Embed Size (px)

Citation preview

TRUE NORTH CONSULTING

Team 1

April 23, 2016

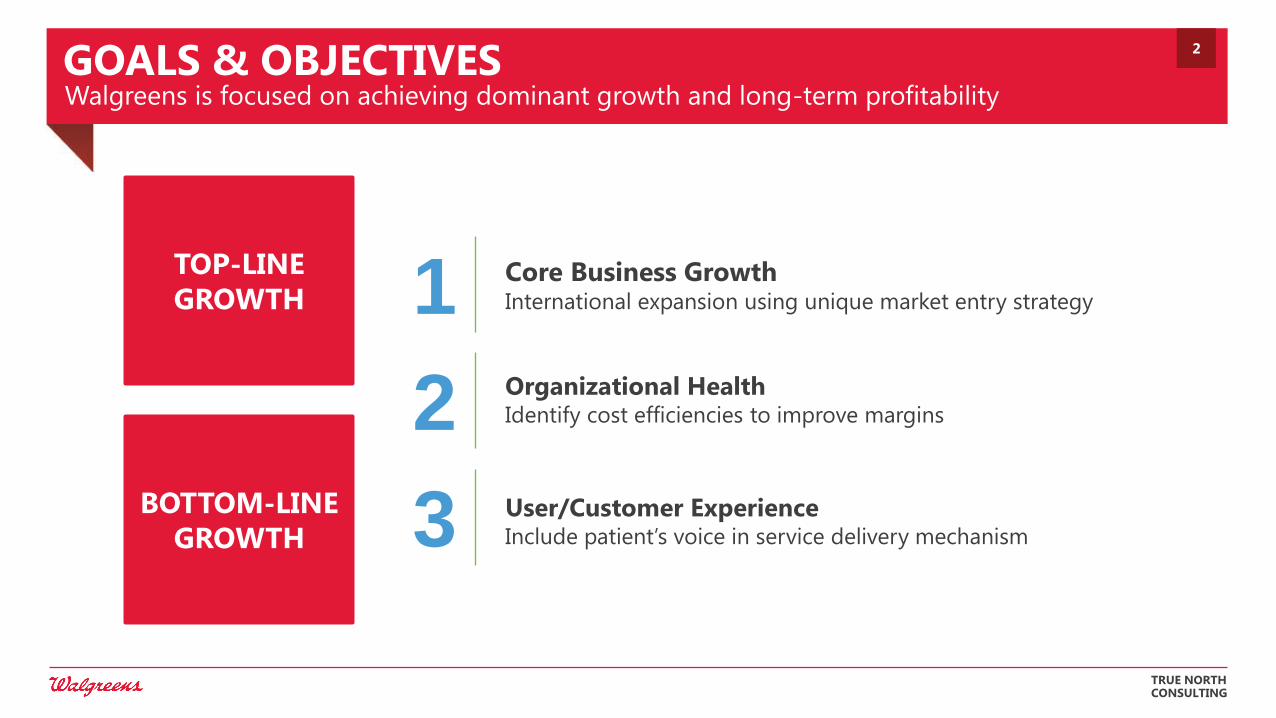

TOP-LINE

GROWTH

BOTTOM-LINE

GROWTH

GOALS & OBJECTIVES Walgreens is focused on achieving dominant growth and long-term profitability

1 Core Business Growth International expansion using unique market entry strategy

Organizational Health Identify cost efficiencies to improve margins

User/Customer Experience Include patient’s voice in service delivery mechanism

2

3

2

TRUE NORTH CONSULTING

DIAGNOSIS DOMINANCE DELIVERY

OUR 3D STRATEGY

DIAGNOSIS DOMINANCE DELIVERY

OUR 3D STRATEGY

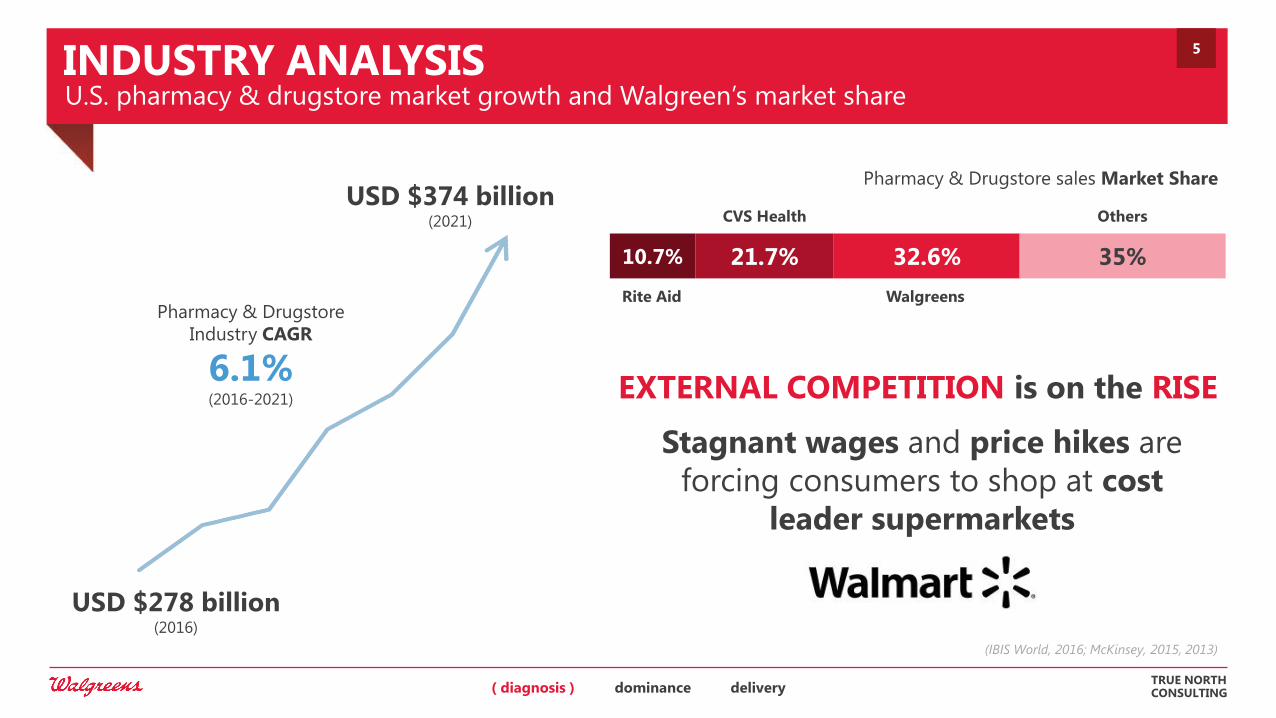

INDUSTRY ANALYSIS U.S. pharmacy & drugstore market growth and Walgreen’s market share

TRUE NORTH CONSULTING

Pharmacy & Drugstore

Industry CAGR

6.1% (2016-2021)

USD $278 billion (2016)

USD $374 billion (2021)

(IBIS World, 2016; McKinsey, 2015, 2013)

10.7% 21.7% 32.6% 35%

Rite Aid

CVS Health

Walgreens

Others

Pharmacy & Drugstore sales Market Share

EXTERNAL COMPETITION is on the RISE

Stagnant wages and price hikes are

forcing consumers to shop at cost

leader supermarkets

( diagnosis ) dominance delivery

5

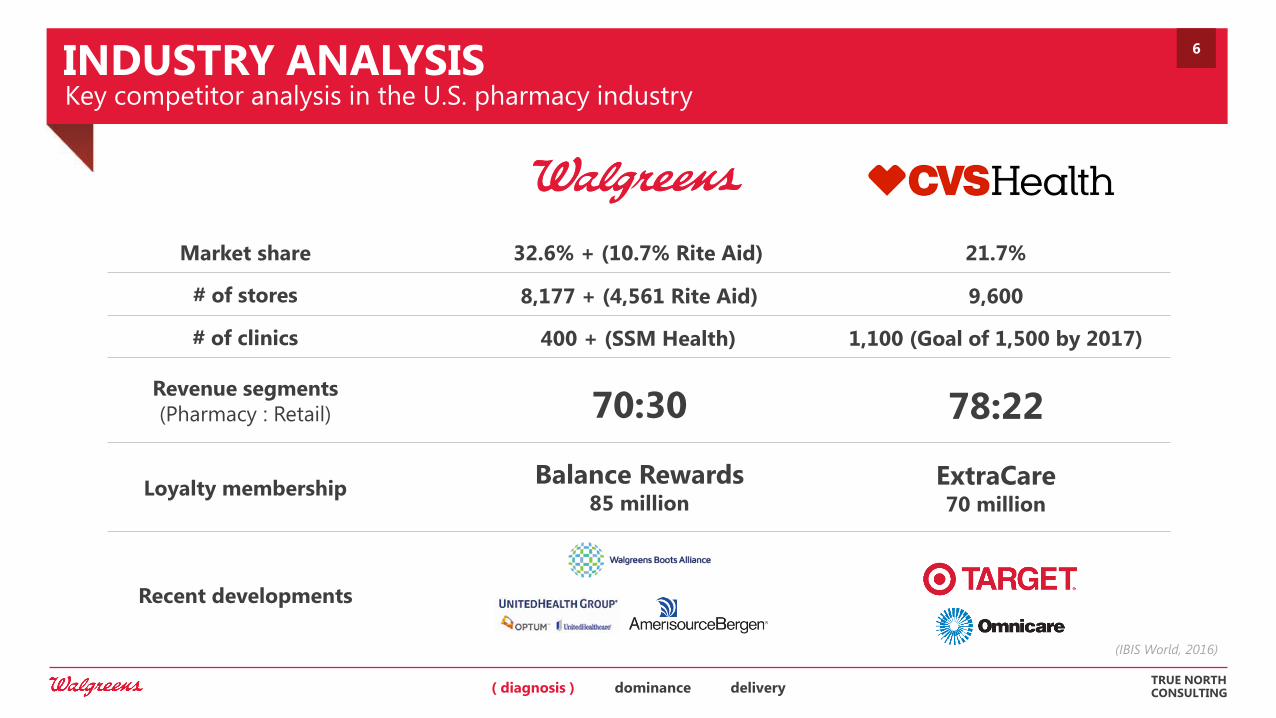

INDUSTRY ANALYSIS Key competitor analysis in the U.S. pharmacy industry

TRUE NORTH CONSULTING

(IBIS World, 2016)

6

( diagnosis ) dominance delivery

Market share

# of stores

# of clinics

Revenue segments

(Pharmacy : Retail)

Loyalty membership

32.6% + (10.7% Rite Aid) 21.7%

8,177 + (4,561 Rite Aid) 9,600

400 + (SSM Health) 1,100 (Goal of 1,500 by 2017)

