Embed Size (px)

Citation preview

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 1/19

Investment Analysis Group

November 9, 2010

Eric Ward

Introduction to Value Investing

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 2/19

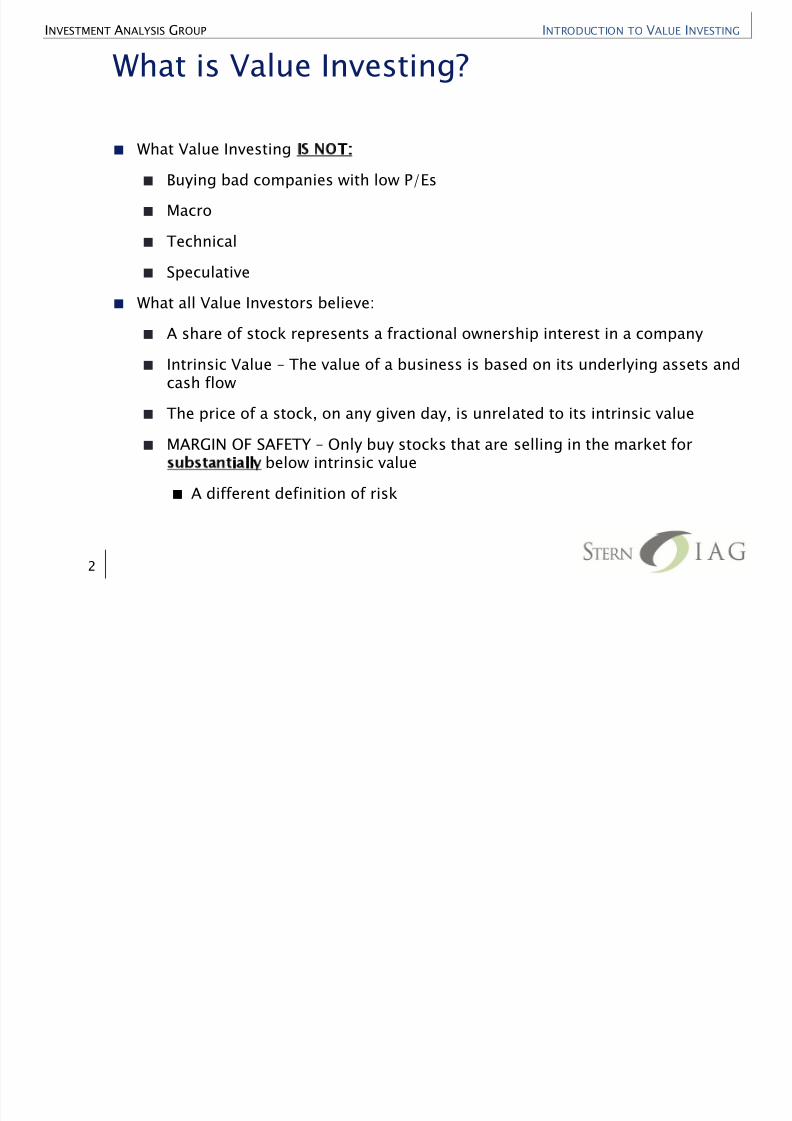

What is Value Investing?

What Value Investing IS NOT:

Buying bad companies with low P/Es

Macro

Technical

Speculative

What all Value Investors believe:

A share of stock represents a fractional ownership interest in a company

Intrinsic Value The value of a business is based on its underlying assets andcash flow

The price of a stock, on any given day, is unrelated to its intrinsic value

MARGIN OF SAFETY Only buy stocks that are selling in the market forsubstantially below intrinsic value

A different definition of risk

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

2

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 3/19

What is Value Investing?

Areas where Value Investors differ:

Selecting securities for valuation

Estimating fundamental values

Quality of business

Required Margin of Safety

Portfolio concentration

When to sell

How to research

Beware value pretenders

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

3

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 4/19

Does it Work?

Other prominent value investors include:

Joel Greenblat Gotham Partners

Seth Klarman - Baupost

Whitney Tilson T2 Partners

Bill Ackman Pershing Square

David Einhorn Greenlight Capital

Martin Whitman Third Avenue Fund

Dan Loeb - ThirdPoint

Chris Brown Tweedy, Brown

Bruce Greenwald - FirstEagle

Howard Marks Oaktree Capital

Andreas Halvorsen Viking Global

David Greenspan & John Griffin Blueridge Capital

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Ask Warren Buffet Doddsville

4

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 5/19

Searching for Value?

