Embed Size (px)

Citation preview

1

SYNOPSIS

Vivimed Labs Ltd engages in the

specialty chemicals & pharmaceuticals

businesses in India.

During the quarter ended, the robust

growth of revenue is increased by

8.20% to Rs.928.50 million.

Vivimed Labs Ltd has acquired Uquifa,

a 75-year-old manufacturer of pharma

APIs and intermediates with

operations in Spain and Mexico.

Vivimed has offices in India, China,

Europe & USA, with manufacturing

facilities focused around Hyderabad

city in India.

Vivimed Labs has floated three

overseas subsidiaries, either directly/

through its subsidiary companies.

Net Sales and PAT of the company are

expected to grow at a CAGR of 32%

and 44% over 2010 to 2013E

respectively.

Years Net sales EBITDA Net Profit EPS P/E

FY 11 3100.97 556.30 277.63 27.32 14.83

FY 12E 4034.73 815.85 395.91 28.41 14.25

FY 13E 4841.68 985.28 496.86 35.66 11.36

Stock Data:

Sector: Pharmaceutical

Face Value Rs. 10.00

52 wk. High/Low (Rs.) 413.00/212.50

Volume (2 wk. Avg.) 34000

BSE Code 532660

Market Cap (Rs. in mn) 5643.27

Share Holding Pattern

1 Year Comparative Graph

BSE SENSEX Vivimed Labs

C.M.P: Rs. 405.00 Target Price: Rs. 466.00 Date: March 24th 2012 BUY

Vivimed Labs Ltd Result Update: Q3 FY 12

2

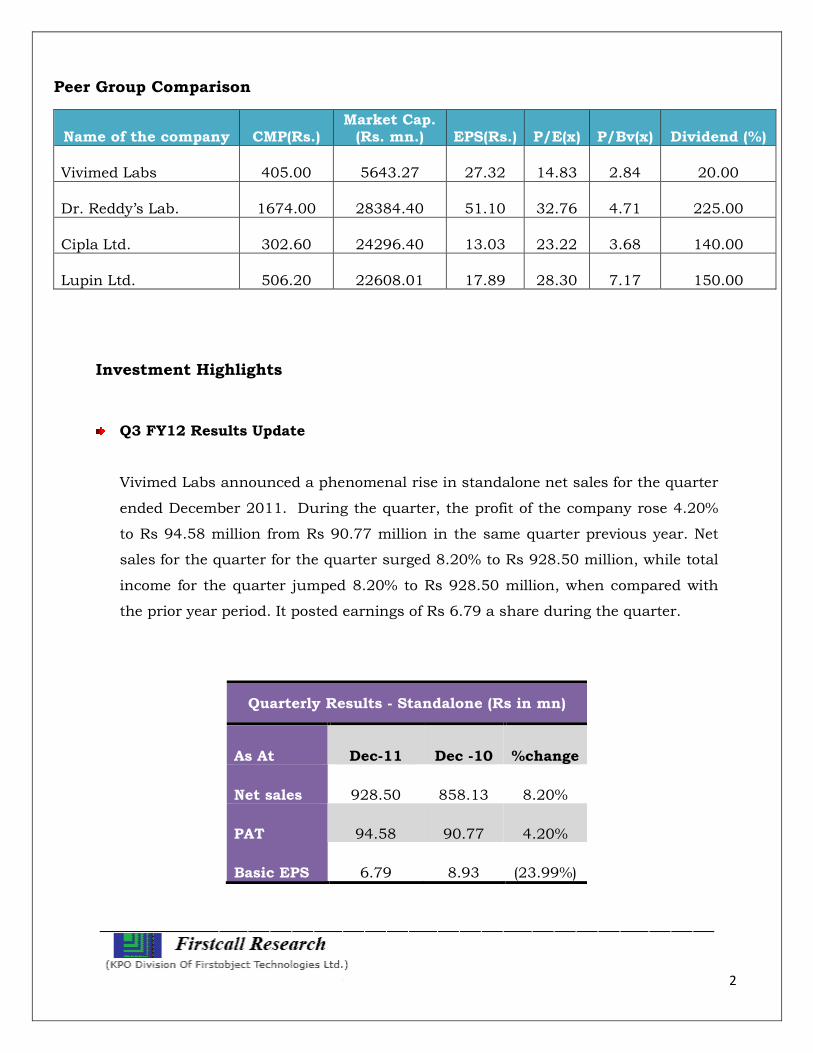

Peer Group Comparison

Name of the company CMP(Rs.) Market Cap. (Rs. mn.) EPS(Rs.) P/E(x) P/Bv(x) Dividend (%)

Vivimed Labs 405.00 5643.27 27.32 14.83 2.84 20.00

Dr. Reddy’s Lab. 1674.00 28384.40 51.10 32.76 4.71 225.00

Cipla Ltd. 302.60 24296.40 13.03 23.22 3.68 140.00

Lupin Ltd. 506.20 22608.01 17.89 28.30 7.17 150.00

Investment Highlights

Q3 FY12 Results Update

Vivimed Labs announced a phenomenal rise in standalone net sales for the quarter

ended December 2011. During the quarter, the profit of the company rose 4.20%

to Rs 94.58 million from Rs 90.77 million in the same quarter previous year. Net

sales for the quarter for the quarter surged 8.20% to Rs 928.50 million, while total

income for the quarter jumped 8.20% to Rs 928.50 million, when compared with

the prior year period. It posted earnings of Rs 6.79 a share during the quarter.

