.

CE 2402 ESTIMATION & QUANTITY SURVEYING Differentiate between B E Civil Engg 4th Yr 7th Sem

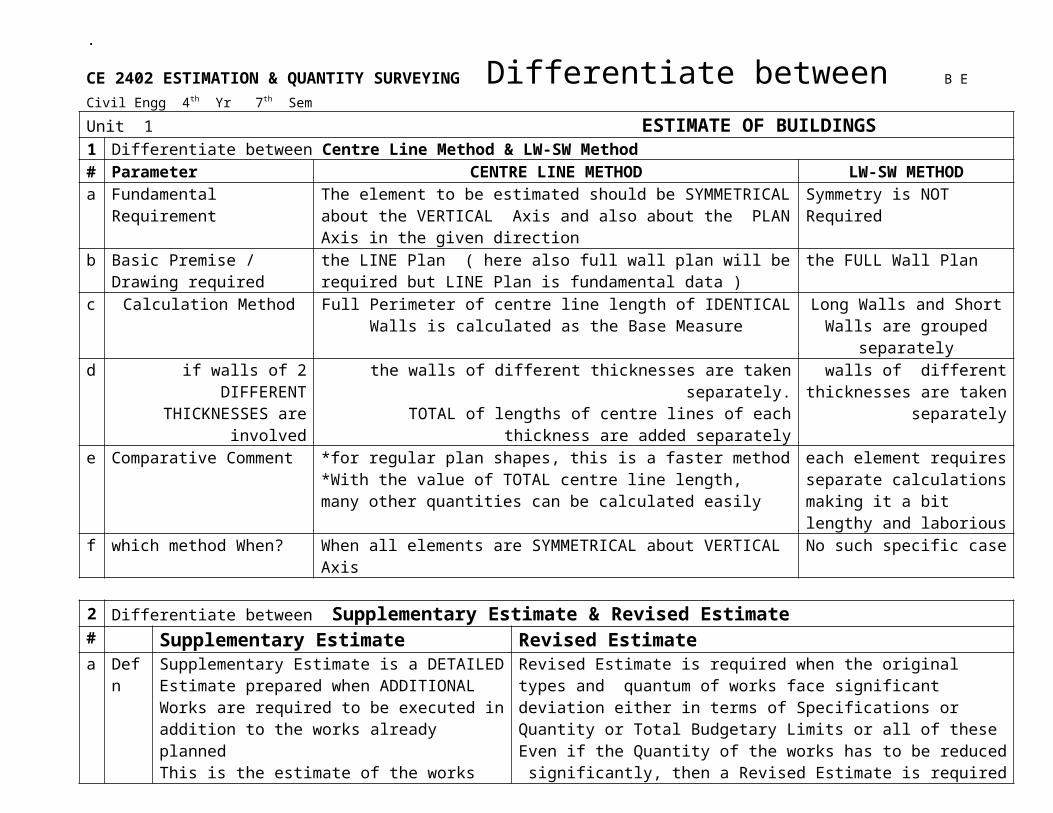

Unit 1 ESTIMATE OF BUILDINGS1 Differentiate between Centre Line Method & LW-SW Method# Parameter CENTRE LINE METHOD LW-SW METHODa Fundamental Requirement The element to be estimated should be SYMMETRICAL about the

VERTICAL Axis and also about the PLAN Axis in the given directionSymmetry is NOT Required

b Basic Premise / Drawing required

the LINE Plan ( here also full wall plan will be required but LINE Plan is fundamental data )

the FULL Wall Plan

c Calculation Method Full Perimeter of centre line length of IDENTICAL Walls is calculated as the Base Measure

Long Walls and Short Walls are grouped separately

d if walls of 2 DIFFERENT THICKNESSES are involved

the walls of different thicknesses are taken separately. TOTAL of lengths of centre lines of each thickness are added separately

walls of different thicknesses are taken separately

e Comparative Comment *for regular plan shapes, this is a faster method*With the value of TOTAL centre line length, many other quantities can be calculated easily

each element requires separate calculations making it a bit lengthy and laborious

f which method When? When all elements are SYMMETRICAL about VERTICAL Axis No such specific case

