Embed Size (px)

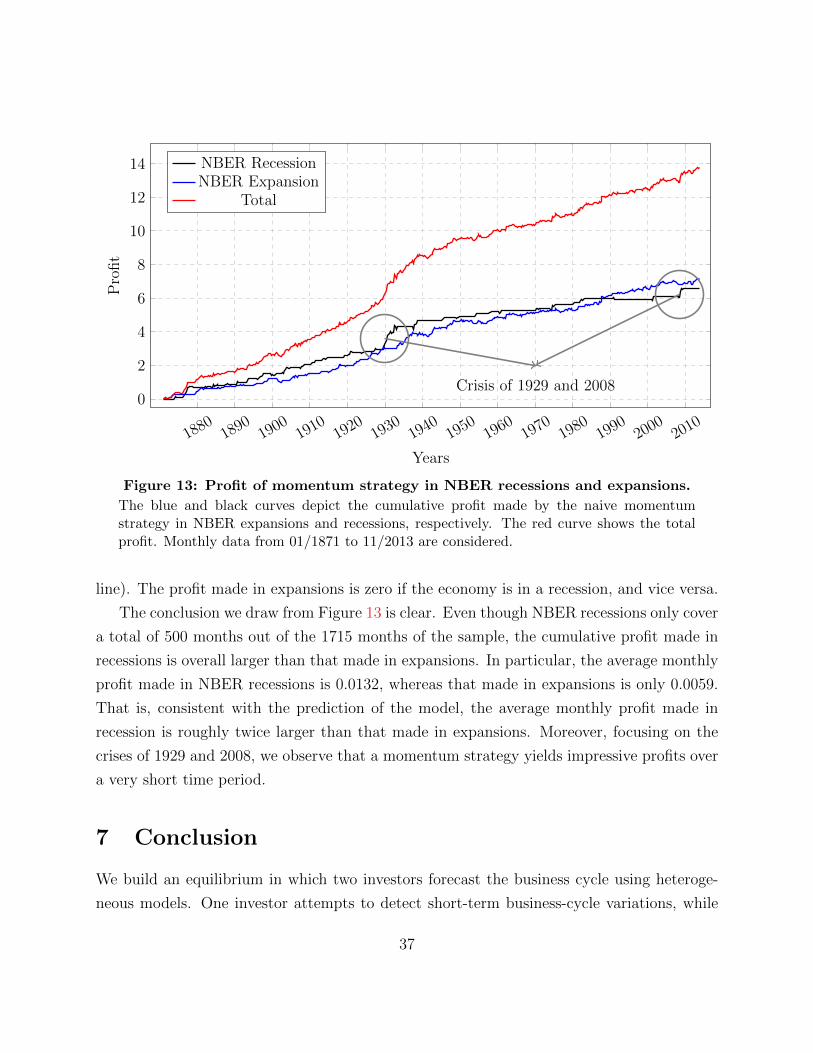

Citation preview

Why Does Return Predictability Concentrate in Bad

Times?∗

Julien Cujean† Michael Hasler‡

November 20, 2014

Abstract

We build an equilibrium model to explain why stock return predictability is con-

centrated in bad times. The key ingredient is countercyclical investors’ disagreement,

which originates from heterogeneous models. As economic conditions deteriorate, dif-

ference in investors’ learning speed increases, disagreement spikes and returns react

to past news. The model explains several findings: the link between disagreement

and future returns, time-series momentum and how it crashes after sharp market re-

bounds, and investors’ superior performance in bad times. The model further predicts

that time-series momentum is related positively to disagreement and negatively to eco-

nomic conditions. We provide empirical support to these new predictions.

Keywords. Equilibrium Asset Pricing, Learning, Disagreement, Business Cycle, Pre-

dictability, Times-Series Momentum, Momentum Crashes.

JEL Classification. D51, D83, G12, G14.

∗We would like to thank Hui Chen, Peter Christoffersen, Pierre Collin-Dufresne, Michel Dubois, Dar-rell Duffie, Bernard Dumas, Laurent Fresard, Steve Heston, Julien Hugonnier, Alexandre Jeanneret, ScottJoslin, Andrew Karolyi, Leonid Kogan, Jan-Peter Kulak, Pete Kyle, Jeongmin Lee, Mark Loewenstein, Se-myon Malamud, Erwan Morellec, Antonio Mele, Lubos Pastor, Lasse Pedersen, Remy Praz, Alberto Rossi,Rene Stulz, Adrien Verdelhan, Pietro Veronesi, Jason Wei, Liyan Yang, and seminar participants at the4th Financial Risks International Forum, Collegio Carlo Alberto, Goethe University Frankfurt, SFI-NCCRWorkshop, University of California at San Diego, University of Geneva, University of Maryland, Universityof Neuchatel, and University of Toronto for their insightful comments. Financial support from the Univer-sity of Maryland and the University of Toronto is gratefully acknowledged. A previous version of this papercirculated under the title “Time-Series Predictability, Investors’ Disagreement, and Economic Conditions”.†University of Maryland, Robert H. Smith School of Business, 4466 Van Munching Hall, College Park,

MD 20742, USA; +1 (301) 405 7707; [email protected]; www.juliencujean.com‡University of Toronto, Rotman School of Management, 105 St. George Street, Toronto, ON, M5S 2E8,

Canada; +1 (416) 946 8494; [email protected]; www.rotman.utoronto.ca/Hasler

1 Introduction

Investors’ disagreement (Diether, Malloy, and Scherbina, 2002) and the content of news

(Tetlock, 2007) predict future returns. Recent evidence further suggests that stock return

predictability using investors’ disagreement (Cen, Wei, and Yang, 2014) and the content of

news (Garcia, 2013) is concentrated in bad times.1 Yet, the mechanism that causes return

predictability to vary over the business cycle remains unclear.

In this paper, we provide an explanation why investors’ disagreement and news’ content

better predict future returns in bad times. We base our explanation on the empirical finding

that disagreement among professional forecasters originates from heterogeneity in models and

moves countercyclically (Patton and Timmermann, 2010).2 The main idea is that investors

learn at different speeds. Some investors focus on sharp variations in the business cycle and

are “fast learners”, while others focus on long-term fluctuations and are “slow learners”. As

economic conditions deteriorate, the difference in learning speeds increases and disagreement

spikes, causing prices to continue to react to past news. Return predictability therefore

concentrates in bad times.

We introduce model heterogeneity within a dynamic general equilibrium populated with

two investors, A and B. Investors trade one stock and a riskless bond and consume the divi-

dends that the stock pays out. Agents do not observe the expected growth rate of dividends,

which we call the fundamental, and have different views regarding the empirical process

that governs it. Agent A focuses on long-term fundamental variations and assumes that the

economy transits smoothly from good to bad times. In contrast, Agent B focuses on short-

term fundamental fluctuations and postulates that the economy may transit precipitously

from good to bad times.3 Although investors observe the same information (past dividend

realizations), they disagree about the fundamental because they use different models and

therefore interpret the data differently.

1See also Loh and Stulz (2014) for similar evidence related to revisions in analysts’ forecasts.2Kandel and Pearson (1995) also show that disagreement stems from model heterogeneity and Veronesi

(1999), Carlin, Longstaff, and Matoba (2013), and Barinov (2014) provide empirical evidence of counter-cyclical disagreement.

3Agent A’s model follows a mean-reverting process (Detemple (1986, 1991), Wang (1993), Brennan andXia (2001), Scheinkman and Xiong (2003), Bansal and Yaron (2004), and Dumas, Kurshev, and Uppal(2009)), while Agent B’s model follows a Markov switching process (David (1997, 2008), Veronesi (1999,2000), Chen (2010), Bhamra, Kuehn, and Strebulaev (2010), and David and Veronesi (2013)).

1

The mechanism through which investors learn may differ significantly depending on eco-

nomic conditions, leading to a pattern of disagreement that changes over the business cycle.4

In good times, investors adjust their expectations at comparable speeds and disagreement

exhibits little variation. Difference in adjustment speeds between Agents A and B becomes

apparent in normal times. While agents expect the economy to move in the same direc-

tion, Agent B—the fast learner—adjusts her expectations significantly faster than Agent

A. This difference in learning speeds exacerbates disagreement in the short-term. In bad

times, model heterogeneity implies that investors expect the economy to move in opposite

directions. This polarization of opinions produces a large spike in disagreement.5

Countercyclical spikes in disagreement cause return predictability to be concentrated

in bad times. To see this, suppose there is a positive news shock today. In bad times,

the news polarizes opinions: while Agent A revises her expectations upwards, Agent B

revises her expectations downwards. Agent B’s pessimism in turn generates a persistent and

negative price reaction to the news shock in the short term, similar to the under-reaction

phenomenon of Jegadeesh and Titman (1993). In normal times, the news exacerbates the

difference in adjustment speeds, precipitating an upward revision in Agent B’s expectations.

Agent B’s overreaction relative to Agent A in turn gives rise to a persistent and positive price

reaction to the news shock in the short term, similar to the over-reaction phenomenon of

De Bondt and Thaler (1985). In the long term, agents’ opinions align, leading to a reversion

to fundamentals. In good times, predictability vanishes because the news generates little

disagreement and reversion to fundamentals therefore occurs instantly.

Price continuation in bad and normal times produces time-series momentum in excess

returns (Moskowitz, Ooi, and Pedersen, 2012). Consistent with empirical findings, returns

exhibit momentum over a one-year horizon and then revert over subsequent horizons (due

to reversion to fundamentals). Moreover, the term structure of returns’ serial correlation is

hump shaped: momentum is strong at short horizons and decays at intermediate horizons.

Importantly, at short horizons, time-series momentum is strongest in bad times. The reason

4In our paper, learning asymmetries arise across agents because agents use different models. In anothercontext, Chalkley and Lee (1998), Veldkamp (2005), and Van Nieuwerburgh and Veldkamp (2006) also obtainasymmetries in learning over the business cycle. Yet, the reason is that the information flow fluctuates witheconomic conditions.

5These dynamics of disagreement are consistent with those observed empirically (Patton and Timmer-mann (2010)). Moreover, they arise naturally as we let agents calibrate their own model to historical data.

2

is that the polarization of opinions in bad times, as opposed to the difference in adjustment

speeds in normal times, leads to a sharper spike in disagreement. By contrast, in good

times, excess returns exhibit strong reversal at short horizons. An important consequence

of this reversal spike is that a time-series momentum strategy may crash after sharp market

rebounds.6 Sharp trend reversals typically occur at the end of financial crises. For instance,

a time-series momentum crash occurred in March 2009.

We provide empirical support to two new predictions of the model. In particular, our

model predicts that time-series momentum is (1) strongest at short horizons in bad times

and (2) increasing in investors’ disagreement. We show that, over the last century, time-

series momentum at a one-month lag is significantly stronger during recessions—momentum

profits are, on average, twice as large in recessions as they are in expansions—consistent

with the first prediction of the model. Second, we find that time-series momentum increases

with the dispersion of analysts’ forecasts, a finding that supports the second prediction of

the model.

The model has additional implications for investors’ trading strategies and profits, as well

as trading volume. First, regarding the long-term investor (Agent A) as a mutual fund, our

model reconciles two empirical findings: mutual funds generate larger profits in bad times7

(Moskowitz, 2000) and focus on market-timing strategies during recessions8 (Kacperczyk, van

Nieuwerburgh, and Veldkamp, 2013). Indeed, the long-term investor trades on momentum

in bad and normal times and reverts her strategy in good times to avoid momentum crashes.

Doing so, she reaps large profits in bad times, precisely when short-term predictability is

strongest, and little profits in good times, when predictability vanishes. Finally, we show

that trading volume is countercyclical (Karpoff, 1987) and therefore positively related to

momentum (Lee and Swaminathan, 2000).

This paper contributes to two strands of literature. First, there is a vast literature on

heterogeneous beliefs. This literature focuses, to a large extent, on volatility, risk premium,

trading volume and bubbles, among other implications of investors’ disagreement.9 Our fo-

6Daniel and Moskowitz (2013) and Barroso and Santa-Clara (2014) document the occurrence of cross-sectional momentum crashes. Moskowitz et al. (2012) document a similar phenomenon in the time-series ofreturns.

7See also Glode (2011), Kosowski (2011), and Lustig and Verdelhan (2010).8Ferson and Schadt (1996) provide evidence that fund managers timing ability varies with economic

conditions. Dangl and Halling (2012) show that market-timing strategies work best in recessions.9See Xiong (2014) for a literature review.

3

cus, instead, is on the time-series predictability of stock returns. Moreover, in this literature,

the dynamics of disagreement are specific to the source of heterogeneous beliefs considered.10

In contrast with the literature, investors in this paper disagree because they use different

models (an Ornstein-Uhlenbeck process and a Markov chain). The resulting pattern of dis-

agreement has distinct implications for the predictability of stock returns. In particular, the

large difference in adjustment speeds across agents and the polarization of their opinions—

which do not arise together with other specifications in the literature—generate counter-

cyclical spikes in disagreement. These countercyclical spikes are key to produce continuing

price reactions to news and explain observed variations in return predictability.

