allcompanies conducting e-commerce.

Enhancing Transaction Efficiency

Companies that can use the Internet to increase trans-action efficiency have the potential to create value forall parties involved in the transaction. Our analysisof the case data revealed that companies that are ableto do this effectively:

❖ Strengthen the supply chain by reducing suppliercosts and integrating vertically.

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

❖ Provide a large array of products and services.❖ Make the transaction convenient for the consumer.❖ Allow the consumer to save time.❖ Reduce the asymmetry of information amongst

parties.

Strengthening the Supply ChainMost companies realise that the changes broughtabout by the Internet will require the reorganisationof their supply chain. We rated the companies in oursample on two measures relating to changes in theirsupply chain: how effectively they reduced suppliercosts, and the degree of integration of the supplychain.

There are many ways by which the Internet enablessuppliers to reduce costs, yet our results show thatfew companies are taking full advantage of the possi-bilities available to them. For example, with thespeed of information, companies can save inventorycosts by having more accurate stock level reports,updating them more rapidly, and even making pro-ducts to order. Obsolescence is reduced by usingthese strategies since the Internet provides companieswith a more efficient medium for testing and refiningnew products. Often, firms are able to gauge cus-tomer response instantly, and then can adjust boththe product and the pricing more rapidly. There aremany available commercial software packages thatallow companies to do this simply and inexpensively.

Often the best way of taking advantage of the rich-ness and reach in a virtual market to realise costreductions is to strengthen the ties that bind the linksin the supply chain, or integrating. The companieswe studied scored high on having a substantialdegree of supply chain integration, but for differentreasons. While some are outsourcing functions tothird parties but strengthening the links betweenthem, others are moving towards complete verticalintegration by occupying many places along thechain. Either way, the links are stronger — there isa greater richness of information flowing betweenparties. Companies that want to compete in virtualmarkets should re-examine their supply chains andquestion whether each function is being performedas efficiently as possible, and whether each link is asstrong as it can be.

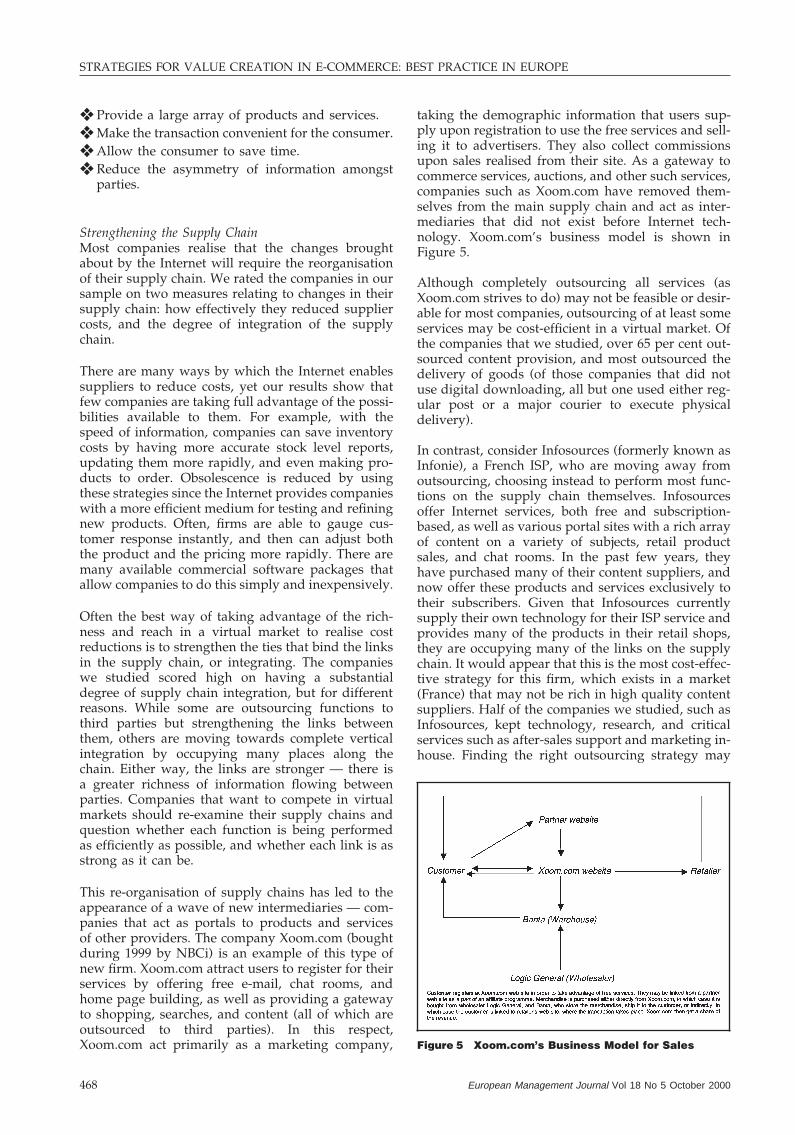

This re-organisation of supply chains has led to theappearance of a wave of new intermediaries — com-panies that act as portals to products and servicesof other providers. The company Xoom.com (boughtduring 1999 by NBCi) is an example of this type ofnew firm. Xoom.com attract users to register for theirservices by offering free e-mail, chat rooms, andhome page building, as well as providing a gatewayto shopping, searches, and content (all of which areoutsourced to third parties). In this respect,Xoom.com act primarily as a marketing company,