70:30 78:22

Balance Rewards 85 million

ExtraCare 70 million

Recent developments

20

15

10

5

0

-5

-10 -10 -5 0 5 10 15 20

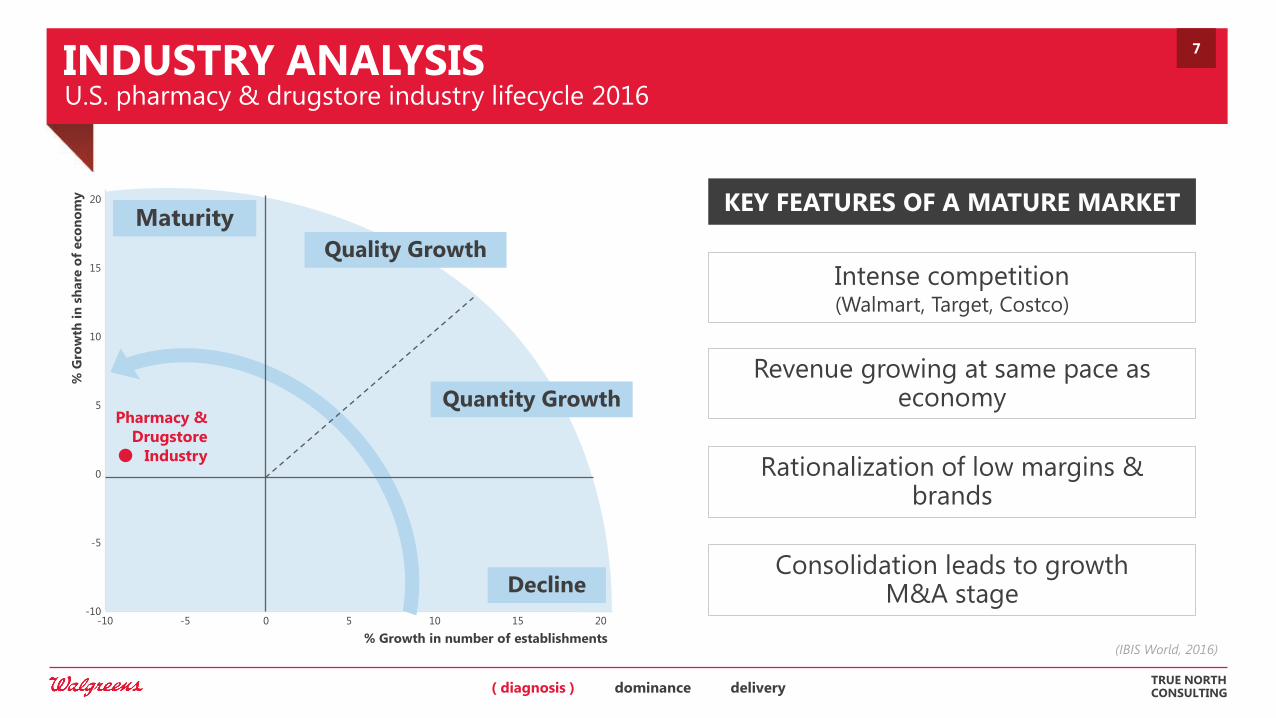

INDUSTRY ANALYSIS U.S. pharmacy & drugstore industry lifecycle 2016

TRUE NORTH CONSULTING

% Growth in number of establishments

% G

row

th i

n s

hare

of

eco

no

my

Quality Growth

Quantity Growth

Decline

Intense competition (Walmart, Target, Costco)

Revenue growing at same pace as economy

Rationalization of low margins & brands

Consolidation leads to growth M&A stage

Maturity

Pharmacy &

Drugstore

Industry

KEY FEATURES OF A MATURE MARKET

(IBIS World, 2016)

7

( diagnosis ) dominance delivery

STRATEGY REVIEW Using the Diamond E Model to identify significant factors of influence

TRUE NORTH CONSULTING

MANAGEMENT PREFERENCES

ORGANIZATION STRATEGY

CAPABILITIES & RESOURCES

ENVIRONMENT

• Mature U.S. market

• High competition; low CAGR

• Increasing regulations

• Growth by consolidation

• PPACA – Increased coverage

• Aging population

• Shift towards multi-format

offerings

GLOBAL MARKET LEADERS

Sustainable growth + Global dominance

• Market leader in the U.S.

• Post-merger integration

• Org: health & culture

• M&A

• Strategic alliances

• Vertical integration

Acquisition of

Rite Aid

($17.2 bn)

Experience in

global markets

(WBA)

Partnership

with Ameri-

sourceBergen

(IBIS World, 2016)

8

( diagnosis ) dominance delivery

DIAGNOSIS DOMINANCE DELIVERY

OUR 3D STRATEGY

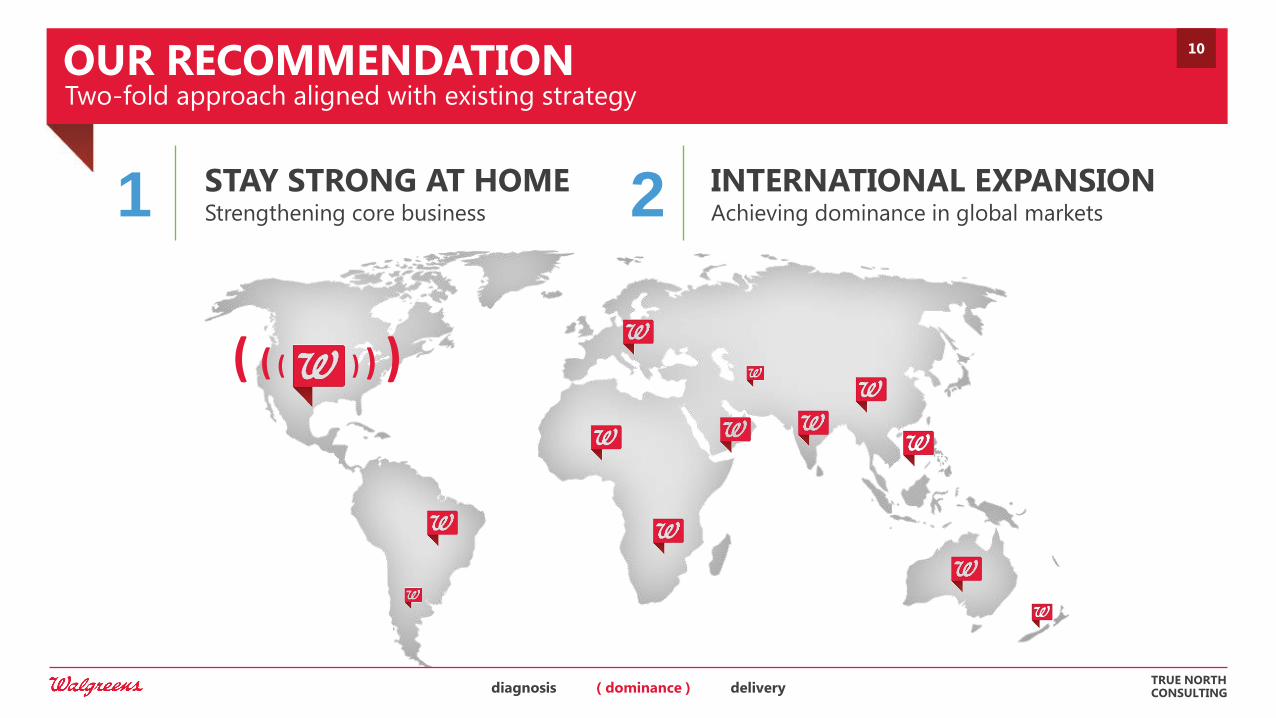

OUR RECOMMENDATION Two-fold approach aligned with existing strategy

TRUE NORTH CONSULTING

STAY STRONG AT HOME Strengthening core business 1 INTERNATIONAL EXPANSION

Achieving dominance in global markets 2

( ( ( ) ) )

10

diagnosis ( dominance ) delivery

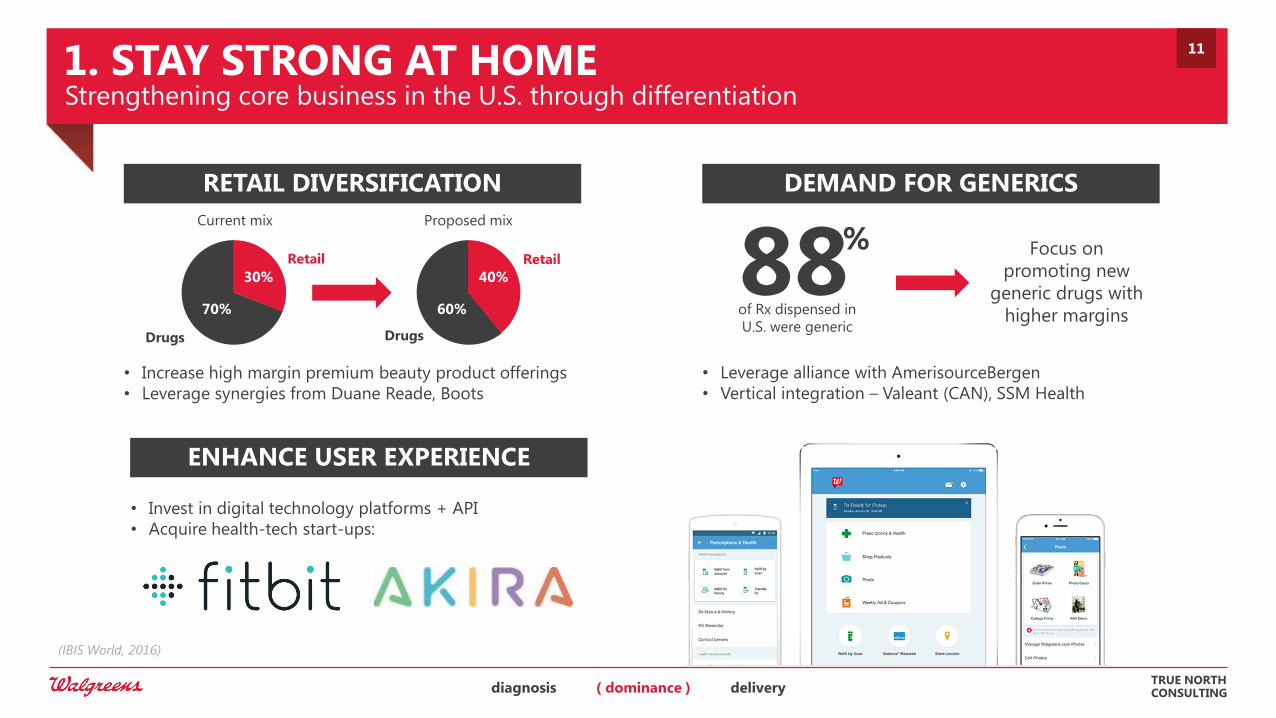

1. STAY STRONG AT HOME Strengthening core business in the U.S. through differentiation

TRUE NORTH CONSULTING

RETAIL DIVERSIFICATION

Current mix

70%

30%

Proposed mix

60%

40%

• Increase high margin premium beauty product offerings

• Leverage synergies from Duane Reade, Boots

DEMAND FOR GENERICS

• Leverage alliance with AmerisourceBergen

• Vertical integration – Valeant (CAN), SSM Health

88 %

of Rx dispensed in

U.S. were generic

Focus on

promoting new

generic drugs with

higher margins

ENHANCE USER EXPERIENCE

• Invest in digital technology platforms + API

• Acquire health-tech start-ups:

