Embed Size (px)

Citation preview

Vladimir FilimonovETH Zurich, D-MTEC, Chair of Entrepreneurial Risks

Modeling financial time series. Effective multifractality and self-excited

multifractal process

Fractals and Related Fields II, Ile de Porquerolles, France, June 13-17, 2011

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

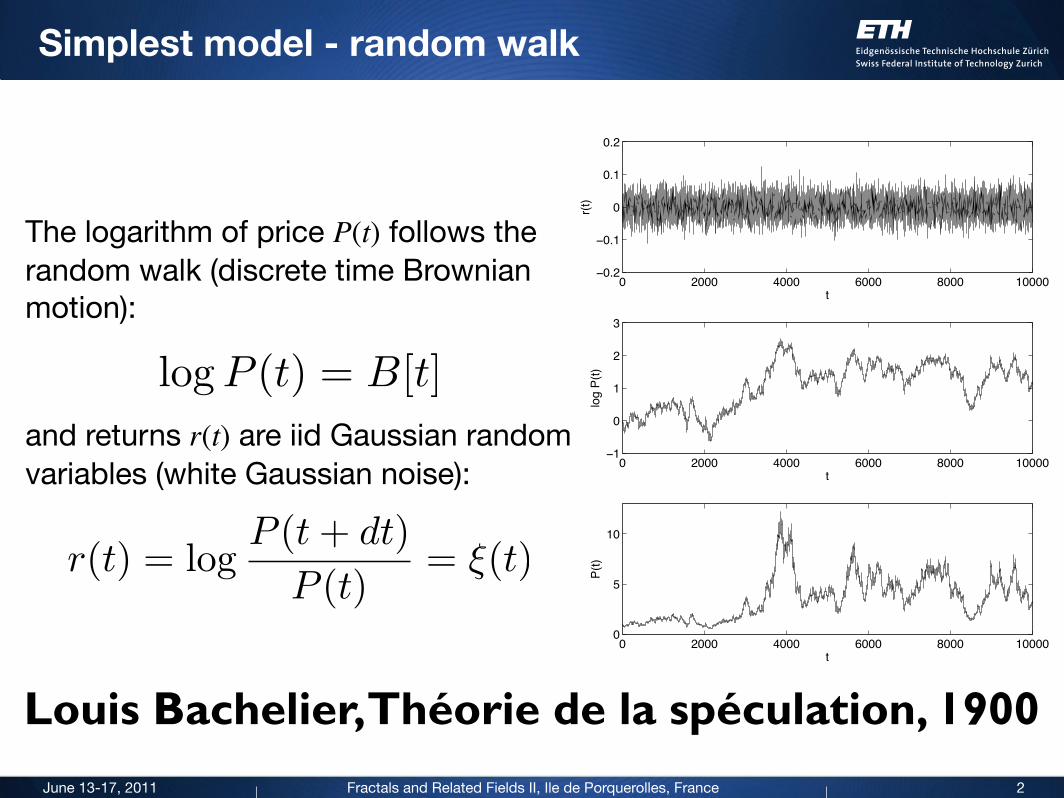

Simplest model - random walk

2

Louis Bachelier, Théorie de la spéculation, 1900

The logarithm of price P(t) follows the random walk (discrete time Brownian motion):

and returns r(t) are iid Gaussian random variables (white Gaussian noise):

0 2000 4000 6000 8000 100000.2

0.1

0

0.1

0.2

t

r(t)

0 2000 4000 6000 8000 100001

0

1

2

3

t

log

P(t)

0 2000 4000 6000 8000 100000

5

10

t

P(t)