Traditional Longs

Businesses with competitiveadvantages

High returns on capital

Owner-oriented management

Old, predictable industries

Contrarian

Cheap, dirty, ugly

Traditional Shorts

Structural business issues

Over-earning

Impossible expectations

Fraud / Bad accounting

Over-levered

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Special Situations

Mergers

Tender offers

Spinoffs

Buybacks

Distress / Turnarounds

Bankruptcy

Thrift conversions

Complex securities

5

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 6/19

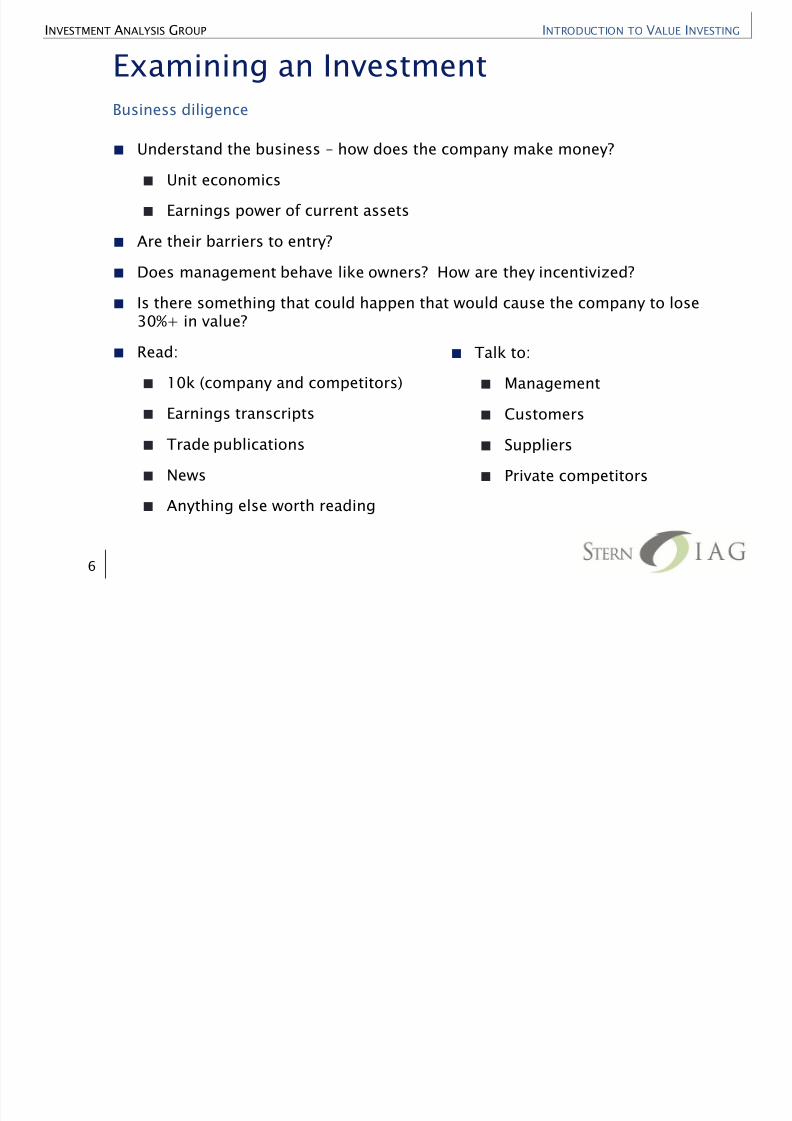

Examining an Investment

Understand the business how does the company make money?

Unit economics

Earnings power of current assets

Are their barriers to entry?

Does management behave like owners? How are they incentivized?

Is there something that could happen that would cause the company to lose30%+ in value?

Read:

10k (company and competitors)

Earnings transcripts

Trade publications

News

Anything else worth reading

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Business diligence

Talk to:

Management

Customers

Suppliers

Private competitors

6

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 7/19

Is it a good business or a bad business?

Does the company have a competitive advantage?

Economies of scale

Network effects

Customer captivity

Captive resource technology, resources, learning curve

Government regulation

The first two advantages are by far the strongest, and they are most compellingwhen found together

Indicators of the existence of a competitive advantage:

Long-term market share stability

Consistent above average returns on invested capital

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Only companies with a competitive advantage can earn above their cost of capital

7

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 8/19

Uncovering Intrinsic Value

How much would it cost to recreate the assets of the business today?

Adjust balance sheet to current values

Earnings Power What cash flows can the company generate with current assets

Look at steady state economics

Earnings = Normalized EBITDA Taxes - Capex

Is there franchise value? Only if barriers to entry exist

If not, growth adds no value

Is there hidden asset value?