Retail Retail

Drugs Drugs

11

diagnosis ( dominance ) delivery

(IBIS World, 2016)

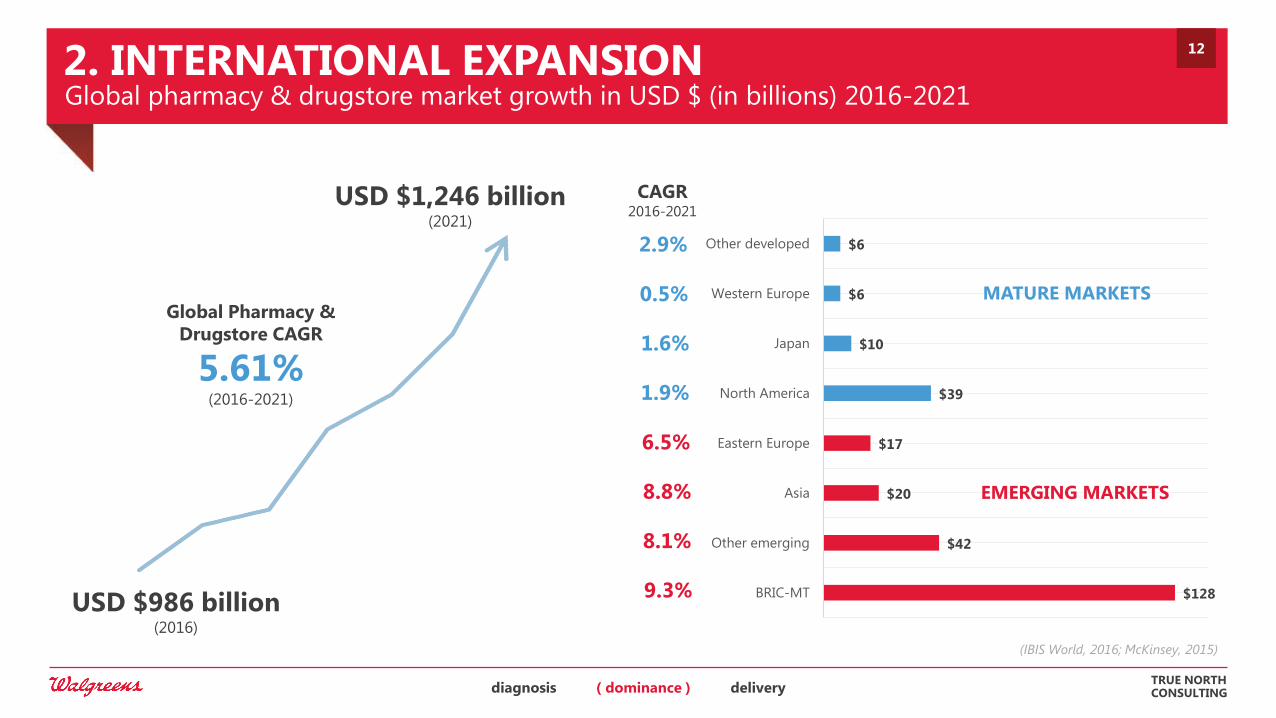

2. INTERNATIONAL EXPANSION Global pharmacy & drugstore market growth in USD $ (in billions) 2016-2021

TRUE NORTH CONSULTING

$128

$42

$20

$17

$39

$10

$6

$6

BRIC-MT

Other emerging

Asia

Eastern Europe

North America

Japan

Western Europe

Other developed

MATURE MARKETS

EMERGING MARKETS

2.9%

0.5%

1.6%

1.9%

6.5%

8.8%

8.1%

9.3%

CAGR 2016-2021

Global Pharmacy &

Drugstore CAGR

5.61% (2016-2021)

USD $986 billion (2016)

USD $1,246 billion (2021)

(IBIS World, 2016; McKinsey, 2015)

12

diagnosis ( dominance ) delivery

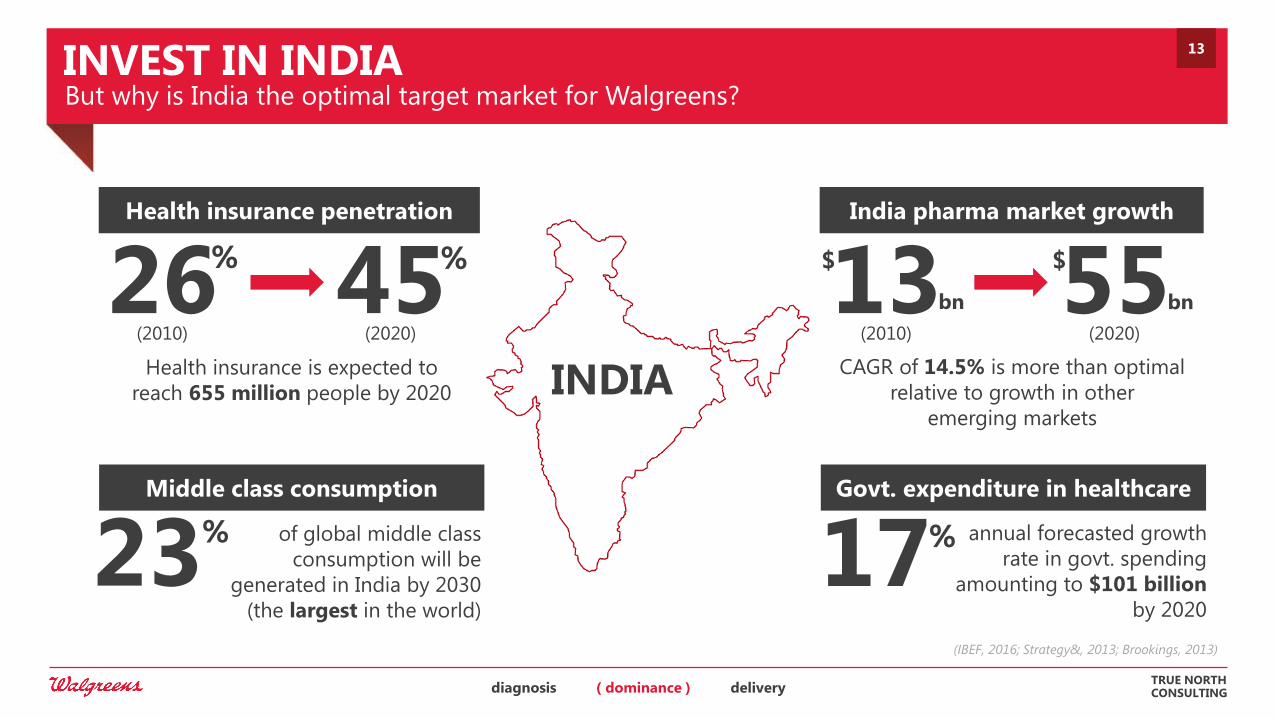

INVEST IN INDIA But why is India the optimal target market for Walgreens?

TRUE NORTH CONSULTING

annual forecasted growth

rate in govt. spending

amounting to $101 billion

by 2020

INDIA Health insurance is expected to

reach 655 million people by 2020

Health insurance penetration

26 45 % %

(2010) (2020)

CAGR of 14.5% is more than optimal

relative to growth in other

emerging markets

India pharma market growth

13 55 bn

(2010) (2020)

bn

$

Middle class consumption Govt. expenditure in healthcare

of global middle class

consumption will be

generated in India by 2030

(the largest in the world)

17

$

% 23 %

13

diagnosis ( dominance ) delivery

(IBEF, 2016; Strategy&, 2013; Brookings, 2013)

20

15

10

5

0

-5

-10 -10 -5 0 5 10 15 20

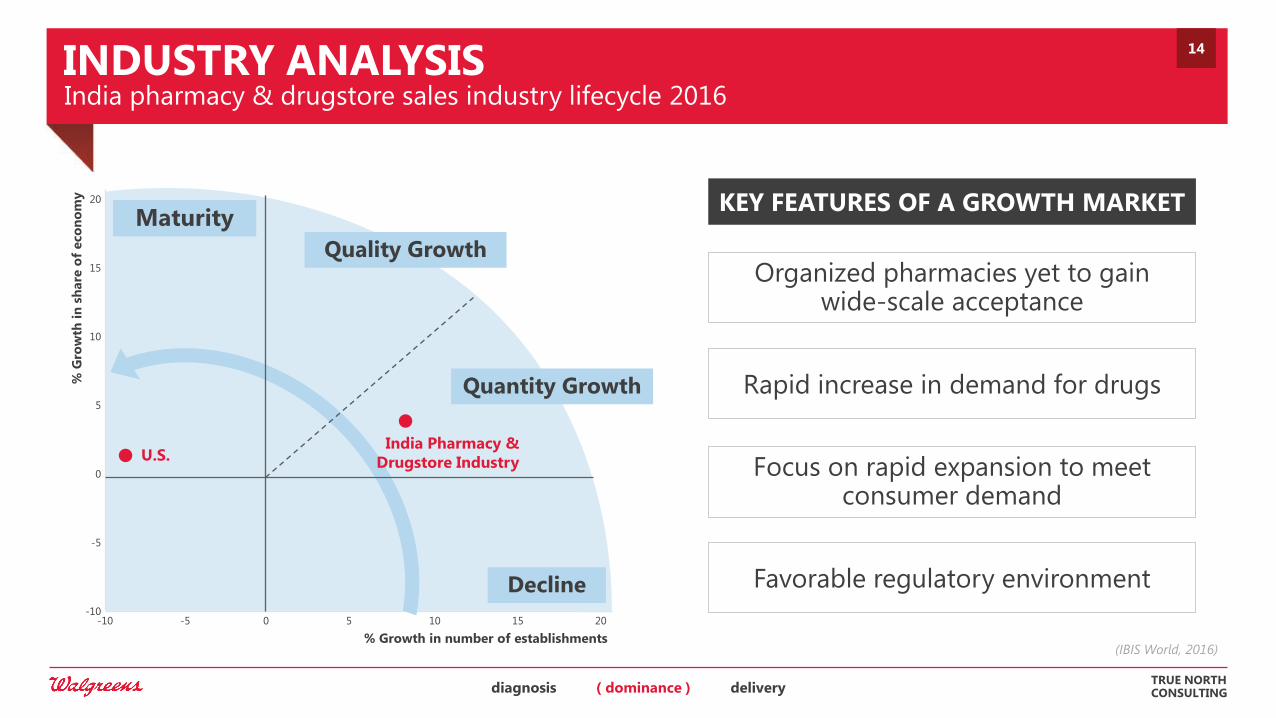

INDUSTRY ANALYSIS India pharmacy & drugstore sales industry lifecycle 2016

TRUE NORTH CONSULTING

% Growth in number of establishments

% G

row

th i

n s

hare

of

eco

no

my

Quality Growth

Quantity Growth

Decline

Organized pharmacies yet to gain wide-scale acceptance

Rapid increase in demand for drugs

Focus on rapid expansion to meet consumer demand

Maturity KEY FEATURES OF A GROWTH MARKET

India Pharmacy &

Drugstore Industry

(IBIS World, 2016)

Favorable regulatory environment

U.S.

