Embed Size (px)

Citation preview

Westdale Mall Market Analysis AECOM Economics

October 2013

Executive Summary

Page 2

Beginning in February of 2013, AECOM Economics (formerly ERA) was engaged by Frew Development to assess real estate market conditions in the Cedar Rapids Metropolitan Area (MSA), focused on the Westdale Mall. Our analysis includes study of broader economic metrics for the Cedar Rapids area, as well as study of retail, office, hotel, residential and senior housing markets. The effort also builds from a prior 2007 market study for Westdale Mall completed by ERA at the request of the City of Cedar Rapids. The 2007 effort included a demographic assessment of Cedar Rapids, identification of target markets that would be supportive of mall revitalization, and case studies of shopping center projects and mixed use communities.

Having completed the analysis, our core findings include:

Economic and Demographic Context

• Cedar Rapids MSA employment growth compare favorably with statewide benchmarks, and unemployment rates are enviably below Midwestern peers.

• Although the recession did not hit Cedar Rapids with the same intensity, the region’s pace of job recovery since 2010 is lagging compared to other Iowa metros. Returning to pre-recession growth rates would suggest an increase to 1,900 new jobs/year, versus the current pace of about 900-1,000 jobs/year.

• The expectation is for the Cedar Rapids market to return to historic form, i.e. steady growth, anchored by manufacturing and health care. Evolving economic linkage between Iowa City and Cedar Rapids broadens trade area potentials for Westdale.

Retail Market

• Estimated “competitive” retail vacancy for the SW side is about 3%, compared to national retail vacancy over 12% (Q4 2012 CBRE).

• Cedar Rapids MSA pull factors are modestly positive, suggesting that existing retail offerings largely serve local residents.

• The Lindale Mall area supports a majority of regional retail space, albeit with a preponderance of older (>15-year old) retail buildings, with limited sites available for new larger scale retail projects.

• Retail sales in Cedar Rapids have been recovering at rates equal to or above state averages since 2010, which is significant, given a slower pace of job growth locally.

• Two competitive retail projects were identified; The Fountains, as well as a proposal to expand the Lindale Mall. The Fountains has secured City incentives and appears ready to move forward.

• Rents paid by national chains appear to be approaching $15 / square foot NNN, with a small number of centers at $20 / SF.

• The US retail industry is still recovery mode, and retailers are just beginning to focus on new (albeit generally smaller stores), even as the internet continues to alter many retailer business plans.

• The analysis showed that the SW side appears under served in apparel, shoes, jewelry, & accessories, electronics, miscellaneous, book stores, and food & beverage.

• Between 1990 and 2009, the Cedar Rapids region added about 250,000 SF of retail space per year, linked with big box stores. Presuming that the market can sustain population growth of 0.9% and income growth of 3.5%, average annual growth in retail space of about 140,000 SF per year is anticipated. However, for the short-term, it is not clear that sufficient national chain tenants exist to meet this demand.

• From a tenanting standpoint, health care tenants are seen as more likely in the future.

Prognosis: For the defined trade areas around Westdale, the analysis identified incremental potential spending support between 2013 and 2017 for up to about 260,000 square feet of retail space tied to defined primary and secondary markets. Reflecting a conservative approach, the analysis did not expressly presume capture from tertiary markets across Cedar Rapids or Iowa City. With the proper tenant mix, competition for regional lifestyle oriented retail and entertainment should be an expectation.

Executive Summary

Page 3

Hotel Market Analysis of a core set of competitive hotels revealed a reasonably attractive market, with growth in room demand and high occupancies (69%), offset by reduced (but still positive) growth in average daily rate. Although the reopening of the convention hotel will increase supply, the combined new hotel and convention venue will allow the region to support larger events. There are a number of brands not yet in the local market, including Hilton Garden Inn and Drury.

Prognosis: “Positive but Tight” The market is positioned to support additional rooms; timing to market will be important for this segment.

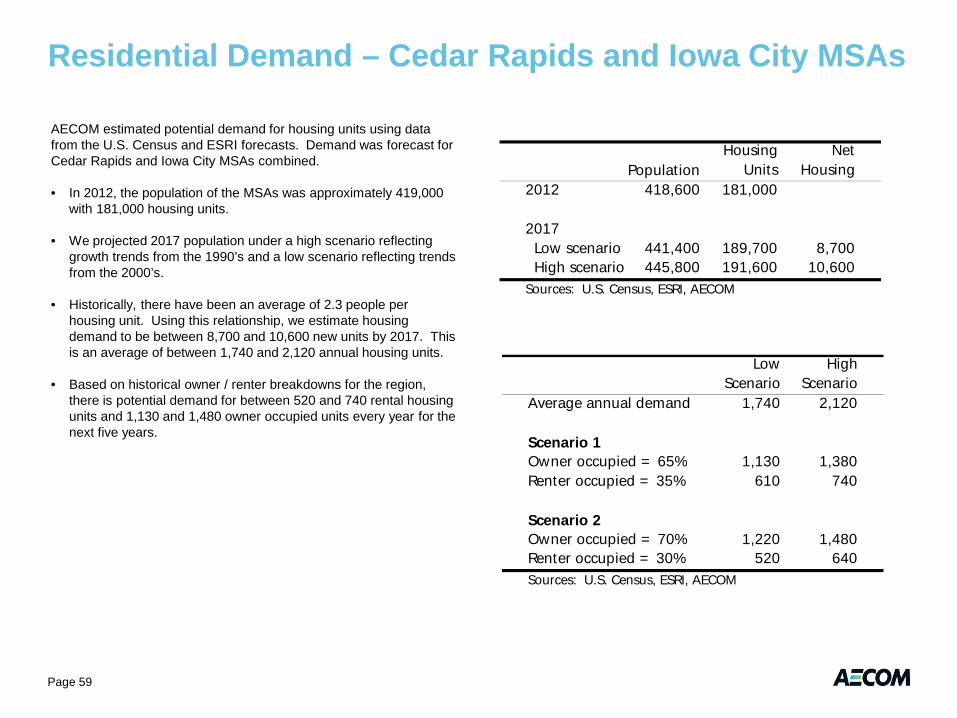

Residential Market Core findings include:

• From a residential standpoint, the Westdale site is viewed as a competitive location for people who currently work in Iowa City, as well as those who work locally. For this reason, our residential approach looked at demand growth in both MSAs.

• The Cedar Rapids MSA has an unusually low cost of living index factor for housing, 25% below the average for all MSAs. In spite of this factor, the analysis identified relevant market premiums for recently-built condominiums (1bedroom @ $150/sf), as well as a small sample of rental units priced above $1/SF/month. For the rental market, newer units are not priced at a premium to older units, which is significant.

• There are very few modern “urban” rental units in the market, and in general, walkability is limited. For boomer age segments in particular, sites with walkability will be a differentiator.

• Senior housing markets are expected grow in the near-term, linked with identified strong growth in 55-64 and 65 to 74 age groups across Iowa City and Cedar Rapids. Based on experience, we would anticipate a gradual shift from condominium and age restricted units to projects offering a continuum of care over the next 20 years. From a real estate standpoint, as projects move toward the continuing care model, the business case is increasingly influenced by insurance and payments for services, rather than monthly rent payments. Locally, a sample of about 900 units was identified with several operators, with

a small share of units built since 2000.

• While the overall senior market appears strong, the historic trend is the majority of seniors choose to age in place. With a significant share of boomers now entering retirement, how this trend may shift will be critical.

Prognosis: “Reasonable” Solid population growth expectations are in place for the regional market, which align with a competitive Westdale site, suitable in our view for residents who work in either Cedar Rapids or Iowa City. Although overall residential unit values are very affordable, the market does include several projects (older as well as newer) which are supporting higher rents and attractive condominium pricing.

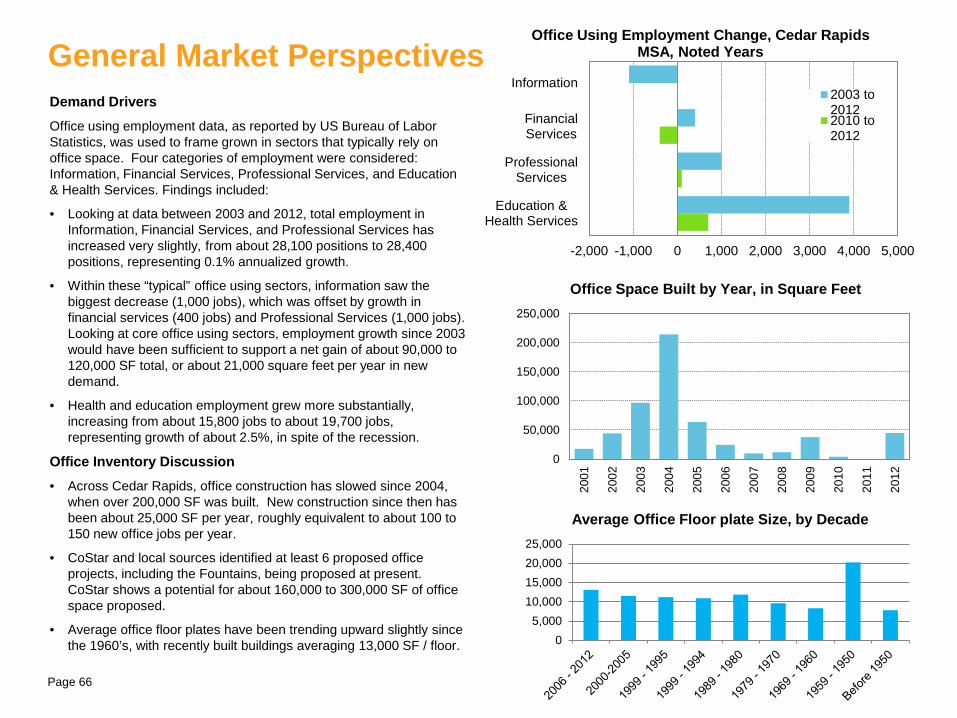

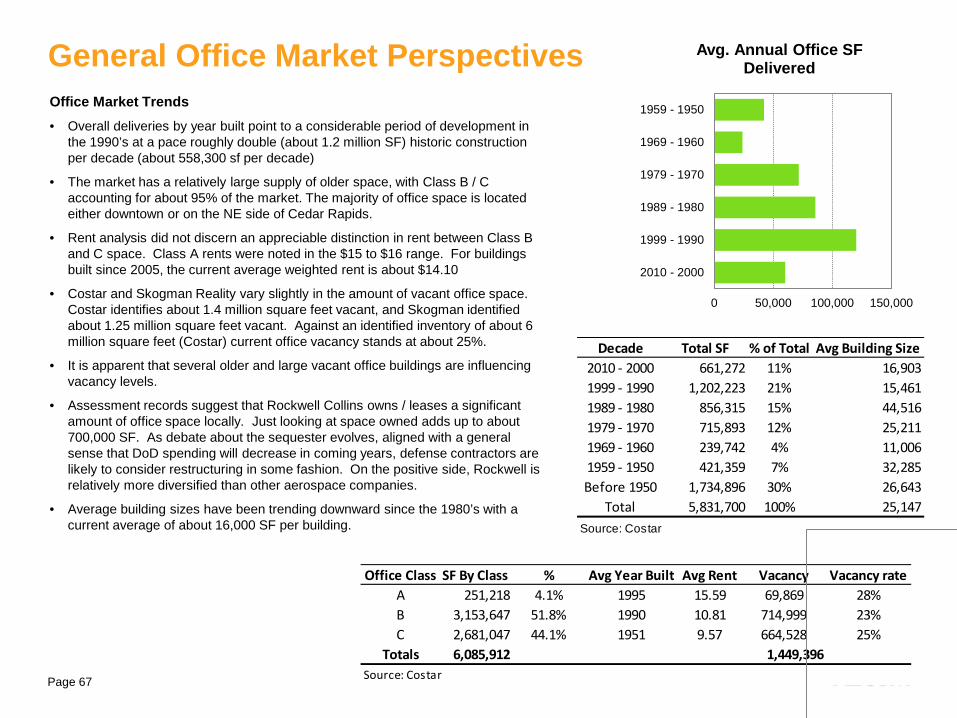

Office Market The local market is reacting to several forces:

1. Modest net growth in employment for traditional sectors that use office space, with stronger growth in medical employment.

2. A considerable supply of older and arguably obsolete space in the market, with overall Vacancy levels above 20%.

3. A small supply of contemporary office space, class A or otherwise.

4. Concern over evolving decisions at Rockwell regarding their space needs.

Prognosis: “Less than ideal”. A near term market that is going to be tenant driven, with gradual recovery toward an average pace of about 50,000 SF of new office construction per year within 2-3 years, with older but not historic buildings being competitively challenged, which will dampen rent growth. A lack of modern space in the market is one clear driver of new space.

More precise Westdale site implications are noted on the following page.

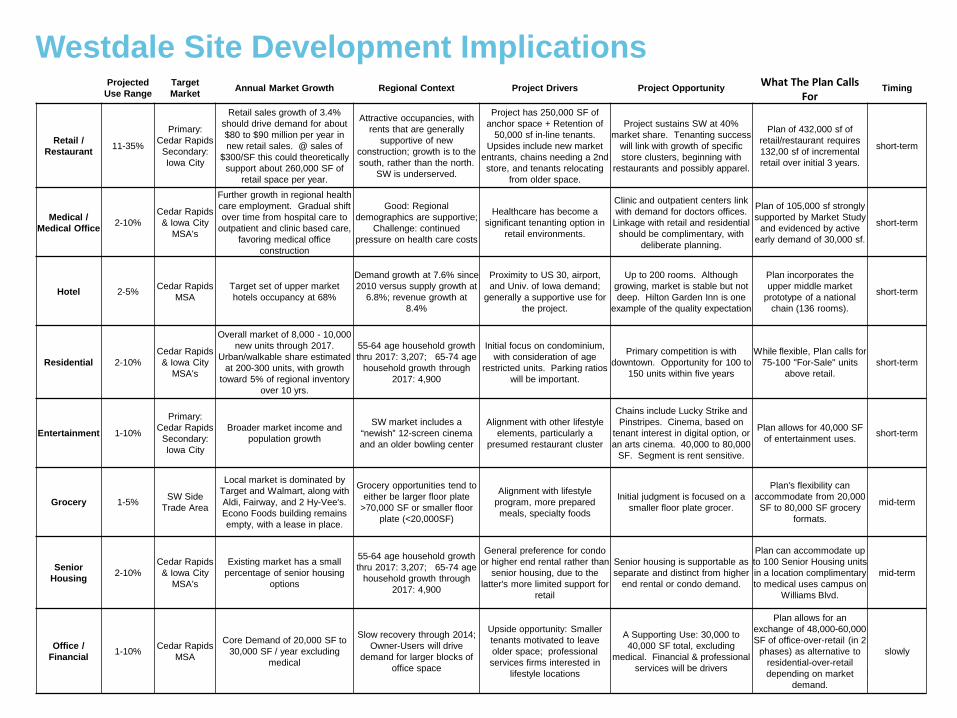

Westdale Site Development Implications

Page 4

Projected Use Range

Target Market Annual Market Growth Regional Context Project Drivers Project Opportunity What The Plan Calls

For Timing

Retail / Restaurant 11-35%

Primary: Cedar Rapids

Secondary: Iowa City

Retail sales growth of 3.4% should drive demand for about $80 to $90 million per year in new retail sales. @ sales of

$300/SF this could theoretically support about 260,000 SF of

retail space per year.

Attractive occupancies, with rents that are generally

supportive of new construction; growth is to the south, rather than the north.

SW is underserved.

Project has 250,000 SF of anchor space + Retention of

50,000 sf in-line tenants. Upsides include new market

entrants, chains needing a 2nd store, and tenants relocating

from older space.

Project sustains SW at 40% market share. Tenanting success

will link with growth of specific store clusters, beginning with

restaurants and possibly apparel.

Plan of 432,000 sf of retail/restaurant requires 132,00 sf of incremental retail over initial 3 years.

short-term

Medical / Medical Office 2-10%

Cedar Rapids & Iowa City

MSA's

Further growth in regional health care employment. Gradual shift over time from hospital care to

outpatient and clinic based care, favoring medical office

construction

Good: Regional demographics are supportive;

Challenge: continued pressure on health care costs

Healthcare has become a significant tenanting option in

retail environments.

Clinic and outpatient centers link with demand for doctors offices.

Linkage with retail and residential should be complimentary, with

deliberate planning.

Plan of 105,000 sf strongly supported by Market Study

and evidenced by active early demand of 30,000 sf.

short-term

Hotel 2-5% Cedar Rapids MSA

Target set of upper market hotels occupancy at 68%

Demand growth at 7.6% since 2010 versus supply growth at

6.8%; revenue growth at 8.4%

Proximity to US 30, airport, and Univ. of Iowa demand;

generally a supportive use for the project.

Up to 200 rooms. Although growing, market is stable but not deep. Hilton Garden Inn is one

example of the quality expectation

Plan incorporates the upper middle market

prototype of a national chain (136 rooms).

short-term

Residential 2-10% Cedar Rapids & Iowa City

MSA's

Overall market of 8,000 - 10,000 new units through 2017.

