ARMZ Uranium Holding: Expanding Global Presence

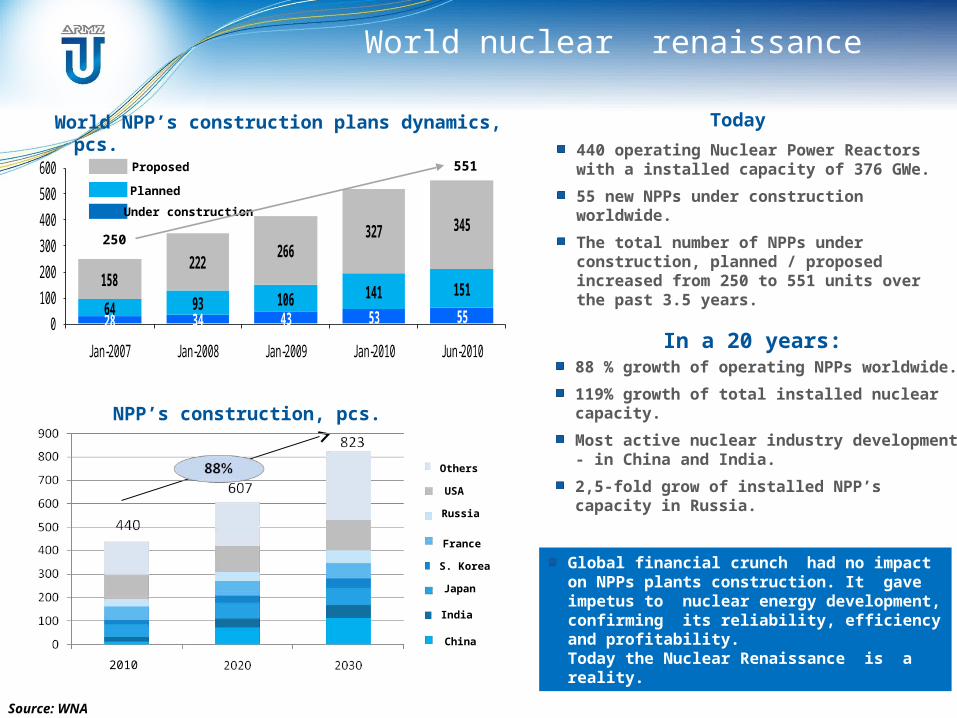

World nuclear renaissance

Today

In a 20 years:

Source: WNA

440 operating Nuclear Power Reactors with a installed capacity of 376 GWe.

55 new NPPs under construction worldwide.

The total number of NPPs under construction, planned / proposed increased from 250 to 551 units over the past 3.5 years.

28 34 43 53 5564 93 106 141 151158222

266327 345

0

100

200

300

400

500

600

Jan-2007 Jan-2008 Jan-2009 Jan-2010 Jun-2010

Under construction

Planned

Proposed

World NPP’s construction plans dynamics, pcs.

250

551

NPP’s construction, pcs.

2010

USA

Russia

Others

China

India

Japan

S. Korea

France

88 % growth of operating NPPs worldwide.

119% growth of total installed nuclear capacity.

Most active nuclear industry development - in China and India.

2,5-fold grow of installed NPP’s capacity in Russia.

Global financial crunch had no impact on NPPs plants construction. It gave impetus to nuclear energy development, confirming its reliability, efficiency and profitability.Today the Nuclear Renaissance is a reality.

33

Uranium conversion and enrichment 40% of world’s uranium enrichment

capacity Enrichment and supply of uranium to the

US, Europe, Asia, and other countries

NPP constructionHolds 16% market share in termsof nuclear power plant construction worldwide

RosatomIs a fully diversified corporation,

with operations ranging fromuranium mining to NPP construction,

power generation, and sales

NPP’s Engineering and equipment supply Supplies equipment and services to the power

generation and Oil & Gas sectors Supplies equipment to over 20 countries

Electricity generation World’s №2 in installed capacity (23.2GW) Operates 32 reactor cores across