European Management Journal Vol 18 No 5 October 2000468

taking the demographic information that users sup-ply upon registration to use the free services and sell-ing it to advertisers. They also collect commissionsupon sales realised from their site. As a gateway tocommerce services, auctions, and other such services,companies such as Xoom.com have removed them-selves from the main supply chain and act as inter-mediaries that did not exist before Internet tech-nology. Xoom.com’s business model is shown inFigure 5.

Although completely outsourcing all services (asXoom.com strives to do) may not be feasible or desir-able for most companies, outsourcing of at least someservices may be cost-efficient in a virtual market. Ofthe companies that we studied, over 65 per cent out-sourced content provision, and most outsourced thedelivery of goods (of those companies that did notuse digital downloading, all but one used either reg-ular post or a major courier to execute physicaldelivery).

In contrast, consider Infosources (formerly known asInfonie), a French ISP, who are moving away fromoutsourcing, choosing instead to perform most func-tions on the supply chain themselves. Infosourcesoffer Internet services, both free and subscription-based, as well as various portal sites with a rich arrayof content on a variety of subjects, retail productsales, and chat rooms. In the past few years, theyhave purchased many of their content suppliers, andnow offer these products and services exclusively totheir subscribers. Given that Infosources currentlysupply their own technology for their ISP service andprovides many of the products in their retail shops,they are occupying many of the links on the supplychain. It would appear that this is the most cost-effec-tive strategy for this firm, which exists in a market(France) that may not be rich in high quality contentsuppliers. Half of the companies we studied, such asInfosources, kept technology, research, and criticalservices such as after-sales support and marketing in-house. Finding the right outsourcing strategy may

Figure 5 Xoom.com’s Business Model for Sales

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

require experimentation, and depends highly uponthe market conditions in which a company is compet-ing.

