Embed Size (px)

Citation preview

YOUR FINANCIAL FUTURE DEPENDS

ON YOU!

Personal Finance

Activity one

Complete the Millionaire game

Budgets

Do you have a budget?Why should you have a budget if you don’t?After considering what you spend money on,

where can you cut so that you can save that money?

How can a budget help you achieve your financial goals?? Short term and long term?

A budget – get one!!

A budget is the first step to financial success!Stick with the budget. Don’t just create one –

USE ONE!Budgets help us see where our money is

going and how we can cut to save money for our short term and long term goals.

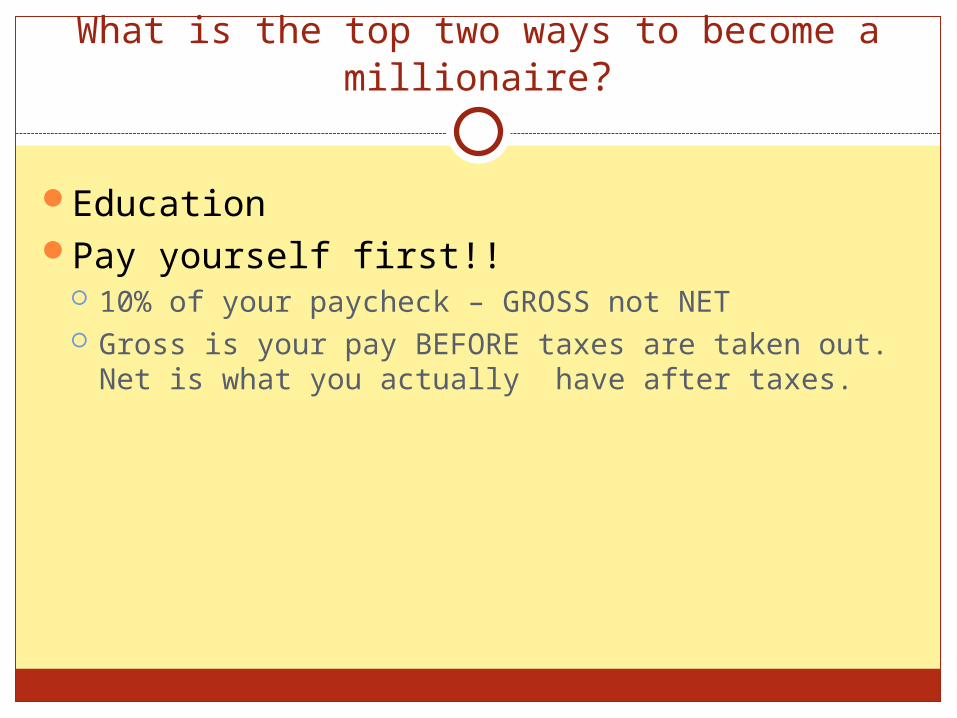

What is the top two ways to become a millionaire?

EducationPay yourself first!!

10% of your paycheck – GROSS not NET Gross is your pay BEFORE taxes are taken out. Net is

what you actually have after taxes.

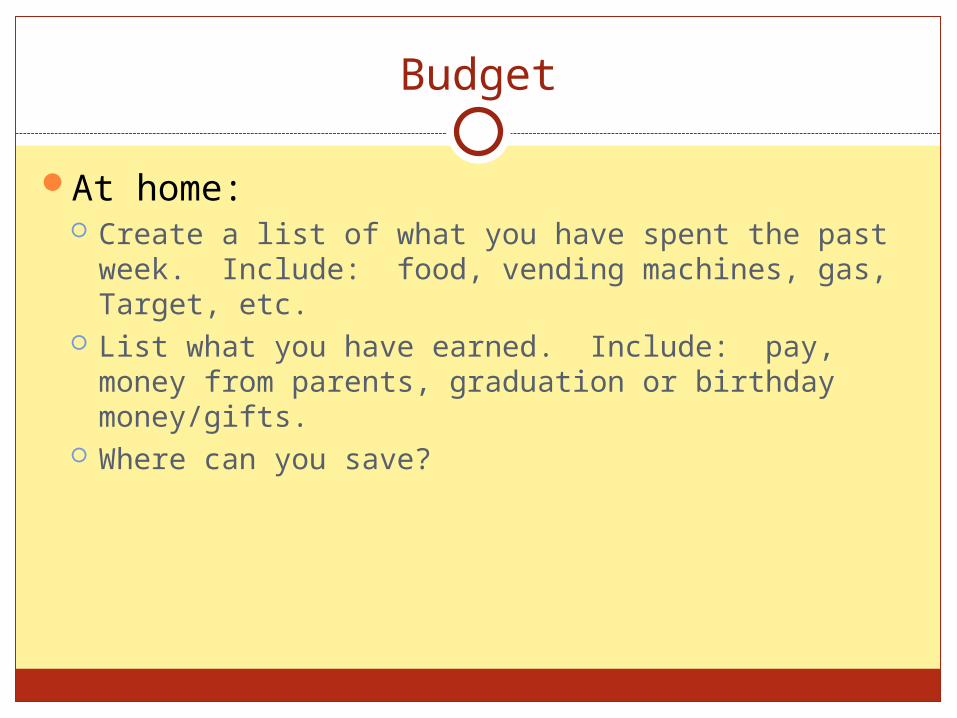

Budget

At home: Create a list of what you have spent the past week.

Include: food, vending machines, gas, Target, etc. List what you have earned. Include: pay, money from

parents, graduation or birthday money/gifts. Where can you save?