Urban/walkable share estimated at 200-300 units, with growth

toward 5% of regional inventory over 10 yrs.

55-64 age household growth thru 2017: 3,207; 65-74 age

household growth through 2017: 4,900

Initial focus on condominium, with consideration of age

restricted units. Parking ratios will be important.

Primary competition is with downtown. Opportunity for 100 to

150 units within five years

While flexible, Plan calls for 75-100 "For-Sale" units

above retail. short-term

Entertainment 1-10%

Primary: Cedar Rapids

Secondary: Iowa City

Broader market income and population growth

SW market includes a “newish” 12-screen cinema and an older bowling center

Alignment with other lifestyle elements, particularly a

presumed restaurant cluster

Chains include Lucky Strike and Pinstripes. Cinema, based on

tenant interest in digital option, or an arts cinema. 40,000 to 80,000

SF. Segment is rent sensitive.

Plan allows for 40,000 SF of entertainment uses. short-term

Grocery 1-5% SW Side Trade Area

Local market is dominated by Target and Walmart, along with Aldi, Fairway, and 2 Hy-Vee's. Econo Foods building remains empty, with a lease in place.

Grocery opportunities tend to either be larger floor plate

>70,000 SF or smaller floor plate (<20,000SF)

Alignment with lifestyle program, more prepared meals, specialty foods

Initial judgment is focused on a smaller floor plate grocer.

Plan's flexibility can accommodate from 20,000 SF to 80,000 SF grocery

formats.

mid-term

Senior Housing 2-10%

Cedar Rapids & Iowa City

MSA's

Existing market has a small percentage of senior housing

options

55-64 age household growth thru 2017: 3,207; 65-74 age

household growth through 2017: 4,900

General preference for condo or higher end rental rather than

senior housing, due to the latter's more limited support for

retail

Senior housing is supportable as separate and distinct from higher

end rental or condo demand.

Plan can accommodate up to 100 Senior Housing units in a location complimentary to medical uses campus on

Williams Blvd.

mid-term

Office / Financial 1-10% Cedar Rapids

MSA

Core Demand of 20,000 SF to 30,000 SF / year excluding

medical

Slow recovery through 2014; Owner-Users will drive

demand for larger blocks of office space

Upside opportunity: Smaller tenants motivated to leave older space; professional services firms interested in

lifestyle locations

A Supporting Use: 30,000 to 40,000 SF total, excluding

medical. Financial & professional services will be drivers

Plan allows for an exchange of 48,000-60,000 SF of office-over-retail (in 2

phases) as alternative to residential-over-retail depending on market

demand.

slowly

Table of Contents

Page 5

Demographic and Economic Analysis Page 6

Retail Market Analysis Page 20

Residential Market Analysis Page 39

Hotel Market Analysis Page 61

Office Market Analysis Page 65

Overall Considerations Page 70

General Limiting Conditions Page 72

Demographic and Economic Analysis

Introduction

The Demographic and Economic Analysis places the Cedar Rapids region in a broader context, focused on how the region has performed in terms of:

• Population and income growth

• Gross domestic product

• Employment and unemployment

The analysis is used to judge the competitive position of the region, and any strategic threats and opportunities.

Page 6

Regional Map

2000 2002 2004 2006 2008 2010 CAGRCedar Rapids 121,360 122,230 122,301 123,647 125,871 126,490 0.4%Cedar Rapids MSA 237,950 242,099 245,108 249,524 255,503 258,310 0.8%Des Moines MSA 483,243 496,276 511,257 532,738 553,644 571,938 1.7%Iowa City MSA 132,173 136,056 140,149 143,698 148,799 152,950 1.5%State of Iowa 2,929,067 2,934,234 2,953,635 2,982,644 3,016,734 3,050,202 0.4%Source: U.S. Census

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Cedar Rapids MSA Des Moines MSA Iowa City MSA Iowa

Source: U.S. Census

Annual Change in Population, 1990-2011

Population by MSA

0

50,000

100,000

150,000

200,000

250,000

300,00019

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

11

Source: U.S. Census

Population in Cedar Rapids MSA

Benton County Jones County Linn County

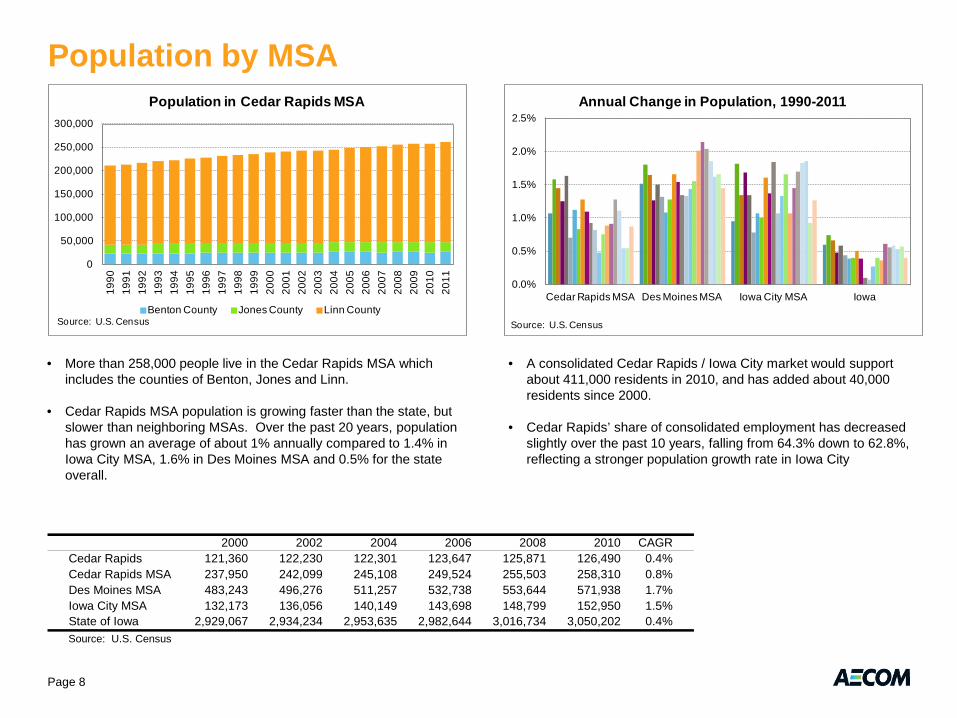

• More than 258,000 people live in the Cedar Rapids MSA which includes the counties of Benton, Jones and Linn.

• Cedar Rapids MSA population is growing faster than the state, but slower than neighboring MSAs. Over the past 20 years, population has grown an average of about 1% annually compared to 1.4% in Iowa City MSA, 1.6% in Des Moines MSA and 0.5% for the state overall.

• A consolidated Cedar Rapids / Iowa City market would support about 411,000 residents in 2010, and has added about 40,000 residents since 2000.

• Cedar Rapids’ share of consolidated employment has decreased slightly over the past 10 years, falling from 64.3% down to 62.8%, reflecting a stronger population growth rate in Iowa City

Page 8

-0.5%0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: US Census

Change in Regional Population, 2001-2011

Cedar Rapids Coralville Hiawatha Marion

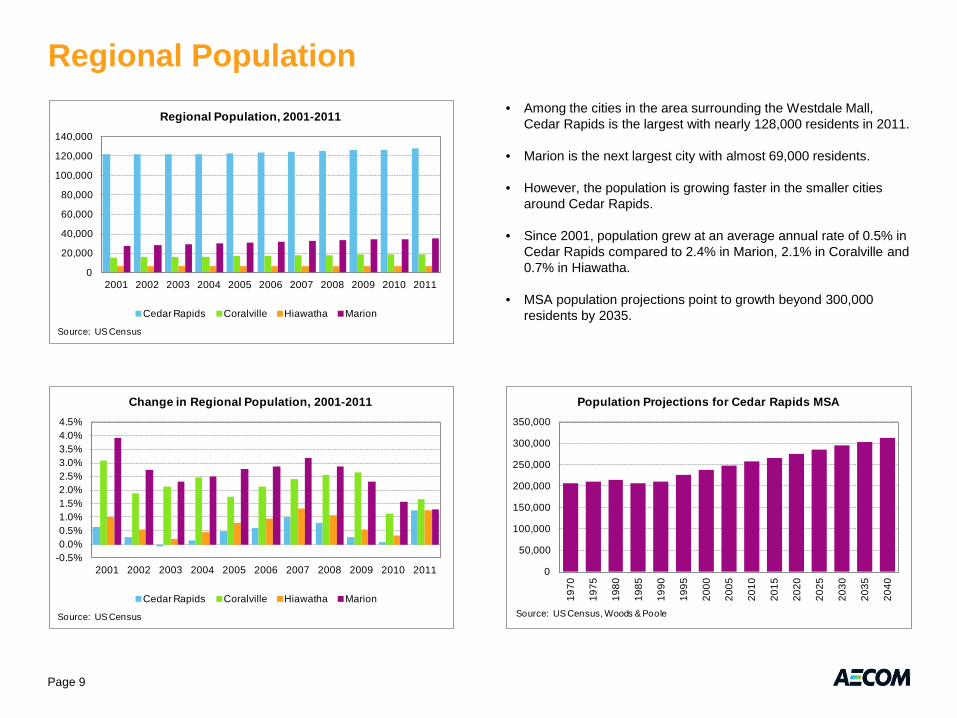

Regional Population • Among the cities in the area surrounding the Westdale Mall,

Cedar Rapids is the largest with nearly 128,000 residents in 2011.

• Marion is the next largest city with almost 69,000 residents.

• However, the population is growing faster in the smaller cities around Cedar Rapids.

• Since 2001, population grew at an average annual rate of 0.5% in Cedar Rapids compared to 2.4% in Marion, 2.1% in Coralville and 0.7% in Hiawatha.

• MSA population projections point to growth beyond 300,000 residents by 2035.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: US Census

Regional Population, 2001-2011

Cedar Rapids Coralville Hiawatha Marion

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

Source: US Census, Woods & Poole

Population Projections for Cedar Rapids MSA

Page 9

Long Range Population Growth Expectations

Page 10

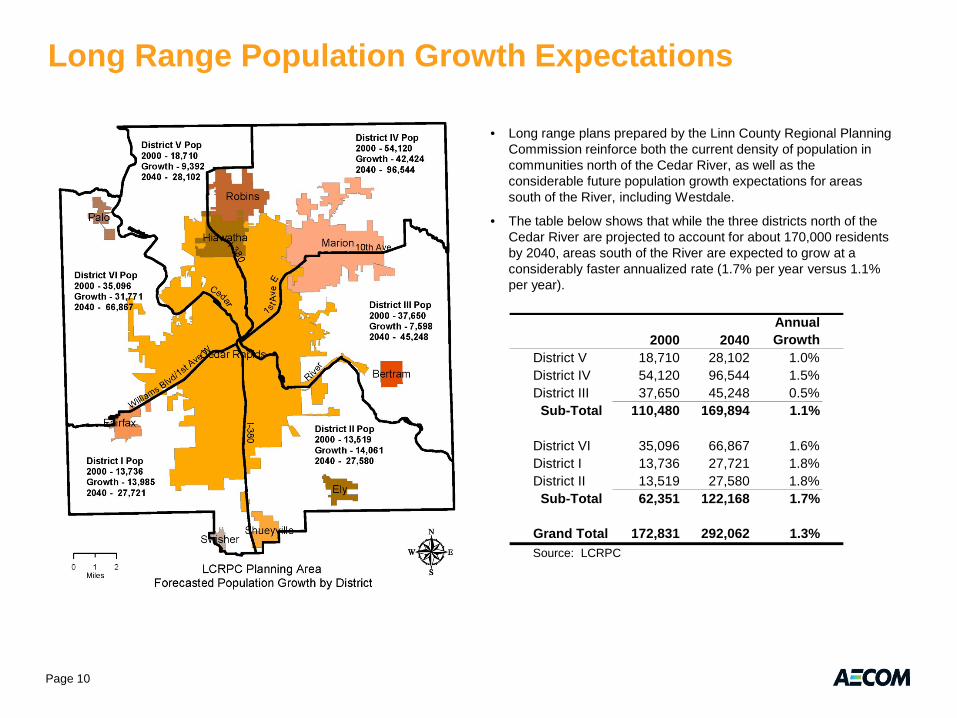

• Long range plans prepared by the Linn County Regional Planning Commission reinforce both the current density of population in communities north of the Cedar River, as well as the considerable future population growth expectations for areas south of the River, including Westdale.

• The table below shows that while the three districts north of the Cedar River are projected to account for about 170,000 residents by 2040, areas south of the River are expected to grow at a considerably faster annualized rate (1.7% per year versus 1.1% per year).

2000 2040Annual Growth

District V 18,710 28,102 1.0%District IV 54,120 96,544 1.5%District III 37,650 45,248 0.5% Sub-Total 110,480 169,894 1.1%

District VI 35,096 66,867 1.6%District I 13,736 27,721 1.8%District II 13,519 27,580 1.8% Sub-Total 62,351 122,168 1.7%

Grand Total 172,831 292,062 1.3%Source: LCRPC

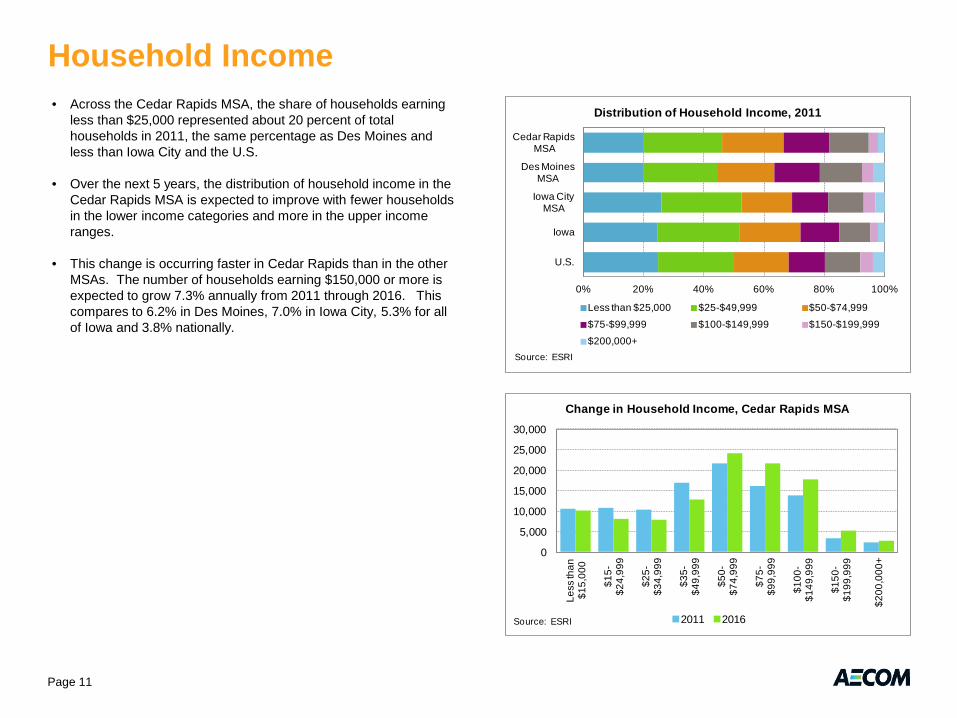

Household Income • Across the Cedar Rapids MSA, the share of households earning

less than $25,000 represented about 20 percent of total households in 2011, the same percentage as Des Moines and less than Iowa City and the U.S.

• Over the next 5 years, the distribution of household income in the Cedar Rapids MSA is expected to improve with fewer households in the lower income categories and more in the upper income ranges.

• This change is occurring faster in Cedar Rapids than in the other MSAs. The number of households earning $150,000 or more is expected to grow 7.3% annually from 2011 through 2016. This compares to 6.2% in Des Moines, 7.0% in Iowa City, 5.3% for all of Iowa and 3.8% nationally.

0

5,000

10,000

15,000

20,000

25,000

30,000

Less

than

$1

5,00

0

$15-

$24,

999

$25-

$34,

999

$35-

$49,

999

$50-

$74,

999

$75-

$99,

999

$100

-$1

49,9

99

$150

-$1

99,9

99

$200

,000

+

Source: ESRI

Change in Household Income, Cedar Rapids MSA

2011 2016

0% 20% 40% 60% 80% 100%

Cedar Rapids MSA

Des MoinesMSA

Iowa City MSA

Iowa

U.S.