Other indicators of value

Stock valuation publicly traded minority interests

Private market transactions

Liquidation values

Asset appraisals

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

8

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 9/19

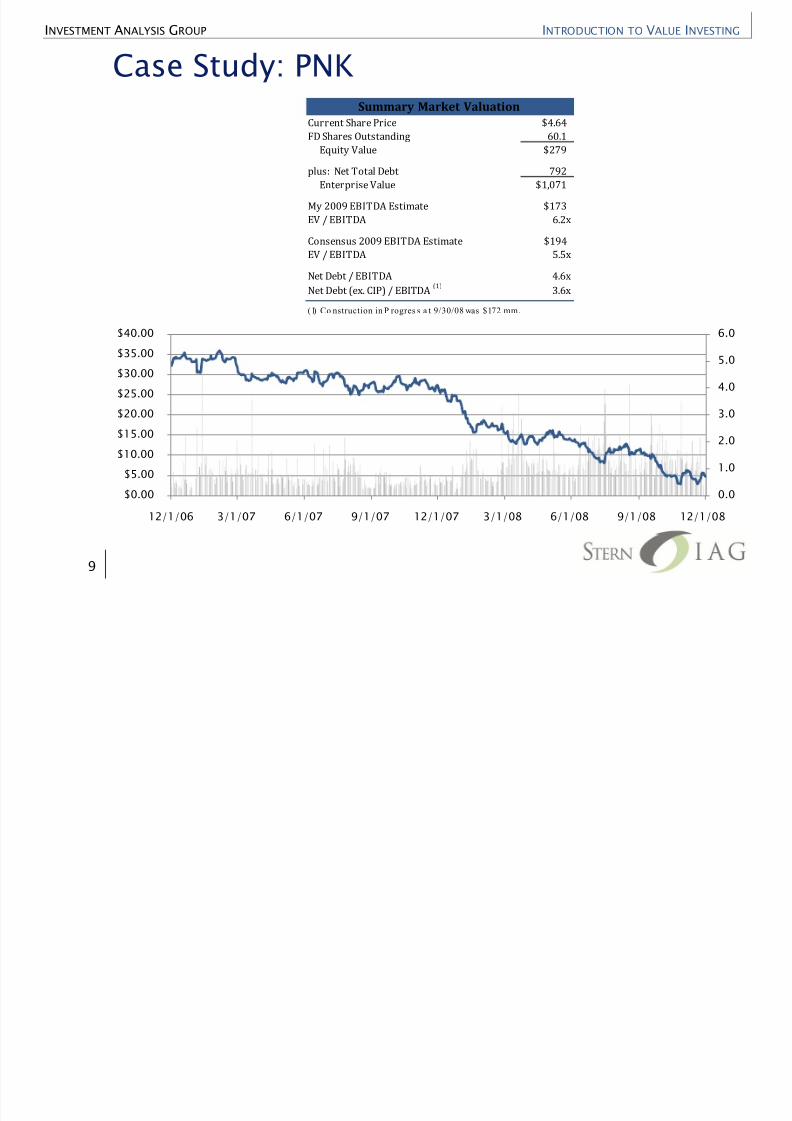

Case Study: PNK

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

12/1/06 3/1/07 6/1/07 9/1/07 12/1/07 3/1/08 6/1/08 9/1/08 12/1/08

Summary Market Valuation

Current Share Price $4.64

FD Shares Outstanding 60.1Equity Value $279

plus: Net Total Debt 792

Enterprise Value $1,071

My 2009 EBITDA Estimate $173

EV / EBITDA 6.2x

Consensus 2009 EBITDA Estimate $194

EV / EBITDA 5.5x

Net Debt / EBITDA 4.6xNet Debt (ex. CIP) / EBITDA

(1)3.6x

(1) Co nstruction in P rogres s a t 9/30/08 was $172 mm.

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 10/19

Case Study: PNK

PNK owns and operates casino hotels in regional gaming markets includingLouisiana, Indiana, Missouri and Mississippi

In 2008 casino valuations decline 70 90% due to:

Declining operating fundamentals

Leverage / financing concerns

Burst of the gaming M&A asset bubble

PNK experiencing revenue and margin compression

4.6x levered; debt maturities coming due in next 18 months

Potential for covenant violations

Ability to finance growth projects in doubt

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

10

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 11/19

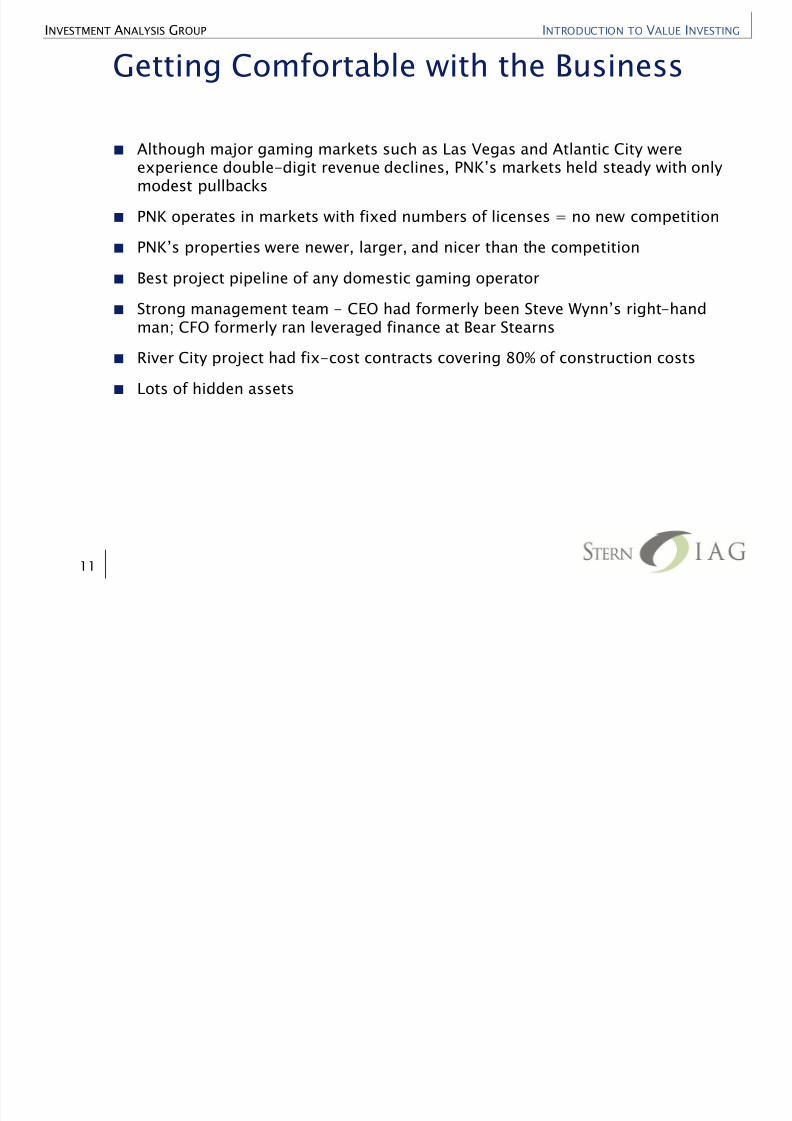

Getting Comfortable with the Business

Although major gaming markets such as Las Vegas and Atlantic City wereexperience double-modest pullbacks

PNK operates in markets with fixed numbers of licenses = no new competition

Best project pipeline of any domestic gaming operator

Strong management team - -handman; CFO formerly ran leveraged finance at Bear Stearns