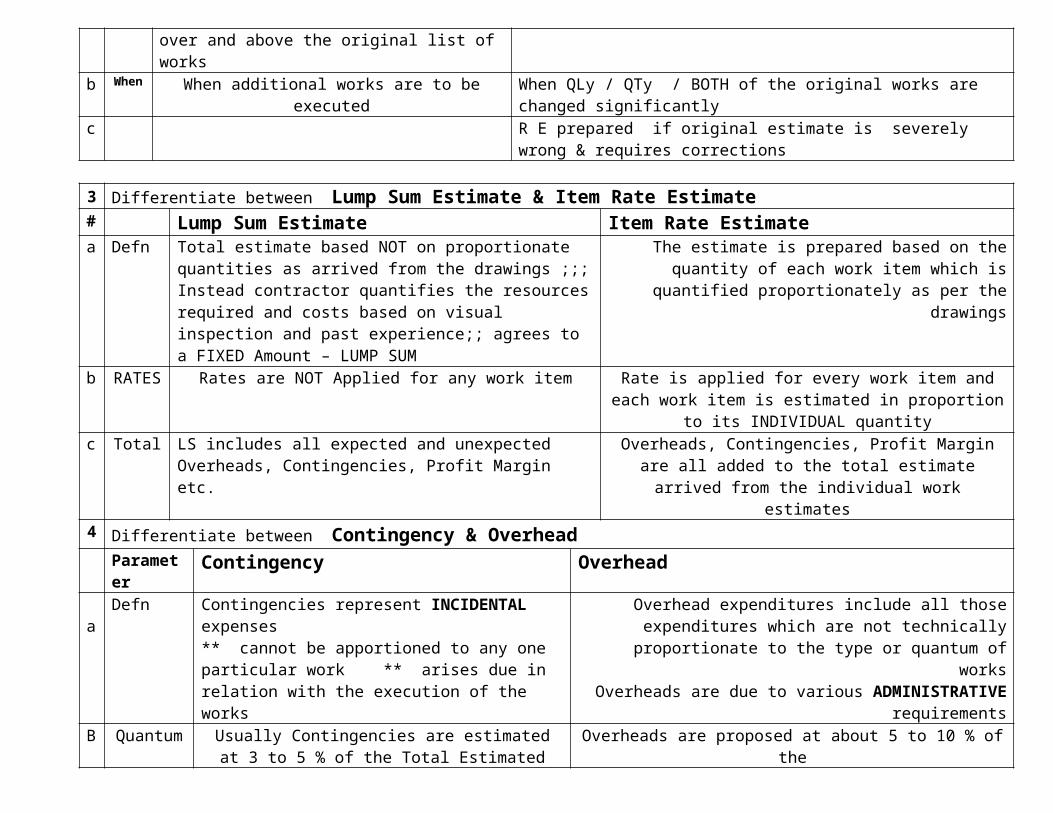

2 Differentiate between Supplementary Estimate & Revised Estimate# Supplementary Estimate Revised Estimatea Defn Supplementary Estimate is a DETAILED Estimate

prepared when ADDITIONAL Works are required to be executed in addition to the works already plannedThis is the estimate of the works over and above the original list of works

Revised Estimate is required when the original types and quantum of works face significant deviation either in terms of Specifications or Quantity or Total Budgetary Limits or all of these

Even if the Quantity of the works has to be reduced significantly, then a Revised Estimate is required

b When When additional works are to be executed When QLy / QTy / BOTH of the original works are changed significantlyc R E prepared if original estimate is severely wrong & requires corrections

3 Differentiate between Lump Sum Estimate & Item Rate Estimate# Lump Sum Estimate Item Rate Estimatea Defn Total estimate based NOT on proportionate quantities as arrived

from the drawings ;;; Instead contractor quantifies the resources required and costs based on visual inspection and past experience;; agrees to a FIXED Amount – LUMP SUM

The estimate is prepared based on the quantity of each work item which is quantified proportionately as per the drawings

b RATES Rates are NOT Applied for any work item Rate is applied for every work item and each work item is estimated in proportion to its INDIVIDUAL quantity

c Total LS includes all expected and unexpected Overheads, Overheads, Contingencies, Profit Margin are all added to the

Contingencies, Profit Margin etc. total estimate arrived from the individual work estimates4 Differentiate between Contingency & Overhead

Parameter Contingency Overhead a

Defn Contingencies represent INCIDENTAL expenses** cannot be apportioned to any one particular work ** arises due in relation with the execution of the works

Overhead expenditures include all those expenditures which are not technically proportionate to the type or quantum of works

Overheads are due to various ADMINISTRATIVE requirementsB Quantum Usually Contingencies are estimated at 3 to 5 % of the