10 power stations Further 7 power stations in construction

Nuclear fuel fabrication and supply Supplies NPPs in Russia and 76 other NPPs

across 14 countries (17% market share) Annual export volume in excess of $1bn

ARMZ, Uranium miningUranium mining and supplyWorld’s №5 in uranium production

Rosatom — Global Leader in Nuclear Industry

4

PhilippinesBrunei

Taiwan

Malaysia

Vietnam

Sri Lanka

Dschibuti

Qatar

JordanIsrael

Georgia

Cyprus

Togo

Serbia

Guinea-BissauGambia

Belgium

Portugal

Kuwait

Croatia

Albania Armenia

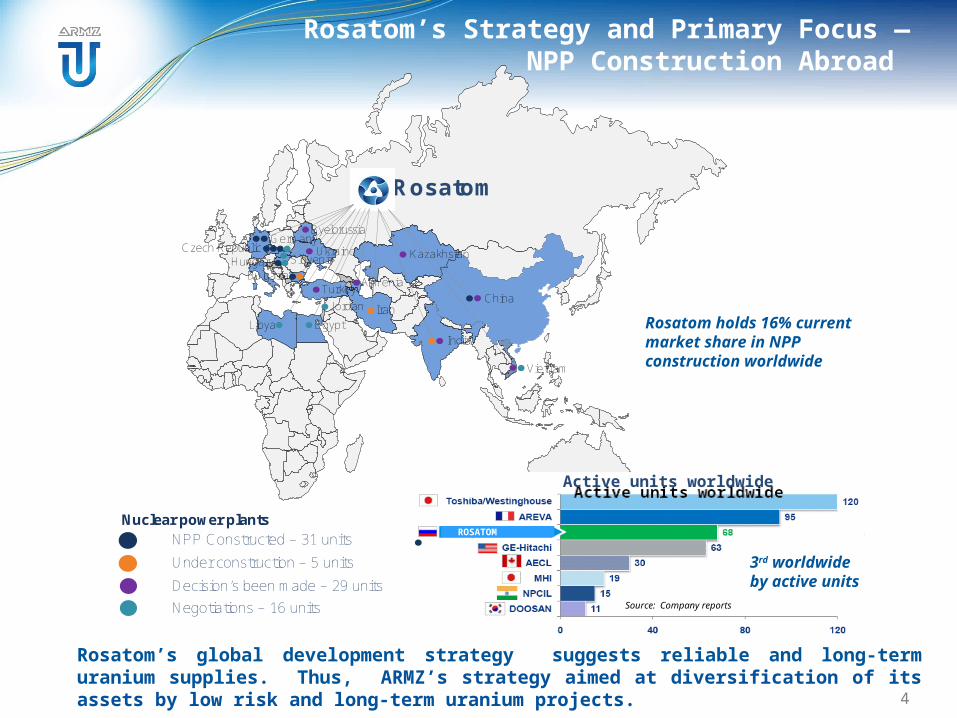

NPP Constructed – 31 units

Under construction – 5 units

Decision’s been made – 29 units

GermanyUkraineCzech Republic

SloveniaHungaryBulgaria

Turkey

Kazakhstan

Byelorussia

Negotiations – 16 units

Armenia

China

India

Vietnam

EgyptLibyaIranJordan

Nuclear power plants

Rosatom

Rosatom’s Strategy and Primary Focus —NPP Construction Abroad

ROSATOM

Active units worldwideActive units worldwide

Rosatom holds 16% current market share in NPP construction worldwide

3rd worldwide by active units

Source: Company reports

Rosatom’s global development strategy suggests reliable and long-term uranium supplies. Thus, ARMZ’s strategy aimed at diversification of its assets by low risk and long-term uranium projects.