This paper also contributes to the large literature on momentum by offering an expla-

nation for fluctuations in time-series momentum over the business cycle.11 In our model,

time-series momentum arises because prices adjust slowly (Hong and Stein, 1999) in bad

times or because prices continue to react to news (Daniel, Hirshleifer, and Subrahmanyam,

1998) in normal times.12 Our emphasis is that these two phenomena may alternate over the

business cycle and that the former effect is stronger at short horizons.

The remainder of the paper is organized as follows. Section 2 presents and solves the

model, Section 3 provides a calibration of the model to the U.S. business cycle, Sections 4

and 5 contain the results, Section 6 tests the main predictions of the model, and Section 7

concludes. Derivations and computational details are relegated to Appendix A.

10The pattern of disagreement differs whether investors are overconfident (e.g., Dumas et al. (2009),Scheinkman and Xiong (2003), Xiong and Yan (2010)), whether they have different initial priors (e.g.,Detemple and Murthy (1994), Zapatero (1998), Basak (2000)), whether they have heterogeneous dogmaticbeliefs (e.g., Kogan, Ross, Wang, and Westerfield (2006), Borovicka (2011), Chen, Joslin, and Tran (2012),Bhamra and Uppal (2013)), or whether they disagree about the parameters of a same model (e.g., David(2008), Buraschi and Whelan (2013), Ehling, Gallmeyer, Heyerdahl-Larsen, and Illeditsch (2013), Buraschi,Trojani, and Vedolin (2014), Andrei, Carlin, and Hasler (2014)).

11Theories of momentum include Berk, Green, and Naik (1999), Holden and Subrahmanyam (2002),Johnson (2002), Sagi and Seasholes (2007), Makarov and Rytchkov (2009), Vayanos and Woolley (2010),Biais, Bossaerts, and Spatt (2010), Cespa and Vives (2012), Cujean (2013), Albuquerque and Miao (2014),and Andrei and Cujean (2014).

12Barberis, Shleifer, and Vishny (1998) provide parameter restrictions that enforce either under-reaction,over-reaction, or both.

4

2 The Model

We develop a dynamic general equilibrium in which investors use heterogeneous models

to estimate the business cycle. We first describe the economy and the learning problem

of investors. We then discuss the dynamics of investors’ disagreement implied by their

heterogeneous models and solve for the equilibrium stock price.

2.1 The Economy and Models of the Business Cycle

We consider an economy with an aggregate dividend that flows continuously over time. The

market consists of two securities, a risky asset—the stock—in positive supply of one unit

and a riskless asset—the bond—in zero net supply. The stock is a claim to the dividend

process δ, which evolves according to

dδt = δtftdt+ δtσδdWt. (1)

The random process (Wt)t≥0 is a Brownian motion under the physical probability measure,

which governs the empirical realizations of dividends. The expected dividend growth rate

f—henceforth the fundamental—is unobservable.

The economy is populated by two agents, A and B, who consume the dividend and trade

in the market. Being rational individuals, agents understand that the fundamental affects

the dividend they consume and the price of the assets they trade. They cannot, however,

observe the fundamental and therefore need to estimate it. To do so, they use the only source

of information available to them, namely the empirical realizations of dividends. But this

information is meaningless without a proper understanding of the data-generating process

that governs dividends; agents need to have a model in mind.

Agent A assumes that the fundamental follows a mean-reverting process. In particular,

she has the following model in mind

dδt = fAt δtdt+ σδδtdWAt

dfAt = κ(f − fAt

)dt+ σfdW

ft , (2)

where WA and W f are two independent Brownian motions under Agent A’s probability

5

measure PA, which reflects her views about the data-generating process. Under Agent A’s

representation of the economy, the fundamental fA transits smoothly from good to bad

states, reverting to a long-term mean f at speed κ.

Agent B, instead, believes that the fundamental follows a 2-state continuous-time Markov

chain and therefore postulates the following model

dδt = fBt δtdt+ σδδtdWBt

fBt ∈ fh, f l with generator matrix Λ =

(−λ λ

ψ −ψ

), (3)

where WB is a Brownian motion under B’s probability measure PB. Under Agent B’s

model, the fundamental fB is either high fh—the economy is in an expansion—or low f l—

the economy is in a recession. The economy transits from the high to the low state with

intensity λ > 0 and from the low to the high state with intensity ψ > 0.

Both agents have a different focus. Agent A focuses on long-term fundamental variations

(Eq. (2)) and can therefore be viewed as a long-term investor. In contrast, Agent B is

interested in identifying sudden fundamental variations (Eq. (3)) and can therefore be

regarded as a short-term investor. Whether an investor adopts a short-term or a long-

term view may depend on the constraints she faces. For instance, mutual fund investors are

typically less sensitive to performance than hedge fund investors, which allows mutual funds

to adopt longer-term investment strategies relative to hedge funds (Ben-David, Franzoni,

and Moussawi, 2012). Moreover, each model has a natural interpretation. While the model

of Agent A reflects the view promoted by the long-run risk literature (Bansal and Yaron

(2004)) that the growth rate of consumption is persistent, the perspective of Agent B is

closer to models used in the economics literature to forecast business cycle turning points.13

The financial economics literature has focused, to a large extent, on the two types of

model presented in Eqs. (2) and (3) to forecast the growth rate of dividends. These models,

13The model in Eq. (2) is adopted by Detemple (1986), Brennan and Xia (2001), Scheinkman and Xiong(2003), Dumas et al. (2009), Xiong and Yan (2010), Colacito and Croce (2013), and Bansal, Kiku, Shalias-tovich, and Yaron (2013) among others. The model in Eq. (3) is based on the work of David (1997) andVeronesi (1999) and extensions thereof. In the Economics literature, time-series models of the business cyclesinclude Threshold AutoRegressive (TAR) models, Markov-Switching AutoRegressive (MSAR) models, andSmooth Transition AutoRegressive (STAR) models. See Hamilton (1994) and Milas, Rothman, and van Dijk(2006) for further details.

6

however, have always been considered separately. In this paper, we consider these models

within a unified framework and show that the resulting disagreement between short-term

and long-term investors can explain several empirical facts related to return predictability.

2.2 Bayesian Learning and Disagreement

Agents learn about the fundamental by observing realizations of the dividend growth rate

and, given the model they have in mind, update their expectations accordingly. Doing so,

they come up with an estimate of the fundamental, which, from now on, we call the filter.

We present the dynamics of the filter of Agents A and B in Proposition 1 below.

Proposition 1. aaa

1. The filter of Agent A is defined by fAt = EPAt

[fAt]

and evolves according to

dfAt = κ(f − fAt

)dt+

γ

σδdWA

t , (4)

where γ =√σ2δ

(σ2δκ

2 + σ2f

)− κσ2

δ denotes the steady-state posterior variance (or

Bayesian uncertainty). WA is a Brownian motion under Agent A’s probability measure

that satisfies

WAt =

1

σδ

∫ t

0

(dδsδs− fAs ds

).

2. The filter of Agent B is defined by fBt = EPBt

[fBt]

= πtfh + (1− πt) f l, where πt =

PBt(fBt = fh

)is the conditional probability assigned to the high state. Agent B’s filter

evolves according to

dfBt = (λ+ ψ)(f∞ − fBt

)dt+

1

σδ

(fBt − f l

)(fh − fBt

)dWB

t , (5)

where f∞ = limt→∞ E[fBt]

= f l + ψλ+ψ

(fh − f l

)is the unconditional mean of the

Markov chain. WB is a Brownian motion under Agent B’s probability measure that

7

satisfies

WBt =

1

σδ

∫ t

0

(dδsδs− fBs ds

).

Proof. aaa

1. See Appendix A.1.

2. See Lipster and Shiryaev (2001).

Learning preserves the mean-reversion of Agent A’s initial model. Her views revert

towards their long-term mean f at speed κ, as shown in Eq. (4): when her filter is below

f her expectations revert upwards and when her filter is above f her expectations revert

downwards. In Section 3.1, we calibrate her model to the U.S. business cycle and find that

the estimated reversion speed is low. As a result, Agent A adjusts her views slowly. That

is, Agent A is a “slow learner”.

The mechanism through which Agent B updates her views differs from that of Agent A.

Her views also mean-revert, yet at a different speed λ + ψ 6= κ and to a different long-term

mean f∞ 6= f , as shown in Eq. (5). Unlike Agent A’s filter that mechanically inherits the

persistence of her initial model, the mean-reversion in Agent B’s filter reflects her effort to

continuously reassess the likelihood of the high state using the information that continuously

flows from dividends. Whether Agent B is faster to adjust her expectations than Agent A

not only depends on her relative mean-reversion speed, but also on the volatility of her filter.

Unlike the volatility of Agent A’s filter, which is constant, the volatility of Agent B’s filter

is stochastic and can therefore change precipitously. That is, Agent B is a “fast learner”.

Sudden changes in Agent B’s expectations typically occur when she is most uncertain

about the current state of the economy, i.e., when she assigns equal probabilities to each

state:

fm ≡1

2f l +

1

2fh.

As her expectations drop below fm, her filter is rapidly attracted towards the down state;

when her expectations rises above fm, her filter gets rapidly absorbed towards the up state.

8

In Section 3.1, we calibrate her model and find that the up state is more persistent than the

down state—the estimated intensity ψ is larger than λ. This asymmetry between the two

regimes implies that her filter tends to stick around the up state over a longer time period.

For reasons that will become apparent in Section 3.1, we choose to work under Agent

A’s probability measure. We convert Agent A’s views into those of Agent B through the

following change of measure:

dPB

dPA

∣∣∣∣Ft

≡ ηt = exp

[−1

2

∫ t

0

g2u

σ2δ

du−∫ t

0

guσδ

dWAu

], (6)

where the process g ≡ fA − fB represents agents’ disagreement about the estimated funda-

mental.

The change of measure in (6) implies that Agents A and B have equivalent perceptions

of the world.14 In particular, the Brownian motions WA and WB are related through

dWBt = dWA

t +gtσδ

dt.

That agents have equivalent perceptions may be surprising, if we consider that Agent B’s

filter is strictly confined within the interval [f l, fh], while Agent A’s filter can reach virtually

any value. To see how both views are compatible, fix a value for Agent A’s filter, say fA

.

This, in turn, imposes a restriction on the possible values of disagreement. Specifically, since

Agent B assigns zero probabilities to the events fB > fh and fB < f l, disagreement is

at least equal to fA − fh and at most equal to f

A − f l. The dynamics of disagreement, g,

are such that this property is always satisfied:

dgt =

[κ(f − fAt

)− (λ+ ψ)

(f∞ + gt − fAt

)− gtσ2δ

(fAt − gt − f l

)(fh + gt − fAt

)]dt

+γ −

(fAt − gt − f l

)(fh + gt − fAt

)σδ

dWAt . (7)

14Disagreement is the difference between an Ornstein-Uhlenbeck process, which is stationary, and abounded process. Disagreement is therefore stationary, the Novikov condition is satisfied and Girsanov’sTheorem applies.

9

The dynamics in Eq. (7) reflect our previous discussion regarding the different learning

mechanisms of the two agents. In particular, agents disagree about three aspects of the

fundamental: its persistence, its long-term mean, and its volatility. These three aspects

together give rise to countercyclical disagreement that persists over long horizons, consis-

tent with the observed pattern of disagreement among professional forecasters (Patton and

Timmermann (2010)). The key ingredient to generate this pattern of disagreement is that

agents use heterogeneous models,15 an assumption that also finds strong empirical support

(e.g., Kandel and Pearson (1995) and Patton and Timmermann (2010)). To consistently

measure disagreement in our model, we let agents calibrate their model to the U.S. business

cycle (Section 3.1) and postpone an extensive discussion of the resulting term structure of

disagreement to Section 3.2.

2.3 Equilibrium

Agents choose their portfolios and consumption plans to maximize their expected lifetime

utility of consumption. They have power utility preferences defined by

U (c, t) ≡ e−ρtc1−α

1− α,

where α > 0 is the coefficient of relative risk aversion and ρ > 0 the subjective discount rate.

Since markets are complete, we solve the consumption-portfolio problem of both agents

using the martingale approach of Karatzas, Lehoczky, and Shreve (1987) and Cox and Huang

(1989). Each agent’s maximization problem is described and solved in Appendix A.2. Im-

posing the market-clearing condition gives the state-price density ξ, which satisfies:

ξt = e−ρtδ−αt

[(ηtφB

) 1α

+

(1

φA

) 1α

]α, (8)

where φA and φB are the Lagrange multipliers associated to Agent A’s and Agent B’s budget

constraints, respectively.

The main mechanism generating stronger predictability in recessions operates through

15These dynamics are specific to model heterogeneity. When agents disagree about the parameters of asame model, the dynamics of disagreement differ significantly. See, for instance, David (2008), Buraschi andWhelan (2013), Ehling et al. (2013), Andrei et al. (2014), and Buraschi et al. (2014).