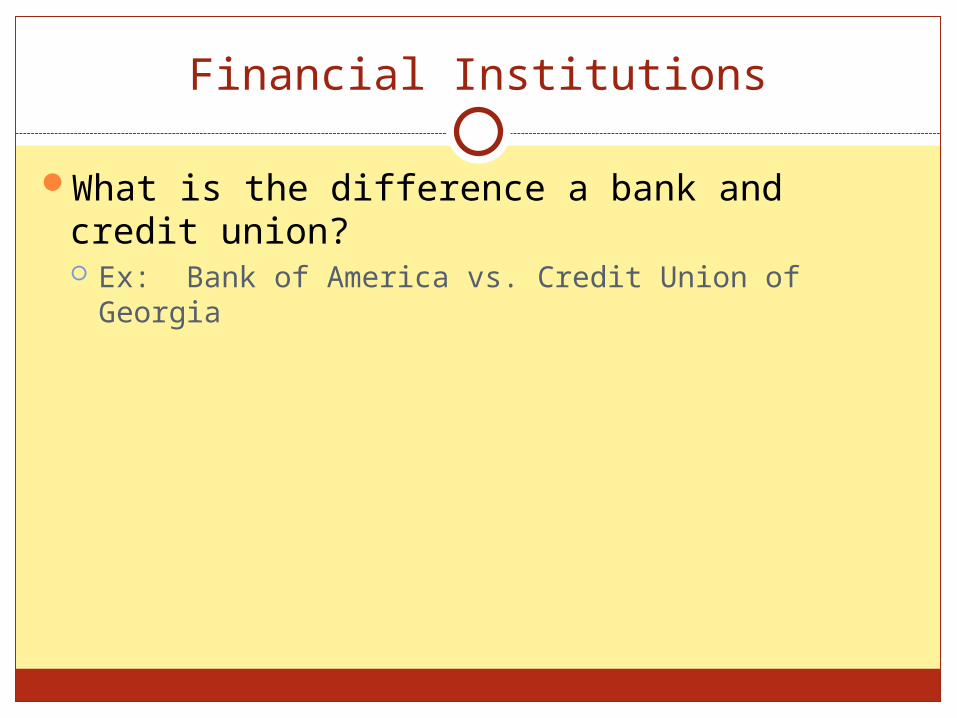

Financial Institutions

What is the difference a bank and credit union? Ex: Bank of America vs. Credit Union of Georgia

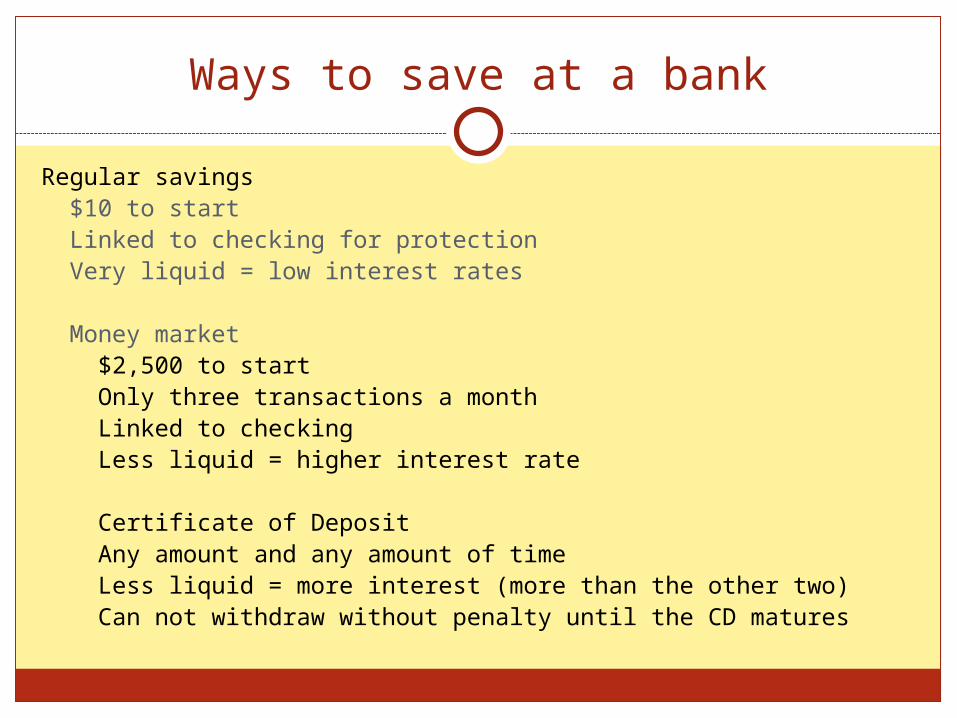

Ways to save at a bank

Regular savings$10 to startLinked to checking for protectionVery liquid = low interest rates

Money market$2,500 to startOnly three transactions a monthLinked to checkingLess liquid = higher interest rate

Certificate of DepositAny amount and any amount of timeLess liquid = more interest (more than the other two)Can not withdraw without penalty until the CD matures

Accounts

Which type of account will best fit your needs? WHY?

Credit Cards – Listen to your parents!

What have your parents told you or warned you about credit cards?

Credit cards….good or EVIL???