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

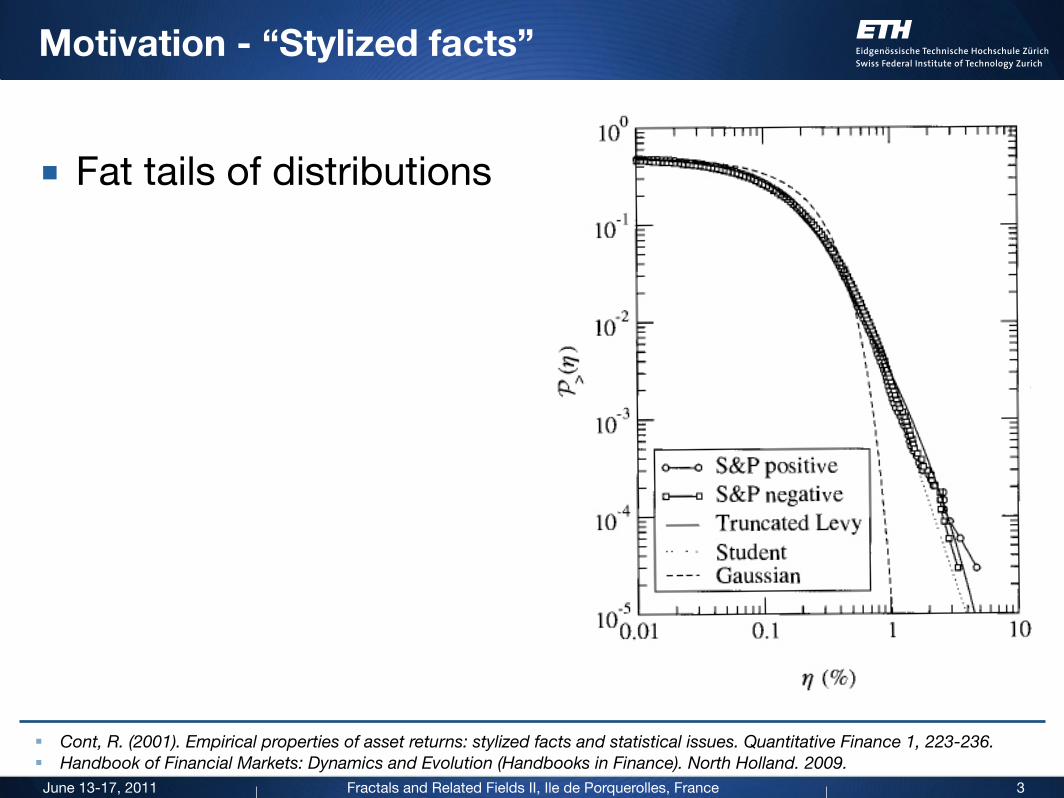

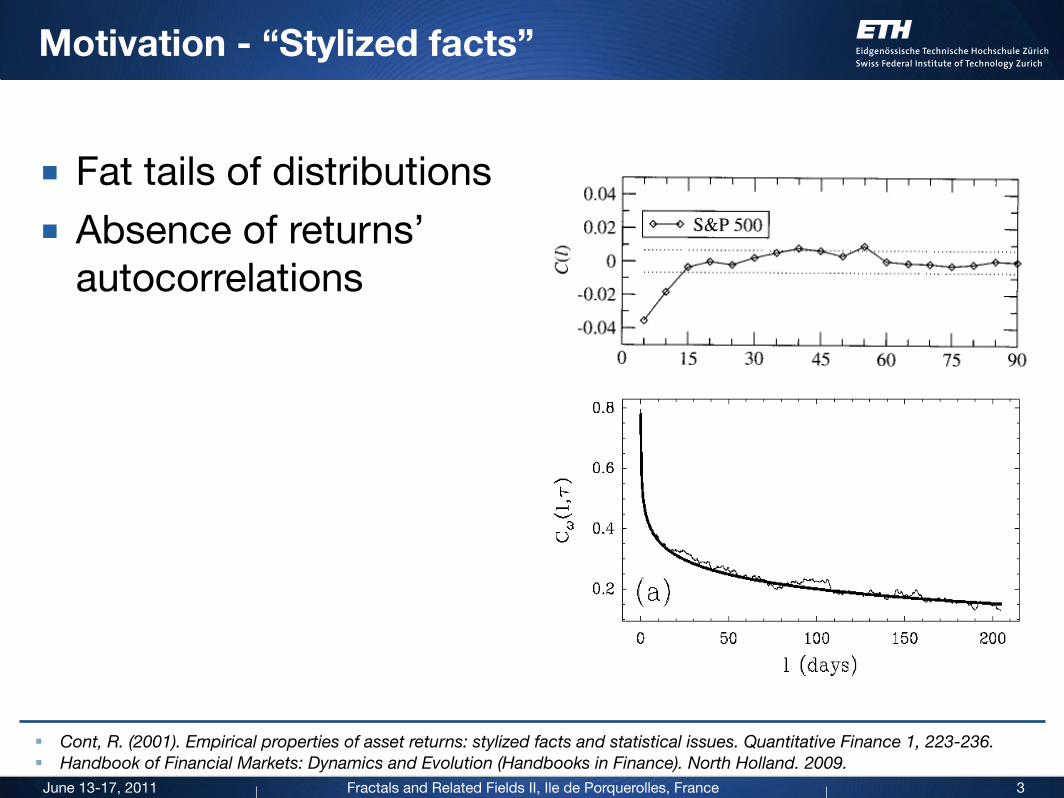

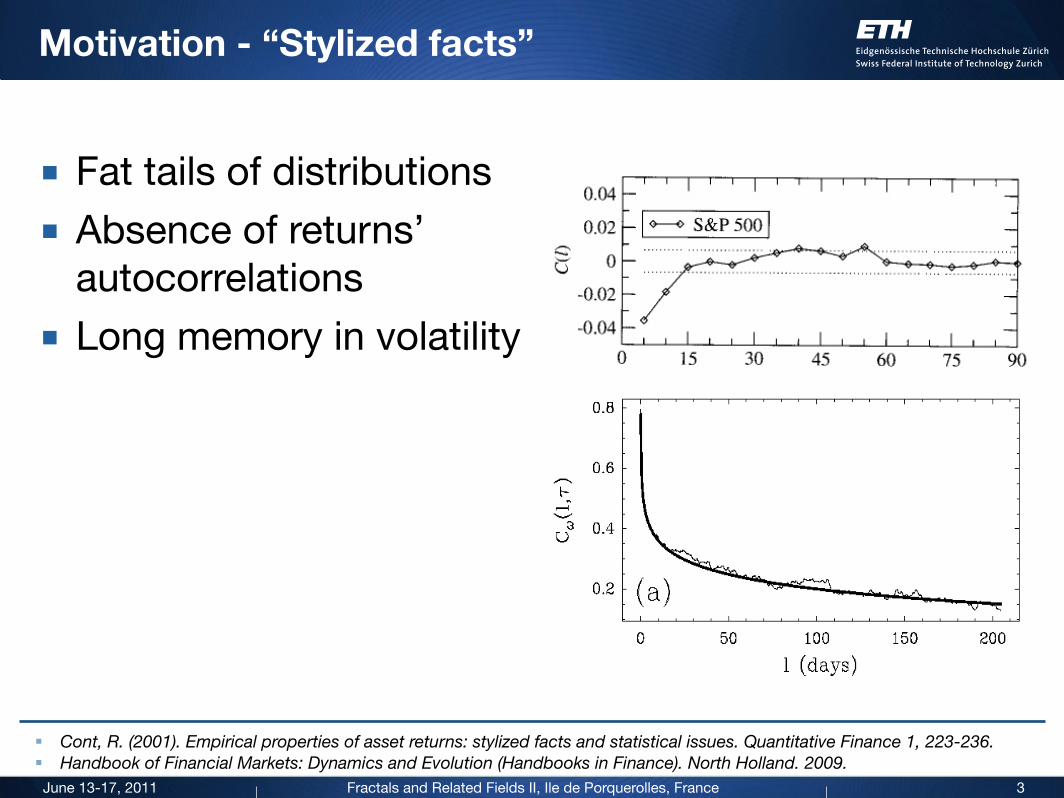

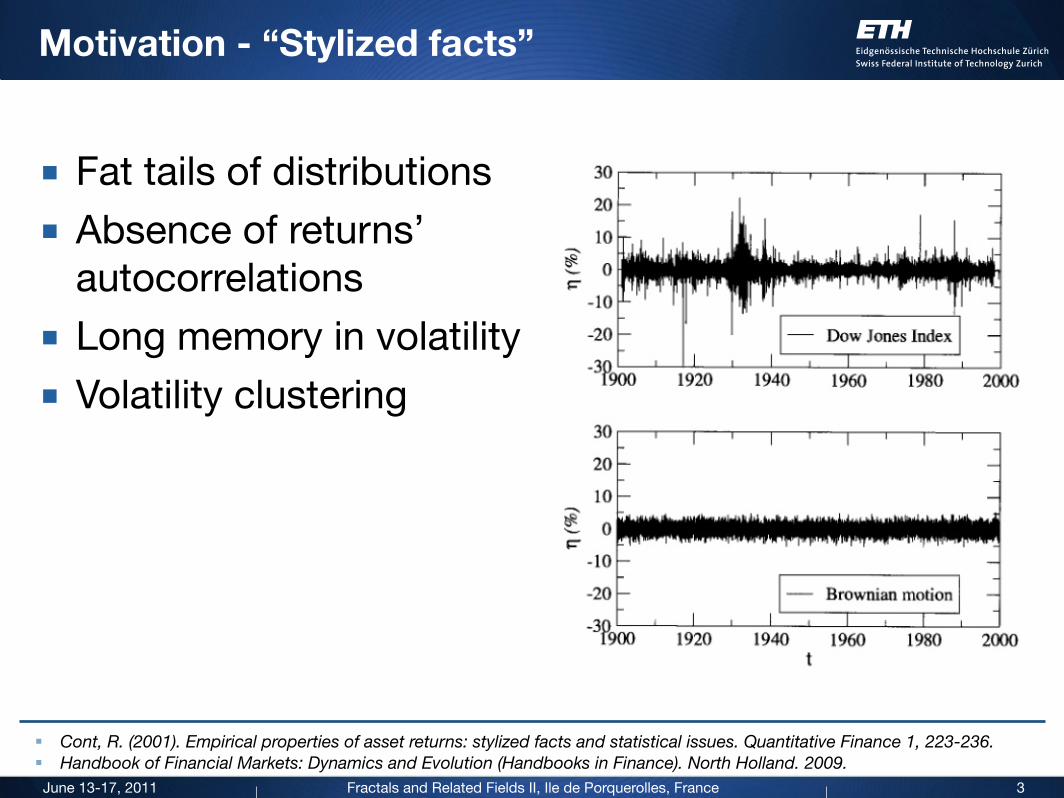

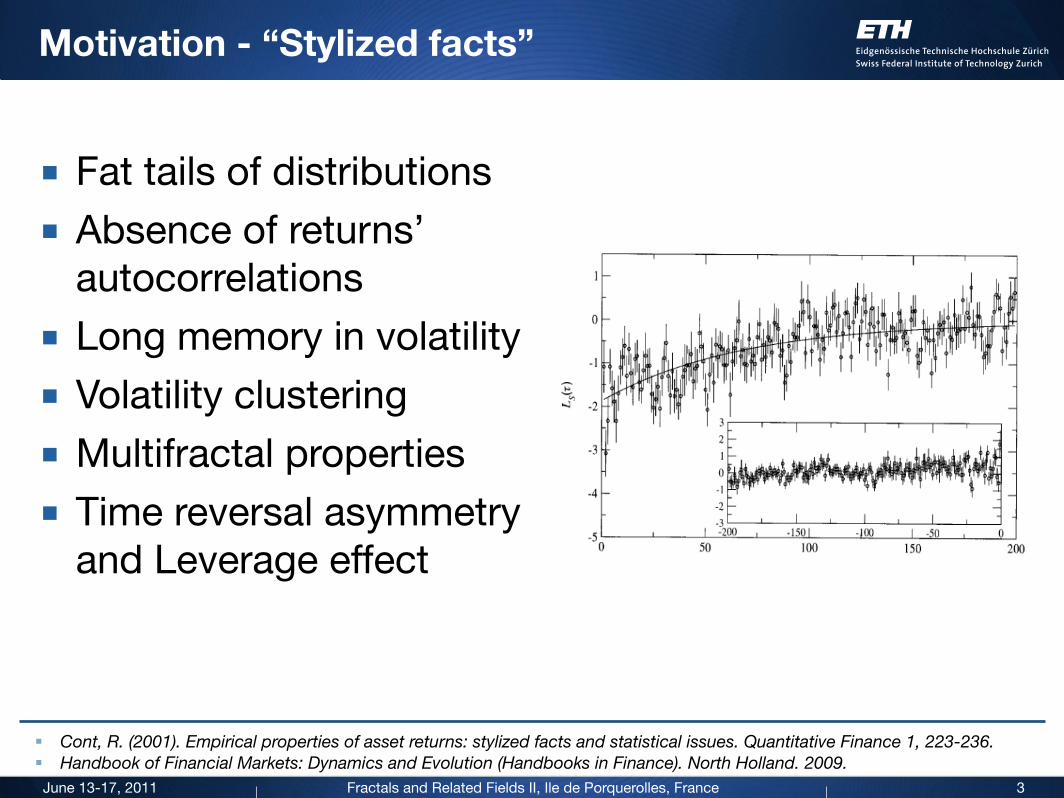

Motivation - “Stylized facts”

■ Fat tails of distributions

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Stylized facts”

■ Fat tails of distributions

■ Absence of returns’ autocorrelations

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Stylized facts”

■ Fat tails of distributions

■ Absence of returns’ autocorrelations

■ Long memory in volatility

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Stylized facts”

■ Fat tails of distributions

■ Absence of returns’ autocorrelations

■ Long memory in volatility

■ Volatility clustering

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Stylized facts”

■ Fat tails of distributions

■ Absence of returns’ autocorrelations

■ Long memory in volatility

■ Volatility clustering

■ Multifractal properties

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Stylized facts”

■ Fat tails of distributions

■ Absence of returns’ autocorrelations

■ Long memory in volatility

■ Volatility clustering

■ Multifractal properties

■ Time reversal asymmetry and Leverage effect

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

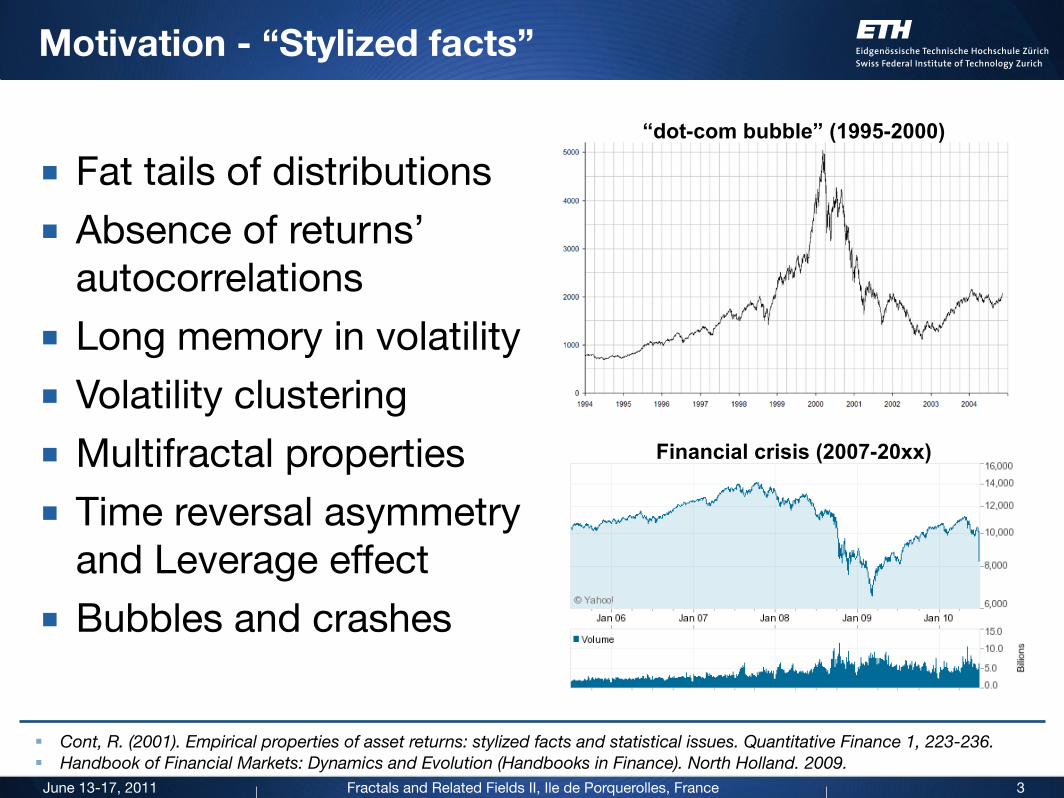

“dot-com bubble” (1995-2000)

Financial crisis (2007-20xx)

Motivation - “Stylized facts”

■ Fat tails of distributions

■ Absence of returns’ autocorrelations

■ Long memory in volatility

■ Volatility clustering

■ Multifractal properties

■ Time reversal asymmetry and Leverage effect

■ Bubbles and crashes

3

§ Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance 1, 223-236.§ Handbook of Financial Markets: Dynamics and Evolution (Handbooks in Finance). North Holland. 2009.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

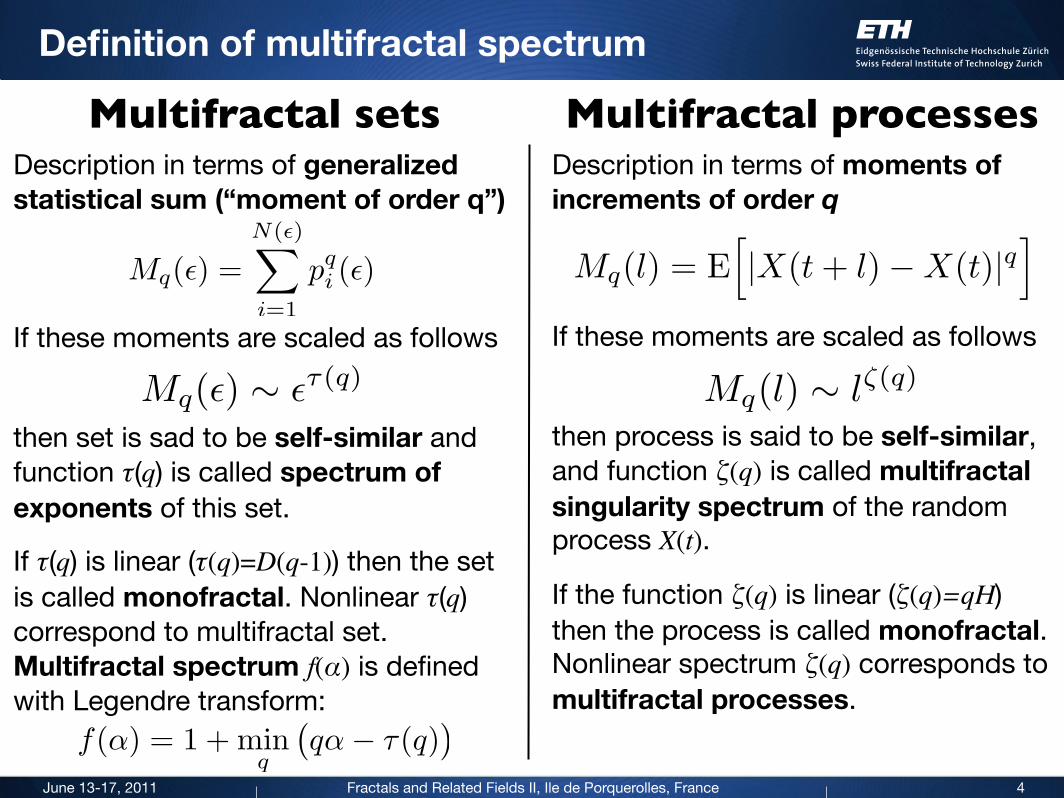

Definition of multifractal spectrum

Description in terms of moments of increments of order q

If these moments are scaled as follows

then process is said to be self-similar, and function ζ(q) is called multifractal singularity spectrum of the random process X(t).

If the function ζ(q) is linear (ζ(q)=qH) then the process is called monofractal. Nonlinear spectrum ζ(q) corresponds to multifractal processes.

4

Multifractal sets Multifractal processesDescription in terms of generalized statistical sum (“moment of order q”)

If these moments are scaled as follows

then set is sad to be self-similar and function τ(q) is called spectrum of exponents of this set.

If τ(q) is linear (τ(q)=D(q-1)) then the set is called monofractal. Nonlinear τ(q) correspond to multifractal set. Multifractal spectrum f(α) is defined with Legendre transform:

