Embed Size (px)

Citation preview

Prepared:In collaboration between Welch LLP Chartered Professional Accountants and MaRS Discovery District

www.welchllp.com

General outline of tasks and activities to assist you with the accounting, financial and tax related issues that must be considered at the outset of your new venture

G U I D E

Seller's GuideWelchGroup Presents:

Prepared by

WelchGroupConsultingwww.w-group.com

Stephan May, MBA

Managing Director

Candace Enman, CPA, CA

President

www.w-group.com

2

Ottawa, ON | Toronto, ON 613.236.9191 | 647.288.9200 [email protected]

Sell-Side ProcessThe following steps outline the M&A process in order to give you an overview of expectations you may have in the upcoming months.

1. Engagement

At this point, you have most likely signed an engagement letter which outlines the terms and conditions of our journey together. This letter will act as a guideline in your businesses’ sell-side pro-cess, and it provides an overview of the services we will provide.

2. Kick-Off Meeting

The WelchGroup Kick-Off Meeting is the first official meeting that we will have with you (the business owner) and the Welch-Group. At this time, we will introduce our team and we will explain the functioning of the M&A process.

Before the meeting, we will provide you with an agenda which will include key discussion items. If there are additional discussion topics you wish to discuss, you are welcome to add them onto the meeting agenda. Then, once we finally sit down to discuss, you get the chance to ask as many questions as need be. Once the meet-ing is over, our next steps and processes will be clear to you.

3. Information Gathering + Invitation to Firmex

After the kick-off meeting, you must provide relevant information about your business that will enable us to sell it. WelchGroup will send you with a “Due Diligence Checklist” that will explain what information you must provide. This information will then be used to create a Confidential Information Memorandum (PitchBook) which will be viewed by future target prospects.

Rather than sending all this information to us through e-mail, you will be granted access to WelchGroup’s “Firmex” – a Virtual Data Room where you can upload documents. A data room is a physical or virtual space where one party can disclose confidential information in a controlled manner to a number of other interested parties. This secured account ensures that your information is kept safe and private. We will use Firmex to sort and organize documents from which we will draw content for the CIM (PitchBook).

4. Valuation

How much is your business really worth? Determining the enter-prise value of the business can be as much an art as science. The value of a business is based on its ability to generate future cash flows and the risk attached to achieving those cash flows. Similar to real estate, the building material, interior fixtures, and land de-termine the underlying asset value. However, the value can also be influenced by intangible characteristics, such as the location, market conditions, etc. A business follows these same principals. A buyer will pay a premium for the intangible value, but it is up to the seller to highlight those attributes. Continuing with the real estate metaphor, selling a business is like selling your home, it is important to stage it and highlight the features to potential buyers.

Based on information and financial statements you will provide us about your business, we will assess your company’s value through the use of appropriate valuation techniques. Some of these techniques are discussed below for your better under-standing of our methodologies.

Determine the Value of Your Business There are many ways to determine the value of your business; however, the two most common ways are the following:

Earning-Based Approach Cost/Asset-Based Approach

The business is valued on a multiple of historical and future earnings

The business is valued on its assets

Regardless of the method you use, the Buyer’s willingness to pay a premium will largely depend on their profile. Buyers typically fall into one of two groups:

• Financial buyers: These buyers are seeking cash flow and strong financial returns

• Strategic buyers: These buyers are more interested in syner-gies, and how the business works with their long term goals

S E L L E R ' S G U I D E

www.w-group.com

3

Guide: Selling

Calculation

EBITA = Earnings before Interest, Taxes, Depreciation, and Amortization

This example illustrates Company XYZ is generating $29,750 as a net income. However, the interest, tax, depreciation, and amor-tization must be added back to the net income. This means that the company's earning potential is actually $200,000. It is with this number that one should base the valuation multiple.