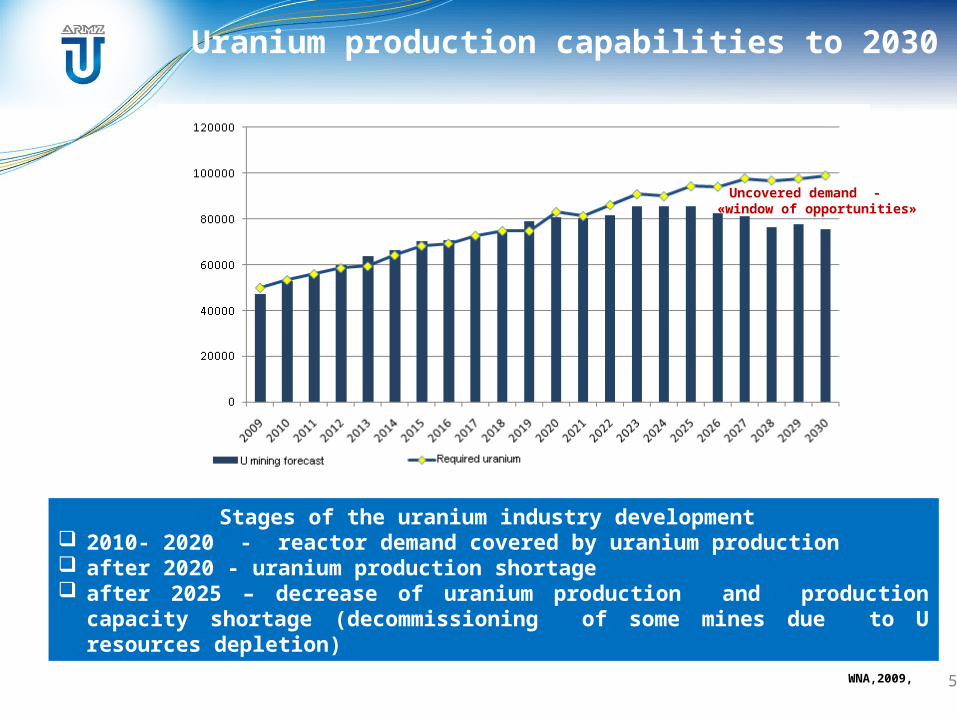

Uranium production capabilities to 2030

5WNA,2009, reference

Stages of the uranium industry development 2010- 2020 - reactor demand covered by uranium production after 2020 - uranium production shortage after 2025 – decrease of uranium production and production capacity shortage

(decommissioning of some mines due to U resources depletion)

Uncovered demand - «window of opportunities»