Source: ESRI

Distribution of Household Income, 2011

Less than $25,000 $25-$49,999 $50-$74,999$75-$99,999 $100-$149,999 $150-$199,999$200,000+

Page 11

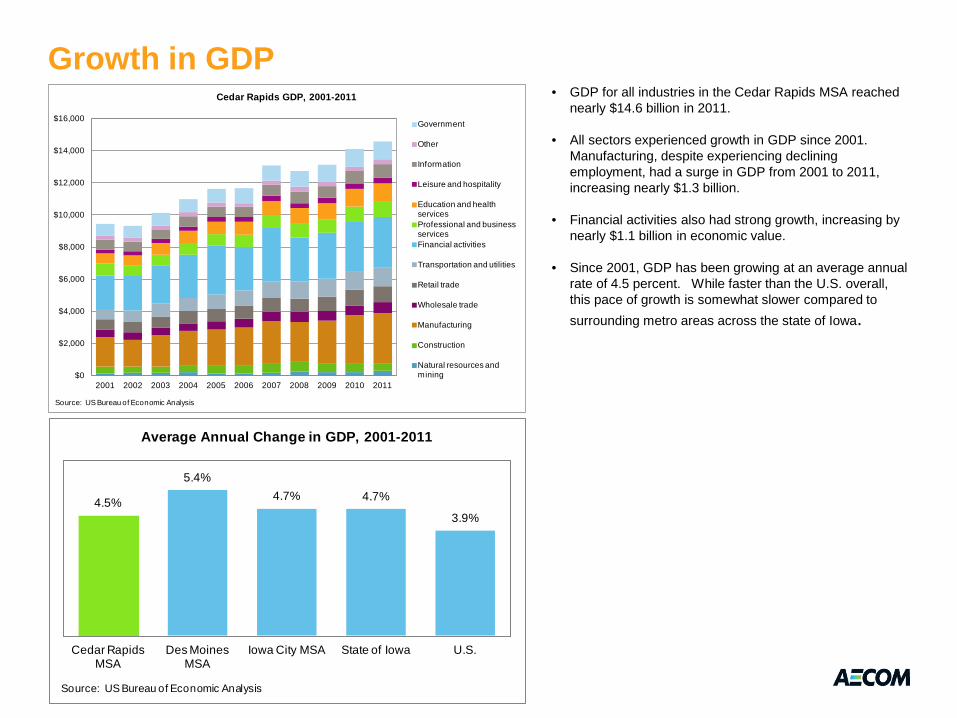

Growth in GDP • GDP for all industries in the Cedar Rapids MSA reached

nearly $14.6 billion in 2011.

• All sectors experienced growth in GDP since 2001. Manufacturing, despite experiencing declining employment, had a surge in GDP from 2001 to 2011, increasing nearly $1.3 billion.

• Financial activities also had strong growth, increasing by nearly $1.1 billion in economic value.

• Since 2001, GDP has been growing at an average annual rate of 4.5 percent. While faster than the U.S. overall, this pace of growth is somewhat slower compared to surrounding metro areas across the state of Iowa.

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: US Bureau of Economic Analysis

Cedar Rapids GDP, 2001-2011

Government

Other

Information

Leisure and hospitality

Education and health servicesProfessional and business servicesFinancial activities

Transportation and utilities

Retail trade

Wholesale trade

Manufacturing

Construction

Natural resources and mining

Page 12

4.5%

5.4%4.7% 4.7%

3.9%

Cedar Rapids MSA

Des Moines MSA

Iowa City MSA State of Iowa U.S.

Source: US Bureau of Economic Analysis

Average Annual Change in GDP, 2001-2011

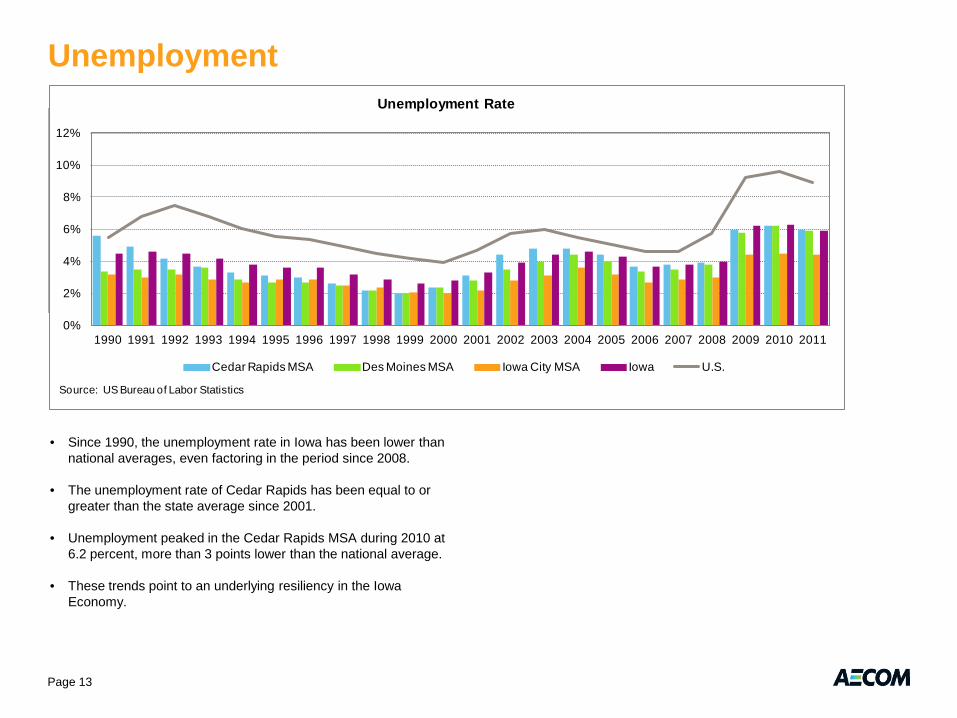

Unemployment

• Since 1990, the unemployment rate in Iowa has been lower than national averages, even factoring in the period since 2008.

• The unemployment rate of Cedar Rapids has been equal to or greater than the state average since 2001.

• Unemployment peaked in the Cedar Rapids MSA during 2010 at 6.2 percent, more than 3 points lower than the national average.

• These trends point to an underlying resiliency in the Iowa Economy.

020,00040,00060,00080,000

100,000120,000140,000160,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: Iowa Workforce Development

Employment in Cedar Rapids MSA

Goods Producing Service Providing

0%

2%

4%

6%

8%

10%

12%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: US Bureau of Labor Statistics

Unemployment Rate

Cedar Rapids MSA Des Moines MSA Iowa City MSA Iowa U.S.

Page 13

Broader Economic Considerations

Page 14

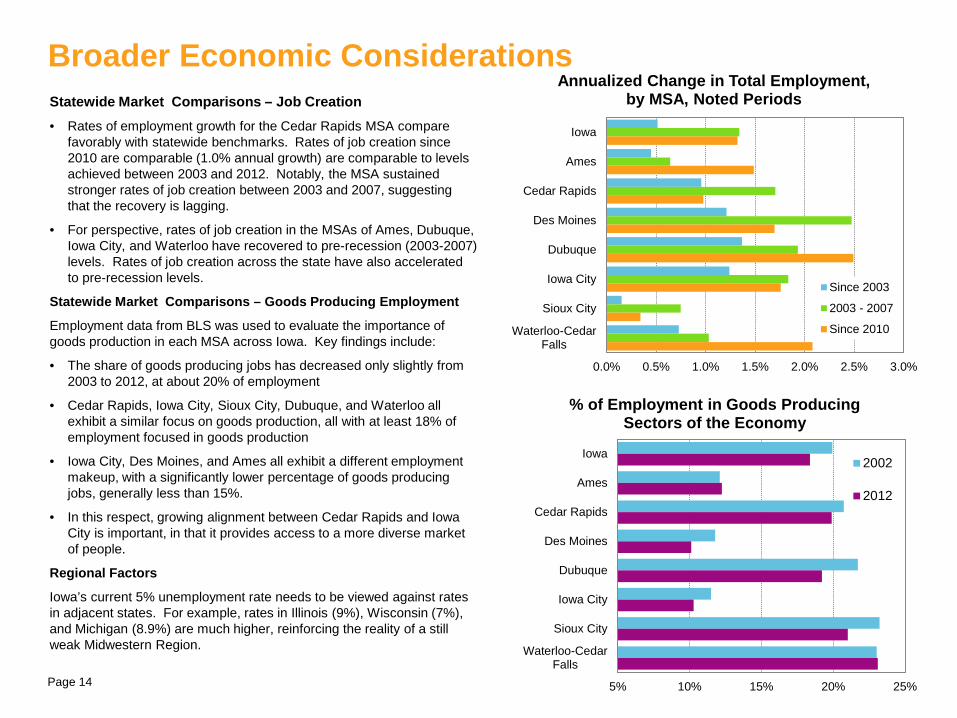

Statewide Market Comparisons – Job Creation • Rates of employment growth for the Cedar Rapids MSA compare

favorably with statewide benchmarks. Rates of job creation since 2010 are comparable (1.0% annual growth) are comparable to levels achieved between 2003 and 2012. Notably, the MSA sustained stronger rates of job creation between 2003 and 2007, suggesting that the recovery is lagging.

• For perspective, rates of job creation in the MSAs of Ames, Dubuque, Iowa City, and Waterloo have recovered to pre-recession (2003-2007) levels. Rates of job creation across the state have also accelerated to pre-recession levels.

Statewide Market Comparisons – Goods Producing Employment

Employment data from BLS was used to evaluate the importance of goods production in each MSA across Iowa. Key findings include:

• The share of goods producing jobs has decreased only slightly from 2003 to 2012, at about 20% of employment

• Cedar Rapids, Iowa City, Sioux City, Dubuque, and Waterloo all exhibit a similar focus on goods production, all with at least 18% of employment focused in goods production

• Iowa City, Des Moines, and Ames all exhibit a different employment makeup, with a significantly lower percentage of goods producing jobs, generally less than 15%.

• In this respect, growing alignment between Cedar Rapids and Iowa City is important, in that it provides access to a more diverse market of people.

Regional Factors

Iowa’s current 5% unemployment rate needs to be viewed against rates in adjacent states. For example, rates in Illinois (9%), Wisconsin (7%), and Michigan (8.9%) are much higher, reinforcing the reality of a still weak Midwestern Region.

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0%

Iowa

Ames

Cedar Rapids

Des Moines

Dubuque

Iowa City

Sioux City

Waterloo-CedarFalls

Annualized Change in Total Employment, by MSA, Noted Periods

Since 2003

2003 - 2007

Since 2010

5% 10% 15% 20% 25%

Iowa

Ames

Cedar Rapids

Des Moines

Dubuque

Iowa City

Sioux City

Waterloo-CedarFalls

% of Employment in Goods Producing Sectors of the Economy

2002

2012

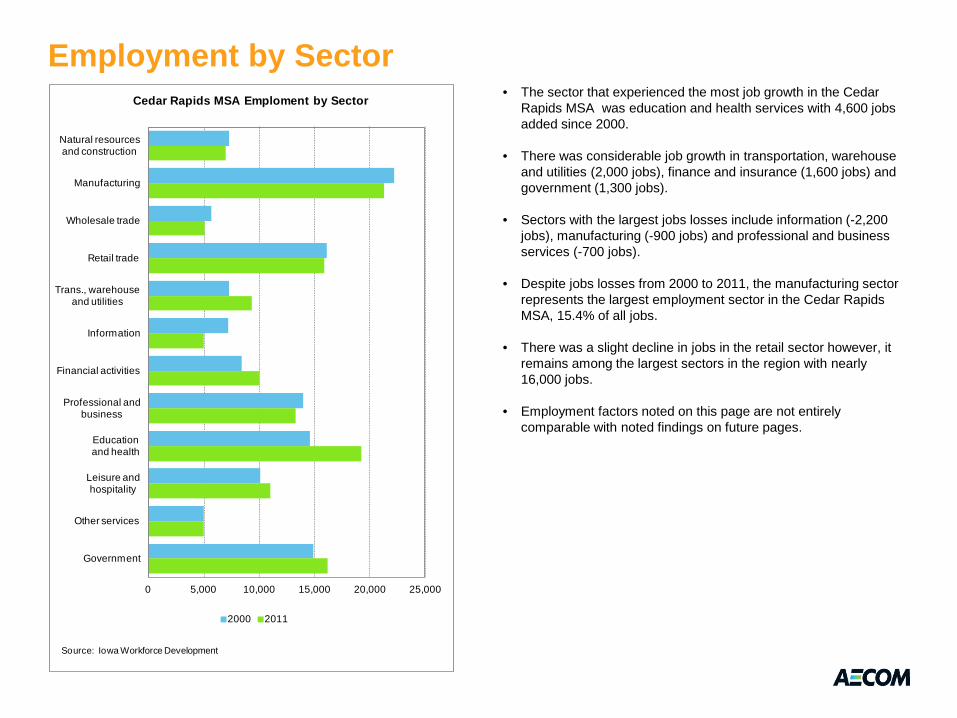

Employment by Sector • The sector that experienced the most job growth in the Cedar

Rapids MSA was education and health services with 4,600 jobs added since 2000.

• There was considerable job growth in transportation, warehouse and utilities (2,000 jobs), finance and insurance (1,600 jobs) and government (1,300 jobs).

• Sectors with the largest jobs losses include information (-2,200 jobs), manufacturing (-900 jobs) and professional and business services (-700 jobs).

• Despite jobs losses from 2000 to 2011, the manufacturing sector represents the largest employment sector in the Cedar Rapids MSA, 15.4% of all jobs.

• There was a slight decline in jobs in the retail sector however, it remains among the largest sectors in the region with nearly 16,000 jobs.

• Employment factors noted on this page are not entirely comparable with noted findings on future pages.

0 5,000 10,000 15,000 20,000 25,000

Natural resources and construction

Manufacturing

Wholesale trade

Retail trade

Trans., warehouse and utilities

Information

Financial activities

Professional and business

Education and health

Leisure and hospitality

Other services

Government

Source: Iowa Workforce Development

Cedar Rapids MSA Emploment by Sector

2000 2011

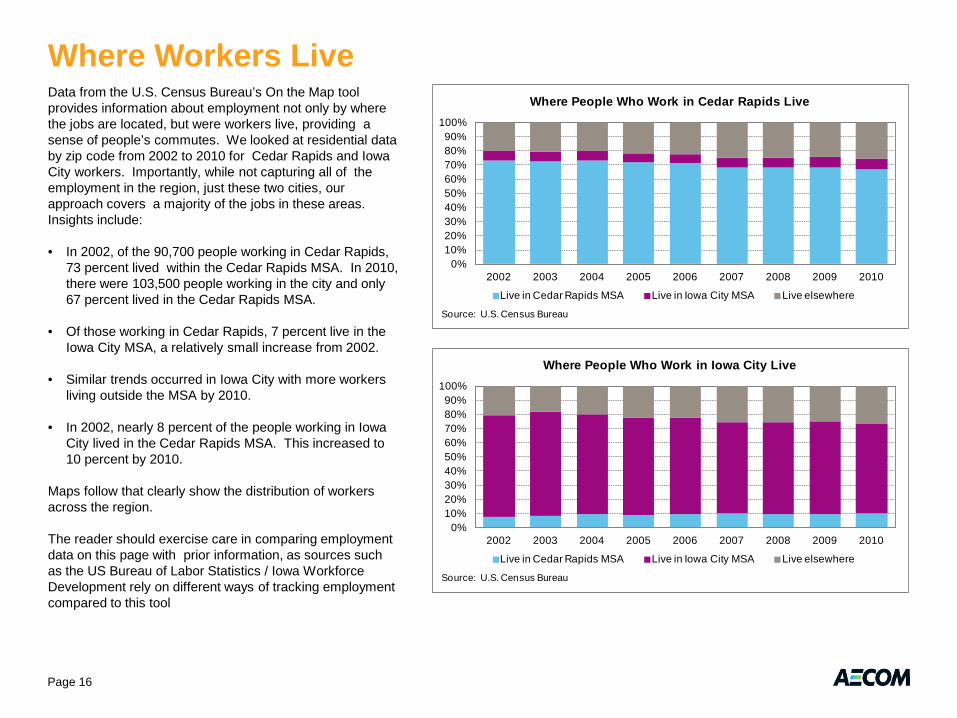

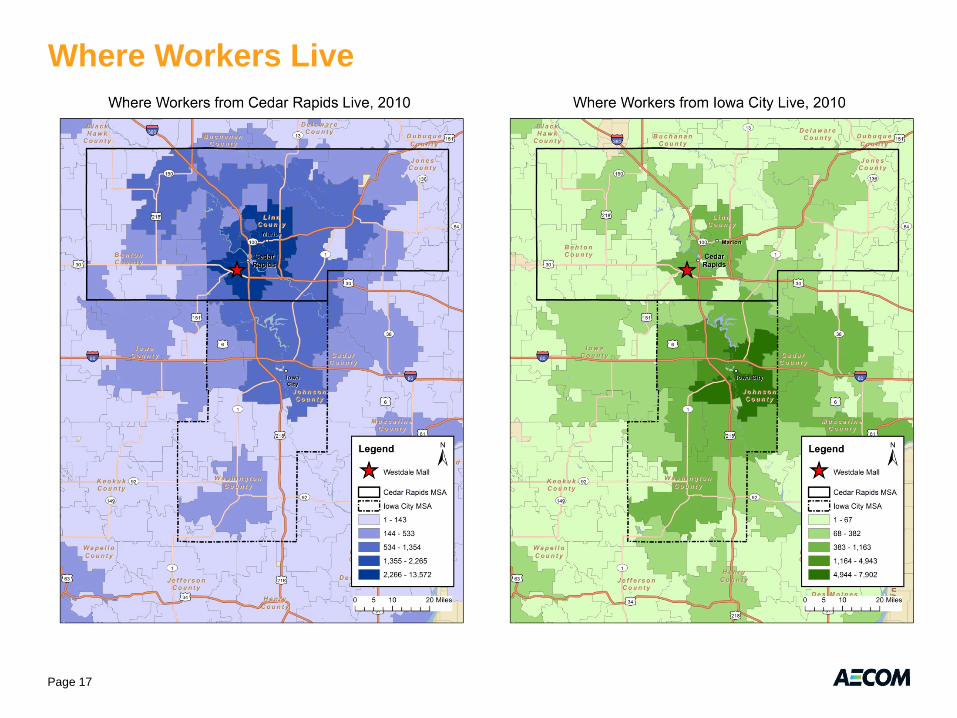

Where Workers Live Data from the U.S. Census Bureau’s On the Map tool provides information about employment not only by where the jobs are located, but were workers live, providing a sense of people’s commutes. We looked at residential data by zip code from 2002 to 2010 for Cedar Rapids and Iowa City workers. Importantly, while not capturing all of the employment in the region, just these two cities, our approach covers a majority of the jobs in these areas. Insights include:

• In 2002, of the 90,700 people working in Cedar Rapids, 73 percent lived within the Cedar Rapids MSA. In 2010, there were 103,500 people working in the city and only 67 percent lived in the Cedar Rapids MSA.