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

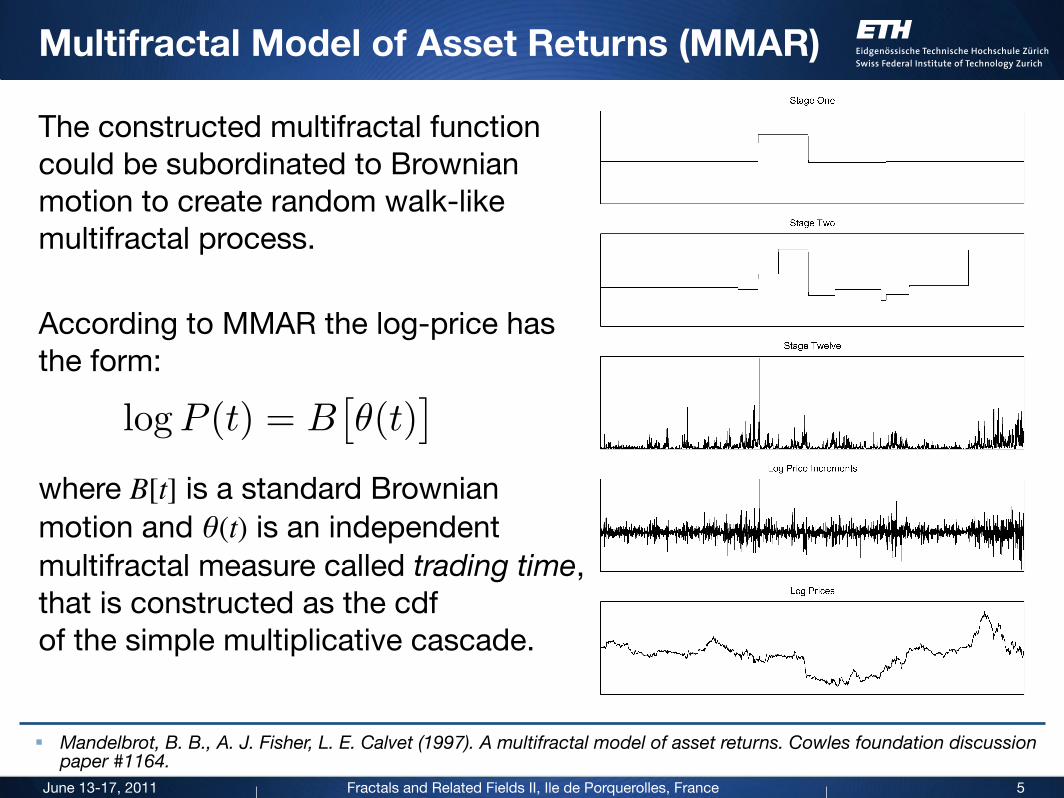

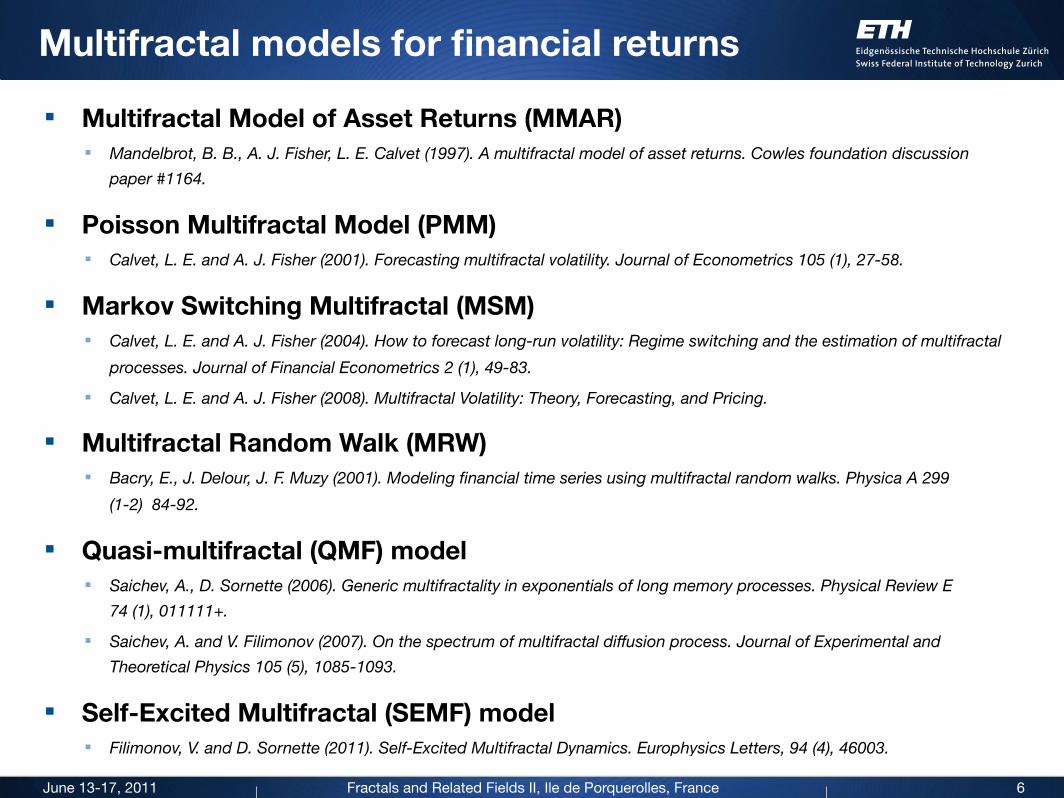

Multifractal Model of Asset Returns (MMAR)

The constructed multifractal function could be subordinated to Brownian motion to create random walk-like multifractal process.

According to MMAR the log-price has the form:

where B[t] is a standard Brownian motion and θ(t) is an independent multifractal measure called trading time, that is constructed as the cdf of the simple multiplicative cascade.

5

32 L. Calvet, A. Fisher / Journal of Econometrics 105 (2001) 27–58

Fig. 1. Construction of a grid-free multifractal process. The !rst three panels show stages inthe construction of a grid-free limit lognormal measure with parameter !=1:09. The !nal twopanels illustrate the corresponding simulated log price increments and log prices, which areobtained by compounding the c.d.f. of the stage 12 measure with a Gaussian white noise. Thereturn series shows long memory volatility clustering and outliers that are produced by inter-mittent bursts of extreme volatility. The construction fully randomizes the timing of volatilityinnovations, and the resulting return process is strictly stationary.

§ Mandelbrot, B. B., A. J. Fisher, L. E. Calvet (1997). A multifractal model of asset returns. Cowles foundation discussion paper #1164.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Multifractal models for financial returns

§ Multifractal Model of Asset Returns (MMAR)§ Mandelbrot, B. B., A. J. Fisher, L. E. Calvet (1997). A multifractal model of asset returns. Cowles foundation discussion

paper #1164.

§ Poisson Multifractal Model (PMM)§ Calvet, L. E. and A. J. Fisher (2001). Forecasting multifractal volatility. Journal of Econometrics 105 (1), 27-58.

§ Markov Switching Multifractal (MSM)§ Calvet, L. E. and A. J. Fisher (2004). How to forecast long-run volatility: Regime switching and the estimation of multifractal

processes. Journal of Financial Econometrics 2 (1), 49-83.

§ Calvet, L. E. and A. J. Fisher (2008). Multifractal Volatility: Theory, Forecasting, and Pricing.

§ Multifractal Random Walk (MRW)§ Bacry, E., J. Delour, J. F. Muzy (2001). Modeling financial time series using multifractal random walks. Physica A 299

(1-2) 84-92.

§ Quasi-multifractal (QMF) model§ Saichev, A., D. Sornette (2006). Generic multifractality in exponentials of long memory processes. Physical Review E

74 (1), 011111+.

§ Saichev, A. and V. Filimonov (2007). On the spectrum of multifractal diffusion process. Journal of Experimental and

Theoretical Physics 105 (5), 1085-1093.

§ Self-Excited Multifractal (SEMF) model§ Filimonov, V. and D. Sornette (2011). Self-Excited Multifractal Dynamics. Europhysics Letters, 94 (4), 46003.

6

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

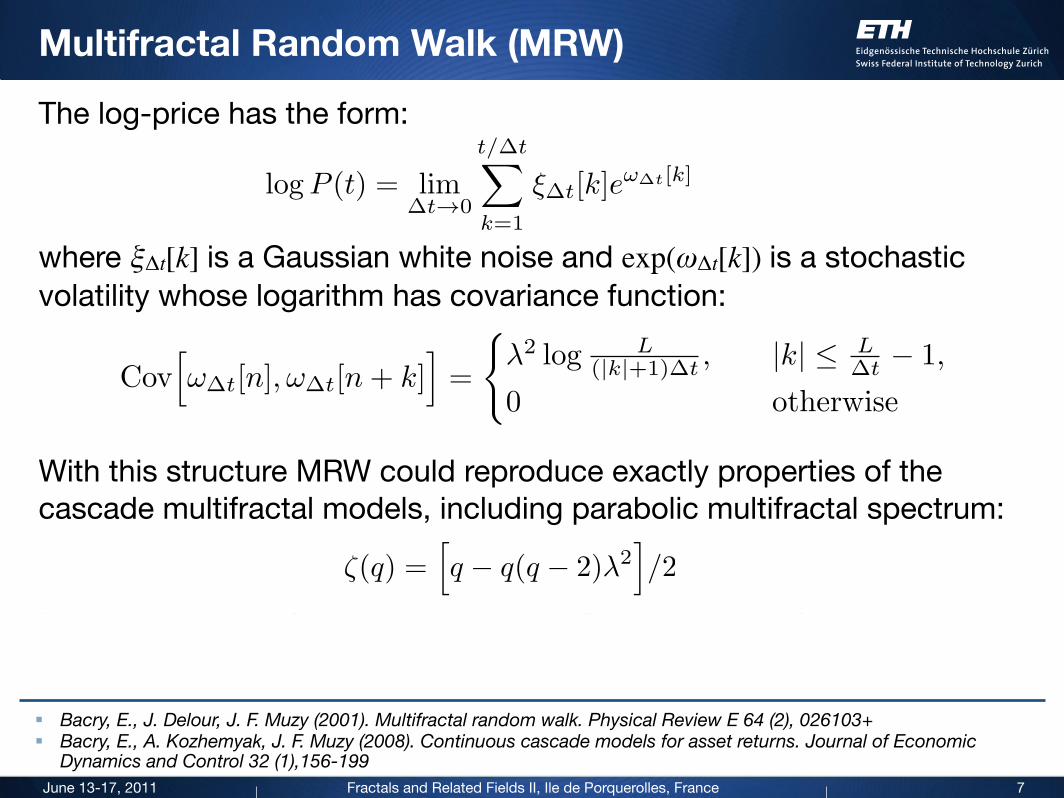

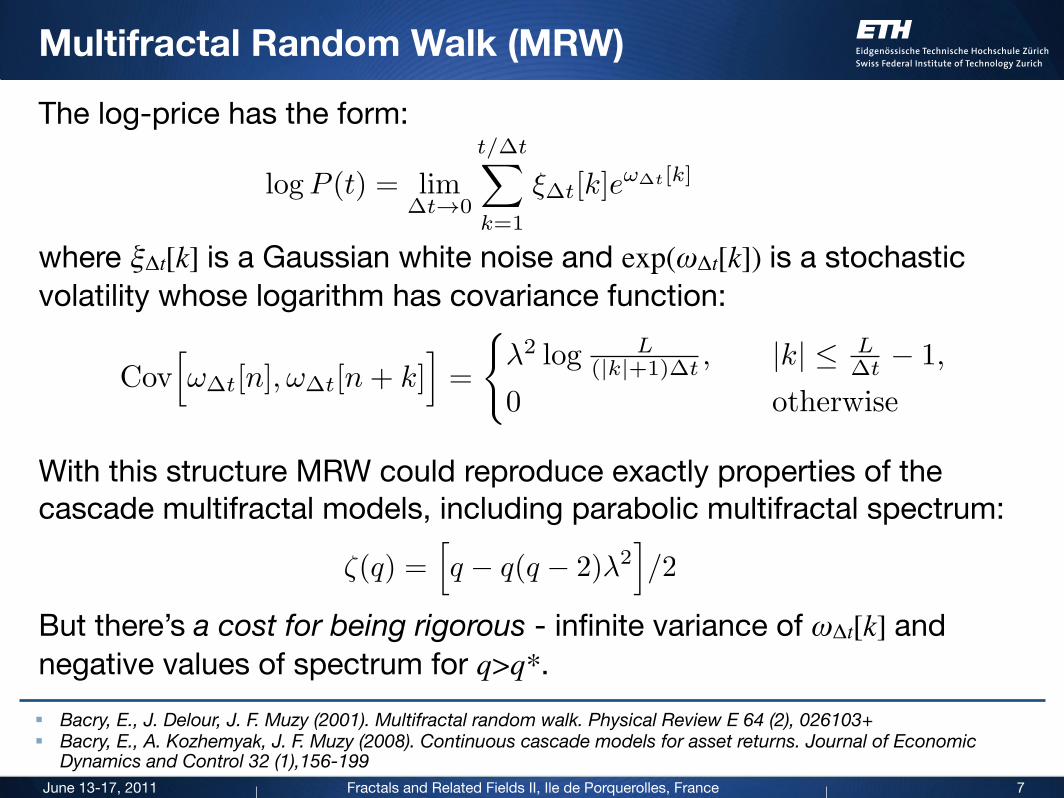

Multifractal Random Walk (MRW)

7

The log-price has the form:

where ξΔt[k] is a Gaussian white noise and exp(ωΔt[k]) is a stochastic volatility whose logarithm has covariance function:

With this structure MRW could reproduce exactly properties of the cascade multifractal models, including parabolic multifractal spectrum:

But there’s a cost for being rigorous - infinite variance of ωΔt[k] and negative values of spectrum for q>q*.

§ Bacry, E., J. Delour, J. F. Muzy (2001). Multifractal random walk. Physical Review E 64 (2), 026103+§ Bacry, E., A. Kozhemyak, J. F. Muzy (2008). Continuous cascade models for asset returns. Journal of Economic

Dynamics and Control 32 (1),156-199

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Multifractal Random Walk (MRW)

7

The log-price has the form:

where ξΔt[k] is a Gaussian white noise and exp(ωΔt[k]) is a stochastic volatility whose logarithm has covariance function:

With this structure MRW could reproduce exactly properties of the cascade multifractal models, including parabolic multifractal spectrum:

But there’s a cost for being rigorous - infinite variance of ωΔt[k] and negative values of spectrum for q>q*.

§ Bacry, E., J. Delour, J. F. Muzy (2001). Multifractal random walk. Physical Review E 64 (2), 026103+§ Bacry, E., A. Kozhemyak, J. F. Muzy (2008). Continuous cascade models for asset returns. Journal of Economic

Dynamics and Control 32 (1),156-199

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

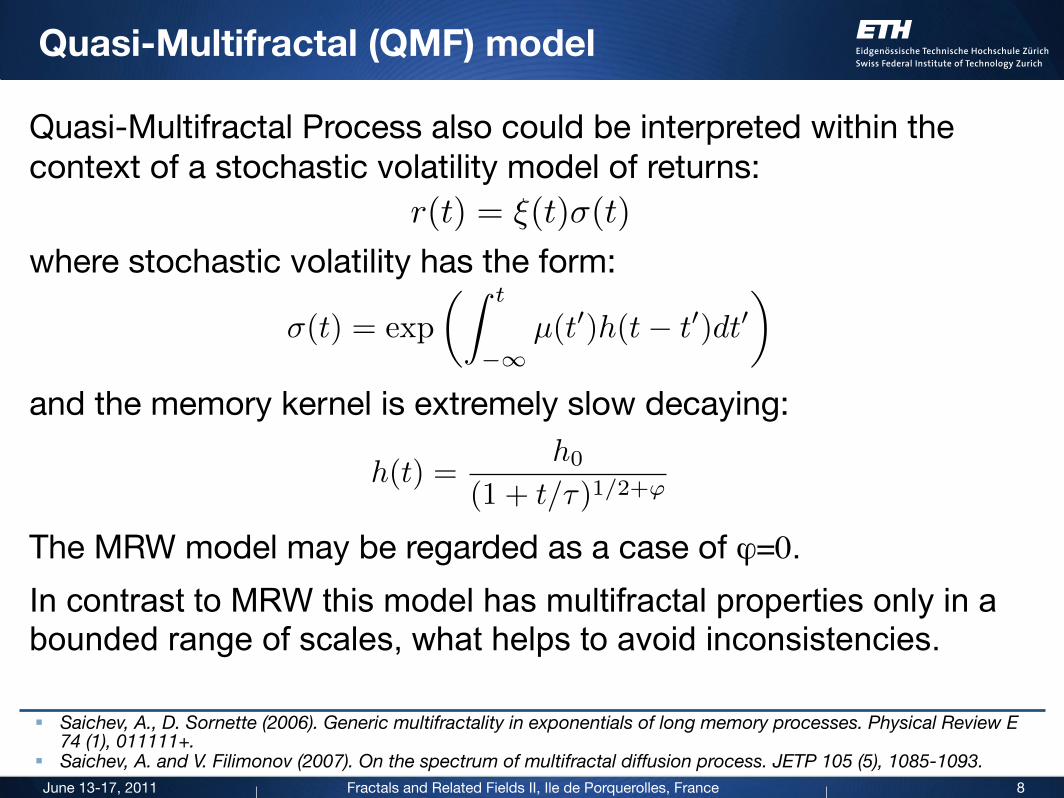

Quasi-Multifractal (QMF) model

Quasi-Multifractal Process also could be interpreted within the context of a stochastic volatility model of returns:

where stochastic volatility has the form:

and the memory kernel is extremely slow decaying:

The MRW model may be regarded as a case of ϕ=0.In contrast to MRW this model has multifractal properties only in a bounded range of scales, what helps to avoid inconsistencies.