tU

production

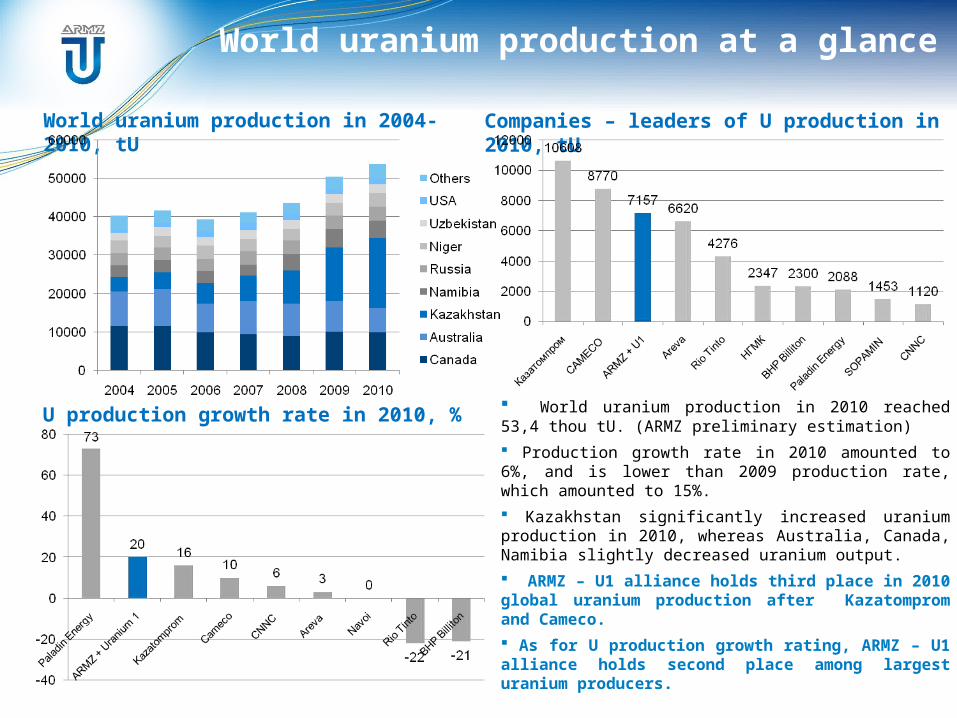

World uranium production at a glance

U production growth rate in 2010, %

World uranium production in 2004-2010, tU Companies – leaders of U production in 2010, tU

40251 4155739357 41102

43648

5030554000

World uranium production in 2010 reached 53,4 thou tU. (ARMZ preliminary estimation)

Production growth rate in 2010 amounted to 6%, and is lower than 2009 production rate, which amounted to 15%.

Kazakhstan significantly increased uranium production in 2010, whereas Australia, Canada, Namibia slightly decreased uranium output.

ARMZ – U1 alliance holds third place in 2010 global uranium production after Kazatomprom and Cameco.

As for U production growth rating, ARMZ – U1 alliance holds second place among largest uranium producers.

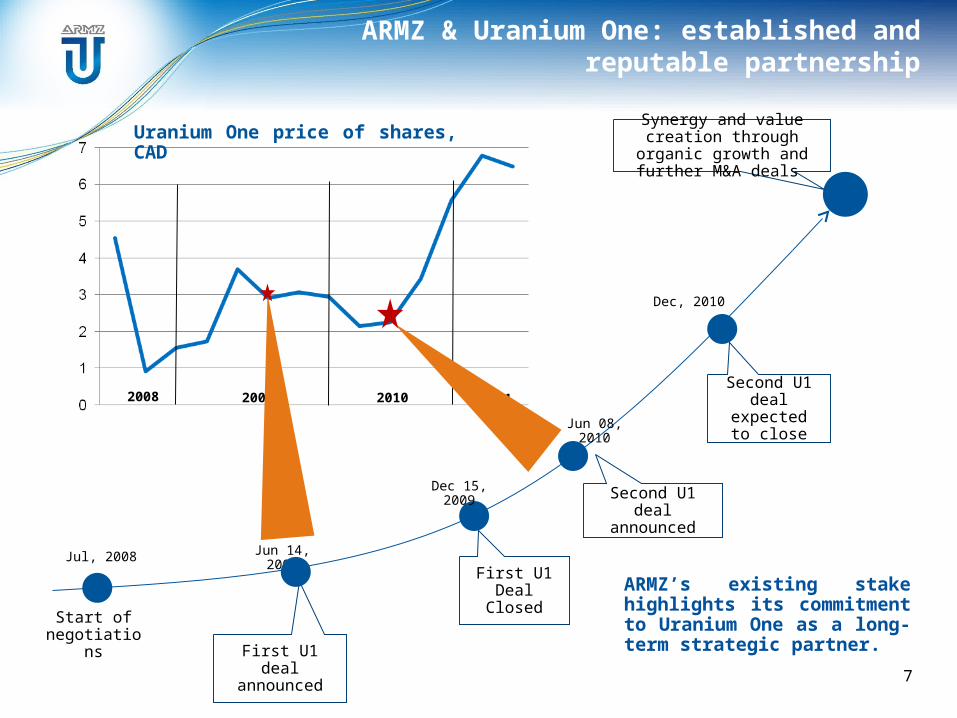

Start of negotiations

Jun 14, 2009

First U1 deal announced

Second U1 deal announced

ARMZ & Uranium One: established and reputable partnership

Synergy and value creation through organic growth and

further M&A deals

First U1 Deal Closed

Dec 15, 2009

ARMZ’s existing stake highlights its commitment to Uranium One as a long-term strategic partner.