River City project had fix-cost contracts covering 80% of construction costs

Lots of hidden assets

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

11

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 12/19

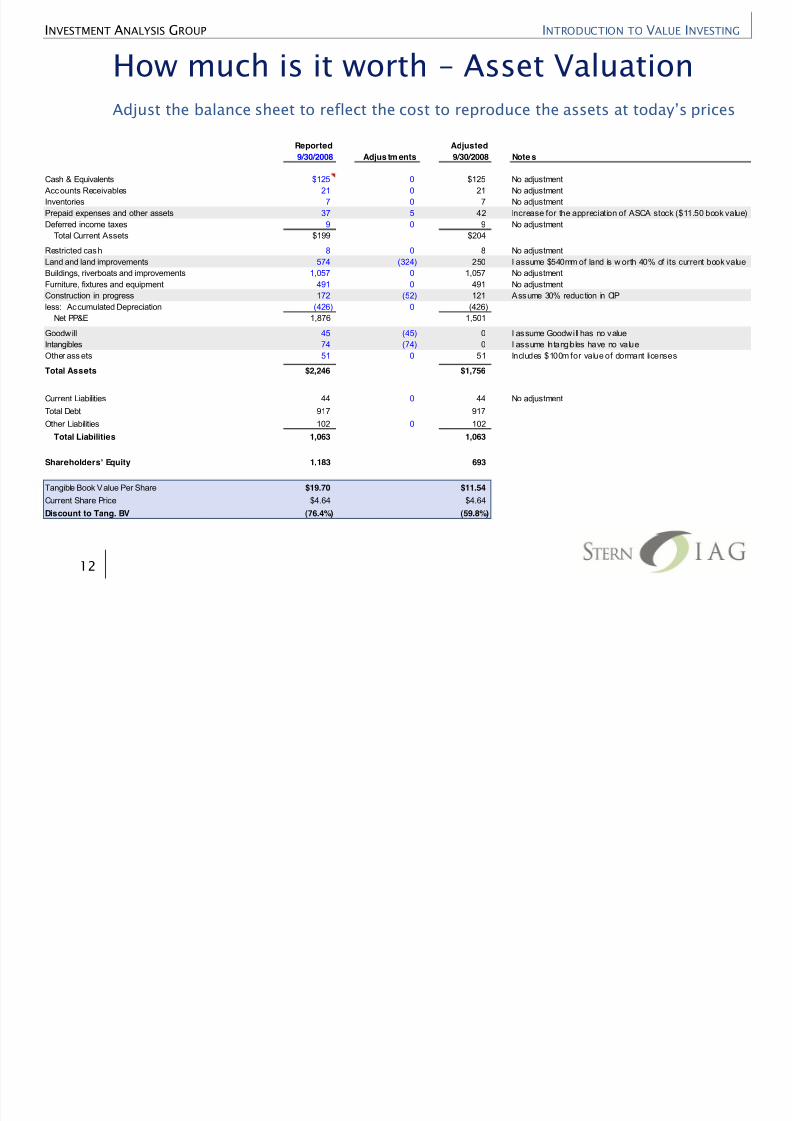

How much is it worth Asset Valuation

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

12

Reported Adjusted

9/30/2008 Adjus tm ents 9/30/2008 Note s

Cash & Equivalents $125 0 $125 No adjustment

Accounts Receivables 21 0 21 No adjustment

Inventories 7 0 7 No adjustment

Prepaid expenses and other assets 37 5 42 Increase for the appreciation of ASCA stock ($11.50 book value)

Deferred income taxes 9 0 9 No adjustment

Total Current Assets $199 $204

Restricted cash 8 0 8 No adjustment

Land and land improvements 574 (324) 250 I assume $540mm of land is w orth 40% of its current book value

Buildings, riverboats and improvements 1,057 0 1,057 No adjustmentFurniture, fixtures and equipment 491 0 491 No adjustment

Construction in progress 172 (52) 121 Assume 30% reduction in CIP

less: Accumulated Depreciation (426) 0 (426)

Net PP&E 1,876 1,501

Goodwill 45 (45) 0 I assume Goodwi ll has no value

Intangibles 74 (74) 0 I assume Intangibles have no value

Other ass ets 51 0 51 Includes $100m for value of dormant licenses

Total Assets $2,246 $1,756

Current Liabilities 44 0 44 No adjustment

Total Debt 917 917Other Liabilities 102 0 102

Total Liabilities 1,063 1,063

Shareholders' Equity 1,183 693

Tangible Book Value Per Share $19.70 $11.54

Current Share Price $4.64 $4.64

Discount to Tang. BV (76.4%) (59.8%)

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 13/19

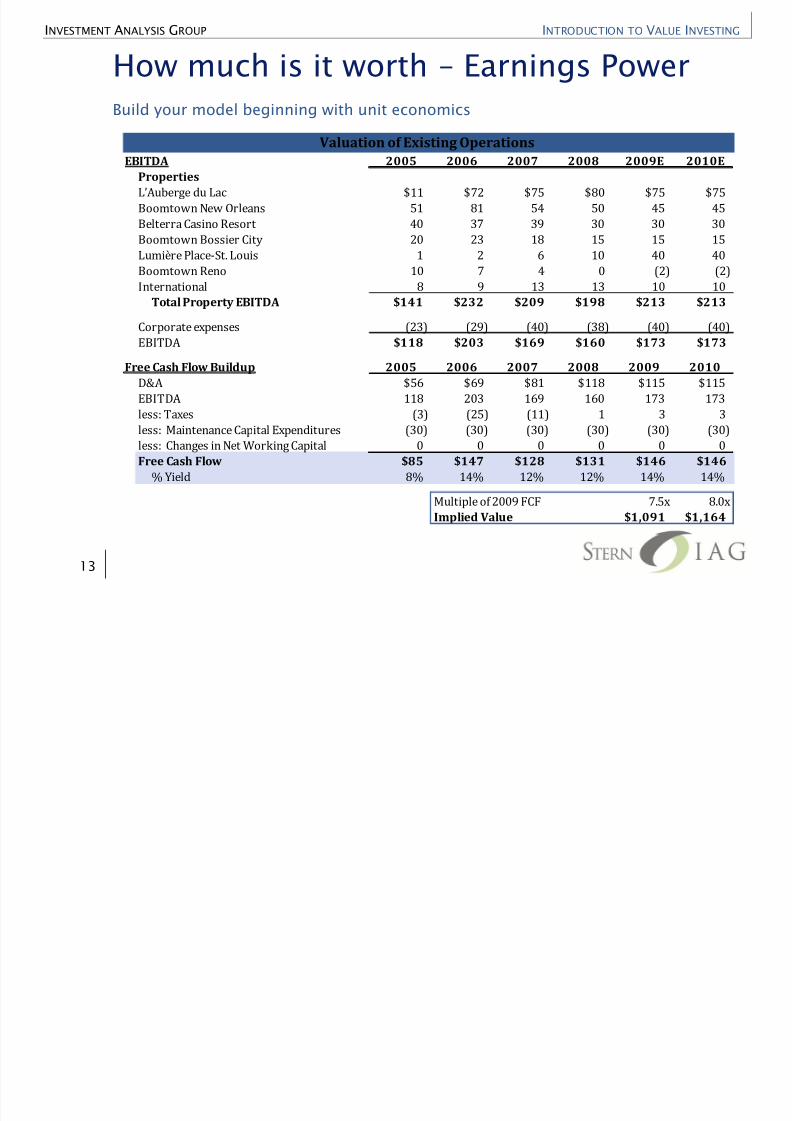

How much is it worth Earnings Power

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Build your model beginning with unit economics