14

diagnosis ( dominance ) delivery

DIAGNOSIS DOMINANCE DELIVERY

OUR 3D STRATEGY

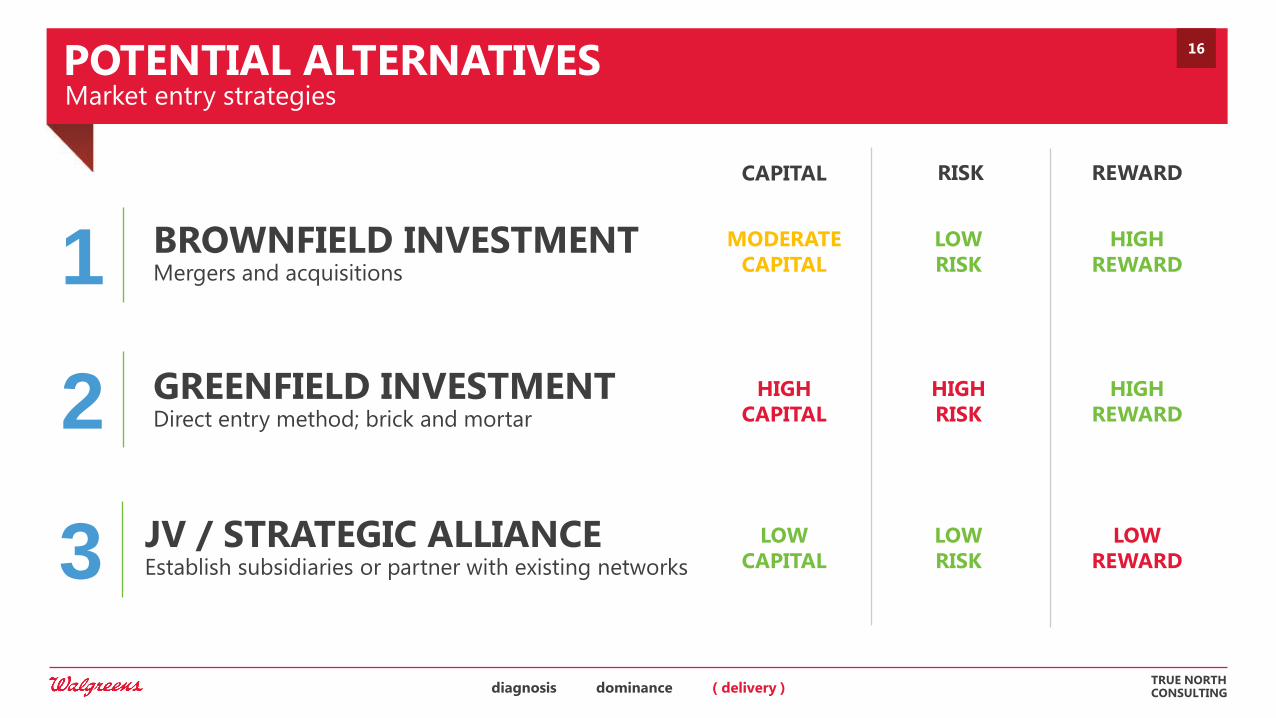

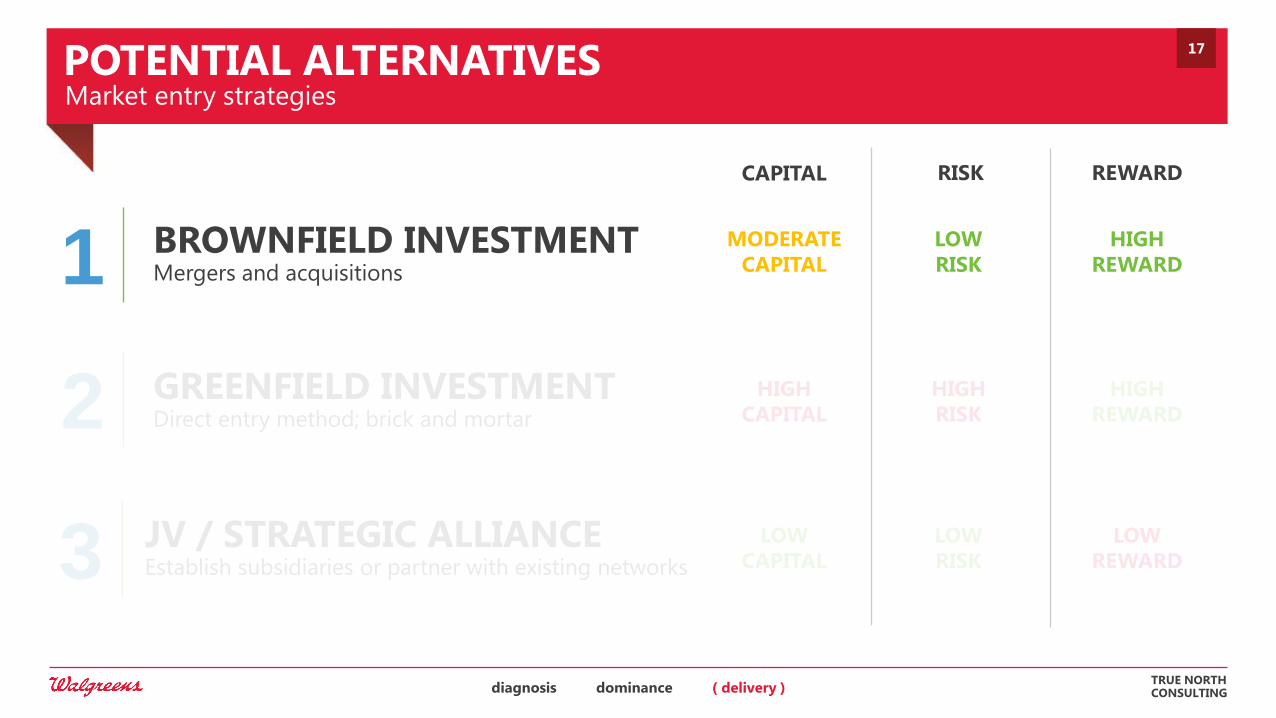

POTENTIAL ALTERNATIVES Market entry strategies

TRUE NORTH CONSULTING

2 GREENFIELD INVESTMENT Direct entry method; brick and mortar

BROWNFIELD INVESTMENT Mergers and acquisitions 1

JV / STRATEGIC ALLIANCE Establish subsidiaries or partner with existing networks 3

CAPITAL RISK REWARD

MODERATE

CAPITAL

LOW

RISK

HIGH

REWARD

HIGH

CAPITAL

HIGH

RISK

HIGH

REWARD

LOW

CAPITAL

LOW

RISK

LOW

REWARD

16

diagnosis dominance ( delivery )

POTENTIAL ALTERNATIVES Market entry strategies

TRUE NORTH CONSULTING

2 GREENFIELD INVESTMENT Direct entry method; brick and mortar

BROWNFIELD INVESTMENT Mergers and acquisitions 1

JV / STRATEGIC ALLIANCE Establish subsidiaries or partner with existing networks 3

CAPITAL RISK REWARD

MODERATE

CAPITAL

LOW

RISK

HIGH

REWARD

HIGH

CAPITAL

HIGH

RISK

HIGH

REWARD

LOW

CAPITAL

LOW

RISK

LOW

REWARD

17

diagnosis dominance ( delivery )

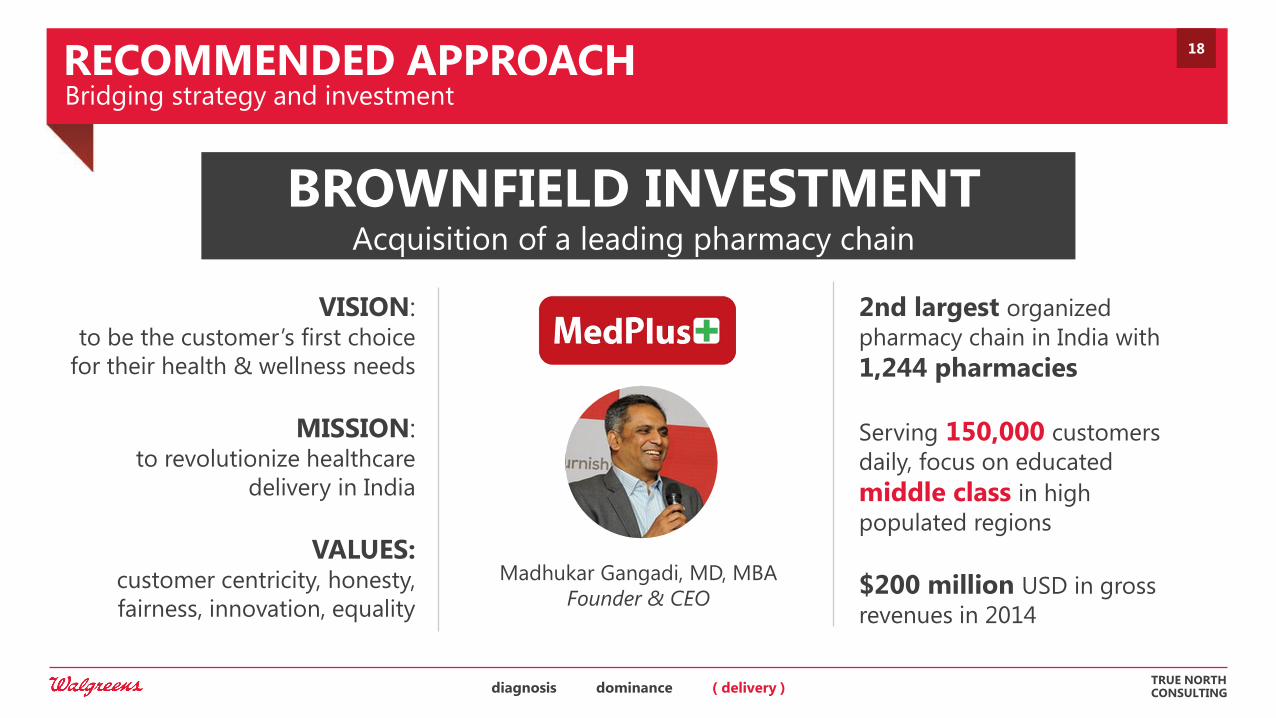

RECOMMENDED APPROACH Bridging strategy and investment

TRUE NORTH CONSULTING

VISION: to be the customer’s first choice

for their health & wellness needs

MISSION: to revolutionize healthcare

delivery in India

VALUES: customer centricity, honesty,

fairness, innovation, equality

2nd largest organized

pharmacy chain in India with

1,244 pharmacies

Serving 150,000 customers

daily, focus on educated

middle class in high

populated regions

$200 million USD in gross

revenues in 2014

BROWNFIELD INVESTMENT Acquisition of a leading pharmacy chain

Madhukar Gangadi, MD, MBA

Founder & CEO

18

diagnosis dominance ( delivery )