10

Eq. (8). Heterogeneous beliefs affect the state-price density through the variable η, the

likelihood of Agent B’s model relative to Agent A’s model. This relative likelihood is, in turn,

determined by the disagreement process (through Eq. (6)). As a result, the disagreement

process drives the dynamics of the state-price density and, hence, the dynamics of stock

returns. In particular, Dumas et al. (2009) note that ξ is concave in η; Jensen’s inequality

along with Eq. (6) together imply that an increase in disagreement reduces the expected

values of future state-price densities under Agent A’s measure, resulting in higher expected

returns. Because fluctuations in disagreement are faster and stronger in recessions (see

Section 3.2), disagreement better predicts future returns in recessions.

An application of Ito’s lemma to the state-price density in Eq. (8) yields the equilibrium

risk-free rate, rf , and market price of risk, θ, of our model:

rft = ρ+ αfAt −1

2α(α + 1)σ2

δ + (1− ω(ηt)) gt

(1

2

α− 1

ασ2δ

ω(ηt)gt − α)

(9)

θt = ασδ +(1− ω(ηt))

σδgt, (10)

where ω(η) denotes Agent A’s consumption share, which we define in Appendix A.2.

If agents did not disagree (g = 0) or if only one agent populated the economy (ω = 0

or ω = 1), the risk-free rate in Eq. (9) and the market price of risk in Eq. (10) would be

those of Lucas (1978). Inspecting the last term in Eq. (10), we conclude that heterogeneous

beliefs cause the market price of risk to exceed that of a Lucas (1978) economy, but only

when Agent A is more optimistic than Agent B (g > 0). In our model, this outcome, which

plays an important role when we study agents’ profits in Section 5, only arises in recessions.

Finally, we provide the equilibrium stock price in Proposition 2 below.

Proposition 2. Assuming that the coefficient of relative risk aversion α is an integer, the

equilibrium stock price satisfies

Stδt

= ω(ηt)αStδt

∣∣∣∣O.U.

+ (1− ω(ηt))αStδt

∣∣∣∣M.C.

+ ω (ηt)αα−1∑j=1

(α

j

)(1− ω (ηt)

ω (ηt)

)jF j(fAt , gt

)(11)

where Sδ

∣∣O.U.

and Sδ

∣∣M.C.

denote the prices in a representative-agent economy populated by

11

Agent A and B, respectively, and where the functions F j(fA, g

)represent price adjustment

for investors’ disagreement. We derive these equilibrium functions in Appendix A.3.

Proof. See Appendix A.3.

The price in Eq. (11) has three terms. When agents have logarithmic utilities (α = 1),

only the first two terms are relevant and the price is just an average of the prices that obtain

in a representative-agent economy populated by Agent A and B, respectively. When agents

are more risk averse than a logarithmic agent (α > 1), the third term becomes relevant.

This term is central to our analysis of predictability as it isolates how the joint interaction

of fundamental and disagreement operates on the price through the function F . In Section

4.1, we focus on this interaction and relate it to the time-series predictability of returns.

3 Calibration and Term Structure of Disagreement

In this section we calibrate the models of Agent A and B and discuss their relative fit to the

U.S. business cycle (Section 3.1). We then study the resulting term structure of disagreement

and show that disagreement is countercyclical and persists over long horizons (Subsection

3.2).

3.1 Calibration and Model Fit to the U.S. Economy

In our model, agents use a single source of information—the time-series of dividends δ—to

update their expectations. As a proxy for the dividend stream, we use the S&P 500 dividend

time-series recorded at a monthly frequency from January 1871 to November 2013, which we

obtain from Robert Shiller’s website. Looking back to the 19th century allows us to cover a

large number of business cycle turning points, but obviously adds strong seasonality effects

(Bollerslev and Hodrick (1992)). To reduce these effects, we apply the filter developed by

Hodrick and Prescott (1997) to the time-series of dividends.

We assume that both agents observe the S&P 500 dividend time-series, after seasonalities

have been smoothed out. Because this data is available monthly, agents need to first esti-

mate a discretized version of their model by Maximum Likelihood.16 Agents then map the

16See Hamilton (1994) for the likelihood function of each model. We present the estimated parameters,their standard errors, and their statistical significance in Table 3 in Appendix A.4.

12

Parameter Symbol ValueVolatility Dividend Growth σδ 0.0225Mean-Reversion Speed fA κ 0.1911Long-Term Mean fA f 0.0630Volatility fA σf 0.0056High State fB fh 0.0794Low State fB f l −0.0711Intensity High to Low λ 0.3022Intensity Low to High ψ 0.3951Relative Risk Aversion α 2Subjective Discount Rate ρ 0.01

Table 1: Parameter calibration

This table reports the estimated parameters of the continuous-time model of Agent A andAgent B along with the relative risk aversion α and the subjective discount rate ρ.

parameters they estimated into their continuous-time model. Doing so, agents obtain the

parameter values presented in Table 1. All discussions and results that follow are based on

these parameter values. For convenience, we discuss the methodological details in Appendix

A.4.

The parameters of Table 1 show that both models produce distinct interpretations of the

data. First, Agent A finds a low reversion speed κ and therefore concludes that the fun-

damental is highly persistent, a conclusion largely supported by the long-run risk literature

(e.g., Bansal and Yaron (2004)). As a result, Agent A is a “slow learner”. Second, Agent B

finds that the high state fh and the low state f l identify an expansion and a recession state,

respectively. Importantly, Agent B finds an asymmetry between the two states—expansions

are more persistent than recessions (ψ > λ). The sum of λ and ψ further imply that Agent

B’s filter reverts about 3.5 times faster than that of Agent A. That is, Agent B is a “fast

learner”. In addition, the long-term mean of Agent B’s filter (f∞ ≈ 0.014) is lower than

that of Agent A (f = 0.063). Finally, in contrast to the volatility of Agent B’s filter, that

of Agent A is constant. Therefore, both models differ with respect to adjustment speeds,

long-term means, and volatilities.

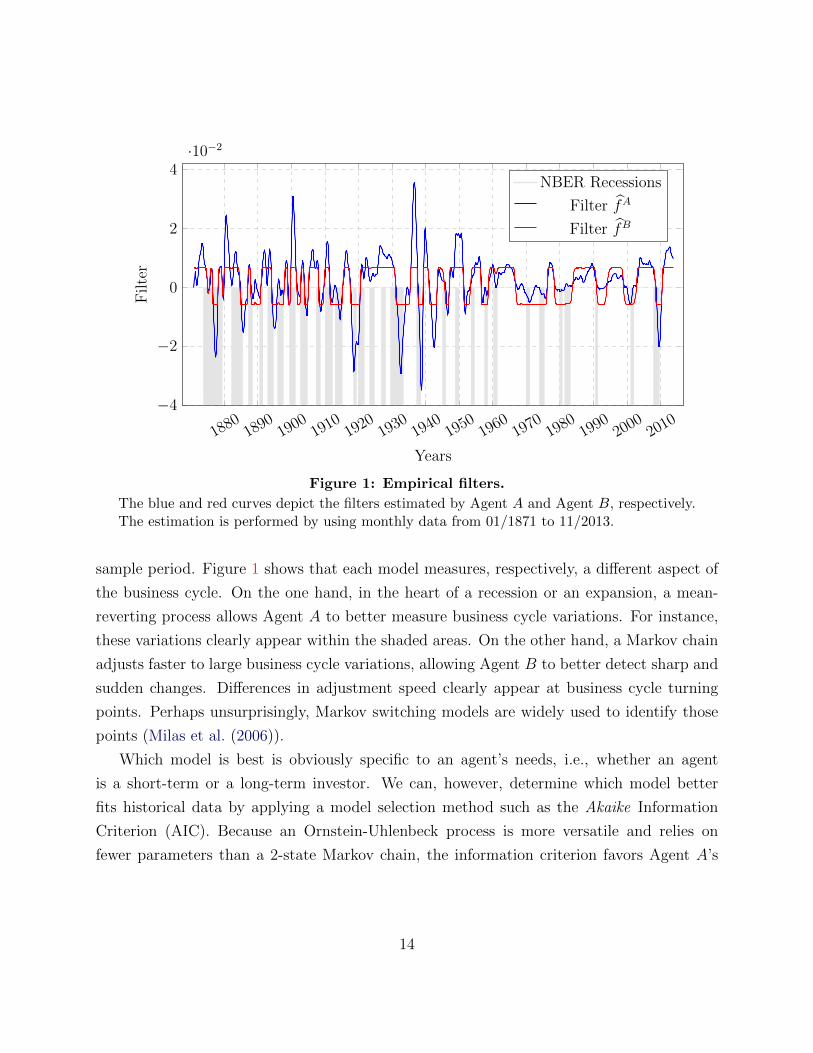

To illustrate how these differences affect agents’ ability to forecast the business cycle, we

plot in Figure 1 agents’ filters against NBER recession dates (the shaded areas) over the

13

18801890

19001910

19201930

19401950

19601970

19801990

20002010

−4

−2

0

2

4·10−2

Years

Filte

r

NBER Recessions

Filter fA

Filter fB

Figure 1: Empirical filters.

The blue and red curves depict the filters estimated by Agent A and Agent B, respectively.The estimation is performed by using monthly data from 01/1871 to 11/2013.

sample period. Figure 1 shows that each model measures, respectively, a different aspect of

the business cycle. On the one hand, in the heart of a recession or an expansion, a mean-

reverting process allows Agent A to better measure business cycle variations. For instance,

these variations clearly appear within the shaded areas. On the other hand, a Markov chain

adjusts faster to large business cycle variations, allowing Agent B to better detect sharp and

sudden changes. Differences in adjustment speed clearly appear at business cycle turning

points. Perhaps unsurprisingly, Markov switching models are widely used to identify those

points (Milas et al. (2006)).

Which model is best is obviously specific to an agent’s needs, i.e., whether an agent

is a short-term or a long-term investor. We can, however, determine which model better

fits historical data by applying a model selection method such as the Akaike Information

Criterion (AIC). Because an Ornstein-Uhlenbeck process is more versatile and relies on

fewer parameters than a 2-state Markov chain, the information criterion favors Agent A’s

14

model.17 Hence, over the last century, Agent A’s probability measure was closer to the

physical probability measure in-sample. This fact ultimately justifies our choice of computing

and analyzing the equilibrium under Agent A’s probability measure PA. It does, however,

not necessarily question Agent B’s rationality—a model that performs better in-sample does

not necessarily perform better out-of-sample.18 In particular, for agents who process the data

in real time, it is difficult to assess the relative fit of their model.

3.2 Term Structure of Disagreement

There exists a term structure of disagreement among professional forecasters. Forecasters’

disagreement, as measured by the dispersion of their forecasts, is large at long horizons,

thus supporting the view that disagreement stems from heterogeneous models, as opposed

to private information (Patton and Timmermann (2010)). Most important to our study

is the fact that this term structure of disagreement is countercyclical. That is, there is

little disagreement in good times and large disagreement in bad times.19 In this section, we

show that model heterogeneity precisely leads to a term structure of disagreement that is

consistent with these facts.

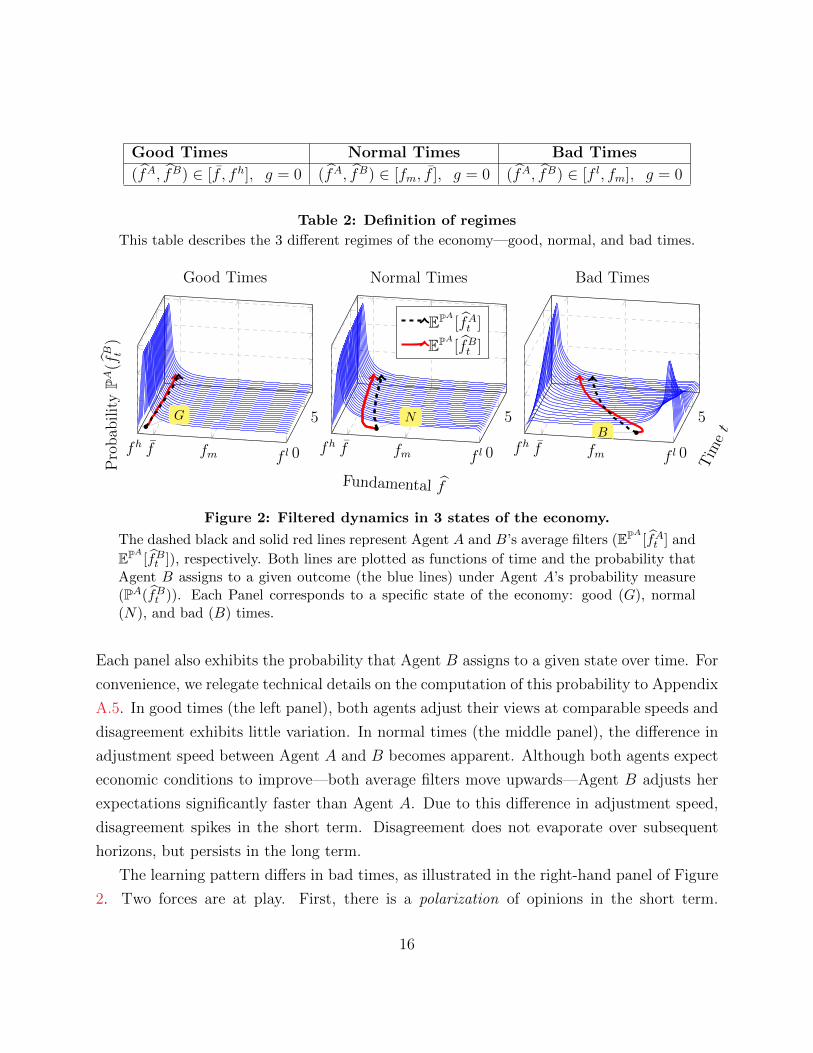

We first define three regimes of the economy on which we focus our study. Based on

the learning patterns of Section 2.2, we say that the economy is in good times when agents’

expectations are above f and in bad times when agents’ expectations are below fm. Finally,

we say the economy is in normal times when filters lie between fm and f . To emphasize that

future disagreement—as opposed to current disagreement—drives our result, we set current

disagreement to zero in each case. Moreover, without loss of generality, we assume that

agents’ filters always start in the middle of each interval. Table 2 summarizes the definition

of the three regimes.