Quarterly Results - Standalone (Rs in mn)

As At Dec-11 Dec -10 %change

Net sales 928.50 858.13 8.20%

PAT 94.58 90.77 4.20%

Basic EPS 6.79 8.93 (23.99%)

3

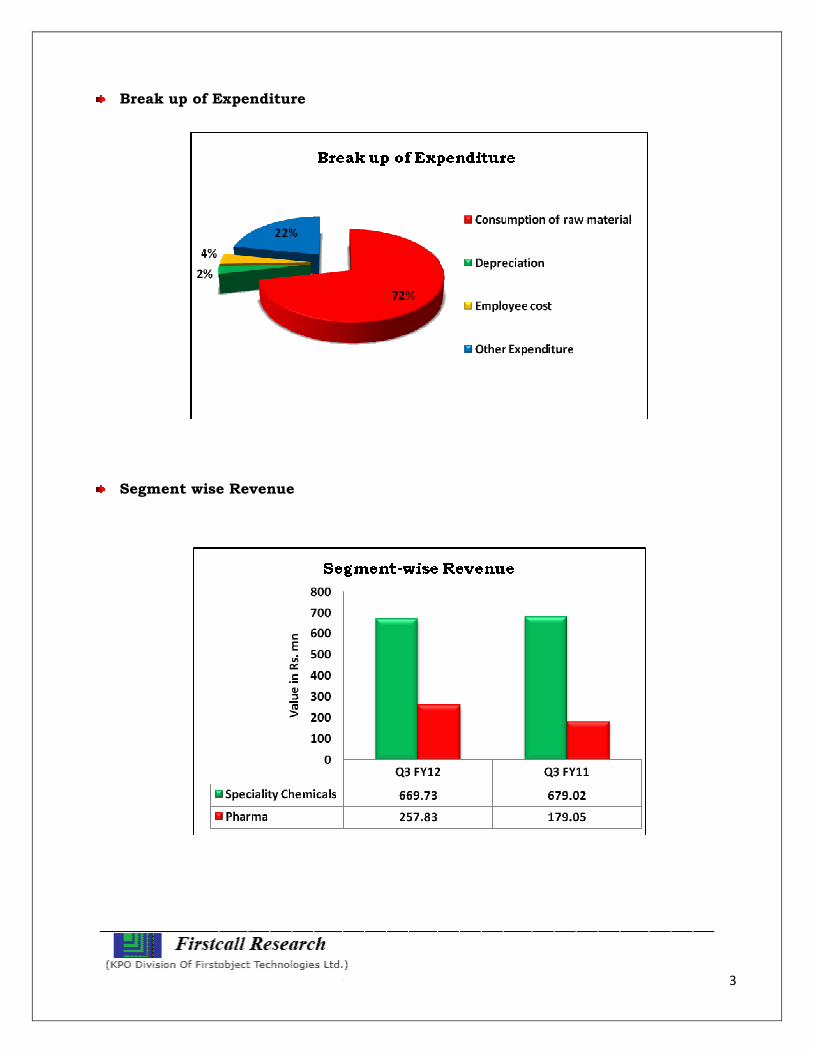

Break up of Expenditure

Segment wise Revenue

4

Acquisition of Uquifa Spain and Uquifa Mexico

Vivimed Labs Ltd has acquired Uquifa, a 75-year-old manufacturer of pharma APIs

and intermediates with operations in Spain and Mexico. In a move to bring in

strategic growth into its product mix and expand the footprint in Europe and the

Americas, the Company has taken a measured stride with the acquisition of Uquifa

Spain and Uquifa Mexico.

Company Profile

Vivimed Labs Ltd was originally incorporated as Emgi Pharmaceuticals & Chemicals

Private Limited with Registrar of Companies of Karnataka, Bangalore & subsequently

converted into a public limited company on April 21, 1994. The name of the company

has been changed to Vivimed Labs Limited on April 22, 1997.

The company was originally promoted by A. M. Rao. In 1989 Santosh Varalwar

and Subhash Varalwar acquired Emgi Pharmaceuticals and Chemicals Limited and

commenced manufacturing of bulk drugs in 1991.

The company’s manufacturing unit is located at Bidar, Karnataka, where it was

originally engaged in the manufacturing of Active Pharmaceutical Ingredients (APIs)

and bulk drugs like Ibuprofen etc. However, due to downward price movement in the

products of the company during 1995, it gradually moved over to manufacturing

specialty chemicals and cosmetic ingredients like Triclosan, Avis etc. catering to global

and domestic markets.