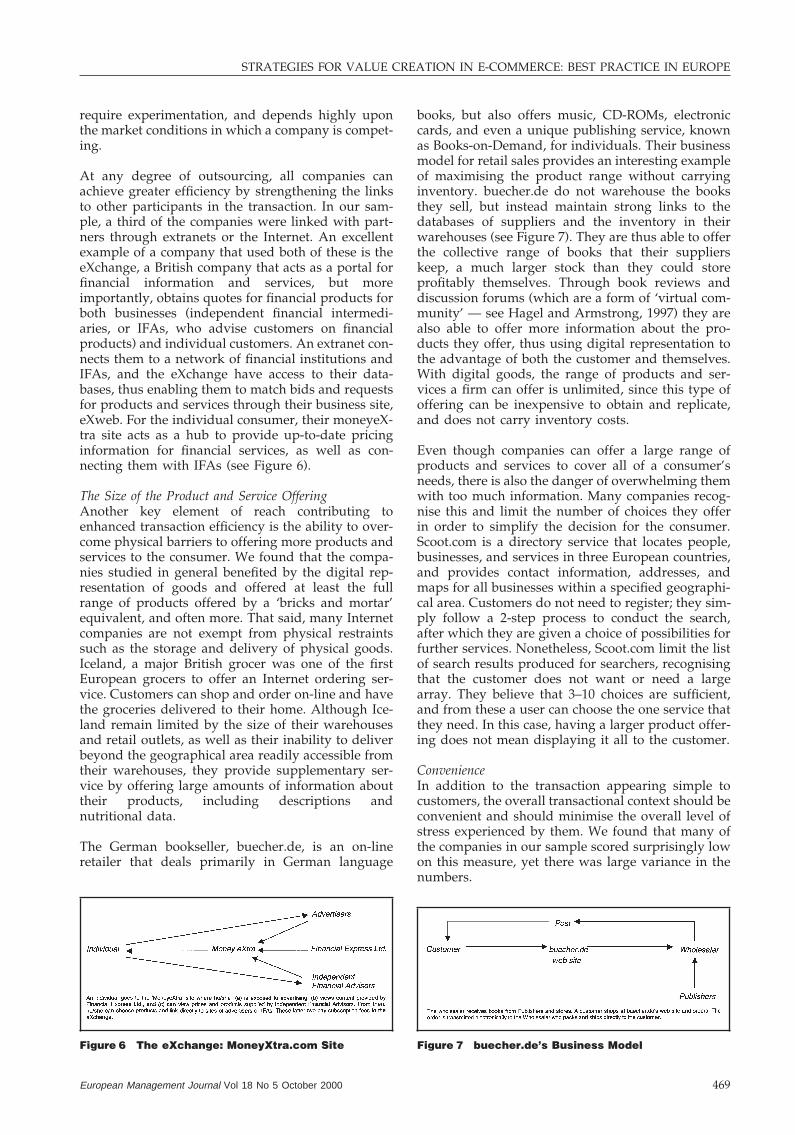

At any degree of outsourcing, all companies canachieve greater efficiency by strengthening the linksto other participants in the transaction. In our sam-ple, a third of the companies were linked with part-ners through extranets or the Internet. An excellentexample of a company that used both of these is theeXchange, a British company that acts as a portal forfinancial information and services, but moreimportantly, obtains quotes for financial products forboth businesses (independent financial intermedi-aries, or IFAs, who advise customers on financialproducts) and individual customers. An extranet con-nects them to a network of financial institutions andIFAs, and the eXchange have access to their data-bases, thus enabling them to match bids and requestsfor products and services through their business site,eXweb. For the individual consumer, their moneyeX-tra site acts as a hub to provide up-to-date pricinginformation for financial services, as well as con-necting them with IFAs (see Figure 6).

The Size of the Product and Service OfferingAnother key element of reach contributing toenhanced transaction efficiency is the ability to over-come physical barriers to offering more products andservices to the consumer. We found that the compa-nies studied in general benefited by the digital rep-resentation of goods and offered at least the fullrange of products offered by a ‘bricks and mortar’equivalent, and often more. That said, many Internetcompanies are not exempt from physical restraintssuch as the storage and delivery of physical goods.Iceland, a major British grocer was one of the firstEuropean grocers to offer an Internet ordering ser-vice. Customers can shop and order on-line and havethe groceries delivered to their home. Although Ice-land remain limited by the size of their warehousesand retail outlets, as well as their inability to deliverbeyond the geographical area readily accessible fromtheir warehouses, they provide supplementary ser-vice by offering large amounts of information abouttheir products, including descriptions andnutritional data.

The German bookseller, buecher.de, is an on-lineretailer that deals primarily in German language

Figure 6 The eXchange: MoneyXtra.com Site

European Management Journal Vol 18 No 5 October 2000 469

books, but also offers music, CD-ROMs, electroniccards, and even a unique publishing service, knownas Books-on-Demand, for individuals. Their businessmodel for retail sales provides an interesting exampleof maximising the product range without carryinginventory. buecher.de do not warehouse the booksthey sell, but instead maintain strong links to thedatabases of suppliers and the inventory in theirwarehouses (see Figure 7). They are thus able to offerthe collective range of books that their supplierskeep, a much larger stock than they could storeprofitably themselves. Through book reviews anddiscussion forums (which are a form of ‘virtual com-munity’ — see Hagel and Armstrong, 1997) they arealso able to offer more information about the pro-ducts they offer, thus using digital representation tothe advantage of both the customer and themselves.With digital goods, the range of products and ser-vices a firm can offer is unlimited, since this type ofoffering can be inexpensive to obtain and replicate,and does not carry inventory costs.

Even though companies can offer a large range ofproducts and services to cover all of a consumer’sneeds, there is also the danger of overwhelming themwith too much information. Many companies recog-nise this and limit the number of choices they offerin order to simplify the decision for the consumer.Scoot.com is a directory service that locates people,businesses, and services in three European countries,and provides contact information, addresses, andmaps for all businesses within a specified geographi-cal area. Customers do not need to register; they sim-ply follow a 2-step process to conduct the search,after which they are given a choice of possibilities forfurther services. Nonetheless, Scoot.com limit the listof search results produced for searchers, recognisingthat the customer does not want or need a largearray. They believe that 3–10 choices are sufficient,and from these a user can choose the one service thatthey need. In this case, having a larger product offer-ing does not mean displaying it all to the customer.

ConvenienceIn addition to the transaction appearing simple tocustomers, the overall transactional context should beconvenient and should minimise the overall level ofstress experienced by them. We found that many ofthe companies in our sample scored surprisingly lowon this measure, yet there was large variance in thenumbers.

Figure 7 buecher.de’s Business Model

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

Where companies did not score highly, the process tocomplete a transaction may be unnecessarily complexand may have had a large number of steps that acustomer must complete to become a buyer. A goodrule of thumb is that there should be no more thanthree clicks to a purchase — any more and the cus-tomer is likely to abort the purchase.

In addition to requiring too many clicks to completea purchase, some firms studied had the shoppingfunction as one amongst many of the choices offeredto consumers, forcing them to search extensivelybefore finding it. Others had overly graphical pagesslowing down page loading.