• Of those working in Cedar Rapids, 7 percent live in the Iowa City MSA, a relatively small increase from 2002.

• Similar trends occurred in Iowa City with more workers living outside the MSA by 2010.

• In 2002, nearly 8 percent of the people working in Iowa City lived in the Cedar Rapids MSA. This increased to 10 percent by 2010.

Maps follow that clearly show the distribution of workers across the region.

The reader should exercise care in comparing employment data on this page with prior information, as sources such as the US Bureau of Labor Statistics / Iowa Workforce Development rely on different ways of tracking employment compared to this tool

0%10%20%30%40%50%60%70%80%90%

100%

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: U.S. Census Bureau

Where People Who Work in Cedar Rapids Live

Live in Cedar Rapids MSA Live in Iowa City MSA Live elsewhere

0%10%20%30%40%50%60%70%80%90%

100%

2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: U.S. Census Bureau

Where People Who Work in Iowa City Live

Live in Cedar Rapids MSA Live in Iowa City MSA Live elsewhere

Page 16

Where Workers Live

Page 17

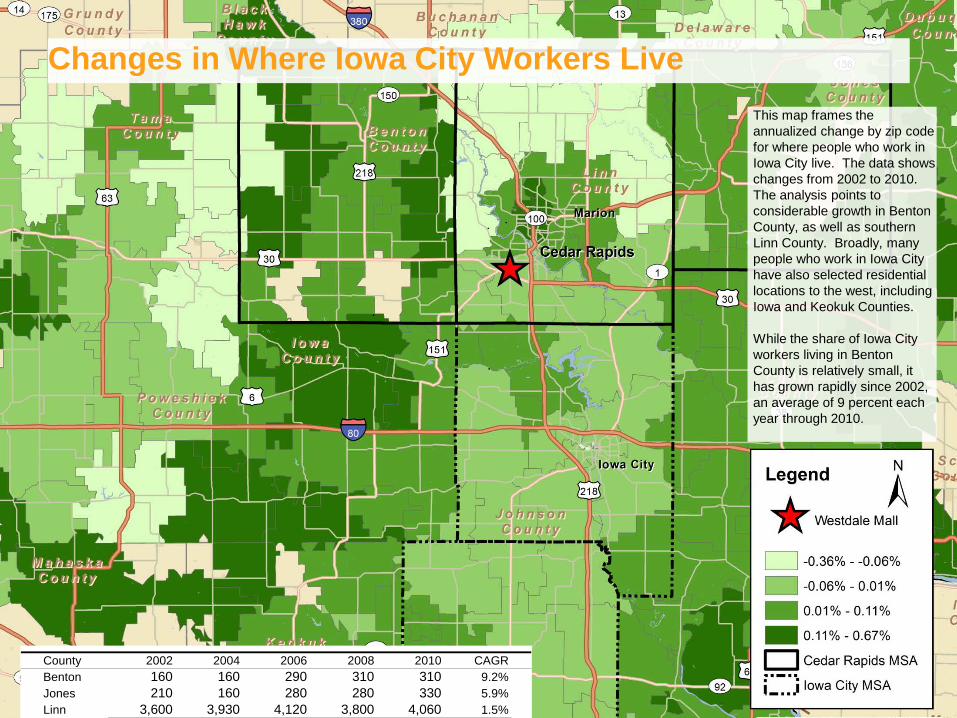

Changes in Where Iowa City Workers Live This map frames the annualized change by zip code for where people who work in Iowa City live. The data shows changes from 2002 to 2010. The analysis points to considerable growth in Benton County, as well as southern Linn County. Broadly, many people who work in Iowa City have also selected residential locations to the west, including Iowa and Keokuk Counties.

While the share of Iowa City workers living in Benton County is relatively small, it has grown rapidly since 2002, an average of 9 percent each year through 2010.

County 2002 2004 2006 2008 2010 CAGRBenton 160 160 290 310 310 9.2%Jones 210 160 280 280 330 5.9%Linn 3,600 3,930 4,120 3,800 4,060 1.5%

Economic / Demographic Findings

Page 19

Findings build from the conclusion that the Cedar Rapids Area, much like the entire state of Iowa, has an established tradition of steady growth, and low unemployment, while avoiding the economic peaks and valleys experienced by other regions. Findings include:

• Rates of employment growth for the Cedar Rapids Metropolitan Statistical Area (MSA) compare favorably with statewide benchmarks. Unemployment rates remain enviably below Midwestern peers.

• Although the recession did not hit Cedar Rapids with an intensity seen elsewhere in the Midwest, the region’s pace of job recovery since 2010 is lagging compared to other Iowa metros. Returning to pre-recession growth rates would suggest an increase to 1,900 new jobs per year, versus the current pace of about 900-1,000 jobs per year.

• The Cedar Rapids Area draws notable strength from a local manufacturing sector which has remained quite resilient comparison with broader declines in manufacturing which have occurred across the Midwest. When combined with other sectors such as health care, it is apparent that the local economy is driven to a relevant extent by private sector activity, which is significant.

• Rockwell Collins is a major regional employer, with a particular concentration of owned and leased space on the NE side of Cedar Rapids. Although they are a diversified aerospace company, concerns about federal spending reductions should be of concern locally over the next 24 months.

• Although Cedar Rapids and Iowa City are defined as separate Metropolitan Statistical Areas by the US Census, interviews reinforce the sense that these two regions are growing closer together economically. US Census data shows that an increasing

number of people who work in Iowa City choose to live in Linn County. For this reason, our study is also presumes a stronger economic “pull” for Cedar Rapids to the south over the long-term, placing the Westdale site in a more favorable regional location.

• A combined Iowa City and Cedar Rapids market is consequential in size, with about 411,000 residents through 2010. While the Cedar Rapids MSA represents 60% of this larger market, the Iowa City MSA growth rate is stronger (1.5% versus 0.8% annually).

• Local voters recently approve a referendum for a new casino in Cedar Rapids, which lays the groundwork for a formal application to the Iowa Gaming Commission. A downtown location appears to be likely. As casinos typically include restaurant and entertainment elements, the evolving nature of this program will need to be monitored in relation to Westdale.

• The flood had a major impact on neighborhoods in and around downtown with a total of about 5,000 housing units that were damaged. Since the flood, City officials indicated that roughly 3,500 have been renovated. Broader Corps of Engineers decision-making regarding flood protection remains a major element, with clearer plans to protect the eastern side of the river. Flood protection for the western side of the river remains in debate locally.

• Further reinforcing the generally positive economic performance for the region, we noted that Eastern Iowa Airport supported about 492,260 enplaned passengers in 2012, an increase of about 30,000 passengers over 2010 levels, reflective of annual growth of about 2%.

Retail Market Analysis Introduction

The Retail Market Analysis folds in several overlapping components:

• Summary of national retail sales trends which have implications for the local market, particularly the impact of internet spending

• Discussion of trends regarding national chains that are expanding or closing stores

• Analysis of local trade area demographics in the Cedar Rapids area

• Review taxable retail sales for Cedar Rapids and Iowa City compared to statewide metrics

• Assessment of retail inventories and vacancy

• Demand and supply implications for Westdale

Page 20

Retail – National Perspective

Page 21

11.3%

2.6%

12.7%

3.5%

8.0%

7.0%

2.8%

15.3%

18.4%

2.9%

6.9%

8.5%

2.8%

3.4%

5.5%

3.9%

6.2%

14.4%

3.6%

14.1%

25.7%

3.0%

8.3%

9.1%

Warehouse clubs and superstores

Sporting goods, hobby, book, and musicstores

Nonstore retailers

Miscellaneous store retailers

Health and personal care stores

General merchandise stores

Furniture, home furnishings, electronicsand appliance stores

Food services and drinking places

Food and beverage stores

Electronics and appliance stores

Clothing and clothing access. stores

Building mat. and garden equip. andsupplies

Source: U.S. Census Bureau

Comparison of Retail Sales, Percentage of Total, By Year, 192 and 2012

1992 2012

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Source: U.S. Census Bureau

Retail Sales Per Person, Noted Years

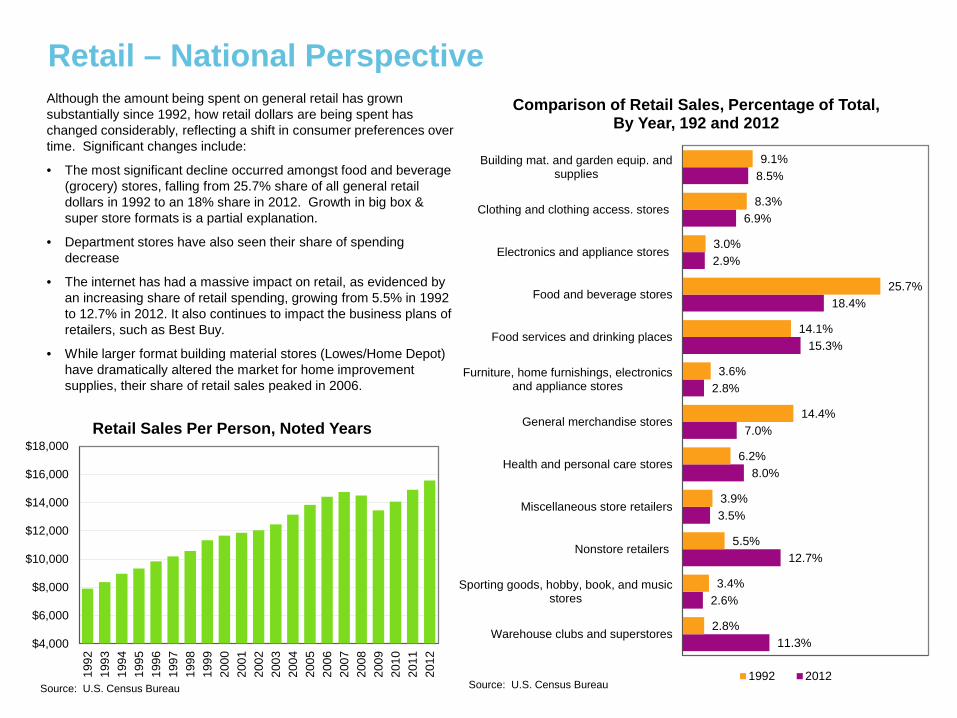

Although the amount being spent on general retail has grown substantially since 1992, how retail dollars are being spent has changed considerably, reflecting a shift in consumer preferences over time. Significant changes include:

• The most significant decline occurred amongst food and beverage (grocery) stores, falling from 25.7% share of all general retail dollars in 1992 to an 18% share in 2012. Growth in big box & super store formats is a partial explanation.

• Department stores have also seen their share of spending decrease

• The internet has had a massive impact on retail, as evidenced by an increasing share of retail spending, growing from 5.5% in 1992 to 12.7% in 2012. It also continues to impact the business plans of retailers, such as Best Buy.

• While larger format building material stores (Lowes/Home Depot) have dramatically altered the market for home improvement supplies, their share of retail sales peaked in 2006.

Retail – National Trends

Page 22

Overall Sales Trajectory • Retail sales spending increased 1.1 percent in February 2013

compared to the previous month. Even after excluding gas, autos and building supply, core retail sales rose 0.4 percent. January sales had been better than expected as well. While two months do not make a trend, 2013 Q1 may perform better than expected in spite of higher taxes and gasoline prices.

• The impact of Federal sequestration and any future changes resulting from Federal budget cuts are still unclear.

• Younger adults are still living at home waiting for the economic recovery to be sustaining. Retail sales depend on household growth and new household formation according to a life cycle pattern. The “normal” pattern has been disrupted due to the “Great Recession”. With small improvements in jobs creation, retail sales will rise.

• Starbucks and Dunkin Donut have announced expansion plans, while others have announced cutbacks. Without solid evidence of consumer demand growth demonstrated by increasing sales, most chains will be slow to grow locations, even as under performing stores are closed.

• Large format retailers continue to look for more market share in saturated areas. Wal-Mart has announced plans to add 115 new outlets at less than 60,000 square feet to put it in position to compete with Dollar General, Walgreens and supermarkets in locations that would not support a superstore format. Wal-Mart will be using its Neighborhood Markets format to compete in smaller towns, its Mercado de Wal-Mart in Hispanic communities and a smaller Wal-Mart on Campus format.

• As a result of the continuing growth of online sales, smart phone ownership and social media, retailers as diverse as Macys, Nordstrom, Saks, Walgreens and Target are using an “omni-channel” strategy in response to the growth of mobile technology and consumer demand for convenience. Omni-channeling presents

a seamless experience model that delivers a consistent shopping experience across all customer touch points.

• Pressure has been growing on Congress to address the sales tax exemption for interstate online retail sales. State and local governments, joined by some business interests, are pressing for the sales tax issue to be addressed as tax receipts for retail sales continue to drop due to the growth of online shopping..

Retail Sector Perspectives

• Spending at health and personal-care stores dropped 0.9% in 2012, perhaps as a function of heavy discounting to increase sales and traffic volume. The industry seems to struggle to increase sales and revenues.

• Chain pharmacies see retail clinics as a way to drive traffic into stores. Visits to retail clinics increased four times from 2007 to 2009. Retail clinic performance varies greatly from chain-to-chain. CVS-owned Minute Clinics represent the most growth in the in-store clinic business, with about 550 locations. Minute Clinics and Walgreens’ Take Care Clinics, with 355 locations, represent two-out-of-three retail clinics in the U.S.

• With the announced merger of Office Depot and OfficeMax, the office supply business will change. The combined business should be in a more competitive position versus sector leader Staples. Both chains had been closing locations already; as the store territories overlap by about 50 percent, additional stores are expected to close. The office supply sector has become a cost-driven commodity business. Linking online sales to in-store, contract sales, and a high sales volume/low costs approach now define success in this sector.

• The Ascena Retail Group’s Fashion Bug women’s apparel stores final 432 closings will happen in 2013. The group will focus on the Lane Bryant and Catherines Plus Sizes stores.

Retail – National Trends

Page 23

Retail Sector Perspectives

• There is considerable consolidation among U.S. apparel retailers in response to weaker sales . Abercrombie & Fitch closed 180 of its under-performing stores in lower tier cities. American Eagle Outfitters and Limited Brands are pursuing a similar strategy.

• Fashion retailer H&M continues its aggressive expansion in the U.S. Currently, the chain has about 200 stores in 30 states and plans to add 325 in beginning 2013. The chain has expanded to the Midwest in the past few years with stores in Illinois, Minnesota and Wisconsin, but has yet to open a store in Iowa.

• JC Penney continues to try to revamp itself through its “shops” merchandising and pricing strategies. The most recent announcement of the introduction of the Canadian Joe Fresh fashion line is an attempt to compete in the “Fast Fashion” approach taken by European retailers Zara and H&M. Penney’s has announced it will roll out the new line in its bigger and more trafficked stores. If successful, this move could help JC Penney re-establish itself as a poplar price point apparel retailer; if unsuccessful, expect more closings to follow.

• Gymboree’s children’s apparel store Crazy 8 has announced plans to open 90 new outlets in 2013. Crazy 8 is already in Iowa with two stores.

• Other stores with significant expansion plans in 2013 include Dollar General, Subway, Five Guys, Pizza Hut, Family Dollar, CVS, Chipotle, Ace Hardware, H&M, and Starbucks.

• According to CoStar, only one traditional enclosed mall has been built since 2006. Malls are physically changing to new formats – “inside-out” with retailers facing outside rather than inward; non-retail uses such as educational and health care; “exploded” formats that reopen the center promenades and courtyards and converting them to Main Street-styles with parking.