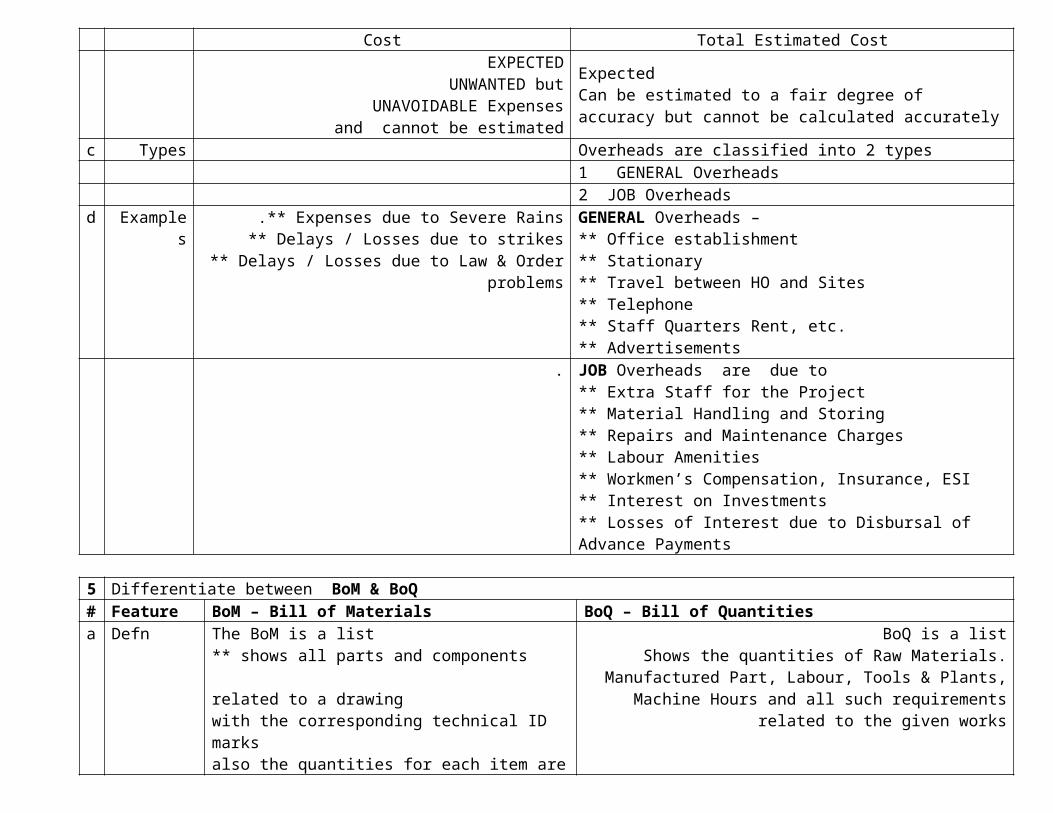

Total Estimated CostOverheads are proposed at about 5 to 10 % of the

Total Estimated CostEXPECTED

UNWANTED butUNAVOIDABLE Expenses

and cannot be estimated

ExpectedCan be estimated to a fair degree of accuracy but cannot be calculated accurately

c Types Overheads are classified into 2 types1 GENERAL Overheads2 JOB Overheads

d Examples .** Expenses due to Severe Rains** Delays / Losses due to strikes

** Delays / Losses due to Law & Order problems

GENERAL Overheads –** Office establishment ** Stationary** Travel between HO and Sites ** Telephone** Staff Quarters Rent, etc. ** Advertisements

. JOB Overheads are due to** Extra Staff for the Project** Material Handling and Storing** Repairs and Maintenance Charges** Labour Amenities** Workmen’s Compensation, Insurance, ESI** Interest on Investments** Losses of Interest due to Disbursal of Advance Payments