Another factor concerns the return of goods. Themedium itself makes the return of physical goodsmore difficult, requiring a buyer to repackage andresend the item. None of the companies studiedadequately addressed the issue of how the consumerwould go about this operation. Providing standard-ised forms or sending instructions might facilitatethis process.

Where companies did score highly was in takingadvantage of the reach and other aspects of the digi-tal representation in the virtual market. The Internetenables round-the-clock ordering. Although an ordermay not be processed until the following businessday, customers are free to shop at their convenience.Companies can provide sales service through morecomplete product descriptions and a list of frequentlyasked questions (FAQ). Companies that provide digi-tal goods and services can offer their products forinstant use by the consumer. Other methods used tomake the transaction context more convenient are theautomatic calculation of tax and delivery charges,and the tracking of delivery, mostly through links tomajor couriers.

The British travel company, e-bookers, shows someexamples of making the transaction convenient forthe customer. Their web site provides travel infor-mation and has a customisable search engine wherecustomers specify travel details including flight timesand their preferred airline. They are then given achoice of flights based on price and availability. Thecompany also leverages their on- and off-lineresources well: tickets are issued from their parentcompany, Flightbookers, who have ‘bricks and mor-tar’ offices in many countries throughout Europe.Customers can then have the ticket delivered, or pickit up at the nearest office at their convenience.

Time SavingAnother key to efficiency is whether or not the elec-tronic transaction allows the customer to save ontransaction time. The companies studied scoredhighly on this measure, mostly by reducing cus-tomers’ search times through clear colour-coded pro-duct categories, with a reasonable amount of sub-cat-egories, and search engines. Companies can further

European Management Journal Vol 18 No 5 October 2000470

reduce search time for the consumer by providing oroffering complementary products — as did half ofour companies. This feature could be either a part oftheir own product offering, or that of a partner,where the consumer may only have to click on a hyp-erlink to be taken to the complementor’s web site.

The German travel booking company i:FAO providesa good illustration of some of these concepts. Thecompany uses its booking software to offer servicessuch as travel information and transportation book-ings through a series of German language web sitesfor business and personal travellers. i:FAO ’s websites offer a customisable search engine and buyersare given a choice of options where they can specifytravelling times, seating choice, and other prefer-ences. Moreover, there are links from the home pageto complementary products such as travel infor-mation, weather reports, travel bookshops, and a cur-rency converter. Finally, if a user is already regis-tered, the buying process is facilitated and he/shereceives, by e-mail, fare updates on specific flightsspecified upon registration.

Asymmetry of InformationPerhaps most importantly, an on-line transaction canincrease the knowledge of both buyers and sellers.This point is critical since value can be created for allstakeholders in a transaction through the reductionof information-based market inefficiencies and asym-metries.

For example, investors are able to make efficient, andmore informed investment choices when they areable to access detailed company information on theInternet. Sellers of goods benefit from having moreinformation regarding the purchasers, their prefer-ences, and demographic backgrounds. With thisinformation, they may be better able to target bothproduct specifications and marketing efforts to betterserve the buyers and sell more. Indeed, the Internethas made information on customers a valuable com-modity; sellers may be able to use this informationfor their own purposes, or, with consumer per-mission, sell it to advertisers. Consumers themselvesare becoming increasingly aware of its value, oftenexpecting something in return. They, too, have accessto more information about the parties with whomthey are transacting, as well as more detailed productand pricing information.

A good example is Artnet.com, a German companyestablished in 1989 that has created a database of fineart auction prices. They are now an e-commerce firmwith a site that features access to the database, fineart auctions, and content in the form of an on-linemagazine, and establishes a community of like-minded users. The company offers consumers e-mailaccounts and the use of chat rooms upon registration,which is free. Individuals can state their preferencesand be notified by e-mail when items by a certainartist or of a certain type come up for auction. For

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

subscribing art galleries, Artnet.com offer free webpage hosting and access to the auctions and database.In their business model, Artnet.com are profiting byreducing the asymmetry of information between sel-lers and buyers in a business (fine art auctions) thathas traditionally profited from this asymmetry.

Listing the historical prices of items, which Art-net.com has done, is especially useful in stock pur-chasing and art auctions where historical prices ofteninfluence current market value. We believe that onceone company in an industry offers comprehensivepricing information, including that of their competi-tors, it will become a sine qua non. Consumers willdemand it, and should a given company not provideit, consumers will go elsewhere to find it. The stakeshave been increased with the use of ‘shopbots’ thatare able to search web sites of competing companiesand put together price lists for consumers, withoutthe consumer having to visit all the web sitesinvolved. As this technology improves (with theadvent of XML — Extensible Markup Language,which creates standards that can be read by intelli-gent agents), companies will have to find even morecreative ways of attracting price-sensitive customers.One way to do this is to develop ‘stickiness’ by whichcompanies make it costly for customers to switch toalternative firms. This is discussed in the followingsection.