LEVERAGING SYNERGIES Strategic rationale & financial benefits of the MedPlus acquisition

TRUE NORTH CONSULTING

STRATEGIC RATIONALE FINANCIAL BENEFITS

1. OPERATIONAL SYNERGIES

Economies of scale

Higher growth in new market

2. FINANCIAL SYNERGIES

Debt capacity

30 million USD

$ In total potential

synergies by the

year 2021

1. Perfectly aligned vision and

values

2. Advances Walgreens strategy

to be global healthcare leaders

3. Allow direct access to fastest

growing pharmacy market

19

diagnosis dominance ( delivery )

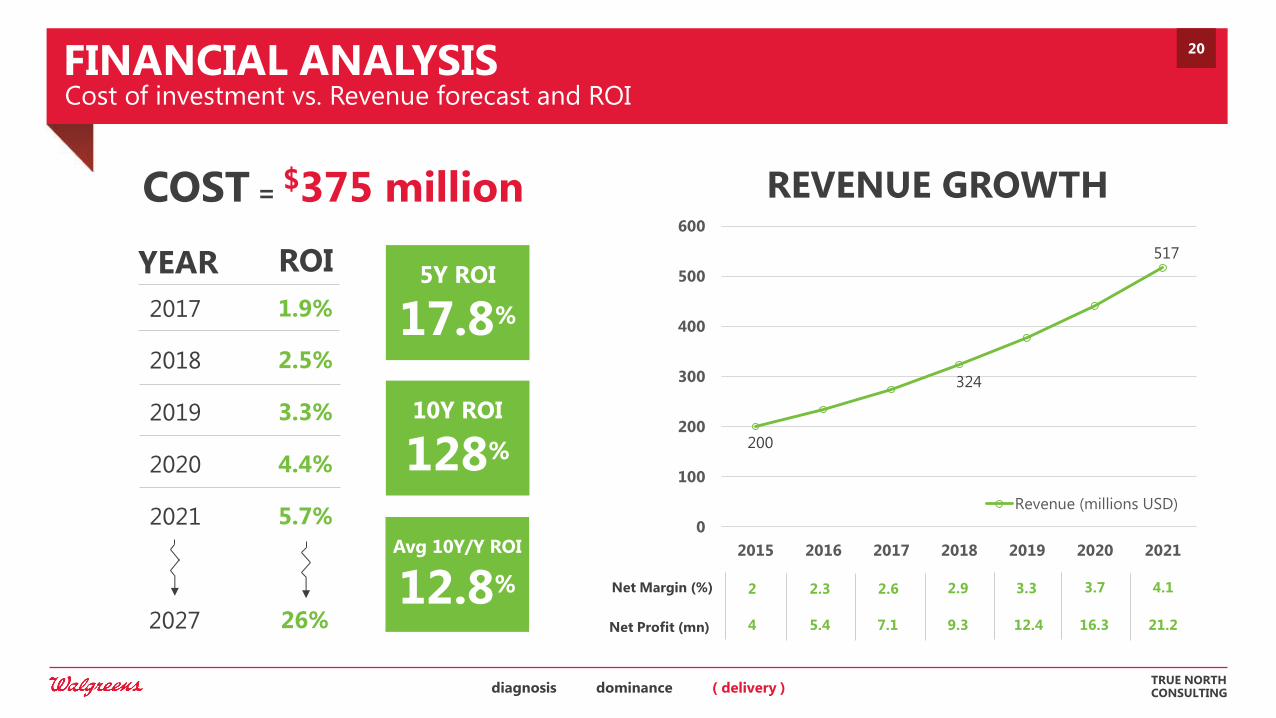

FINANCIAL ANALYSIS Cost of investment vs. Revenue forecast and ROI

TRUE NORTH CONSULTING

200

324

517

0

100

200

300

400

500

600

2015 2016 2017 2018 2019 2020 2021

REVENUE GROWTH

Revenue (millions USD)

Net Margin (%)

Net Profit (mn)

2 2.3 2.6 2.9 3.3 3.7 4.1

4 5.4 7.1 9.3 12.4 16.3 21.2

COST = $375 million

ROI YEAR

2017

2018

2019

2020

2021

1.9%

2.5%

3.3%

4.4%

5.7%

5Y ROI

17.8%

Avg 10Y/Y ROI

12.8%

10Y ROI

128%

2027 26%

20

diagnosis dominance ( delivery )

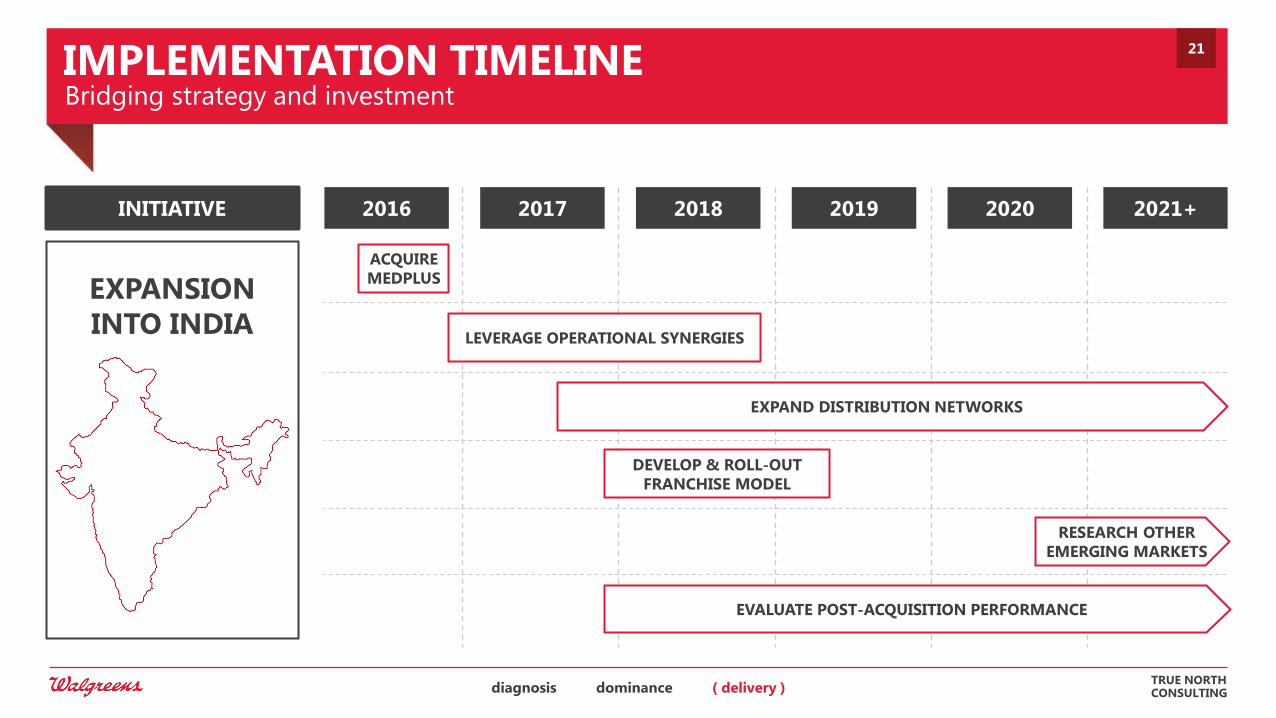

IMPLEMENTATION TIMELINE Bridging strategy and investment

TRUE NORTH CONSULTING

INITIATIVE 2016 2017 2018 2019 2020 2021+

EXPANSION

INTO INDIA

ACQUIRE

MEDPLUS

LEVERAGE OPERATIONAL SYNERGIES

EXPAND DISTRIBUTION NETWORKS

DEVELOP & ROLL-OUT

FRANCHISE MODEL

RESEARCH OTHER

EMERGING MARKETS

EVALUATE POST-ACQUISITION PERFORMANCE

21

diagnosis dominance ( delivery )

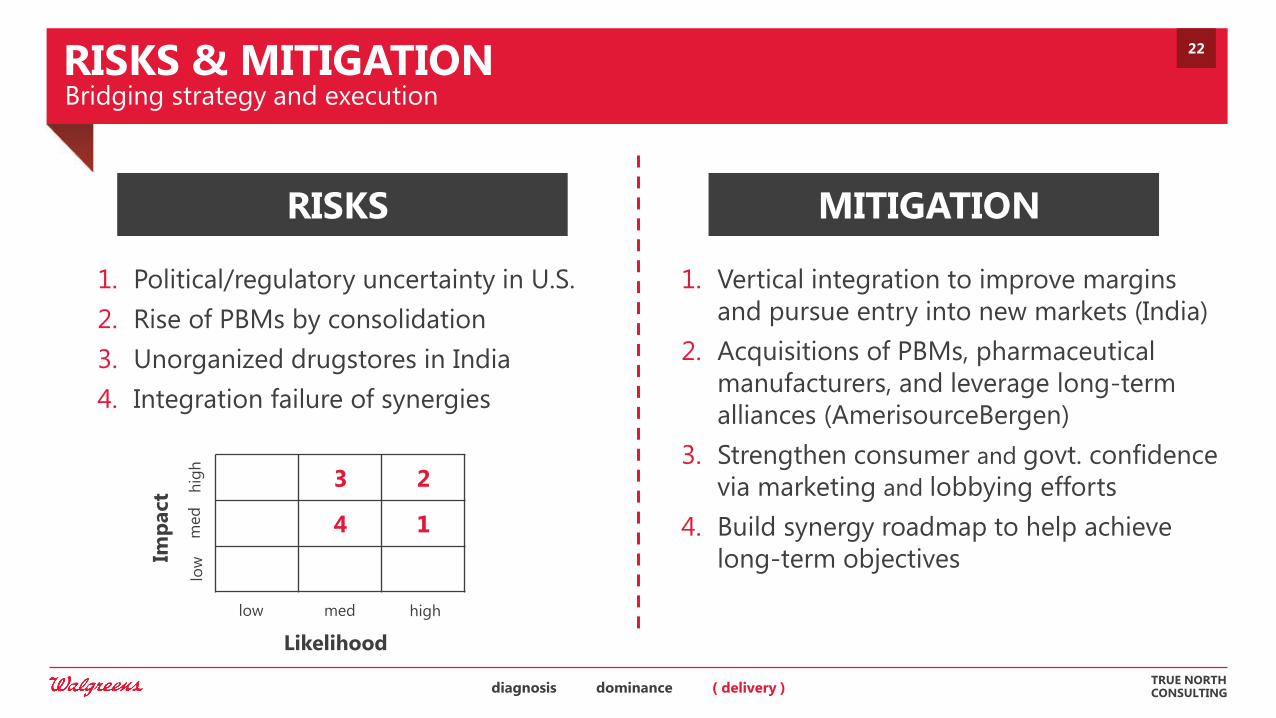

RISKS & MITIGATION Bridging strategy and execution

TRUE NORTH CONSULTING

RISKS MITIGATION

Likelihood

Imp

act

low

low

m

ed

h

igh

med high

3 2

4 1

1. Political/regulatory uncertainty in U.S.

2. Rise of PBMs by consolidation

3. Unorganized drugstores in India

4. Integration failure of synergies

1. Vertical integration to improve margins

and pursue entry into new markets (India)