Select a Valuation Multiple

There are many factors to consider when determining your company’s valuation multiple. Most importantly, you must consider the predictability and stability of cash flows. We determined that Company XYZ generated $200,000 in EBITDA. However, if the EBITDA in the previous year the was $125,000, and in the year before that it was $250,000, this would signal to the prospective Buyer that the cash flows are unpredictable, and therefore, the prospective Buyer may be inclined to offer a lower multiple. In addition to predictability, each prospective buyer will have their own required return. For a strategic buyer, they may be okay with a payback over four years and generating an 8% return, while a financial buyer may expect a greater return as demonstrated in the table below.

Buyer's Investment

Cash Flow: Year 1

Cash Flow: Year 2

Cash Flow: Year 3

Cash Flow: Year 4

Cash Flow: Year 5

Rate of Return

4x EBITA (800,000) 200,000 200,000 200,000 200,000 200,000 8%

3x EBITA (600,000) 200,000 200,000 200,000 200,000 200,000 20%

2x EBITA (400,000) 200,000 200,000 200,000 200,000 200,000 41%

Another term commonly used is Normalized EBITDA. This is the processes of adding back discretionary spending. It is not uncommon for small business owners to mix personal and business expenses. For example, cars, wife/husband on pay roll, season tickets, member-ships, etc. If expenses are not related to the business, these expenses should be added back to the Net Income. Often, business owners will aggressively categorize capital expenses as repairs in order to minimize taxes. While this practice may reduce annual taxes, it will hurt the valuation when the business is sold by reducing historical EBITDA. Below is a list of other EBITDA adjustments:

1. Non-Arms-Length Revenue or Expenses

2. Revenue or Expenses Generated by Redundant Assets

3. One Time Professional Fees

4. Repairs and Maintenance

5. Inventories

6. Owner Salaries and Bonuses

7. Rent of Facilities at Prices Above or Below Fair Market Value

8. Lawsuits

9. Other Income and Expenses

Maximize the value of your Business

W E LC H G R O U P C O N S U LT I N G

www.w-group.com

4

Ottawa, ON | Toronto, ON 613.236.9191 | 647.288.9200 [email protected]

Cost or Asset-Based Approach

When a company has very little in way of cash flow or predictability, or is no longer a going-concern, the company is generally evaluated based on its assets (tangible and intangible). Below is a list of assets and how they are commonly valuated in a cost or asset-based approach:

• Accounts Receivables are generally valued on the likelihood of collecting. Therefore, the profile of the customer owning money will determine the value.

• Furniture and fixtures are generally estimated on what you could get selling by selling to an auction or used furniture wholesaler.

• Intangible assets, such as patents, royalty agreements, and franchise agreements typically have little to no value.

• Inventory is generally assessed on condition, and whether the product can be sold at full market price.

• Leasehold improvements usually have no value.

• Other assets (Goodwill, brand, development cost, costumer list, etc.) are worth nothing if the business is not a going concern.

• Prepaid expenses such as deposits, are deemed to be worth the full value if it is determined that the amount is refundable.

• Real Estate (Land or building) are valued at their fair market value.

Form of Payment

More often than not, the Buyer will NOT be offering an all-cash deal. Typically, the prospective Buyer will provide a portion in cash, and the balance as a Vendor Take Back (VTB), and/or an Earn-Out. A Vendor Take Back is when the vendor (seller) provides some or all of the financ-ing in order to sell the business. This is a concept that many business owners struggle to understand. A common response is “You want me to fund the buyer from the cash my business it generates? If that’s the case, I may as well keep running the business.” It is true that you could just keep the business, however, with that comes the added responsibility, stress, and headaches that come with running a business. Furthermore, most buyers do not have the amount of cash required to complete the deal. Therefore, if you are able to provide financing, you increase the likelihood of finding the right buyer for your business.

Furthermore, most buyers do not have the amount of cash required to complete the deal. Therefore, if you are able to provide financing, you increase the likelihood of finding the right buyer for your business.