Creating ‘Stickiness’ to Facilitate RepeatTransactions

One of the major strategies for value creation throughe-commerce is ‘stickiness’ — the ability of web sitesto draw and retain customers. This is of criticalimportance (Shapiro and Varian, 1999) — the compe-tition for ‘eyeballs’ (i.e. visitors to the site) will growas the number of consumers and vendors increases.The inflated marketing budgets of many e-commercecompanies reflect this argument and the bankruptcyof high profile Boo.com is a recent testament to thedifficulty companies have in supporting financiallythe marketing required to establish their name andcompete. A complementary, perhaps better way ofdriving repeat traffic is the creation of stickiness.

Stickiness creates value by increasing transaction vol-umes. We have identified a few effective means bywhich the companies in our sample create stickiness:

❖ Reward customers for their loyalty.❖ Personalise the product or customise the service.❖ Build virtual communities.❖ Establish their reputation for trust in the trans-

action.

We believe that the companies that scored high inthese categories are more likely to see customers

European Management Journal Vol 18 No 5 October 2000 471

make a purchase, return to a site, and stay for longerperiods of time when they do come back.

Loyalty ProgrammesLoyalty programmes are not a new idea as a meansof encouraging repeat purchasing. Rewarding buyerswith a form of compensation that can be accumulatedand redeemed for goods and services has long beenpopular in the ‘bricks and mortar’ world. Doing thisleads to more frequent purchasing by a given cus-tomer and greater sales volume in the long run. Jup-iter Communications (1999) estimates that 56 per centof on-line customers would buy more if they wereawarded loyalty points. Award programmes alsohelp establish a better relationship between the sellerand the buyer. In return for the reward, the seller canaccumulate information about the buyer’s purchas-ing pattern and preferences and is then able to servehim or her better in the future.

Most of the companies that we studied did not useloyalty programmes. Of all the questions in our sur-vey, this had the lowest overall score, which webelieve indicates that the technique is under-utilised.Globally, loyalty programmes are best knownthrough a few players in specific industries (e.g. air-lines that reward frequent fliers with prizes such asfree tickets). The Internet has seen the appearance ofcompanies such as the American company MyPointsand the European company Beenz, that areattempting to be the fastest movers amongst Internetloyalty programmes. They are creating commonpoint systems that can be sold to other companies,thereby creating a network of partners and a criticalmass of companies using the same system. Beenz, aBritish company expected to have an IPO in 2000, selltheir points known as ‘beenz’ to companies, who inturn use them to reward their customers for buyingcertain products, entering information, or visitingcertain areas of their web site. Companies can use thepoints as an incentive to move customers to sectionsof their web site or to help sell slow-moving pro-ducts. They can also accept ‘beenz’ as payment forobsolete items. In return, Beenz buys the points backat a less expensive rate. By increasing the number ofuser sites in the affiliation programme, the overallvalue to customers increases.

Personalisation of Product or Customisation of ServiceAnother means of keeping customers is by tailoringproducts or services to fit their particular personalityor tastes. Tailoring can take various forms — pro-ducts can be made to order, or personalised by theseller, or the interface (i.e. the web page that the cus-tomer sees when visiting the web site) can beadapted, or customised by the consumer. These tail-oring tactics are possible when the firm has adequateknowledge about the consumer, a by-product of therichness in the virtual market. Companies have theopportunity to build a closer relationship with thecustomer by using the information that the customergives upon registering or opening an account. There

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

are many ways that a company can put this infor-mation to value-creating use. It can be used to speedup the purchasing process (by calling up previousorders or payment information), to cross-sell otherproducts, and to increase the level of service that auser receives. Knowing a consumer’s tastes is also agood marketing tool. Targeted product offerings canbe made by selective banner advertising, or by send-ing e-mails notifying clients about special offers,enticing the consumer to return to the site and makea purchase.

Services can also be customised in exchange for per-sonal information about the customer. Examples ofthese services include gift registries (where users canregister at a site and choose from a list of gifts thatthey would like to receive), web page hosting, ande-mail accounts. Indirectly, personal informationabout the user can be gathered by the placement of‘cookies,’ a common means of recognising a repeatuser when he/she returns to a site. Although manyof the companies studied in this project use them,European Internet users might be apprehensiveabout their misuse, forcing companies to be forth-right about their installation and use or risk poorpublicity.

Surprisingly, there was markedly high variance inthe amount of personalisation used by the companieswe studied. Although most of the companies welooked at were using a high degree of personalis-ation, seven firms were using none, indicating thatthese sites may not be effectively using informationabout the customer.