2. Acquisitions of PBMs, pharmaceutical

manufacturers, and leverage long-term

alliances (AmerisourceBergen)

3. Strengthen consumer and govt. confidence

via marketing and lobbying efforts

4. Build synergy roadmap to help achieve

long-term objectives

22

diagnosis dominance ( delivery )

INDIA

BROWNFIELD

INVESTMENT

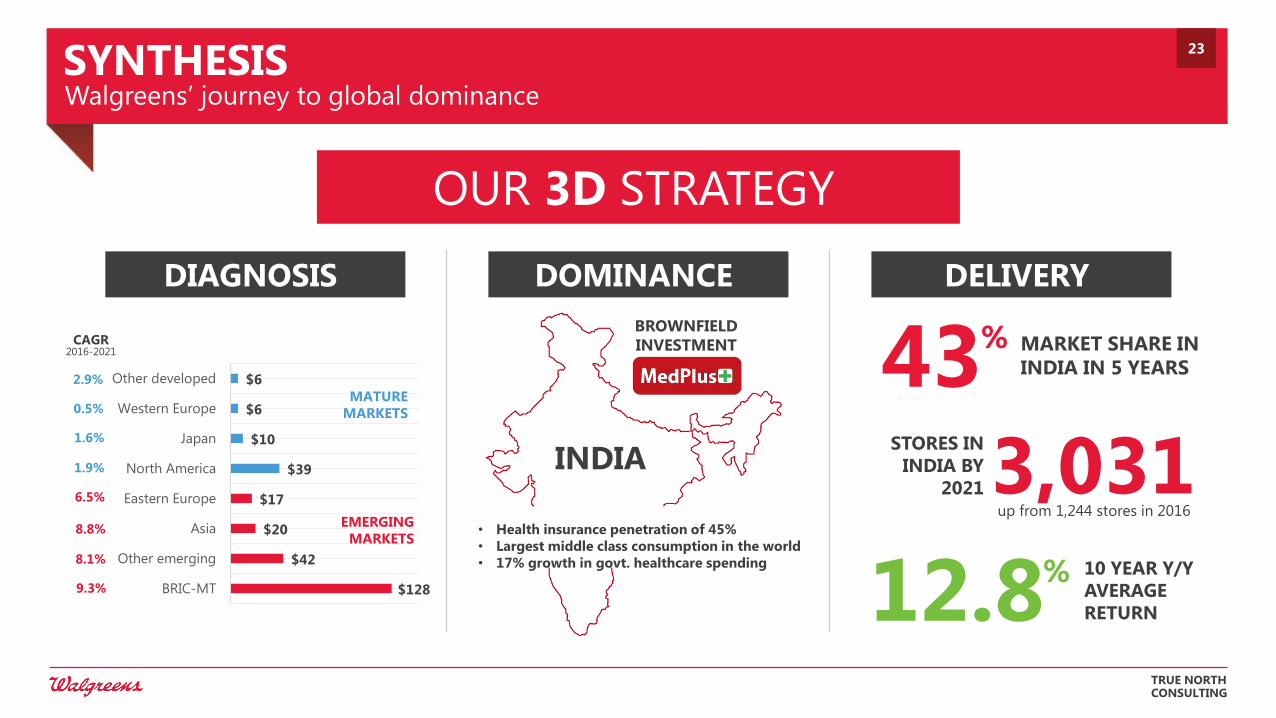

SYNTHESIS Walgreens’ journey to global dominance

TRUE NORTH CONSULTING

DIAGNOSIS DOMINANCE DELIVERY

OUR 3D STRATEGY

• Health insurance penetration of 45%

• Largest middle class consumption in the world

• 17% growth in govt. healthcare spending

$128

$42

$20

$17

$39

$10

$6

$6

BRIC-MT

Other emerging

Asia

Eastern Europe

North America

Japan

Western Europe

Other developed

MATURE

MARKETS

EMERGING

MARKETS

2.9%

0.5%

1.6%

1.9%

6.5%

8.8%

8.1%

9.3%

CAGR 2016-2021 43 % MARKET SHARE IN

INDIA IN 5 YEARS

3,031 STORES IN

INDIA BY

2021

12.8 % 10 YEAR Y/Y

AVERAGE

RETURN

23

up from 1,244 stores in 2016

TRUE NORTH CONSULTING

Team 1

April 23, 2016

Thank you for your time

Appendix 1

Market share

calculations

Appendix 2

Financial

forecast

Appendix 3

Consumer

demographics

Appendix 4

Alternative

regions

Appendix 5

Price conscious

consumers

Appendix 6

Industry cost

structure

Appendix 7

Health issues

in India

Appendix 8

Organizational

Values

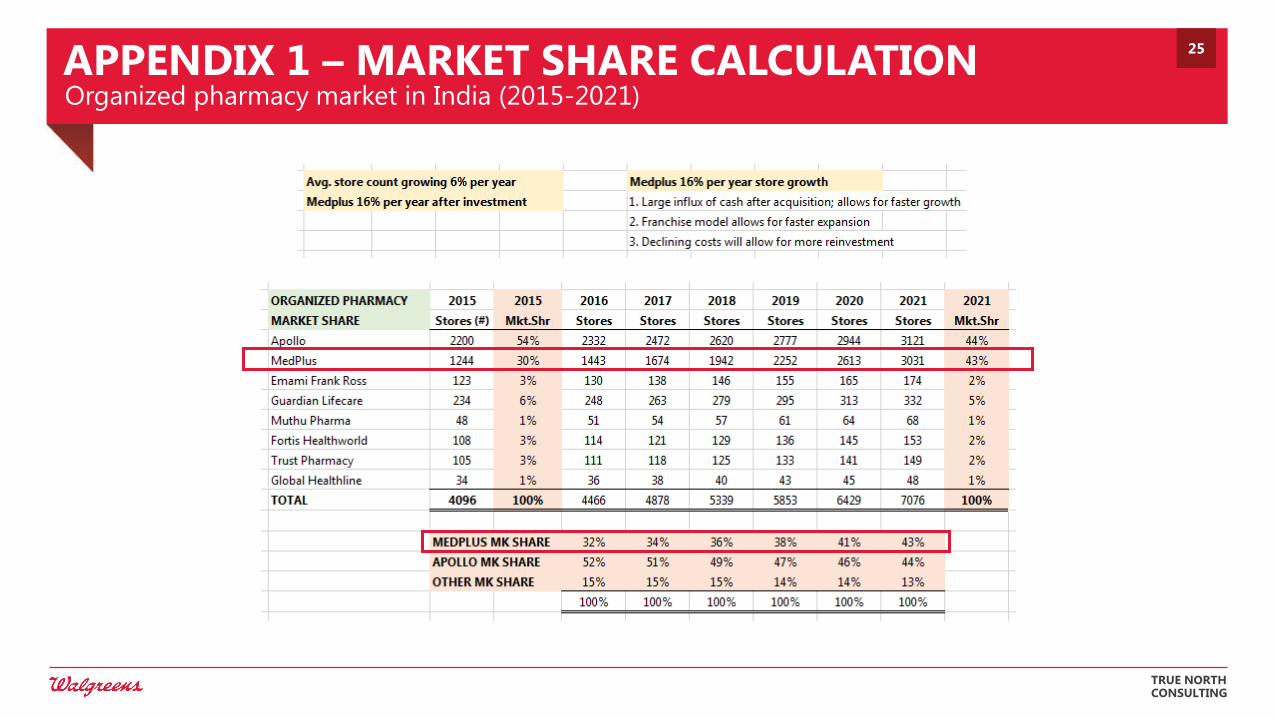

APPENDIX 1 – MARKET SHARE CALCULATION Organized pharmacy market in India (2015-2021)

TRUE NORTH CONSULTING

25

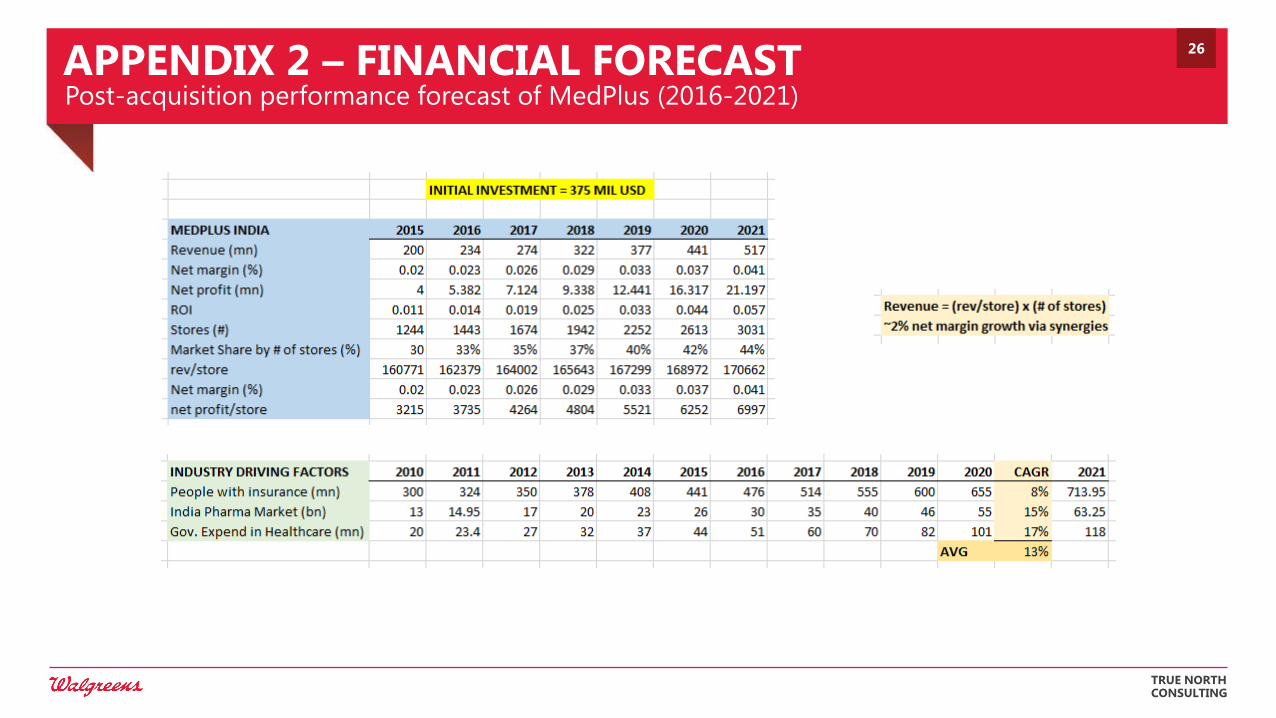

APPENDIX 2 – FINANCIAL FORECAST Post-acquisition performance forecast of MedPlus (2016-2021)