Good way to build credit Credit cards do go on your credit reportWhen shopping for a credit card, look for

APR – Annual percentage rate Introductory rates Late fees Any perks of the card

Good things about credit cards

It builds credit – proof of financial maturityIt allows you to buy nowIt is better for booking or securing a flight,

room, or depositIt is good to have for an emergencyYou do not pay interest unless you can not

pay off your card (balance) at the end of the month.

If used wisely, you can be debt free, but get the benefits of the card perks, like sky miles.

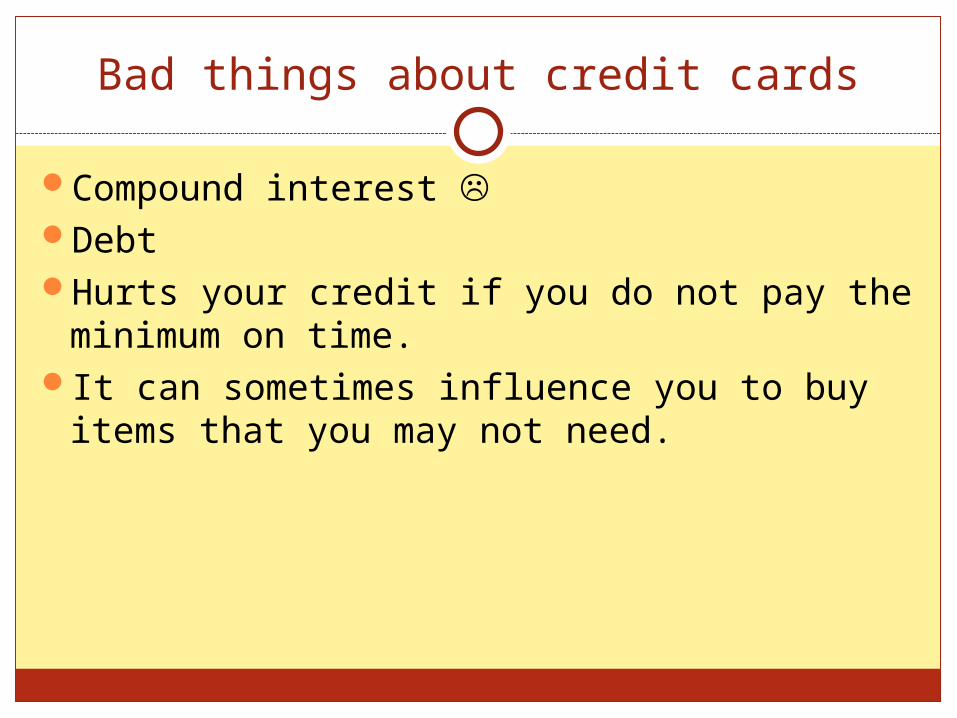

Bad things about credit cards

Compound interest DebtHurts your credit if you do not pay the

minimum on time.It can sometimes influence you to buy items

that you may not need.

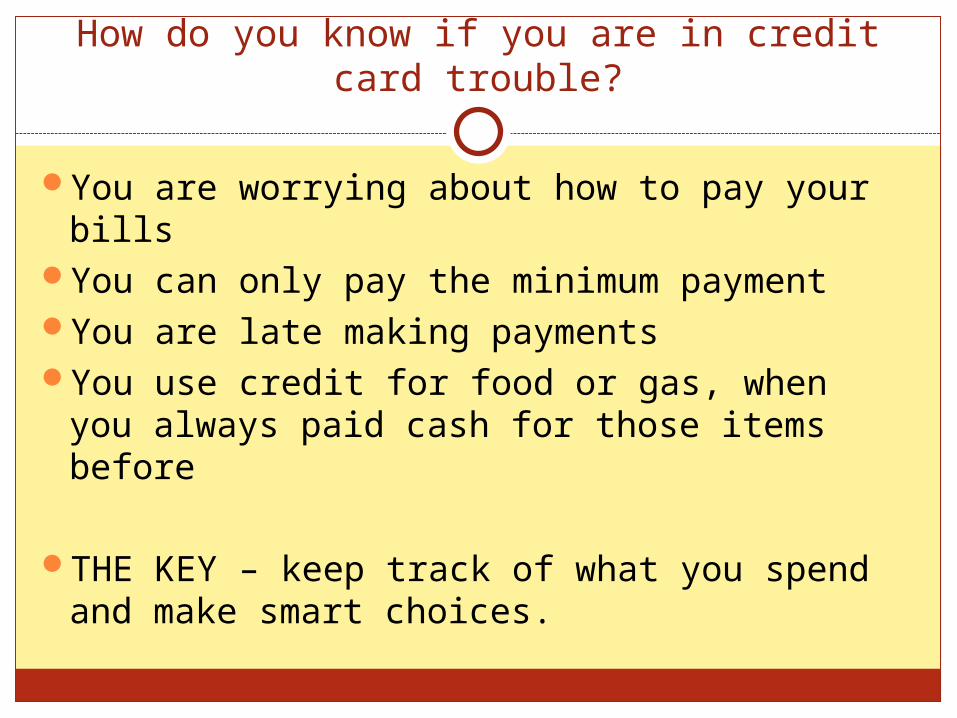

How do you know if you are in credit card trouble?

You are worrying about how to pay your billsYou can only pay the minimum paymentYou are late making paymentsYou use credit for food or gas, when you

always paid cash for those items before

THE KEY – keep track of what you spend and make smart choices.