The Specialty Pharma division of Vivimed is a merged entity of VVS Pharma and

Creative Healthcare. The Specialty Pharma Division has its inherent strengths in drug

delivery ad drug discovery. The division is focused on providing cures in oncology

space, arthritis, syndrome X, macular degeneration, psoriasis and stress.

Vivimed has offices in India, China, Europe and USA, with manufacturing facilities

focused around Hyderabad city in India and across nearly 50 countries. The company

is now set to expand its operations into the fast-emerging and highly demanding

sector of Printable Electronics and Organic Semiconductors.

5

Vivimed Products

Vivimed brands touch the lives of people around the world through its products

segment in various areas with different ingredients within daily routine. Vivimed

products are acknowledged in following ways:

� Oral care

Maintaining good oral hygiene is an essential part of overall healthcare and well-

being. Vivimed's products for Oral Care find applications in some of the most

effective products in the market for good oral health-antibacterial for toothpaste and

mouthwash, neutraceuticals for dental enamel protection.

� Sun care

The most important skin-care products available for the prevention of wrinkles and

skin damage are sunscreens.

Exposure to damaging ultraviolet light from the sun's rays, UV-A or UV-B,

accounts for 90% of the symptoms of premature skin ageing such as wrinkles and

skin cancers. UV-A radiation (320-400nm) is linked with the loss of skin elasticity,

wrinkling and premature ageing, whilst the more powerful UV-B radiation (290-

320nm) is linked to sunburn, cell damage and cancer risk.

� Skin care

Vivimed's range of skin care ingredients covers active anti-wrinkle, anti-ageing

compounds, anti-oxidants, skin-lightening actives and emollients. Proven care in a

harsh world - the beauty of chemistry.

� Hair care

Under the well-known Jarocol® trademark, Vivimed offers a full range of hair dye

intermediates for use in permanent, semi-permanent and temporary colorants. They

offer a variety of products, including anti-dandruff agents, UV absorbers, hair loss

actives and guar gums for the formulation of shampoos, conditioners and styling

products.

6

� Thickeners and Conditioners

Vivimed's range of speciality Co-Guar thickeners and conditioners is derived from

natural extract of Guar bean. A range of cationic guar-gum products across a

spectrum of pH and viscosity profiles cover many personal care and cosmetic

applications; thickeners for hand and face creams, lotions, body washes and shower

gels; stabilisers for shampoos and conditioners which build body for hair, improve

combability and add bounce.

� Reversacol Photochromic Dyes

Vivimed is a world leader in the development of innovative photochromic dyes.

Under the Reversacol trade name, Vivimed manufactures and markets the most

comprehensive range of patented, high performance dyes available in the world.

This portion have 30 vibrant colors in their dye portfolio, including a unique

selection of single-molecule, neutral grey photochromic dyes.

� Anti-Microbials & Preservatives

Vivimed's range of effective and established anti-microbial actives finds uses in a

wide range of applications from plastics additives through to anti-bacterial hand

washes. Catering to the personal care markets and industrial sectors Vivimed

provides effective preservatives for a wide range of formulations.

� Imaging Chemicals

Vivimed is a major manufacturer of photographic chemicals used for areas of

traditional photographic imaging technology such as medical and industrial X-ray

imaging, consumer photography and litho-plate production for the graphic arts

industry.