• Simon Property is remodeling 15 to 20 malls a year, adding such amenities as electric-car charging stations and stadium-seating theaters. Mega-churches have taken over former anchor spaces.

Restaurant Sector Perspectives • Starbucks has announced major expansion in the U.S., including

adding or expanding 900 drive-through locations over the next five years. Dunkin Donuts plans to add 330-360 total stores in 2013.

• Bob Evans Farms Inc. has sold its Mimi’s Cafe chain to Le Duff America Inc.; Ignite Restaurant Group Inc. acquired Romano’s Macaroni Grill from Golden Gate Capital; and Landry’s Inc. is trying to acquire Ark Restaurants Corp.

• Fast Casual restaurants make up 27.25% of total food service sales. Limited-service restaurants are estimated at $173.8 billion in annual sales (NRA).

• 5 Guys Burgers, Jimmy John’s, Chipotle Mexican Grill, BJs Restaurant & Brewery and Cheddar’s are the top five chains in sales growth in the US.

• Reduced household spending and changing eating habits continue to hurt fine dining. Full-service restaurants saw sales growth last year of 8.1 percent. Most of the shift in sales has been to Quick Service.

• A growing emphasis on Asian food bodes well for restaurants with a pan-Asian orientation such as Pei-Wei Asian Diner (owned by P.F. Chang).

• Many restaurants focus on Millenials, but it's their slower income rise has caused cutbacks in food away spending.

• Baby Boomers continue to work longer, aren’t cutting back as much and have a greater need for convenience.

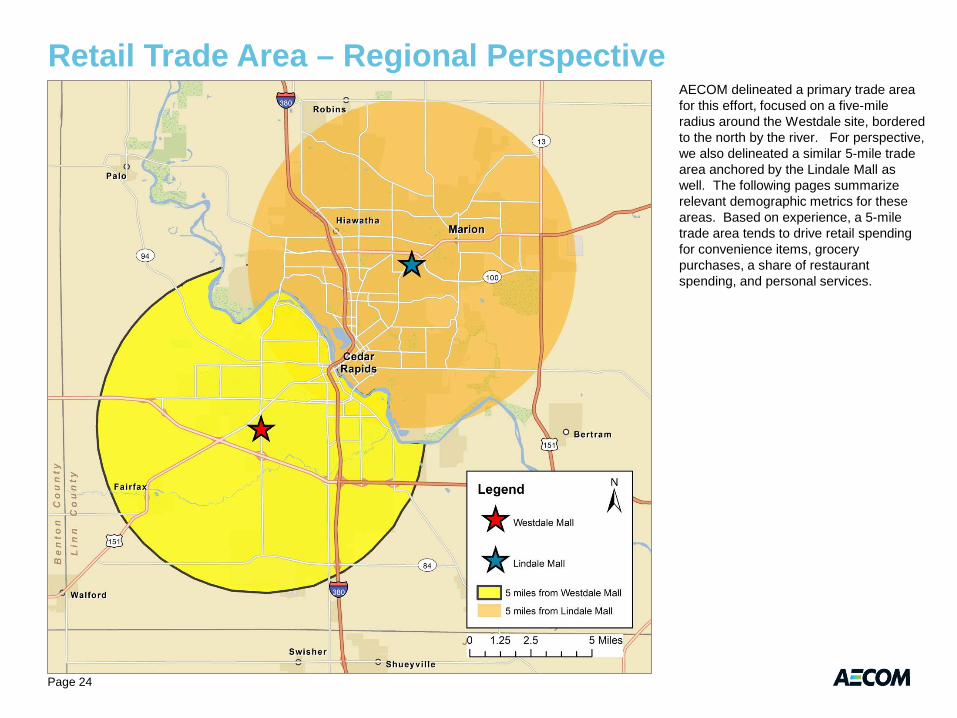

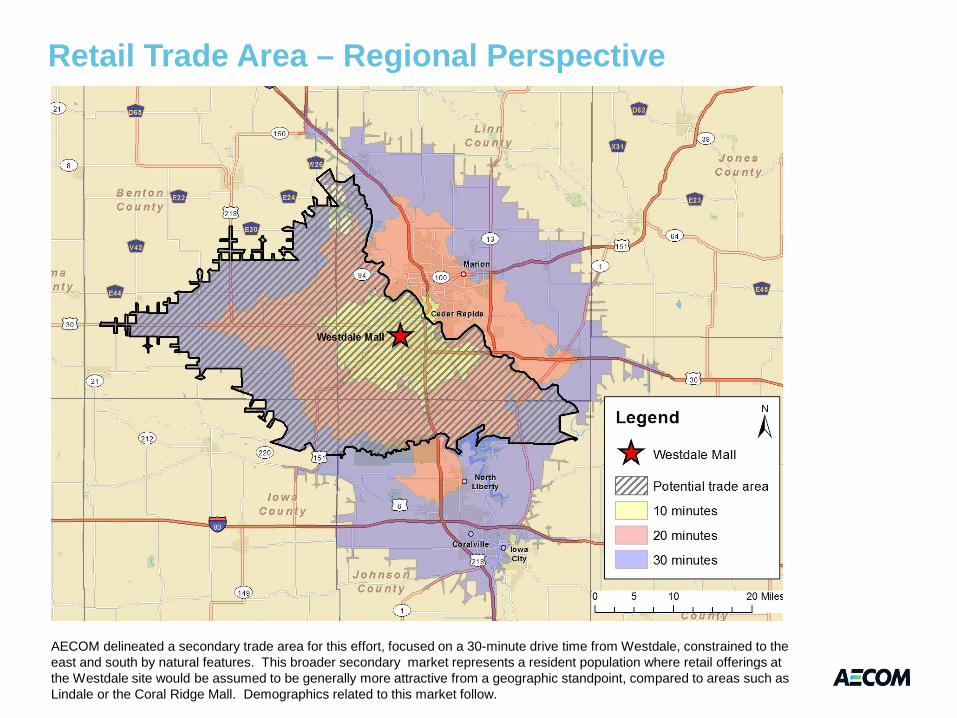

Retail Trade Area – Regional Perspective

Page 24

AECOM delineated a primary trade area for this effort, focused on a five-mile radius around the Westdale site, bordered to the north by the river. For perspective, we also delineated a similar 5-mile trade area anchored by the Lindale Mall as well. The following pages summarize relevant demographic metrics for these areas. Based on experience, a 5-mile trade area tends to drive retail spending for convenience items, grocery purchases, a share of restaurant spending, and personal services.

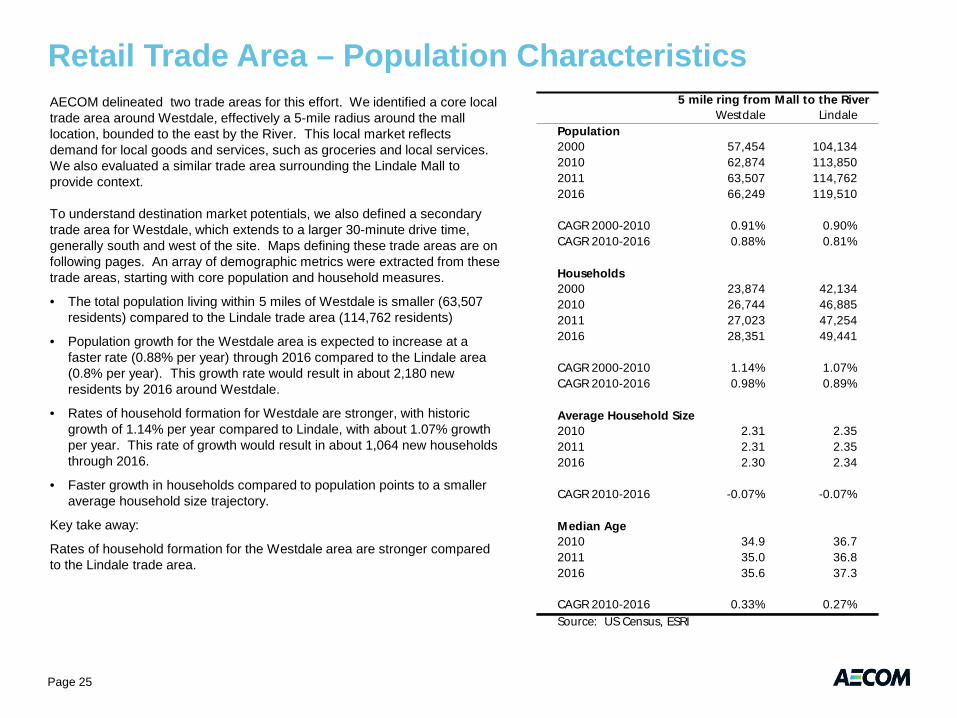

Retail Trade Area – Population Characteristics AECOM delineated two trade areas for this effort. We identified a core local trade area around Westdale, effectively a 5-mile radius around the mall location, bounded to the east by the River. This local market reflects demand for local goods and services, such as groceries and local services. We also evaluated a similar trade area surrounding the Lindale Mall to provide context.

To understand destination market potentials, we also defined a secondary trade area for Westdale, which extends to a larger 30-minute drive time, generally south and west of the site. Maps defining these trade areas are on following pages. An array of demographic metrics were extracted from these trade areas, starting with core population and household measures.

• The total population living within 5 miles of Westdale is smaller (63,507 residents) compared to the Lindale trade area (114,762 residents)

• Population growth for the Westdale area is expected to increase at a faster rate (0.88% per year) through 2016 compared to the Lindale area (0.8% per year). This growth rate would result in about 2,180 new residents by 2016 around Westdale.

• Rates of household formation for Westdale are stronger, with historic growth of 1.14% per year compared to Lindale, with about 1.07% growth per year. This rate of growth would result in about 1,064 new households through 2016.

• Faster growth in households compared to population points to a smaller average household size trajectory.

Key take away:

Rates of household formation for the Westdale area are stronger compared to the Lindale trade area.

5 mile ring from Mall to the RiverWestdale Lindale

Population2000 57,454 104,1342010 62,874 113,8502011 63,507 114,7622016 66,249 119,510

CAGR 2000-2010 0.91% 0.90%CAGR 2010-2016 0.88% 0.81%

Households2000 23,874 42,1342010 26,744 46,8852011 27,023 47,2542016 28,351 49,441

CAGR 2000-2010 1.14% 1.07%CAGR 2010-2016 0.98% 0.89%

Average Household Size2010 2.31 2.352011 2.31 2.352016 2.30 2.34

CAGR 2010-2016 -0.07% -0.07%

Median Age2010 34.9 36.72011 35.0 36.82016 35.6 37.3

CAGR 2010-2016 0.33% 0.27%Source: US Census, ESRI

Page 25

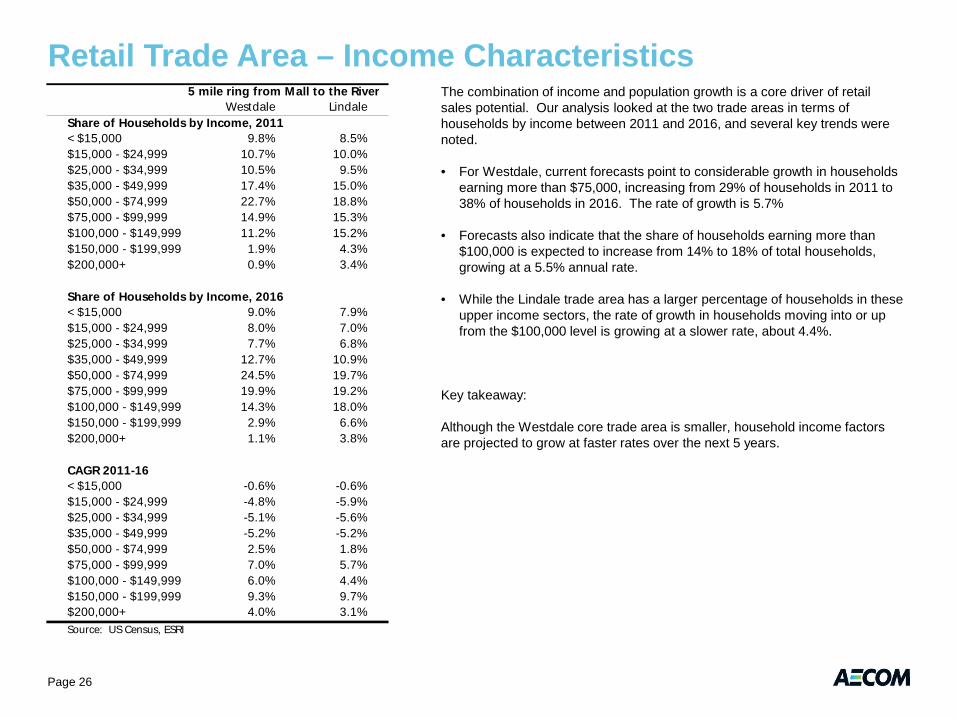

5 mile ring from Mall to the RiverWestdale Lindale

Share of Households by Income, 2011< $15,000 9.8% 8.5%$15,000 - $24,999 10.7% 10.0%$25,000 - $34,999 10.5% 9.5%$35,000 - $49,999 17.4% 15.0%$50,000 - $74,999 22.7% 18.8%$75,000 - $99,999 14.9% 15.3%$100,000 - $149,999 11.2% 15.2%$150,000 - $199,999 1.9% 4.3%$200,000+ 0.9% 3.4%

Share of Households by Income, 2016< $15,000 9.0% 7.9%$15,000 - $24,999 8.0% 7.0%$25,000 - $34,999 7.7% 6.8%$35,000 - $49,999 12.7% 10.9%$50,000 - $74,999 24.5% 19.7%$75,000 - $99,999 19.9% 19.2%$100,000 - $149,999 14.3% 18.0%$150,000 - $199,999 2.9% 6.6%$200,000+ 1.1% 3.8%

CAGR 2011-16< $15,000 -0.6% -0.6%$15,000 - $24,999 -4.8% -5.9%$25,000 - $34,999 -5.1% -5.6%$35,000 - $49,999 -5.2% -5.2%$50,000 - $74,999 2.5% 1.8%$75,000 - $99,999 7.0% 5.7%$100,000 - $149,999 6.0% 4.4%$150,000 - $199,999 9.3% 9.7%$200,000+ 4.0% 3.1%Source: US Census, ESRI

Retail Trade Area – Income Characteristics The combination of income and population growth is a core driver of retail sales potential. Our analysis looked at the two trade areas in terms of households by income between 2011 and 2016, and several key trends were noted.

• For Westdale, current forecasts point to considerable growth in households earning more than $75,000, increasing from 29% of households in 2011 to 38% of households in 2016. The rate of growth is 5.7%

• Forecasts also indicate that the share of households earning more than $100,000 is expected to increase from 14% to 18% of total households, growing at a 5.5% annual rate.

• While the Lindale trade area has a larger percentage of households in these upper income sectors, the rate of growth in households moving into or up from the $100,000 level is growing at a slower rate, about 4.4%.

Key takeaway:

Although the Westdale core trade area is smaller, household income factors are projected to grow at faster rates over the next 5 years.

Page 26

Retail Trade Area – Regional Perspective

AECOM delineated a secondary trade area for this effort, focused on a 30-minute drive time from Westdale, constrained to the east and south by natural features. This broader secondary market represents a resident population where retail offerings at the Westdale site would be assumed to be generally more attractive from a geographic standpoint, compared to areas such as Lindale or the Coral Ridge Mall. Demographics related to this market follow.

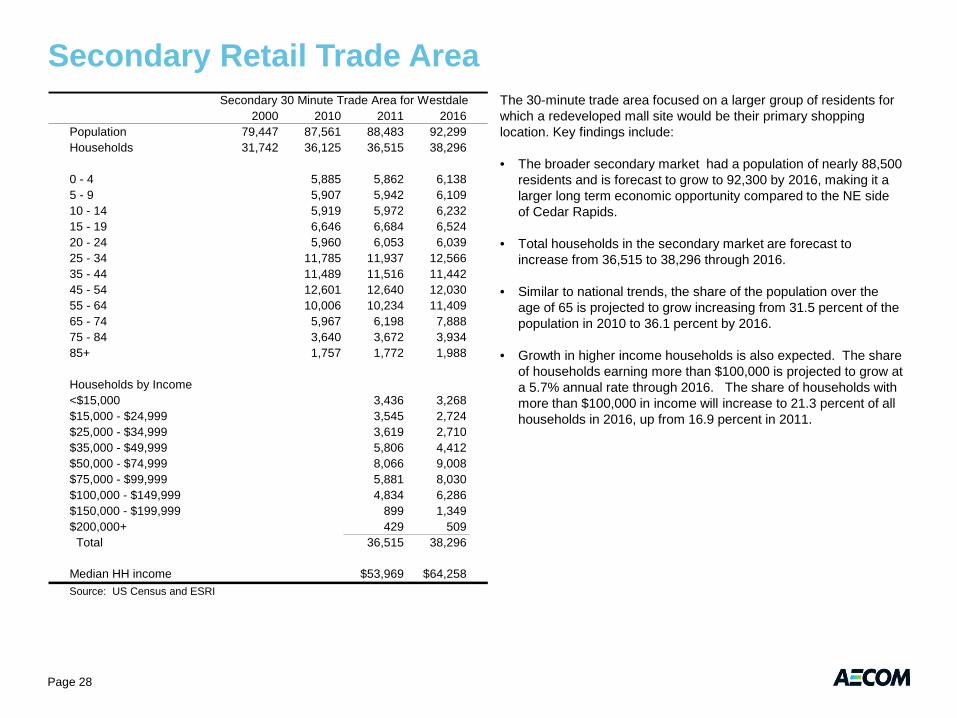

Secondary Retail Trade Area The 30-minute trade area focused on a larger group of residents for which a redeveloped mall site would be their primary shopping location. Key findings include:

• The broader secondary market had a population of nearly 88,500 residents and is forecast to grow to 92,300 by 2016, making it a larger long term economic opportunity compared to the NE side of Cedar Rapids.