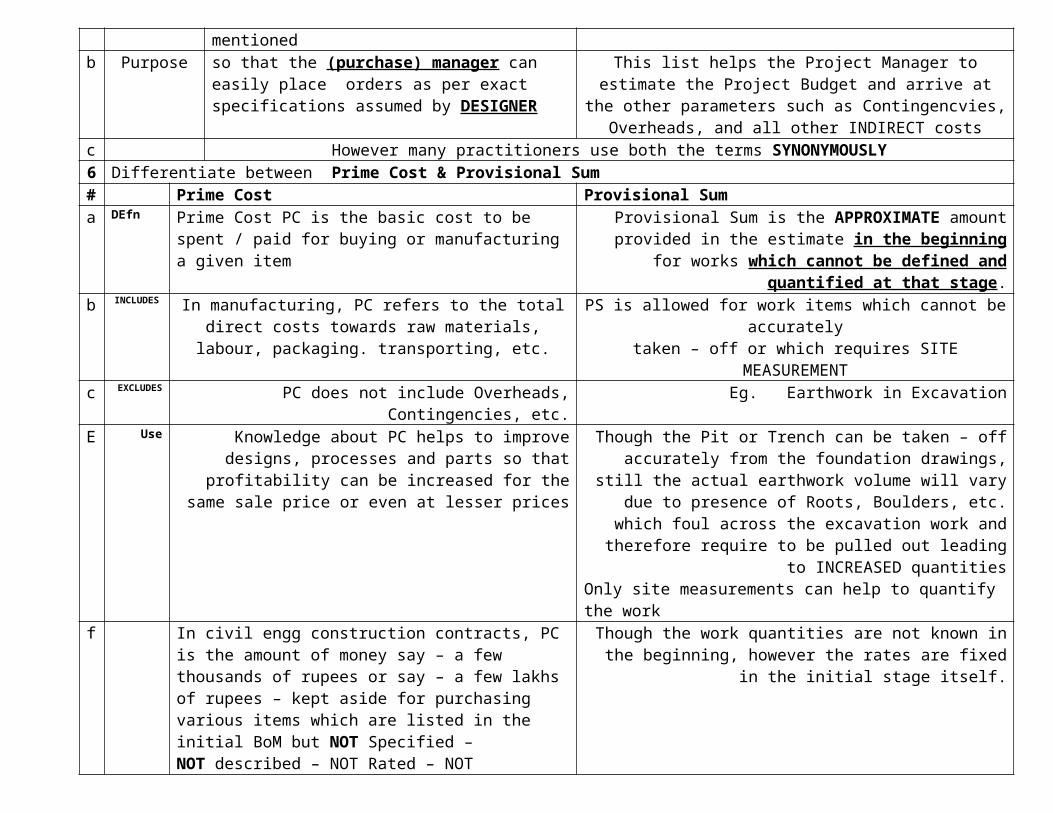

5 Differentiate between BoM & BoQ# Feature BoM – Bill of Materials BoQ – Bill of Quantitiesa Defn The BoM is a list

** shows all parts and components related to a drawingwith the corresponding technical ID marksalso the quantities for each item are mentioned

BoQ is a listShows the quantities of Raw Materials. Manufactured Part,

Labour, Tools & Plants, Machine Hours and all such requirements related to the given works

b Purpose so that the (purchase) manager can easily place orders as per exact specifications assumed by DESIGNER

This list helps the Project Manager to estimate the Project Budget and arrive at the other parameters such as Contingencvies,

Overheads, and all other INDIRECT costs

c However many practitioners use both the terms SYNONYMOUSLY6 Differentiate between Prime Cost & Provisional Sum# Prime Cost Provisional Suma DEfn Prime Cost PC is the basic cost to be spent / paid for buying

or manufacturing a given itemProvisional Sum is the APPROXIMATE amount provided in the

estimate in the beginning for works which cannot be defined and quantified at that stage.

b INCLUDES In manufacturing, PC refers to the total direct costs towards raw materials, labour, packaging. transporting, etc.

PS is allowed for work items which cannot be accuratelytaken – off or which requires SITE MEASUREMENT

c EXCLUDES PC does not include Overheads, Contingencies, etc. Eg. Earthwork in ExcavationE Use Knowledge about PC helps to improve designs, processes

and parts so that profitability can be increased for the same sale price or even at lesser prices

Though the Pit or Trench can be taken – off accurately from the foundation drawings, still the actual earthwork volume will vary

due to presence of Roots, Boulders, etc. which foul across the excavation work and therefore require to be pulled out leading to

INCREASED quantitiesOnly site measurements can help to quantify the work

f In civil engg construction contracts, PC is the amount of money say – a few thousands of rupees or say – a few lakhs of rupees – kept aside for purchasing various items which are listed in the initial BoM but NOT Specified –NOT described – NOT Rated – NOT quantifiedAll specifications, rating, quantification, etc. done only later

Though the work quantities are not known in the beginning, however the rates are fixed in the initial stage itself.

g Eg ** Sanitaryware ** Tiles ** Modular Kitchen ** Paints ** Air Conditioning Ducts ** Plumbing and Sanitaryware** Interiors and Finishes for different work cabins in an office** the type of Machine Foundation Pedestal for a particular machine in a factory ( the type of machine itself is still not specified in the beginning when the factory floor is designed )

h Payment Contractor is paid the ACTUALS for purchase of these PC itemsFor installing or fixing or executing these work items under PC, the rates for execution alone are already QUOTED by Contractor and Agreed To upon by the Client in the beginning itself

Eg. Rate for Painting -- Rs XX per sq. ft for 2 coatsMentioned in the initial estimates / bids / quotations

But rate of paint material not quotedIt is marked as PCThe client earmarks some amount towards Purchase of Paint