8

σ(t) = exp

�� t

−∞µ(t�)h(t− t�)dt�

�

h(t) =h0

(1 + t/τ)1/2+ϕ

§ Saichev, A., D. Sornette (2006). Generic multifractality in exponentials of long memory processes. Physical Review E 74 (1), 011111+.

§ Saichev, A. and V. Filimonov (2007). On the spectrum of multifractal diffusion process. JETP 105 (5), 1085-1093.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Quasi-Multifractal (QMF) model

Quasi-Multifractal Process also could be interpreted within the context of a stochastic volatility model of returns:

where stochastic volatility has the form:

and the memory kernel is extremely slow decaying:

The MRW model may be regarded as a case of ϕ=0.In contrast to MRW this model has multifractal properties only in a bounded range of scales, what helps to avoid inconsistencies.

8

σ(t) = exp

�� t

−∞µ(t�)h(t− t�)dt�

�

h(t) =h0

(1 + t/τ)1/2+ϕ

§ Saichev, A., D. Sornette (2006). Generic multifractality in exponentials of long memory processes. Physical Review E 74 (1), 011111+.

§ Saichev, A. and V. Filimonov (2007). On the spectrum of multifractal diffusion process. JETP 105 (5), 1085-1093.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

“Effective” (“quasi-”) multifractality

9

100 105 1010 1015 1020 10251.3

1.4

1.5

1.6

1.7

1.8

1.9

2

105 1010 1015105

1010

1015

1020

1025

1030

§ Saichev, A. and V. Filimonov (2007). On the spectrum of multifractal diffusion process. JETP 105 (5), 1085-1093.

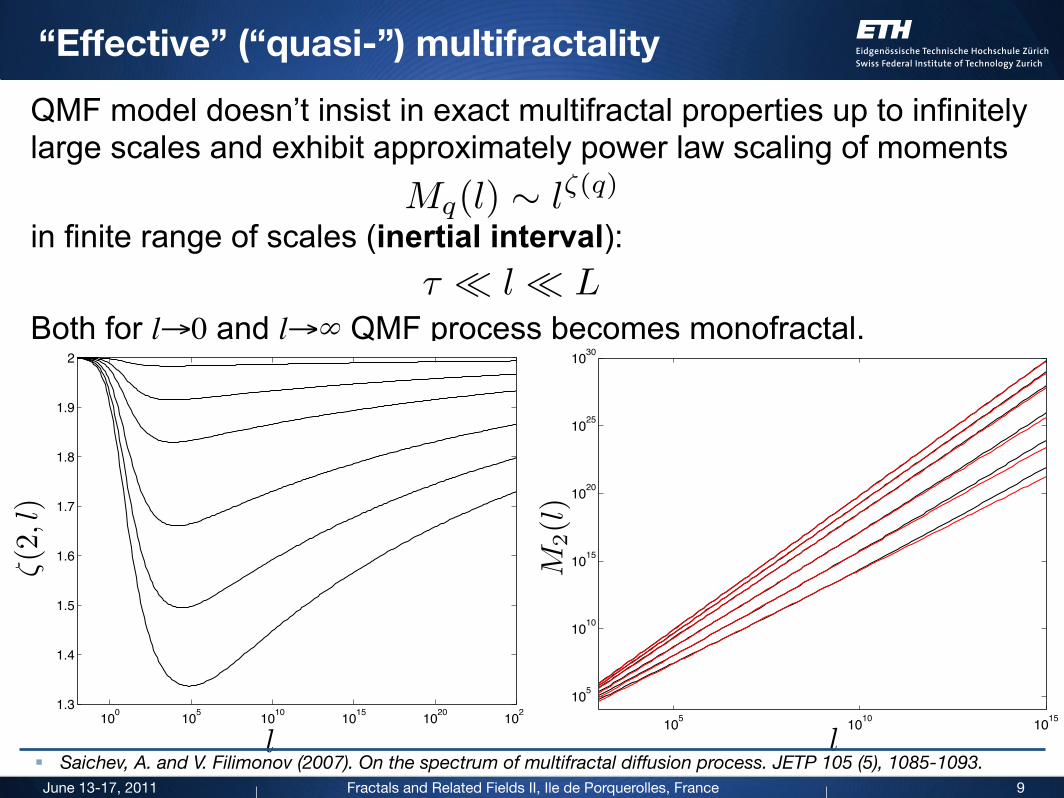

QMF model doesn’t insist in exact multifractal properties up to infinitely large scales and exhibit approximately power law scaling of moments

in finite range of scales (inertial interval):

Both for l→0 and l→∞ QMF process becomes monofractal.τ � l � L

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

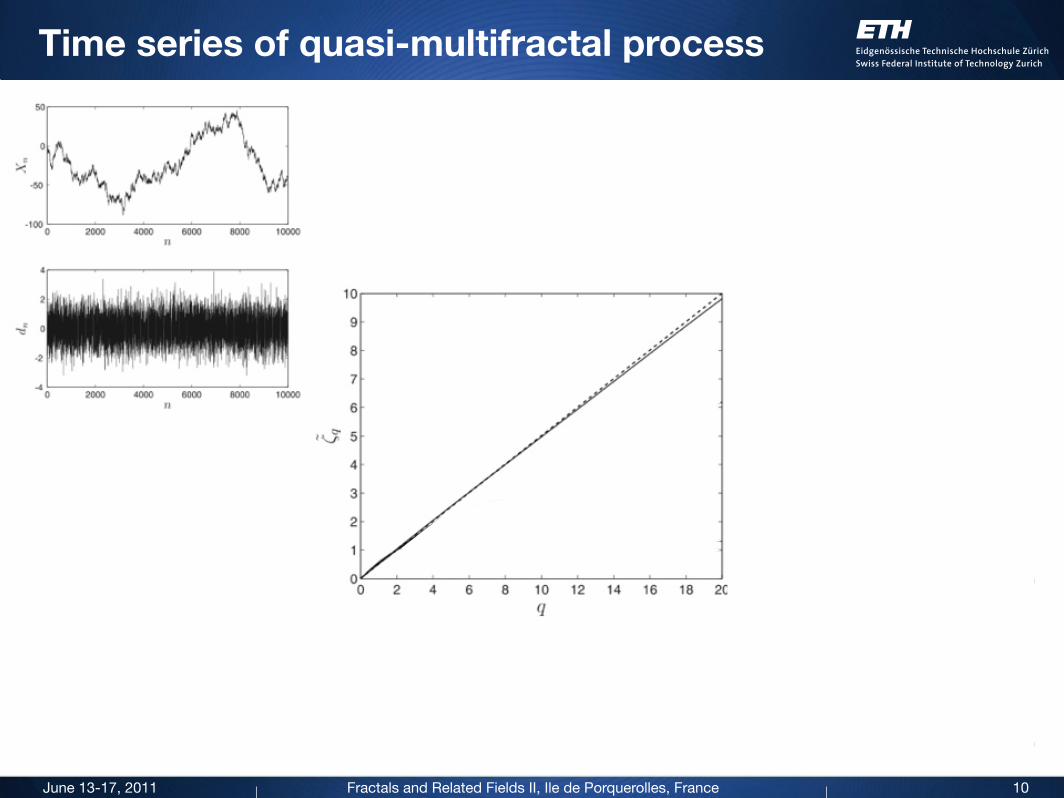

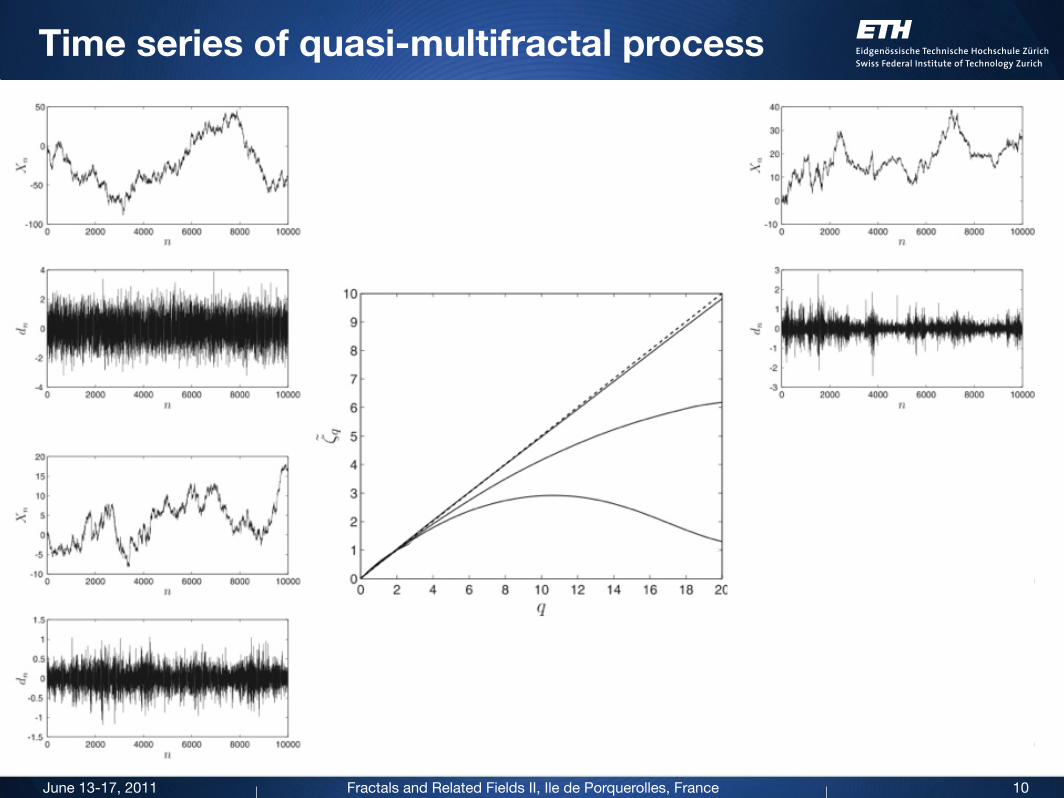

Time series of quasi-multifractal process

10

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

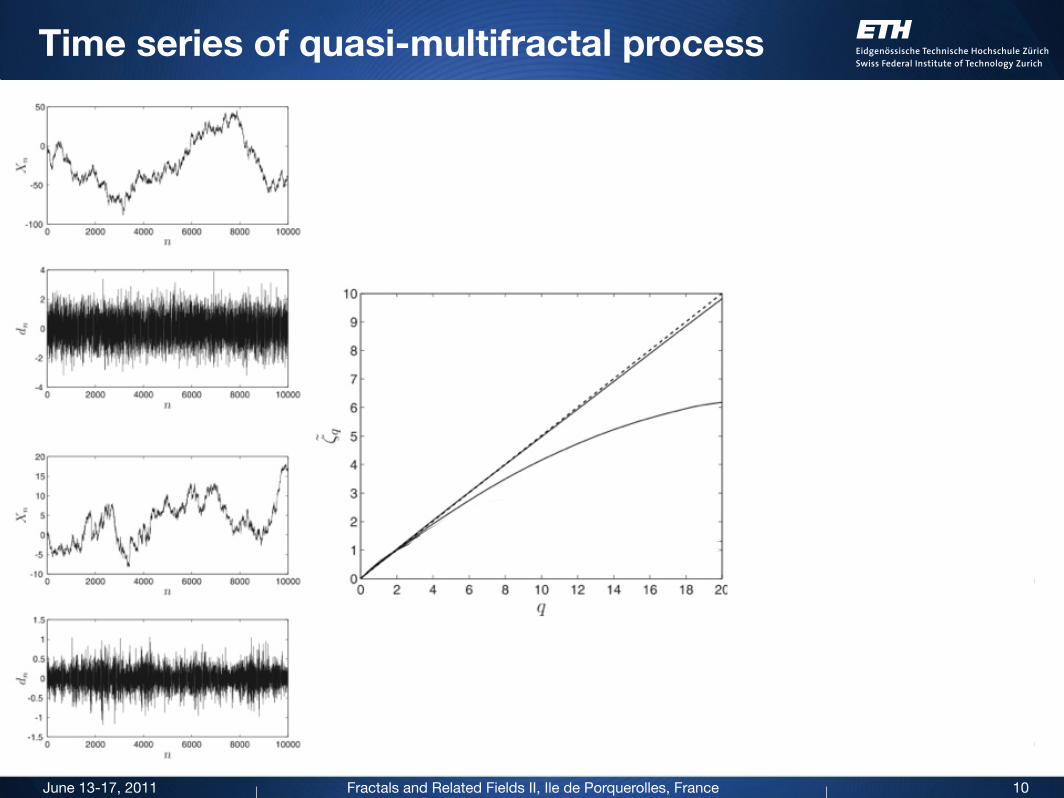

Time series of quasi-multifractal process

10

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Time series of quasi-multifractal process