Virtual CommunitiesCreating virtual communities (Hagel and Armstrong,1997) has benefits for both consumers and vendors.Consumers are able to share their experiences, accesscompeting vendors and ideas, and shape the contentthey receive. Vendors can better target their productofferings to specific audiences that have segmentedthemselves. Since users arrange themselves accord-ing to interests, communities can also be a means ofleveraging the reach of the Internet to improve com-munication flow.

The overall score for this category was moderateamongst the companies we surveyed, indicating thatonly a few firms, and only firms in specific industries,had created virtual communities. Of all the toolsavailable for creating a community, the most popularseems to be the chat room. In this model, people con-nect through the web site and communicate in realtime with other users with similar interests. Thesecommunities are so powerful that new businesseshave evolved around them whose web sites areamongst the stickiest on the World Wide Web. Forexample, I-D Media is a German media company thatconsults on web page design and offers active webpage software. In addition, they have created a chatcommunity called Cycosmos where users are able to

European Management Journal Vol 18 No 5 October 2000472

create virtual characters called avatars that personifytheir own characteristics and interests, while theusers themselves remain anonymous (an aspect ofDigital Representation in a virtual market). The com-pany believes that people will be more honest andforthright about their true interests under a mask ofanonymity. As users volunteer personal informationto become members of a community, the companycan use their profiles to send them targeted market-ing offers.

A more static version of the chat room concept is thebulletin board, where users can post messages toeach other or to the general community. Townpa-ges.net is a British on-line directory that provideslocal and national information in the UK on eventsand organisations. They also host electronic bulletinboards for small communities, which serve to uniteusers around their interest within a particular com-munity. The site can be accessed from PCs, but alsofrom strategically placed informational kiosksaround the UK. Users interact by posting messagesin forums based on various subjects according totheir interests.

The community concept is not limited to specialitysites. Any firm that is able to identify common inter-ests amongst users, and then provide a mediumwhere they can interact, share information, and buildinterest around the product, can build a community.Other forms of community include game playingcommunities and communities of knowledge. In theformer, users play against each other through theweb site, enter into tournaments, and join discussiongroups, sharing their opinions and experiences. Inthe latter, users ask and answer each other’s ques-tions, thereby sharing knowledge and reviewing pro-ducts or sellers, as is the case with the buyer andseller ratings seen at auction sites.

TrustThe issue of trust, particularly consumers’ perceptionof the lack of security in e-commerce, is one of thelargest impediments to e-commerce growth,especially in Europe, where it has been cited as oneof the main reasons consumers do not purchase on-line. This mistrust stems partly from the lack ofphysical representation, since buyers cannot touchand feel products on the Internet, and partly fromconcerns regarding credit card abuse. The companieswe studied scored well on this measure, indicatingthat most European e-commerce companies feel theneed to address consumers’ perceptions of security,both with safe payment processes and confidentialityof personal information.

Encrypting the exchange using a ‘secure service,’such as Netscape’s SSL protocol or Veri-Sign, hasbecome the standard method used by companies tosecure transactions. Most sites not only show the logoof the securing agency on their home page, but theyalso assure users of the security again when they are

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

making a purchase. Vendors benefit from these well-known securing brands, as consumers may be morelikely to trust a retailer who shows the brand on itssite. Another means of addressing the issue of trustis by confirming the purchase through e-mail. Thismay alleviate fears of technological failures blockingthe completion of a transaction.

Some firms are able to elicit trust by displaying a con-nection with a well-known partner or associatebrand, or by making a connection to their history asa ‘bricks and mortar’ operation. Affiliate networks(associate programmes where companies may posteach others’ banners on their sites, often in exchangefor a share of revenue for sales from transactionsoriginating at the partner site) are also popular. Thesepermit newer ‘pure plays’ that do not have strongbrand recognition to ally with an established brandand gain credibility by association — distinguishingthemselves from other newcomers in the Internetspace.

The French on-line brokerage, Bourse Direct, demon-strates some of these methods. As one of many on-line services that allow customers to buy and sellstocks, they were the first such company in France topublicly list. They gained instant credibility by trum-peting their partnership with XEOD, part of a majorFrench bank, Banque Populaire, who execute alltrades on their behalf. Further, users must open anaccount with Bourse Direct and use a password toaccess to open their accounts. Users are thus ensuredhigh levels of transaction safety and protection fromunauthorized access.

Consumers may be afraid of not only payment secur-ity, but also of the misuse of their personal infor-mation. European laws are strong in protecting themisuse of consumer data, but only 60 per cent of thecompanies we studied explicitly guarantee the con-fidentiality of consumer information and state thatthey will not misuse it, such as by selling it to compa-nies that send unsolicited e-mails (i.e. ‘spam’). Ifusers must register, they are often given a passwordso that others cannot enter the site under their name.Other sites do not require the user to give personalinformation, allowing anonymity, and thereforeinvolving no risk to the user. Companies can educatethe customer with information regarding the safetyof e-commerce, but only 10 per cent of those studiedfelt the need to address customers’ fears explicitly.