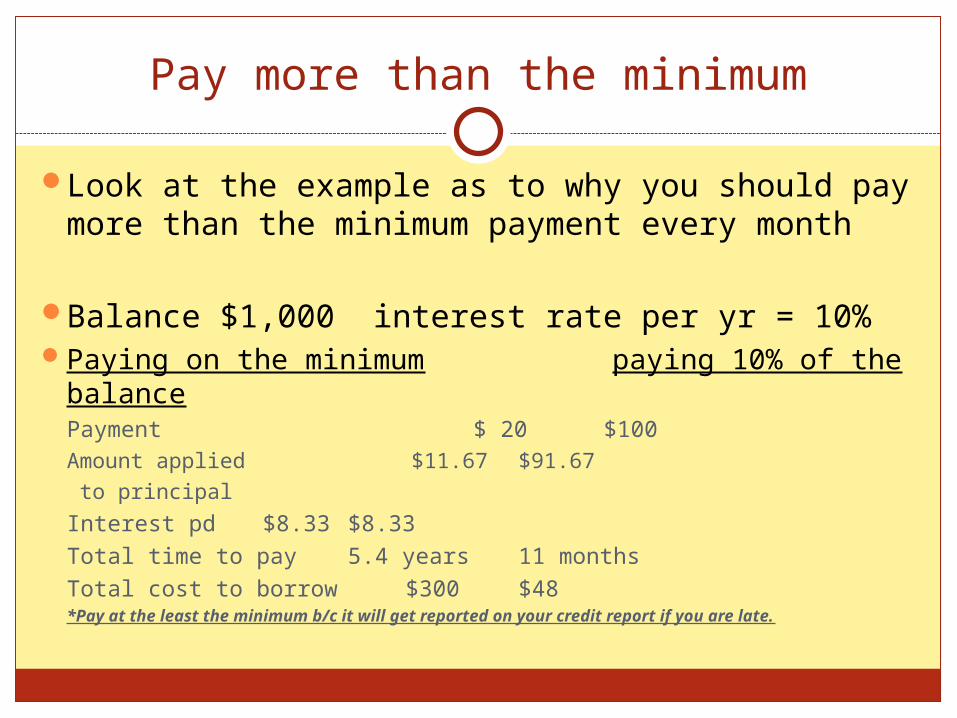

Pay more than the minimum

Look at the example as to why you should pay more than the minimum payment every month

Balance $1,000 interest rate per yr = 10%Paying on the minimum paying 10% of the

balancePayment $ 20 $100Amount applied $11.67 $91.67 to principal

Interest pd $8.33 $8.33Total time to pay 5.4 years 11 monthsTotal cost to borrow $300 $48*Pay at the least the minimum b/c it will get reported on your credit report if you are

late.

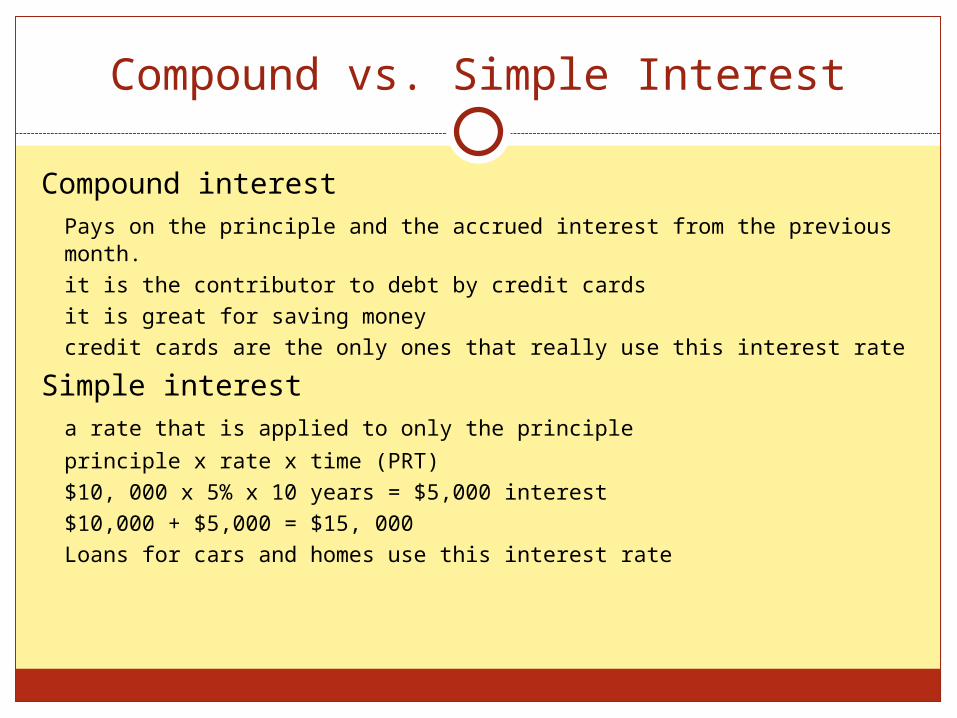

Compound vs. Simple Interest

Compound interestPays on the principle and the accrued interest from the previous month.

it is the contributor to debt by credit cards

it is great for saving money

credit cards are the only ones that really use this interest rate

Simple interesta rate that is applied to only the principle

principle x rate x time (PRT)