Client allows actual payment to the main contractor or to the specialist sub-contractor engaged by the main contractor or

engaged directly

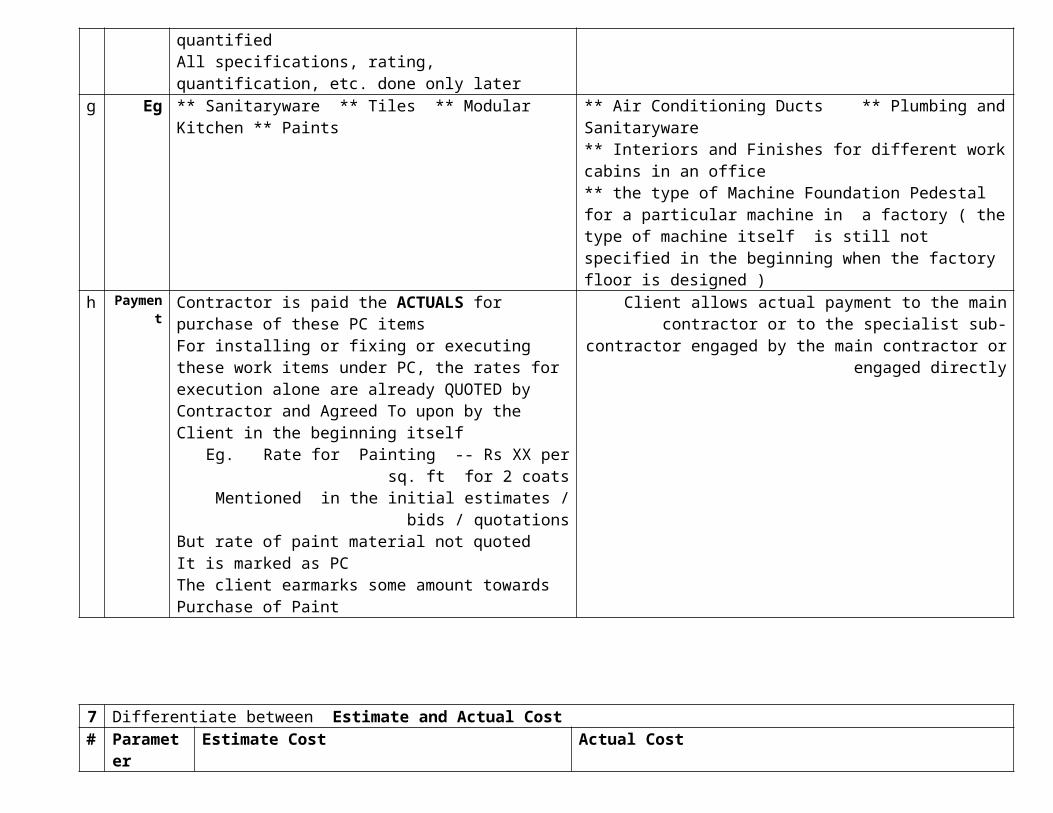

7 Differentiate between Estimate and Actual Cost# Parameter Estimate Cost Actual CostA Preparing

stagePrepared before the beginning of the work Prepared at the end of the work

B Concept Based on the Drawings, Specifications, Past Experience and some predictions

Based on the actual bills, and other payments made based on the actual field measurements

C Accuracy Prone to variations and deviations due to unavoidable changes in the work

Very less error --Errors too will be due to willful negligence,

or due to unnoticed omissionsor unavoidable situations where measurements could not be taken