One company that does this effectively is Consodata,a French marketing firm that collects consumer datathrough mail-in and Internet surveys. The firm usescoupons and special offers to encourage consumersto fill out the surveys. Consodata states clearly to cus-tomers how this information will be used, and incon-veniences the customer as little as possible (e.g. cus-tomers fill out short surveys only twice every6 months upon visiting the web site, and then haveunlimited access to all special offers). Moreover, the

European Management Journal Vol 18 No 5 October 2000 473

company states that it is inspected frequently by theFrench Government Agency, la Commission Nation-ale de l’Informatique et des Libertes, to assure cus-tomers that their personal information is protectedfrom abuse.

Conclusion

In this paper, we have argued that e-commerce isfundamentally changing the way business is conduc-ted. We have anchored our arguments in the uniquecharacteristics of virtual markets: reach, richness, anddigital representation. Based on an exploratory studyof thirty successful European e-commerce firms, wehave identified two major strategies for value cre-ation, namely efficiency and stickiness. We have alsoillustrated best practices of European e-commercefirms by citing numerous examples of companies thateffectively leveraged these strategies.

We found that there are wide variations in the degreeto which successful European companies have achi-eved efficiency and stickiness in their business mod-els. Many companies excelled in certain facets ofthese multi-component constructs, for example, inbuilding trust in the transaction, allowing the con-sumer to save time, and finding creative ways ofattracting and keeping the consumer. However, mostof the companies studied focused on small subsets ofstrategies for value creation and did not make useof the full spectrum available. Strategies that weretypically under-utilised included decreasing theasymmetry of information between players, makingthe transactional context more convenient for theconsumer, and making greater use of loyalty pro-grammes and virtual communities. We believe thatthese represent untapped opportunities for e-com-merce companies to create value.

The identified strategies for value creation, and theexamples cited as ‘best practice’ in this paper shouldenable managers of e-commerce firms to gain a betterawareness of the competitive benchmarks that aredriving e-commerce in Europe today. They shouldalso help individual companies evaluate their ownperformance, and take steps to affect improvementswhere appropriate, by using the evidence presentedin this paper to enrich their own offering withnovel ideas.

Acknowledgements

The authors are grateful to the 3i Venturelab at INSEAD, andto the Snider Entrepreneurship Research Centre and theGoergen Entrepreneurial programmes at the Wharton Schoolfor generous financial support of this research.

References

Amit, R. and Zott, C.(2000) Value Drivers of E-commerce Busi-ness Models. INSEAD Working Paper 2000/06/ENT/SM, 6.

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

Boston Consulting Group (2000) The Race for On-line Riches: e-retailing in Europe. http://www.bcg.com/new ideas/europe download report.asp

Evans, P. and Wurster, T.S. (1999), Blown to Bits: How the NewEconomics of Information Transforms Strategy. HarvardBusiness School, Boston.

Goldman Sachs (1999) B2B: 2B or not 2B. Industry report, pp.24–25.

Glaser, B.G. and Strauss, A.L. (1967) The Discovery of GroundedTheory: Strategies for Qualitative Research. Aldine de Gru-yter, New York.

Global Reach (2000) Global Internet Statistics by Language.http://www.glreach.com/globstats/index.php3

Hagel III, J. and Armstrong, A.G. (1997) Net Gain: ExpandingMarkets Through Virtual Communities. Harvard BusinessSchool Press, Boston.

IDC (2000) Consumer e-commerce went mainstream in Eur-ope in 1999. Press release, 12 January.

Jupiter Communications (1999) European retailers fail distri-

Appendix A

Company List

Company Core Country IPO date Where listed Web siteproduct/business

AB Soft Communications France 12/03/97 Nouveau www.absoft.frsoftware Marche*

Amadeus Airline tickets Spain 10/19/99 Madrid www.amadeus.netArtnet.com Art sales Germany 05/17/99 Neuer Markt* www.artnet.comBeate Uhse Erotic goods Germany 05/27/99 Frankfurt www.beateuhse.deBeenz Loyalty UK n/a** n/a** www.beenz.com

marketingBourse Direct On-line France 11/10/99 Nouveau www.boursedirect.fr

brokerage Marche*buecher.de Books Germany 07/05/99 Neuer Markt* www.buecher.deCommtouch E-mail Israel 07/13/99 NASDAQ www.commtouch.comConsodata Consumer France 10/12/99 Nouveau www.consodata.fr

data/information Marche*Cryo-Interactive Computer games France 12/08/98 Nouveau www.cryo-