$10, 000 x 5% x 10 years = $5,000 interest

$10,000 + $5,000 = $15, 000

Loans for cars and homes use this interest rate

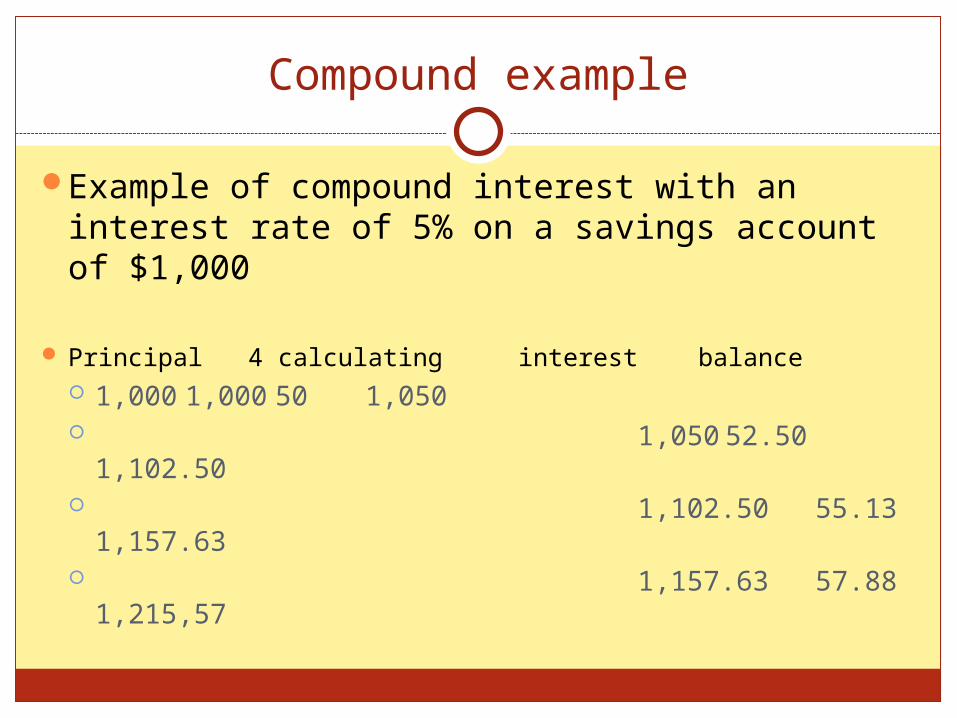

Compound example

Example of compound interest with an interest rate of 5% on a savings account of $1,000

Principal 4 calculating interestbalance 1,000 1,000 50 1,050 1,050 52.50

1,102.50 1,102.50 55.13 1,157.63 1,157.63 57.88 1,215,57

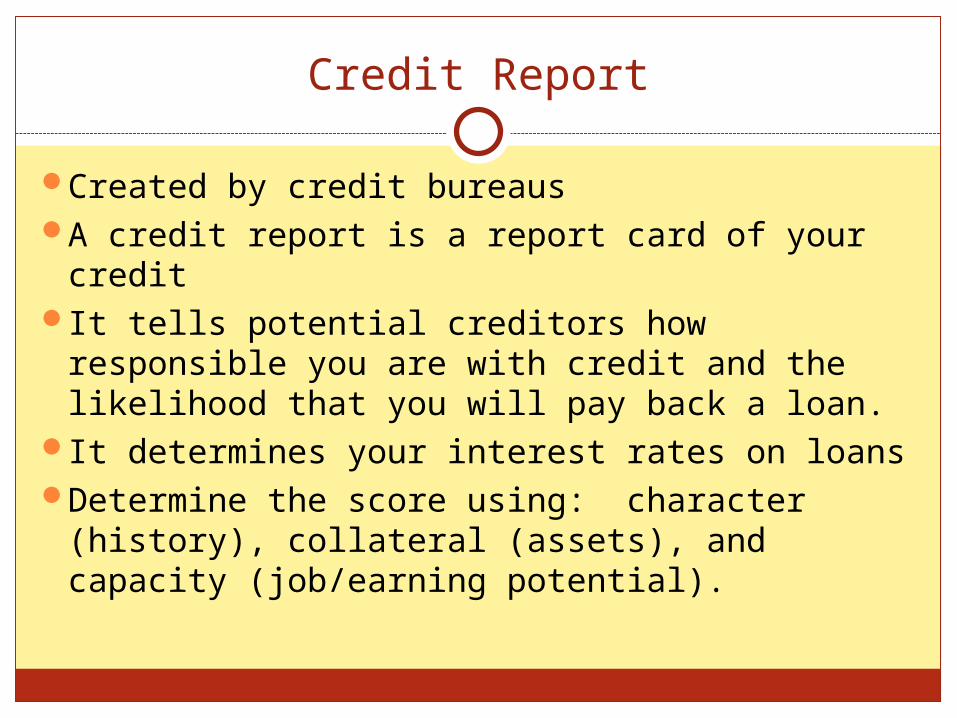

Credit Report

Created by credit bureausA credit report is a report card of your creditIt tells potential creditors how responsible

you are with credit and the likelihood that you will pay back a loan.

It determines your interest rates on loansDetermine the score using: character

(history), collateral (assets), and capacity (job/earning potential).