Jun 08, 2010

Dec, 2010

Second U1 deal expected

to close

7

Jul, 2008

2008 2009 2010 2011

Uranium One price of shares, CAD

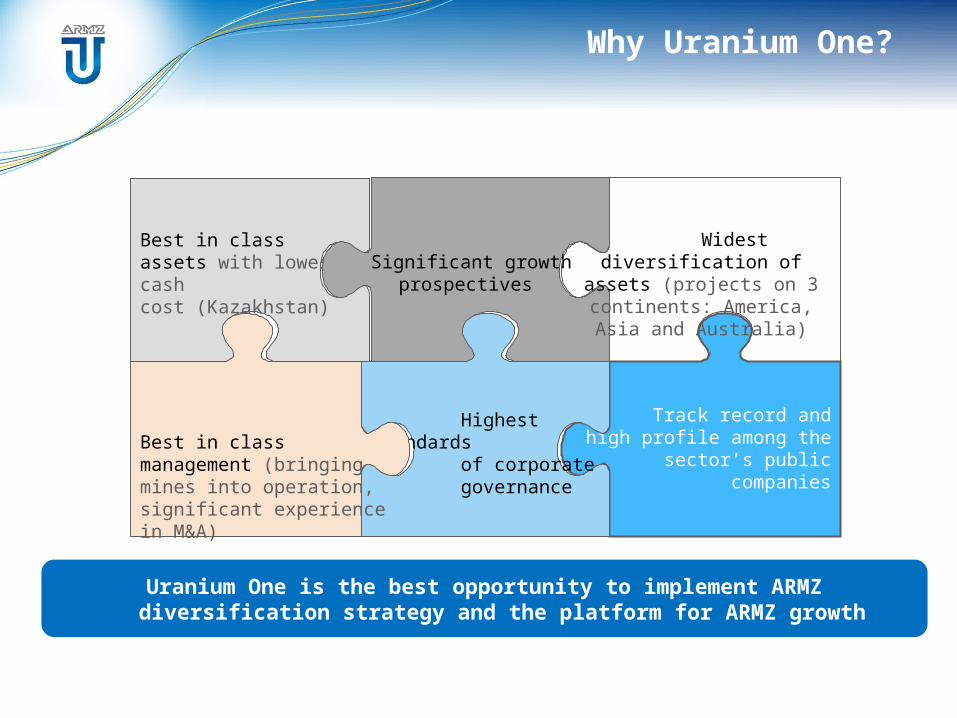

Why Uranium One?

Uranium One is the best opportunity to implement ARMZ diversification strategy and the platform for ARMZ growth

Track record and high profile among the sector’s

public companies

Highest standards of corporate governance

Best in class management (bringing mines into operation, significant experience in M&A)

Best in class assets with lowest cash cost (Kazakhstan)

Significant growth prospectives

Widest diversification of assets (projects on 3

continents: America, Asia and Australia)

