Embed Size (px)

Citation preview

Selling Your Value

Part 1 - Measuring the Impact Your Products/Services Provide

A friend of mine complained the other day that customers didn’t seem to value therelationship anymore, that they just wanted a lower price. This surprised me because Iknew he had good relationships with his customers and was not the lowest price supplier.

After a brief discussion, the real problem became clear: several of his customers had been given cost reduction goals. As a result he was told that he must reduce his price. Like many suppliers, he can no longer just talk about the value his company provides. He has to show it, in dollars, or he risks loosing the account or being forced to drop his price to keep it.

Measuring the Impact Your Products/Services Provide

The reason for this is simple: most customers don’t know how to measure total cost. And when they are given cost reduction goals they focus on what they can measure…price. Even when they know one supplier adds more “value”, they either don’t know how much more it is worth, or don’t have the ability to justify paying a higher price.

Yet value added services/products offer suppliers a significant competitive advantageprecisely because they can help reduce the customer’s costs, if the supplier can get the customer to see the impact.

Measuring the Impact Your Products/Services Provide

Getting the customers to see your value, whether from services or product features,comes down to four key points:

1. Document the impact your value provides the customer (Part 1). It is up to thesupplier to document their value because very few customers know how.2. Knowing who to sell your value to (Part 2). Identify those within the customer’sorganization who are responsible for the cost savings you provide. Selling thevalue to the right person (person responsible for that cost) is as important asshowing the impact.3. Show how your value helps customers to achieve their objectives (Part 3).Determine which company objectives, departmental goals and key performancemeasures are affected by your services/products.4. Differentiate your company in the proposal (Part 4). Too often the customer seeslittle or no difference between suppliers. In such cases it often reverts back toprice as the deciding factor.

Documenting Your Value

The first step in effectively using value to create a competitive advantage is to determine what it is you do that adds value to your customers. For example:

1. Vendor Managed Inventory (VMI)2. Introduction of a new product that reduces warranty costs3. A product substitution that results in energy savings4. Process/equipment design support5. Installation support6. Early project involvement7. Project management8. Testing9. Predictive/preventive maintenance10. E-commerce solutions

Documenting Your Value

Each of these events can be a value added opportunity with measurable results. A mistake suppliers make when trying to explain their value, is to promote their strengths and assets as the value added opportunity. While these strengths and assets often provide the means to add value, they are not themselves measurable.

Value Examples

To better understand this, consider the following examples:

1. Inventory. Many suppliers look at the fact that they have lots of inventory as avalue added service. But as hard as this sounds, having inventory does not addvalue. It does, however, offer the means for suppliers to provide certain valueadded services, such as: emergency deliveries, inventory reductions, or Just-In-Time deliveries (J.I.T.). This may sound like semantics, but it is not. You cannotmeasure the cost reductions that occur because you have inventory. But you canmeasure the cost reductions that the customer achieves because you were capableof doing an emergency delivery or providing J.I.T.

2. Salespeople. Having “knowledgeable salespeople” is not a value added event.But when the salesperson applies that knowledge he/she may be adding value,such as when the salesperson solves a downtime problem, finds ways to reduceenergy costs, or introduces a product that performs better. These actions addvalue that is measurable. The salesperson is the critical asset or strength thatallows the value to be added.

To effectively document and sell your value, you have to separate your company’sabilities that allow you to provide the value, from the services and products that actually make the customer more profitable. With that said, it should also be pointed out that these strengths and assets need to be part of your value proposition. They can help create the distinction between you and your competition, even when the competition offers the same value added services/products (see Part 4).

Value Examples

Once you have identified your value added product/services, you must determine theimpact these have on your customers’ profits. The impact on most customers will fallinto four primary Total Cost of Ownership categories:

1. Revenues: minimized downtime, increased production rates, or other changes thatincrease the customer’s sales.

2. Assets: reductions in possession costs when inventory, equipment or facilityrequirements are minimized.

3. Expenditures: reductions in the price paid for products/services, energy costs,freight, or other aspects of annual spend.