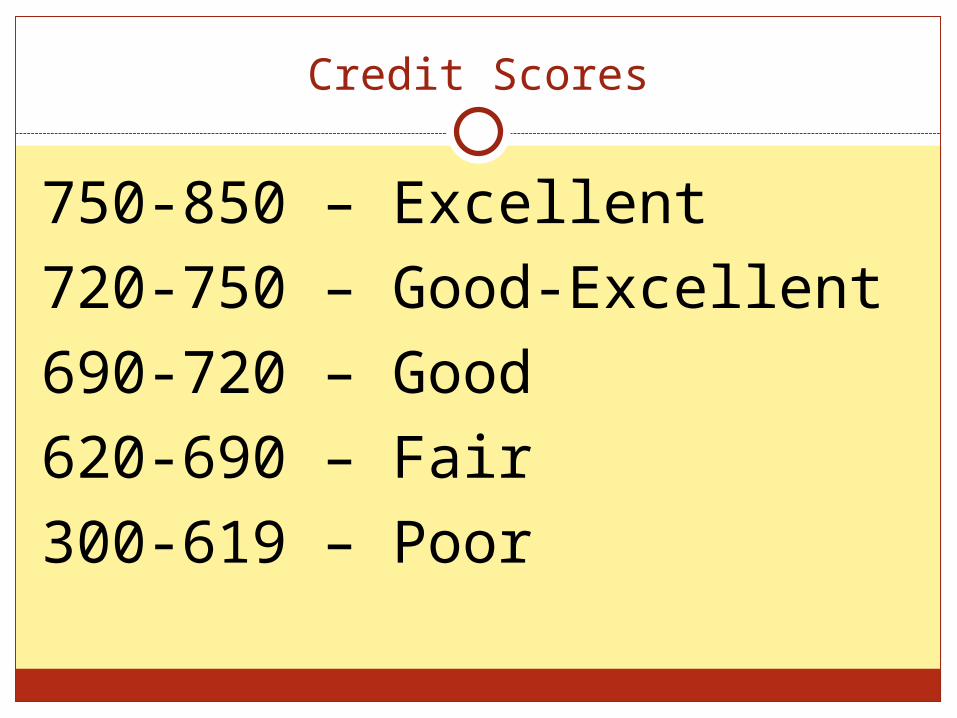

Credit Scores

750-850 – Excellent720-750 – Good-Excellent690-720 – Good620-690 – Fair300-619 – Poor

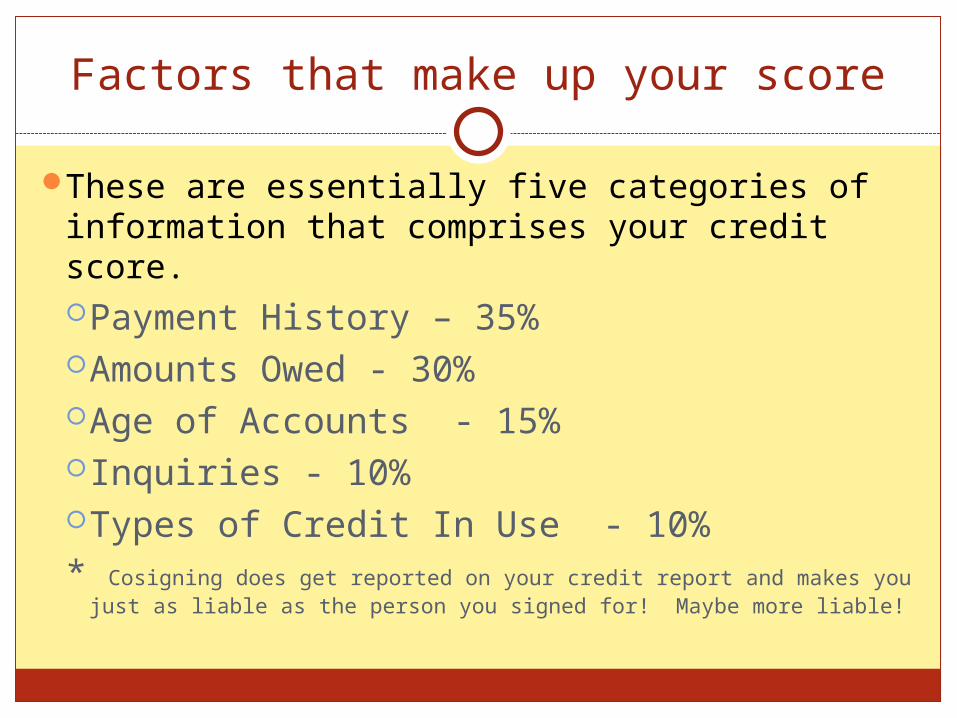

Factors that make up your score

These are essentially five categories of information that comprises your credit score.Payment History – 35%Amounts Owed - 30%Age of Accounts - 15%Inquiries - 10%Types of Credit In Use - 10%* Cosigning does get reported on your credit report and makes you just

as liable as the person you signed for! Maybe more liable!