To illustrate how agents update their expectations in each regime, we plot Agent A

and B’s average filter over time in Figure 2. Each panel corresponds to a different regime.

17The Akaike Information Criterion is defined as follows: AIC = 2K − 2 log (L), where K is the numberof parameters estimated and L is the Likelihood function. Therefore, the smaller the criterion is, the betteris the model. We find that the AIC for Agent A and B’s model are AICAgent A = −1.7229 × 104 andAICAgent B = −1.2154× 104.

18For instance, Welch and Goyal (2008) show that, while any predictive model performs better than thehistorical mean in-sample, the latter tends to have better predictive power out-of-sample.

19Massa and Simonov (2005) show that forecasters strongly disagree about recession probabilities. Veronesi(1999) and Barinov (2014) show that the dispersion of analysts forecasts increases during recessions.

15

Good Times Normal Times Bad Times

(fA, fB) ∈ [f , fh], g = 0 (fA, fB) ∈ [fm, f ], g = 0 (fA, fB) ∈ [f l, fm], g = 0

Table 2: Definition of regimes

This table describes the 3 different regimes of the economy—good, normal, and bad times.

0

5

f lfmffh

G

Pro

bab

ilit

yPA

(fB t

)

Good Times

0

5

f lfmffh

N

Fundamental f

Normal Times

EPA [fAt ]

EPA [fBt ]

0

5

f lfmffhB

Tim

et

Bad Times

Figure 2: Filtered dynamics in 3 states of the economy.

The dashed black and solid red lines represent Agent A and B’s average filters (EPA [fAt ] and

EPA [fBt ]), respectively. Both lines are plotted as functions of time and the probability thatAgent B assigns to a given outcome (the blue lines) under Agent A’s probability measure(PA(fBt )). Each Panel corresponds to a specific state of the economy: good (G), normal(N), and bad (B) times.

Each panel also exhibits the probability that Agent B assigns to a given state over time. For

convenience, we relegate technical details on the computation of this probability to Appendix

A.5. In good times (the left panel), both agents adjust their views at comparable speeds and

disagreement exhibits little variation. In normal times (the middle panel), the difference in

adjustment speed between Agent A and B becomes apparent. Although both agents expect

economic conditions to improve—both average filters move upwards—Agent B adjusts her

expectations significantly faster than Agent A. Due to this difference in adjustment speed,

disagreement spikes in the short term. Disagreement does not evaporate over subsequent

horizons, but persists in the long term.

The learning pattern differs in bad times, as illustrated in the right-hand panel of Figure

2. Two forces are at play. First, there is a polarization of opinions in the short term.

16

That is, agents disagree about the direction in which the economy is heading and average

filters diverge. In particular, Agent A is optimistic and expects the economy to recover,

while Agent B is pessimistic and expects economic conditions to further deteriorate. This

polarization of opinions creates a spike in disagreement in the short term. Second, the

difference in adjustment speed reappears in the long run. As Agent B realizes that the

economy is recovering, she rapidly catches up with Agent A and eventually becomes more

optimistic than Agent A. As a result, disagreement evaporates in the medium term and

regenerates in the long term through the difference in adjustment speeds (Agent B adjusts

her views significantly faster than Agent A).

Overall, the polarization of opinions in the short term along with the difference in adjust-

ment speeds in the long term generate strong disagreement in bad times. This conclusion is

consistent with empirical evidence. In particular, Veronesi (1999), Patton and Timmermann

(2010), Carlin et al. (2013), and Barinov (2014) find that disagreement is larger in downturns

than in upturns.

4 Disagreement driving Stock Return Predictability

Recent evidence shows that stock return predictability is concentrated in bad times.20 In

this section, our objective is to determine the mechanism that causes return predictability to

vary over the business cycle. We show that countercyclical disagreement leads to downward

price pressures (Section 4.1) and continuing price reaction to past news (Section 4.2), which

are concentrated in bad times. Moreover, we show that these phenomena produce time-series

momentum and crashes in time-series momentum following sharp market rebounds (Section

4.3).

4.1 Disagreement and Downward Price Pressure

There is evidence that high disagreement predicts low future returns at short horizons (e.g.,

Diether et al. (2002)). Recently, Cen et al. (2014) find that this relation is concentrated in

bad times. In this section, we show that our model offers an explanation for this fact.

20Garcia (2013) shows that the content of news better predict stock returns in recessions. Rapach, Strauss,and Zhou (2010), Henkel, Martin, and Nardari (2011), and Dangl and Halling (2012) find that macro variableshave better predictive power in recessions.

17

In our model, predictability arises through the relation between disagreement and fun-

damentals. This relation operates on prices through two opposite forces. On the one hand,

an increase in the fundamental and/or in relative optimism improves investment opportuni-

ties. As a result, agents delay consumption to increase their holdings in the stock and the

price increases. We call this the investment effect. On the other hand, an increase in the

fundamental and/or in relative optimism predicts high future consumption. Because agents

want to smooth consumption over time, they disinvest to consume more today and the price

decreases. We call this the consumption effect.

Whether the investment or the consumption effect dominates depends on the interac-

tion between fundamental and disagreement in the future and therefore on the state of the

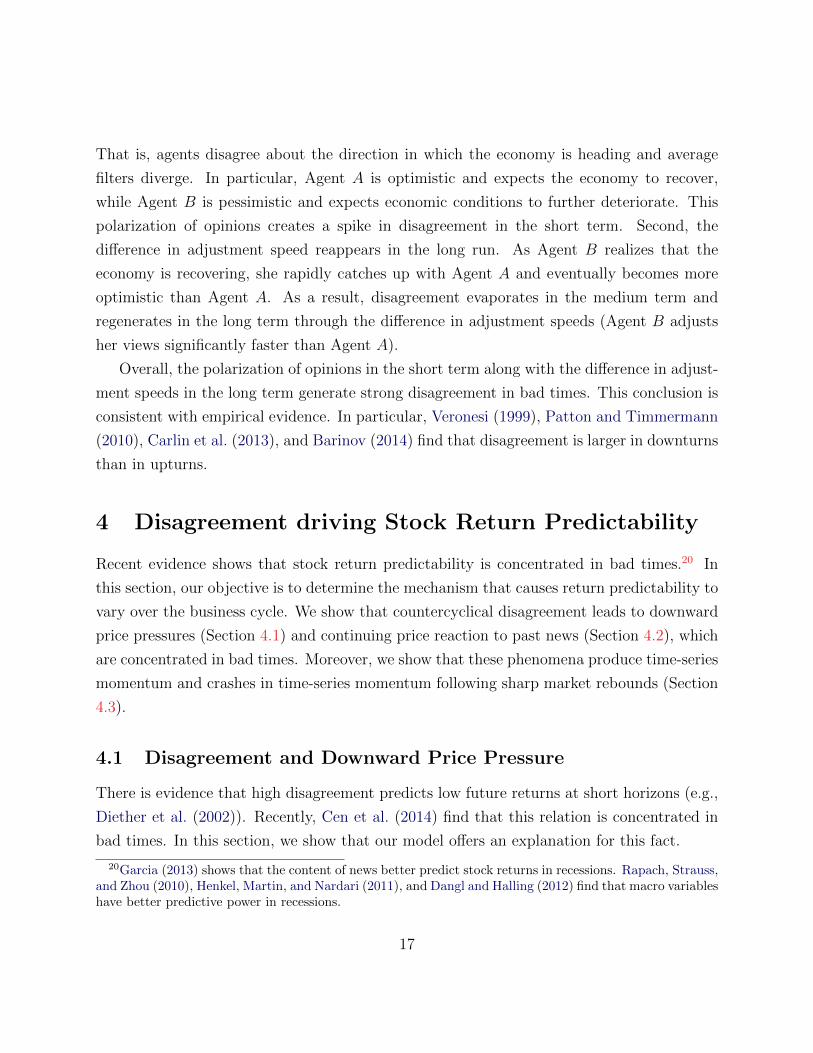

economy. To show this, we first isolate the component of prices that exclusively captures

this interaction, namely the function F in Eq. (11). We plot this price component (the

blue surface) in Figure 3, both as a function of disagreement and fundamental. This sur-

face provides a static view on prices, disagreement, and fundamental. To understand how

these three dimensions interact dynamically, we draw their average path over time (the red

arrows). In general, the higher the fundamental is, the stronger the investment effect is. We

now study in which regime the investment effect actually dominates.

In bad times (B), polarization of opinions creates a spike in disagreement in the short

term, causing Agent A to be optimistic relative to Agent B (the red arrow moves towards

the left). This spike in disagreement dominates reversion to fundamentals in the short-term

(the red arrow does not revert upwards immediately). In this case, the consumption effect

is stronger and disagreement therefore causes a strong downward pressure on prices. As

Agent B realizes the economy is recovering, opinions align and agent’s expectations only

differ with respect to their adjustment speed (the red arrow changes direction). A decrease

in disagreement in turn allows reversion to fundamentals to drive prices back up. Hence, in

the long term, the investment effect dominates.

In normal times (N), difference in adjustment speeds produces a spike in disagreement

in the short term, causing Agent A to be pessimistic relative to Agent B (the red arrow

moves towards the right). As in bad times, disagreement dominates reversion to fundamen-

tals in the short term, which leads to a downward price pressure. In this case, however, the

downward price pressure arises through the investment effect. Moreover, because disagree-

ment decreases monotonically over time (the red arrow reverts back towards zero), reversion

18

0

0.05

-0.02-0.01

00.01

0.02

2

4

N

G

B

Fund

amen

tal f

A

Disagreement g

Pri

ceF

(fA,g

)

Figure 3: Disagreement, fundamental, and expected prices.

The blue surface represents the middle price component in Eq. (11), plotted as a functionof disagreement and fundamentals. The red arrows describe the average price paths overthe next 7 years, each corresponding to a state of the economy—good (G), normal (N), andbad (B) times.

to fundamentals occurs faster in normal times (relative to bad times). Finally, in good

times (G), both disagreement and fundamentals exhibit little variation (the red arrow stays

confined to a small area) and prices tend to stick around the same level.

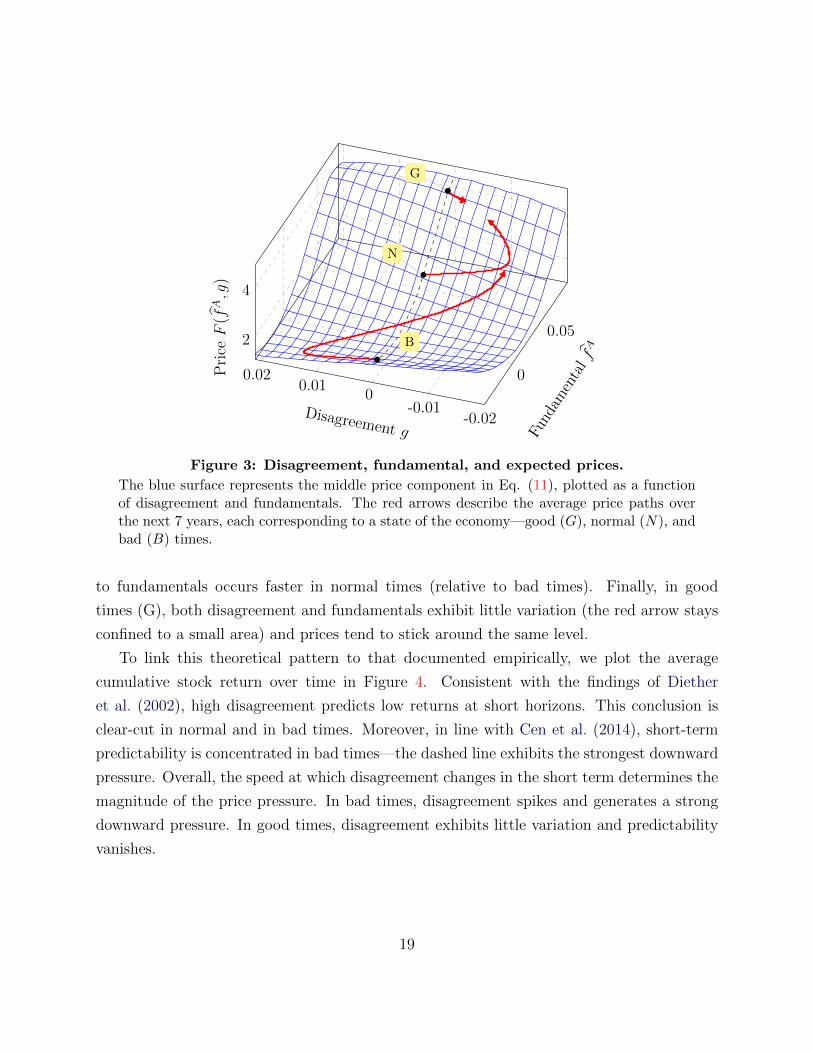

To link this theoretical pattern to that documented empirically, we plot the average

cumulative stock return over time in Figure 4. Consistent with the findings of Diether

et al. (2002), high disagreement predicts low returns at short horizons. This conclusion is

clear-cut in normal and in bad times. Moreover, in line with Cen et al. (2014), short-term

predictability is concentrated in bad times—the dashed line exhibits the strongest downward

pressure. Overall, the speed at which disagreement changes in the short term determines the

magnitude of the price pressure. In bad times, disagreement spikes and generates a strong

downward pressure. In good times, disagreement exhibits little variation and predictability

vanishes.