• Total households in the secondary market are forecast to increase from 36,515 to 38,296 through 2016.

• Similar to national trends, the share of the population over the age of 65 is projected to grow increasing from 31.5 percent of the population in 2010 to 36.1 percent by 2016.

• Growth in higher income households is also expected. The share of households earning more than $100,000 is projected to grow at a 5.7% annual rate through 2016. The share of households with more than $100,000 in income will increase to 21.3 percent of all households in 2016, up from 16.9 percent in 2011.

2000 2010 2011 2016Population 79,447 87,561 88,483 92,299Households 31,742 36,125 36,515 38,296

0 - 4 5,885 5,862 6,1385 - 9 5,907 5,942 6,10910 - 14 5,919 5,972 6,23215 - 19 6,646 6,684 6,52420 - 24 5,960 6,053 6,03925 - 34 11,785 11,937 12,56635 - 44 11,489 11,516 11,44245 - 54 12,601 12,640 12,03055 - 64 10,006 10,234 11,40965 - 74 5,967 6,198 7,88875 - 84 3,640 3,672 3,93485+ 1,757 1,772 1,988

Households by Income<$15,000 3,436 3,268$15,000 - $24,999 3,545 2,724$25,000 - $34,999 3,619 2,710$35,000 - $49,999 5,806 4,412$50,000 - $74,999 8,066 9,008$75,000 - $99,999 5,881 8,030$100,000 - $149,999 4,834 6,286$150,000 - $199,999 899 1,349$200,000+ 429 509 Total 36,515 38,296

Median HH income $53,969 $64,258Source: US Census and ESRI

Secondary 30 Minute Trade Area for Westdale

Page 28

-4%

-2%

0%

2%

4%

6%

8%

Apparel Buildingmaterials

Eating and

drinking

Food dealers

General merch.

Home furn.

Service Specialty retail

Source: Iowa DOR

Percent Change in Retail Sales by Store Type, 2010 to 2012

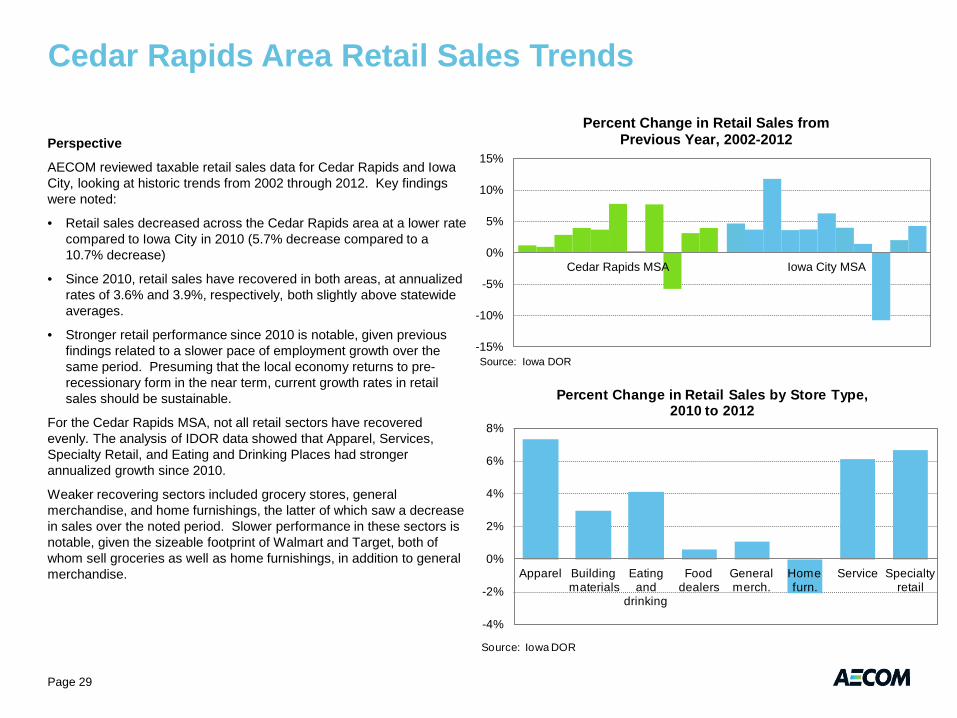

Cedar Rapids Area Retail Sales Trends

Page 29

Perspective

AECOM reviewed taxable retail sales data for Cedar Rapids and Iowa City, looking at historic trends from 2002 through 2012. Key findings were noted:

• Retail sales decreased across the Cedar Rapids area at a lower rate compared to Iowa City in 2010 (5.7% decrease compared to a 10.7% decrease)

• Since 2010, retail sales have recovered in both areas, at annualized rates of 3.6% and 3.9%, respectively, both slightly above statewide averages.

• Stronger retail performance since 2010 is notable, given previous findings related to a slower pace of employment growth over the same period. Presuming that the local economy returns to pre-recessionary form in the near term, current growth rates in retail sales should be sustainable.

For the Cedar Rapids MSA, not all retail sectors have recovered evenly. The analysis of IDOR data showed that Apparel, Services, Specialty Retail, and Eating and Drinking Places had stronger annualized growth since 2010.

Weaker recovering sectors included grocery stores, general merchandise, and home furnishings, the latter of which saw a decrease in sales over the noted period. Slower performance in these sectors is notable, given the sizeable footprint of Walmart and Target, both of whom sell groceries as well as home furnishings, in addition to general merchandise.

-15%

-10%

-5%

0%

5%

10%

15%

Cedar Rapids MSA Iowa City MSA

Source: Iowa DOR

Percent Change in Retail Sales from Previous Year, 2002-2012

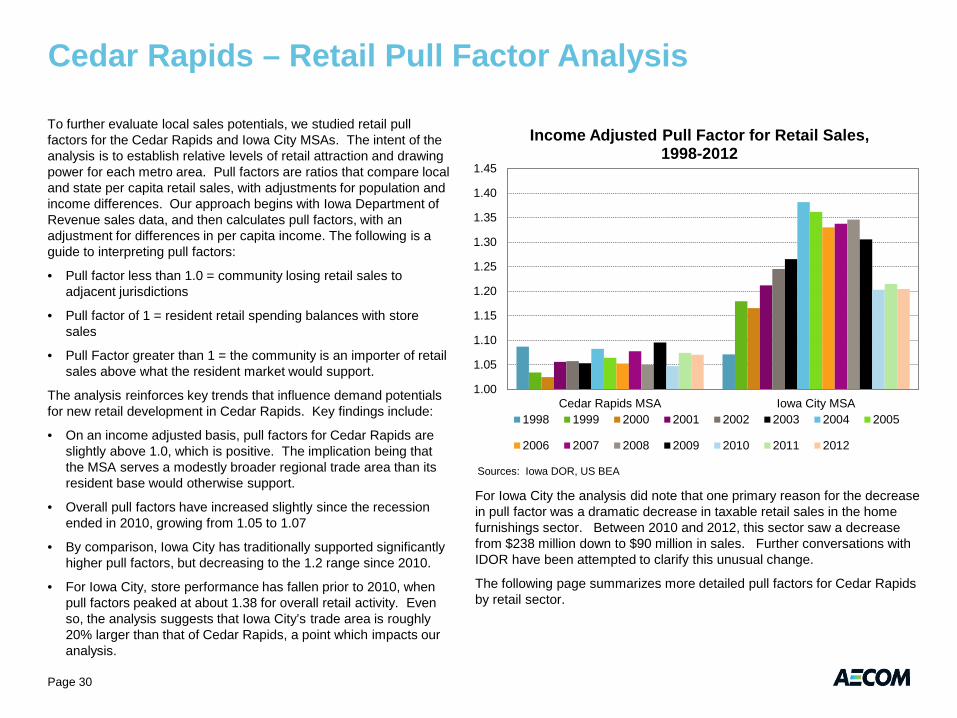

Cedar Rapids – Retail Pull Factor Analysis

Page 30

To further evaluate local sales potentials, we studied retail pull factors for the Cedar Rapids and Iowa City MSAs. The intent of the analysis is to establish relative levels of retail attraction and drawing power for each metro area. Pull factors are ratios that compare local and state per capita retail sales, with adjustments for population and income differences. Our approach begins with Iowa Department of Revenue sales data, and then calculates pull factors, with an adjustment for differences in per capita income. The following is a guide to interpreting pull factors:

• Pull factor less than 1.0 = community losing retail sales to adjacent jurisdictions

• Pull factor of 1 = resident retail spending balances with store sales

• Pull Factor greater than 1 = the community is an importer of retail sales above what the resident market would support.

The analysis reinforces key trends that influence demand potentials for new retail development in Cedar Rapids. Key findings include:

• On an income adjusted basis, pull factors for Cedar Rapids are slightly above 1.0, which is positive. The implication being that the MSA serves a modestly broader regional trade area than its resident base would otherwise support.

• Overall pull factors have increased slightly since the recession ended in 2010, growing from 1.05 to 1.07

• By comparison, Iowa City has traditionally supported significantly higher pull factors, but decreasing to the 1.2 range since 2010.

• For Iowa City, store performance has fallen prior to 2010, when pull factors peaked at about 1.38 for overall retail activity. Even so, the analysis suggests that Iowa City’s trade area is roughly 20% larger than that of Cedar Rapids, a point which impacts our analysis.

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

Cedar Rapids MSA Iowa City MSA

Sources: Iowa DOR, US BEA

Income Adjusted Pull Factor for Retail Sales, 1998-2012

1998 1999 2000 2001 2002 2003 2004 2005

2006 2007 2008 2009 2010 2011 2012

For Iowa City the analysis did note that one primary reason for the decrease in pull factor was a dramatic decrease in taxable retail sales in the home furnishings sector. Between 2010 and 2012, this sector saw a decrease from $238 million down to $90 million in sales. Further conversations with IDOR have been attempted to clarify this unusual change.

The following page summarizes more detailed pull factors for Cedar Rapids by retail sector.

Cedar Rapids – Retail Pull Factor Analysis

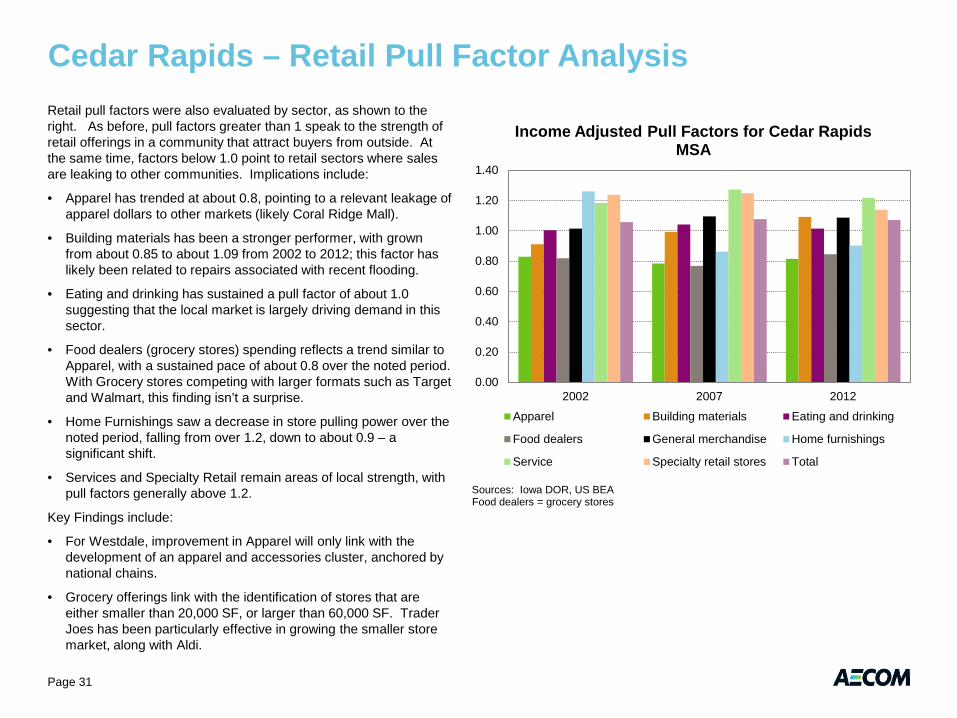

Page 31

Retail pull factors were also evaluated by sector, as shown to the right. As before, pull factors greater than 1 speak to the strength of retail offerings in a community that attract buyers from outside. At the same time, factors below 1.0 point to retail sectors where sales are leaking to other communities. Implications include:

• Apparel has trended at about 0.8, pointing to a relevant leakage of apparel dollars to other markets (likely Coral Ridge Mall).

• Building materials has been a stronger performer, with grown from about 0.85 to about 1.09 from 2002 to 2012; this factor has likely been related to repairs associated with recent flooding.

• Eating and drinking has sustained a pull factor of about 1.0 suggesting that the local market is largely driving demand in this sector.

• Food dealers (grocery stores) spending reflects a trend similar to Apparel, with a sustained pace of about 0.8 over the noted period. With Grocery stores competing with larger formats such as Target and Walmart, this finding isn’t a surprise.

• Home Furnishings saw a decrease in store pulling power over the noted period, falling from over 1.2, down to about 0.9 – a significant shift.

• Services and Specialty Retail remain areas of local strength, with pull factors generally above 1.2.

Key Findings include:

• For Westdale, improvement in Apparel will only link with the development of an apparel and accessories cluster, anchored by national chains.

• Grocery offerings link with the identification of stores that are either smaller than 20,000 SF, or larger than 60,000 SF. Trader Joes has been particularly effective in growing the smaller store market, along with Aldi.

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2002 2007 2012

Sources: Iowa DOR, US BEA Food dealers = grocery stores

Income Adjusted Pull Factors for Cedar Rapids MSA

Apparel Building materials Eating and drinking

Food dealers General merchandise Home furnishings

Service Specialty retail stores Total

Cedar Rapids Retail Perspective

Page 32

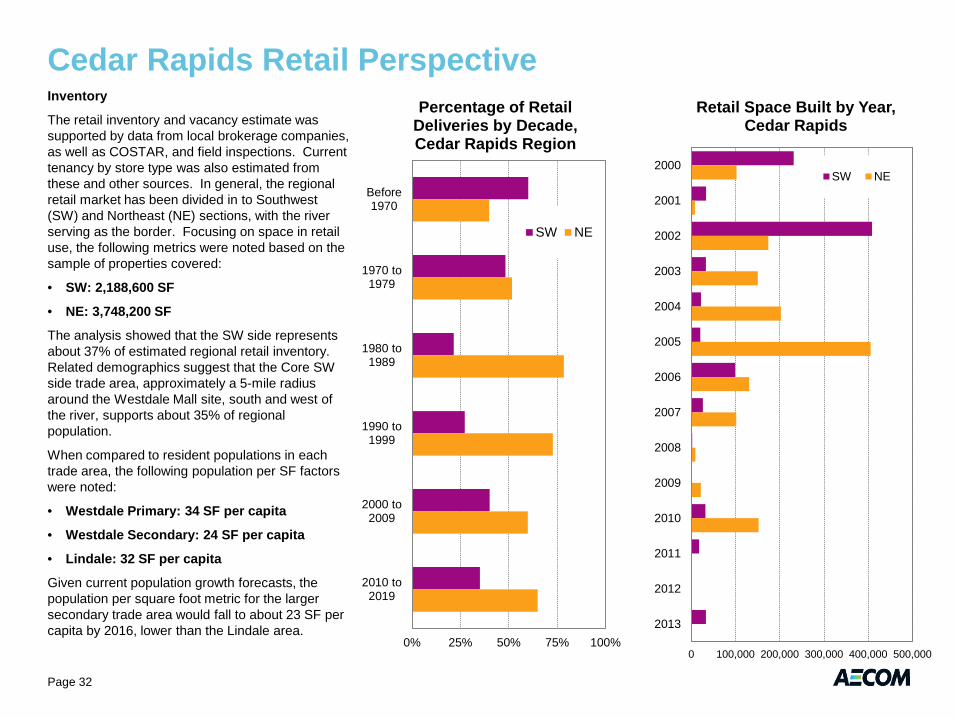

Inventory

The retail inventory and vacancy estimate was supported by data from local brokerage companies, as well as COSTAR, and field inspections. Current tenancy by store type was also estimated from these and other sources. In general, the regional retail market has been divided in to Southwest (SW) and Northeast (NE) sections, with the river serving as the border. Focusing on space in retail use, the following metrics were noted based on the sample of properties covered:

• SW: 2,188,600 SF

• NE: 3,748,200 SF

The analysis showed that the SW side represents about 37% of estimated regional retail inventory. Related demographics suggest that the Core SW side trade area, approximately a 5-mile radius around the Westdale Mall site, south and west of the river, supports about 35% of regional population.