7

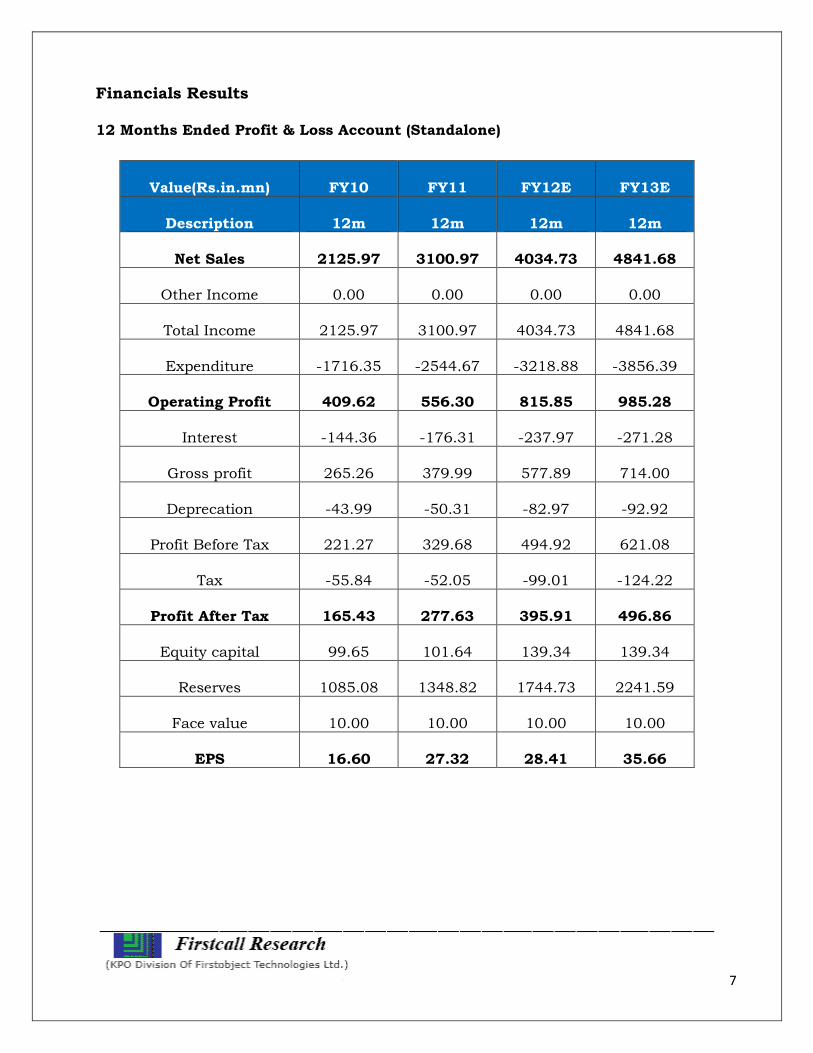

Financials Results

12 Months Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) FY10 FY11 FY12E FY13E

Description 12m 12m 12m 12m

Net Sales 2125.97 3100.97 4034.73 4841.68

Other Income 0.00 0.00 0.00 0.00

Total Income 2125.97 3100.97 4034.73 4841.68

Expenditure -1716.35 -2544.67 -3218.88 -3856.39

Operating Profit 409.62 556.30 815.85 985.28

Interest -144.36 -176.31 -237.97 -271.28

Gross profit 265.26 379.99 577.89 714.00

Deprecation -43.99 -50.31 -82.97 -92.92

Profit Before Tax 221.27 329.68 494.92 621.08

Tax -55.84 -52.05 -99.01 -124.22

Profit After Tax 165.43 277.63 395.91 496.86

Equity capital 99.65 101.64 139.34 139.34

Reserves 1085.08 1348.82 1744.73 2241.59

Face value 10.00 10.00 10.00 10.00

EPS 16.60 27.32 28.41 35.66

8

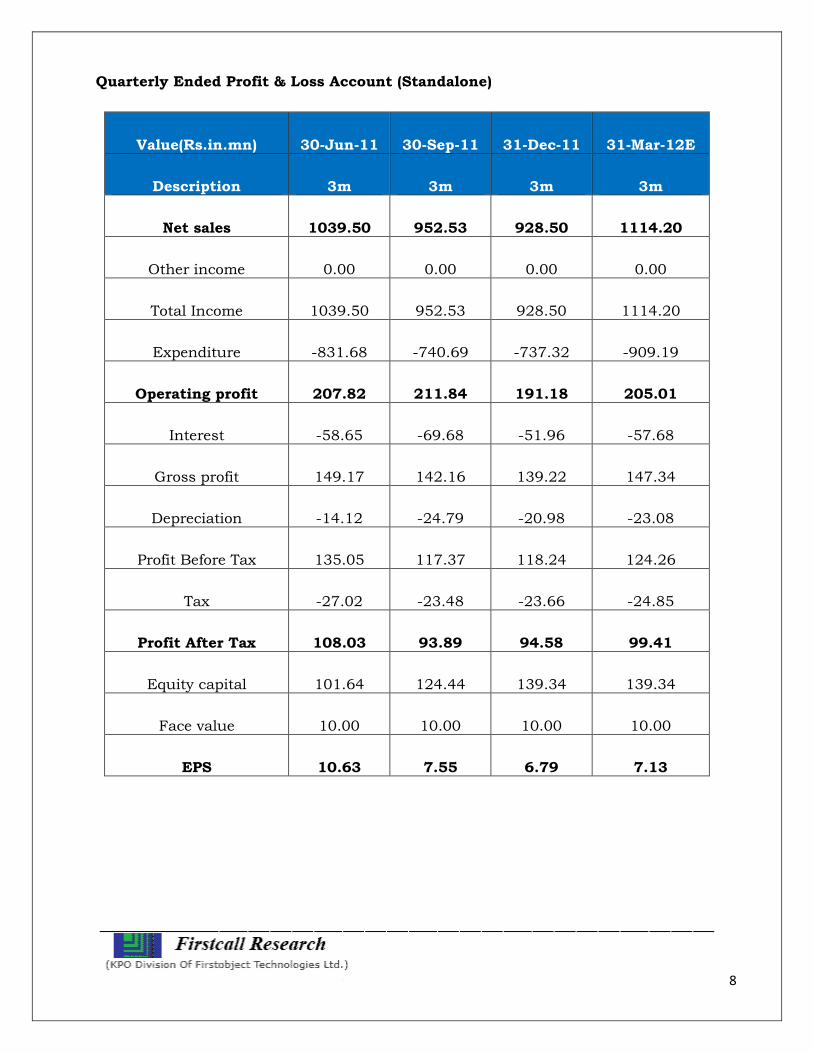

Quarterly Ended Profit & Loss Account (Standalone)