4. Process costs: reductions in personnel costs due to the elimination orminimization of tasks needing to be performed.

Value Examples

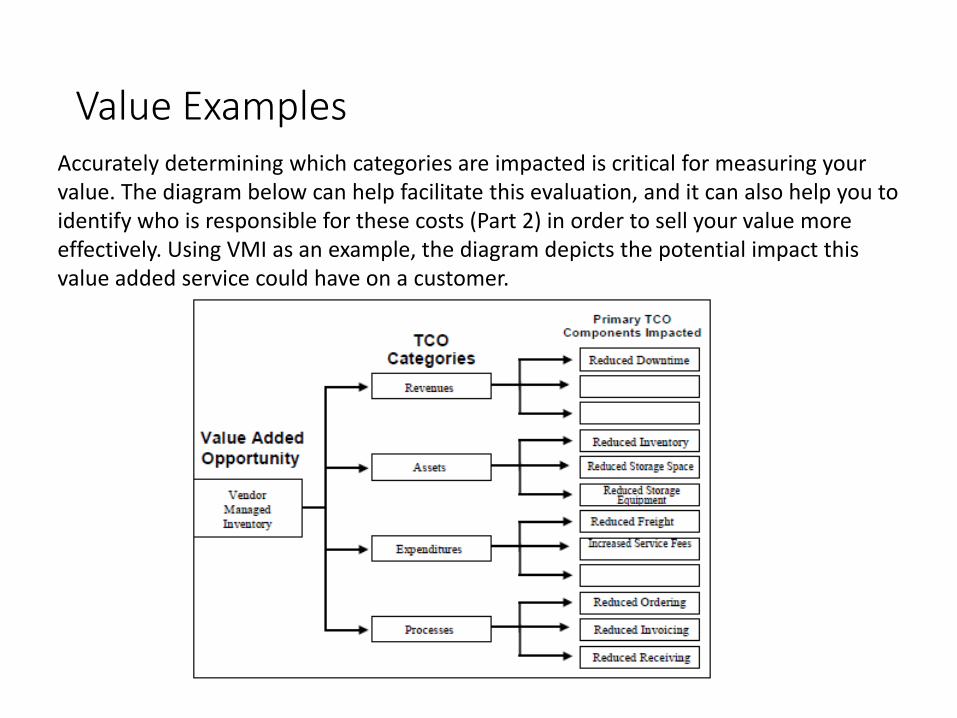

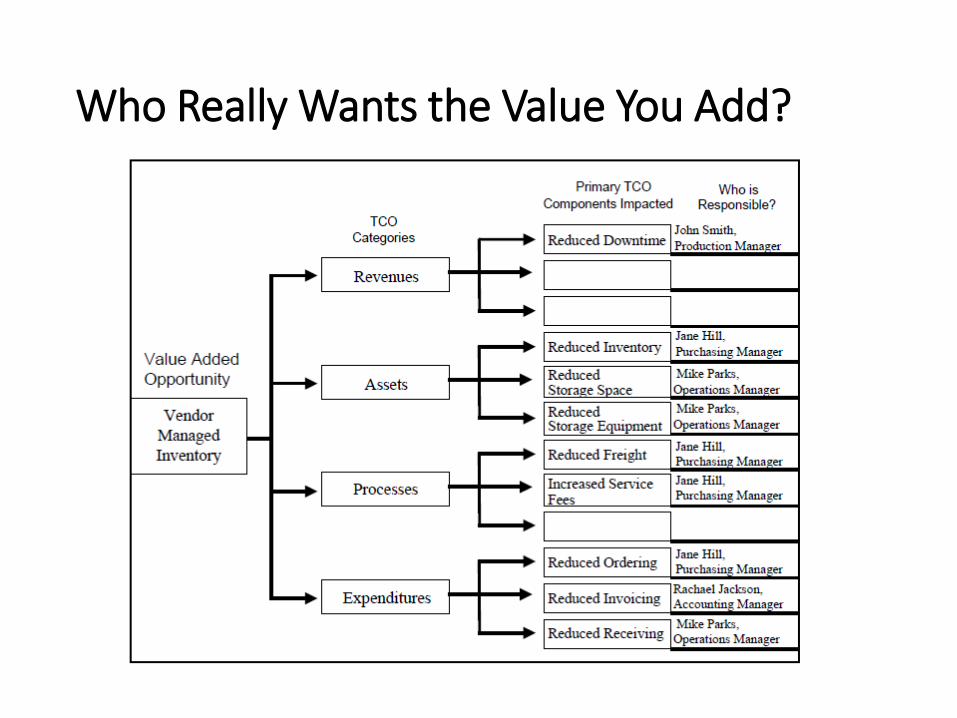

Accurately determining which categories are impacted is critical for measuring yourvalue. The diagram below can help facilitate this evaluation, and it can also help you toidentify who is responsible for these costs (Part 2) in order to sell your value moreeffectively. Using VMI as an example, the diagram depicts the potential impact thisvalue added service could have on a customer.

Value Examples

The diagram starts on the left side with the name of the value added opportunity being provided. The user then determines which TCO categories are affected, in this case all four. The user then moves to the right side, which is the most critical section. This section shows the Primary TCO Components Impacted (or the where the supplier impacts a customer’s profits).

To better understand the impact shown, an explanation of each TCO component isprovided below:

Revenues - In some cases (not all) VMI leads to reduced stock-outs. If thisreduces the customer’s downtime it could allow the customer to produce moreproducts.Assets – VMI can result in reduced inventories. This in turn could also reducestorage space and storage/handling equipment requirements (minimal impact inmost cases).Expenditures – When providing VMI services, the suppliers usually consolidatesshipments. Fewer shipments can lower overall freight costs. Additionally, somesuppliers charge for this service, which should also be shown.Processes – Consolidated shipments lead to lower processing costs such as:ordering, invoicing, and receiving/stocking.

Value Examples

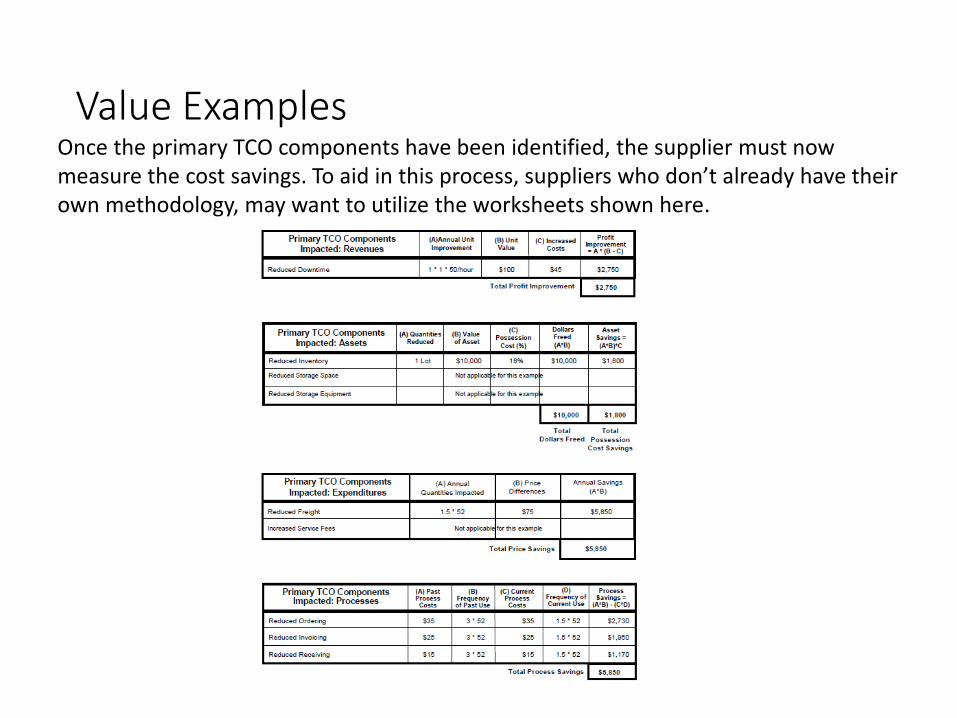

Once the primary TCO components have been identified, the supplier must now measure the cost savings. To aid in this process, suppliers who don’t already have their own methodology, may want to utilize the worksheets shown here.