When compared to resident populations in each trade area, the following population per SF factors were noted:

• Westdale Primary: 34 SF per capita

• Westdale Secondary: 24 SF per capita

• Lindale: 32 SF per capita

Given current population growth forecasts, the population per square foot metric for the larger secondary trade area would fall to about 23 SF per capita by 2016, lower than the Lindale area.

0% 25% 50% 75% 100%

Before1970

1970 to1979

1980 to1989

1990 to1999

2000 to2009

2010 to2019

Percentage of Retail Deliveries by Decade, Cedar Rapids Region

SW NE

0 100,000 200,000 300,000 400,000 500,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Retail Space Built by Year, Cedar Rapids

SW NE

Cedar Rapids Retail Perspective

Page 33

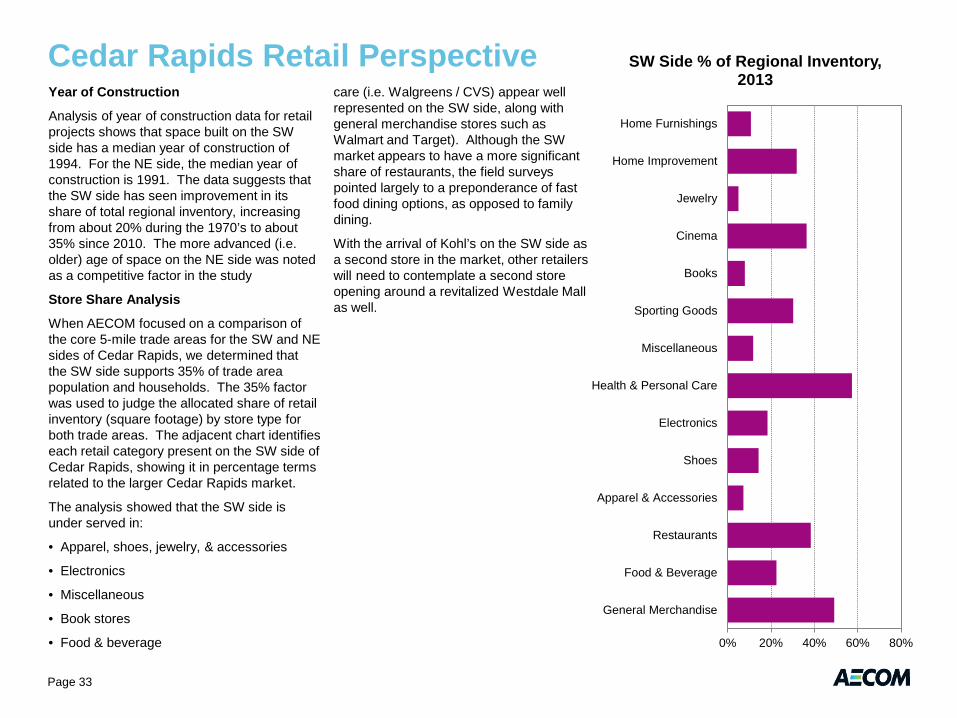

Year of Construction

Analysis of year of construction data for retail projects shows that space built on the SW side has a median year of construction of 1994. For the NE side, the median year of construction is 1991. The data suggests that the SW side has seen improvement in its share of total regional inventory, increasing from about 20% during the 1970’s to about 35% since 2010. The more advanced (i.e. older) age of space on the NE side was noted as a competitive factor in the study

Store Share Analysis

When AECOM focused on a comparison of the core 5-mile trade areas for the SW and NE sides of Cedar Rapids, we determined that the SW side supports 35% of trade area population and households. The 35% factor was used to judge the allocated share of retail inventory (square footage) by store type for both trade areas. The adjacent chart identifies each retail category present on the SW side of Cedar Rapids, showing it in percentage terms related to the larger Cedar Rapids market.

The analysis showed that the SW side is under served in:

• Apparel, shoes, jewelry, & accessories

• Electronics

• Miscellaneous

• Book stores

• Food & beverage

care (i.e. Walgreens / CVS) appear well represented on the SW side, along with general merchandise stores such as Walmart and Target). Although the SW market appears to have a more significant share of restaurants, the field surveys pointed largely to a preponderance of fast food dining options, as opposed to family dining.

With the arrival of Kohl’s on the SW side as a second store in the market, other retailers will need to contemplate a second store opening around a revitalized Westdale Mall as well.

0% 20% 40% 60% 80%

General Merchandise

Food & Beverage

Restaurants

Apparel & Accessories

Shoes

Electronics

Health & Personal Care

Miscellaneous

Sporting Goods

Books

Cinema

Jewelry

Home Improvement

Home Furnishings

SW Side % of Regional Inventory, 2013

Trade Area Retail Potential

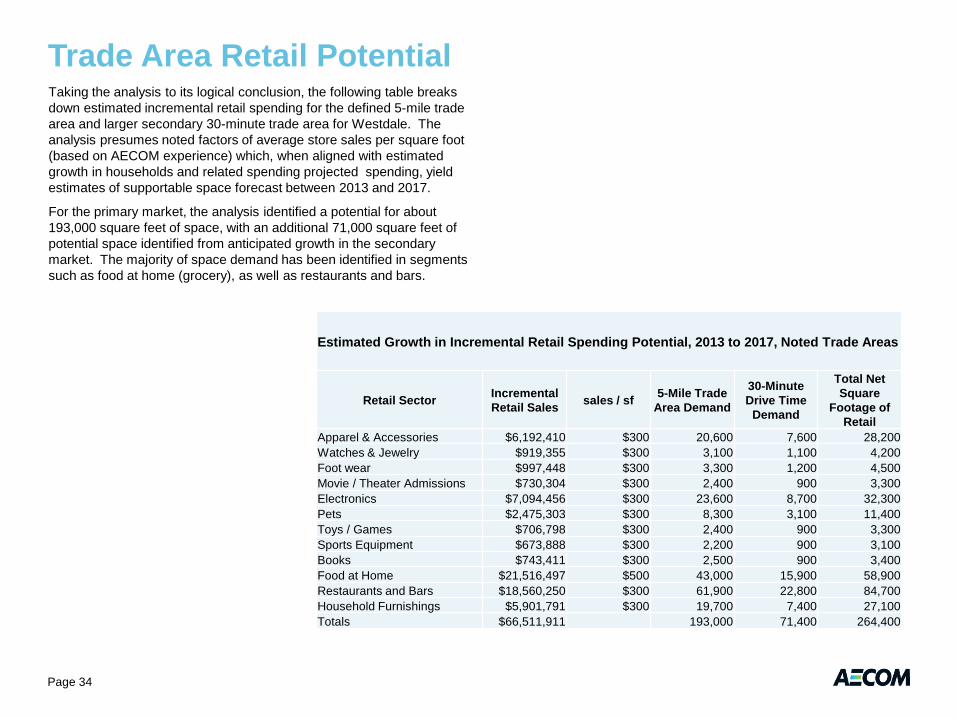

Page 34

Taking the analysis to its logical conclusion, the following table breaks down estimated incremental retail spending for the defined 5-mile trade area and larger secondary 30-minute trade area for Westdale. The analysis presumes noted factors of average store sales per square foot (based on AECOM experience) which, when aligned with estimated growth in households and related spending projected spending, yield estimates of supportable space forecast between 2013 and 2017.

For the primary market, the analysis identified a potential for about 193,000 square feet of space, with an additional 71,000 square feet of potential space identified from anticipated growth in the secondary market. The majority of space demand has been identified in segments such as food at home (grocery), as well as restaurants and bars.

Estimated Growth in Incremental Retail Spending Potential, 2013 to 2017, Noted Trade Areas

Retail Sector Incremental Retail Sales sales / sf 5-Mile Trade

Area Demand

30-Minute Drive Time

Demand

Total Net Square

Footage of Retail

Apparel & Accessories $6,192,410 $300 20,600 7,600 28,200 Watches & Jewelry $919,355 $300 3,100 1,100 4,200 Foot wear $997,448 $300 3,300 1,200 4,500 Movie / Theater Admissions $730,304 $300 2,400 900 3,300 Electronics $7,094,456 $300 23,600 8,700 32,300 Pets $2,475,303 $300 8,300 3,100 11,400 Toys / Games $706,798 $300 2,400 900 3,300 Sports Equipment $673,888 $300 2,200 900 3,100 Books $743,411 $300 2,500 900 3,400 Food at Home $21,516,497 $500 43,000 15,900 58,900 Restaurants and Bars $18,560,250 $300 61,900 22,800 84,700 Household Furnishings $5,901,791 $300 19,700 7,400 27,100 Totals $66,511,911 193,000 71,400 264,400

Cedar Rapids Cinema Perspective

Page 35

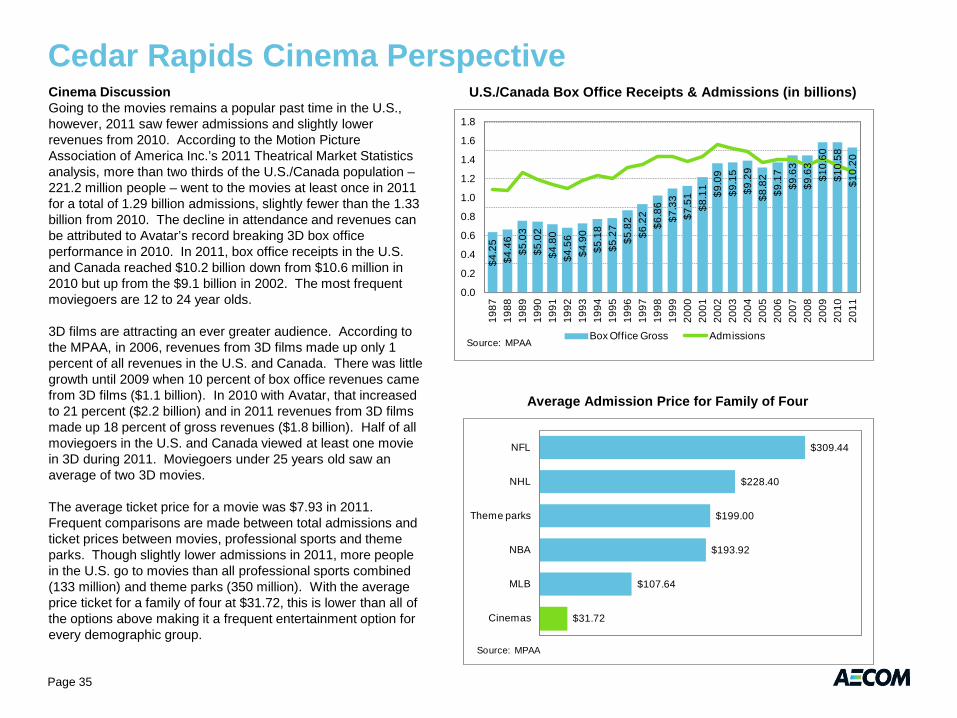

Cinema Discussion Going to the movies remains a popular past time in the U.S., however, 2011 saw fewer admissions and slightly lower revenues from 2010. According to the Motion Picture Association of America Inc.’s 2011 Theatrical Market Statistics analysis, more than two thirds of the U.S./Canada population – 221.2 million people – went to the movies at least once in 2011 for a total of 1.29 billion admissions, slightly fewer than the 1.33 billion from 2010. The decline in attendance and revenues can be attributed to Avatar’s record breaking 3D box office performance in 2010. In 2011, box office receipts in the U.S. and Canada reached $10.2 billion down from $10.6 million in 2010 but up from the $9.1 billion in 2002. The most frequent moviegoers are 12 to 24 year olds. 3D films are attracting an ever greater audience. According to the MPAA, in 2006, revenues from 3D films made up only 1 percent of all revenues in the U.S. and Canada. There was little growth until 2009 when 10 percent of box office revenues came from 3D films ($1.1 billion). In 2010 with Avatar, that increased to 21 percent ($2.2 billion) and in 2011 revenues from 3D films made up 18 percent of gross revenues ($1.8 billion). Half of all moviegoers in the U.S. and Canada viewed at least one movie in 3D during 2011. Moviegoers under 25 years old saw an average of two 3D movies. The average ticket price for a movie was $7.93 in 2011. Frequent comparisons are made between total admissions and ticket prices between movies, professional sports and theme parks. Though slightly lower admissions in 2011, more people in the U.S. go to movies than all professional sports combined (133 million) and theme parks (350 million). With the average price ticket for a family of four at $31.72, this is lower than all of the options above making it a frequent entertainment option for every demographic group.

U.S./Canada Box Office Receipts & Admissions (in billions)

$4.2

5$4

.46

$5.0

3$5

.02

$4.8

0$4

.56

$4.9

0$5

.18

$5.2

7$5

.82

$6.2

2$6

.86

$7.3

3$7

.51

$8.1

1 $9.0

9$9

.15

$9.2

9$8

.82

$9.1

7$9

.63

$9.6

3$1

0.60

$10.

58$1

0.20

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Source: MPAABox Office Gross Admissions

Average Admission Price for Family of Four

$31.72

$107.64

$193.92

$199.00

$228.40

$309.44

Cinemas

MLB

NBA

Theme parks

NHL

NFL

Source: MPAA

Cedar Rapids Cinema Perspective

Page 36

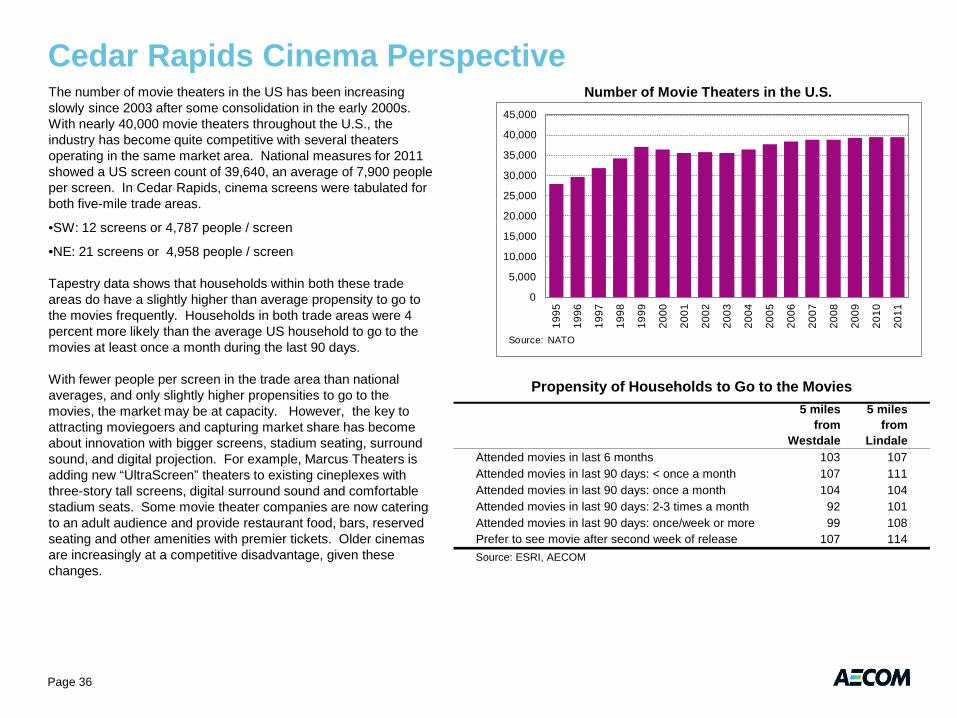

The number of movie theaters in the US has been increasing slowly since 2003 after some consolidation in the early 2000s. With nearly 40,000 movie theaters throughout the U.S., the industry has become quite competitive with several theaters operating in the same market area. National measures for 2011 showed a US screen count of 39,640, an average of 7,900 people per screen. In Cedar Rapids, cinema screens were tabulated for both five-mile trade areas.

•SW: 12 screens or 4,787 people / screen

•NE: 21 screens or 4,958 people / screen Tapestry data shows that households within both these trade areas do have a slightly higher than average propensity to go to the movies frequently. Households in both trade areas were 4 percent more likely than the average US household to go to the movies at least once a month during the last 90 days. With fewer people per screen in the trade area than national averages, and only slightly higher propensities to go to the movies, the market may be at capacity. However, the key to attracting moviegoers and capturing market share has become about innovation with bigger screens, stadium seating, surround sound, and digital projection. For example, Marcus Theaters is adding new “UltraScreen” theaters to existing cineplexes with three-story tall screens, digital surround sound and comfortable stadium seats. Some movie theater companies are now catering to an adult audience and provide restaurant food, bars, reserved seating and other amenities with premier tickets. Older cinemas are increasingly at a competitive disadvantage, given these changes.