19

0 1 2 3 4 5 6 7

−0.3

−0.2

−0.1

0

0.1

Time u− t

EPA

t

[ S u−St

St

]Normal TimesGood TimesBad Times

Figure 4: Expected cumulative stock return over time.

This figure plots the expected trajectory of the cumulative stock return over time (7 years).Each line corresponds to a state of the economy—good (dashed black), normal (solid red),and bad (dash-dotted blue) times.

4.2 Price Reaction to News

In this section, we relate short-term predictability to the content of news. Empirically, the

content of news, as proxied by media pessimism, predicts stock returns in the short term

(Tetlock, 2007). Our model allows to explain why the predictive power of news’ content is

concentrated in bad times (Garcia, 2013). In bad times, news polarizes opinions, causing

prices to persistently and negatively react to the news. In normal times, news exacerbates

the difference in adjustment speed, causing prices to persistently and positively react to the

news. In good times, the news provokes an immediate price adjustment.

To show how prices react to news in our model, we conduct the following experiment.

We consider a trajectory of news. In our model, the only source of news is the Brownian

innovation WA. We then introduce a news surprise today (an initial perturbation of the

news trajectory) and keep the news trajectory otherwise unchanged, as illustrated in the

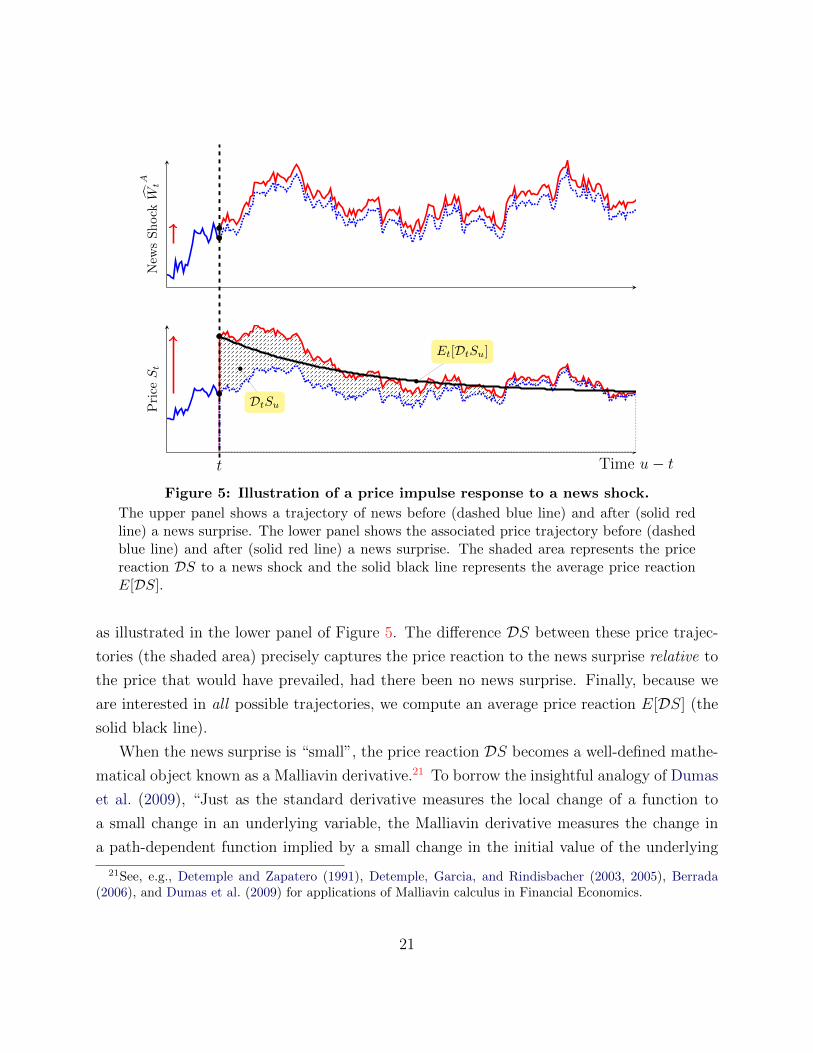

upper panel of Figure 5.

To each news trajectory, both perturbed and unperturbed, corresponds a price trajectory,

20

New

sS

hockW

t

A

t

Et[DtSu]

DtSu

Time u− t

Pri

ceSt

Figure 5: Illustration of a price impulse response to a news shock.

The upper panel shows a trajectory of news before (dashed blue line) and after (solid redline) a news surprise. The lower panel shows the associated price trajectory before (dashedblue line) and after (solid red line) a news surprise. The shaded area represents the pricereaction DS to a news shock and the solid black line represents the average price reactionE[DS].

as illustrated in the lower panel of Figure 5. The difference DS between these price trajec-

tories (the shaded area) precisely captures the price reaction to the news surprise relative to

the price that would have prevailed, had there been no news surprise. Finally, because we

are interested in all possible trajectories, we compute an average price reaction E[DS] (the

solid black line).

When the news surprise is “small”, the price reaction DS becomes a well-defined mathe-

matical object known as a Malliavin derivative.21 To borrow the insightful analogy of Dumas

et al. (2009), “Just as the standard derivative measures the local change of a function to

a small change in an underlying variable, the Malliavin derivative measures the change in

a path-dependent function implied by a small change in the initial value of the underlying

21See, e.g., Detemple and Zapatero (1991), Detemple, Garcia, and Rindisbacher (2003, 2005), Berrada(2006), and Dumas et al. (2009) for applications of Malliavin calculus in Financial Economics.

21

Brownian motions.” Its economic meaning is that of an impulse-response function following

a shock in initial values; in our case, a news shock. However, unlike a standard impulse-

response function, a Malliavin derivative takes future uncertainty into account. That is, it

does not assume that the world becomes deterministic after the shock has occurred. For

that reason, we compute an average price response, as described in Proposition 3.

Proposition 3. The expected average price response to a news surprise satisfies

EPAt [DtSu] = σδEPA

t [Su] +γ

κσδ

((1− αe−κ(u−t))EPA

t [Su] + (α− 1)EPAt

[∫ ∞u

ξsξuδse−κ(s−t)ds

])︸ ︷︷ ︸

fundamental effect

(12)

+1

σ2δ

EPAt

[∫ ∞u

ξsξuδs

((ω(ηs)− ω(ηu))

∫ u

t

gvDtgvdv − (1− ω(ηs))

∫ s

u

gvDtgvdv)

ds

]︸ ︷︷ ︸

disagreement effect

,

where the disagreement response Dg to a news surprise solves

dDtgv = ∇µg(fAv , gv)>(

γσδe−κ(v−t)

Dtgv

)dv +∇σg(fAv , gv)>

(γσδe−κ(v−t)

Dtgv

)dWA

v , (13)

with initial condition Dtgt = σg(fAt , gt) and where µg and σg represent the drift and the

diffusion of disagreement in Eq. (7), respectively. The operator ∇ stands for the gradient.

Proof. See Appendix A.6.

The news surprise affects prices through three different channels. The first term in Eq.

(12) represents the dividend channel; it is just a scaled average price, which we discussed

in the previous section. The second term captures the filter channel. This term is initially

negative; it becomes gradually positive and brings prices closer to their fundamental levels.

The last term accounts for the disagreement channel.

Our calibration indicates that the first two effects will be of small short-term magnitude as

compared to the disagreement channel. Disagreement is therefore the main channel through

which the price reacts to the news surprise in the short term. In particular, the news

22

0 1 2 3

−4

−2

0

2

4

Time u− t

EPA

t[D

tSu]

Price Impulse Responseaa

Normal TimesGood TimesBad Times

0 1 2 3

−1

0

1

·10−3

Bis

pes

sim

isti

cB

isov

erly

opti

mis

tic

Time u− t

EPA

t[guDtgu]

Disagreement Impulse Responseaa

Figure 6: Impulse response to a news shock.

The left-hand panel shows the average price response EPAt [DtSu] to a news shock. The right-

hand panel shows the average price response of disagreement to a news shock multiplied bydisagreement EPA

t [guDtgu]. Each is plotted as a function of time. Each line corresponds to adifferent regime. Optimism and pessimism describe the views of Agent A relative to AgentB.

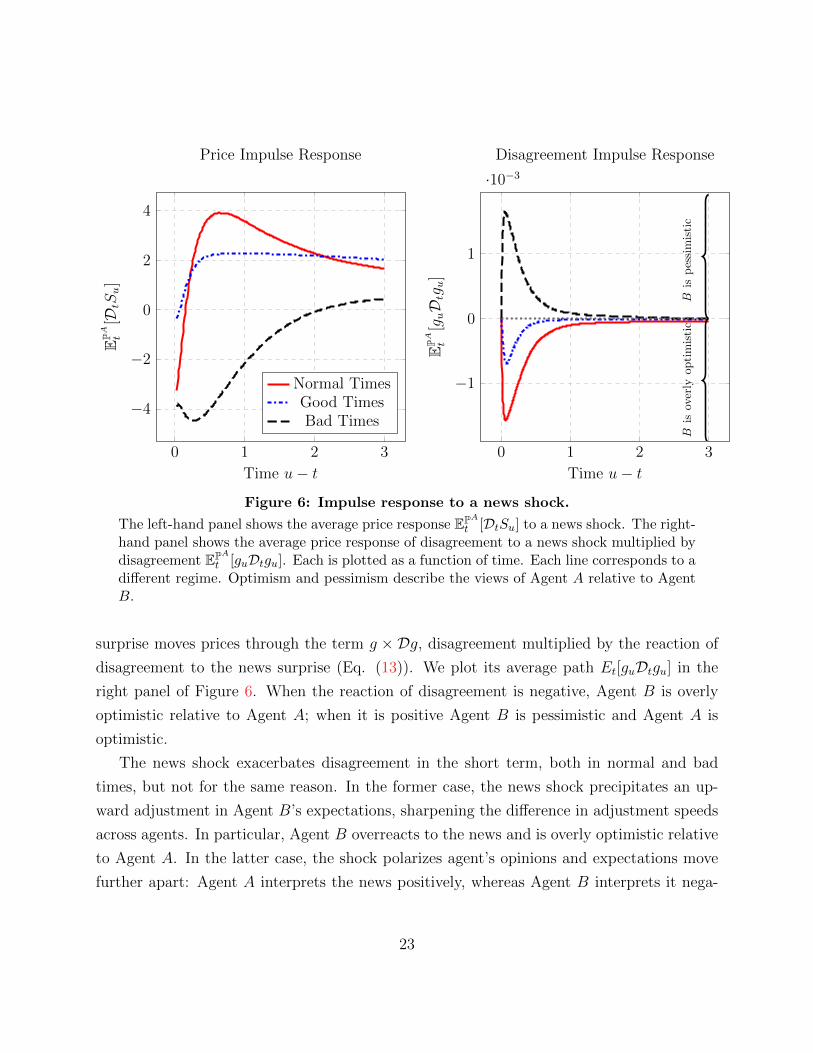

surprise moves prices through the term g × Dg, disagreement multiplied by the reaction of

disagreement to the news surprise (Eq. (13)). We plot its average path Et[guDtgu] in the

right panel of Figure 6. When the reaction of disagreement is negative, Agent B is overly

optimistic relative to Agent A; when it is positive Agent B is pessimistic and Agent A is

optimistic.

The news shock exacerbates disagreement in the short term, both in normal and bad

times, but not for the same reason. In the former case, the news shock precipitates an up-

ward adjustment in Agent B’s expectations, sharpening the difference in adjustment speeds

across agents. In particular, Agent B overreacts to the news and is overly optimistic relative

to Agent A. In the latter case, the shock polarizes agent’s opinions and expectations move

further apart: Agent A interprets the news positively, whereas Agent B interprets it nega-

23

tively. In good times, the reaction of disagreement is similar to that in normal times; it is,

however, less pronounced and less persistent.