10

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Time series of quasi-multifractal process

10

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

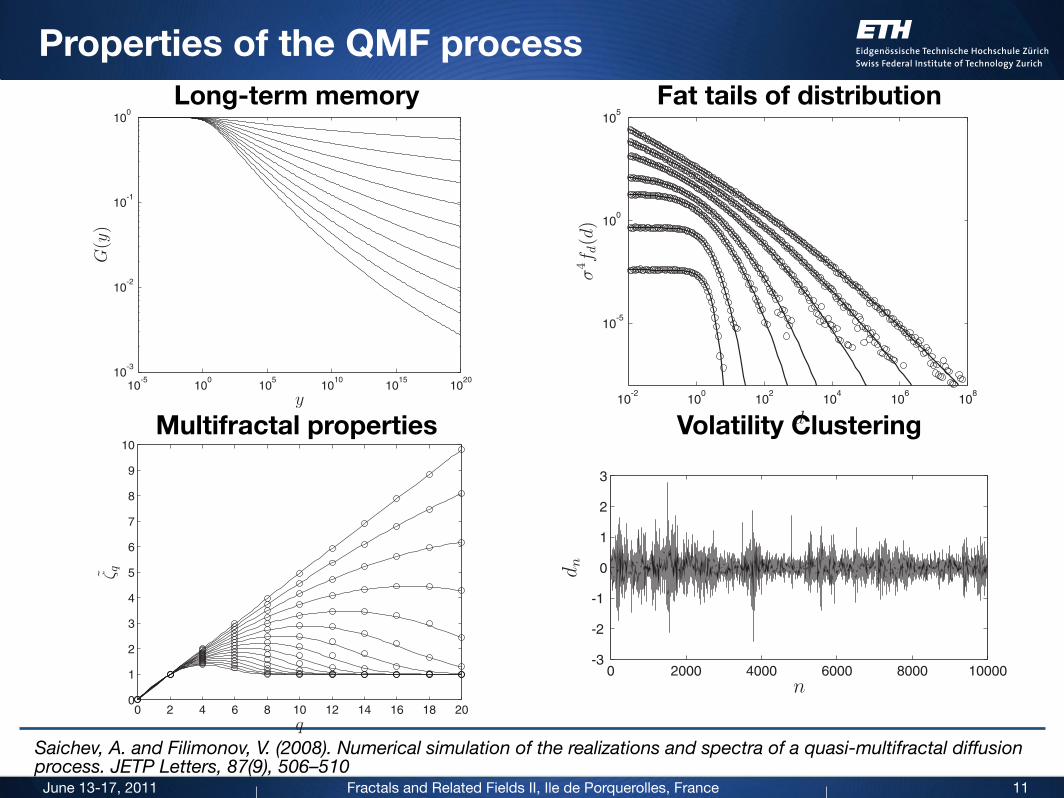

Properties of the QMF process

11

Saichev, A. and Filimonov, V. (2008). Numerical simulation of the realizations and spectra of a quasi-multifractal diffusion process. JETP Letters, 87(9), 506–510