Value(Rs.in.mn) 30-Jun-11 30-Sep-11 31-Dec-11 31-Mar-12E

Description 3m 3m 3m 3m

Net sales 1039.50 952.53 928.50 1114.20

Other income 0.00 0.00 0.00 0.00

Total Income 1039.50 952.53 928.50 1114.20

Expenditure -831.68 -740.69 -737.32 -909.19

Operating profit 207.82 211.84 191.18 205.01

Interest -58.65 -69.68 -51.96 -57.68

Gross profit 149.17 142.16 139.22 147.34

Depreciation -14.12 -24.79 -20.98 -23.08

Profit Before Tax 135.05 117.37 118.24 124.26

Tax -27.02 -23.48 -23.66 -24.85

Profit After Tax 108.03 93.89 94.58 99.41

Equity capital 101.64 124.44 139.34 139.34

Face value 10.00 10.00 10.00 10.00

EPS 10.63 7.55 6.79 7.13

9

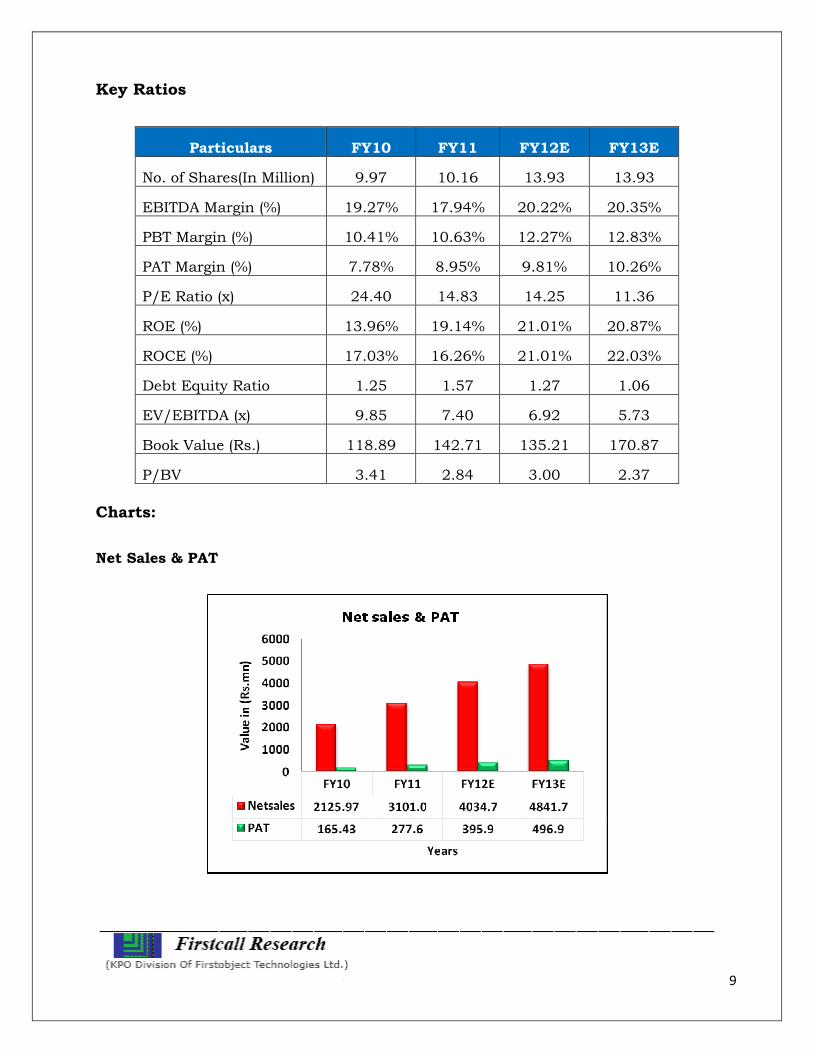

Key Ratios

Particulars FY10 FY11 FY12E FY13E

No. of Shares(In Million) 9.97 10.16 13.93 13.93

EBITDA Margin (%) 19.27% 17.94% 20.22% 20.35%

PBT Margin (%) 10.41% 10.63% 12.27% 12.83%

PAT Margin (%) 7.78% 8.95% 9.81% 10.26%

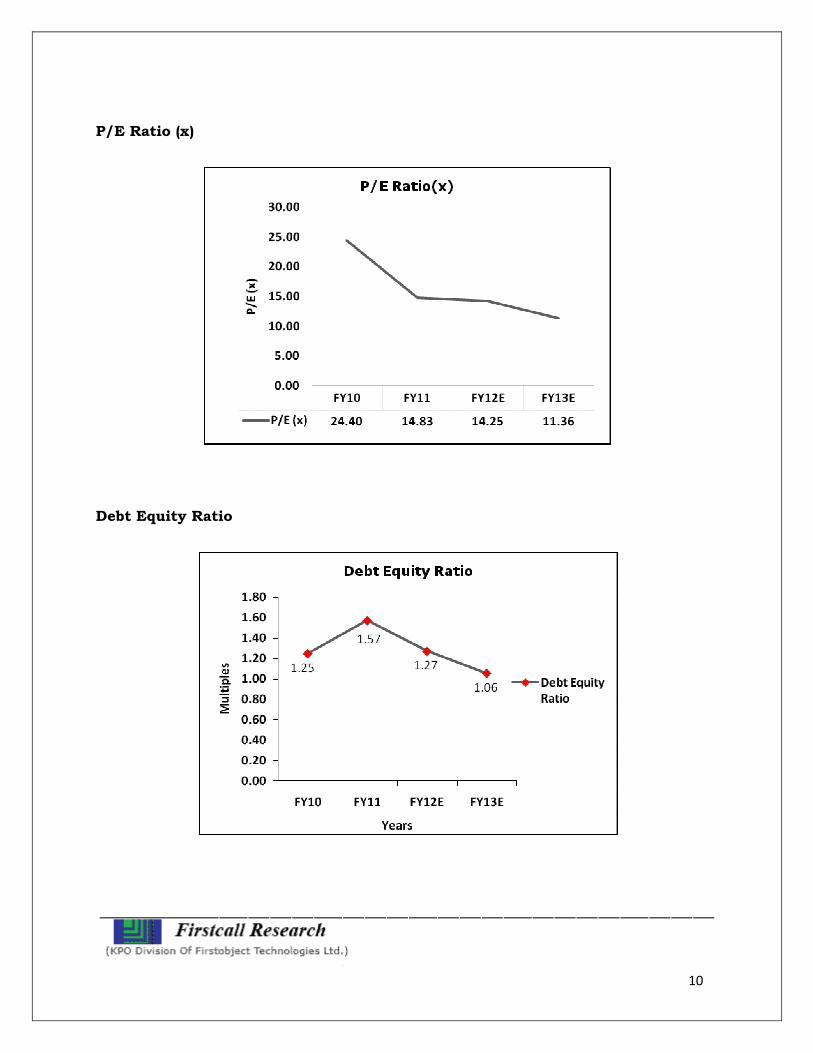

P/E Ratio (x) 24.40 14.83 14.25 11.36

ROE (%) 13.96% 19.14% 21.01% 20.87%

ROCE (%) 17.03% 16.26% 21.01% 22.03%

Debt Equity Ratio 1.25 1.57 1.27 1.06

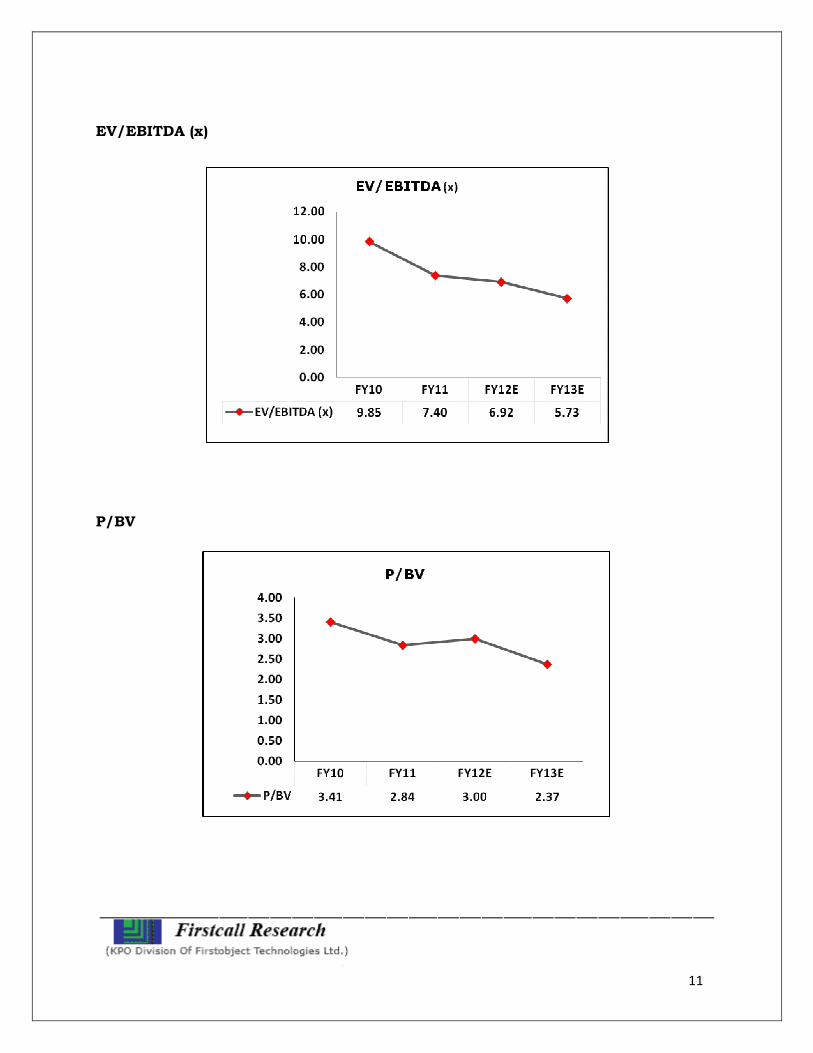

EV/EBITDA (x) 9.85 7.40 6.92 5.73

Book Value (Rs.) 118.89 142.71 135.21 170.87

P/BV 3.41 2.84 3.00 2.37

Charts:

Net Sales & PAT

10

P/E Ratio (x)

Debt Equity Ratio

11

EV/EBITDA (x)

P/BV

12

Outlook and Conclusion

At the current market price of Rs. 405.00, the stock is trading at 14.25 x FY12E

and 11.36 x FY13E respectively.

Earning per share (EPS) of the company for the earnings for FY12E and FY13E

is seen at Rs.28.41 and Rs.35.66 respectively.

Net Sales and PAT of the company are expected to grow at a CAGR of 32% and

44% over 2010 to 2013E respectively.

On the basis of EV/EBITDA, the stock trades at 6.92 x for FY12E and 5.73 x for

FY13E.

Price to Book Value of the stock is expected to be at 3.00 x and 2.37 x

respectively for FY12E and FY13E.