We now study how the reaction of disagreement drives the reaction of prices. We plot

the 3-year average price response to a news shock today in the left panel of Figure 6. As

the news surprise hits, the price experiences an initial drop. In bad times (the black dashed

line), agents interpret the news in opposite ways and their dispute slows down the price

adjustment to the news shock. Because Agent B is pessimistic, the price continues to react

negatively to the news. The price then slowly corrects as opinions gradually align. In normal

times (the solid red line), while agents interpret the news shock in similar ways, Agent B

overreacts. Because Agent B is overly optimistic relative to Agent A, the price continues

to react positively to the news. The price then slowly corrects as Agent A catches up with

Agent B. In good times (the dash-dotted blue line), the news induces little disagreement

and prices revert immediately. Hence, the content of news predicts future returns (Tetlock,

2007) and this effect concentrates in bad times (Garcia, 2013).

Overall, in our model, prices continue to react to news only if disagreement spikes in

the short term. The polarization of opinions and the difference in adjustment speeds then

drive the direction of the price reaction. In bad times, Agent B’s pessimism slows down the

price reaction to the shock (decreasing reaction). In normal times, Agent B’s overreaction

accelerates the price response to the shock (increasing reaction). The former result resembles

the continuing under-reaction of Hong and Stein (1999), while the latter result is similar to

the continuing over-reaction of Daniel et al. (1998). Our emphasis is that these two effects

may alternate over the business cycle.

We now turn to the implications of these price reaction patterns for the serial correlation

of returns.

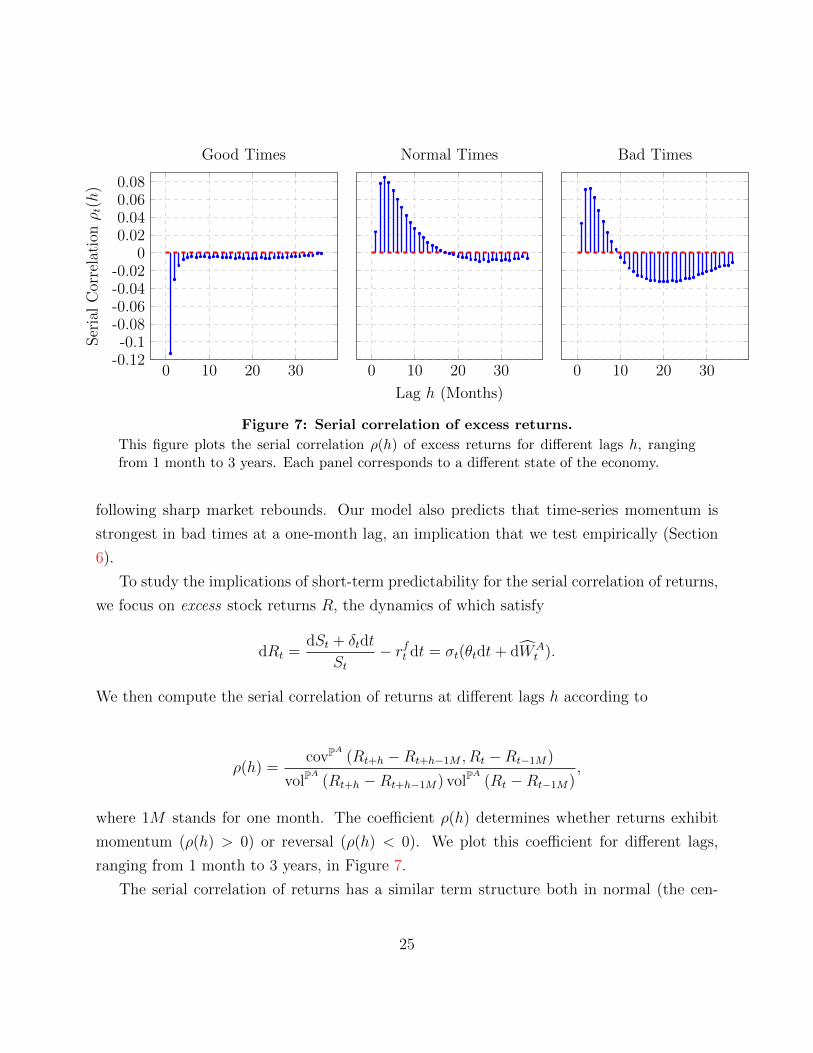

4.3 Implications for Time-Series Momentum and Momentum Crashes

One of the most pervasive facts in finance is momentum (Jegadeesh and Titman, 1993).

Recently, Moskowitz et al. (2012) uncover a similar pattern in the time-series of returns,

which they coin “time-series momentum”. Time-series momentum is a direct implication of

our previous results. In this section, we show that countercyclical disagreement can explain

both the term structure of time-series momentum and crashes in time-series momentum

24

0 10 20 30-0.12-0.1

-0.08-0.06-0.04-0.02

00.020.040.060.08

Ser

ial

Cor

rela

tion

ρt(h

)

Good Times

0 10 20 30

Lag h (Months)

Normal Times

0 10 20 30

Bad Times

Figure 7: Serial correlation of excess returns.

This figure plots the serial correlation ρ(h) of excess returns for different lags h, rangingfrom 1 month to 3 years. Each panel corresponds to a different state of the economy.

following sharp market rebounds. Our model also predicts that time-series momentum is

strongest in bad times at a one-month lag, an implication that we test empirically (Section

6).

To study the implications of short-term predictability for the serial correlation of returns,

we focus on excess stock returns R, the dynamics of which satisfy

dRt =dSt + δtdt

St− rft dt = σt(θtdt+ dWA

t ).

We then compute the serial correlation of returns at different lags h according to

ρ(h) =covPA (Rt+h −Rt+h−1M , Rt −Rt−1M)

volPA

(Rt+h −Rt+h−1M) volPA

(Rt −Rt−1M),

where 1M stands for one month. The coefficient ρ(h) determines whether returns exhibit

momentum (ρ(h) > 0) or reversal (ρ(h) < 0). We plot this coefficient for different lags,

ranging from 1 month to 3 years, in Figure 7.

The serial correlation of returns has a similar term structure both in normal (the cen-

25

ter panel) and in bad times (the right panel). In particular, returns exhibit time-series

momentum over an horizon of 10 to 15 months, followed by reversal over subsequent hori-

zons. Moreover, the magnitude of momentum varies according to the horizon considered:

momentum is large at short horizons (up to three months) and then decays over longer

horizons. Both the magnitude and the time horizon of these effects are line with empirical

evidence. Moskowitz et al. (2012) find significant time-series momentum at short horizons

(1 to 6 months), weaker momentum at intermediate horizons (7 to 15 months), and reversal

at longer horizons. The pattern of serial correlation in our model is particularly consistent

with that documented for equity and commodities.

Based on our previous results, time-series momentum arises in our model because prices

continue to react to past news through the spike in disagreement. Hence, although similar,

the term structures of momentum in normal and in bad times differ in two respects. First,

because the price reaction to news shock is more persistent in normal times (see Figure

6), momentum persists over a longer horizon in that regime. Second, because the spike in

disagreement induced by the polarization of opinions is sharper than that induced by the

difference in adjustment speeds, momentum at a one-month lag is significantly larger in bad

times. This second implication finds strong empirical support (see Section 6).

Excess returns have different time-series properties in good times (the left panel). In

particular, returns exhibit strong reversal in the very short term and weak reversal over

subsequent months. The reason is that, in good times, the main force driving prices is

reversion to fundamentals, as opposed to disagreement (see Figure 6). Specifically, the

following mechanism operates. Suppose there is a bad news today. Investors, who want to

smooth consumption over time, save by increasing their holdings in the stock, thus causing

an immediate price increase. As the fundamental reverts, they unwind part of their stock

holdings, leading to a price decrease and thus to reversal.

An important consequence of the initial reversal spike in good times is that a time-series

momentum strategy may crash if the market rises sharply. To see this, suppose we start

implementing a momentum strategy in bad times. The right panel then indicates that this

strategy remains profitable as long as the market does not rise suddenly, i.e., as long as the

economy does not transit suddenly from bad to good times. If, instead, the market sharply

rebounds, the trend suddenly reverts and the momentum strategy crashes. Sharp trend

reversals typically occur at the end of financial crises. For instance, a time-series momentum

26

crash occurred at the end of the Global Financial Crisis in March, April and May of 2009

(Moskowitz et al., 2012). Daniel and Moskowitz (2013) and Barroso and Santa-Clara (2014)

document a similar phenomenon in the cross-section of stocks.

5 Trading Strategies and Momentum Timing

Evidence suggests that institutional investors exploit variations in return predictability to

time the market.22 In this section, our objective is to identify the trading strategy that

allows an investor to take advantage of short-term predictability over the business cycle. We

focus on the strategy of the long-term investor, Agent A. We show that she implements

a momentum strategy in bad and normal times and follows a contrarian strategy in good

times. Because predictability increases as economic conditions deteriorate, her strategy

makes significantly more money in bad times. In addition, we show that trading volume

is countercyclical and positively related to short-term momentum (Lee and Swaminathan

(2000)).

To identify Agent A’s trading strategy, we compute her wealth and deduce from it the

two components of her strategy. We highlight Agent A’s wealth in Proposition 4 below.

Proposition 4. Agent A’s wealth, V , satisfies

Vt = EPAt

[∫ ∞t

ξuξtcAudu

]= δtω (ηt)

αα−1∑j=0

(α− 1

j

)(1− ω (ηt)

ω (ηt)

)jEPAt

[∫ ∞t

e−ρ(u−t)(ηuηt

) jα(δuδt

)1−α

du

](α=2)

= δtω (ηt)2 Stδt

∣∣∣∣O.U.

+ δtω (ηt) (1− ω (ηt))F(fAt , gt

). (14)

Proof. See Dumas et al. (2009).

22Moskowitz (2000), Glode (2011), and Kosowski (2011) show that fund managers perform significantlybetter in recessions than in expansions. Kacperczyk et al. (2013) provide evidence that fund managers timethe market in recessions and pick stocks in expansions.

27

Our calibration (α = 2) implies that Agent A’s wealth is the sum of two terms, both

of which have an intuitive interpretation. If Agent A were the only agent populating the

economy, she would hold one unit of the stock over time, otherwise markets would not

clear. For that reason, her wealth would be exactly equal to the price that prevails in a

representative agent economy, hence the first term in Eq. (14). But, because she can trade

with Agent B, her portfolio fluctuates over time; it fluctuates in a way that reflects both her

expectations of the fundamental and how they differ from Agent B’s. The second term in

Eq. (14) precisely accounts for that. In particular, the function F is the price component

we plotted in Figure 3, which represents how the interaction between fundamentals and

disagreement operates on prices.

From Agent A’s wealth, we now deduce the strategy she implements. We present her

strategy in Proposition 5.

Proposition 5. The number Q of shares held by Agent A satisfies

Q =1

σS

∂V∂δ

σδδ +∂V

∂fA

γ

σδ+∂V

∂g

γ −(fA − g − f l

)(fh + g − fA

)σδ

− ∂V

∂η

gη

σδ

, (15)

where σ denotes the diffusion of stock returns, which satisfies

σ = σδ +1

S

∂S

∂fA

γ

σδ+∂S

∂g

γ −(fA − g − f l

)(fh + g − fA

)σδ

− ∂S

∂η

gη

σδ

. (16)

The number of shares Q ≡ M + H can be further decomposed into a myopic portfolio M =µ−rfασ2

VS

and a hedging portfolio

H = Q−M =α− 1

ασtStEPAt

[∫ ∞t

ξsξtcAs

(Dtξsξs− Dtξt

ξt

)ds

]. (17)

Proof. See Appendix A.7.

Agent A’s portfolio in Equation (15) has two parts. The first part, M , is a myopic

demand through which Agent A seeks to extract the immediate Sharpe ratio. The second

term, H, is an hedging demand through which Agent A seeks to exploit return predictability.