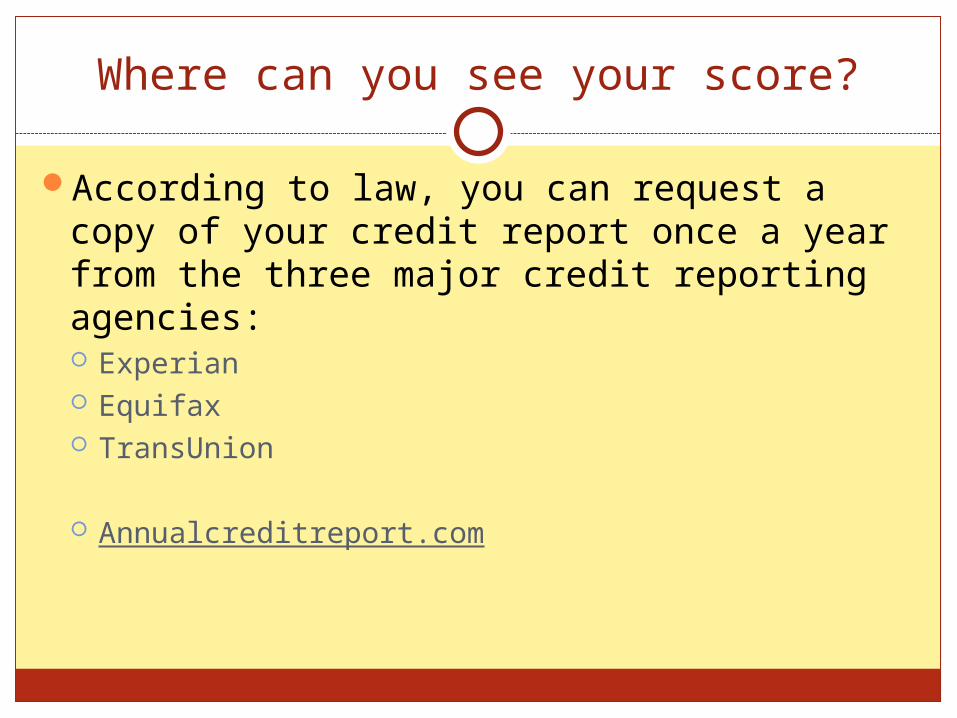

Where can you see your score?

According to law, you can request a copy of your credit report once a year from the three major credit reporting agencies: Experian Equifax TransUnion

Annualcreditreport.com

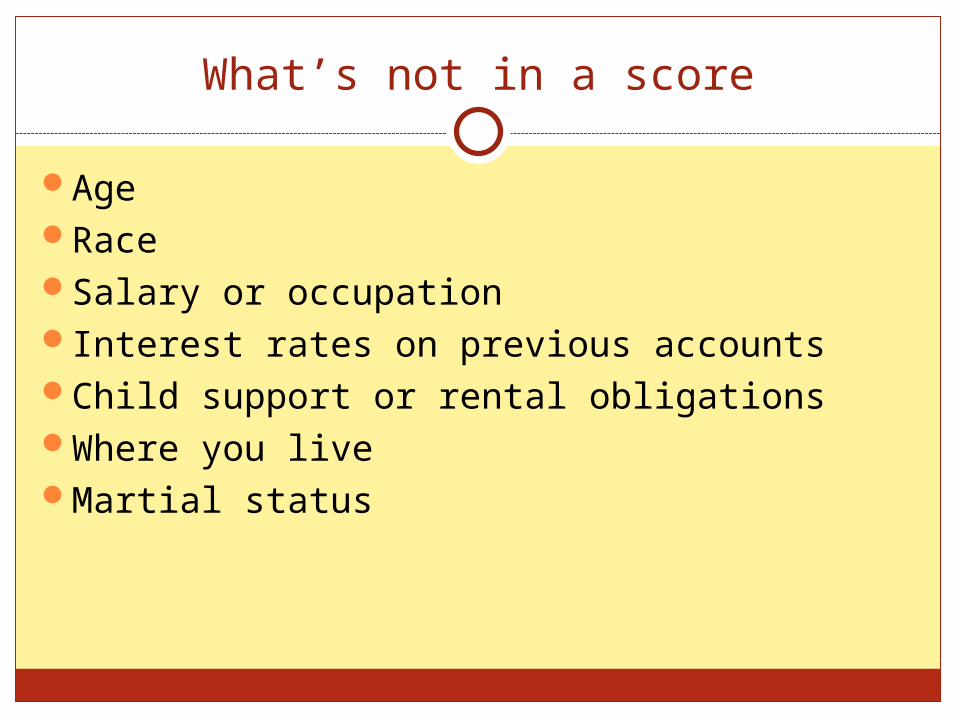

What’s not in a score

AgeRaceSalary or occupationInterest rates on previous accountsChild support or rental obligationsWhere you liveMartial status

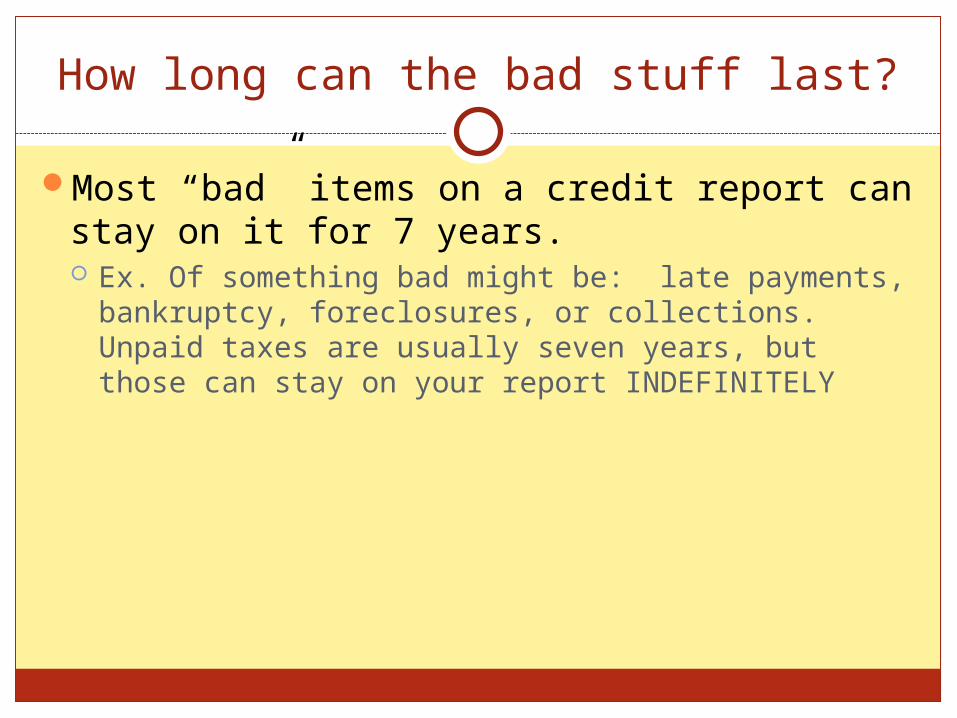

How long can the bad stuff last?