We recommend ‘BUY’ in this particular scrip with a target price of Rs.466.00

for Medium term investment.

Industry Overview

The Indian chemical and petrochemical industry was worth $83bn in 2010 and it was

the third largest in Asia and 12th worldwide by volume. The industry has consistently

been moving towards knowledge based speciality products but with recognition of the

importance of being self-sufficient in primary feedstocks to service the growing

demand for higher added value products.

The global speciality chemicals market, at $740bn represents 22% of the global

chemical industry; saw a sharp rebound from the downturn in 2009.

Increasing raw material costs continued to be a major factor, accelerating further in

h2 2010 and impacting on margins but this was mitigated by the increase in demand

enabling some companies to improve margins and post higher sales levels. Many

companies undertook restructurings to reduce costs and thus took greater advantage

from higher volumes. Other companies restructured the portfolio towards even higher

margin specialties and quality products.

13

Towards the back end of 2010 and into 2011, the level of M&A activity increased

leading to further consolidation within the market with the largest deal being BASF’s

acquisition of cognis. The global crisis and recovery also signaled the overall strength

of Asia in chemical manufacture and the growing importance of India as both a

producer and consumer of speciality chemicals.

The Indian speciality chemicals (excluding Knowledge chemicals) market was

estimated at $15bn in 2010 and is forecasted to grow at 15% pa to 2015 primarily

driven by the growth in the number of middle class consumers who are able to afford

products which consume speciality chemicals. This in turn is underpinned by growth

in exports to meet the demands in existing global markets for competitively priced

solutions to customer needs.

Due to the investment in base petrochemicals and other feedstock within India, MNEs