28

0 0.5 1 1.5 2 2.5 3

−1

−0.5

0

0.5

1

Contrariantrading

Momentumtrading

Time

Cor

r(dH,dP

)

Bad TimesNormal TimesGood Times

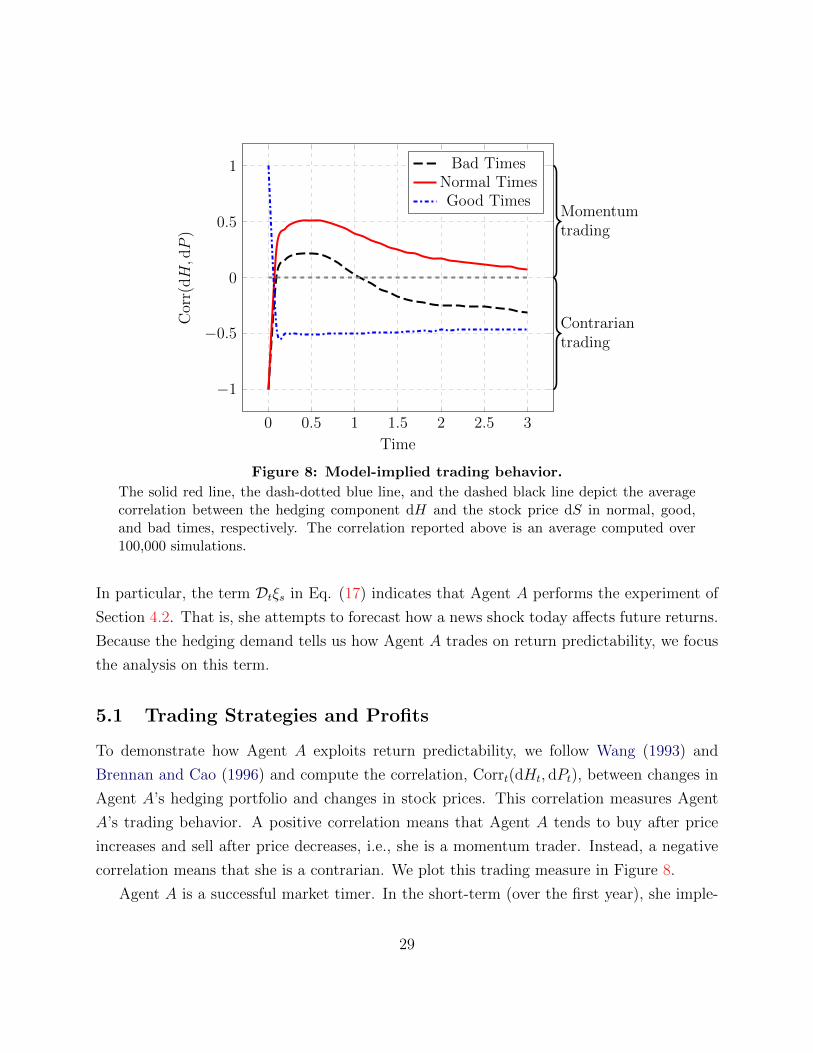

Figure 8: Model-implied trading behavior.

The solid red line, the dash-dotted blue line, and the dashed black line depict the averagecorrelation between the hedging component dH and the stock price dS in normal, good,and bad times, respectively. The correlation reported above is an average computed over100,000 simulations.

In particular, the term Dtξs in Eq. (17) indicates that Agent A performs the experiment of

Section 4.2. That is, she attempts to forecast how a news shock today affects future returns.

Because the hedging demand tells us how Agent A trades on return predictability, we focus

the analysis on this term.

5.1 Trading Strategies and Profits

To demonstrate how Agent A exploits return predictability, we follow Wang (1993) and

Brennan and Cao (1996) and compute the correlation, Corrt(dHt, dPt), between changes in

Agent A’s hedging portfolio and changes in stock prices. This correlation measures Agent

A’s trading behavior. A positive correlation means that Agent A tends to buy after price

increases and sell after price decreases, i.e., she is a momentum trader. Instead, a negative

correlation means that she is a contrarian. We plot this trading measure in Figure 8.

Agent A is a successful market timer. In the short-term (over the first year), she imple-

29

ments a momentum strategy both in normal times (the solid red line) and in bad times (the

dashed black line). In particular, Agent A anticipates that prices will continue to react to

news shocks in normal and bad times. Continuing price reaction in turn generates time-series

momentum, which she extracts by implementing a momentum strategy. Moreover, Agent

A recognizes that time-series momentum reverts faster in bad times than in normal times.

Therefore, in bad times, she eventually reverts her strategy and becomes a contrarian. In

good times, Agent A exclusively engages in contrarian trading (the dash-dotted blue line).

She anticipates that reversion to fundamentals will be fast and strong, and consistently

reverts her strategy. Doing so, she avoids crashes in time-series momentum and exploits

reversal.

Agent B takes the other side of the market. In normal times, because Agent A—the long-

term investor—is a momentum trader, Agent B—the short-term investor—is a contrarian.

Our model therefore predicts that long-term investors tend to be momentum traders, while

short-term investors tend to be contrarians. This prediction is in line with Goetzmann

and Massa (2002), who show that infrequent traders follow momentum strategies, whereas

frequent traders are contrarians.

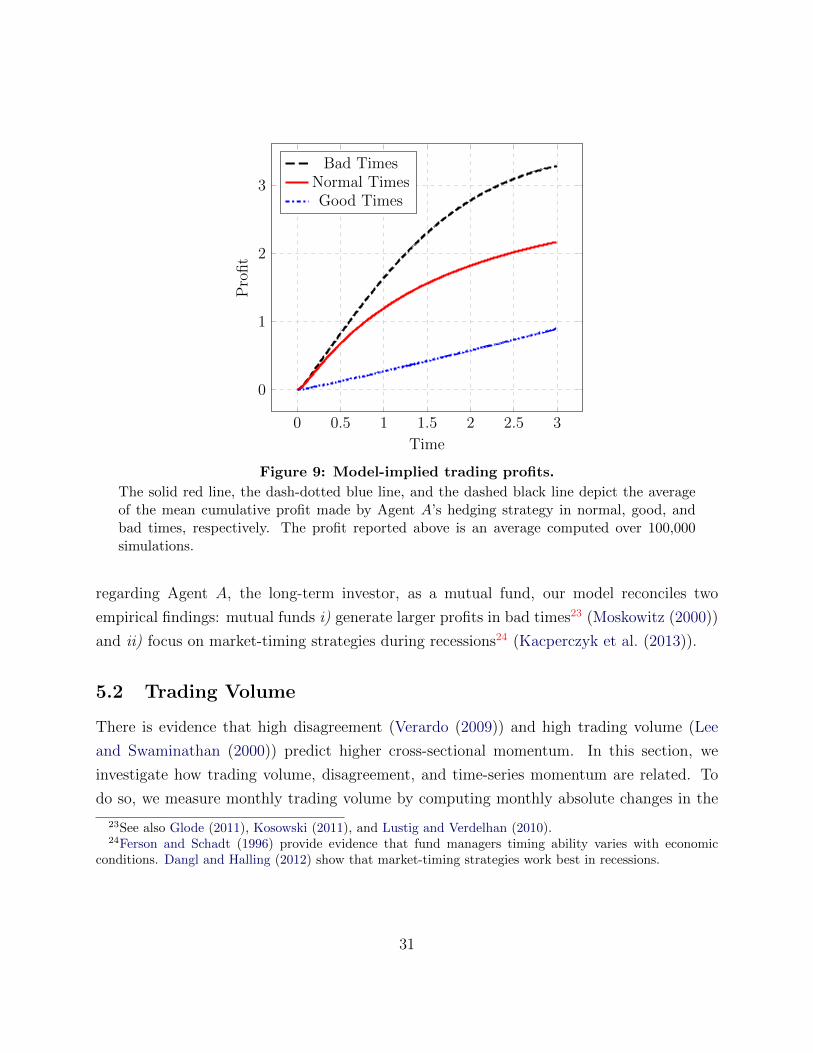

We now want to understand in which state of the business cycle Agent A’s strategy is

most profitable. To do so, we compute the mean cumulative profit P that her strategy

generates. It satisfies

Pt =

∫ t

0

(QuSu −

µu − rfuασ2

u

Vu

)(µu − rfu

)du =

∫ t

0

HuSu(µu − rfu

)du. (18)

The profits in Eq. (18) represents the cumulative expected dollar amount made by following

a fully leveraged dynamic strategy that consists in borrowing HS dollars in the bond and

investing this amount in the stock. We plot the average cumulative profit P in Figure 9.

The profits that Agent A’s strategy generates are smallest in good times and largest in

bad times. The reason is as follows. In good times, prices accommodate news shocks almost

instantly, which makes it challenging for Agent A to reap large profits. In normal and bad

times, however, stock prices exhibit short-term predictability (continuing price reaction).

Agent A exploits this information to make larger profits. In particular, Agent A makes the

largest profits in bad times, that is when short-term predictability is strongest. Time-series

momentum therefore delivers larger profits in bad times (Moskowitz et al., 2012). Moreover,

30

0 0.5 1 1.5 2 2.5 3

0

1

2

3

Time

Pro

fit

Bad TimesNormal TimesGood Times

Figure 9: Model-implied trading profits.

The solid red line, the dash-dotted blue line, and the dashed black line depict the averageof the mean cumulative profit made by Agent A’s hedging strategy in normal, good, andbad times, respectively. The profit reported above is an average computed over 100,000simulations.

regarding Agent A, the long-term investor, as a mutual fund, our model reconciles two

empirical findings: mutual funds i) generate larger profits in bad times23 (Moskowitz (2000))

and ii) focus on market-timing strategies during recessions24 (Kacperczyk et al. (2013)).

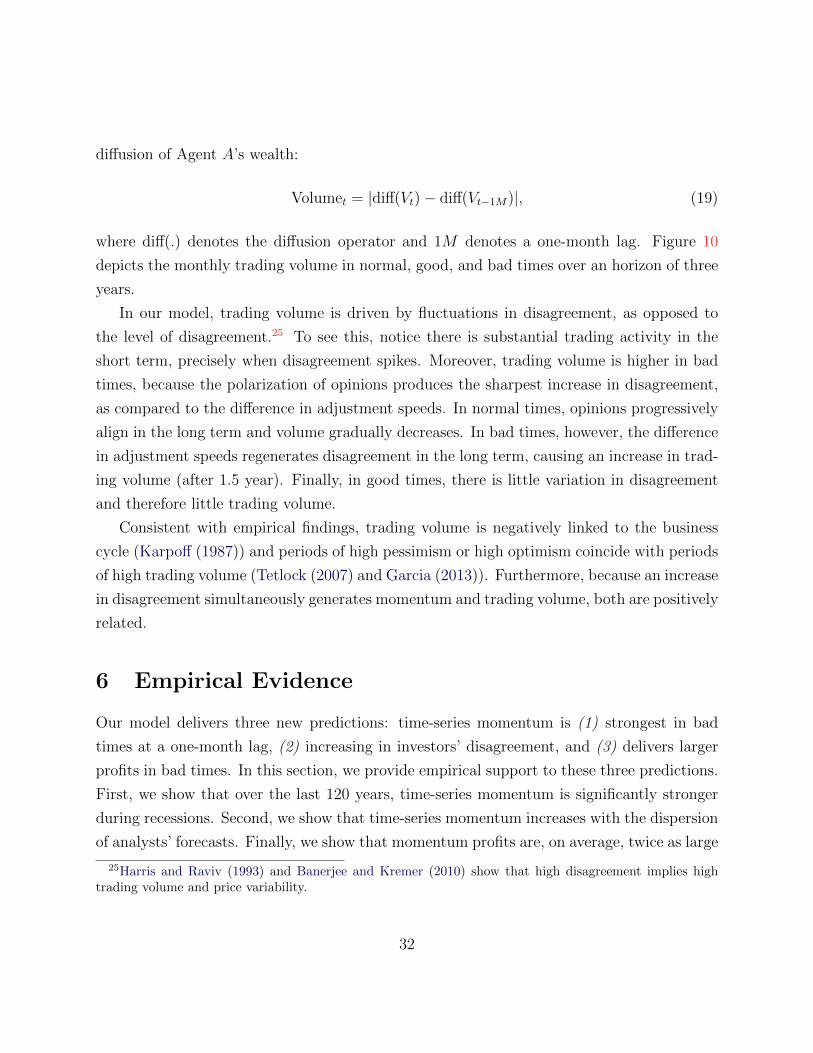

5.2 Trading Volume

There is evidence that high disagreement (Verardo (2009)) and high trading volume (Lee

and Swaminathan (2000)) predict higher cross-sectional momentum. In this section, we

investigate how trading volume, disagreement, and time-series momentum are related. To

do so, we measure monthly trading volume by computing monthly absolute changes in the

23See also Glode (2011), Kosowski (2011), and Lustig and Verdelhan (2010).24Ferson and Schadt (1996) provide evidence that fund managers timing ability varies with economic

conditions. Dangl and Halling (2012) show that market-timing strategies work best in recessions.

31

diffusion of Agent A’s wealth:

Volumet = |diff(Vt)− diff(Vt−1M)|, (19)

where diff(.) denotes the diffusion operator and 1M denotes a one-month lag. Figure 10

depicts the monthly trading volume in normal, good, and bad times over an horizon of three

years.

In our model, trading volume is driven by fluctuations in disagreement, as opposed to

the level of disagreement.25 To see this, notice there is substantial trading activity in the

short term, precisely when disagreement spikes. Moreover, trading volume is higher in bad

times, because the polarization of opinions produces the sharpest increase in disagreement,

as compared to the difference in adjustment speeds. In normal times, opinions progressively

align in the long term and volume gradually decreases. In bad times, however, the difference

in adjustment speeds regenerates disagreement in the long term, causing an increase in trad-

ing volume (after 1.5 year). Finally, in good times, there is little variation in disagreement

and therefore little trading volume.

Consistent with empirical findings, trading volume is negatively linked to the business

cycle (Karpoff (1987)) and periods of high pessimism or high optimism coincide with periods

of high trading volume (Tetlock (2007) and Garcia (2013)). Furthermore, because an increase

in disagreement simultaneously generates momentum and trading volume, both are positively

related.

6 Empirical Evidence

Our model delivers three new predictions: time-series momentum is (1) strongest in bad

times at a one-month lag, (2) increasing in investors’ disagreement, and (3) delivers larger

profits in bad times. In this section, we provide empirical support to these three predictions.