If you are able to provide financing, you increase the likelihood of finding the right buyer for your business.

S E L L E R ' S G U I D E

www.w-group.com

5

Guide: Selling

1. Executive Summary

2. Company Overview

3. Industry Analysis

4. Financial Assessment

5. Presentation of the Opportunity

Confidential Information Memorandum

Earn-Outs

Earn-outs are usually prevalent when the Seller presents a strong growth forecast for which he/she wants to value. The Buyer typ-ically leans on historical data as much as possible. Therefore, the Buyer will use an earn-out as a method of protecting themselves if the Sellers forecast does not materialize. If you achieve $XXX in revenue, you will earn another $XXX amount. Earn-outs can be a very positive if the Seller believes there is some growth ahead and would like to be compensated for that upside. An earn-out should only be considered if the Seller plans to have an active role post-transaction and if the Seller can directly influence the outcome of the target. For example, it would not make sense to accept an earn-out clause that stipulated that the business is required to stay at 10% profitability if the Seller was not going to be responsible for the day-to-day management.

Vendor Take Back

A VTB is when the seller takes back a debt note on a portion of the outstanding purchase price. The note usually bears an interest, and therefore the Buyer pays the seller the principal and interest monthly, quarterly, etc. on the balance of the owing pur-chase price over a pre-determined period of time. This note may be secure or unsecure depending on what assets the company may own. In addition, the note usually comes with the right to take back the company if the Buyer fails to pay.

5. Creation + Approval of the CIM (PitchBook)

A confidential information memorandum (CIM) is a document drafted by an M&A advisory firm or investment banker used in a sell-side engagement to market a business to prospective buyers. Not only is this is a marketing tool; in the due diligence phase, the CIM will answer 90% of questions that need to be answered for careful assessment. Once the CIM is complete, you must review its infor-mation to confirm that everything is in order. Once you approve this document, it will be finalized and ready for going out to market.

W E LC H G R O U P C O N S U LT I N G

www.w-group.com

6

Ottawa, ON | Toronto, ON 613.236.9191 | 647.288.9200 [email protected]

S E L L E R ' S G U I D E

www.w-group.com

7

Guide: Selling

6. Prospect Approval

Prospects are potential buyers/ sellers who may want to engage in a M&A transaction. Companies and individuals have all kinds of motives for purchasing a business. Such motives can be finan-cial, strategic, emotional... and some motives are not rational at all! In fact, economists have all kinds of theories about irrational consumers who make inexplicable purchase decisions. None-theless, there are 5 strategic reasons why companies merge or acquire:

1. Synergy

2. Diversification/Sharpening Business Focus

3. Growth

4. Increase Supply-Chain Pricing Power

5. Eliminate Competition

WelchGroup will compile a list of prospect buyers/ sellers for you to review. You must confirm that you are okay with having our team contact these businesses; due to confidentiality and competition, there may be situations where you prefer for us to not reach out to specific prospects. You may also recommend businesses or individuals who you think we should consider as prospects – after all, you are industry experts who best understand the market and its players!

Welchgroup maintains a list of prospective buyers. In addition, Welchgroup has access its vast client base across Ontario and North America. In addition, WelchGroup affiliation with BKR, an International association of independent accounting and business advisory firms with ver 145 firms in 300 offices in over 70 countries around the world

7. Creation + Release of Teaser

The teaser (sometimes called an executive summary) is a one-page document that the Seller sends to the potential Buyer. It includes just enough information to make the Buyer want to learn more about the business at hand.

Teasers include very general information about the industry, company size, type of customers, geographic location, and some high-level financials. They are anonymous meaning that the Buyer does not know which specific company is referred to in the document.

8. Non-Disclosure Agreement (NDA)

A non-disclosure agreement (NDA) is a legal contract between at least two parties that outlines confidential material, knowledge, or information that the parties wish to share with one another for certain purposes, but wish to restrict access to third parties. Businesses must sign this document to get access to the CIM (pitchbook) to protect the confident nature of your transaction.