Value Examples

You will notice that the first column of the worksheets and the last column of the impact diagram show the same information (TCO components impacted). The impact diagram is used to identify what is impacted and the worksheets are used to measure the dollar value of the impact. A explanation of each TCO component, and of the calculations / data in the worksheets, is provided below:

Reduced DowntimeThe supplier was able to eliminate one downtime from occurring:A. 1 - downtime reduced* 1 hour - production time saved (based on previous downtime situations)• 50 - units produced per hour

B. $100 - selling price for each unit being produced

C. $45 - raw material cost for each additional unit produced

Result: A $2,750 increase in profit.

Value Examples

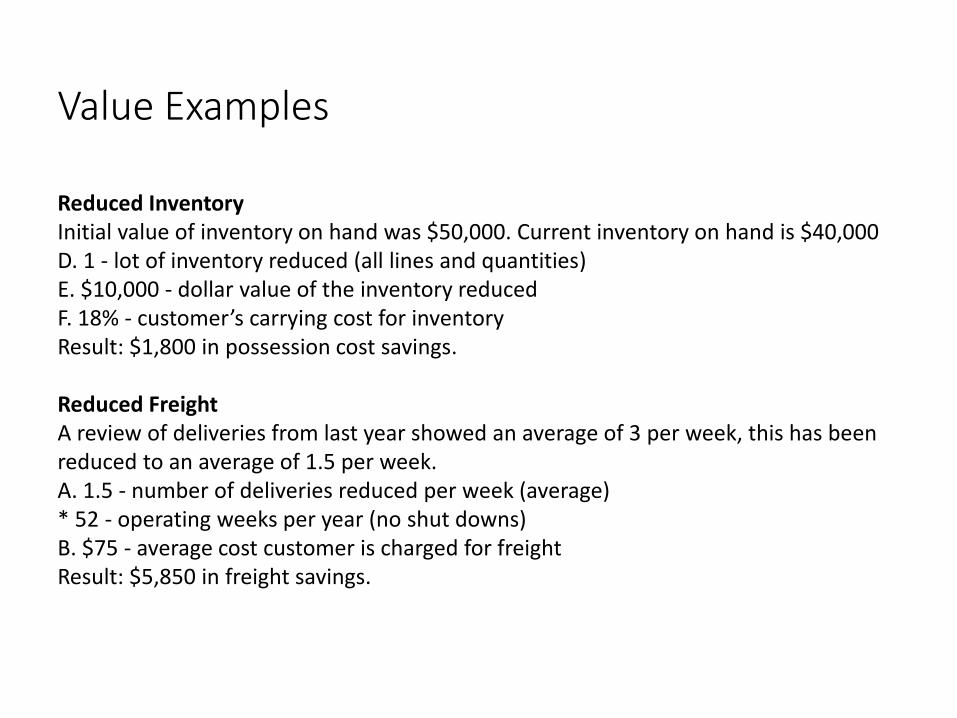

Reduced InventoryInitial value of inventory on hand was $50,000. Current inventory on hand is $40,000D. 1 - lot of inventory reduced (all lines and quantities)E. $10,000 - dollar value of the inventory reducedF. 18% - customer’s carrying cost for inventoryResult: $1,800 in possession cost savings.

Reduced FreightA review of deliveries from last year showed an average of 3 per week, this has beenreduced to an average of 1.5 per week.A. 1.5 - number of deliveries reduced per week (average)* 52 - operating weeks per year (no shut downs)B. $75 - average cost customer is charged for freightResult: $5,850 in freight savings.