Marche** interactive.come-bookers.com Travel booking UK 11/12/99 Neuer Markt* www.ebookers.comFortunecity.com Community Germany 03/19/99 Neuer Markt* www.fortunecity.comFreeserve ISP UK 07/26/99 LSE/NASDAQ www.freeserve.comgameplay.com Computer games UK 08/02/99 AIM www.gameplay.comi:FAO Travel booking Germany 03/01/99 Neuer Markt* www.ifao.netIceland Group Grocery UK 10/16/84 LSE www.iceland.co.ukID Media Community/ Germany 06/17/99 Neuer Markt* www.I-

software dmedia.comInfonie/ ISP France 03/20/96 Nouveau www.infosources.frInfosources Marche*Lernout and Speech/ Belgium 06/23/97 EASDAQ/ www.lhs.comHauspie translation NASDAQ

softwareQXL.com Auctions UK 10/14/99 LSE/NASDAQ www.qxl.comricardo.de Auctions Germany 07/21/99 Neuer Markt* www.ricardo.deScoot.com Directory UK 03/10/97 LSE/NASDAQ www.scoot.com

servicesSportingbet.com On-line betting UK 02/22/99 OFEX www.sportingbet.comTerra Networks ISP Spain 11/17/99 Madrid/ www.terra.es

NASDAQThe eXchange Financial services UK 08/06/99 LSE www.exchange.co.uk

European Management Journal Vol 18 No 5 October 2000474

bution test as customers migrate online. Press release,23 September. http://www.jup.com/company/pressrelease.jsp?doc 5 pr990922

Lau, D. (1999) European Internet deals soar hoping to repli-cate the success of U.S. Internet deals, VCs race to backhot start-ups across the Atlantic. Venture Capital Journal39(12), 37–40.

Morgan Stanley Dean Witter (1999) The European InternetReport, p. 239. http://www.msdw.com/techresearch/euroinet/euro1.pdf

Shapiro, C. and Varian, H.R. (1999) Information Rules: A Stra-tegic Guide to the Network Economy. Harvard BusinessSchool Press, Boston.

Van Maanen, J. (1979) Reclaiming qualitative methods fororganizational research. Administrative Science Quarterly24, 520–526.

Yin, R.K. (1989) Case Study Research: Design and Methods. SagePublications, Beverly Hills.

STRATEGIES FOR VALUE CREATION IN E-COMMERCE: BEST PRACTICE IN EUROPE

Tiscali ISP Italy 10/27/99 Nuovo Mercato* www.tiscali.itTopjobs.net Job portal UK 04/28/99 NASDAQ www.topjobs.netTown Pages Directory UK 04/30/99 AMEX www.townpages.co.uk

servicesVocaltec Internet Israel 02/07/96 NASDAQ www.vocaltec.com

telephonyXoom.com Retail/auction/ USA 12/09/98 NASDAQ/ www.xoom.com

advertising EASDAQ

*Companies listed on the Neuer Markt, Nuovo Mercato, and the Nouveau Marche are also listed on theEuro.NM. **Beenz is a privately owned company.

CHRISTOPH ZOTT, RAPHAEL ("RAFFI")INSEAD, Boulevard de AMIT, The WhartonConstance, 77305 Fontaine- School, University ofbleau Cedex, France. E-mail: Pennsylvania, 3620 [email protected] Walk, Philadelphia, PA

19104-6370. E-mail: amit@-Christoph Zott is Assistant wharton.upenn.eduProfessor of Entrepreneurshipand Coordinator of the Raffi Amit is the Robert B.Entrepreneurship Area at Goergen Professor of Entre-INSEAD, where he teaches preneurship and a Professorcourses on new venture cre- of Management at the

ation, entrepreneurial finance and venture capital. He Wharton School. He is the Director of the Whartonholds graduate degrees in Industrial Engineering from Business Initiative (WeBI) and also serves as the Aca-the Universitat Karlsruhe in Germany and from the demic Director of the Goergen Entrepreneurial Man-Institut National Polytechnique de Grenoble in France. agement Programs at Wharton. His research and teach-Dr Zott received his Ph.D. in Commerce and Business ing interests center on entrepreneurship in independentAdministration from the University of British Colum- and corporate settings and on strategic management.bia. His current research focuses on e-commerce busi- Dr Amit holds B.A. and M.A. degrees in economics,ness models, e-commerce strategies and dynamic capa- and received his Ph.D. in management from North-bilities. western University.

JON DONLEVY,INSEAD, Department ofEntrepreneurship, Boul-evard de Constance, 77305Fontainebleau Cedex,France. E-mail: [email protected]

Jon J. Donlevy is an inde-pendent e-commerce Con-sultant currently researchingat INSEAD. He has a Mas-

ter’s in International Business from the Ecole Nationalede Ponts et Chaussees in Paris and a B.Sc. in Chemis-try from St Francis Xavier University in Nova Scotia,Canada. His research interest is business models in thenew economy.

European Management Journal Vol 18 No 5 October 2000 475