W E LC H G R O U P C O N S U LT I N G

www.w-group.com

8

Ottawa, ON | Toronto, ON 613.236.9191 | 647.288.9200 [email protected]

9. Viewer Tracking

After signing the non-disclosure agreement, the prospect is invited to view the CIM (pitchbook) on Firmex. WelchGroup Consulting is able to see metrics in regards to how much time is being spent looking at the pitchbook, how often, and which pages are viewed the longest. After viewing the pitchbook, the prospect will have enough information at hand to decide whether he/ she is seriously interested in purchasing the business at hand.

10. Negotiations + Letter of Intent

Now it is time for your prospect to make a decision. If the prospect is seriously interested in the business, he or she will sign a letter of intent (LOI). This document outlines the terms of a deal and serves as an agreement between two parties. A LOI is similar to a term sheet in its content, but differs in structure (one formatted as a letter, the other as a list of terms). Once this is signed, you have a seri-ous and official offer.

However, before agreeing to specific terms, WelchGroup will engage in negotiations that will provide desirable and beneficial out-comes for both parties. The following are two different types of negotiating styles that are commonly used:

Distributive Negotiation

Distributive Negotiating (Win-Lose Negotiating) is where each party negotiates on their behalf to win the biggest piece of the figurative “pie”. This is because distributive negotiation assumes there is a "fixed pie", and therefore a zero-sum. This style is often referred to as “win-lose”, because it is implied that if you are gaining, the other is losing. Everyday examples include buying a car, or real estate. This style tends to be the way we sell a business. The owner is trying to get the most money, while the prospective buyer is trying to pay less. In this style, it is the more skilled negotiator that will likely walk away the winner. Tactics include:

• Anchoring: Establishing a reference point around which negotiations are to be made. For example, real estate uses this tech-nique once the seller sets their price.

• Counter Anchoring: Don't let the other side set the bargaining range with an anchor unless you think it is a reasonable starting point.

• Timing: Use the clock to your advantage (deal fatigue or artifical deadlines)

Integrative Negotiation

Integrative Negotiation looks to expand the “pie”. The goal is to consider the underlying interests of both parties, rather than be adversaries. In this style, you cooperate to achieve maximum benefits. This style of negotiating is often referred to as “Win-Win”. Tactics include:

• Ask open-ended questions to learn about the other party's needs• Listen closely to the opposing party's responses• Look for options that exploit differences• Continual evaluation and preparation

S E L L E R ' S G U I D E

www.w-group.com

9

Guide: Selling

Three Steps to Successfully Negotiate a Deal

1. Consider what you would consider to be a good outcome for you. Review your goals to gain a better understanding of the position you hope to attain for a favourable outcome.

2. Once you have identified your goals, it is important to learn everything you can about the other party. In order to be an integrative negotiater, you must listen and understand the other side's interests.

3. Identify potential value creation opportunities that include the interest of both parties.

11. Final Due Diligence

You have managed to agree to terms, however, the prospective Buyer will want to conduct a thorough due diligence before he/she moves forward. This process can be long or quick, and length of time is largely determined by the Seller. Being organized and pre-pared to deliver the requested information to the Prospective Buyer will likely speed up the process.Due Diligence (DD) is the investigation or audit of a potential investment. Due diligence serves to confirm all material facts in re-gards to a sale. It is an exhaustive review of all business documents and records in an effort to assess the health and viability of the business that is in question. Due diligence is a lengthy process that ensures a good sale without any surprises, hidden problems or unexpected strings attached. It aims to achieve three primary objectives:

1. Assures the potential Buyer that financial matters, management practices, operations, and legal matters are in good order and without unexpected issues/risks

2. Conducted as a level of judgement, care, prudence, determination, and activity that a person would reasonably be expected/should take before entering into an agreement or a transaction with another party.