13

Valuation of Existing OperationsEBITDA 2005 2006 2007 2008 2009E 2010E

Properties

$11 $72 $75 $80 $75 $75

Boomtown New Orleans 51 81 54 50 45 45

Belterra Casino Resort 40 37 39 30 30 30

Boomtown Bossier City 20 23 18 15 15 15

Lumière Place-St. Louis 1 2 6 10 40 40

Boomtown Reno 10 7 4 0 (2) (2)

International 8 9 13 13 10 10

Total Property EBITDA $141 $232 $209 $198 $213 $213

Corporate expenses (23) (29) (40) (38) (40) (40)

EBITDA $118 $203 $169 $160 $173 $173

Free Cash Flow Buildup 2005 2006 2007 2008 2009 2010

D&A $56 $69 $81 $118 $115 $115

EBITDA 118 203 169 160 173 173

less: Taxes (3) (25) (11) 1 3 3less: Maintenance Capital Expenditures (30) (30) (30) (30) (30) (30)

less: Changes in Net Working Capital 0 0 0 0 0 0

Free Cash Flow $85 $147 $128 $131 $146 $146

% Yield 8% 14% 12% 12% 14% 14%

Multiple of 2009 FCF 7.5x 8.0x

Implied Value $1,091 $1,164

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 14/19

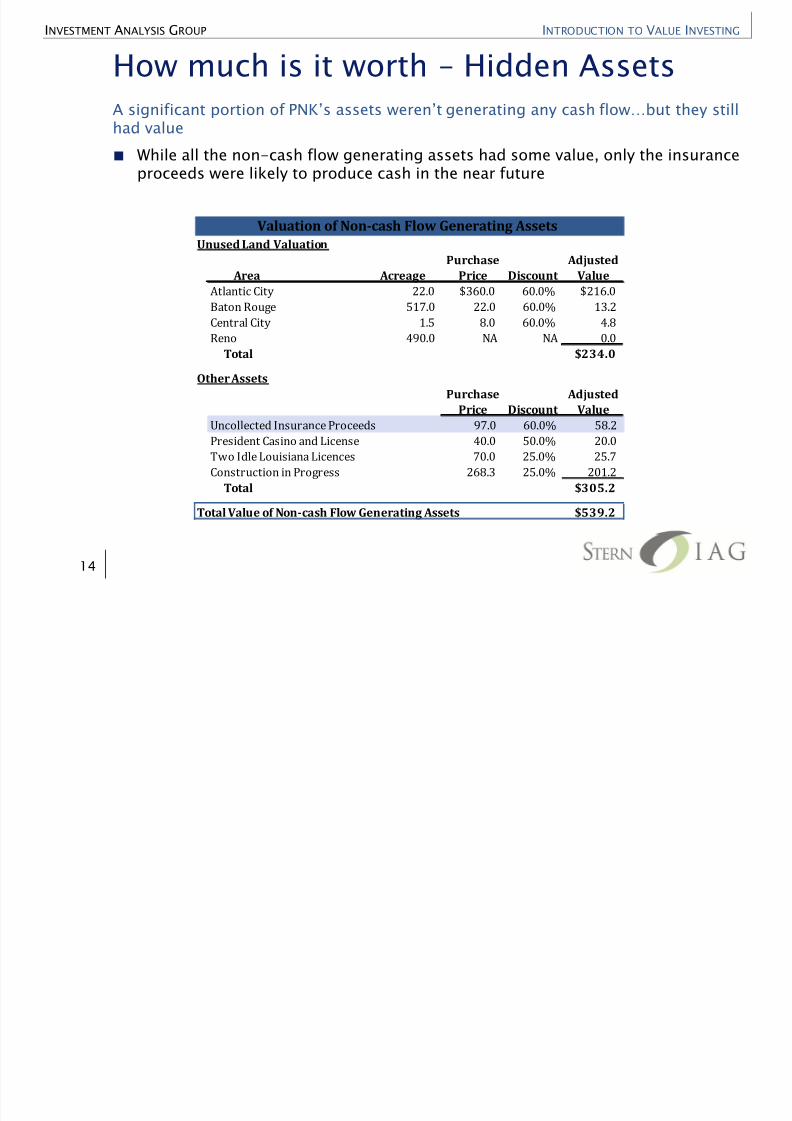

How much is it worth Hidden Assets

While all the non-cash flow generating assets had some value, only the insuranceproceeds were likely to produce cash in the near future