Long-term memory Fat tails of distribution

Multifractal properties Volatility Clustering

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

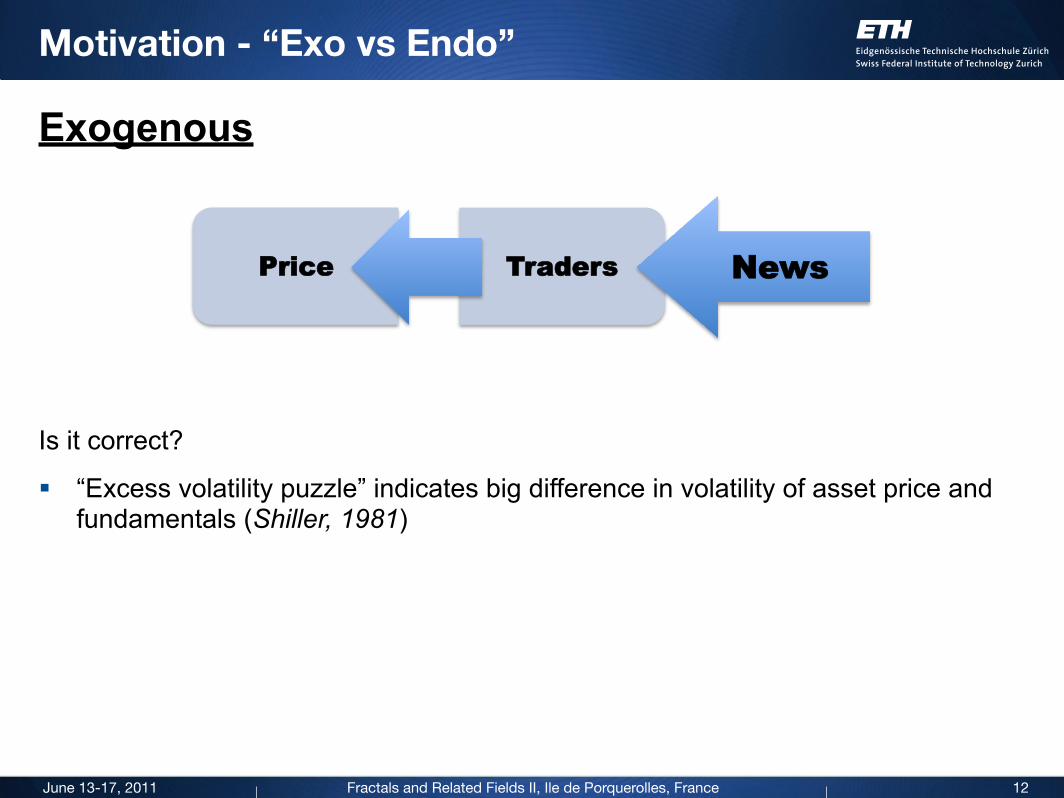

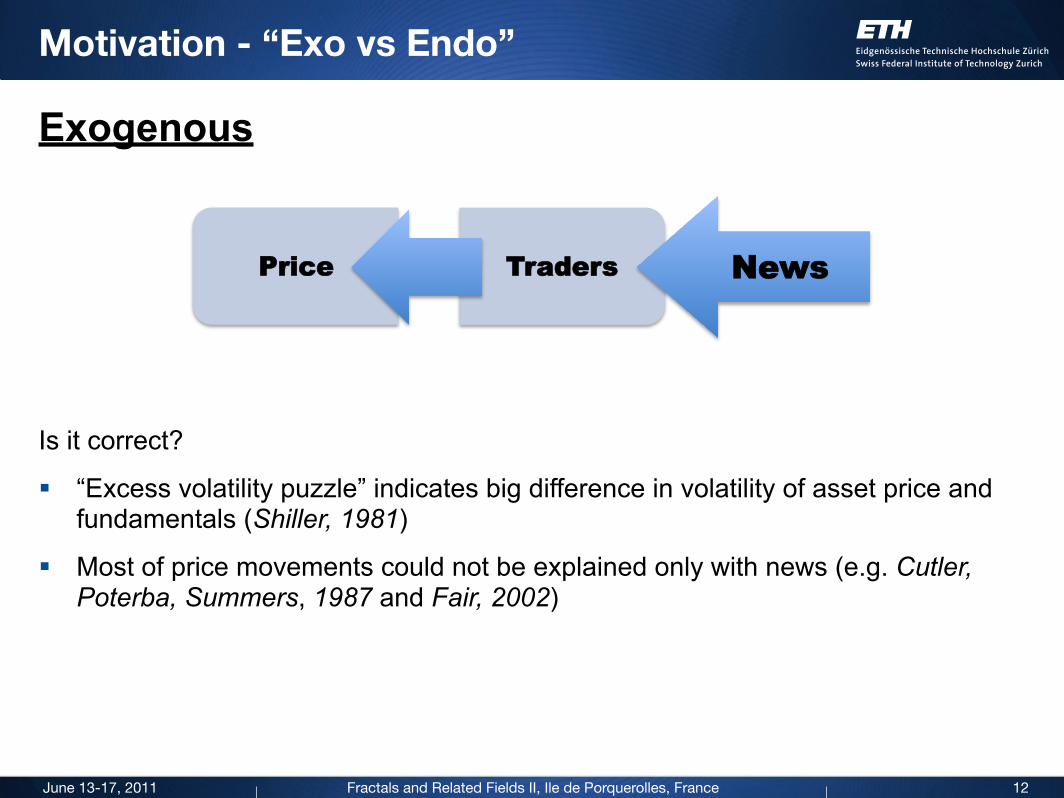

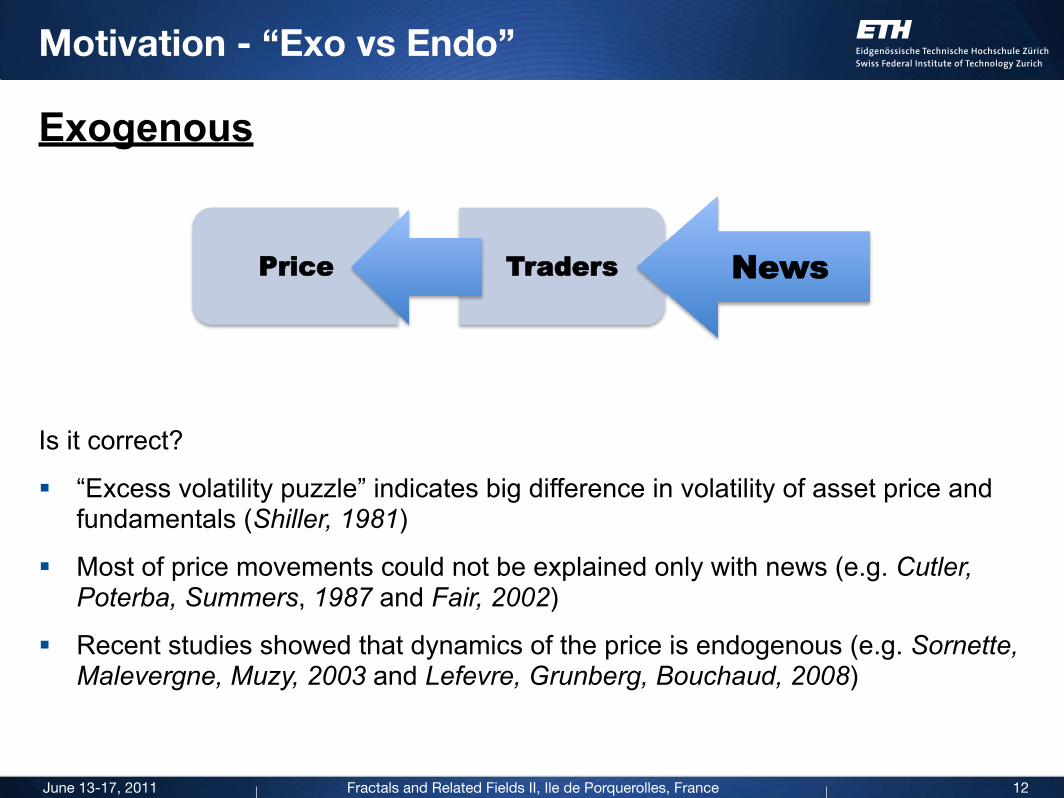

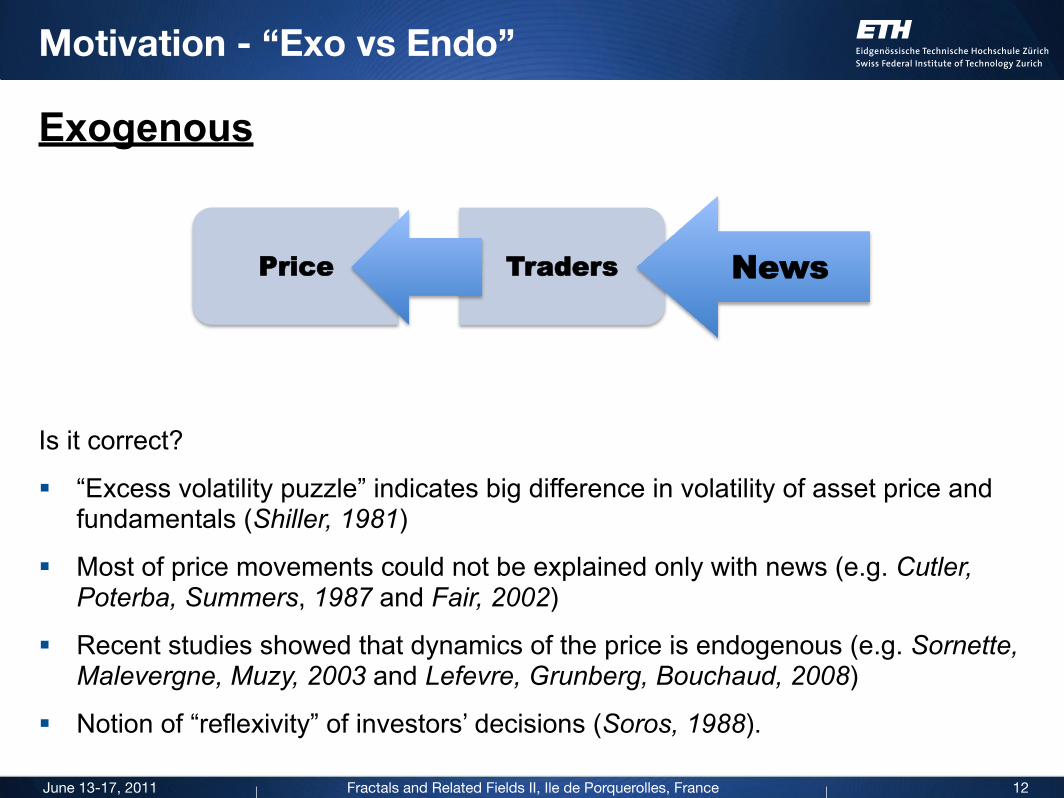

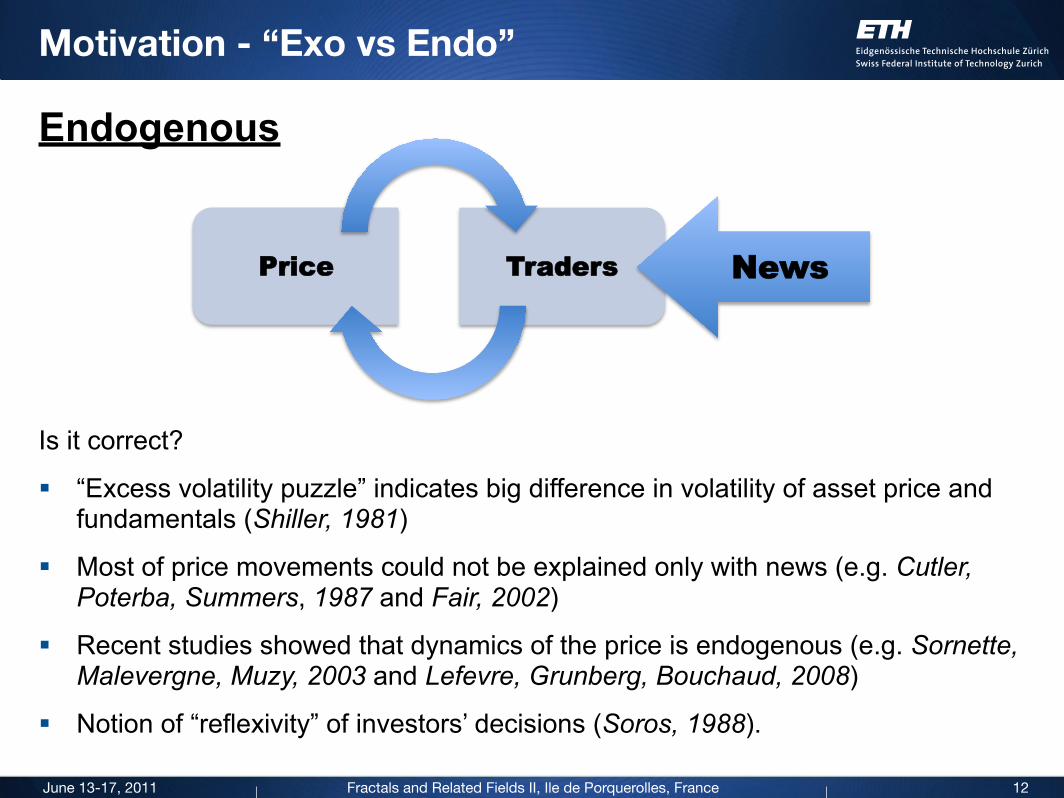

Motivation - “Exo vs Endo”

12

Price Traders News

Exogenous

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Exo vs Endo”

12

Price Traders News

Exogenous

Is it correct?

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Exo vs Endo”

12

Price Traders News

Exogenous

Is it correct?

§ “Excess volatility puzzle” indicates big difference in volatility of asset price and fundamentals (Shiller, 1981)

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Exo vs Endo”

12

Price Traders News

Exogenous

Is it correct?

§ “Excess volatility puzzle” indicates big difference in volatility of asset price and fundamentals (Shiller, 1981)

§ Most of price movements could not be explained only with news (e.g. Cutler, Poterba, Summers, 1987 and Fair, 2002)

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Exo vs Endo”

12

Price Traders News

Exogenous

Is it correct?

§ “Excess volatility puzzle” indicates big difference in volatility of asset price and fundamentals (Shiller, 1981)

§ Most of price movements could not be explained only with news (e.g. Cutler, Poterba, Summers, 1987 and Fair, 2002)

§ Recent studies showed that dynamics of the price is endogenous (e.g. Sornette, Malevergne, Muzy, 2003 and Lefevre, Grunberg, Bouchaud, 2008)

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Exo vs Endo”

12

Price Traders News

Exogenous

Is it correct?

§ “Excess volatility puzzle” indicates big difference in volatility of asset price and fundamentals (Shiller, 1981)

§ Most of price movements could not be explained only with news (e.g. Cutler, Poterba, Summers, 1987 and Fair, 2002)

§ Recent studies showed that dynamics of the price is endogenous (e.g. Sornette, Malevergne, Muzy, 2003 and Lefevre, Grunberg, Bouchaud, 2008)

§ Notion of “reflexivity” of investors’ decisions (Soros, 1988).

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Motivation - “Exo vs Endo”

12

Price Traders News

Endogenous

Is it correct?

§ “Excess volatility puzzle” indicates big difference in volatility of asset price and fundamentals (Shiller, 1981)

§ Most of price movements could not be explained only with news (e.g. Cutler, Poterba, Summers, 1987 and Fair, 2002)

§ Recent studies showed that dynamics of the price is endogenous (e.g. Sornette, Malevergne, Muzy, 2003 and Lefevre, Grunberg, Bouchaud, 2008)

§ Notion of “reflexivity” of investors’ decisions (Soros, 1988).

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

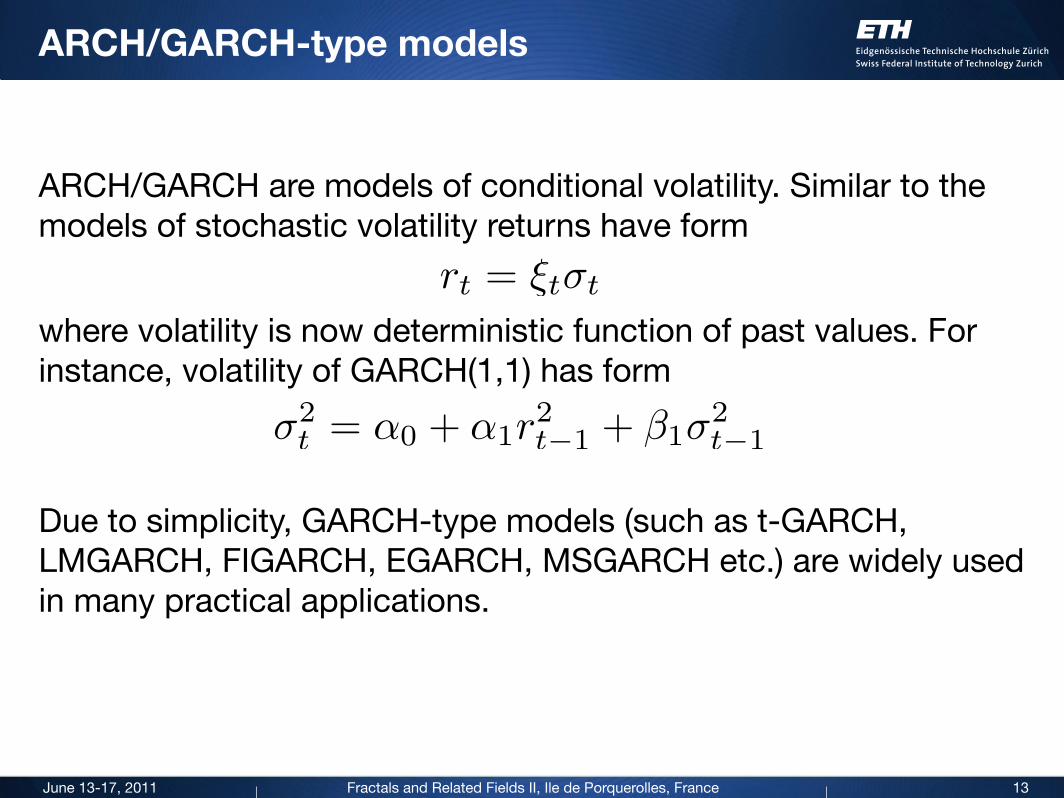

ARCH/GARCH-type models

13

ARCH/GARCH are models of conditional volatility. Similar to the models of stochastic volatility returns have form

where volatility is now deterministic function of past values. For instance, volatility of GARCH(1,1) has form

Due to simplicity, GARCH-type models (such as t-GARCH, LMGARCH, FIGARCH, EGARCH, MSGARCH etc.) are widely used in many practical applications.

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

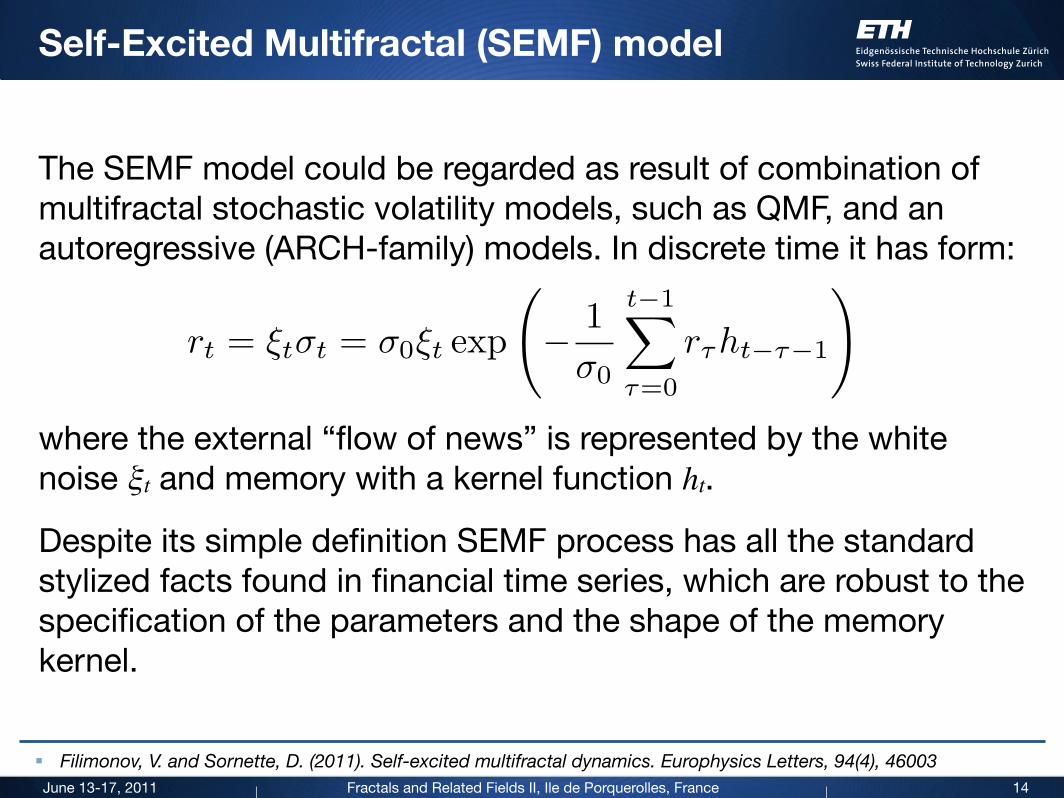

Self-Excited Multifractal (SEMF) model

The SEMF model could be regarded as result of combination of multifractal stochastic volatility models, such as QMF, and an autoregressive (ARCH-family) models. In discrete time it has form:

where the external “flow of news” is represented by the white noise ξt and memory with a kernel function ht.

Despite its simple definition SEMF process has all the standard stylized facts found in financial time series, which are robust to the specification of the parameters and the shape of the memory kernel.

14

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

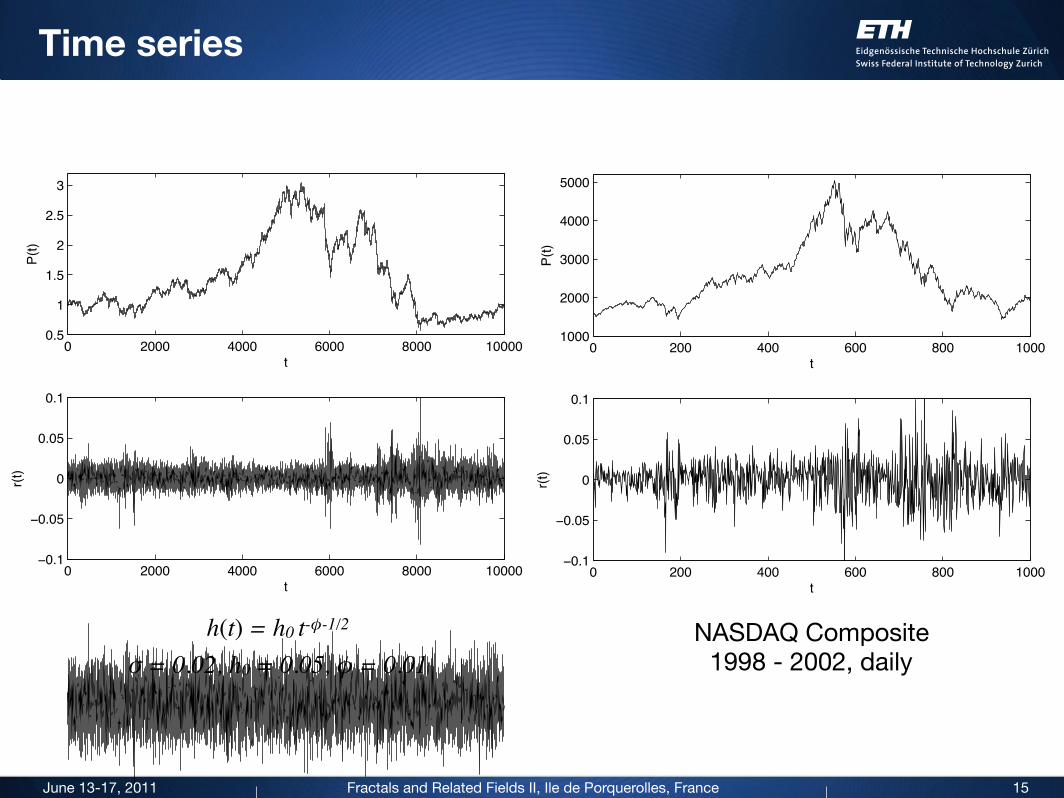

Time series

15

0 2000 4000 6000 8000 100000.5

1

1.5

2

2.5

3

t

P(t)