3. Identifies potential risks and negative synergies.

W E LC H G R O U P C O N S U LT I N G

Additional Areas for Consideration:

• Financial Information• Sales and Marketing• Product and Services • Customers and Target Market • Management and Employees• Employee Analysis • Operational Information• Logistics• Executive Summary

• Corporate Details • SWOT Analysis • Customers List• Corporate Culture • Unique technology, proprietary processes and other competitive advantage • Research and Development • A summary of historical and prospective key performance indicators• Technology and Service• References

www.w-group.com

10

Ottawa, ON | Toronto, ON 613.236.9191 | 647.288.9200 [email protected]

11. Closing

Deal closing is the very last step in the M&A sell-side process. It is a moment of celebration during which the sale of your business becomes official, and the transition process can officially begin. Now that you have agreed to terms, it is time to formalize those terms and set the transition in motion. Like selling a home, at this stage, you will require the help of legal counsel to draft the many agreements. Your Lawyer will work with you to ensure all liabilities and transfers of assets are done properly. If you have agreed to finance some of the transaction, your lawyer will draft the Vendor Take Bake and secure it against the business assets. In addition, he will be responsible for the corporate transfer of the business to the Buyer.

Once due diligence is conducted, the terms of the contracts become official and the sale of the business becomes finalized. Then, when closing is finally complete, WelchGroup’s transitionary services are complete as well. Nevertheless, we will keep in touch with your team to make sure you are doing well after selling your business.

S E L L E R ' S G U I D ES E L L E R ' S G U I D E

www.w-group.com

11

Guide: Selling

Our Tools + Software

Navatar M&A cloud helps us manage all activities and records associated with prospects and buyers, all marketing and communications initiatives, and all aspects of business development.

Salesforce is a customer relationship management (CRM) used to manage customer/ contact rela-tionships.

IBISWorld is a global business intelligence leader specializing in Industry Market Research and Pro-curement and Purchasing research reports.

Business Reference Guide (BRG) is the essential guide to pricing businesses, providing business transaction professionals with up-to-date rules of thumb and pricing information for 700+ types of businesses. The Business Reference Guide is published by Business Brokerage Press.

PitchBook is a data and technology provider for the global private equity & venture capital markets. This powerful tool is used for analyzing activity in rapidly evolving industries by accessing powerful insights across the entire investment lifecycle.

Firmex facilitates secure document sharing across corporate firewalls. This company is a leader in licensing Online Virtual Data Room solutions for corporate transactions, governance and compliance matters. Firmex focuses on delivering highly secure, reliable, fast and intuitive technology with top tier 24/7 client support.

Profitcents by Sageworks is a suite of web-based financial analysis solutions that use real-time in-dustry data on private companies to find industry benchmarks. These benchmarks are used to advise clients on how they compare to industry standards.

W E LC H G R O U P C O N S U LT I N G

www.w-group.com

12

Ottawa, ON | Toronto, ON 613.236.9191 | 647.288.9200 [email protected]