within the speciality chemical industry are focusing on India as a manufacturing base

for both the local and global markets.

Pharma industry:

The Indian pharmaceutical market is expected to grow to US$ 55 billion by 2020 from

the 2009 levels of US$ 12.6 billion, as per a McKinsey & Company report titled “ India

Pharma 2020: Propelling access and acceptance realising true potential”. The industry

further holds potential to reach US$ 70 billion, at a CAGR of 17 per cent.

India’s pharmaceutical industry constitutes of about 8 per cent of the world’s

pharmaceutical production. Over the last couple of years, Indian pharma companies

have been increasingly targeted by multinationals for both collaborative agreements

and acquisition, as per a Espicom report titled, “The Pharmaceutical Market: India

Opportunities and Challenges”.

14

Sector Structure/ Market Size

The US$ 12 billion valued pharmaceutical industry in India is expected to grow at an

annual compound annual growth rate (CAGR) of 10-11 per cent. The industry spends

around 18 per cent of its revenue on research and development (R&D).

India is one of the most significant emerging markets for the global pharmaceutical

industry. Moreover, India is expected to join the league of top 10 global

pharmaceuticals markets in terms of sales by 2020 with the total value reaching US$

50 billion, according to a report by PricewaterhouseCoopers (PwC).

The domestic pharma market is expected to grow at a CAGR of 15 to 20 percent to

reach a value anywhere between USD 50 and 74 billion by 2020, says a PwC report

titled ‘India Pharma Inc: Enhancing Value through Alliances & Partnerships’.

Growth

The drugs and pharmaceuticals sector attracted foreign direct investments (FDI) worth

US$ 4.89 billion between April 2000 and August 2011, according to the latest data

published by Department of Industrial Policy and Promotion (DIPP).