Value Examples

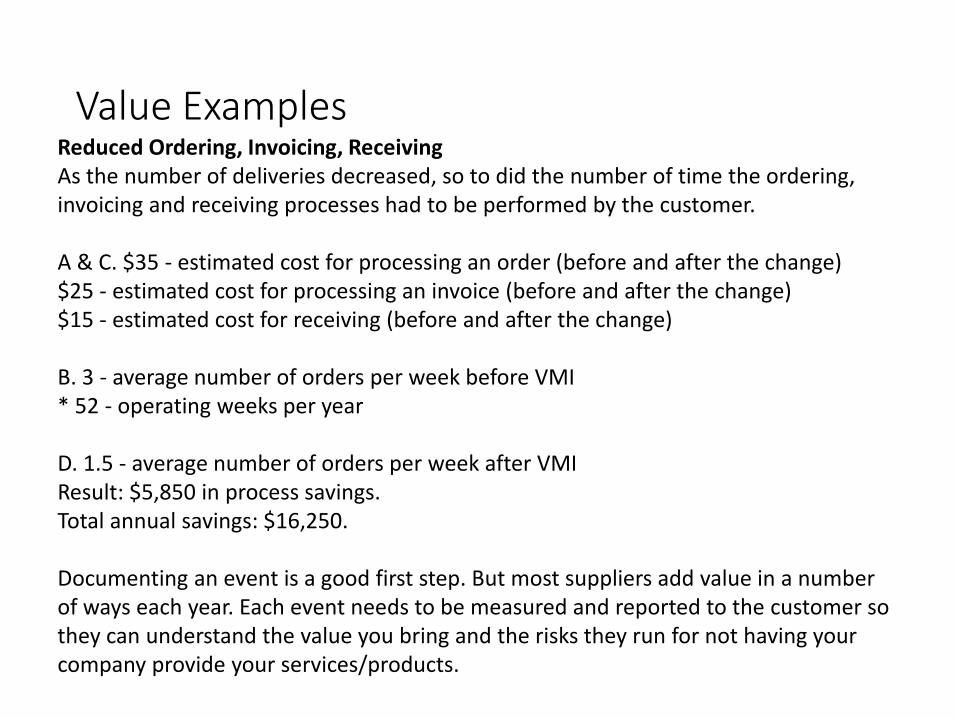

Reduced Ordering, Invoicing, ReceivingAs the number of deliveries decreased, so to did the number of time the ordering,invoicing and receiving processes had to be performed by the customer.

A & C. $35 - estimated cost for processing an order (before and after the change)$25 - estimated cost for processing an invoice (before and after the change)$15 - estimated cost for receiving (before and after the change)

B. 3 - average number of orders per week before VMI* 52 - operating weeks per year

D. 1.5 - average number of orders per week after VMIResult: $5,850 in process savings.Total annual savings: $16,250.

Documenting an event is a good first step. But most suppliers add value in a number of ways each year. Each event needs to be measured and reported to the customer so they can understand the value you bring and the risks they run for not having your company provide your services/products.

Value Examples

While documenting your value in this way may not stop your customer from demanding a lower price, it may make them hesitant about loosing your support. And if a supplier can estimate the value of additional opportunities, these may provide you with an alternative to lowering your price when the customer comes to you looking for cost savings.

But documenting your value can do more than just allow you to retain accounts. It canalso help you to penetrate accounts based on the potential savings you offer. And forthose suppliers who add a lot of value, it can be a critical means of achieving acompetitive advantage.

Value Examples

Selling Your Value:Part 2 – Who Really Wants the Value You Add?

• In Part 1 of this series: Measuring the Impact Your Products/Services Provide, we discussed the need to show the dollar impact that the customer achieves through your value, and how to measure it. In today’s marketplace this is critical. Customers are putting more and more pressure on prices to reduce their costs, and documenting your value you can help create a competitive advantage that minimizes pricing as the only way to save your customer money. But only if you “sell” the value you add to the “right” person.

Who Really Wants the Value You Add?

Almost every supplier has been confronted at some point by a customer that does not see the value added as real, even when the impact from the value provided has beendocumented. When this happens the sale often reverts back to price as the decidingfactor as to whom the customer will buy from. This is often a signal that the salesperson may be selling their value to the wrong person!

Each cost that you affect has the potential of impacting a different person. It could besomeone in purchasing, maintenance, operations, quality control, engineering, or even sales & marketing. And much of the value a supplier adds impacts these areas, not purchasing.

In which case you may be trying to sell someone who is responsible for the price paid,into paying more so that someone else in the organization would benefit. Often a verytough sales call, and the buyer’s response is that the value is great, but you have to drop your price.

To sell your value effectively you need to know who to sell it to, and it may not beanyone you are calling on today. Consider the Vendor Managed Inventory (VMI)example we used in Part 1 of this series. We created an Impact Diagram that showed us what costs were impacted by VMI. We have now added a new section on the right side to help us to identify “who” we should be selling our value to (see diagram below).

Who Really Wants the Value You Add?

Who Really Wants the Value You Add?

Most people sell to the people who “buy” the product or to those that use it. And theyshould. But when you are trying to get someone to buy on the impact from the value you add, you need to sell to the person who is “responsible” for that cost. This is what the section on the right side of the Impact Diagram is used for - to help you identify whom you should be selling your value to.

Ask yourself whose budget is affected by the Primary TCO Component Impacted? Orbetter yet, ask your customer. A user may want a product/service because it makes their job easier, and as such they should be part of your sales plan. But that person may not be responsible for the maintenance budget. If it saves time and money, the personresponsible for that budget should be part of your sales plan as well. That is the personyou sell your value to.

Most value added events impact a number of people, and not just because there are anumber of TCO Components. In the example above, only one person is shown as beingresponsible for each component, but often it could impact several people’s budgets.Downtime for example is an issue important to both maintenance and productionmanagers.

Who Really Wants the Value You Add?

Who Really Wants the Value You Add?

You’ll also notice the emphasis on management. Value generally has to be sold up the organization, and this can create problems. Most managers do not want to spend a lot of time with salespeople. They have subordinates for this. But these same managers will spend time with a person that talk less about products, and more about problem solving and profit improvements.

While many salespeople have excellent product knowledge, they often lack the skills to discuss Profit & Loss Statements, and total cost issues. Managers want to see the impact, not the product/service (that comes later). The impact is the results.

• Discuss the amount of increased product that can be produced and the profit

impact from this increase.

• Show how utility costs will be reduced and the savings that will be achieved

because of this.

• Talk about how their inventory will be reduced by 30% and the savings that will

accrue.

Discuss profits. Then when they ask for details on how this can be achieved, that’s when you discuss your product/service features and benefits. The “hook” for management is the impact on costs/profits, or how you help them accomplish their objectives (Part 3 of this series). While it may be the product or service that saves them the money, their focus is the savings, and it should yours as well when selling to these people.

But only the savings they are responsible for. And as you add different types of value,you impact different people. For example:

1. Operations Manager through Vendor Managed Inventory (VMI)2. Sales Manager because a new product reduced their customer’s complaints3. Purchasing Manager when a product substitution resulted in energy savings4. Engineering Supervisor through equipment design support5. Production Manager when you provided installation support6. Project Manager through early project involvement7. Quality Control Supervisor by providing testing8. Maintenance Supervisor through predictive/preventive maintenance9. I.T. Manager by providing E-commerce solutions

Who Really Wants the Value You Add?