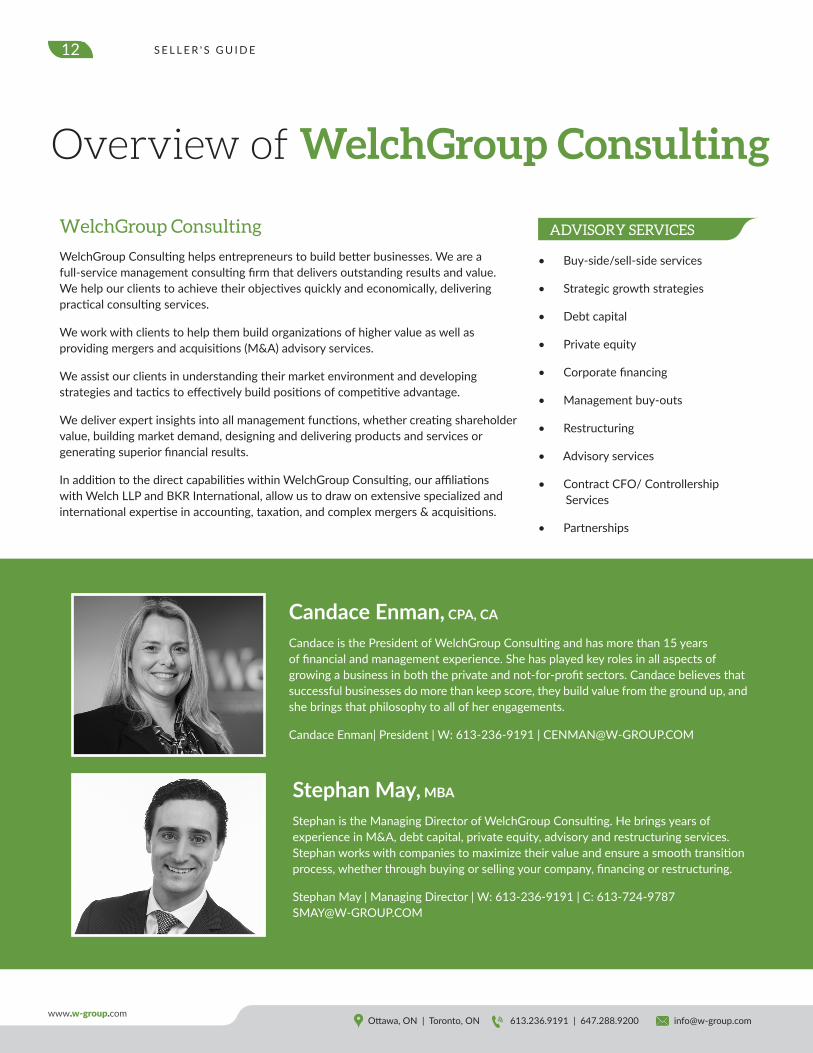

Overview of WelchGroup Consulting

WelchGroup Consulting

WelchGroup Consulting helps entrepreneurs to build better businesses. We are a full-service management consulting firm that delivers outstanding results and value. We help our clients to achieve their objectives quickly and economically, delivering practical consulting services.

We work with clients to help them build organizations of higher value as well as providing mergers and acquisitions (M&A) advisory services.

We assist our clients in understanding their market environment and developing strategies and tactics to effectively build positions of competitive advantage.

We deliver expert insights into all management functions, whether creating shareholder value, building market demand, designing and delivering products and services or generating superior financial results.

In addition to the direct capabilities within WelchGroup Consulting, our affiliations with Welch LLP and BKR International, allow us to draw on extensive specialized and international expertise in accounting, taxation, and complex mergers & acquisitions.

• Buy-side/sell-side services

• Strategic growth strategies

• Debt capital

• Private equity

• Corporate financing

• Management buy-outs

• Restructuring

• Advisory services

• Contract CFO/ Controllership Services

• Partnerships

ADVISORY SERVICES

Candace Enman, CPA, CA

Candace is the President of WelchGroup Consulting and has more than 15 years of financial and management experience. She has played key roles in all aspects of growing a business in both the private and not-for-profit sectors. Candace believes that successful businesses do more than keep score, they build value from the ground up, and she brings that philosophy to all of her engagements.

Candace Enman| President | W: 613-236-9191 | [email protected]

Stephan May, MBA

Stephan is the Managing Director of WelchGroup Consulting. He brings years of experience in M&A, debt capital, private equity, advisory and restructuring services. Stephan works with companies to maximize their value and ensure a smooth transition process, whether through buying or selling your company, financing or restructuring.

Stephan May | Managing Director | W: 613-236-9191 | C: 613-724-9787 [email protected]

S E L L E R ' S G U I D E

www.w-group.com

13

Guide: Selling

Seller's Guide

WelchGroup Consultingwww.w-group.com