0 2000 4000 6000 8000 100000.1

0.05

0

0.05

0.1

t

r(t)

0 2000 4000 6000 8000 100004

2

0

2

4

t

(t)

0 200 400 600 800 10001000

2000

3000

4000

5000

t

P(t)

0 200 400 600 800 10000.1

0.05

0

0.05

0.1

t

r(t)

0 200 400 600 800 10000

0.2

0.4

0.6

0.8

1

t

(t)

h(t) = h0 t-φ-1/2

σ = 0.02, h0 = 0.05, φ = 0.01NASDAQ Composite

1998 - 2002, daily

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

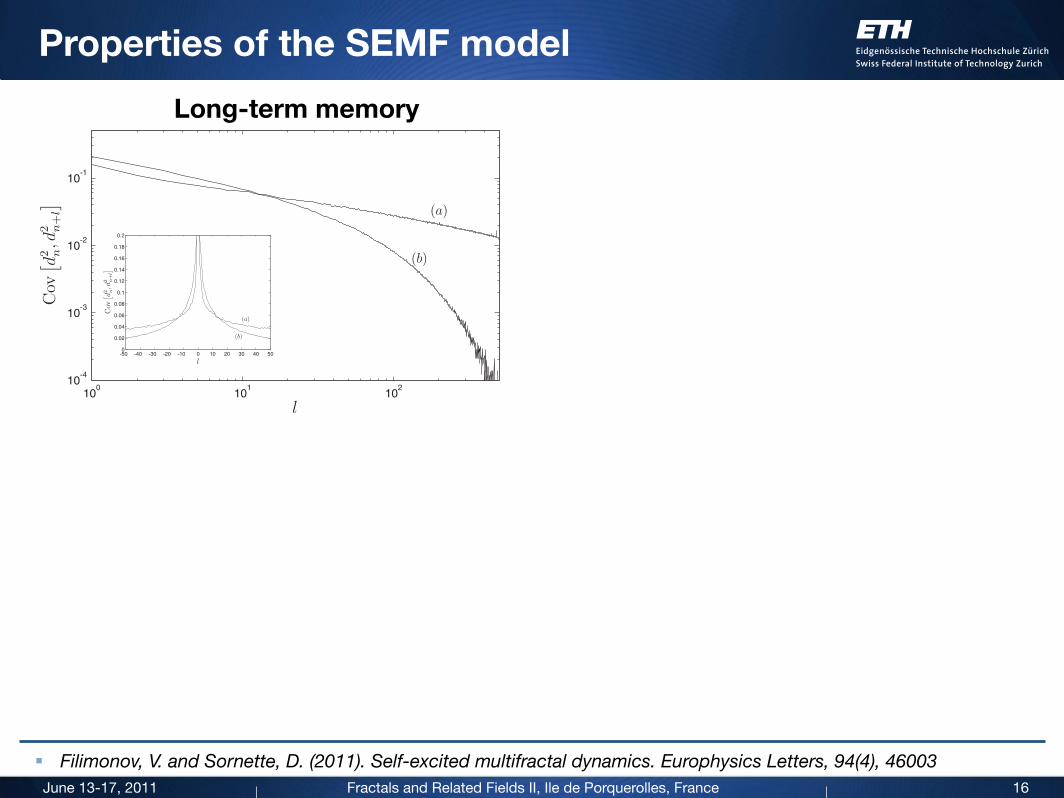

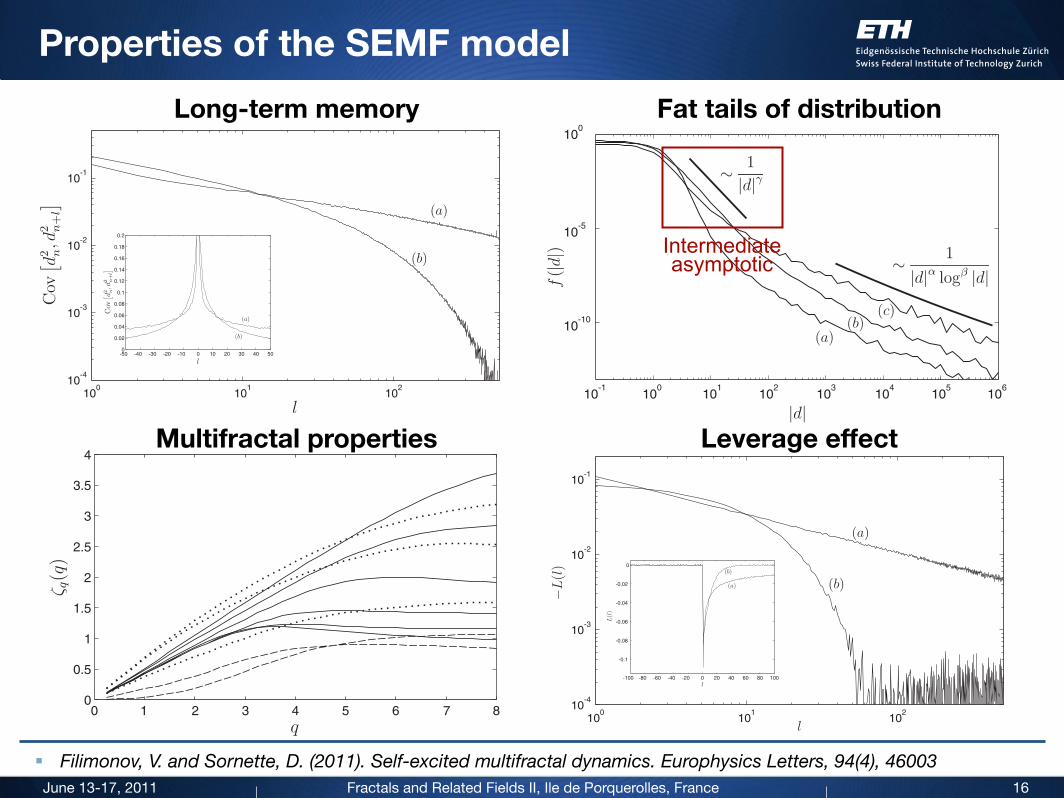

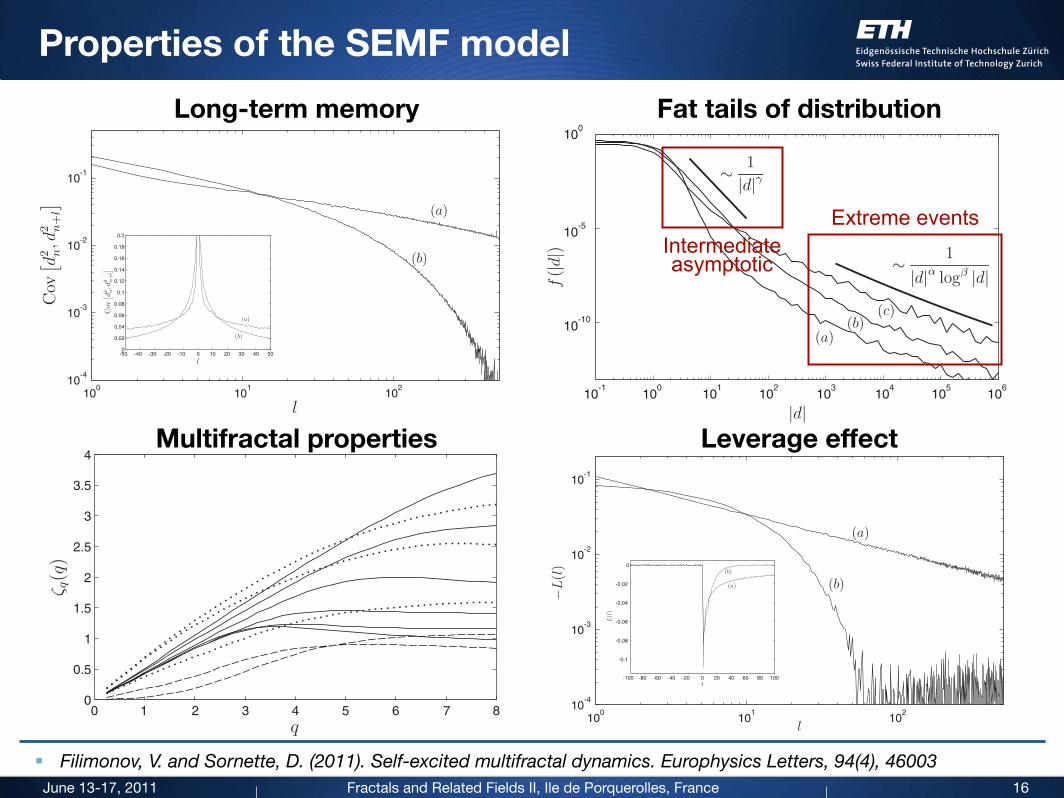

Properties of the SEMF model

16

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Long-term memory

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

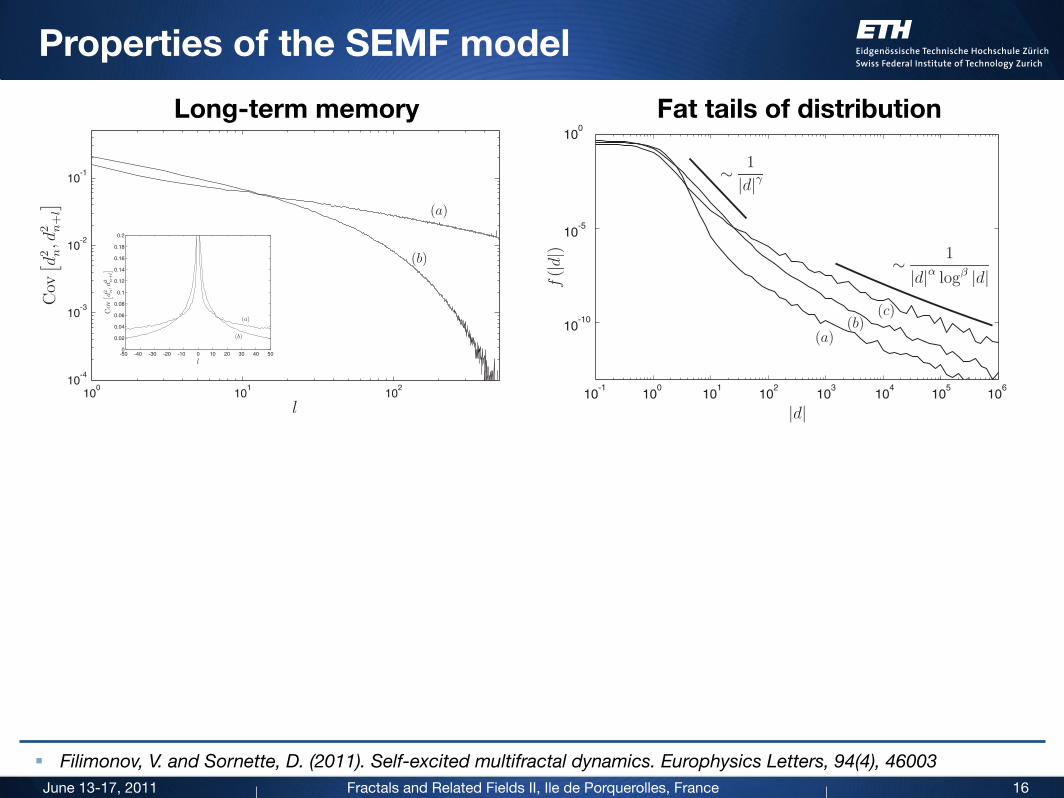

Properties of the SEMF model

16

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Long-term memory Fat tails of distribution

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Properties of the SEMF model

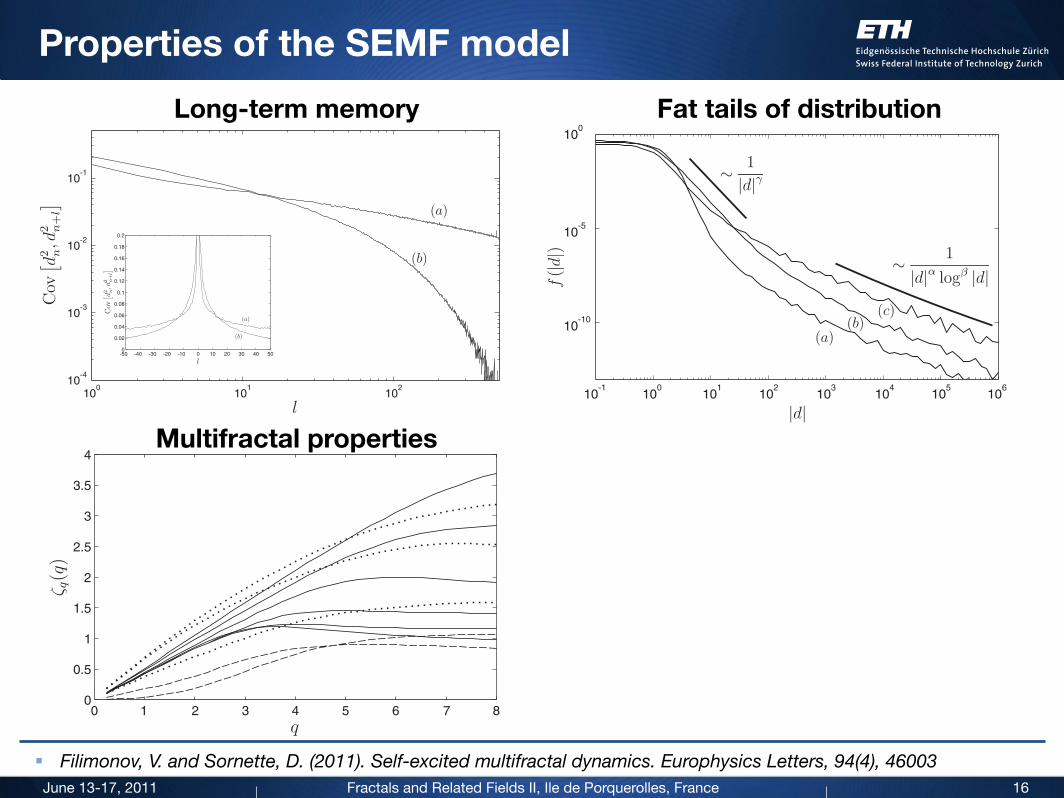

16

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Long-term memory Fat tails of distribution