Most “bad” items on a credit report can stay on it for 7 years. Ex. Of something bad might be: late payments,

bankruptcy, foreclosures, or collections. Unpaid taxes are usually seven years, but those can stay on your report INDEFINITELY

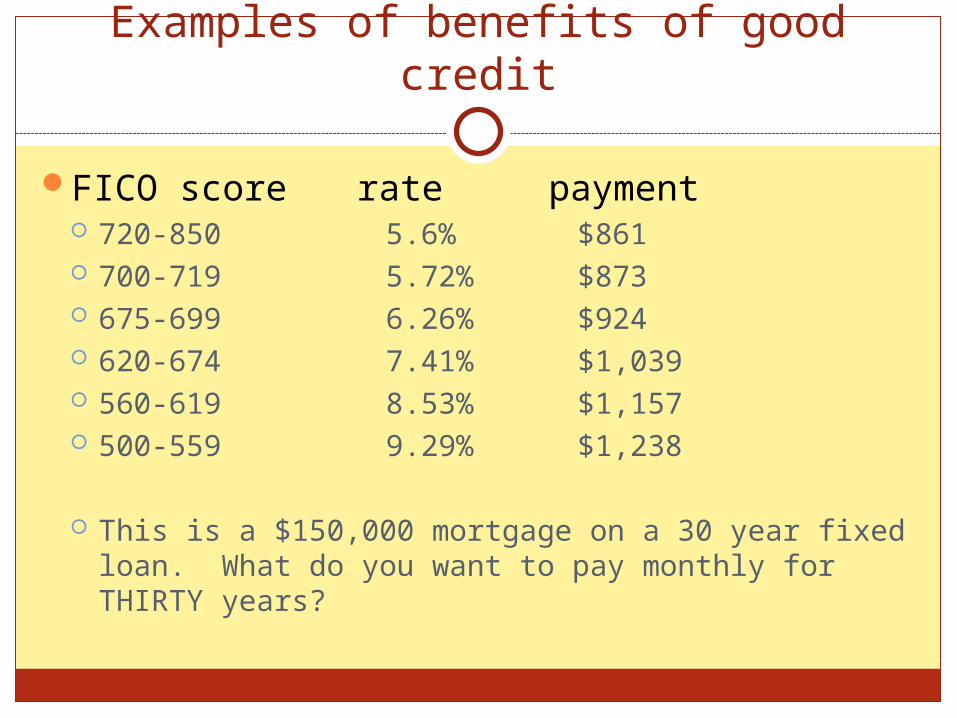

Examples of benefits of good credit

FICO score rate payment 720-850 5.6% $861 700-719 5.72% $873 675-699 6.26% $924 620-674 7.41% $1,039 560-619 8.53% $1,157 500-559 9.29% $1,238

This is a $150,000 mortgage on a 30 year fixed loan. What do you want to pay monthly for THIRTY years?

Cost/Benefits of credit

Costs – finance charges, late fees, costs may be higher for the item, danger of identity theft

Benefits – get the item now, get to take advantage of sales, easy to pay and keep track of spending, safer than cash

POSTER TIME

You and a partner are to make a credit card poster warning students about credit card abuse. In other words, make the poster informational about why to be careful when using credit cards.

You much include: Two warnings Two positives One visual

PAYDAY LOANSSTORE CARDSTITLE PAWN LOANS

Loans to stay away from..

Types of Insurance

Health – doctor, specialist, emergency room visitsLife – deathCar – protects you if you hit someone or if

someone hits you (liability vs. full coverage)Gap insurance – covers negative equity in the car

if the car is totaledDisability – coverage if you become disabled or

unable to work – about 60% of your incomeHomeowners – protects your home against fire,

burglary, natural disasterRenters – protects your property if you rent

Insurance

What does deductable mean?What does a premium mean?Where do I go to get insurance? Life, car, all

of it?

Fed and Fiscal Policy on your budget!

If the Government (Fiscal Policy) raises taxes, this could effect your paycheck and your budget. This will lower the amount of money that you have to pay bills, live on, and save. This could also affect your tax returns in April causing you to possibly have to pay the government instead of gaining a return. Gross Income – money earned BEFORE taxes are

taken Net Income – money that is on your paycheck – taxes

have already been taken out.

Fed and FP on your budget - Continued

If the Fed increases or lowers rates, this will affect your accounts and loans that you are considering – maybe a new house (a mortgage). It will not affect loans that you already have.

Types of taxes that come out of your income

State income tax – money paid to the state based on your income to fund state programs.

Federal Income tax – money paid to the Federal government based on your income to fund Federal programs

Sales Tax – tax paid on the purchase of good/services at places like Walmart.

Property tax – tax paid on your property – ex. House

Tag Tax – tax paid on your car – due on your birthday