Obviously these examples would impact many others that just the one person shown here as was seen in the VMI example earlier. The point is how well do you sell to thesepeople? How often are you calling on them? And what do you talk to them about:products or profits/problem solving?

These people influence the purchase. If they see it in their best interest, they can makethe sale happen. And if the savings are big enough, they will. But they are not going towant to hear from us every time we add a little value. Which means we have to combine the value we provide into cost savings reports to get their attention and make them want to see us.

There are three reports you should consider using:1. Event report – provided immediately after the value is provided2. Quarterly report – summarization of the value provided that quarter3. Annual report – total cost improvement for the year and relationship

Who Really Wants the Value You Add?

The event report is the documentation of what you did and the dollar impact that resulted. This should be provided to the customer within a few days of providing theservice/product that reduced their total cost. Often this is a projection of savings that will accrue over a year. But it is important to estimate the savings now, because if you wait the perceived value diminishes over time. People leave, change positions, or just forget how important that product/service was to them. The estimate can always be revised later if needed.

Also, by documenting your value as it occurs and providing key people with a copy, itreminds them of how valuable you are to them. Many companies will also put it in your file, which can be useful if your contacts do change. Generally though this report stays in the lower levels of the customer’s organization, unless the impact was significant. At which point you may want to copy the managers you impacted.

The quarterly report however needs to go everyone you impacted. Meaning those people responsible for the costs reduced. It should consist of a summary page that lists the events, the total dollar impact for each event and a graph of the savings. Then, if appropriate, include one-page descriptions of each event.

Who Really Wants the Value You Add?

It is surprising how many managers upon reviewing such a report will want to discusswhat you did, how you measured it and what’s next. So few people provide them thisthat even minimal detailed reports get a lot of exposure. But while they may call you todiscuss it with them, it is usually just a print out that you send them.

The annual report is different. When possible try to present it to the managersresponsible for the costs impacted. This can be a series of one-on-one meeting, but a 30- minute review prior to lunch with everyone present works great. It would help if youbrought in one of your top managers too (customer person like to see your company’smanagement committed too). The added benefit of having everyone present is that itcreates a comfort level across the company about working with you and a commonunderstanding of the total value you provide.

Using these reports works well for retaining accounts where you are providing value. Itshows the decision makers how beneficial you are, and the risk they run if they looseyour services. But providing a different report, a proposal, of the potential savings youcan provide can help you penetrate accounts as well (this is discussed in Part 4 of thisseries).

Who Really Wants the Value You Add?

While not every customer will be willing to meet with you, many will. But even withthose that are not willing to meet, providing these reports to the right people can helpmake the difference between keeping and losing an account. Many suppliers add value. Documenting it and getting it to the right people can help create the competitive advantage you need to win/keep that account.

Who Really Wants the Value You Add?

Part 3 - Helping Customers to Achieve Their Objectives

In Part 2 of this series we looked at who you should be selling your value to, based on where your value added products and services were impacting your customer’s costs. The ability to show different customer personnel the dollar impact you have on the costs they are responsible for is a very powerful way to sell. But this dollar impact is only part of the benefit your value may be providing. In Part 3 we want to look at another aspect: how your products and services can help your customers to accomplish their objectives.

Helping customers to accomplish their objectives is an integral part of the sales efforts for many suppliers, and is often the first step in selling the value they add. But to effectively sell this side of your value, you need to understand the objectives of each of your contacts (a contact is anyone you sell to now or anyone you identified as being impacted by your value).

This is similar to knowing who you are impacting with the cost side of your value (Part 2). Discussing inventory reduction with someone who is responsible for reducing downtime may not get you very far. They may see the inventory reduction as a threat to their goals in the same way purchasing often sees higher prices as a negative even if it reduces overall costs.

Helping Customers to Achieve Their Objectives

This is similar to knowing who you are impacting with the cost side of your value (Part2). Discussing inventory reduction with someone who is responsible for reducingdowntime may not get you very far. They may see the inventory reduction as a threat to their goals in the same way purchasing often sees higher prices as a negative even if it reduces overall costs.

There are a number of issues important to each contact that you could affect, most ofwhich fall into these five categories:

• Objectives/goals: Corporate, departmental, individual goals the contact is held accountable for accomplishing (what’s in it for the company).

• Key Performance Indicators (KPI): how the contact is evaluated internally.• Incentives: often tied to KPIs, but with the focus on how you impact their

compensation package (what’s in it for your contact).• Projects: major efforts they are involving in implementing. • Problems: What is going wrong for them.

Helping Customers to Achieve Their Objectives

• Knowing what is important to each contact allows you to determine how you can help them through the products and services you offer. Most of us do this informally, but in such cases we can forget some of the issues each contact discussed with us. And as the sale becomes more complex, meaning you have to sell to a number of different people, the need to plan the sales call in terms of the objectives you impact becomes more critical, because too often the salesperson talks about the same value to everyone.

• To win larger contracts or become the supplier of choice, you often need to help different contacts achieve different objectives. Discussing the same points, such as inventory reduction, does little good when they are not responsible for that goal. You need to focus on the issues important to that contact and then summarize the other benefits.