First, we show that over the last 120 years, time-series momentum is significantly stronger

during recessions. Second, we show that time-series momentum increases with the dispersion

of analysts’ forecasts. Finally, we show that momentum profits are, on average, twice as large

25Harris and Raviv (1993) and Banerjee and Kremer (2010) show that high disagreement implies hightrading volume and price variability.

32

0 0.5 1 1.5 2 2.5 3

0

0.1

0.2

0.3

0.4

0.5

Time

Tra

din

gV

olum

e

Bad TimesNormal TimesGood Times

Figure 10: Model-implied trading volume.

The solid red line, the dash-dotted blue line, and the dashed black line depict the tradingvolume in normal, good, and bad times, respectively. The trading volume reported aboveis obtained by substituting the average paths (computed over 100,000 simulations) of thestate variables in our definition of trading volume (see Eq. (19)).

in recessions as they are in expansions.

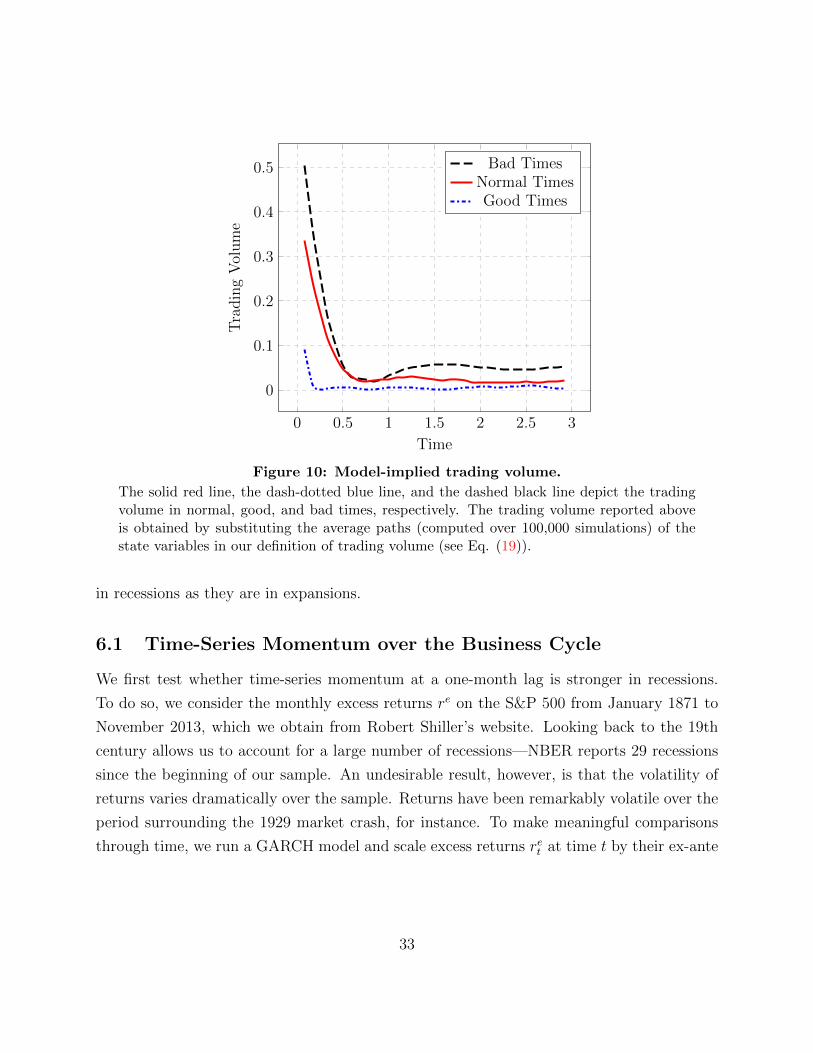

6.1 Time-Series Momentum over the Business Cycle

We first test whether time-series momentum at a one-month lag is stronger in recessions.

To do so, we consider the monthly excess returns re on the S&P 500 from January 1871 to

November 2013, which we obtain from Robert Shiller’s website. Looking back to the 19th

century allows us to account for a large number of recessions—NBER reports 29 recessions

since the beginning of our sample. An undesirable result, however, is that the volatility of

returns varies dramatically over the sample. Returns have been remarkably volatile over the

period surrounding the 1929 market crash, for instance. To make meaningful comparisons

through time, we run a GARCH model and scale excess returns ret at time t by their ex-ante

33

0 3 6 9 12−1

0

1

2

3

Lag h (Months)

β2,h

t-st

at

Excess Momentum: G(.) = sign(.)

0 3 6 9 12−1

0

1

2

3

Lag h (Months)β

2,h

t-st

at

Excess Momentum: G(.) = identity(.)

Figure 11: Excess time-series momentum during recessions.

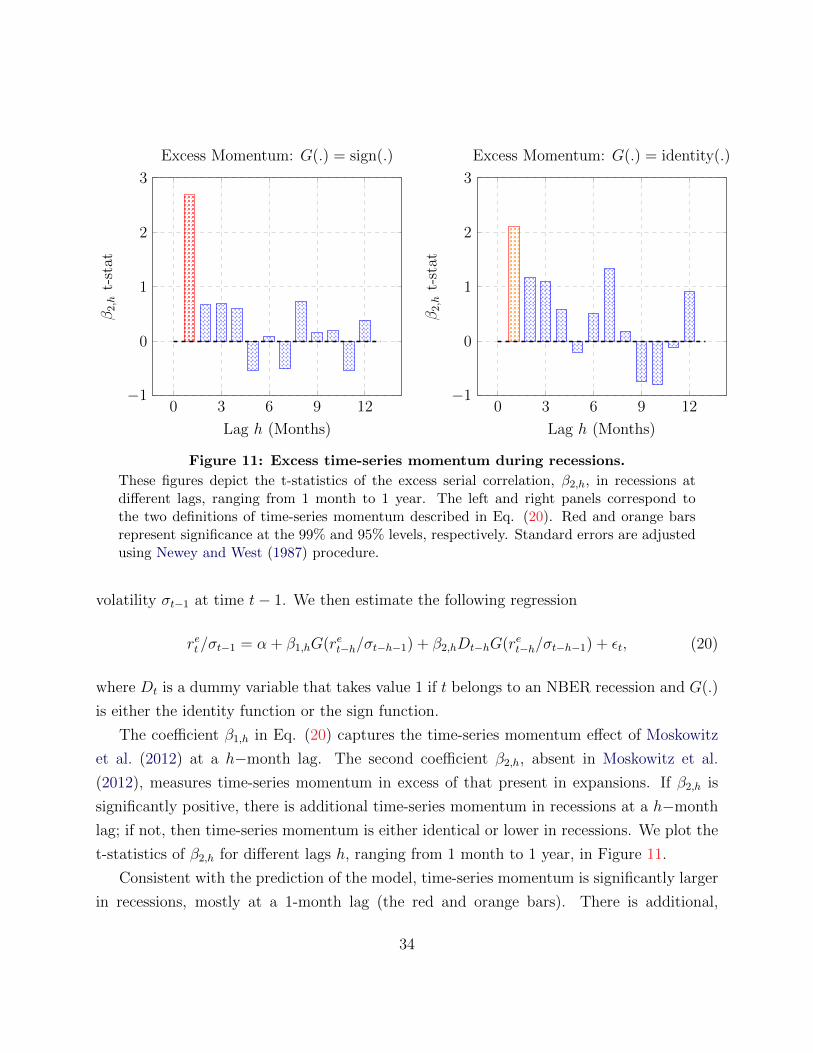

These figures depict the t-statistics of the excess serial correlation, β2,h, in recessions atdifferent lags, ranging from 1 month to 1 year. The left and right panels correspond tothe two definitions of time-series momentum described in Eq. (20). Red and orange barsrepresent significance at the 99% and 95% levels, respectively. Standard errors are adjustedusing Newey and West (1987) procedure.

volatility σt−1 at time t− 1. We then estimate the following regression

ret/σt−1 = α + β1,hG(ret−h/σt−h−1) + β2,hDt−hG(ret−h/σt−h−1) + εt, (20)

where Dt is a dummy variable that takes value 1 if t belongs to an NBER recession and G(.)

is either the identity function or the sign function.

The coefficient β1,h in Eq. (20) captures the time-series momentum effect of Moskowitz

et al. (2012) at a h−month lag. The second coefficient β2,h, absent in Moskowitz et al.

(2012), measures time-series momentum in excess of that present in expansions. If β2,h is

significantly positive, there is additional time-series momentum in recessions at a h−month

lag; if not, then time-series momentum is either identical or lower in recessions. We plot the

t-statistics of β2,h for different lags h, ranging from 1 month to 1 year, in Figure 11.

Consistent with the prediction of the model, time-series momentum is significantly larger

in recessions, mostly at a 1-month lag (the red and orange bars). There is additional,

34

although statistically insignificant, momentum in recessions up to the 4-month lag. Excess

momentum in recessions then vanishes over subsequent lags. In Section 6.3, we show that

superior predictability at a 1-month lag is sufficient to make significantly larger profits in

recessions than in expansions.

Our finding that time-series momentum is stronger in recessions contrasts with evidence

reported in the cross-section of returns. In particular, Chordia and Shivakumar (2002) and

Cooper, Gutierrez, and Hameed (2004) find that cross-sectional momentum is weaker in

down-markets than in up-markets. While Moskowitz et al. (2012) show that time-series and

cross-sectional momentum are strongly related, our results suggest that their relation varies

over the business cycle.

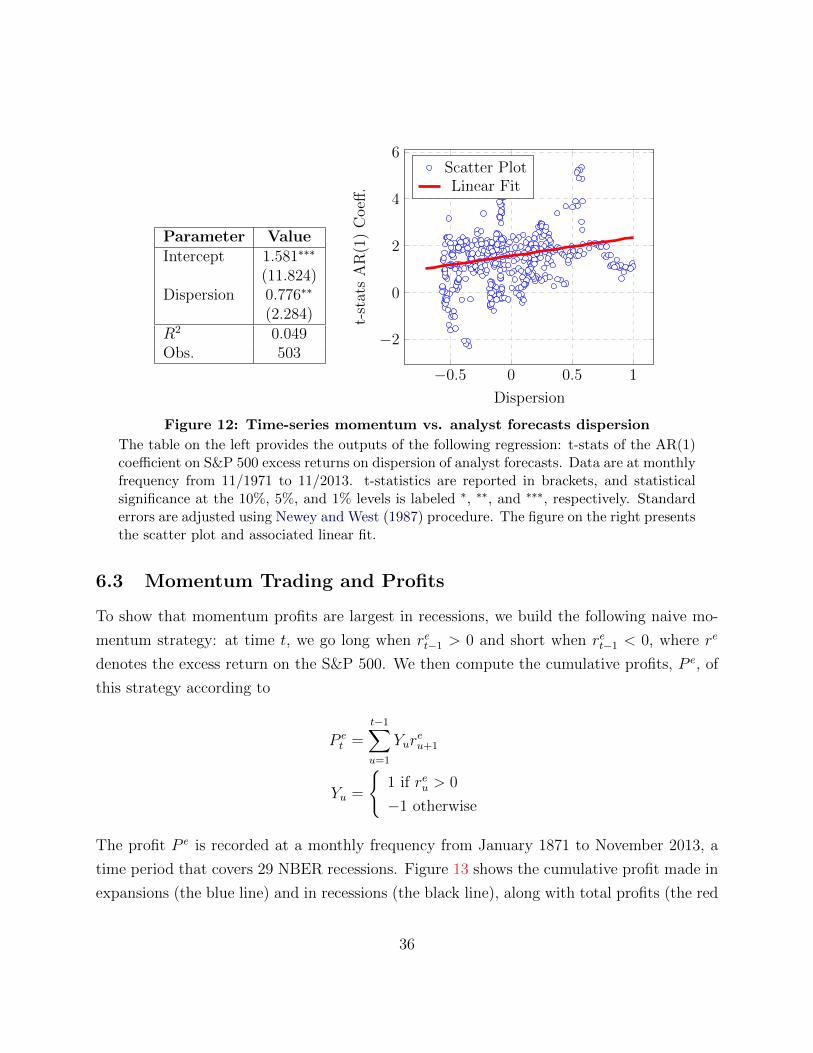

6.2 Time-Series Momentum and Disagreement

To test whether time-series momentum increases with disagreement, we proxy for disagree-

ment using the dispersion of analyst forecasts on the 1-quarter-ahead real GDP growth rate.

We consider the time-series of dispersion in analyst forecasts from 1968 to 2013, which we

obtain from the Federal Reserve Bank of Philadelphia’s website. This time-series exhibits

a strong linear downward trend and is only available quarterly. We therefore de-trend it

and interpolate it before computing a moving average over a 3-year rolling window to get a

measure of dispersion at the monthly frequency. We then construct a measure of time-series

momentum by computing the one-month lag serial correlation of excess returns on the S&P

500 over a 3-year rolling window.

We regress time-series momentum on our measure of disagreement and plot the result

in Figure 12. The data shows that there exists an increasing relation between time-series