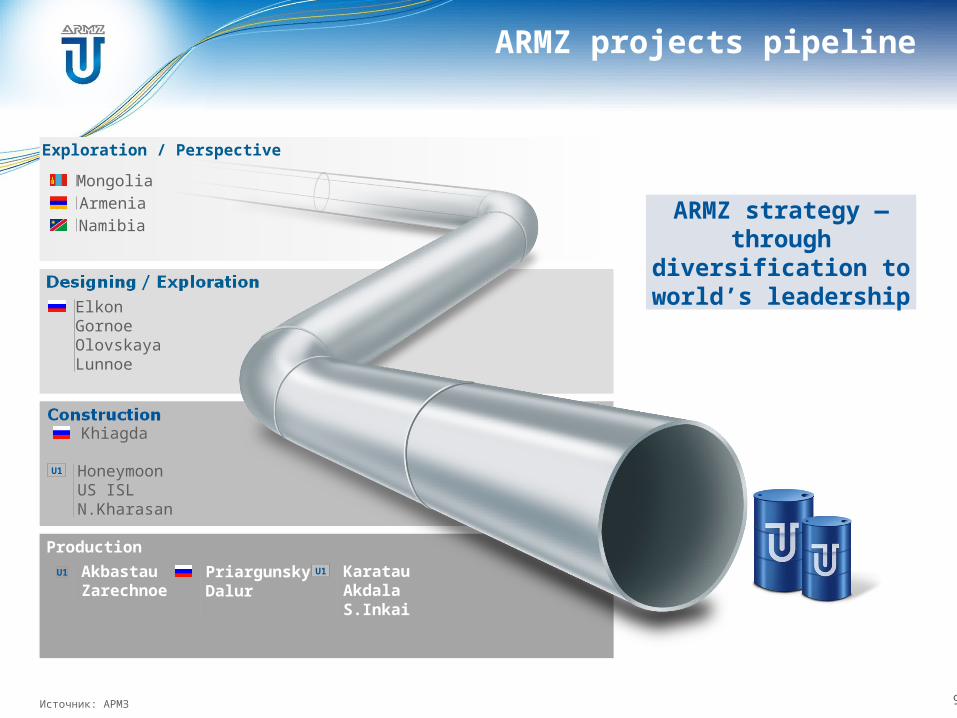

ARMZ projects pipeline

Exploration / Perspective

9Источник: АРМЗ

ARMZ strategy — through

diversification to world’s leadership

Production

AkbastauZarechnoe

ElkonGornoeOlovskayaLunnoe

MongoliaArmeniaNamibia

HoneymoonUS ISLN.Kharasan

U1

PriargunskyDalur

KaratauAkdalaS.Inkai

U1

Khiagda

U1

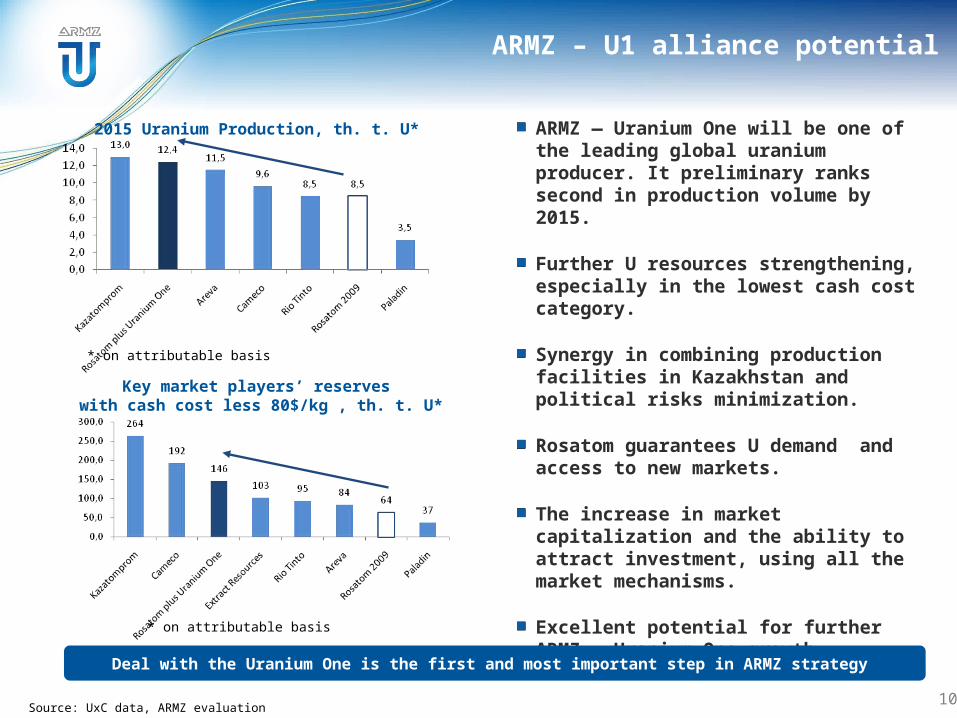

ARMZ – U1 alliance potential

10

ARMZ — Uranium One will be one of the leading global uranium producer. It preliminary ranks second in production volume by 2015.

Further U resources strengthening, especially in the lowest cash cost category.

Synergy in combining production facilities in Kazakhstan and political risks minimization.