Indian pharmaceutical market is predicted to grow to US$ 55 billion by 2020 from

US$ 12.6 billion in 2009, according to a report by McKinsey.

On back of a high middle-class population base, improvements in medical

infrastructure and the establishment of intellectual property rights, the Indian pharma

industry is estimated to grow manifold.

Generics

Generics will continue to dominate the market while patent-protected products are

likely to constitute 10 per cent of the pie till 2015, according to McKinsey report ‘India

Pharma 2015 - Unlocking the potential of Indian Pharmaceuticals market’. Moreover,

as per a press release by research firm RNCOS, the report titled ‘Booming Generics

15

Drug Market in India'. The report further projects the Indian generic drug market to

grow at a CAGR of around 17 per cent between 2010-11 and 2012-13.

India tops the world in exporting generic medicines worth US$ 11 billion. Currently,

the Indian pharmaceutical industry is one of the world's largest and most developed,

according to Mr Srikant Kumar Jena, Union Minister of State for Chemicals and

Fertilisers.

• Dr Reddy's Laboratories Ltd has entered into a MoU with Tokyo-based Fujifilm

Corporation to form a joint venture (JV) in Japan. The venture would develop,

manufacture and promote generic drugs in Japan

• Ranbaxy Laboratories announced that it is on track to launch the generic

version of the world's largest-selling drug, Lipitor-the anti-cholesterol pill, on

November 30, 2011 in the United States (US), as per Tsutomu Une, Chairman,

Ranbaxy

• Natco Pharma has applied for India's first compulsory licence to sell a generic

version of Bayer's patented medicine, stating in its application that the German

company's drug was unaffordable for the average Indian

• Natco Pharma has also entered into an exclusive agreement with Mabxience,

part of Chemo Sa Lugano of Switzerland. Natco will purchase four drug

substances (biogenerics) from Chemo Sa Lugano and use them for

manufacturing finished dosage pharma formulations

Investments

• Strides Arcolab Ltd, maker of intellectual property led pharmaceutical products

announced that it has received US FDA approval for clindamycin injection,

USP, an antibiotic used to treat bacterial infections

• Sanofi-aventis Group is setting up its largest vaccine making facility in

Hyderabad. "The new plant, our biggest facility in the world, is coming up here,"

according to Christopher A Viehbacher, Chief Executive Officer, Sanofi-aventis

16

• GlaxoSmithKline (GSK) has set aside US$ 1-2 billion to support its expansion

plans in India. "We can afford a deal worth US$ 1- US$ 2 billion in the Indian

pharmaceutical space," as per Andrew Witty, global CEO, GSK

• Lupin is set to enter the US oral contraceptive market. The company has

received final approval from the US Food and Drug Administration (USFDA) to

market a generically similar version of Watson's oral contraceptive NOR-QD

tablets

• Daiichi Sankyo Company Ltd and Ranbaxy Laboratories Ltd have announced

expansion of their business in Mexico, to maximise their hybrid business

model. As part of the plan, the two companies will launch Olmesartan

Medoxomil, used to treat high blood pressure, in Mexico before the year-end

• Aventis Pharma Ltd, a unit of France's Sanofi, plans to acquire unlisted

Universal Medicare's nutraceuticals business to boost its consumer healthcare

and wellness segment in India. Aventis was close to buying the over-the-counter

(OTC) business of Universal Medicare for about US$ 109.5 million

Road Ahead

On back of aggressive marketing initiatives, the pharma companies witnessed rural

market sales doubling. India's rural drug market grew by 18.8 per cent in the 12

months period ended April 2011 as compared with 10.9 per cent in the previous year.

With the focus of companies shifting to smaller deals catering to niche segments and

markets, partnerships seems to be the new norm in the pharmaceutical sector. Today,

domestic pharmaceutical majors are talking less of patent litigation and more of

patent settlements. The fight seems to be giving way to partnerships and experts

consider this the new way forward. Companies such as Ranbaxy and Dr Reddy’s were

known for big acquisitions.

Interestingly, the international drug-makers have introduced generic or low-priced

version of popular medicines and have also decreased prices of their existing products

- in order to increase their share in the globally important market - in India. The

Indian-makers business model is built around selling large volume of cheap generic

17

medicines at lower margins in the country, to add to twin purpose of affordability and

popularity.

"The industry posting healthy growth consecutively for the second year reflects the

inherent strengths of the industry and improving healthcare standards in the

country... demand for drugs and pharmaceuticals is on the rise, and is likely to

continue next year as well. The nutraceutical segment will continue to have better-

than-average growth with people getting more conscious of their general health and

well-being," as per Ganesh Nayak, Executive Director, Zydus Cadila.

________________ ____ _________________________ Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

18

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

A. Rajesh Babu FMCG

H.Lavanya Oil & Gas

Ashish.Kushwaha Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s,Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions(domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor,Sankalp,The Bureau,Dr.R.C.Marg,Chembur,Mumbai 400 071

Tel. : 022-2527 2510/2527 6077/25276089 Telefax : 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com