TRUE NORTH CONSULTING

26

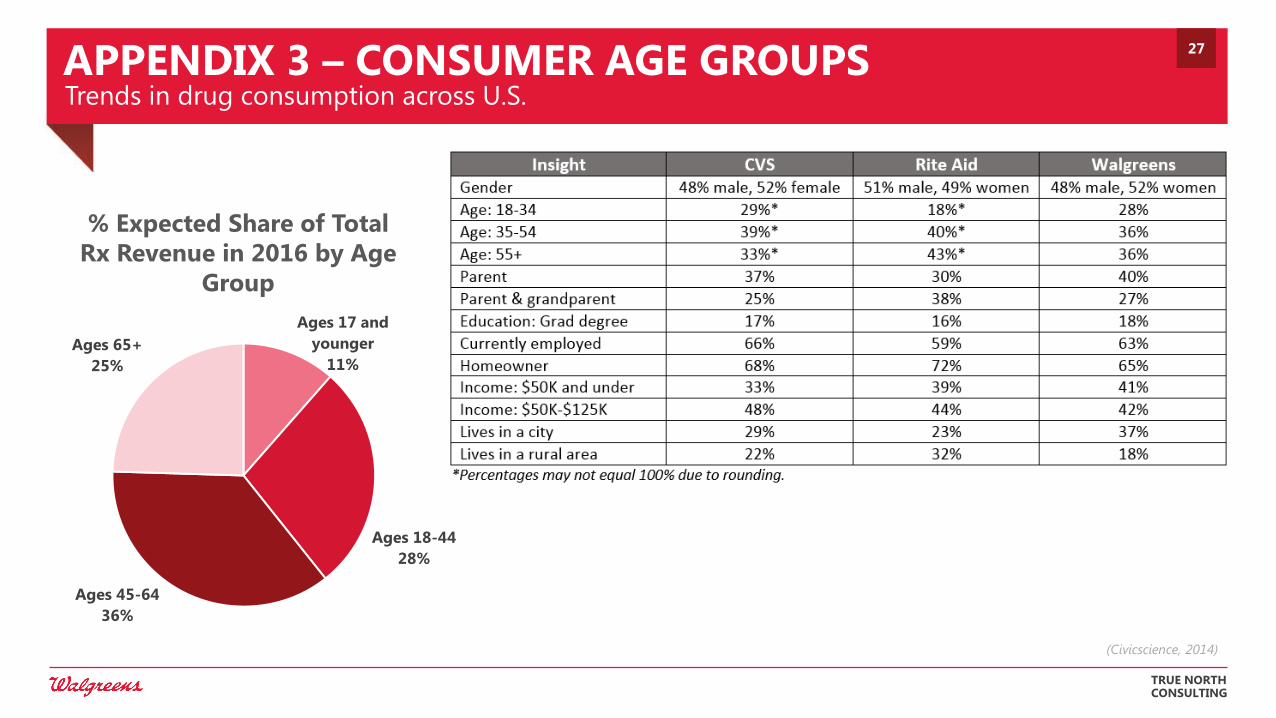

APPENDIX 3 – CONSUMER AGE GROUPS Trends in drug consumption across U.S.

TRUE NORTH CONSULTING

Ages 17 and

younger

11%

Ages 18-44

28%

Ages 45-64

36%

Ages 65+

25%

% Expected Share of Total

Rx Revenue in 2016 by Age

Group

(Civicscience, 2014)

27

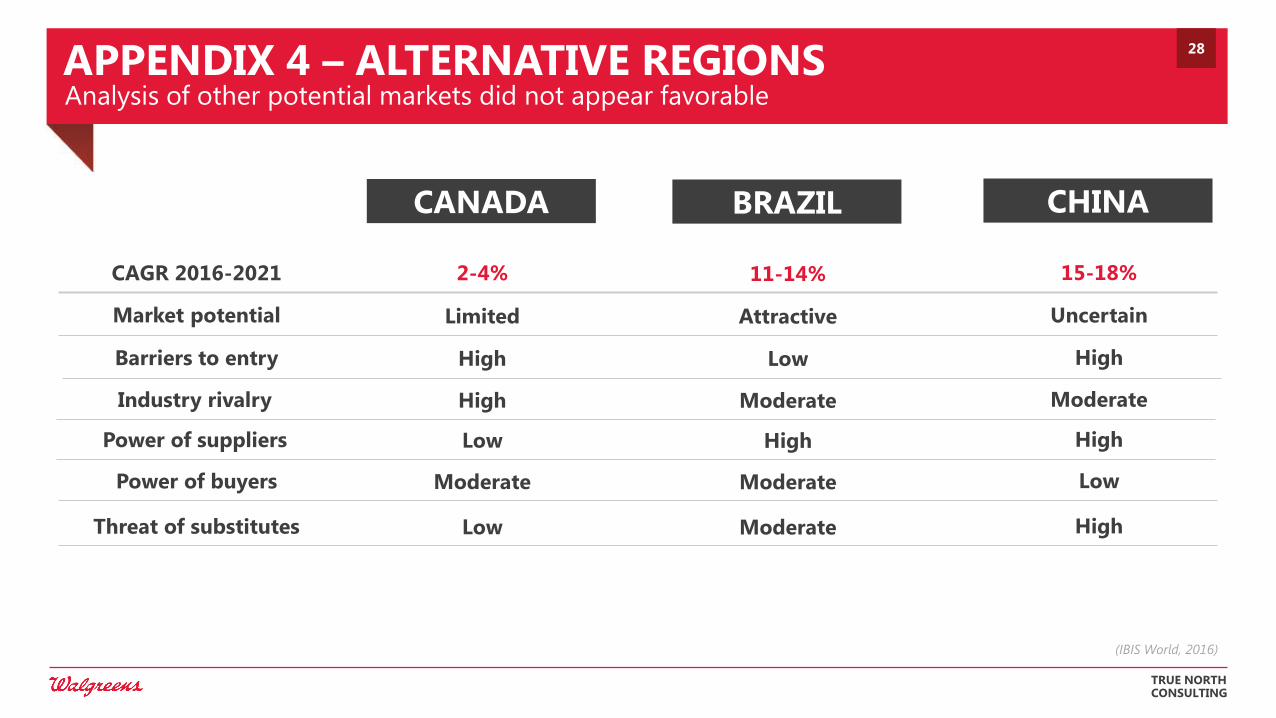

APPENDIX 4 – ALTERNATIVE REGIONS Analysis of other potential markets did not appear favorable

TRUE NORTH CONSULTING

CANADA BRAZIL CHINA

CAGR 2016-2021

Market potential

Barriers to entry

2-4% 11-14%

Limited

High

Industry rivalry High

Power of suppliers Low

Power of buyers Moderate

Attractive

Low

Moderate

High

Moderate

15-18%

Uncertain

High

Moderate

High

Low

Threat of substitutes Low Moderate High

(IBIS World, 2016)

28

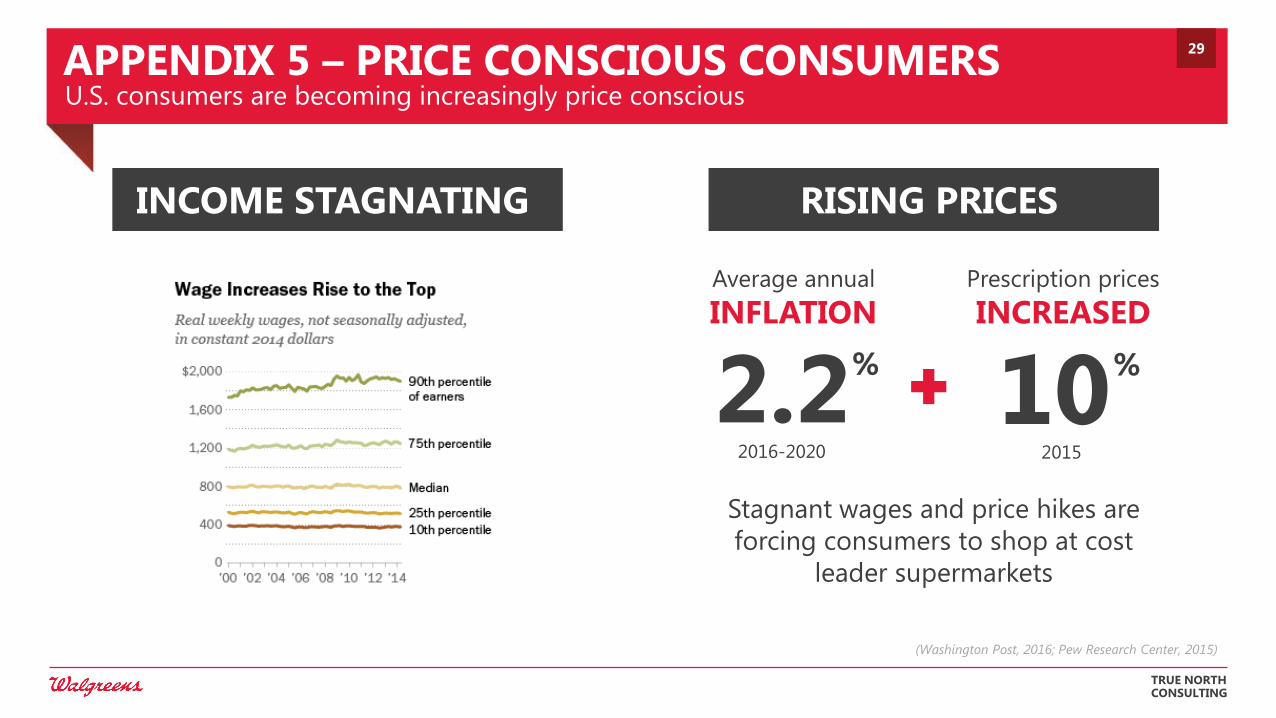

APPENDIX 5 – PRICE CONSCIOUS CONSUMERS

INCOME STAGNATING RISING PRICES

(Washington Post, 2016; Pew Research Center, 2015)