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

had value

14

Valuation of Non-cash Flow Generating Assets

Unused Land Valuation

Purchase Adjusted

Area Acreage Price Discount ValueAtlantic City 22.0 $360.0 60.0% $216.0

Baton Rouge 517.0 22.0 60.0% 13.2

Central City 1.5 8.0 60.0% 4.8

Reno 490.0 NA NA 0.0

Total $234.0

Other Assets

Purchase Adjusted

Price Discount ValueUncollected Insurance Proceeds 97.0 60.0% 58.2

President Casino and License 40.0 50.0% 20.0

Two Idle Louisiana Licences 70.0 25.0% 25.7

Construction in Progress 268.3 25.0% 201.2

Total $305.2

Total Value of Non-cash Flow Generating Assets $539.2

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 15/19

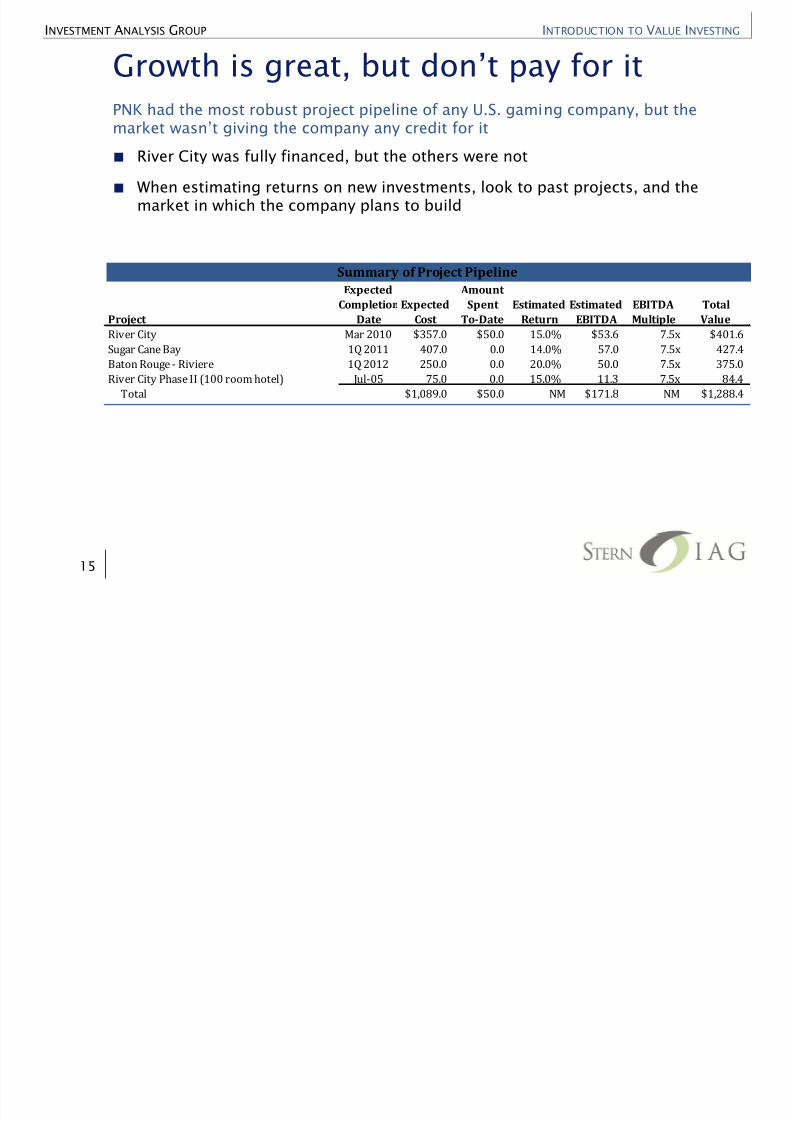

River City was fully financed, but the others were not

When estimating returns on new investments, look to past projects, and themarket in which the company plans to build