Rosatom guarantees U demand and access to new markets.

The increase in market capitalization and the ability to attract investment, using all the market mechanisms.

Excellent potential for further ARMZ – Uranium One growth.

Deal with the Uranium One is the first and most important step in ARMZ strategy

Source: UxC data, ARMZ evaluation

2015 Uranium Production, th. t. U*

* on attributable basis

Key market players’ reserves with cash cost less 80$/kg , th. t. U*

* on attributable basis

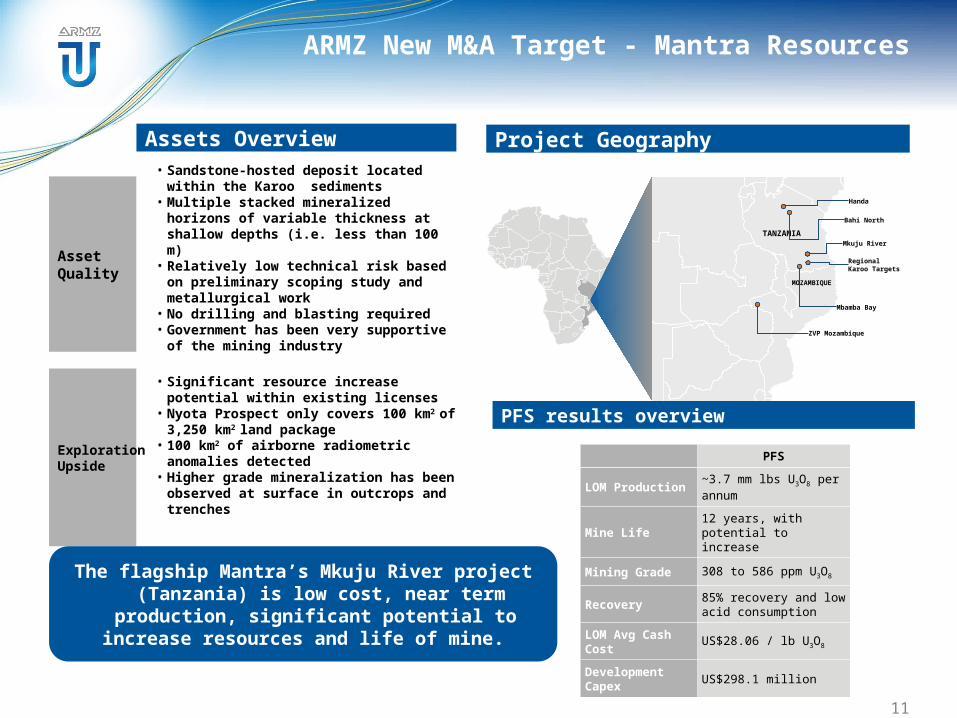

ARMZ New M&A Target - Mantra Resources

AssetQuality

• Sandstone-hosted deposit located within the Karoo sediments

• Multiple stacked mineralized horizons of variable thickness at shallow depths (i.e. less than 100 m)

• Relatively low technical risk based on preliminary scoping study and metallurgical work

• No drilling and blasting required• Government has been very supportive of the

mining industry

Assets Overview

ExplorationUpside

• Significant resource increase potential within existing licenses

• Nyota Prospect only covers 100 km2 of 3,250 km2 land package

• 100 km2 of airborne radiometric anomalies detected

• Higher grade mineralization has been observed at surface in outcrops and trenches

PFS

LOM Production ~3.7 mm lbs U3O8 per annum

Mine Life12 years, with potential to increase

Mining Grade 308 to 586 ppm U3O8

Recovery85% recovery and low acid consumption

LOM Avg Cash Cost

US$28.06 / lb U3O8

Development Capex

US$298.1 million

Handa

Bahi North

Mkuju River

Mbamba Bay

Regional Karoo Targets

ZVP Mozambique

TANZANIA

MOZAMBIQUE

Project Geography

PFS results overview

11

The flagship Mantra’s Mkuju River project (Tanzania) is low cost, near term

production, significant potential to increase resources and life of mine.

Recommended