Multifractal properties

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Properties of the SEMF model

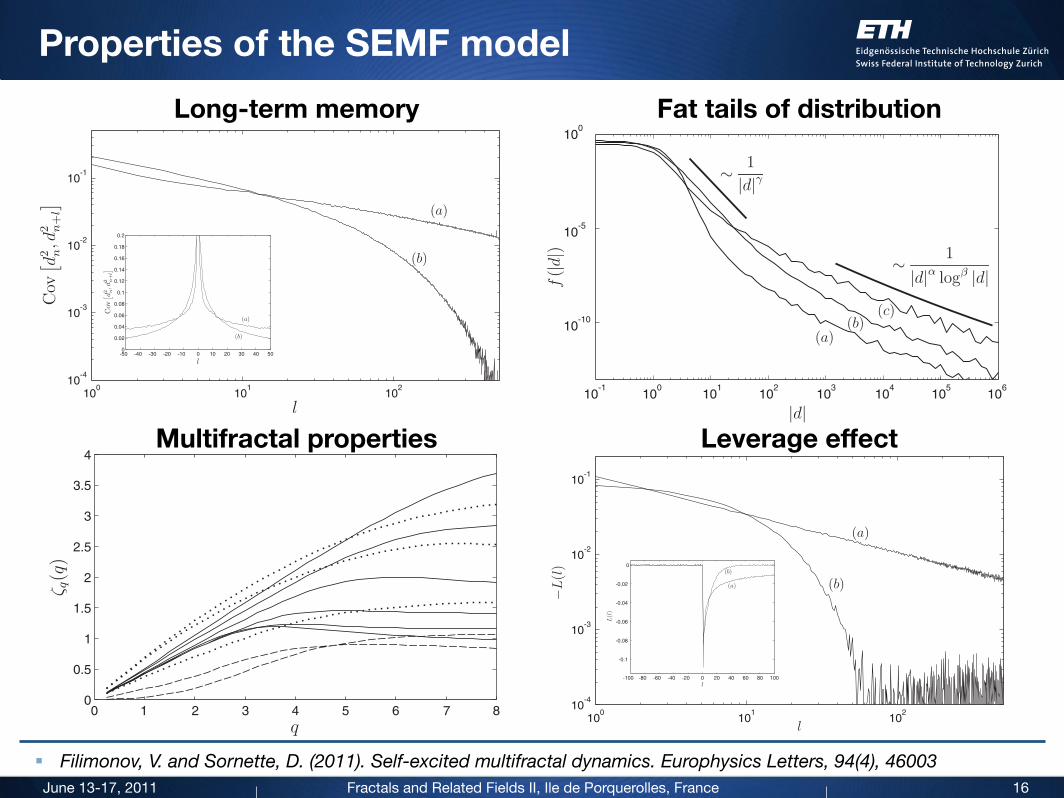

16

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Long-term memory Fat tails of distribution

Multifractal properties Leverage effect

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Properties of the SEMF model

16

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Long-term memory Fat tails of distribution

Multifractal properties Leverage effect

Intermediate asymptotic

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Properties of the SEMF model

16

§ Filimonov, V. and Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003

Long-term memory Fat tails of distribution

Multifractal properties Leverage effect

Intermediate asymptotic

Extreme events

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

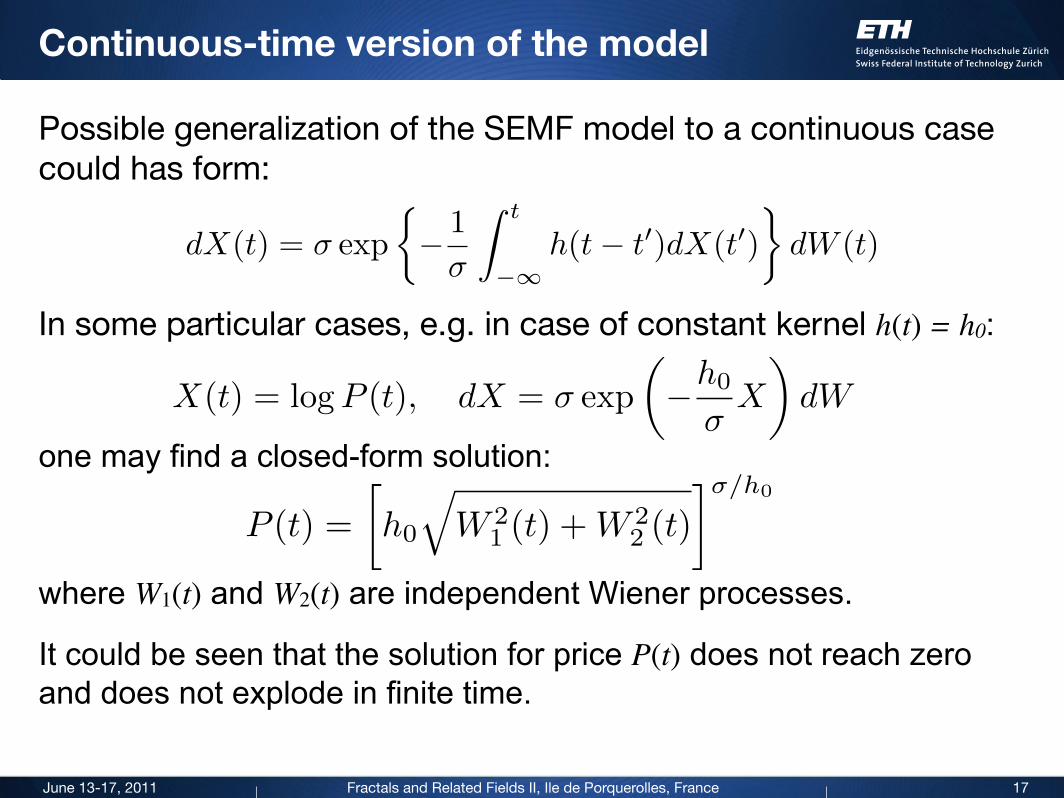

Continuous-time version of the model

17

Possible generalization of the SEMF model to a continuous case could has form:

In some particular cases, e.g. in case of constant kernel h(t) = h0:

one may find a closed-form solution:

where W1(t) and W2(t) are independent Wiener processes.

It could be seen that the solution for price P(t) does not reach zero and does not explode in finite time.

X(t) = logP (t), dX = σ exp

�−h0

σX

�dW

P (t) =

�h0

�W 2

1 (t) +W 22 (t)

�σ/h0

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Continuous-time version of the model

17

Possible generalization of the SEMF model to a continuous case could has form:

In some particular cases, e.g. in case of constant kernel h(t) = h0:

one may find a closed-form solution:

where W1(t) and W2(t) are independent Wiener processes.

It could be seen that the solution for price P(t) does not reach zero and does not explode in finite time.

X(t) = logP (t), dX = σ exp

�−h0

σX

�dW

P (t) =

�h0

�W 2

1 (t) +W 22 (t)

�σ/h0

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011 18

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

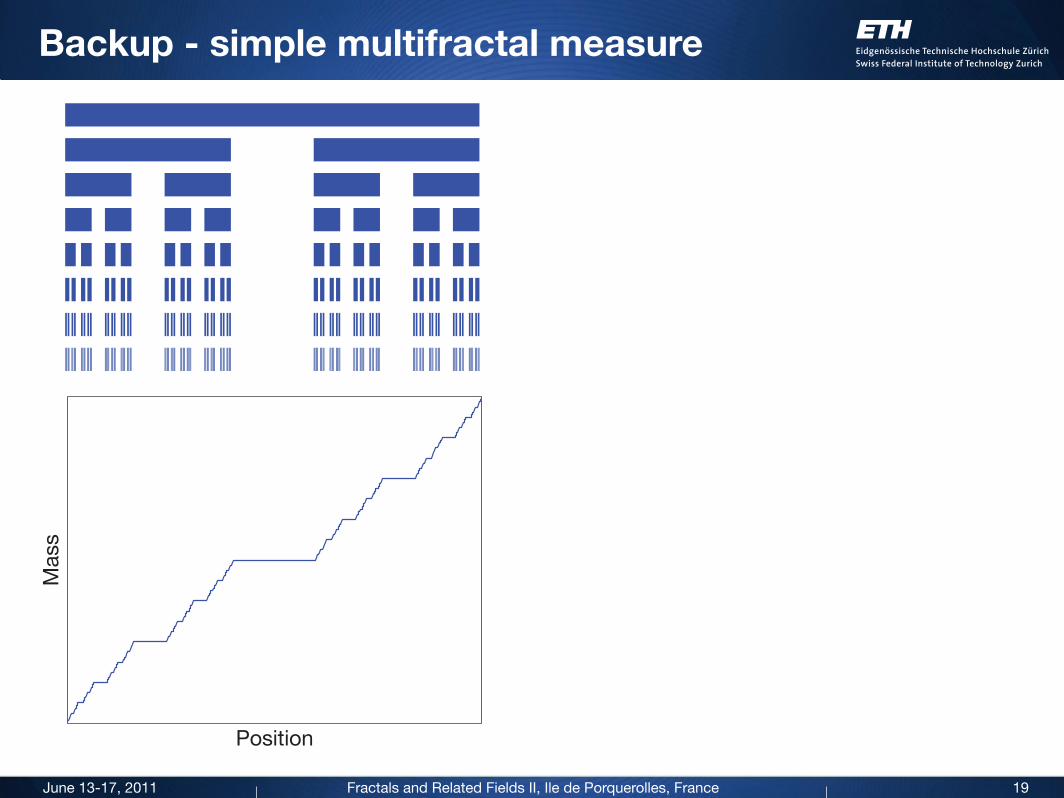

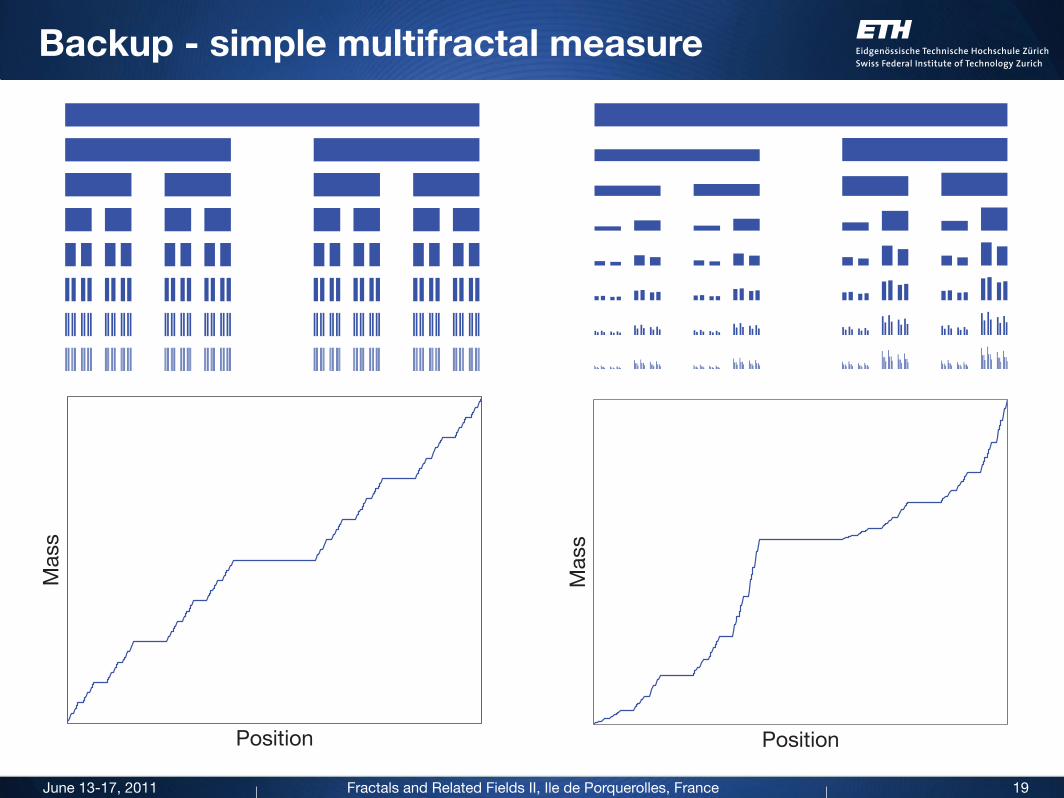

Backup - simple multifractal measure

19

Position

Mas

s

Fractals and Related Fields II, Ile de Porquerolles, FranceJune 13-17, 2011

Backup - simple multifractal measure

19

Position

Mas

s

Position

Mas

s