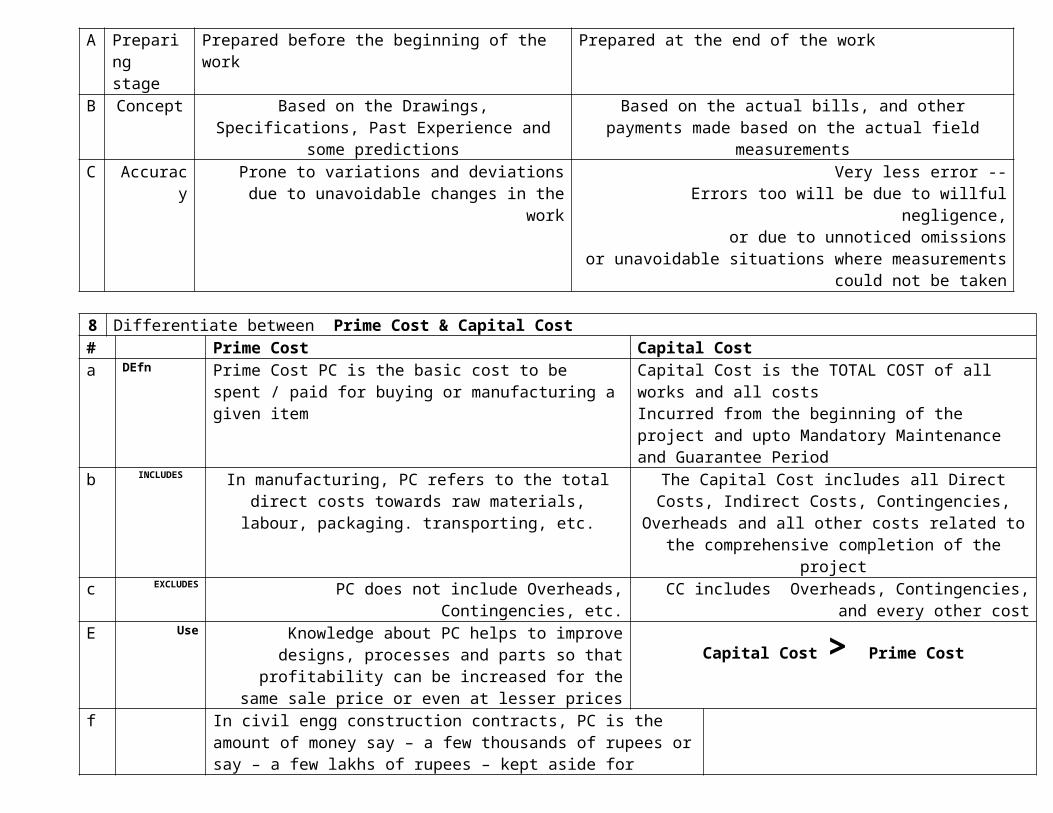

8 Differentiate between Prime Cost & Capital Cost# Prime Cost Capital Costa DEfn Prime Cost PC is the basic cost to be spent / paid for buying or

manufacturing a given itemCapital Cost is the TOTAL COST of all works and all costsIncurred from the beginning of the project and upto Mandatory Maintenance and Guarantee Period

b INCLUDES In manufacturing, PC refers to the total direct costs towards raw materials, labour, packaging. transporting, etc.

The Capital Cost includes all Direct Costs, Indirect Costs, Contingencies, Overheads and all other costs related to the

comprehensive completion of the projectc EXCLUDES PC does not include Overheads, Contingencies, etc. CC includes Overheads, Contingencies, and every other costE Use Knowledge about PC helps to improve designs, processes and

parts so that profitability can be increased for the same sale price or even at lesser prices

Capital Cost > Prime Cost

f In civil engg construction contracts, PC is the amount of money say – a few thousands of rupees or say – a few lakhs of rupees – kept aside for purchasing various items which are listed in the initial BoM but NOT Specified –NOT described – NOT Rated – NOT quantifiedAll specifications, rating, quantification, etc. done only later

g Eg ** Sanitaryware ** Tiles ** Modular Kitchen ** Paintsh Payment Contractor is paid the ACTUALS for purchase of these PC items

For installing or fixing or executing these work items under PC, the rates for execution alone are already QUOTED by Contractor and Agreed To upon by the Client in the beginning itself

Eg. Rate for Painting -- Rs XX per sq. ft for 2 coatsMentioned in the initial estimates / bids / quotations

But rate of paint material not quotedIt is marked as PCThe client earmarks some amount towards Purchase of Paint