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

PNK had the most robust project pipeline of any U.S. gaming company, but the

15

Summary of Project PipelineExpected Amount

Completio Expected Spent Estimated Estimated EBITDA Total

Project Date Cost To-Date Return EBITDA Multiple Value

River City Mar 2010 $357.0 $50.0 15.0% $53.6 7.5x $401.6

Sugar Cane Bay 1Q 2011 407.0 0.0 14.0% 57.0 7.5x 427.4

Baton Rouge - Riviere 1Q 2012 250.0 0.0 20.0% 50.0 7.5x 375.0

River City Phase II (100 room hotel) Jul-05 75.0 0.0 15.0% 11.3 7.5x 84.4

Total $1,089.0 $50.0 NM $171.8 NM $1,288.4

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 16/19

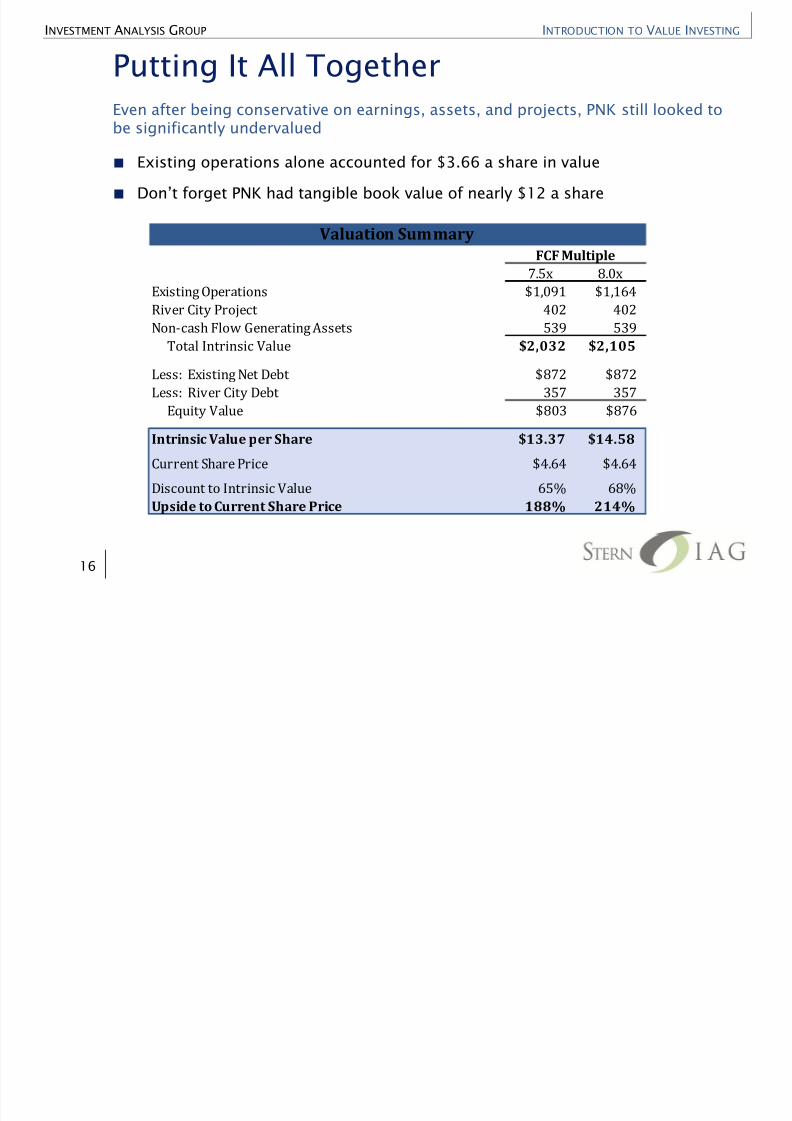

Putting It All Together

Existing operations alone accounted for $3.66 a share in value

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Even after being conservative on earnings, assets, and projects, PNK still looked tobe significantly undervalued

16

Valuation Summary

FCF Multiple

7.5x 8.0xExisting Operations $1,091 $1,164

River City Project 402 402

Non-cash Flow Generating Assets 539 539

Total Intrinsic Value $2,032 $2,105

Less: Existing Net Debt $872 $872

Less: River City Debt 357 357

Equity Value $803 $876Intrinsic Value per Share $13.37 $14.58

Current Share Price $4.64 $4.64

Discount to Intrinsic Value 65% 68%

Upside to Current Share Price 188% 214%

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 17/19

Additional Thoughts

Know not only if something is undervalued, but why it is

-economic rationale driving other investors decisions

Understand the risk / reward of your investments only take bets where it skewsheavily in your favor (e.g. 5:1)

seek to know as muchas you can about the issues that matter most

Develop a circle of competence

Catalysts are nice, but you can buy stocks without them for less

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

17

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 18/19

Conclusion

Philosophy

Refine your philosophy with each investment you examine

What characteristics do you like/dislike. What gives you comfort?

What is my time frame?

How much Margin of Safety do I need to sleep at night?

Process

Fish where the fish live

Be systematic keep a record of what you look at and why to play or pass

Develop mental models to frame economic behavior and investing situations

Read everything

Hone your investigative research skills

Be humble know the extent of your knowledge

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

Successful investing requires the right philosophy and process

18

8/3/2019 Ward Value Investing

http://slidepdf.com/reader/full/ward-value-investing 19/19

Additional Resources

Books: See handout

Value Investors Club (www.valueinvestorsclub.com)

Cultivate mentors and build friendships

INTRODUCTION TO VALUE INVESTINGINVESTMENT ANALYSIS GROUP

19