TRUE NORTH CONSULTING

Average annual

INFLATION

2.2 %

Prescription prices

INCREASED

10 %

U.S. consumers are becoming increasingly price conscious

Stagnant wages and price hikes are

forcing consumers to shop at cost

leader supermarkets

2016-2020 2015

29

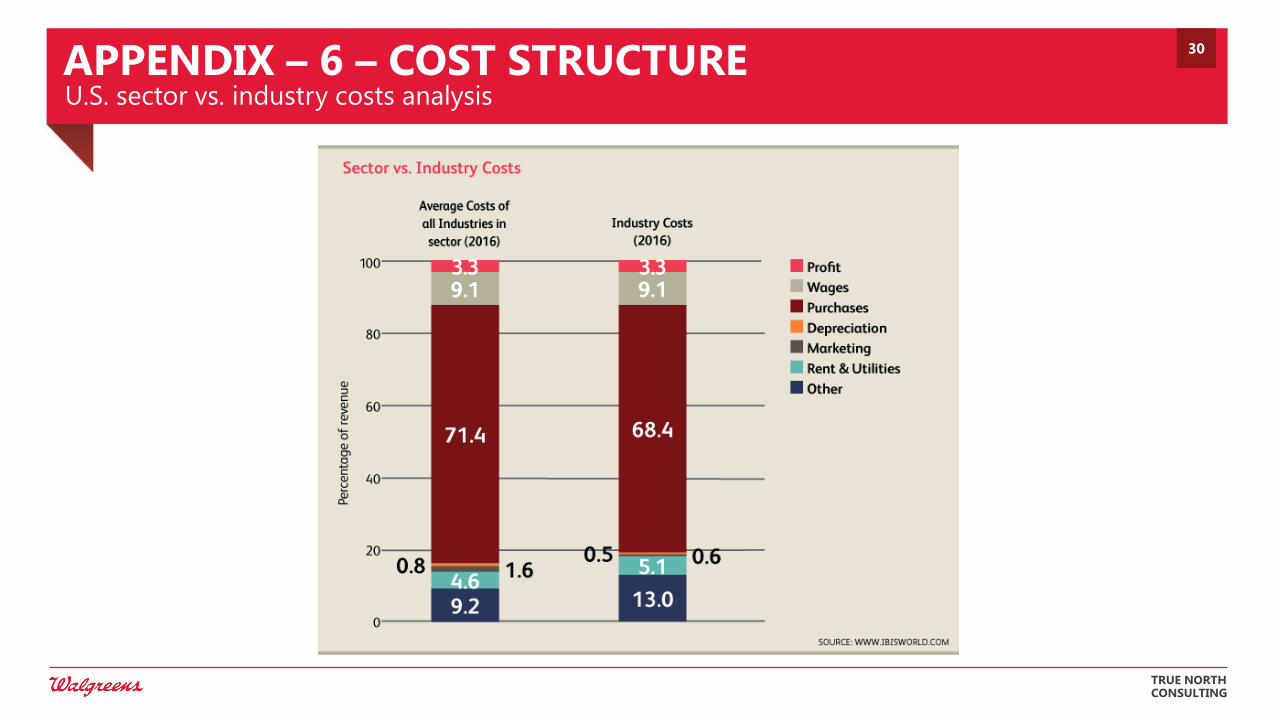

APPENDIX – 6 – COST STRUCTURE U.S. sector vs. industry costs analysis

TRUE NORTH CONSULTING

30

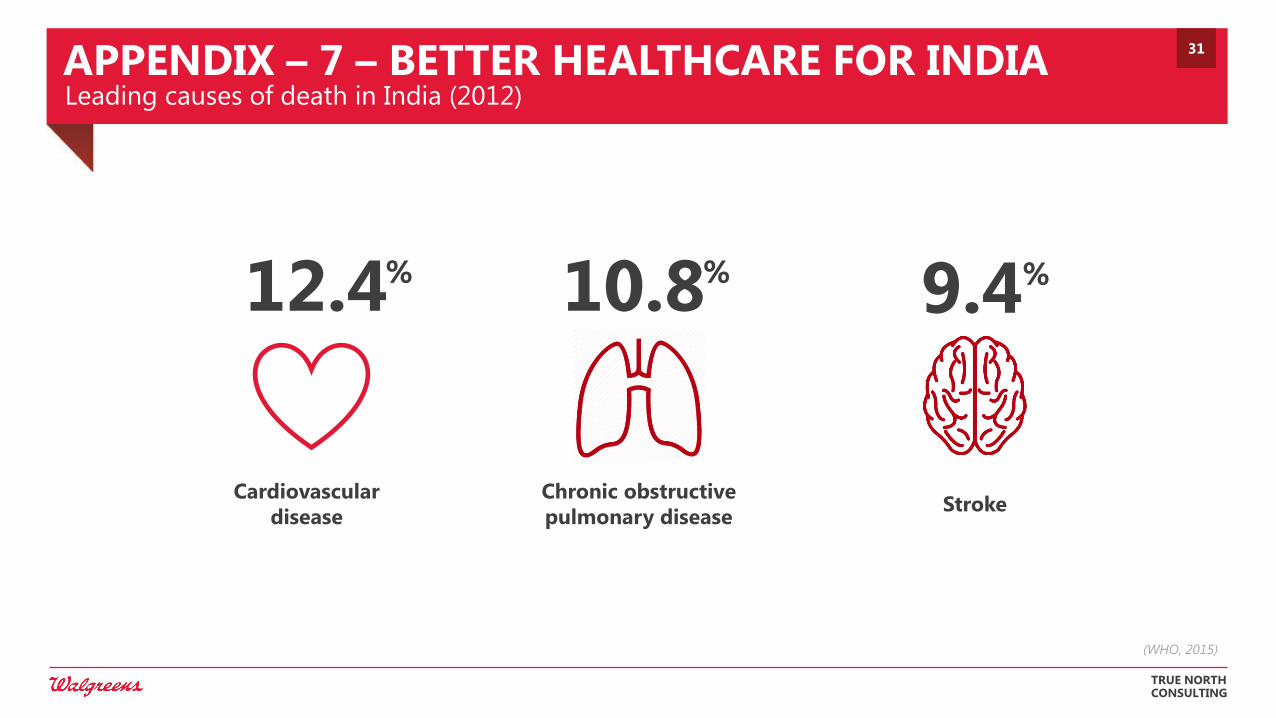

APPENDIX – 7 – BETTER HEALTHCARE FOR INDIA Leading causes of death in India (2012)

TRUE NORTH CONSULTING

(WHO, 2015)

Cardiovascular

disease

Chronic obstructive

pulmonary disease Stroke

12.4 % 10.8 % 9.4 %

31

APPENDIX – 8 – ORGANIZATIONAL VALUES Mission, vision and core values of Walgreens

TRUE NORTH CONSULTING

(Walgreens Corporate, 2016)

Our Mission To be America's most loved pharmacy-led health, wellbeing and beauty retailer.

Our Purpose To champion everyone’s right to be happy and healthy.

Our Values Based on the principles upon which Walgreens was founded more than a century ago:

Honesty, trust, and integrity with our customers, our shareholders, suppliers, the communities we serve, and among

ourselves.

Quality through consistent and reliable service, advice, and products across every touchpoint and channel.

Caring, compassionate and driven to delivering a great customer and patient experience through outstanding service

and a desire for healthy outcomes.

A strong community commitment and presence built through service, expertise, and the personal engagement of every

Walgreen team member.

32

REFERENCES Comprehensive list of source materials

TRUE NORTH CONSULTING

Apollo Hospitals. (2015). Annual Report 2015. Retrieved from Apollo Hospitals: https://www.apollohospitals.com/apollo_pdf/annual-report-year-2015.pdf

Ascher, J., Bogdan, B., Dreszer, J., & Zhou, G. (2015, July). Pharma's Next Challenge. Retrieved from McKinsey: http://www.mckinsey.com/industries/pharmaceuticals-and-medical-products/our-insights/pharmas-next-challenge

Civic Science, Inc. (2014, October). Insight Report: Researching the Personas of CVS, Rite Aid, and Walgreens Fans. Retrieved from Civic Science: https://civicscience.com/ourinsights/insightreports/insight-report-researching-the-personas-of-cvs-rite-aid-and-walgreens-fans/

CVS Health. (2015). Annual Report 2015. Retrieved from CVS Health: http://investors.cvshealth.com/financial-information/annual-report-archive

CVS Health. (2016, April). About. Retrieved from CVS Health: http://cvshealth.com/about

Euromonitor International. (2013, July). Opinion: Loblaws Cos and Shoppers Drug Mart.

Euromonitor International. (2015, May). Industry Overview: Beauty and Personal Care in Canada.

Euromonitor International. (2015, July). Industry Overview: Beauty and Personal Care in India.

Euromonitor International. (2015, May). Industry Overview: Beauty and Personal Care in the US.

Euromonitor International. (2015, December). Industry Overview: Consumer Health in Canada.

Euromonitor International. (2015, November). Industry Overview: Consumer Health in India.

Euromonitor International. (2015, December). Industry Overview: Consumer Health in the US.

IBISWorld. (2015, November). Beauty, Cosmetics & Fragrance Stores in the US.

IBISWorld. (2016, March). Beauty, Cosmetics & Fragrance Stores in Canada.

IBISWorld. (2016, March). Pharmacies & Drug Stores in Canada.

IBISWorld. (2016, April). Pharmacies & Drug Stores in the US.

India Brand Equity Foundation. (2016, February). Indian Pharmaceutical Industry. Retrieved from http://www.ibef.org/industry/pharmaceutical-india.aspx

Kharas, H. (2011, June). The Emerging Middle Class in Developing Countries. Retrieved from Brookings Institution: http://www.brookings.edu/

Mattioli, D., Siconolfi, M., & Cimilluca, D. (2015, October). Walgreens, Rite Aid Unite to Create Drugstore Giant. Retrieved from Wall Street Journal: http://www.wsj.com/articles/walgreens-boots-alliance-nears-deal-to-buy-rite-aid-1445964090

McKinsey & Company. (2007). India Pharma 2020. Retrieved from McKinsey: http://www.mckinsey.com/global-locations/asia/india/en/latest-thinking

McKinsey & Company. (2012). Unlocking Pharma Growth. Retrieved from McKinsey: http://www.mckinsey.com/

Meyer, A. (2013, March). Walgreens Broadens its Horizons. Retrieved from Retail Leader: http://www.retailleader.com/article-walgreens_broadens_its_horizons-5708-part1.html

PwC (Strategy&). (2013). Pharma Emerging Markets 2.0. Retrieved from PwC: http://www.strategyand.pwc.com/media/file/Strategyand_Pharma-Emerging-Markets-2.0.pdf

PwC. (2007). Pharma 2020: The Vision. Retrieved from PwC: http://www.pwc.com/gx/en/pharma-life-sciences/pdf/pharma2020final.pdf

Reingold, J., & Jones, M. (2016, February 1). The Billionaire Behind Walgreens' Quest for Global Dominance. Retrieved from Fortune: http://fortune.com/walgreens-greg-wasson-stefano-pessina/

Sachdev, A. (2015, August). Walgreens Strives for Cost-Effective In-Store Clinics in Partnership. Retrieved from Chicago Tribune: http://www.chicagotribune.com/business/ct-walgreens-health-clinic-0821-biz-20150820-story.html

Walgreens. (2016, April). http://www.walgreens.com/topic/about/company.jsp. Retrieved from Walgreens: http://www.walgreens.com/topic/about/company.jsp

Walgreens Boots Alliance, Inc. (2015). Annual Report 2015. Retrieved from Walgreens Boots Alliance: http://investor.walgreensbootsalliance.com/annuals-proxies.cfm

33