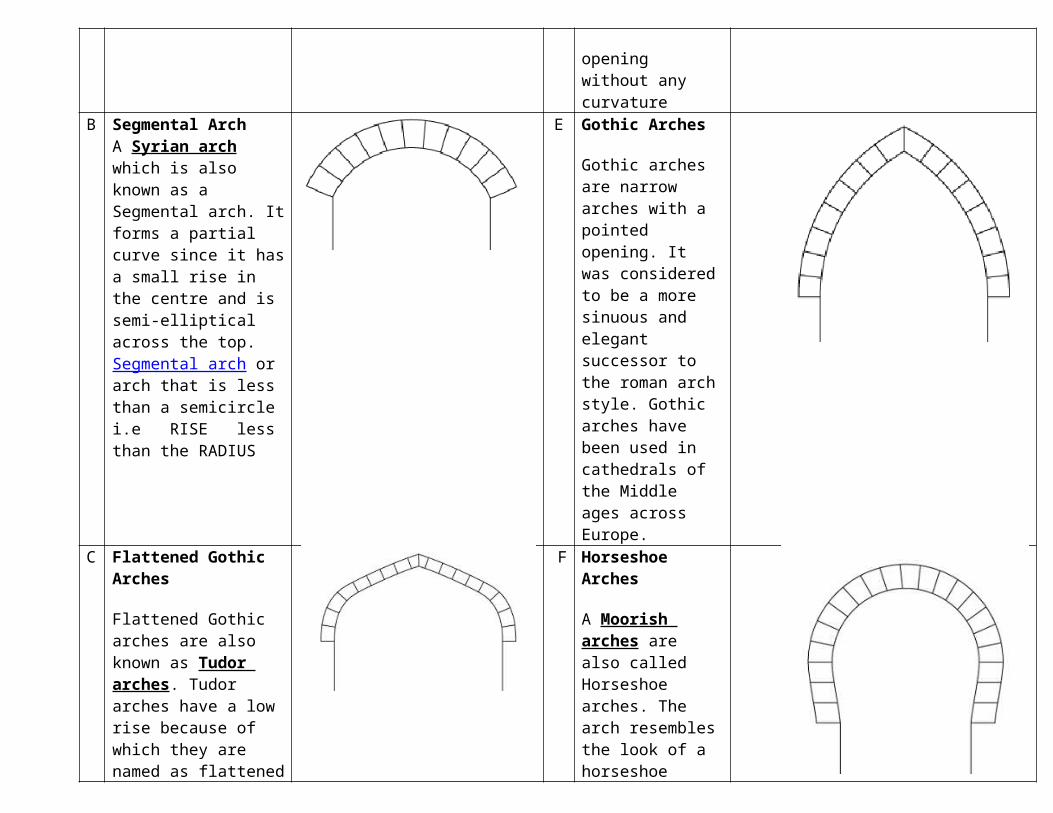

9 Differentiate between various Types of Arches

A Semi-circular arch or Roman Arch

RISE equal to RADIUS

D Flat arches

Flat arches are also known as straight arches. As the name itself suggests, the arch spans straight across the opening without any curvature

B Segmental ArchA Syrian arch which is also known as a Segmental arch. It forms a partial curve since it has a small rise in the centre and is semi-elliptical across the top.Segmental arch or arch that is less than a semicirclei.e RISE less than the RADIUS

E Gothic Arches

Gothic arches are narrow arches with a pointed opening. It was considered to be a more sinuous and elegant successor to the roman arch style. Gothic arches have been used in cathedrals of the Middle ages across Europe.

C Flattened Gothic Arches

Flattened Gothic arches are also known as Tudor arches. Tudor arches have a low rise because of which they are named as flattened gothic arches. Gothic arches are generally narrower than the flattened gothic arches.

F Horseshoe Arches

A Moorish arches are also called Horseshoe arches. The arch resembles the look of a horseshoe magnet. The curved arch line extends beyond the semi-circular line of the arch.