Helping Customers to Achieve Their Objectives

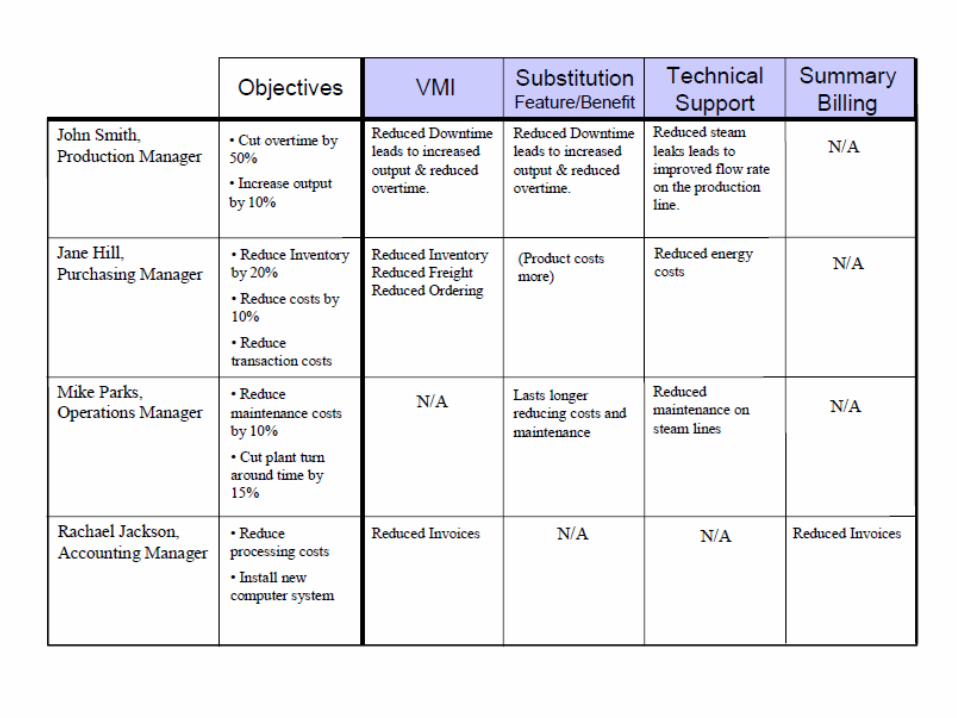

A simple tool to use to help accomplish this is to list your contacts on the left side of a matrix and the objectives of each of these people immediately to the right. Then across the top, list all of the Value Added opportunities you offer this account (both provided and proposed). As you discover the issues important to your customer identify how your value could impact them to accomplish these objectives.

Helping Customers to Achieve Their Objectives

Over time, you will discover that a single value added opportunity can impact various people in different ways, and that the impact generally varies based on their position in the organization. This is true both in terms of their department, as seen above, but also based on the level of your contact within the organization:

Users, those people who actually use the products or services you provide, are generally more interested in the features and benefits, and how this can make

their job easier. They can often influence small purchasing decisions, but usually have limited influence over larger contracts.

The Commodity/Service Group, those people who you identified in Part 2, are more concerned with the dollar and objective impact you can have on their position. They are usually higher in the organization and have a much greater influence over large purchasing decisions.

The higher in the organization you go, the more important it becomes to show them both the impact to their position, as well as the impact on the entire organization in terms of costs and objectives.

Helping Customers to Achieve Their Objectives

Utilizing this method is not about getting a single order from the customer, it is about creating a relationship that survives over time or about winning a major contract. It is focus on getting each contact to see you as the supplier of choice because you are making their job easier and/or because you are helping to reduce costs and achieve objectives for which they are responsible.

Profiling the position can also help you if someone new takes over. Generally that person will be facing the same issues as your previous contact. If you have tracked how you have helped the other person in that position, it shows the new contact the risk of not having you to work with, and allows you to show them what addition impact you can have that can make them successful in this position. Additionally, if a position is profiled in one location, the needs are often transferable to other locations. This can help you to penetrate that account in other cities / plants.

This brings us to the sales steps you use to win the account. Every salesperson has what is known as a Sales Cycle Plan. It may be an informal plan, but there are steps everyone follows because they have found it works for them. While the steps vary between people and organizations, they generally follow the same basic path: Make contact with a few key people, find out their needs, determine what you can provide to satisfy those needs, present your product/service and ask for the order.

Helping Customers to Achieve Their Objectives

The same basic steps can be used to sell the value you add as well, but they need to be slightly adjusted, because you are not asking for an order, you are building/strengthening the relationship or trying to win a major contract. You can continue to utilize your own sales cycle, but use the steps below as a ways to identify how you can improve the success rate in selling your value.

1. Investigate: Determine what your customers’ produce, the products/services

currently being utilizing, potential or current problems, market/competitive issues,

and other factors where your company could make a difference.

2. Analyze: Determine what products/services you provide that could reduce their

costs and/or help them to accomplish their objectives, measure the impact, and

determine who would be impacted by your value.

3. Endorsement: Get each contact to agree to the impact on their position. Just their

TCO Component (Part 1 & 2) and their objectives. Get them to want your value

on an individual basis.

4. Proposal: Present the entire impact to the customer and offer a “next step” for

achieving the impact you are proposing.

Helping Customers to Achieve Their Objectives

You have to work through the Sales Cycle with each contact. Sometimes everything can be accomplish in one visit, and for those contacts higher in the organization, should be done with a minimal of visits. These people are often busy and do not respond well to frequent “interruptions”. For these customers, much of the information can be gathered from your other contacts prior to visiting them.

The first two steps in the above sales cycle focus on gathering the information needed in order to measure the impact you bring the customer, and to be able to present your solutions (Part 4), and there are a number of places where you can get this information. Many suppliers already have detailed data about transactions, prices, and product capabilities. This can provide you with a good place to start. But additional data can be gathered from industry publications, websites (the customer’s, industry, and competitors’ sites), price lists (competitors’ and current customer’s), estimates/data from customer personnel, other accounts, annual reports, maintenance/product logs, and many other sources.

Helping Customers to Achieve Their Objectives

The best source for the information is of course your customer, but often the person you are dealing with does not know the information you need, or they know only a piece of the information and you have to get the rest somewhere else. Using estimates or industry figures can generally start the process, and then the customer can correct any minor point. For example they might use 23% not a 20% carrying cost.