Number of Movie Theaters in the U.S.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Source: NATO

5 miles from

Westdale

5 miles from

LindaleAttended movies in last 6 months 103 107Attended movies in last 90 days: < once a month 107 111Attended movies in last 90 days: once a month 104 104Attended movies in last 90 days: 2-3 times a month 92 101Attended movies in last 90 days: once/week or more 99 108Prefer to see movie after second week of release 107 114Source: ESRI, AECOM

Propensity of Households to Go to the Movies

Cedar Rapids Retail Perspective

Page 37

Retail Competition

There are a number of competitive retail projects in various planning stages across the Cedar Rapids region. These include the Fountains, which appears to be the primary competitor to Westdale. The proposed program includes about 36,000 SF of retail space, as well as an additional 200,000 SF of office and/or retail space. The project will benefit from a 5-year tax abatement, in part linked with proposed construction of new class A office space. Retail rents are advertised at $14.95 per SF NNN.

Interviews suggest that the Lindale Mall is contemplating an expansion. Conversations with City staff only confirmed that conversations with mall ownership have not started yet.

There are several smaller proposed strip centers across the region, mostly in Marion and Hiawatha. These smaller 8,000 to 15,000 SF projects are viewed as modest competitive threats, only to the extent that specific restaurant chains are evaluating alternative locations on the SW or NE side of the Region; Lincoln View Square in Marion is one example, with quoted rents at $15.95 per SF.

The larger Cedar Rapids / Iowa City Region continues to be influenced by the decision made several years ago to build the Coral Ridge Mall. While resulting impacts on Westdale are known, it is also interesting to watch impacts on the Sycamore Mall in Iowa City. This mall entered bankruptcy in October 2012, related to reports that Von Maur has planned to leave the mall in 2013.

Rents

A majority of older but recently built vacant retail spaces are advertised at between $12 and $14 per SF NNN. One or two projects were identified with rent levels approaching $18 to $20 per SF, located near the Lindale Mall. Rent perspective include:

• Westwood Plaza (70,000 SF) $6-$9/SF

• Marketplace on 1st (6,000 SF) $20-$24/SF

• Collins Road Sq. (36,900 SF) $6-$9/SF

• Marion Square (1,500 SF) $12 per SF

• Town & Country SC (28,600 SF) $6-$9/SF

• Czech Lane Plaza (3,400 SF) $13/SF

The majority of projects noted above with rents below $10 per SF were built before 1990. Newer, post 1990 projects all appear to be sustaining rents above $12 per SF.

Vacancy

The Vacancy analysis considered both the total amount of vacant space, as well as a determination of “competitive” vacant space, which excludes two larger stores in the SW market. These two stores include:

• Econo Foods (65,000 SF)

• Kmart (130,000 SF)

• Old Target (63,000 SF)

Considering these three buildings, our analysis arrived at the following vacancy factors

• SW Total: 321,700 SF (15% Vacant)

• SW Competitive: 63,900 SF (2.9% Vacant

• NE Total: 128,900 SF (3.3%)

The SW side accounts for about 33% of competitive vacant space.

In general, the “competitive” retail vacancy measures noted here are indicative of a healthy market, one that could support new development.

Retail Market Findings

Page 38

Core findings include:

• “Competitive” retail vacancy for the SW side is about 3%, compared to national retail vacancy over 12% (Q4 2012 CBRE).

• Retail pull factors for the Cedar Rapids MSA are modestly positive, suggesting that existing retail offerings largely serve local residents.

• While the Lindale Mall area currently supports the majority of regional retail space, assessments noted a preponderance of older (>15-year old) retail space, with limited sites available for new larger scale retail projects.

• Retail sales in Cedar Rapids have been recovering at rates equal to or above state averages since 2010, which is significant. As the regional economy’s pace of job creation recovers toward historic averages, further support for retail spending is presumed.

• Two competitive retail projects were identified; The Fountains, as well as a proposal to expand the Lindale Mall. The Fountains has secured City incentives and appears ready to move forward in search of tenants

• Current rents for newer space with national chains are driving rents toward $15 per square foot NNN, with a small number of centers at $20 per SF.

• The US retail industry is still recovery mode, and retailers are just beginning to focus on new stores, even as the internet continues to alter many retailer business plans, with one clear result being smaller store sizes. A majority of chains are still weighing closure

of underperforming stores as new sites are considered.

• The analysis showed that the SW side appears under served in apparel, shoes, jewelry, & accessories, electronics, miscellaneous, book stores, and food & beverage.

• Between 1990 and 2009, the Cedar Rapids region added about 250,000 SF of retail space per year, fueled in large part by big box store development. Presuming that the local market can sustain population growth of 0.9% and income growth of 3.5%, we anticipate that future development will unfold at a slower average annual pace, of about 140,000 SF per year. In the short-term, while it is not clear that sufficient national chain tenants exist to meet this demand, one clear offset relates to tenants who choose to vacate older space at the end of their lease-term, to locate in new space at a roughly comparable rent.

• For the defined trade areas around Westdale, the analysis identified incremental potential spending support between 2013 and 2017 for up to about 260,000 square feet of retail space tied to defined primary and secondary markets. Reflecting a conservative approach, the analysis did not expressly presume capture from tertiary markets across Cedar Rapids or Iowa City. With the proper tenant mix, competition for regional lifestyle oriented retail and entertainment spending should be an expectation.

• From a tenanting standpoint, health care tenants are seen as more likely in the future.

Residential Market Analysis Introduction

The Residential Market Analysis folds in several components:

• Analysis of changes in underlying population and household growth for the City and Metropolitan Area.

• Assessment of Building Permit data by quadrant for the City

• Analysis of rental apartment rates on a per SF basis

• Analysis of condominium unit pricing

• Assessment of senior markets

• Evaluation of overall market demand growth in coming years

• Discussion of senior housing trends

Page 39

General Market Perspective

Page 40

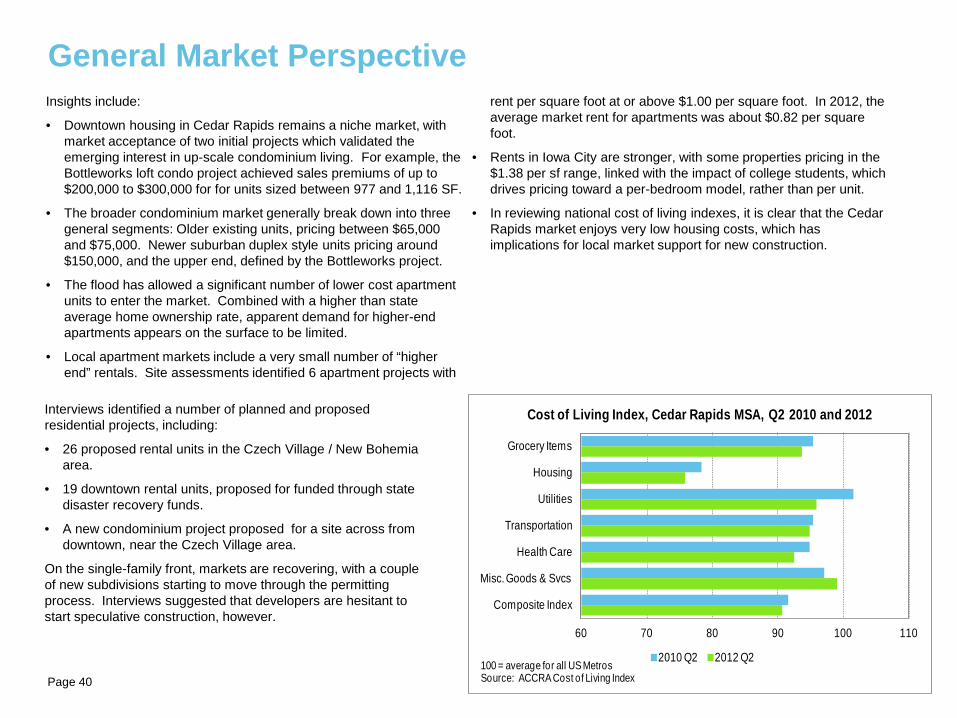

Insights include:

• Downtown housing in Cedar Rapids remains a niche market, with market acceptance of two initial projects which validated the emerging interest in up-scale condominium living. For example, the Bottleworks loft condo project achieved sales premiums of up to $200,000 to $300,000 for for units sized between 977 and 1,116 SF.

• The broader condominium market generally break down into three general segments: Older existing units, pricing between $65,000 and $75,000. Newer suburban duplex style units pricing around $150,000, and the upper end, defined by the Bottleworks project.

• The flood has allowed a significant number of lower cost apartment units to enter the market. Combined with a higher than state average home ownership rate, apparent demand for higher-end apartments appears on the surface to be limited.

• Local apartment markets include a very small number of “higher end” rentals. Site assessments identified 6 apartment projects with

rent per square foot at or above $1.00 per square foot. In 2012, the average market rent for apartments was about $0.82 per square foot.

• Rents in Iowa City are stronger, with some properties pricing in the $1.38 per sf range, linked with the impact of college students, which drives pricing toward a per-bedroom model, rather than per unit.

• In reviewing national cost of living indexes, it is clear that the Cedar Rapids market enjoys very low housing costs, which has implications for local market support for new construction.

Interviews identified a number of planned and proposed residential projects, including:

• 26 proposed rental units in the Czech Village / New Bohemia area.

• 19 downtown rental units, proposed for funded through state disaster recovery funds.

• A new condominium project proposed for a site across from downtown, near the Czech Village area.

On the single-family front, markets are recovering, with a couple of new subdivisions starting to move through the permitting process. Interviews suggested that developers are hesitant to start speculative construction, however.

60 70 80 90 100 110

Grocery Items

Housing

Utilities

Transportation

Health Care

Misc. Goods & Svcs

Composite Index

100 = average for all US MetrosSource: ACCRA Cost of Living Index

Cost of Living Index, Cedar Rapids MSA, Q2 2010 and 2012

2010 Q2 2012 Q2

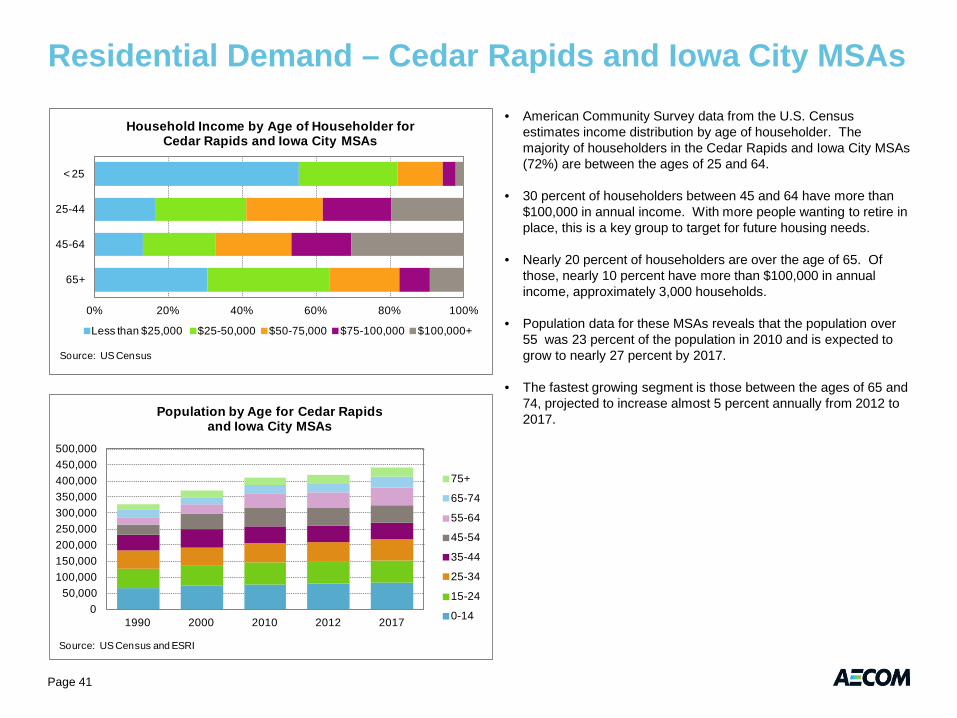

• American Community Survey data from the U.S. Census estimates income distribution by age of householder. The majority of householders in the Cedar Rapids and Iowa City MSAs (72%) are between the ages of 25 and 64.

• 30 percent of householders between 45 and 64 have more than $100,000 in annual income. With more people wanting to retire in place, this is a key group to target for future housing needs.

• Nearly 20 percent of householders are over the age of 65. Of those, nearly 10 percent have more than $100,000 in annual income, approximately 3,000 households.

• Population data for these MSAs reveals that the population over 55 was 23 percent of the population in 2010 and is expected to grow to nearly 27 percent by 2017.

• The fastest growing segment is those between the ages of 65 and 74, projected to increase almost 5 percent annually from 2012 to 2017.

Residential Demand – Cedar Rapids and Iowa City MSAs

0% 20% 40% 60% 80% 100%

< 25

25-44

45-64

65+

Source: US Census

Household Income by Age of Householder for Cedar Rapids and Iowa City MSAs

Less than $25,000 $25-50,000 $50-75,000 $75-100,000 $100,000+

050,000

100,000150,000200,000250,000300,000350,000400,000450,000500,000

1990 2000 2010 2012 2017

Source: US Census and ESRI

Population by Age for Cedar Rapids and Iowa City MSAs

75+

65-74

55-64

45-54

35-44

25-34

15-24

0-14

Page 41

Residential Market Net Demand – 2012 to 2017

Page 42

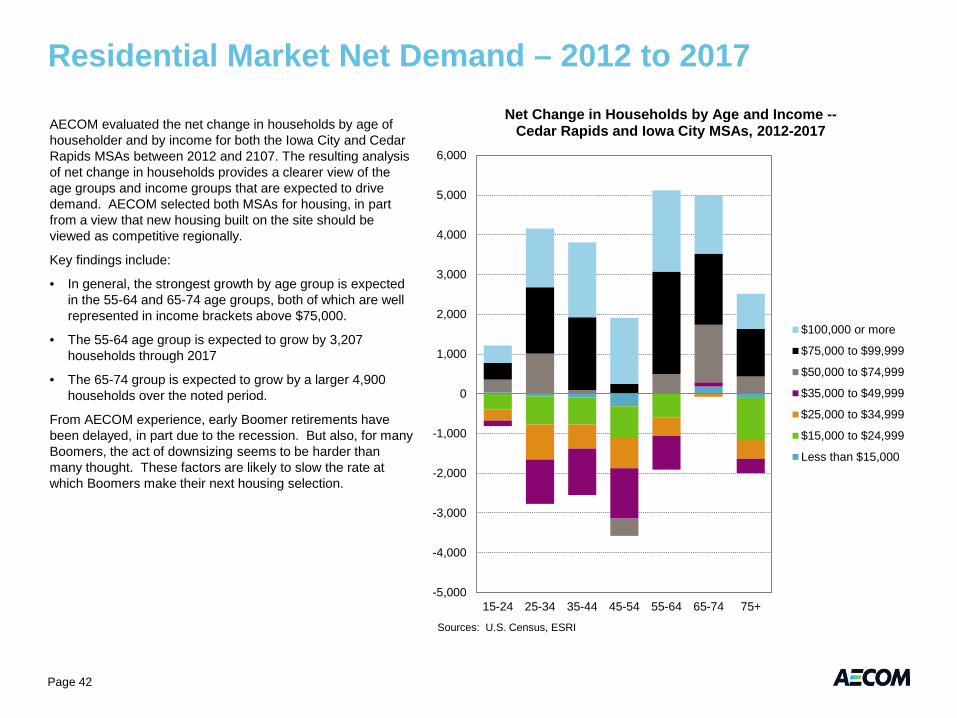

AECOM evaluated the net change in households by age of householder and by income for both the Iowa City and Cedar Rapids MSAs between 2012 and 2107. The resulting analysis of net change in households provides a clearer view of the age groups and income groups that are expected to drive demand. AECOM selected both MSAs for housing, in part from a view that new housing built on the site should be viewed as competitive regionally.

Key findings include:

• In general, the strongest growth by age group is expected in the 55-64 and 65-74 age groups, both of which are well represented in income brackets above $75,000.

• The 55-64 age group is expected to grow by 3,207 households through 2017

• The 65-74 group is expected to grow by a larger 4,900 households over the noted period.

From AECOM experience, early Boomer retirements have been delayed, in part due to the recession. But also, for many Boomers, the act of downsizing seems to be harder than many thought. These factors are likely to slow the rate at which Boomers make their next housing selection.

-5,000

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

15-24 25-34 35-44 45-54 55-64 65-74 75+

Sources: U.S. Census, ESRI

Net Change in Households by Age and Income -- Cedar Rapids and Iowa City MSAs, 2012-2017

$100,000 or more

$75,000 to $99,999

$50,000 to $74,999

$35,000 to $49,999

$25,000 to $34,999

$15,000 to $24,999

Less than $15,000