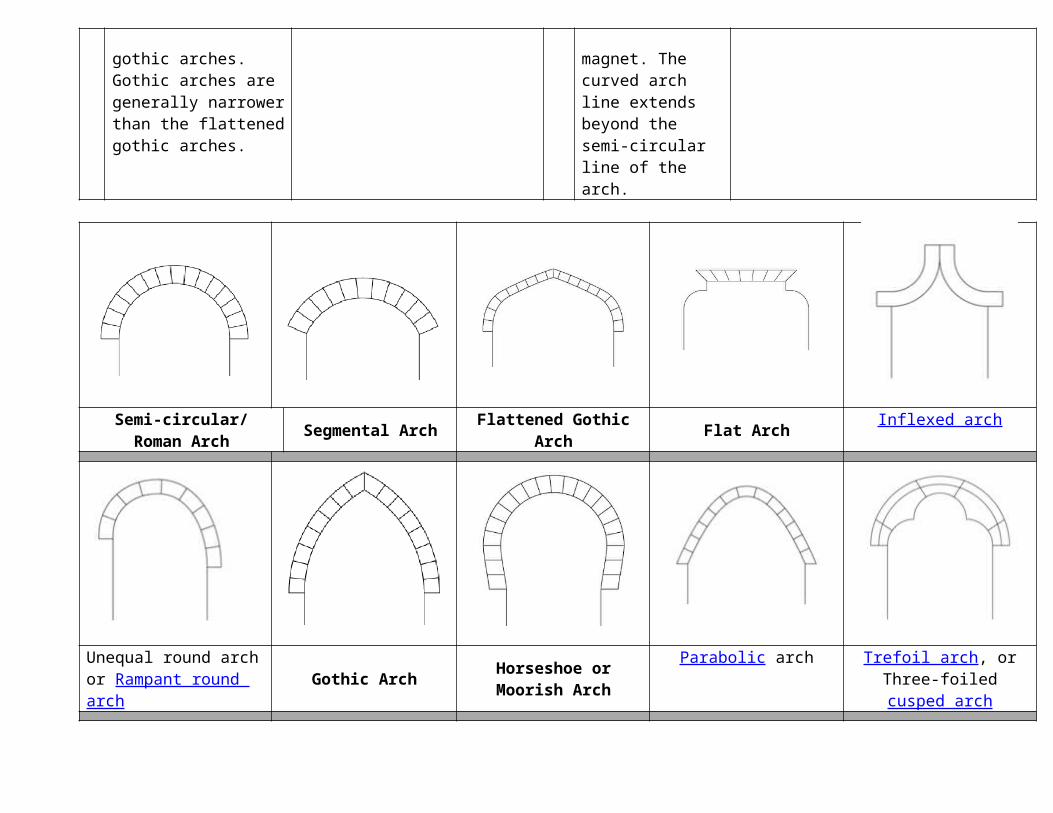

Semi-circular/ Roman Arch Segmental Arch Flattened Gothic Arch Flat Arch Inflexed arch

Unequal round arch or Rampant round arch

Gothic ArchHorseshoe or Moorish

ArchParabolic arch Trefoil arch, or Three-

foiled cusped arch

A masonry arch1. Keystone 2. Voussoir 3. Extrados 4. Impost 5. Intrados 6. Rise 7. Clear span 8. Abutment

Triangular arch

.10

Differentiate between the various types of AREAS in a building and campus

# Type of Area Definition1 Plot Area The total land area available for construction with EXCLUSIVE Ownership2 Undivided

Share

UDS

In a plot with many houses built one above the other, ( multi-storey type) the actual share of the LAND / PLOT an individual house owner can get is called UDS

UDS = Total PLOT AreaNo .of Owners

( this formula is applicable ONLY when all the owners have the SAME type of flats )

( if there are different types of flats in same plot, then UDS calculation depends on Area of each flat )) see Eg. below )3 Plinth Area Area occupied by a building – built-up and covered area at the plinth level including wall thickness but WITHOUT

Plinth OFFSETS The Plinth Area can be measured at upper storey levels also4 Floor Area FA = Plinth Area MINUS Wall Thickness Area5 Carpet Area Carpet Area is the EFFECTIVELY USABLE area within the Floor area; following elements NOT INCLUDED in Carpet Area

Areas NOT Included in the

Carpet Area

Verandah Corridor and passage; Entrance hall and porch Shaft and machine room for lift;

Bathroom and lavatory; Kitchen and pantry; Store; Canteen; Air-conditioning duct and plant room

Shaft for sanitary/water supply installations

garbage chute, electrical and fire fighting

air-conditioning, telecommunication, lift.

Staircase and stair-cover ( mumty )

6 Circulation Area

The area used for facilitating the people to move around WITHIN the same building or from One Building to ANOTHER building WITHIN the SAME campus Eg Corridor, Staircase, Pathways, …..

7 Common Area Areas within a building common to MORE THAN ONE OWNER within the same premises( Eg. Satircase, Corridor, Lift, Parking, Gate, Approach Ways, ….. )

8 Covered Area Any are overed at top by roof i.e NOT Open to sky9 FECA Fully Enclosed Covered Area -- Covered at top by roof & Enclosed on all 4 sides by walls with proper access doors10 UCA Unenclosed Covered Area - only top is covered but one or more of the 4 vertical sides open without walls

Balcony, Sit-outs, Porch, Portico, Parking Areas, ….11 Usable Floor Area The actual portion of the Floor area usable12 Service Area Area within used for services -- Lift Shaft, Garbage Chute, Wash Areas, ….13 Non-habitable Area Sunshade, though a covered area, but is not habitable14 Built-up Area Area on the plot on which buildings are constructed15 Reserved Areas Areas within the building or plot reserved for certain functions --- Eg. Side Offsets reserved for parking,16 Offset Area Areas left UNBUILT on all 4 sides of the building for Ventilation, Fire Safety, etc.17 Area earmarked for Future Expansion18 OSR Open Space Reservation --- fully open area UNBUILT – Uncovered, UNENCLOSED; used only for Greenery purpose, ---

usually before the building on the roadside19 Terrace Area Area left free and fully open to sky in the Terrace Level

20 OTS - Outside Open to Sky Area OUTSIDE the Buildings - Front , Rear and Side OFFSETS,21 OTS - Inside Open to Sky Area INSIDE the Buildings

UDS Calculation Total Land Area 5,600 sq, ft Type A Flat 800 sq. ft per flat

UDS = Plot Area

Total Floor Area * Floor Area of the given Owner

No . of Flats 9 Type B Flat 1,000 sq. ft per flat

UDS for Type A Owner = 5,600

(3∗800+6∗1,000 )∗800= 533.33 sq. ft UDS for Type B Owner =

5,600(3∗800+6∗1,000 )

∗1,000= 666.667 sq. ft

Recommended