You want this correction to occur during the Endorsement stage. This stage is like a mini-proposal, and you want each contact comfortable and supporting the impact on their position, both in terms of dollars and objectives, so that during the proposal stage objections are at a minimal.

The Proposal stage can then be more of an effort to bring everyone to consensus that you are the right supplier, both for their position and for their company. That is what the fourth and final part of this series is about: How to make the proposal to your customer in such away that they see the dollar and objective impact your company provides and to select you as the supplier of choice.

Part 4 - Developing a Unique Selling Proposition

In part 2 of this series we talked about retaining key accounts by showing them the value we have already added and the impact this has had on their total operating costs. In the final part of this series we want to look at how you present potential savings as a means for gaining more business or when the current account is threatened.

To do this, we need to develop a unique selling proposition. We need to be able to propose how we can save the customer more money than they would get from either the lower price your competitors are offering or to meet the cost reduction goals the customer is trying to achieve, as well as how we can help them to accomplish their objectives.

Developing a Unique Selling Proposition

To build this proposal we first need to determine what our savings goal for the customer needs to be. If we already have the account they may have told us the goal, such as the need to reduce costs by 10%, or that another supplier approached them and offered to save them $20,000 per year. And if you are bidding on a contract you typically have a feel by how much your competitors will try to under cut your price.

Example 1: Setting A Savings Goal. If the customer expects to achieve $20,000 in cost reductions we could use this amount as our target goal. However, we may want to aim for a higher amount, such as $30,000, in case the customer rejects some of our savings as “soft” thereby ensuring we do not loose the account.

Once you have determined your savings goal, and if you have helped this account save money in the past, you need to make a decision: do you include past events that will continue to save them money as part of this goal?

Developing a Unique Selling Proposition

Doing so creates a risk for you because past savings, even if they continue to keep costs lower, are often not accepted and could therefore result in the savings goal not being reached. However, sometimes there are not enough new value added opportunities identified to allow you to reach the savings goal without the past events being included.

Keep in mind that past savings should almost always be shown. But if new opportunities can be utilized, without significantly impacting your profits, you have a greater likelihood of winning the contract by not including these savings in this goal. These previous savings can be used as a risk factor. Meaning show these to the customer as costs that can creep back in if they do not continue to utilize your products and services.

Example 2: Past Savings. Let’s assume that you have provided technical support, energy audits, emergency deliveries and several product substitutions in the past. These amounted to $15,000 in annual savings for the customer, and the customer sees two-thirds of this potentially creeping back in without you as the supplier, resulting in a $10,000 risk factor. So if your competition is offering $20,000 in savings, and the customer is likely to incur another $10,000 in costs because they loose this value, the net savings offered by your competitor is really only $10,000.

Developing a Unique Selling Proposition

Remember that both the past and new savings are typically only important to the people who are responsible for those costs (discussed in part 2 of this series). It is therefore critical to make the proposal to the people impacted so they can influence the supplier selection internally.

There are two types of meeting you might have to present your total cost proposal. The first, and most common, are one-on-one meetings with key personnel. The second format is to meet with all, or most, of the key personnel in one large meeting. The second one has the advantage of getting everyone on the same page at the same time, but is often harder to pull off. The first format has the advantage of allowing you to customize the presentation to each individual, but often does not create the synergy of the larger meeting.

Developing a Unique Selling Proposition

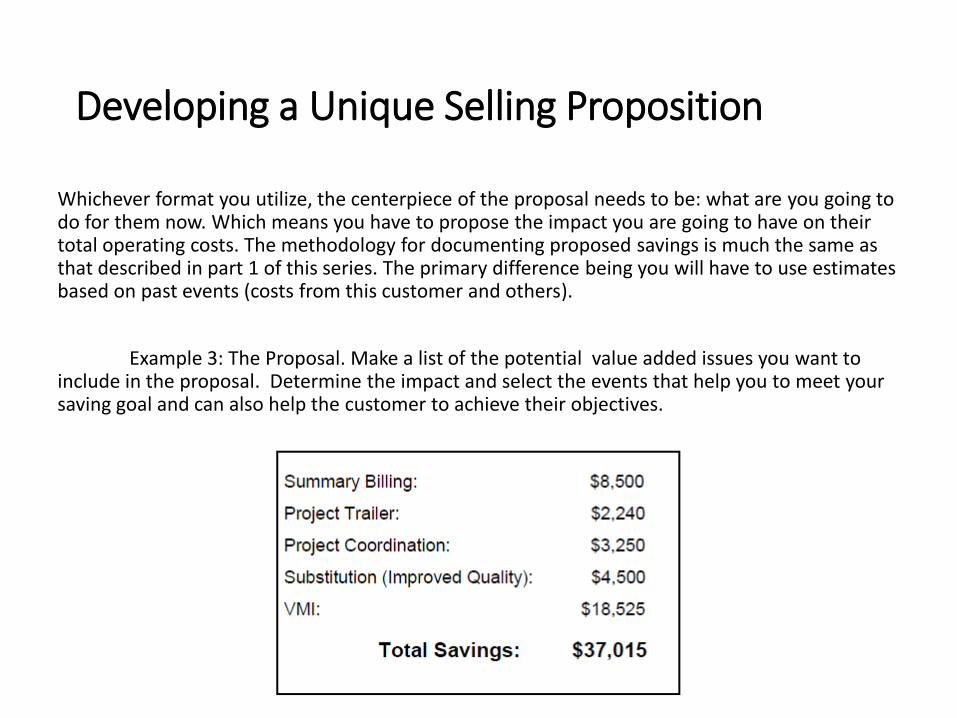

Whichever format you utilize, the centerpiece of the proposal needs to be: what are you going to do for them now. Which means you have to propose the impact you are going to have on their total operating costs. The methodology for documenting proposed savings is much the same as that described in part 1 of this series. The primary difference being you will have to use estimates based on past events (costs from this customer and others).

Example 3: The Proposal. Make a list of the potential value added issues you want to include in the proposal. Determine the impact and select the events that help you to meet your saving goal and can also help the customer to achieve their objectives.

Developing a Unique Selling Proposition

The estimated total savings will generally get their attention, but they will want more details on each event. As each event is presented, explain where the primary savings will be coming from (for example the costs identified from the impact diagram for VMI used in part 1). If you determined who is responsible for these savings (part 2), you can also discuss the costs important to each person. This in turn can help you focus on the objectives you can impact for them (part 3), allowing you to tie your value to accomplishing both a lower cost and providing solutions to their other needs.

Developing a Unique Selling Proposition

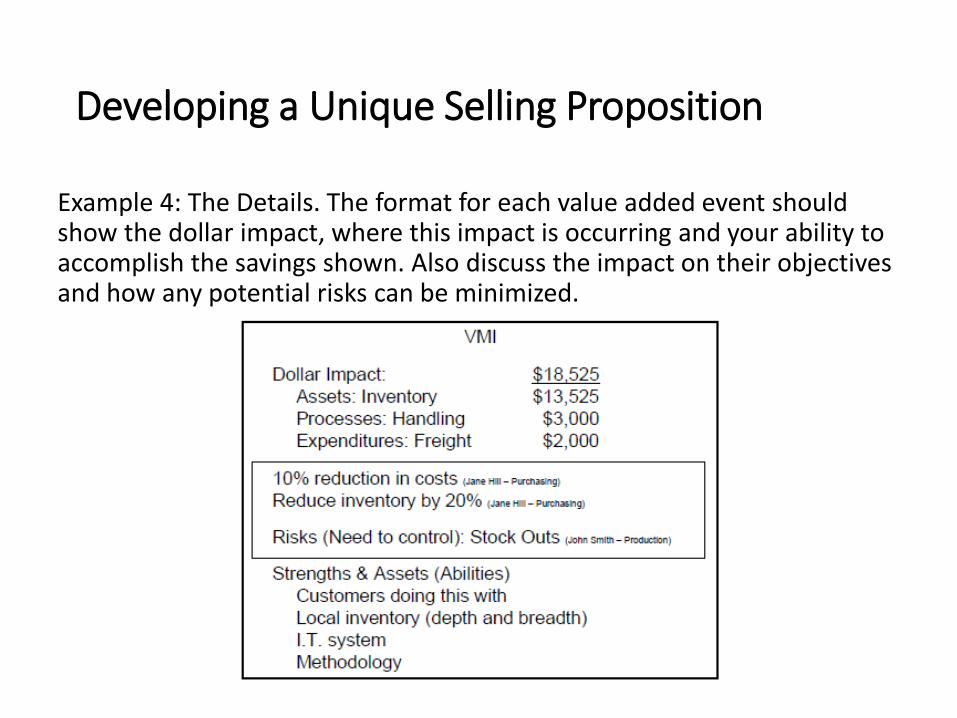

Example 4: The Details. The format for each value added event should show the dollar impact, where this impact is occurring and your ability to accomplish the savings shown. Also discuss the impact on their objectives and how any potential risks can be minimized.

Developing a Unique Selling Proposition

Do not include the objectives impacted in the presentation material. They are discussed, but not shown (the box around the objectives indicates the timing for when to discuss them). At the same time, any potential risks the customer might face are also discussed and how your company can minimize these risks.

Knowing the risks the customer might face for each event is critical. These risks become their objections or concerns to your proposal. If you identify them ahead of time, and prepare for them, the presentation is much more effective because the customer is more comfortable with your abilities to control these risks.

Once the savings, objectives and risk are covered, point out the key strengths and assets you bring which can ensure them that you can accomplish the proposed opportunities. It is important to tie your abilities to accomplishing the value added opportunity as you explain each event. This format is then repeated for each opportunity in your proposal.

Developing a Unique Selling Proposition

A common mistake when making proposals is to spend too much time in the beginning of the presentation talking about your strengths and assets, before you make the proposal. This creates two major drawbacks. First, the customer wants to know what you are going to do for them. Talking about your abilities before you talk about what this means for them, can result in the customer not paying attention. The second drawback is that the customer may not link your abilities to the solution you offer.

As such it is important to discuss your abilities as each opportunity is presented. However, a short introduction of your company and some of your key strengths can help the customer get a better understanding of who you are if some of the people in the room do not know you well. But the operative word for such an introduction is “short”.

Once the savings are discussed, you can spend additional time at the end of the proposal providing additional details on your strengths and assets as a means to distinguish your company from other suppliers. The timing is critical, because it follows the way the customer thinks: What are you going to do for me (proposal) and can you actually do what you say you can do (abilities: strengths and assets).

Developing a Unique Selling Proposition

Remember to leave time at the end of the proposal for a quick discussion on how to move forward. Proposals of this nature are generally used for longer-term relationships and not day-to-day selling situations. As such, “asking for the order” rarely gets you anything, because there are generally many people and issues being impacted, and if a contract is involved, approval often has to come from higher in the organization.

However, while asking for the order may not help, offering quick, low commitment, next step plans can move the contract forward in your favor, or be used as a means for getting into a new account. The proposal creates the desire for your products and services. Once the desire is created, offer them ways to get this value added without signing a contract by having a series of “next steps” that allows the customer to start getting the benefits you are offering immediately. In return, you start getting more of the business.

Developing a Unique Selling Proposition

Make sure the steps are simple enough to implement without a great deal of effort from the customer, and provide documented savings as you go along. This savings is what they need to show their management. And it is your value that provides it, not a lower price.

This is the real benefit to documenting your value: the ability to focus the customer on total cost as the deciding factor, not price. The benefit for you is the ability to maintain higher margins while distinguishing your company from competitors.